THE BRINK’S COMPANY

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 20132014

TABLE OF CONTENTS

PART I

| Page | ||

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 7 |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

| Executive Officers of the Registrant | ||

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer | |

| Purchases of Equity Securities | ||

| Item 6. | Selected Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| Item 9B. | Other Information | |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accountant Fees and Services | |

| PART IV | ||

| Item 15. | Exhibits and Financial Statement Schedules |

| PART I |

ITEM 1. BUSINESS

Overview

The Brink’s Company is a premier provider of secure logistics and security solutions, including cash-in-transit, ATM replenishment and maintenance, secure international transportation of valuables, and cash management services, to financial institutions, retailers, government agencies including(including central banks,banks), mints, jewelers and other commercial operations around the world. Our internationalglobal network serves customers in more than 100 countries and employsincludes ownership interest in 41 countries and agency relationships with companies in additional countries. We employ approximately 65,100 people. Our64,100 people and our operations include approximately 1,0001,100 facilities and 12,70012,300 vehicles. Brink’s was founded in 1859 and The Brink’s Company was first incorporated in 1930 under the laws of the State of Delaware (at that time, the Company was named The Pittston Company). It succeeded to the business of a Virginia corporation in 1986 and was renamed The Brink’s Company in 2003. Our headquarters are located in Richmond, Virginia. A significant portion of our business is conducted internationally, with 82% of our $3.9 billion in revenues earned outside the United States. The Brink’s Company, along with its subsidiaries, is referred to as “we,” “our,”, “us,” “Brink’s,” or “the Company” throughout this Form 10-K.

Brink’s operations are located throughout the world with the majority80% of our revenues (77%) and segment94% of operating profit (98%) earned outside of North America.

| (In millions) | 2014 | % total | % change | 2013 | % total | % change | 2012 | % total | % change | |||||||

| Revenues by segment: | ||||||||||||||||

| Largest 5 Markets: | ||||||||||||||||

| U.S. | $ | 727.8 | 20 | 3 | $ | 707.5 | 19 | - | $ | 706.7 | 20 | (4) | ||||

| France | 517.4 | 15 | - | 517.6 | 14 | 1 | 511.4 | 14 | (1) | |||||||

| Mexico | 388.2 | 11 | (8) | 423.9 | 11 | 7 | 395.0 | 11 | 2 | |||||||

| Brazil | 364.1 | 10 | 3 | 354.4 | 9 | (3) | 363.6 | 10 | 1 | |||||||

| Canada | 179.7 | 5 | (6) | 191.4 | 5 | 2 | 187.5 | 5 | (1) | |||||||

| Largest 5 Markets | 2,177.2 | 61 | (1) | 2,194.8 | 58 | 1 | 2,164.2 | 60 | (1) | |||||||

| Latin America | 592.4 | 17 | (31) | 854.2 | 23 | 15 | 744.4 | 21 | 17 | |||||||

| EMEA | 556.3 | 16 | 3 | 540.6 | 14 | 7 | 503.1 | 14 | (4) | |||||||

| Asia | 139.8 | 4 | 4 | 134.2 | 4 | 7 | 125.9 | 4 | - | |||||||

| Global Markets | 1,288.5 | 36 | (16) | 1,529.0 | 40 | 11 | 1,373.4 | 38 | 7 | |||||||

| Payment Services | 96.6 | 3 | 76 | 54.8 | 1 | 37 | 40.0 | 1 | (1) | |||||||

| Total Revenues | $ | 3,562.3 | 100 | (6) | $ | 3,778.6 | 100 | 6 | $ | 3,577.6 | 100 | 2 | ||||

| Amounts may not add due to rounding. | ||||||||||||||||

| (In millions) | 2013 | % total | % change | 2012 | % total | % change | 2011 | % total | % change | ||||||||||||||||

| Revenues by region: | |||||||||||||||||||||||||

| Latin America: | |||||||||||||||||||||||||

| Mexico | $ | 450.4 | 11 | 6 | $ | 424.0 | 11 | 2 | $ | 415.2 | 11 | fav | |||||||||||||

| Venezuela | 447.1 | 11 | 31 | 342.6 | 9 | 27 | 269.2 | 7 | 45 | ||||||||||||||||

| Brazil | 392.0 | 10 | 1 | 388.3 | 10 | - | 386.8 | 11 | 28 | ||||||||||||||||

| Other | 431.2 | 11 | 2 | 424.5 | 11 | 9 | 389.5 | 11 | 16 | ||||||||||||||||

| Total | 1,720.7 | 44 | 9 | 1,579.4 | 42 | 8 | 1,460.7 | 40 | 66 | ||||||||||||||||

| EMEA | |||||||||||||||||||||||||

| France | 542.5 | 14 | 1 | 535.5 | 14 | (2) | 545.2 | 15 | 7 | ||||||||||||||||

| Other | 635.8 | 16 | 8 | 590.4 | 16 | (1) | 597.8 | 16 | 16 | ||||||||||||||||

| Total | 1,178.3 | 30 | 5 | 1,125.9 | 30 | (1) | 1,143.0 | 31 | 12 | ||||||||||||||||

| North America | |||||||||||||||||||||||||

| U.S. | 707.5 | 18 | - | 706.7 | 19 | (4) | 733.5 | 20 | - | ||||||||||||||||

| Canada | 190.9 | 5 | 2 | 186.6 | 5 | (2) | 189.9 | 5 | 2 | ||||||||||||||||

| Total | 898.4 | 23 | 1 | 893.3 | 24 | (3) | 923.4 | 25 | 1 | ||||||||||||||||

| Asia Pacific | 144.8 | 4 | 6 | 136.4 | 4 | - | 135.8 | 4 | 27 | ||||||||||||||||

| Total Revenues | $ | 3,942.2 | 100 | 6 | $ | 3,735.0 | 100 | 2 | $ | 3,662.9 | 100 | 25 | |||||||||||||

| Amounts may not add due to rounding. | |||||||||||||||||||||||||

Geographic financial information related to revenues and long-lived assets is included in the consolidated financial statements on page 82.77.

1

Mission and Strategy

Our mission is to be the world’s leading provider of secure logistics services for cash and other valuables. Our goal is to achieve consistent growth in revenues, profits, cash flows and shareholder value. Our near-term focus is on maximizing operating efficiency to enhance profitability and competitive position. We believe this will enhance our ability to pursue growth opportunities.

Our primary strategy is to focus our efforts and investments on our five largest countries (U.S., France, Mexico, Brazil and Canada). Our greatest near-term opportunity is to execute profit turnarounds in the U.S. and Mexico, which together generated revenues of $1.1 billion in 2014.

Our cost and productivity initiatives are supplemented by efforts to expand the breadth of our supply chain services. As we achieve success in our large markets, we will integrate these services into smaller markets.

Growing Profits with Cost and Productivity Improvements

Achieving substantial improvements in operational efficiency is critical to enhancing our competitive position and pursuing future growth. Our efforts to improve operational efficiency include:

| · | consolidating organizational structure to streamline management and administrative expenses |

| · | centralizing support functions to reduce costs and enable country-level operating management to focus on customers and operations |

| · | using “Lean” principles to improve processes and reduce costs at the branch level |

| · | improving route logistics with IT-based productivity tools |

| · | leveraging global purchasing power to reduce costs for vehicles, equipment, maintenance, travel and other services |

Growing Revenues by Expanding Service Offerings

Collaborating with customers and providing new services will help us grow our business. We plan to expand our services across our customers’ entire cash and valuable supply chains and business processes. Improving our customers’ supply-chain efficiency reduces the total cost of the process, improves our value-added pricing and generates opportunities for customers to outsource more services to Brink’s. These opportunities include:

| · | integrated armored transportation and money processing services |

| · | full-service management of entire ATM networks |

| · | CompuSafe® service (“intelligent safes”) |

| · | new market opportunities for Global Services |

Transforming Culture: Accountability, Customer Focus and Trust (“ACT”)

As part of our ongoing cultural transformation, we continue to promote ACT and endeavor to ensure that our employees demonstrate these values and related behaviors. We will place leaders who consistently demonstrate ACT behaviors in our most critical roles.

