UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year ended December 31, 201630, 2017

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to _______________

Commission File Number 0-599001-35383

THE EASTERN COMPANY

(Exact name of registrant as specified in its charter)

Connecticut | 06-0330020 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

112 Bridge Street, Naugatuck, Connecticut | 06770 |

| (Address of principal executive offices) | (Zip Code) |

Securities registered pursuant to Section 12(b) of the Act: Common Stock No Par Value The NASDAQ Stock Market LLC

(Title of each class) (Name of each exchange

on which registered)

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [X] No [

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’sregistrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See definitions of “large"large accelerated filer”, “accelerated filer”filer," "accelerated filer," "smaller reporting company," and “smaller reporting company”"emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] | Accelerated filer [X] |

Non-accelerated filer [ ] (Do not check if a smaller reporting company) | Smaller reporting company [ ] |

Emerging growth company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

As of July 2, 2016,1, 2017, the last day of registrant’sregistrant's most recently completed second fiscal quarter, the aggregate market value of the voting stock held by non-affiliates of the registrant was $87,125,916$155,324,724 (based on the closing sales price of the registrant’sregistrant's common stock on the last trading date prior to that date). Shares of the registrant’sregistrant's common stock held by each officer and director and shares held in trust by the pension plans of the Company have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 13, 2017, 6,256,098February 27, 2018, 6,263,245 shares of the registrant’sregistrant's common stock, no par value per share, were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Company's shareholders, which will be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after December 30, 2017.

The Eastern Company

FOR THE FISCAL YEAR ENDED DECEMBER 31, 201630, 2017

TABLE OF CONTENTS

| Page | |||

| 3. | |||

| | |||

| 4. | |||

| | |||

| 14. | |||

3

LITIGATION REFORM ACT OF 1995

This Annual Report on Form 10-K (this "Form 10-K") contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements reflect the Company’sCompany's current expectations regarding its products, its markets and its future financial and operating performance. These statements, however, are subject to risks and uncertainties that may cause the Company’sCompany's actual results in future periods to differ materially from those expected. Such risks and uncertainties include, but are not limited to, unanticipated slowdowns in the Company’sCompany's major markets, changing customer preferences, lack of success of new products, loss of customers, competition, increased raw material prices, problems associated with foreign sourcing of parts and products, worldwide conditions and foreign currency fluctuations that may affect results of operations, and other factors discussed in itemItem 1A of this Annual Report on Form 10-K and, from time to time, in the Company’sCompany's filings with the Securities and Exchange Commission. The Company is not obligatedundertakes no obligation to update, alter, or otherwise revise the aforementionedany forward-looking statements, for thosewhether written or oral, that may be made from time to time, whether as a result of new developments.information, future events, or otherwise.

(a) General Development of Business

The Eastern Company (the “Company”"Company," "Eastern," "we," "us," or "our") was incorporated under the laws of the State of Connecticut in October, 1912, succeeding a co-partnership established in October, 1858.

The business of the Company is the design, manufacture and sale of industrial hardware, security products and metal products from six U.S. operations and seven wholly-owned foreign subsidiaries. Theproducts.

Today, the Company maintains thirteensixteen physical locations.locations across North America and Asia.

RECENT DEVELOPMENTS

On January 13, 2016,April 3, 2017, the Board of DirectorsCompany completed a Securities Purchase Agreement (the "Securities Purchase Agreement") with Velvac Holdings, Inc., a Delaware corporation ("Velvac"), Jeffery R. Porter, W. Greg Bland, John Backovitch, Dave Otto, Bob Otto, Timothy Rintelman, Robert Brester, Dan Mcgrew, Mark Moeller, and Prospect Partners II, L.P. (collectively, the "Sellers"). Pursuant to the Securities Purchase Agreement, the Company acquired 100% of the issued and outstanding stock of Velvac from the Sellers (the "Velvac Acquisition") for $39.5 million and an earnout consideration contingent upon Velvac achieving minimum earnings performance levels and based on sales of Velvac's new proprietary Road-iQ product line (the "Earnout Consideration"). The Velvac Acquisition was financed with a $31 million term loan from People's United Bank, National Association ("People's"), a $5 million draw down on the Company's $10 million revolving credit facility with People's and $3.5 million in cash. In addition, the Company approved amendmentspaid a working capital adjustment of $0.6 million by which working capital exceeded a pre-determined target amount. Please refer to the Certificate of IncorporationCompany's Current Report on Form 8-K filed on April 7, 2017 and the By-Laws of the Company which will eliminate the classification of the Board of Directors in a phased in manner and will provideamendment thereto filed on June 19, 2017 for the election of directors by a majority of the votes cast at the Annual Meeting of Shareholders. The declassification of the Board of Directors and the election of Directors by a majority of the votes cast became effective at the Annual Meeting of Shareholders held on April 27, 2016.further details.

(b) Financial Information about Industry Segments

Financial information about industry segments is included in Note 1110 to the Company’sCompany's financial statements, included atin Item 8 of this Annual Report on Form 10-K.

(c) Narrative Description of Business

The Eastern Company actively manages niche industrial divisions that focus on the design, manufacture and sale of particular products and industrial services and are leaders in their specific market sector. We believe Eastern's divisions operate in industries with long-term macroeconomic growth opportunities, have positive and stable cash flows, face minimal threats of technological or competitive obsolescence, and have strong management teams largely in place.

Eastern focuses on proactive financial and operational management of its divisions in order to increase earnings and increase long-term shareholder value. Among other things, Eastern regularly monitors financial and operational performance, instilling consistent financial discipline and assisting management in their analysis and pursuit of prudent organic growth strategies.

4

Eastern also identifies and works with division management to execute attractive external growth and acquisition opportunities. In addition, Eastern recruits and retains talented managers to operate its divisions.

Eastern continuously reviews acquisitions of businesses that have the potential for significant long-term value creation and periodically evaluates the retention and disposition of its existing divisions and investments. We seek to acquire businesses that produce stable and growing earnings and cash flows. Eastern may pursue acquisitions in industries other than those in which its divisions currently operate if an acquisition presents an attractive opportunity.

The Company operates in three business segments: Industrial Hardware, Security Products and Metal Products.

Industrial Hardware

The Industrial Hardware business segment consists of Eberhard Manufacturing, Eberhard Hardware Manufacturing Ltd., Eastern Industrial Ltd, Velvac, Canadian Commercial Vehicles Corporation, Composite Panel Technologies Eastern Industrial Ltd. and Sesamee Mexicana, S.A. de C.V. The unitsThese divisions design, manufacture and market a diverse product line of custom and standard vehicular and industrial hardware, including passenger restraint and vehicular hardware throughout North America. The segment’s locks, latches, hinges, handles, lightweight composite structuresmirrors, mirror-cameras, light-weight sleeper boxes and related hardwaretruck bodies. These products can be found on tractor-trailer trucks, moving vans, off-road constructionspecialty commercial vehicles, recreational vehicles, fire and farming equipment,rescue vehicles, school buses, military vehicles

and recreational boats. They are also used on pickup trucks, sport utility vehicles and fire and rescueother vehicles. In addition, the segment designs and manufactures a wide selection of fasteners and other closure devices used to secure access doors on various types of industrial equipment such as metal cabinets, machinery housings and electronic instruments. Eastern Industrial expands the range of offerings of thisThe segment to include plastic injection molding.

