POWELL INDUSTRIES, INC.

TABLE OF CONTENTS

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS;

RISK FACTORS

Unless otherwise indicated, all references to “we,” “us,” “our,” “Powell” or “the Company” include Powell Industries, Inc. and its consolidated subsidiaries.

Forward-Looking Statements

This Annual Report on Form 10-K (Annual Report) includes forward-looking statements based on our current expectations, which are subject to risks and uncertainties. Forward-looking statements include information concerning future results of operations and financial condition. Statements that contain words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “continue,” “should,” “could,” “may,” “plan,” “project,” “predict,” “will” or similar expressions may be forward-looking statements. These forward-looking statements are subject to risks and uncertainties, and many factors could affect the future financial results and condition of the Company. Factors that may have a material effect on our revenues, expenses and operating results include, among other things, adverse business or market conditions, our ability to meet our customers’ scheduling requirements, our customers’ financial conditions and their ability to secure financing to support current and future projects, the availability and cost of materials from suppliers, availability of skilled labor force, adverse competitive developments and changes in customer requirements as well as those circumstances discussed under “Item“Part I, Item 1A. Risk Factors,” below. Accordingly, actual results may differ materially from those expressed or implied by the forward-looking statements contained in this Annual Report. Any forward-looking statements made by or on our behalf are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

The forward-looking statements contained in this Annual Report are based on current assumptions that we will continue to develop, market, manufacture and ship products and provide services on a competitive and timely basis; that economic and competitive conditions in our markets will not change in a materially adverse way; that we will accurately identify and meet customer needs for products and services; that we will be able to hire and retain skilled laborers and key employees; that our products and capabilities will remain competitive; that the financial markets and banking systems will remain stable and availability of credit will continue; that risks related to shifts in customer demand are minimized and that there will be no material adverse change in the operations or business of the Company. Assumptions relating to these factors involve judgments that are based on available information, which may not be complete, and are subject to changes in many factors beyond the Company’s control that can materially affect results. Because of these and other factors that affect our operating results, past financial performance should not be considered an indicator of future performance, and investors should not use historical trends to anticipate results or trends in future periods.

3

PART I

Item 1. Business

Overview

Powell Industries, Inc. was incorporated in the state ofis a Delaware in 2004 as a successor to a Nevada company incorporated in 1968. The Nevada company was the successor to a companycorporation founded by William E. Powell in 1947,1947. We develop, design, manufacture and service custom-engineered equipment and systems which merged into(1) distribute, control and monitor the Company in 1977.flow of electrical energy and (2) provide protection to motors, transformers and other electrically powered equipment. We are headquartered in Houston, Texas, and our major subsidiaries, all of which are wholly owned, include: Powell Electrical Systems, Inc.; Powell (UK) Limited; Powell Canada, Inc.; and Powell Industries International, B.V.

Our website is powellind.com. We make available, free of charge on or through our website, copies of thisour Annual ReportReports on Form 10-K, and other reports,Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as is reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC). Additionally, all of our reports filed with the SEC are available via their website at http://www.sec.gov, or may be readwww.sec.gov.

References to Fiscal 2021, Fiscal 2020 and copied at the SEC Public Reference Room at 100 F Street, NE, Washington, DC 20549.Fiscal 2019 used throughout this Annual Report relate to our fiscal years ended September 30, 2021, 2020 and 2019, respectively.

Our principal products include integrated power control room substations (PCRs®), custom-engineered modules, electrical houses (E-Houses), traditional and arc-resistant distribution switchgear and control gear, medium-voltage circuit breakers, monitoring and control communications systems, motor control centers, switches and bus duct systems. These products are designed for application voltages ranging from 480 volts to 38,000 volts and are used in oil and gas refining, onshore and offshore oil and gas production, petrochemical, liquefied natural gas (LNG) terminals, pipeline, terminal, mining and metals, light rail traction power, electric utility, pulp and paper and other heavy industrial markets. Our product scope includes designs tested to meet both U.S. and international standards, under both the American National Standards Institute (ANSI) and international standardsInternational Electrotechnical Commission (IEC). We assist customers by providing value-added services such as spare parts, field service inspection, installation, commissioning, modification and repair, retrofit and retrofill components for existing systems and replacement circuit breakers for switchgear that is obsolete or that is no longer produced by the original manufacturer. We seek to establish long-term relationships with the end users of our systems as well as the engineering, procurementdesign and construction (EPC)engineering firms contracted by those end users.

Products and services are principally sold directly to the end user or to an EPCengineering, procurement and construction (EPC) firm on behalf of the end user. Each project is specifically engineered and manufactured to meet the exact specifications and requirements of the individual customer. Powell’s expertise is in the design and engineering, manufacturing, project management and integration of the various systems into a single, custom-engineered deliverable. We market and sell our products and services, which are typically awarded in competitive bid situations, to a wide variety of customers and governmental agencies spanning across diverse markets and geographic regions. Contracts often represent large-scale and complex projects with an individual customer. By their nature, these projects are typically nonrecurring. Thus, multiple and/or continuous projects of similar magnitude with the same customer may vary. As such, theare not predictable. The timing of large project awards may cause material fluctuations in our revenues and gross profits.

Occasionally our contracts may operate under a consortium or teaming arrangement. Typically, we enter into these arrangements with reputable companies with which we have conducted business with previously. These arrangements are generally made to leverage competitive positioning or where scale and/or size dictates the use of such arrangement.

Due to the nature and timing of large projects, a significant percentage of our revenues in a given period may result from one specific contract or customer. Although we could be adversely impacted by a significantThe large domestic industrial project that was awarded in Fiscal 2020 accounted for approximately 20% of our consolidated revenues in Fiscal 2021 and represents approximately 25% of our consolidated backlog going into Fiscal 2022. We believe the reduction in business volume from a particular industry we do not believeor the loss of any specifica major customer wouldcould have a materialan adverse effect on our business. However, from

From time to time, an individual manufacturing facility may have significant volume from one particular customer whichthat would be material to that facility. If during that time the customer were to experience financial distress, a decline in business or circumstances that would otherwise necessitate a cancellation of a project with us, our revenue could be adversely impacted. No customer accounted for more than 10% of our consolidated revenues in Fiscal 2017, Fiscal 20162020 or Fiscal 2015. 2019.

4

Research and development activities are critical to Powell’s future and are focused on both the development of new products and services as well as enhancing current product offerings. Our expertise in vacuum circuit breaker engineering is internationally recognized, and we have a sustained commitment to incorporating continuous product improvements that will ensure operational safety and reliability across the markets we serve.

Markets

We strive to be the supplier of choice for custom-engineered system solutions and services to a variety of customers and markets. Our activities are predominantly in the oil and gas and the electric utility industries, but also include other markets where customers need to manage, monitor and control large amounts of electrical energy.energy through a complex network of electrical components and systems. The majority of our business is in support of capital investment projects that are highly complex and competitively bid. Our customized systems are designed to meet the specifications of our customers. Each system is designed, engineered and manufactured to the specific requirements of the particular application. We consider our engineering, project management, systems integration and technical support capabilities vital to the success of our business.

Specific to the oil and gas sector (excluding petrochemical), we serve the upstream, midstream and downstream end markets. Within the downstream segment, our primary customers typically are engaged in refining activities and/or leveraging natural gas feedstocks for the production of petrochemical or LNG products. We have developed strong relationships with our customers over the years and strive to maintain our position as a preferred service provider to solve our customers' complex electrical needs.