2014 Reorganization and Restructuring

We announced a reorganization and restructuring of Brink’s global organization in the fourth quarter of 2014, followed by the announcement in February 2015 of an additional reduction in our global workforce. These actions accelerate the execution of our growth strategy by reducing costs and providing for a more streamlined and centralized organization. We believe these actions will save direct costs of approximately $45 to $50 million in 2015 compared to 2014, excluding severance, lease termination and pension settlement charges. Following is a summary of key actions in connection with the reorganization and restructuring:

| · | We reorganized the majority of Brink’s country operations under two business units: Largest 5 Markets (including U.S., France, Mexico, Brazil and Canada), and Global Markets (the 36 countries besides the Largest 5 Markets). Country operations typically provide Cash-in-Transit (“CIT”) Services, ATM Services, Cash Management Services and Global Services. Reporting lines within these two business units are supplemented by a matrixed centralized management of the Global Services operations. |

| · | We decided to maintain our centralized organization structure for the Payment Services business. |

| · | We centralized the reporting structure of our support functions, including IT, HR, finance, legal, procurement, security and project management. Under the new structure, field employees now report to the global functional leaders instead of the country or regional leaders. |

| · | We eliminated regional roles and structures in Europe, Middle East and Africa (“EMEA”) and Latin America and are planning to exit the regional office leased spaces in 2015. |

| · | We substantially completed a global workforce reduction of 1,700 positions, which accounts for $30 to $35 million of the projected 2015 savings. |

2

Beginning in 2014, as a result of the restructuring, we report financial results in the following nine operating segments:

| · | Each of the five countries within Largest 5 Markets (U.S., France, Mexico, Brazil and Canada) |

| · | Each of the three regions within Global Markets (Latin America, EMEA and Asia representing a total of 36 countries) |

| · | Payment Services |

Previously, the our reportable segments were: Latin America, EMEA, North America and Asia Pacific.

Financial information related to our segments and amounts not allocated to segments is included in the consolidated financial statements on pages 74–78.

Other Important Events and Transactions in 2014

In addition to the 2014 Reorganization and Restructuring, the following key events and transactions occurred in 2014.

U.S. retirement plans. We contributed $87 million to our primary U.S. pension plan in 2014 and do not expect to contribute additional amounts in the future. We also completed a buy-out of the pension benefits of 4,300 plan participants. After the buy-out, there are approximately 15,200 beneficiaries in the plan. The buy-out significantly reduced the plan assets and obligations and resulted in a settlement loss in the fourth quarter of 2014 of $56 million. We adopted new mortality tables to estimate the obligations of our U.S. retirement plans, which increased the obligations by approximately $90 million.

Venezuela. We adopted a new currency exchange rate in March 2014 to report our Venezuela operations. The new rate is 88% less favorable than the previous rate. Translating our Venezuelan operations at the new rate significantly reduces the portion of our consolidated results attributable to Venezuela.

Sale of Netherlands business. We sold our Netherlands operations in December 2014 after a major customer notified us we would lose their business in 2015. The business had $126 million in revenues in 2014.

Sale of ownership interest in Peru business. We sold a noncontrolling interest in a CIT business based in Peru during 2014.

Services

Core Services (55%52% of total revenues in 2013)2014)

CIT and ATM Services are core services we provide to customers throughout the world. We charge customers per service performed or based on the value of goods transported. As a result, revenues are affected by the level of economic activity in various markets as well as the volume of business for specific customers. Core services generated approximately $2.2$1.9 billion of revenues in 2013.2014.

CIT Services – Serving customers since 1859, our success in CIT is driven by a combination of rigorous security practices, high-quality customer service, risk management and logistics expertise. CIT Services generally include the secure transportation of:

| · | cash between businesses and financial institutions, such as banks and credit unions |

| · | cash, securities and other valuables between commercial banks, central banks and investment banking and brokerage firms |

| · | new currency, coins, bullion and precious metals for central banks and other customers |

ATM Services – We manage 91,000 ATMs worldwide. We provide customers who own and operate ATMs a variety of service options. We manage 88,800 ATMs worldwide.provide basic ATM management services using our secure transportation network, including cash replenishment and first and second line maintenance. We also provide comprehensive services for ATM management through our Brink's Integrated Managed Services (“Brink’s IMS”) offering. Brink's IMS’s offerings include cash replenishment, replenishment forecasting, cash optimization, ATM remote monitoring, service call dispatching, transaction processing, installation services, and first and second line maintenance.

High-Value Services (37%39% of total revenues in 2013)2014)

Our Core Services, combined with our brand and global infrastructure, provide a substantial platform from which we offer additional High-Value Services. High-Value Services generated approximately $1.5$1.4 billion of revenues in 2013.2014.

Global Services – Serving customers in more than 100 countries, Brink’s is a leading global provider of secure logistics, serving customers in over 100 countries. We provide customers with secure transportation services, picking up valuables from customer locations, packing them for valuables includingtransport, and managing customs clearance as the package enters a country. We also offer secure vault storage and inventory management of customer valuables. We use a combination of armored vehicles and secure air and sea transportation. Valuables transported by our Global Services business include diamonds, jewelry, precious metals, securities, currency, high-tech devices, electronics and pharmaceuticals. Our comprehensive suite of services includes packing, pickup, secure storage, inventory management, customs clearance, consolidation and secure transport and delivery through a combination of armored vehicles and secure air and sea transportation to leverage our extensive global network. Our specialized diamond and jewelry operations have offices in the world’s major diamond and jewelry centers.

Cash Management Services – We offer customized Cash Management Services based on customers’ unique needs. A customer may have simple requirements or may benefit from Brink’s offers a fully integrated approach to managing thetheir supply chain of cash,cash. Customers may elect to receive logistic support from point-of-sale through transport, vaulting, bank deposit and related credit. We believe the quality and scope of our money processing and information systems differentiate our Cash Management Services from competitive offerings. Cash Management Services include:

| · | money processing (e.g., counting, sorting, wrapping, checking condition of bills, etc.) and other cash management services |

| · | deploying and servicing “intelligent” safes and safe control devices, including our patented CompuSafe® service |

| · | integrated check and cash processing services (“Virtual Vault”) |

| · | check imaging services |

Brink’s offers a variety of advanced technology applications, including online cash tracking, cash inventory management, check imaging for real-time deposit processing, and a variety of other web-based tools that enable banks and other customers to reduce costs while improving service to their customers.

Brink’s CompuSafe® Service. Brink’s CompuSafe service offers customers an integrated, closed-loop system for preventing theft and managing cash. We market CompuSafe services to a variety of cash-intensive customers, such as convenience stores, gas stations, restaurants, retail chains and entertainment venues. Once the specialized safe is installed, the customer’s employees deposit currency into the safe’s cassettes, which can only be removed by Brink’s personnel. Upon removal, the cassettes are securely transported to a vault for processing where contents are verified and transferred for deposit. Our CompuSafe service features currency-recognition and counterfeit-detection technology, multi-language touch screens and an electronic interface between the point-of-sale, back-office systems and external banks. Our electronic reporting interface with external banks enables customers to receive same-day credit on their cash balances, even if the cash remains on the customer’s premises.

Virtual Vault. Virtual Vault services combine CIT Services, Cash Management Services, vaulting and electronic reporting technologies to help banks expand into new markets while minimizing investment in vaults and branch facilities. In addition to providing secure storage, we process deposits, provide check imaging and reconciliation services, perform currency inventory management, process ATM replenishment orders and electronically transmit banking transactions.

Payment Services – We provide convenient payment services, including bill payment processing, mobile phone top-up, and Brink’s Money™ prepaid cards, and the Brink’s Checkout service.cards.

Latin America. Bill payment processing services include bill payment acceptance and processing services on behalf of utility companies and other billers. Consumers can pay bills, top-up prepaid mobile phones and manage accounts at Brink’s payment locations orretail agent locations that we operate on behalf of utility companies and banks.banks as well as a small number of leased payment locations. This service is offered at over 20,00025,000 locations in Brazil, Mexico, Colombia and Panama.

United States. We offer Brink’s Money™ general purpose reloadable prepaid cards and payroll cards to consumers and employers. Our general purpose reloadable cards are sold to consumers through our direct-to-consumer marketing efforts while our payroll cards are sold to employers so that they canwho use them to pay their employees electronically. Brink’s Money™ cards can be used at stores, restaurants and online retailers, and provide access to cash at ATM’s worldwide, and are more efficient than traditional paper paychecks.ATMs worldwide. This product is targeted to the millions of unbanked and under-banked Americans looking for alternative financial products.

Commercial Security Systems –We provide commercial security system services in designated markets in Europe. Our security system design and installation services include alarms, motion detectors, closed-circuit televisions, digital video recorders, and access control systems, including card and biometric readers, electronic locks, and turnstiles. Monitoring services may also be provided after systems have been installed.

Other Security Services (8%9% of total revenues in 2013)2014)

We offer security and guarding services in France, Luxembourg, Greece, Germany, Brazil and Germany.Ireland. A portion of this business involves long-term contracts related primarily to security services at airports and embassies. Generally, guarding contracts are for a one-year period, and the majority of contracts are extended.