Security Products

The Security Products business segment made upconsists of Greenwald Industries, Argo EMS (formerly Argo Transdata), Illinois Lock Company/CCL Security Products, World Lock Company Ltd., Dongguan Reeworld Security Products Ltd. and, World Security Industries Ltd., is a leading manufacturerGreenwald Industries ("Greenwald"), and Argo EMS (formerly Argo Transdata). Illinois Lock Company/CCL Security Products designs, manufactures and distributes custom engineered and standard closing and locking systems, including vehicular accessory locks, cabinet locks, cam locks, electric switch locks, tubular key locks and combination padlocks. Some of security products. This segment manufactures electronic and mechanical locking devices, both keyed and keyless, for the computer, electronics, vending and gaming industries. The segment also supplies its products are sold under the names SESAMEE®, PRESTOLOCK® andSEARCHALERT™. These products are sold to the luggage, furniture, laboratoryoriginal equipment manufacturers, distributors, route operators, and commercial laundry industries.locksmiths through in-house salesmen and outside sales representatives. Greenwald manufactures and markets coin acceptors and other coin security products used primarily in the commercial laundry markets, as well as hardware and accessories for the appliance industry. In addition, the segment provides a new level of security for the commercial laundry industry through the use of “smart card” technology. Argo EMS supplies printed circuit boards and other electronic assemblies to Original Equipment Manufacturers (“OEM”) in industries such as measurement systems, semiconductor equipment manufacturing, and industrial controls, medical and military markets.

military products. The Security Products segment continuously seeks new markets where it can offer competitive pricing and provide customers with engineered solutions for theirthat meet manufacturers' security needs.

Metal Products

The Company believes that its Metal Products business segment, based at the Company’sCompany's Frazer & Jones facility, is the largest and most efficient producer of expansion shells for use in supporting the roofs of underground mines. This segment also manufactures specialty malleable and ductile iron castings.

Typical products include mine roof support anchors, couplers for railroad braking systems, support anchoring for construction and couplers/fittings for utility (oil, water and gas) industries. Mine roof support anchors are sold to bolt manufacturers while specialty castings are sold to original equipment manufacturers or machine houses. Frazer & Jones will not be effected by the new metals tariff since all metals are purchased domestically.

General

The Company obtains materials from domestic, Asian affiliated and nonaffiliated sources. Raw materials and outside services were readily available from domestic sources for all of the Company’sCompany's segments during 20162017 and are expected to be readily available in 20172018 and the foreseeable future. The Company also obtains materials from Asian affiliated and nonaffiliated sources. The Company has not experienced any significant problems obtaining material from its Asian sources in 2016 and does not expect any such problems in 2017. In 2014,2017, the Company experienced price increases for many of the raw materials used in producing its products, including: scrap iron, zinc, brass and stainless steel. In 20152016, the Company experienced a price decline for many of these same materials. TheAt this time, the Company expects raw material prices to stabilize and then continue to increase as demand for raw materials increases

5

as the worldglobal economy grows. These raw material cost increases could negatively impact the Company’sCompany's gross margin if raw material prices increase too rapidly for the Company

to recover those cost increases through either price increases to our customers or cost reductions in other areas of the businesses.business.

Patent and trademark protection for the various product lines within the Company is limited, but believed by the Company to be sufficient to protect the Company’sCompany's competitive positions. No business segment is dependent on any patent nor would the loss of any patent have any material adverse effect on the Company's business. Foreign sales and license agreements are not significant.

None of the Company’s businessCompany's division segments are seasonal.

Customers for all business segments are broad-based geographically and by markets, and sales are generally not highly concentrated by customer. One customer of the Metal Products segment, Jennmar Corporation, accounted for 10.5% of the Company’s consolidated sales in 2014. No otherone customer exceeded 10% of total consolidated sales in 2017, 2016 2015 or 2014.2015.

The dollar amount of the backlog of orders received by the Company is believed to be firm as of the fiscal year endended December 31, 2016 is $26,993,000,30, 2017. Such backlogs was $34,991,000 at December 30, 2017, as compared to $27,622,000$26,993,000 at January 2,December 31, 2016. The primary reasons for the decreasechange from 20152016 to 20162017 were the acquisition of Velvac on April 3, 2017 and the timing of orders received from customers.

The Company encounters competition in all of its business segments. The Company has been successful in dealing with this competition by offering high quality diversified products with the flexibility of meeting customer needs on a timely basis. This is accomplished by effectively using internal engineering resources and cost effective manufacturing capabilities, expanding product lines through product development and acquisitions, and maintaining sufficient inventory for fast turnaround of customer orders. Imports from Asia and Latin America with favorable currency exchange rates and low cost labor have created additional competitive pressures.pricing pressure. The Company currently utilizes fourcompetes successfully by offering high quality custom engineered products on a timely basis. To compete, the Company deploys internal engineering resources, maintains cost effective manufacturing capabilities through its wholly-owned Asian subsidiaries, in Asia to help offset offshore competition.expands its product lines through product development and acquisitions, and maintains sufficient inventory for fast turnaround of customer orders.

Research and development expenditures in 20162017 were $1,526,000$3,678,000 and represented less than 1%1.8% of gross revenues. In 2016 and 2015, such expenditures were $1,526,000 and 2014 they were $1,219,000, and $1,080,000, respectively. The research and developments costs are primarily attributable to the Greenwald IndustriesVelvac and Eberhard Manufacturing divisions. GreenwaldVelvac performs ongoing research, in both the mechanical and electronic product lines, whichand in RoadIQ. This research is necessary in orderfor the Company to remain competitive and to continue to provide technologically advanced electronic systems. Eberhard Manufacturing develops new products for the various markets they serveit serves based on changing customer requirements to remain competitive. Other research projects include the development of various latches and rotaries and various transportation and industrial hardware products.

The Company does not anticipate that compliance with federal, state or local environmental laws or regulations is likely to have a material effect on the Company’sCompany's capital expenditures, earnings or competitive position.

The average number of employees in 2017 was 1,189.

The Company's ratio of working capital to sales improved in 2017 to 33.7% from 47.1% in 2016 and 41.6% in 2015. The improvement in working capital was 862.the result of a reduction in inventory in the Metal business segment and partially the result of the Velvac acquisition. Working capital includes cash held in various foreign subsidiaries. With the passage of recent tax legislation cash previously held in foreign countries can be repatriated back to the United States and used for other business needs thus reducing working capital further. Other factors affecting working capital include our average days' sales in accounts receivable, inventory turnover ratio and payment of vendor accounts payable. In some cases, the company must hold extra inventory due to extended lead time in receiving products ordered from our foreign subsidiaries to ensure product is available for our customers. The Company continues to monitor its working capital needs with the goal of reducing our ratio of working capital to sales to 25%.

(d) Financial Information about Geographic Areas

The Company includes six separate operating divisions located within the United States, two wholly-owned Canadian subsidiaries (one located in Tillsonburg, Ontario, Canada, and one in Kelowna, British Columbia, Canada), a wholly-owned Taiwanese subsidiary located in Taipei, Taiwan, a wholly-owned subsidiary located in Hong Kong, two wholly-owned Chinese subsidiaries (one located in Shanghai, China, and one located in Dongguan, China), a wholly-owned subsidiary located in Reynosa, Mexico, and a wholly-owned subsidiary located in Lerma, Mexico.

Individually, the Canadian, Taiwanese, Hong Kong, Chinese and Mexican subsidiaries’ revenuesubsidiaries' revenues and assets are not significant. Substantially all other revenues are derived from customers located in the United States.

6

Financial information about foreign and domestic operations’operations' revenues and identifiable assets is included in Note 1110 to the Company’sCompany's financial statements, included atin Item 8 of this Annual Report on Form 10-K. Information about risks attendant to the Company’sCompany's foreign operations is set forth atin Item 1A of this Annual Report on Form 10-K.

(e) e) Available Information

The Company makes available, free of charge through its Internet website at http://www.easterncompany.com, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission.Commission (the "SEC"). The public may read and

copy any materials that the Company files with the SEC at the SEC’sSEC's Public Reference Room, 100 F Street, N.E., Washington, DC 20549 or by calling the SEC at 1-800-SEC-0330. The Company’sCompany's reports filed with, or furnished to, the SEC are also available on the SEC’sSEC's website at www.sec.gov.

