UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934 |

For fiscal year ended December 31, 20222023

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-01342

Canadian Pacific RailwayKansas City Limited

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Canada | | 98-0355078 |

(State or Other Jurisdiction

of Incorporation or Organization) | | (IRS Employer

Identification No.) |

| | | |

| 7550 Ogden Dale Road S.E., Calgary, Alberta, | | |

CalgaryCanada | | AB | T2C 4X9 |

(Address of Principal Executive Offices)principal executive offices) | | (Zip Code) |

Registrant's

(403) 319-7000

Registrant’s Telephone Number, Including Area Code: (403) 319-7000

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Title of Each Classeach class | | | Trading Symbol(s) | | | Name of Each Exchangeeach exchange on which Registered | |

Common Shares, without par value, of

Canadian Pacific RailwayKansas City Limited | | CP | | New York Stock Exchange |

| | |

Common Shares, without par value, of

Canadian Pacific Kansas City Limited | | CP | | Toronto Stock Exchange |

| | |

| Perpetual 4% Consolidated Debenture Stock of Canadian Pacific Railway Company | | CP/40 | | New York Stock Exchange |

| | | |

| Perpetual 4% Consolidated Debenture Stock of Canadian Pacific Railway Company | | BC87 | | London Stock Exchange |

| | | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | þ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting

company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

As of June 30, 2022,2023, the last business day of the registrant's most recently completed second fiscal quarter, the aggregate market value of the voting stock held by non-affiliates of the registrant, in U.S. dollars, was $64,936,373,457,$75,204,483,138, based on the closing sales price per share as reported by the New York Stock Exchange on such date.

As of the close of business on February 23, 2023,26, 2024, there were 930,767,959932,428,454 shares of the registrant's common shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Not applicable.

EXPLANATORY NOTE

Canadian Pacific RailwayKansas City Limited ("CPRL"CPKC"), a corporation incorporated under the Canada Business Corporations Act, qualifies as a foreign private issuer in the U.S. for purposes of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Although as a foreign private issuer CPRLCPKC is no longer required to do so, CPRLCPKC currently continues to file annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K with the Securities and Exchange Commission ("SEC") instead of filing reports on forms available to foreign private issuers.

CPRLCPKC prepares and files a management information circular and related material under Canadian requirements. As CPRL'sCPKC's management information circular is not filed pursuant to Regulation 14A, CPRLCPKC may not incorporate by reference information required by Part III of this Form 10-K from its management information circular. Accordingly, in reliance upon and as permitted

by Instruction G(3) to Form 10-K, CPRLCPKC will be filing an amendment to this Form 10-K containing the Part III information no later than 120 days after the end of the fiscal year covered by this Form 10-K. All references to websites (including our websiteswebsite) contained herein do not constitute incorporation by reference of information contained on such websites and such information should not be considered part of this document.

CP 2022CPKC 2023 ANNUAL REPORT / 1

CANADIAN PACIFIC RAILWAYKANSAS CITY LIMITED

FORM 10-K TABLE OF CONTENTS

| | | | | | | | |

| PART I | | Page |

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 1C. | Cybersecurity | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

| Information about our Executive Officers | |

| | |

| PART II | | |

| Item 5. | Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | [Reserved] | |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| Item 9B. | Other Information | |

Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |

| | |

| PART III | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accounting Fees and Services | |

| | |

| PART IV | | |

| Item 15. | Exhibits, Financial Statement Schedule | |

| Item 16. | Form 10-K Summary | |

| Signatures | |

2 / CP 2022CPKC 2023 ANNUAL REPORT

PART I

CP 2022CPKC 2023 ANNUAL REPORT / 3

ITEM 1. BUSINESS

Company Overview

On April 14, 2023, Canadian Pacific Railway Limited (“CPRL”CPRL" or "CP") assumed control of Kansas City Southern ("KCS") (through an indirect wholly-owned subsidiary), together with its subsidiaries (“CP”and filed articles of amendment to change CPRL's name to Canadian Pacific Kansas City Limited ("CPKC"),. CPKC owns and operates a transcontinentalthe only freight railway inspanning Canada, and the United States (“("U.S.”"). CP, and Mexico. CPKC provides rail and intermodal transportation services over a network of approximately 13,000 miles, directly 20,000 miles, serving the principal business centres ofacross Canada, from Montréal, Québec, to Vancouver, British Columbia ("B.C.")the U.S., and the U.S. Northeast and Midwest regions. CP’s railway network feeds directly into the U.S. Midwest from the East and West coasts. Agreements with other carriers extend CP's market reach in Canada, through the U.S. and into Mexico. CPCPKC transports bulk commodities, merchandise freight, and intermodal traffic. For additional information regarding CP'sCPKC's network and geographical locations, refer to Item 2. Properties.

CPRLThe Company was originally incorporated on June 22, 2001, under the Canada Business Corporations Act and controls and owns all of the Common Shares of Canadian Pacific Railway Company (“CPRC”), which was incorporated in 1881 by Letters Patent pursuant to an Act of the Parliament of Canada. CPRL'sCPKC's registered, executive and corporate head office is located at 7550 Ogden Dale Road S.E., Calgary, Alberta, T2C 4X9, Canada. CPRL'sCPKC's U.S. head office is located at 427 West 12 Street, Kansas City, Missouri, 64105. CPKC's Common Shares (the "Common Shares") are listed on the Toronto Stock Exchange (“TSX”) and the New York Stock Exchange (“NYSE”) under the symbol “CP”.

For purposes of this annual report, unless the context indicates otherwise, all references herein to “CP”“CPKC”, “the Company”, “we”, “our” and “us” refer to CPRL,Canadian Pacific Kansas City Limited and its subsidiaries, which includes KCS as a consolidated subsidiary on and from April 14, 2023. Prior to April 14, 2023, KCS was held as an equity investment accounted for by the equity method of accounting. For purposes of this annual report, unless the context indicates otherwise, all references herein to “legacy CP” refer to CPRL and its subsidiaries CPRLprior to April 14, 2023. For purposes of this annual report, unless the context indicates otherwise, all references herein to“legacy KCS” refer to KCS and one or more of its subsidiaries or one or more of CPRL's subsidiaries, as the context may require.prior to April 14, 2023. All references to currency amounts included in this annual report, including the Consolidated Financial Statements, are in Canadian dollars unless specifically noted otherwise.

Strategy

The Company’s strategy remains focused on precision scheduled railroading as embedded within our five foundations:

•Provide Service: Providing efficient and consistent transportation solutions for the Company’s customers. “Doing what we say we are going to do” is what drives the Company in providing a reliable product with a lower cost operating model. Centralized planning aligned with local execution is bringing the Company closer to the customer and accelerating decision-making.

•Control Costs: Controlling and removing unnecessary costs from the organization, eliminating bureaucracy, and continuing to identify productivity enhancements are the keys to success.

•Optimize Assets: Through longer and heavier trains, and improved asset utilization, the Company is moving increased volumes with fewer locomotives and cars while unlocking capacity for future growth potential.

•Operate Safely: Each year, the Company safely moves millions of carloads of freight across North America while ensuring the safety of our people and the communities through which we operate. Safety is never to be compromised. The Company strives for continuous implementation of state-of-the-art safety technology, safety management systems, and safety culture with our employees to ensure safe, efficient operations across our network.

•Develop People: The Company recognizes that none of the other foundations can be achieved without its people. Every employee is a railroader and the Company has established a culture focused on our values of accountability, diversity and pride, in everything we do. Coaching and mentoring all employees into becoming leaders will continue to drive the Company forward.

Today, we continue to apply our long-term strategy: leverage our lower cost base, network strengths, and improve service to drive sustainable, profitable growth. While the accomplishments during the operational turnaround were tremendous, the Company's journey to become North America's best-performing rail carrier is far from over. As a Company, we remain focused on our next level of service, productivity, and innovation to continue to generate sustainable value for our customers, employees, and shareholders.