Industry and Competition

Brink’s competes with large multinational, regional and smaller companies throughout the world. Our largest multinational competitors are G4S plc (U.K.); Loomis AB (Sweden); Prosegur, Compania de Seguridad, S.A. (Spain); and Garda World Security Corporation (Canada).

We believe the primary factors in attracting and retaining customers are security expertise, service quality, and price. Our competitive advantages include:

| · | brand name recognition |

| · | reputation for a high level of service and security |

| · | risk management and logistics expertise |

| · |

| global infrastructure and customer base |

| · | proprietary cash processing |

| · | proven operational excellence |

| · | high-quality insurance coverage and financial strength |

Although we face competitive pricing pressure in many markets, we resist competing on price alone. We believe our high levels of service and security, as well as value-added solutions differentiate us from competitors.

Insurance Coverage

The availability of high-quality and reliable insurance coverage is an important factor in our ability to attract and retain customers and manage the risks inherent in our business. We purchase insurance coverage for losses in excess of what we consider to be prudent levels of self-insurance. Our insurance policies cover losses from most causes, with the exception of war, nuclear risk and certain other exclusions typical in such policies.

Insurance for security is provided by different groups of underwriters at negotiated rates and terms. Premiums fluctuate depending on market conditions. The security loss experience of Brink’s and, to a limited extent, other armored carriers affects our premium rates.

Service Mark and Patents

BRINKS is a registered service mark in the U.S. and certain foreign countries. The BRINKS mark, name and related marks are of material significance to our business. We own patents for safes and related services, including our integrated CompuSafe® service, which expire between 2015 and 2027.2028. These patents provide us with important advantages; however, we are not dependent on the existence of these patents.

We have licensed the Brink’s name to a limited number of companies, including a distributor of security products (padlocks, door hardware, etc.) offered for sale to consumers through major retail chains.

Government Regulation

Our U.S. operations are subject to regulation by the U.S. Department of Transportation with respect to safety of operations, equipment and financial responsibility. Intrastate operations in the U.S. are subject to state regulation. Operations outside of the United States are regulated to varying degrees by the countries in which we operate.

5

Employee Relations

At December 31, 2013,2014, our company had approximately 65,10064,100 full-time and contract employees, including approximately 7,6007,800 employees in the United States (of whom approximately 950750 were classified as part-time employees) and approximately 57,50056,300 employees outside the United States. At December 31, 20132014, Brink’s was a party to twelve collective bargaining agreements in North America with various local unions covering approximately 1,700 employees. The agreements have various expiration dates from 20142015 to 2020.2019. Outside of North America, approximately 58%59% of employees are represented by trade union organizations. We believe our employee relations are satisfactory.

Discontinued Operations

Below is a summary of the significant businesses we disposed in the last three years. See note 1819 to the consolidated financial statements for more information on these dispositions. The results of these operations, except for the sale of the noncontrolling interest, have been excluded from continuing operations and are reported as discontinued operations for the current and prior periods. We continue to operate our Global Services business in eachmost of these countries.

Cash-in-transit operations sold or shut down:

| · | Poland (sold in March 2013) |

| · | Turkey (shut down in June 2013) |

| · | Hungary (sold in September 2013) |

| · | Germany (sold in December 2013) |

| · | Australia (sold in October 2014) |

| · | Puerto Rico (shut down in November 2014) |

| · | Netherlands (sold in December 2014) |

Guarding operations sold:

| · | Morocco (December 2012) |

| · | France (January 2013) |

| · | Germany (July 2013) |

Other operations sold:

| · | We sold Threshold Financial Technologies, Inc. in Canada in November 2013. Threshold operated private-label ATM network and payment processing businesses. Brink’s continues to own and operate Brink’s Integrated Managed Services for ATM customers. |

| · | We sold ICD Limited and other affiliated subsidiaries in November 2013. ICD had operations in China and other locations in Asia. ICD designed and installed security systems for commercial customers. |

Available Information and Corporate Governance Documents

The following items are available free of charge on our website (www.brinks.com) as soon as reasonably possible after filing or furnishing them with the Securities and Exchange Commission (the “SEC”):

| · | Annual reports on Form 10-K |

| · | Quarterly reports on Form 10-Q |

| · | Current reports on Form 8-K, and amendments to those reports |

The following documents are also available free of charge on our website:

| · | Corporate |

| · |

| · | The charters of the following committees of our Board of Directors (the “Board”): Audit and Ethics, Compensation and Benefits, and Corporate Governance and Nominating |

Printed versions of these items will be mailed free of charge to shareholders upon request. Such requests can be made by contacting the Corporate Secretary at 1801 Bayberry Court, P. O. Box 18100, Richmond, Virginia 23226-8100.

6

ITEM 1A. RISK FACTORS

We operate in highly competitive industries.

We compete in industries that are subject to significant competition and pricing pressures in most markets. In addition, our business model requires significant fixed costs associated with offering many of our services including costs to operate a fleet of armored vehicles and a network of secure branches. Because we believe we have competitive advantages such as brand name recognition and a reputation for a high level of service and security, we resist competing on price alone. However, continued pricing pressure from competitors or failure to achieve pricing based on the competitive advantages identified above could result in lost volume of business and have an adverse effect on our business, financial condition, results of operations and cash flows. In addition, given the highly competitive nature of our industries, it is important to develop new solutions and product and service offerings to help retain and expand our customer base. Failure to develop, sell and execute new solutions and offerings in a timely and efficient manner could also negatively affect our ability to retain our existing customer base or pricing structure and have an adverse effect on our business, financial condition, results of operations and cash flows.

Decreased use of cash could have a negative impact on our business.

The proliferation of payment options other than cash, including credit cards, debit cards, stored-value cards, mobile payments and on-line purchase activity, could result in a reduced need for cash in the marketplace and a decline in the need for physical bank branches and retail stores. To mitigate this risk, we are developing new lines of business and investing in adjacent security-related markets, but there is a risk that these initiatives may not offset the risks associated with our traditional cash-based business and that our business, financial condition, results of operations and cash flows could be negatively impacted.

Our growth strategy may not be successful.

One element of our growth strategy is to expand our offerings to customers. We may not be successful in designing or marketing additional products and services to customers. In addition we may fail to achieve our strategic objectives and anticipated operating profit improvements, which would adversely affect our results of operations and cash flows.

We have significant operations outside the United States.

We currently serve customers in more than 100 countries, including 4341 countries where we operate subsidiaries. Eighty-twoEighty percent (82%(80%) of our revenuerevenues in 20132014 came from operations outside the U.S. We expect revenuerevenues outside the U.S. to continue to represent a significant portion of total revenue.revenues. Business operations outside the U.S. are subject to political, economic and other risks inherent in operating in foreign countries, such as:

| · | the difficulty of enforcing agreements, collecting receivables and protecting assets through foreign legal systems; |

| · | trade protection measures and import or export licensing requirements; |

| · | difficulty in staffing and managing widespread operations; |

| · | required compliance with a variety of foreign laws and regulations; |

| · | enforcement of our global compliance program in foreign countries with a variety of laws, cultures and customs; |

| · | varying permitting and licensing requirements in different jurisdictions; |

| · | foreign ownership laws; |

| · | changes in the general political and economic conditions in the countries where we operate, particularly in emerging markets; |

| · | threat of nationalization and expropriation; |

| · |

| higher costs and risks of doing business in a number of foreign jurisdictions; |

| · | laws or other requirements and restrictions associated with organized labor; |

| · | limitations on the repatriation of earnings; |

| · | fluctuations in equity, revenues and profits due to changes in foreign currency exchange rates, including measures taken by governments to devalue official currency exchange rates; |

| · | inflation levels exceeding that of the U.S; and |

| · | inability to collect for services provided to government entities. |

7

We are exposed to certain risks when we operate in countries that have high levels of inflation, including the risk that:

| · | the rate of price increases for services will not keep pace with the cost of inflation; |

| · | adverse economic conditions may discourage business growth which could affect demand for our services; |

| · | the devaluation of the currency may exceed the rate of inflation and reported U.S. dollar revenues and profits may decline; and |

| · | these countries may be deemed “highly inflationary” for U.S. generally accepted accounting principles (“GAAP”) purposes. |

We manage these risks by monitoring current and anticipated political and economic developments, monitoring adherence to our global compliance program and adjusting operations as appropriate. Changes in the political or economic environments of the countries in which we operate could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We may be unable to achieve, or may be delayed in achieving, our costinitiatives to drive efficiency and control initiatives.costs.

