| Document | Part of Form 10-K | |||||||

Portions of the Proxy Statement for the Annual Meeting of Stockholders scheduled to be held in March | Part III | |||||||

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Annual Report on Form 10-K

for the Fiscal Year Ended October 31, 20192021

Table of Contents

| PART I | Page | |||||||

| Item 1. | Business | |||||||

| Item 1A. | Risk Factors | |||||||

| Item 1B. | Unresolved Staff Comments | |||||||

| Item 2. | Properties | |||||||

| Item 3. | Legal Proceedings | |||||||

| Item 4. | Mine Safety Disclosures | |||||||

| PART | ||||||||

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |||||||

| Item 6. | Selected Financial Data | |||||||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |||||||

| Item 7A. | Quantitative and Qualitative Disclosure about Market Risk | |||||||

| Item 8. | Financial Statements and Supplementary Data | |||||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||||||

| Item 9A. | Controls and Procedures | |||||||

| Item 9B. | Other Information | |||||||

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |||||||

| PART III | ||||||||

| Item 10. | Directors, Executive Officers and Corporate Governance | |||||||

| Item 11. | Executive Compensation | |||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |||||||

| Item 14. | Principal Accounting Fees and Services | |||||||

| PART IV | ||||||||

| Item 15. | Exhibits and Financial Statement Schedules | |||||||

Item 16. | Form 10-K Summary | |||||||

3

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

PART I

Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934 and the Private Securities Litigation Reform Act of 1995. These include statements relating to plans, prospects, goals, strategies, future actions, events or performance and other statements which are other than statements of historical fact, including all statements regarding the expected impact of the ongoing Coronavirus disease 2019 (COVID-19) pandemic on our business; and statements regarding acquisitions including the acquired companies' financial position, market position, product development and business strategy, expected cost synergies, expected timing and benefits of the transaction, difficulties in integrating entities or operations, as well as estimates of the Cooper Companies, Inc.our and the acquired entities' future expenses, sales and earnings per share are forward-looking. In addition, all statements regarding anticipated growth in our revenue,net sales, anticipated effects of any product recalls, anticipated market conditions, planned product launches and expected results of operations and integration of any acquisition are forward-looking. To identify these statements, look for words like “believes,” “outlook,” “probable,” “expects,” “may,” “will,” “should,” “could,” “seeks,” “intends,” “plans,” “estimates” or “anticipates” and similar words or phrases. Forward-looking statements necessarily depend on assumptions, data or methods that may be incorrect or imprecise and are subject to risks and uncertainties. Among the factors that could cause our actual results and future actions to differ materially from those described in forward-looking statements are:are those described in our Securities and Exchange Commission filings, including the “Business,” “Risk Factors” and “Management's Discussion and Analysis of Financial Condition and Results of Operations” sections in this Annual Report on Form 10-K for the fiscal year ended October 31, 2021, as such Risk Factors may be updated in quarterly filings.

4

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Summary Risk Factors

Our business faces significant risks. In addition to the summary below, you should carefully review the “Risk Factors” section of this Annual Report on Form 10-K. We may be subject to additional risks and uncertainties not presently known to us or that we currently deem immaterial. Our business, financial condition and results of operations could be materially adversely affected by any of these risks, and the trading prices of our common stock could decline by virtue of these risks. These risks should be read in global political and economic conditions,conjunction with the other information in this report. Some of the more significant risks relating to our business include:

•The effects of the ongoing COVID-19 pandemic and related uncertainty caused byeconomic disruptions and new governmental regulations on our business, results of operations, cash flow and financial condition, including but not limited to the United Kingdom’s election to withdraw from the European Union and its potential impact on among other things, the movement of goodsour sales, operations and materials in our supply chain, additional regulatory approvals and requirements, and increased tariffs and duties.chain.

•Adverse changes in the global or regional general business, political and economic conditions, including the impact of continuing uncertainty and instability of certain countries, that could adversely affect our global markets, and the potential adverse economic impact and related uncertainty caused by these items, including but not limited to, the ongoing COVID-19 pandemic, inflation, and escalating global trade barriers, including additional tariffs, by countries such as China.

•Changes in tax laws or their interpretation, and changes in statutory tax rates, and adverse outcomes in tax disputes including but not limited to, the U.S.United States (U.S.), the United Kingdom (UK) and other countries may affect our taxation of earnings recognized in foreign jurisdictions, result in unexpected tax liabilities, and/or negatively impact our effective tax rate.

•Foreign currency exchange rate and interest rate fluctuations including the risk of fluctuations in the value of foreign currencies or interest rates that would decrease our revenuesnet sales and earnings.

•Our existing and future variable rate indebtedness and associated interest expense most of which is variable and impacted by rate increases, which could adversely affect our financial health or limit our ability to borrow additional funds.

•Acquisition-related adverse effects including the failure to successfully obtainachieve the anticipated revenues,net sales, margins and earnings benefits of acquisitions, integration delays or costs and the requirement to record significant adjustments to the preliminary fair value of assets acquired and liabilities assumed within the measurement period, required regulatory approvals for an acquisition not being obtained or being delayed or subject to conditions that are not anticipated, adverse impacts of changes to accounting controls and reporting procedures, contingent liabilities or indemnification obligations, increased leverage and lack of access to available financing (including financing for the acquisition or refinancing of debt owed by us on a timely basis and on reasonable terms).

•Compliance costs and potential liability in connection with U.S. and foreign laws and health care regulations pertaining to privacy and security of third- partypersonal information, such as HIPAA and the California Consumer Privacy Act (CCPA) in the U.S. and the General Data Protection Regulation (GDPR) requirements in Europe, including but not limited to those resulting from data security breaches.

•A major disruption in the operations of our manufacturing, accounting and financial reporting, research and development, distribution facilities or raw material supply chain due to the ongoing COVID-19 pandemic, integration of acquisitions, man-made or natural disasters, cybersecurity incidents or other causes.

•A major disruption in the operations of our manufacturing, accounting and financial reporting, research and development or distribution facilities due to technological problems, including any

5

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

related to our information systems maintenance, enhancements or new system deployments, integrations or upgrades.

•Market consolidation of large customers globally through mergers or acquisitions resulting in a larger proportion or concentration of our business being derived from fewer customers.

•Disruptions in supplies of raw materials, particularly components used to manufacture our silicone hydrogel lenses.

•New U.S. and foreign government laws and regulations, and changes in existing laws, regulations and enforcement guidance, which affect areas of our operations including, but not limited to, those affecting the health care industry, including the contact lens industry specifically and the medical device or pharmaceutical industries generally, including but not limited to the EU Medical Devices Regulation (MDR), and the EU In Vitro Diagnostic Medical Devices Regulation (IVDR), and the medical device excise tax under the U.S. Affordable Care Act..

•Legal costs, insurance expenses, settlement costs and the risk of an adverse decision, prohibitive injunction or settlement related to product liability, patent infringement or other litigation.

•Limitations on sales following product introductions due to poor market acceptance.

•New competitors, product innovations or technologies, including but not limited to, technological advances by competitors, new products and patents attained by competitors, and competitors' expansion through acquisitions.

•Reduced sales, loss of customers and costs and expenses related to product recalls and warning letters.

•Failure to receive, or delays in receiving, regulatory approvals or certifications for products.

•Failure of our customers and end users to obtain adequate coverage and reimbursement from third-party payors for our products and services.

•The requirement to provide for a significant liability or to write off, or accelerate depreciation on, a significant asset, including goodwill, other intangible assets and idle manufacturing facilities and equipment.

•The success of our research and development activities and other start-up projects.

•Dilution to earnings per share from acquisitions or issuing stock.

•Impact and costs incurred from changes in accounting standards and policies.

•Environmental risks, including increasing environmental legislation and the broader impacts of climate change.

6

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Item 1. Business.

The Cooper Companies, Inc. (Cooper, we or the Company), a Delaware corporation organized in 1980, is a global medical device company publicly traded on the NYSE (NYSE: COO). Cooper operates through two business units, CooperVision and CooperSurgical.

