UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20212023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

COMMISSION FILE NUMBER: 000-16509

CITIZENS, INC.

(Exact name of registrant as specified in its charter)charter)

| | | | | | | | |

| Colorado | | 84-0755371 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. employer identification no.) |

11815 Alterra Pkwy, Suite 1500, Austin, TX 78758

(Address (Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code (512) 837-7100

| | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act |

|

| Class A Common Stock | CIA | New York Stock Exchange |

| (Title of each class) | (Trading symbol(s)) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☒ | | Non-accelerated filer | ☐ | | Smaller reporting company | ☐☒ | | Emerging growth company | ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

As of June 30, 2021,2023, the aggregate market value of the Class A common stock held by non-affiliates of the registrant was approximately $294,118,656.$115,859,350.

NumberAs of March 6, 2024, the Registrant had 49,572,398 shares of Class A common stock outstanding as of March 04, 2022.

Class A: 49,028,634

Class B: —outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Report incorporates by reference certain portions of the definitive proxy materials to be delivered to stockholders in connection with the 20222024 Annual Meeting of Shareholders (the "2022"2024 Proxy Statement"). The 20222024 Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

TABLE OF CONTENTS

| | | | | | | | |

| | Page |

| PART I | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| PART II | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| PART IV | | |

| Item 15. | | |

| Item 16. | | |

| | |

| | |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (“Form 10-K”) contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Many of the forward-looking1995. All statements are locatedcontained in Part II, Item 7 of this Form 10-K under the heading “Management’s Discussionother than statements of historical fact, including statements regarding our future results of operations and Analysis of Financial Conditionfinancial position, our business strategy and Results of Operations.”plans, our expected capital needs, and our objectives for future operations, are forward-looking statements. Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Forward-looking statements can alsomay be identified by words such as “future,” “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “will,” “would,” “could,” “can,” “may,” and similar terms. Forward-lookingWe have based these forward-looking statements include, butlargely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in Part I, Item 1A, Risk Factors in this Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not limited to, statements regarding: •the Company being positioned to offer stability topossible for our management team, employees and independent sales force in order to move forward with our business and strategic initiatives;

•cross-selling opportunities leading to revenue growth;

•efforts to develop and enhance our products, incentivize our sales force and make process and technology improvements to put the Company on a stronger financial footing and drive sustainable growth;

•competitive advantages over competitors;

•continued premium growth in the Home Service Insurance segment via new products and increased focus on direct sales through our independent agents;

•the attractiveness and competitiveness of our standard commission structure;

•the long-term value of providing agent campaigns and promotions with additional incentives;

•predict all risks, nor can we assess the impact of our retention efforts on the decline in renewal premiums;

•the increasing need for age-related products and increasing demand for living benefit products rather than death benefit products; and

•the impact of the COVID-19 pandemicall factors on our first year premium revenue.business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this Form 10-K may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

Forward-looking statements are not guarantees of future performance and the Company’s actual results may differ significantly from the results discussed in the forward-looking statements. Factors that might cause such differences include, but are not limited to, those discussed in Part I, Item 1A of this Form 10-K under the heading “Risk Factors.” Currently, some of the most significant factors that could cause our actual results to differ significantly from our forward-looking statements include risks related to the ongoing COVID-19 pandemic, such as:

•a higher level of claims due to COVID-19 deaths;

•decreased premium revenue due to disruption to our workforce or distribution channel resulting from required isolation, travel limitations and business restrictions;

•higher surrenders and lapses due to cash needs our policyholders may have due to concerns over COVID-19 economic impacts, particularly in our international business; and

•volatility in our investment portfolio due to market disruptions caused by COVID-19 related concerns such as inflation.

The Company assumesWe assume no obligation to revise or update any forward-looking statements for any reason, except as required by law. You should be aware that factors not referred to above could affect the accuracy of our forward-looking statements and use caution and common sense when considering our forward-looking statements.

ACCESS TO INFORMATION

The U.S. Securities and Exchange Commission ("SEC") maintains a website that contains reports, proxy and information statements, and other information regarding issuers, including the Company, that file electronically with the SEC. The public can obtain any documents that the Company files with the SEC at http://www.sec.gov. We also make available, free of charge, through our Internet website (http://www.citizensinc.com), our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Section 16 Reports filed by officers and directors, and, if applicable, amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934,

December 31, 2021 | 10-K 1

as soon as reasonably practicable after we electronically file such reports with, or furnish such reports to, the SEC. We are not including any of the information contained on our website as part of, or incorporating it by reference into, this Form 10-K.

December 31, 20212023 | 10-K 21

PART I

Item 1. BUSINESS

OVERVIEW

Citizens, Inc. ("Citizens" or the "Company") is an insurance holding company incorporated in Colorado serving the life insurance needs of individuals in the United States since 1969 and internationally since 1975. Through our domestic insurance subsidiaries, we are licensed to provide insurance benefits to residents in 39 U.S. states and through our international subsidiaries, we provide insurance benefits to residents in 31 U.S. states and more than 70over 75 different countries. We pursue a strategy of offering traditional insurance products in niche markets where we believe we are able to achieve competitive advantages. We had approximately $1.9$1.7 billion of assets and approximately $4.9 billion of direct insurance in force at December 31, 2021 and approximately $4.2 billion of insurance in force. 2023.

We operate in two business segments:

•Life Insurance segment - Internationally, we sell U.S. dollar-denominated ordinary whole life insurance, endowment and endowmentcritical illness policies predominantly sold to non-U.S. residents, located principally in Latin America and the Pacific Rim through independent marketing consultants andRim. Domestically, we sell whole life insurance, sold domestically through independent agents;life insurance with living benefits, critical illness, credit life and disability products throughout the U.S.

•Home Service Insurance segment - We sell final expense life insurance and property insurance policies marketed to middle- and lower-income households, as well as whole life products with higher allowable face values, in Louisiana, Mississippi and Arkansas, and sold through independent agents and through funeral homes.Arkansas.

Our Principal Brands

LIFE INSURANCE SEGMENT

| | | | | |

| Internationally, we conduct our Life Insurance segment business through CICA Life, A.I., a Puerto Rico company ("CICA International"). |

| Domestically, we conduct our Life Insurance segment business through CICA Life Insurance Company of America ("CICA Domestic"). |

HOME SERVICE INSURANCE SEGMENT

| | | | | |

| We conduct our Home Service Insurance segment through Security Plan Life Insurance Company ("SPLIC") and Magnolia Guaranty Life Insurance Company ("Magnolia"). |

As an insurance provider, we collect premiums on an ongoing basis from our policyholders and invest the majority of the premiums to pay future benefits, including claims, surrenders and policyholder dividends. Accordingly, the Company derives its revenues principally from: (1) life insurance premiums earned for insurance coveragecoverages provided to insureds in our policyholders;two operating segments; and (2) net investment income. In addition to paying and reserving for insurance benefits that we pay to our policyholders, our expenses consist primarily of the costs of selling our insurance products (e.g., commissions, underwriting, marketing expenses), operating expenses and income taxes.

Because collection of premiums is the primary source of our revenues, our overall financial performance depends primarily upon the development and distribution of our products. A key to product development is the pricing of our insurance products and the accuracy of our pricing assumptions. The Company seeksWe seek to price our insurance policies such that insurance premiums and future net investment income earned on premiums received will cover the ultimate cost of paying claims on our policies, our expenses and will also yield a profit margin. Pricing adequacy depends on a number of factors, including proper evaluation of underwriting risks, the ability to project future losses based on historical loss experience adjusted for

December 31, 2023 | 10-K 2

known trends, proper evaluation of underwriting risks, the Company’s response to competitors, the ability to obtain regulatory approvalcommission payments for rate changes,selling our products, expectations about interest rates and regulatory andor legal developments, and expense levels.

In order to manage the risks related to pricing, we employ medical underwriting procedures to assess and quantify risks before we issue policies. Insurance applications are reviewed to make two determinations: first, eligibility based on established underwriting guidelines and second, the applicable premium. We periodically review our underwriting requirements and may make changes as needed.

