UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

T ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20112012

or

£ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to _________

Commission File Number 000-07246

PETROLEUM DEVELOPMENT CORPORATIONPDC ENERGY, INC.

(Exact name of registrant as specified in its charter)

(Doing Business as PDC Energy)

|

| |

| Nevada | 95-2636730 |

(State of Incorporation)incorporation) | (I.R.S. Employer Identification No.) |

1775 Sherman Street, Suite 3000

Denver, Colorado 80203

(Address of principal executive offices) (Zip Code)code)

Registrant's telephone number, including area code: (303) 860-5800

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes T No £

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No T

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes T No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes T No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

| |

Large accelerated filer £x | Accelerated filer xo |

Non-accelerated filer £ (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes £ No T

The aggregate market value of our common stock held by non-affiliates on June 30, 20112012, was $699,417,474735,547,944 (based on the then closing price of $29.9124.52) per share).

As of February 17, 20128, 2013, there were 23,634,45630,316,670 shares of our common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

We hereby incorporate by reference into this document the information required by Part III of this Form, which will appear in our definitive proxy statement to be filed pursuant to Regulation 14A for our 20122013 Annual Meeting of Stockholders.

PETROLEUM DEVELOPMENT CORPORATION

(dba PDC Energy)ENERGY, INC.

20112012 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

| | | |

| | PART I | | Page |

| | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART II | | |

| | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART III | | |

| | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | PART IV | | |

| | | | |

| | | |

| | | | |

| | | | |

| | | | |

| | | | |

PART I

REFERENCES TO THE REGISTRANT

In July 2010,At our annual meeting of stockholders held on June 7, 2012, the stockholders approved a change of the Company's legal name from Petroleum Development Corporation established in 1969, began conducting business asto PDC Energy. The Company'sEnergy, Inc. Reflecting this change, on July 16, 2012, our common stock continues to tradebegan trading on the NASDAQ Global Select Market under the ticker symbol PETD. The Company's website, www.petd.com, reflects the PDC Energy name and brand identity. At the Company's annual stockholders' meeting to be held in June 2012, we plan to request shareholders to approve and amend the Company's articles of incorporation to formally change the corporate name to PDC Energy, Inc."PDCE." Information contained on or linked to our website, www.pdce.com, is not part of this report and is not hereby incorporated by reference and should not be considered part of this report.

Unless the context otherwise requires, references in this report to "PDC Energy," "PDC, Energy," "the Company," "we," "us," "our," "ours" or "ourselves" refer to the registrant, Petroleum Development Corporation,PDC Energy, Inc. and all subsidiaries consolidated for the purposes of its financial statements, including our proportionate share of the financial position, results of operations, cash flows and operating activities of our affiliated partnerships and PDC Mountaineer, LLC ("PDCM"), a joint venture currently owned 50% each by PDC and Lime Rock Partners, LP, formed for the purpose of exploring and developing the Marcellus Shale formation in the Appalachian Basin ("Marcellus JV").Basin. Unless the context otherwise requires, references in this report to "Appalachian Basin" includes PDC's proportionate share of our affiliated partnerships' and the Marcellus JV'sPDCM's assets, results of operations, cash flows and operating activities.

See Note 1, Nature of Operations and Basis of Presentation, to our consolidated financial statements included elsewhere in this report for a description of our consolidated subsidiaries.

GLOSSARY OF UNITS OF MEASUREMENTS AND INDUSTRY TERMS

Units of measurements and industry terms defined in the Glossary of Units of Measurements and Industry Terms, included at the end of this report, are set in boldface type the first time they appear.

WHERE YOU CAN FIND ADDITIONAL INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the United States Securities and Exchange Commission ("SEC"). Our SEC filings are available free of charge from the SEC’s website at www.sec.gov or from our website at www.petd.com. You may also read or copy any document we file at the SEC’s public reference room in Washington, D.C., located at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at (800) SEC-0330 for further information on the public reference room. We also make available free of charge any of our SEC filings by mail. For a mailed copy of a report, please contact Petroleum Development Corporation, dba PDC Energy, Investor Relations, 1775 Sherman Street, Suite 3000, Denver, CO 80203, or call toll free (800) 624-3821.

We recommend that you view our website for additional information, as we routinely post information that we believe is important for investors. Our website can be used to access such information as our recent news releases, bylaws, committee charters, code of business conduct and ethics, shareholder communication policy, director nomination procedures and our whistle-blower hotline. While we recommend that you view our website, the information available on our website is not part of this report and is not hereby incorporated by reference.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 ("Securities Act") and Section 21E of the Securities Exchange Act of 1934 ("Exchange Act") regarding our business, financial condition, results of operations and prospects. All statements other than statements of historical facts included in and incorporated by reference into this report are "forward-looking statements" within the meaning of the safe harbor provisions of the United States ("U.S.") Private Securities Litigation Reform Act of 1995. Words such as expects, anticipates, intends, plans, believes, seeks, estimates and similar expressions or variations of such words are intended to identify forward-looking statements herein. These statements include:relate to, among other things: estimated natural gas, natural gas liquids ("“NGLs"”) and crude oil production andreserves; expected operational, midstreamfuture production (including the components of such production), expenses, cash flows, margins and marketing synergies from PDCM's Seneca-Upshur acquisition;liquidity; anticipated capital projects, expenditures and opportunities, including our ability to fund our 2012 capital budget; increased focus ondrilling locations and downspacing potential; future exploration and development activities; availability of additional midstream facilities and services in the Wattenberg Field and liquid-rich areas;timing of that availability; availability of sufficient funding for our horizontal Niobrara drilling plans in 2012; planned refracturescapital program and recompletions in 2012; expected usesources of proceeds fromthat funding; potential for infrastructure projects to improve our Permian divestiture; the expected benefit of operational diversity in the Rocky Mountain region; our ability to mitigate risks by sharing costs of exploratory drilling in the Marcellus Shale with our joint venture partner; our intent to mitigate risks by maintaining a natural gas and liquids mix to counter a decline in the market price of one of our commodities; our expected term for inventory of projects for drilling activity; planned limited development in Piceance in 2012 due to the commodity pricing environment; drilling plans in the Utica Shale in 2012; that development drilling will remain the foundation of our drilling program; addition of 8 Bcfe of reserves at December 31, 2011 from the Seneca Upshur acquisition; our belief that pricing provisions in our natural gas contracts are customary; our belief that our exploration program has the potential to replenish our portfolio with new projects for significant production and reserves growth;NGL pricing; our compliance with our debt covenants and the indenture restrictions governingrenewal of a letter of credit under our senior notes and expected continued compliance; sufficient liquidity to meet our partnership repurchase obligations; our belief that the acquisition of partnerships will provide us with growth in production and proved reserves and operational benefits; therevolving credit facility; adequacy of our casualty insurance coverage as managing general partnerinsurance; the future effect of numerous partnershipscontracts, policies and as operator of our own wells; the impact of decreased commodity prices on future borrowing base redeterminations; thatprocedures we hold good and defensible titlebelieve to our natural gas and crude oil properties in accordance with industry standards; thebe customary; effectiveness of our derivative

policies program in achievingproviding a degree of price stability; our risk management objectives;future dividend policy; closing of, and expected proceeds from, our expected remaining liability for uncertain tax positions;pending asset disposition; and our ability to secure a joint venture partner for our Utica Shale acreage; the impact of outstanding legal issues; our ability to benefit from crude oil and natural gas price differential; and ourfuture strategies, plans and objectives.

The above statements are not the exclusive means of identifying forward-looking statements herein. Although forward-looking statements contained in this report reflect our good faith judgment, such statements can only be based on facts and factors currently known to us. Consequently, forward-looking statements are inherently subject to risks and uncertainties, including known and unknown risks and uncertainties incidental to the exploration for, and the acquisition, development, production and marketing of natural gas, NGLs and crude oil, and actual outcomes may differ materially from the results and outcomes discussed in the forward-looking statements.

