0000070858us-gaap:ResidentialMortgageMemberus-gaap:ResidentialPortfolioSegmentMember2019-01-012019-12-310000070858bac:TradingAccountLiabilitiesEquitySecuritiesMember2019-01-012019-12-31PrincipalForgivenessMemberbac:CreditCardandOtherConsumerPortfolioSegmentMember2023-01-012023-12-310000070858us-gaap:ValuationTechniqueDiscountedCashFlowMembersrt:WeightedAverageMemberus-gaap:FairValueInputsLevel3Memberbac:MeasurementInputWeightedAverageLifeVariableRateMemberus-gaap:FairValueMeasurementsRecurringMember2023-01-012023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 20212023

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from to

Commission file number:

1-6523

Exact name of registrant as specified in its charter:

Bank of America Corporation

State or other jurisdiction of incorporation or organization:

Delaware

IRS Employer Identification No.:

56-0906609

Address of principal executive offices:

Bank of America Corporate Center

100 N. Tryon Street

Charlotte, North Carolina 28255

Registrant’s telephone number, including area code:

(704) 386-5681

Securities registered pursuant to section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | BAC | New York Stock Exchange |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrE | New York Stock Exchange |

| of Floating Rate Non-Cumulative Preferred Stock, Series E |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrB | New York Stock Exchange |

| of 6.000% Non-Cumulative Preferred Stock, Series GG |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrK | New York Stock Exchange |

| of 5.875% Non-Cumulative Preferred Stock, Series HH |

| 7.25% Non-Cumulative Perpetual Convertible Preferred Stock, Series L | BAC PrL | New York Stock Exchange |

| Depositary Shares, each representing a 1/1,200th interest in a share | BML PrG | New York Stock Exchange |

| of Bank of America Corporation Floating Rate |

| Non-Cumulative Preferred Stock, Series 1 |

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Depositary Shares, each representing a 1/1,200th interest in a share | BML PrH | New York Stock Exchange |

| of Bank of America Corporation Floating Rate |

| Non-Cumulative Preferred Stock, Series 2 |

| Depositary Shares, each representing a 1/1,200th interest in a share | BML PrJ | New York Stock Exchange |

| of Bank of America Corporation Floating Rate |

| Non-Cumulative Preferred Stock, Series 4 |

| Depositary Shares, each representing a 1/1,200th interest in a share | BML PrL | New York Stock Exchange |

| of Bank of America Corporation Floating Rate |

| Non-Cumulative Preferred Stock, Series 5 |

| Floating Rate Preferred Hybrid Income Term Securities of BAC Capital | BAC/PF | New York Stock Exchange |

| Trust XIII (and the guarantee related thereto) |

| 5.63% Fixed to Floating Rate Preferred Hybrid Income Term Securities | BAC/PG | New York Stock Exchange |

| of BAC Capital Trust XIV (and the guarantee related thereto) |

| Income Capital Obligation Notes initially due December 15, 2066 of | MER PrK | New York Stock Exchange |

| Bank of America Corporation |

| Senior Medium-Term Notes, Series A, Step Up Callable Notes, due | BAC/31B | New York Stock Exchange |

| November 28, 2031 of BofA Finance LLC (and the guarantee |

| of the Registrant with respect thereto) |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrM | New York Stock Exchange |

| of 5.375% Non-Cumulative Preferred Stock, Series KK |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrN | New York Stock Exchange |

| of 5.000% Non-Cumulative Preferred Stock, Series LL |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrO | New York Stock Exchange |

| of 4.375% Non-Cumulative Preferred Stock, Series NN |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrP | New York Stock Exchange |

| of 4.125% Non-Cumulative Preferred Stock, Series PP |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrQ | New York Stock Exchange |

| of 4.250% Non-Cumulative Preferred Stock, Series QQ |

| Depositary Shares, each representing a 1/1,000th interest in a share | BAC PrS | New York Stock Exchange |

| of 4.750% Non-Cumulative Preferred Stock, Series SS |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑☐ No ☐☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | | Accelerated filer | ☐ | | Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

As of June 30, 2021,2023, the aggregate market value of the registrant’s common stock (“Common Stock”)(Common Stock) held by non-affiliates was approximately $349,925,254,902.$228,187,725,798. At February 18, 2022,16, 2024, there were 8,069,801,3017,872,657,542 shares of Common Stock outstanding.

Documents incorporated by reference: Portions of the definitive proxy statement relating to the registrant’s 20222024 annual meeting of shareholders are incorporated by reference in this Form 10-K in response to Items 10, 11, 12, 13 and 14 of Part III.

Table of Contents

Bank of America Corporation and Subsidiaries

Part I

Bank of America Corporation and Subsidiaries

Item 1. Business

Bank of America Corporation is a Delaware corporation, a bank holding company (BHC) and a financial holding company. When used in this report, “Bank of America,” “the Corporation,” “we,” “us” and “our” may refer to Bank of America Corporation individually, Bank of America Corporation and its subsidiaries, or certain of Bank of America Corporation’s subsidiaries or affiliates. As part of our efforts to streamline the Corporation’s organizational structure and reduce complexity and costs, the Corporation has reduced and intends to continue to reduce the number of its corporate subsidiaries, including through intercompany mergers.

Bank of America is one of the world’s largest financial institutions, serving individual consumers, small- and middle-market businesses, institutional investors, large corporations and governments with a full range of banking, investing, asset management and other financial and risk management products and services. Our principal executive offices are located in the Bank of America Corporate Center, 100 North Tryon Street, Charlotte, North Carolina 28255.

Bank of America’s website is www.bankofamerica.com, and the Investor Relations portion of our website is http:https://investor.bankofamerica.com. We use our website to distribute company information, including as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. We routinely post and make accessible financial and other information, including environmental, social and governance (ESG) information, regarding the Corporation on our website. Investors should monitor our website, including the Investor Relations portion of our website, in addition to our press releases, U.S. Securities and Exchange Commission (SEC) filings, public conference calls and webcasts. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (Exchange Act) are available on the Investor Relations portion of our website as soon as reasonably practicable after we electronically file such reports with, or furnish them to, the SEC and at the SEC’s website, www.sec.gov. Notwithstanding the foregoing, the information contained on our website as referenced in this paragraph, or otherwise in this Annual Report on Form 10-K, is not incorporated by reference into this Annual Report on Form 10-K. Also, we make available on the Investor Relations portion of our website: (i) our Code of Conduct; (ii) our Corporate Governance Guidelines; and (iii) the charter of each active committee of our Board of Directors (the Board). Our Code of Conduct constitutes a “code of ethics” and a “code of business conduct and ethics” that applies to the required individuals associated with the Corporation for purposes of the respective rules of the SEC and the New York Stock Exchange. We also intend to disclose any amendments to our Code of Conduct and waivers of our Code of Conduct required to be disclosed by the rules of the SEC and the New York Stock Exchange on the Investor Relations portion of our website. All of these corporate governance materials are also available free of charge in print to shareholders who request them in writing to: Bank of America Corporation, Attention: Office of the Corporate Secretary, Bank of America Corporate Center, 100 North Tryon Street, NC1-007-56-06, Charlotte, North Carolina 28255.