We believe that our products and services, integration capabilities, technical and project management strengths,acumen, application engineering expertise and specialty contracting experience, together with our responsivenessfinancial strength and flexibilityresponsiveness to the needs of our customers, and our financial strength, give us a sustainable competitive advantage in our markets. We compete with a small number of multinational competitors that sell to a broad industrial and geographic market, as well as smaller, regional competitors that typically have limited capabilities and scope of supply. Some of our competitors are significantly larger and have substantially greater global resources such as engineering, manufacturing and marketing. Our principal competitors include ABB, Eaton, General Electric Company, Schneider and Siemens. The competitive factors used during bid evaluation by our customers vary from project to project and may include technical support and application expertise, engineering and manufacturing capabilities, equipment rating, delivered value, scheduling and price. While projects are typically non-recurring, a significant portion of our business is from repeat customers and many times involves third-party EPC firms hired by the end user and with whichwhom we also have long, and established relationships. Ultimately, our competitive position is dependent upon our ability to provide quality custom-engineered products, services and systems on a timely basis at a competitive price.

Backlog

Backlog represents management's estimate of the dollar amount of revenue that we expect to realizeremaining unsatisfied performance obligation from work to be performed on our firm orders under uncompleted contracts and customer purchase orders, including approved change orders as well as new contractual agreements on which work has not begun. Our backlog will be recognized as revenue as we complete the remaining performance obligations. Our backlog does not include service and maintenance type contracts for which we have the rights to invoice as services are performed. Typically, our contracts may have an early termination for convenience clause at the discretion of our customers; however, most of these contracts typically provide for the reimbursement of our costs incurred and a reasonable margin in the event of such early termination. Our methodology for determining backlog may not be comparable to the methodology used by other companies. Orders included in our backlog are represented by customer purchase orders and contracts, which we believe to be firm.

Our backlog at September 30, 20172021 totaled $250.1$414.9 million compared to $291.4$476.8 million at September 30, 2016. Backlog declined primarily due to lower demand in our core oil, gas and petrochemical markets.2020. We anticipate that approximately $235.3$291.0 million of Fiscal 20172021 ending backlog will be fulfilled during our fiscal year ending September 30, 2018.2022. Backlog may not be indicative of future operating results as orders in our backlog may be cancelled or modified by our customers.customers and may not be indicative of continuing revenue performance over future fiscal quarters.

Raw Materials and Suppliers

The principal raw materials used in our operations include steel, copper and aluminum and various electrical components. Material costs represented 49% of revenues in Fiscal 2021 and 47% of revenues in both Fiscal 20172020 and Fiscal 2016 and 46% in Fiscal 2015.2019. Unanticipated changes in material requirements, market conditions and disruptions in suppliesthe supply chain or price increases could impact production costs and affect our consolidated results of operations.

5

Our supply base for certain key components and raw materials is limited. Changes in our design to accommodate similar components from other suppliers could be implemented to resolve a supply problem related to a sole-sourced component. In this circumstance, supply problems could result in delays in our ability to meet commitments to our customers. We believe that sources of supply for raw materials and components are generally sufficient, and we do not believe a temporary shortage of materials will cause any significant adverse impact in the future. While we are not dependent on any one supplier for the majority of our raw materials, we are highly dependent on our suppliers in order to meet commitments to our customers. During Fiscal 2021, as a result of the challenges created by global transportation issues, the COVID-19 pandemic and market volatility, we experienced minor supply disruptions and anticipate that supply disruptions and material shortages may continue. We continue to work with our key suppliers who have been impacted by these supply disruptions to ensure that we are able to meet our customer commitments. While we have not currently experienced significant or unusual issues in the purchase of key raw materials or components, inwe continue to monitor the past three fiscal years. availability (including transportation) and price of components and raw materials on a regular basis, as well as any potential impact on our operations.

Our business is subject to the effects of changing material prices. DuringWhile raw material costs have been relatively stable in the last three fiscalpast few years, during Fiscal 2021 we have begun to encounter availability constraints from key suppliers as well as cost increases driven by using alternate suppliers, increased commodity costs as well as higher logistics expense. While these availability challenges have not experienced significant price volatility for raw materials or component parts usedcurrently created execution challenges, we continue to monitor material availability closely. We cannot, however, provide assurance that we will continue to mitigate these material shortages, in the productionwhich case our results of our products.operations may be adversely affected. While the cost outlook for commodities used in the production of our products is not certain, we believe we can manage this volatility through contract pricing adjustments, with material-cost predictive estimating and by actively pursuing internal cost reduction efforts. We did not enter into any derivative contracts to hedge our exposure to commodity price changes in Fiscal 2017, 20162021, 2020 or 2015.2019.

At September 30, 2017,2021, we had 1,8411,892 full-time employees and 181 contract employees located primarily in the U.S., Canada and the U.K. Our employees are not represented by unions, and we believe that our relationship with our employees is good. Periodically, demand for qualified personnel increases in certain geographic areas due to increased construction or economic activity. We continue to monitor our demand for skilled and unskilled labor and provide training and competitive compensation packages in an effort to attract and retain skilled employees. Labor shortages or increased labor costs could impair our ability to maintain our business, meet customer commitments or grow our revenues, and may adversely impact our business and results of operations.

Three of our top human capital priorities are workplace safety, internal promotion and key employee retention. Powell emphasizes a culture of safety that runs throughout the Company. We establish annual goals and monthly operating metrics, which have resulted in a safety incident rate that is one-half the industry average across Powell. We believe that internal promotion and key employee retention are critical components to our long-term success. The average tenure of our employees is 11 years. Our annual Organizational Capabilities Review is focused on succession planning within our organization and is reviewed annually by our Board of Directors. We measure our success based on the percentage of internal promotions to key positions and our ability to attract and retain key employees.

Intellectual Property

While we are the holder ofhold various patents, trademarks, servicemarks, copyrights and licenses, we do not consider any individual intellectual property to be material to our consolidated business operations.

Seasonality

Our operations are not generally affected by seasonality. However, weather and natural phenomena can temporarily impact the performance of our operations. Furthermore, quarterly operating results may fluctuate in our first fiscal quarter due to the reduction in the number of workdays related to the number of holidays in that fiscal quarter.

Government Regulations

We are subject to various government regulations in the United States as well as various international locations where we operate. These regulations cover diverse areas including environmental compliance, import and export controls, economic sanctions, data and privacy protection, transfer pricing rules, anti-bribery, anti-trafficking and anti-trust provisions. Our policies mandate compliance with applicable laws and regulations administered by various state, federal and international agencies. We maintain various training programs to educate our employees on compliance with governmental regulations, as well as applied

6

legal and ethical practices in our everyday work. We do not believe that compliance with governmental regulations will have a material impact on our capital expenditures, results of operations or competitive position.

Item 1A. Risk Factors

Our business is subject to a variety of risks and uncertainties, including, but not limited to, the risks and uncertainties described below. If any of the following risks actually occur, our business,the business's financial condition, cash flows, liquidity and results of operations couldmay be negatively impacted, and we may not be able to achieve our quarterly, annual or long-range plans. Additional risks and uncertainties not known to us or not described below may also negatively impact our business and results of operations. This Annual Report also includes statements reflecting assumptions, expectations, projections, intentions or beliefs about future events that are intended as “forward-looking statements” under the Private Securities Litigation Reform Act of 1995 and should be read in conjunction with the discussion under “Forward-Looking Statements,” above.

Risk Factors Related to our Business and Industry

Our business is largely dependent on customers insubject to the oil and gascyclical nature of the end markets andthat we are adversely impacted by extended periods of low oil or gas prices, which decrease our customers’ spending, the demand for our products and services and the prices we are able to charge.serve. This has had, and may continue to have, an adverse effect on our future operating results.

Our industry is highly competitive.