Business Developments

Kansas City Southern ("KCS")KCS transaction

The U.S.On March 15, 2023, the United States Surface Transportation Board'sBoard ("STB") reviewissued a final decision approving CPRL and KCS's joint merger application, subject to certain conditions. On March 17, 2023, the CPRL announced its acceptance of CP's proposedthe STB's final decision and its intent to assume control of KCS while KCS is inon April 14, 2023 (the "Control Date"). On the Control Date, the voting trust is expectedwas terminated and the CPRL assumed control of KCS (through an indirect wholly-owned subsidiary), and changed CPRL's name to be completed in the first quarter of 2023. Upon obtaining control approval from the STB, provided it is granted, the two companies will be combined. Mr. Creel will serve as the Chief Executive Officer of the combined company. The combined business will be named Canadian Pacific Kansas City Limited ("CPKC"). Calgary, Alberta will be the global headquarters of CPKC, and Kansas City, Missouri will be designated as the U.S. headquarters. The Mexico headquarters will remain in Mexico City and Monterrey. CP's current U.S. headquarters in Minneapolis-St. Paul, Minnesota will remain an important base of operations. Four KCS Directors are expected to join CP's expanded Board at the appropriate time, bringing their experience and expertise in overseeing KCS's multinational operations.Limited.

4 / CP 2022CPKC 2023 ANNUAL REPORT

The transaction will combine the two railroads to create the first rail network connecting the U.S., Mexico, and Canada and will deliver dramatically expanded market reach for customers served by CP and KCS, provide new competitive transportation service options, and support North American economic growth.

Specific risk factors related to the KCS transaction are included in Part I, Item 1A. Risk Factors.

Other current business developments

In the fourth quarter of 2022,2023, the Company was named to the S&P Global Dow Jones Sustainability World Index ("(“DJSI World"World”) for the first time and to the North American Index ("(“DJSI North America"America”) for the third consecutive year.. According to S&P Global, the DJSI North America comprisestracks the performance of North American sustainability leaders as identified through the Corporate Sustainability Assessment. The index represents the top 20% of the largest 600 North AmericanCanadian and United States companies in the S&P Global Broad Market Index and measures corporate sustainability leaders' performance based on long-term economic, environmental, and social criteria.that lead the field in terms of sustainability. The DJSI World Index comprises global sustainability leaders as identified by S&P Global throughtracks the Corporate Sustainability Assessment. It representsperformance of the top 10% of the largest 2,500 companies in the S&P Global BMI based on long-term economic, environmental and social criteria.

Additionally,that lead the Company was named to CDP Worldwide ("CDP")’s A List for the second consecutive year. CDP is an international nonprofit organization that annually assesses organizations on environmental performance and transparency. According to CDP, nearly 20,000 organizations disclosed climate-related and environmental metrics and information through the organizationfield in 2022.terms of sustainability.

On July 20, 2022, KCSJune 28, 2023, CPKC, CSX Corporation ("CSX"), and its affiliate Kansas City Southern de México, S.A. de C.V.Genesee & Wyoming Inc. ("KCSM"G&W") announced an agreement, effective July 14, 2022, extendingthat they have reached agreements which, when completed, will create a new direct CPKC-CSX interchange connection in Alabama. As part of the concession exclusivity rights grantedseries of proposed transactions, CPKC and CSX will each acquire or operate portions of Meridian & Bigbee Railroad, L.L.C., a G&W-owned railway in Mississippi and Alabama, to KCSMestablish a new freight corridor for an additional 10 years to now expire in 2037. Additionally, KCSM reached an agreementshippers that connects Mexico and Texas with the Mexican Ministry of Infrastructure, Communications and Transportation to fund a new investment in the Celaya-NBA Line Railway Bypass and other infrastructure.

On May 3, 2022, the Company became the first freight rail company in North America to participate in the United Nations ("UN") Global Compact, a voluntary leadership platform for the development, implementation and disclosure of socially responsible business practices. Launched in 2000, the UN Global Compact is the largest corporate sustainability initiative in the world, with more than 15,000 participating companies in over 160 countries.

On April 27, 2022, at the Company's Annual and Special Meeting of Shareholders, all nine director nominees were elected to the Board of DirectorsU.S. Southeast. Certain portions of the Company.

On March 16, 2022, the Company issued a 72-hour noticetransactions are subject to the Teamsters Canada Rail Conference ("TCRC") - Train & Engine, of its plan to lock-out employees at 00:01 Eastern Time on March 20, 2022 if the TCRC leadershipregulatory review and the Company were unable to come to a negotiated settlementapproval from, or agree to binding arbitration. The TCRC represents approximately 3,000 locomotive engineers, conductors, and train and yard workers across Canada. On March 19, 2022, while the Company was still engaged in ongoing negotiations facilitated by federal mediators, the TCRC withdrew its services in the final hours before the deadline for a legal strike or lockout to potentially occur. On March 22, 2022, the Company reached an agreement with the TCRC Negotiating Committee to enter into binding arbitration. This agreement enabled the Company's employees to return to work effective at noon on March 22, 2022 local time to resume our essential services for our customers and the North American supply chain. On August 15, 2022, the Company entered into a new two-year collective agreement with the TCRC following binding arbitration. The new agreement includes a 3.5 percent wage increase in 2022 and 2023 as well as increased benefits. Under the arbitration decision, the TCRC has joined a pension improvement account. The new collective agreement is effective from January 1, 2022 to December 31, 2023.

Prior Developments

On December 14, 2021, following approval of the transactionexemption by, the shareholders of both the Company and KCS, receipt of Mexican regulatory approvals, and satisfaction or waiver of customary closing conditions and pursuant to the terms set forth in the Agreement and Plan of Merger (the "Merger Agreement") with KCS dated September 15, 2021, the acquisition of KCS was consummated and all outstanding stock of KCS was deposited into a voting trust and held by a single trustee as trust stock. Under the terms of the Merger Agreement, the Company issued 262.6 million Common Shares to existing KCS common stockholders at the exchange ratio of 2.884 Common Shares per share of KCS common stock and paid cash consideration to existing KCS stockholders of U.S. $90 per share of KCS common stock held and U.S. $37.50 per share of KCS preferred stock held for a total of approximately $10.5 billion (U.S. $8.2 billion). Share consideration, cash consideration, and the above described payments to KCS totaled approximately $36 billion (U.S. $28 billion). For additional information regarding this acquisition, refer to Item 8. Financial Statements and Supplementary Data, Note 10 Business acquisitions.

On September 15, 2021, upon KCS's termination of the Agreement and Plan of Merger with Canadian National Railway Company ("CN") (the "CN Merger Agreement"), the Company entered into the Merger Agreement with KCS. Pursuant to the terms of the CN Merger Agreement, KCS paid a merger termination fee of U.S. $700 million and refunded the CP merger termination fee of U.S. $700 million to CN (together, the "CN merger termination

fees"). In connection with the Merger Agreement, the Company remitted $1,773 million (U.S. $1,400 million) to KCS on September 15, 2021 in connection with KCS's payment of the CN merger termination fees.

On April 21, 2021, the five-for-one Share Split of the issued and outstanding Common Shares was approved at the Annual and Special Meeting of Shareholders. On May 13, 2021, the Company’s shareholders of record as of May 5, 2021 received four additional Common Shares for every Common Share held. Ex-distribution trading in the Company’s Common Shares on a split-adjusted basis commenced on May 14, 2021. Proportional adjustments were also made to outstanding awards under the Company's stock-based compensation plans in order to reflect the share split. All outstanding Common Shares, stock-based compensation awards, and per share amounts herein have been retrospectively adjusted to reflect the share split.STB.

Operations

The Company operates in only one operating segment: rail transportation. Although the Company provides a breakdown of revenue by business line, the overall financial and operational performance of the Company is analyzed as one segment due to the integrated nature of the rail network. Additional information regarding the Company's business and operations, including revenue and financial information, and information by geographic location is presented in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 8. Financial Statements and Supplementary Data, Note 2628 Segmented and geographic information.

Lines of Business

The Company transports freight consisting of bulk commodities, merchandise, and intermodal traffic. Bulk commodities, which typically move in large volumes across long distances, include Grain, Coal, Potash, and Fertilizers and sulphur. Merchandise freight consists of industrial and consumer products, such as Forest products, Energy, chemicals and plastics, Metals, minerals and consumer products, and Automotive. Intermodal traffic consists largely of retail goods in overseas containers that can be transported by train, ship and truck, and in domestic containers that can be moved by train and truck.

In 2022,2023, the Company generated Freight revenues totalling $8,627$12,281 million ($7,8168,627 million in 2021)2022). For purposes of this annual report, the following charts are presented as CPKC, which includes KCS as a consolidated subsidiary comprising a component of total freight revenues on and from April 14, 2023. Prior to April 14, 2023, the Company's 100% interest in KCS was reported as an equity-method investment.