Segments

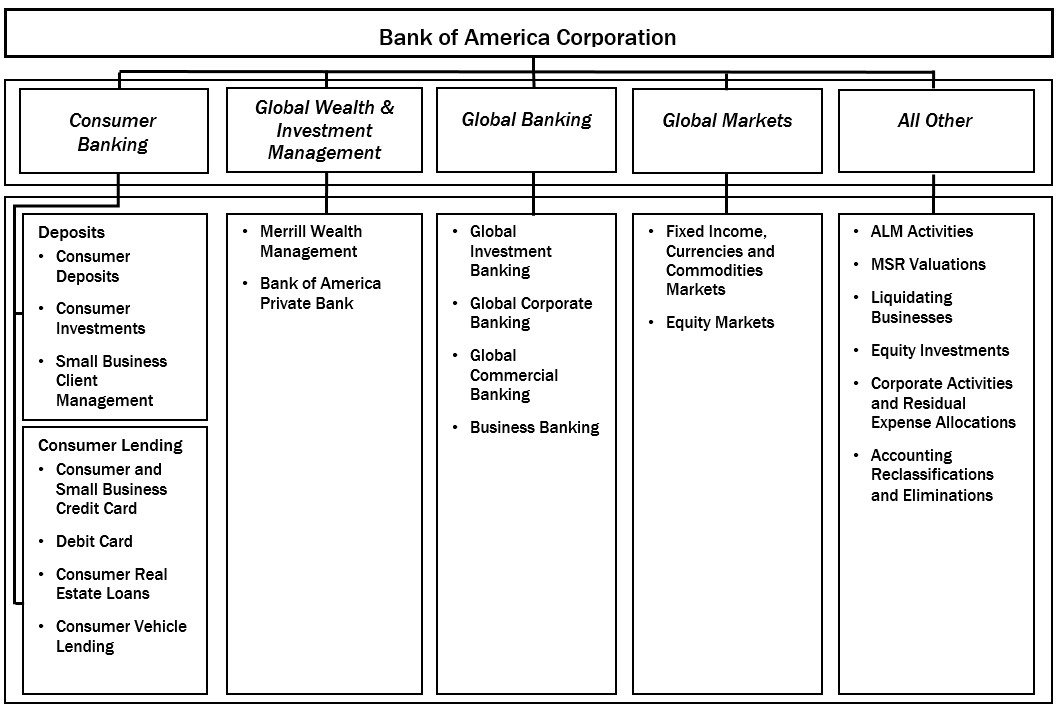

Through our various bank and nonbank subsidiaries throughout the U.S. and in international markets, we provide a diversified range of banking and nonbank financial services and products through four business segments: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking and Global Markets, with the remaining operations recorded in All Other. Additional information related to our business segments and the products and services they provide is included in the information set forth on pages 3634 through 4643 of Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) and Note 23 – Business Segment Information to the Consolidated Financial Statements.

Competition

We operate in a highly competitive environment. Our competitors include banks, thrifts, credit unions, investment banking firms, investment advisory firms, brokerage firms, investment companies, insurance companies, mortgage banking companies, credit card issuers, mutual fund companies, hedge funds, private equity firms, and e-commerce and other internet-based companies.companies, including merchant banks and companies providing nonbank financial services. We compete with some of these competitors globally and with others on a regional or product-specific basis. We are increasingly competing with firms offering products solely over the internet and with nonfinancial companies, including firms utilizing emerging technologies, such as digital assets, rather than, or in addition to, traditional banking products.

Competition is based on a number of factors including, among others, customer service and convenience, the pricing, quality and range of products and services offered, technology, price, fees, reputation, interest rates on loans and deposits, lending limits, customer conveniencethe quality and delivery of our technology and our reputation, experience and relationships in relevant markets. Our ability to continue to compete effectively also depends in large part on our ability to attract new employees and develop, retain and motivate our existing employees, while managing compensation and other costs.

Human Capital Resources

We strive to make Bank of America a great place to work for our employees. We value our employees and seek to establish and maintain human resource policies that are consistent with our core values and that help to realize the power of our people. Our Board and its Compensation and Human Capital Committee provide oversight of our human capital management strategies, programs, initiatives and practices. The Corporation’s senior management provides regular briefings on human capital matters to the Board and its Committees to facilitate the Board’s oversight.

At December 31, 20212023 and 2020,2022, the Corporation employed approximately 208,000213,000 and 213,000217,000 employees, of which 8078 percent and 8279 percent were located in the U.S., respectively. None of our U.S. employees are subject to a collective bargaining agreement. Additionally, in 20212023 and 2020,2022, the Corporation’s compensation and benefits expense was $36.1$38.3 billion and $32.7$36.4 billion, or 6158 percent and 59 percent, of total noninterest expense.

Diversity and Inclusion

The Corporation’s commitment to diversity and inclusion starts at the top with oversight from our Board and CEO.Chief Executive Officer (CEO). The Corporation’s senior management sets the diversity and inclusion goals, and the Chief Human Resources Officer and Chief Diversity & Inclusion Officer partner with our CEO and senior management to drive our diversity and inclusion strategy, programs, initiatives and policies. TheOur Global Diversity and Inclusion Council, which has been in place for over 20 years, is chaired by our CEO and consists of senior executives from every line of business and region, is chaired by our CEO and has

been in place for over 20 years.region. The Council sponsors and supports business, operating unit and regional diversity and inclusion councils to ensure alignment with enterprisealign diversity and inclusion strategies and goals.aspirational goals across the enterprise.

Our practices and policies have resulted in strong representation across the Corporation where our broad employee population mirrors the clients and communities we serve. We have aOur Board and senior management team that are 5062 percent and 55 percent racially, ethnically and gender diverse. As of December 31, 2021, ofThe following table presents diversity metrics for our global employees who self-identified 50 percent of employees wereas women and amongour U.S.-based employees who self-identified 49 percent wereas people of color, including 13 percentthose who wereself-identified as Asian, 14 percent who were Black/African American and 19 percent who were Hispanic/Latino. As of December 31, 2021, the Corporation’s top three management levels in relation to the CEO were composed of more than 42 percent women globally and 24 percent people of color in the U.S., including eight percent who were Asian, nine percent who were Black/African American and six percent who were Hispanic/Latino. Additionally, as of December 31, 2021, the Corporation’s managers at all levels were composed of 42 percent women globally and 41 percent people of color in the U.S., including 13 percent who were Asian, 10 percent who were Black/African American and 16 percent who were Hispanic/Latino. These workforce diversity metrics are reported regularly to the senior management team and to the Board.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Diversity Metrics as of December 31, 2023 |

| | | | | | |

| Total Employees | | Top Three Management Levels | | Managers at All Levels |

| Global employees | | | | | |

| Women | 50 | % | | 41 | % | | 42 | % |

| U.S.-based employees | | | | | |

| People of color | 51 | | | 27 | | | 43 | |

| Asian | 14 | | | 11 | | | 14 | |

| Black/African American | 15 | | | 8 | | | 10 | |

| Hispanic/Latino | 19 | | | 7 | | | 16 | |

We invest in our talent by offering a range of development programs and resources that are designed to allow all employees to develop and progress in their careers. We reinforce our commitment to diversity and inclusion by investing internally in our employee networks and by facilitating voluntary enterprise-wide learning and conversations about various diversity and inclusion topics and issues. Further,topics. In addition, we partner with various external organizations, which focus on advancing diverse talent. We also have practices in place for attracting and retaining diverse talent, including campus recruitment. For example, in 2021, 462023, 44 percent of our global campus hires were women and, in the U.S., 5362 percent were people of color.