We have launched a number of cost control initiatives, including the 2014 Reorganization and Restructuring described on page 2, to improve operating efficiencies and reduce operating costs. Although we have achieved annual cost savings associated with these initiatives, we may be unable to sustain the cost savings that we have achieved. In addition, if we are unable to achieve, or have any unexpected delays in achieving, additional cost savings, our results of operations and cash flow may be adversely affected. Even if we meet our goals as a result of these initiatives, we may not receive the expected financial benefits of these initiatives.

We may not be successful in pursuing strategic investments or acquisitions or realize the expected benefits of strategic acquisitionsthose transactions because of integration difficulties and other challenges, which may adversely affect our financial condition, results of operations or cash flows.challenges.

While we may identify opportunities for investments to support our growth strategy, as well as acquisition and divestiture opportunities, our due diligence examinations and positions that we may take with respect to appropriate valuations for acquisitions and divestitures and other transaction terms and conditions may hinder our ability to successfully complete business transactions to achieve our strategic goals. Our ability to realize the anticipated benefits from recent acquisitions will depend, in part, on successfully integrating each business with our company as well as improving operating performance and profitability through our management efforts and capital investments. The risks to a successful integration and improvement of operating performance and profitability include, among others, failure to implement our business plan, unanticipated issues in integrating operations with ours, unanticipated changes in laws and regulations, labor unrest resulting from union

operations, regulatory, environmental and permitting issues, the effect on our internal controls and compliance with the regulatory requirements under the Sarbanes-Oxley Act of 2002, and difficulties in fully identifying and evaluating potential liabilities, risks and operating issues. The occurrence of any of these events may adversely affect our expected benefits of the recentany acquisitions and may have a material adverse effect on our financial condition, results of operations or cash flows.

We have significant deferred tax assets in the United States that may not be realized.

Deferred tax assets are future tax deductions that result primarily from net operating losses and the net tax effects of temporary differences between the carrying amount of assets and liabilities for financial statement and income tax purposes. We have $242$287 million of U.S. deferred tax assets recorded at the end of 20132014 primarily related to our retirement plan obligations. These future tax deductions may not be realized if our expectations oftax rules change or if projected future margin improvements of our U.S. business are not attained.taxable income is insufficient. Consequently, not realizing our U.S. deferred tax assets may significantly and materially affect our financial condition, results of operations and cash flows.

8

We have significant retirement obligations. Poor investment performance of retirement plan holdings and / or lower interest rates used to discount the obligations could unfavorably affect our liquidity and results of operations.

We have substantial pension and retiree medical obligations, a portion of which have been funded. The amount of these obligations is significantly affected by factors that are not in our control, including interest rates used to determine the present value of future payment streams, investment returns, medical inflation rates, participation rates and changes in laws and regulations. The funded status of the primary U.S. pension plan was approximately 88% as of December 31, 2013.2014. Based on actuarial assumptions at the end of 2013,2014, we do not expect that we will be required to make any contributions totaling $110 million toin the plan over the next five years. Thisfuture. A change in assumptions could result in funding obligations that could adversely affect our liquidity and our ability to use our resources to make acquisitions and to otherwise grow our business.

We have $589$721 million of actuarial losses recorded in accumulated other comprehensive income (loss) at the end of 2013.2014. These losses relate to changes in actuarial assumptions that have increased the net liability for benefit plans. These losses have not been recognized in earnings. These losses will be recognized in earnings in future periods to the extent they are not offset by future actuarial gains. Our projections of future cash requirements and expenses for these plans could be adversely affected if our retirement plans have additional actuarial losses.

Our earnings and cash flow could be materially affected by increased losses of customer valuables.

We purchase insurance coverage for losses of customer valuables for amounts in excess of what we consider prudent deductibles and/or retentions. Insurance is provided by different groups of underwriters at negotiated rates and terms. Coverage is available to us in major insurance markets, although premiums charged are subject to fluctuations depending on market conditions. Our loss experience and that of other companies in our industry affects premium rates. We are not insured for losses below our coverage limits and recognize expense up to these limits for actual losses. Our insurance policies cover losses from most causes, with the exception of war, nuclear risk and various other exclusions typical for such policies. The availability of high-quality and reliable insurance coverage is an important factor in obtaining and retaining customers and managing the risks of our business. If our losses increase, or if we are unable to obtain adequate insurance coverage at reasonable rates, our financial condition, results of operations and cash flows could be materially and adversely affected.

The Venezuelan government recently announced a new currency exchange process, known locally as “SIMADI.” The new process is expected to replace the existing SICAD II exchange process. We currently use the SICAD II rate to measure our Venezuelan operations for our financial statements. We have not yet concluded whether the new rate will be used for our financial statements. We expect the exchange rate under the proposed exchange will be much less favorable than current rates, which could adversely affect our reported results for our Venezuelan operations in future years.

The new SIMADI currency exchange is expected to exchange Venezuelan bolivars to U.S. dollars at rates significantly less favorable than the current SICAD II exchange rates. The SICAD II rates have approximated 50 bolivars to the U.S. dollar since its inception in March 2014. At December 31, 2014, we held $12.6 million of cash and cash equivalents and $10.9 million other net monetary assets denominated in bolivars based on the official exchange rate we use to remeasure our Venezuelan operations. The SIMADI rate has ranged from 170 to 174 bolivars to the dollar between February 12 and February 26. Had we used a rate of 170, our revenues in 2014 would have declined by $183 million and our operating profit before items not allocated to segments would have declined by $39 million. Had a rate of 170 been in effect at December 31, 2014, we would have recognized additional currency losses to write down our net monetary assets of $16 million.

Currency restrictions in Venezuela limit our ability to use earnings and cash flows outside of Venezuela and may negatively affect ongoing operations in Venezuela.

Because most of our past requests to convert bolivars to dollars have not been approved and certain past processes to obtain dollars are no longer available, we do not expect to be able to repatriate cash from Venezuela for the foreseeable future. Therefore, we do not expect to be able to use cash held in Venezuela for any purpose outside of that country, including reducing our U.S. debt, funding growth or business acquisitions or returning cash to shareholders.

We believe that currency exchange restrictions in Venezuela may disrupt the operation of our business in Venezuela because we may be unable to pay for goods and services that are required to be paid in dollars. This could reduce our ability to provide services to our customers in Venezuela, or could increase the cost of delivering the services, which would negatively affect our earnings and cash flows, and could result in a loss of control, deconsolidation, shutdown or loss of the business in Venezuela.

9

Currency restrictions in Argentina may require us to use more expensive methods to repatriate earnings.

The Argentinean government has, from time-to-time, imposed limits on the exchange of local pesos into U.S. dollars. As a result, we have elected in the past and may elect in the future to repatriate cash from Argentina using alternative legal methods, which may result in less favorable exchange rates. At December 31, 2014, our Argentinean operations held $6.6 million in Argentinean pesos.

We have risks associated with confidential individual information.

In the normal course of business, we collect, process and retain sensitive and confidential information, including information about individuals. Despite the security measures we have in place, our facilities and systems, and those of third-party service providers and business partners, could be vulnerable to security breaches (including cybersecurity breaches), acts of vandalism, computer viruses, misplaced or lost data, programming or human errors or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or by third-party service providers, could damage our reputation, expose us to the risks of litigation and liability, disrupt our business or otherwise have a material adverse effect on our business, financial condition, results of operations and cash flows.

Negative publicity to our name or brand could lead to a loss of revenuerevenues or profitability.

We are in the security business and our success and longevity are based to a large extent on our reputation for trust and integrity. Our reputation or brand, particularly the trust placed in us by our customers, could be negatively impacted in the event of perceived or actual breaches in our ability to conduct our business ethically, securely and responsibly. Any damage to our brand could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Failures of our IT system could have a material adverse effect on our business.

We are heavily dependent on our information technology (IT) infrastructure. Significant problems with our infrastructure, such as telephone or IT system failure, cybersecurity breaches, or failure to develop new technology platforms to support new initiatives and product and service offerings, could halt or delay our ability to service our customers, hinder our ability to conduct and expand our business and require significant remediation costs. In addition, we continue to evaluate and implement upgrades to our IT systems. We are aware of inherent risks associated with replacing these systems, including accurately capturing data and system disruptions, and believe we are taking appropriate action to mitigate these risks through testing, training, and staging implementation. However, there can be no assurances that we will successfully launch these systems as planned or that they will occur without disruptions to our operations. Any of these events could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We operate in regulated industries.

