Washington, D. C. 20549

PIONEER ENERGY SERVICES CORP.

with drilling rigs that have more varied capabilities for drilling in unconventional plays and improves our efficiency and safety.safety, as described in more detail below.

collars, casing, and other necessary items to the drilling rig floor. Its function has significant safety advantages and can reduce the overall time required to complete the well.

We believe that our drilling rigs and other related equipment are in good operating condition. Our employees perform periodic maintenance and minor repair work on our drilling rigs. We rely on various oilfield service companies for major repair work and overhaul of our drilling equipment when needed. We also engage in periodic improvement and upgrades of our drilling equipment. In the event of major breakdowns or mechanical problems, our rigs could be subject to significant idle time and a resulting loss of revenue if the necessary repair services are not immediately available.

Newly drilled wells require completion services to prepare the well for production. The completion process may involve selectively perforating the well casing in the productive zones to allow oil or gas to flow into the well bore, stimulating and testing these zones and installing the production string and other downhole equipment. The completion process typically requires a few days to several weeks, depending on the nature and type of the completion, and generally requires additional auxiliary equipment. Accordingly, completion services require less well-to-well mobilization of equipment and can provide higher operating margins than regular maintenance work. The demand for completion services is directly related to drilling activity levels, which are sensitive to changes in oil and gas prices.

Regular maintenance is required throughout the life of a well to sustain optimal levels of oil and gas production. Common maintenance services include repairing inoperable pumping equipment in an oil well, replacing defective tubing in a gas well, cleaning a live well, and servicing mechanical issues. Our maintenance services involve relatively low-cost, short-duration jobs which are part of normal well operating costs. The need for maintenance does not directly depend on the level of drilling activity, although it is somewhat impacted by short-term fluctuations in oil and gas prices. Accordingly, maintenance services generally experience relatively stable demand; however, when oil or gas prices are too low to justify additional expenditures, operating companies may choose to temporarily shut in producing wells rather than incur additional maintenance costs.

In addition to periodic maintenance, producing oil and gas wells occasionally require major repairs or modifications called workovers, which are typically more complex and more time consuming than maintenance operations. Workover services include extensions of existing wells to drain new formations either through perforating the well casing to expose additional productive zones not previously produced, deepening well bores to new zones, or the drilling of lateral well bores to improve reservoir drainage patterns. Workovers also include major subsurface repairs such as repair or replacement of well casing, recovery or replacement of tubing and removal of foreign objects from the well bore. A workover may require a few days to several weeks and generally requires additional auxiliary equipment. The demand for workover services is sensitive to oil and gas producers’ intermediate and long-term expectations for oil and gas prices.

At the end of the well life cycle, a process is required to permanently close oil and gas wells that are no longer capable of producing in economic quantities. Many well operators bid this work on a “turnkey” basis, requiring the service company to perform the entire job, including the sale or disposal of equipment salvaged from the well as part of the compensation received, and complying with state regulatory requirements. Plugging and abandonment work can provide favorable operating margins and is less sensitive to oil and gas pricing than drilling and workover activity since well operators must plug a well in accordance with state regulations when it is no longer productive.

Well servicing rigs are frequently used to complete newly drilled wells to minimize the use of higher cost drilling rigs in the completion process. Our well servicing rigs are also used to convert former producing wells to injection wells through which water or carbon dioxide is then pumped into the formation for enhanced oil recovery operations. Extensive workover operations are normally performed by a well servicing rig with additional specialized auxiliary equipment, which may include rotary drilling equipment, mud pumps, mud tanks and fishing tools, depending upon the particular type of workover operation. All of our well servicing rigs are designed to perform complex workover operations. We also perform plugging and abandonment work throughout our core areasAdditionally, all of operation in conjunction with equipment provided by other service companies.

Electric wireline contains a conduit that allows signals to be transmitted to or from tools located in the well. These tools can be used to measure pressures and temperatures as well as the condition of the casing and the cement that holds the casing in place. In order for oil and gas exploration and production companies to better understand the reservoirs they are drilling or producing, they require logging services to accurately characterize reservoir rocks and fluids. We provide both openopen- and cased-hole logging services. Other applications for wireline tools include placing equipment in or retrieving equipment (or debris) from the wellbore, installing bridge plugs, perforating the casing in order to prepare the well for production, or cutting off pipe that is stuck in the well so that the free section can be recovered.

We believe that an important competitive factor in establishing and maintaining long-term client relationships is having an experienced, skilled and well-trained work force. In recent years, many of our larger clients have placed increased

emphasis on the safety performance and quality of the crews, equipment and services provided by their contractors. We have devoted, and will continue to devote, substantial resources toward employee safety and training programs. Although price is generally the primary factor, we believe our clients consider all of these factors price is generally the primary factor in determining which service provider is awarded the work. However, we believework, and that many clients are willing to pay a slight premium for the quality and safe, efficient service we provide.

The need for our services fluctuates primarily in relation to the price (or anticipated price) of oil and natural gas, which in turn is driven by the supply of and demand for oil and natural gas. The level of our revenues, earnings and cash flows are substantially dependent upon, and affected by, the level of domestic and international oil and gas exploration and development activity, as well as the equipment capacity in any particular region. For a more detailed discussion, see Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The materials and supplies we use in our drilling and production services operations include fuels to operate our equipment, drilling mud, drill pipe, drill collars, drill bits, cement and other job materials such as explosives and perforating guns and

Our operations are subject to the many hazards inherent in exploration and production activity, including the risks of:

•damage to producing or potentially productive oil and gas formations through which we drill; and

•environmental damage.

We seek to protect ourselves from some but not all operating hazards through insurance coverage. However, some risks are either not insurable or insurance is available only at rates that we consider uneconomical. Those risks include, among other things, pollution liability in excess of relatively low limits. Depending on competitive conditions and other factors, we attempt to obtain contractual protection against uninsured operating risks from our clients. However, clients who provide contractual indemnification protection may not in all cases maintain adequate insurance or otherwise have the financial resources necessary to support their indemnification obligations. Our insurance or indemnification arrangements may not adequately protect us against liability or loss from all the hazards of our operations. The occurrence of a significant event that we have not fully insured or indemnified against or the failure of a client to meet its indemnification obligations to us could materially and adversely affect our results of operations and financial condition. Furthermore, we may be unable to maintain adequate insurance in the future at rates we consider reasonable.

Our current insurance coverage includes property insurance on our rigs, drilling equipment, production services equipment, and real property. Our insurance coverage for property damage to our rigs, drilling equipment and production services equipment is based on our estimates of the cost of comparable used equipment to replace the insured property. The policy provides for a deductible of no more than $750,000$750,000 per drilling rig and a deductible on production services equipment of $100,000$250,000 per occurrence.occurrence, with an additional $350,000 annual aggregate deductible. Our third-party liability insurance coverage is $101$101 million per occurrence and in the aggregate, with a $500,000 self-insured retention, an additional $500,000 aggregate deductible, of $250,000 per occurrence and an additional $250,000 annual aggregate deductible.deductible of $1,000,000 on the first layer of excess coverage. We also carry insurance coverage for pollution liability up to $20$20 million with a deductible of $500,000.$500,000. We believe that we are adequately insured for public liability and property damage to others with respect to our operations. However, such insurance may not be sufficient to protect us against liability for all consequences of well disasters, extensive fire damage or damage to the environment.

Employees

We currently have approximately 2,300 employees, the majority of which work in our drilling and production services operations and are primarily compensated on an hourly basis. The number of employees in operations fluctuates depending on the utilization of our drilling rigs, well servicing rigs, wireline units and coiled tubing units at any particular time. None of our employment arrangements are subject to collective bargaining arrangements.

