| | 2019 individual performance factor | | | | | | | | The individual performance factor

for the CEO has a cap, so his

individual performance factor

cannot exceed the corporate

performance factor. This ensures the payout factor for

the CEO aligns with the CEO’s

overall responsibility for CP’s

performance. | | | | 155 | % | | | | | | | | | | | | 175 | % | | | | | | | | | | | | 175 | % | | | | | | | | | | | | 150 | % | | | | | | | | | | | | 150 | % | | | | | | | | | | | | 150 | % | | | | | | | | | | | | | | | | | | | | | | The Compensation Committee sets the individual performance factor for the CEO. The CEO reviews the performance of his direct reports against their objectives, and recommends their individual performance factors to the Compensation Committee. | | | | | | | | Total |

| | First main track | 12,683 |

| Second and other main track | 1,088 |

| Passing sidings and yard track | 4,353 |

| Industrial and way track | 779 |

| Total track miles | 18,903 |

|

Rail Facilities

CP operates numerous facilities including: terminals for intermodal, transload, automotive and other freight; classification rail yards for train-building and switching, storage-in-transit and other activities; offices to administer and manage operations; dispatch centres to direct traffic on the rail network; crew quarters to house train crews along the rail line; shops and other facilities for fuelling; maintenance and repairs of locomotives; and facilities for maintenance of freight cars and other equipment. The Company continues to invest in terminal upgrades and new facilities to accommodate incremental growth in volumes, such as creating additional capacity with the redesign of the classification yard at Alyth in Calgary. The Company’s average terminal dwell is an indicator of efficient utilization of yard capacity, discussed in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, Performance Indicators. Typically in all of our major yards, CP Police Services has offices to ensure the safety and security of the yards and operations.

CP 2019 ANNUAL REPORT/ 24

The following table includes the major yards, terminals and transload facilities on CP's network:

| | | | Major Classification Yards | Major Intermodal Terminals | Transload Facilities | |

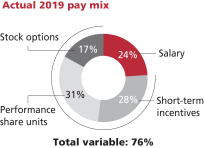

See the profiles beginning on page 28 to read about each executive’s individual performance in 2019. Compensation Committee Discretion The Compensation Committee has developed principles for the use of discretion. Adjustments should not relieve management from the consequences of their decision making. Adjustments should also neither reward nor penalize management for decisions on discretionary transactions, events outside their control (such as foreign exchange rates and fuel prices that are beyond the assumptions used in the planning process) or transactions outside normal corporate planning and budgeting. As a result, the Compensation Committee can reduce the corporate performance factor for any executive officer as it deems appropriate, as long as it follows the principles. The Board can also use its discretion to adjust the targets and payouts up or down, following the principles set out by the Compensation Committee. The Compensation Committee did not exercise any such discretion in 2019. Long-term incentive awards focus executives on medium and longer-term performance to create sustainable shareholder value. Target awards are set based on the competitive positioning of each executive’s compensation and the practices of companies in our peer group in order to attract and retain experienced railroad executives with highly specialized skills. Vancouver, British Columbia | Vancouver, British Columbia | Vancouver, British Columbia | Calgary, Alberta | Calgary, Alberta | Toronto, Ontario | Edmonton, Alberta | Edmonton, Alberta | Hamilton, Ontario | Moose Jaw, Saskatchewan | Regina, Saskatchewan | Lachine, Québec | Winnipeg, Manitoba | Winnipeg, Manitoba | | Toronto, Ontario | Vaughan, Ontario | Performance share units (60%) | | Stock options (40%) | | What they are | | • notional share units that vest at the end of three years based on absolute and relative performance and the price of our shares | | • right to buy CP shares at a specified price in the future | | Payout | | • cliff vest at the end of three years based on performance against threepre-defined financial and market metrics • no guarantee of a minimum payout | | • vest 25% every year beginning on the anniversary of the grant date • expire at the end of seven years • only have value if our share price increases above the exercise price |

| | | | | Montréal, Québec | Montréal, Québec | Performance share units (60%) | | Stock options (40%) | | Dividend equivalents | | • earned quarterly and compound over the three-year period | | • do not earn dividend equivalents | | Restrictions | | • must meet minimum level of performance • performance multiplier is capped for exceptional performance | | • cannot be exercised during a blackout period | | If the executive retires | | • must give three months’ notice • award continues to vest and executive is entitled to receive the full value as long as they have worked for six months of the performance period, otherwise the award is forfeited | | • must give three months’ notice • options continue to vest, but expire five years after the retirement date or on the normal expiry date, whichever is earlier |

Stock options are usually granted in January immediately after the fourth quarter financial statement blackout period ends, while performance share units (PSUs) are awarded in February after the Compensation Committee has reviewed theyear-end financial results in detail. Grants are also made for special situations like retention or new hires. Special grants can include PSUs, RSUs, DSUs or stock options. These grants are made on the first Tuesday of the month following approval. If we are in a blackout period, the grant is made after the blackout has been lifted. | | | Chicago, IllinoisNon-Compete andNon-Solicitation | Chicago, Illinois | | CP is mindful that the demand for experienced and talented railroaders is high, particularly those with backgrounds in precision scheduled railroading. To manage near-term retention risk, the company’s long-term incentive award agreements containnon-compete, non-solicitation and other restrictive clauses, includingnon-disclosure restrictions. Non-compete andnon-solicitation provisions will apply if a recipient fails to comply with certain commitments for atwo-year period following the end of employment. | | |

2019 long-term incentive awards To determine the appropriate value of long-term incentive grants provided to the NEOs, the Compensation Committee considers the practices of our comparator group and external market data, as well as internal factors including executive retention, dilutive impact and long-term value creation. The table below shows the 2019 long-term incentives awarded to the NEOs. | | | | | St. Paul, Minnesota | Minneapolis, Minnesota | Target as a % of base salary | | | | | 500% | | | | | 275% | | | | | 225% | | | | | 200% | | | | | 225% | | | | | 225% | |

Effective January 1, 2019, Mr. Creel’s long-term incentive target was increased to 600% of his base salary; however, consistent with Mr. Creel’s 2016 employment agreement, his 600% LTI target has been reduced by 100% until the end of 2021 to fund an upfront performance grant that he received in 2017. Therefore, his target was 500% of his base salary in 2019.

Equipment| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | incentive | | | | | | | | | | | award | | | | | | | | | | | | | | | | | (grant value) ($) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 9,512,269 | | | | | | | | 5,870,208 | | | | 21,901 | | | | | | | | 3,642,061 | | | | 54,202 | | | | | 2,531,053 | | | | | | | | 1,552,110 | | | | 5,788 | | | | | | | | 978,943 | | | | 16,313 | | | | | 1,893,801 | | | | | | | | 1,196,771 | | | | 4,465 | | | | | | | | 697,030 | | | | 10,453 | | | | | 1,313,416 | | | | | | | | 810,534 | | | | 3,024 | | | | | | | | 502,882 | | | | 7,484 | | | | | 959,877 | | | | | | | | 604,824 | | | | 2,167 | | | | | | | | 355,053 | | | | 5,293 | | | | | 1,643,916 | | | | | | | | 1,014,508 | | | | 3,785 | | | | | | | | 629,408 | | | | 9,367 | |

CP's equipment includes: owned

See the summary compensation table on page 43 for details about how we calculated the grant date fair values of the PSUs and leased locomotivesstock options. Both were calculated in accordance with FASB ASC Topic 718. The grant value of the awards based on the NYSE trading price has been converted to Canadian dollars using a 2019 average exchange rate of $1.3269. On February 14, 2019, additional stock options were granted to Mr. Brooks as a result of his promotion to Executive Vice-President. On September 3, 2019, additional PSUs and railcars; heavy maintenance equipmentstock options were granted to Mr. Redd as a result of his promotion to Executive Vice-President. PSU awards focus executives on achieving medium-term goals within a three-year performance period. The Board sets performance measures, thresholds and machinery; other equipmenttargets at the beginning of the performance period. The number of units that vest is based on our performance over the three-year period. We must achieve threshold performance on a measure, otherwise the payout factor for that measure is zero and tools ina portion of the award is forfeited. If performance is exceptional on a measure, the Board may approve a payout of up to 200%. PSUs earn additional units as dividend equivalents at the same rate as dividends paid on our shops, offices and facilities; and vehicles for maintenance, transportation of crews, and other activities. In this section, owned equipment includes units acquired by CP, equipment leased to third parties, and units held under finance leases, and leased equipment includes units under a short-term or long-term operating lease.shares.