Important factors that could cause actual results to differ materially from the forward-looking statements include, but are not limited to:

changes in production volumes and worldwide demand, including economic conditions that might impact demand;

volatility of commodity prices for natural gas, NGLs and crude oil;

the impact of governmental fiscal termspolicies and/or regulations, including changes in environmental and other laws, the regulationinterpretation and enforcement related to those laws and regulations, liabilities arising thereunder and the costs to comply with those laws as well as otherand regulations;

declinepotential declines in the values of our natural gas and crude oil properties resulting in impairments;

changes in estimates of proved reserves;reserves;

inaccuracy of reserve estimates and expected production rates;

the potential for production decline rates from our wells to be greater than expected;

the timing and extent of our success in discovering, acquiring, developing and producing reserves;

our ability to acquire leases, drilling rigs, supplies and services at reasonable prices;

the timing and receipt of necessary regulatory permits;

risks incidental to the drilling and operation of natural gas and crude oil wells;

our future cash flow,flows, liquidity and financial position;condition;

competition in the oil and gas industry;

availability and cost of capital to us;

reductions in the borrowing base under our revolving credit facility;

the availability of sufficient pipeline, gathering and other transportation facilities and related infrastructure to carryprocess and transport our production, particularly in the Wattenberg Field, and the impact of these facilities on price;the prices we receive for our production;

our success in marketing natural gas, NGLs and crude oil;

the effect of natural gas and crude oil derivatives activities;

the impact of environmental events, governmental and other third-party responses to thesuch events, and our ability to insure adequately against such events;

the cost of pending or future litigation;

effect that acquisitions we may pursue have on our capital expenditures;

potential obstacles to completing our pending asset disposition or other transactions, in a timely manner or at all, and purchase price or other adjustments relating to those transactions that may be unfavorable to us;

our ability to retain or attract senior management and key technical employees; and

the success of strategic plans, expectations and objectives for future operations of the Company.

Further, we urge you to carefully review and consider the cautionary statements and disclosures, specifically those under Item 1A, Risk Factors, made in this report and our other filings with the SECU.S. Securities and Exchange Commission ("SEC") for further information on risks and uncertainties that could affect our business, financial condition, results of operations and cash flows. We caution you not to place undue reliance on forward-looking statements, which speak only as of the date of this report. We undertake no obligation to update any forward-looking statements in order to reflect any event or circumstance occurring after the date of this report or currently unknown facts or conditions or the occurrence of unanticipated events. All forward-looking statements are qualified in their entirety by this cautionary statement.

ITEMS 11. AND 2. BUSINESS AND PROPERTIES

The Company

Effective July 15, 2010, Petroleum Development Corporation began conducting business as PDC Energy. A new logo and corporate identity accompanied this change. Our common stock continues to trade on the NASDAQ Global Select Market under the ticker symbol PETD. We continue to maintain our website address, www.petd.com, which reflects the new PDC Energy name and brand identity. This change reflects the transitioning in our business model, from a company that was predominately a sponsor of limited partnerships to an exploration and production company that explores for and acquires, develops, produces and markets natural gas and oil resources.

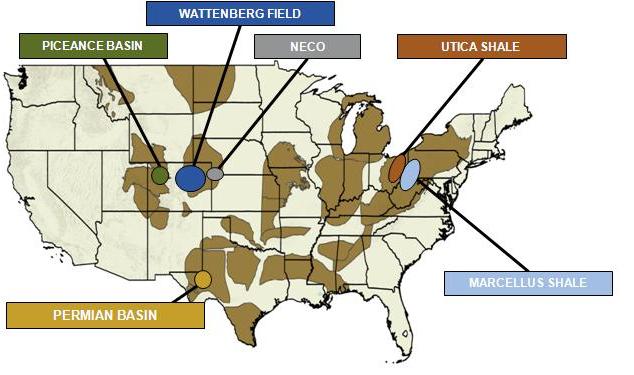

We are a domestic independent exploration and production company that acquires, develops, explores and produces natural gas, NGLs and crude oil.oil with operations in the Western and Eastern regions of the United States. Our Western Operating Region is primarily focused on development in the Wattenberg Field in Colorado, particularly in the liquid-rich horizontal Niobrara play and on the ongoing development of refractures and recompletions of our Wattenberg wells.Codell plays. In our Eastern Operating Region, we are currently focused on horizontal development in the Marcellus Shale in northern West Virginia, and recently initiated exploration and development activity in the liquid-rich portion of the Utica Shale play in Ohio. We are also pursuing horizontal development in the Marcellus Shale in northern West Virginia through our 50% joint venture interest in PDCM. We own an interest in approximately 6,5007,200 gross producing wells and maintained an average December 2011 production rate of approximately 146135.6 MMcfe per day for the year ended December 31, 2012, which was comprised of 62%65.3% natural gas, 27%10.2% NGLs and 24.5% crude oil and 11% NGLs.

Asoil. This represents production growth of 10.2% from continuing operations as compared to the year ended December 31, 2011 an independent petroleum engineering firm estimated our total. As of December 31, 2012, we had approximately 1.2 Tcfe of proved reserves to be approximately 1

Tcfe with a PV-10%present value of future net revenues (“PV-10”) value, which is not a financial measure under Accounting Principles Generally Accepted in the United States of America (“U.S. GAAP”), of $1.7 billion, a non-U.S. GAAP financial measure, of $1.3 billion. Approximately 46% of our total proved reserves have been classified as proved developed. Our total proved reserves consist of 66% natural gas and 34% crude oil and NGLs. Our internal estimaterepresenting growth of proved, probable141 Bcfe and possible ("3P") reserves has increased from 1.4 Tcfe$359 million, respectively, relative to the totals as of December 31, 2010, to 2.1 Tcfe as of December 31, 2011. The percentage of our proved reserves represented by NGLs and includes a significant multi-year inventorycrude oil rose to 48% as of horizontal and vertical drilling projectsDecember 31, 2012, up from 34% as well as multiple refracture and recompletion projects in existing wells.of

December 31, 2011. See Part I, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations - Reconciliation of Non-U.S. GAAP Financial Measures,, for a definition of PV-10% and a reconciliation of our PV-10% value to our standardized measure.measure.

2011 Overview

In 2011, we focusedThe increase in our estimated proved reserves and production is primarily attributable to liquid-rich horizontal drilling activities in the liquid-rich Wattenberg Field and our June 2012 acquisition of certain Wattenberg Field properties and related assets from affiliates of Merit Energy (the "Merit Acquisition") for $304.6 million, after certain post-closing adjustments. The acquired assets comprise approximately 29,800 net acres, after post-closing adjustments, located almost entirely in northern Colorado where wethe core Wattenberg Field with significant overlay with our existing acreage position. We believe that the Merit Acquisition should provide us with an opportunity to continue our rapid growth in the Wattenberg Field and to substantially increase our oil and NGL production. We drilled 1737 horizontal Niobrara wells, 80 verticaland Codell wells, completed 190 160 refracture and/or and recompletion projects and participated in 4819 non-operated drilling projects. During the year, we reduced our drilling of vertical wells to refocus our efforts on our horizontal Niobrara drilling program. We have successfully de-risked much of the horizontal Niobrara potential throughout our core Wattenberg acreage position and generated over 350 gross horizontal well projects in inventory. PDCM drilled six horizontal Marcellus wells, completed five horizontal wells and initiated several midstream projects. the Wattenberg Field in 2012.

In October, we announced that we entered the Utica Shale play, whereour Eastern Operating Region, we have the rights to acquire up toacquired an estimated 40,000 45,000 net acres targeting the wet gas and crude oil windows of the Utica Shale in southeast Ohio,Ohio. Our year-end 2012 proved reserves do not include reserves associated with our Utica Shale properties. We drilled and throughcompleted two horizontal Utica Shale wells in 2012, both of which are currently shut-in awaiting pipeline connections. We also drilled one vertical Utica Shale well and completed two vertical Utica test wells in 2012 for the primary purpose of providing engineering and geological data in support of the horizontal play. In addition, PDCM drilled three and completed the Seneca-Upshur acquisitionsix horizontal Marcellus wells and constructed various midstream projects in 2012.