CooperVision is a global manufacturer providing products for contact lens wearers. CooperVision develops, manufactures and markets a broad range of single-use, two-week and monthly contact lenses, featuring advanced materials and optics. CooperVision designs its products to solve vision challenges such as astigmatism, presbyopia, myopia, ocular dryness and eye fatigues; with a broad collection of spherical, toric and multifocal contact lenses. Acquisitions alsoCooperVision offers contact lenses in a variety of materials including silicone hydrogel Aquaform® technology and phosphorylcholine technology (PC) Technology™. Further, acquisitions expanded CooperVision's access to myopia management and specialty eye care markets with new products, such as orthokeratology (ortho-k) and scleral lenses. In November 2019, CooperVision received United States Food &and Drug Administration (FDA) approval for its MiSight® 1day1 day lens, which is the first and only FDA-approved product indicated to slow the progression of myopia in children with treatment initiated between the ages of 8-12 and is expected to bebecame available in the United States induring fiscal 2020. Further,In August 2021, CooperVision offers contact lenses in a variety of materials including silicone hydrogel Aquaformreceived Chinese National Medical Products Administration (NMPA) approval for its MiSight® technology and phosphorylcholine technology (PC) Technology™.1 day lens for use in China. CooperVision’s major manufacturing and distribution facilities are located in Belgium, Costa Rica, Hungary, Puerto Rico, the United Kingdom Puerto Rico, Hungary, Costa Rica, Belgium and the United States, with other smaller locations also existing in multiple locations around the world.

CooperSurgical's business competes in the general health care market with a focus on advancing the health of women, babies and families through a diversified portfolio of products and services including medical devices, fertility, diagnostics and contraception. CooperSurgical has established its market presence and distribution system by developing products and acquiring companies, products and services that complement its business model. We categorize CooperSurgical product sales based on the point of health care delivery, which includes products used in medical office and surgical procedures, primarily by Obstetricians/Gynecologists (OB/GYN); and fertility products/equipment and genetic testing services used primarily in fertility clinics and laboratories. CooperSurgical's major manufacturing and distribution facilities are located in the United States, Costa Rica, the Netherlands, the United Kingdom and the United KingdomStates, with other smaller locations also existing in multiple locations around the world.

CooperVision and CooperSurgical each operate in highly competitive environments. Both of Cooper's businesses compete predominantly on the basis of product quality and differentiation, technological benefit, price, service and reliability.

COOPERVISION

CooperVision competes in the worldwide soft contact lens market and services three primary regions: the Americas, EMEA (Europe, Middle East and Africa) and Asia Pacific. The contact lens market has two major product categories:

•Spherical lenses including lenses that correct near- and farsightedness uncomplicated by more complex visual defects.

•Toric and multifocal lenses including lenses that, in addition to correcting near- and farsightedness, address more complex visual defects such as astigmatism and presbyopia by adding optical properties of cylinder and axis, which correct for irregularities in the shape of the cornea.

7

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

In order to achieve comfortable and healthy contact lens wear, products are sold with recommended replacement schedules, often defined as modalities, with the primary modalities being single-use lenses and frequently replaced lenses, which are designed for two-week and monthly replacement.

CooperVision offers spherical, toric, multifocal and toric multifocal lens products in most modalities. We believe that in order to compete successfully in the numerous categories of the contact lens market, companies must offer differentiated products that are priced competitively and manufactured efficiently. CooperVision believes that it is the only contact lens manufacturer to use threeuses different manufacturing processes, primarily cast molding, to produce its lenses: lathing, cast molding and FIPS™, a cost-effective combination of lathing and molding.lenses. We believe this manufacturing flexibility allows CooperVision to compete in its markets by:

•Producing high, medium and low volumes of lenses made with a variety of materials for a broader range of market niches: single-use, two-week, monthly and quarterly disposable sphere, toric and multifocal lenses, and custom toric lenses for patients with a high degree of astigmatism.astigmatism, and myopia management contact lenses.

•Offering a wide range of lens parameters, leading to a higher rate of successful fitting for practitioners and better visual acuity for patients.

The market for spherical lenses is growing with the addition of new value-added products, such as spherical lenses to alleviate dry eye symptoms, reduce eye fatigue from use of digital devices and add aspherical optical properties and/or higher oxygen permeable lenses such as silicone hydrogels.hydrogels, and myopia management contact lenses.

Sales of contact lenses utilizing silicone hydrogel materials continue to grow. Silicone hydrogel materials supply a higher level of oxygen to the cornea, as measured by the transmissibility of oxygen through a given thickness of material, or “dk/t,” than traditional hydrogel lenses. We believe our ability to compete successfully with a full range of silicone hydrogel products is an important factor to achieving success in our business. Silicone hydrogel lenses represent a significant portion of CooperVision's contact lens sales and our Biofinity® brand is CooperVision's leading product line.line in terms of sales. Under the Biofinity® brand, CooperVision markets monthly silicone hydrogel spherical (including Biofinity Energys®), toric, multifocal and toric multifocal lens products.

CooperVision markets single-use silicone hydrogel lenses with a complete line of spherical, toric, extended toric and multifocal lenses under our clariti® 1day1 day brand and single-use silicone hydrogel spherical, toric and toricmultifocal lenses under our MyDay® brand. We also compete in the traditional hydrogel single-use product segment with several lenses including our Proclear® 1 day lenses. We believe the global market for single-use contact lenses will continue to grow and that our competitive silicone hydrogel and traditional hydrogel product offerings represent an opportunity for our business.

In addition to its silicone hydrogel product offerings, CooperVision competes in the contact lens market with other traditional hydrogel products.

CooperVision believes that our key accounts which include optical chains, global retailers, certain buying groups and mass merchandisers are growing faster than the overall market. We are focused on supporting the growth of all our customers by investing in selling, promotional and advertising activities. Further, we are increasing investment in our distribution and packaging capabilities to support the growth of our business and to continue providing quality service with our industry leading SKU range and customized offerings.

CooperVision believes that myopia management opens up an attractive new market for contact lenses. With MiSight, CooperVision offers the only FDA approved and first Chinese NMPA approved product to control the progression of myopia in children. CooperVision is investing to create this new market by educating eye care practitioners, patients and their families which increases awareness.

8

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

CooperVision is focused on greater worldwide market penetration of recently introduced products, and we continue to expand our presence in existing and emerging markets, including through acquisitions. In fiscal 2019,2021, CooperVision acquired Blanchard Contact Lenses,a privately held medical device company and a privately-held scleral lens company, which expands CooperVision's specialty and scleral lens portfolio.UK contact lenses manufacturer. In fiscal 2018,2020, CooperVision acquired Paragon Vision services, a leading provider of ortho-k, specialty contact lenses and oxygen permeable rigidprivately-held U.S. contact lens material,manufacturer focusing on ortho-k lenses. These acquisitions expanded CooperVision’s specialty eye care portfolio and Blueyes Ltd. (Blueyes), a long-standing distribution partner, with a leading positionits leadership in addressing the distributionincreasing severity and prevalence of contact lenses to the Optical and Pharmacy sector in Israel.myopia.