The Company’s locomotive fleetaward is composedpaid out in cash based on the number of largely high-adhesion alternating current locomotivesunits that are more fuel efficientearned and reliable and have superior hauling capacity as compared with standard direct current locomotives. The Company is continuing a modernization program on severalthe average closing share price for the 30 trading days prior to the end of the oldest locomotivesperformance period on the TSX or NYSE, as applicable. The award may be paid out in shares purchased on the open market, on the CEO’s recommendation, using theafter-tax value.The performance period for the 2019 PSU awards is January 1, 2019 to December 31, 2021. In 2019, CP returned to measuring total shareholder return (TSR) performance based on the Class 1 Railways and the S&P TSX 60 Index from the S&P Road and Rail Index and the S&P TSX Capped Industrial Index. The Class 1 Railways align us more closely to our industry peers. Additionally, the S&P TSX 60 Index is a more common benchmark for the broader investment community and a more widely recognized index than the S&P TSX Capped Industrial Index. Performance will be assessed against the measures in the fleet in ordertable below. Awards will be prorated if results fall between threshold and exceptional. | | | | | | | | | | | | | | | | | | | | 2019 PSU performance measures | | Why the measure is important | | | | | | | | | | | | | PSU three-year average return on invested capital (ROIC) Net operating profit after tax divided by average invested capital | | Focuses executives on the effective use of capital as we grow Ensures shareholders’ capital is employed in a value-accretive manner | | | 15.3% | | | | 16% | | | | 16.4% | | | | 70% | | Measured over three years. The percentile ranking of CP’s TSX Compound Annual Growth Rate (CAGR) relative to the companies that make up the S&P/TSX 60 | | Compares our TSR on the TSX to the broader S&P/TSX60 to reflect our progress relative to the Canadian market Aligns long-term incentive compensation with long-term shareholder interests | | | 25th

percentile |

| | | 50th

percentile |

| | | 75th

percentile |

| | | 15% | | Measured over three years. The ordinal ranking of CP’s NYSE CAGR relative to the Class 1 Railroads | | Compares our TSR on the NYSE to the publicly traded Class 1 Railroads to ensure we are competitive against our primary competitors. Aligns long-term incentive compensation with long-term shareholder interests | | | 4th | | | | 3rd | | | | 1st | | | | 15% | |

At the end of the three-year performance period, the starting point for determining relative TSR will be the10-day average closing share price of our shares on the appropriate index prior to improve reliabilityJanuary 1, 2019 and availability,the closing point will be the10-day average closing share price of our shares on the appropriate index prior to January 1, 2022. TSR is adjusted over the period to reflect dividends paid. The payout multiplier is interpolated if our performance falls between 50% and 200%. If results are below the threshold level for any of the performance measures, units for that specific measure will be forfeited. The table below shows the details of the 2019 annual PSU award grant. | | | | | | | | | | | | | | | | | | | | | | | | | | | | 5,870,208 | | | | 21,901 | | | | US$202.00 (NYSE) | | | | | 1,552,110 | | | | 5,788 | | | | $268.16 (TSX) | | | | | 1,196,771 | | | | 4,465 | | | | US$202.00 (NYSE) | | | | | 810,534 | | | | 3,024 | | | | US$202.00 (NYSE) | | | | | 432,874 | | | | 1,615 | | | | US$202.00 (NYSE)

US$234.76 (NYSE) |

| | | | 1,014,508 | | | | 3,785 | | | | US$202.00 (NYSE) | |

On September 3, 2019, additional PSUs were granted to Mr. Redd as well asa result of his promotion to introduce new technologyExecutive Vice-President. The grant value of the PSU awards based on the NYSE trading price have been converted to Canadian dollars using a 2019 average exchange rate of $1.3269. We calculated the number of PSUs to be granted to each executive by dividing the grant value by the theoretical value of a PSU (using the Willis Towers Watson binomial lattice model methodology), applied to our30-day average closing share price on the TSX or the NYSE prior to the fleet. CP’s locomotive productivity,day of the grant. Stock options focus executives on longer term performance. Options have a seven-year term and vest 25% each year beginning on the anniversary date of the grant. The grant price is the last closing price of our common shares on the TSX or the NYSE on the applicable the grant date. Options only have value for the holder if our current share price increases above the grant price. The table below shows the details of the 2019 annual stock option award grant. | | | | | | | | | | | | | | | | | | | | | | | | | | | | 3,642,061 | | | | 54,202 | | | | US$205.31 (NYSE) | | | | | 978,943 | | | | 16,313 | | | | $271.50 (TSX) | | | | | 502,881 | | | | 7,484 | | | | US$205.31 (NYSE) | | | | | 502,882 | | | | 7,484 | | | | US$205.31 (NYSE) | | | | | 268,508 | | | | 3,996 | | | | US$205.31 (NYSE) | | | | | 629,408 | | | | 9,367 | | | | US$205.31 (NYSE) | |

On February 14, 2019, additional stock options were granted to Mr. Brooks as a result of his promotion to Executive Vice-President. On September 3, 2019, additional options were granted to Mr. Redd as a result of his promotion to Executive Vice-President. The grant value of the stock option awards based on the NYSE trading price have been converted to Canadian dollars using a 2019 average exchange rate of $1.3269. We calculated the number of options to be granted to each executive by dividing the grant value by the theoretical value of an option (using the Willis Towers Watson binomial option pricing methodology), applied to our30-day average closing share price on the TSX or the NYSE prior to the day of the grant.

About the stock option plan The management stock option incentive plan (the stock option plan) was introduced in October 2001. Stock options awarded on or after January 1, 2017 have a seven-year term. If the expiry date falls within a blackout period, the expiry date will be extended to 10 business days after the end of the blackout period date. If a further blackout period is imposed before the end of the extension, the term will be extended another 10 days after the end of the additional blackout period. Regular stock options granted before 2017 expire 10 years from the date of grant and generally vest 25% each year over four years, beginning on the anniversary of the grant date. The table below sets out the limits for issuing options under the plan: | | | | | As a % of the number of shares outstanding | Maximum number of shares that may be reserved for issuance to insiders as options | | | Maximum number of options that may be granted to insiders in aone-year period | | | Maximum number of options that may be granted to any insider in aone-year period | | | | | As a % of the number of shares outstanding at the time the shares were reserved | Maximum number of options that may be granted to any person | | |

We measuredilution by determining the number of options available for issuance and the number of options outstanding as a percentage of outstanding shares. Our potential dilution at the end of 2019 was 1.8%. Notwithstanding the limits noted above, the dilution level, measured by the number of options available for issuance as a percentage of outstanding shares continues to be capped, at the discretion of the Board, at 7%. The option grant price is the last closing market price of shares on the grant date on the TSX or the NYSE (for grants after December 15, 2014 depending on the currency of the grant). The table below shows theburn rate for the last three fiscal years, calculated by dividing the number of stock options granted in the fiscal year by the weighted average number of outstanding shares for the year. | | | | | | | | | | | | | | | | | | | | | | | | Number of options granted | | | 369,980 | | | | 282,125 | | | | 224,730 | | Weighted number of shares outstanding | | | 145,863,318 | | | | 142,885,817 | | | | 138,771,939 | | | | | 0.25% | | | | 0.20% | | | | 0.16% | |

The table below shows the options outstanding and available for grant from the Stock Option Plan as at December 31, 2019. | | | | | | | | | | | | | | | | Percentage of outstanding shares | | Options outstanding (as at December 31, 2019) | | | 1,416,346 | | | | 1.03 | % | Options available to grant (as at December 31, 2019) | | | 1,098,707 | | | | 0.80 | % | Shares issued on exercise of options in 2019 | | | 260,267 | | | | 0.19 | % | | | | 224,730 | | | | 0.16 | % |

Since the launch of the stock option plan in October 2001, a total of 18,078,642 shares have been available for issuance under the plan and 15,563,589 shares have been issued through the exercise of options. We do not provide financial assistance to option holders to facilitate the purchase of shares under the stock option plan. There is a double trigger on options so that if there is a change of control and only if an option holder is terminated without cause, all of his or her stock options will vest immediately according to the change in control provisions in the stock option plan.

If an employee retires, the options continue to vest and expire on the original expiry date or five years from retirement, whichever is earlier. If an employee is terminated without cause, the employee has six months to exercise any vested options. If the employee resigns, the employee has 30 days to exercise any vested options. If an employee is terminated with cause, all options are cancelled. Options will continue to vest and expire on the scheduled expiry date if the holder’s employment ends due to permanent disability. If an option holder dies, the options will expire 12 months following his or her death and may be exercised by the holder’s estate. Options can only be assigned to the holder’s family trust, holding corporation or retirement trust, or a legal representative of an option holder’s estate or a person who acquires the option holder’s rights by bequest or inheritance. The CEO, the Chair of the Board and the Compensation Committee chair have authority to grant options to certain employees based on defined parameters, such as the daily average gross ton-miles (“GTMs”) dividedposition of the employee and the expected value of the option award. In 2019, the Compensation Committee authorized a pool of 50,000 options for allocation by daily average operating horsepower,the CEO, who granted 19,456 options to 13 employees to recognize performance and for retention. Making changes to the years ended December 31, 2019, 2018,stock option plan The Board can make the following changes to the stock option plan without shareholder approval: changes to clarify information or to correct an error or omission changes of an administrative or a housekeeping nature changes to eligibility to participate in the stock option plan terms, conditions and mechanics of granting stock option awards changes to vesting, exercise, early expiry or cancellation amendments that are designed to comply with the law or regulatory requirements The Board must receive shareholder approval to make other changes, including the following, among other things: an increase to the maximum number of shares that may be issued under the plan a decrease in the exercise price a grant of options in exchange for, or related to, options being cancelled or surrendered The Board has made two amendments to the stock option plan since it was introduced in 2001: on February 28, 2012, the stock option plan was amended so that a change of control would not trigger accelerated vesting of options held by a participant, unless the person is terminated without cause or constructively dismissed; and on November 19, 2015, the stock option plan was amended to providenet stock settlement as a method of exercise, which allows an option holder to exercise options without the need for us to sell the securities on the open market, resulting in less dilution.

