UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2020

2023 |

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission File No. 1-7657

American Express Company

(Exact name of registrant as specified in its charter)

| | | | | |

| New York | 13-4922250 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

200 Vesey Street New York, New York | 10285 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (212) 640-2000

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Shares (par value $0.20 per Share) | AXP | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company ☐ | Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management'smanagement’s assessment of the effectiveness of its internal control over financial reporting under section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑þ

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

As of June 30, 2020,2023, the aggregate market value of the registrant’s voting shares held by non-affiliates of the registrant was approximately $76.6$128.1 billion based on the closing sale price as reported on the New York Stock Exchange.

As of February 3, 2021,1, 2024, there were 805,588,980723,869,787 common shares of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III: Portions of Registrant’s Proxy Statement to be filed with the Securities and Exchange Commission in connection with the Annual Meeting of Shareholders to be held on May 4, 2021.6, 2024.

TABLE OF CONTENTS

| | | | | | | | |

Form 10-K

Item Number | | Page |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| 9C. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

TABLE OF CONTENTS

This Annual Report on Form 10-K, including the “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to risks and uncertainties. You can identify forward-looking statements by words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “aim,” “will,” “may,” “should,” “could,” “would,” “likely,” “estimate,” “predict,” “potential,” “continue” or other similar expressions. We discuss certain factors that affect our business and operations and that may cause our actual results to differ materially from these forward-looking statements under “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.” You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We undertake no obligation to update publicly or revise any forward-looking statements.

This report includes trademarks, such as American Express®, which are protected under applicable intellectual property laws and are the property of American Express Company or its subsidiaries. This report also contains trademarks, service marks, copyrights and trade names of other companies, which are the property of their respective owners. Solely for convenience, our trademarks and trade names referred to in this report may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names.

Throughout this report the terms “American Express,” “we,” “our” or “us,” refer to American Express Company and its subsidiaries on a consolidated basis, unless stated or the context implies otherwise. The use of the term “partner” or “partnering” in this report does not mean or imply a formal legal partnership, and is not meant in any way to alter the terms of American Express’ relationship with any third parties. Refer to the “MD&A ―“ Glossary of Selected Terminology” under “MD&A” for the definitions of other key terms used in this report.

PART I

ITEM 1. BUSINESS

Overview

American Express is a globally integrated payments company, that provides ourproviding customers with access to products, insights and experiences that enrich lives and build business success. We are a leader in providing credit and charge cards to consumers, small businesses, mid-sized companies and large corporations around the world. American Express® cards issued by American Expressus, as well as by third-party banks and other institutions on the American Express network, permitcan be used by Card Members to charge purchases of goods and services at the millions of merchants around the world that accept cards bearing our logo.

Our various products and services are soldoffered globally to diverse customer groups through various channels, including mobile and online applications, affiliate marketing, customer referral programs, third-party vendorsservice providers and business partners, direct mail, telephone, in-house sales teams and direct response advertising. Business travel-related services are offered through our non-consolidated joint venture, American Express Global Business Travel (the GBT JV).

We were founded in 1850 as a joint stock association and were incorporated in 1965 as a New York corporation. American Express Company and its principal operating subsidiary, American Express Travel Related Services Company, Inc. (TRS), are bank holding companies under the Bank Holding Company Act of 1956, as amended (the BHC Act), subject to supervision and examination by the Board of Governors of the Federal Reserve System (the Federal Reserve).

We principally engage in businesses comprising threefour reportable operating segments: GlobalU.S. Consumer Services Group (GCSG)(USCS), Global Commercial Services (GCS)(CS), International Card Services (ICS) and Global Merchant and Network Services (GMNS). Corporate functions and certain other businesses are included in Corporate & Other. Our businesses are global in scope and function together to form our end-to-end integrated payments platform, which we believe is a differentiator that underpins our business model. The COVID-19 pandemic has brought unprecedented challenges to businesses and economies around the world. While our business was significantly impacted by the pandemic in 2020 as further described in this report, we believe our progress in managing through it confirms the resilience of our differentiated business model.

For further information about our reportable operating segments, please see “Business Segment Results of Operations” under “MD&A.”

Our Integrated Payments Platform and Technology

Through our general-purpose card-issuing, merchant-acquiring and card network businesses, we are able to connect participants and provide differentiated value across the commerce path. We maintain direct relationships with both our Card Members (as a card issuer) and merchants (as an acquirer), and we handle all key aspects of those relationships. These relationships create a “closed loop” in that we havewhich provides us with direct access to information at both ends of the card transaction, which distinguishesdistinguishing our integrated payments platform from the bankcard networks.

Our integrated payments platform allows us to analyze information on Card Member spending and build algorithms and other analytical tools that we use to underwrite risk, reduce fraud and provide targeted marketing and other information services for merchants and special offers and services to Card Members, all while respecting Card Member preferences and protecting Card Member and merchant data in compliance with applicable policies and legal requirements. Through contractual relationships, we also obtain information from third-party card issuers, merchant acquirers, aggregators and processors with whom we do business.

Our integrated payments platform and the systems and infrastructure that underlie it allow us to analyze information on Card Member spending, build models and use analytical tools to help us underwrite risk, reduce fraud and provide targeted marketing and other information services for merchants and partners and special offers and services to Card Members, all while maintaining our commitment to respect Card Member preferences and protect Card Member and merchant data in compliance with applicable policies and legal requirements. We also leverage technology to allow for faster introduction and greater differentiation of products, as well as to develop and improve our service capabilities to continue to deliver a high-quality customer experience.

Card Issuing Businesses

Our global proprietary card-issuing businesses are conducted through our GCSGUSCS, CS and GCSICS reportable operating segments. We offer a broad set of card products, rewards and services to a diverse consumer and commercial customer base, in the United States and internationally. We acquire and retain high-spending, engaged and creditworthy Card Members by:

•Designing innovative credit, charge and debit card products and featurespayment and lending solutions that appeal to our target customer base and meet their spending and borrowing needs

•Using incentives to drive spending on our various card products and engender loyal Card Members,increase customer engagement, including our Membership Rewards® program,and Amex® Offers programs, cash-back reward features, interest rates offered on deposits and participation in loyalty programs sponsored by our cobrand and other partners

•Providing digital and mobile services and an array of benefits and experiences across card products, such as airport lounge access, dining experiences and other travel and lifestyle benefits which we believe are difficult for others to replicate and help increase Card Member engagement

•Creating world-class service experiences by delivering exceptional customer care

•Developing a wide range of partner relationships, including with other corporations and institutions that sponsor certain of our cards under cobrand arrangements and provide benefits and services to our Card Members

During 2020,Over the last several years, we enhancedhave focused on broadening the appeal of our value propositions on manyproducts to attract new customers, particularly Millennial and Gen Z customers, as well as expanding our position with small and mid-sized enterprise (SME) customers by providing more ways to help them manage and grow their businesses. We have a number of products that complement our card products, including adjusting our rewards programs and adding limited time offers and statement credits in categories that are relevant in the current environment, such as wireless, streaming services,our business essentialschecking and food delivery. We also created a Customer Pandemic Relief Program to provide short-term support for customers impacted by COVID-19,consumer rewards checking account products, our business-to-business (B2B) payment products and we enhancedother non-card payment and expandedfinancing products, our longer-term Financial Relief Program for Card Members who need additional financial assistance during this time.Business Blueprint digital cash flow management hub, our Resy restaurant platform and other new digital capabilities. Additionally, we participatedare focused on driving growth and efficiencies internationally, including a greater focus on local priorities in international jurisdictions. Jurisdictions that represent a significant portion of our billed business outside of the U.S. Small Business Administration Paycheck Protection Program (PPP)United States include the United Kingdom (UK), designed to provide small businesses with support to cover payrollthe European Union (EU), Australia, Japan, Canada and certain other expenses.Mexico.