Our operations require the services of employees having the technical training and experience necessary to achieve proper operational results. As a result, our operations depend, to a considerable extent, on the continuing availability of such personnel. From time to time, shortages of qualified personnel have occurred in our industry. If we should suffer any material

loss of personnel to competitors or be unable to employ additional or replacement personnel with the requisite level of training and experience to adequately operate our equipment, our operations could be materially and adversely affected. While we believe our wage rates are competitive and our relationships with our employees are satisfactory, a significant increase in the wages paid by other employers could result in a reduction in our workforce, increases in wage rates, or both. The occurrence of either of these events for a significant period of time could have a material adverse effect on our financial condition and results of operations.

Facilities

We lease our corporate office facilities located at 1250 N.E. Loop 410, Suite 1000 San Antonio, Texas 78209. We conduct our business operations through 50 other real estate locations, of which we own 12, located throughout the United States in Texas, Oklahoma, Colorado, Montana, North Dakota, Pennsylvania, Wyoming, Mississippi, Arkansas, Louisiana and Kansas, and one property is located internationally in Colombia. These real estate locations are primarily used for regional offices and storage and maintenance yards.

Governmental Regulation

Many aspects of our operations are subject to various federal, state and local laws and governmental regulations, including laws and regulations governing:

•remediation of contamination;

•preservation of natural resources;

Environment Protection. Our operations are subject to stringent federal, state and local laws, rules and regulations governing the protection of the environment and human health and safety.

Some of the laws, rules and regulations applicable to our industry relate to the disposal of hazardous substances, oilfield waste and other waste materials and restrict the types, quantities and concentrations of those substances that can be released into the environment. Several of those laws also require removal and remedial action and other cleanup under certain circumstances, commonly regardless of fault. Our operations routinely involve the handling of significant amounts of waste materials, some of which are classified as hazardous wastes and/or hazardous substances. Planning, implementation and maintenance of protective measures are required to prevent accidental discharges. Spills of oil, natural gas liquids, drilling fluids and other substances may subject us to penalties and cleanup requirements. Handling, storage and disposal of both hazardous and non-hazardous wastes are also subject to these regulatory requirements. In addition, our operations are often conducted in or near ecologically sensitive areas, such as wetlands or protected species habitats, which are subject to special protective measures and which may expose us to additional operating costs and liabilities for accidental discharges of oil, gas, drilling fluids, contaminated water or other substances, or for noncompliance with other aspects of applicable laws and regulations.

Environmental laws and regulations are complex and subject to frequent change.change, and the new Biden Administration is expected to revise existing environmental regulations and to pursue new initiatives. Failure to comply with governmental requirements or inadequate cooperation with governmental authorities could subject a responsible party to administrative, civil or criminal action. We may also be exposed to environmental or other liabilities originating from businesses and assets which we acquired from others. Our compliance with amended, new or more stringent requirements, stricter interpretations of existing requirements or the future discovery of contamination or regulatory

noncompliance may require us to make material expenditures or subject us to liabilities that we currently do not anticipate.

There are a variety of regulatory developments, proposals or requirements and legislative initiatives that have been introduced in the United States and international regions in which we operate that are focused on restricting the emission of carbon dioxide, methane and other greenhouse gases. Further, President Biden has announced that he intends to take aggressive action to address climate-related issues and to set the United States on a path to be carbon-neutral by 2050.

Hydraulic fracturing of wells and subsurface water disposal are also under public and governmental scrutiny due to concerns regarding potential environmental and physical impacts, including groundwater and drinking water impacts, as well as whether such activities may cause earthquakes. Increased regulation and attention given to the hydraulic fracturing process could lead to greater opposition, including litigation, to oil and gas production activities using hydraulic fracturing techniques. Additional legislation or regulation could also lead to operational delays or increased operating costs in the production of oil and natural gas, including from the developing shale plays, incurred by our clients. The adoption of any federal, state or local laws or the implementation of regulations or ordinances restricting or increasing the costs of hydraulic fracturing

could cause a decrease in the completion of new oil and natural gas wells and an associated decrease in demand for our drilling and well servicing activities, any or all of which could adversely affect our financial position, results of operations and cash flows.

Our wireline operations involve the use of radioactive isotopes along with other nuclear, electrical, acoustic, and mechanical devices. Our activities involving the use of isotopes are regulated by the U.S. Nuclear Regulatory Commission and specified agencies of certain states. Additionally, we use high explosive charges for perforating casing and formations, and we use various explosive cutters to assist in wellbore cleanout. Such operations are regulated by the U.S. Department of Justice, Bureau of Alcohol, Tobacco, Firearms, and Explosives and require us to obtain licenses or other approvals for the use of densitometers as well as explosive charges. We have obtained these licenses and approvals when necessary and believe that we are in substantial compliance with these federal requirements.

In addition, our business depends on the demand for land drilling and production services from the oil and gas industry and, therefore, is affected by tax, environmental and other laws relating to the oil and gas industry generally, by changes in those laws and by changes in related administrative regulations. It is possible that these laws and regulations may in the future add significantly to our operating costs or those of our clients, or otherwise directly or indirectly affect our operations. It is possible that the Biden Administration will severely restrict oil and gas development on public lands. For example, the President has already announced a hold on new drilling permits for federal lands and waters and has proposed a moratorium on hydraulic fracturing on federal lands and waters. In addition, the new administration may restrict new oil and gas leasing on public lands.

See Item 1A—“Risk Factors” in Part I of this Annual Report on Form 10-K for a detailed discussion of risks we face concerning laws and governmental regulations.

Transportation. Among the services we provide, we operate as a motor carrier for the transportation of our own equipment and therefore are subject to regulation by the U.S. Department of Transportation and by various state agencies. These regulatory authorities exercise broad powers, governing activities such as the authorization to engage in motor carrier operations and regulatory safety. There are additional regulations specifically relating to the trucking industry, including testing and specification of equipment and product handling requirements. The trucking industry is subject to possible regulatory and legislative changes that may affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. Some of these possible changes include increasingly stringent environmental regulations, changes in the hours of service regulations which govern the amount of time a driver may drive in any specific period, onboard black box recorder devices or limits on vehicle weight and size.

Interstate motor carrier operations are subject to safety requirements prescribed by the U.S. Department of Transportation. To a large degree, intrastate motor carrier operations are subject to state safety regulations that mirror federal regulations. Such matters as weight and dimension of equipment are also subject to federal and state regulations.

From time to time, various legislative proposals are introduced, including proposals to increase federal, state, or local taxes, including taxes on motor fuels, which may increase our costs or adversely impact the recruitment of drivers. We cannot predict whether, or in what form, any increase in such taxes applicable to us will be enacted.

Worker safety. Our ability to retain existing customers and attract new business is dependent on many factors, including our ability to demonstrate that we can reliably and safely operate our business in a manner that is consistent with applicable laws, rules and permits. An accident or other event resulting in significant environmental or property damage, or injuries or fatalities involving our employees or other persons could also trigger investigations by federal, state or local authorities. Such an accident or other event could cause us to incur substantial expenses in connection with the investigation, remediation and resolution, as well as cause lasting damage to our reputation, loss of customers and an inability to obtain insurance.