Payout of 2017 was 202, 198, and 201 GTMs per Operating horsepower, respectively. Operating horsepower excludes units offline, tied up or in storage, or in use on other railways, and includes foreign units online. As ofPSU award On December 31, 2019, the Company had 314 locomotives in storage. As a result, the Company does not foresee the need to acquire new locomotives2017 PSU grant for the next several years. Asperiod of January 1, 2017 to December 31, 2019 CP owned or leasedvested and was paid out on February 7, 2020. The NEOs received a payout of 193% on the following locomotive units: award, which includes dividends earned up to the payment date. The table below shows the difference between the actual payout value and the grant value for each NEO. | | | | | | | | | | | Locomotives | Owned |

| Leased |

| Total |

| Average Age (in years) |

| | Line haul | 731 |

| 88 |

| 819 |

| 13 |

| | Road switcher | 560 |

| — |

| 560 |

| 28 |

| | Total locomotives | 1,291 |

| 88 |

| 1,379 |

| 19 |

|

CP’s2017 grant value(2017 PSU award+Dividend equivalents)x2017 PSU performance factorxMarket share price=PSU value($)(# of units)(# of units)(0-200%)($)Keith Creel4,407,78822,294680193%US$245.0114,138,889Nadeem Velani782,3953,903119193%$323.562,517,052John Brooks428,4422,16766193%US$245.011,374,360Laird Pitz394,2371,99461193%US$245.011,264,578Mark Redd367,3491,85857193%US$245.011,178,305Robert Johnson958,7054,849148193%US$245.013,075,226 Closing market share price is calculated on days when both the TSX and NYSE markets are open. For Mr. Velani, the market share price was calculated using $323.56, the average in-service utilization percentage for freight cars, for the years ended30-day closing price of our shares prior to December 31, 2019 2018,on the TSX. For Mr. Creel, Mr. Brooks, Mr. Pitz, Mr. Redd and 2017,Mr. Johnson, the market share price was 81%, 84%, and 84%, respectively. Average in-service utilization is defined asUS$245.01, the average active fleet for the year divided by total cars, excluding company service cars and tank cars as these are utilized only as required for non-revenue movements. As30-day closing price of our shares prior to December 31, 2019 CP ownedon the NYSE, and leased the following unitsvalue of freight cars:these shares were converted to Canadian dollars using theyear-end exchange rate of $1.2988. For comparability, for Mr. Creel, Mr. Brooks, Mr. Pitz, Mr. Redd and Mr. Johnson, the 2017 grant value was converted using an exchange rate of $1.2986. How we calculated the 2017 PSU performance factor | | | | | | | | | Freight cars | Owned | Leased |

| Total | Average Age (in years) |

| | Box car | 2,594 | 250 |

| 2,844 | 30 |

| | Covered hopper | 7,607 | 9,699 |

| 17,306 | 24 |

| | Flat car | 1,461 | 770 |

| 2,231 | 26 |

| | Gondola | 3,648 | 1,440 |

| 5,088 | 21 |

| | Intermodal | 1,319 | 150 |

| 1,469 | 15 |

| | Multi-level autorack | 2,894 | 719 |

| 3,613 | 26 |

| | Company service car | 2,396 | 174 |

| 2,570 | 45 |

| | Open top hopper | 105 | — |

| 105 | 32 |

| | Tank car | 33 | 9 |

| 42 | 12 |

| | Total freight cars | 22,057 | 13,211 |

| 35,268 | 25 |

|

As ofThe PSU performance factor for the three-year period from January 1, 2017 to December 31, 2019 CP owned and leased the following units of intermodal equipment:

| | | | | | | | Intermodal equipment | Owned | Leased |

| Total | Average Age (in years) | | Containers | 8,804 | — |

| 8,804 | 7 | | Chassis | 6,290 | 601 |

| 6,891 | 11 | | Total intermodal equipment | 15,094 | 601 |

| 15,695 | 9 |

Headquarters Office Building

CP owns and operates a multi-building campus in Calgary encompassing the head office building, a data centre, training facility and other office and operational buildings.

The Company's main dispatch centre is located in Calgary, and is the primary dispatching facility in Canada. Rail traffic controllers coordinate and dispatch crews, and manage the day-to-day locomotive management along the network, 24 hours a day, and seven days a week. The operations centre has a complete backup system193%, as shown in the event of any power disruption.

In addition to fully operational redundant systems, CPtable below. The payout value has a fully integrated Business Continuity Centre, should CP's operations centre be affected by any natural disaster, fire, cyber-attack or hostile threat.

CP also maintains a secondary dispatch centre locatedbeen calculated in Minneapolis, where a facility similar toaccordance with the one in Calgary exists. It services the dispatching needs of locomotives and train crews working in the U.S.

Capital Expenditures

The Company incurs expenditures to expand and enhance its rail network, rolling stock and other infrastructure. These expenditures are aimed at improving efficiency and safety of our operations. Such investments are also an integral partterms of the Company's multi-year capital programPSU plan and support growth initiatives. For further details, refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, Liquidity and Capital Resources.the 2017 award agreement.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 3 Year Average Adjusted Return on Invested Capital (1) | | | 14.5% | | | | 15% | | | | 15.5% | | | | | | | | 60% | | | | 200% | | TSR to S&P/TSX Capped Industrial Index | | | 25th

percentile |

| | | 50th

percentile |

| | | 75th

percentile |

| | | 80th

percentile |

| | | 20% | | | | 200% | | TSR to S&P 1500 Road and Rail Index | | | 25th

percentile |

| | | 50th

percentile |

| | | 75th

percentile |

| | | 66.7th

percentile |

| | | 20% | | | | 167% | | | | | | | | | | | | | | | | | | | | | | | | | 193% | |

Encumbrances

Refer to Item 8. Financial Statements and Supplementary Data, Note 18 Debt, for information on the Company's finance lease obligations and assets held as collateral under these agreements.

| (1) | Adjusted Return on Invested Capital is a non-GAAP measure. Non-GAAP measures are defined and reconciled on pages 54-62 of CP’s Annual Report on Form 10-K for the year ended December 31, 2019. |

ITEM 3. LEGAL PROCEEDINGSFor further details, refer to Item 8. Financial Statements and Supplementary Data, Note 26 Commitments and contingencies.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

KEITH E. CREEL PRESIDENT AND CHIEF EXECUTIVE OFFICERCP 2019 ANNUAL REPORT/ 26

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

Our executive officers are appointed by the Board of Directors and they hold office until their successors are appointed, subject to resignation, retirement or removal by the Board of Directors. There are no family relationships among our officers, nor any arrangement or understanding between any officer and any other person pursuant to which the officer was selected. As of the date of this filing, the executive officers’ names, ages and business experience are:

| | |  | | Name, Age and Position | Business Experience | KeithMr. Creel 51 was appointed as President and Chief Executive Officer | Mr. Creel became President and CEO of CP (CEO) on January 31, 2017. Previously,2017, a planned transition that had been in place since he was recruited to CP in February 2013 as President and Chief Operating Officer ("COO") from February 5, 2013, to January 30, 2017.

(COO). Prior to joining CP, Mr. Creel was Executive Vice-Presidenthad a very successful operating career that began in 1992 at Burlington Northern as a management trainee in operations and eventually led to his becoming the EVP and COO at CN in 2010. Mr. Creel obtained a Bachelor of Science in marketing from January 2010Jacksonville State University and has completed the Advanced Management Program at the Harvard Business School. He served as a commissioned officer in the U.S. Army during which time he served in the Persian Gulf War. The end of 2019 marked Mr. Creel’s third year as our President and CEO. This past year, Mr. Creel was focused on developing people, driving safety improvements and pursuing continued sustainable, profitable growth. Mr. Creel was recognized byInstitutional Investor as a member of the 2020All-Canada Executive Team and was ranked as the top CEO in the Capital Goods/Industrials sector. |

2019 individual performance CP’s purpose is to deliver transportation solutions that connect North America and the world. By doing this safely and efficiently, we create long-term, sustainable value for our shareholders and the broader economy. We remain grounded in the foundations of precision scheduled railroading. We operate safely, optimize assets, control costs, provide service and develop people. From our multi-year strategic and business plans to our daily operations and sales and marketing playbooks, everything we do is driven by, and tested against, our purpose, our values and the foundations of precision scheduled railroading. In 2019, Mr. Creel focused on the following key areas: In 2019, Mr. Creel championed the roll out of CP’s three core values of accountability, diversity and pride and appointed a Chief Culture Officer to help sustain and improve its industry-best culture. He also spent considerable time across the CP network engagingwith CP employees, including joining his senior operating team for three CEO town halls. This past year, he led the development and launch of an employee perspective survey to gather actionable data regarding management employee satisfaction and engagement and oversaw the seamless transition of CP’s operating team due to the retirements of Robert Johnson (Executive Vice-President Operations) and Tony Marquis (Senior Vice-President Operations East). Developing leaders internally is essential to CP’s continued success. That commitment is evidenced by Mr. Creel’s continued leadership on CP’s Coaching Capability Program, designed for high-potential managers to expand their leadership skills and create a deep bench of talent at CP. The company also continued its executive coaching program for existing and future leaders to receivecoaching and a customized development program from a certified executive coach. Mr. Creel also led CP’s first executive leadership forum. The forum focused on furthering the development of thought leadership and employee performance potential. Under Mr. Creel’s leadership, 2019 also saw CP release its first ever diversity and inclusion report, numerous panel discussions involving senior leadership focused on the advancement of women at CP, and CP being named the fourth overall Military Friendly® employer in the United States. Driving safety improvements For the 14th year in a row, CP had the lowestFRA-reportable train accident frequency of any North American Class 1 railway. That said, safety is not about a destination, but a constant journey. Mr. Creel led the initiative to increase the weighting on CP’s safety measure within our STIP, reinforcing CP’s commitment to safety. Under his leadership, CP continues to highlight the Home Safe program, which empowers all employees to begin a safety conversation, regardless of seniority or position, in the workplace and at home. This program, along with a personal commitment from each of CP’s employees, has led to a 20% reduction in personal injury rate since its inception. This past year, CP also hosted its first Safety Awards for Excellence gala, celebrating outstanding employee safety leadership.