The following table presents our historical proved reserve estimates as of December 31, 2012 based on a reserve report prepared by Ryder Scott Company, L.P. (“Ryder Scott”), our independent petroleum engineering consulting firm:

|

| | | | | | | | | | | | | | |

| | Proved Reserves at December 31, 2012 | | | | | | |

| | Proved Reserves (Bcfe) | | % of Total Proved Reserves | | % Proved Developed | | % Liquids | | Proved Reserves to Production Ratio (in years) | | Production (MMcfe) |

| Western | | | | | | | | | | | |

| Wattenberg Field | 893.5 | | 77 | % | | 41 | % | | 62 | % | | 33.4 | | 26,748 |

| Other | 84.6 | | 8 | % | | 100 | % | | 1 | % | | 5.1 | | 16,672 |

| Total Western | 978.1 | | 85 | % | | 46 | % | | 56 | % | | 22.5 | | 43,420 |

| Eastern | | | | | | | | | | | |

| Appalachian Basin | 178.8 | | 15 | % | | 23 | % | | — | % | | 28.9 | | 6,192 |

| Total Eastern | 178.8 | | 15 | % | | 23 | % | | — | % | | 28.9 | | 6,192 |

| Total proved reserves | 1,156.9 | | 100 | % | | 42 | % | | 48 | % | | 23.3 | | 49,612 |

On February 4, 2013, we entered into a purchase and sale agreement with certain affiliates of Caerus Oil and Gas LLC (“Caerus”), pursuant to which added 90,000 gross acres to our Marcellus position. During the fourth quarter, we closed on the sale of our non-core Permian Basin assets to an unrelated third party for a sales price of $13.2 million. In December, we executed a definitive agreementhave agreed to sell to Caerus our core Permian WolfberryPiceance Basin, NECO and certain non-core Colorado oil and gas properties, leasehold mineral interests and related assets, to another unrelated third partyincluding derivatives, for a sales priceaggregate cash consideration of $173.9approximately $200 million, subject to customary post-closingcertain adjustments. On February 28,As of December 31, 2012, total estimated proved reserves related to these assets were 84.6 Bcfe. See Note 19, Subsequent Events, to our consolidated financial statements included elsewhere in this divestiture was completed with total proceeds received of $184.4 million after preliminaryreport for additional information regarding the planned divestiture. There can be no assurance we will be successful in closing adjustments.such divestiture.

In addition to our oil and gas exploration and production activities, we engage in natural gas marketing through our subsidiary Riley Natural Gas (“RNG”).

Our Strengths

Multi-year project inventory targeting highly economic oil and NGL production growth.We have a significant operational presence in three key U.S. onshore basins and have identified a substantial inventory of approximately 4,100 gross capital projects across our assets. This inventory includes approximately 3,300 gross projects in the liquid-rich Wattenberg Field, of which approximately 1,400 are horizontal Niobrara and Codell proved and probable locations that we expect to be capable of providing liquid-rich production growth for the next several years at attractive rates of return based on current strip prices. Potential downspacing of future drill sites would provide the opportunity for additional locations. In the core area of the Wattenberg Field, we have achieved an average of 335 MBoe gross reserves per horizontal well, with approximately 75% liquids contribution. In the Appalachian Basin, we have approximately 600 gross Marcellus Shale drilling locations in inventory, of which approximately 360 gross wells in our core focus area would be expected to generate reserves of 5 to 7 Bcfe per well. In addition, our leasehold position in the emerging Utica Shale play is expected to provide approximately 200 horizontal drilling opportunities in liquid rich areas. With the development of the horizontal Niobrara and Codell and exploration and delineation of acreage in the Utica Shale, we are focused on transitioning our portfolio to a higher mix of oil and NGLs that we believe is capable of delivering higher margins and improved capital efficiencies.

Track record of reserve and production growth.Our proved reserves have grown from 323 Bcfe at December 31, 2006 to approximately 1.2 Tcfe at December 31, 2012, representing a compound annual growth rate (“CAGR”) of 23.7%. During the same time period, our proved crude oil and NGL reserves grew at a CAGR of 52.7%. Our annual production grew from 16.9 Bcfe in 2006 to 49.6 Bcfe in 2012 from continuing operations, representing a CAGR of 19.7%.

Horizontal drilling and completion experience.We have a proven track record of applying technical expertise toward developing unconventional resources through horizontal drilling, having drilled 108 Niobrara, Codell, Marcellus and Utica horizontal wells as of December 31, 2012. We have begun multi-well pad drilling to further optimize costs and enhance horizontal drilling efficiencies. Pad drilling enables us to streamline the transition to increased well density in the horizontal Niobrara and Codell plays. We have approximately 2,000 gross horizontal proved and probable locations in inventory from our Wattenberg and Marcellus positions. Our current leasehold position in the emerging Utica Shale play is expected to provide approximately 200 horizontal drilling opportunities in liquid-rich areas.

Significant operational control in our core areas.As a result of successfully executing our strategy over time of acquiring largely concentrated acreage positions with a high working interest, we operate and manage approximately 89% of our oil and natural gas properties. Our high percentage of operated properties enables us to exercise a significant level of control with respect to drilling, production, operating and administrative costs, in addition to leveraging our base of technical expertise in our core operating areas.

Access to liquidity.As of December 31, 2012, we had $2.5 million of cash and cash equivalents and $396.1 million available for

borrowing under our revolving credit facility. We have no near-term debt maturities, although we periodically repay borrowings outstanding under our revolving credit facility. We actively hedge our future exposure to commodity price fluctuations by entering into oil and natural gas swaps and collars. We have hedged approximately 28.7 Bcf of our natural gas production for 2013 at an average minimum price of $4.15 per Mcf. We have hedged approximately 2,326 MBbls of our oil production in 2013 at an average minimum price of $88.75 per Bbl. As of December 31, 2012, the net fair value of all of our hedges was approximately $30.3 million.

Management experience and operational expertise.We have a management team with a proven track record of performance and a technical and operational staff with significant expertise in the basins in which we operate, particularly with horizontal well development activities.

Business Strategy

Our business strategy focuses on generating shareholder value through the organic growth of our reserves, production and productioncash flows in our high-value, liquid-rich and high impact horizontal plays. We allocate capital to high return projects in our portfolio capable of maximizing our cash flow and return on capital. We place a strong emphasis on organic growth through active horizontal drilling programs, emphasize low-risk development drilling, programs. We also engage in targeted exploratory drilling in of unconventional resources and maintain an active acquisition program. We pursue various midstream, marketing and cost reduction initiatives designed to increase our per unit operating margins and maintain a conservative and disciplined financial strategy focused on providing sufficient liquidity and balance sheet strength to execute our business strategy.

Drill and Develop

Our leasehold consists primarilyinterests consist of interests in developed and undeveloped natural gas, NGLs and crude oil resources located in our Western and Eastern Operating Regions. We seek to maximize the value of our existing wells through a successful program of well refractures, recompletions and workovers. Based on our prior acreage holdings and recent acquisitions, we have accumulatedidentified a multi-yearsubstantial inventory of approximately 4,100 gross capital projects for development primarily through horizontal and vertical developmental drilling projects,in high-return, liquid-rich plays, as well as refracture and recompletion and exploration projects.opportunities.