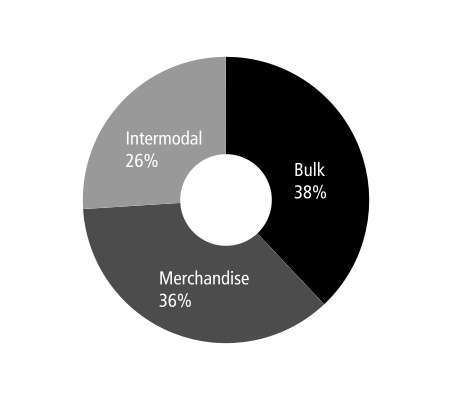

The following chart shows the percentage of the Company’s total Freight revenues derived from each of the three major business lines in 2022:2023:

| | | | |

20222023 Freight Revenues | | |

6 CP 2022CPKC 2023 ANNUAL REPORT/ 5

BULK

The Company's Bulk business represented approximately 38%35% of total Freight revenues in 2022.2023.

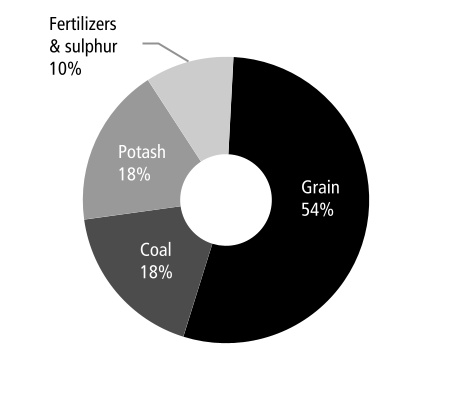

Bulk includes the Grain, Coal, Potash, and Fertilizer and sulphur lines of business. Bulk traffic predominantly moves in unit train service moving from one origin to one destination onby a single train without reclassification. The following chart shows the percentage of the Company's Bulk freight revenues by Lineline of business in 2022:2023:

| | | | |

20222023 Bulk Revenues | | |

(38%35% of Freight Revenues) | | |

Grain

The Company’s Grain business represented approximately 54%58% of Bulk revenues and was 20% of total Freight revenues in 2022.2023.

The Company's Grain network is unique among railways in North America as it is strategically positioned in the heart of grain-producing regions of western Canada and the Northern Plains of the U.S. The Company provides a service advantage to its customers through grain transportation in 8,500-foot High Efficiency Product ("HEP") trainsTrainsTM including high-capacity hopper cars, which enables the Company to efficiently serve farmers, shippers, and the entire grain supply chain. The 8,500-foot HEP trainTrainsTM can move approximately 40 percent more grain than the prior generation of grain train.

The following chart shows the percentage of the Company's Grain freight revenues generated from Canadian and U.S. shipments in 2023:

Canadian grain transported by the Company consists of both whole grains, such as wheat, durum, canola, and pulses, and soybeans, andas well as processed products such as meals, oils and malt.meals. This business is centred in the Canadian Prairies (Saskatchewan, Manitoba, and Alberta), with grain shipped primarily west to the Port of Vancouver, British Columbia and east to the Port of Thunder Bay, Ontario for export. Grain is also shipped to the U.S., and eastern Canada and Mexico for domestic consumption.

Canadian grain includes a division of business that is regulated by the Canadian government through the Canada Transportation Act (the “CTA”). This regulated business is subject to a maximum revenue entitlement (“MRE”). Under the CTA, railways can set their own rates for individual movements. However, the MRE governs aggregate revenue earned by the railway based on a formula that factors in the total volumes, length of haul, average revenue per ton, and inflationary adjustments. The regulation applies to western Canadian export grain shipments to the ports of Vancouver and Thunder Bay.

6 / CPKC 2023 ANNUAL REPORT

U.S. grain transported by the Company consists of both whole grains, such as corn, wheat, and soybeans, and durum, andas well as processed products such as meals, feed, meals, oils, and flour.oils. This business is centred in the states of Minnesota, North Dakota, and Iowa. Grain destined for domestic consumption is interchanged with other carriers to the U.S. Midwest, the U.S Northeast via Chicago, Illinois,Northern Plains and the U.S. Pacific Northwest.Midwest. The Company also delivers direct shipments of U.S. grain to western Canada primarily for animal feed. In partnership with other railways, the Company moves U.S. grain to facilities in Mexico, export terminals in the U.S. Pacific Northwest, and to various other destinations across the Gulf of Mexico. Export U.S. grain traffic is also shipped to the Port of Vancouver and the ports at Superior, Wisconsin and Duluth, Minnesota.Canada for domestic consumption.

Coal

The Company’s Coal business represented approximately 18%20% of Bulk revenues and was 7% of total Freight revenues in 2022.2023.

The following chart shows the percentage of the Company's Coal freight revenues generated from metallurgical and thermal coal in 2023:

In Canada, the Company handles mostly metallurgical coal destined for export for use in the steelmaking process. The Company’s Canadian coal traffic originates mainly from Teck Resources Limited’s mines in southeastern B.C. The Company primarily moves coal west from the mines to port terminals for export to world markets (Pacific Rim, Europe, and South America), and east for the U.S. Midwest markets..

In the U.S., the Company moves primarily thermal coal from connecting railways, serving the thermal coal fields in the Powder River Basin in Montana and Wyoming, which is delivered to power-generating facilities in the U.S. Gulf Coast and the U.S. Midwest.

Potash

The Company's Potash business represented approximately 18%13% of Bulk revenues and was 7%5% of total Freight revenues in 2022.2023.

The Company’s Potash traffic moves mainly from Saskatchewan to offshore markets through the portsPort of Vancouver, the Port of Portland, Oregon, and Thunder Bay, andthe U.S. Gulf Coast, as well as to domestic markets in the U.S.U.S Midwest. All potash shipments for export beyond Canada and the U.S. are marketed by Canpotex Limited or K+S Potash Canada. Canpotex is an export company owned in equal sharesequally by Nutrien Ltd. and The Mosaic Company. Independently, The Mosaic Company, Nutrien Ltd., and K+S Potash Canada move domestic potash with the Company primarily to the U.S. Midwest and eastern Canada for local application.

Fertilizers and Sulphur

The Company's Fertilizers and sulphur business represented approximately 10%9% of Bulk revenues and was 4%3% of total Freight revenues in 2022.2023.

The Company’s fertilizer traffic includes dry fertilizers, which are phosphate, urea, nitrate, and ammonium sulphate, and wet fertilizers, which are primarily anhydrous ammonia. Approximately half of the Company's fertilizer shipments originate from production facilities in Alberta, where abundant sources of natural gas and other chemicals provide feedstock for fertilizer production.

Most sulphur is produced in Alberta as a byproduct of oil and gas activity. Sulphur is a raw material used primarily in the manufacturing of sulphuric acid, which is used most extensively in the production of phosphate fertilizers.

CPKC 2023 ANNUAL REPORT / 7

MERCHANDISE

The Company’s Merchandise business represented approximately 36%45% of total Freight revenues in 2022.2023.

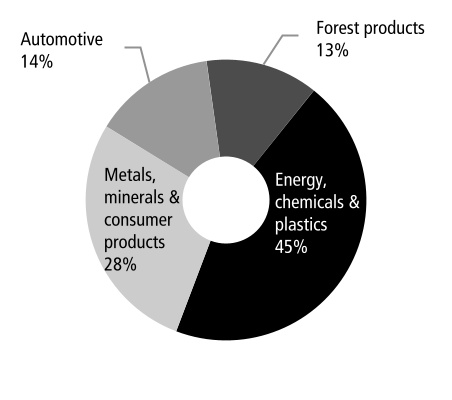

Merchandise products move in both mixed freight and unit trains in a variety of car types. Service involves delivering products to many different customers and destinations. In addition to traditional rail service, the Company moves merchandise traffic through a network of truck-rail transload facilities, expanding the reach of the Company's network to non-rail served facilities. The following chart shows the percentage of the Company's Merchandise freight revenue by Lineline of Businessbusiness in 2022:2023:

| | | | |

20222023 Merchandise Revenues | | |

(36%45% of Freight Revenues) | | |

Forest Products

The Company’s Forest products business represented approximately 13%12% of Merchandise revenues and was 5% of total Freight revenues in 2022.2023.

Forest products traffic primarily includes pulp and paper andas well as lumber and panel products shipped from key producing areas in the U.S. Gulf Coast, B.C., Ontario, Alberta, Québec, the U.S. Southeast, New Brunswick,Ontario, and the U.S. Northeast,Alberta to destinations throughout North America including the U.S. Midwest, the U.S. Northeast,Mexico, the U.S. Southeast, the U.S. Gulf Coast, and to export markets via Vancouver.the U.S. Northeast.