Employee Engagement and Talent Retention

As part of our ongoing efforts to make the Corporation a great place to work, we have conductedconduct a confidential annual Employee Engagement Survey (Survey) and have done so for nearly two decades. The Survey results are reviewed by the Board and senior management and used to assist in reviewing the Corporation’s human capital strategies, programs, initiatives and practices. In 2021, 892023, 88 percent of the Corporation’s employees participated in the Survey, and our Employee Engagement Index, an overall measure of employee satisfaction with the Corporation, was 8887 percent. Our turnover among employees was 12eight percent in 20212023 and seven13 percent in 2020. Our pre-pandemic levels of turnover in 2019 and 2018 were 11 percent and 12 percent.2022.

Additionally, the Corporation provides a variety of resources to help employees grow in their current roles and build new skills, including resources to help employees find new opportunities, re-skill and seek leadership positions. The learning and development strategy is grounded in the

development of horizontal skills delivered throughout the organization. Senior leaders, managers and teammates are onboarded and build both horizontal skills, as well asand role-specific skills, to help drive high performance. This approach also facilitateshelps facilitate internal mobility and promotion of talent to build a bench of qualified managers and leaders. In 2021,2023, more than 26,0005,000 employees found new roles within the Corporation, and we

delivered more than 10approximately 6.7 million hours of training and development to our teammates through the Corporation’s training academy.Bank of America Academy. Additionally, our Board oversees CEO and senior management succession planning, which is formally reviewed at least annually.

Fair and Equitable Compensation

Our compensation philosophy is to pay for performance over the long term, as well as on an annual basis. Our performance considerations encompass both financial and nonfinancial measures, including the manner in which results are achieved. These considerations are designed to reinforce and promote our Responsible Growth strategy and maintain alignment with our Risk Framework.

The Corporation is committed to racial and gender pay equity by strivingand strives to compensate all of our employees fairly and equitably. We maintain robust policies and practices that reinforce our commitment, including reviews conducted by a third-party consultant with oversight from our Board and senior management. In 2021,2023, our review covered our regional hubs (U.S., U.K., France, Ireland, Hong Kong and Singapore) and India and showed that compensation received by women globally, on average, was greater than 99 percent of that received by men in comparable positions and, inpositions. In the U.S., compensation received by people of color was, on average, greater than 99 percent of that received by teammates who are not people of color in comparable positions.

We also strive to pay our employees fairly based on market rates for their roles, experience and how they perform. We regularly benchmark against other companies both within and outside our industry to help ensureconfirm our pay is competitive. In 2021, the fourth quarter of 2021, we raised ourCorporation announced it would increase its minimum hourly wage for U.S. employees to $21 per hour, which is above all governmental minimum wage levels in all jurisdictions in which we operate in the U.S., and announced plans to increase to $25 per hour by 2025. In October 2023, as a next step towards that goal, the Corporation increased its hourly minimum wage for U.S. employees to $23 per hour. In addition, in January 2024, for the seventh year since 2017, we announced that we recognized our teammates with Sharing Success compensation awards for their efforts during 2023. Approximately 97 percent of employees globally will receive an award in the first quarter of 2024.

Health and Wellness – 20212023 Focus

The Corporation is also is committed to supporting employees’providing employees with access to leading benefits and programs that help promote their physical, emotional and financial wellness by offering flexiblewellness. Investments we make in our teammates are designed to help them thrive, both at work and competitive benefits, including comprehensive healthat home, enabling them to better deliver for our clients, communities and insurance benefits and wellness resources. In 2021, we continued efforts to support our employees through the ongoing health crisis resulting from the Coronavirus Disease 2019 (COVID-19) pandemic (the pandemic). We continued to monitor guidance from the U.S. Centers for Disease Control and Prevention, medical boards and health authorities and prioritized sharing such guidance with our teammates. Other benefits and resources related to the pandemic included offering no-cost COVID-19 testing, paid time off to allow teammates to get vaccinated for COVID-19, providing teammates with incentives for getting the vaccine and booster, hosting a medical expert education series and providing on-site COVID-19 vaccine and booster clinics.each other.

We continued our efforts around providingto provide affordable access to healthcare, including offering no-cost, 24/7 access to virtual general medical and behavioral health resources to help our enrolled U.S. teammates stay healthy, both physically and emotionally.healthy. We kept U.S. health insurance premiums unchanged for teammates earning less than $50,000 for the nintheleventh year in a row and had nominal premium increases for teammates earning from $50,000 up to $100,000 for the fifthseventh year in a row. We also provided in-network generic prescription medications at no cost for teammates enrolled in a U.S. bank medical PPO or Consumer Direct plan, and we continue to provide preventative care medications at no cost for U.S.all teammates enrolled in the Bank’sU.S. medical plan.

plans. We have expanded our child and adult care solutions for eligible U.S. teammates to help better support their families and dependents, including providing up to 50 days of backup care for both adults and children and expanding access to our reimbursement program to help employees manage child care expenses. Additional support to working parents includes parental leave and time off from work to care for and bond with a newborn or adopted child (16 weeks paid plus 10 weeks unpaid for a total of up to 26 weeks).also

continued to enhance access to care across the Corporation, through near-site health centers, vaccination clinics and wellness screenings in many of our U.S. locations, as we believe primary and preventive care are important to our teammates’ health and safety.

We offer an extensive benefit package and support work-life balance for our teammates, which includes in the U.S., 16 weeks of paid parental leave for both primary and secondary caregivers and 50 days per year of child and adult backup dependent care. Globally, teammates and members of their households can utilize our Employee Assistance Program for 12 free, in-person confidential counseling sessions, and unlimited phone consultations. Beginning in 2023, teammates celebrating at least 15 years of continuous service with the Corporation may participate in its global Sabbatical Program.

For more information about our human capital management, see the Corporation’s website and 20212023 Annual Report to shareholders that willwe expect to be available on the Investor Relations portion of our website in March 20222024 (the content of which is not incorporated by reference into this Annual Report on Form 10-K).

Government Supervision and Regulation

The following discussion describes, among other things, elements of an extensive regulatory framework applicable to BHCs, financial holding companies, banks and broker-dealers, including specific information about Bank of America.

We are subject to an extensive regulatory framework applicable to BHCs, financial holding companies and banks and other financial services entities. U.S. federal regulation of banks, BHCs and financial holding companies is intended primarily for the protection of depositors and the Deposit Insurance Fund (DIF) rather than for the protection of shareholders and creditors.

As a registered financial holding company and BHC, the Corporation is subject to the supervision of, and regular inspection by, the Board of Governors of the Federal Reserve System (Federal Reserve). Our U.S. bank subsidiaries (the Banks), organized as national banking associations, are subject to regulation, supervision and examination by the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve. In addition, the Federal Reserve and the OCC have adopted guidelines that establish minimum standards for the design, implementation and board oversight of BHCs’ and national banks’ risk governance frameworks. U.S. financial holding companies, and the companies under their control, are permitted to engage in activities considered “financial in nature” as defined by the Gramm-Leach-Bliley Act and related Federal Reserve interpretations. The Corporation's status as a financial holding company is conditioned upon maintaining certain eligibility requirements for both the Corporation and its U.S. depository institution subsidiaries, including minimum capital ratios, supervisory ratings and, in the case of the depository institutions, at least satisfactory Community Reinvestment Act ratings. Failure to be an eligible financial holding company could result in the Federal Reserve limiting Bank of America's activities, including potential acquisitions. Additionally, we are subject to a significant number of laws, rules and regulations that govern our businesses in the U.S. and in the other jurisdictions in which we operate, including permissible activities, minimum levels of capital and liquidity, compliance risk management, consumer products and sales practices, privacy, data protection and executive compensation, among others.