Available Information

Our Websitewebsite address is www.pioneeres.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, are available free of charge through our Websitewebsite as soon as reasonably practicable after we electronically file those materials with, or furnish those materials to, the Securities and Exchange Commission. The public may read and copy these materials at the Securities and Exchange Commission’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. For additional information on the operations of the Securities and Exchange Commission’s Public Reference Room, please call 1-800-SEC-0330. In addition, the Securities and Exchange Commission maintains an Internet site at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically. We have also posted on our Websitewebsite our: Charters for the Audit, Compensation, and Nominating and Corporate Governance Committees of our Board; Code of Business Conduct and Ethics; Rules of Conduct Applicable to All Employees; Corporate Governance Guidelines; and Company Contact Information. Information on our website is not incorporated into this report or otherwise made part of this report.

| |

ITEM 1A. | RISK FACTORSITEM 1A. RISK FACTORS |

The information set forth in this Item 1A should be read in conjunction with the rest of the information included in this report, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 and the financial statements and related notes this report contains. While we attempt to identify, manage and mitigate risks and uncertainties associated with our business to the extent practical under the circumstances, some level of risk and uncertainty will always be present. Additional risks and uncertainties that are not presently known to us or that we currently believe are immaterial also may negatively impact our business, financial condition or operating results.

Set forth below are various risks and uncertainties that could adversely impact our business, financial condition, results of operations and cash flows.

Risks Relating to Our Emergence from Bankruptcy

•We recently emerged from bankruptcy, which may adversely affect our business and relationships.

As a result of our bankruptcy filing and recent emergence:

•key suppliers, vendors or other contract counterparties may terminate their relationships with us or require additional financial assurances or enhanced performance from us;

•our ability to renew existing contracts and compete for new business may be adversely affected;

•our ability to attract, motivate and/or retain key executives and employees may be adversely affected;

•our competitors may take business away from us, and our ability to attract and retain customers may be negatively impacted;

•our employees may be distracted from performance of their duties or more easily attracted to other employment opportunities; and

•we may have difficulty obtaining the capital we need to run and grow our business.

The occurrence of one or more of these events could have a material adverse effect on our operations, financial condition and reputation.

•Upon our emergence from Chapter 11, the composition of our stockholder base and concentration of equity ownership changed significantly.

As a result of the concentration of our equity ownership, the future strategy and plans of the Company may differ materially from those in the past. Upon our emergence from Chapter 11, twelve stockholder groups were the

beneficial owners of approximately 95% (the “Significant Stockholders”) of our issued and outstanding common stock and, therefore, have significant control on the outcome of matters submitted to a vote of stockholders, including, but not limited to, electing directors and approving corporate transactions. In addition, our incurrence of additional indebtedness requires the consent of each of our current stockholders that, together with their affiliates and related funds, owns more than 17.5% of our outstanding common stock on a fully-diluted basis, and the consent of one particular stockholder is required for us to issue additional equity as long as such stockholder, together with its affiliates and related funds, owns more than 12.5% of our outstanding common stock on a fully-diluted basis. As a result, our future strategy and plans may differ materially from those of the past. Circumstances may occur in which the interests of the Significant Stockholders could be in conflict with the interests of other stockholders, and the Significant Stockholders would have substantial influence to cause us to take actions that align with their interests. Should conflicts arise, we can provide no assurance that the Significant Stockholders would act in the best interests of other stockholders or that any conflicts of interest would be resolved in a manner favorable to our other stockholders.

•Upon our emergence from Chapter 11, the composition of our board of directors changed significantly.

Pursuant to the Plan, the composition of our board of directors (the “Board”) changed significantly. Upon emergence, our Board consisted of five directors, only one of whom, our former Chief Executive Officer, Wm. Stacy Locke, had served on the Board prior to our emergence from Chapter 11. In July 2020, Wm. Stacy Locke resigned his officer and director positions, at which time Matthew S. Porter, a member of the Board, was also appointed to serve as Interim Chief Executive Officer, and he was subsequently appointed to serve as the Company’s President and Chief Executive Officer, effective January 1, 2021. Our Board currently consists of four members.

The new directors have different backgrounds, experiences and perspectives from those individuals who previously served on our Board and, thus, may have different views on the issues that will determine our future. As a result, the future strategy and our plans may differ materially from those of the past.

•Certain information contained in our historical financial statements will not be comparable to the information contained in our financial statements after the application of fresh start accounting.

Upon our emergence from Chapter 11, we adopted fresh start accounting in accordance with ASC Topic 852 and became a new entity for financial reporting purposes. As a result, we revalued our assets and liabilities based on our estimate of our enterprise value and the fair value of each of our assets and liabilities. These estimates, projections and enterprise valuation were prepared solely for the purpose of the bankruptcy proceedings and should not be relied upon by investors for any other purpose. At the time they were prepared, the determination of these values reflected numerous estimates and assumptions, and the fair values recorded based on these estimates may not be fully realized in periods subsequent to our emergence from Chapter 11.

The consolidated financial statements after the Effective Date are not comparable with the consolidated financial statements on or before that date as indicated by the “black line” division in the financial statements and footnote tables, which emphasizes the lack of comparability between amounts presented. This will make it difficult for stockholders to assess our performance in relation to prior periods. Please see Note 2, Emergence from Voluntary Reorganization under Chapter 11, of the Notes to Consolidated Financial Statements included in Part II, Item 8 Financial Statements and Supplementary Data for further information.

Risks Relating to the Oil and Gas Industry

•We derive all our revenues from companies in the oil and gas exploration and production industry, a historically cyclical industry with levels of activity that are significantly affected by the levels and volatility of oil and gas prices.

As a provider of contract land drilling services and oil and gas production services, our business depends on the level of exploration and production activity in the geographic markets where we operate. The oil and gas exploration and production industry is a historically cyclical industry characterized by significant changes in the levels of exploration and development activities.

Oil and gas prices, and market expectations of potential changes in those prices, significantly affect the levels of those activities. Oil and gas prices have been volatile historically and, we believe, will continue to be so in the future. Worldwide political, economic, and military events as well as natural disasters have contributed to oil and gas price volatility historically and are likely to continue to do so in the future. Many factors beyond our control affect oil and gas prices, including:

•the worldwide supply and demand for oil and gas;

•domestic or global health concerns, including the outbreak of contagious or pandemic diseases, such as the recent coronavirus;

•the cost of exploring for, producing and delivering oil and gas;

•the discovery rate of new oil and gas reserves;

•the rate of decline of existing and new oil and gas reserves;

•available pipeline and other oil and gas transportation capacity;

•the levels of oil and gas storage;

•the ability of oil and gas exploration and production companies to raise capital;

•economic conditions in the United States and elsewhere;

•actions by the Organization of Petroleum Exporting Countries, which we refer to as OPEC;

•political instability in oil and gas producing regions;

•governmental regulations, both domestic and foreign;

•domestic and foreign tax policy;

•weather conditions in the United States and elsewhere;

•the pace adopted by foreign governments for the exploration, development and production of their national reserves, or their investments in oil and gas reserves located in other countries; and

•the price of foreign imports of oil and gas.

Additionally, the above factors can also be affected by technological advances affecting energy consumption and the supply and demand within the market for renewable energy resources.