We also seek to manage pricing risk through:

•favorable risk selection and diversification;

•management of claims;

•use of reinsurance;

•careful monitoring of our mortality and morbidity experience; and

•management of our expense ratio.

In addition to insurance premiums, the investment return, or yield, on invested assets is an important element of the Company’s earnings since life insurance products are priced with the assumption that premiums received can be invested for a period of time before benefits are paid. Pursuant to regulatory guidelines, most of the Company’s invested assets are held in available-for-sale ("AFS") fixed maturity securities, primarily in asset classes of corporate bonds, municipal bonds, and government obligation bonds. The interest rate environment has a

December 31, 2021 | 10-K 3

significant impact on the determination of insurance contract liabilities, our investment rates and yields, and our asset/liability management. The profitability of our "spread-based" product features depends largely on the Company’s ability to earn higher returns on invested assets than the interest we credit to policyholders.

The primary investment objective for the Company is to maximize economic value, consistent with acceptable risk parameters, including the management of credit risk and interest rate sensitivity of invested assets, while generating sufficient after-tax income to meet policyholder and corporate obligations. The Company maintains a prudent investment strategy that may vary based on a variety of factors including business needs, regulatory requirements and tax considerations.

IN 2021, WE BECAME A NON-CONTROLLED COMPANY

Throughout most of our history, the Company was led and controlled by our founder Harold E. Riley and his family members. Mr. Riley passed away in 2017 and in 2020, a change-in-control of our Company occurred when the shares held by the Harold E. Riley Trust were transferred to the Harold E. Riley Foundation (the “Foundation”). As a result of this change-in-control:

•On August 5, 2020, Geoffrey Kolander, our Chief Executive Officer and President resigned and Gerald W. Shields, the Vice Chairman of the Board of Directors of the Company, was appointed Interim Chief Executive Officer and President; and

•In February 2021, the Company entered into an agreement with the Foundation to purchase all of the outstanding shares of Class B common stock for a purchase price of $9.1 million (the “B Share Transaction”).

In April 2021, the Company and the Foundation obtained all regulatory approval required to consummate the B Share Transaction. In accordance with Colorado law, the shares of Class B common stock are now classified as authorized, but unissued shares and the Company's Board of Directors (the "Board") has resolved not to vote the shares of Class B common stock as long as they are so classified. Accordingly, since April 2021:

•the Company has only one class of stock outstanding: the Class A common stock, which is registered under the Securities Exchange Act of 1934, as amended, and listed on the New York Stock Exchange (“NYSE”); and

•the Class B Shares do not have any voting rights; and

•the holders of the Class A shares are entitled to elect all of the directors at the Company’s annual meetings; and

•for the first time in over 30 years, we are no longer a “controlled” company as defined under the NYSE rules.

After the consummationcompletion of the B Share Transaction, Mr. Shields, then acting as our Interim Chief Executive Officer, began working with the Board and management to create and implement a new strategy for the Company in order to set a course for long-term profitable growth. In December 2021, the Board announced that effective January 1, 2022, Mr. Shields would become the permanent CEO and President.

After the B Share Transaction and the appointment of Mr. Shields as our permanenta new Chief Executive Officer, we believe the Company believes that it iswas positioned to offer stability to our management team, employees and independent sales force in orderand was able to move forward with ournew business and strategic initiatives, as described below.

STRATEGIC INITIATIVES

As mentionedHistorically, our insurance companies have only issued a few products and had limited distribution channels. Since the change-in-control described above, in 2021, the Company became a non-controlled company for the first time in over 30 years. This change allowed the Board and management to reset and clearly define our priorities to set a course for long-term profitable growth. Our growth strategy consists ofshifted to focusing on first year sales growth improvedthrough introduction of new products and new distribution channels, retaining renewal premiums through policy retention roadmapefforts, focused execution, and financial and expense discipline. We believe these factors will lead to growth and profitability.

We believe that our roadmap execution process is key to achieving sales growth,our strategic goals as it helps us improve sales and service across our three markets (international life, domestic life and home services) by focusingfocus on three specific sales

December 31, 2021 | 10-K 4

levers in each market-market - products, promotions and processes. Specifically, we implemented a five-quarter roadmap that lays out the following:

•Products. We are focusinghave a robust product development process that focuses on our customer needs by offeringdeveloping new products tailored to our specific markets, working with partners to develop products tailored to their markets, and enhancing existing products. New products also help our sales force, as they can sell additional products to existing customers and offer a broader portfolio of products to entice prospective customers. A broader product portfolio also helps attract new distributors. Our management team meets on a monthly basis to ensure we are bringing the right products to market at the right time.

•Promotions. We are focused on implementing sales promotions and campaigns in order to align our sales consultant compensation opportunities with our premium revenue goals and our growth and retention initiatives.

•Processes. We are implementing process improvements and new technologies in order to get products to our customers faster and improve servicesthe experience for both our policyholders and our agents, as well as helpingagents. We also implemented new processes and technologies to help our employees work more effectively and efficiently.

December 31, 2023 | 10-K 3

Status of New and Enhanced Products; Trends in Market Demand

As mentioned above, offering new and enhanced products are key to achieving our strategic goals. In 20212023 we:

•Introduced New Products3 new products in both English and Spanish under our CICA Domestic brand, leading to first year premium revenue growth of 13% in our Home ServiceLife Insurance Segment. Over the past 18 months, our Home Service Insurance business has been a focus of transformation to drive sales growth for the Company. Prior to mid-2020, the focus of this segment was collections, i.e. renewal premiums and our sales force had sold the same life insurance product for over 30 years. In 2021, we introduced a higher face value whole life product in this segment, allowing us to expand our target customer. In December 2021, we launched a critical illness product that offers a true living benefit to policyholders by paying a lump sum amount in the event of a covered critical illness to use at the policyholder's discretion. As we continue to expand our product offerings in this market, we believe that cross-selling opportunities (i.e., selling new products to existing customers and offering more than one product to a new customer) will lead to revenue growth.segment.

Reevaluated expansion of Life Insurance Segment into Hispanic US Market•. Obtained an A.M. Best rating for the first time ever in July 2023.

◦As we previously disclosed, in 2021 we undertook an initiative toCICA Domestic is rated as a B++ with a "Very Strong" balance sheet. We believe this will help us expand our Life Insurance segment todistribution networks and the Hispanic market in the U.S. by bringing our infrastructure to complete insurance transactions end-to-end in Spanish to the Florida market. We launched three products in this market in 2021. While we still believe that there is a need for this typeappeal of product and service in the U.S., our efforts to recruit agents to sell our products have been slower than we expected and we are re-evaluating our sales distribution approach, initiatives and domestic life insurance offerings in the Florida market in 2022.to consumers.

Retention

As policy surrenders have increased in our business overCompleted the last several years, in 2021, we formed a retention steering team in an effort to curb policy surrenders. This team focused on cultivating and executing on ideas that would increase eachmove of our segments' overall retention, while being beneficialinternational business from Bermuda to Puerto Rico, which we believe will drive greater demand for our policyholders. Both our Life Insurance segment and our Home Service Insurance segment improved policy retention in 2021 due to these efforts.international products.

As we seek to optimize value for the Company's shareholders, customers and distributors, we believe our efforts to develop and enhance our products, incentivize our sales force and make process and technology improvements will continue to put the Company on a stronger financial footing and drive sustainable growth.

December 31, 2021 | 10-K 5

LIFE INSURANCE

OurUntil December 31, 2022, our Life Insurance segment primarily operatesoperated through CICA Life Ltd. ("CICA International"Bermuda"), a Bermuda company. Upon surveying the market demands and needs of our policyholders, in 2022 we formed a new subsidiary in Puerto Rico, CICA Life, A.I. ("CICA International"). CICA International received a license in September 2022 to issue business as a Puerto Rico international insurer for the Company’s international portion of its Life Insurance segment. Beginning January 1, 2023, all new international policies are issued by CICA International (CICA Life, A.I.) and on August 31, 2023, CICA Bermuda transferred all of its insurance in force business to CICA International and we voluntarily surrendered our insurance license in Bermuda. Because CICA International provides our non-U.S. policyholders the ability to purchase policies in a U.S. territory and in a jurisdiction where the primary language spoken is Spanish, which is the primary language of the majority of our international policyholders, we believe this change will drive sales and improve policy retention, leading to revenue growth.