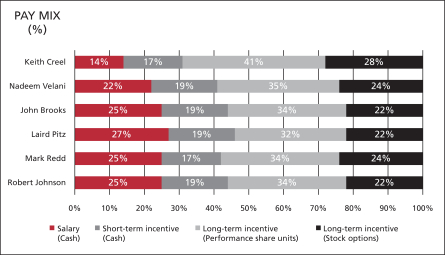

Driving sustainable, profitable growth Under Mr. Creel’s leadership, CP was able to achieve its highest-ever revenues and lowest-ever yearly operating ratio in 2019. This is a result of the company’s disciplined approach to sustainable, profitable growth - a plan rooted in the foundations of precision scheduled railroading. Despite challenging macroeconomic conditions, revenues increased 7 percent to a record $7.79 billion. Diluted earnings per share (EPS) increased 30 percent to a record $17.69 from $13.61 and adjusted diluted EPS(1) rose 13 percent to a record $16.44 from $14.51. As a result of Mr. Creel’s efforts and leadership, CP led the industry in volume growth and revenue growth for a second consecutive year. In 2019, CP realized gains in intermodal, automotive, forest products, and energy, chemicals and plastics. Across all lines of business, there were key contract wins throughout the year that set CP up well for 2020 and beyond. Mr. Creel spearheaded CP’s efforts to extend its reach through various initiatives in 2019 including the acquisition of the Central Maine & Quebec Railway and the opening of new compounds and transload terminals across the CP network. Additionally, this past year Mr. Creel held several meetings with a broad range of external stakeholders, including investors, Indigenous Peoples, industry associations, government, regulators, customers and policy makers. He also met regularly with current and prospective shareholders at industry conferences, at CP’s headquarters, and at shareholder offices across Canada, the United States and Europe. With Mr. Creel at the helm, the company remains focused on safely harnessing our network capacity to provide unique solutions that leverage our network strengths and superior service. The assessment was reviewed by the Compensation Committee and reviewed and approved by the Board. The table below shows the compensation awarded to Mr. Creel for 2019. | | | | | | | | | Compensation (in CAD $‘000) | | | | | | | | | | | | | | 1,538 | | | | | | | | | | | | 2,979 | | | | | | | | | | | | 5,870 | | | | | | 3,642 | | | Total direct compensation | | | 14,029 | | | Total target direct compensation | | | 11,147 | | | | Salary is the actual amount received in the year. Payments made in U.S. dollars have been converted to February 2013. During his timeCanadian dollars using an average exchange rate for the year of $1.3269. | | | | |

Mr. Creel’s salary was increased to US$1,158,750 in 2019.

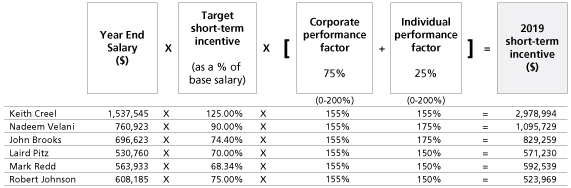

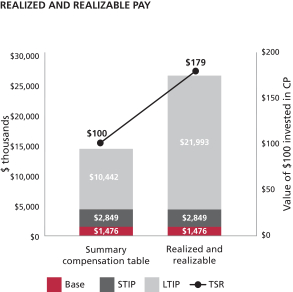

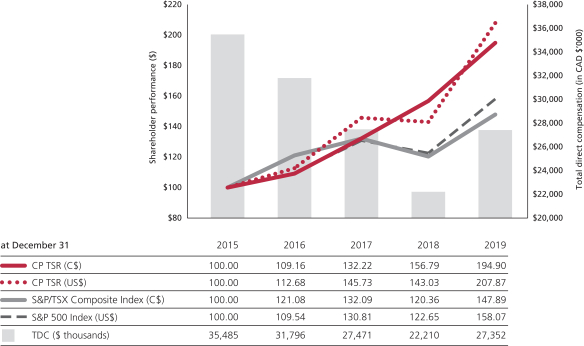

2019 Short-term incentive Based on our 2019 corporate performance and the board’s assessment of his individual performance, Mr. Creel received a cash bonus of $2,978,994 for 2019, calculated as follows: Year EndSalary ($)XTargetshort-termincentiveX[Corporateperformancefactor ($)+Individualperformancefactor ($)]=2019short-termincentive ($)(as a % ofbase salary)155%x 75%155%x 25%(0-200%)(0-200%)1,537,545125%2,234,245744,7492,978,994 Hisyear-end salary and the 2019 STIP award were paid in U.S. dollars and have been converted to Canadian dollars using an average exchange rate of $1.3269 for 2019. Mr. Creel received annual 2019 long-term incentive awards with a total grant value of $9,512,269, 100% of his target award. The grant was allocated as 60% PSUs and 40% stock options. Realized and realizable pay The value of Mr. Creel’s incentive compensation is based on our performance over the period and, for the long-term incentive, our share price when the awards vest. The graph below shows the three-year average of Mr. Creel’s granted and realized and realizable pay from 2017 to 2019. Summary compensation table: average of salary earned, actual cash bonus received, and long-term incentives granted (using the grant date fair value from 2017 to 2019 as disclosed in the summary compensation table on page 43). The compensation figures have been converted to Canadian dollars using the following average exchange rates: $1.3269 for 2019, $1.2957 for 2018 and $1.2986 for 2017.Realized and realizable pay: average of salary earned, actual cash bonus received, the value of long-term incentive awards that have vested or been exercised, and the estimated current value of unvested long-term incentive awards granted from 2017 to 2019.the value of vested 2017 PSUs paid in February 2020 was calculated using the30-day average trading price of our shares prior to December 31, 2019 of US$245.01 on the NYSE with a performance multiplier of 1.93 and includes dividends earned up to the payment date.

the value of unvested 2018 and 2019 PSUs are based on the closing price of our shares on December 31, 2019 of US$254.95 on the NYSE with a performance multiplier of 1.0. PSUs include reinvestment of additional units received as dividend equivalents the value of unvested/unexercised stock options is based on the closing price of our shares on December 31, 2019 of US$254.95 on the NYSE the compensation figures for salary earned and actual bonus received have been converted to Canadian dollars using the following average exchange rates: $1.3269 for 2019, $1.2957 for 2018 and $1.2986 for 2017. the value of any realized and realizable PSUs and Stock Options have been converted into Canadian dollars using the 2019year-end exchange rate of $1.2988 Theup-front performance stock options grant received in 2017 is included in realizable pay We also compare the realized and realizable value of $100 awarded in total direct compensation to Mr. Creel in each year to the value of $100 invested in our shares on the first trading day of the period, assuming reinvestment of dividends to show a meaningful comparison of shareholder value. Pay linked to shareholder value The table below shows Mr. Creel’s total direct compensation in Canadian dollars in each of the last three years, compared to its realized and realizable value as at December 31, 2019. We also compare the realized and realizable value of $100 awarded in total direct compensation to Mr. Creel in each year to the value of $100 invested in CP shares on the first trading day of the period, assuming reinvestment of dividends, to show a meaningful comparison of shareholder value. | | | | | | | | | | | | | | | | | | | | | | | (in CAD $‘000) | | | | | | | | | | | Value of $100 | | | | | | | | Realized and realizable value of compensation as at

December 31, 2019 | | | | | | | | | | | | | | 18,780,304 | | | | 48,994,522 | | | | Jan 1, 2017 to Dec 31, 2019 | | | | 260.88 | | | | 178.55 | | | | | 11,491,066 | | | | 14,640,604 | | | | Jan 1, 2018 to Dec 31, 2019 | | | | 127.41 | | | | 147.41 | | | | | 14,029,129 | | | | 15,318,711 | | | | Jan 1, 2019 to Dec 31, 2019 | | | | 109.19 | | | | 138.38 | |

Mr. Creel’s compensation awarded is as disclosed in the summary compensation table. Mr. Creel’s realized and realizable value for salary earned and actual bonus received have been converted to Canadian dollars using the following average exchange rates: $1.2986 for 2017, $1.2957 for 2018 and for $1.3269 for 2019. The value of any realized and realizable long-term incentive is converted into Canadian dollars using the 2019year-end exchange rate of $1.2988. Equity ownership (at February 28, 2020)| | | | | | | | | | | | | | | | (as a multiple of salary) | | Minimum

ownership value ($) | | | Shares ($) | | Deferred share

units ($) | | Total ownership

value ($) | | Total ownership

(as a multiple of salary) | | | | | 9,616,608 | | | 1,166,073 | | 10,666,164 | | 11,832,237 | | | 7.38x | |