In addition to the other information contained in this Form 10-K and the exhibits hereto and the Company’sCompany's other filings with the SEC, the following risk factors should be considered carefully in evaluating the Company’sCompany's business. The Company’sCompany's business, financial condition or results of operation could be materially adversely affected by any of these risks or additional risks not presently known to the Company, or by risks the Company currently deems immaterialimmaterial. which may also adversely affect its business, financial condition or results of operations, such as: changes in the economy, including changes in inflation, tax rates, interest rates and currency exchange rates; risk associated with possible disruption in the Company’sCompany's operations due to terrorism, cybersecurity threats and other manmade or natural disasters; future regulatory actions, legal issues or environmental matters; loss of, or changes in, executive management; and changes in accounting standards whichthat are adverse to the Company. Also,Additionally, there can be no assurance that the Company has correctly identified and appropriately assessed all factors affecting its business or that information publicly available with respect to these matters is complete and correct.

The Company’sCompany's business is subject to risks associated with conducting business overseas.

International operations could be adversely affected by changes in political and economic conditions, trade protection measures, restrictions on repatriation of earnings, differing intellectual property rights and changes in regulatory requirements that restrict the sales of products or increase costs. Changes in exchange rates between the U.S. dollar and otherforeign currencies could result in increases or decreases in earnings and may adversely affect the value of the Company’sCompany's assets outside the United States. The Company’sCompany's operations are also subject to the effects of international trade agreements and regulations. Although generally theseThese trade agreements have positive effects, they can alsocould impose requirements that adversely affect the Company’sCompany's business, such as, but not limited to, setting quotas on productproducts that may be imported from a particular country into the Company’sCompany's key markets in North America.

The Company’sCompany's ability to import products in a timely and cost-effective manner may also be affected by conditions at ports or issues that otherwise affect transportation and warehousing providers, such as port and shipping capacity, labor disputes, severe weather or increased homeland security requirements in the United States or other countries. These issues could delay importation of products or require the Company to locate alternative ports or warehousing providers to avoid disruption to customers. These alternatives may not be available on short notice or could result in higher transit costs, which could have an adverse impact on the Company’sCompany's business, financial conditions or results of operations.

Indebtedness may affect our business and may restrict our operating flexibility.

As of December, 31, 2017, the Company had $35,225,000 in total consolidated indebtedness. Subject to restrictions contained in our credit facility, the Company may incur additional indebtedness in the future, including indebtedness incurred to finance acquisitions. The level of indebtedness and servicing costs associated with that indebtedness could have important effects on our operation and business strategy. For example, the indebtedness could:

| · | Place the Company at a competitive disadvantage relative to the Company's competitors, some of which have lower debt service obligations and greater financial resources; |

| · | Limit our ability to borrow additional funds; |

7

| · | Limit our ability to complete future acquisitions; |

| · | Limit our ability to pay dividends; |

| · | Limit our ability to make capital expenditures; and |

| · | Increase the Company's vulnerability to general adverse economic and industry conditions. |

The Company's ability to make scheduled principal payments, to pay interest on, or to refinance our indebtedness and to satisfy other debt obligations will depend upon future operating performance, which may be affected by factors beyond the Company's control. In addition, there can be no assurance that future borrowings or the issuance of equity would be available to the Company on favorable terms for the payment or refinancing of the Company's debt. If the Company is unable to service its indebtedness, the business, financial condition and results of operation would be materially adversely affected.

The Company's credit facility contains covenants requiring the Company to achieve certain financial and operations results and maintain compliance with specified financial ratios. The Company's ability to meet the financial covenants or requirements in its credit facility may be affected by events beyond our control, and the Company may not be able to satisfy such covenants and requirements. A breach of these covenants or the Company's inability to comply with the financial ratios, tests or other restrictions contained in our credit facility could result in an event of default under such credit facility. Upon the occurrence of an event of default under our credit facility and/or the expiration of any grace periods, the lenders could elect to declare all amounts outstanding under our credit facility, together with accrued interest, to be immediately due and payable. If this were to occur, the Company's assets may not be sufficient to fully repay the amounts due under our credit facility or the Company's other indebtedness. See also “"ITEM 7A - QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK”" of this Form 10-K.

In addition, the Company’sCompany's growth strategy involves expanding sales of its products into foreign markets. There is no guarantee that the Company’sCompany's products will be accepted by foreign customers or how long it may take to develop sales of the Company’sCompany's products in these foreign markets.

Increases in the price or reduced availability of raw materials.

Raw materials needed to manufacture products are obtained from numerous suppliers. Under normal market conditions, these raw materials are readily available on the open market from a variety of producers. However, from time to time, the prices and availability of these raw materials fluctuate, which could impair the Company’sCompany's ability to procure the required raw materials for its operations or increase the cost of manufacturing its products. If the price of raw materials increases, the Company may be unable to pass these increases on to its customers and could experience reductionreductions to its profit margins. Also, any decrease in the availability of raw materials could impair the Company’sCompany's ability to meet production requirements in a timely manner.

The Company obtains raw materials, including stainless steel used in the production of its products from domestic, Asian affiliated and nonaffiliated sources. The President of the United States recently announced a proposal to impose tariffs of 25 percent on imported steel and 10 percent on imported aluminum through the issuance of an executive order. If implemented, such tariffs may cause an increase in costs for all domestic entities, including the Company, that purchase imported steel or aluminum. Because steel are raw materials used in a wide-range of the Company's products, a broad-based cost increase would result in an increase in the Company's cost of goods sold, which may require us to increase prices for some of our products. However, our inability to pass along such price increases to our customers, or an inability of our suppliers to meet our raw material requirements, may have a material adverse impact on our business, results of operations or financial condition.

Changes in competition in the markets that the Company services could impact revenues and earnings.

Any change in competition may result in lost market share or reduced prices, which could result in reduced profitprofits and margins. This may impair the ability to grow or even maintain current levels of revenues and earnings. While the Company has an extensive

customer base, loss of certain customers could adversely affect the Company’sCompany's business, financial condition or results of operations until such business is replaced, and no assurances can be made that the Company would be able to regain or replace any lost customers.

8

The Company is required to evaluate its internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act of 2002.

The Company is an “accelerated filer”"accelerated filer" as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, and is thus required to comply with Section 404 of the Sarbanes-Oxley Act of 2002. Section 404 requires the Company to include in its report management’smanagement's assessment of the effectiveness of the Company’sCompany's internal control over financial reporting as of the end of the fiscal period for which the Company is filing its Annual Report on Form 10-K. This report must also include disclosure of any material weaknesses in internal control over financial reporting that the Company has identified. Additionally, the Company’sCompany's independent registered public accounting firm is required to issue a report on the Company’sCompany's internal control over financial reporting and their evaluation of the operating effectiveness of the Company’sCompany's internal control over financial reporting. The Company’sCompany's assessment requires it to make subjective judgments, and the independent registered public accounting firm may not agree with the Company’sCompany's assessment. If the Company or its independent registered public accounting firm were unable to complete the assessments within the period prescribed by Section 404 and thus be unable to conclude that the internal control over financial reporting is effective, investors could lose confidence in the Company’sCompany's reported financial information, which could have an adverse effect on the market price of the Company’sCompany's common stock or impact the Company’sCompany's borrowing ability. In addition, changes in operating conditions and changes in compliance with policies and procedures currently in place may result in inadequate internal control over financial reporting in the future.

The inability to identify or complete acquisitionsdevelop new products could limit future growth.

Demand for new products and the inability to develop and introduce new competitive products at favorable profit margins could adversely affect the Company’sCompany's performance and prospects for future growth, and the Company would not be positioned to maintain current levels of revenues and earnings.