Western Operating Region. Our primary focus in the liquid-rich Wattenberg Field is the horizontal developmentNiobrara and Codell plays. We have begun multi-well pad drilling ofto further optimize costs and enhance horizontal drilling efficiencies in the Wattenberg Field. Pad drilling enables us to streamline the transition to increased well density in the horizontal Niobrara formation.and Codell plays. We also maintain a vertical drilling inventory in the Niobrara and Codell formationsformations. We currently estimate that we have 3,300 gross capital projects, which include over 1,400 gross proved and probable projects for the horizontal Niobrara and Codell. Depending upon commodity prices and the number of drilling rigs operating, we believe that this inventory of projects provides us with over 10 years of drilling activity.

Of our total capital budget of $324 million for 2013, approximately 75%, or $245 million, is expected to be spent on development activities, substantially all of which is expected to be invested in the Wattenberg Field for an expanded horizontal Niobrara and continueCodell drilling program and participation in various non-operated projects. We plan to execute on multiple refracturerun a two-rig program in the Wattenberg Field through the second quarter of the year and recompletion projects. add a third rig during the third quarter. Under this drilling program, we expect to drill approximately 63 horizontal Niobrara or Codell wells in 2013.

Additionally, we operate natural gas assets in the Piceance Basin in western Colorado and in northeast Colorado ("NECO"), where we currently focusfocused on production optimization and increasing operating margins.

Approximately 65%margins in 2012. On February 4, 2013, we entered into a purchase and sale agreement with certain affiliates of our 2012 capital budget, or $184 million, is expectedCaerus, pursuant to be spent on development activities, approximately 97% of which is expected to be invested in the Wattenberg Field for an expanded horizontal Niobrara drilling program, increased pace of refractures and recompletions and participation in various non-operated projects. We currently estimate that we have more than 1,750 gross drilling projects, which include over 350 gross projects for the horizontal Niobrara, and approximately 1,450 refracture and recompletion projects in existing wells in the Wattenberg Field. Depending on the number of drilling rigs operating and commodity prices, we believe that this inventory of projects provides us with approximately 10 years of drilling activity. In 2012, we planagreed to run a one-rig program in Wattenberg to drill between between 25 and 30 horizontal Niobrara wells, along with completing an estimated 250 to 265 refracture and recompletion projects on existing wells.

In 2011, we drilled a total of 17 development wells in the Piceance Basin. We currently estimate that we have more than 390 gross drilling projects, representing multiple years of inventory depending on the number of drilling rigs operating and commodity prices. We expect to maintain a disciplined approach to the development ofsell our Piceance Basin, NECO and certain non-core Colorado oil and gas acreage holdings in 2012, with plans to complete only those wells previously drilled in this area in 2011 as we focus our capital budget in areas expected to generate higher rates of return.

Drilling activity in the Permian Basin in 2011 included 23 development wells,properties, leasehold mineral interests and related assets, including two determined to bederivatives. See Note 19, dry holes. In October 2011, we announced our intent to divest our Permian Basin assets. The divestiture was completed on February 28, 2012. See Acquisitions and Divestitures below and Note 13, Assets Held for Sale, Divestitures and Discontinued Operations, and Note 18Subsequent Events, Subsequent Event, to our consolidated financial statements included elsewhere in this report for additional details related toinformation regarding the divestiture of our Permian assets.planned divestiture. There can be no assurance we will be successful in closing such divestiture.

Eastern Operating Region. We continue to delineate and develop our leasehold position in the Utica Shale. To date, we have drilled two vertical test wells to collect geologic data and two horizontal wells to test the productivity of the acreage. We currently estimate we have approximately 200 gross projects for horizontal drilling in the Utica Shale. In 2013, we expect to devote approximately $53 million of our 2013 capital program primarily toward drilling and completion activity in the Utica Shale, where we plan to drill approximately five horizontal wells targeting the wet gas and crude oil windows of the play.

Our primaryother focus in the Eastern Operating Region is on horizontal drilling in the Marcellus Shale natural gas play consists of horizontal drilling in West Virginia. In 2011,2012, PDCM drilledcompleted a total of 6six gross 3 net,(three net) horizontal wells and constructed various midstream assets to gather and compress its Marcellus gas. PDCM recently announced it has elected to temporarily suspendWe currently estimate we have approximately 600 gross projects for horizontal drilling in the Marcellus Shale play due to the current depressed natural gas price environment. Prior to suspending its drilling activities in 2012,Shale. PDCM expects to drill a total of 414 gross horizontal

Marcellus wells and complete 7 wells, including 3 wells that were in-process as of December 31, 2011.

With the addition of our Ohio leaseholds in late 2011, we have recently begun to focus on exploratory and delineation drilling targeting the wet gas and crude oil windows of the Utica Shale. We drilled one vertical well to total depth in mid-December, which was fracture treated early in 2012. In 2012, we expect to drill approximately two horizontal shale wells with an option to drill two additional vertical wells. Currently, we are pursuing an industry joint venture partner to participate in and share in funding the growth and development in this play. While we expect to identify a partner by mid-2012, we cannot assure we will be successful in securing a partner or developing this acreage.2013.

The following table presents information regarding the number of wells we drilled or participated in and the number of refractures and/or recompletions we performed.Strategically acquire

|

| | | | | | | | | | | | | | | | | | |

| | | Drilling Activity |

| | | Year Ended December 31, |

| | 2011 | | 2010 | | 2009 |

| Operating Region | | Gross | | Net | | Gross | | Net | | Gross | | Net |

| Western (1) | | 186 |

|

| 139.6 |

|

| 204 |

|

| 164.9 |

|

| 92 |

|

| 71.2 |

|

| Eastern | | 9 |

| | 5.2 |

| | 9 |

| | 5.2 |

| | 8 |

| | 8.0 |

|

| Total wells drilled | | 195 |

| | 144.8 |

| | 213 |

| | 170.1 |

| | 100 |

| | 79.2 |

|

| Refractures and Recompletions (2) | | 192 |

| | 177.6 |

| | 46 |

| | 33.7 |

| | 37 |

| | 35.4 |

|

| | | | | | | | | | | | | |

__________

| |

(1) | Includes drilling activity in the Permian Basin. As of December 31, 2011, our Permian assets were held for sale and, on February 28, 2012, the divestiture closed. See Note 13, Assets Held for Sale, Divestitures and Discontinued Operations, and Note 18, Subsequent Event, to our consolidated financial statements included in this report for additional details related to the divestiture of our Permian assets. |

| |

(2) | 190 of the refractures and recompletions occurred in the Wattenberg Field. |

The following tables set forth our developmental and exploratory well drilling activity. There is no correlation between the number of productive wells completed during any period and the aggregate reserves attributable to those wells. Productive wells consist of wells spudded, turned in line and producing during the period. In-process wells represent wells that are in the process of being drilled or have been drilled and are waiting to be fractured and/or for gas pipeline connection during the period.

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Net Development Well Drilling Activity |

| | | Year Ended December 31, |

| | | 2011 | | 2010 | | 2009 |

| Operating Region/Area | | Productive | | In-Process | | Dry | | Productive | | In-Process | | Dry | | Productive | | In-Process | | Dry |

| Western | | | | | | | | | | | | | | | | | | |

| Wattenberg Field | | 86.5 |

| | 13.1 |

| | — |

| | 106.9 |

| | 26.5 |

| | — |

| | 58.3 |

| | 6.9 |

| | — |

|

| Piceance Basin | | 14.0 |

| | 3.0 |

| | — |

| | 18.0 |

| | 7.0 |

| | — |

| | 1.0 |

| | — |

| | — |

|

| Permian Basin (1) | | 14.5 |

| | 5.5 |

| | 2.0 |

| | — |

| | 5.0 |

| | — |

| | — |

| | — |

| | — |

|

| Other | | — |

| | — |

| | — |

| | 0.5 |

| | — |

| | — |

| | 2.0 |

| | — |

| | 1.0 |

|

| Total Western | | 115.0 |

| | 21.6 |

| | 2.0 |

| | 125.4 |

| | 38.5 |

| | — |

| | 61.3 |

| | 6.9 |

| | 1.0 |

|

| Eastern | | | | | | | | | | | | | | | | | | |

| Appalachian Basin | | 0.9 |

| | 2.0 |

| | — |

| | 0.6 |

| | 1.1 |

| | — |

| | 2.0 |

| | — |

| | — |

|

| Total Eastern | | 0.9 |

| | 2.0 |

| | — |

| | 0.6 |

| | 1.1 |

| | — |

| | 2.0 |

| | — |

| | — |

|

| Total net development wells | | 115.9 |

| | 23.6 |

| | 2.0 |

| | 126.0 |

| | 39.6 |

| | — |

| | 63.3 |

| | 6.9 |

| | 1.0 |

|

| | | | | | | | | | | | | | | | | | | |

__________

| |

(1) | As of December 31, 2011, our Permian assets were held for sale and, on February 28, 2012, the divestiture closed. See Note 13, Assets Held for Sale, Divestitures and Discontinued Operations, and Note 18, Subsequent Event, to our consolidated financial statements included in this report for additional details related to the divestiture of our Permian assets. |