The scope of the laws and regulations and the intensity of the supervision to which we are subject have increased over the past several years, beginning with the response to the 2008 financial crisis, as well as other factors such as technological and market changes. In addition, the banking and financial services sector is subject to substantial regulatory enforcement and fines. Many of these changes have occurred as a result of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act (the Financial Reform Act). We cannot assess whether or not there will be any additional major changes in the regulatory environment and expect that our business will remain subject to continuing and extensive regulation and supervision.

We are also subject to various other laws and regulations, as well as supervision and examination by other regulatory agencies, all of which directly or indirectly affect our entities, management and ability to make distributions to shareholders. For instance, our broker-dealer subsidiaries are subject to both U.S. and international regulation, including supervision by the SEC, Financial Industry Regulatory Authority and New York Stock Exchange, among others; our futures commission merchant subsidiariessubsidiary supporting commodities and derivatives businesses in the U.S. areis subject to regulation by and

supervision of the U.S. Commodity Futures Trading Commission (CFTC), National Futures Association, the Chicago Mercantile Exchange, and in the case of the Banks, certain banking regulators; our insurance activities are subject to licensing and regulation by state insurance regulatory agencies; and our consumer financial products and services are regulated by the Consumer Financial Protection Bureau (CFPB). In addition, certain U.S. and foreign subsidiaries are also registered with the CFTC as swap dealers, and conditionally registered with the SEC as security-based swap dealers.

Our non-U.S. businesses are also subject to extensive regulation by various non-U.S. regulators, including governments, securities exchanges, prudential regulators, central banks and other regulatory bodies, in the jurisdictions in which those businesses operate. For example, our financial services entities in the United Kingdom (U.K.), Ireland and France are subject to regulation by the Prudential Regulatory Authority and Financial Conduct Authority, the European Central Bank and Central Bank of Ireland, and the Autorité de Contrôle Prudentiel et de Résolution and Autorité des Marchés Financiers, respectively.

The Corporation is also subject to extensive laws, rules and regulations in the U.S. and in the other jurisdictions in which it operates regarding bribery and corruption, know-your-customer requirements, anti-money laundering, embargo programs and economic sanctions. For example, we are subject to the U.S. Bank Secrecy Act (BSA), which contains anti-money laundering and financial transparency laws designed to detect and deter money laundering and the financing of terrorism, as well as record-keeping, reporting, due diligence and customer verification requirements, various sanctions programs administered and enforced by the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) and foreign jurisdictions, which target entities or individuals that are, or are located in countries that are, involved in activities, such as terrorism, hostilities, drug trafficking or human rights violations and the U.S. Foreign Corrupt Practices Act (FCPA) and the U.K. Bribery Act, relating to corrupt and illegal payments to government officials and others.

Source of Strength

Under the Financial Reform Act and Federal Reserve policy, BHCs are expected to act as a source of financial strength to

each subsidiary bank and to commit resources to support each such subsidiary. Similarly, under the cross-guarantee provisions of the Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA), in the event of a loss suffered or anticipated by the FDIC, either as a result of default of a bank subsidiary or related to FDIC assistance provided to such a subsidiary in danger of default, the affiliate banks of such a subsidiary may be assessed for the FDIC’s loss, subject to certain exceptions.

Transactions with Affiliates

Pursuant to Section 23A and 23B of the Federal Reserve Act, as implemented by the Federal Reserve’s Regulation W, the Banks are subject to restrictions that limit certain types of transactions between the Banks and their nonbank affiliates. In general, U.S. banks are subject to quantitative and qualitative limits on extensions of credit, purchases of assets and certain other transactions involving their nonbank affiliates. Additionally, transactions between U.S. banks and their nonbank affiliates are required to be on arm’s length terms and must be consistent with standards of safety and soundness.

Deposit Insurance

Deposits placed at U.S. domiciled banks are insured by the FDIC, subject to limits and conditions of applicable law and the FDIC’s regulations. Pursuant to the Financial Reform Act, FDIC insurance coverage limits are $250,000 per depositor, per insured bank for each account ownership category. All insured depository institutions are required to pay assessments to the FDIC in order to fund the DIF.

The FDIC is required to maintain at least a designatedstatutory minimum ratio of the DIF to insured deposits in the U.S. The FDIC adopted regulations that establishof at least 1.35 percent and has established a long-term targetgoal of a two percent DIF ratio of greater than two percent.ratio. As of the date of this report, the DIF ratio is below this required target,the statutory minimum ratio and the FDIC’s long-term goal. In October 2022, the FDIC has adopted a restoration plan that may resultincludes an increase in increased deposit insurance assessments.assessments across the industry of two basis points (bps). The FDIC has indicated that it intends to maintain such assessment rates for the foreseeable future. Deposit insurance assessment rates are subject to change by the FDIC and will be impacted by the overall economy and the stability of the banking industry as a whole. The FDIC also has the authority to charge special assessments from time to time, including in connection with systemic risk events. For example, on November 16, 2023, the FDIC issued its final rule to impose a special assessment to recover the loss to the DIF resulting from the closure of Silicon Valley Bank and Signature Bank. For more information on the impact to the Corporation of the FDIC special assessment, see Executive Summary – Recent Developments in the MD&A on page 26. For more information regarding deposit insurance, see Item 1A. Risk Factors – Regulatory, Compliance and Legal on page 18.17.

Capital, Liquidity and Operational Requirements

As a financial holding company, we and our bank subsidiaries are subject to the regulatory capital and liquidity rules issued by the Federal Reserve and other U.S. banking regulators, including the OCC and the FDIC. These rules are complex and are evolving as U.S. and international regulatory authorities propose and enact amendments to these rules. The Corporation seeks to manage its capital position to maintain sufficient capital to satisfy these regulatory rules and to support our business activities. These continually evolving rules are likely to influence our planning processes and may require additional regulatory capital and liquidity, as well as impose additional operational and compliance costs on the Corporation.

For more information on regulatory capital rules, capital composition and pending or proposed regulatory capital changes, see Capital Management on page 49,47 and Note 16 – Regulatory Requirements and Restrictions to the Consolidated Financial Statements, which are incorporated by reference in this Item 1.

Distributions

We are subject to various regulatory policies and requirements relating to capital actions, including payment of dividends and common stock repurchases. For instance, Federal Reserve regulations require major U.S. BHCs to submit a capital plan as part of an annual Comprehensive Capital Analysis and Review (CCAR).

Our ability to pay dividends and make common stock repurchases depends in part on our ability to maintain regulatory capital levels above minimum requirements plus buffers and non-capital standards established under the FDICIA. To the extent that the Federal Reserve increases our stress capital buffer (SCB), global systemically important bank (G-SIB) surcharge or countercyclical capital buffer, our returns of capital to shareholders, including dividends and common stock repurchases, could decrease. As part of its CCAR, the Federal Reserve conducts stress testing on parts of our business using hypothetical economic scenarios prepared by the Federal Reserve. Those scenarios may affect our CCAR stress test results, which may impact the level of our SCB. For example, based on the results of our 2023 CCAR stress test, the Corporation’s SCB decreased to 2.5 percent. Additionally, the Corporation’s G-SIB surcharge increased to 3.0 percent on January 1, 2024. The Federal Reserve maycould also impose limitations or prohibitions on taking capital actions such as paying or increasing common stock dividends or repurchasing common stock. For example, as a result of the economic uncertainty resulting from the COVID-19 pandemic, in the second half of 2020, the Federal Reserve introduced certain limitations to capital distributions for all large banks, including the Corporation, which were removed effective July 1, 2021.