The uncertainties associated with developing and introducing new products, such as the market demands and the costs of development and production, may impede the successful development and introduction of new products. Acceptance of the new products may not meet sales expectations due to several factors, such as the Company’s failureCompany's potential inability to accurately predict market demand or its inability to resolve technical issues in a timely and cost-effectivecost effective manner. Additionally, the inability to develop new products on a timely basis could result in the loss of business to competitors.

The inability to identify or complete acquisitions could limit growth.

The Company's future growth may partly depend on its ability to acquire and successfully integrate new businesses. The Company intends to seek additional acquisition opportunities, both to expend into new markets and to enhance the Company's position in existing markets. However, there can be no assurances that the Company will be able to successfully identify suitable candidates, negotiate appropriate terms, obtain financing on acceptable terms, complete proposed acquisitions, successfully integrate acquired businesses or expand into new markets. Once acquired, operations may not achieve anticipated levels of revenues or profitability.

Acquisitions involve risk, including difficulties in the integration of the operations, technologies, services and products of the acquired companies and the diversion of management's attention from other business concerns. Although the Company's management will endeavor to evaluate the risks inherent in any particular transaction, there can be no assurances that the Company's management will properly ascertain all such risks. In addition, prior acquisitions have resulted, and future acquisitions could result in the incurrence of substantial debt and other expenses. Future acquisitions may also result in potentially dilutive issuances of equity securities. Difficulties encountered with acquisitions may have a material adverse effect on our business, financial condition and results of operations.

Environmental compliance costs and liabilities could increase the Company's expenses and adversely affect the Company's financial condition.

The Company's operations and properties are subject to laws and regulations relating to environmental protection, including air emissions, water discharges, waste management and workplace safety. These laws and regulations can result in the imposition of substantial fines and sanctions for violations and could require the installation of pollution control equipment or operational changes to limit pollution emissions and/or decrease the likelihood of accidental hazardous substance releases. The Company must conform its operations and properties to these laws and adapt to regulatory requirements in the countries in which the Company's divisions operate as these requirements change.

9

The Company uses and generates hazardous substances and wastes in its operations and, as a result, could be subject to potentially material liabilities relating to the investigation and clean-up of contaminated properties and to claims alleging personal injury. The Company has experienced, and expects to continue to experience, costs relating to compliance with environmental laws and regulations. In connection with the Company's acquisitions, the Company may assume significant environmental liabilities, some of which it may not be aware of at the time of acquisition. In addition, new laws and regulations, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements could require the Company to incur costs or become the basis for new or increased liabilities that could have a material adverse effect on our business, financial condition and results of operations.

Our technology is important to the Company's success and the failure to protect this technology could put the Company at a competitive disadvantage.

Some of the Company's products rely on proprietary technology; therefore, the Company believes that the development and protection of intellectual property rights through patents, copyrights, trade secrets, trademarks, confidentiality agreements and other contractual provisions are important to the future success of its business. Despite the Company's efforts to protect proprietary rights, unauthorized parties or competitors may copy or otherwise obtain and use the Company's products or technology. Actions to enforce these rights may result in substantial costs and diversion of resources and the Company make no assurances that any such actions will be successful.

The Company relies on information and technology for many of its business operations, which could fail and cause disruption to the Company's business operations.

The Company's business operations are dependent upon information technology networks and systems to securely transmit, process and store electronic information and to communicate among its locations around the world and with clients and vendors. A shut-down of, or inability to access, one or more of the Company's facilities, a power outage or a failure of one or more of the Company's information technology, telecommunications or other systems could significantly impair the Company's ability to perform such functions on a timely basis. Computer viruses, cyberattacks, other external hazards and human error could result in the misappropriation of assets or sensitive information, corruption of data or operational disruption. If sustained or repeated, such a business interruption, system failure, service denial or data loss and damage could result in a deterioration of the Company's ability to write and process orders, provide customer service or perform other necessary business functions.

A breach in the security of the Company's software could harm its reputation, result in a loss of current and potential customers and subject the Company to material claims, which could materially harm our operating results and financial condition.

If the Company's security measures are breached, an unauthorized party may obtain access to the Company's data or users' or customers' data. In addition, cyber-attacks and similar acts could lead to interruptions and delays in customer processing or a loss or breach of a customer's data. Because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and often are not recognized until launched against a target, the Company may be unable to anticipate these techniques or to implement adequate preventative measures. The risk that these types of events could seriously harm the Company's business is likely to increase as the Company expands the number of web-based products we offer, the services we provide, and our global operations.

Regulatory authorities around the world are considering a number of legislative and regulatory proposals concerning data protection. In addition, the interpretation and application of consumer and data protection laws in the United States and elsewhere are often uncertain and in flux. It is possible that these laws may be interpreted and applied in a manner that is inconsistent with the Company's data practices. If so, in addition to the possibility of fines, this could result in an order requiring that the Company change its data practices, which could have an adverse effect on its business and results of operations.

Any security breaches for which the Company is, or is perceived to be, responsible, in whole or in part, could subject us to legal claims or legal proceedings, including regulatory investigations, which could harm the Company's reputation and result in significant litigation costs and damage awards or settlement amounts. Any imposition of liability, particularly liability that is not covered by insurance or is in excess of insurance coverage, could materially harm our operating results and financial condition. Security breaches also could cause the Company to lose current and potential customers, which could have an adverse effect on

10

our business. Moreover, the Company might be required to expend significant financial and other resources to further protect against security breaches or to rectify problems caused by any security breach.

The Company could be subject to litigation, which could have a material impact on the Company’sCompany's business, financial condition or results of operations.

From time to time, the Company’sCompany's operations are parties to or targets of lawsuits, claims, investigations and proceedings, including product liability, personal injury, patent and intellectual property, commercial, contract, and environmental and employment matters, which are defended and settled in the ordinary course of business. While the Company is unable to predict the outcome of any of these matters, it does not believe, based upon currently available information, that the resolution of any pending matter will have a material adverse effect on its business, financial condition or results of operations. See “ITEM"ITEM 3 – LEGAL PROCEEDINGS”PROCEEDINGS" in this Form 10-K for a discussion of current litigation.

The Company could be subject to additional tax liabilities.

The Company is subject to income tax laws inof the United States, its states and municipalities and those of other foreign jurisdictions in which the Company has business operations. These laws are complex and subject to interpretations by the taxpayer and the relevant governmental taxing authorities. Significant judgment and interpretation is required in determining the Company’sCompany's worldwide provision for income taxes. In the ordinary course of business, transactions arise where the ultimate tax determination is uncertain. Although the Company believes itsthat our tax estimates are reasonable, the final outcome of tax audits and any related litigation could be materially different from that which is reflected in historical income tax provisions and accruals. Based on the status of a given tax audit or related litigation, a material effect on the Company’sCompany's income tax provision or net income may result during the period or periods from the initial recognition of a particular matter in the Company’sCompany's reported financial results to the final closure of that tax audit or settlement of related litigation when the ultimate tax and related cash flow is known with certainty.

The Company’sCompany's goodwill or indefinite-lived intangible assets may become impaired, which could require a significant charge to earnings to be recognized.

Under accounting principles generally accepted in the United States, goodwill and indefinite-lived intangible assets are not amortized but are reviewed for impairment at least annually. Future operating results used in the assumptions, such as sales or profit forecasts, may not materialize, and the Company could be required to record a significant charge to earnings in the financial statements during the period in which any impairment is determined, resulting in an unfavorable impact on our results of operations. Numerous assumptions are used in the evaluation of impairment, and there is no guarantee that the Company’sCompany's independent registered public accounting firm would reach the same conclusion as the Company or an independent valuation firm, which could result in a disagreement between management and the Company's independent registered public accounting firm.