Energy, Chemicals and Plastics

The Company’s Energy, chemicals and plastics business represented approximately 45%42% of Merchandise revenues and was 16%19% of total Freight revenues in 2022.2023.

The Company moves energy products consisting of commodities such as fuel oil, liquefied petroleum gas ("LPG"L.P.G."), fuel oil, asphalt, gasoline, and other energy products. The majority of the Company’s western Canadian energy traffic originates in the Alberta Industrial Heartland Canada's(Canada's largest hydrocarbon processing region,region), the U.S. Gulf Coast, Saskatchewan, and Saskatchewan.Mexico. The Company accesses key destinations and export markets in Mexico, the U.S. Midwest, western Canada, the U.S. West Coast, and the U.S. Gulf Coast. The Company is a main transportation provider of refined fuels from the U.S. Gulf Coast into Mexico.

The Company’s chemical traffic includes products such as ethylene glycol, caustic soda, sulphuric acid, soda ash, and other chemical products. These shipments mainly originate from the U.S. Northeast,Gulf Coast, western Canada, and the U.S. Midwest and Mexico.move to end markets in the U.S., Mexico, Canada, and overseas.

The most commonly shipped plastics products are polyethylene and polypropylene. The majority of the Company’s plastics traffic originates from the U.S. Gulf Coast and Alberta and moves to various North American destinations.

The Company's biofuels traffic originates mainly from facilities in the U.S. Midwest, shipping primarily to destinations in the U.S. Northeast, the U.S. Gulf Coast,Southeast, and Alberta.

The Company moves crude primarily from production facilities throughout Alberta and Saskatchewan to refining markets primarily in the U.S. Gulf Coast. The majority of the Company’s crude is now moving as DRUbitTM, a sustainable heavy crude oil specifically designed for rail transportation and produced using an innovative facility known as a Diluent Recovery Unit, ("DRU"), which enables the removal of diluent at origin. This technology enables the safe and economical transportation of crude oil and is cost competitive with pipeline transportation. The Company transports DRUbitTM on a single line haul from the Hardisty Rail Terminal in Alberta to Port Neches, Texas, via interchange in Kansas City.Arthur, Texas.

The Company’s chemical traffic includes products such as ethylene glycol, caustic soda, sulphuric acid, methanol, and other chemical products. These shipments originate from western Canada, the Gulf Coast, eastern Canada, and the U.S. Midwest, and move to end markets in the U.S., Canada, and overseas.

The most commonly shipped plastics products are polyethylene and polypropylene. Approximately half of the Company’s plastics traffic originates in central and northern Alberta and moves to various North American destinations.

Metals, Minerals and Consumer Products

The Company’s Metals, minerals and consumer products business represented approximately 28%29% of Merchandise revenues and was 10%13% of total Freight revenues in 2022.2023.

The Company's Metals, minerals and consumer products freight revenues are generated from steel, aggregates, (including frac sand), steel, food and consumer products, and non-ferrous metals. Aggregate products include coarse particulate and composite materials such as frac sand, cement, limestone, gypsum,sand and other aggregate products.

The majority of frac sand originates at mines located along the Company's network in Wisconsinstone, clay bentonite, and moves to the Bakken and Marcellus shale formations, Permian shale basin, and other shale formations across North America.

Cement is shipped directly from production facilities in Alberta, the U.S. Midwest, Ontario, and Québec to energy and construction projects in the U.S. Midwest, western Canada, and the U.S. Pacific Northwest.gypsum.

The Company transports steel in various forms from mills in Mexico, the U.S. Midwest, the Canadian Prairies,U.S. Southeast, and Ontariowestern Canada to a variety of industrial users. The Company carries base metals such as aluminum, zinc, and lead. The Company also moves ores from mines to smelters and refineries for processing, and theas well as processed metalmetals to automobile and consumer productsproduct manufacturers.

The majority of frac sand originates at mines located along the Company's network in Wisconsin and Iowa and moves to the Bakken and Marcellus shale formations as well as other shale formations across North America.

Cement is shipped directly from production facilities in the U.S. Midwest, Alberta, Ontario, and Mexico to energy and construction projects in the U.S. Midwest, western Canada, Mexico, and western U.S.

Food, consumer, and other products traffic consists of a diverse mix of goods, including railway equipment, food products, railway equipment, building materials, and waste products.large domestic use appliances.

Automotive

The Company’s Automotive business represented approximately 14%17% of Merchandise revenues and was 5%8% of total Freight revenues in 2022.2023.

The Company’s Automotive portfolio consists of four finished vehicle traffic components: Canadian-produced vehicles that ship tooriginating from Canadian production facilities in Ontario, the U.S. from Ontario production facilities; vehicles, Mexico, and from overseas that moveare imported through the Port of VancouverVancouver. Finished vehicles are primarily to eastern Canadian markets as well as western Canadian markets; U.S.-produced vehicles that ship cross-border to Canadian markets as well as within the U.S.; and Mexican-produced vehicles that shipshipped to Canada, and the U.S., and Mexico. In addition to finished vehicles, the Company also ships pre-owned vehicles,automotive parts, machinery, and automotive parts.pre-owned vehicles. A comprehensive network of automotive compounds is utilized to facilitate final delivery of vehicles to dealers throughout Canada, the U.S, and inMexico. The Company services the U.S.majority of automotive plants within Mexico.

INTERMODAL

The Company’s Intermodal business represented approximately 26%20% of total Freight revenues in 2022.2023.

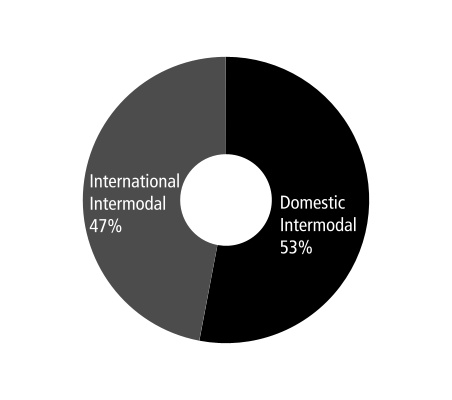

The Company's Intermodal freight revenues are generated from domestic and international movements. Domestic intermodal freight consists primarily of manufactured consumer products that are predominantly moved in 53-foot containers within North America. International intermodal freight moves in marine containers to and from ports and North American inland markets. The following chart shows the percentage of the Company's Intermodal freight revenues generated from domestic intermodal and international intermodal in 2022:2023:

| | | | |

20222023 Intermodal Revenues | | |

(26%20% of Freight Revenues) | | |

CPKC 2023 ANNUAL REPORT / 9

Domestic Intermodal

The Company's domestic business represented approximately 53%56% of Intermodal revenues and was 14%11% of total freight revenues in 2022.2023.

The Company’s domestic intermodal business moves goods from a broad spectrum of industries including wholesale, retail, food, and various other commodities. Key service factors in domestic intermodal include consistent on-time delivery and the ability to provide door-to-door service. The majority of the Company’s domestic intermodal business originates in Canada, where the Company markets its services directly to retailers and manufacturers and maintains direct relationships with its customers. In the U.S., and Mexico, the Company’s service is delivered mainly through intermodal marketing companies. In 2023, the Company launched the Mexico Midwest Express ("MMX") Series premium intermodal service to provide the first truck-competitive, single-line rail service option between the U.S. Midwest and Mexico.

International Intermodal

The Company's international business represented approximately 47%44% of Intermodal revenues and was 12%9% of total freight revenues in 2022.2023.

The Company’s international intermodal business consists primarily of containerized traffic moving between the portsPort of Vancouver,Vancouver; the Port of Montréal, Québec; the Port of Lázaro Cárdenas, Michoacán; the Port of Saint John, New Brunswick; and inland points across Canada and the U.S.North America. Import traffic from the Port of Vancouver is mainly long-haul business destined for eastern Canada and the U.S. Midwest. The Company works closely with the Port of Montréal, a major year-round East Coast gateway to Europe, to serve markets primarily in Canada and the U.S. Midwest. Import traffic from the Port of Lázaro Cárdenas is primarily destined for Mexico. The Company's access to the Port of Saint John provides the fastest rail service from the east coastEast Coast to thewestern Canadian and U.S. Midwest markets for import from and export cargo fromto Europe, South America, and Asia.

