Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large“large accelerated filer," "accelerated” “accelerated filer," "smaller” “smaller reporting company"company” and "emerging“emerging growth company"company” in Rule 12b-2 of the Exchange Act.

The aggregate market value of the shares of registrant’s Common Stock, $1 par value, held by nonaffiliates of the registrant was approximately $1,810,436,970$1,810,436,970 as of June 28, 2019.

Our growth strategy is driven by constant refresh and expansionoutstanding shares of our

product and solution offerings to meet marketplace needs. This organic growth approach extends to a constantly evolving set of supply chain services that are designed to lower the customer’s total cost of procuring, owning and deploying the products we sell. We have identified security, professional audio/visual, wireless, industrial automation, electrical grid upgrades, as well as emerging technologies such as 5G and IoT as growth opportunities we are pursuing. Organic growth will periodically be supplemented with acquisitions where the benefits associated with geographic expansion, market penetration or new product line additions are weighted in favor of "buying versus building."common stock.| | | | | Amount and Nature of | | | | |

| Title of Class | | Name and Address of Beneficial Owner | | Beneficial Ownership | | | Percent of Class | |

| Common | | BlackRock, Inc. | | | 4,758,853 | (1) | | | 14.0 | % |

| | | 55 East 52nd Street | | | | | | | | |

| | | New York, NY 10055 | | | | | | | | |

| | | | | | | | | | | |

| Common | | Samstock/SZRT, L.L.C. | | | 1,329,432 | (2) | | | 10.7 | % |

| | | Samstock/SIT, L.L.C. | | | 362,147 | | | | | |

| | | KMJZ Investments L.L.C. | | | 526,277 | | | | | |

| | | Samstock/ZFT, L.L.C. | | | 55,588 | | | | | |

| | | Samstock/Alpha, L.L.C. | | | 55,587 | | | | | |

| | | KZ 2007 Holdings, LLC | | | 40,000 | | | | | |

| | | MZ 2007 Holdings, LLC | | | 40,000 | | | | | |

| | | JZ 2007 Holdings, LLC | | | 40,000 | | | | | |

| | | SZ Intervivos QTIP Trust | | | 28,700 | | | | | |

| | | Samuel Zell | | | 15,666 | | | | | |

| | | Zell Family Foundation | | | 1,147,940 | | | | | |

| | | Two North Riverside Plaza | | | | | | | | |

| | | Chicago, IL 60606 | | | | | | | | |

| | | | | | | | | | | |

| Common | | The Vanguard Group, Inc. | | | 3,098,946 | (3) | | | 9.1 | % |

| | | 100 Vanguard Blvd. | | | | | | | | |

| | | Malvern, PA | | | | | | | | |

| | | 19355 | | | | | | | | |

| | | | | | | | | | | |

| Common | | Dimensional Fund Advisors LP | | | 2,318,912 | (4) | | | 6.9 | % |

| | | Building One | | | | | | | | |

| | | 6300 Bee Cave Road | | | | | | | | |

| | | Austin, Texas 78746 | | | | | | | | |

| (1) | According to Schedule 13G, dated February 3, 2020, BlackRock, Inc. has sole power to vote 4,665,900 shares and sole power to dispose of 4,758,853 shares. |

| (2) | Samstock/SZRT, L.L.C. is a limited liability company whose sole member is Samuel Zell Revocable Trust. The trustee of Samuel Zell Revocable Trust is Mr. Zell. Samstock/SIT, L.L.C. is a limited liability company whose sole member is Sam Investment Trust, whose trustee is Chai Trust, a limited liability company. The beneficiaries of Sam Investment Trust are Samuel Zell and members of his family. Samstock/ZFT, L.L.C. is a limited liability company whose sole member is ZFT Partnership, an Illinois general partnership, whose sole partners are the Zell Trusts. Samstock/Alpha, L.L.C. is a limited liability company whose sole member is Alphabet Partners, an Illinois general partnership, whose sole partners are the Zell Trusts. KMJZ Investments L.L.C. is a limited liability company whose sole members are the Zell Trusts. KZ 2007 Holdings, LLC, is a limited liability company, whose sole member is KZ 2007 Trust. MZ 2007 Holdings, LLC, is a limited liability company, whose sole member is MZ 2007 Trust. JZ 2007 Holdings, LLC, is a limited liability company, whose sole member is JZ 2007 Trust. The trustee of all of the Zell Trusts, the SZ Intervivos QTIP Trust, the KZ 2007 Trust, the MZ 2007 Trust, and the JZ 2007 Trust is Chai Trust. Mr. Zell is neither a director nor an officer of Chai Trust and does not have voting or dispositive power over such shares indirectly held by such trusts, and accordingly, Mr. Zell has disclaimed beneficial ownership of such shares, except to the extent of any pecuniary interest therein. The amounts shown for Mr. Zell include (i) 14,666 of such shares held by Samuel Zell Revocable Trust, the trustee of which is Mr. Zell, and (ii) 1,000 shares held by Helen Zell Revocable Trust, the trustee of which is Helen Zell, spouse of Mr. Zell, and to which Mr. Zell disclaims beneficial ownership. Also includes 1,147,940 shares held by the Zell Family Foundation to which Mr. Zell disclaims beneficial ownership. The total does not include 95,374 restricted stock units owned by Mr. Zell. |

| (3) | According to Schedule 13G, dated February 10, 2020, The Vanguard Group Inc. has sole power to vote 29,459 shares, shared power to vote 4,603 shares, sole power to dispose of 3,068,876 shares and shared power to dispose of 30,070 shares. |

| (4) | According to Schedule 13G, dated February 12, 2020, Dimensional Fund Advisors LP has sole power to vote 2,238,978 shares and sole power to dispose of 2,318,912 shares. |

Business Segments and Products

We have identified Network & Security Solutions ("NSS"), Electrical & Electronic Solutions ("EES") and Utility Power Solutions ("UPS") as reportable segments. Equity Compensation Plan Information

The following is a brief descriptiontable summarizes information, as of each of our reportable segments and business activities.

Within our segments, we are also organized by geographies. Our geographies consist of North America, which includes the U.S. and Canada, EMEA, which includes Europe, the Middle East and Africa, and Emerging Markets, which includes Asia Pacific and Central and Latin America ("CALA").

Network & Security Solutions ("NSS")

The Network & Security Solutions segment, with sales in approximately 55 countries, supplies products and customized Supply Chain Solutions to customers in a diverse range of industries including technology, finance, telecommunications service providers, transportation, education, government, healthcare and retail. NSS sells these products directly to end users or through various channels including data communications contractors, security, network, professional audio/visual and systems integrators. NSS has a broad product portfolio that includes copper and fiber optic cable and connectivity, access control, video surveillance, intrusion and fire/life safety, cabinets, power, cable management, wireless, professional audio/video, voice and networking switches and other ancillary products. The NSS segment includes over 2,300 technically trained salespeople, approximately 70 Supply Chain Solutions specialists and a global technical support organization that provides support across all three reportable segments to aid in design, product specification and complete bills of materials inclusive of all Anixter solutions.

Through a variety of value-added supply chain solutions, including inventory management, product packaging and enhancement, and customized supply chain services, NSS helps customers reduce the risk, complexity and cost associated with their IT infrastructure and physical security deployments. The NSS commitment to quality products and services and technical leadership is demonstrated by its participation in many global standards organizations. NSS technical expertise extends to performance and interoperability testing at our Infrastructure Solutions LabSM, which provides NSS the opportunity to demonstrate solutions and proofs-of-concept to customers. Anixter's Infrastructure as a Platform and ipAssuredSM programs help customers make intelligent buying decisions around network and security infrastructure and improve efficiency to meet their sustainability goals.

Electrical & Electronic Solutions ("EES")

The Electrical & Electronic Solutions segment, with sales in approximately 40 countries, supplies a broad range of wire and cable, control, power/gear, lighting and core electrical products and customized supply chain solutions to the Commercial and Industrial ("C&I") and Original Equipment Manufacturer ("OEM") markets. The C&I group supplies products for the transmission of power and signals in industrial applications to customers in key markets including oil, gas and petrochemical, alternative energy, utility, power generation and distribution, transportation, commercial, industrial, natural resource and water and wastewater treatment. It sells directly to end users or through channels including electrical contractors, security and automation integrators, and engineering, procurement and construction firms. The OEM group supplies products used in the manufacturing of automotive, industrial, medical, transportation, marine, military and communications equipment, selling to OEM and panel, cable and harness shops. The product portfolio in this global business includes electrical and electronic wire and cable, shipboard cable, support and supply products, low-voltage cable, instrumentation cable, industrial communication and control products, security cable, connectors, and industrial Ethernet switches. Value-added services, including supply chain management services and technical support, are tailored to position us as a specialist in fast growing emerging markets, OEMs and industrial verticals. EES helps customers achieve their sustainability goals by using its value-added services to minimize scrap, reduce lead times and improve operational efficiency.