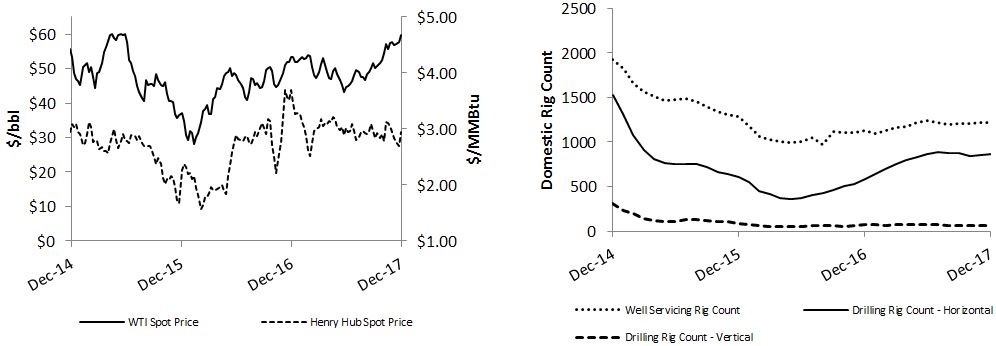

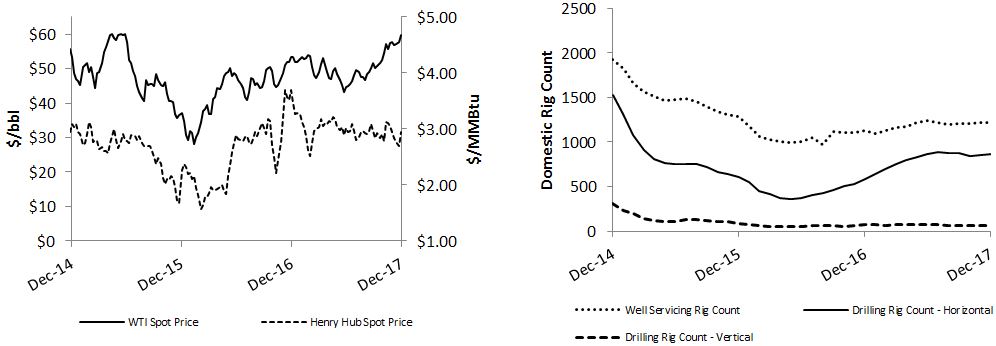

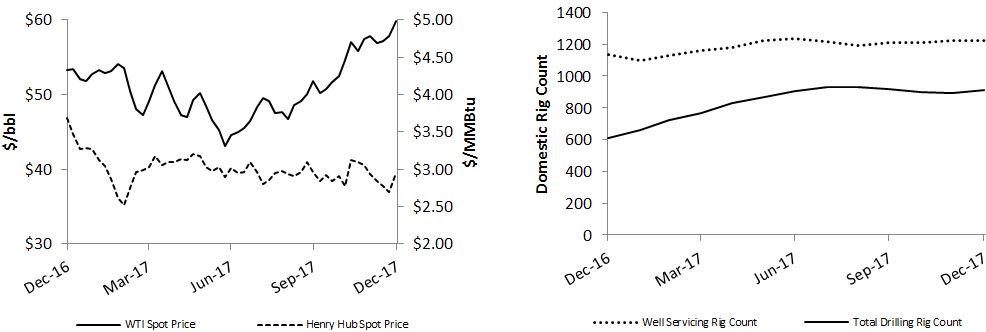

As a result of the decline in oil prices that began in late 2014, our clients reduced spending on exploration and production projects in 2015 and 2016, resulting in a significant decrease in demand for our services, which has improved during 2017.

•Oil and natural gas prices, and market expectations of potential changes in these prices, significantly impact the level of worldwide drilling and production services activities.

Reduced demand for oil and natural gas generally results in lower prices for these commodities and often impacts the economics of planned drilling projects and ongoing production projects, resulting in the curtailment, reduction, delay or postponement of such projects for an indeterminate period of time. When drilling and production activity and spending declines, both dayrates and utilization historically decline as well.

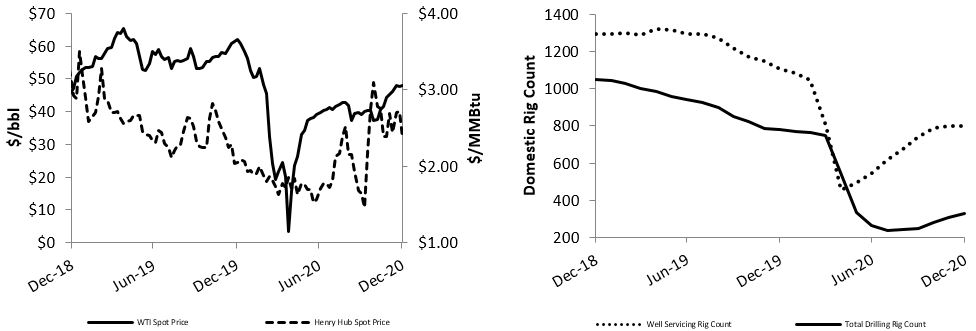

BeginningSince January 2020, the COVID-19 pandemic and oil and natural gas market volatility have resulted in October 2014,a significant decrease in oil prices worldwide dropped significantly. Our clients significantly reduced both their operating and capital expenditures during 2015significant disruption and 2016, which adversely affected our business. In 2017, our clients modestly increased their spending as compared to 2016 levels, and we expect continued increasesuncertainty in 2018. However, if the oil and natural gas market. Beginning in March 2020, the decline in demand due to the COVID-19 pandemic coincided with the announcement of price reductions and possible production increases by members of OPEC and other oil exporting nations, including Russia. Although OPEC and other oil exporting nations ultimately agreed to cut production, these extreme supply and demand dynamics caused significant crude oil price declines, negatively impacting our industry’s oil producers who responded with significant cuts in their recent and projected spending.

Additionally, because our business depends on the level of spending by our clients, we are also affected by our clients’ ability to access the capital markets. After several consecutive years without significant improvement in commodity prices, again decline, oil and gasmany exploration and production companies may cancelhave limited their spending to a level which can be supported by net operating cash flows alone, as access to the capital markets through debt or curtail their drilling programsequity financings has become more challenging in our industry. This challenge has increased recently due to the major stock market and further reduce production spending on existing wells, thereby reducing demand for our services. bond market indices experiencing elevated levels of volatility during 2020.

If the reduction in the overall level of exploration and development activities, whether resulting from changes in oil and gas prices or otherwise, continues or worsens, it could materially and adversely affect us further by negatively impacting:

•our revenues, cash flows and profitability;

•the fair market value of our drilling rig fleet and production services equipment;fleets;

•our ability to maintain or increase our borrowing capacity;obtain additional debt financing;

•our ability to obtain additional capital to finance our business or make acquisitions, and the cost of that capital;

•the collectability of our receivables; and

•our ability to retain skilled operations personnel.

Risks Relating to Our Business

•Reduced demand for or excess capacity of drilling services or production services could adversely affect our profitability.

Our profitability in the future will depend on many factors but largely on pricing and utilization rates for our drilling and production services. A reduction in the demand for drilling rigsour equipment and services or an increase in the supply of drilling rigs, whether through new constructioncomparable equipment in our industry or refurbishment, couldany particular regional market would likely decrease the dayratespricing and utilization rates for our drilling services,affected service offerings, which would adversely affect our revenues and profitability. An increaseThe commodity price environment and global oversupply of oil during 2020 resulted in supplyan oversupply of well servicing rigs, wireline unitsequipment in our industry, declining rig counts and coiled tubing units, without a corresponding increase in demand, could similarly decrease the pricingdayrates, and utilization rates ofsubstantially reduced activity for all our production services, which would adversely affect our revenues and profitability.service offerings.

•We operate in a highly competitive, fragmented industry in which price competition could reduce our profitability.