Fuel Cost Adjustment Program

The short-term volatility in fuel prices may adversely or positively impact revenues. The Company employs a fuel cost adjustment program designed to respond to fluctuations in fuel prices and help reduce volatility to changing fuel prices. Fuel surcharge revenues are earned on individual shipments and are based primarily on the price of On-Highway Diesel.Diesel in Canada and the U.S. and the public fuel price for Petróleos Mexicanos ("PEMEX") TAR Irapuato in Mexico. As such, fuel surcharge revenues are a function of freight volumes and fuel prices. Fuel surcharge

revenues accounted for approximately 15%13% of the Company's Freight revenues in 2022.2023. The Company is also subject to carbon taxation systems and levies in some jurisdictions in which it operates, the costs of which are passed on to the shipper. As such, fuel surcharge revenue includes carbon taxes and levy recoveries.

Freight revenues included fuel surcharge revenues of $1,303$1,623 million in 2022,2023, an increase of $768$320 million, or 144%25%, from $535$1,303 million in the same period of 2021.2022. This increase was primarily due to the impact of the KCS acquisition, the favourable impact from the timing of recoveries under the Company's fuel cost adjustment program, the favourable impact of the change in foreign exchange ("FX"), and higher volumes, partially offset by lower fuel prices and increased carbon tax recoveries.prices.

Significant Customers

For each of the years ended December 31, 20222023 and 2021,2022, the Company's revenues and operations were not dependent on any major customers.

Competition

The Company is in the ground transportation and logistics business. The Company sees competition in this segment from other railways, motor carriers, ship and barge operators, and pipelines. Depending on the specific market, competing railways, motor carriers, and other competitors may exert pressure on price and service levels. The Company continually evaluates the market needs and the competition. The Company responds as it deems appropriate to provide competitive services to the market. This includes developing new offerings such as transload facilities, new train services, and other logistics services.

Seasonality

Volumes and revenues from certain goods are stronger during different periods of the year. First-quarter revenues are typically lower mainly due to winter weather conditions, which results in reduced capacity under the winter operating plan with train length restrictions, the closure of the Port of Thunder Bay, and reduced transportation of retail goods. Second and third quarter revenues generally improve compared to the first quarter, as fertilizer volumes are typically highest during the second quarter and demand for construction-related goods is generally highest in the third quarter. Revenues are typically strongest in the fourth quarter, primarily as a result of the transportation of grain after the harvest, fall fertilizer programs, and increased demand for retail goods moved by rail. Operating income is also affected by seasonal fluctuations. Operating income is typically lowest in the first quarter due to lower freight revenue and higher operating costs associated with winter conditions.

Government Regulation

The Company’s railway operations are subject to extensive federal laws, regulations, and rules in the countries in which it operates, which directly affect how operations and business activities are managed.

10 / CPKC 2023 ANNUAL REPORT

Canada

The Company’s rail operations in Canada are subject to economic regulation by the Canadian Transportation Agency (the "Agency”) pursuant to authorities under the CTA. The CTA establishes a common carrier obligation and it indirectly regulates rates by providing shippers access to regulatory mechanisms for challenging freight rates, including ancillary charges, and access to regulated interswitching rates and long-haul interswitching rates; and regulatory mechanisms to challenge level of service. The CTA also establishes an MRE for the transportation of Canadian export grain and other agriculture products, which is administered by the Agency. Finally, the Agency makes regulatory determinations regarding the construction and abandonment of railway lines, commuter and passenger access, and noise and vibration-related disputes.

The Company’s rail operations in Canada are subject to safety and security regulatory requirements enforced by Transport Canada ("TC") pursuant to the Railway Safety Act ("RSA") and the Transportation of Dangerous Goods Act (the "TDGA"). The RSA regulates safety-related aspects of railway operations in Canada, including the delegation of inspection, investigation, and enforcement powers to TC. TC is also responsible for overseeing the safe and secure transportation of dangerous goods.

Various other regulators directly and indirectly affect the Company’s operations in areas such as health, safety, environment, climate, sustainability and other matters.

U.S.

The Company’s U.S. rail operations are subject to economic regulation by the STB. The STB provides economic regulatory oversight and administers Title 49 of the United States Code and related Code of Federal Regulations. The STB has jurisdiction over railroad rate and service issues, proposed railroad mergers, and other transactions.

The Company’s U.S. operations are subject to safety regulations enforced by the Federal Railroad Administration (the “FRA”), and the Pipeline and Hazardous Materials Safety Administration (“PHMSA”). The FRA regulates safety-related aspects of the Company’s railway operations in the U.S. under the Federal Railroad Safety Act, as well as rail portions of other safety statutes. The PHMSA regulates the safe transportation of hazardous materials by

rail. The Company’s U.S. rail operations are also subject to security regulations and directives by the Transportation Security Administration ("TSA"), a component of the U.S. Department of Homeland Security.

Various other regulators directly and indirectly affect the Company’s operations in areas such as health, safety, security, environmental, climate, sustainability and other matters.

Mexico

Primary regulatory oversight of the Company’s Mexican operations is provided by the Mexican Agencia Reguladora del Transporte Ferroviario (also known as Mexico's Railway Transport Regulatory Agency) (the "ARTF"). The ARTF establishes regulations concerning railway safety and operations, and is responsible for resolving disputes between railways and customers. Kansas City Southern de México, S.A. de C.V. (also known as Canadian Pacific Kansas City Mexico) ("CPKCM") must register its maximum rates with the ARTF and make regular reports to the ARTF and the Secretaría de Infraestructura, Comunicaciones y Transportes (also known as Secretariat of Infrastructure, Communications and Transportation) (the "SICT").

CPKCM must provide reports on investments, traffic volumes, theft and vandalism on the general right of way, customer complaints, fuel consumption, number of locomotives, railcars and employees, and activities around maintenance of way, sidings and spurs, among other financial information and reports. The Company may freely set rates on a non-discriminatory basis up to the maximum rates registered with the ARTF. At any time, the ARTF may request additional information regarding the determination of maximum rates and may issue recommendations with respect to proposed rate increases. If the ARTF or another party considers there to be no effective competition, they may request an opinion from the Comisión Federal de Competencia Económica (also known as Mexican Antitrust Commission) (the “COFECE”) regarding market conditions. If the COFECE determines that there is no effective competition for particular movements, the ARTF could set rates for those movements or grant limited trackage rights to another railroad while the condition of no effective competition remains.

CPKCM holds a concession from the Mexican government until June 2047, which is renewable under certain conditions for additional periods of up to 50 years (the "Concession"). CPKCM has the exclusive right to provide the freight rail service through 2037, subject to certain trackage and haulage rights granted to other freight rail concessionaires, and subject to trackage and haulage rights afforded to concessionaires of concessions that may be granted by the SICT to provide passenger rail service in the future. The Concession authorizes CPKCM to provide freight transportation services over north-east rail lines, which are a primary commercial corridor of the Mexican railroad system. CPKCM is required to provide freight railroad services to all users on a fair and non-discriminatory basis and in accordance with efficiency and safety standards approved periodically by the Mexican government. CPKCM has the right to use, but does not own, all track and buildings that are necessary for the rail lines’ operation. CPKCM is obligated to maintain the right of way, track structure, buildings and related maintenance facilities to the operational standards specified in the Concession agreement and to return the assets in that condition at the end of the Concession period. During the remainder of the Concession period, CPKCM is required to pay the Mexican government an

CPKC 2023 ANNUAL REPORT / 11

annual concession duty equal to 1.25% of gross revenues. The ARTF may request information to verify CPKCM´s compliance with the Concession and any applicable regulatory framework.

Environmental Laws, Regulations and RegulationsStrategies

The Company’s operations and real estate assets are subject to extensive federal, provincial, state, and local environmental laws and regulations, including those governing air pollutants, greenhouse gas ("GHG") emissions, (please see “Sustainability-Related Laws, Regulations and Strategies” for further discussion), management and remediation of historical contaminant sites, discharges to waters and the handling, storage, transportation, and disposal of waste and other materials. If the Company is found to have violated such laws or regulations, itor to have acted in a manner that is inconsistent with regulatory expectations, such a finding could have a material adverse effect on the Company’s business, financial condition, or operating results. In addition, in operating a railway, it is possible that releases of hazardous materials during derailments or other accidents have, or may occur, that could cause harm to human health or to the environment. Costs of remediation, damages and changes in regulations could materially affect the Company’s operating results, financial condition, and reputation. Please see “Legal and Regulatory Risks” in Item 1A. Risk Factors for further discussion.