Mr. Creel has met his share ownership requirements. Values are based on US$248.77, the closing price of our shares on the NYSE on February 28, 2020 and have been converted using an exchange rate of $1.3429. The Compensation Committee, in collaboration with Kingsdale, reviewed Mr. Creel’s compensation relative to our Class 1 Railroad peers. Through this benchmarking, it was determined that Mr. Creel’s long-term incentive target was considerably below the median. Effective January 1, 2020, Mr. Creel received a 3% increase in base salary, and his long-term incentive target became 660% of his base salary. Consistent with Mr. Creel’s 2016 employment agreement, his 660% long-term incentive target has been reduced by 100% (to a total of 560% each year) until the end of 2021 to fund an upfront performance grant that he received in 2017. | (1) | Adjusted diluted EPS is anon-GAAP measure.Non-GAAP measures are defined and reconciled on pages 54-62 of CP’s Annual Report on Form10-K for the year ended December 31, 2019. |

NADEEM S. VELANI EXECUTIVE VICE-PRESIDENT AND CHIEF FINANCIAL OFFICER | | |  | | Mr. Velani was appointed Vice-President and Chief Financial Officer (CFO) on October 18, 2016 and was appointed Executive Vice-President and Chief Financial Officer on October 17, 2017. Mr. Velani is a key member of the senior management team responsible for the long-term strategic direction of the Company. Other responsibilities include financial planning, reporting and accounting systems, as well as pension, treasury, investor relations and tax functions. Mr. Velani joined CP in March 2013 and most recently served as Vice-President Investor Relations. Prior to CP, Mr. Velani spent approximately 15 years at CN where he worked in a variety of positions in financial planning, sales and marketing, investor relations and the Office of the President and CEO. |

2019 individual performance The CEO assessed Mr. Velani’s performance against his individual performance objectives. In 2019, Mr. Velani: executed the company’s strategic multi-year plan to drive sustainable profitable growth; championed company-wide leadership development including as Chair of CP’s Leadership Development Steering Committee; improved the forecasting and budgeting process to help align resources in a volatile macro-economic environment, and continued to implement CP’s pension asset management strategy. Mr. Velani also delivered on CP’s financial principles, including a capital allocation strategy to support robust, long-term shareholder returns. Mr. Velani was recognized byInstitutional Investor as a member of the inaugural 2020All-Canada Executive Team. He was ranked as the top CFO in the Capital Goods/Industrials sector as voted on bybuy-side analysts, money managers and sell-side researchers. Mr. Velani was assessed as exceeding his individual performance objectives for the year. The assessment was reviewed by the Compensation Committee and reviewed and approved by the Board. The table below is a summary of the compensation awarded to Mr. Velani for 2019. | | | | | | | | | Compensation (in CAD $‘000) | | | | | | | | | | | | | | 751 | | | | | | | | | | | | 1,096 | | | | | | | | | | | | 1,552 | | | | | | 979 | | | Total direct compensation | | | 4,378 | | | Total target direct compensation | | | 3,538 | |

Mr. Velani’s salary was increased to US $566,500 in 2019. His salary was paid in Canadian dollars based on a foreign exchange rate of $1.3432. 2019 short-term incentive Based on our 2019 corporate performance and the CEO’s assessment of his individual performance, Mr. Velani received a cash bonus of $1,095,729 for 2019, calculated as follows: Year EndSalary ($)XTargetshort-termincentiveX[Corporateperformancefactor ($)+Individualperformancefactor ($)]=2019short-termincentive ($)(as a % ofbase salary)155%x 75%175%x 25%(0-200%)(0-200%)760,92390%796,116299,6131,095,729

Mr. Velani received annual 2019 long-term incentive awards with a total grant value of $2,531,053, 100% of his target award. The grant was allocated as 60% PSUs and 40% stock options. Equity ownership (at February 28, 2020)| | | | | | | | | | | | | | | | | | | | | | (as a multiple of salary) | | Minimum

ownership value ($) | | | Shares ($) | | | Deferred share

units ($) | | | Total ownership

value ($) | | | Total ownership

(as a multiple of salary) | | | | | 2,363,511 | | | | 204,541 | | | | 2,373,218 | | | | 2,577,759 | | | | 3.27x | |

Mr. Velani has met his share ownership requirements. Values are based on $332.67, the closing price of our common shares on the TSX on February 28, 2020. A comprehensive market review was conducted to assess Mr. Velani’s compensation relative to our peer group median. It was determined that Mr. Velani’s total direct compensation was below the market median. Therefore, effective January 1, 2020, his long-term incentive target was increased to 300% of base salary from 275%. He also received a 6% increase in base salary effective February 1, 2020.

JOHN K. BROOKS EXECUTIVE VICE-PRESIDENT AND CHIEF MARKETING OFFICER | | |  | | Mr. CreelBrooks was appointed Executive Vice-President and Chief Marketing Officer (CMO) on February 14, 2019. During the financial year ended December 31, 2018, Mr. Brooks was CP’s Senior Vice-President and Chief Marketing Officer. During Mr. Brooks’ sales and marketing career he has held various positionssenior responsibilities in all lines of business, including coal, chemicals, merchandise products, grain and intermodal. He began his railroading career with Union Pacific and later helped start I&M Rail Link, LLC, which was purchased by the Dakota, Minnesota and Eastern Railroad (DM&E) in 2002. Mr Brooks was Vice-President of Marketing at the DM&E prior to it being acquired by CP in 2007. In the role of CMO, Mr. Brooks is responsible for CP’s business units and leading a group of highly capable sales and marketing professionals across North America. In addition, Mr. Brooks is responsible for strengthening partnerships with existing customers, generating new opportunities for growth, enhancing the value of the company’s service offerings and developing strategies to optimize CP’s book of business. |

2019 individual performance The CEO assessed Mr. Brooks’ performance in 2019 against his individual performance objectives, which included the ongoing development and organization of the sales and marketing team, revenue growth, improving the quality of revenue, customer relationships and network development by expanding our reach through new market offerings, transloads and short lines and enhancing our product offering. Throughout 2019, Mr. Brooks was also focused on proactive customer engagement which included: measuring customer experience, hosting a customer advisory council, hosting meetings of short line railroads and transload operators, recognizing customers through initiatives such as our safe shipper awards and the new grain elevator of the year award. In addition, Mr. Brooks leads his team in the development, measurement and presentation of CP’s annual and multi-year business plan. Mr. Brooks was assessed as having exceeded his overall individual performance objectives. The assessment was reviewed by the Compensation Committee and reviewed and approved by the Board. The table below is summary of the compensation awarded to Mr. Brooks for 2019. | | | | | | | | | Compensation (in CAD $‘000) | | | | | | | | | | | | | | 670 | | | | | | | | | | | | 829 | | | | | | | | | | | | 1,197 | | | | | | 697 | | | Total direct compensation | | | 3,393 | | | Total target direct compensation | | | 2,782 | | | Salary is the actual amount received that year. Payments made in U.S. dollars have been converted to Canadian dollars using an average exchange rate for the year of $1.3269. | |

Effective February 14, 2019, Mr. Brooks was promoted to Executive Vice-President and Chief Marketing Officer. His salary was increased to US$525,000.

2019 short-term incentive Mr. Brooks’ annual bonus target was prorated to 74.4% of his base salary in 2019 to reflect his time at the new target associated with his promotion. Based on our 2019 corporate performance and the CEO’s assessment of his individual performance, Mr. Brooks received a cash bonus of $829,259 for 2019, calculated as follows: Year EndSalary ($)XTargetshort-termincentiveX[Corporateperformancefactor ($)+Individualperformancefactor ($)]=2019short-termincentive ($)(as a % ofbase salary)155%x 75%175%x 25%(0-200%)(0-200%)696,62374.40%602,509226,750829,259 Hisyear-end salary and the 2019 STIP award were paid in U.S. dollars and have been converted to Canadian dollars using an average exchange rate of $1.3269 for 2019. Mr. Brooks’ long-term incentive target was increased to 225% of his annual salary. He received 2019 long-term incentive awards with a total grant value of $1,893,801 which included a top up stock option grant received in February 2019 with a grant value of $194,149 to bring him to the Executive Vice-President level. The grants were allocated as 60% PSUs and 40% stock options. Equity ownership (at February 28, 2020)| | | | | | | | | | | | | | | | | | | | | | (as a multiple of salary) | | Minimum

ownership value ($) | | | Shares ($) | | | Deferred share

units ($) | | | Total ownership

value ($) | | | Total ownership

(as a multiple of salary) | | | | | 2,220,821 | | | | 692,832 | | | | 615,076 | | | | 1,307,908 | | | | 1.77x | |

Mr. Brooks is on track to meet his share ownership requirements by February 2024. Values are based on US$248.77, the closing price of our shares on the NYSE on February 28, 2020 and have been converted using an exchange rate of $1.3429. Mr. Brooks was promoted to Executive Vice-President and Chief Marketing Officer on February 14, 2019. Commensurate with his promotion and supplemented by a competitive market review, effective January 1, 2020, his short-term incentive target was increased to 90% of his base salary from 75% and his long-term incentive target was increased to 275% of base salary from 225%. He also received a 5% increase in base salary effective February 1, 2020.