If the Federal Reserve finds that any of our Banks are not “well-capitalized” or “well-managed,” we would be required to enter into an agreement with the Federal Reserve to comply with all applicable capital and management requirements, which may contain additional limitations or conditions relating to our activities. Additionally, the applicable federal regulatory authority is authorized to determine, under certain circumstances relating to the financial condition of a bank or BHC, that the payment of dividends would be an unsafe or unsound practice and to prohibit payment thereof.

For more information regarding the requirements relating to the payment of dividends, including the minimum capital requirements, see Note 13 – Shareholders’ Equity and Note 16 – Regulatory Requirements and Restrictions to the Consolidated Financial Statements.

Many of our subsidiaries, including our bank and broker-dealer subsidiaries, are subject to laws that restrict dividend payments, or authorize regulatory bodies to block or reduce the

flow of funds from those subsidiaries to the parent company or other subsidiaries. The rights of the Corporation, our shareholders and our creditors to participate in any distribution of the assets or earnings of our subsidiaries are further subject to the prior claims of creditors of the respective subsidiaries.

For more information regarding distributions, including the minimum capital requirements, see Note 13 – Shareholders’ Equity and Note 16 – Regulatory Requirements and Restrictions to the Consolidated Financial Statements.

Resolution Planning

As a BHC with greater than $250 billion of assets, the Corporation is required by the Federal Reserve and the FDIC to periodically submit a plan for a rapid and orderly resolution in the event of material financial distress or failure.

Such resolution plan is intended to be a detailed roadmap for the orderly resolution of the BHC, including the continued operations or solvent wind down of its material entities, pursuant to the U.S. Bankruptcy Code under one or more hypothetical scenarios assuming no extraordinary government assistance.

If both the Federal Reserve and the FDIC determine that the BHC’s plan is not credible, the Federal Reserve and the FDIC may jointly impose more stringent capital, leverage or liquidity requirements or restrictions on growth, activities or operations. A summary of our plan is available on the Federal Reserve and FDIC websites.

The FDIC also requires the submission of a resolution plan for Bank of America, National Association, (BANA), which must describe how the insured depository institution would be resolved under the bank resolution provisions of the Federal Deposit Insurance Act. A description of this plan is available on the FDIC’s website.

We continue to make substantial progress to enhance our resolvability, which includes continued improvements to our preparedness capabilities to implement our resolution plan, both from a financial and operational standpoint.

Across international jurisdictions, resolution planning is the responsibility of national resolution authorities (RA) and central resolution authorities (CA). Among those, the jurisdictions with the greatest impact to the Corporation’s subsidiaries are the U.K., Ireland and France, where rules have been issued requiring the submission of significant information about locally incorporated subsidiaries as well as the Corporation’s banking branches located in those jurisdictions that are deemed to be material for resolution planning purposes. As a result of the RA'sRA’s and CA's review of the submitted information, we could be required to take certain actions over the next several years that could increase operating costs and potentially result in the restructuring of certain businesses and subsidiaries.

For more information regarding our resolution plan, see Item 1A. Risk Factors – Liquidity on page 10.9.

Insolvency and the Orderly Liquidation Authority

Under the Federal Deposit Insurance Act, the FDIC may be appointed receiver of an insured depository institution if it is insolvent or in certain other circumstances. In addition, under the Financial Reform Act, when a systemically important financial institution (SIFI) such as the Corporation is in default or danger of default, the FDIC may be appointed receiver in order to conduct an orderly liquidation of such institution. In the event of such appointment, the FDIC could, among other things, invoke the orderly liquidation authority, instead of the U.S. Bankruptcy Code, if the Secretary of the Treasury makes certain financial distress and systemic risk determinations. The orderly liquidation authority is modeled in part on the Federal Deposit Insurance Act, but also adopts certain concepts from the U.S. Bankruptcy Code.

The orderly liquidation authority contains certain differences from the U.S. Bankruptcy Code. For example, in certain circumstances, the FDIC could permit payment of obligations it determines to be systemically significant (e.g., short-term creditors or operating creditors) in lieu of paying other obligations (e.g., long-term creditors) without the need to obtain creditors’ consent or prior court review. The insolvency and resolution process could also lead to a large reduction or total

elimination of the value of a BHC’s outstanding equity, as well as impairment or elimination of certain debt.

Under the FDIC’s “single point of entry” strategy for resolving SIFIs, the FDIC could replace a distressed BHC with a bridge holding company, which could continue operations and result in an orderly resolution of the underlying bank, but whose equity is held solely for the benefit of creditors of the original BHC.

Furthermore, the Federal Reserve requires that BHCs maintain minimum levels of long-term debt required to provide adequate loss absorbing capacity in the event of a resolution.

For more information regarding our resolution, see Item 1A. Risk Factors – Liquidity on page 10.9.

Limitations on Acquisitions

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 permits a BHC to acquire banks located in states other than its home state without regard to state law, subject to certain conditions, including the condition that the BHC, after and as a result of the acquisition, controls no more than 10 percent of the total amount of deposits of insured depository institutions in the U.S. and no more than 30 percent or such lesser or greater amount set by state law of such deposits in that state. At June 30, 2021,2023, we held greater than 10 percent of the total amount of deposits of insured depository institutions in the U.S.

In addition, the Financial Reform Act restricts acquisitions by a financial institution if, as a result of the acquisition, the total liabilities of the financial institution would exceed 10 percent of the total liabilities of all financial institutions in the U.S. At June 30, 2021,2023, our liabilities did not exceed 10 percent of the total liabilities of all financial institutions in the U.S.

The Volcker Rule

The Volcker Rule prohibits insured depository institutions and companies affiliated with insured depository institutions (collectively, banking entities) from engaging in short-term proprietary trading of certain securities, derivatives, commodity futures and options for their own account. The Volcker Rule also imposes limits on banking entities’ investments in, and other relationships with, hedge funds and private equity funds. The Volcker Rule provides exemptions for certain activities, including market making, underwriting, hedging, trading in government obligations, insurance company activities and organizing and offering hedge funds and private equity funds. The Volcker Rule also clarifies that certain activities are not prohibited, including acting as agent, broker or custodian. A banking entity with significant trading operations, such as the Corporation, is required to maintain a detailed compliance program to comply with the restrictions of the Volcker Rule.

Derivatives

Our derivatives operationsbusinesses are subject to extensive regulation globally. These operations are subject to regulationglobally, including under the Financial Reform Act, the European Union (EU) Markets in Financial Instruments Directive and Regulation, the European Market Infrastructure Regulation, analogous U.K. regulatory regimes and similar regulatory regimes in other jurisdictions that regulate or will regulate the derivatives markets in which we

operate by,jurisdictions. These regulations, among other things: requiringthings, require clearing and exchange trading of certain derivatives; enforcing existing or imposing newderivatives, establish capital, margin, reporting, registration and business conduct requirements for certain market participants; imposingparticipants, set position limits on certain over-the-counter (OTC) derivatives;derivatives and imposingset out derivatives trading transparency requirements. These regulations are already in effect in many markets in which we operate.