The Company has implemented an Environmental Management System to facilitate the reduction of environmental risk. Specific environmental programs are in place and designed to address areas such as locomotive air emissions, GHG reporting, management of vegetation, wastewater, chemicals and waste, storage tanks, and fueling facilities. The Company has also undertaken environmental impact assessments and risk assessments designed to identify, prevent, and mitigate environmental risks. There is continued focus on preventing spills and other incidents that have a negative impact on the environment. There is an established strategic emergency response contractor network, and spill equipment kits are located across its network to ensuresupport a rapid and efficient response in the event of an environmental incident. In addition, emergency preparedness and response plans are regularly updated and tested.

The Company has developedestablished an environmental audit program that comprehensively, systematically,aimed at conducting thorough, systematic, and regularly assesses the Company’sroutine assessments of its facilities forto ensure compliance with legal requirements and the Company’s policies for conformanceadherence to accepted industry standards. Included in this isstandards, accompanied by a corrective action follow-up process and review by senior management.management review.

The Company focuses on key strategies, identifying tactics and actions to support and operationalize our environmental commitments. The Company’s environmental strategies include:

•Implementing measures to minimize or prevent environmental impacts from our operations and facilities, and to ensure compliance with applicable environmental laws and regulations;

•Maintaining an Environmental Management System to provide consistent, effective guidance and resources to the Company's employees in regard to the management of air emissions, dangerous goods and waste materials, emergency preparedness and response, petroleum products management, and water and wastewater systems;

•Reducing environmental and safety risk through business processes to identify and mitigate potential environmental impacts related to all the Company's operations and activities;

•Ensuring that new or altered operations and other business activities are evaluated, planned, permitted in accordance with applicable regulations, and executed to mitigate environmental risk;

•Engaging with relevant stakeholders to consider and discuss the Company’s environmental management practices and environmental issues and concerns associated with our operations;

•Employing best practices, proven technologies, and safe operating standards for activities involving elevated environmental risk; and

•Planning and preparing for emergency responses to ensure all appropriate steps are taken in the event of a derailment, spill, or other incident involving a release to the environment.

Security

The Company is subject to statutory and regulatory requirements across its network that address security concerns. The Company plays a critical role in the North American transportation system. Rail lines, facilities and equipment, including railcars carrying hazardous materials, could be direct targets or indirect casualties of terrorist attacks, actions by criminal and non-criminal organizations, and activities by individuals. Regulations by the U.S. Department of Transportation and the U.S. Department of Homeland Security include speed restrictions, chain of custody, and security measures, which can impact service and increase costs for the transportation of hazardous materials, especially materials that are toxic inhalation hazards ("TIH") materials.. Regulations issued by TC under the TDGA have added requirements for railway companies to take actions to mitigate security risks of transporting dangerous goods by rail.

The Company takes the following security measures:

•The Company employs its own police service that works closely with communities and other law enforcement and government agencies to promote railway safety and infrastructure security. As a railway law enforcement agency, the Company's Police Services hashave a central headquarterheadquarters that oversees police officers assigned to field offices responsible for railway police operations across its network. The Company's Police Services operate on the Company's rail network as well as in areas where the Company has non-railway operations;

12 / CPKC 2023 ANNUAL REPORT

•The Company's Corporate Security department is committed to providing a safe and secure work environment for the Company’s employees, contractors, visitors, and other authorized persons on the Company's property, and to protecting the Company’s assets, operations, information, the

public and the environment from damage, interference, and undue liability. As part of this commitment, Corporate Security is responsible for ensuring:overseeing: the security of the International Supply Chaininternational supply chain and its requisite programs; providing training and awareness to employees and contractors; assessing the risk and vulnerability of the Company’s properties; establishing appropriate countermeasurecountermeasures to secure and protect the Company’s properties and assets; and engage with customers and the public. Specifically, the Company employs the following to support these initiatives:

◦The Company’s Security Management Plan is a comprehensive, risk-based plan modelled on and developed in conjunction with the security plan prepared by the Association of American Railroads post-September 11, 2001. Under this plan, the Company routinely examines and prioritizes railway assets, physical and cyber vulnerabilities, and threats, as well as tests and revises measures to provide essential railway security;

◦The Company’s Public Safety Communication Centre ("PSCC") operates 24 hours a day. PSCC receives reports of emergencies, dangerous or potentially dangerous conditions, and other safety and security issues from our employees, the public, and law enforcement and other government officials. PSCC ensures that proper emergency responders and governing bodies are notified; and

•To address cyber security risks, the Company’s Enterprise Security Department implements mitigation programs that evolve with the changing technology threat environment. The Company has also worked diligently to establish backup sites to ensure a seamless transition in the event that the Company's operating systems are the target of a cyber-attack. By doing so, the Company is ableexpects to maintain network fluidity. Please see Item 1C. Cybersecurity for further discussion.

While the risk of theft and vandalism is comparatively higher in Mexico, we believe CPKCM remains among the safest and most secure methods of transportation for freight shipments in Mexico. CPKCM’s sector leading security record is due in large part to the implementation of a secure corridor: integrating a multi-layered safety and security process throughout the CPKCM network. In addition to having its own internal system, the process is connected to, and supported by, federal, state and local law enforcement. A primary focus of this effort involves maintaining diligence, intelligence and counterintelligence operations, technology-reporting applications and active vigilance while enhancing overall system velocity, which reduces the residual risk for incidents to occur.

Focus on Sustainability - Related Laws, Regulations and Strategies

Sustainability at the Company is rooted in a long-standing legacy of building for the future. We recognize that integrating sustainability into our business processes is imperative to future growth and long-term success as an organization. As one of North America’s top-performing railways, we seek to continue to innovate and to advance practices to create value for the Company’s stakeholders, including employees, customers, shareholders, suppliers, and local and Indigenous communities. We are proud to be recognized as a corporate sustainability leader in our industry.

To ensure thatThrough ongoing engagement and collaboration across and beyond our organization, the Company manages thecontinually refines our sustainability topics most significantapproach, including as part of our integration of KCS. Please see “Climate-Related Risks—Transition Risks" in Item 1A. Risk Factors for further discussion. We value feedback from our stakeholders, strive to learn from our businessperformance and stakeholders, we have structuredconstantly challenge ourselves to improve our management approach across three strategic areas. Ourpractices, including our sustainability practice is grounded in our commitment to safety, operational excellence, and social impact, and is designed to inspire action across our business.

In recent years, federal, state and international lawmakers and regulators have increased their focus on companies’ risk oversight, disclosures and practices in connection with climate change and other ESG matters. Recent legal developments with respect to climate- and other ESG-related matters include the rulemaking activities of securities regulatory authorities in Canada and the United States. In addition, recently enacted or proposed ESG-related statutes or regulations in certain U.S. states may impact the operations, preferences, activities and financial conditions of the Company and its customers and other stakeholders. We are monitoring these legal developments, as well as trends in climate and other ESG-related litigation and regulatory investigations, as well as their potential impact on the Company’s climate and other ESG-related activities (including its strategies, disclosure and risk management practices). Please see “Legal and Regulatory Risks” in Item 1A. Risk Factors for further discussion.

Sustainability Governance

Recognizing the importance of sustainability to our business and to our internal and external stakeholders, theThe Company has established a clear governance structure to effectively communicate and respond to environmental, social and governance ("ESG")relevant ESG topics, while proactivelystriving to be proactive in implementing ourits sustainability commitments and practices. The Board of Directors, through its committees, is responsible for the monitoring measurement and oversight of the Company's key risks and strategies andon sustainability topics. The Risk and Sustainability Committee of the Board reviewsis responsible for reviewing ESG performance against short- and long-term sustainability objectives, as well as strategic plans and evaluates results of stakeholder engagementopportunities to ensure alignmentalign sustainability objectives with the Company’s strategic planning.long-term climate strategy.

With oversight from the President and CEOChief Executive Officer of the Company, decisions on day-to-day implementation of the Company’s sustainability priorities areobjectives is guided by a cross-functional executive Sustainability Steering Committee. The Sustainability Steering Committee regularlyUpdates and progress reports progress and advances recommendations on the Company’sCompany's sustainability objectives policies, and management approach to sustainability topics are regularly provided to the Risk and Sustainability Committee of the Board.

Through ongoing engagement and collaboration across and beyond our organization, the Company continually refines its sustainability approach, which is driven by our values and based on a shared sense of purpose, community, and vision for the future. We value feedback from our stakeholders, strive to learn from our performance and constantly challenge ourselves to improve our practices. As we continue to embed sustainability practices in our business, we are committed to improving our ESG disclosures to align with best practices and recognized sustainability disclosure standards.