Some of our competitors are significantly larger and have substantially greater global resources such as engineering, manufacturing and marketing resources.resources, and at various times, may be a customer or supplier on any given project. Competition in the industry depends on a number of factors, including the number of projects available, technical ability, production capacity, location and price.the ability to win projects we bid. Certain of our competitors may have lower cost structures and may, therefore, be able to provide their products or services at lower prices than we are able to provide.prices. Similarly, we cannot be certain that we will be able to maintain or enhance our competitive position within our industry, maintain our customer base at current levels, increase our customer base or continue to provide technologically superior products at a competitive price. New companies may enter the markets in which we compete, or industry consolidation may occur, further increasing competition in our markets. Our failure to compete effectively and secure projects we bid could adversely affect future revenues and have an adverse impact on our results of operations.

Technological innovations by competitors may make existing products and production methods obsolete.

All of the products that we manufacture and sell depend upon the best available technology for success in the marketplace. The industries in which we operate are characterized by intense competition and are highly sensitive to technological innovation and customer requirements. It is possible for competitors (both domestic and international) to develop products or production methods that will make current products or methods obsolete or at a minimum hasten their obsolescence; therefore, we cannot be certain that our competitors will not develop the expertise, experience and resources to provide products and services that are superior in both price and quality. Our future success will depend, in part, on our ability to anticipate and offer products that meet changing customer specifications.specifications as well as fund our research and development costs. Consumer demand for further automation is changing the markets we operate in. Failure to successfully develop new products, or to enhance existing products, could result in the loss of existing customers to competitors, the inability to attract new business or an overall reduction in our competitive position, any of which may adversely affect our business or results of operations.

7

Unforeseen difficulties with expansions, relocations, or consolidations of existing facilities could adversely affect our operations.

From time to time we may decide to enter new markets, build or lease additional facilities, expand our existing facilities, or relocate or consolidate one or more of our operations.operations or exit a facility we may own or lease. Increased costs and production delays arising from the staffing, relocation, sublease, expansion or consolidation of our facilities could adversely affect our business and results of operations.

Quality problems with our products could harm our reputation and erode our competitive position.

The success of our business depends upon the quality of our products and our relationships with customers. In the event that one of our products fails to meet our customers' standards or safety requirements or fails to operate effectively, our reputation could be harmed, which would adversely affect our marketing and sales efforts. We provide warranties to our customers for our products and the cost to satisfy customer warranty claims, which may include, among other things, costs for the repair or replacement of products, could adversely impact our business and results of operations.

Growth and product diversification through strategic acquisitions involves a number of risks.

Our strategy includes the pursuit of growth and product diversification through the acquisition of companies or assets and entering into joint ventures that will enable us to expand our geographic coverage and product and service offerings. We periodically review potential acquisitions; however, we may be unable to successfully implement this strategy. Acquisitions involve certain risks, including difficulties in the integration of operations and systems; failure to realize cost savings; the termination of relationships by key personnel and customers of the acquired company and a failure to add additional employees to handle the increased volume of business. Additionally, financial and accounting challenges and complexities in areas such as valuation, tax planning, treasury management and financial reporting from our acquisitions may impact our operating results. Due diligence may not be adequate or reveal all risks and challenges associated with our acquisitions. Companies that we acquire may not achieve revenues, profitability or cash flows that we expected, or that ultimately justify the investment. It is possible that impairment charges resulting from the overpayment for an acquisition may negatively impact our results of operations. Financing for acquisitions may require us to obtain additional equity or debt financing, which may not be available on attractive terms, if at all, or which may be restricted under the terms of our credit facilitiesfacility or other financing arrangements. Any failure to successfully complete or successfully integrate acquisitions could have a material adverse effect on our business and results of operations.

Our business requires skilled and unskilled labor, and we may be unable to attract and retain qualified employees.

Our ability to maintain our productivity at competitive levels may be limited by our ability to employ, compensate, train and retain personnel necessary to meet our requirements. We face competition for qualified personnel in our industry. We may experience shortages of qualified personnel such as engineers, project managers and select skilled trades. We cannot be certain that we will be able to maintain an adequate skilled or unskilled labor force or key technical personnel necessary to operate efficiently and to support our growth strategy and operations. We cannot be certain that our labor costs will not increase as a result of a shortage in the supply of skilled, unskilled and technical personnel or any governmental regulations. Labor shortages or increased labor costs could impair our ability to maintain our business, meet customer commitments or grow our revenues, and may adversely impact our business and results of operations.

We are exposed to risks relating to the use of subcontractors on some of our projects.

We hire subcontractors to perform work on some projects and sometimes depend on third-party suppliers to provide equipment and materials necessary to complete or ship our products. If our subcontractors do not perform as expected for any reason, we may experience delays in completing our projects or incur additional costs. In addition, we may have disputes with these independent subcontractors arising from, among other things, the quality and timeliness of the work they have performed. Any of these factors could adversely impact our business and results of operations.

8

Misconduct by our employees or subcontractors, or a failure to comply with laws or regulations, could harm our reputation, damage our relationships with customers and subject us to criminal and civil enforcement actions.

Misconduct, fraud, non-compliance with applicable laws and regulations, or other improper activities by one or more of our employees or subcontractors could have a significant negative impact on our business and reputation. While we take precautions to prevent and detect these activities, such precautions may not be effective and are subject to inherent limitations, including human error and fraud. Acts of misconduct, or our failure to comply with applicable laws or regulations, could subject us to fines and penalties, harm our reputation, damage our relationships with customers and could adversely impact our business and results of operations.

Unsatisfactory safety performance may subject us to penalties, negatively impact customer relationships, result in higher operating costs, and negatively impact employee morale and turnover.

We place great emphasis on workplace safety in our entire organization through various safety initiatives and training. We have both indoor and outdoor manufacturing facilities that are susceptible to numerous industrial safety risks that can lead to personal injury, loss of life, damage to property and equipment, as well as potential environmental damage. While we take every precaution to avoid incidents, we have experienced accidents in the past and may again in the future, which can negatively affect our safety record. A poor safety record can harm our reputation with existing and potential customers, jeopardize our relationship with employees, increase our insurance costs and could adversely impact our business and results of operations.

Catastrophic events, including natural disasters, health epidemics (including the COVID-19 pandemic), acts of war and terrorism, among others, could disrupt our business.

The occurrence of catastrophic events, ranging from natural disasters to health epidemics (including the COVID-19 pandemic), to acts of war and terrorism, among others, could disrupt or delay our ability to operate our business and complete projects for our customers and could potentially expose us to third-party liability claims. A significant portion of our operations are located near the Texas Gulf Coast. Our operations have been and are subject to the potential impacts of weather-related events such as hurricanes and flooding. Future weather events could cause significant damage to our property and equipment and adversely impact our operations. We may declare the existence of a force majeure event under our contracts in certain situations; however, a customer may dispute our force majeure claim, which may result in additional liabilities. Losses arising from such events may or may not be fully covered by our various insurance policies or may be subject to deductibles or exceed coverage limits. In addition, such events could result in temporary or long-term delays and/or cancellations of orders for raw materials from our suppliers that could impact our project execution. These situations or other disruptions are outside of our control and may adversely impact our business and results of operations.

The COVID-19 pandemic continues to create significant uncertainty and economic disruption across the world. It is difficult to predict the economic impact that the COVID-19 pandemic may continue to have on our business, results of operations and cash flows going forward. Certain of our customers have asked that we delay or cancel our manufacturing on their projects as their operations have been negatively impacted by this pandemic. These delays and cancellations may have a negative effect on the timing of revenue recognition and cash flow. We have experienced supply disruptions and anticipate these supply disruptions may continue. Any delays in the supply of material or labor could negatively impact our production schedule and delay the completion of certain projects. The extent to which the COVID-19 pandemic specifically will impact our business will depend on numerous factors that are hard to predict, some of which include: the duration, spread and severity of the pandemic; governmental actions in response to the pandemic; including travel restrictions and quarantine or related orders; any closures of our offices and facilities or those of our suppliers as a result of the pandemic, and how quickly and to what extent normal economic and operating conditions can resume. Any of these factors, as well as other related business impacts resulting from COVID-19, could contribute to the risks and uncertainties described in this Annual Report. As a result, the magnitude of the impact on our business, results of operations and cash flows is not currently known.