Our U.S. operations are subject to regulation by the U.S. Department of Transportation with respect to safety of operations and equipment and financial responsibility. Intrastate operations in the U.S. are subject to regulation by state regulatory authorities and interprovincial operations in Canada are subject to regulation by Canadian and provincial regulatory authorities. Our international operations are regulated to varying degrees by the countries in which we operate. Many countries have permit requirements for security services and prohibit foreign companies from providing different types of security services.

Changes in laws or regulations could require a change in the way we operate, which could increase costs or otherwise disrupt operations. In addition, failure to comply with any applicable laws or regulations could result in substantial fines or revocation of our operating permits and licenses. If laws and regulations were to change or we failed to comply, our business, financial condition, results of operations and cash flows could be materially and adversely affected.

10

Our inability to access capital or significant increases in our cost of capital could adversely affect our business.

Our ability to obtain adequate and cost-effective financing depends on our credit ratings as well as the liquidity of financial markets. A negative change in our ratings outlook or any downgrade in our current investment-grade credit ratings by the rating agencies could adversely affect our cost and/or access to sources of liquidity and capital. Additionally, such a downgrade could increase the costs of borrowing under available credit lines. Disruptions in the capital and credit markets could adversely affect our ability to access short-term and long-term capital. Our access to funds under short-term credit facilities is dependent on the ability of the participating banks to meet their funding commitments. Those banks may not be able to meet their funding commitments if they experience shortages of capital and liquidity. Longer disruptions in the capital and credit markets as a result of uncertainty, changing or increased regulation, reduced alternatives, or failures of significant financial institutions could adversely affect our access to capital needed for our business.

We have retained obligations from the sale of BAX Global.

Our credit facilities as well as our unsecured notes are subject to financial covenants, including a limit on the ratio of debt to earnings before interest, taxes, depreciation, and amortization, limits on the ability to pledge assets, limits on the total amount of indebtedness we can incur, limits on the use of proceeds of asset sales and minimum coverage of interest costs. Although we believe none of these covenants are presently restrictive to operations, the ability to meet the financial covenants can be affected by changes in our results of operations or financial condition. We cannot provide assurance that we will meet these covenants. A breach of any of these covenants could result in a default under existing credit facilities. Upon the occurrence of an event of default under any of our credit facilities, the lenders could cause amounts

outstanding to be immediately payable and terminate all commitments to extend further credit. The occurrence of these events would have a significant effect on our liquidity and cash flows.

Our effective income tax rate could change.

We serve customersoperate subsidiaries in more than 10041 countries, including 43 countries where we operate subsidiaries, all of which have different income tax laws and associated income tax rates. Our effective income tax rate can be significantly affected by changes in the mix of pretax earnings by country and the related income tax rates in those countries. In addition, our effective income tax rate is significantly affected by the ability to realize deferred tax assets, including those associated with net operating losses. Changes in income tax laws, income apportionment, or estimates of the ability to realize deferred tax assets, could significantly affect our effective income tax rate, financial position and results of operations. We are subject to the regular examination of our income tax returns by various tax authorities. We regularly assess the likelihood of adverse outcomes resulting from these examinations to determine the adequacy of our provision for taxes. There can be no assurance that the outcomes from these examinations will not have a material adverse effect on our business.

11

We have certain environmental and other exposures related to our former coal operations.

We may incur future environmental and other liabilities in connection with our former coal operations, which could materially and adversely affect our financial condition, results of operations and cash flows.

We may be exposed to certain regulatory and financial risks related to climate change.

Growing concerns about climate change may result in the imposition of additional environmental regulations to which we are subject. Some form of federal regulation may be forthcoming with respect to greenhouse gas emissions (including carbon dioxide) and/or "cap and trade" legislation. The outcome of this legislation may result in new regulation, additional charges to fund energy efficiency activities or other regulatory actions. Compliance with these actions could result in the creation of additional costs to us, including, among other things, increased fuel prices or additional taxes or emission allowances. We may not be able to recover the cost of compliance with new or more stringent environmental laws and regulations from our customers, which could adversely affect our business. Furthermore, the potential effects of climate change and related regulation on our customers are highly uncertain and may adversely affect our operations.

Forward-Looking Statements

This document contains both historical and forward-looking information. Words such as “anticipates,” “assumes,” “estimates,” “expects,” “projects,” “predicts,” “intends,” “plans,” “potential,” “believes,” “may,” “should” and similar expressions may identify forward-looking information. Forward-looking information in this document includes, but is not limited to, statements regarding future performance of The Brink’s Company and its global operations, including anticipated savings and other impacts of our 2014 Reorganization and Restructuring and additional; 2015 workforce reductions, revenues, organic revenue growth and segment operating profit margin, in 2014,income from continuing operations, non-operating income or expense and earnings per share; 2016 revenues, operating profit margin and earnings per share, the repatriation of cash from our Venezuelan and Argentinean operations, the anticipated financial effect of pending litigation, revenue and depreciation, profit growth and expected margins in the Company’s operating segments, the acquisition of new vehicles in the United States with capital leases, interest expense and rental expense related to the U.S. fleet, expected non-segment income and expenses, 2014 projected interest expense and interest and other income, the realization of deferred tax assets, our anticipated effective tax rate for 20142015 and our tax position, the reinvestment of earnings on operations outside the United States, net income (loss) attributable to noncontrolling interests, expected earnings in Venezuela, projected currency impact on revenue,revenues, capital expenditures, capital leases and depreciation and amortization, the funding of future acquisitions and pension obligations, the ability to meet liquidity needs, future payment of bonds issued by the Peninsula Ports Authority of Virginia, expenses and payouts for the U.S. retirement plans and the non-U.S. pension plans and the expected long-term rate of return and funded status of the primary U.S. pension plan, expected liability for and future contributions to the UMWA plans, liability for black lung obligations, the projected impact of future excise tax on the UMWA plans, our ability to obtain U.S. dollars to operate our business in Venezuela, future devaluation in Venezuela, the effect of accounting rule changes, the performance of counterparties to hedging agreements, the recognition of unrecognized tax positions, expected future amortizations into net periodic pensionpayments under contractual obligations, and post-retirement cost, the deductibility of goodwill, projected minimum repayments of long-term debt, the replacementfuture use of operating leases, future minimum lease payments, and the recognition of costs related to equity awards.leases. Forward-looking information in this document is subject to known and unknown risks, uncertainties, and contingencies, which are difficult to quantify and which could cause actual results, performance or achievements to differ materially from those that are anticipated.

These risks, uncertainties and contingencies, many of which are beyond our control, include, but are not limited to:

| · | our ability to improve profitability in our largest five markets; |

| · | our ability to identify and execute further cost and operational improvements and efficiencies in our core businesses; |

| · | continuing market volatility and commodity price fluctuations and their impact on the demand for our services; |

| · | our ability to maintain or improve volumes at favorable pricing levels and increase cost and productivity efficiencies, particularly in the United States and |

| · | investments in information technology and |

| · | our ability to develop and implement solutions for our customers and gain market acceptance of those solutions; |

| · | our ability to maintain an effective IT infrastructure and safeguard confidential information; |

| · | risks customarily associated with operating in foreign countries including changing labor and economic conditions, currency restrictions and devaluations, safety and security issues, political instability, restrictions on repatriation of earnings and capital, nationalization, expropriation and other forms of restrictive government actions; |

| · | the strength of the U.S. dollar relative to foreign currencies and foreign currency exchange rates; |

| · | the stability of the Venezuelan economy, changes in Venezuelan policy regarding foreign-owned businesses; |

| · | regulatory and labor issues in many of our global operations, including negotiations with organized labor and the possibility of work stoppages; |

| · | our ability to integrate successfully recently acquired companies and improve their operating profit margins; |

| · | costs related to dispositions and market exits; |

| · | our ability to identify evaluate and pursue acquisitions and other strategic |

| · | the willingness of our customers to absorb fuel surcharges and other future price increases; |

| · | our ability to obtain necessary information technology and other services at favorable pricing levels from third party service providers; |

| · | variations in costs or expenses and performance delays of any public or private sector supplier, service provider or customer; |

| · | our ability to obtain appropriate insurance coverage, positions taken by insurers with respect to claims made and the financial condition of insurers, safety and security performance, our loss experience, and changes in insurance costs; |

| · | security threats worldwide and losses of customer valuables; |

| · | costs associated with the purchase and implementation of cash processing and security equipment; |

| · | employee and environmental liabilities in connection with our former coal operations, including black lung claims incidence; |

| · | the impact of the Patient Protection and Affordable Care Act on black lung liability and the Company's ongoing operations; |

| · | changes to estimated liabilities and assets in actuarial assumptions due to payments made, investment returns, interest rates and annual actuarial revaluations, the funding requirements, accounting treatment, investment performance and costs and expenses of our pension plans, the VEBA and other employee benefits, mandatory or voluntary pension plan contributions; |

| · | the nature of our hedging relationships; |

| · | changes in estimates and assumptions underlying our critical accounting policies; |

| · | our ability to realize deferred tax assets; |

| · | the outcome of pending and future claims, litigation, and administrative proceedings; |

| · | public perception of the |

| · | access to the capital and credit markets; |

13

| · | seasonality, pricing and other competitive industry factors; and |

| · | the promulgation and adoption of new accounting standards and interpretations, new government regulations and |

The information included in this document is representative only as of the date of this document, and The Brink’s Company undertakes no obligation to update any information contained in this document.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. PROPERTIES

We have property and equipment in locations throughout the world. Branch facilities generally have office space to support operations, a vault to securely process and store valuables and a garage to house armored vehicles and serve as a vehicle terminal. Many branches have additional space to repair and maintain vehicles.