The EES team of nearly 1,200 technically trained sales personnel, supply chain specialists, industrial communication specialists and engineers. EES provides world-class technical assistance, products and support through code and standards interpretation, product selection assistance, on-site customer training and customer specification reviews. EES brings value to its customers through its global reach, ability to provide global infrastructure project coordination, technical and engineering support, financial strength, and sourcing and supplier relationships. These capabilities help customers reduce costs and risks and gain competitive advantage in their marketplace.

Utility Power Solutions ("UPS")

The Utility Power Solutions segment, with primary operations in the U.S. and Canada, supplies electrical transmission and distribution products, power plant maintenance, repair and operations supplies and smart-grid products, and arranges materials management and procurement outsourcing for the power generation, power transmission and electricity distribution industries. The UPS segment serves the electric utility markets. Products include conductors such as wire and cable, transformers, overhead transmission and distribution hardware, switches, protective devices and underground distribution, connectors used in the construction or maintenance and repair of electricity transmission and substation distribution infrastructure and supplies, lighting and conduit used in non-residential and residential construction. UPS also provides materials management and procurement outsourcing services. Its capabilities allow us to integrate with our customers and perform part of our customers' sourcing and procurement function. The UPS segment includes nearly 300 technically trained salespeople and approximately 40 Supply Chain Solutions specialists.

For more information concerning our business segments, foreign and domestic operations and export sales, see Note 7. "Income Taxes" and Note 10. "Business Segments" in the Notes to the Consolidated Financial Statements.

Suppliers

We source products from thousands of suppliers, with approximately one-quarter of our annual dollar volume purchases sourced from our five largest suppliers. An important element of our overall business strategy is to develop and maintain close relationships with our key suppliers, which include the world’s leading manufacturers of communication cabling, connectivity, support and supply products, electrical wire and cable, and utility products. Such relationships emphasize joint product planning, inventory management, technical support, advertising and marketing. In support of this strategy, we generally do not compete with our suppliers in product design or manufacturing activities. We do, however, sell a small amount of private label products that carry a brand name exclusive to us.

Our typical distribution agreement generally includes the following significant terms:

•a non-exclusive right to resell products to any customer in a geographical area (typically defined as a country, with the exception of our UPS business which is typically defined as a county or state);

•cancelable upon 60 to 90 days notice by either party for any reason;

•no minimum purchase requirements, although pricing may change with volume on a prospective basis; and

•the right to pass through the manufacturer’s warranty to our customers.

Distribution and Service Platform

We cost-effectively serve our customers’ needs through our computer systems, which connect the majority of our warehouses and sales offices throughout the world. The systems are designed for sales support, order entry, inventory status, order tracking, credit review and material management. Customers may also conduct business through our e-commerce platform.

We operate a series of large, modern, regional distribution centers in key geographic locations in North America, EMEA and Emerging Markets that provide for cost-effective, reliable storage and delivery of products to our customers. We have designated 20 warehouses as regional distribution centers. Collectively, these facilities store approximately 35% of our inventory. In certain cities, some smaller warehouses are also maintained to maximize transportation efficiency and to provide for the local needs of customers. Our network of regional distribution centers, local distribution centers, service centers, branch locations and sales offices consists of 245 locations in the United States, 30 in Canada, 24 in the United Kingdom, 23 in Continental Europe and the Middle East, 28 in Latin America, 12 in Asia and 18 in Australia and New Zealand.

We have developed close relationships with certain freight, package delivery and courier services to minimize transit times between our facilities and customer locations, as well as a dedicated delivery fleet of over 500 vehicles in our UPS segment. The combination of our information systems, distribution network and delivery partnerships allows us to provide a high level of customer service while maintaining a reasonable level of investment in inventory and facilities.

Employees

At January 3, 2020, we employed over 9,400 people. Approximately 50% of the employees are engaged in sales or sales-related activities, approximately 35% are engaged in warehousing and distribution operations, and approximately 15% are engaged in support activities, including inventory management, information services, finance, human resources and general management. We do not have any significant concentrations of employees subject to collective bargaining agreements within any of our segments.

Competition

Given our role as an aggregator of many different types of products from many different sources and because these products are sold to many different industry groups, there is no well-defined industry group against which we compete. We view the competitive environment as highly fragmented with hundreds of distributors and manufacturers that sell products directly or through multiple distribution channels to end users or other resellers. There is significant competition within each end market and geography served that creates pricing pressure and the need for excellent service. Competition is based primarily on breadth of products, quality, services, relationships, price and geographic proximity. We believe that we have a significant competitive advantage duerelating to our comprehensive product and service offerings, global distribution network, technically-trained sales team and customized supply chain solutions. We believeequity compensation plans under which our global distribution platform provides a competitive advantage to serving multinational customers’ needs. Our operations and logistics platform gives us the ability to ship orders from inventorycommon stock is authorized for delivery within 24 to 48 hours to all major global markets.

We enhance our value proposition to both key suppliers and customers through our technical expertise, global standards participation testing and demonstration facilities and numerous quality assurance certification programs such as ISO 9001:2015 and ISO/TS 16949:2009. Our NSS, EES and UPS segments leverage our certified Infrastructure Solutions Lab located at our suburban Chicago headquarters to support customers with technology needs related to enterprise networks, data centers, physical security, building technologies and industrial communications and control. At this lab, we evaluate performance and interoperability to help customers reduce risk through informed purchasing decisions. Our Solutions Briefing Centers, premier technology education and demonstration facilities locatedissuance.| | | Number of

securities to be

issued upon exercise

of outstanding

options, warrants

and rights(1) | | | Weighted-average

exercise price of

outstanding options,

warrants and

rights(2) | | | Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding

securities

reflected in the first

column)(3) | |

| Equity compensation plans approved by security holders | | | 1,270,420 | | | | 62.27 | | | | 1,302,182 | |

| (1) | The number shown is the number of shares that, as of January 3, 2020, may be issued upon exercise of 200,738 outstanding options and vesting of 1,069,682 restricted stock units. |

| (2) | Weighted-average exercise price of outstanding stock options (excludes restricted stock units, which vest at no cost to participants). |

| (3) | The number shown is the number of shares that, as of January 3, 2020, may be issued upon exercise of options and other equity awards that may be granted in the future under the plans. |

Change in various regions around the globe, focus Control

As previously disclosed, on providing our customers with the necessary information to make informed decisions around complex, end-to-end technology solutions.

Contract Sales and Backlog

We have a number of customers who purchase products under long-term contractual arrangements. In such circumstances, the relationship with the customer may involve a high degree of material requirements planning and information systems interfaces and, in some cases, may require the maintenance of a dedicated distribution facility or dedicated personnel and inventory at, or in close proximity to, the customer site to meet the needs of the customer. Such contracts do not generally require the customer to purchase any minimum amount of goods from us, but could require that materials acquired by us, as a result of joint material requirements planning between us and the customer, be purchased by the customer. Backlog orders represent approximately five to six weeks of sales and the majority of these orders ship to customers within 30 to 60 days from order date.

Seasonality

The operating results are not significantly affected by seasonal fluctuations except for the impact resulting from variations in the number of billing days from quarter to quarter. Our EES and UPS segments experience some seasonality as weather can restrict project work. Consecutive quarter sales from the third to fourth quarters are generally lower due to the holidays and lower number of billing days as compared to other consecutive quarter comparisons. There were 257 billing days in 2019 and 253 billing days in both 2018 and 2017.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to these reports can be found at the Investor Relations section of our company website at http://www.anixter.com. These forms are available without charge as soon as reasonably practical following the time they are filed with or furnished to the Securities and Exchange Commission ("SEC"). Shareholders and other interested parties may request email notifications of the posting of these documents through the Investor Relations section of our website. In addition, copies of our reports will be made available, free of charge, upon written request.

Our website also contains corporate governance information including corporate governance guidelines; audit, compensation and nominating and governance committee charters; nomination process for directors; and our business ethics and conduct policy.

ITEM 1A. RISK FACTORS.

The following factors could materially adversely affect our operating results and financial condition. Although we have tried to discuss key factors, please be aware that other risks may prove to be important in the future. New risks may emerge at any time, and we cannot predict those risks or estimate the extent to which they may affect our financial performance.

The pendency of our agreement to be acquired by WESCO International, Inc. could have an adverse effect on our business.