The Company may need additional capital in the future, and itwhich may not be available on acceptable terms, if at all.

From time-to-time, the Company has historically relied on outside financing to fund expanded operations, capital expenditure programs and acquisitions. The Company may require additional capital in the future to fund operations or strategic opportunities. The Company cannot be assured that additional financing will be available on favorable terms, or at all. In addition, the terms of available financing may place limits on the Company’sCompany's financial and operating flexibility. If the Company is unable to obtain sufficient capital in the future, the Company may not be able to expand or acquire complementary businesses and may not be able to continue to develop new products or otherwise respond to changing business conditions or competitive pressures.

The Company’sCompany's stock price may become highly volatile due to low float, which is the number of shares of the Company’s common stock that are outstanding and available for trading by the public.volatile.

The Company’sCompany's stock price may change dramatically when buyers seeking to purchase shares of the Company’sCompany's common stock exceed the shares available on the market, or when there are no buyers to purchase shares of the Company’sCompany's common stock when shareholders are trying to sell their shares.

11

The Company may not be able to reach acceptable terms for contracts negotiated with its labor unions and be subject to work stoppages or disruption of production.

During 2017,2018, union contracts covering approximately 14%9% of the Company's total workforce of the Company will expire. The Company has been successful in negotiating new contracts over the years, but cannot guarantee that will continue. Failure to negotiate new union contracts could result in the disruption of production, inability to deliver product or a number of unforeseen circumstances, any of which could have an unfavorable material impact on the Company’sCompany's results of operations or financial statements.condition.

Deterioration in the creditworthiness of several major customers could have a material impact on the Company’sCompany's business, financial condition or results of operations.

Included as a significant asset on the Company’sCompany's balance sheet are accounts receivable from our customers. If several large customers become insolvent or are otherwise unable to pay for products, or become unwilling or unable to make payments in a timely manner, it could have an unfavorable material impact on the Company’sCompany's results of operations or financial statements.condition.

Although the Company is not dependent on any one customer, deterioration in several large customers at the same time could have an unfavorable material impact on the Company’sCompany's results of operations or financial statements.condition. No customersone customer exceeded 10% of total accounts receivable for 2017, 2016 2015 or 2014.2015.

The Company’sCompany's operating results may fluctuate, which makes the results of operations difficult to predict and could cause the results to fall short of expectations.

The Company’sCompany's operating results may fluctuate as a result of a number of factors, many of which are outside of our control. As a result, comparing the Company’sCompany's operating results on a period-to-period basis may not be meaningful, and past results should not be relied upon as an indication of future performance. Quarterly, year to date and annual costs and expenses as a percentage of revenuerevenues may differ significantly from historical or projected rates.levels. Future operating results may fall below expectations. These types of events could cause the price of the Company’sCompany's stock to fall.

New or existing U.S. or foreign laws could subject the Company to claims or otherwise impact the Company’sCompany's business, financial condition or results of operations.

The Company is subject to a variety of laws in both the U.S. and foreign countries that are costly to comply with, can result in negative publicity and diversion of management time and effort and can subject the Company to claims or other remedies.

None.

The corporate office of the Company is located in Naugatuck, Connecticut in a two-story, 8,000 square foot administrative building on 3.2 acres of land.

All of the Company’sCompany's properties are owned or leased and are adequate to satisfy current requirements. All of the Company’sCompany's properties have the necessary flexibility to cover any long-term expansion requirements.

The Industrial Hardware Group includes the following:

The Eberhard Manufacturing Division in Strongsville, Ohio owns 9.6 acres of land and a building containing 157,580 square feet, located in an industrial park. The building is steel frame, is one-story havingand has curtain walls of brick, glass and insulated steel panel.panels. The building has two high bays, one of which houses two units of automated warehousing.

12

Eberhard Hardware Manufacturing, Ltd., a wholly-owned Canadian subsidiary in Tillsonburg, Ontario, owns 4.4 acres of land and a building containing 31,000 square feet in an industrial park. The building is steel frame, is one-story, havingand has curtain walls of brick, glass and insulated steel panel.panels. It is particularly suited for light fabrication, assembly and warehousing and is adequate for long-term expansion requirements.

The Composite Panel Technologies Division (“CPT”("CPT") in Salisbury, North Carolina, leases 70,000 square feet of building space located in an industrial park. The building is made from brick and concrete, contains approximately 6,600 square feet of office space on one level and houses a modern paint booth for finishing our products. The building is protected by a water sprinkler fire suppression system and is alarmed for fire and security. The current lease expires on October 31, 2019 and is renewable.

The Sesamee Mexicana subsidiary leases 42,588 square feet in a facility located in an industrial park in Lerma, Mexico. The current lease expires on November 30, 2020 and is renewable. The building is steel framedframe with concrete block and glass curtain walls.

Velvac, Inc., a wholly-owned subsidiary in New Berlin, Wisconsin, leases a 98,000 square foot building. The building includes 17,000 square feet of office space and 81,000 square feet of warehousing and distribution operations. The current lease expires on May 31, 2021.

Velvac de Reynosa, S. De R.L De C.V., a maquiladora wholly-owned in Reynosa, Tamaulipas, Mexico, leases 90,000 square feet of building space located in an industrial park identified as Buildings 19, 20 and 21 and on a tract of land with an area of 165,507 square feet. The building is one level and is made from brick and concrete. The building is protected by a 24 hour security system and onsite security. The current lease expires on August 31, 2021.

Velvac, Inc. also leases a 9,300 square foot building in Bellingham, Washington. The premises are used solely for software development and research and development. The current lease expires on September 30, 2021.

The Security Products Group includes the following:

The Greenwald Industries Division in Chester, Connecticut owns 26 acres of land and a building containing 120,000 square feet. The building is steel frame, one story, havingis one-story, and has brick over concrete blocks.

The Illinois Lock Company/CCL Security Products Division owns 2.5 acres of land and a building containing 44,000 square feet in Wheeling, Illinois. The building is brick and is located in an industrial park.

The Argo EMS Division leases approximately 17,000 square feet of space in a building located in an industrial park in Clinton, CT.Connecticut. The building is a two-story steel framedframe structure and is situated on 2.9 acres of land. The current lease expires on March 31, 2019.

The World Lock Co. Ltd. subsidiary leases 5,285 square feet of space in a building located in Taipei, Taiwan. The building is made from brick and concrete and is protected by a fire alarm and sprinklers. A two-year lease was signed in 2016, which expires on July 31, 2018 and is renewable.

13

The Dongguan Reeworld Security Products Company Ltd. subsidiary was established in July 2013 to manufacture locks and hardware and leases 118,000 square feet of space in concrete buildings that are located in an industrial park located in Dongguan, China. A five-year lease was signed in 2013, which expires on June 30, 2018 and is renewable.

The Metal Products Group consists of:

The Frazer and Jones Division in Solvay, New York owns 17.9 acres of land and buildings containing 205,000 square feet constructed for foundry use. These facilities are well adapted to handle the division’sdivision's current and future casting requirements.

All owned properties are free and clear of any encumbrances.

In 2010, the Company was contacted by the State of Illinois regarding potential ground contamination at ourits plant in Wheeling, Illinois. The Company signed up withentered into a voluntary remediation program in Illinois and has engaged an environmental clean-up company to perform testing and develop a remediation plan. Since 2010, the environmental company has completed a number of tests and the design of a final remediation system designis currently being reviewed and is expected to be approved in Fiscal 2017. the first quarter of 2018. The total estimated cost for the proposed remediation system is anticipated to be approximately $50,000.