|

| | | | | | | | | | | | | | | |

| | Net Exploratory Well Drilling Activity |

| | | Year Ended December 31, |

| | 2011 | | 2010 | | 2009 |

| Operating Region/Area | | In-Process | | Productive | | In-Process | | Productive | | In-Process |

| Western | | | | | | | | | | |

| Wattenberg Field | | — |

| | — |

| | 1.0 |

| | — |

| | — |

|

| Other | | 1.0 |

| | — |

| | — |

| | 1.0 |

| | 1.0 |

|

| Total Western | | 1.0 |

| | — |

| | 1.0 |

| | 1.0 |

| | 1.0 |

|

| Eastern | | | | | | | | | | |

| Appalachian Basin | | 2.3 |

| | 2.8 |

| | 0.7 |

| | 5.0 |

| | 1.0 |

|

| Total Eastern | | 2.3 |

| | 2.8 |

| | 0.7 |

| | 5.0 |

| | 1.0 |

|

| Total net exploratory wells | | 3.3 |

| | 2.8 |

| | 1.7 |

| | 6.0 |

| | 2.0 |

|

| | | | | | | | | | | |

Acquisitions and Divestitures

We typically pursue the acquisition of assets that have a balance of value in producing wells, behind-pipe reserves reserves and high qualityhigh-quality undeveloped drilling locations. In 2010, we began seeking liquid-rich properties with large undeveloped drilling upside where we believe we can utilize our operational abilities to add shareholder value. As weWe have an experienced team of management, engineering and geosciences professionals who identify and evaluate investment opportunities, we may also seek to divest non-core assets to optimize our property portfolio.acquisition opportunities.

Acquisitions

In 2010,June 2012, we initiated a plan to purchase our affiliated partnerships. The acquisition of these partnerships have provided us with immediate growth in both production and proved reserves from assets in which we currently own an operated working interest. We believe that these acquisitions will also allow us to realize operational benefits as well ascompleted the potential to accelerate the refracture/recompletion program of the wells acquired, thus allowing us to optimize revenue opportunities. As of December 31, 2011, we had acquired a total of 12 affiliated partnershipsMerit Acquisition for an aggregate purchase price of $107.7approximately $304.6 million eight, after certain post-closing adjustments. We financed the purchase with cash from the May 2012 offering of which occurredour common stock and a draw on our revolving credit

facility. The acquired assets comprise approximately 29,800 net acres, after post-closing adjustments, located almost entirely in 2011 for an aggregate purchase price of $73 million. We estimate that the 2011 acquisitions added approximately 40 Bcfe in total proved reserves as of December 31, 2011, which includes the non-affiliated investor partners' remaining working interests in a total of 299 gross, 204.2 net, wells located in ourcore Wattenberg Field and Piceance Basin.with significant overlay with our existing acreage position. Following the closing of the Merit Acquisition, our total position in the core Wattenberg Field is approximately 98,600 net acres.

During 2011 and 2012, we obtained the rights to acquireacquired approximately 45,000 net acres of Utica leasehold acres from unrelated third partiesleaseholds, targeting the wet natural gas and crude oil windows of the Utica Shale play throughout southeastern Ohio. Should we exercise our right to acquire all 40,000 acres, we estimate that theOhio, for a purchase price of such leaseholds will approximate $70approximately $92.3 million. A portionAs an early entrant into the development of the options related to these leaseholds will expireUtica Shale, we believe we have gained valuable experience and expertise in August 2012. Currently, we are pursuing an industry joint venture partner to participate inproactively addressing title and share in fundingother issues associated with the growth and development in thisof the play. While we expect to identify a partner by mid-2012, we cannot assure we will be successful in securing a partner or developing this acreage.

In October 2011, PDCM acquired from an unrelated third party 100% of the membership interests of Seneca-Upshur Petroleum, LLC ("Seneca-Upshur"Seneca-Upshur”), a West Virginia limited liability company, from an unrelated third-party for the purchase price of $162.9$139.2 million including a post-closing working capital adjustment of $10.4 million.. The acquisition included approximately 1,340 gross wells producing natural gas from the shallow Devonian Shale and Mississippian formations and all rights and depths to an estimated 100,000 net acres in West Virginia, of which 90,000 acres are prospective for the Marcellus Shale. Substantially all of the acreage acquired is held by production prospective for the Marcellus Shale and is in close proximity to PDCM's existing properties. Pursuant to our joint venture interest in PDCM, our portion of the purchase price was $81.5$69.6 million and we hold a 50% interest in both the wells and acreage acquired. We estimate that the acquisition added approximately 8 Bcfe

In 2010, we initiated a plan to purchase our total proved reserves asaffiliated partnerships. As of December 31, 2011.2012, we had acquired a total of 12 affiliated partnerships for an aggregate purchase price of $107.7 million. The acquisition of these partnerships have provided us with immediate growth in both production and proved reserves from assets in which we currently own an operated working interest.

Manage operational and financial risk

We focus on development drilling programs in resource plays that offer repeatable results capable of driving growth in reserves, production and cash flows. We regularly review acquisition opportunities in our core areas of operation as we believe we can extract additional value from such assets through production optimization, refractures and recompletions and development drilling. In addition, core acquisitions can potentially provide synergies that result in economies of scale from a combined position. While we believe development drilling will remain the foundation of our capital programs, we continue our disciplined approach to acquisitions and exploratory drilling, both of which have the potential to identify new development opportunities.

We believe we proactively employ strategies to help reduce the financial risks associated with the oil and gas industry. One such strategy is to maintain a balanced production mix of natural gas and liquids. Our Western Operating Region produces natural gas, NGLs and crude oil, with a production mix of approximately 60.5% natural gas to 39.5% liquids during 2012. We expect that the Merit Acquisition and our horizontal drilling program will allow us to substantially increase our crude oil and NGL production. While our legacy properties in the Eastern Operating Region primarily produce natural gas, our Ohio properties are prospective in the wet gas and crude oil windows of the Utica Shale. This strategy of a diversified commodity mix helps to mitigate the financial impact from a decline in the market price in any one of our commodities. In addition, we utilize commodity-based derivative instruments to manage a substantial portion of our exposure to price volatility with regard to our natural gas and crude oil sales and natural gas marketing. As of December 31, 2012, we had natural gas and crude oil derivative positions in place for 2013 covering approximately 28.7 Bcfe of our natural gas production and approximately 2,326 MBbls of our crude oil production. Currently, we do not hedge our NGL production. See Part II, Item 7A, Quantitative and Qualitative Disclosures about Market Risk, for a detailed summary of our open derivative positions.