For the year ended December 31, 2020,2023, worldwide proprietary billed business (spending on American Express cards issued by us) was $870.7$1,460 billion and at December 31, 2020,2023, we had 68.980.2 million proprietary cards-in-force worldwide.

Merchant Acquiring Business

Our GMNS reportable operating segment builds and manages relationships with millions of merchants around the world that choose to accept American Express cards. This includes signing new merchants to accept our cards, agreeing on the discount rate (a fee charged to the merchant for accepting our cards) and handling servicing for merchants. We also build and maintain relationships with merchant acquirers, aggregators and processors to manage aspects of our merchant services business. For example, through our OptBlue® merchant-acquiring program, third-party acquirersprocessors contract directly with small merchants for card acceptance on our network and determine merchant pricing. We continue to grow merchant acceptance of American Express cards around the world and work with merchant partners so that our Card Members are warmly welcomed and encouraged to spend in the millions of places where their American Express cards are accepted.

Table We also seek to drive greater usage of Contentsthe American Express network by deepening merchant engagement and increasing Card Member awareness through initiatives such as our Shop Small campaigns and expanding our payment options such as through debit and B2B capabilities.GMNS also provides fraud-prevention tools, marketing solutions, data analytics and other programs and services to merchants and other partners that leverage the capabilities of our integrated payments platform.

During 2020, we adjusted certain policies to back our merchant partners in the current environment, including raising contactless transaction thresholds and reminding them that we do not require Card Members’ signatures at the point

Card Network Business

We operate a payments network through which we establish and maintain relationships with third-party banks and other institutions in approximately 98110 countries and territories, licensing the American Express brand and extending the reach of our global network. These network partners are licensed to issue local currency American Express-branded cards in their countries and/or serve as the merchant acquirer for local merchants on our network.

During 2020, our joint venture with Lianlian DigiTech Co., Ltd, a Chinese fintech services company, received approval from the People’s Bank of China for a network clearing license and began processing transactions in mainland China.

For the year ended December 31, 2020,2023, worldwide network services billed businessprocessed volume (spending on American Express cards issued by third parties) was $139.9$220.5 billion and at December 31, 2020,2023, we had 43.161.0 million cards-in-force issued by third parties worldwide.

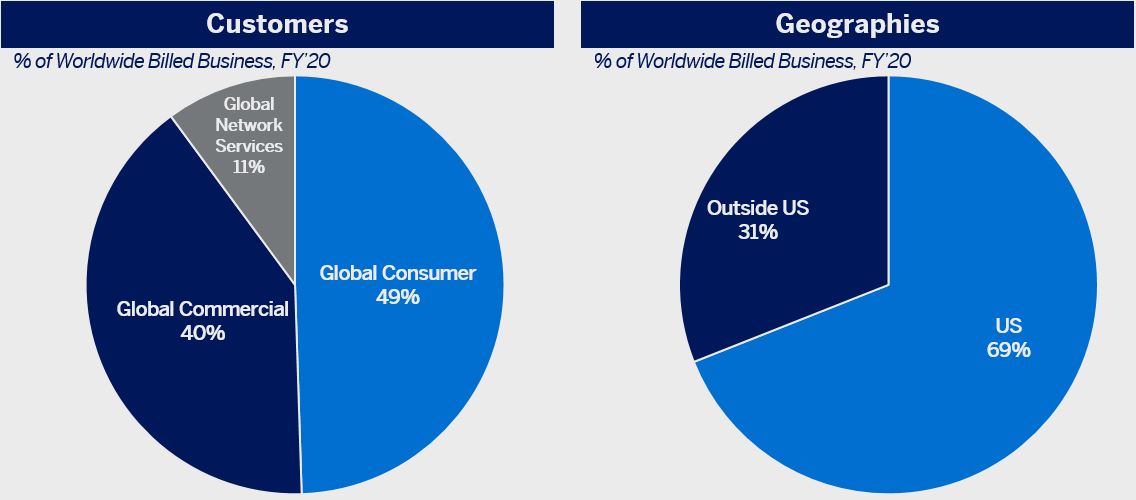

Diverse Customer Base and Global Footprint

Our broad and diverse customer base spans consumers, small businesses, mid-sized companies and large corporations around the world. The following charts providechart provides a summary of our diverse set of customers and broad geographic footprint based on billed businessworldwide network volumes:

Partners and Relationships

Our integrated payments platform allows us to work with a range of business partners, and our partners in return help drive the scale and relevance of the platform.

There are many examples of how we connectwork with partners, with our integrated payments platform, including: issuing cards under cobrand arrangements with other corporations and institutions (e.g., Delta Air Lines (Delta), Marriott International, Hilton Worldwide Holdings and British Airways); offering innovative ways for our Card Members to earn and use points with our merchants (e.g., Pay with Points at Amazon.com); providing greater value to our Card Members (e.g., Amex Offers and statement credits for purchases with partners); expanding merchant acceptance with third-party acquirers and processors (e.g., OptBlue partners); operating through joint ventures in certain jurisdictions (e.g., in China, the Middle East and Switzerland); developing new capabilities and features with our digital partners (e.g., PayPal)PayPal and i2c); integrating into the supplier payment processes of our business customers (e.g., Bill.com, SAP AribaBILL and Coupa)Extend); and extending the platform intoenhancing our travel services with American Express leisurebenefits and business travelservices (e.g., Fine Hotels and Resorts). We also have a significant ownership position in, and extensive commercial arrangements with, Global Business Travel Group, Inc. (GBTG), which provides business travel-related services.

Delta Air Lines is our largest strategic partner. Our relationships with, and revenues and expenses related to, Delta are significant and represent a significantan important source of value for our Card Members. We issue cards under cobrand arrangements with Delta and the Delta cobrand portfolio represented approximately 910 percent of our worldwide billed businessnetwork volumes and approximately 21 percent of worldwide Card Member loans as of December 31, 2020.2023. The Delta cobrand portfolio generates fee revenue and interest income from Card Members and discount revenue from Delta and other merchants for spending on Delta cobrand cards. The current Delta cobrand agreement runs through the end of 2029 and we expect to continue to make significant investments in this partnership. Among other things, Delta is also a key participant in our Membership Rewards program, provides travel-related benefits and services, including airport lounge access for certain American Express Card Members, accepts American Express cards as a merchant and is a corporate payments customer.

Working with all of our partners, we seek to provide value, choice and unique experiences across our customer base.

Our Spend-Centric Model and Revenue Mix

Our “spend-centric” business model focuses on generating revenues primarily by driving spending on our cards and secondarily through finance charges and fees. Spending on our cards, which is higher on average on a per-card basis versus our network competitors, offers superior value to merchants in the form of loyal customers and larger transactions. Because of the revenues generated from having high-spending Card Members and the annual card fees we charge on many of our products, we are able to invest in attractive rewards and other benefits for Card Members, as well as targeted marketing and other programs and investments for merchants. This creates incentives for Card Members to spend more on their cards and positively differentiates American Express cards.