In Fiscal 2016, the Company had expensescreated a plan to remediate a landfill of $10,738 relatedspent foundry sand maintained at the Company's Metal Casting facility in New York. This plan was presented to this issue. Finalthe New York Department of Environmental Conservation (the "DEC") for approval in the first quarter of 2018. The Company is in final negotiations with the DEC, and, based on estimates provided by the Company's environmental engineers, the anticipated cost to remediate have not been determined at this time.and monitor the landfill is $380,000. The Company accrued for and expensed such estimated cost in the second and third quarters of 2017.

There are no other legal proceedings, other than ordinary routine litigation incidental to the Company’sCompany's business, to which either the Company or any of its subsidiaries is a party or toof which any property of their propertythe Company or any subsidiary is the subject.

Not applicable.

14

| ITEM 5 | MARKET FOR |

The Company’sCompany's common stock is tradedquoted on the NASDAQ (tickerGlobal Market under the symbol EML)"EML". The approximate number of record holders of the Company common stock on December 31, 201630, 2017 was 369.354.

The following table sets forth the high and low per share sales priceprices of the Company’sCompany's common stock, and the per share annualquarterly dividend declared on the Company’sCompany's common stock, for each quarter of the pastimmediately preceding two years.years as reported on the NASDAQ Global Market.

| 2016 | 2015 | 2017 | 2016 | ||||||||||||||||||||||||||||||

| Market Price | Market Price | Market Price | Market Price | ||||||||||||||||||||||||||||||

| Quarter | High | Low | Dividend | Quarter | High | Low | Dividend | High | Low | Dividend | Quarter | High | Low | Dividend | |||||||||||||||||||

| First | $19.04 | $15.01 | $.11 | First | $20.67 | $16.75 | $.11 | $ | 21.50 | $ | 18.85 | $ | 0.11 | First | $ | 19.04 | $ | 15.01 | $ | 0.11 | |||||||||||||

| Second | 17.21 | 15.74 | .11 | Second | 20.66 | 18.10 | .11 | 31.50 | 21.06 | 0.11 | Second | 17.21 | 15.74 | 0.11 | |||||||||||||||||||

| Third | 20.12 | 16.39 | .11 | Third | 18.74 | 15.75 | .12 # | 31.15 | 24.35 | 0.11 | Third | 20.12 | 16.39 | 0.11 | |||||||||||||||||||

| Fourth | 21.50 | 18.90 | .11 | Fourth | 19.27 | 15.82 | .11 | 30.85 | 25.10 | 0.11 | Fourth | 21.50 | 18.90 | 0.11 | |||||||||||||||||||

The Company expects to continue its policy of paying regular cash dividends, although there iscan be no assurance as to future dividends because they are dependent on future earnings, capital requirements and financial conditions.condition. The payment of dividends is subject to the restrictions of the Company’sCompany's loan agreement if such payment would result in an event of default. See Item 7 – Management’sManagement's Discussion and Analysis of Financial Condition and Results of Operations, and Note 5 to the Company’sCompany's financial statements included atin Item 8 of this Annual Report on Form 10-K.

The following table sets forth information regarding securities authorized for issuance under the Company’sCompany's equity compensation plans as of December 31, 2016,30, 2017, consisting of the Company’sCompany's 2010 plan.Executive Stock Incentive Plan (the "2010 Plan").

| Equity Compensation Plan Information | ||||||||||||

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | |||||||||

| (a) | (b) | (c) | ||||||||||

| Equity compensation plans approved by security holders | 56,330 | 20.36 | 333,500 | 1 | ||||||||

| Equity compensation plans not approved by security holders | - | - | - | |||||||||

| Total | 56,330 | 20.36 | 333,500 | |||||||||

1 Includes shares available for future issuance under the 2010 plan.Plan.

Each director who is not an employee of the Company (“("Outside Director”Director") is paid a director’sdirector's fee for his services at the annual rate of $30,000. Effective August 1, 2017, the chairman of the board will receive an annual fee of $60,000 for his services and all chairs of the varying committees will receive additional compensation. All annual fees paid to non-employee members of the Board of Directors of the Company are paid in common stock of the Company or cash, in accordance with the Directors Fee Program adopted by the shareholders on March 26, 1997 and amended on January 5, 2004. The directors make an annual election, within a reasonable time before their first quarterly payment, to receive their fees in the form of cash, stock or a combination thereof. The election remains in force for one year.

15

During fiscal years 2017, 2016 2015 or 2014,2015, there were no sales by the Company of its securities of the registrant sold whichthat were not registered under the Securities Act.

Act of 1933, as amended (the "Securities Act").

The Company doesdid not have any share repurchase plans or programs.programs in effect during fiscal year 2017.

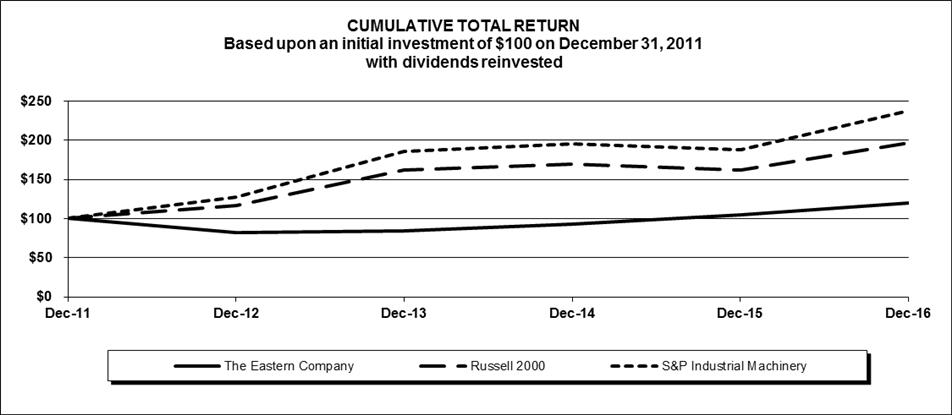

Stock Performance Graph

The following graph sets forth the Company’sCompany's cumulative total shareholder return based upon an initial $100 investment made on December 31, 20112012 (i.e., stock appreciation plus dividends during the past five fiscal years) compared to the Russell 2000 Index and the S&P Industrial Machinery Index.

The Company manufactures and markets a broad range of locks, latches, fasteners and other security hardware that meets the diverse security and safety needs of industrial and commercial customers. Consequently, while the S&P Industrial Machinery Index being used for comparison is the standard index most closely related to the Company, it does not completely represent the Company’sCompany's products or market applications. The Russell 2000 is a small cap market index of the smallest 2,000 stocks in the Russell 3000 Index.

| Dec. 12 | Dec. 13 | Dec. 14 | Dec. 15 | Dec. 16 | Dec. 17 | |||||||||||||||||||

| The Eastern Company | $ | 100 | $ | 103 | $ | 114 | $ | 129 | $ | 147 | $ | 187 | ||||||||||||

| Russell 2000 | $ | 100 | $ | 139 | $ | 146 | $ | 139 | $ | 169 | $ | 194 | ||||||||||||

| S&P Industrial Machinery | $ | 100 | $ | 146 | $ | 153 | $ | 147 | $ | 187 | $ | 249 | ||||||||||||

| Copyright© 2018 Standard & Poor's, a division of S&P Global. All rights reserved. | ||||||||||||||||||||||||

| Copyright© 2018 Russell Investment Group. All rights reserved. | ||||||||||||||||||||||||

| Dec. 11 | Dec. 12 | Dec. 13 | Dec. 14 | Dec. 15 | Dec. 16 | |

| The Eastern Company | $100 | $82 | $84 | $93 | $105 | $120 |

| Russell 2000 | $100 | $116 | $162 | $169 | $162 | $196 |

| S&P Industrial Machinery | $100 | $127 | $186 | $195 | $188 | $238 |

| Copyright© 2017 Standard & Poor's, a division of S&P Global. All rights reserved. | ||||||