Divestitures

Permian Basin. In October 2011, we announced our intent to divest our acreage located in the Wolfberry Trend in the Permian Basin in West Texas to focus our efforts inour horizontal drilling programs and to provide funding for our 2012 capital budget. During the fourth quarter of 2011, we completed the sale of our non-core Permian assets to unrelated third parties for a total of $13.2 million. On December 20, 2011, we executed a purchase and sale agreement with another unrelated third party for the sale of our core Permian assets for a total price of $173.9 million, subject to customary post-closing adjustments. The transaction closed on February 28, 2012 with total proceeds received of $184.4 million after preliminary closing adjustments. The proceeds from the sales were used to pay down our corporate credit facility, until needed to fund our 2012 capital budget. The Permian Basin assets were classified as held for sale as of December 31, 2011 and 2010, and the results of operations related to those assets were reported as discontinued operations in 2010, year of acquisition, and 2011 on our consolidated statements of operations included in this report.

North Dakota. In December 2010, we effected a letter of intent with an unrelated third party for the sale of our North Dakota assets. The North Dakota assets were classified as held for sale as of December 31, 2010, and the results of operations related to those assets were reported as discontinued operations in 2009, 2010 and 2011 on our consolidated statements of operations included in this report. In February

2011, we executed a purchase and sale agreement and subsequently closed with the same unrelated party. Proceeds from the sale were $9.5 million, net of non-affiliated investor partners' share of $3.8 million, resulting in a pretax gain on sale of $3.9 million.

ExplorationSelective exploration

We believe that our disciplined exploration program has the potential to consistently replenish our portfolio with new exploration projects capable of positioning us for significant production and reserve growth in future years. Due to the continued decline in natural gas prices, we have focused our efforts toward liquid-rich plays to take advantage of the current attractive economics associated with crude oil and NGL weighted projects. We strive to identify potential plays in their early stages in an attempt to accumulate significant leasehold positions prior to competitive forces driving up the cost of entry. We seek investment in leasehold positions that are in the proximity of existing or emerging pipeline infrastructures. We believe the leaseholdsleasehold we acquired targeting the Utica Shale meetmeets these criteria and we see these leaseholdsthe derisking and delineation of this leasehold as our primary exploration playfocus during for 2012.

Manage Operational and Financial Risk

We focus on lower risk development drilling programs in resource plays with repeatable drilling opportunities that will grow reserves and production while maintaining or growing cash flows. We regularly review acquisition opportunities in our core areas of operation as we believe we can enhance the value of such opportunities through economies of scale. We believe development drilling will remain the foundation of our drilling programs; however, we view a disciplined approach to exploratory drilling as having the potential to identify new development opportunities, as we have done in recent years with our horizontal Niobrara and Marcellus drilling programs.

We engage in limited exploratory drilling as such activities involve numerous risks, including the risk that we may not be successful in the discovery of commercially productive natural gas and crude oil reservoirs. Costs associated with exploratory activities can be quite high. In an effort to mitigate in part the financial risk associated with exploratory activities, we may seek opportunities to participate in joint venture arrangements to share in the potential high costs and risks of exploratory drilling while maximizing the potential returns. We believe our Marcellus JV has effectively served to mitigate the risks associated with exploring the Marcellus Shale. We are currently seeking an investment partner to participate with us in exploring our newly acquired Ohio properties, which are prospective for the wet gas and crude oil windows of the Utica Shale. We cannot assure we will be successful in securing a joint venture partner or developing this acreage.

We believe we proactively employ strategies to help reduce the financial risks associated with the oil and gas industry. One such strategy is to maintain a balanced production mix of natural gas and liquids. Our Western Operating Region produces natural gas, NGLs and crude oil, with a production mix of approximately 65% natural gas to 35% liquids. While our legacy properties in the Eastern Operating Region primarily produce natural gas, our Ohio properties are prospective for the wet gas and crude oil windows of the Utica Shale. This strategy of a diversified commodity mix helps to mitigate the financial impact from a decline in the market price in any one of our commodities. In addition, we utilize commodity-based derivative instruments to manage a portion of our exposure to price volatility with regard to our natural gas and crude oil sales and natural gas marketing. We utilize both financial and physical derivative instruments. The financial instruments consist of floors, collars, swaps and basis swaps and consist of NYMEX, CIG and PEPL-based contracts. We may utilize derivatives based on other indices or markets where appropriate. The contracts provide price stability for up to 80% of our committed and anticipated natural gas and crude oil sales and purchases forecasted to occur within the next five-year period. Our policies prohibit the use of commodity derivatives for speculative purposes and permit utilization of derivatives only if there is an underlying physical position. As of December 31, 2011, we had natural gas and crude oil derivative positions in place for 2012 covering 59.1% of our expected natural gas production and 60.8% of our expected crude oil production. Currently, we do not hedge our NGL production. See Item 7A, Quantitative and Qualitative Disclosures about Market Risk, for a detailed summary of our open derivative positions.

Riley Natural Gas ("RNG"), a wholly-owned subsidiary, uses financial derivatives in its gas marketing operations to augment its fixed purchases and sales. RNG also enters into back-to-back fixed-price physical purchases and sales contracts with counterparties. RNG does not always hedge the area basis risk for third party trades with back-to-back fixed price purchases and sales. We continue to evaluate the potential for reducing this risk by entering into derivative transactions. Further, we may choose to close out any portion of a derivative contract existing at any time, which may result in a realized gain or loss on that derivative transaction.2013.

Business Segments

We divide our operating activities into two segments: (1) Oil and Gas Exploration and Production and (2) Gas Marketing.

Oil and Gas Exploration and Production

Our Oil and Gas Exploration and Production segment primarily reflects revenues and expenses from the production and sale of natural gas, NGLs and crude oil.

Natural gas. We primarily sell our natural gas to midstream marketers, utilities, industrial end-users and other wholesale purchasers. We primarilygenerally sell the natural gas that we produce under contracts with indexed or NYMEX monthly pricing provisions, with the remaining production sold under contracts with daily pricing provisions. Virtually all of our contracts include provisions wherein prices change monthly with changes in the market, for which certain adjustments may be made based on whether a well delivers

to a gathering or transmission line and the quality of the natural gas and prevailing supply and demand conditions.gas. Therefore, the price of the natural gas fluctuates to remain competitive with other available natural gas supplies. As a result, our revenues from the sale of

natural gas, holding production volume constant, increase as market prices increase and decrease as market prices decline. We believe that the pricing provisions of our natural gas contracts are customary in the industry.

NGLs. The majority of our NGLs are sold to one NGL marketer in the Wattenberg Field. Our NGL production is sold under both short- and long-term purchase contracts with monthly pricing provisions based on an average daily price.

Crude oil. We do not refine any of our crude oil production. We sell our crude oil to oil marketers and refiners. Our crude oil production is sold to purchasers at or near our wells under both short and long-term purchase contracts with monthly pricing provisions based on an average daily price.

NGLs. The majority of our NGLs are sold to one NGL marketer in the Wattenberg Field. Our NGL production is sold under both shortshort- and long-term purchase contracts with monthly pricing provisions based on an average daily price.

We enter into financial derivatives in order to reduce the impact of possible price volatility regarding the physical sales market. See Part II, Item 7, Management’sManagement's Discussion and Analysis of Financial Condition and Results of Operations: Results of Operations –- Commodity Price Risk Management, Net, Natural Gas and Crude Oil Derivative Activities, Item 7A, Quantitative and Qualitative Disclosures about Market Risk, and Note 4, Derivative Financial Instruments, to our consolidated financial statements included elsewhere in this report.

Our Oil and Gas Exploration and Production segment also reflects revenues and expenses related to well operations and pipeline services. We are paid a monthly operating fee for the portion of each well we operate that is owned by others, including our affiliated partnerships. We believe the fee is competitive with rates charged by other operators in the area. As we acquire the working interest of our non-affiliated investor partners in our affiliated partnerships, revenues related to well operations and pipeline services will decrease.

We construct, own and operate gathering systems in some of our areas of operations. Pipelines and related facilities can represent a significant portion of the capital costs of developing wells, particularly in new areas located at a distance from existing pipelines. We consider these costs in the evaluation of our leasing, development and acquisition opportunities.