We believe our spend-centric model gives us the ability to provide differentiated value to Card Members, merchants and business partners.

The American Express Brand and Service Excellence

Our brand and its attributes—trust, security and service—are key assets. We invest heavily in managing, marketing, promoting and protecting our brand, including through the delivery of our products and services in a manner consistent with our brand promise. The American Express brand is consistently ranked as one ofamong the most valuable brands in the world. We place significant importance on trademarks, service marks and patents, and seek to secure our intellectual property rights around the world.

We aim to provide the world’s best customer experience every day and our reputation for world-class service has been recognized by numerous awards over the years. Our customer care professionals, travel consultants and partners treat servicing interactions as an opportunity to bring the brand to life for our customers, add meaningful value and deepen relationships.

Our Business Strategies

Our framework for managing through the pandemic and the challenging economic environment is built on four principles: supporting our colleagues and winning as a team; protecting our customers and our brand; structuring the company for growth in the future; and remaining financially strong. We remain focused on what we can control in the short term while identifying opportunities across our businesses to position ourselves for growth in the longer term. And we seek to grow our business over the longer term by focusing on four strategic imperatives:

First, we aim to expand our leadership in the premium consumer space by continuing to deliver membership benefits that span our customers’ everyday spending, borrowing, travel and lifestyle needs, expanding our roster of business partners around the globe and developing a range of experiences that attract high-spending customers.

Second, we seek to build on our strong position in commercial payments by evolving our card value propositions, further differentiating our corporate card and accounts payable expense management solutions and designing innovative products and features, including financing, banking and supplier payment solutions for our business customers.

Third, we are focused on strengthening our global, integrated network to provide unique value by continuing to helpincrease merchant acceptance, providing merchants navigate the convergence of online and offline commerce with fraud protection services, marketing insights and digital connections to higher-spending Card Members and continuing to workworking with our network partners to offer expanded products and services.

Finally, we want to continue to make American Expressbuild on our unique global position, seeking ways to use our differentiated business model and global presence as we progress against our other strategic imperatives.

We also have an essential part of our customers’ digital lives by developing more digital features, solutionsEnvironmental, Social and Governance (ESG) strategy that focuses on three pillars. The Building Financial Confidence pillar seeks to provide responsible, secure and transparent products and services expandingto help people and businesses build financial resilience. The Advancing Climate Solutions pillar focuses on enhancing our digital partnershipsoperations and making targeted acquisitions.

Our Colleagues

Our colleagues are integral to executing our business strategies and to our overall success. As of December 31, 2023, we employed approximately 74,600 people, whom we refer to as colleagues, with approximately 26,000 colleagues in the United States and approximately 48,600 colleagues outside the United States. In 2023, we continued to invest in our colleagues, building on a wide range of learning and development opportunities and enhancing our competitive benefits in key areas including holistic health and wellness, total compensation and flexibility.

We are committedconduct an annual Colleague Experience Survey to deliveringbetter understand our colleagues’ needs and overall experience at American Express, and in 2023, 91 percent of colleagues who participated in the survey said they would recommend American Express as a great colleague experience every day, cultivatingplace to work.

To attract and retain the best talent, and developing new ways of workingwe strive to unlock enterprise value. We workoffer a compelling value proposition to foster an inclusive and diverse culture and help our colleagues, thrive both professionally and personally. Whenwhich represents the ways in which we do,support our colleagues are more engaged, committed, creativein four key areas: (1) our culture; (2) career growth and effective in driving results.development; (3) rewards and holistic well-being; and (4) diversity, equity and inclusion.

Our Culture

Our culture is built on strong relationships, shared values and purpose and a commitment to back our customers, communities and each other. At the heart of our culture is what we call our Blue Box Values – a set of guiding principles that reflect whoserve as the foundation for how we are and what we stand for. In 2020, we updated our Blue Box Values to be more explicit about our efforts to create an inclusive and diverse workforce:

operate: | | | | | | |

| We Do What’s Right | | | | | | | | We Embrace Diversity |

| We Back Our Customers | | We Embrace DiversityStand for Equity and Inclusion |

| We Make It Great | | We Stand for Inclusion |

We Do What's Right | | We Win as A Team |

| We Respect People | | We Support Our Communities |

Career Growth and Development

We continuously invest in programs, benefits and resources to foster the personal and professional growth of our colleagues. We start with opportunities for colleagues to learn on the job, build cross-functional skills and grow in their careers through a defined, collaborative process for performance management. Colleagues have access to a wide variety of resources: career coaching, mentoring, professional networking, and rotation opportunities, as well as courses on-demand and with classroom-style instruction.

Rewards and Holistic Well-Being

We aim to provide our colleagues with competitive compensation and leading benefits and take a holistic approach to servingwell-being, providing resources that address the physical, financial and mental health of our colleagues. Our financial well-being program, Smart Saving, provides tools and resources to help colleagues build their knowledge and skills for all life stages. We support our colleagues’ physical health and well-being through our corporate wellness program, Healthy Living. We also provide resources and support to increase awareness about mental health among our colleagues by offering them a varietythrough our Healthy Minds Program.

Diversity, Equity and Inclusion

We continue to work to build an inclusive and diverse workplace that values our colleagues’ voices, rewards teamwork, celebrates different points of resources that support their physical, financial, emotional, socialview and overall well-being. Throughoutreflects the pandemic, onediversity of our top priorities has been to ensure our colleagues have the flexibility and resources they need to stay safe, healthy and productive.

communities in which we operate. As of December 31, 2020, we employed approximately 63,700 people, whom we refer to as colleagues, with approximately 22,700 colleagues in the United States and approximately 41,000 colleagues outside the United States. We conduct an annual Colleague Experience Survey to better understand our colleagues’ needs and overall experience at American Express and in 2020, 94 percent of colleagues who participated in the survey said they would recommend American Express as a great place to work. Our 2020 annual company scorecard included talent retention and diversity representation goals to globally increase minority and2023, women representation at management levels and retain our key talent. As of December 31, 2020, female colleagues comprised 52represented 53.2 percent of our global workforce and Asian, Black/African American and Hispanic/Latinx people represented 19.720.6 percent, 12.015.6 percent and 13.014.3 percent, respectively, of our U.S. workforce based on preliminary data for our 20202023 U.S. EEO-1 submission.

As of December 31, 2023, 50 percent of our Executive Committee were women or from diverse races and ethnic backgrounds (based on self-identified characteristics). We also regularly review our compensation practices to ensure colleagues in the same job, level and location are compensated fairly regardless of gender globally, and regardless of race and ethnicity in the United States. These reviews consider several factors known to affect compensation, including role, level, tenure, performance and geography. In the few instances where a review has found inconsistencies, we have made adjustments. After making these adjustments, we believe we achievedmaintained 100 percent pay equity in 20202023 for colleagues across genders globally and across races and ethnicities in the United States.