We own or lease armored vehicles, panel trucks and other vehicles that are primarily service vehicles. Our armored vehicles are of bullet-resistant construction and are specially designed and equipped to provide security for the crew and cargo.

The following table discloses leased and owned facilities and vehicles for Brink’s most significant operations as of December 31, 2013.2014.

| Facilities | Vehicles | ||||||||||||||

| Region | Leased | Owned | Total | Leased | Owned | Total | |||||||||

| U.S. | 131 | 26 | 157 | 1,920 | 183 | 2,103 | |||||||||

| Canada | 38 | 14 | 52 | 480 | 14 | 494 | |||||||||

| Latin America | 373 | 121 | 494 | 593 | 5,701 | 6,294 | |||||||||

| EMEA | 210 | 37 | 247 | 580 | 2,556 | 3,136 | |||||||||

| Asia Pacific | 97 | - | 97 | 6 | 638 | 644 | |||||||||

| Total | 849 | 198 | 1,047 | 3,579 | 9,092 | 12,671 | |||||||||

| Facilities | Vehicles | |||||||||||||||||||||||

| Leased | Owned | Total | Leased | Owned | Total | |||||||||||||||||||

| Largest 5 Markets | ||||||||||||||||||||||||

| U.S. | 128 | 25 | 153 | 1,919 | 179 | 2,098 | ||||||||||||||||||

| France | 84 | 34 | 118 | 870 | 568 | 1,438 | ||||||||||||||||||

| Mexico | 161 | 67 | 228 | 91 | 2,551 | 2,642 | ||||||||||||||||||

| Brazil | 59 | 4 | 63 | 441 | 774 | 1,215 | ||||||||||||||||||

| Canada | 37 | 14 | 51 | 464 | 11 | 475 | ||||||||||||||||||

| Global Markets | ||||||||||||||||||||||||

| Latin America | 159 | 55 | 214 | - | 2,255 | 2,255 | ||||||||||||||||||

| EMEA | 114 | 3 | 117 | 437 | 1,024 | 1,461 | ||||||||||||||||||

| Asia | 101 | - | 101 | 7 | 652 | 659 | ||||||||||||||||||

| Payment Services | 34 | - | 34 | 85 | 7 | 92 | ||||||||||||||||||

| Total | 877 | 202 | 1,079 | 4,314 | 8,021 | 12,335 | ||||||||||||||||||

As of December 31, 2013,2014, we had approximately 19,10020,400 units for our CompuSafe® service installed worldwide, of which approximately 15,40016,100 units were located in the U.S.

ITEM 3. LEGAL PROCEEDINGS

For a discussion of legal proceedings, see note 2223 to the consolidated financial statements, “Other Commitments and Contingencies,” in Part II, Item 8 of this 10-K.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

Executive Officers of the Registrant

The following is a list as of February 21, 2014,27, 2015, of the names and ages of the executive officers of The Company indicating the principal positions and offices held by each. There are no family relationships among any of the officers named.

| Name | Age | Positions and Offices Held | Held Since | |||||

| Thomas C. Schievelbein | 60 | Chairman, President and Chief Executive Officer | 2012 | |||||

| Joseph W. Dziedzic | 45 | Vice President and Chief Financial Officer | 2009 | |||||

| McAlister C. Marshall, II | 44 | Vice President and General Counsel | 2008 | |||||

| Darren M. McCue | 40 | Vice President and Chief Commercial Strategy Officer | 2013 | |||||

| Matthew A. P. Schumacher | 55 | Controller | 2001 | |||||

| Holly R. Tyson | 42 | Vice President and Chief Human Resources Officer | 2012 | |||||

| Patricia A. Watson | 47 | Vice President and Chief Information Officer | 2013 |

| Name | Age | Positions and Offices Held | Held Since | ||||||

| Thomas C. Schievelbein | 61 | Chairman, President and Chief Executive Officer | 2012 | ||||||

| Joseph W. Dziedzic | 46 | Executive Vice President and Chief Financial Officer | 2009 | ||||||

| Michael F. Beech | 53 | Executive Vice President, Strategy and Focus Markets | 2014 | ||||||

| McAlister C. Marshall, II | 45 | Vice President and General Counsel | 2008 | ||||||

| Matthew A. P. Schumacher | 56 | Vice President and Controller | 2001 | ||||||

| Holly R. Tyson | 43 | Vice President and Chief Human Resources Officer | 2012 | ||||||

| Patricia A. Watson | 48 | Vice President and Chief Information Officer | 2013 | ||||||

| Amit Zukerman | 43 | Executive Vice President, Global Operations | 2014 | ||||||

Executive and other officers of the Company are elected annually and serve at the pleasure of the Board.

Mr. Schievelbein is the Chairman, President and Chief Executive Officer of the Company and has held that position since June 2012, prior to which he served as the interim President and Chief Executive Officer of the Company from December 2011 to June 2012 and the interim Executive Chairman of the Company from November 2011 to December 2011. He has also served as a director of the Company since March 2009. He was President of Northrop Grumman Newport News, a subsidiary of the Northrop Grumman Corporation, a global defense company, from November 2001 until November 2004, and was a business consultant from November 2004 to November 2011. Mr. Schievelbein currently also serves as a director of Huntington Ingalls Industries, Inc. and New York Life Insurance Company.

Mr. Dziedzic is thewas appointed Executive Vice President of the Company in December 2014 and has served as Chief Financial Officer since 2009. From August 2009 to December 2014, Mr. Dziedzic served as Vice President of the Company. Mr. Dziedzic was hired in May 2009 and appointed to this position in August 2009. Before joining the Company, Mr. Dziedzic was Chief Financial Officer at GE Aviation Services,currently serves as a producer, seller and servicerdirector of jet engines, turboprop and turbo shaft engines and related replacement parts, from March 2006 to May 2009.Greatbatch, Inc.

Mr. Marshall was appointed Vice President and General Counsel of the Company in September 2008. He also previously held the office of Secretary from September 2008 to July 2009 and from June 2012 to November 2013.

Mr. McCue is the Vice President and Chief Commercial Strategy Officer of the Company. Mr. McCue joined the Company andBeech was appointed to this position in February 2013. Before joining the Company, Mr. McCue was Executive Vice President, of Strategy and Business DevelopmentFocus Markets of the Company in December 2014. He served as President, Europe, Middle East and Africa for Consumer Financial Solutions at Aetna Inc.the Company’s operating subsidiary, Brink’s, Incorporated, from 2011 to 2013. He also servedDecember 2014; as President, Asia Pacific from 2011 to 2012; and as Vice President, Global Security from 2009 to 2011.

Mr. Zukerman was appointed as the Company’s Executive Vice President, of StrategyGlobal Operations and Product DevelopmentBrink’s Global Services in December 2014. He served as President, Brink’s Global Services and Asia Pacific for PayFlex Systems USA, Inc.the Company’s operating subsidiary, Brink’s, Incorporated, from 2007 until the company was acquired by Aetna in 2011. 2012 to December 2014 and as President, Brink’s Global Services from 2008 to 2012.

Mr. Schumacher has served as Vice President and Controller of the Company since August 2014 and was appointed Controller in his present position for more than the past five years.July 2001.

Ms. Tyson is thewas appointed Vice President and Chief Human Resources Officer of the Company. Ms. Tyson was hired in August 2012 and appointed to this positionCompany in September 2012. Before joining the Company, Ms. Tyson was with Bristol-Myers Squibb Company, a global biopharmaceutical company, where she was Vice President U.S. Pharmaceuticals Human Resources from 2010 to 2012, and Executive Director World Wide Pharmaceuticals Talent & U.S. Pharmaceutical Sales Learning from 2009 to 2010, Senior Director Human Resources & U.S. Pharmaceuticals Sales Learning from 2008 to 2009.2010.