INTERNATIONAL LIFE INSURANCE

Sales and Distribution

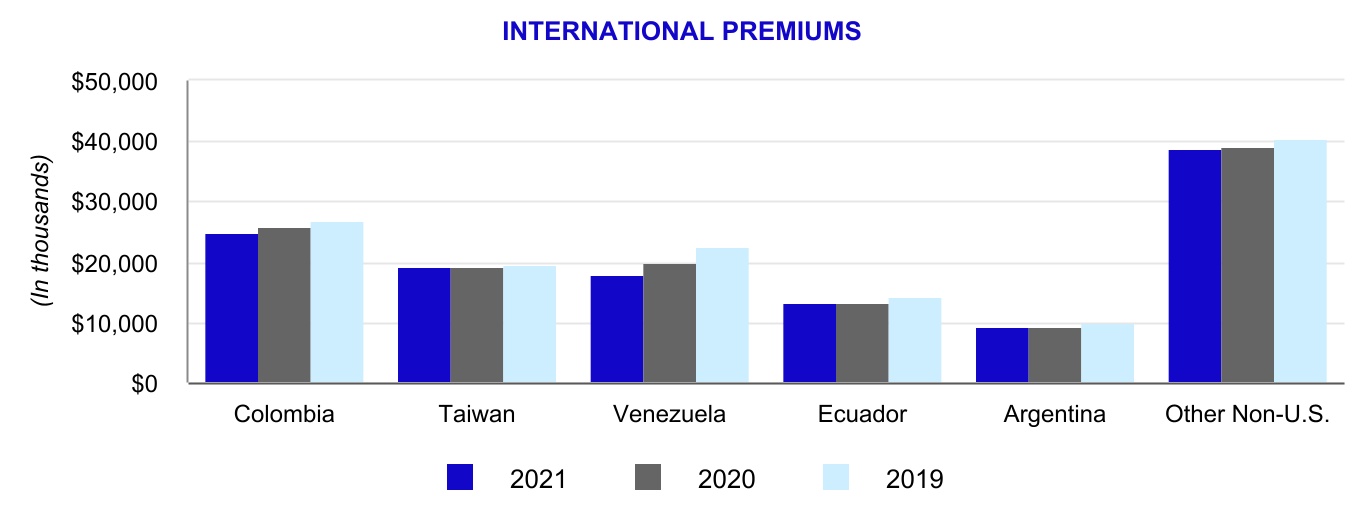

We focus our international sales to residents in Latin America and the Pacific Rim. As of December 31, 2021,2023, we had insurance policies in force in more than 70over 75 foreign countries and receive the majority of our premiums from Colombia, Taiwan, Venezuela, Taiwan, Ecuador and Argentina. International direct premiums comprised approximately 96%97% of total direct premiums in the Life Insurance segment and 68%70% of our total consolidated direct premiums in 2021.2023.

December 31, 2023 | 10-K 4

We believe positive attributes of our international insurance business typically include:

•larger face amount policies issued when compared to our U.S. operations, which results in lowerlow underwriting and administrative costs per dollar of coverage;

•high persistency and low mortality charges due to our customer demographics; and

•premiums paid annually at the beginning of each policy year rather than monthly or quarterly, which reduces our administrative expenses, accelerates cash flow and results in lower policy lapse rates than premium payment options with more frequently scheduled payments.

Our international sales force consists ofWe sell our products internationally through independent marketing agencies and consultants who specialize in marketing life insurance products and generally have several years of insurance marketing experience.products. We enter into sales and service contracts with the independent marketing agencies pursuant to which they recruit, train and supervise their managers and associates in the sales and service of our products. These agencies receive commissions for products they sell and service, as well as commission overrides on the business that their agents produce and, in return for the override, they guarantee any debt their agents owe to us. Their sales agents also contract directly with us as independent consultants and receive commission compensation directly from us. This allows us to develop a relationship with their associates so if an agency contract is terminated for any reason, we may seek to continue the existing independent consultant marketing arrangements with the associates of such agency. Our agreements typically provide that the agencies and their agents are independent consultants responsible for their own operational expenses and are the representative of the prospective insured. Our contracts require the independent marketing agencies and consultants to understand and comply with all laws applicable to sales of our products in their country.

Products

CICA International issues primarily ordinary whole life insurance and endowment products in U.S. dollar-denominated amounts to non-U.S. residents. The whole life insurance products are designed to provide a fixed amount of insurance coverage over the life of the insured and can include rider benefits to provide additional coverage and annuity benefits to enhance accumulations. Our endowment contracts are principally accumulation contracts that incorporate an element of life insurance protection. These products have premium rates that are competitive with most foreign local companies and have been structured to provide the policyowners with:

•U.S. dollar-denominated cash values that accumulate, beginning in the first policy year, throughout a policyholder’s lifetime;

•protection against devaluation of the policyowners' local currency;currency and local hyper-inflation;

•capital investment in a more secure economic environment (i.e., the U.S.); and

•lifetime income guarantees for an insured or for surviving beneficiaries.

Our international products have both living and death benefit features. Most policies contain guaranteed cash values and are participating (i.e., provide for cash dividends as apportioned by CICA International's board of directors). Once a policyowner pays the annual premium and the policy is issued, the owner becomes entitled to policy cash dividends and may elect to receive annual premium benefits. The policyowner has several options with regards to the policy dividends and annual premium benefits, which include, among other things, electing to receive cash, crediting such amounts towards the payment of premiums on the policy, leaving such amounts on deposit with the Company to accumulate at a defined interest rate or assigning them to a third-party. Under the "assigned to a

December 31, 2021 | 10-K 6

third-party" provision, the Company has historically allowed policyowners, after receiving a copy of the Citizens, Inc. Stock Investment Plan (the "CISIP""SIP") prospectus and acknowledging their understanding of the risks of investing in CitizensCitizens' Class A common stock, the right to assign policy values outside of the policy to the CISIP,SIP, which is administered in the United States by Computershare Trust Company, N.A., our third-party plan administrator and an affiliate of Computershare, Inc., our transfer agent. The CISIPSIP is a direct stock purchase plan available to policyowners, shareholders, our employees and directors, independent consultants, and other potential investors through the Computershare website. The Company has registered the shares of Class A common stock issuable to participants under the CISIPSIP on a registration statement under the Securities Act of 1933, as amended, (the "Securities Act") that is on file with the SEC. Computershare administers the CISIPSIP in accordance with the terms and conditions of the CISIP,SIP, which is available on the Computershare website and as part of the Company’s registration statement on file with the SEC.

December 31, 2023 | 10-K 5

Competition

The life insurance business is highly competitive. Internationally, we compete with a number of life insurance companies, as well as with financial institutions that offer insurance products.

We face competition from other insurance companies that operate in the same markets and manner as we do. Additionally, some of our competitors are local companies formed and operated in the country in which an insured resides, and others are companies foreign to the countries in which their products are sold, but issue insurance policies denominated in the local currency of those countries or issue products approved by regulators of those countries. Some of these companies may have a competitive advantage over us due to their greater financial resources, histories of successful operations and brand recognition, local licensing, partnering with local insurance companies and larger marketing forces.

We believe that we have a competitive advantage over some of our competitors because premiums on our international policies are paid in U.S. dollars, cash value is accumulated in U.S. dollars, and we pay claims and benefits in U.S. dollars. We believe this provides security and stability to our insureds, who are generally individuals in the middlemiddle- to upper-middle class in their respective countries with significant net worth and earnings. Therefore, our products protect them from the inflationary risks and economic crises that have been common in many of our top-producing foreign countries.