| Copyright© 2017 Russell Investment Group. All rights reserved. | ||||||

16

| 2016 | 2015 | 2014 | 2013 | 2012 | 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||||||||||

| INCOME STATEMENT ITEMS (in thousands) | INCOME STATEMENT ITEMS (in thousands) | INCOME STATEMENT ITEMS (in thousands) | |||||||||||||||||||||||||

| Net sales | Net sales | $ 137,608 | $ 144,568 | $ 140,825 | $ 142,458 | $ 157,509 | Net sales | $ | 204,240 | $ | 137,608 | $ | 144,568 | $ | 140,825 | $ | 142,458 | ||||||||||

| Cost of products sold | Cost of products sold | 103,315 | 112,187 | 108,339 | 112,311 | 124,157 | Cost of products sold | 154,189 | 103,315 | 112,187 | 108,339 | 112,311 | |||||||||||||||

| Depreciation and amortization | Depreciation and amortization | 3,814 | 3,921 | 3,486 | 3,825 | 3,440 | Depreciation and amortization | 4,719 | 3,814 | 3,921 | 3,486 | 3,825 | |||||||||||||||

| Interest expense | Interest expense | 122 | 185 | 255 | 323 | 369 | Interest expense | 977 | 122 | 185 | 255 | 323 | |||||||||||||||

| Income before income taxes | Income before income taxes | 11,223 | 8,021 | 11,529 | 10,114 | 13,225 | Income before income taxes | 11,455 | 11,223 | 8,021 | 11,529 | 10,114 | |||||||||||||||

| Income taxes | Income taxes | 3,438 | 2,294 | 3,867 | 3,212 | 4,599 | Income taxes | 6,410 | 3,438 | 2,294 | 3,867 | 3,212 | |||||||||||||||

| Net income | Net income | 7,785 | 5,727 | 7,661 | 6,902 | 8,626 | Net income | 5,045 | 7,785 | 5,727 | 7,661 | 6,902 | |||||||||||||||

| Dividends # | Dividends # | 2,751 | 2,811 | 2,987 | 2,613 | 3,109 | Dividends # | 2,755 | 2,751 | 2,811 | 2,987 | 2,613 | |||||||||||||||

| BALANCE SHEET ITEMS (in thousands) | BALANCE SHEET ITEMS (in thousands) | BALANCE SHEET ITEMS (in thousands) | |||||||||||||||||||||||||

| Inventories | Inventories | $ 34,030 | $ 36,842 | $ 34,402 | $ 30,658 | $ 29,385 | Inventories | $ | 47,269 | $ | 34,030 | $ | 36,842 | $ | 34,402 | $ | 30,658 | ||||||||||

| Working capital | Working capital | 64,831 | 60,105 | 57,845 | 57,379 | 56,920 | Working capital | 68,751 | 64,831 | 60,105 | 57,845 | 57,379 | |||||||||||||||

| Property, plant and equipment, net | Property, plant and equipment, net | 26,166 | 26,801 | 28,051 | 27,392 | 25,661 | Property, plant and equipment, net | 29,192 | 26,166 | 26,801 | 28,051 | 27,392 | |||||||||||||||

| Total assets | Total assets | 124,198 | 121,739 | 121,271 | 113,858 | 115,854 | Total assets | 176,458 | 124,198 | 121,739 | 121,271 | 113,858 | |||||||||||||||

| Shareholders’ equity | 82,468 | 79,405 | 74,975 | 81,505 | 71,582 | ||||||||||||||||||||||

| Shareholders' equity | Shareholders' equity | 86,931 | 82,468 | 79,405 | 74,975 | 81,505 | |||||||||||||||||||||

| Capital expenditures | Capital expenditures | 2,863 | 2,538 | 3,633 | 5,524 | 4,217 | Capital expenditures | 2,763 | 2,863 | 2,538 | 3,633 | 5,524 | |||||||||||||||

| Long-term obligations, less current portion | Long-term obligations, less current portion | 893 | 1,786 | 3,214 | 4,286 | 6,071 | Long-term obligations, less current portion | 28,675 | 893 | 1,786 | 3,214 | 4,286 | |||||||||||||||

| PER SHARE DATA | PER SHARE DATA | PER SHARE DATA | |||||||||||||||||||||||||

| Net income per share | Net income per share | Net income per share | |||||||||||||||||||||||||

| Basic | Basic | $ 1.25 | $ .92 | $ 1.23 | $ 1.11 | $ 1.39 | Basic | $ | .81 | $ | 1.25 | $ | 0.92 | $ | 1.23 | $ | 1.11 | ||||||||||

| Diluted | Diluted | 1.25 | .92 | 1.23 | 1.11 | 1.38 | Diluted | 0.80 | 1.25 | 0.92 | 1.23 | 1.11 | |||||||||||||||

Dividends # | Dividends # | .44 | .45 | .48 | .42 | .50 | Dividends # | 0.44 | 0.44 | 0.45 | 0.48 | 0.42 | |||||||||||||||

| Shareholders’ equity (Basic) | 13.19 | 12.71 | 12.04 | 13.10 | 11.51 | ||||||||||||||||||||||

| Shareholders' equity (Basic) | Shareholders' equity (Basic) | 13.89 | 13.19 | 12.71 | 12.04 | 13.10 | |||||||||||||||||||||

| Average shares outstanding: | Basic | 6,251,535 | 6,245,057 | 6,225,068 | 6,220,928 | 6,216,931 | Basic | 6,259,139 | 6,251,535 | 6,245,057 | 6,225,068 | 6,220,928 | |||||||||||||||

| Diluted | 6,251,535 | 6,245,057 | 6,237,914 | 6,237,758 | 6,233,375 | ||||||||||||||||||||||

| Diluted | Diluted | 6,294,773 | 6,251,535 | 6,245,057 | 6,237,914 | 6,237,758 | |||||||||||||||||||||

# - Dividends for 2015 dividends include a $0.01 per share redemption for the termination of the 2008 Shareholder Rights Agreement. Dividends for 2014 dividends include a one-time extra payment of $0.04 per share distributed on 9/15/September 15, 2014. 2012 dividends include a one-time extra payment of $0.10 per share distributed on 12/14/2012.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States ("U.S. GAAP") requires management to make judgments, estimates and assumptions regarding uncertainties that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities and the reported amounts of revenues and expenses. Areas of uncertainty that require judgments, estimates and assumptions include items such as the accounting for derivatives; environmental matters; the testing of goodwill and other intangible assets for impairment; proceeds on assets to be sold; pensions and other postretirement benefits; and tax matters. Management uses historical experience and all available information to make its estimates and assumptions, but actual results will inevitably differ from the estimates and assumptions that are used to prepare the Company's financial statements at any given time. Despite these inherent limitations, management believes that Management's Discussion and Analysis of Financial Condition and Results of Operations and the financial statements and related footnotes provide a meaningful and fair presentation of the Company.

Management believes that the application of these estimates and assumptions on a consistent basis enables the Company to provide the users of the financial statements with useful and reliable information about the Company's operating results and financial condition.

Allowance for Doubtful Accounts

The Company maintains an allowance for doubtful accounts for estimated losses resulting from the inability of its customers to make required payments. The Company reviews the collectability of its receivables on an ongoing basis, taking into account a

17

combination of factors. The Company reviews potential problems, such as past due accounts, a bankruptcy filing or deterioration in the customer's financial condition, to ensure that the Company has adequately accrued for potential loss. Accounts are considered past due based on when payment was originally due. If a customer's situation changes, such as a bankruptcy or its creditworthiness, or there is a change in the current economic climate, the Company may modify its estimate of the allowance for doubtful accounts. The Company will write off accounts receivable after reasonable collection efforts have been made and the accounts are deemed uncollectible.