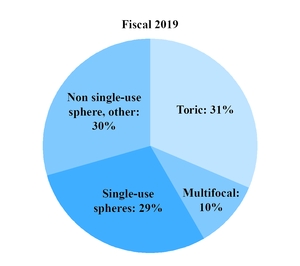

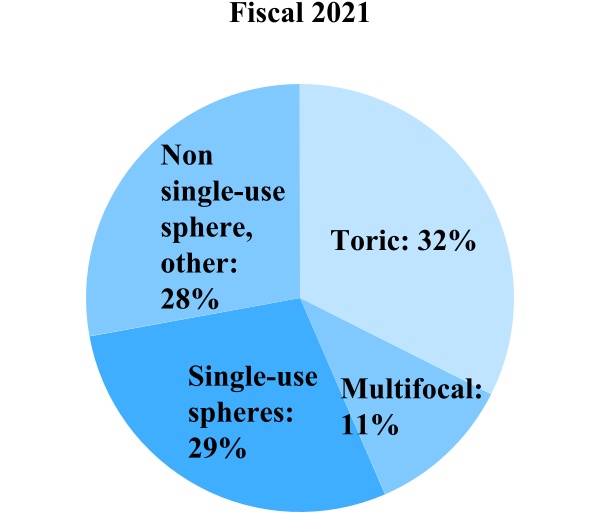

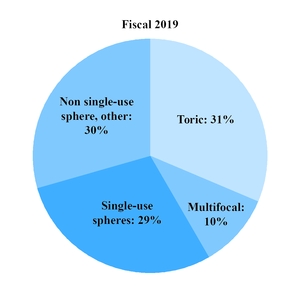

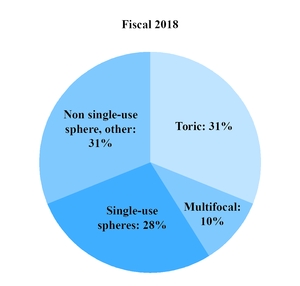

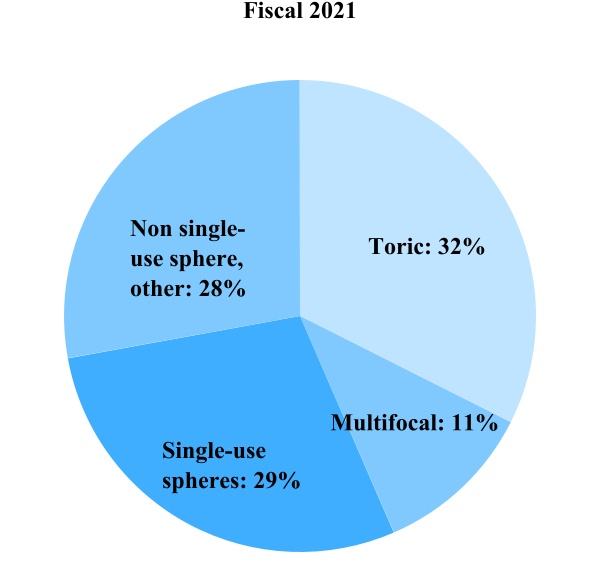

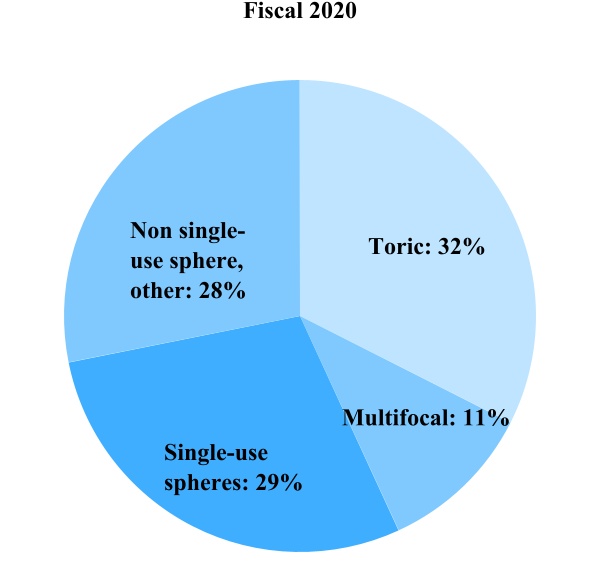

Contact Lens Product Sales

Single-use spheres – Our single-use lens portfolio includes clariti 1 day, MyDay, MiSight, Proclear 1 day and Biomedics 1 day

Toric – Toric lenses include Biofinity toric, MyDay toric, clariti 1 day toric, Biomedics toric, Proclear toric and Avaira Vitality toric

Multifocal – Multifocal lenses include Biofinity multifocal, Biofinity toric multifocal, clariti 1 day multifocal, MyDay multifocal and Proclear 1 day multifocal

Non single-use sphere, other – Our FRP (frequent replacement product) lens portfolio and other include Biofinity, Biofinity Energys, Avaira Vitality, Biomedics, Proclear, clariti, ortho-k, scleral and custom lens, solutions and other

CooperVision Competition

The contact lens market is highly competitive. CooperVision's largest competitors in the worldwide market and its primary competitors in the spherical, toric and multifocal lens categories of that market are Johnson & Johnson Vision Care, Inc., Alcon Inc. and Bausch Health Companies Inc. and Alcon Inc.

CooperVision's competitors may have greater financial resources, larger research and development budgets, larger sales forces, greater market penetration and/or larger manufacturing volumes. CooperVision seeks to offer a high level of customer service through its direct sales organizations around the world and through telephone sales and technical service representatives who consult with eye care professionals about the use of our lens products.

CooperVision also competes with manufacturers of eyeglasses and with refractive surgical procedures that correct visual defects including laser vision correction. CooperVision believes that laser vision correction is not a significant threat to its sales of contact lenses based on the growth of the contact lens market over the past decade.

9

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

CooperVision competes in the silicone hydrogel segment of the market with its following products: Biofinity monthly spherical, toric and multifocal lenses; Avaira VitalityTM two-week spherical and toric lenses; clariti 1day1 day brand of single-use sphere, toric and multifocal lenses; MyDay® single-use spherical, toric and MyDay single-usemultifocal lenses; Biofinity monthly spherical, toric, multifocal and toric multifocal lenses and Avaira Vitality® two-week spherical and toric lenses. CooperVision believes the clariti 1day1 day and MyDay brands of single-use contact lenses provide the broadest product portfolio in the single-use silicone hydrogel market. CooperVision offers both branded and private label options in contact lenses. Its private label option is frequently offered as part of a larger customized solution for its customers. It also competes in the specialty contact lens space with its FDA approved MiSight 1 day contact lens for myopia management as well as ortho-k and scleral lenses.

In addition to a broad offering of silicone hydrogel and specialty contact lenses, CooperVision competes with different manufacturing processes which allow it to produce a broad range of spheres, toric and multifocal lens parameters, which we believe provides wide choices for patient and practitioner and a high level of visual acuity. We also compete based on our customer and professional services. CooperVision believes that there are opportunities for contact lenses to gain market share, particularly in markets where the penetration of contact lenses in the vision correction market is low.

COOPERSURGICAL

CooperSurgical offers a broad array of products and services focused on advancing the health of women, babies and families through a diversified portfolio of products and services including medical devices, fertility, genomics, diagnostics and contraception. We offer quality products, innovative technologies and superior services to clinicianshealth care professionals and patients worldwide. CooperSurgical collaborates with clinicianshealth care professionals to

identify products and new technologies from disposable products to diagnostic tests to sophisticated instruments and equipment, to bring new products to market. The result is a broad portfolio of products and services that are intended to aid in the delivery of improved clinical outcomes that health care professionals use routinely in the diagnosis and treatment of a wide spectrum of family and women's health and reproductive issues.

One of CooperSurgical’s focus areas is key accounts which include large group practices, integrated delivery networks and certain buying groups within the office/surgical business and fertility clinic networks within the fertility business. We believe our portfolio of offerings and focus on service, quality and clinical education will support the accelerated growth of our business in the key account groups.

Since its inception in 1990, CooperSurgical has established its market presence and distribution system by developing products and acquiring products and companies that complement its business model.

In fiscal 2021, CooperSurgical competesacquired three privately-held medical device companies and one privately-held in the global in-vitrovitro fertilization (IVF) market withcryo-storage software solutions company. In fiscal 2020, CooperSurgical acquired a product portfolioprivately-held distributor of IVF mediamedical devices and assisted reproductive technology solutions including genetic testing designed to enhance the work of fertility professionals to the benefit of women, babies and families.

On November 6, 2021, subsequent to the fiscal year ended October 31, 2021, CooperSurgical entered into an Agreement and Plan of Merger (the “Merger Agreement”) to acquire Generate Life Sciences, a privately held leading provider of donor egg and sperm for fertility treatments, fertility cryopreservation services and newborn stem cell (cord blood and cord tissue) storage. The aggregate consideration is $1.605 billion in cash, subject to adjustment as set forth in the Merger Agreement. The transaction is anticipated to close in the first quarter of fiscal 2022 and is subject to customary closing conditions, including regulatory approval. See Note 15. Subsequent Events of the Consolidated Financial Statements for more details.

10

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Market for Women's and Family Reproductive Health Care

CooperSurgical participates in the market for family health care with its diversified product lines in three major categories based on the point of health care delivery: hospitals and surgical centers, OB/GYN medical offices and fertility clinics.