On January 10, 2020,

wethe Company, WESCO International, Inc., a Delaware corporation (“WESCO”) and Warrior Merger Sub, Inc., a Delaware corporation and a wholly owned subsidiary of WESCO (“Merger Sub”), entered into

a definitivean Agreement and Plan of Merger (as it may be amended, modified or supplemented from time to time, the “merger agreement”). On the terms and subject to the conditions of the merger agreement,

under which we agreedMerger Sub will be merged with and into the Company (the “merger”), with the Company surviving the merger (the “surviving corporation”) as a wholly owned subsidiary of WESCO. Following the completion of the merger, the Company will cease to be

acquireda publicly traded company.If the merger contemplated by WESCO International, Inc. ("WESCO"). Underthe merger agreement is completed, the Company’s stockholders will be entitled to receive for each share of the Company’s common stock (i) $70.00 in cash, without interest, subject to adjustment pursuant to the terms of the merger agreement, at closing, each share of Anixter common stock will be converted into the right to receive (i) $70.00 in cash, without interest (subject to adjustment as set forth in the merger agreement), (ii) 0.2397 shares of WESCO common stock, (subjectsubject to adjustment as set forth inpursuant to the terms of the merger agreement)agreement, and (iii) 0.6356 depositary shares, each representing a 1/1,000th interest in a share of newly issued WESCO Series A fixed-rate reset cumulative perpetual WESCO preferred stock, $25,000 stated amount per whole preferred (subjectshare, subject to adjustment as set forth inpursuant to the terms of the merger agreement),agreement, in each case, less any applicable withholding taxes. See Note 13. “Subsequent Event” in the notesEach Company stockholder who would otherwise have been entitled to the Consolidated Financial Statements. Because the exchange ratio is fixed for the common stock portion of the merger consideration and the market pricereceive a fractional share of WESCO common stock has fluctuated and will continue to fluctuate, at the time of the special meeting of stockholders to approveor a fractional depositary share in the merger our stockholders will not know or be able to determine the market valueinstead receive a cash payment in lieu of the merger consideration they would receive upon completion of the merger. After the merger, our stockholders will have lower ownership and voting interest in WESCO than they currently have in Anixter and will exercise less influence over management.

The announcement and pendency of the merger could cause disruption in our business, including the potential loss or disruption of commercial relationships prior to the completion of the merger.For example, parties with which we do business may be uncertain as to the effects on them of the merger, including with respect to their current or future business relationships with us. These relationships may be subject to disruption as customers, suppliers and other persons with whom we have a business relationship may delay or defer certain business decisions or might decide to terminate, change or renegotiate their relationships with us or consider entering into business relationships with other parties. These disruptions could have an adverse effect on the results of our operations, cash flows and financial position.The announcement and pendency of the merger could also have a potential negative effect on our ability to retain management, sales and other key personnel.

The merger agreement generally requires us to operate our business in the ordinary course of business pending consummation of the merger, but includes certain contractual restrictions on the conduct of our business prior to completion of the merger.These restrictions may prevent us from taking certain specified actions or otherwise pursuing business opportunities during the pendency of the merger that may be beneficial to us. The merger agreement also contains provisions that limit our ability to pursue alternatives to the merger and that could discourage a potential competing acquirer of Anixter form making a favorable alternative transaction proposal. In addition, matters relating to the merger (including integration planning) will require substantial commitments of time and resources by our management, which could divert their time and attention.We have also incurred, and will continue to incur, significant non-recurring costs in connection with the merger that we may be unable to recover. Further, the merger agreement requires us to pay a substantial termination fee to WESCO in certain circumstances.

The risk, and adverse effect, of any disruption could be exacerbated by a delay in completion of the merger or termination of the merger agreement. Completion of the merger is subject to the satisfaction or waiver of a number of conditions, many of which are not within our control. The failure to satisfy all of the required conditions could delay the completion of the merger for a significant period of time or prevent it from occurring. We cannot provide assurance that our pending merger with WESCO will be completed. Failure to complete the merger could also negatively affect our stock price and our future business and financial results.

Transactions like the merger are frequently the subject of litigation or other legal proceedings, including actions alleging that either our board of directors breached their respective fiduciary duties to their stockholders by entering into the merger agreement, by failing to obtain a greater value in the transaction for their stockholders or otherwise. We believe that any such litigation or proceedings would be without merit, but there can be no assurance that they will not be brought. Indeed, between December 9, 2019 and December 19, 2019, four lawsuits were filed by purported stockholders of Anixter in connection with the now-terminated merger agreement with Clayton, Dubilier & Rice, LLC. If litigation or other legal proceedings are brought against us or against our board in connection with the merger agreement, we will defend against it, but we might not be successful in doing so. An adverse outcome in such matters, as well as the costs and efforts of a defense even if successful, could have a material adverse effect on our business, results of operation or financial position, including through the possible diversion of either company’s resources or distraction of key personnel.

All of the matters described above, alone or in combination, could materially and adversely affect our business, financial condition, results of operations and stock price. fractional share.The foregoing description of our pending acquisition by WESCO isthe merger and the merger agreement does not purport to be complete and is qualified in its entirety by reference to the registration statement on Form S-4,merger agreement, which contains a preliminary proxy statement/prospectus with respectis filed as Exhibit 2.1 to the merger, filed by WESCO with the SEC on February 7, 2020. We urge you to read the registration statement on Form S-4 because it contains important information about the merger, including relevant risk factors.

A change in sales strategy or financial viability of our suppliers could adversely affect our sales or earnings.

Most of our agreements with suppliers are terminable by either party on short notice for any reason. We currently source products from thousands of suppliers. However, approximately one-quarter of our annual dollar volume purchases are sourced from our five largest suppliers. If any of these suppliers changes its sales strategy to reduce its reliance on distribution channels, or decides to terminate its business relationship with us, our sales and earnings could be adversely affected until we are able to establish relationships with suppliers of comparable products. Although we believe our relationships with these key suppliers are good, they could change their strategies as a result of a change in control, expansion of their direct sales force, changes in the marketplace or other factors beyond our control, including a key supplier becoming financially distressed.

We have risks associated with the sale of nonconforming products and services.

Historically, we have experienced a small number of cases in which our vendors supplied us with products that did not conform to the agreed upon specifications without our knowledge. Additionally, we may inadvertently sell a product not suitable for a customer’s application. We address this risk through our quality control processes, by seeking to limit liability and our warranty in our customer contracts, by obtaining indemnification rights from vendors and by maintaining insurance responsive to these risks. However, there can be no assurance that we will be able to include protective provisions in all of our contracts, that vendors will have the financial capability to fulfill their indemnification obligations to us, or that insurance can be obtained with sufficiently broad coverage or in amounts sufficient to fully protect us.

Our foreign operations are subject to political, economic, currency and other risks.

We derive approximately one quarter of our revenues from sales outside of the U.S. Economic and political conditions in some of these foreign markets may adversely affect our results of operations, cash flows and financial condition in these foreign markets. Our results of operations and the value of our foreign assets are affected by fluctuations in foreign currency exchange rates (as further discussed in "Item 7A. Quantitative and Qualitative Disclosures About Market Risk") and different legal, tax, accounting and regulatory requirements. In addition, some of the products that we distribute are produced in foreign countries, which involve longer and more complex supply chains that are vulnerable to numerous risks that could cause significant interruptions or delays in delivery of such products. Many of these factors are beyond our control and include risks, such as political instability, financial instability of suppliers, suppliers' noncompliance with applicable laws, trade restrictions, labor disputes, currency fluctuations, changes in tariff or import policies, severe weather, public health crises, terrorist attacks and transport capacity and cost. For example, the recent outbreak of a novel strain of coronavirus, a respiratory illness, in China, could adversely affect our supply chains involving China and other affected regions. The extent to which the coronavirus will impact our business, results of operation or financial condition is difficult to assess at this stage as much depends on future developments, which are uncertain, including information concerning the severity of the coronavirus and the methods to contain and treat the virus. A significant interruption in our supply chains caused by any of the above factors could result in increased costs or delivery delays and result in a decrease in our net sales and profitability.

We have risks associated with inventory.

We must identify the right product mix and maintain sufficient inventory on hand to meet customer orders. Failure to do so could adversely affect our sales and earnings. However, if circumstances change (for example, an unexpected shift in market demand, pricing or customer defaults) there could be a material impact on the net realizable value of our inventory. To guard against inventory obsolescence, we have negotiated various return rights and price protection agreements with certain key suppliers. We also maintain an inventory valuation reserve account against declines in the value or salability of our inventory. However, there is no guaranty that these arrangements will be sufficient to avoid write-offs in excess of our reserves in all circumstances.

Our operating results are affected by copper prices.