Information About Our Executive Officers

Set forth below, in alphabetical order, is a list of our executive officers as of February 12, 2021,9, 2024, including each executive officer’s principal occupation and employment during the past five years and reflecting recent organizational changes.years. None of our executive officers has any family relationship with any other executive officer, and none of our executive officers became an officer pursuant to any arrangement or understanding with any other person. Each executive officer has been elected to serve until the next annual election of officers or until his or her successor is elected and qualified. Each officer’s age is indicated by the number in parentheses next to his or her name.

| | | | | |

| DOUGLAS E. BUCKMINSTER — | Group President, Global Consumer Services GroupVice Chairman |

Mr. Buckminster (60)(63) has been Vice Chairman since April 2021. Prior thereto, he had been Group President, Global Consumer Services Group since February 2018. Prior thereto, he had been President, Global Consumer Services Group since October 2015. |

| |

| JEFFREY C. CAMPBELL — | Chief Financial OfficerVice Chairman |

Mr. Campbell (60)(63) has been Vice Chairman since April 2021. He also served as Chief Financial Officer since(CFO) from August 2013.2013 to August 2023. |

| |

| HOWARD GROSFIELD — | President, U.S. Consumer Services |

| Mr. Grosfield (55) has been President, U.S. Consumer Services since May 2022. Prior thereto, he had been Executive Vice President and General Manager of U.S. Consumer Marketing and Global Premium Services since February 2021 and Executive Vice President and General Manager of U.S. Consumer Marketing Services from January 2016 to February 2021. |

| MARC D. GORDON — | Chief Information Officer

Mr. Gordon (60) has been Chief Information Officer since September 2012. |

| |

| MONIQUE HERENA — | Chief Colleague Experience Officer |

Ms. Herena (49)(52) has been Chief Colleague Experience Officer since April 2019. Ms. Herena joined American Express from BNY Mellon, where she served as the Chief Human Resources Officer and Senior Executive Vice President, Human Resources, Marketing and Communications since 2014. |

| |

| RAYMOND JOABAR — | Chief Risk Officer andGroup President, Global Risk & ComplianceMerchant and Network Services |

Mr. Joabar (55)(58) has been Chief Risk Officer andGroup President, Global Risk & ComplianceMerchant and Network Services since September 2019.April 2021. Prior thereto, he had been President, Global Risk and Compliance and Chief Risk Officer since September 2019. He also served as President of International Consumer Services and Global Travel and Lifestyle Services from February 2018 to September 2019. |

|

| CHRISTOPHE Y. LE CAILLEC — | Chief Financial Officer |

Mr. Le Caillec (58) has been CFO since August 2023. Prior thereto, he had been Deputy CFO since December 2021 and Head of Corporate Planning since February 2018.2019. He also served as Executive Vice President,Business CFO for the Global Servicing NetworkConsumer Services Group from FebruaryMay 2016 to February 20182019. |

| |

| RAFAEL MARQUEZ — | President, International Card Services |

Mr. Marquez (52) has been President, International Card Services since May 2022. Prior thereto, he had been President, International Consumer Services and Global Loyalty Coalition since September 2019 and Executive Vice President World Serviceof International Consumer Services Europe, Joint Ventures EMEA and International Member Engagement from November 2015 to February 2016.September 2019. |

| |

| ANNA MARRS — | Group President, Global Commercial Services and Credit & Fraud Risk |

Ms. Marrs (47)(50) has been Group President, GlobalCommercial Services and Credit & Fraud Risk since April 2021. Prior thereto, she had been President, Commercial Services since September 2018. Ms. Marrs joined American Express from Standard Chartered Bank, where she served as Regional CEO, ASEAN and South Asia since November 2016 and CEO, Commercial and Private Banking since October 2015. |

| |

| GLENDA MCNEAL — | Chief Partner Officer |

| Ms. McNeal (63) has been Chief Partner Officer since February 2024. Prior thereto, she had been President, Enterprise Strategic Partnerships since March 2017. |

| |

| DAVID NIGRO — | Chief Risk Officer |

| Mr. Nigro (62) has been Chief Risk Officer since April 2021. Prior thereto, he had been Executive Vice President and Chief Credit Officer, Global Consumer Services and Credit and Fraud Risk Capability since April 2018. |

| |

| DENISE PICKETT — | President, Global Services Group |

Ms. Pickett (55)(58) has been President, Global Services Group since September 2019. Prior thereto, she had been Chief Risk Officer and President, Global Risk, Banking & Compliance since February 2018 and President, U.S. Consumer Services since October 2015.2018. |

| |

| |

| |

|

| |

| |

|

| |

| |

|

| |

| |

|

| |

| |

|

| |

| |

|

| | | | | |

| RAVI RADHAKRISHNAN — | Chief Information Officer |

| Mr. Radhakrishnan (52) has been Chief Information Officer since January 2022. Mr. Radhakrishnan joined American Express from Wells Fargo & Company, where he served as Chief Information Officer for the Commercial Banking and Corporate & Investment Banking businesses since May 2020. Prior thereto, he had been Chief Information Officer, Wholesale, Wealth & Investment Management and Innovation from May 2019 to May 2020. He also served as Enterprise Chief Information Officer from March 2017 to May 2019. |

| |

| ELIZABETH RUTLEDGE — | Chief Marketing Officer |

Ms. Rutledge (59)(62) has been Chief Marketing Officer since February 2018. Prior thereto, she had been Executive Vice President, Global Advertising & Media since February 2016 and Executive Vice President, Card Products & Benefits since May 2013. |

| |

| LAUREEN E. SEEGER — | Chief Legal Officer |

Ms. Seeger (59)(62) has been Chief Legal Officer since July 2014. |

| |

| JENNIFER SKYLER — | Chief Corporate Affairs Officer |

Ms. Skyler (44)(47) has been Chief Corporate Affairs Officer since October 2019. Ms. Skyler joined American Express from The We Company,WeWork, where she had beenserved as Chief Communications Officer from January 2018 to September 2019. Prior thereto, she had been Global Head of Public Affairs from January 2016 to January 2018. |

| |

| STEPHEN J. SQUERI — | Chairman and Chief Executive Officer |

Mr. Squeri (61)(64) has been Chairman and Chief Executive Officer since February 2018. Prior thereto, he had been Vice Chairman since July 2015. |

| |

| ANRÉ WILLIAMS — | Group President, Global Merchant and NetworkEnterprise Services |

Mr. Williams (55)(58) has been Group President, Enterprise Services since April 2021. Prior thereto, he had been Group President, Global Merchant and Network Services since February 2018. Prior thereto, he had been PresidentMr. Williams also serves as the Chief Executive Officer of Global Merchant Services and Loyalty since October 2015.American Express National Bank. |

COMPETITION

We compete in the global payments industry with card networks, issuers and acquirers, paper-based transactions (e.g., cash and checks), bank transfer models (e.g., wire transfers and Automated Clearing House, or ACH), as well as evolving and growing alternative mechanisms, systems and products that leverage new technologies, business models and customer relationships to create payment, financing or financingbanking solutions. The payments industry continues to undergo dynamic changes in response to evolving technologies, consumer habits and merchant needs, some of which have accelerated as a result of the pandemic, such as an increased shift to e-commerce and demand for contactlessdigital payments.

As a card issuer, we compete with financial institutions that issue general-purpose credit and debit cards. We also encounter competition fromcards, as well as businesses that issue private label cards, operate mobile wallets, provide payment services or extend credit. We face intense competition in the premium space and for cobrand relationships, as both card issuer and network competitors have targeted high-spending customers and key business partners with attractive value propositions. We also face competition for partners and other differentiated offerings, such as lounge space in U.S. and global hub airports, restaurant reservation capabilities and other experiential offerings to customers. Our banking products also face strong competition, such as with respect to the rates offered on deposits.