LAIRD J. PITZ SENIOR VICE-PRESIDENT AND CHIEF RISK OFFICER | | |  | | Mr. Pitz was promoted to Senior Vice-President and Chief Risk Officer in October of 2017. This was part of the overall realignment of the risk and insurance functions for succession purposes, and to retain Mr. Pitz for the necessary development of the succession candidates. He is responsible for all aspects of risk-management in Canada and the U.S., including police services, casualty and general claims, environmental risk, field safety and systems, operational regulatory affairs and training, disability management and forensic audit investigations. Mr. Pitz joined CP on April 2, 2014, as Vice-President of Security and Risk Management. Mr. Pitz, a Vietnam War veteran and former FBI special agent, is a40-year career professional who has directed strategic and operational risk-mitigation, security and crisis-management functions for companies operating in a wide range of fields including defense, logistics and transportation. |

2019 individual performance The CEO assessed Mr. Pitz’s performance in 2019 against his individual performance objectives, which focused on the development of succession candidates in risk mitigation and safety and sustainability; and managing risk and reducing liability in several key areas: safety, environmental, insurance, police, security, casualty management, damage prevention, regulatory, operating practices, forensic and disability management. Under Mr. Pitz’s leadership, CP has made significant progress in mitigating its overall risk and liability, while supporting sustainable growth including the following results in 2019: $88 million cost control of monetary exposure; evaluating our most significant environmental, social and governance topics impacting the company; securing an independent insurance portfolio to protect the company against uncertain insurable losses; executing a resilient emergency response and crisis preparedness practice; and improving CP’s safety culture through Home Safe initiatives and technical training programs resulting in a 4% reduction in FRA Personal Injury frequency to 1.42 (lowest in CP’s history) and industry leading FRA Train Accident frequency of 1.06. Mr. Pitz was assessed as having exceeded his overall individual performance objectives. The assessment was reviewed by the Compensation Committee and reviewed and approved by the Board. The table below is a summary of the compensation awarded to Mr. Pitz for 2019. | | | | | | | | | Compensation (in CAD $‘000) | | | | | | | | | | | | | | 529 | | | | | | | | | | | | 571 | | | | | | | | | | | | 811 | | | | | | 503 | | | Total direct compensation | | | 2,414 | | | Total target direct compensation | | | 1,964 | | | Salary is the actual amount received that year. Payments made in U.S. dollars have been converted to Canadian dollars using an average exchange rate for the year of $1.3269. | |

Mr. Pitz’s salary was increased to US$400,000 in 2019.

2019 short-term incentive Based on our 2019 corporate performance and the CEO’s assessment of his individual performance, Mr. Pitz received a cash bonus of $571,230 for 2019, calculated as follows: Year EndSalary ($)XTargetshort-termincentiveX[Corporateperformancefactor ($)+Individualperformancefactor ($)]=2019short-termincentive ($)(as a % ofbase salary)155%x 75%150%x 25%(0-200%)(0-200%)530,76070%431,906139,324571,230 Hisyear-end salary and 2019 STIP award were made in U.S. dollars and have been converted to Canadian dollars using an average exchange rate of $1.3269 for 2019. Mr. Pitz also received 2019 annual long-term incentive awards with a total grant value of $1,313,416, 100% of his target award. The grant was allocated 60% PSUs and 40% stock options. Equity ownership (at February 28, 2020)| | | | | | | | | | | | | | | | | | | | | | (as a multiple of salary) | | Minimum

ownership value ($) | | | Shares ($) | | | Deferred share

units ($) | | | Total ownership

value ($) | | | Total ownership

(as a multiple of salary) | | | | | 1,106,550 | | | | 25,724 | | | | 1,485,075 | | | | 1,510,799 | | | | 2.73x | |

Mr. Pitz has met his share ownership requirements. Values are based on US$248.77, the closing price of our shares on the NYSE on February 28, 2020 and have been converted using an exchange rate of $1.3429.

MARK A. REDD EXECUTIVE VICE-PRESIDENT OPERATIONS | | |  | | Mr. Redd was appointed Executive Vice-President Operations Senioreffective September 1, 2019. Mr. Redd oversees the 24/7 operations of CP’s network including those teams responsible for network transportation, operations, mechanical, engineering, procurement and labour relations. Mr. Redd brings to his role considerable leadership experience in rail operations and safety excellence. Mr. Redd joined CP in October 2013. In April 2016, he was appointed Vice-President Eastern Region, Senior Vice-PresidentOperations Western Region, and Vice-President of the Prairie Division. Mr. Creel began his railroad career at Burlington Northern Railway in 1992 as an intermodal ramp manager in Birmingham, Alabama. He also spent part of his career at Grand Trunk Western Railroad as a superintendent and general manager, and at Illinois Central Railroad as a trainmaster and director of corridor operations, priorwas promoted to its merger with CN in 1999.

| Mark Redd, 49

Executive Vice-President, Operations

| Mr. Redd has been Executive Vice-President Operations since September 1, 2019. Before this appointment, he was Senior Vice-President Operations Western Region fromin February 2, 2017 to August 31, 2019 and Vice-President Operations Western Region from April 20, 2016 to February 1, 2017.

Previous Prior to these roles, he was General Manager Operations U.S. West and General Manager Operations Central Division. He was named CP'sCP’s 2016 Railroader of the Year. Prior to joining CP in October 2013,

Mr. Redd worked forbegan his railroading career at Midsouth Rail in Jackson, Mississippi, as a brakeman and conductor, before moving to Kansas City Southern (KCS) as an engineer. Throughout his over 20 years at Kansas City Southern Railway where heKCS, Mr. Redd held a variety of leadership positions in network and field operations. Mr. Redd holds bachelor and Master of Business Administration ("MBA") degrees from the University of Missouri – Kansas City. | Nadeem Velani, 47

Executiveoperations, including Vice-President and Chief Financial Officer

| Mr. Velani has been Executive Vice-President and CFO of CP since October 17, 2017. Previous to this appointment, he was the Vice-President and CFO of CP from October 19, 2016 to October 16, 2017, Vice-President, Investor Relations from October 28, 2015 and Assistant Vice-President, Investor Relations from March 11, 2013.

Prior to joining CP, Mr. Velani spent 15 years at CNTransportation where he workedoversaw key operating functions in a variety of positions in Strategicthe U.S. and Financial Planning, Investor Relations, Sales and Marketing, andMexico. During this time, he also served as the OfficeChairman of the President and CEO.

Mr. Velani holds a Bachelor of Economics degree from Western University and an MBAoperating board for the Port Terminal Railroad Association in Finance/International Business from McGill University.Houston, Texas.

| John Brooks, 49

Executive Vice-President and Chief Marketing Officer

| Mr. Brooks has been Executive Vice-President and Chief Marketing Officer ("CMO") of CP since February 14, 2019. Previous to this appointment, he was the Senior Vice-President and CMO of CP from February 14, 2017 to February 13, 2019. He has worked in senior marketing roles at CP since he joined the Company in 2007, most recently as Vice-President, Marketing – Bulk and Intermodal.

Mr. Brooks began his railroading career with UP and later helped start I&M Rail Link, LLC, which was purchased by DM&E in 2002. Mr. Brooks was Vice-President, Marketing at DM&E prior to it being acquired by CP in 2007.

With more than 20 years in the railroading business, Mr. Brooks brings a breadth of experience to the CMO role that is pivotal to CP's continued and future success.

| James Clements, 50

Senior Vice-President, Strategic Planning and Technology Transformation

| Mr. Clements has been Senior Vice-President, Strategic Planning and Technology Transformation since September 1, 2019. Before this appointment, he was the Vice-President, Strategic Planning and Transportation Services of CP since 2014. Mr. Clements has responsibilities that include strategic network issues, Network Service Centre operations and Information Services. In addition, he has responsibility for all of CP’s facilities and real estate across North America.

Mr. Clements has been at CP for 25 years and his previous experience covers a wide range of areas of CP’s business, including car management, finance, joint facilities agreements, logistics, grain marketing and sales in both Canada and the U.S., as well as marketing and sales responsibility for various other lines of business at CP.

He has an MBA in Finance/International Business from McGill University and a Bachelor of Science in Computer Science and Mathematics from McMaster University.

|

27 /SERVICE EXCELLENCE

2019 individual performance

| | | Jeffrey Ellis, 52

Chief Legal Officer and Corporate Secretary

| Mr. Ellis has been Chief Legal Officer and Corporate Secretary of CP since November 23, 2015. Mr. Ellis is accountable for the overall strategic leadership, oversight andThe CEO assessed Mr. Redd’s performance of the legal, corporate secretarial, government relations and public affairs functions of CP in Canada and the U.S.

Prior to joining CP in 2015, Mr. Ellis was the U.S. General Counsel at BMO Financial Group. Before joining BMO in 2006, Mr. Ellis was with the law firm of Borden Ladner Gervais LLP in Toronto, Ontario.