CooperSurgical expects patient visits to OB/GYNWomen’s Health provider offices in the United States to increase over the next decade. Office visit activity relatedFrom adolescent care to menopause, abnormal bleeding, incontinencegeriatrics, there is increased awareness of women’s health issues. During the reproductive years, fertility awareness and osteoporosis,family planning are expectedkey areas of focus. The attention in maternity care to improving access to safe, effective, and equitable obstetrical care continues. As we expect an increase slightly overin the next decade. Driving the growth is a growing population of women over the age of 65, (according to the United States Census estimates), a largeoffice visits focused around abnormal bleeding, incontinence and stable middle-aged population, and a steady number of reproductive age women with increasing fertility issues as well as women interested in contraception that is reversible such as with the PARAGARD® IUS. CooperSurgical expects growth in fertility treatments as more women choose to delay childbearing to the mid-thirties and beyond.menopause will likely increase.

Another trend in the market for women's health care includes the continued migration of OB/GYN clinicianshealth care professionals away from private practice ownership and toward aligning with group practices or employment with hospitals and health care systems. This overall trend of consolidation of healthcare systems includes the increasing influence of supply chain controls, such as value analysis committees, on product evaluation and procurement.procurement across these care-delivery systems. CooperSurgical believes that the market factors that are driving this trend will continue in the near term. We believe our broad product portfolio can be a benefit in this changing environment as health systems look to standardize and consolidate vendors.

Recent trends of patient-centered, value-based care in the United States market include the development of more cost-effective health care delivery models, including moving treatment out of hospitals and surgery centers and into the office setting without compromising care. We expect this trend to continue.see continued changes in reimbursement and clinical best practices as payment models and policies continue to evolve.

Some significant features of thisthe OB/GYN market are:

•Evaluation and management (E/M) office visits: assessment of menstrual disorders, vaginitis (inflammation of vaginal tissue), treatment ofpelvic infections, urinary incontinence, abnormal Pap smears, osteoporosis (reduction in bone mass) and the management of menopause,fertility concerns, pregnancy and reproductive management.

•Office-based procedures are increasing given high patient satisfaction, reduction of health system cost and comparative clinical outcomes.

•Hysterectomy and cesarean section remain common hospital surgical interventions in women worldwide.

•Initial evaluation and treatments for contraceptive management.

CooperSurgical expects growth in fertility treatments as:

•Infertility rates are common treatments in these cases.

•The number of fertility clinics is rising worldwide.

•The fertility market is fueled by dynamics such as increasing maternal age, single parents by choice, and LGBTQ+ identifying individuals starting families.

11

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

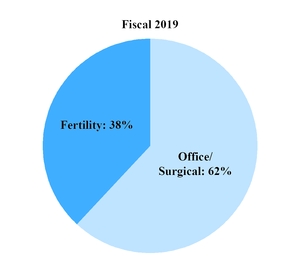

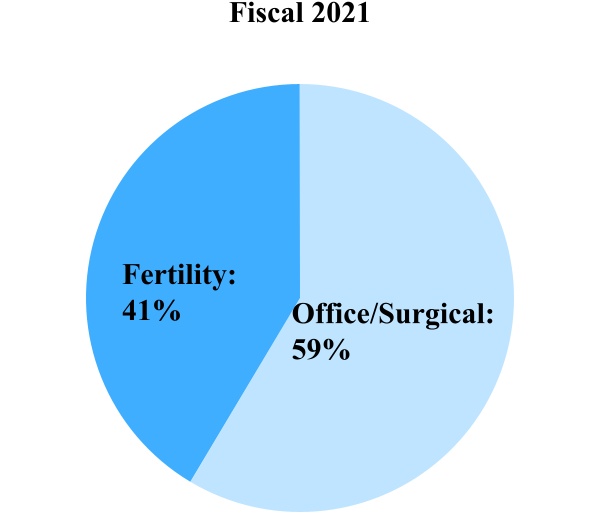

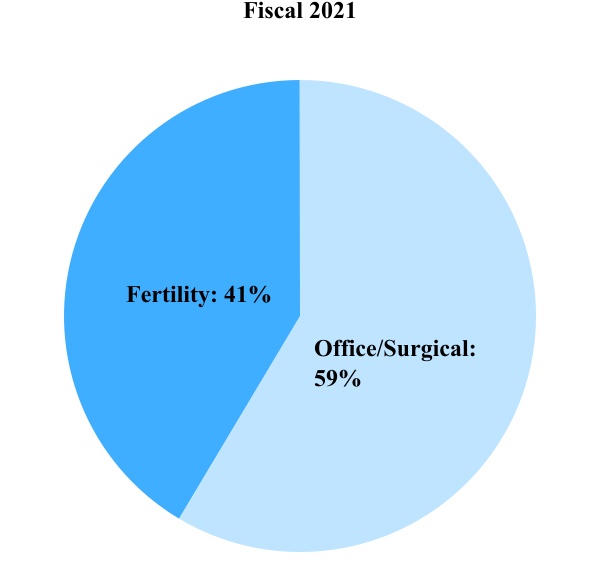

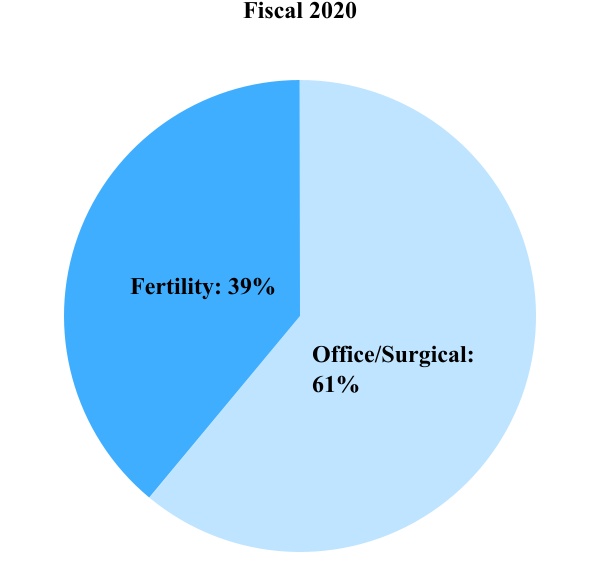

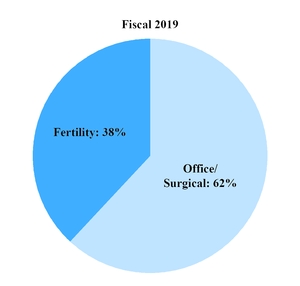

Women's and Family Reproductive Health Care Product Sales

Office/Surgical – Our significant office and surgical products include PARAGARD, Uterine Manipulators, Retractors, Closure products, Point-of-Care products, LEEP products, Endosee, Illuminate and Fetal Pillow

Fertility – Our significant fertility products and services include fertility consumables, fertility equipment, Embryo Options and preimplantation genetic testing

CooperSurgical Competition

CooperSurgical focuses on selected segments of the family and women's health care market supplying diagnosticwith a diversified portfolio of products and services including medical devices in outpatient and surgical instrumentsoperating room settings, fertility and accessories.contraception. In some instances, CooperSurgical offers all the items needed for a complete procedure. CooperSurgical believes that opportunities exist for continued market consolidation of smaller technology-driven firms that generally offer only one or two product lines. Most are privately owned or divisions of public companies including some owned by companies with greater financial resources than Cooper.consolidation.

Competitive factors in these segments in which CooperSurgical competes include technological and scientific advances, product quality and availability, price, customer service including response time and effective communication of product information to physicians, fertility clinics and hospitals. CooperSurgical competes based on our sales and marketing expertise and the technological advantages of our products. Competition in the medical device industry is dynamic and involves the search for technological and therapeutic innovations. CooperSurgical's strategy includes developing and acquiring new products, including those used in new medical procedures. As CooperSurgical expands its product line, we also offer educational programs for medical professionals in the appropriate use of our products.solutions.

CooperSurgical continues to expand its presence in the significantly larger hospital and outpatient surgical procedure segment of the market that is at present dominated by bigger competitors such as Johnson & Johnson, Boston Scientific, Hologic Olympus and Medtronic. These competitors have well-established positions within the operating room environment. CooperSurgical leverages its relationship with gynecologic surgeons and focus on devices specific to gynecologic surgery to facilitate our expansion within the surgical segment of the market.