We encounter substantial competition from other drilling contractors and other oilfield service companies. Our primary market areas are highly fragmented and competitive. The fact that drilling and production services equipment are mobile and can be moved from one market to another in response to market conditions heightens the competition in the industry and may result in an oversupply of equipment in an area. Contract drilling companies and other oilfield service companies compete primarily on a regional basis, and the intensity of competition may vary significantly from region to region at any particular time. If demand for drilling or production services improves in a region where we operate, our competitors might respond by moving in suitable rigs and production services equipment from other regions. An influx of equipment from other regions could rapidly intensify competition, reduce profitability, and make any improvement in demand for our services short-lived.

Most drilling services contracts and production services contracts are awarded on the basis of competitive bids, which also results in price competition. In addition to pricing and equipment availability, we believe the following factors are also important to our clients in determining which drilling services or production services provider to select:

•the type, capability and condition of each of the competing drilling rigs, well servicing rigs, and wireline units and coiled tubing units;

•the mobility and efficiency of the equipment;

•the quality of service and experience of the crews;

•the reputation and safety record of the company providing the services;

•the offering of integrated and/or ancillary services; and

•the ability to provide drilling and production services equipment adaptable to, and personnel familiar with, new technologies and drilling and production techniques.

While we must be competitive in our pricing, our competitive strategy generally emphasizes the quality of our equipment, our safety record, our ability to offer ancillary services, the experience of our crews and the quality of service we provide to differentiate us from our competitors. This strategy is less effective when lower demand for drilling and production services intensifies price competition and makes it more difficult for us to compete on the basis of factors other than price. In all of the markets in which we compete, an oversupply of drilling rigs or production services equipment generally causes greater price competition and reduced profitability.

•We face competition from many competitors with greater resources.

Some of our competitors have greater financial, technical and other resources than we do. Their greater capabilities in these areas may enable them to:

•better withstand industry downturns;

•compete more effectively on the basis of price and technology;

•better attract and retain skilled personnel; and

•build new rigs or acquire and refurbish existing rigs and place them into service more quickly than us in periods of high drilling demand.

•Technological advancements and trends in our industry also affect the demand for certain types of equipment, and can affect the overall demand for equipment in our industry.

Technological advancements and trends inthe services our industry also affect the demand for certain types of equipment, and can affect the overall demand for equipment in our industry. For several years, prior to late 2014, higher oil prices drove industry equipment utilization and revenue rates up, particularly in oil-producing regions and certain shale regions. However, advancements in technology improved the efficiency of drilling rigs and overall demand remained steady, while the demand for certain drilling rigs decreased, particularly in vertical well markets. The decline was a result of higher demand for drilling rigs that are able to drill horizontally and the increased use of “pad drilling” which enables a series of horizontal wells to be drilled in succession by walking or skidding a drilling rig at a single pad-site location, thereby improving the productivity of exploration and production activities and minimizing mobilization costs. This trend, then coupled with the downturn, resulted in significantly reduced demand for drilling rigs that do not have the ability to walk or skid and to drill horizontal wells, and could further reduce the overall demand for all drilling rigs.

In drilling, all rig classes were severely impacted by the industry downturn. However, AC drilling rigs equipped with either a walking or skidding system are the best suited for horizontal pad drilling and we believe they are the most desirable rig design available.provides.

Although we take measures to ensure that we use advanced technologies for drilling and production services equipment, changes in technology or improvements in our competitors’ equipment could make our equipment less competitive or require significant capital investments to keep our equipment competitive, which could have an adverse effect on our financial condition and operating results.

•We derive a significant portion of our revenue from a limited number of major clients, and our business, financial condition and results of operations could be materially adversely affected if we are unable to maintain relationships with these clients, or if their demand for our services decreases.

In the past,Historically, we have derived a significant portion of our revenue from a limited number of major clients. ForWhile none of our clients individually accounted for more than 10% of our total revenues in either of the years ended December 31, 2017, 2016 and 2015,2020 or 2019, our drilling and production services provided to our top three clients accounted for approximately 20%, 26%,19% and 29%18%, respectively, of our revenue. The loss of one or more of our major clients, or their decrease in demand for our services, could have a material adverse effect on our business, financial condition and results of operations. We experienced significantly reduced demand for our services during 2015 and 2016 from all clients, including our major clients, but we experienced a modest recovery in demand during 2017. For a detail

•Certain of our three largestcontracts are subject to cancellation by our clients as a percentagewithout penalty and/or with little or no notice.

Some of our total revenuescurrent drilling contracts, and some drilling contracts that we may enter into in the future, may include terms allowing our clients to terminate the contracts without cause, with little or no prior notice and/or without penalty or early termination payments. The likelihood that a client may seek to terminate a contract is increased during periods of market weakness.

In periods of extended market weakness, our clients may not be able to honor the last three fiscal years, see Item 1—“Business”terms of existing contracts, may terminate contracts even where there may be onerous termination fees, or may seek to renegotiate contract dayrates and terms in Part Ilight of this Annual Report on Form 10-K.

Our indebtedness could restrict our operations and make us more vulnerable to adverse economicdepressed market conditions.

Our indebtedness is primarily During depressed market conditions, as a result of commodity prices, restricted credit markets, economic downturns, changes in priorities or strategy or other factors beyond our control, a client may no longer want or need a drilling rig that is currently under contract or may be able to obtain a comparable drilling rig at a lower dayrate. For these reasons, clients may seek to renegotiate the acquisitions of the well servicing and wireline services businesses which we acquired in 2008 and the coiled tubing business that we acquired in 2011, as well as organic growth investments. At December 31, 2017, our total debt consists of $300 million outstanding under our Senior Notes and $175 million outstanding under our Term Loan, with additional borrowing availability under our ABL Facility.

Our current and future indebtedness could have important consequences, including:

limiting our ability to use operating cash flow in other areasterms of our business because we must dedicate a substantial portion of these fundsexisting drilling contracts, terminate our contracts without justification, leverage their termination rights in an effort to make principal and interest payments on our indebtedness;

making us more vulnerable to a downturn in our business, our industry or the economy in general as a substantial portion of our operating cash flow could be required to make principal and interest payments on our indebtedness, making it more difficult to react to changes in our business, industry and market conditions;

limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

impairing our ability to make investments and obtain additional financing for working capital, capital expenditures, acquisitions or other general corporate purposes;

limiting our ability to obtain additional financing that may be necessary to operate or expand our business;

putting us at a competitive disadvantage to competitors that have less debt; and

increasing our vulnerability to rising interest rates.

We currently expect that cash and cash equivalents, cash generated from operations, proceeds from sales of certain non-strategic assets, and available borrowings under our ABL Facility are adequate to cover our liquidity requirements for at least the next 12 months. However, our ability to make payments on our indebtedness, and to fund planned capital expenditures, will depend on our ability to generate cash in the future. This, to a certain extent, is subject to:

conditions in the oil and gas industry;

general economic and financial conditions;

competition in the markets where we operate;

the impact of legislative and regulatory actions on how we conduct our business; and

other factors, all of which are beyond our control.

If our business does not generate sufficient cash flow from operations to service our outstanding indebtedness, we may have to undertake alternative financing plans, subject to the limitations imposed by our Term Loan, ABL Facility and Senior Notes, such as:

refinancing or restructuring our debt;

selling assets;

reducing or delaying acquisitions or capital investments, such as refurbishments of our rigs and related equipment; and/or

seeking to raise additional capital.

However, we may be unable to implement alternative financing plans, if necessary, on commercially reasonablerenegotiate contract terms, or at all, and any such alternative financing plans might be insufficient to allow us to meet our debt obligations. If we are unable to generate sufficient cash flow or are otherwise unable to obtain the funds required to make principal and interest payments on our indebtedness, or if we otherwise fail to comply withperform their obligations under our contracts.