Inventory Reserve

Inventories are valued at the lower of cost or market and or net realizable value. Cost is determined by the last-in, first-out ("LIFO") method at the Company's U.S. facilities. Accordingly, a LIFO valuation reserve is calculated using the dollar value link chain method.

We review the net realizable value of inventory in detail on an ongoing basis, giving consideration to deterioration, obsolescence and other factors. Based on these assessments, we provide for an inventory reserve in the period in which an impairment is identified. The reserve fluctuates with market conditions, design cycles and other economic factors.

Goodwill and Other Intangible Assets

Intangible assets with finite useful lives are generally amortized on a straight-line basis over the periods benefited. Goodwill and other intangible assets with indefinite useful lives are not amortized. The Company performed its most recent qualitative assessment as of the end of fiscal 2017 and determined that it is more likely than not that no impairment of goodwill existed at the end of 2017. The Company will perform annual qualitative assessments in subsequent years as of the end of each fiscal year. Additionally, the Company will perform interim analysis whenever conditions warrant.

Pension and Other Postretirement Benefits

The amounts recognized in the consolidated financial statements related to pension and other postretirement benefits are determined from actuarial valuations. Inherent in these valuations are assumptions about such factors as expected return on plan assets, discount rates at which liabilities could be settled, rate of increase in future compensation levels, mortality rates, and trends in health insurance costs. These assumptions are reviewed annually and updated as required. In accordance with GAAP, actual results that differ from the assumptions are accumulated and amortized over future periods and, therefore, affect the expense recognized and obligations recorded in future periods.

The discount rate used is based on a single equivalent discount rate derived with the assistance of our actuaries by matching expected future benefit payments in each year to the corresponding spot rates from the Citigroup Pension Liability Yield Curve, comprised of high quality (rated AA or better) corporate bonds. Effective January 1, 2017, the Company elected to refine its approach for calculating its service and interest costs in future years by applying the specific spot rates along the selected yield curve to the relevant projected cash flows. The Company believes this method more precisely measures its obligations.

The expected long-term rate of return on assets is also developed with input from the Company's actuarial firms. We consider the Company's historical experience with pension fund asset performance, the current and expected allocation of our plan assets and expected long-term rates of return. The long-term rate-of-return assumption used for determining net periodic pension expense was 7.5% for 2017 and 8.0% for 2016. The Company reviews the long-term rate of return each year. Effective January 1, 2017, the Company lowered the long-term rate-of-return assumption to 7.5% to better reflect the expected returns of its current investment portfolio.

Future actual pension income and expense will depend on future investment performance, changes in future discount rates and various other factors related to the population of participants in the Company's pension plans.

The Company expects to make cash contributions of approximately $510,000 and $105,000 to our pension plans and other postretirement plan, respectively, in 2018. The Company may contribute $1,000,000 to $2,000,000 in 2018 to take advantage of the 34% corporate tax rate that would be applied to its 2017 federal tax return. The Company has until September 15, 2018, or until the Company files its 2017 federal tax return to make that determination and contribution.

In connection with our pension and other postretirement benefits, the Company reported a $0.6 million, ($1.1) million, and $3.5 million gain/(loss) (net of tax) on its Consolidated Statement of Comprehensive Income for Fiscal Years 2017, 2016 and 2015, respectively. While the main factor driving this gain/(loss) was the change in the discount rate during the applicable period, the Company froze the benefits of our salaried pension plan effective May 31, 2016, resulting in an approximate $2.5 million gain for this significant event.

18

Assumptions used to determine net periodic pension benefit cost for the fiscal years indicated were as follows:

2017 | 2016 | 2015 | ||||||||||

| Discount rate | 4.04% - 4.08 | % | 4.24%-4.28 | % | 3.90 | % | ||||||

| Expected return on plan assets | 7.5 | % | 8.0 | % | 8.0 | % | ||||||

| Rate of compensation increase | 0.0 | % | 3.25 | % | 3.25 | % | ||||||

Assumptions used to determine net periodic other postretirement benefit cost are the same as those assumptions used for the pension benefit cost, except that the rate of compensation is not applicable for other postretirement benefit cost.

The changes in assumptions had the following effect on the net periodic pension and other postretirement costs recorded in Other Comprehensive Income as follows:

| Year ended | ||||||||||||

| December 30 | December 31 | January 2 | ||||||||||

| 2017 | 2016 | 2016 | ||||||||||

| Discount rate | $ | (6,382,182 | ) | $ | (2,394,216 | ) | $ | 4,208,918 | ||||

| Mortality table | -- | -- | -- | |||||||||

| Additional recognition due to significant event | (496,899 | ) | 2,534,589 | -- | ||||||||

| Asset gain or loss | 6,043,672 | (4,358,254 | ) | (577,892 | ) | |||||||

| Amortization of: | ||||||||||||

| Unrecognized gain or loss | 1,153,885 | 1,610,942 | 1,947,102 | |||||||||

| Unrecognized prior service cost | 157,430 | 176,678 | 194,696 | |||||||||

| Other | 140,969 | 776,658 | (415,479 | ) | ||||||||

| Comprehensive income, before tax | 616,875 | (1,653,603 | ) | 5,357,345 | ||||||||

| Income tax | 62,632 | (543,297 | ) | 1,899,285 | ||||||||

| Comprehensive income, net of tax | $ | 554,243 | $ | (1,110,306 | ) | $ | 3,458,060 | |||||

The Plan has been investing a portion of the assets in long-term bonds in an effort to better match the impact of changes in interest rates on its assets and liabilities and thus reduce some of the volatility in Other Comprehensive Income. Please refer to Note 9 – Retirement Benefit Plans in Item 8 of this Form 10-K for additional disclosures concerning the Company's pension and other postretirement benefit plans.

Software Development Costs

Software development costs, including costs to develop software sold, leased, or otherwise marketed, that are incurred subsequent to the establishment of technological feasibility are capitalized if significant. Costs incurred during the application development stage for internal-use software are capitalized if significant. Capitalized software development costs are amortized using the straight-line amortization method over the estimated useful life of the applicable software. Such software development costs required to be capitalized have not been material to date.

Items Impacting Earnings

To supplement our consolidated financial statements presented in accordance with GAAP, we disclose certain non-GAAP financial measures, including adjusted net income and adjusted earnings per diluted share. Adjusted net income and adjusted earnings per diluted share exclude transaction-related expenses, a charge to costs of goods sold as a result of the impact of purchase accounting and environmental remediation costs. In addition, reported growth in the Industrial Hardware business segment excludes the results of the Velvac division, which was acquired on April 3, 2017. Furthermore, we show the impact of the one-time charge related to the Tax Cuts and Jobs Act of 2017. These measures are not in accordance with GAAP.

Management uses such measures to evaluate performance period over period, to analyze the underlying trends in our business, including our business segments, to assess our performance relative to our competitors and to establish operational goals and

19

forecasts that are used in allocating resources. These financial measures should not be considered in isolation from, or as a replacement for, GAAP financial measures.

We believe that presenting non-GAAP financial measures in addition to GAAP financial measures provides investors greater transparency to the information used by our management for its financial and operational decision-making. We further believe that providing this information better enables our investors to understand our operating performance and to evaluate the methodology used by management to evaluate and measure such performance.

| Reconciliation of expenses from GAAP to Non-GAAP financial measures | ||||||||||||||||

| For the Three and Twelve Months ended December 30, 2017 | ||||||||||||||||

| Three Months Ended | Twelve Months Ended | |||||||||||||||

| December 30, 2017 | December 30, 2017 | |||||||||||||||

| Net Income as reported per generally accepted accounting principles (GAAP) | $ | (168,769 | ) | $ | 5,045,255 | |||||||||||

| Earnings Per Share as reported under generally accepted accounting principles (GAAP): | ||||||||||||||||

| Basic | $ | (0.03 | ) | $ | 0.81 | |||||||||||