9

Risk Factors Related to our Financial Condition and Markets

Economic uncertainty and financial market conditions may impact our customer base, suppliers and backlog.

Various factors drive demand for our products and services, including the price and demand for oil and gas, capital expenditures, economic forecasts and financial markets. Unanticipated increases in raw material requirements or prices, the imposition of tariffs, and changes in supplier availability or supplier consolidation, could increase production costs and adversely affect profitability. Uncertainty regarding these factors could impact our customers and severely impact the demand for projects and orders for our products and services. Additionally, the loss of significant volume from one particular customer at one of our facilities could adversely impact the operating results of that facility. If one or more of our suppliers or subcontractors experiences difficulties that result in a reduction, delay or interruption in supply to us, or they fail to meet our manufacturing requirements, our business could be adversely impacted until we are able to secure alternative sources. Furthermore, our ability to maintain or expand our business would be limited in the future if we are unable to maintain or increase our bonding capacity or our bank credit facility on favorable terms or at all. Similarly, disruptions in the capital markets may also adversely impact our customer's ability to finance projects, which could result in contract cancellations or delays. These disruptions could lead to reduced demand for our products and services and could have an adverse impact on our business, financial condition and results of operations.

Our backlog is subject to unexpected adjustments, cancellations and scope reductions and, therefore, may not be a reliable indicator of our future earnings.

We have a backlog of uncompleted contracts. Backlog represents management's best estimate of the remaining performance obligation from work to be performed on uncompleted contracts, including new contractual agreements on which work has not begun. From time to time, projects are cancelled, delayed or modified due to customer, industry or macroeconomic conditions. While we may be reimbursed for certain costs, we may not have a contractual right to the total revenue reflected in our backlog. We may be unable to recover certain direct costs and cancelled projects may also result in additional unrecoverable costs due to the underutilization of our assets. Accordingly, the amounts recorded in backlog may not be a reliable indicator of our future operating results and may not be indicative of continuing revenue performance over future fiscal quarters.

Revenues recognized over time from our fixed-price contracts could result in volatility in our results of operations.

As discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Critical Accounting Estimates” and in the Notes to Consolidated Financial Statements included elsewhere in this Annual Report, the majority of our revenues are recognized over time. Revenues are recognized as work is performed and costs are incurred. The revenue earned to date is calculated by multiplying the total contract price by the percentage of performance to date, which is based on total costs incurred to date compared to the total estimated costs at completion. The determination of the revenue recognized requires the use of estimates of costs to be incurred for the performance of the contract. The timing of the costs incurred may lead to fluctuations in revenue recognized on a quarterly and annual basis. The cost estimation process is based upon the professional knowledge and experience of our management teams, engineers, project managers and financial professionals. We bear the risk of cost overruns in most of our contracts, which may result in reduced profits. Contract losses are recognized in full when determined, and estimates of revenue and cost to complete are adjusted based on ongoing reviews of estimated contract performance. Previously recorded estimates of revenues and costs are adjusted as the project progresses and circumstances change. In certain circumstances, it is possible that such adjustments to costs and revenues could have an adverse impact on our results of operations.

Many of our contracts contain performance obligations that may subject us to penalties or additional liabilities.

Many of our customer contracts have schedule and performance obligation clauses that, if we fail to meet, could subject us to penalty provisions, liquidated damages or claims against the company or our outstanding letters of credit or performance bonds. In addition, some customer contracts stipulate protection against our gross negligence or willful misconduct. Each individual contract defines the conditions under which the customer may make a claim against us. It is possible that adjustments arising from such claims, or our failure to manage our contract risk, may not be covered by insurance and could have an adverse impact on our results of operations.

10

Fluctuations in the price and supply of materials used to manufacture our products may reduce our profits and could adversely impact our ability to meet commitments to our customers.

Our material costs represented 49% of our consolidated revenues for Fiscal 2021. Unanticipated increases in raw material requirements, rising prices due to overall inflationary pressure, the imposition of tariffs, changes in supplier availability, delays in transportation, or supplier consolidation could increase production costs and adversely affect profitability as fixed-price contracts may prohibit our ability to charge the customer for the increase in raw material prices. We purchase a wide variety of materials and component parts from various suppliers to manufacture our products, including steel, aluminum, copper and various components. Our supply base for certain key components and raw materials is limited and may come from a single supplier. If we are unable to obtain key components and raw materials from these suppliers, the key components and raw materials may not be readily available from other suppliers or available with acceptable terms. Our success depends on our ability to meet customer commitments and could be negatively impacted if a supplier experiences a disruption or discontinuance in their operations or we experience a delay in transportation of materials and components from our suppliers. The time and effort associated with the selection and qualification of a new supplier and changes in our design and testing to accommodate similar components from other suppliers could be significant. Additionally, we rely on certain competitors for key materials used in our products. This could negatively impact our ability to manufacture our products if the relationships change or become adversarial.

Obtaining surety bonds, letters of credit, bank guarantees, or other financial assurances, may be necessary for us to successfully bid on and obtain certain contracts.

We are often required to provide our customers security for the performance of their projects in the form of surety bonds, letters of credit or other financial assurances. Our continued ability to obtain surety bonds, letters of credit or other financial assurances will depend on our capitalization, working capital and financial performance. Our ability to issue letters of credit is dependent upon the availability of adequate credit issued by our banks and could be negatively impacted by our compliance with our financial covenants. Future compliance with such financial covenants may be affected by factors beyond our control, including general or industry-specific economic downturns. We are also dependent on the overall bonding capacity, pricing and terms available in the surety markets. As such, we cannot guarantee our ability to maintain a sufficient level of bonding capacity in the future. The restriction, reduction or termination of our surety bond agreements could limit our ability to bid on new opportunities and would require us to issue letters of credit under our bank facilities in lieu of surety bonds, thereby reducing availability under our credit facility, which could have an adverse impact on our business and results of operations.

Failure to remain in compliance with covenants or obtain waivers or amendments under our credit agreement could adversely impact our business.

Our credit agreement contains various financial covenants and restrictions, which are described in Note G of the Notes to Consolidated Financial Statements. Our ability to remain in compliance with such financial covenants and restrictions may be affected by factors beyond our control, including general or industry-specific economic downturns. If we fail to remain in compliance with such covenants and restrictions, absent an amendment or waiver, this could result in an event of default under the credit agreement. Among other things, the occurrence of an event of default could limit our ability to issue letters of credit, obtain additional financing or result in acceleration of outstanding amounts under the credit agreement or a termination of the agreement, any of which could have an adverse impact on our liquidity, business and results of operations.

We extend credit to customers in conjunction with our performance under fixed-price contracts which subjects us to potential credit risks.

We typically agree to allow our customers to defer payment on projects until certain milestones have been met or until the projects are substantially completed, and customers typically withhold some portion of amounts due to us as retainage. Our payment arrangements subject us to potential credit risk related to changes in business and economic factors affecting our customers, including material changes in our customers' revenues or cash flows. If we are unable to collect amounts owed to us, or retain amounts paid to us, our cash flows would be reduced, and we could experience losses if those amounts exceed current allowances. Any of these factors could adversely impact our business and results of operations.