Our operating results have been affected by changes in prices of copper, which is a major component in a portion of the electrical wire and cable products we sell. As our purchase costs with suppliers change to reflect the changing copper prices, our percent mark-up to customers remains relatively constant, resulting in higher or lower sales revenue and gross profit depending upon whether copper prices are increasing or decreasing.

We have risks associated with the integration of acquired businesses.

In connection with recent and future acquisitions, it is necessary for us to continue to create an integrated business from the various acquired entities. This requires the establishment of a common management team to guide the acquired businesses, the conversion of numerous information systems to a common operating system, the establishment of a brand identity for the acquired businesses, the streamlining of the operating structure to optimize efficiency and customer service and a reassessment of the inventory and supplier base to ensure the availability of products at competitive prices. No assurance can be given that these various actions can be completed without disruption to the business, in a short period of time or that anticipated improvements in operating performance can be achieved. Any inability on our part to successfully implement strategic transactions could have an adverse impact on our reputation, business, financial condition, operating results and cash flows. There can be no assurance that any businesses acquired will meet performance expectations or that business judgments concerning the value, strengths and weaknesses of businesses acquired will prove to be correct. In addition, any acquisition that we make may not deliver the synergies and other benefits that were anticipated when entering into such acquisition.

Our debt agreements could impose restrictions on our business.

Our debt agreements contain certain financial and operating covenants that limit our discretion with respect to certain business matters. These covenants restrict our ability to, among other things:

•incur additional indebtedness;

•create liens on assets;

•make certain investments;

•transfer, lease or dispose of assets; and

•engage in certain mergers, acquisitions, consolidations or other fundamental changes.

These covenants also limit the amount of dividends or share repurchases we may make. As a result of these restrictions, we are limited in how we may conduct business and may be unable to compete effectively or take advantage of new business opportunities. Our ability to comply with the covenants and restrictions contained in our debt agreements may be affected by economic, financial and industry conditions or regulatory changes beyond our control. The breach of any of these covenants or restrictions could result in a default under our revolving lines of credit or the indentures governing our outstanding notes that would permit the applicable lenders or noteholders, as the case may be, to declare all outstanding amounts to be due and payable, together with accrued and unpaid interest. If we are unable to repay indebtedness, lenders having secured obligations, such as the lenders under our revolving lines of credit, could proceed against the collateral securing these obligations. This could have a significant negative impact on our financial condition and operating results.

We have substantial debt which could adversely affect our profitability, limit our ability to obtain financing in the future and pursue certain business opportunities.

As of January 3, 2020, we had an aggregate principal amount of $1.06 billion of outstanding debt. As a result, a substantial portion of our cash flow from operations must be dedicated to the payment of principal and interest on our indebtedness, thereby reducing the funds available to us for other purposes. This may also limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions, debt service requirements, and general corporate purposes in the future. Our indebtedness also reduces our flexibility to adjust to changing market conditions or may prevent us from making capital investments that are necessary or important to our operations and strategic growth.

If our cash flow and capital resources are not sufficient to fund our debt service obligations, we could face liquidity problems and may be required to reduce or delay capital expenditures, sell assets, seek to obtain additional equity capital or refinance our debt. We cannot make assurances that we will be able to refinance our debt on terms acceptable to us, or at all. Our debt agreements and the indentures governing our outstanding notes restrict our ability to dispose of assets and how we use the proceeds from any such dispositions. We cannot make assurances that we will be able to consummate those dispositions, or if we do, what the timing of the dispositions will be or whether the proceeds that we realize will be adequate to meet our debt service obligations when due.

We have risks associated with accounts receivable.

A significant portion of our working capital consists of accounts receivable. Although no single customer accounts for more than 3% of our sales, a payment default by one of our larger customers could have a negative short-term impact on earnings or liquidity. A financial or industry downturn could have an adverse effect on the collectability of our accounts receivable, which could result in longer payment cycles, increased collection costs and defaults.

A decline in project volume could adversely affect our sales and earnings.

While much of our sales and earnings are generated by comparatively smaller and more frequent orders, the fulfillment of large orders for capital projects generates significant sales and earnings. Slow macro-economic growth rates, difficult credit market conditions for our customers, weak demand for our customers’ products or other customer spending constraints can result in project delays or cancellations, potentially having a material adverse effect on our financial results.

The level of returns on pension plan assets and the actuarial assumptions used for valuation purposes could affect our earnings and cash flows in future periods. Changes in government regulations could also affect our pension plan expenses and funding requirements.

The funding obligations for our pension plans are impacted by the performance of the financial markets, particularly the equity markets, and interest rates. Funding obligations are determined under government regulations and are measured each year based on the value of assets and liabilities on a specific date. If the financial markets do not provide the long-term returns that are expected under the governmental funding calculations, we could be required to make larger contributions. The equity markets can be very volatile, and therefore our estimate of future contribution requirements can change dramatically in relatively short periods of time. Similarly, changes in interest rates and legislation enacted by governmental authorities can impact the timing and amounts of contribution requirements. An adverse change in the funded status of the plans could significantly increase our required contributions in the future and adversely impact our liquidity. At January 3, 2020, our projected benefit obligations exceeded the fair value of plan assets by $71.0 million.

Assumptions used in determining projected benefit obligations and the fair value of plan assets for our pension plans are determined by us in consultation with outside actuaries. In the event that we determine that changes are warranted in the assumptions used, such as the discount rate, expected long-term rate of return on assets, or mortality rates, our future pension benefit expenses could increase or decrease. Due to changing market conditions, the assumptions that we use may differ from actual results, which could have a significant impact on our pension liabilities and related costs and funding requirements.

Any significant disruption, interruption or failure of our information systems could disrupt our business, result in increased costs and decreased revenues, harm our reputation, and expose us to liability.

We rely on the proper functioning and availability of our information systems to successfully operate our business, including managing inventory, processing customer orders, shipping products and providing service to customers, and compiling financial results. Our information systems may be disrupted due to natural disasters, power or telecommunications outages, unauthorized access, or other causes. Any significant or prolonged unavailability or failure of our critical information systems could materially impair our ability to maintain proper levels of inventories, process orders, meet the demands of our customers in a timely manner, and other harmful effects. We seek to continually enhance our information systems, and such changes could potentially create a disruption or failure of our existing information technology. Additionally, efforts to align portions of our business on common platforms, systems and processes could result in unforeseen interruptions, increased costs or liability, and other negative effects.

We may experience a failure in or breach of our operational or information security systems, or those of our third-party service providers, as a result of cyber attacks or information security breaches.

Information security risks have generally increased in recent years because of the proliferation of new technologies and the increased sophistication and activities of perpetrators of cyber attacks. A failure in or breach of our operational or information security systems, or those of our third-party service providers, as a result of cyber attacks, mailicious intrusions or information security breaches could disrupt our business, result in the disclosure or misuse of confidential or proprietary information, damage our reputation, increase our costs and/or cause losses. As a result, cyber security and the continued development and enhancement of the controls and processes designed to protect our systems, computers, software, data and networks from attack, damage or unauthorized access remain a priority for us. Although we believe that we have robust information security procedures and other safeguards in place, as cyber threats continue to evolve, we may be required to expend additional resources to continue to enhance our information security measures and/or investigate and remediate any information security vulnerabilities. If our information systems are compromised, we may face regulatory sanctions or penalties under applicable laws, experience increases in operating expenses or an impairment in our ability to conduct our operations, incur expenses or lose revenues as a result of a data privacy breach, information technology outages or disruptions, or suffer other adverse consequences including lawsuits or other legal action and damage to our reputation.

Disruptions to our logistics capability or supply chain may have an adverse impact on our operations.

Our global logistics services are operated through distribution centers around the world. We also depend on transportation service providers for the delivery of products to our customers. Any significant interruption or disruption in service at one or more of our distribution centers due to severe weather, natural disasters, information technology upgrades, operating issues, disruptions to our transportation network, public heath crises (such as the recent outbreak of a novel strain of coronavirus) or other unanticipated events, could impair our ability to obtain or deliver inventory in a timely manner, cause cancellations or delays in shipments to customers or otherwise disrupt our normal business operations.

We are subject to various laws and regulations globally and any failure to comply could adversely affect our business.