CooperSurgical also competes in the fertility category of the women's and family health care market. We have broad product offerings for fertility evaluations and IVF procedures by OB/GYN, reproductive endocrinologists and embryologists. These include products for use by the OB/GYN in their offices for initial evaluations with office-based hysteroscopy and first line treatments such as intrauterine insemination. In fertility clinics, our products include media, micro toolsmicro-tools and lab equipment;equipment. Additionally, services offered to clinics and to improve IVF outcomes we offerfamilies undergoing assisted reproductive technologies include embryo screening testing, services intended to increase implantation ratesgenetic counseling and decrease miscarriages.

management of storage options. CooperSurgical leverages its relationshipcompetes with fertility clinics to expand its presencea large number of competitors in the fertility market against competitors in the mediaincluding Vitrolife, FujiFilm-Irvine Scientific, Cook, Hamilton Thorne, Natera and microtools categories that include Vitrolife, Cook and Irvine Scientific and competitors in fertility and familial reproductive genetic testing that include Natera, Invitae and Igenomix.

12

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

CooperSurgical competes in the IUSIntrauterine Device (IUD) contraceptive market. PARAGARD is the only FDA approved non-hormonal IUSIUD option in the United States and has a 10-year use indication. In the United States, where all IUSsIUDs within the Long-Acting Reversible Contraceptive (LARC) space are regulated as pharmaceuticals,drug products, we compete with manufacturers of hormonal IUSsIUDs including Bayer and Allergan.AbbVie Allergan and manufacturers of other forms of birth control. Outside of the United States, non-hormonal IUSsIUDs are more typically regulated as devices and are sold by a number of manufacturers. Currently, PARAGARD is not sold outside of the United States.

RESEARCH AND DEVELOPMENT

The Company employs approximately 222300 people in research and development. CooperVision's product development and clinical research is supported by internal and external specialists in lens design, formulation science, polymer chemistry, engineering, clinical trials, microbiology and biochemistry. CooperVision's research and development activities primarily include programs to develop new contact lens designs and manufacturing technology, along with improving formulations and existing products.

CooperSurgical conducts research and development in-house and has consulting agreements with external specialists.specialists in software, hardware and electrical engineering, genetic science and embryology. CooperSurgical's research and development activities include the design and improvement of surgical procedure devices, the advancement and expansion of CooperSurgical's portfolio of assisted reproductive technology (ART) products, genetic screening and testing, as well as products within the general OB/GYN offerings.

GOVERNMENT REGULATION

Medical Device and Pharmaceutical Regulation in the United States

Most of our products are medical devices subject to extensive regulation by the FDA in the United States and other regulatory bodies abroad. The Federal Food, Drug, and Cosmetic Act (FDCA) and FDA regulations govern, among other things, medical device design and development, testing, manufacturing, labeling, storage, record keeping, premarket clearance or approval, advertising and promotion, and sales and distribution. Unless an exemption applies, each medical device we wish to distribute commercially in the United States will require either prior noticepremarket notification to the FDA requesting clearance for commercial distribution under Section 510(k) of the FDCA, or premarket approval (PMA) from the FDA. A majority of the medical devices we currently market have received FDA clearance through the 510(k) process or approval through the PMA process. Because we cannot be assured that any new products we develop, or any product enhancements, will be exempt from the premarket clearance or approval requirements or will be subject to the shorter 510(k) clearance process rather than the PMA process, significant delays in the introduction of any new products or product enhancements may occur.

Device Classification

The FDA classifies medical devices into one of three classes - classes—Class I, II or III - III—depending on the degree of risk associated with each medical device and the extent of control needed to ensure its safety and effectiveness. Both CooperVision and CooperSurgical develop and market medical devices undersubject to different levels of FDA regulation depending on the classification of the device. Class III devices, such as flexible and extended wear contact lenses, require extensive premarket testing and approval, while Class I and II devices require lower levels of regulation. The majority of CooperSurgical's products are Class II devices.

Class I devices are devices with the lowest risk and are those for which safety and effectiveness can be assured by adherence to the FDA's general regulatory controls for medical devices, which include compliance with the applicable portions of the FDA's Quality System Regulation (QSR), facility

13

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

registration and product listing, reporting of adverse medical events, and appropriate, truthful and non-misleading labeling, advertising, and promotional materials (General Controls). Some Class I devices also require premarket clearance by the FDA through the 510(k) premarket notification process described below.

Class II devices are moderate risk devices, which are subject to the FDA's General Controls, and any other special controls as deemed necessary by the FDA to ensure the safety and effectiveness of the device, such as performance standards, post-market surveillance, FDA guidelines or particularized labeling requirements. Premarket review and clearance by the FDA for Class II devices is accomplished through the 510(k) premarket notification procedure. Pursuant to the Medical Device User Fee and ModernizationAmendments to the FDA Reauthorization Act of 2002 (MDUFMA)(MDUFA IV), unless a specific exemption applies, 510(k) premarket notification submissions are subject torequire payment of user fees. Certain Class II devices are exempt from this premarket review process.

Class III devices are those devices deemed by the FDA to pose the greatest risk, such as life-sustaining, life-supporting or certain implantable devices, or which have a new intended use, or use advanced technology that is not substantially equivalent to that of a legally marketed device. The safety and effectiveness of Class III devices cannot be assured solely by the General Controls and other special controls such as those listed above. These devices almost always require formal clinical studies to demonstrate safety and effectiveness and must be approved through the PMA process described below. PMA applications (and supplemental PMA applications) are subject to significantlysubstantially higher user fees under MDUFMAMDUFA IV than are 510(k) premarket notifications.

510(k) Clearance Pathway

When we are required to obtain a 510(k) clearance for a Class I or Class II device that we wish to market, we must submit a premarket notification to the FDA demonstrating that the device is substantially equivalent to a previously cleared 510(k)legally marketed predicate device. A predicate device oris a legally marketed device that is not subject to a PMA, a device that was legally marketed in commercial distribution in the United States before May 28, 1976 (a pre-amendments device) and, for which the FDA has not yet called for the submission of a PMA, applications.a device that has been reclassified from Class III to Class II or I, or a device that was found substantially equivalent through the 510(k) premarket notification process. The FDA aims to respond tomake substantial equivalence determinations following receipt of a 510(k) premarket notification within 90 days of submission of the notification, but as a practical matter, clearance can take significantly longer. Although many 510(k) pre-market notifications are cleared without clinical data, in some cases, the FDA requires additional information to support substantial equivalence. If the FDA agrees that the device is substantially equivalent to a predicate device, currently on the market, it will grant 510(k) clearance to commercially market the device. If the FDA determines that the device is not substantially equivalent to a previously clearedlegally marketed predicate, the device theis automatically designated as a Class III device. The device sponsor must fulfill more rigorous PMA requirements, or can request a risk-based classification determination for the device in accordance with the de novo process.process, which is a route to market for novel medical devices that are low to moderate risk and are not substantially equivalent to a predicate device.

After a device receives 510(k) clearance, any modification that could significantly affect its safety or effectiveness, or that changeswould constitute a major change or modification in its intended use, will require a new 510(k) clearance or, could require premarket approval.depending on the modification, PMA approval or de novo classification. The FDA requires each manufacturer to make this determination initially, but the FDA can review any such decision and can disagree with a manufacturer's determination. If the FDA disagrees with a manufacturer's determination that a new clearance or approval is not required for a particular modification, the FDA may require the manufacturer to cease marketing and/or recall the modified device until 510(k) clearance or until premarket approval is obtained.obtained or a de novo classification request is granted. In these circumstances, a manufacturer also may be subject to significant regulatory fines or

14

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

penalties. We have made and plan to continue to make additional product enhancements and modifications to our devices that we believe do not require new 510(k) clearances.

Over the last several years, the FDA has proposed reforms to its 510(k) clearance process, and such proposals could include increased requirements for clinical data and a longer review period, or could make it more difficult for manufacturers to utilize the 510(k) clearance process for their products. For example, in November 2018, FDA officials announced forthcoming steps that the FDA intends to take to modernize the premarket notification pathway under Section 510(k) of the FDCA. Among other things, the FDA announced that it planned to develop proposals to drive manufacturers utilizing the 510(k) pathway toward the use of newer predicates. These proposals included plans to potentially sunset certain older devices that were used as predicates under the 510(k) clearance pathway, and to potentially publish a list of devices that have been cleared on the basis of demonstrated substantial equivalence to predicate devices that are more than 10 years old. These proposals have not yet been finalized or adopted, and the FDA may work with Congress to implement such proposals through legislation.