Our natural gas and NGLs areis transported through our own and third partythird-party gathering systems and pipelines, and we incur gathering, processing and transportation expenses to move our natural gas from the wellhead to a purchaser-specified delivery point. These expenses vary based onupon the volume and distance shipped, andas well as the fee charged by the third-party processor or transporter. Capacity on these gathering systems and pipelines is occasionally interrupted due to operational issues, repairs or improvements. A majorityportion of our natural gas is transported under interruptible contracts and thusthe remainder under firm transportation agreements, either directly with RNG or through third-party processors or marketers. Therefore, interruptions in natural gas sales could result if pipeline space is constrained, resultconstrained. As discussed in an interruption inPart II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations - Operational Overview, our 2012production was adversely affected by high line pressures experienced by our principal third-party provider of natural gas sales.gathering, processing and transportation facilities in the Wattenberg Field. The high line pressure was the result of a series of operational issues and capacity constraints, primarily in the second and third quarters. The operational issues included downtime on downstream third-party NGL transportation and fractionation facilities and abnormally warm weather, which limited third-party gathering system compression capacity. We are working closely with our primary midstream provider who is implementing a multi-year facility expansion capable of significantly increasing long-term gathering and processing capacity in the Wattenberg Field. However, we do not expect the impact of this increased capacity to substantially benefit us until late 2013. While our ability to market these volumes of natural gas has been only infrequently limited or delayed, if transportation space is restricted or is unavailable, our production and cash flowflows from the affected properties could be adversely affected.

In certain instances, we enter into firm transportation agreements to provide for pipeline capacity to flow and sell a portion of our natural gas volumes. In order to meet pipeline specifications, we are required, in some cases, to process our natural gas before we can transport it. We typically contract with third parties in the Piceance Basin and the NECO areasarea of our Western Operating Region and our Eastern Operating Region for firm transportation of our natural gas. We also may enter into firm sales agreements to ensure that we are selling to a purchaser who has contracted for pipeline capacity. These agreements are subject to the same limitations discussed above in this paragraph. See Note 11, Commitments and Contingencies - Firm Transportation Agreements, to our consolidated financial statements included elsewhere in this report for our long-term firm sales, processing and transportation agreements for pipeline capacity.

Our crude oil production is marketed directly to purchasers in the Wattenberg Field area under a combination of annual and short-term monthly agreements. The majority of our crude oil is delivered to local area refineries with other volumes being either trucked or shipped via pipeline out of the Wattenberg area.

See Part II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations - Results of Operations, Summary Operating Results, for production, sales, prices and lifting cost data for each of the years in the three-year period ended December 31, 2011.2012.

Gas Marketing

Our Gas Marketing segment is comprised solely of the operating activities of RNG. RNG specializes in the purchase, aggregation and sale of natural gas production in the Eastern Operating Region. RNG purchases for resale natural gas produced by third partythird-party producers, as well as natural gas produced by us, PDCM and our affiliated partnerships. The natural gas is marketed to third partythird-party marketers, natural gas utilities as well asand industrial and commercial customers, either directly through our gathering system or through transportation services provided by regulated interstate pipeline companies. Additionally, RNG markets our natural gas production in the NECO area.

For additional information regarding our business segments, see Note 17,18, Business Segments, to our consolidated financial statements included elsewhere in this report.

Areas of Operations

The following map presents the general locations of our development, production and exploration activities as of December 31, 2011.2012. With the divestiture of our Permian Basin assets on February 28, 2012, our development, production and exploration efforts are primarily focused in two geographic areas of the U.S.

(1) On February 4, 2013, we entered into a purchase and sale agreement with certain affiliates of Caerus, pursuant to which we have agreed to sell our Piceance Basin, NECO and certain non-core Colorado oil and gas properties, leasehold mineral interests and related assets, including derivatives. See Note 19, Subsequent Events, to our consolidated financial statements included elsewhere in this report for additional information regarding the planned divestiture. There can be no assurance we will be successful in closing such divestiture.

Western Operating Region

Our primary focus in the Western Operating Region for 20122013, and we expect for the near termnext several years, is on horizontal Niobrara and Codell development drilling. We divide our Western Operating Region into two majorthe following areas: the Wattenberg Field and Piceance Basin.

Wattenberg Field, DJ Basin, Colorado. WellsCurrently, wells drilled in this area have historically been vertical and range from approximately 7,000 to 8,000 feet in depth. Theseare horizontal wells targettargeting the liquid-rich reservoirs in the Codell and Niobrara formations that have historically contained about 50% crude oil and NGLs. In October 2010, we began aformations. These horizontal drilling program targeting the liquid-rich Niobrara formation. The horizontal Niobrara wells have a vertical depth range from approximately 7,000 to 8,000 feet, with an average lateral length of 4,000 feet. OperationsWe drill multi-well pads to further optimize costs and enhance horizontal drilling efficiencies in the Wattenberg Field. Pad drilling enables us to streamline the transition to increased well density in the horizontal Niobrara and Codell plays. We have approximately 3,300 gross projects, including over 1,400 proved and probable horizontal projects, in the liquid-rich Wattenberg Field.

In June 2012, we completed an acquisition of approximately 29,800 net acres in the core area, which positions us as the third largest producer and leaseholder in the core Wattenberg area. We estimate that the Wattenberg Field has approximately 400 horizontal drilling locations based on 4 gross wells per section for our proved undeveloped reserves ("PUDs"). Additional potential upside exists as we continue testing the Codell formation and plan to test downspacing to 10 gross wells per section in addition to developmental drilling, include athe play as part of our 2013 horizontal program, which is the basis for our estimate of refractures and recompletion projects on existingover 1,400 horizontal wells in the Codellour proved and Niobrara reservoirs.probable inventory.

Piceance Basin, Colorado. Wells in this area predominately target natural gas withfrom the area's volume ofWilliams Fork formation. For 2012, we removed all PUD reserves in the Piceance Basin due to low natural gas prices. Our 2012 Piceance natural gas reserves representingwere 66.5 Bcfe, or approximately 47%6% of our total proved natural gasequivalent reserves. Our Piceance reserves which equates to approximately 32% of our total proved reserves. Reserves in this area represent approximately 1%2% of our

present valuePV-10% as of future net revenues ("PV-10%"), a non-U.S. GAAP measure.December 31, 2012. See table in the Properties -Proved- Proved Reserves section below for information regarding our proved reserves and PV-10% as of December 31, 2011. While all inputs to the cash flow model must be evaluated at each date that the estimate of future cash flows for each producing basin is calculated, a significant decrease in long-term forward natural gas prices alone could result in a significant impairment for our properties that are sensitive to declines in natural gas prices.2012.

The majority of the wells drilled in this area are drilled directionally from multi-well drilling pads, generally range from two to ten wells per pad and range from 7,000 to 9,500 feet in depth. Reserves in this area originate from multiple sandstone reservoirs in the Mesaverde Williams Fork formation. Well spacing is approximately ten acres per well.

Northeastern Colorado ("NECO"). Wells drilled in this arearea range from 1,500 to 3,000 feet in depth and target natural gas reserves in the shallow Niobrara reservoir. We have not conducted drilling activity in this area since 2009.Well spacing is approximately 40 acres per well.

Permian Basin.As of December 31, 2011, our Permian assets were held for sale and,noted above, on February 28, 2012,4, 2013, we entered into a purchase and sale agreement with Caerus pursuant to which Caerus agreed to purchase our Piceance Basin, NECO and other non-core Colorado leasehold mineral interests and various other assets within these basins for an aggregate cash consideration of approximately $200 million, subject to post-closing adjustments. The cash consideration is subject to customary adjustments, including adjustments based upon title and environmental due diligence, and by certain firm transportation obligations and natural gas hedging positions that will be assumed by Caerus as part of the divestiture closed. See Note 13, Assets Held for Sale, Divestiturestransaction. The effective date of the transaction is January 1, 2013. We intend to use the proceeds from the sale to repay a portion of amounts outstanding under our revolving credit facility and Discontinued Operations, and Note 18, Subsequent Event, topartially fund our consolidated financial statements included2013 capital program. There can be no assurance we will be successful in this report for additional details related to the divestiture of our Permian assets.

closing such divestiture.