We are subject to a broad range of laws and regulations in the jurisdictions where we operate globally, including, among others, those relating to data privacy and protection, cyber security, import and export requirements, anti-bribery and corruption, product compliance, supplier regulations regarding the sources of supplies or products, environmental protection, health and safety requirements, intellectual property, foreign exchange controls and cash repatriation restrictions, labor and employment, e-commerce, advertising and marketing, anti-competition and tax. Compliance with these domestic and foreign laws, regulations and requirements may be burdensome, increasing our cost of compliance and doing business. In addition, as a supplier to federal, state, and local government agencies, we must comply with certain laws and regulations relating specifically to our governmental contracts. Although we have implemented policies and procedures designed to facilitate compliance with these laws, we cannot assure you that our employees, contractors, or agents will not violate such laws and regulations, or our policies and procedures. Any such violations could result in the imposition of fines and penalties, damage to our reputation, and, in the case of laws and regulations relating to governmental contracts, the loss of those contracts.

We may be adversely affected by the United Kingdom's withdrawal from the European Union (Brexit) and their future relationship with other countries.

On January 31, 2020, the United Kingdom formally withdrew from the European Union (“Brexit”). This started a transition period that will last until at least December 31, 2020 during which time the United Kingdom remains in the European Economic Area, single market and customs union, and European Union laws continues to apply in the United Kingdom. The United Kingdom and European Union have made a non-binding political declaration setting out a framework for the future relationship between the United Kingdom and the European Union after the transition period. Negotiations on the future relationship between the United Kingdom and the European Union have been and will likely continue to be complex and protracted. The United Kingdom will also negotiate its future trading relationship with other countries.

We have significant operations in the United Kingdom and other member countries of the European Union. The withdrawal by the United Kingdom and its future trading relationships could have an adverse effect on the tax, tax treaty, currency, operational, legal and regulatory regimes to which our businesses in the region are subject. The end of the transition period and the future trading relationship between the United Kingdom and European Union could also, among other potential outcomes, disrupt the free movement of goods, services and people between the United Kingdom and the European Union and significantly disrupt trade between the United Kingdom and the European Union and other parties. The uncertainty concerning the timing could also have a negative impact on the business activity, political stability and economic conditions in the United Kingdom, the European Union and the other economies in which we operate, which could result in customers reducing or delaying spending decisions on our products. Our United Kingdom business has deferred tax assets totaling $6.8 million. A downturn in our United Kingdom business caused by a material adverse effect could require us to record a valuation allowance against those deferred tax assets. Any of these developments could have a material adverse effect on our business, financial condition, operating results and cash flows.

We may be adversely affected by unanticipated changes in our tax provisions.

We are a U.S.-owned multinational company subject to income and other taxes in the U.S. and jurisdictions abroad. Tax laws are subject to change as new laws are passed and new interpretations of laws are issued or applied. Such changes in U.S. or foreign tax laws, regulations, other administrative guidance and common law interpretation could affect our tax expense and profitability as evidenced by the enactment of the Tax Cuts and Jobs Act on December 22, 2017. Further, the final determination of tax audits or litigation could ultimately be materially different from our historical income tax provisions and accruals. Changes in our tax provision and tax liabilities, whether due to changes in law, the interpretation, or a final determination of audits or litigation, could have a material adverse impact on our financial condition, operating results and cash flows.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

ITEM 2. PROPERTIES.

Our distribution network consists of 309 warehouses/branch locations in approximately 50 countries with approximately 9 million square feet of space. This includes 20 regional distribution centers (100,000 — 500,000 square feet), 44 local distribution centers (35,000 — 100,000 square feet), 187 service centers and 58 branch locations. Additionally, we have 71 sales offices throughout the world. All but five of these facilities are leased. No one facility is material to our overall operations, and we believe there is ample supply of alternative warehousing space available on similar terms and conditions in each of our markets.

ITEM 3. LEGAL PROCEEDINGS.

Incorporated by reference to Note 6. "Commitments and Contingencies" in the notes to the Consolidated Financial Statements of this AnnualCurrent Report on Form 10-K.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table lists the name, age as of February 20, 2020, position, offices and certain other information with respect to our executive officers. The term of office of each executive officer will expire upon the appointment of his successor by the Board of Directors.

| | | | | | | | | | | | | | |

William A. Galvin, 57 | | President and Chief Executive Officer since July 2018; President and Chief Operating Officer from July 2017 to June 2018; Executive Vice President - Network & Security Solutions of the Company from 2012 to June 2017; Executive Vice President - North America and EMEA Enterprise Cabling and Security Solutions from 2007 to 2012. Mr. Galvin has held several sales and marketing management roles over his 30 years of experience with the Company. | | |

| | | | |

Theodore A. Dosch, 60 | | Executive Vice President - Finance and Chief Financial Officer of the Company since July 2011; Senior Vice President - Global Finance of the Company from January 2009 to June 2011; CFO - North America and Vice President - Maytag Integration at Whirlpool Corporation from 2006 to 2008; Corporate Controller at Whirlpool Corporation from 2004 to 2006; CFO - North America at Whirlpool Corporation from 1999 to 2004. Mr. Dosch has also been a Director of UGI Corporation since 2017. | | |

| | | | |

Justin C. Choi, 54 | | Executive Vice President - General Counsel & Corporate Secretary of the Company since May 2013; Vice President - General Counsel & Corporate Secretary of the Company from June 2012 to May 2013; Executive Vice President, General Counsel and Secretary -Trustwave Holdings from January 2011 to June 2012; Senior Vice President, General Counsel & Secretary - Andrew Corporation from March 2006 to December 2007; Vice President of Law - Avaya Inc. from September 2000 to February 2006. | | |

| | | | |

William C. Geary II, 49 | | Executive Vice President - Network & Security Solutions of the Company since July 2017; Senior Vice President - Global Markets - Network & Security Solutions from January 2017 to June 2017. Before moving to Anixter, Mr. Geary served 22 years and held a variety of senior management roles at the U.S. based communications distributor Accu-Tech. | | |

| | | | |

Robert M. Graham, 52 | | Executive Vice President - Electrical & Electronic Solutions of the Company since July 2015; Senior Vice President - U.S. Electrical and Electronic Wire and Cable from 2011 to 2015. Mr. Graham came to Anixter with the acquisition of the Pentacon business in September 2002, and since then, he has held various senior leadership roles for Anixter’s former OEM Fastener business with his most recent position before joining the Wire & Cable division being Senior Vice President for the North American business. | | |

| | | | |

Steve M. Dean, 50 | | Executive Vice President - Utility Power Solutions since January 2020; Senior Vice President - Sales, Utility Power Solutions from July 2019 to January 2020; Senior Vice President - Sales, Public Power, Utility Power Solutions from October 2018 to July 2019; Senior Vice President - Global EPC and Capital Projects, Electrical & Electronic Solutions from January 2017 to October 2018; Senior Vice President - Strategic Sales Solutions, Electrical & Electronic Solution from March 2016 to January 2017; Vice President - Industrial Automation, Wire & Cable division from May 2011 to March 2016. Mr. Dean held various roles in business development and marketing since joining the Company in 1999. | | |

| | | | |

Scott Ramsbottom, 46 | | Executive Vice President - Chief Information Officer since February 2015; Senior Vice President Global Information Services from February 2014 to February 2015. Mr. Ramsbottom held various roles in the information services group since joining the Company in 1999. | | |

| | | | |

Rodney A. Smith, 62 | | Executive Vice President - Human Resources of the Company since May 2013; Vice President - Human Resources from August 2006 to May 2013. Prior to Anixter, Mr. Smith was the Vice President of Human Resources at UOP, LLC, and also held various human resources roles with Union Carbide and Exxon Corporation. | | |

| | | | |

Orlando McGee, 58 | | Executive Vice President - Operations of the Company since January 2018; Senior Vice President - Strategic and EMEA Operations from August 2017 to January 2018; Senior Vice President - Strategic Operations from June 2016 to August 2017. Prior to joining the Company, Mr. McGee served in a number of management positions at Cintas Corporation from 2012 to 2016, most recently as Vice President Distribution & Logistics. | | |

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Anixter International Inc.’s Common Stock is traded on the New York Stock Exchange under the symbol AXE. Shareholders of record are set forth in Note 12. "Selected Quarterly Financial Data (Unaudited)" in the Notes to the Consolidated Financial Statements. There have been no sales of unregistered securities.