DOMESTIC LIFE INSURANCE

We operatePrior to July 1, 2023, our domestic life insurance business operated through CICA Life Insurance Company of America ("CICA")Domestic and Citizens National Life Insurance Company ("CNLIC"). CNLIC merged into CICA Domestic on July 1, 2023 in order to streamline and focus our domestic life insurance business in one entity. In 2021,2023, domestic direct life insurance premiums comprised approximately 4%3% of total direct premiums in the Life Insurance segment and 3%2% of our consolidated total direct premiums. The majority of our domestic in force business results from renewal premiums from blocks of business of insurance companies we have acquired over the years. In late 2022, we began our "white label" program to expand our distribution, we began expanding CICA Domestic's state licenses, developing new final expense and CNLIC issued domestic ordinary whole lifeliving benefit products, and endowment life insurance products prior to 2017, and except for ourfiling these new domestic initiative described below, continues to sell primarily credit life and accident and health products in Texas.

In 2021, we undertook an initiative to re-start domestic sales in Florida. We believe that our experience in developing and selling products in Latin America will help us expand into the large Hispanic market in the U.S. However, our efforts to recruit agents to sell our product have been slower than we expected and we are re-evaluating our sales distribution approach, initiatives and domestic offerings in the Florida market in 2022.multiple states.

HOME SERVICE INSURANCE SEGMENT

We operate our domestic Home Service Insurance segment only in the U.S. through our subsidiaries Security Plan Life Insurance Company ("SPLIC"),SPLIC and Magnolia Guaranty Life Insurance Company ("MGLIC") and prior to June 30, 2023, Security Plan Fire Insurance Company ("SPFIC"). SPLIC and MGLIC focus onissues final expense life insurance needs ofand critical illness products to middle- and lower-income markets, primarily in Louisiana, Mississippi and Arkansas. Prior to 2021, all of our Home Service Insurance products issued by SPLIC were soldindividuals, primarily through employee agents who worked on a debit route system. Startinghome service distribution model based in late 2020 and continuing throughout 2021, we have been transforming this segment by converting a large portion of our sales force to independent agents, reducing layers of management and introducing

December 31, 2021 | 10-K 7

new products for the first time in almost 35 years. This transformation led to increased sales and decreased operational expenses in 2021.

Louisiana. Policies issued by MGLICMagnolia are primarily burial policies which are sold and serviced through funeral homes, who are also typically the beneficiaries of the policies.

SPFIC is a limited liability casualty company that

sellsprior to June 30, 2023, sold small face value property insurance policies covering dwelling and contents, primarily in Louisiana.

We ceased operations on June 30, 2023 as explained in more detail in Part II, Item 7, Managements' Discussion and Analysis, Overview section. In 2021, we expanded our product offering to Arkansas in part to mitigate the risk of hurricane-related claims that have impacted our business over the last two years.

In 2021,2023, our Home Service Insurance segment comprised 29%27% of our total consolidated direct premiums.

Products and Competition

Our Home Service Insurance products consist primarily of small face amount ordinary whole life and pre-need policies, which are designed to fund final expenses for the insured (e.g., funeral and burial costs). The average life insurance policy face amount issued in 20212023 was approximately $7,900$12,900 per policy. Due to the lower risk associated with small face amount polices, the underwriting performed on these applications is limited. As part of the Home ServicesService Insurance segment transformation mentioned above, in 2021 we introduced a new product, Security Plan Plus, which has a higher allowed face amount. In December 2021, we also introduced a critical illness product, which pays the insured a lump sum following the diagnosis of an illness covered under the plan. To a much lesser extent, our Home Service Insurance segment sellssold property insurance policies covering dwellings and content.content until it ceased operations on June 30, 2023. We provideprovided $30,000 maximum coverage on any one dwelling and contents policy, while content-only coverage and dwelling-only coverage arewere both limited to $20,000.

We face competition in Louisiana, Mississippi and Arkansas from other companies specializing in final expense insurance as well as from other property & casualty insurance companies.insurance. We seek to compete based upon our emphasis onby delivering exceptional personal service to our customers.customers, enhancing our

December 31, 2023 | 10-K 6

management team and upgrading our agent field force. We intend to continue premium growth within this segment via our new products and increased focusby focusing on direct sales through our independent agents.agent-to-consumer sales.

REINSURANCE

We follow the industry practice of reinsuring a portion of our insurance risks with unaffiliated reinsurers. In a reinsurance transaction, a reinsurer agrees to indemnify another insurer for part or all of its liability under a policy or policies it has issued for an agreed upon premium. We participate in reinsurance activities in order to minimize exposure to significant risks, limit losses, and provide additional capacity for future growth. We enter into various agreements with reinsurers that cover individual risks, group risks or defined blocks of business, primarily on a coinsurance and yearly renewable term excess of loss or catastrophe excess basis.

For the majority of our life insurance business, we generally retain the first $100,000 of risk on any one life and reinsure the remainder of the risk. Therefore, under the terms of the reinsurance agreements, the reinsurers agree to reimburse us for the ceded amount (i.e., the death benefit amount less our retained risk) in the event a claim is paid. Cessions under reinsurance agreements do not discharge our obligations as the primary insurer. In the event reinsurers do not meet their obligations under the terms of the reinsurance agreements, reinsurance recoverable balances could become uncollectible.

For SPFIC, we obtain catastrophic reinsurance in order to minimize the risks related to payments we owe our insureds due to catastrophic events, such as hurricanes. Upon the occurrence of a catastrophic event, we retain (i.e., pay) the first $500,000 in claims, and then the reinsurer pays the next $10.5 million in claims. Upon the occurrence of a catastrophic event, in order to continue receiving reinsurance, we also have to pay reinstatement premiums in order to be covered for another catastrophic event in the same calendar year.

Our amounts recoverable from reinsurers represent receivables from and/or reserves ceded to reinsurers. The amountsamount recoverable from reinsurers were $5.5was $4.0 million as of December 31, 2021.2023.

We focus on obtaining reinsurance from a diverse group of well-established reinsurers. We have restructuredAll of our reinsurance relationships as of January 1, 2021 and reinsure our international business with three different

December 31, 2021 | 10-K 8

reinsurers and our domestic business with two reinsurers.are rated A- (Excellent) or higher by A.M. Best. We regularly evaluate the financial condition of our reinsurers and monitor concentration risk with our reinsurers.

OTHER NON-INSURANCE ENTERPRISES

Other Non-Insurance Enterprises includes the results of our parent company, Citizens, Inc. and our non-insurance subsidiary, Computing Technology, Inc., which entities primarily provide the Company's corporate-support and information technology and corporate-support functions to the insurance operations.

OPERATIONS AND TECHNOLOGY

Most of our operations are based at our corporate headquarters in Austin, Texas. We also conduct operations for our Home Service Insurance segment from our district offices in Louisiana, Arkansas and Mississippi, as well as our service center in Donaldsonville, Louisiana. AtFor the international portion of our Bermuda office, we performLife Insurance segment, operations including underwriting, policy issuance, claims processing, accounting and reporting related to CICA International's policies.certain international policies were conducted in Bermuda until December 31, 2023 and are now conducted in Puerto Rico.

We have a proprietary single, integrated information technology system for our entire Company, which is a centrally-controlled, mainframe-based policy administrative system. Functionssystem ("PAS") that we use for all of our policy administrative systeminsurance companies. Our PAS performs various functions to effectively handle our insurance operations. These functions include policy set-up, administration, billing and collections, commission calculation, valuation, automated data edits, storage backup, image management and other related functions. Each company and block of business we have acquired has been converted onto our administrative system.PAS. The Company is actively engaged in continued modernization of technology to invest and expand into new opportunities. This system has been in place for more than 30 yearsmodernization allows us to bring new products to market rapidly and has been updated on an ongoing basisautomate insurance interactions to enhance user experience. This investment is foundational to the Company's growth strategy as technology has evolved.we pursue new product innovation and provides:

•our customers and agents with portals to be able to access account information 24/7;

•our policyholder service and claims representatives with a customer account-centric view of our policyholders and beneficiaries, reducing customer inquiry response time and claims processing time; and

•business-to-business solutions.

December 31, 2023 | 10-K 7

REGULATION

The insurance industry is heavily regulated and both Citizens and our insurance subsidiaries are subject to regulation and supervision by the U.S. states in which they do business, by U.S. federal laws, and for CICA International, by Bermuda.Puerto Rico.