Eastern Operating Region

Our primary focus in the Eastern Operating Region is on horizontal drilling in the Utica Shale in southeastern Ohio and the Marcellus Shale play in northern West Virginia and, with the addition of leaseholds in Ohio during 2011, exploratory and delineation drilling in the emerging Virginia.

Utica Shale, play.

8Ohio. We have acquired approximately 45,000 net acres targeting the wet natural gas and crude oil windows of the Utica Shale play throughout southeastern Ohio. To date, we have drilled and completed two horizontal wells in Guernsey County that are currently waiting on first production, as well as two stratigraphic vertical test wells to collect engineering and geologic data to test the productivity of the acreage. The horizontal wells have a vertical depth range of approximately 7,000 feet, with an average lateral length of 4,000 feet.

Marcellus Shale, West Virginia. In October 2009, through our contribution of the majority of our Eastern Operating Region assets, consisting of acreage, producing properties and related reserves, gathering assets and equipment, and a cash contribution byThrough our joint venture, partner,PDCM, we formed the joint venture PDCM. The wells contributed were producing from the shallow Devonian and Mississippian aged tight sandstone reservoirs, ranging from 1,200 to 6,000 feet in depth. In October 2011, PDCM acquired all rights and depths to 100,000have over 236,000 net acres of which 90,000 netin the Appalachian Basin, with approximately 152,000 acres are prospective for the Marcellus Shale, and added an additional 1,340 gross wells producing from the Devonian and Mississippian formations.majority of which is in northern West Virginia. PDCM is primarily focused on horizontal drilling targeting theand has approximately 600 Marcellus Shale formation in northerngross drilling locations on the West Virginia.Virginia acreage. These wells have a vertical depth range from approximately 7,000 to 8,000 feet, with lateral lengths ranging from 4,000 to 6,000 feet.

In addition to our ownership interest in the wells held by PDCM, we own an interest in approximately 311236 gross 106.2 net,(77.9 net) natural gas and crude oil wells in West Virginia Pennsylvania and Tennessee.

Utica Shale, Ohio. Our newest prospect is the Utica Shale play in southeastern Ohio, with our initial leasehold acquisitions occurring in 2011. Exploratory drilling activity began in the fourth quarter, with one vertical well drilled to total depth, approximately 9,600 feet, and subsequently fracture treated in early 2012. We continue to pursue an industry joint venture partner to participate in and share in funding the growth and development in this play; however, we cannot assure we will be successful in securing a partner or developing the play.

Pennsylvania.

Properties

Productive Wells

The following table presents our productive wells.wells:

| | | | | Productive Wells | | Productive Wells |

| | | As of December 31, 2011 | | As of December 31, 2012 |

| | | Natural Gas | | Crude Oil | | Total | | Natural Gas | | Crude Oil | | Total |

| Operating Region/Area | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net |

| Western | | | | | | | | | | | | | | | | | | | | | | | | |

| Wattenberg Field | | 1,762 |

| | 1,456.0 |

| | 24 |

| | 19.1 |

| | 1,786 |

| | 1,475.1 |

| | 2,523 |

| | 2,181.2 |

| | 91 |

| | 71.8 |

| | 2,614 |

| | 2,253.0 |

|

| Piceance Basin | | 348 |

| | 301.4 |

| | — |

| | — |

| | 348 |

| | 301.4 |

| |

| Permian Basin (1) | | — |

| | — |

| | 58 |

| | 54.5 |

| | 58 |

| | 54.5 |

| |

| NECO | | 618 |

| | 410.0 |

| | — |

| | — |

| | 618 |

| | 410.0 |

| |

| Other | | 97 |

| | 95.0 |

| | 3 |

| | 0.7 |

| | 100 |

| | 95.7 |

| | 1,057 |

| | 800.7 |

| | — |

| | — |

| | 1,057 |

| | 800.7 |

|

| Total Western | | 2,825 |

| | 2,262.4 |

| | 85 |

| | 74.3 |

| | 2,910 |

| | 2,336.7 |

| | 3,580 |

| | 2,981.9 |

| | 91 |

| | 71.8 |

| | 3,671 |

| | 3,053.7 |

|

| Eastern | | | | | | | | | | | | | | | | | | | | | | | | |

| Appalachian Basin | | 3,568 |

| | 1,652.4 |

| | 39 |

| | 15.5 |

| | 3,607 |

| | 1,667.9 |

| | 3,565 |

| | 1,654.5 |

| | 6 |

| | 3.7 |

| | 3,571 |

| | 1,658.2 |

|

| Total Eastern | | 3,568 |

| | 1,652.4 |

| | 39 |

| | 15.5 |

| | 3,607 |

| | 1,667.9 |

| | 3,565 |

| | 1,654.5 |

| | 6 |

| | 3.7 |

| | 3,571 |

| | 1,658.2 |

|

| Total productive wells | | 6,393 |

| | 3,914.8 |

| | 124 |

| | 89.8 |

| | 6,517 |

| | 4,004.6 |

| | 7,145 |

| | 4,636.4 |

| | 97 |

| | 75.5 |

| | 7,242 |

| | 4,711.9 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

__________

| |

(1) | As of December 31, 2011, our Permian assets were held for sale and, on February 28, 2012, the divestiture closed. See Note 13, Assets Held for Sale, Divestitures and Discontinued Operations, and Note 18, Subsequent Event, to our consolidated financial statements included in this report for additional details related to the divestiture of our Permian assets. |

Proved Reserves

Our proved reserves are sensitive to future natural gas, NGLs and crude oil sales prices and theirthe related effect on the economic productive life of producing properties. Increases in commodity prices may result in a longer economic productive life of a property or result in more economically viable proved undeveloped reserves to be recognized. Decreases in commodity prices may result in negative impacts of this nature.

All of our proved reserves are located onshore in the U.S. Our reserve estimates are prepared with respect to reserve categorization, using the definitions for proved reserves set forth in SEC Regulation S-X, Rule 4-10(a) and subsequent SEC staff regulations, interpretations and guidance. AllAs of December 31, 2012, all of our proved reserves, as of December, 31, 2011, including the reserves of all subsidiaries consolidated for the purposes of our financial statements, have been estimated by independent petroleum engineers.

We have a comprehensive process that governs the determination and reporting of our proved reserves. As part of our internal control process, our reserves are reviewed annually by an internal team composed of reservoir engineers, geologists and accounting personnel for adherence to SEC guidelines through a detailed review of land records, available geological and reservoir data, as well as production performance data. The process includes a review includes, but is not limited to, confirmation that reserve estimates (1) include all properties owned, (2) are based on properof applicable working and net revenue interests and (3) reflect reasonable cost estimates and field performance.performance data. The internal team compiles the reviewed data and forwards the data to an independent engineering firm engaged to estimate our reserves.

Our reserve estimates as of December 31, 2011,2012 were based on a reserve report prepared by Ryder Scott Company, L.P. ("Ryder Scott").Scott. When preparing our reserve estimates, the independent petroleum engineerRyder Scott did not independently verify the accuracy and completeness of information and data furnished by us with respect to ownership interests, production volumes, well test data, historical costs of operations and development, product prices or any agreements relating to current and future operations of properties and sales of production.

The independent petroleum engineerRyder Scott prepares an estimate of our reserves in conjunction with an ongoing review by our engineers. A final comparison of data is performed to ensure that the reserve estimates are complete, determined by acceptable industry methods and to a level of detail we deem appropriate. TheRyder Scott's final independent petroleum engineer's estimated reserve report is reviewed and approved by our engineering staff and management.