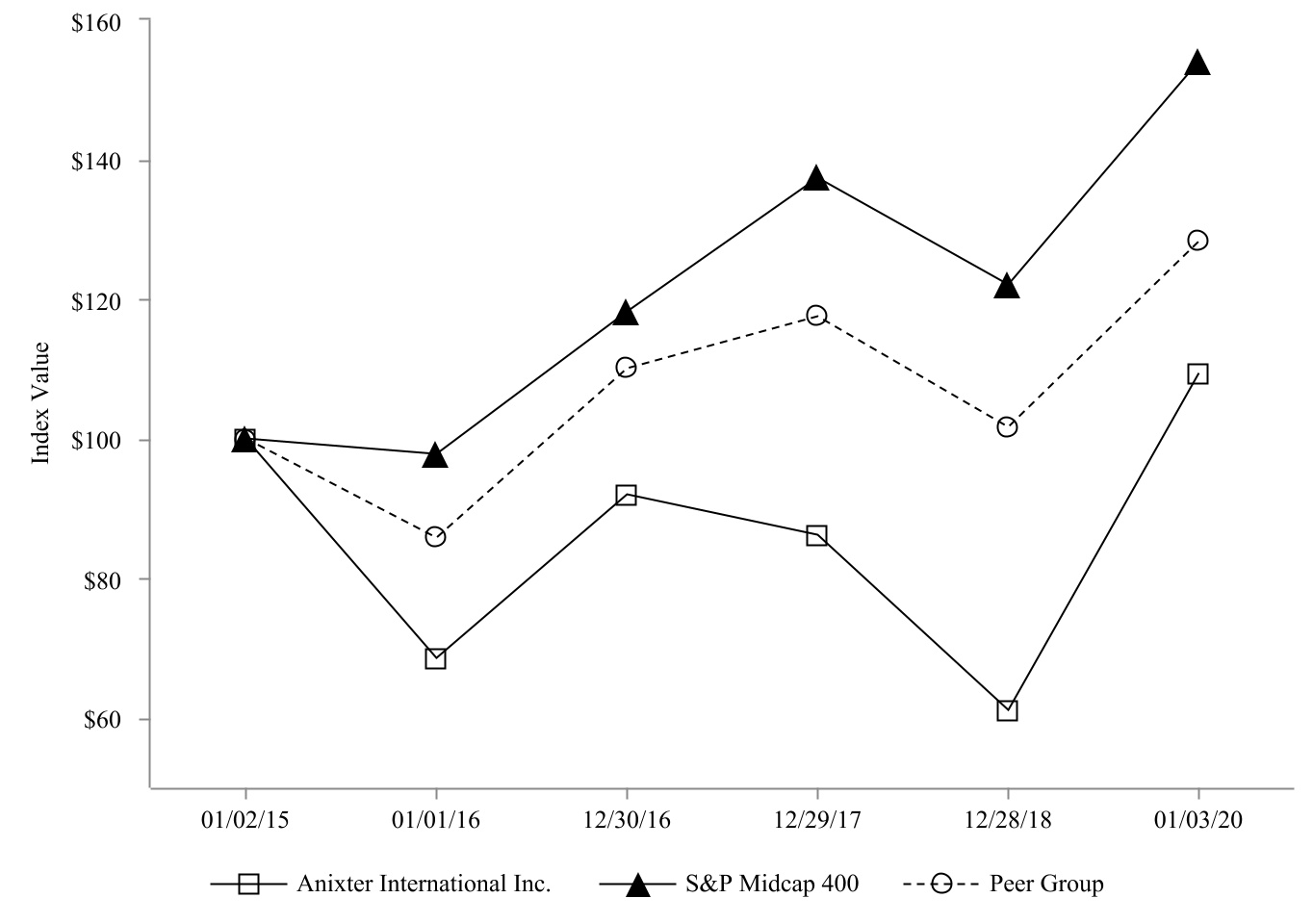

PERFORMANCE GRAPH

The following graphs set forth the annual changes for the five-year period indicated in a theoretical cumulative total shareholder return of an investment of $100 in our common stock and each comparison index, assuming reinvestment of dividends. These graphs reflect the comparison of shareholder return on our common stock with that of a broad market index and a peer group index. Our Peer Group Index for 2019 consists of the following companies: Arrow Electronics Inc., Avnet Inc., Belden Inc., CommScope Inc., Fastenal Company, MRC Global, MSC Industrial Direct Co. Inc., Rexel, Scansource Inc., Watsco, Inc., WESCO International, Inc., and W.W. Grainger Inc. This peer group was selected based on a review of publicly available information about these companies and our determination that they are engaged in businesses similar to ours.

ITEM 6. SELECTED FINANCIAL DATA.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In millions, except per share amounts) | | Fiscal Year | | | | | | | | |

| | | 2019 | | 2018 | | 2017 | | 2016 | | 2015 |

| Selected Income Statement Data: | | | | | | | | | | |

| Net sales | | $ | 8,845.6 | | | $ | 8,400.2 | | | $ | 7,927.4 | | | $ | 7,622.8 | | | $ | 6,190.5 | |

| Operating income | | 367.5 | | | 309.7 | | | 312.9 | | | 295.5 | | | 267.1 | |

Interest expense and other, net (a) | | (74.1) | | | (86.5) | | | (75.3) | | | (98.0) | | | (84.2) | |

| Net income from continuing operations | | 262.9 | | | 156.3 | | | 109.0 | | | 121.1 | | | 96.9 | |

| Net (loss) income from discontinued operations | | — | | | — | | | — | | | (0.6) | | | 30.7 | |

| Net income | | $ | 262.9 | | | $ | 156.3 | | | $ | 109.0 | | | $ | 120.5 | | | $ | 127.6 | |

| Diluted Income (Loss) Per Share: | | | | | | | | | | |

| Continuing operations | | $ | 7.67 | | | $ | 4.58 | | | $ | 3.21 | | | $ | 3.61 | | | $ | 2.90 | |

| Discontinued operations | | $ | — | | | $ | — | | | $ | — | | | $ | (0.02) | | | $ | 0.91 | |

| Net income | | $ | 7.67 | | | $ | 4.58 | | | $ | 3.21 | | | $ | 3.59 | | | $ | 3.81 | |

| Dividend declared per common share | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

| Selected Balance Sheet Data: | | | | | | | | | | |

| Total assets | | $ | 4,808.9 | | | $ | 4,653.1 | | | $ | 4,252.2 | | | $ | 4,093.6 | | | $ | 4,142.0 | |

| Total long-term debt | | $ | 1,059.7 | | | $ | 1,252.7 | | | $ | 1,247.9 | | | $ | 1,378.8 | | | $ | 1,642.9 | |

| Stockholders’ equity | | $ | 1,860.9 | | | $ | 1,570.4 | | | $ | 1,459.0 | | | $ | 1,292.2 | | | $ | 1,179.4 | |

| Book value per diluted share | | $ | 54.25 | | | $ | 46.05 | | | $ | 42.95 | | | $ | 38.51 | | | $ | 35.26 | |

| Weighted-average diluted shares | | 34.3 | | | 34.1 | | | 34.0 | | | 33.6 | | | 33.4 | |

| Year-end outstanding shares | | 34.2 | | | 33.9 | | | 33.7 | | | 33.4 | | | 33.3 | |

| Other Financial Data: | | | | | | | | | | |

| Working capital | | $ | 1,544.4 | | | $ | 1,543.0 | | | $ | 1,483.0 | | | $ | 1,424.6 | | | $ | 1,571.6 | |

| Capital expenditures | | $ | 40.0 | | | $ | 42.4 | | | $ | 41.1 | | | $ | 32.6 | | | $ | 26.7 | |

| Depreciation | | $ | 37.2 | | | $ | 31.7 | | | $ | 28.2 | | | $ | 27.9 | | | $ | 22.2 | |

| Amortization of intangible assets | | $ | 35.0 | | | $ | 37.3 | | | $ | 36.1 | | | $ | 37.6 | | | $ | 24.9 | |

(a) Interest expense and other, net in 2018 includes $4.6 million of loss on the extinguishment of debt on the retirement of our $350.0 million 5.625% Senior Notes due 2019.

Items Impacting Comparability of Results

Over the last five years, we have completed two material acquisitions and the respective sales and operating income have impacted the comparability of the results as reflected below. The acquisitions were accounted for as purchases and the results of operations of the acquired businesses are included in the Consolidated Financial Statements from the dates of acquisition. The following represents the incremental impact of the results for the one year period following the acquisitions:

| | | | | | | | | | | | | | |

| (In millions) | | Years Ended | | |

| | | December 30,

2016 | | January 1,

2016 |

| | (a) | | (a)(b) |

| Net sales | | $ | 1,501.9 | | | $ | 921.2 | |

| Operating income | | 43.3 | | | 29.3 | |

(a)October 2015 acquisition of Power Solutions for $829.4 million.

(b)September 2014 acquisition of Tri-Ed for $418.4 million.

In 2015, we sold our Fasteners business for $371.8 million in cash, resulting in a pre-tax gain of $40.3 million ($23.3 million, net of tax). As a result of this divestiture, results of this business are reflected as "Discontinued operations".