11

A significant portion of our revenues may be concentrated among a small number of customers.

Due to the nature and timing of large projects, a significant percentage of our revenues in a given period may result from one specific contract or customer. During Fiscal 2021, approximately 20% of our consolidated revenues were generated from our large domestic industrial project that was awarded in Fiscal 2020. We believe the reduction in business volume from a particular industry or the loss of a major customer could have an adverse effect on our business. From time to time, an individual manufacturing facility may have significant volume from one particular customer that would be material to that facility. If during that time the customer were to experience financial distress, a decline in business or circumstances that would otherwise necessitate a cancellation of a project with us, our revenue could be adversely impacted.

We carry insurance against many potential liabilities, but our management of risk may leave us exposed to unidentified or unanticipated risks.

Although we maintain insurance policies with respect to our related exposures, including certain casualty, property, professional, business interruption, cyber security and self-insured medical and dental programs, these policies contain deductibles, self-insured retentions and limits of coverage. In addition, we may not be able to continue to obtain insurance at commercially reasonable rates, or at the policy limits we may require or may be faced with liabilities not covered by insurance, such as, but not limited to, environmental contamination or terrorist attacks. We estimate our liabilities for known claims and unpaid claims and expenses based on information available as well as projections for claims incurred but not reported. However, insurance liabilities, some of which are self-insured, are difficult to estimate due to various factors. If any of our insurance policies, coverage limits or programs are not effective in mitigating our risks, we may incur losses that are not covered by our insurance policies, that are subject to deductibles or that exceed our estimated accruals or our insurance policy limits, which could adversely impact our business and results of operations.

Our international operations expose us to risks that are different from, or possibly greater than, the risks we are exposed to domestically and may adversely affect our operations.

Revenues associated with projects located outside of the U.S., including revenues generated from our operations in the U.K. and Canada, accounted for approximately 25% of our consolidated revenues in Fiscal 2021. While our manufacturing facilities are located in developed countries with historically stable operating and fiscal environments, our business and results of operations could be adversely affected by a number of factors, including: political and economic instability; social unrest, acts of terrorism, force majeure, war or other armed conflict; inflation; changes in tax laws; the application of foreign labor regulations; currency fluctuations, devaluations and conversion restrictions and/or governmental activities that limit or disrupt markets, restrict payments or limit the movement of funds and trade restrictions or economic embargoes imposed by the U.S. or other countries. Additionally, the compliance with foreign and domestic import and export regulations and anti-corruption laws, such as the U.S. Foreign Corrupt Practices Act, General Data Protection Regulation, or similar laws of other jurisdictions outside the U.S., could adversely impact our ability to compete for contracts in such jurisdictions. Moreover, the violation of such laws or regulations, by us or our representatives, could result in severe penalties including monetary fines, criminal proceedings and suspension of export privileges.

Additionally, fluctuating foreign currency exchange rates may impact our financial results. The functional currency of our foreign operations is typically the currency of the country in which the foreign operation is located. Accordingly, our financial performance is subject to fluctuations due to changes in foreign currency exchange rates relative to the U.S. dollar.

Failures or weaknesses in our internal controls over financial reporting could adversely affect our ability to report on our financial condition and results of operations accurately and/or on a timely basis.

We are required to comply with Section 404 of the Sarbanes-Oxley Act of 2002, which requires, among other things, an assessment by our management of our internal control over financial reporting. Preparing our financial statements involves a number of complex processes, many of which are performed manually and are dependent upon individual data input or review. We are continually working to maintain and strengthen our internal controls over financial reporting, however, any system of controls has limitations, including the possibility of human error, the circumvention or overriding of controls and/or fraud. Our failure to maintain effective internal controls over financial reporting could adversely affect our ability to report our financial results on a timely and accurate basis, which could result in a loss of investor confidence in our financial reports or have an adverse impact on our business and results of operations.

12

A failure in our business systems or cyber security attacks on any of our facilities, or those of third parties, could adversely affect our business and our internal controls.

Our organization is dependent upon the proper functioning of our business systems that support our production, engineering, human resources, estimating, finance, and project management functions. If any of our financial, operational, or other data processing systems fail or have other significant shortcomings due to natural disaster, power loss, telecommunications failures, cyber security attacks or other similar events, our business or results of operations could be adversely affected. In addition, despite implementation of security measures, our business systems may be vulnerable to computer viruses, ransomware attacks, cyber-attacks, the accidental release of sensitive information and other unauthorized access. These failures of our business systems or security breaches could impact our customers, employees and reputation and result in a disruption to our operations or in legal claims or proceedings. A material network breach of our business systems could involve the theft of intellectual property, financial data, employee or customer data, which may be used by competitors. We rely on third-party systems which could also suffer operational system failure or cyber-attacks. Any of these occurrences may not be covered by insurance and could disrupt our business, result in potential liability or reputational damage or otherwise have an adverse effect on our business or results of operations.

Network security and internal control measures have been implemented to address these risks and disruptions to our business. However, our portfolio of hardware and software products, solutions and services and information contained within our enterprise information technology (IT) systems may be vulnerable to damage or disruption caused by circumstances beyond our control such as catastrophic events, cyber-attacks, other malicious activities from unauthorized third parties, power outages, natural disasters, computer system or network failures or computer viruses. Any significant disruption or failure could damage our reputation or have a material adverse effect on our business and our results of operations.

Risk Factors Related to our Common Stock

Our stock price could decline or fluctuate significantly due to unforeseen circumstances. These fluctuations may cause our stockholders to incur losses.

Our stock price could fluctuate or decline due to a variety of factors including, but not limited to, the risks factors described herein, the timing and cancellation of projects, changes in our estimated costs to complete projects, investors' opinions of the sectors and markets in which we operate or failure of our operating results to meet the expectations of securities analysts or investors, which could reduce investor confidence. These factors could adversely affect our business, and the trading price of our common stock could decline significantly.

There can be no assurance that we will declare or pay future dividends on our common stock.

Our Board of Directors has approved a regular quarterly dividend since Fiscal 2014. The declaration, amount and timing of future dividends are subject to capital availability and determinations by our Board of Directors that cash dividends are in the best interest of our stockholders and are in compliance with all respective laws and applicable agreements. Our ability to declare and pay dividends will depend upon, among other factors, our financial condition, results of operations, cash flows, current and anticipated expansion plans, requirements under Delaware law and other factors that our Board of Directors may deem relevant. A reduction in or elimination of our dividend payments could have a material negative effect on our stock price.

Risk Factors Related to Legal and Regulatory Matters

Our operations could be adversely impacted by the effects of government regulations.

We are subject to various government regulations in the United States as well as various international locations where we operate. These regulations cover several areas including environmental compliance, import and export controls, economic sanctions, data and privacy protection, transfer pricing rules, anti-bribery, anti-trafficking and anti-trust provisions. These laws and regulations are administered by various state, federal and international agencies. Changes in policy, laws or regulations, including those affecting oil and gas exploration and development activities or climate change matters and the resulting decisions by customers and other industry participants, could reduce demand for our products and services, which would have a negative impact on our operations. Various regulations have been implemented around the world related to safety and certification requirements applicable to oil and gas drilling and production activities, and we cannot predict whether operators will be able to satisfy these requirements. Further, we cannot predict future changes in any country in which we operate and how those changes may affect our ability to perform projects in those regions.

The Dodd-Frank Wall Street Reform and Consumer Protection Act requires disclosure of use of "conflict" minerals mined from the Democratic Republic of Congo and adjoining countries and our efforts to prevent the use of such minerals. In our industry,

13

conflict minerals are most commonly found in metals. As there may be only a limited number of suppliers offering "conflict-free" metals, we cannot be sure that we will be able to obtain necessary metals in sufficient quantities or at competitive prices. Also, we may face challenges with our customers and suppliers if we are unable to sufficiently verify that the metals used in our products are "conflict-free."