In addition, many G-20 jurisdictions, including the U.S., EU, U.K., and Japan, have adopted resolution stay regulations to address concerns that the close-out of derivatives and other

financial contracts in resolution could impede orderly resolution of G-SIBs, and additional jurisdictions are expected to follow suit. In addition, the EU has implemented EU-wide resolution stay requirements. Generally, these resolution stay regulations require amendment of certain financial contracts to provide for contractual recognition of stays of termination rights under various statutory resolution regimes and a stay on the exercise of cross-default rights based on an affiliate’s entry into insolvency proceedings. Resolution regulations may also require contractual recognition by the counterparty that amounts owed to them may be written down or converted into equity as part of a bail in. As resolution stay regulations of a particular jurisdiction applicable to us go into effect, we amend impacted financial contracts in compliance with such regulations either as a regulated entity or as a counterparty facing a regulated entity in such jurisdiction.

Consumer Regulations

Our consumer businesses are subject to extensive regulation and oversight by federal and state regulators. Certain federal consumer finance laws to which we are subject, including the Equal Credit Opportunity Act, Home Mortgage Disclosure Act, Fair Housing Act, Electronic Fund Transfer Act (EFTA), Fair Credit Reporting Act, Real Estate Settlement Procedures Act, prohibitions on unfair, deceptive, or abusive acts or practices, (UDAAP), Truth in Lending Act and Truth in Savings Act, are enforced by the CFPB. Other federal consumer finance laws, such as the Servicemembers Civil Relief Act, are enforced by the OCC.

Privacy and Information Security

We are subject to many U.S. federal, state and international laws and regulations governing requirements for maintaining policies and procedures regarding the collection, disclosure, use and protection of the non-public confidential information of our customers and employees. The Gramm-Leach-Bliley Act requires us to periodically disclose Bank of America’s privacy policies and practices relating to sharing such information and enables retail customers to opt out of our ability to share information with unaffiliated third parties, under certain circumstances. The Gramm-Leach-Bliley Act and other laws also require us to

implement a comprehensive information security program that includes administrative, technical and physical safeguards to provide the security and confidentiality of customer records and information. Security and privacy policies and procedures for the protection of personal and confidential information are in effect across all businesses and geographic locations.

Other laws and regulations, at the international, federal and state level, impact our ability to share certain information with affiliates and non-affiliates for marketing and/or non-marketing purposes, or contact customers with marketing offers and establish certain rights of consumers in connection with their personal information. For example, California’s Consumer Privacy Act (CCPA), which went into effect in January 2020, as modified by the California Privacy Rights Act (CPRA), provides consumers with the right to know what personal data is being collected, know whether their personal data is sold or disclosed and to whom and opt out of the sale of their personal data,

among other rights. In addition, in the EU and other countries around the world, similar laws, like the General Data Protection Regulation (GDPR) replaced the Data Protection Directive(GDPR), afford those countries’ residents with certain rights related to their information and related implementing national laws in its member states. The CCPA's, CPRA's and GDPR’smay impose additional obligations on financial institutions. These laws’ impact on the Corporation was assessed and addressed through comprehensive compliance implementation programs. These existing and evolving legal requirements in the U.S. and abroad, as well as court proceedings and changing guidance from regulatory bodies, with respect toincluding the validity of cross-border data transfer mechanisms from the EU and other jurisdictions, continue to lend uncertainty to privacy compliance globally.

Additionally, the Corporation is subject to evolving information security (including cybersecurity) laws, rules and regulations enacted by U.S. federal and state governments and non-U.S. jurisdictions, including requirements to develop cybersecurity programs, policies and frameworks, as well as provide disclosure and/or notifications of certain cybersecurity incidents and data breaches.

Item 1A. Risk Factors

The discussion below addresses the Corporation’sour material risk factors of which we are aware. Any risk factor, either by itself or together with other risk factors, could materially and adversely affect our businesses, results of operations, cash flows and/or financial condition. The considerationsReferences to third parties may include suppliers, service providers, counterparties, financial market utilities, exchanges and risks that follow are organized within relevant headings butclearing houses, data aggregators and other partners and their upstream and downstream service providers (e.g., fourth parties, fifth parties) who may be relevantalso contribute to other headings as well.our risks. Other factors not currently known to us or that we currently deem immaterial could also adversely affect our businesses, results of operations, cash flows and/or financial condition. Therefore, the risk factors below should not be considered all of the potential risks that we may face. For more information on how we manage risks, see Managing Risk in the MD&A beginning on page 46.44. For more information about the risks contained in the Risk Factorsthis section, see Item 1. Business beginning on page 2, MD&A beginning on page 2625 and Notes to Consolidated Financial Statements beginning on page 94.

Summary of Risk Factors

Coronavirus Disease

●Market The impacts of the pandemic have adversely affected, and may continue to adversely affect us, and the pandemic’s duration and future impacts remain uncertain.

Market

● Our business and results of operationsWe may be adversely affected by the financial markets, fiscal, monetary, and regulatory policies, and economic conditions.

General economic, political, social and health conditions generally.in the U.S. and abroad affect financial markets and our business. In particular, global markets may be affected by the level and volatility of interest rates, availability and market conditions of financing, changes in gross domestic product (GDP), economic growth or its sustainability, inflation, supply chain disruptions, consumer spending, employment levels, labor shortages, challenging labor market conditions, wage stagnation, federal government shutdowns, energy prices, home prices, commercial property values, bankruptcies and a default by a significant market participant or class of counterparties, including companies in emerging markets. Global markets also may be affected by adverse developments impacting the U.S. or global banking industry, including bank failures and liquidity concerns, fluctuations or other significant changes in both debt and equity capital markets and currencies, the transition of benchmark rates, including the Bloomberg Short-Term Bank Yield Index (BSBY), to alternative reference rates (ARRs), the impact of the volatility of digital assets on the broader market, the rate of growth of global trade and commerce, trade policies, the availability and cost of capital and credit, disruption of communication, transportation or energy infrastructure, recessionary fears, investor sentiment and the U.S. and global election cycles, including resulting changes to policy and the geopolitical environment. Global markets, including energy and commodity markets, may also be adversely affected by the current or anticipated impact of climate change, acute and/or chronic extreme weather events or natural disasters, the emergence or continuation of widespread health emergencies or pandemics, cyberattacks, military conflict, terrorism, or other geopolitical events. Market fluctuations may impact our margin requirements and affect our liquidity. Any sudden or prolonged market downturn, as a result of the above factors or otherwise, could result in a decline in net interest income and noninterest income and adversely affect our results of operations and financial condition, including capital and liquidity levels. Elevated inflation and interest rate levels, monetary tightening by central banks, and geopolitical developments, including the Russia/Ukraine conflict and the conflict in the Middle East, have adversely impacted and may continue to adversely impact

financial markets and macroeconomic conditions and could result in additional market volatility and disruptions.