Our clients may also seek to terminate contracts for cause, such as the various covenantsloss of or major damage to the drilling unit or other events that cause the suspension of drilling operations beyond a specified period of time. If we experience operational problems or if our equipment fails to function properly and cannot be repaired promptly, our clients will not be able to engage in our Term Loan, ABL Facility,drilling operations and Senior Notes, we could bemay have the right to terminate the contracts. If equipment is not timely delivered to a client or does not pass acceptance testing, a client may in default undercertain circumstances have the terms of such instruments. right to terminate the contract.

In the event of a default, our lenders could elect to declare allcancellation, the loans made under our Term Loan, ABL Facility, and Senior Notes to be due and payable together with accrued and unpaid interest and terminate their commitments thereunder and wepayment of a termination fee may not fully compensate us for the loss of the contract. Additionally, the early termination of a contract may result in a drilling rig or oneother equipment being idle for an extended period of time. The cancellation or morerenegotiation of a number of our subsidiaries could be forced into bankruptcy or liquidation. Any of the foregoing consequencescontracts could materially and adversely affect our business, financial condition, results of operations and prospects.

Our Term Loan, ABL Facility, and Senior Notes impose significant covenants on us that may affect our ability to successfully operate our business.

Our Term Loan contains customary restrictions that, among other things, and subject to certain exceptions, limit our ability to:

incur or permit liens on assets;

make investments and acquisitions;

consolidate or merge with another company;

engage in asset sales; and

pay dividends or make distributions.

In addition, our Term Loan requires us to maintain certain financial covenants and to satisfy certain financial conditions, which may require us to reduce our debt or take some other action in order to comply with them.revenues and profitability.

Our ABL Facility contains restrictive covenants that, among other things, and subject to certain exceptions, limit our ability to:

declare dividends and make other distributions;

issue or sell certain equity interests;

optionally prepay, redeem or repurchase certain of our subordinated indebtedness;

make loans or investments (including acquisitions);

incur additional indebtedness or modify the terms of permitted indebtedness;

grant liens;

change our business or the business of our subsidiaries;

merge, consolidate, reorganize, recapitalize, or reclassify our equity interests;

sell our assets, and

enter into certain types of transactions with affiliates.

The Indenture governing our Senior Notes, among other things, limits us and certain of our subsidiaries, subject to certain exceptions, in our ability to:

pay dividends on stock, repurchase stock, redeem subordinated indebtedness or make other restricted payments and investments;

incur, assume or guarantee additional indebtedness or issue preferred or disqualified stock;

create liens on our or their assets;

enter into sale and leaseback transactions;

borrow, pay dividends, or transfer other assets from certain of our subsidiaries;

consolidate with or merge with or into, or sell all or substantially all of our properties to any other person;

enter into transactions with affiliates; and

enter into new lines of business.

The failure to comply with any of these covenants would cause an event of default under our Term Loan, ABL Facility, or Senior Notes. An event of default, if not waived, could result in acceleration of the outstanding indebtedness, in which case the debt would become immediately due and payable. If this occurs, we may not be able to pay our debt or borrow sufficient funds to refinance it. Even if new financing is available, it may not be available on terms that are acceptable to us. These covenants could also limit our ability to obtain future financing, make needed capital expenditures, withstand a downturn in our business or the economy in general, or otherwise conduct necessary corporate activities. We also may be prevented from taking advantage of business opportunities that arise because of the limitations imposed on us by the restrictive covenants under our Term Loan, ABL Facility, and Senior Notes.

•Our operations involve operating hazards, which, if not insured or indemnified against, could adversely affect our results of operations and financial condition.

Our operations are subject to the many hazards inherent in exploration and production activity, including the risks of:

•fires and explosions;

•collapse of the borehole;

•damaged or lost drilling equipment; and

•damage or loss from natural disasters.

Any of these hazards can result in substantial liabilities or losses to us from, among other things:

•suspension of operations;

•damage to, or destruction of, our property and equipment and that of others;

•personal injury and loss of life;

•damage to producing or potentially productive oil and gas formations through which we drill; and

We seek to protect ourselves from some but not all operating hazards through insurance coverage. However, some risks are either not insurable or insurance is available only at rates that we consider uneconomical. Those risks include, among other things, pollution liability in excess of relatively low limits. Depending on competitive conditions and other factors, we attempt to obtain contractual protection against uninsured operating risks from our clients. However, clients who provide contractual indemnification protection may not in all cases maintain adequate insurance or otherwise have the financial resources necessary to support their indemnification obligations. Our insurance or indemnification arrangements may not adequately protect us against liability or loss from all the hazards of our operations. The occurrence of a significant event that we have not fully insured or indemnified against or the failure of a client to meet its indemnification obligations to us could materially and adversely affect our results of operations and financial condition. Furthermore, we may be unable to maintain adequate insurance in the future at rates we consider reasonable.

•We could be adversely affected if shortages of equipment, supplies or personnel occur.

FromWhile we are not currently experiencing a shortage of equipment or supplies, from time to time, there have been shortages of drilling and production services equipment and supplies during periods of high demand, which we believe could recur. Additionally, trade and economic sanctions or other restrictions imposed by the United States or other countries could also affect the supply of equipment and supplies which are needed in our operations. Shortages could result in increased prices for equipment or supplies that we may be unable to pass on to clients. In addition, during periods of shortages,clients and could substantially lengthen the delivery times for equipment and supplies can be substantially longer.supplies. Any significant delays in our obtaining equipment or supplies could limit our operations and jeopardize our relations with clients. In addition, shortages of equipment or suppliesclients and could delay and adversely affect our ability to obtain new contracts for our rigs, whichrigs. Any of the above could have a material adverse effect on our financial condition and results of operations.

Our strategy of constructing drilling rigs during periods of peak demand requires that we maintain an adequate supply of drilling rig components to complete our rig building program. Our suppliers may be unable to continue providing us the needed drilling rig components if their manufacturing sources are unable to fulfill their commitments.

Our operations require the services of employees having the technical training and experience necessary to achieve proper operational results. As a result, our operations depend, to a considerable extent, on the continuing availability of such personnel. ShortagesFrom time to time in the past, temporary shortages of qualified personnel have occurred in our industry. Recently, we have begun to experience the effects of a tightening labor market and the resulting increased labor costs associated with the limited availability of qualified personnel. If we should suffer any material loss of personnel to competitors or be unable to employ additional or replacement personnel with the requisite level of training and experience to adequately operate our equipment, our operations could be materially and adversely affected. A significant increase in the wages paid by other employers could result in a reduction in our workforce, increases in wage rates, or both. The occurrence of either of these events for a significant period of time could have a material adverse effect on our financial condition and results of operations.

Our acquisition strategy exposes us to various risks, including those relating to difficulties in identifying suitable acquisition opportunities and integrating businesses, assets and personnel, as well as difficulties in obtaining financing for targeted acquisitions and the potential for increased leverage or debt service requirements.

A component of our long-term business strategy is a pursuit of acquisitions of complementary assets and businesses, subject to the limitations imposed by our Term Loan, ABL Facility, and Senior Notes. This acquisition strategy in general involves numerous inherent risks, including:

unanticipated costs and assumption of liabilities and exposure to unforeseen liabilities of acquired businesses, including environmental liabilities;

difficulties in integrating the operations and assets of the acquired business and the acquired personnel;

limitations on our ability to properly assess and maintain an effective internal control environment over an acquired business in order to comply with applicable periodic reporting requirements;

potential losses of key employees and clients of the acquired businesses;

risks of entering markets in which we have limited prior experience; and

increases in our expenses and working capital requirements.