Changes in and compliance with environmental laws and regulations, including those regarding climate change, could adversely impact our financial results.

Private lawsuits or enforcement actions by federal, state, provincial or foreign regulatory agencies may materially increase our costs. Certain environmental laws may make us potentially liable for the remediation of contamination at or emanating from our properties or facilities. Although we seek to obtain indemnities against liabilities relating to historical contamination at the facilities we own or operate, we cannot provide any assurance that we will not incur liabilities relating to the remediation of potential contamination, including contamination we did not cause. These potential environmental liabilities may or may not be fully covered by our various insurance policies and may adversely affect our business and results operations.

Climate change regulations could require us or our customers to incur additional expenditures to either purchase new, or modify existing, equipment or processes. These laws and regulations may also increase our raw materials cost from our suppliers. The potential for future environmental, social and governance (ESG) and climate risk reporting requirements may result in additional costs to monitor, track and report sustainability measures. Additionally, increased attention to climate change, conservation measures, energy transition and consumer demand for alternatives to oil and gas could reduce the demand for oil and gas and have an adverse impact on demand for the products produced by our customers and therefore reduce demand for our products, which could adversely impact our business and results of operations.

Provisions of our charter documents or Delaware law could delay or prevent an acquisition of our company, even if the acquisition would be beneficial to our stockholders, and could make it more difficult to change management.

Because we are governed by Delaware law, we are subject to the provisions of Section 203 of the Delaware General Corporation Law. These provisions prohibit a publicly held Delaware corporation from engaging in a business combination with an interested stockholder, generally, a person who, together with its affiliates, owns, or within the last three years has owned, 15% of our voting stock, for a period of three years after the date of the transaction in which the person became an interested stockholder, unless the business combination is approved in a prescribed manner.

In addition, provisions of our Certificate of Incorporation and bylaws may discourage, delay or prevent a merger, acquisition or other change in control that stockholders might otherwise consider favorable, including transactions in which stockholders might otherwise receive a premium for their shares. These provisions may frustrate or prevent any attempt by our stockholders to replace or remove our current management by making it more difficult to replace or remove our boardBoard of directors.Directors.

Additional restrictions or economic disincentives on U.S. or international trade such as significant increases in tariffs on goods could adversely impact our business. Changes in U.S. or international social, political, regulatory and operating results,economic conditions or in laws and the trading price of our common stock could decline significantly.

Actual and potential claims, lawsuits and proceedings could ultimately reduce our profitability and liquidity and weaken our financial condition.

We could be named as a defendant in compliancelegal proceedings that claim damages in connection with covenants or obtain waivers or amendments underthe operation of our credit agreement could adversely impact our business.

Changes in tax laws and regulations may change our effective tax rate and could have a material effect on our financial results.

We are subject to income taxes in the U.S. and numerous foreign jurisdictions. A change in tax laws, deductions or credits, treaties or regulations, or their interpretation, in the countries in which we operate could result in a higher tax rate on our pre-tax income, which could have a material impact on our net income. We are regularly under audit by tax authorities, and our tax estimates and tax positions could be materially affected by many factors including the final outcome of tax audits and related litigation, the introduction of new tax accounting standards, legislation, regulations and related interpretations, our global mix of earnings, the extent to which deferred tax assets are realized and changes in uncertain tax positions. A significant increase in our statutory tax rates could have a material impact on our net income or loss and cash flow.

The departure of key personnel could disrupt our business.

We depend on the continued efforts of our executive officers, senior management and other key professionals. We cannot be certain that any individual will continue in such capacity for any particular period of time. The loss of key personnel, or the inability to hire and retain qualified employees, could negatively impact our ability to perform and manage our business.

15

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

We own our principal manufacturing and fabrication facilities and periodically lease smaller facilities throughout the U.S., Canada and the U.K. Our facilities are generally located in areas that are readily accessible to materials and labor pools and are maintained in good condition. These facilities are expected to meet our needs for the foreseeable future.

Our principal locations as of September 30, 2017,2021, are as follows:

| Location | Description | Acres | Approximate Square Footage | |||||||||||

| Houston, TX | Corporate office and manufacturing facility | 21.4 | 428,515 | |||||||||||

| Houston, TX | Office and manufacturing facility | 53.4 | 290,554 | |||||||||||

| Houston, TX | Office, fabrication facility and yard | 63.3 | 82,320 | |||||||||||

| North Canton, OH | Office and manufacturing facility | 8.0 | 115,200 | |||||||||||

| Northlake, IL | Office and manufacturing facility | 10.0 | 103,500 | |||||||||||

| Bradford, U.K. | Office and manufacturing facility | 7.9 | 129,200 | |||||||||||

| Acheson, Alberta, Canada | Office and manufacturing facility | 20.1 | 330,168 | |||||||||||

Item 3. Legal Proceedings

We are involved in various legal proceedings, claims and other disputes arising from our commercial operations, projects, employees and other matters which, in general, are subject to uncertainties and in which the outcomes are not predictable. These legal proceedings and claims may not be covered by our insurance policies or may exceed our policy limits. Although we can give no assurances about the resolution of pending claims, litigation or other disputes and the effect such outcomes may have on us, management believes that any ultimate liability resulting from the outcome of pending legalsuch proceedings, claims and other disputes, we doto the extent not believe that the ultimate conclusion of these disputes could materially affectotherwise provided or covered by insurance, will not have a material adverse effect on our consolidated financial position or results of operations cash flow and financial position.or liquidity.

Item 4. Mine Safety Disclosures

Not applicable.

16

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock trades on the NASDAQ Global Market (NASDAQ) under the symbol “POWL.” The following table sets forth, for the periods indicated, the high and low sales prices per share as reported on the NASDAQ for our common stock.

| High | Low | ||||||

| Fiscal 2016: | |||||||

| First Quarter | $ | 35.89 | $ | 25.99 | |||

| Second Quarter | 30.41 | 23.00 | |||||

| Third Quarter | 39.47 | 26.22 | |||||

| Fourth Quarter | 41.10 | 34.40 | |||||

| Fiscal 2017: | |||||||

| First Quarter | $ | 46.68 | $ | 34.81 | |||

| Second Quarter | 40.00 | 30.86 | |||||

| Third Quarter | 35.58 | 31.12 | |||||

| Fourth Quarter | 33.47 | 27.28 | |||||

As of December 1, 2017,6, 2021, the closing price of our common stock on the NASDAQ was $28.53$25.07 per share. As of December 1, 2017,6, 2021, there were 308250 stockholders of record of our common stock. All common stock held in street names areis recorded in the Company’s stock register as being held by one stockholder.

See “Part III, Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of this Annual Report for information regarding securities authorized for issuance under our equity compensation plans.