Mr. Ellis has Bachelor of Arts and Master of Arts degrees from the University of Toronto, Juris Doctor and Master of Laws degrees from Osgoode Hall Law School, and an MBA from the Richard Ivey School of Business, Western University. Mr. Ellis is a member of the bars of New York, Illinois, Ontario and Alberta.

| Mike Foran, 46

Vice-President, Market Strategy and

Asset Management

| Mr. Foran has been Vice-President, Market Strategy and Asset Management of CP since February 14, 2017. His prior roles with CP include Vice-President Network Transportation from 2014 to 2017, Assistant Vice-President Network Transportation from 2013 to 2014, and General Manager – Asset Management from 2012 to 2013. In over 20 years at CP, Mr. Foran has worked in operations, business development, marketing and general management.

Mr. Foran holds an Executive MBA from the Ivey School of Business at Western University and a Bachelor of Commerce from the University of Calgary.

| Michael Redeker, 59

Vice-President and Chief Information Officer

| Mr. Redeker has been Vice-President and Chief Information Officer ("CIO") of CP since October 15, 2012.

Prior to joining CP, Mr. Redeker was Vice-President and CIO of Alberta Treasury Branch from May 2007 to September 2012. He also spent 11 years at IBM Canada, where he focused on delivering quality information technology services within the financial services industry.

| Laird Pitz, 75

Senior Vice-President and Chief Risk Officer

| Mr. Pitz has been Senior Vice-President and Chief Risk Officer ("CRO") of CP since October 17, 2017. Previously, he was the Vice-President and CRO of CP from October 29, 2014 to October 16, 2017 and the Vice-President, Security and Risk Management of CP from April 2014 to October 2014.

Prior to joining CP, Mr. Pitz was retired from March 2012 to April 2014, and Vice-President, Risk Mitigation of CN from September 2003 to March 2012.

Mr. Pitz, a Vietnam War veteran and former Federal Bureau of Investigation special agent, is a 40-year career professional who has directed strategic and operational risk mitigation, security and crisis management functions for companies operating in a wide range of fields, including defence, logistics and transportation.

| Chad Rolstad, 43

Vice-President, Human Resources and Chief Culture Officer

| Mr. Rolstad has been Vice-President, Human Resources since February 14, 2019 and the Chief Culture Officer since September 1, 2019. Previous to this appointment, he was Assistant Vice-President, Human Resources of CP from August 1, 2018 to February 13, 2019 and Assistant Vice-President, Strategic Procurement of CP from April 10, 2017 to July 31, 2018.

Prior to joining CP, Mr. Rolstad held various leadership positions at BNSF Railway in marketing and operations.

Mr. Rolstad has a Bachelor of Science from the Colorado School of Mines and an MBA from Duke University.

|

CP 2019 ANNUAL REPORT/ 28

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Share Information

The Common Shares are listedagainst his individual performance objectives. Mr. Redd focused on the TSXtransitioning his leadership team which included delivering world class service to our customers by executing CP’s precision scheduled railroading model, leading CP’s safety efforts, and on the NYSE under the symbol "CP".

Share Capital

At February 18, 2020, the latest practicable date priorcontinuing to the date of this Annual Report on Form 10-K, there were 136,748,767 Common Shares and no preferred shares issued and outstanding, which consists of 13,928 holders of record of the Common Shares. In addition, CP has a Management Stock Option Incentive Plan (“MSOIP”), under which key officers and employees are granted options to purchase the Common Shares. Each option granted can be exercised for one Common Share. At February 18, 2020, 1,569,063 options were outstanding under the MSOIP and stand-alone option agreements entered into with Mr. Keith Creel. There are 895,948 options available to be issued by the Company’s MSOIPdevelop his team in the future. CParea of technical and leadership skills at all levels. Aligning his team through collaboration while maintaining healthy constructive tension within the teams has a Director's Stock Option Plan (“DSOP”), underallowed the operations department to excel in supporting CP’s five foundations. Mr. Redd promoted and advanced CP’s Home Safe efforts which directors are granted options to purchase Common Shares. There are no outstanding options under the DSOP, which has 340,000 options available to be issuedresulted in the future.

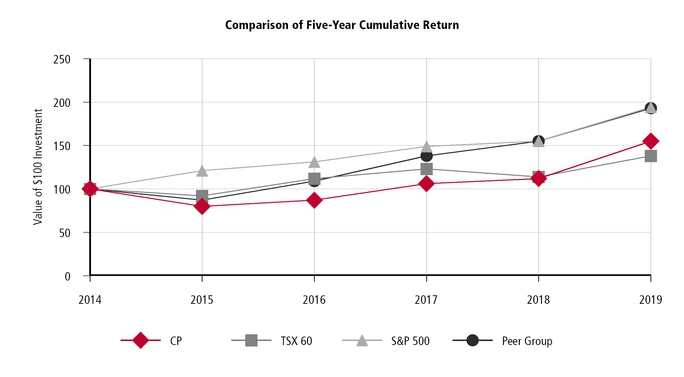

Stock Performance Graph

The following graph provides an indicator of cumulative total shareholder return on the Common Shares, of an assumed investment of $100, as compared to the TSX 60 Index (“TSX 60”), the Standard & Poor's 500 Stock Index (“S&P 500”),lowest personal injury rates and the peer group index (comprising CN, KCS, UP, NS and CSX) on December 31 for each of the years indicated. The values for the assumed investments depicted on the graph andfrequency in the table have been calculated assuming that any dividends are reinvested.

CP 2019 ANNUAL REPORT/ 30

Issuer Purchasehistory of Equity Securities

CPCP. Decreased cycle times for bulk trains yielded record results in several commodity groups for carload and tonnage moved. Mr. Redd’s persistent focus on precision scheduled railroading has established a share repurchase program which is further describedimproved operating efficiencies, proven by CP’s industry-leading third quarter results and positioning the company well in Item 8. Financial Statements and Supplementary Data, Note 22 Shareholders' equity. During 2019, CP repurchased 3.8 million Common Shares for $1,141 million at a weighted average price of $300.65. The following table presents the number of Common Shares repurchased during each month for the fourth quarter of 2019 and the average price paid by CP for the repurchase of such Common Shares.into 2020. Mr. Redd was assessed as having exceeded his overall individual performance objectives.

The assessment was reviewed by the Compensation Committee and reviewed and approved by the Board. | | | | | | | | | | | | 2019 | Total number of shares purchased(1) |

| Average price paid per share(2) |

| Total number of shares purchased as part of publicly announced plans or programs |

| Maximum number of shares (or units) that may yet be purchased under the plans or programs |

| | October 1 to October 31 | 312,279 |

| $ | 284.65 |

| 312,279 |

| — |

| | November 1 to November 30 | — |

| — |

| — |

| — |

| | December 1 to December 31 | 298,409 |

| 333.96 |

| 298,409 |

| 4,502,453 |

| | Ending Balance | 610,688 |

| $ | 308.74 |

| 610,688 |

| N/A |

|

2019 compensation (1) Includes shares repurchased but not yet cancelled at quarter end.

(2) Includes brokerage fees.

31 /SERVICE EXCELLENCE

ITEM 6. SELECTED FINANCIAL DATA

The following table presents as of, and for the years ended, December 31, selected financial data related to the Company’s financial results for the last five fiscal years. The selected financial data should be read in conjunction with Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8. Financial Statements and Supplementary Data.

For information regarding historical exchange rates, please see Impact of Foreign Exchange on Earnings in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

| | | | | | | | | | | | | | | | | | (in millions, except per share data, percentage and ratios) | 2019 |

| 2018 |

| 2017 |

| 2016 |

| 2015 |

| | Financial Performance and Liquidity | | | | | | | Total revenues | $ | 7,792 |