Our global card network competes in the global payments industry with other card networks, including, among others, China UnionPay, Visa, Mastercard, JCB, Discover and Diners Club International (which is owned by Discover). We are the fourth largest general-purpose card network globally based on purchase volume, behind China UnionPay, Visa and Mastercard. In addition to such networks, a range of companies globally, including merchant acquirers, processors and web- and mobile-based payment platforms (e.g., Alipay, PayPal and Venmo), as well as regional payment networks (such as the National Payments Corporation of India), carry out some activities similar to those performed by our GMNS business.

The principal competitive factors that affect the card-issuing, merchant and network businesses include:

•The features, value and quality of the products and services, including customer care, rewards programs, partnerships, travel and lifestyle-related benefits, and digital and mobile services, andas well as the costs associated with providing such features and services

•Reputation and brand recognition

•The number, spending characteristics and credit performance of customers

•The quantity, diversity and quality of the establishments where the cards can be used

•The attractiveness of the value proposition to card issuers, merchant acquirers, cardholders, corporate clients and merchants (including the relative cost of using or accepting the products and services, and capabilities such as fraud prevention and data analytics)

•The number and quality of other cards and other forms of payment and financing available to customers

•The success of marketing and promotional campaigns

•The speed of innovation and investment in systems, technologies and product and service offerings

•The nature and quality of expense management tools, electronic payment methods and data capture and reporting capabilities, particularly for business customers

•The security of cardholder, merchant and network partner information

Another aspect of competition is the dynamic and rapid growth of alternative payment and financing mechanisms, systems and products, which include payment facilitators and aggregators, digital payment, open banking and electronic wallet platforms, point-of-sale lenders and buy now, pay later products, real-time settlement and processing systems, financial technology companies, digital currencies developed by both governmentscentral banks and the private sector, blockchain and similar distributed ledger technologies, prepaid systems and gift cards, and systems linked to customer accounts or that provide payment solutions. Various competitors are integrating more financial services into their product offerings and competitors are seeking to attain the benefits of closed-loop, loyalty and rewards functionalities, such as ours.

In addition to the discussion in this section, see “Our operating results may materially suffer because of substantial and increasingly intense competition worldwide in the payments industry” inunder “Risk Factors” for further discussion of the potential impact of competition on our business, and “Our business is subject to evolving and comprehensive government regulation and supervision, which could materially adversely affect our results of operations and financial condition”condition” and “Legal proceedings regarding provisions in our merchant contracts, including non-discrimination and honor-all-cards provisions, could have a material adverse effect on our business and result in additional litigation and/or arbitrations, changes to our merchant agreements and/or business practices, substantial monetary damages and damage to our reputation and brand” inunder “Risk Factors” for a discussion of the potential impact on our ability to compete effectively due to government regulations or if ongoing legal proceedings limit our ability to prevent merchants from engaging in various actions to discriminate against our card products.

SUPERVISION AND REGULATION

Overview

We are subject to evolving and extensive government regulation and supervision in jurisdictions around the world, and the costs of ongoing compliance are substantial. The financial services industry is subject to rigorous scrutiny, high regulatory expectations, a range of regulations and a stringent and unpredictable enforcement environment.

Governmental authorities have focused, and we believe will continue to focus, considerable attention on reviewing compliance by financial services firms and payment systems with laws and regulations, and as a result, we continually work to evolve and improve our risk management framework, governance structures, practices and procedures. Reviews by us and governmental authorities to assess compliance with laws and regulations, by governmental authorities, as well as our own internal reviews to assess compliance with internal policies, including errors or misconduct by colleagues or third parties or control failures, have resulted in, and are likely to continue to result in, changes to our products, practices and procedures, restitution to our customers and increased costs related to regulatory oversight, supervision and examination. We have also been subject to regulatory actions and may continue to be the subject of such actions, including governmental inquiries, investigations, enforcement proceedings and the imposition of fines or civil money penalties, in the event of noncompliance or alleged noncompliance with laws or regulations. In addition,For example, as previously disclosed, we are cooperating with governmental investigations related to certain of our historical sales practices, which are described in more detail in Note 12 to the “Consolidated Financial Statements.” External publicity concerning investigations can increase the scope and scale of those investigations and lead to further regulatory inquiries.

Policymakers around the world continue to propose and adopt new and increasingly complex laws and regulations governing a wide variety of issues that may impact our business or change our operating environment in substantial and unpredictable ways. For example, legislators and regulators in various countries in which we operate have focused on the offering of consumer financial products and the operation of payment networks, resulting in changes to certain practices or pricing of card issuers, merchant acquirers and payment networks, and, in some cases, the establishment of broad and ongoing regulatory oversight regimes.

The following discussion summarizes elements of the extensive regulatory environment in which we operate; it does not purport to be complete or to describe all of the laws or regulations to which we are subject or all possible or proposed changes in laws or regulations that may become applicable to us. See “Operational and Compliance/Legal Risks” under “Risk Factors—Legal, Regulatory and Compliance Risks”Factors” for a discussion of the potential impact legislativethat changes in applicable law or regulation, and in their interpretation and application by regulatory changesagencies and other governmental authorities, may have on our business, results of operations and financial condition.

Banking Regulation

FederalAmerican Express entities are subject to banking regulation in the United States and in certain jurisdictions internationally. U.S. federal and state banking laws, regulations and policies extensively regulate the Company, (which, for purposes of this section, refers to American Express Company as a bank holding company), TRS and our U.S. bank subsidiary, American Express National Bank (AENB). For purposes of this Supervision and Regulation section, the “Company” refers only to American Express Company, a bank holding company, and does not include its subsidiaries. Both the Company and TRS are subject to comprehensive consolidated supervision, regulation and examination by the Federal Reserve and AENB is supervised, regulated and examined by the Office of the Comptroller of the Currency (OCC). The Company and its subsidiaries are also subject to the rulemaking, enforcement and examination authority of the Consumer Financial Protection Bureau (CFPB). Banking regulators have broad examination and enforcement power, including the power to impose substantial fines, limit dividends and other capital distributions, restrict operations and acquisitions and require divestitures, any of which could compromise our competitive position. Many aspects of our business also are subject to rigorous regulation by other U.S. federal and state regulatory agencies and by non-U.S. government agencies and regulatory bodies. For example, non-U.S. regulators supervising our international regulated financial institutions use many of the same principles of regulation and supervision that are used by U.S. federal bank regulators.

Activities

The BHC Act generally limits bank holding companies to activities that are considered to be banking activities and certain closely related activities. As noted above, each of the Company and TRS is a bank holding company and each has elected to become a financial holding company, which is authorized to engage in a broader range of financial and related activities. In order to remain eligible for financial holding company status, we must meet certain eligibility requirements. Those requirements include that each of the Company and AENB must be “well capitalized” and “well managed,” and AENB must have received at least a “satisfactory” rating on its most recent assessment under the Community Reinvestment Act of 1977 (the CRA). The Company and TRS engage in various activities permissible only for financial holding companies, including, in particular, providing travel agency

services, acting as a finder and engaging in certain insurance underwriting and agency services. If the Company fails to meet eligibility requirements for financial holding company status, it and its subsidiaries are likely to be barred from engaging in new types of financial activities or making certain types of acquisitions or investments in reliance on its status as a financial holding company, and ultimately could be required to either discontinue the broader range of activities permitted to financial holding companies or divest AENB. In addition, the Company and its subsidiaries are prohibited by law from engaging in practices that the relevant regulatory authority deemsauthorities deem unsafe or unsound (which such authorities generally interpret broadly). and regulatory authorities have discretion in determining whether new or modified activities can be conducted in a safe and sound manner.