Dividend Policy

Performance Graph

The following Performance Graph and related information shall not be deemed “soliciting material” or to be “filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

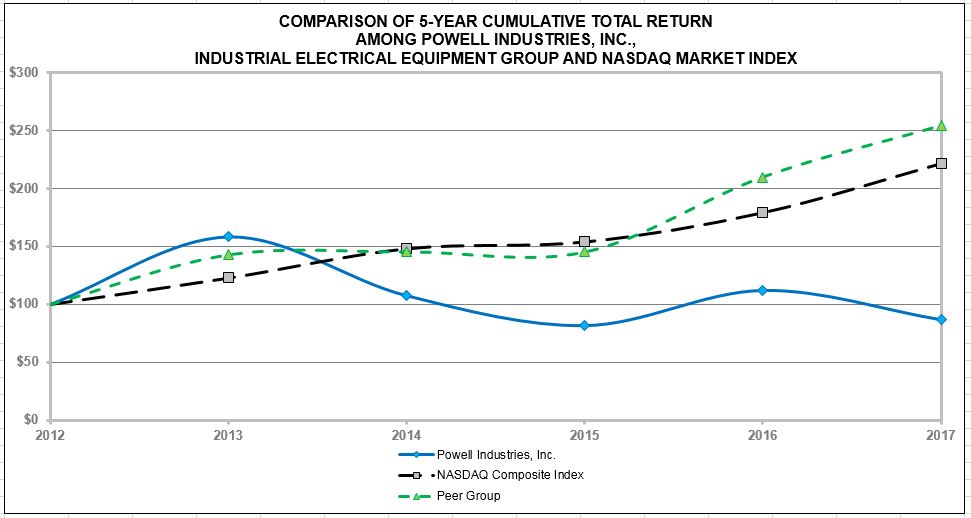

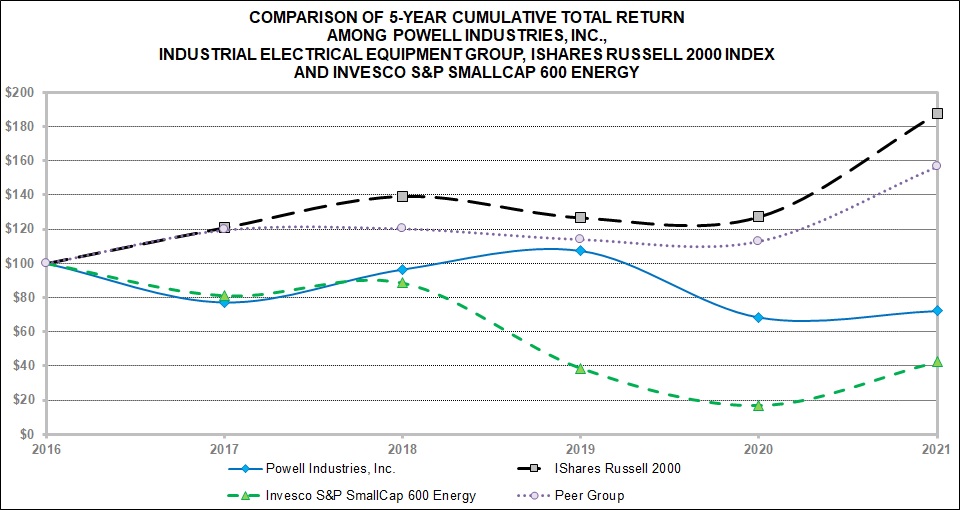

The following graph compares, for the period from October 1, 20122016 to September 30, 2017,2021, the cumulative stockholder return on our common stock with the cumulative total return on the NASDAQ Market IndexIShares Russell 2000, the Invesco S&P SmallCap 600 Energy, and the Industrial Electrical Equipment Group (a select group of peer companies – Altra Industrial Motion Corp.; Ameresco, Inc.; AZZ Inc.; Belden Inc.; Daktronics Inc.; Electro Scientific Industries, Inc.; EnerSys; Franklin Electric Co, Inc.; Littelfuse Inc.; LSI Industries Inc.; Preformed Line Products; A O Smith CorporationCorporation; Thermon Group Holdings and Woodward, Inc.). The comparison assumes that $100 was invested on October 1, 2012,2016, in our common stock, the NASDAQ Market IndexIShares Russell 2000, the Invesco S&P SmallCap 600 Energy, and the Industrial Electrical Equipment Group, and that all dividends were re-invested. The stock price performance reflected on the following graph is not necessarily indicative of future stock price performance.

17

Item 6. SelectedFinancial Data

The selected financial data shown below for the past five years was derived from our audited financial statements, adjusted for discontinuing operations. The historical results are not necessarily indicative of the operating results to be expected in the future. The selected financial data should be read in conjunction with “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this Annual Report.

| Years ended September 30, | |||||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||||

| Statement of Operations: | (In thousands, except per share data) | ||||||||||||||||||||||||||||

| Revenues | $ | 470,559 | $ | 518,499 | $ | 517,180 | $ | 448,716 | $ | 395,911 | |||||||||||||||||||

| Cost of goods sold | 395,496 | 423,924 | 430,204 | 383,361 | 345,142 | ||||||||||||||||||||||||

| Gross profit | 75,063 | 94,575 | 86,976 | 65,355 | 50,769 | ||||||||||||||||||||||||

| Selling, general and administrative expenses | 67,217 | 67,662 | 69,950 | 66,768 | 61,524 | ||||||||||||||||||||||||

| Research and development expenses | 6,670 | 6,265 | 6,327 | 6,717 | 6,906 | ||||||||||||||||||||||||

| Amortization of intangible assets | 157 | 177 | 177 | 205 | 355 | ||||||||||||||||||||||||

| Insurance proceeds | — | — | (950) | — | — | ||||||||||||||||||||||||

| Restructuring and other, net | — | 1,400 | 11 | 787 | 1,322 | ||||||||||||||||||||||||

| Operating income (loss) | 1,019 | 19,071 | 11,461 | (9,122) | (19,338) | ||||||||||||||||||||||||

| Other income | — | (506) | — | (747) | (2,029) | ||||||||||||||||||||||||

| Interest (income) expense, net | (73) | (753) | (873) | (676) | (390) | ||||||||||||||||||||||||

| Income (loss) before income taxes | 1,092 | 20,330 | 12,334 | (7,699) | (16,919) | ||||||||||||||||||||||||

Income tax provision (benefit) (1) | 461 | 3,670 | 2,444 | (547) | (7,433) | ||||||||||||||||||||||||

| Net income (loss) | $ | 631 | $ | 16,660 | $ | 9,890 | $ | (7,152) | $ | (9,486) | |||||||||||||||||||

| Earnings (loss) per share: | |||||||||||||||||||||||||||||

| Basic | $ | 0.05 | $ | 1.43 | $ | 0.85 | $ | (0.62) | $ | (0.83) | |||||||||||||||||||

| Diluted | $ | 0.05 | $ | 1.42 | $ | 0.85 | $ | (0.62) | $ | (0.83) | |||||||||||||||||||

| Years ended September 30, | |||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

| Statement of Operations: | (In thousands, except per share data) | ||||||||||||||||||

| Revenues | $ | 395,911 | $ | 565,243 | $ | 661,858 | $ | 647,814 | $ | 640,867 | |||||||||

| Cost of goods sold | 345,142 | 459,038 | 553,597 | 522,340 | 502,375 | ||||||||||||||

| Gross profit | 50,769 | 106,205 | 108,261 | 125,474 | 138,492 | ||||||||||||||

| Selling, general and administrative expenses | 61,524 | 74,924 | 76,801 | 87,756 | 79,707 | ||||||||||||||

| Research and development expenses | 6,906 | 6,731 | 6,980 | 7,608 | 7,615 | ||||||||||||||

| Amortization of intangible assets | 355 | 352 | 435 | 779 | 1,659 | ||||||||||||||

| Restructuring and separation expenses | 1,322 | 8,441 | 3,397 | — | 3,927 | ||||||||||||||

| Operating income | (19,338 | ) | 15,757 | 20,648 | 29,331 | 45,584 | |||||||||||||

| Gain on settlement | — | — | — | — | (1,709 | ) | |||||||||||||

| Other income | (2,029 | ) | (2,029 | ) | (2,402 | ) | (1,522 | ) | — | ||||||||||

| Interest expense (net) | (390 | ) | (7 | ) | 59 | 165 | 167 | ||||||||||||

| Income (loss) from continuing operations before income taxes | (16,919 | ) | 17,793 | 22,991 | 30,688 | 47,126 | |||||||||||||