The following reflects various items that impact the comparability of the results for the last five fiscal years:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Items Impacting Comparability of Results from Continuing Operations: | | | | | | | | | | |

| (In millions, except per share amounts) | | Years Ended | | | | | | | | |

| | January 3,

2020 | | December 28,

2018 | | December 29,

2017 | | December 30,

2016 | | January 1,

2016 |

| Items impacting operating expense and operating income: | | Favorable / (Unfavorable) | | | | | | | | |

| Amortization of intangible assets | | $ | (35.0) | | | $ | (37.3) | | | $ | (36.1) | | | $ | (37.6) | | | $ | (24.9) | |

| Merger costs | | (12.8) | | | — | | | — | | | — | | | — | |

| Restructuring charge | | — | | | (9.4) | | | — | | | (5.4) | | | (8.2) | |

| Acquisition and integration costs | | 0.3 | | | (2.9) | | | (2.3) | | | (5.1) | | | (13.2) | |

| CEO retirement agreement expense | | — | | | (2.6) | | | — | | | — | | | — | |

| U.K. facility relocation costs | | — | | | (1.0) | | | — | | | — | | | — | |

| Impairment of intangible assets | | — | | | — | | | (5.7) | | | — | | | — | |

| U.K. pension settlement | | — | | | — | | | — | | | (9.6) | | | (0.4) | |

| Latin America bad debt provision | | — | | | — | | | — | | | (7.6) | | | (11.7) | |

| Write-off of capitalized software | | — | | | — | | | — | | | — | | | (3.1) | |

| Dilapidation provision | | — | | | — | | | — | | | — | | | (1.7) | |

| Total of items impacting operating expense and operating income | | $ | (47.5) | | | $ | (53.2) | | | $ | (44.1) | | | $ | (65.3) | | | $ | (63.2) | |

| Items impacting interest expense: | | | | | | | | | | |

| Write-off of deferred financing costs | | — | | | — | | | — | | | — | | | (0.3) | |

| Total of items impacting interest expense | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | (0.3) | |

| Items impacting other expenses: | | | | | | | | | | |

| Loss on extinguishment of debt | | — | | | (4.6) | | | — | | | — | | | (0.9) | |

| Foreign exchange loss | | — | | | — | | | — | | | — | | | (3.6) | |

| Total of items impacting other expenses | | $ | — | | | $ | (4.6) | | | $ | — | | | $ | — | | | $ | (4.5) | |

| Total of items impacting pre-tax income | | $ | (47.5) | | | $ | (57.8) | | | $ | (44.1) | | | $ | (65.3) | | | $ | (68.0) | |

| Items impacting income taxes: | | | | | | | | | | |

| Tax impact of items above impacting pre-tax income | | 8.8 | | | 12.6 | | | 14.8 | | | 18.8 | | | 27.4 | |

| Transition tax on deferred foreign income | | — | | | 2.8 | | | (50.0) | | | — | | | — | |

| Rate change impact of net deferred tax liability | | — | | | (0.7) | | | 14.4 | | | — | | | — | |

| Reversal/(establishment) of deferred income tax valuation allowances | | 45.9 | | | 1.4 | | | — | | | (1.1) | | | (11.3) | |

| Tax expense related to domestic permanent tax differences | | — | | | (0.7) | | | — | | | — | | | — | |

| Tax (expense) benefit related to prior year tax positions | | (0.8) | | | (0.1) | | | (1.3) | | | 3.2 | | | — | |

| Other tax items | | — | | | — | | | — | | | — | | | (0.5) | |

| Total of items impacting income taxes | | $ | 53.9 | | | $ | 15.3 | | | $ | (22.1) | | | $ | 20.9 | | | $ | 15.6 | |

| Net income impact of these items | | $ | 6.4 | | | $ | (42.5) | | | $ | (66.2) | | | $ | (44.4) | | | $ | (52.4) | |

| Diluted EPS impact of these items | | $ | 0.19 | | | $ | (1.25) | | | $ | (1.95) | | | $ | (1.32) | | | $ | (1.56) | |

The following table presents a reconciliation from net income from continuing operations to EBITDA and Adjusted EBITDA:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Fiscal Year | | | | | | | | |

| (In millions) | | 2019 | | 2018 | | 2017 | | 2016 | | 2015 |

| Net income from continuing operations | | $ | 262.9 | | | $ | 156.3 | | | $ | 109.0 | | | $ | 121.1 | | | $ | 96.9 | |

| Interest expense | | 77.1 | | | 76.3 | | | 74.7 | | | 78.7 | | | 63.8 | |

| Income taxes | | 30.5 | | | 66.9 | | | 128.6 | | | 76.4 | | | 86.0 | |

| Depreciation | | 37.2 | | | 31.7 | | | 28.2 | | | 27.9 | | | 22.2 | |

| Amortization of intangible assets | | 35.0 | | | 37.3 | | | 36.1 | | | 37.6 | | | 24.9 | |

| EBITDA | | $ | 442.7 | | | $ | 368.5 | | | $ | 376.6 | | | $ | 341.7 | | | $ | 293.8 | |

Total of items impacting operating income (a) | | 12.5 | | | 13.3 | | | 8.0 | | | 27.7 | | | 38.3 | |

| Foreign exchange and other non-operating (income) expense | | (3.0) | | | 10.2 | | | 0.6 | | | 19.3 | | | 20.4 | |

| Stock-based compensation | | 20.0 | | | 18.9 | | | 18.1 | | | 16.5 | | | 13.9 | |

| Adjusted EBITDA | | $ | 472.2 | | | $ | 410.9 | | | $ | 403.3 | | | $ | 405.2 | | | $ | 366.4 | |

(a) Items impacting operating income excludes amortization of intangible assets and CEO retirement agreement expense in the calculation of adjusted EBITDA as amortization is already added back in the EBITDA calculation and CEO retirement agreement expense is added back as part of stock-based compensation.

ANIXTER INTERNATIONAL INC.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

Executive Overview

Total company sales increased 5.3% to $8,845.6 million in 2019. Excluding the unfavorable impacts from foreign exchange and copper and the favorable impact from acquisitions, we delivered organic sales growth of 5.6%, as summarized in the table below. The current year had 257 billing days compared to 253 billing days in the prior year period. However, due to the timing of holidays, it is estimated that there were 2 1/2 more effective selling days in 2019 compared to 2018. Excluding the favorable impact from these extra selling days, adjusted daily sales increased 4.6%. Additional highlights of the year included:

•$227.9 million of cash flow from operations; and

•Earnings per diluted share of $7.67.

Organic sales growth from 2018 to 2019 excludes the impact of the following items and is summarized by segment and geography below:

•$64.3 million unfavorable impact from the fluctuation in foreign exchange;

•$15.1 million unfavorable impact from the lower average price of copper; and

•$48.4 million favorable impact from acquisitions.

Adjusted daily sales growth further excludes the favorable impact from 2 1/2 more effective selling days in 2019.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales Growth Trends | | | | | | | | | | | | | | | | | | | | | | |

| | Twelve Months Ended January 3, 2020 | | | | | | | | Twelve Months Ended December 28, 2018 | | | | | | Growth/(Decline) | | | | | | |

| ($ millions) | | As Reported | | Foreign Exchange Impact | | Copper Impact | | As Adjusted | | As Reported | | Acquisitions Impact | | Adjusted for Acquisitions | | | | | | Adjusted 2018 for Effective Selling Days | | Adjusted Daily Sales |

| | | | | | | | | | | | | | | | Actual | | Organic | | | | |

| Network & Security Solutions (NSS) | | | | | | | | | | | | | | | | | | | | | | |

| North America | | $ | 3,484.6 | | | $ | 9.1 | | | $ | — | | | $ | 3,493.7 | | | $ | 3,295.4 | | | $ | — | | | $ | 3,295.4 | | | 5.7 | % | | 6.0 | % | | $ | 3,327.9 | | | 5.0 | % |

| EMEA | | 387.3 | | | 15.3 | | | — | | | 402.6 | | | 403.3 | | | 1.7 | | | 405.0 | | | (4.0) | % | | (0.6) | % | | 409.0 | | | (1.6) | % |

| Emerging Markets | | 824.3 | | | 16.3 | | | — | | | 840.6 | | | 648.3 | | | 46.7 | | | 695.0 | | | 27.2 | % | | 21.0 | % | | 701.8 | | | 19.8 | % |

| NSS | | $ | 4,696.2 | | | $ | 40.7 | | | $ | — | | | $ | 4,736.9 | | | $ | 4,347.0 | | | $ | 48.4 | | | $ | 4,395.4 | | | 8.0 | % | | 7.8 | % | | $ | 4,438.7 | | | 6.7 | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Electrical & Electronic Solutions (EES) | | | | | | | | | | | | | | | | | | | | | | | | |