Ms. Watson iswas appointed Vice President and Chief Information Officer of the Company. Ms. Watson joined the Company in January 2013 and was appointed to this position in February 2013. Prior to joining the Company, Ms. Watson was Senior Technology Executive with Bank of America’s Treasury, Credit and Payments division from 2007 to 2012.

PART II |

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock trades on the New York Stock Exchange under the symbol “BCO.” As of February 18, 2014,19, 2015, there were 1,6411,561 shareholders of record of common stock.

The dividends declared and the high and low prices of our common stock for each full quarterly period within the last two years are as follows:

| 2013 Quarters | 2012 Quarters | |||||||||||||||||

1st | 2nd | 3rd | 4th | 1st | 2nd | 3rd | 4th | |||||||||||

| Dividends declared per common share | $ | 0.1000 | 0.1000 | 0.1000 | 0.1000 | $ | 0.1000 | 0.1000 | 0.1000 | 0.1000 | ||||||||

| Stock prices: | ||||||||||||||||||

| High | $ | 30.75 | 28.36 | 28.76 | 34.76 | $ | 29.64 | 26.73 | 25.82 | 29.87 | ||||||||

| Low | 25.90 | 24.07 | 25.41 | 26.58 | 23.39 | 20.91 | 21.70 | 24.67 | ||||||||||

| 2014 Quarters | 2013 Quarters | |||||||||||||||||||||||||||||||

1st | 2nd | 3rd | 4th | 1st | 2nd | 3rd | 4th | |||||||||||||||||||||||||

| Dividends declared per common share | $ | 0.1000 | 0.1000 | 0.1000 | 0.1000 | $ | 0.1000 | 0.1000 | 0.1000 | 0.1000 | ||||||||||||||||||||||

| Stock prices: | ||||||||||||||||||||||||||||||||

| High | $ | 35.73 | 30.56 | 28.80 | 24.71 | $ | 30.75 | 28.36 | 28.76 | 34.76 | ||||||||||||||||||||||

| Low | 27.59 | 24.25 | 23.85 | 19.15 | 25.90 | 24.07 | 25.41 | 26.58 | ||||||||||||||||||||||||

See note 1718 to the consolidated financial statements for a description of limitations of our ability to pay dividends in the future.

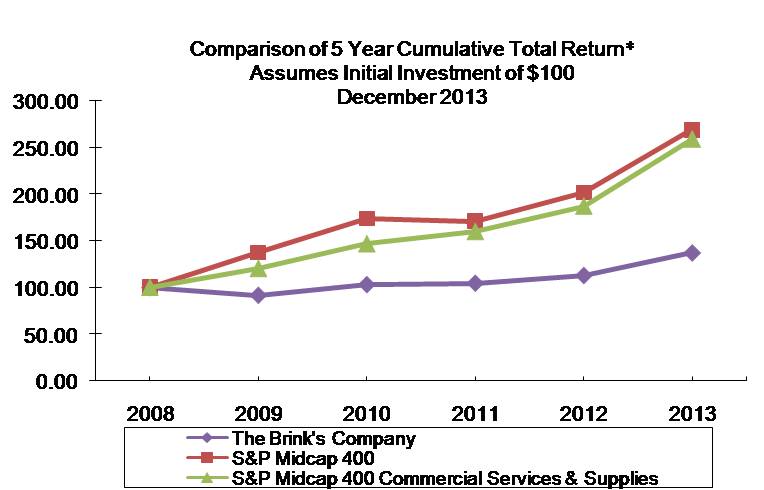

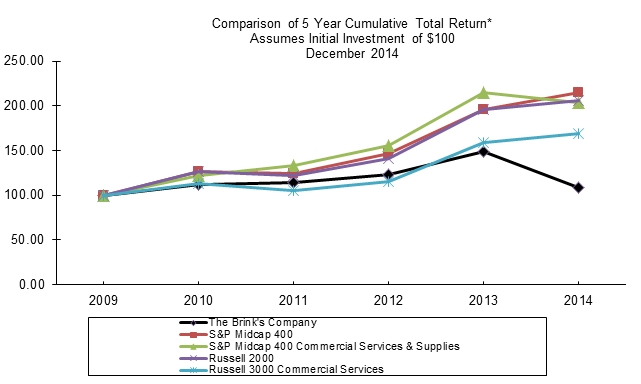

The following graph compares the cumulative 5-year total return provided to shareholders of The Brink’s Company’s common stock compared to the cumulative total returns of the Russell 2000 Index and Russell 3000 Commercial Services Index, as well as the S&P Midcap 400 index and the S&P Midcap 400 Commercial Services & Supplies Index.index. The graph tracks the performance of a $100 investment in our common stock and in each index from December 31, 2008,2009, through December 31, 2013.2014. The performance of The Brink’s Company’s common stock assumes that the shareholder reinvested all dividends received during the period.

Fiscal year ending December 31.

Source: Zacks Investment Research, Inc.

Comparison of Five-Year Cumulative Total Return Among

| Years Ended December 31, | ||||||||||||||

| 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |||||||||

| The Brink's Company | $ | 100.00 | 91.90 | 103.26 | 104.75 | 112.95 | 137.04 | |||||||

| S&P Midcap 400 Index | 100.00 | 137.38 | 173.98 | 170.96 | 201.53 | 269.04 | ||||||||

| S&P Midcap 400 Commercial Services & Supplies Index | 100.00 | 120.33 | 146.78 | 159.85 | 187.08 | 258.89 | ||||||||

Copyright© 2014, Standard & Poor's, a division of The McGraw-Hill Companies, Inc. All rights reserved. | ||||||||||||||

| Years Ended December 31, | ||||||||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||||||||

| The Brink's Company | $ | 100.00 | 112.36 | 113.99 | 122.92 | 149.12 | 108.25 | |||||||||||||||||

| S&P Midcap 400 Index | 100.00 | 126.64 | 124.45 | 146.70 | 195.84 | 214.97 | ||||||||||||||||||

| S&P Midcap 400 Commercial Services & Supplies Index | 100.00 | 121.98 | 132.85 | 155.47 | 215.15 | 203.74 | ||||||||||||||||||

| Russell 2000 Index | 100.00 | 126.81 | 121.52 | 141.42 | 196.32 | 205.93 | ||||||||||||||||||

| Russell 3000 Commercial Services Index | 100.00 | 112.75 | 105.14 | 115.03 | 158.91 | 169.25 | ||||||||||||||||||

| (a) | For the line designated as “The Brink’s Company” the graph depicts the cumulative return on $100 invested in The Brink’s Company’s common |

| GAAP Basis | |||||||||||||

| (In millions, except for per share amounts) | 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||

| Revenues and Operating Profit | |||||||||||||

| Revenues | $ | 3,942.2 | 3,735.0 | 3,662.9 | 2,925.3 | 2,959.3 | |||||||

| Segment operating profit | $ | 252.8 | 263.9 | 262.3 | 244.6 | 237.3 | |||||||

| Non-segment income (expense) | (81.1) | (88.9) | (59.8) | (62.6) | (46.6) | ||||||||

| Operating profit | $ | 171.7 | 175.0 | 202.5 | 182.0 | 190.7 | |||||||

| Income attributable to Brink’s: | |||||||||||||

| Income from continuing operations | 71.9 | 111.2 | 100.3 | 87.1 | 220.1 | ||||||||