Acquisitions and Investments

Applicable federal and state laws place limitations on the ability of persons to invest in or acquire control of us without providing notice to or obtaining the approval of one or more of our regulators. In addition, we are subject to banking laws and regulations that limit our investments and acquisitions and, in some cases, subject them to the prior review and approval of our regulators, including the Federal Reserve and the OCC. Federal banking regulators have broad discretion in evaluating proposed acquisitions and investments that are subject to their prior review or approval.

Financial Regulatory ReformEnhanced Prudential Standards

In October 2019,The Company is subject to the U.S. federal bank regulatory agencies finalizedagencies’ rules that tailor the application of the enhanced prudential standards to bank holding companies and depository institutions (the Tailoring Rules) pursuant to the amendments to the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd Frank) introduced by the Economic Growth, Regulatory Relief, and Consumer Protection Act. The Tailoring Rules assign each U.S. bank holding company with $100 billion or more in total consolidated assets,assets. Under these rules, each such bank holding company, as well as its bank subsidiaries, is assigned to one of four categories based on its status as a U.S. global systemically important banking organization and five other risk-based indicators: (i) size,total assets, (ii) cross-jurisdictional activity, (iii) non-bank assets, (iv) off-balance sheet exposure, and (v) weighted short-term wholesale funding.

funding, with the most stringent requirements applying to Category I firms and the least stringent requirements applying to Category IV firms. Under the Tailoring Rules,these rules, the Company (and pursuant to the Tailoring Rules, its depository institution subsidiary, AENB) is currently subject to Category IV standards.

Because a firm’s categorization under However, changes in the Tailoring Rules is determined by, and can change over time dependent upon, how the firm measures against the risk-based indicator thresholds, we are required to monitor and periodically reportlevels of these risk-based indicators and there can be no assurance thatat the Company will continuecould result in changes to beour regulatory tailoring category. Category III firms include those firms with greater than $250 billion but less than $700 billion in total consolidated assets, calculated based on a four-quarter trailing average. Our total consolidated assets were $251 billion and $261 billion as of September 30 and December 31, 2023, respectively, and, accordingly, we anticipate becoming a Category IVIII firm in 2024. Category III firms are subject to heightened capital, liquidity and prudential requirements, single-counterparty credit limits and additional stress tests, which in some cases are subject to a transition period following a financial institution becoming a Category III firm. Moreover, further changes in the future.risk-based indicators described above, such as if we have $75 billion or more in cross-jurisdictional activity (calculated based on a four-quarter trailing average), could result in us becoming a Category II firm and subject to more stringent capital, liquidity and prudential requirements. Our cross-jurisdictional activity was $67 billion as of December 31, 2023, and the four-quarter trailing average was $60 billion.

Capital and Liquidity Regulation

Capital Rules

The Company and AENB are required to comply with the applicable capital adequacy rules established by federal banking regulators. These rules are intended to ensure that bank holding companies and depository institutions (collectively, banking organizations) have adequate capital given their level of assets and off-balance sheet obligations. The federal banking regulators’ current capital rules (the Capital Rules) implement the Basel Committee on Banking Supervision’s (the Basel Committee) framework for strengthening international capital regulation, known as Basel III. For additional information regarding our capital ratios, see “Consolidated Capital Resources and Liquidity” under “MD&A.”

Under the Capital Rules, banking organizations are required to maintain minimum ratios for Common Equity Tier 1 (CET1)(CET1 capital), Tier 1 capital (that is, CET1 capital plus additional Tier 1 capital) and Total capital (that is, Tier 1 capital plus Tier 2 capital) to risk-weighted assets. We report our capital adequacy ratios using risk-weighted assets calculated under the standardized approach. As a Category IV firm, wefirms such as us and Category III firms are not subject to the advanced approaches capital requirements.requirements, whereas Category II firms are subject to the advanced approaches capital requirements under current capital rules, which introduce additional complexities in the methodologies used to calculate risk-weighted assets for purposes of determining capital adequacy ratios.

On July 27, 2023, the Basel Committee published standardsU.S. federal bank regulatory agencies issued a notice of proposed rulemaking that among other things,would significantly revise U.S. regulatory capital requirements for large banking organizations, including the Company and AENB. The proposed rules would apply a new expanded risk-based approach to calculating risk-based capital ratios, and large banking organizations would be required to calculate their risk-based capital ratios under both (i) the standardized approach and (ii) the expanded risk-based approach and use the lower of the two ratio calculations to determine binding capital constraints under each risk-based capital ratio. The expanded risk-based approach to calculating risk-weighted assets would apply more granular risk-weighting methodologies for credit risk, (including by recalibratinginclude a new standardized methodology for operational risk, weightsinclude new approaches for calculating market and introducingcredit valuation adjustment risk and revise the treatment of equity exposures not subject to market risk capital requirements. The new approach to calculating market risk also would apply to calculations under the standardized approach. The methodology for operational risk would include differential treatment of fee and other non-interest revenues as compared to interest income for purposes of determining operational risk-weighted assets. The proposed rules would also include additional credit risk capital requirements for certain “unconditionally cancellable commitments” such as unused credit cardportions of committed lines of credit)credit (e.g., credit cards), and providewould create a new standardized calculationproxy methodology to assign capital requirements to credit exposure on products that carry no pre-set spending limits such as charge cards.

Under the proposal, the revisions would become effective on July 1, 2025, subject to a three-year transition period for operational risk capital requirements. If adoptedcertain provisions, including phasing in the United Statesuse of risk-weighted assets under the expanded risk-based approach. While the U.S. federal bank regulatory agencies have solicited comments on the proposal and the rule may not be adopted as issued byproposed, based on a preliminary analysis, we estimate that the Basel Committeeincrease in our risk-weighted assets under the expanded risk-based approach as currently proposed could consume the capital buffer between our minimum regulatory requirements and applicableour current CET1 risk-based capital ratio. See below for additional information on our minimum CET1 regulatory requirement and “Consolidated Capital Resources and Liquidity — Capital Strategy” under “MD&A” for additional information on our current CET1 risk-based capital ratio. This estimated impact reflects our current understanding of the proposal, the application to us,our businesses as currently conducted and the new standardscurrent composition of our balance sheet, and therefore does not reflect the impact of any changes we may make in the future as a result of the expanded risk-based approach or otherwise. The ultimate impact will depend on the final rulemaking, future minimum regulatory requirements as well as management decisions regarding our product constructs, capital distributions and target capital levels, and the actual impact of any final rule could result in higher capital requirements for us.materially differ from our current estimate.