| North America | | $ | 1,870.6 | | | $ | 7.3 | | | $ | 11.2 | | | $ | 1,889.1 | | | $ | 1,836.2 | | | $ | — | | | $ | 1,836.2 | | | 1.9 | % | | 2.9 | % | | $ | 1,854.5 | | | 1.9 | % |

| EMEA | | 238.2 | | | 10.3 | | | 1.3 | | | 249.8 | | | 257.0 | | | — | | | 257.0 | | | (7.3) | % | | (2.8) | % | | 259.5 | | | (3.8) | % |

| Emerging Markets | | 243.2 | | | 1.6 | | | 2.1 | | | 246.9 | | | 249.5 | | | — | | | 249.5 | | | (2.6) | % | | (1.1) | % | | 252.0 | | | (2.0) | % |

| EES | | $ | 2,352.0 | | | $ | 19.2 | | | $ | 14.6 | | | $ | 2,385.8 | | | $ | 2,342.7 | | | $ | — | | | $ | 2,342.7 | | | 0.4 | % | | 1.8 | % | | $ | 2,366.0 | | | 0.8 | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Utility Power Solutions (UPS) | | | | | | | | | | | | | | | | | | | | | | | | |

| North America | | $ | 1,797.4 | | | $ | 4.4 | | | $ | 0.5 | | | $ | 1,802.3 | | | $ | 1,710.5 | | | $ | — | | | $ | 1,710.5 | | | 5.1 | % | | 5.4 | % | | $ | 1,727.5 | | | 4.3 | % |

| UPS | | $ | 1,797.4 | | | $ | 4.4 | | | $ | 0.5 | | | $ | 1,802.3 | | | $ | 1,710.5 | | | $ | — | | | $ | 1,710.5 | | | 5.1 | % | | 5.4 | % | | $ | 1,727.5 | | | 4.3 | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Total | | $ | 8,845.6 | | | $ | 64.3 | | | $ | 15.1 | | | $ | 8,925.0 | | | $ | 8,400.2 | | | $ | 48.4 | | | $ | 8,448.6 | | | 5.3 | % | | 5.6 | % | | $ | 8,532.2 | | | 4.6 | % |

| | | | | | | | | | | | | | | | | | | | | | | |

| Geographic Sales | | | | | | | | | | | | | | | | | | | | | | | |

| North America | | $ | 7,152.6 | | | $ | 20.8 | | | $ | 11.7 | | | $ | 7,185.1 | | | $ | 6,842.1 | | | $ | — | | | $ | 6,842.1 | | | 4.5 | % | | 5.0 | % | | $ | 6,909.9 | | | 4.0 | % |

| EMEA | | 625.5 | | | 25.6 | | | 1.3 | | | 652.4 | | | 660.3 | | | 1.7 | | | 662.0 | | | (5.3) | % | | (1.5) | % | | 668.5 | | | (2.4) | % |

| Emerging Markets | | 1,067.5 | | | 17.9 | | | 2.1 | | | 1,087.5 | | | 897.8 | | | 46.7 | | | 944.5 | | | 18.9 | % | | 15.2 | % | | 953.8 | | | 14.0 | % |

| Total | | $ | 8,845.6 | | | $ | 64.3 | | | $ | 15.1 | | | $ | 8,925.0 | | | $ | 8,400.2 | | | $ | 48.4 | | | $ | 8,448.6 | | | 5.3 | % | | 5.6 | % | | $ | 8,532.2 | | | 4.6 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Note: There were 257 billing days in 2019 compared to 253 billing days in 2018. However, due to the timing of holidays, it is estimated that there were 2 1/2 more effective selling days in 2019 compared to 2018, resulting in 255 1/2 and 253 effective selling days in 2019 and 2018, respectively. | | | | | | | | | | | | | | | | | | | | | | |

ANIXTER INTERNATIONAL INC.

As we enter 2020, we remain focused on delivering strong organic growth, continued gross margin improvement and strong expense discipline. We are also beginning to benefit from our movement to a U.S.-center-led business model where we drive strategies to achieve global network synergies. We continue to see generally positive sales trends in the business, based on our solid backlog and pipeline, and discussions with our customers and suppliers. Overall we expect full year 2020 organic sales growth in the 1 - 5% range.

Acquisition of Businesses

During the second quarter of 2018, we completed the acquisition of security businesses in Australia and New Zealand. These acquisitions have been accretive to earnings in the first full year of operation, exclusive of transaction and integration costs.

Consolidated Results of Operations

| | | | | | | | | | | | | | | | | | | | |

| (In millions, except per share amounts) | | Years Ended | | | | |

| | | January 3,

2020 | | December 28,

2018 | | December 29,

2017 |

| Net sales | | $ | 8,845.6 | | | $ | 8,400.2 | | | $ | 7,927.4 | |

| Gross profit | | 1,775.8 | | | 1,658.0 | | | 1,571.0 | |

| Operating expenses | | 1,408.3 | | | 1,348.3 | | | 1,258.1 | |

| Operating income | | 367.5 | | | 309.7 | | | 312.9 | |

| Other expense: | | | | | | |

| Interest expense | | (77.1) | | | (76.3) | | | (74.7) | |

| Other, net | | 3.0 | | | (10.2) | | | (0.6) | |

| Income before income taxes | | 293.4 | | | 223.2 | | | 237.6 | |

| Income tax expense | | 30.5 | | | 66.9 | | | 128.6 | |

| Net income | | $ | 262.9 | | | $ | 156.3 | | | $ | 109.0 | |

| Diluted income per share | | $ | 7.67 | | | $ | 4.58 | | | $ | 3.21 | |

ANIXTER INTERNATIONAL INC.

Items Impacting Comparability of Results

In addition to the results provided in accordance with U.S. Generally Accepted Accounting Principles ("U.S. GAAP") above, this report includes certain non-GAAP financial measures as defined by the Securities and Exchange Commission. Specifically, net sales comparisons to the prior corresponding period, both worldwide and in relevant segments, are discussed in this report both on a U.S. GAAP and non-GAAP basis. We believe that by providing non-GAAP organic growth, which adjusts for the impact of acquisitions (when applicable), foreign exchange fluctuations, copper prices and the number of billing days, both management and investors are provided with meaningful supplemental sales information to understand and analyze our underlying trends and other aspects of our financial performance. We calculate the year-over-year organic sales growth impact related to acquisitions by including their comparable period results prior to the acquisitions with our results, as we believe this represents the most accurate representation of organic growth, considering the nature of the companies we acquired and the synergistic revenues that have been or will be achieved. Historically, and from time to time, we may also exclude other items from reported financial results (e.g., impairment charges, inventory adjustments, restructuring charges, tax items, currency devaluations, pension settlements, etc.) in presenting adjusted operating expense, adjusted operating income, adjusted income taxes and adjusted net income so that both management and financial statement users can use these non-GAAP financial measures to better understand and evaluate our performance period over period and to analyze the underlying trends of our business. We have also excluded amortization of intangible assets associated with purchase accounting from acquisitions from the adjusted amounts for comparison of the non-GAAP financial measures period over period.

EBITDA is defined as net income from continuing operations before interest, income taxes, depreciation and amortization. Adjusted EBITDA is defined as EBITDA before foreign exchange and other non-operating expense and non-cash stock-based compensation, excluding the other items from reported financial results, as defined above. We believe that adjusted operating income, EBITDA and Adjusted EBITDA provide relevant and useful information, which is widely used by analysts, investors and competitors in our industry as well as by our management in assessing both consolidated and business segment performance. Adjusted operating income provides an understanding of the results from the primary operations of our business by excluding the effects of certain items that do not reflect the ordinary earnings of our operations. We use adjusted operating income to evaluate our period over period operating performance because we believe this provides a more comparable measure of our continuing business excluding certain items that are not reflective of expected ongoing operations. This measure may be useful to an investor in evaluating the underlying performance of our business. EBITDA provides us with an understanding of earnings before the impact of investing and financing charges and income taxes. Adjusted EBITDA further excludes the effects of foreign exchange and other non-cash stock-based compensation, and certain items that do not reflect the ordinary earnings of our operations and that are also excluded for purposes of calculating adjusted net income, adjusted earnings per share and adjusted operating income. EBITDA and Adjusted EBITDA are used by our management for various purposes including as measures of performance of our operating entities and as a basis for strategic planning and forecasting. Adjusted EBITDA may be useful to an investor because this measure is widely used to evaluate a company’s operating performance without regard to items excluded from the calculation of such measure, which can vary substantially from company to company depending on the accounting methods, book value of assets, capital structure and the method by which the assets were acquired, among other factors. They are not, however, intended as an alternative measure of operating results or cash flow from operations as determined in accordance with U.S. GAAP.