CPKC 2023 ANNUAL REPORT / 13

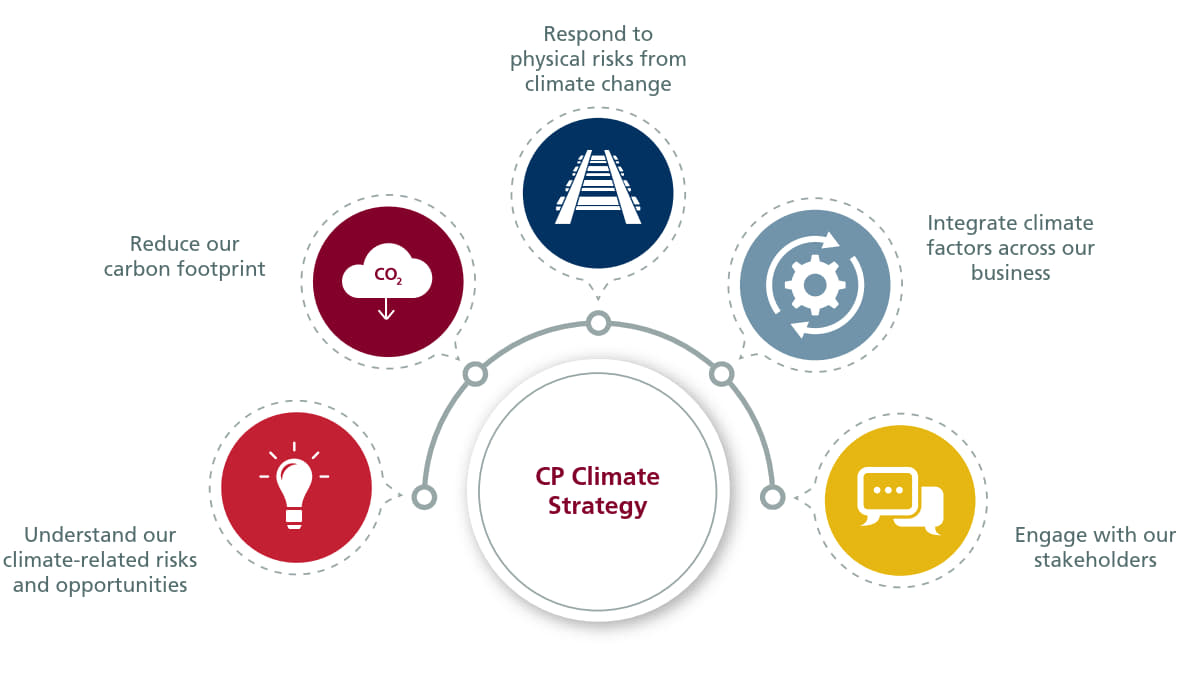

Climate Change

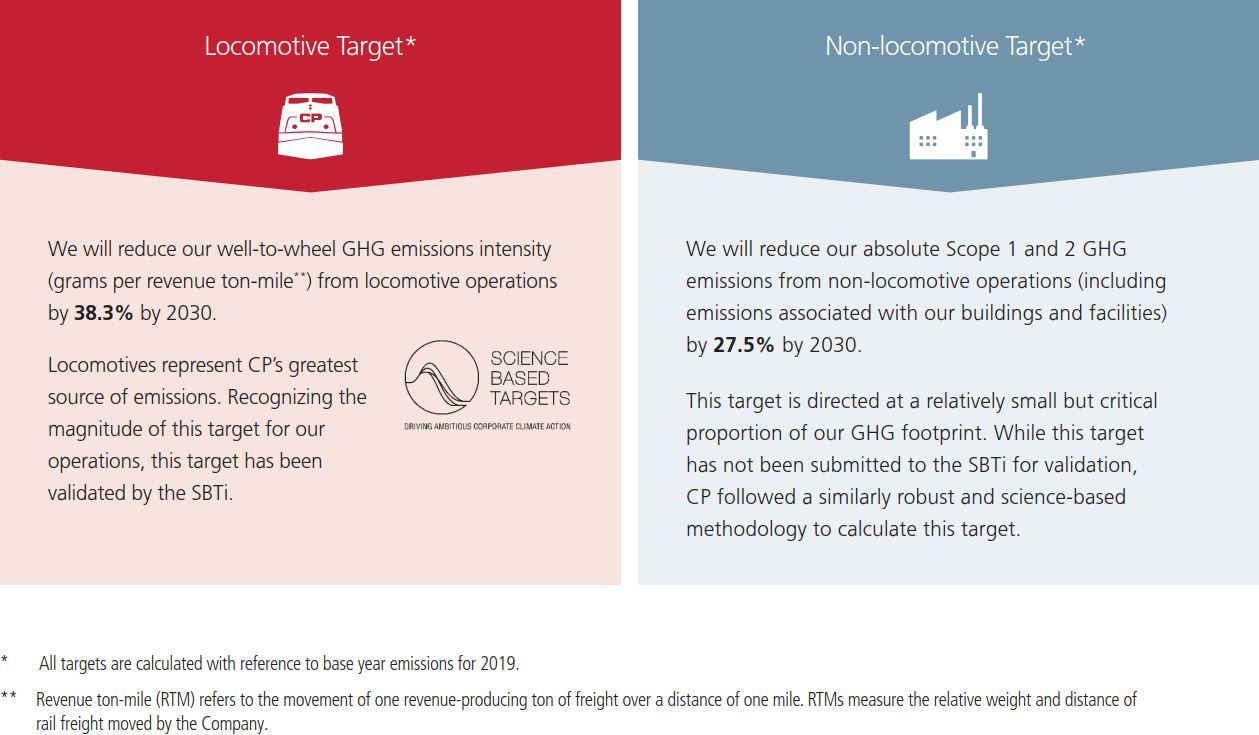

ClimateThe Company recognizes that climate change represents a significant global challengepresents both risks and the Company is committedopportunities to adapting our business and operations.business. The Company published its first Climate Strategy in 2021, outlining our approach to managing potential climate-related impacts reducing our carbon footprint, and seeking to positionacross the Company as an industry leader in the transition to a low-carbon future. As part of the Climate Strategy, the Company established science-based GHG emissions reduction targets covering 100% of Scope 1 and 2 emissions and more than half of our Scope 3 emissions.business.

Science-based targets are used by many companies to establish a pathway for GHG emissions reduction across their organizations. Emissions reduction targets are considered science-based if they align with both current climate science and the objectives of the Paris Agreement. Over the past year, the Company has taken action to support the execution of our Climate Strategy. The Science Based Targets initiative (SBTi) workscarbon reduction efforts, including in connection with our integration of KCS. In June 2023, the private sector to set and validate science-based emissions targets, and align corporate ambitions with global goals and investor expectations for business resilience inCompany announced a net-zero economy. The SBTi has developed standardized tools, resources, and sector-specific methodologies to support company-specificconsolidated 2030 locomotive GHG emissions reduction targets.target using the SBTi’s sectoral-based approach for freight railroads and a well-below 2⁰C global warming scenario. The SBTi is a partnership ofconsolidated 2030 target for the World Resources Institute, CDP, United Nations Global Compact, andCompany's combined locomotive operations was validated by the World Wildlife Fund for Nature.

14 CP 2022 ANNUAL REPORT

SBTi.

To respond to the risks and opportunities posed by climate change and meet our decarbonization commitments, our Climate Strategy includes actions across five strategic pillars. We are strengthening roles and responsibilities for climate governance. The Company's President and CEO's oversight of the Sustainability Steering Committee includes performance related to climate change, while the Risk and Sustainability Committee of the Board provides oversight and reviews climate-related risks and opportunities. To lead our focus on decarbonization, in 2022 we have established a Carbon Reduction Task Force, composed of the Company’s industry-leading engineers and operations experts. Reporting to the Sustainability Steering Committee, the Carbon Reduction Task Force evaluates, recommends, and implements climate action measures to reduce GHG emissions and drive performance in the direction of our science-based targets.

CPThe Company also strives to advance implementation of our climate strategy by exploring carbon reduction opportunities that are aligned to the demands of our business. For example, the Company is building North America’s first line-haul hydrogen-powered locomotive using fuel cells and batteries to power the locomotive’s electric traction motors. In 2022,2023, the Company advancedcontinued to advance our hydrogen locomotive program, placing two converted hydrogen locomotive into service and advancing production on three hydrogen locomotive conversions and installinga third, as well the installation of hydrogen production and fueling facilities. This industry-leading project is demonstrating the technical performance in real-world operations and generating critical industry knowledge and experience that is informing future commercialization and development activities. CP's Hydrogen Locomotive program passed a significant milestone in 2022 by completing the first successful movement and freight service testing on the initial hydrogen locomotive.