In September 2019, the FDA published updated guidance describing an optional “safety and performance based” premarket review pathway for manufacturers of “certain, well-understood device types” to demonstrate substantial equivalence under the 510(k) clearance pathway by showing that such device meets objective safety and performance criteria established by the FDA, thereby obviating the need for manufacturers to compare the safety and performance of their medical devices to specific predicate devices in the clearance process. The FDA intends to develop and maintain a list of device types appropriate for the “safety and performance based” pathway and will continue to develop product-specific guidance documents that identify the performance criteria for each such device type, as well as the testing methods recommended in the guidance documents, where feasible.

Premarket Approval Pathway

A PMA application must be submitted if the device cannot be cleared through the 510(k) premarket notification procedures or if the device has been previously classified as Class III.III (unless otherwise 510(k) exempt). The PMA process is much more demanding than the 510(k) premarket notification process. A PMA application must be supported by extensive data including, but not limited to, technical, non-clinical, clinical trials, manufacturing and labeling to demonstrate to the FDA's satisfaction the safety and effectiveness of the device for its intended use.

Following receipt of a PMA application, the FDA conducts an administrative review to determine whether the application is sufficiently complete to permit a substantive review. If it is not, the agency will refuse to file the PMA. If it is, the FDA will accept the application for filing and begin the review. The FDA, by statute and regulation, has 180 days to review an accepted PMA application, although the review generally occurs over a significantly longer period of time, and can take up to several years. During this review period, the FDA may request additional information, including clinical data, non-clinical data or clarification of information already provided, and the FDA may issue a major deficiency letter to the applicant, requesting the applicant's response to deficiencies communicated by the FDA. The FDA considers a PMA or PMA supplement to have been voluntarily withdrawn if an applicant fails to respond to an FDA request for information (e.g., major deficiency letter) within 180 days after the FDA issues such request. Also, during the review period, an advisory panel of experts from outside the FDA may be convened to review and evaluate the application and provide recommendations to the FDA as to the approvability of the device. In addition, the FDA will conduct a preapproval inspection of the manufacturing facility to ensure compliance with the QSR, which, among other things requires manufacturers to implement and follow elaborate design, testing, control, documentation and other quality assurance procedures in the device design and manufacturing process.

The FDA will approve the new device for commercial distribution if it determines that the data and information in the PMA constitute valid scientific evidence and that there is reasonable assurance that the device is safe and effective for its intended use(s). The FDA may approve a PMA application with post-approvalpost-

15

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

approval conditions intended to ensure the safety and effectiveness of the device including, among other things, restrictions on labeling, promotion, sale and distribution and collection of long-term follow-up data from patients in the clinical study that supported approval. The FDA may also condition approval of a PMA application on some form of post-market surveillance when deemed necessary to protect the public health or to provide additional safety and efficacy data for the device in a larger population or for a longer period of use. In such cases, the manufacturer might be required to follow certain patient groups for a number of years and to make periodic reports to the FDA on the clinical status of those patients. Failure to comply with the conditions of approval can result in materially adverse enforcement action, including the loss or withdrawal of the approval. New PMA applications amendments to a PMA application or PMA application supplements are required for significant modifications to the manufacturing process, labeling and design of a device that is approved through the PMA process. PMA supplements often require submission of the same type of information as a PMA application, except that the supplement is limited to information needed to support any changes from the device covered by the original PMA application, and may not require as extensive clinical data or the convening of an advisory panel.

Clinical Trials for Medical Devices

A clinical trial is almost always required to support a PMA application and is rarelysometimes required forto obtain clearance of a 510(k) premarket notification. These trials generallymay require submission of an application for an investigational device exemption (IDE) to the FDA. Some typesFDA depending on the device. If the device under evaluation does not present a significant risk to human health, then the device sponsor is not required to submit an IDE application to the FDA before initiating human clinical trials, but must still comply with abbreviated IDE requirements when conducting such trials. A significant risk device is one that presents a potential for serious risk to the health, safety or welfare of studies deemeda patient and either is implanted, used in supporting or sustaining human life, substantially important in diagnosing, curing, mitigating or treating disease or otherwise preventing impairment of human health, or otherwise presents a potential for serious risk to present "non-significant risk" are deemed to have an approved IDE once certain requirements are addressed and Institutional Review Board approval is obtained.a subject. If the device presents a "significant risk"“significant risk” to human health, as defined by the FDA, the sponsor must submit an IDE application to the FDA and obtain IDE approval prior to commencing the human clinical trials. The IDE application, which includes a clinical study protocol, must be supported by appropriate data, such as animal and laboratory testing results, showing that the potential benefits of testing the device in humans and the importance of the knowledge to be gained outweighs the risks toto human subjects from the proposed investigation that the testing protocol is scientifically sound and there is reason to believe that the device as proposed for use will be effective. The IDE applicationwill automatically become effective 30 days after receipt by the FDA unless the FDA notifies the company that the investigation may not begin. If the FDA determines that there are deficiencies or other concerns with an IDE for which it requires modification, the FDA may permit a clinical trial to proceed under a conditional approval. Regardless of the degree of risk presented by the medical device, clinical studies must be approved in advance by, and conducted under the FDAoversight of, an Institutional Review Board (IRB) for a specified numbereach clinical site. The IRB is responsible for the initial and continuing review of patients, unless the product is deemed a non-significant risk devicestudy, and eligiblemay pose additional requirements for more abbreviated investigational device exemption requirements. Clinical trials for a significant risk device may begin once the IDE application is approved by bothconduct of the FDA and the appropriate institutional review boards at the clinical trial sites.study. There can be no assurance that submission of an IDE will result in the ability to commence clinical trials. Additionally, after a trial begins, the FDA may place it on hold or terminate it if, among other reasons, it concludes that the clinical subjects are exposed to unacceptable health risks that outweigh the benefits of participation in the study. During a study, we are required to comply with the FDA's IDE requirements for investigator selection, trial monitoring, reporting, record keeping and prohibitions on the promotion of investigational devices or making safety or efficacy claims for them. We are also responsible for the appropriate labeling and distribution of investigational devices. All of Cooper's currently marketed products have been cleared by all appropriate regulatory agencies, and Cooper has no product currently being marketed under an IDE.

Continuing FDA and Other Government Agency Regulation of Medical Devices

After a device is placed on the market, numerous regulatory requirements apply. These include: establishment registration and device listing with the FDA; the QSR, which requires manufacturers to follow design, testing, production, control, complaint handling, documentation and other quality assurance procedures during the manufacturing process; labeling regulations, which prohibit the

16

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

promotion of products for uncleared or unapproved or “off-label” uses and impose other restrictions on labeling, advertising and promotion; new FDA unique device identifier regulations, which require changes to labeling and packaging; and medical device reporting regulations, which require that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if it were to recur. The FDA has broad post-market and regulatory enforcement powers. We are subject to unannounced inspections for cause by the FDA to determine our compliance with the QSR and other regulations.

Failure to comply with applicable regulatory requirements, which are subject to new legislation and change, can result in enforcement action by the FDA, or other federal and state government agencies which may include, but may not be limited to, any of the following sanctions or consequences: warning letters or untitled letters; fines, injunctions and civil penalties; recall, seizure or import holds of our products; operating restrictions, suspension or shutdown of production; refusing to issue certificates to foreign governments needed to export products for sale in other countries; refusing our request for 510(k) clearance or premarket approval of new or modified products; withdrawing 510(k) clearance or premarket approvals that are already granted; and criminal prosecution.

Laboratory Developed Tests

Even under its current enforcement discretion policy, the FDA has issued warning letters to IVD manufacturers for clinical use and designed, manufactured and used within a single laboratory. We believe our geneticcommercializing laboratory tests fall withinthat were purported to be LDTs but that the FDA alleged failed to meet the definition of an LDT. As a result, we believe our tests areLDT or otherwise were not currently subject to the FDA’s policy on enforcement discretion because they presented a potential safety risk. Additionally, the FDA could change its policy of enforcement discretion for LDTs, even without legislation. For example, in recent years, the FDA has stated its intention to modify its enforcement discretion policy with respect to LDTs. Specifically, on July 31, 2014, the FDA notified Congress of its intent to modify, in a risk-based manner, its policy of enforcement discretion with respect to LDTs. On October 3, 2014, the FDA issued two draft guidance documents entitled “Framework for Regulatory Oversight of Laboratory Developed Tests (LDTs),” or the Framework Guidance, and “FDA Notification and Medical Device Reporting for LDTs,” or the Reporting Guidance. The Framework Guidance stated that FDA intended to modify its policy of enforcement discretion with respect to LDTs in a risk-based manner consistent with the classification of medical devicedevices generally in Classes I through III. The Reporting Guidance would have further enabled the FDA to collect information regarding the LDTs currently being offered for clinical use through a notification process, as well as to enforce its regulations for reporting safety issues and collecting information on any known or suspected adverse events related to the use of an LDT. The FDA halted finalization of this guidance in November 2016 to allow for further public discussion on an appropriate oversight approach for LDTs and to give congressional authorizing committees the opportunity to develop a legislative solution. In January 2017, the FDA issued a discussion paper on possible approaches to LDT regulation.