REGULATION OF OUR INTERNATIONAL REGULATIONBUSINESS

BermudaPuerto Rico

CICA International, our BermudaPuerto Rico domiciled subsidiary, is subject to regulation and supervisionregulated by the Bermuda Monetary Authority (the "BMA"Puerto Rico Office of the Insurance Commissioner (“OIC”) and compliance with all applicable Bermuda laws and insurance statutes and regulations, including but not limitedis licensed pursuant to Bermuda’sthe Puerto Rico Insurance Act of 1978Code (the "Insurance Act"Code").

Although Puerto Rico is a U.S. territory, it has its own tax code and own insurance code, including a provision under its Insurance Code that allows CICA International which is incorporated to conduct long-term business, is registered as a Class E insurer, which is the license class for long-term insurers and reinsurers with total assets of more than $500 million that are not registrable as a single-parent or multi-owner long-term captive insurer or reinsurer. CICA International is not licensed to conduct any business other than life insurance business. The Insurance Act regulates the insurance business of CICA International and provides that no person may conduct any insurance business in or within Bermuda unless registeredbe established as an insurer under the Insurance Act by the BMA."international insurer" and thus export insurance to international markets. We may not insure risks of residents of Puerto Rico with this type of license and we do not issue policies to U.S. risks through CICA International.

The Insurance Act imposes solvency and liquidity standards as well as auditing and reporting requirements and confers on the BMA powers to supervise, investigate and intervene in the affairs of insurance companies. Certain requirements of the Insurance Act include: the filing of annual statutory financial returns; the filing of annual U.S. GAAP financial statements; the filing of an annual capital and solvency return; the delivery of a declaration of compliance; compliance withCode does not specifically set forth minimum enhanced capital requirements; compliance with the BMA’s Insurance Code of Conduct; compliance with minimum solvency margins; limitations on dividends and distributions that CICA International may make to Citizens, its parent company; preparation of an annual Financial Condition Report providing details of measures governing the business operations, corporate governance framework, solvency and financial performance; preparation of an assessment of an insurer's own risk and solvency requirements, referred to as a Commercial Insurer’s Solvency Self-Assessment; the establishment and maintenance of a head and principal office in Bermuda; appointment of an independent auditor; and appointment of an actuary approved by the BMA.

The BMA measures an insurer’s risk and determines appropriate levels of capitalization by using a risk-based capital model called the Bermuda Solvency Capital Requirement (“BSCR”), which CICA International uses to

December 31, 2021 | 10-K 9

calculate its solvency requirements. The BSCR employs a standard mathematical model that correlates the risk underwritten by Bermuda insurers to their capital.

In order to minimize the risk of a shortfall in capital arising from an unexpected adverse deviation or excess risk, the BMA requires Bermuda insurers to maintain available statutory capital and surplus atstandards, but rather requires that an insurer submit a level equalbusiness plan for approval to or in excess of the enhanced capital requirement, which requires a threshold capital level (termed the Target Capital Level ("TCL")), of 120% of a company’s enhanced capital requirement. The TCL serves as an early warning tool for the BMA. In addition to being required to meet the TCL, at the request of the BMA, on April 15, 2021, Citizens and CICA International entered into a “Keep Well Agreement.” The Keep Well Agreement requires Citizens to contribute up to $10 million in capital to CICA International as necessary to ensureOIC that it has aincludes proposed minimum capital level of 120%.

Bermuda law distinguishes between those companies that are at least 60% owned and controlled by Bermudians, which are "local companies", and those which are owned and controlled by non-Bermudians, which are "exempted companies". Exempted companies may be resident in Bermuda and conduct business from Bermuda in connection with transactions and activities which are external to Bermuda or with other exempted companies, and exempted companies must obtain a license to conduct business activities within Bermuda from the Minister of Finance of Bermuda. Generally, it is not permitted without a special license granted by the Minister of Finance of Bermuda to ensure Bermuda domestic risks or risks of persons of, in or based in Bermuda and we do not offer insurance products to residents of Bermuda.

In December 2018, the Economic Substance Act (the "ES Act") came into force. The ES Act, as amended, and the regulations promulgated thereunder (collectively, "ES Law"), apply to any "relevant entity" that conducts any "relevant activity" in a "relevant financial period". Under the ES Law, insurance and holding entities are each defined as a "relevant activity" and thus the ES Act applies to CICA International. Under the provisions of the ES Law, a relevant entity that conducts a relevant activity must satisfy the economic substance requirements under the ES Law (the "ES Requirements") in relation to the relevant activity and where a relevant entity is conducting more than one relevant activity, it must meet the ES Requirements with respect to each relevant activity that it conducts. A relevant entity complies with the ES Requirements if: (a) the relevant entity is managed and directed from Bermuda; (b) the core income-generating activities are undertaken in Bermuda with respect to each relevant activity; (c) the relevant entity maintains an adequate physical presence in Bermuda; (d) there are adequate full-time employees in Bermuda with suitable qualifications; and (e) there is adequate operating expenditure incurred in Bermuda in relation to each relevant activity.

surplus. CICA International is required to demonstratemaintain a minimum of $750,000 in capital and maintain a premium to surplus ratio of 7 to 1. The Insurance Code requires us to file annual U.S. GAAP financial statements with the OIC that include schedules providing information regarding premiums written and reinsurance assumed and ceded, as well as an annual actuarial certification.

In addition to compliance with the ES Requirements by filing an annual economic substance declarationInsurance Code, CICA International must comply with other laws and regulations of Puerto Rico, most of which apply to our domestic subsidiaries as well, including the Registrar of Companies in Bermuda no later than six months after the last dayU.S. Bank Secrecy Act and other anti-money laundering laws and regulations of the relevant financial period. Companies that conduct insurance as a relevant activity are deemed to comply with the ES Requirements, with respect to their insurance business, if they comply with the existing regulatory requirements under the Insurance Act and the corporate governance provisions of the Companies Act 1981. CICA International is in compliance with these requirements as of December 31, 2021.United States.

Other International Regulation

Generally, all foreign countries in which we offer insurance products require a license or other authority to conduct insurance business in that country. Some of these countries also require that local regulatory authorities approve the terms of any insurance product sold to residents of that country. Other than formerly in Bermuda, we have never qualified to do business in any foreign country, or jurisdiction and we have never submitted our international insurance policies for approval byto any foreign or domestic insurance regulatory agency. As described above, we sell our policies to residents of foreign countries through independent marketing agencies and independent consultants located in those countries and we rely on our independent consultants to comply with laws applicable to them in marketing and servicing our insurance products in their respective countries.

We have undertaken a comprehensive compliance review of risks associated with the potential application of foreign laws to our sales of insurance policies in foreign countries. The application of foreign laws to our sales of insurance policies in foreign countries varies by country. There is a lack of uniform regulation, lack of clarity in certain regulations and lack of legal precedent in addressing circumstances similar to ours. Our compliance review has confirmed certain risks related to foreign insurance laws associated with our current business model, at least in certain jurisdictions, as described in detail in Item 1A. Risk Factors.

December 31, 2021 | 10-K 10

U.S. REGULATION

In the United States, insurance is primarily regulated at the state level. Our domestic insurance subsidiariesprimary regulator in the U.S. is the Colorado Division of Insurance, as both Citizens and CICA Domestic are primarilyColorado companies. We are also regulated by the insurance departments of the stateinsurance in which they are domiciled (Colorado, Louisiana Texas(SPLIC and Mississippi). They are also regulated inSPFIC) and Mississippi (Magnolia), as well as each of the 3139 states and the District of Columbia in which we conduct insurance business. In supervising and regulating insurance companies, state insurance departments generally aim to protect policyholders and the public rather than investors, and enjoy broad authority and discretion in applying applicable insurance laws and regulation for that purpose. The extent of this regulation varies, but most U.S. jurisdictions have laws and regulations based upon the National Association of Insurance Commissioners ("NAIC") model rules governing the financial condition of insurers, including standards of solvency, types and concentration of investments, establishment and maintenance of reserves, credit for reinsurance and requirements of capital adequacy,adequacy; and the business conduct of insurers,

December 31, 2023 | 10-K 8

including marketing and sales practices and claims handling. In addition, statutes and regulations usually require the licensing of insurers and their agents, the approval of most types of policy forms and related materials (such as advertising) and the approval of rates for certain types of insurance products.