| $ | 7,316 |

| $ | 6,554 |

| $ | 6,232 |

| $ | 6,712 |

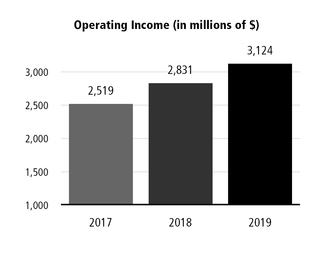

| | Operating income | 3,124 |

| 2,831 |

| 2,519 |

| 2,411 |

| 2,618 |

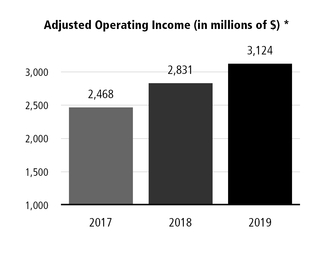

| Adjusted operating income(1) | 3,124 |

| 2,831 |

| 2,468 |

| 2,411 |

| 2,550 |

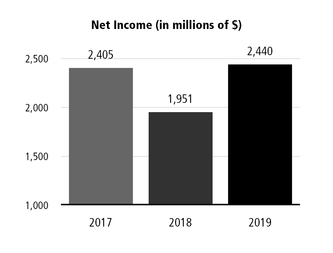

| | Net income | 2,440 |

| 1,951 |

| 2,405 |

| 1,599 |

| 1,352 |

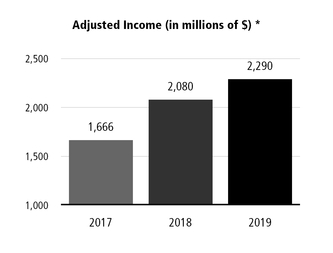

| Adjusted income(1) | 2,290 |

| 2,080 |

| 1,666 |

| 1,549 |

| 1,625 |

| | Basic earnings per share ("EPS") | 17.58 |

| 13.65 |

| 16.49 |

| 10.69 |

| 8.47 |

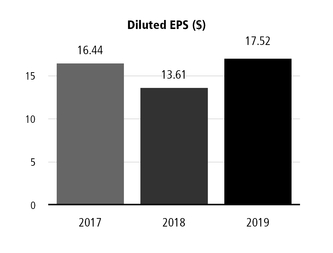

| | Diluted EPS | 17.52 |

| 13.61 |

| 16.44 |

| 10.63 |

| 8.40 |

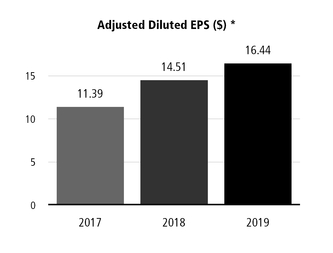

| Adjusted diluted EPS(1) | 16.44 |

| 14.51 |

| 11.39 |

| 10.29 |

| 10.10 |

| | Dividends declared per share | 3.1400 |

| 2.5125 |

| 2.1875 |

| 1.8500 |

| 1.4000 |

| | Cash provided by operating activities | 2,990 |

| 2,712 |

| 2,182 |

| 2,089 |

| 2,459 |

| | Cash used in investing activities | (1,803 | ) | (1,458 | ) | (1,295 | ) | (1,069 | ) | (1,123 | ) | | Cash used in financing activities | (1,111 | ) | (1,542 | ) | (700 | ) | (1,493 | ) | (957 | ) | Free cash(1) | 1,357 |

| 1,289 |

| 874 |

| 1,007 |

| 1,381 |

| | Financial Position | | | | | | Total assets(2) | $ | 22,367 |

| $ | 21,254 |

| $ | 20,135 |

| $ | 19,221 |

| $ | 19,637 |

| | Total long-term debt, including current portion | 8,757 |

| 8,696 |

| 8,159 |

| 8,684 |

| 8,957 |

| | Total shareholders' equity | 7,069 |

| 6,636 |

| 6,437 |

| 4,626 |

| 4,796 |

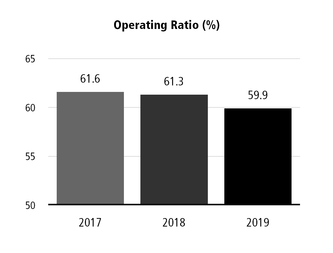

| | Financial Ratios | | | | | | Operating ratio(3) | 59.9 | % | 61.3 | % | 61.6 | % | 61.3 | % | 61.0 | % | Adjusted operating ratio(1) | 59.9 | % | 61.3 | % | 62.4 | % | 61.3 | % | 62.0 | % | Return on invested capital ("ROIC")(1) | 17.9 | % | 15.3 | % | 20.5 | % | 14.4 | % | 12.9 | % | Adjusted ROIC(1) | 16.9 | % | 16.2 | % | 14.7 | % | 14.0 | % | 15.2 | % | Dividend payout ratio(4) | 17.9 | % | 18.5 | % | 13.3 | % | 17.4 | % | 16.7 | % | Adjusted dividend payout ratio(1) | 19.1 | % | 17.3 | % | 19.2 | % | 18.0 | % | 13.9 | % | Long-term debt to Net income ratio(5) | 3.6 |

| 4.5 |

| 3.4 |

| 5.4 |

| 6.6 |

| Adjusted net debt to adjusted EBITDA ratio(1) | 2.4 |

| 2.6 |

| 2.6 |

| 2.9 |

| 2.8 |

|

| | | | | | | | These measures have no standardized meanings prescribed by accounting principles generally accepted in the United States of America ("GAAP") and, therefore, may not be comparable to similar measures presented by other companies. These measures are defined and reconciled in Non-GAAP Measures in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

| | (2)Compensation (in CAD $‘000) | Current period amount is as reported in compliance with GAAP following the adoption of Accounting Standards Update ("ASU") 2016-02 under the cumulative effect adjustment transition approach, discussed further in Item 8. Financial Statements and Supplementary Data, Note 2 Accounting changes. The comparative periods' amounts have not been restated and continue to be reported under the accounting standards in effect for those periods. |

| | | Operating ratio is defined as operating expenses divided by revenues. |

| | (4)

| Dividend payout ratio is defined as dividends declared per share divided by Diluted EPS. |

| | (5)

| Long-term debt to Net income ratio is defined as long-term debt, including long-term debt maturing within one year, divided by Net income. |

CP 2019 ANNUAL REPORT/ 32

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

INDEX TO MANAGEMENT'S DISCUSSION AND ANALYSIS

| | | | | Page | Executive Summary | | 2020 Outlook | | Performance Indicators | | Results of Operations | | Impact of Foreign Exchange on Earnings | | Impact of Fuel Price on Earnings | | Impact of Share Price on Earnings | | Operating Revenues | | Operating Expenses | | Other Income Statement Items | | Liquidity and Capital Resources | | Non-GAAP Measures | | Off-Balance Sheet Arrangements | | Critical Accounting Estimates | | Forward-Looking Statements | |

The following discussion and analysis should be read in conjunction with the Company’s Consolidated Financial Statements and the related notes in Item 8. Financial Statements and Supplementary Data, and other information in this annual report. Except where otherwise indicated, all financial information reflected herein is expressed in Canadian dollars.

Executive Summary

2019 Results

| | • | Financial performance– In 2019, CP reported Diluted earnings per share ("EPS") of $17.52, a 29%increase from $13.61 in 2018. Adjusted diluted EPS increased to $16.44, a 13% improvement compared to $14.51 in 2018. CP’s commitment to service and operational efficiency produced an Operating ratio of 59.9%. Adjusted diluted EPS is defined and reconciled in Non-GAAP Measures and discussed further in Results of Operations of this Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

|

| | • | Total revenues– CP’s Total revenues increased by 7% to $7,792 million in 2019 from $7,316 million in 2018, driven primarily by higher freight rates.

|

| | • | Operating performance – CP's average train speed increased by 3% to 22.2 miles per hour and average dwell time decreased by 6% to 6.4 hours in 2019 primarily due to the completion of network infrastructure projects which improved network fluidity. Average train weight remained relatively unchanged at 9,129 tons and average train length increased by 1% to 7,388 feet due to improvements in operating plan efficiency, in each case compared to 2018. These metrics are discussed further in Performance Indicators of this Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

|

The following table compares 2019 outlook to actual results:

| | | | | | | RTM growth | Adjusted diluted EPS(1)Base earnings | Capital expenditures | | 491 | | Outlook |

Revised at the end of the third quarter to low-single digits

| Double-digit Adjusted diluted EPS growth from full-year 2018 Adjusted diluted EPS of $14.51 | Approximately $1.60 billion | Actual outcomes | Revenue ton-miles ("RTMs") increased by 171 million, or 0.1% | Adjusted diluted EPS growth of 13% to $16.44 | $1.65 billion |

(1) Adjusted diluted EPS is defined and reconciled in Non-GAAP Measures of this Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations. As described in the 2020 Outlook section below, CP had not calculated an outlook for Diluted EPS in 2019.

The update in RTM volume expectations was due to delays in the Canadian grain harvest and export potash volumes, as well as general macroeconomic softness. During the fourth quarter of 2019, CP's volumes were lower primarily due to decreased shipments of export potash, Coal and Metals, minerals and consumer products. This decrease was partially offset by increased volumes of crude, and Intermodal.

2020 Outlook

With a 2020 plan that encompasses profitable sustainable growth, CP expects RTM growth to be in the mid-single digit and Adjusted diluted EPS growth to be in the high single-digit to low double-digits. CP’s expectations for Adjusted diluted EPS growth in 2020 are based on Adjusted diluted EPS of $16.44 in 2019. For the purposes of this outlook, CP assumes an effective tax rate of 25 percent. CP estimates other components of net periodic benefit recovery to decrease by approximately $40 million versus 2019. As CP continues to invest in service, productivity and safety, the Company plans to invest approximately $1.6 billion in capital programs in 2020. Capital programs are defined and discussed further in Liquidity and Capital Resources of this Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Adjusted diluted EPS is defined and discussed further in Non-GAAP Measures and in Forward-Looking Statements of this Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. Although CP has provided a forward-looking Non-GAAP measure (Adjusted diluted EPS), management is unable to reconcile, without unreasonable efforts, the forward-looking Adjusted diluted EPS to the most comparable GAAP measure, due to unknown variables and uncertainty related to future results. These unknown variables may include unpredictable transactions of significant value. In past years, CP has recognized significant asset impairment charges, management transition costs related to senior executives and discrete tax items. These or other similar, large unforeseen transactions affect diluted EPS but may be excluded from CP’s Adjusted diluted EPS. Additionally, the U.S.-to-Canadian dollar exchange rate is unpredictable and can have a significant impact on CP’s reported results but may be excluded from CP’s Adjusted diluted EPS. In particular, CP excludes the foreign exchange ("FX") impact of translating the Company’s debt and lease liabilities, the impact from changes in income tax rates and a provision for uncertain tax item from Adjusted diluted EPS. Please see Forward-Looking Statements of this Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations for further discussion.

CP 2019 ANNUAL REPORT/ 34