CP aligns our reporting by including the recommendations from the Task Force on Climate-related Financial Disclosure ("TCFD") and has issued a TCFD aligned Index to demonstrate CP's full alignment to the recommendations. In addition, we regularly report on climate-related efforts through CDP and supplemental sustainability disclosures.

Human Capital Management

The Company is focused on attracting, developing, and retaining a resilient, high-performing workforce that delivers on providing service for our customers. The Company's culture is guided by three core values:the values of Accountability, Diversity, and Pride. TheseBuilt on a bedrock of respect, these values drive our actions. Everything we do is grounded in precision scheduled railroading and our five foundations of Provide Service, Control Costs, Optimize Assets, Operate Safely, and Develop People.

A team of approximately 13,00020,000 railroaders across North America underpins the Company’s success and brings value to our customers and shareholders. Accordingly, Develop People is one of the foundations of how we do business, illustrating our focus and energy towards empowering our people, providing an engaging culture, and cultivating an industry leading team.

Total Employees and Workforce

An employee is defined by the Company as an individual currently engaged in full-time, part-time, or seasonal employment with CP.the Company. The total number of employees as of December 31, 20222023, was 12,754,19,927 for CPKC, an increase of 9207,173 compared to 11,83412,754 for legacy CP only as at December 31, 2021.2022.

Workforce is defined as total employees plus contractors and consultants. The total workforce as at December 31, 20222023 was 12,824,20,038 for CPKC, an increase of 9527,214 compared to 11,87212,824 for legacy CP only as at December 31, 2021.2022.

Unionized Workforce

Class I railways are party to collective bargaining agreements with various labour unions. The majority of the Company's employees belong to labour unions and are subject to these agreements. The Company manages collaborative relationships with union members in both Canada, and the U.S. and Mexico.

Unionized employees represent nearly 74% of our workforce and are represented by 3775 active bargaining units.

Canada

Within Canada there are nine bargaining units representing approximately 7,200 Canadian unionized active employees. From time to time, we negotiate to renew collective agreements with various unionized groups of employees. In such cases, the collective agreements remain in effect until the bargaining process has been exhausted (pursuant to the Canada Labour Code). FourThree agreements are open for renewal of which one has been tentatively agreedreferred to binding Mediation/Arbitration and incollective bargaining has commenced with the ratification stage.Teamsters Canada Rail Conference for the other two. Agreements are in place with the other fivesix bargaining units in Canada, of which two collective agreements are effective until December 31, 2023, one is effective until December 31, 2024, one istwo are effective until December 31, 2025 and the last onetwo are effective until December 31, 2026.

U.S.

In the U.S., there are currently 2865 active bargaining units on fournine subsidiary railroads representing approximately 2,3004,400 unionized active employees. Agreements are in place with respect to 1762 bargaining units which will expire in or beyond 2023.2024. Negotiations have concluded on 2 agreements that are pending ratification, and negotiations are ongoing with the remaining 9three agreements.

14 / CPKC 2023 ANNUAL REPORT

Mexico

In Mexico, approximately 3,200 of CPKCM employees are covered by a single labour agreement. The compensation terms under this labour agreement are subject to renegotiation on an annual basis and all other benefits are subject to negotiation every two years. The current agreement terms will remain in effect until new terms have been negotiated in 2024.

Health and Safety

The Company is an industry leader in rail safety and we are committed to protecting our employees, our communities, our environment, and our customers’ goods. The Company remained an industry leader in train accident statistics for the 17th consecutive year and achievedfinished 2023 with the lowest everFRA train accident frequency recorded by aamong Class I railway. FRA personal injury frequency for 2022 was alsorailways: building on the second lowest ever recorded byCP's 17 consecutive years leading the Company.industry. The Company's leadership approach has been the most impactful driver of the strong safety performance metrics and we are committed to continually improving on them. Aside from running trains, many of our employees work in yards, terminals, and shops across our network with machinery and heavy equipment, orand often in extreme weather conditions. Their safety is of utmost importance to the Company and through 20222023 we have continued to look at ways to improve safety in these areas of the operation. Operate Safely is one of our five foundations of successful railroading and it starts with knowing and following the rules. The FRA reportable train accident and personal injury frequency rates are key metrics as part of the Company's annual incentive plan.

The ongoing reinforcement ofDuring 2023, we rolled out our HomeSafe initiative continues to drive improvement byKCS and CPKCM tapping into the human side of safety and promotingwhat it means to promote both safety engagement and feedback. HomeSafe defines the commitment and actions needed to ensure everyone goes home safely each day. HomeSafe puts everyone on the same level and empowers all employees to begin a safety conversation, no matter their role or position. We intend to continue strengthening our strongExpanding HomeSafe, culture in 2023 through active peer engagement, safetySafety walkabouts and awareness initiatives.other safety initiatives to the KCS and CPKCM has been instrumental in maintaining a strong safety performance in 2023.

Our reportable personal injury incidents rate per 200,000 employee-hours increased 10%15% to 1.01 (20211.16 (2022 - 0.92)1.01) and our reportable train accident rate per million train-miles decreased 15%increased 14% to 0.93 (20211.06 (2022 - 1.10)0.93). The 2022 numbers reflect legacy CP on a standalone basis. The Company’s safety performance is disclosed publicly on a quarterly basis using standardized metrics set out by the FRA.

Talent Management

The Company’s approach for talent management begins with our Human Resources department, which oversees recruitment, development, engagement, and retention with the current and future workforce and leadership of the Company.

The Management Resources and Compensation Committee of the Board of Directors reviews and informs the Company’s compensation plan and programming, and makes recommendations to the Board on succession planning for senior management and processes to identify, develop, and retain executive talent. Additionally, as part of the Company’s succession planning program, senior leaders are actively engaged in building the pool of future leaders and present their development plans to the Board.

The Company maintains a number of internal policies and processes related to recruitment, relocation, compensation, employment equity, and diversity and inclusion. The effective implementation of these policies alongside our ongoing workforce initiatives ensures the Company’s attraction and

recruitment, employee development, succession, engagement, and diversity and inclusion practices are consistent and aligned with the Company’s commitments, foundations, and values.

Attraction and Recruitment

We employ a number of recruitment strategies and retention tactics to attract and retain talent across North America. The Company offers many rewarding career opportunities in a variety of roles within the organization in both operating and support functions. We base our recruitment strategy on workforce planning needs, and our focusgoal is on ensuring that weto have a diverse candidate pool to fill our open positions.

The Company recognizes the valuable skills and experience that veterans have gained from serving their country. Our veteran program was recognized as part of Canada's Best Diversity Employers® of 2021 and weWe were named part of the top 10 Military Friendly® Employers in the U.S. for 2023.2024. The Company was also named Canada's Top 100 Employers for 20232024 as well as Alberta's Top 7580 Employers for 2023.2024.

The Company tracks recruitment performance and success rates to better understand which tactics, benefits, and strategic partnerships are most successful in bringing in and retaining new talent.

TalentTraining and Leadership Development & Succession

As partOne of our core foundation and commitmentthe Company’s five foundations is to Develop People, we encouragePeople. CPKC achieves this by providing its diverse workforce with an array of training and development opportunities.

CPKC 2023 ANNUAL REPORT / 15

Our strategy involves delivering specialized training, best practices, and skill-broadening opportunities to all employees. The Company offers a variety of training opportunities, including, but not limited to, technical/on-the-job training, role-specific offerings as well as optional courses. Training includes instructor-led in-person and virtual classes, blended, e-learning and self-directed online learning.

Non-union employees also complete annual performance reviews with development action plans with their leaders to set individual goals tied to the Company's five foundations and track progress against Company expectations as well as career development goals. Additionally, the Company offers a robust set of leadership development programs to support employees career growth.

The Company encourages all employees to take an active role in their career planning and development. We believe that investing in our employees leads to improved workplace morale and fosters a supportive working environment.

Training and Development

One of the Company’s five foundations is to Develop People, which is integral to the way we do business at the railway. Our strategy involves delivering specialized training, best practices, and skill-broadening opportunities to all employees.

The Company offers a variety of training opportunities, providing both technical/on-the-job training, role-specific offerings as well as optional courses. Training includes instructor-led classes and online on-demand, self-directed online learning.

Non-union employees also complete annual performance management and development action plans with their leaders to set individual goals tied to the Company's five key foundations and track progress against Company expectations as well as career development goals.

Diversity and Inclusion