Loss income from discontinued operations(a) | (15.1) | (22.3) | (25.8) | (30.0) | (19.9) | ||||||||

| Net income attributable to Brink’s | $ | 56.8 | 88.9 | 74.5 | 57.1 | 200.2 | |||||||

| Financial Position | |||||||||||||

| Property and equipment, net | $ | 758.7 | 793.8 | 749.2 | 698.9 | 549.5 | |||||||

| Total assets | 2,498.0 | 2,553.9 | 2,406.2 | 2,270.5 | 1,879.8 | ||||||||

| Long-term debt, less current maturities | 330.5 | 335.6 | 335.3 | 323.7 | 172.3 | ||||||||

| Brink’s shareholders’ equity | 693.9 | 501.8 | 408.0 | 516.2 | 534.9 | ||||||||

| Supplemental Information | |||||||||||||

| Depreciation and amortization | $ | 173.6 | 155.7 | 148.1 | 123.9 | 122.3 | |||||||

| Capital expenditures | 177.7 | 177.9 | 183.7 | 135.7 | 160.4 | ||||||||

| Earnings per share attributable to Brink’s common shareholders | |||||||||||||

| Basic: | |||||||||||||

| Continuing operations | $ | 1.48 | 2.30 | 2.10 | 1.81 | 4.65 | |||||||

Discontinued operations(a) | (0.31) | (0.46) | (0.54) | (0.62) | (0.42) | ||||||||

| Net income | $ | 1.17 | 1.84 | 1.56 | 1.18 | 4.23 | |||||||

| Diluted: | |||||||||||||

| Continuing operations | $ | 1.47 | 2.29 | 2.09 | 1.80 | 4.63 | |||||||

Discontinued operations(a) | (0.31) | (0.46) | (0.54) | (0.62) | (0.42) | ||||||||

| Net income | $ | 1.16 | 1.83 | 1.55 | 1.18 | 4.21 | |||||||

| Cash dividends | $ | 0.4000 | 0.4000 | 0.4000 | 0.4000 | 0.4000 | |||||||

| Weighted-average Shares | |||||||||||||

| Basic | 48.7 | 48.4 | 47.8 | 48.2 | 47.2 | ||||||||

| Diluted | 49.0 | 48.6 | 48.1 | 48.4 | 47.5 | ||||||||

| Non-GAAP Basis* | ||||||||||||

| (In millions, except for per share amounts) | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||

| Revenues | $ | 3,942.2 | 3,735.0 | 3,662.9 | 2,925.3 | 2,721.4 | ||||||

| Segment operating profit | $ | 283.4 | 268.1 | 267.6 | 246.8 | 196.8 | ||||||

| Non-segment income (expense) | (42.6) | (42.3) | (40.6) | (36.2) | (34.7) | |||||||

| Operating profit | $ | 240.8 | 225.8 | 227.0 | 210.6 | 162.1 | ||||||

| Amounts attributable to Brink’s: | ||||||||||||

| Income from continuing operations | 115.9 | 112.7 | 112.5 | 118.9 | 91.1 | |||||||

| Diluted EPS – continuing operations | $ | 2.37 | 2.32 | 2.34 | 2.46 | 1.92 | ||||||

| *Reconciliations to GAAP results are found beginning on page 40. | ||||||||||||

18

ITEM 6. SELECTED FINANCIAL DATA

Five Years in Review

| GAAP Basis | ||||||||||||||||||||

| (In millions, except for per share amounts) | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||

| Revenues | $ | 3,562.3 | 3,778.6 | 3,577.6 | 3,515.4 | 2,810.7 | ||||||||||||||

| Operating profit (loss) | (27.5 | ) | 163.2 | 162.2 | 199.7 | 175.2 | ||||||||||||||

| Income (loss) attributable to Brink’s | ||||||||||||||||||||

| Continuing operations | $ | (54.8 | ) | 66.0 | 102.3 | 98.7 | 82.9 | |||||||||||||

| Discontinued operations | (29.1 | ) | (9.2 | ) | (13.4 | ) | (24.2 | ) | (25.8 | ) | ||||||||||

| Net income (loss) attributable to Brink’s | $ | (83.9 | ) | 56.8 | 88.9 | 74.5 | 57.1 | |||||||||||||

| Financial Position | ||||||||||||||||||||

| Property and equipment, net | $ | 669.5 | 758.7 | 793.8 | 749.2 | 698.9 | ||||||||||||||

| Total assets | 2,192.2 | 2,498.0 | 2,553.9 | 2,406.2 | 2,270.5 | |||||||||||||||

| Long-term debt, less current maturities | 373.3 | 330.5 | 335.6 | 335.3 | 323.7 | |||||||||||||||

| Brink’s shareholders’ equity | 434.0 | 693.9 | 501.8 | 408.0 | 516.2 | |||||||||||||||

| Supplemental Information | ||||||||||||||||||||

| Depreciation and amortization | $ | 161.9 | 165.8 | 148.4 | 140.0 | 116.6 | ||||||||||||||

| Capital expenditures | 136.1 | 172.9 | 170.9 | 176.0 | 128.4 | |||||||||||||||

| Earnings (loss) per share attributable to Brink’s common shareholders | ||||||||||||||||||||

| Basic: | ||||||||||||||||||||

| Continuing operations | $ | (1.12 | ) | 1.36 | 2.12 | 2.06 | 1.72 | |||||||||||||

| Discontinued operations | (0.59 | ) | (0.19 | ) | (0.28 | ) | (0.51 | ) | (0.54 | ) | ||||||||||

| Net income (loss) | $ | (1.71 | ) | 1.17 | 1.84 | 1.56 | 1.18 | |||||||||||||

| Diluted: | ||||||||||||||||||||

| Continuing operations | $ | (1.12 | ) | 1.35 | 2.11 | 2.05 | 1.71 | |||||||||||||

| Discontinued operations | (0.59 | ) | (0.19 | ) | (0.28 | ) | (0.50 | ) | (0.53 | ) | ||||||||||

| Net income (loss) | $ | (1.71 | ) | 1.16 | 1.83 | 1.55 | 1.18 | |||||||||||||

| Cash dividends | $ | 0.40 | 0.40 | 0.40 | 0.40 | 0.40 | ||||||||||||||

| Weighted-average Shares | ||||||||||||||||||||

| Basic | 49.0 | 48.7 | 48.4 | 47.8 | 48.2 | |||||||||||||||

| Diluted | 49.0 | 49.0 | 48.6 | 48.1 | 48.4 | |||||||||||||||

| Non-GAAP Basis* | ||||||||||||||||||||

| (In millions, except for per share amounts) | 2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||

| Revenues | $ | 3,562.3 | 3,778.6 | 3,577.6 | 3,515.4 | 2,810.7 | ||||||||||||||

| Operating profit | 169.0 | 227.3 | 207.0 | 219.9 | 197.6 | |||||||||||||||

| Amounts attributable to Brink’s | ||||||||||||||||||||

| Income from continuing operations | $ | 73.2 | 104.5 | 97.8 | 106.4 | 109.5 | ||||||||||||||

| Diluted EPS – continuing operations | $ | 1.49 | 2.13 | 2.01 | 2.21 | 2.26 | ||||||||||||||

| *Reconciliations to GAAP results are found beginning on page 36. | ||||||||||||||||||||

19

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

THE BRINK’S COMPANY

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FOR THE YEAR ENDED DECEMBER 31, 20132014

TABLE OF CONTENTS

| Page | ||

| OPERATIONS | ||

| RESULTS OF OPERATIONS | ||

| 23 | ||

| Analysis of Results: 2014 versus 2013 | 25 | |

| Analysis of Results: 2013 versus 2012 | 27 | |

| Other Operating Income and Expense | ||

| Nonoperating Income and Expense | ||

| Income Taxes | ||

| Noncontrolling Interests | ||

| Loss from Discontinued Operations | ||

| Non-GAAP Results | ||

| Foreign Operations | ||

| LIQUIDITY AND CAPITAL RESOURCES | ||

| Overview | ||

| Operating Activities | ||

| Investing Activities | ||

| Financing Activities | ||

| Effect of Exchange Rate Changes on Cash and Cash Equivalents | 42 | |

| Capitalization | ||

| Off Balance Sheet Arrangements | ||

| Contractual Obligations | ||

| Contingent Matters | ||

| APPLICATION OF CRITICAL ACCOUNTING POLICIES | ||

| Deferred Tax Asset Valuation Allowance | ||

| Goodwill, Other Intangible Assets and Property and Equipment Valuations | ||

| Retirement and Postemployment Benefit Obligations | ||

| Foreign Currency Translation | ||

| 56 | ||

OPERATIONS

The Brink’s Company offers transportation and logistics management services for cash and valuables throughout the world. These services include:

| · | Cash-in-Transit (“CIT”) Services – armored vehicle transportation of valuables |

| · | ATM Services – replenishing and maintaining customers’ automated teller machines; providing network infrastructure services |

| · | Global Services* – secure international transportation of valuables |

| · | Cash Management Services* |

| o | Currency and coin counting and sorting; deposit preparation and reconciliations; other cash management services |

| o | Safe and safe control device installation and servicing (including our patented CompuSafe® service) |

| o | Check and cash processing services for banking customers (“Virtual Vault Services”) |

| o | Check imaging services for banking customers |

| · | Payment Services* – bill payment and processing services on behalf of utility companies and other billers at any of our Brink’s or Brink’s – operated payment locations in Latin |

| · |

* We consider these to be High-Value Services as described in more detail on page 3.