Legislative and administrative proposals proposing to amend the FDA’s oversight of LDTs have been introduced in recent years and we expect that new legislative and administrative proposals will continue to be introduced from time to time. For example, key congressional committees with jurisdiction over FDA matters have indicated an interest in continuing negotiations on potential legislation regarding

17

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

LDTs. In March 2020, the VALID Act was introduced in the House and an identical version of the bill was introduced in the U.S. Senate. If passed in its current form, the VALID Act would create a new category of medical products separate from medical devices called “in vitro clinical tests,” or IVCTs. As proposed, the bill would establish a risk-based approach to imposing requirements related to premarket review, quality systems, and labeling requirements on all IVCTs, including LDTs, but would create exemptions for certain LDTs marketed before the effective date of the bill (though other regulatory requirements may apply, such as registration and adverse event reporting). In June 2021, a revised version of the VALID Act was reintroduced in both the House and the applicable FDCA provisions. However,Senate. It is unclear whether the IVDR will regulateVALID Act or any other legislative proposals (including any proposals to reduce FDA oversight of LDTs) would be passed by Congress or signed into law by the testing of human embryos which will be classified as Class C. In addition, even though we commercialize our tests as LDT, our tests may inPresident. Depending on the futureapproach adopted under any potential legislation, certain LDTs could become subject to more onerous regulation bysome form of premarket review, potentially with a transition period for compliance and a grandfathering provision. Moreover, in August 2020, the FDA.U.S. Department of Health and Human Services issued a rescission order stating that the FDA will not require premarket review of LDTs absent changes in policy implemented through formal notice-and-comment rulemaking procedures. The degree to which this rescission order will affect FDA’s enforcement discretion policy or its oversight over LDTs remains unclear.

If Congress does not take action in connection with the VALID Act or other LDT legislation, it is possible that the FDA could change its regulatory policy governing LDTs in a way that could require that our currently marketed genetic tests, and any future products that we anticipate marketing as LDTs, comply with certain additional FDA requirements.

As we operate a genetic testing laboratory, we are required to hold certain federal, state and local licenses, certifications and permits to conduct our business. Under the Clinical Laboratory Improvement Amendments of 1988, or CLIA, we are required to hold a certificate applicable to the type of laboratory tests we perform and to comply with standards applicable to our operations, including test processes, personnel, facilities administration, equipment maintenance, recordkeeping, quality systems and proficiency testing. We have current certification under CLIA to perform testing at our New Jersey facility. To renew our CLIA certificate, we are subject to survey and inspection every two years to assess compliance with program standards. The regulatory and compliance standards applicable to the testing we perform may change over time, and any such changes could have a material effect on our business. Penalties for non-compliance with CLIA requirements include suspension, limitation or revocation of the laboratory’s CLIA certificate, as well as a directed plan of correction, state on-site monitoring, civil money penalties, civil injunctive suit or criminal penalties.

In addition to federal certification requirements of laboratories under CLIA, licensure is required and maintained for our laboratory under state law. Such laws establish standards for the day-to-day operation of a clinical reference laboratory, including the training and skills required of personnel and quality control. In addition, state laws mandate proficiency testing, which involves testing of specimens that have been specifically prepared for the laboratory. In addition, certain states require licensing of out-of-state laboratories in order to receive and test specimens from those tests. If a laboratory is out of compliance with such statutory or regulatory standards, the state may suspend, limit, revoke or annul the laboratory’s license, censure the holder of the license or assess civil money penalties.

Pharmaceutical Regulation in the United States

In the United States, the FDA regulates drugs under the FDCA and its implementing regulations. The process of obtaining regulatory approvals and the subsequent compliance with applicable federal, state, local and foreign statutes and regulations requires the expenditure of substantial time and financial resources. Failure to comply with the applicable U.S. requirements at any time during the product

18

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

development process, approval process or after approval, may subject an applicant to a variety of administrative or judicial sanctions, such as the FDA’s refusal to approve pending New Drug Applications (NDA), withdrawal of an approval, imposition of a clinical hold, untitled letters, warning letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, refusals of government contracts, restitution, disgorgement or civil or criminal penalties.

Any drug products manufactured or distributed by us pursuant to FDA approvals are subject to continuing regulation by the FDA, including manufacturing, periodic reporting, product sampling and distribution, advertising, promotion, drug shortage reporting, compliance with any post-approval requirements imposed as a conditional of approval such as Phase 4 clinical trials, a Risk Evaluation and Mitigation Strategy (REMS), and surveillance, recordkeeping and reporting requirements, including adverse experiences.

After approval, most changes to the approved product, such as adding new indications or other labeling claims are subject to further testing to new clinical investigation requirements and prior FDA review and approval. There also are continuing, annual program fee requirements for any approved products and the establishments at which such products are manufactured, as well as new application fees for supplemental applications with clinical data. Drug manufacturers and their subcontractors are required to register their establishments with the FDA and certain state agencies and to list their drug products and are subject to periodic announced and unannounced inspections by the FDA and these state agencies for compliance with Good Manufacturing Practices, or cGMPs, and other requirements, which impose procedural and documentation requirements upon us and our third-party manufacturers.

Changes to the manufacturing process are strictly regulated and often require prior FDA approval before being implemented, or FDA notification. FDA regulations also require investigation and correction of any deviations from cGMPs specifications and impose reporting and documentation requirements upon the sponsor and any third-party manufacturers that the sponsor may decide to use. Accordingly, manufacturers must continue to expend time, money and effort in the area of production and quality control to maintain cGMP compliance.

Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, or with manufacturing processes, or failure to comply with regulatory requirements, may result in withdrawal of marketing approval, mandatory revisions to the approved labeling to add new safety information or other limitations, imposition of post-market studies or clinical trials to assess new safety risks, or imposition of distribution or other restrictions under a REMS program, among other consequences.

The FDA closely regulates the marketing and promotion of drugs. A company can make only those claims relating to safety and efficacy, purity and potency that are approved by the FDA. Physicians, in their independent professional medical judgement, may prescribe legally available products for uses that are not described in the product’s labeling and that differ from those tested by us and approved by the FDA. We, however, are prohibited from marketing or promoting drugs for uses outside of the approved labeling.

In addition, the distribution of prescription pharmaceutical products, including samples, is subject to the Prescription Drug Marketing Act (PDMA), which regulates the distribution of drugs and drug samples at the federal level, and sets minimum standards for the registration and regulation of drug distributors by the states. Both the PDMA and state laws limit the distribution of prescription pharmaceutical product samples and impose requirements to ensure accountability in distribution. The Drug Supply Chain Security Act also imposes obligations on manufacturers of pharmaceutical products related to product and tracking and serialization.

Failure to comply with any of the FDA’s requirements, which are subject to new legislation and change, could result in significant adverse enforcement actions. These include a variety of administrative or

19

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

judicial sanctions, such as refusal to approve pending applications, license suspension or revocation, withdrawal of an approval, imposition of a clinical hold or termination of clinical trials, warning letters, untitled letters, cyber letters, modification of promotional materials or labeling, product recalls, product seizures or detentions, refusal to allow imports or exports, total or partial suspension of production or distribution, debarment, injunctions, fines, consent decrees, corporate integrity agreements, refusals of government contracts and new orders under existing contracts, exclusion from participation in federal and state healthcare programs, restitution, disgorgement or civil or criminal penalties, including fines and imprisonment. It is also possible that failure to comply with the FDA’s requirements relating to the promotion of prescription drugs may lead to investigations alleging violations of federal and state healthcare fraud and abuse and other laws, as well as state consumer protection laws. Any of these sanctions could result in adverse publicity, among other adverse consequences.