Risk-basedIn order for insurance regulators to monitor solvency, insurance companies are subject to risk-based capital ("RBC") requirements are imposedrequirements. The RBC requirement is a statutory minimum level of capital that is based on lifetwo factors - (1) the insurance company's size, and property and casualty insurance companies. The NAIC has established minimum capital requirements in(2) the form of RBC. RBC requirements weight the type of business underwritten by an insurance company, the qualityinherent riskiness of its financial assets and various other aspects of an insurance company's businessoperations, i.e. a company must hold capital in proportion to developits risk. The RBC requirement thus determines a minimum level of capital called "authorized control level risk-based capital"required for an insurer to support its operations and compares this levelwrite coverage. The purpose of the RBC requirements is to adjusted statutoryidentify weakly capitalized companies, which facilitates regulatory actions to ensure that the policyholders will receive the benefits promised. Regulators have the legal authority to take preventive and corrective measures depending on the capital that includes capital and surplus as reported under statutory accounting principles, plus certain investment reserves. Shoulddeficiency indicated by the RBC result. If a company's ratio of total adjusted statutory capital to control level risk-based capital fallis above 200%, no regulatory intervention is needed. If it falls below 200%, interventions range from submission of action plans to a seriesregulatory takeover of actions would be required by the affectedmanagement of the company, including submitting a capital planwhich occurs if the ratio is below 70%. We have committed to the departmentColorado Division of insurance in the insurance company's state of domicile.Insurance that we will keep CICA Domestic's RBC ratio at or above 350%.

InsuranceIn addition to monitoring our financial condition, insurance regulatory authorities (including state law enforcement agencies and attorneys general) periodically make inquiries and regularly conduct examinations regarding compliance by us and our subsidiaries with insurance and other laws and regulations regarding the conduct of our insurance businesses. It is our practice to fully and consistently cooperate with such inquiries and examinations and take corrective action when warranted.

In order to sell products in any state, we first have to become licensed in that state. States have various rules for obtaining a license, including capital deposit requirements and seasoning requirements, among others. Once we are licensed in a state, most states require us to file our products for their approval before being able to sell the products. The application and product forms must comply with state insurance laws regarding policy requirements. Once an application or product is approved in that state, we must use the approved forms to sell our products. We have to file our domestic forms in both English and Spanish for separate approvals. We are also subject to laws related to our advertising and may have to file certain marketing documents with state regulators as well.

Because Citizens is a holding company that directly and indirectly owns insurance operating subsidiaries, we are also subject to regulation in our fourthree domiciliary states that require us to furnish the respective insurance regulators with financial and other information concerning the operations of, and the interrelationships and transactions among, the companies within our holding company system that may materially affect the operations, management or financial condition of the insurers within the system. Generally, these laws and regulations require that all transactions within a holding company system between an insurer and its affiliates be fair and reasonable and that the insurer's statutory capital and surplus following any transaction with an affiliate be both reasonable in relation to its outstanding liabilities and adequate to its financial needs. For certain types of agreements and transactions between an insurer and its affiliates, these laws and regulations require prior notification to, and non-disapproval or approval by, the insurance regulatory authority of the insurer's jurisdiction of domicile. These laws also require that a controlling party obtain the approval of the insurance commissioner of the insurance company's jurisdiction of domicile prior to acquiring or divesting control of the insurer.

The payment of dividends or other distributions to Citizens by our insurance subsidiaries is also regulated by the insurance laws and regulations of their respective state or jurisdiction of domicile. The laws and regulations of some of these jurisdictions also prohibit an insurer from declaring or paying a dividend except out of its earned surplus or require the insurer to obtain regulatory approval before it may do so. In addition, insurance regulators may prohibit the payment of ordinary dividends or other payments by our insurance subsidiaries to us (such as a payment under a tax sharing agreement or for employee or other services) if they determine such payment could be adverse to policyholders or insurance contract holders of the subsidiary.

In additionBecause we maintain sensitive data regarding our customers, we are also subject to additional state insurance-specific laws, U.S. laws,regulations in states where we do business, such as data security and state privacy laws.

December 31, 2023 | 10-K 9

While primarily regulated at the USA Patriot Act of 2001, the Foreign Corrupt Practices Act, the Gramm-Leach-Bliley Act of 1999, the International Money Laundering Abatement and Financial Anti-Terrorism Act of 2001, the Sarbanes-Oxley Act of 2002, the Dodd-Frank Wall Street Reform and Consumer Protection Act and the Tax Cuts and Jobs Act, are examples of U.S. laws that affectstate level, our business. We aredomestic business is subject to comprehensive regulations undervarious federal laws and regulations. Some of the primary federal laws include:

•USA Patriot Act and the U.S. Bank Secrecy Act, which require us to institute certain measures to detect and prevent money laundering;

•Foreign Corrupt Practices Act, which makes it unlawful to bribe foreign officials for the purpose of obtaining or retaining business;

•Gramm-Leach-Bliley Act, which requires us to explain our information-sharing practices to our customers and to safeguard sensitive data;

•Securities Act, Securities Exchange Act and Sarbanes-Oxley Act, which establish various requirements for Citizens, as a public company, to comply with, respect to money laundering, as well as federal regulations regarding privacyincluding registration of our Class A common stock, reporting and confidentiality. disclosure requirements, and public company audit and internal control requirements;

Our U.S.-based insurance products and thus our businesses also are affected by U.S. federal, state and local tax laws.

December 31, 2021 | 10-K 11

HUMAN CAPITAL RESOURCES

Composition and Demographics

Our human capital is a critical component to our success. Our employees implement and drive our strategic initiatives and contribute to the success of our products (development, underwriting, pricing adequacy, customer service), promotions and processes. Our employees in our claims department are ultimately tasked with "keeping our promise". Our independent consultants and agents also drive our key goals, as they sell our insurance products and provide local services to our global base of policyholders. We also believe that we derive a great deal of strength from our diverse workforce. Fostering an equitable and inclusive workplace with diverse teams produces more creative solutions, and results in more innovative products and services and is crucial to our efforts to attract, develop and retain key talent.