In December 2018, federal banking regulators issued a final rule that provides an optional three-year phase-in period for the adverse regulatory capital effects of adopting the Current Expected Credit Loss (CECL) methodology pursuant to new accounting guidance for the recognition of credit losses on certain financial instruments, which became effective January 1, 2020. In August 2020, federal banking regulators issued a final rule that provides an option to delay the estimated impact of the adoption of the CECL methodology on regulatory capital for up to two years, followed by the three-year phase-in period.period at 25 percent once per year beginning in January 1, 2022. We elected to adoptdelay the two-year delayrecognition of $0.7 billion of reduction in regulatory capital from the adoption of the CECL methodology for two years, followed by the three-year phase-in period. Therefore,As of January 1, 2024, the Company will begin phasinghas phased in the cumulative amount that is not recognized in regulatory capital at 2575 percent per year beginning January 1, 2022.of such amount. See "Critical“Critical Accounting Estimates"Estimates” under "MD&A"“MD&A” for additional information on CECL.

The Company and AENB must each maintain CET1 capital, Tier 1 capital and Total capital ratios of at least 4.5 percent, 6.0 percent and 8.0 percent, respectively. On top of these minimum capital ratios, the Company is subject to a dynamic stress capital buffer (SCB) composed entirely of CET1 capital with a floor of 2.5 percent and AENB is subject to a static 2.5 percent capital conservation buffer (CCB). The SCB equals (i) the difference between a bank holding company’s starting and minimum projected CET1 capital ratios under the supervisory severely adverse scenario under the Federal Reserve'sReserve’s stress tests described below, plus (ii) one year of planned common stock dividends as a percentage of risk-weighted assets.

In August 2020,On July 27, 2023, the Federal Reserve confirmed the SCB requirement for the Company was set atof 2.5 percent. A bank holding company’s SCB requirement is generally effective on October 1 of each year and will remainpercent, which remained unchanged from the level announced in effect through September 30 of the following year unless it is reset in connection with resubmission of a capital plan, as discussed below.August 2022. As a result, the effective minimum ratios for the Company (taking into account the SCB requirement) and AENB (taking into account the CCB requirement) are 7.0 percent, 8.5 percent and 10.5 percent for the CET1 capital, Tier 1 capital and Total capital ratios, respectively. Banking organizations whose ratios of CET1 capital, Tier 1 Capitalcapital or Total capital to risk-weighted assets are below these effective minimum ratios face constraints on discretionary distributions such as dividends, repurchases and redemptions of capital securities, and executive compensation. The capital distribution restrictions for the first quarter of 2021 discussed under “Stress Testing and Capital Planning” below are in addition to the SCB distribution constraints forA bank holding companies at leastcompany’s SCB requirement is effective on October 1 of each year and will remain in effect through March 31, 2021. TheSeptember 30 of the following year unless it is reset in connection with resubmission of a capital plan, as discussed below.

Category III firms are also subject to (i) if enacted by the Federal Reserve, is expecteda CET1 countercyclical capital buffer requirement of up to announce by March 31, 2021 any recalibrationan additional 2.5 percent and (ii) a minimum supplementary leverage ratio of the SCB requirements announced in August 2020.3.0 percent that takes into account both on‐balance sheet and certain off‐balance sheet exposures.

We are also required to comply with minimum leverage ratio requirements. The leverage ratio is the ratio of a banking organization’s Tier 1 capital to its average total consolidated assets (as defined for regulatory purposes). All banking organizations are required to maintain a leverage ratio of at least 4.0 percent.

Liquidity Regulation

The Federal Reserve’s enhanced prudential standards rule includes heightened liquidity and overall risk management requirements. The rule requires the maintenance of a liquidity buffer, consisting of highly liquid assets, that is sufficient to meet projected net outflows for 30 days over a range of liquidity stress scenarios, and a minimum liquidity coverage ratio (LCR) that measures a firm’s high-quality liquid assets to its projected net outflows. Under the Tailoring Rules, Category IV firms with less than $50 billion in weighted short-term wholesale funding, such as the Company, are not subject to any LCR requirement.

A second standard provided for in the Basel III liquidity framework, referred to as the net stable funding ratio (NSFR), requires a minimum amount of longer-term funding based on the assets and activities of banking entities. Under the final NSFR rule published in October 2020,As a Category IV firmsfirm with less than $50 billion in weighted short-term wholesale funding, we are not currently subject to a specific LCR or NSFR requirement; however, as described above, we anticipate becoming a Category III firm in 2024. Category III firms and their depository institution subsidiaries are subject to LCR and NSFR requirements but at a reduced level (that is, at 85 percent of the full requirements), unless they have $75 billion or more in weighted short-term wholesale funding, in which case the full requirements would apply. Category II firms and their depository institution subsidiaries are subject to the full requirements of the LCR and NSFR, as well as a requirement to submit a liquidity monitoring report on a daily (rather than monthly) basis.

Proposed Long-Term Debt Requirements

On August 29, 2023, the U.S. federal bank regulatory agencies issued a notice of proposed rulemaking that, if adopted as proposed, would require covered bank holding companies such as the Company are not subject to any NSFR requirement.issue and maintain minimum amounts of eligible external long-term debt with specific terms for purposes of absorbing losses or recapitalizing the covered bank holding company and its operating subsidiaries. The notice of proposed rulemaking also proposed requiring certain insured depository institutions that have at least $100 billion in consolidated assets, such as AENB, to maintain minimum amounts of eligible internal long-term debt for purposes of absorbing losses or recapitalizing the insured depository institution.

Stress Testing and Capital Planning

Under the Federal Reserve’s regulations, the Company is subject to supervisory stress testing requirements that are designed to evaluate whether a bank holding company has sufficient capital on a total consolidated basis to absorb losses and support operations under adverse economic conditions. As part of the Comprehensive Capital Analysis and Review (CCAR), the Federal Reserve uses pro-forma capital positions and ratios under such stress scenarios to determine the size of the SCB for each CCAR participating firm.

Because the Company is currently a Category IV firm, the Company was subject to the Federal Reserve’s supervisory stress tests in 2020 and will beit is required to participate in the supervisory stress tests every other year thereafter.

We areand is subject to the Federal Reserve’s supervisory stress tests in 2024. The Company is required to develop and submit to the Federal Reserve an annual capital plan. In January 2021, the Federal Reserve finalized changes to the capital plan rule, which will, among other things, provide firms subject toon or before April 5 of each year.

For Category IV standards additional flexibility to develop their capital plans. In addition, these changes provide that for Category IV firms, such as the Company, the portion of the SCB based on the Federal Reserve'sReserve’s supervisory stress tests will beis calculated every other year. During a year in which a Category IV firm does not undergo a supervisory stress test, the firm will receivereceives an updated SCB that reflects the firm'sfirm’s updated planned common stock dividends. A Category IV firm will also be able tocan elect to participate in the supervisory stress test in an “off year” and consequently receive an updated SCB. The Company must notify the Federal Reserve by April 5, 2021 if it elects to participate in the 2021 supervisory stress test. As part of the Comprehensive Capital Analysis and Review (CCAR), the Federal Reserve evaluates whether the Company has sufficient capital to continue operations by assessing our pro-forma capital position and ratios under a scenario of economic and financial market stress, and uses that information to determine the size of the SCB for each CCAR participating firm.