Global uncertainties regarding fiscal and monetary policies present economic challenges. Actions taken by the Federal Reserve or central banks in other jurisdictions, including changes in target rates, balance sheet management and lending facilities, are beyond our control and difficult to predict, particularly in an elevated inflation environment. This can affect interest rates and the value of financial instruments and other assets, such as debt securities, and impact our borrowers and potentially increase delinquency rates and may also raise government debt levels, adversely affect businesses and household incomes, adversely impact the banking sector generally, and increase uncertainty surrounding monetary policy. Monetary policy in response to high inflation has led to a significant increase in market interest rates and a flattening and/or inversion of the yield curve. This has resulted in and may continue to result in volatility of equity and other markets, further volatility of the U.S. dollar, a widening in credit spreads and higher interest rates and recessionary concerns, and could result in elevated unemployment, which could impact investor risk appetite and our borrowers, potentially increasing delinquency rates. Financial market volatility could also result from uncertainty about the timing and extent of rate cuts by the Federal Reserve in response to moderating inflation and/or weakening economic conditions. Elevated inflation may limit the scope of monetary support, including cuts to the federal funds rate, in the event of an economic downturn, resulting in a more protracted period of a flat and/or inverted yield curve.

Any future change in monetary policy by the Federal Reserve, in an effort to stimulate the economy or otherwise, resulting in lower interest rates would likely result in lower revenue through lower net interest income, which could adversely affect our results of operations. Additionally, changes to existing U.S. laws and regulatory policies and evolving priorities, including those related to financial regulation, taxation, international trade, fiscal policy, climate change (including efforts to transition to a low-carbon economy) and healthcare, may adversely impact U.S. or global economic activity and our customers', our counterparties' and our earnings and operations. Globally, many central banks have simultaneously reduced monetary accommodation through interest rate or balance sheet policy, which has contributed and may continue to contribute to elevated financial and capital market volatility and significant changes to asset values. While higher interest rates have positively impacted our net interest income, higher interest rates have negatively impacted and could continue to negatively impact investment securities, deposits, loan demand and funding costs. In addition to higher interest rates, wider credit spreads can negatively impact capital by reducing the value of debt securities. High and rising federal debt levels and uncertainty about the U.S. budget process could lead to higher interest rates and financial market volatility, potentially impacting broader economic activity. Further, if the U.S. government’s debt ceiling limit is not raised in January 2025, the ramifications could result in market volatility, ratings downgrades and limit fiscal policy responses to recessionary conditions. This could have a negative and potentially severe impact on the U.S. and world economy and financial and capital markets, including higher interest rates, higher volatility, lower asset values, lower liquidity, downgrades to U.S. debt, and a weakened U.S. dollar.

Changes to international trade and investment policies by the U.S. could negatively impact financial markets. Escalation of tensions between the U.S. and the People’s Republic of China

●(China) could lead to further U.S. measures that adversely affect financial markets, disrupt world trade and commerce and lead to trade retaliation, including through the use of tariffs, foreign exchange measures or the large-scale sale of U.S. Treasury bonds. Any restrictions on the activities of businesses, could also negatively affect financial markets.

These developments could adversely affect our businesses, customers, securities and derivatives portfolios, including the risk of lower re-investment rates within those portfolios, our level of charge-offs and provision for credit losses, the carrying value of our deferred tax assets, our capital levels, our liquidity and our results of operations.

Increased market volatility and adverse changes in financial or capital market conditions may increase our market risk.

● WeOur liquidity, competitive position, business, results of operations and financial condition are affected by market risks such as changes in interest and currency exchange rates, fluctuations in equity, commodity and futures prices, trading volumes and prices of securitized products, the implied volatility of interest rates and credit spreads and other economic and business factors. These market risks may adversely affect, among other things, the value of our securities, including our on- and off-balance sheet securities, trading assets and other financial instruments, the cost of debt capital and our access to credit markets, the value of assets under management (AUM), fee income relating to AUM, customer allocation of capital among investment alternatives, the volume of client activity in our trading operations, investment banking, underwriting and other capital market fees, which have already been negatively impacted, the general profitability and risk level of the transactions in which we engage and our competitiveness with respect to deposit pricing. The value of certain of our assets is sensitive to changes in market interest rates. If the Federal Reserve or a non-U.S. central bank changes or signals a change in monetary policy, market interest rates or credit spreads could be affected, which could adversely impact the value of such assets. Changes to fiscal policy, including expansion of U.S. federal deficit spending and resultant debt issuance, could also affect market interest rates. If interest rates decrease, our results of operations could be negatively impacted, including future revenue and earnings growth.

Our models and strategies to assess and control our market risk exposures are subject to inherent limitations. In times of market stress or other unforeseen circumstances, previously uncorrelated indicators may become correlated. Such changes to the relationship between market parameters may limit the effectiveness of our hedging strategies and cause us to incur significant losses. Changes in correlation can be exacerbated where market participants use risk or trading models with assumptions or algorithms similar to ours. In these and other cases, it may be difficult to reduce our risk positions due to activity of other market participants or widespread market dislocations, including circumstances where asset values are declining significantly or no market exists. Where we own securities that do not have an established liquid trading market or are otherwise subject to restrictions on sale or hedging, or where the degree of accessible liquidity declines significantly, we may not be able to reduce our positions and risks associated with such holdings, so we may suffer larger than expected losses when adverse price movements take place. This risk can be exacerbated where we hold a position that is large relative to the available liquidity.

If asset values decline, we may incur losses if assetand negative impacts to capital and liquidity requirements.

We have a large portfolio of financial instruments, including loans and loan commitments, securities financing agreements, asset-backed secured financings, derivative assets and liabilities, debt securities, marketable equity securities and certain other assets and liabilities that we measure at fair value and are subject to valuation and impairment assessments. We determine these values decline, including duebased on applicable accounting guidance, which, for financial instruments measured at fair value, requires an entity to changesbase fair value on exit price and to maximize the use of observable inputs and minimize the use of unobservable inputs in fair value measurements. The fair values of these financial instruments include adjustments for market liquidity, credit quality, funding impact on certain derivatives and other transaction-specific factors, where appropriate.

Gains or losses on these instruments can have a direct impact on our results of operations, unless we have effectively mitigated the risk of our exposures. Increases in interest rates may cause decreases in residential mortgage loan originations and prepayment speeds.could impact the origination of corporate debt. In addition, increases in interest rates or changes in spreads may continue to adversely impact the fair value of our debt securities and, accordingly, for debt securities classified as available-for-sale (AFS), adversely affect accumulated other comprehensive income and, thus, our capital levels. Increases in interest rates could also adversely impact our regulatory liquidity position and requirements, which include certain AFS debt securities and the use of repurchase agreements against a portion of the held-to-maturity (HTM) debt securities. As our liquidity is dependent on the fair value of these assets, increases in market interest rates, which have adversely impacted and may continue to adversely impact the fair value of debt securities, could adversely affect liquidity levels.

Fair values may be impacted by declining values of the underlying assets or the prices at which observable market transactions occur and the continued availability of these transactions or indices. The financial strength of counterparties, with whom we have economically hedged some of our exposure to these assets, also will affect the fair value of these assets. Sudden declines and volatility in the prices of assets may curtail or eliminate trading activities in these assets, which may make it difficult to sell, hedge or value these assets. The inability to sell or effectively hedge assets reduces our ability to limit losses in such positions, and the difficulty in valuing assets may increase our risk-weighted assets (RWA), which requires us to maintain additional capital and increases our funding costs. Values of AUM also impact revenues in our wealth management and related advisory businesses for asset-based management and performance fees. Declines in values of AUM can result in lower fees earned for managing such assets.

Liquidity

●If we are unable to access the capital markets, or continue to maintainhave prolonged net deposits outflows, or our borrowing costs increase, our liquidity and competitive position will be negatively affected.