December 31, 2023 | 10-K 10

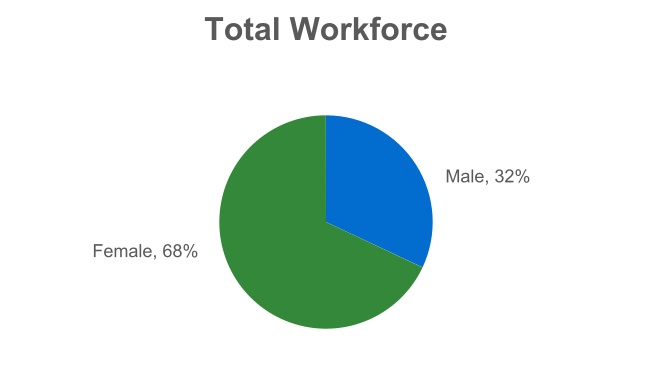

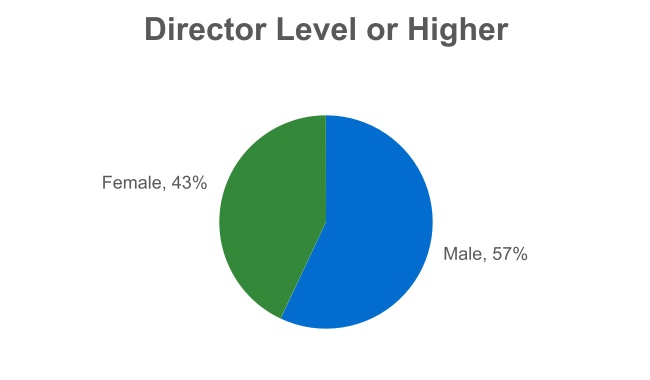

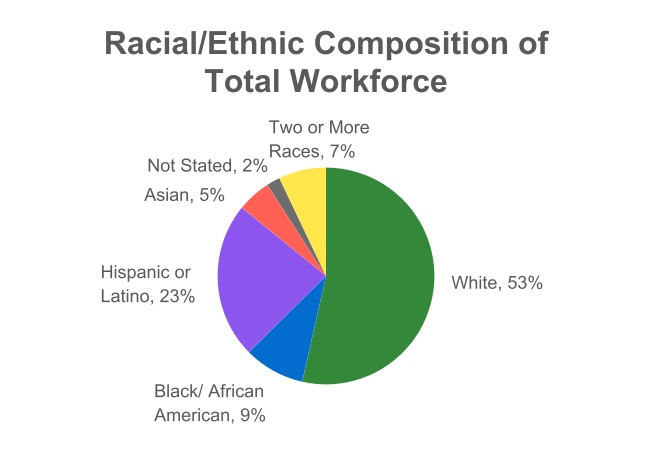

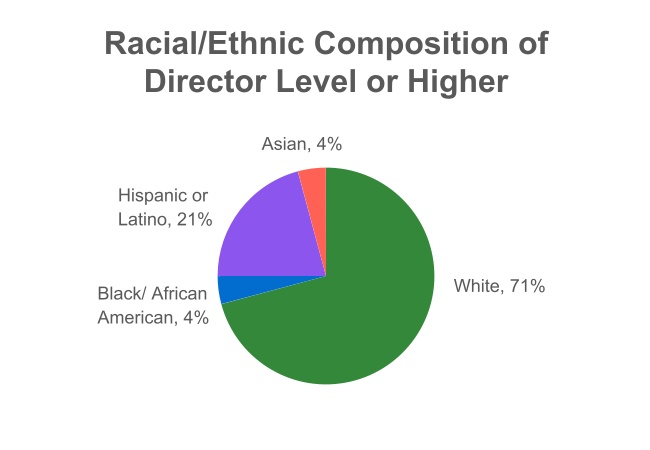

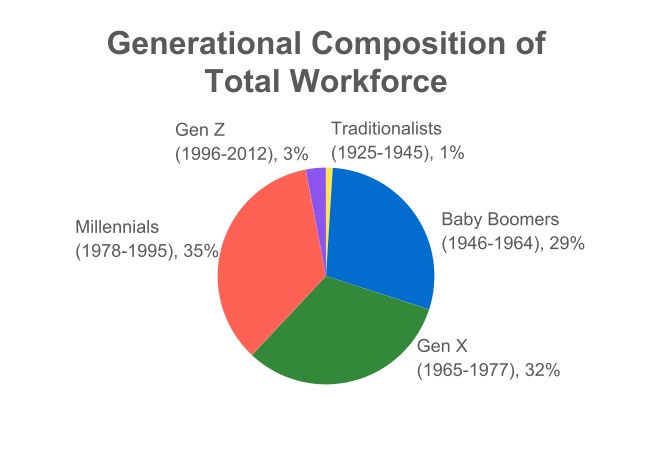

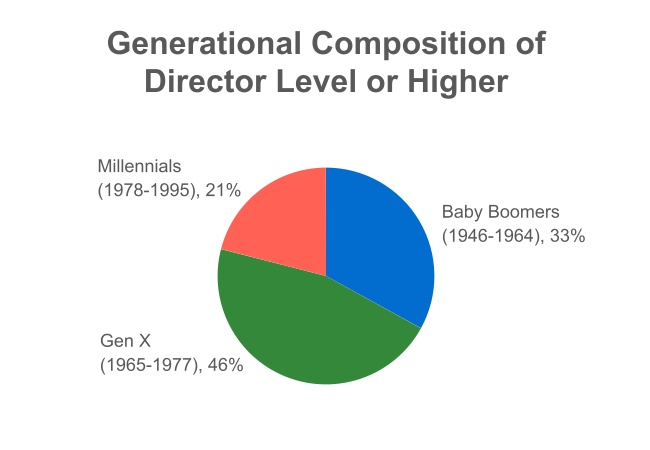

As of December 31, 2021,2023, we had 215232 employees. The pie charts below illustrate the gender, racial, ethnicity, and generational make-up of our total employee workforce as of such date.

Racial/Ethnic Composition

Generational Composition

December 31, 2021 | 10-K 12

We determine race, ethnicity, gender, and generation based on our employees' self-identification or other information compiled to meet requirements of the U.S. government.

None of our employees are subject to a collective bargaining agreement.

We currently do not utilize captive employee agents to distribute our products and thus contract with almostover 1,000 actively producing independent consultants internationally and over 5002,000 independent agencies and agents domestically to sell and service our insurance products. Our international independent agentsconsultants generally reflect the demographics of the areas in which they sell their products, i.e., our agents in Latin America are almost all Hispanic or Latino and our agents in Taiwan are almost all Asian.products.

In order to continue to develop, sell and administer our products, it is crucial that we continue to attract and retain both experienced employees and independent agents.

December 31, 2023 | 10-K 11

CompensationOVERVIEW

Citizens, Inc. ("Citizens" or the "Company") is an insurance holding company incorporated in Colorado serving the life insurance needs of individuals in the United States since 1969 and Benefitsinternationally since 1975. Through our domestic insurance subsidiaries, we are licensed to provide insurance benefits to residents in 39 U.S. states and through our international subsidiaries, we provide insurance benefits to residents in over 75 different countries. We pursue a strategy of offering traditional insurance products in niche markets where we believe we are able to achieve competitive advantages. We had approximately $1.7 billion of assets and approximately $4.9 billion of direct insurance in force at December 31, 2023.

We operate in two business segments:

•Life Insurance - Internationally, we sell U.S. dollar-denominated ordinary whole life insurance, endowment and critical illness policies to non-U.S. residents, located principally in Latin America and the Pacific Rim. Domestically, we sell whole life insurance, life insurance with living benefits, critical illness, credit life and disability products throughout the U.S.

•Home Service Insurance - We sell final expense life insurance policies to middle- and lower-income households, as well as whole life products with higher allowable face values, in Louisiana, Mississippi and Arkansas.

Our compensation program is designedPrincipal Brands

LIFE INSURANCE SEGMENT

| | | | | |

| Internationally, we conduct our Life Insurance segment business through CICA Life, A.I., a Puerto Rico company ("CICA International"). |

| Domestically, we conduct our Life Insurance segment business through CICA Life Insurance Company of America ("CICA Domestic"). |

HOME SERVICE INSURANCE SEGMENT

| | | | | |

| We conduct our Home Service Insurance segment through Security Plan Life Insurance Company ("SPLIC") and Magnolia Guaranty Life Insurance Company ("Magnolia"). |

As an insurance provider, we collect premiums on an ongoing basis from our policyholders and invest the majority of the premiums to attractpay future benefits, including claims, surrenders and retain talented individuals who possesspolicyholder dividends. Accordingly, the skills necessaryCompany derives its revenues principally from: (1) life insurance premiums earned for insurance coverages provided to supportinsureds in our business objectives, assist in the achievement of our strategic goalstwo operating segments; and create long-term value for our stockholders. We provide employees with compensation packages that include base salary and annual performance-based bonus opportunities that include cash, and for our executive officers, long-term equity awards currently in the form of restricted stock units ("RSUs"). We believe that a compensation program with both short-term cash awards and long-term equity awards provides fair and competitive compensation and aligns employee and stockholder interests.(2) net investment income. In addition to cashpaying and equity compensation,reserving for insurance benefits that we also offer standard employee benefits such as lifepay to our policyholders, our expenses consist primarily of the costs of selling our insurance products (e.g., commissions, underwriting, marketing expenses), operating expenses and health (medical, dental & vision) insurance, HSA contributions, paid parental leave, and a 401(k) plan.income taxes.