Due to the continued economic uncertainty from the coronavirus pandemic, in June 2020, the Federal Reserve required all bank holding companies participating in CCAR to resubmit their capital plans in November 2020. In addition, the Federal Reserve prohibited share repurchases in the third and fourth quarters of 2020 for all bank holding companies participating in CCAR and allowed them to pay common stock dividends provided (a) they did not increase the amount of the dividend and (b) the dividends did not exceed the average of a firm’s net income for the four preceding calendar quarters. On December 18, 2020, the Federal Reserve released the results of its second round of supervisory stress tests for all bank holding companies participating in CCAR based on economic scenarios reflecting changes in financial markets and the macroeconomic outlook. The Federal Reserve announced that it would allow bank holding companies participating in CCAR to pay common stock dividends and repurchase common stock in the first quarter of 2021 provided (a) the dividends and repurchases, in the aggregate, do not exceed the average of a firm’s net income for the four preceding calendar quarters and (b) the firm does not increase the amount of its common stock dividends beyond the level paid in the second quarter of 2020. The Federal Reserve also announced that it would permit stock repurchases equal to the amount of share issuances related to expensed employee compensation. For additional information regarding our capital distributions, see “Consolidated Capital Resources and Liquidity” under “MD&A.”

We may be required to revise and resubmit our capital plan following certain events or developments, such as a significant acquisition or an event that could result in a material change in our risk profile or financial condition. If we are required to resubmit our capital plan, we must receive prior approval from the Federal Reserve for any capital distributions (including common stock dividend payments and share repurchases), other than a capital distribution on a newly issued capital instrument.

Category III firms are subject to annual supervisory stress tests, with the SCB calculated each year, and must conduct company‐run stress tests every other year (commonly referred to as Dodd‐Frank Act Stress Tests or “DFASTs”). Category II firms must conduct company-run stress tests on an annual basis rather than every other year.

Dividends and Other Capital Distributions

The Company and TRS, as well as AENB and the Company’s insurance and other regulated subsidiaries, are limited in their ability to pay dividends by statutes, regulations and supervisory policy.

Common stock dividend payments and share repurchases by the Company are subject to the oversight of the Federal Reserve, as described above. The Company will be subject to limitations and restrictions on capital distributions if, among other things, (i) the Company'sCompany’s regulatory capital ratios do not satisfy applicable minimum requirements and buffers or (ii) the Company is required to resubmit its capital plan.

In general, federal laws and regulations prohibit, without first obtaining the OCC’s approval, AENB from making dividend distributions to TRS, if such distributions are not paid out of available recent earnings or would cause AENB to fail to meet capital adequacy standards. In addition to specific limitations on the dividends AENB can pay to TRS, federal banking regulators have authority to prohibit or limit the payment of a dividend if, in the banking regulator’s opinion, payment of a dividend would constitute an unsafe or unsound practice in light of the financial condition of the institution.

Prompt Corrective Action

The Federal Deposit Insurance Act (FDIA) requires, among other things, that federal banking regulators take prompt corrective action in respect of depository institutions insured by the FDIC (such as AENB) that do not meet minimum capital requirements. The FDIA establishes five capital categories for FDIC-insured banks: well capitalized, adequately capitalized, undercapitalized, significantly undercapitalized and critically undercapitalized. The FDIA imposes progressively more restrictive constraints on operations, management and capital distributions, depending on the capital category in which an institution is classified. In order to be considered “well capitalized,” AENB must maintain CET1 capital, Tier 1 capital, Total capital and Tier 1 leverage ratios of 6.5 percent, 8.0 percent, 10.0 percent and 5.0 percent, respectively.

Under the FDIA, AENB could be prohibited from accepting brokered deposits (i.e., deposits raised through third-party brokerage networks) or offering interest rates on any deposits significantly higher than the prevailing rate in its normal market area or nationally (depending upon where the deposits are solicited), unless (1) it is well capitalized or (2) it is adequately capitalized and receives a waiver from the FDIC. A portion of our outstanding U.S. retail deposits are considered brokered deposits for bank regulatory purposes. If a federal regulator determines that we are in an unsafe or unsound condition or that we are engaging in unsafe or unsound banking practices, the regulator may reclassify our capital category or otherwise place restrictions on our ability to accept or solicit brokered deposits.

On December 15, 2020, the FDIC finalized a rule intended to update and modernize the FDIC’s brokered deposit regulations. The final rule, among other things, expands the definition of “deposit broker” and updates the interest rate restrictions for less than well capitalized banks. The final rule is expected to become effective on April 1, 2021.

Resolution Planning

Pursuant to Dodd Frank, certainCertain bank holding companies are required to submit resolution plans to the Federal Reserve and FDIC providing for the company’s strategy for rapid and orderly resolution in the event of its material financial distress or failure. However, in connection with the release of the Tailoring Rules, the Federal Reserve and FDIC finalized rules in October 2019 which, among other things, adjust the review cycles and applicability of the agencies’ resolution planning requirements. Under these rules, Category IV firms such as the Company are not required to submit a holding company resolution plan.plan, while Category III firms are required to submit a holding company resolution plan every three years.

AENB continues to be required to prepare and provide a separate resolution plan to the FDIC that would enable the FDIC, as receiver, to effectively resolve AENB under the FDIA in the event of failure. The FDIC issued an Advance Notice of Proposed RulemakingUnder the FDIC’s rule and its accompanying June 2021 statement on potential revisions to this separate resolution plan requirementplans for insured depository institutions, in April 2019 and temporarily suspended resolution planning requirements for insured depository institutions. In January 2021,institutions with $100 billion or more in assets, such as AENB, are required to submit resolution plans on a three-year cycle. AENB submitted its most recent resolution plan in December 2022, as required.

On August 29, 2023, the FDIC lifted the moratorium on resolution plan submissions forissued a notice of proposed rulemaking that would require insured depository institutions with $100 billion or more in assets, including AENB, and will provide at least 12-months advance notice to firms required to submit full resolution plans.plans every two years with interim supplements in non-submission years. Under the proposal, resolution plans would be subject to more stringent standards with respect to their assumptions and content, as well as enhanced credibility standards for the FDIC’s evaluation of resolution plans and expanded expectations regarding engagement and capabilities testing.

Orderly Liquidation Authority

The Company could become subject to the Orderly Liquidation Authority (OLA), a resolution regime under which the Treasury Secretary may appoint the FDIC as receiver to liquidate a systemically important financial institution, if the Company is in danger of default and is determined to present a systemic risk to U.S. financial stability. As under the FDIC resolution model, under the OLA, the FDIC has broad power as receiver. Substantial differences exist, however, between the OLA and the FDIC resolution model for depository institutions,U.S. Bankruptcy Code, including the right of the FDIC under the OLA to disregard the strict priority of creditor claims in limited circumstances, the use of an administrative claims procedure to determine creditor claims (as opposed to the judicial procedure used in bankruptcy proceedings), and the right of the FDIC to transfer claims to a “bridge” entity.

The FDIC has developed a strategy under OLA, referred to as the “single point of entry” or “SPOE” strategy, under which the FDIC would resolve a failed financial holding company by transferring its assets (including shares of its operating subsidiaries) and, potentially, very limited liabilities to a “bridge” holding company; utilize the resources of the failed financial holding company to recapitalize the operating subsidiaries; and satisfy the claims of unsecured creditors of the failed financial holding company and other claimants in the receivership by delivering securities of one or more new financial companies that would emerge from the bridge holding company. Under this strategy, management of the failed financial holding company would be replaced and its shareholders and creditors would bear the losses resulting from the failure.

FDIC Powers upon Insolvency of AENB