●Liquidity is essential to our businesses. We fund our assets primarily with globally sourced deposits in our bank entities, as well as secured and unsecured liabilities transacted in the capital markets. We rely on certain secured funding sources, such as repo markets, which are typically short-term and credit-sensitive. We also engage in asset securitization transactions, including with the government-sponsored enterprises (GSEs), to fund consumer lending activities. Our liquidity could be adversely affected by any inability to access the capital markets, illiquidity or volatility in the capital markets, the decrease in value of eligible collateral or increased collateral requirements (including as a result of credit concerns for short-term

borrowing), changes to our relationships with our funding providers based on real or perceived changes in our risk profile, prolonged federal government shutdowns, or changes in regulations, guidance or GSE status that impact our funding.

Additionally, our liquidity or cost of funds may be negatively impacted by the unwillingness or inability of the Federal Reserve to act as lender of last resort, unexpected simultaneous draws on lines of credit or deposits, slower customer payment rates, restricted access to the assets of prime brokerage clients, the withdrawal of or failure to attract customer deposits or invested funds (which could result from attrition driven by customers seeking higher yielding deposits or securities products, customer desire to utilize an alternative financial institution perceived to be safer, changes in customer spending behavior due to inflation, decline in the economy or other drivers resulting in an increased need for cash), increased regulatory liquidity, capital and margin requirements for our U.S. or international banks and their nonbank subsidiaries, which could result in the inability to transfer liquidity internally and inefficient funding, changes in patterns of intraday liquidity usage resulting from a counterparty or technology failure or other idiosyncratic event or failure or default by a significant market participant or third party (including clearing agents, custodians, central banks or central counterparty clearinghouses (CCPs)). These factors may increase our borrowing costs and negatively impact our liquidity.

Several of these factors may arise due to circumstances beyond our control, such as general market volatility, disruption, shock or stress, the emergence or continuation of widespread health emergencies or pandemics, and military conflicts (including the Russia/Ukraine conflict and the conflict in the Middle East). Federal Reserve policy decisions (including fluctuations in interest rates or Federal Reserve balance sheet composition), negative views or loss of confidence about us or the financial services industry generally or due to a specific news event, changes in the regulatory environment or governmental fiscal or monetary policies, actions by credit rating agencies or an operational problem that affects third parties or us. The impact of these potentially sudden events, whether within our control or not, could include an inability to sell assets or redeem investments, unforeseen outflows of cash, the need to draw on liquidity facilities, the reduction of financing balances and the loss of equity secured funding, debt repurchases to support the secondary market or meet client requests, the need for additional funding for commitments and contingencies and unexpected collateral calls, among other things, the result of which could be increased costs, a liquidity shortfall and/or impact on our liquidity coverage ratio.

Our liquidity and cost of obtaining funding may be directly related to investor behavior and confidence, debt market disruption, firm specific concerns or prevailing market conditions, including changes in interest and currency exchange rates, significant fluctuations in equity and futures prices, lower trading volumes and prices of securitized products and our credit spreads. Increases in interest rates and our credit spreads can increase the cost of our funding and result in mark-to-market or credit valuation adjustment exposures. Changes in our credit spreads are market driven and may be influenced by market perceptions of our creditworthiness, including changes in our credit ratings or changes in broader financial market and macroeconomic conditions. Changes to interest rates and our credit spreads occur continuously and may be unpredictable and highly volatile. We may also experience net interest margin compression as a result of offering higher than expected deposit rates in order to attract and maintain deposits. Concentrations within our funding profile, such as maturities,

currencies or counterparties, can also reduce our funding efficiency.

Reduction in our credit ratings could significantly limit our access to funding or the capital markets, increase borrowing costs or trigger additional collateral or funding requirements.

●Our borrowing costs and ability to raise funds are directly impacted by our credit ratings. Credit ratings are also important to investors, customers or counterparties when we compete in certain markets and seek to engage in certain transactions, including over-the-counter (OTC) derivatives. Our credit ratings are subject to ongoing review by rating agencies, which consider a number of financial and nonfinancial factors, including our franchise, financial strength, performance and prospects, management, governance, risk management practices, capital adequacy, asset quality and operations, among other criteria, as well as factors not under our control, such as regulatory developments, the macroeconomic and geopolitical environment and changes to the methodologies used to determine our ratings.

Rating agencies could adjust our credit ratings at any time and there can be no assurance as to whether or when a downgrade could occur. Any reduction could result in a wider credit spread and negatively affect our access to credit markets, the related cost of funds, our businesses and certain trading revenues, particularly in those businesses where counterparty creditworthiness is critical. If the short-term credit ratings of our parent company, bank or broker-dealer subsidiaries were downgraded, we may experience loss of access to short-term funding sources such as repo financing, and/or incur increased cost of funds and increased collateral requirements. Under the terms of certain OTC derivative contracts and other trading agreements, if our or our subsidiaries’ credit ratings are downgraded, the counterparties may require additional collateral or terminate these contracts or agreements.

While certain potential impacts are contractual and quantifiable, the full consequences of a credit rating downgrade are inherently uncertain and depend upon numerous dynamic, complex and inter-related factors and assumptions, including the relationship between long-term and short-term credit ratings and the behaviors of customers, investors and counterparties.

Bank of America Corporation is a holding company, is dependent on its subsidiaries for liquidity and may be restricted from transferring funds from subsidiaries.

Bank of America Corporation, as the parent company, is a separate and distinct legal entity from our bank and nonbank subsidiaries. We evaluate and manage liquidity on a legal entity basis. Legal entity liquidity is an important consideration as there are legal, regulatory, contractual and other limitations on our ability to utilize liquidity from one legal entity to satisfy the liquidity requirements of another, including the parent company, which could result in adverse liquidity events. The parent company depends on dividends, distributions, loans and other payments from our bank and nonbank subsidiaries to fund dividend payments on our preferred stock and common stock and to fund all payments on our other obligations, including debt obligations. Any inability of our subsidiaries to transfer funds, pay dividends or make payments to us may adversely affect our cash flow, liquidity and financial condition.

Many of our subsidiaries, including our bank and broker-dealer subsidiaries, are subject to laws that restrict dividend payments, or authorize regulatory bodies to block or reduce the flow of funds from those subsidiaries to the parent company or other subsidiaries. Our bank and broker-dealer subsidiaries are subject to restrictions on their ability to lend or transact with affiliates, minimum regulatory capital and liquidity requirements

● Ourand restrictions on their ability to use funds deposited with them in bank or brokerage accounts to fund their businesses. Intercompany arrangements we entered into in connection with our resolution planning submissions could restrict the amount of funding available to the parent company from our subsidiaries under certain adverse conditions.

Additional restrictions on related party transactions, increased capital and liquidity requirements and additional limitations on the use of funds on deposit in bank or brokerage accounts, as well as lower earnings, can reduce the amount of funds available to meet the obligations of the parent company and even require the parent company to provide additional funding to such subsidiaries. Also, regulatory action that requires additional liquidity at each of our subsidiaries could impede access to funds we need to pay our obligations or pay dividends. In addition, our right to participate in a distribution of assets upon a subsidiary’s liquidation or reorganization is subject to prior claims of the subsidiary’s creditors.

Bank of America Corporation’s liquidity and financial condition, and the ability to pay dividends to shareholders and to pay obligations, could be materially adversely affected in the event of a resolution.