Independent agents work for themselvesBecause collection of premiums is the primary source of our revenues, our overall financial performance depends primarily upon the development and may selldistribution of our products. A key to product development is the pricing of our insurance products and the accuracy of our pricing assumptions. We seek to price our insurance policies such that insurance premiums and future net investment income earned on premiums received will cover the ultimate cost of paying claims on our policies, our expenses and will also yield a profit margin. Pricing adequacy depends on a number of factors, including the ability to project future losses based on historical loss experience adjusted for

December 31, 2023 | 10-K 2

known trends, proper evaluation of underwriting risks, the Company’s response to competitors, commission payments for selling our products, expectations about interest rates and regulatory or legal developments, and expense levels.

In addition to insurance premiums, the investment return, or yield, on invested assets is an important element of the Company’s earnings since life insurance products are priced with the assumption that premiums received can be invested for a period of time before benefits are paid. Pursuant to regulatory guidelines, most of the Company’s invested assets are held in available-for-sale ("AFS") fixed maturity securities, primarily in asset classes of corporate bonds, municipal bonds, and government obligation bonds. The interest rate environment has a significant impact on the determination of insurance contract liabilities, our investment rates and yields, and our asset/liability management. The profitability of our "spread-based" product features depends largely on the Company’s ability to earn higher returns on invested assets than the interest we credit to policyholders.

The primary investment objective for the Company is to maximize economic value, consistent with acceptable risk parameters, including the management of credit risk and interest rate sensitivity of invested assets, while generating sufficient after-tax income to meet policyholder and corporate obligations. The Company maintains a prudent investment strategy that may vary based on a variety of insurersfactors including business needs, regulatory requirements and make most of their money through sales commissions and bonuses. We attract and retain our independent agent sales force through the use of our commission structure and agent campaigns and promotions. We believe that our standard commission structure is attractive and competitive in the market. In our Life Insurance segment, we believe our campaigns and promotions provide an extra incentive to agents that not only promote first year premium growth, but also create improvements within policyholder retention. In our Home Service Insurance segment, we believe our agent campaigns and promotions are critical in attracting and retaining our independent agent sales force. This business contains a large block of existing in force policies. To ensure we maintain this book of business, the agent campaigns and promotions provide an extra incentive to not only grow the business but to collect on the existing policies. We believe that providing agent campaigns and promotions with additional incentives that provide long-term value creates an advantage for Citizens over our competition.tax considerations.

WellnessIN 2021, WE BECAME A NON-CONTROLLED COMPANY

Throughout most of our history, the Company was led and controlled by our founder Harold E. Riley and his family members. Mr. Riley passed away in 2017 and in 2020, a change-in-control of our Company occurred when the shares held by the Harold E. Riley Trust were transferred to the Harold E. Riley Foundation (the “Foundation”). In February 2021, the Company entered into an agreement with the Foundation to purchase all of the outstanding shares of Class B common stock for a purchase price of $9.1 million (the “B Share Transaction”). After the completion of the B Share Transaction and the appointment of a new Chief Executive Officer, we believe the Company was positioned to offer stability to our management team, employees and independent sales force and was able to move forward with new business and strategic initiatives, as described below.

STRATEGIC INITIATIVES

Historically, our insurance companies have only issued a few products and had limited distribution channels. Since the change-in-control described above, our growth strategy shifted to focusing on first year sales growth through introduction of new products and new distribution channels, retaining renewal premiums through policy retention efforts, focused execution, and financial and expense discipline. We believe these factors will lead to growth and profitability.

We are committedbelieve that our roadmap execution process is key to the healthachieving our strategic goals as it helps us focus on three specific sales levers in each market - products, promotions and safety of our work force and compliance with applicable regulatory and legal requirements. In response to the COVID-19 pandemic, in 2021processes. Specifically, we implemented operating changesa five-quarter roadmap that we determined were inlays out the best interest of the health of our employees, including offering a hybrid work environment where our employees can work part- or full-time from home, depending on their position and circumstances. We also have implemented training programs to assist our independent agents with online sales efforts in order to minimize face-to-face interactions with potential customers and our policyholders.following:

Item 1A.•Products RISK FACTORS. We have a robust product development process that focuses on our customer needs by developing new products tailored to our specific markets, working with partners to develop products tailored to their markets, and enhancing existing products. New products help our sales force, as they can sell additional products to existing customers and offer a broader portfolio of products to entice prospective customers. A broader product portfolio also helps attract new distributors. Our management team meets on a monthly basis to ensure we are bringing the right products to market at the right time.

You should carefully consider•Promotions. We are focused on implementing sales promotions and campaigns in order to align our sales consultant compensation opportunities with our premium revenue goals and our growth and retention initiatives.

December 31, 20212023 | 10-K 133

BecauseStatus of the following factors, as well as other factors affecting the Company’s financial conditionNew and operating results, past financial performance should not be considered to be a reliable indicator of future performance, and investors should not use historical trends to anticipate results or trendsEnhanced Products; Trends in future periods.Market Demand

A SUBSTANTIAL PORTION OF OUR REVENUE IS GENERATED FROM INSURANCE PRODUCTS SOLD OUTSIDE OF THE UNITED STATES. WHILE OUR PRODUCTS ARE PRICED AND PAID FOR IN U.S. DOLLARS, OUR FOREIGN OPERATIONS MAY SUBJECT US TO SEVERAL RISKS.

Our salesAs mentioned above, offering new and enhanced products are key to residents of foreign countries expose us to unknown risks related to foreign regulation, foreign currency and tax laws, and political instability. A significant loss of sales in these foreign markets would have a material adverse effect onachieving our results of operations and financial condition.strategic goals. In 2023 we:

•Introduced 3 new products in both English and Spanish under our CICA Domestic brand, leading to first year premium revenue growth of 13% in our Life Insurance segment.

•Obtained an A.M. Best rating for the first time ever in July 2023.

◦CICA Domestic is rated as a B++ with a "Very Strong" balance sheet. We believe this will help us expand our distribution networks and the appeal of our products to consumers.

•Completed the move of our international business from Bermuda to Puerto Rico, which we believe will drive greater demand for our international products.

As we seek to optimize value for the Company's shareholders, customers and distributors, we believe our efforts to develop and enhance our products, incentivize our sales force and make process and technology improvements will continue to put the Company on a stronger financial footing and drive sustainable growth.

LIFE INSURANCE SEGMENT

Until December 31, 2022, our Life Insurance segment primarily operated through CICA Life Ltd. ("CICA Bermuda"), a Bermuda company. Upon surveying the market demands and needs of our policyholders, in 2022 we formed a new subsidiary in Puerto Rico, CICA Life, A.I. ("CICA International"). CICA International Regulatory Risks.A substantialreceived a license in September 2022 to issue business as a Puerto Rico international insurer for the Company’s international portion of its Life Insurance segment. Beginning January 1, 2023, all new international policies are issued by CICA International (CICA Life, A.I.) and on August 31, 2023, CICA Bermuda transferred all of its insurance in force business to CICA International and we voluntarily surrendered our insurance license in Bermuda. Because CICA International provides our non-U.S. policyholders the ability to purchase policies in a U.S. territory and in a jurisdiction where the primary language spoken is Spanish, which is the primary language of the majority of our direct insurance premiums, approximately 68% at December 31, 2021, are frominternational policyholders, in foreign countries, primarily thosewe believe this change will drive sales and improve policy retention, leading to revenue growth.

INTERNATIONAL LIFE INSURANCE

Sales and Distribution

We focus our international sales to residents in Latin America and the Pacific Rim. As of December 31, 2023, we had insurance policies in force in over 75 foreign countries and receive the majority of our premiums from Colombia, Taiwan, Venezuela, Ecuador and Argentina. International direct premiums comprised approximately 97% of total direct premiums in the Life Insurance segment and 70% of our total consolidated direct premiums in 2023.

December 31, 2023 | 10-K 4

We believe positive attributes of our international insurance business typically include:

•larger face amount policies issued compared to our U.S. operations, which results in low underwriting and administrative costs per dollar of coverage;

•high persistency and low mortality charges due to our customer demographics; and

•premiums paid annually at the beginning of each policy year rather than monthly or quarterly, which reduces our administrative expenses, accelerates cash flow and results in lower policy lapse rates than premium payment options with more frequently scheduled payments.