| Income tax provision (benefit) (1) | (7,433 | ) | 2,283 | 13,552 | 11,068 | 7,387 | |||||||||||||

| Income (loss) from continuing operations | (9,486 | ) | 15,510 | 9,439 | 19,620 | 39,739 | |||||||||||||

| Income from discontinued operations, net of tax (2) | — | — | — | 9,604 | 2,337 | ||||||||||||||

| Net income (loss) | $ | (9,486 | ) | $ | 15,510 | $ | 9,439 | $ | 29,224 | $ | 42,076 | ||||||||

| Earnings (Loss) per share: | |||||||||||||||||||

| Continuing operations | $ | (0.83 | ) | $ | 1.36 | $ | 0.80 | $ | 1.63 | $ | 3.32 | ||||||||

| Discontinued operations | — | — | — | 0.80 | 0.20 | ||||||||||||||

| Basic earnings (loss) per share | $ | (0.83 | ) | $ | 1.36 | $ | 0.80 | $ | 2.43 | $ | 3.52 | ||||||||

| Continuing operations | $ | (0.83 | ) | $ | 1.36 | $ | 0.79 | $ | 1.62 | $ | 3.32 | ||||||||

| Discontinued operations | — | — | — | 0.80 | 0.19 | ||||||||||||||

| Diluted earnings (loss) per share | $ | (0.83 | ) | $ | 1.36 | $ | 0.79 | $ | 2.42 | $ | 3.51 | ||||||||

(1) For an explanation of the effective tax rate for the last three fiscal years, see Note HI of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.

| Years ended September 30, | |||||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||||

| Balance Sheet Data: | (In thousands) | ||||||||||||||||||||||||||||

Cash, cash equivalents and short-term investments (1) | $ | 133,981 | $ | 178,921 | $ | 124,681 | $ | 49,754 | $ | 95,188 | |||||||||||||||||||

| Property, plant and equipment, net | 109,457 | 114,372 | 120,812 | 128,764 | 139,420 | ||||||||||||||||||||||||

| Total assets | 436,192 | 472,278 | 467,411 | 429,951 | 414,986 | ||||||||||||||||||||||||

| Long-term debt, including current maturities | 400 | 800 | 1,200 | 1,600 | 2,000 | ||||||||||||||||||||||||

| Total stockholders' equity | 301,223 | 306,626 | 299,153 | 301,644 | 321,296 | ||||||||||||||||||||||||

| Total liabilities and stockholders' equity | 436,192 | 472,278 | 467,411 | 429,951 | 414,986 | ||||||||||||||||||||||||

| Dividends paid on common stock | 12,142 | 12,066 | 11,998 | 11,916 | 11,875 | ||||||||||||||||||||||||

| Years ended September 30, | |||||||||||||||||||

| 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

| Balance Sheet Data: | (In thousands) | ||||||||||||||||||

| Cash, cash equivalents and short-term investments (3) | $ | 95,188 | $ | 97,720 | $ | 43,569 | $ | 103,118 | $ | 107,411 | |||||||||

| Property, plant and equipment, net | 139,420 | 144,977 | 154,594 | 156,896 | 144,495 | ||||||||||||||

| Total assets | 414,986 | 462,516 | 468,824 | 541,443 | 530,903 | ||||||||||||||

| Long-term debt, including current maturities | 2,000 | 2,400 | 2,800 | 3,200 | 3,616 | ||||||||||||||

| Total stockholders' equity | 321,296 | 335,317 | 333,262 | 371,097 | 355,226 | ||||||||||||||

| Total liabilities and stockholders' equity | 414,986 | 462,516 | 468,824 | 541,443 | 530,903 | ||||||||||||||

| Dividends paid on common stock | 11,875 | 11,845 | 12,358 | 11,998 | — | ||||||||||||||

| Years ended September 30, | |||||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||||

| Other Financial Data: | (In thousands) | ||||||||||||||||||||||||||||

| Backlog | $ | 414,918 | $ | 476,819 | $ | 419,012 | $ | 260,900 | $ | 250,123 | |||||||||||||||||||

| Bookings, net of cancellations and scope reductions | 403,860 | 576,782 | 676,051 | 458,884 | 355,064 | ||||||||||||||||||||||||

18

Item 7. Management’sDiscussionand Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations for the twelve months ended September 30, 2021 compared to the twelve months ended September 30, 2020 should be read in conjunction with the accompanying consolidated financial statements and related notes. We have elected to omit discussion on the earliest of the three years covered by the consolidated financial statements presented. Refer to Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and Liquidity and Capital Resources located in our Form 10-K for the fiscal year ended September 30, 2020, filed on December 9, 2020, for reference to discussion of the fiscal year ended September 30, 2019, the earliest of the three fiscal years presented. Any forward-looking statements made by or on our behalf are made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Readers are cautioned that such forward-looking statements involve risks and uncertainties, and the actual results may differ materially from those projected in the forward-looking statements. For a description of the risks and uncertainties, please see “Cautionary Statement Regarding Forward-Looking Statements; Risk Factors” and “Item“Part I, Item 1A. Risk Factors”Factors,” included elsewhere in this Annual Report.

Overview

We develop, design, manufacture and service custom-engineered equipment and systems for the distribution,which (1) distribute, control and monitoringmonitor the flow of electrical energy. Headquarteredenergy and (2) provide protection to motors, transformers and other electrically powered equipment. We are headquartered in Houston, Texas, weand serve the oil and gas refining,and petrochemical markets, which includes onshore and offshore oilproduction, LNG facilities and gas production,terminals, pipelines, refineries and petrochemical pipeline, terminal, miningplants. Additional markets include electric utility and metals, light rail traction power electric utility,as well as mining and metals, pulp and paper and other heavymunicipal, commercial and industrial markets. Revenues and costs are primarily related to custom engineered-to-order equipment and systems and are accounted for under percentage-of-completion accounting, which precludes us from providing detailed price and volume information. Our backlog includes various projects that typically take a number of months to produce.

The markets in which we participate are capital intensivecapital-intensive and cyclical in nature. Cyclicality is predominantly driven by customer demand, global economic conditions and anticipated environmental, safety or regulatory changes that affect the manner in which our customers proceed with capital investments. Our customers analyze various factors, including the demand and price for oil, gas and electrical energy, the overall economic and financial environment, governmental budgets, regulatory actions and environmental concerns. These factors influence the release of new capital projects by our customers, which are traditionally awarded in competitive bid situations. Scheduling of projects is matched to the customer requirements, and projects typically take a number of months to produce. Schedules may change during the course of any particular project, and our operating results can, therefore, be impacted by factors outside of our control.

Historically, the combination of a growing global economy, abundant sources of favorably priced natural gas feedstock, and an energy industry focus on transition to natural gas and cleaner-burning fuels drove an increase in capital investment opportunities, specifically across the oil, gas and petrochemical sectors. Some of these opportunities were for natural gas related projects targeting global demand for cleaner-burning fuels. Additionally, projects within the domestic petrochemical sector benefited from the low feedstock prices of natural gas. Specific to natural gas, the business was awarded a substantial contract in the second quarter of Fiscal 2020 that will support the integrated electrical distribution requirements for a large domestic industrial complex and should be substantially completed in Fiscal 2022. We began to experience reduced commercial activity in Fiscal 2020 driven in large part by the uncertainties across our industrial end markets in the U.S. resulting from the COVID-19 pandemic. Considering the long cycle nature of our business, these cyclical conditions may persist into Fiscal 2022.

19

Impact of the COVID-19 Pandemic and Oil and Gas Commodity Market Volatility on Powell