The process of integrating an acquired business may involve unforeseen costs and delays or other operational, technical and financial difficulties that may require a disproportionate amount of management attention and financial and other resources. Our failure to achieve consolidation savings, to incorporate the acquired businesses and assets into our existing operations successfully or to minimize any unforeseen operational difficulties could have a material adverse effect on our financial condition and results of operations.

In addition, we may not have sufficient capital resources to complete additional acquisitions. Historically, we have funded business acquisitions and the growth of our rig fleet through a combination of debt and equity financing. We may incur substantial additional indebtedness to finance future acquisitions and also may issue equity securities or convertible securities in connection with such acquisitions. Debt service requirements could represent a significant burden on our results of operations and financial condition and the issuance of additional equity or convertible securities could be dilutive to our existing shareholders. Furthermore, we may not be able to obtain additional financing on satisfactory terms or at all.

Even if we have access to the necessary capital, we may be unable to continue to identify additional suitable acquisition opportunities, negotiate acceptable terms or successfully acquire identified targets.

Our cash and cash equivalents and short term investments could be adversely affected if the financial institutions in which we hold our cash and cash equivalents fail.

We maintain cash balances at third-party financial institutions in excess of the Federal Deposit Insurance Corporation insurance limit. While we monitor the cash balances in the operating accounts and adjust the balances as appropriate, we may incur a loss to the extent such loss exceeds the insurance limitation, and there could be a material impact on our business, if one or more of the financial institutions with which we deposit fails or is subject to other adverse conditions in the financial or credit markets and bank regulators elect to impose losses on uninsured depositors. To date, we have experienced no loss or lack of access to our invested cash or cash equivalents. However, in the future, our invested cash and cash equivalents could be adversely affected by adverse conditions in the financial and credit markets.

•Our international operations are subject to political, economic and other uncertainties not generally encountered in our domestic operations.

Our international operations are subject to political, economic and other uncertainties not generally encountered in our U.S. operations which include, among potential others:

•risks of war, terrorism, civil unrest and kidnapping of employees;

•employee strikes, work stoppages, labor disputes and other slowdowns;

•expropriation, confiscation or nationalization of our assets;

•renegotiation or nullification of contracts;

foreign taxation, such as the tax for equality and the net-worth tax in Colombia;18

•foreign taxation;

•the inability to repatriate earnings or capital due to laws limiting the right and ability of foreign subsidiaries to pay dividends and remit earnings to affiliated companies;

•changing political conditions and changing laws and policies affecting trade and investment;

•trade and economic sanctions or other restrictions imposed by the United States or other countries;

•concentration of clients;

•regional economic downturns;

•the overlap of different tax structures;

•the burden of complying with multiple and potentially conflicting laws;

•the risks associated with the assertion of foreign sovereignty over areas in which our operations are conducted;

•the risks associated with any lack of compliance with the Foreign Corrupt Practices Act of 1977 (“FCPA”) or other anti-corruption laws;

•the risks associated with fluctuating currency values, hard currency shortages and controls of foreign currency exchange, and higher rates of inflation as compared to our domestic operations;

•difficulty in collecting international accounts receivable; and

•potentially longer payment cycles.

Additionally, we may be subject to foreign governmental regulations favoring or requiring the awarding of contracts to local contractors or requiring foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. These regulations could adversely affect our ability to compete.

We are committed to doing business in accordance with applicable anti-corruption laws and our code of conduct and ethics. We are subject, however, to the risk that our employees and agents may take action determined to be in violation of anti-corruption laws, including the FCPA or other similar laws. Any violation of the FCPA or other applicable anti-corruption laws could result in substantial fines, sanctions, civil and/or criminal penalties and curtailment of operations in certain jurisdictions and might materially adversely affect our business, results of operations or financial condition. In addition, actual or alleged violations could damage our reputation and ability to do business. Further, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of our senior management.

•Our operations are subject to various laws and governmental regulations that could restrict our future operations and increase our operating costs.

Many aspects of our operations are subject to various federal, state and local laws and governmental regulations, including laws and regulations governing:

•remediation of contamination;

•preservation of natural resources;

Environment Protection. Our operations are subject to stringent federal, state and local laws, rules and regulations governing the protection of the environment and human health and safety.

Some of the laws, rules and regulations applicable to our industry relate to the disposal of hazardous substances, oilfield waste and other waste materials and restrict the types, quantities and concentrations of those substances that can be released into the environment. Several of those laws also require removal and remedial action and other cleanup under certain circumstances, commonly regardless of fault. Our operations routinely involve the handling of significant amounts of waste materials, some of which are classified as hazardous wastes and/or hazardous substances. Planning, implementation and maintenance of protective measures are required to prevent accidental discharges. Spills of oil, natural gas liquids, drilling fluids and other substances may subject us to penalties and cleanup requirements. Handling, storage and disposal of both hazardous and non-hazardous wastes are also subject to these regulatory requirements. In addition, our operations are often conducted in or near ecologically sensitive areas, such as wetlands or protected species habitats, which are subject to special protective measures and which

may expose us to additional operating costs and liabilities for accidental discharges of oil, gas, drilling fluids, contaminated water or other substances, or for noncompliance with other aspects of applicable laws and regulations.

The federal Clean Water Act; the Oil Pollution Act; the federal Clean Air Act; the federal Resource Conservation and Recovery Act; the federal Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA); the Safe Drinking Water Act (SDWA); the federal Outer Continental Shelf Lands Act; the Occupational Safety and Health Act (OSHA); regulations implementing these federal statutes (such as the 2015“Navigable Waters of the United States rule, which may be rescinded pursuant to a proposalProtection Rule” issued in June 2017)on January 23, 2020); and their state counterparts and similar statutes are the primary statutes that impose the requirements described above and provide for civil, criminal and administrative penalties and other sanctions for violation of their requirements. The OSHA hazard communication standard, the Environmental Protection Agency (EPA) “community right-to-know” regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require us to organize and report information about the hazardous materials we use in our operations to employees, state and local government authorities and local citizens. In addition, CERCLA, also known as the “Superfund” law, and similar state statutes impose strict liability, without regard to fault or the legality of the original conduct, on certain classes of persons who are considered responsible for the release or threatened release of certain hazardous substances into the environment. These persons generally include the current owner or operator of a facility where a release has occurred, the owner or operator of a facility at the time a release occurred, and companies that disposed of or arranged for the disposal of hazardous substances found at a particular site. This liability may be joint and several. Such liability, which may be imposed for the conduct of others and for conditions others have caused, includes the cost of removal and remedial action as well as damages to natural resources. Few

defenses exist to the liability imposed by many environmental laws and regulations. It is also common for third parties to file claims for personal injury and property damage caused by substances released into the environment.

Environmental laws and regulations are complex and subject to frequent change.change, and the new Biden Administration is expected to revise existing environmental regulations and to pursue new initiatives. Failure to comply with governmental requirements or inadequate cooperation with governmental authorities could subject a responsible party to administrative, civil or criminal action. We may also be exposed to environmental or other liabilities originating from businesses and assets which we acquired from others. Our compliance with amended, new or more stringent requirements, stricter interpretations of existing requirements or the future discovery of contamination or regulatory noncompliance may require us to make material expenditures or subject us to liabilities that we currently do not anticipate.