Foreign Regulation

Health authorities in foreign countries regulate Cooper's clinical trialsstudies and medical device sales. The regulations vary widely from country to country. Even if the FDA has cleared or approved a product in the United States, the regulatory agencies or notified bodies in other countries must approve or certify new products before they may be marketed there. The time required to obtain approval or certification in another country may be longer or shorter than that required for FDA clearance or approval, and the requirements may differ. There is a trend towards harmonization of quality system standards among the European Union (EU), United States, Canada and various other industrialized countries. Japan has one of the most rigorous regulatory systems in the world and requires in-country clinical trials. The Japanese quality and regulatory standards remain stringent even with the more recent harmonization efforts and updated Japanese regulations. China is also updating its regulations and is requiring rigorous in-country product testing.

These regulatory procedures require a considerable investment in time and resources and usually result in a substantial delay between new product development and marketing. If the Company does not maintain compliance with regulatory standards or if problems occur after marketing, product approval may be withdrawn.

In addition to FDA regulatory requirements, CooperVision maintains ISO 13485 certification and CE markMark approvals for its products and CooperSurgical maintains ISO 13485 certification for medical devices and ISO 15189 certification for the Genomics laboratories. A CE markMark is an international symbol of adherence to certain standards and compliance with applicable European medical device requirements. These quality programs and approvals are required by the European Medical Device DirectiveRegulation and must be maintained for all products intended to be sold in the European market. The ISO 13485 Quality Measurement System registration is now also required for registration of products in Asia Pacific and Latin American countries. In order to maintain these quality benchmarks, the Company is subjected to rigorous biannual reassessment audits of its quality systems and procedures.

Regulation of Medical Devices and In Vitro Diagnostic Medical Devices in the European Union

The EU has adopted specific directives and regulations regulating the design, manufacture, clinical investigations, conformity assessment, labeling and adverse event reporting for medical devices (including in vitro diagnostic medical devices (IVDs)).

In the EU, until May 25, 2021, medical devices were regulated by the Council Directive 93/42/EEC, or the EU Medical Devices Directive, which has been repealed and replaced by Regulation (EU) No 2017/745 (the EU MDR). Unlike directives, regulations are directly applicable in all EU member states without the need for member states to implement into national law. IVDs are currently regulated by the EU In Vitro Diagnostic Medical Devices Directive (Directive 98/79/EC) (the IVDD). However, on April 5, 2017, Regulation (EU) 2017/746 of the MDR (Regulation 2017/745)European Parliament and of the Council on IVDs and repealing Directive 98/79/EC and Commission Decision 2010/227/EU (the EU IVDR) was adopted.adopted to establish a modernized and more robust EU legislative framework, with the aim of ensuring better protection of public health and patient safety. The MDREU IVDR will however, only become applicable threefive years after publication (in (on

20

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

May 2020)26, 2022). Once applicable,However, on October 14, 2021, the European Commission proposed a “progressive” roll-out of the EU IVDR to prevent disruption in the supply of IVDs. Consequently, if the European Parliament and Council adopt the proposed regulation, the EU IVDR will fully apply on May 26, 2022, but there will be a tiered system extending the grace period for many devices (depending on their risk classification) before they have to be fully compliant with the regulation.

Both the EU MDR and IVDR seek to:

•strengthen the rules on placing devices on the market and reinforce surveillance once they are available;

•establish explicit provisions on manufacturers’ responsibilities for the follow-up of the quality, performance and safety of devices placed on the market;

•establish explicit provisions on importers’ and distributors’ obligations and responsibilities;

•impose an obligation to identify a responsible person who is ultimately responsible for all aspects of compliance with the requirements of the new regulations will bring significant newregulation;

•improve the traceability of medical devices throughout the supply chain to the end-user or patient through the introduction of a unique identification number, to increase the ability of manufacturers and regulatory authorities to trace specific devices through the supply chain and to facilitate the prompt and efficient recall of medical devices that have been found to present a safety risk;

•set up a central database (Eudamed) to provide patients, healthcare professionals and the public with comprehensive information on products available in the EU; and

•strengthen rules for the assessment of certain high-risk devices that may have to undergo an additional check by experts before they are placed on the market.

In the EU, there is currently no premarket government review of medical devices (including IVDs). However, all medical devices (including IVDs) placed on the EU market must respectively meet general safety and performance requirements for many medical devices including enhancedand essential requirements for IVDs, including that a medical device must be designed and manufactured in such a way that, during normal conditions of use, it is suitable for its intended purpose. Medical devices must be safe and effective and must not compromise the clinical evidencecondition or safety of patients, or the safety and documentation, increased focus on device identificationhealth of users and, traceability,where applicable, other persons, provided that any risks which may be associated with their use constitute acceptable risks when weighed against the benefits to the patient and additional post market surveillanceare compatible with a high level of protection of health and vigilance. safety, taking into account the generally acknowledged state of the art.

Compliance with the MDRessential or general safety and performance requirements is a prerequisite for European Conformity Marking, or CE Mark, without which medical devices cannot be marketed or sold in the EU. To demonstrate compliance with the essential or general safety and performance requirements medical device manufacturers must undergo a conformity assessment procedure, which varies according to the type of medical device and its (risk) classification. Except for low-risk medical devices (Class I) or general IVDs, where the manufacturer can self-assess the conformity of its products with the essential or general safety and performance requirements (except for any parts which relate to sterility, metrology or reuse aspects of a medical device), a conformity assessment procedure requires the intervention of a notified body. Notified bodies are independent organizations designated by EU member states to assess the conformity of devices before being placed on the market. A notified body would typically audit and examine a product’s technical dossiers and the manufacturers’ quality system (notified body must presume that quality systems which implement the relevant harmonized standards—ISO 13485:2016 for Quality Management Systems—conform to these requirements). If satisfied that the relevant product conforms to the essential or general safety and performance requirements, the notified body issues a certificate of conformity, which the manufacturer uses as a basis for its own declaration of conformity. The manufacturer may then apply the CE Mark to the device, which allows the device to be placed on the market throughout the EU.

21

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Throughout the term of the certificate of conformity, the manufacturer will require re-certificationbe subject to periodic surveillance audits to verify continued compliance with the applicable requirements. In particular, there will be a new audit by the notified body before it will renew the relevant certificate(s).

All manufacturers placing medical devices on the market in the EU must comply with the EU medical device vigilance system. Under this system, serious incidents and Field Safety Corrective Actions (FSCAs) must be reported to the relevant authorities of manythe EU member states. Manufacturers are required to take FSCAs to prevent or reduce a risk of oura serious incident associated with the use of a medical device that is made available on the market. An FSCA may include the recall, modification, exchange, destruction or retrofitting of the device.

The advertising and promotion of medical devices is subject to some general principles set forth by EU directives. Only devices that are CE-marked may be marketed and advertised in the EU in accordance with their intended purpose. Directive 2006/114/EC concerning misleading and comparative advertising and Directive 2005/29/EC on unfair commercial practices, while not specific to the advertising of medical devices, also apply to the advertising thereof and contain general rules, for example requiring that advertisements are evidenced, balanced and not misleading. Specific requirements are defined at the national level. EU member states laws related to the advertising and promotion of medical devices, which vary between jurisdictions, may limit or restrict the advertising and promotion of products to the enhanced standards. Further, products soldgeneral public and may impose limitations on promotional activities with healthcare professionals.

In the EU, regulatory authorities have the power to carry out announced and, if necessary, unannounced inspections of companies, as IVDs in Europe willwell as suppliers and/or sub-contractors and, where necessary, the facilities of professional users. Failure to comply with regulatory requirements (as applicable) could require time and resources to respond to the regulatory authorities’ observations and to implement corrective and preventive actions, as appropriate. Regulatory authorities have broad compliance and enforcement powers, and if such issues cannot be regulated under the In Vitro Diagnostics Directive (98/79/EC). A new regulation, the IVDR (EU) 2017/746, the IVDR, has been released and will become fully enforceable in 2022. These regulations include requirements for both presentation and reviewresolved to their satisfaction can take a variety of performance data and quality-system requirements.actions, including untitled or warning letters, fines, consent decrees, injunctions, or civil or criminal penalties.