There are a variety of regulatory developments, proposals or requirements and legislative initiatives that have been introduced in the United States and international regions in which we operate that are focused on restricting the emission of carbon dioxide, methane and other greenhouse gases. Further, President Biden has announced that he intends to take aggressive action to address climate-related issues and to set the United States on a path to be carbon-neutral by 2050. Among these developments at the international level is the United Nations Framework Convention on Climate Change, which produced the “Kyoto Protocol” (an internationally applied protocol, which has been ratified in Colombia, which is a location where we provide drilling services) in 1992. More recently, in December 2015, 195 countries adopted under the Framework Convention a resolution known as the “Paris Agreement” to reduce emissions of greenhouse gases with a goal of limiting global warming to below 2 °C (3.6 °F)2°C (36°F). The Paris Agreement does not establish enforceable emissions reduction targets, but countries may establish greenhouse gas reduction measures pursuant to the agreement. The agreement went into effect in November 2016. The United States ratified the Paris Agreement in September 2016. It2016 but withdrew in November 2020. President Biden has since notifiedsigned an order to rejoin the Paris Agreement. The new President has also announced a focus on climate-related issues and a goal of setting the United Nations of its intentStates on the path to withdraw from the Paris Agreement, but under the terms of the agreement the U.S. will remain a party until approximately August 2020. net-zero carbon emissions by 2050.

In addition, the U.S. Congress has from time to time considered legislation to reduce emissions of greenhouse gases, primarily through the development of greenhouse gas cap and trade programs. Also, more than one-third of the states already have begun implementing legal measures to reduce emissions of greenhouse gases. There have been two multi-state organizations devoted to climate action. The Regional Greenhouse Gas Initiative (RGGI) is located in the Northeastern and Mid-Atlantic United States. The Western Regional Climate Action Initiative once included multiple U.S. states and much of Canada, but allowance trading is now comprisedlimited to only California and Quebec, with a separate trading program administered for the province of California, British Columbia, Manitoba, Ontario, and Quebec.Nova Scotia.

In 2007, the United States Supreme Court, in Massachusetts, et al. v. EPA, held that carbon dioxide may be regulated as an “air pollutant” under the federal Clean Air Act. In December 2009, the EPA responded to this decision and issued a finding that the current and projected concentrations of greenhouse gases in the atmosphere threaten the public health and welfare of current and future generations, and that certain greenhouse gases from motor vehicles contribute to the atmospheric concentrations of greenhouse gases and hence to the threat of climate change.

Based on these findings, in 2010 Subsequently, the EPA adopted two setshas a number of climate change regulations, that restrict emissions of greenhouse gases under existing provisions of the federal Clean Air Act, including one that requires a reduction in emissions of greenhouse gases from motor vehicles and another that requires certain construction and operating permit reviews for greenhouse gas emissions from certain large stationary sources. In June 2014, the U.S. Supreme Court invalidated elements of the greenhouse gascontrol and permitting rule; however, the EPA can still impose certain greenhouse gas control requirements for certain large stationary sources. In addition, the EPA adopted rules requiring the monitoringsources, fuel economy standards for vehicles and reporting of greenhouse gases from certain sources, including, among others, onshore oil and natural gas production facilities.emissions standards for power plants.

In April 2012, the EPA issued regulations specifically applicableSpecific to the oil and gas industry, that require operatorsin April 2012, the EPA issued regulations to significantly reduce volatile organic compounds, or VOC, emissions from natural gas wells that are hydraulically fractured through the use of “green completions” to capture natural gas that would otherwise escape into the air. The EPA also issued regulations that establish standards for VOC emissions from several types of equipment at natural gas well sites, including storage tanks, compressors, dehydrators and pneumatic controllers.

In August 2015, the EPA finalized rules to limit carbon dioxide emissions from new and existing electric utility generating units. New units must meet specified carbon dioxide emissions limitations. The rules for existing units, known as the “Clean Power Plan,” were to require by 2030 an overall reduction in carbon dioxide emissions of 32% below the amount of carbon dioxide emitted in 2005. Although the EPA proposed repeal of the Clean Power Plan in October and December 2017, on December 28, 2017, the EPA issued an Advance Notice of Proposed Rulemaking soliciting comments on emissions reductions that might be promulgated in place of the Clean Power Plan.

In May 2016, the EPA issued a rule to reduce methane (a greenhouse gas) and VOC emissions from additional oil and gas operations. Among other requirements, the rules impose standards for hydraulically fractured oil wells and equipment leaks at oil and gas production sites and extend certain existing standards to downstream oil and gas operations. In April 2017,2020, the EPA granted reconsideration of aspects of this rule.amended the rule to relax regulatory requirements and to remove certain operations (relating to transport and storage) from rule applicability. We expect that the Biden Administration will reverse these changes. It is also possible that the new administration will impose more stringent requirements or promulgate additional rules concerning oil and gas emissions.

Although it is not possible at this time to predict whether proposed climate change initiatives will be adopted as initially written, if at all, or how legislation or new regulations that may be adopted to address greenhouse gas emissions would impact our business, any such future laws and regulations could result in increased compliance costs or additional operating restrictions. Any additional costs or operating restrictions associated with legislation or regulations regarding greenhouse gas emissions could have a material adverse effect on our operating results and cash flows. In addition, these developments could curtail the demand for fossil fuels such as oil and gas in areas of the world where our clients operate and thus adversely affect demand for our services, which may in turn adversely affect our future results of operations. Finally, we cannot predict with any certainty whether changes to temperature, storm intensity or precipitation patterns as a result of climate change will have a material impact on our operations.

In addition, our business depends on the demand for land drilling and production services from the oil and gas industry and, therefore, is affected by tax, environmental and other laws relating to the oil and gas industry generally, by changes in those laws and by changes in related administrative regulations. It is possible that these laws and regulations may in the future add significantly to our operating costs or those of our clients, or otherwise directly or indirectly affect our operations. It is possible that the Biden Administration will severely restrict oil and gas development on public lands. For example, the President has already announced a hold on new drilling permits for federal lands and waters and has proposed a moratorium on hydraulic fracturing on federal lands and waters. In addition, the new administration may restrict new oil and gas leasing on public lands.

Oil and gas development restrictions are also possible due to voter initiatives. For example, in 2018, Colorado voted on Proposition 112, which would have increased drilling location setbacks from 500 feet to 2,500 feet, severely limiting access to oil and gas minerals. Although Proposition 112 was defeated, future voter initiatives are possible in certain jurisdictions. Further, state legislators and regulators could seek to impose similar restrictions.

Our wireline operations involve the use of radioactive isotopes along with other nuclear, electrical, acoustic, and mechanical devices. Our activities involving the use of isotopes are regulated by the U.S. Nuclear Regulatory Commission and specified agencies of certain states. Additionally, we use high explosive charges for perforating casing and formations, and we use various explosive cutters to assist in wellbore cleanout. Such operations are regulated by the U.S. Department of Justice, Bureau of Alcohol, Tobacco, Firearms, and Explosives and require us to obtain licenses or other approvals for the use of densitometers as well as explosive charges. We have obtained these licenses and approvals when necessary and believe that we are in substantial compliance with these federal requirements.

Transportation. Among the services we provide, we operate as a motor carrier for the transportation of our own equipment and therefore are subject to regulation by the U.S. Department of Transportation and by various state agencies. These regulatory authorities exercise broad powers, governing activities such as the authorization to engage in motor carrier operations and regulatory safety. There are additional regulations specifically relating to the

trucking industry, including testing and specification of equipment and product handling requirements. The trucking industry is subject to possible regulatory and legislative changes that may affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. Some of these possible changes include increasingly stringent environmental regulations, changes in the hours of service regulations which govern the amount of time a driver may drive in any specific period, onboard black box recorder devices or limits on vehicle weight and size.