0000759944 us-gaap:ConsumerPortfolioSegmentMember cfg:HomeEquityLineofCreditServicedbyOthersMember cfg:FinancingReceivablesEqualToOrGreaterThan30DaysPastDueMember 2018-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X]☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended

December 31, 20182019

[ ]☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period From

(Not Applicable)

Commission File Number 001-36636

(Exact name of the registrant as specified in its charter)

|

| | |

| Delaware | | 05-0412693 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification Number) |

One Citizens Plaza, Providence, RI02903

(Address of principal executive offices, including zip code)

(401) 456-7000

(401) 456-7000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading symbol(s) | Name of each exchange on which registered |

| Common stock, $0.01 par value per share | CFG | New York Stock Exchange |

Depositary Shares, each representing a 1/40th40th interest in a share of 6.350% Fixed-to-Floating Rate Non-Cumulative Perpetual Preferred Stock, Series D

| CFG PrD | New York Stock Exchange |

Depositary Shares, each representing a 1/40th interest in a share of 5.000% Fixed-Rate Non-Cumulative Perpetual Preferred Stock, Series E

| CFG PrE | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ü] ☑Yes [ ]☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ]☐ Yes [ü] ☑No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. [ü] ☑Yes [ ]☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). [ü] ☑Yes [ ]☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ü]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

|

| | | |

| Large accelerated filer | [ü]

☑ | Accelerated filer | [ ]☐ |

| Non-accelerated filer | [ ]☐ | Smaller reporting company | [ ]☐ |

| | | Emerging growth company | [ ]☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ]☐ Yes [ü]☑ No

The aggregate market value of voting stock held by nonaffiliates of the Registrant was $18,789,421,828$16,145,696,534 (based on the June 30, 20182019 closing price of Citizens Financial Group, Inc. common shares of $38.90$35.36 as reported on the New York Stock Exchange). There were 460,390,006427,434,404 shares of Registrant’s common stock ($0.01 par value) outstanding on February 1, 2019.5, 2020.

Documents incorporated by reference

Portions of Citizens Financial Group, Inc.’s proxy statement to be filed with the United States Securities and Exchange Commission in connection with Citizens Financial Group, Inc.’s 20192020 annual meeting of stockholders (the “Proxy Statement”) are incorporated by reference into Part III hereof. Such Proxy Statement will be filed within 120 days of Citizens Financial Group, Inc.’s fiscal year ended December 31, 2018.2019.

|

| | | | |

| | | | | |

| | | | |

| | | Table of Contents | | |

| | | | | |

| | | Page | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| �� | | | |

| | | | |

CITIZENS FINANCIAL GROUP, INC.

|

| | |

| | Citizens Financial Group, Inc. | 1 |

GLOSSARY OF ACRONYMS AND TERMS

The following listing providesis a comprehensive referencelist of common acronyms and terms we regularly use in our financial reporting:

|

| | |

| 2017 Tax Legislation | | An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget for Fiscal Year 2018 (Tax Cuts and Jobs Act) |

| ACL | | Allowance for Credit Losses |

| Acquisitions | | Refers to acquisitions after second quarter 2018, including Franklin American Mortgage Company, Clarfeld Financial Advisors, LLC and Bowstring Advisors LLC |

| AFS | | Available for Sale |

| ALLL | | Allowance for Loan and Lease Losses |

| ALM | | Asset and Liability Management |

| AOCI | | Accumulated Other Comprehensive Income (Loss) |

| ASU | | Accounting Standards Update |

| ATM | | Automated Teller Machine |

| Bank Holding Company Act | | The Bank Holding Company Act of 1956 |

| Board or Board of Directors | | The Board of Directors of Citizens Financial Group, Inc. |

| bps | | Basis Points |

C&I | | Commercial and Industrial |

| Capital Plan Rule | | Federal Reserve’sReserve Regulation Y Capital Plan Rule |

| CBNA | | Citizens Bank, National Association |

| CBPA | | Citizens Bank of Pennsylvania |

| CCAR | | Comprehensive Capital Analysis and Review |

| CCB | | Capital Conservation Buffer |

| CCMI | | Citizens Capital Markets, Inc. |

| CECL | | Current Expected Credit Losses (ASU 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments) |

| CET1 | | Common Equity Tier 1 |

| CET1 capital ratio | | Common Equity Tier 1 capital divided by total risk-weighted assets as defined under the U.S. Basel III Standardized approach |

| CFPB | | Consumer Financial Protection Bureau |

| CFTC | | Commodity Futures Trading Commission |

| Citizens or CFG or the Company, we, us, or our | | Citizens Financial Group, Inc. and its Subsidiaries |

| CLTV | | Combined Loan-to-Value |

| CLO | | Collateralized Loan Obligation |

| CMO | | Collateralized Mortgage Obligation |

| CRA | | Community Reinvestment Act |

| CRE | | Commercial Real Estate |

DFAST | | Dodd-Frank Act Stress Test |

| DIF | | Deposit Insurance Fund |

| Dodd-Frank Act | | The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 |

| EGRRCPA | | Economic Growth, Regulatory Relief and Consumer Protection Act |

| EPS | | Earnings Per Share |

| ESPP | | Employee Stock Purchase Program |

| ERISA | | Employee Retirement Income Security Act of 1974 |

| Exchange Act | | The Securities Exchange Act of 1934 |

| FAMC | | Franklin American Mortgage Company |

| FAMC acquisition | | The August 1, 2018 acquisition of Franklin American Mortgage Company |

| Fannie Mae (FNMA) | | Federal National Mortgage Association |

| FASB | | Financial Accounting Standards Board |

|

| | |

| | Citizens Financial Group, Inc. | 2 |

|

| | |

| FDIA | | Federal Deposit Insurance Act |

| FDIC | | Federal Deposit Insurance Corporation |

| FFIEC | | Federal Financial Institutions Examination Council |

| FHLB | | Federal Home Loan Bank |

| FICO | | Fair Isaac Corporation (credit rating) |

| FINRA | | Financial Industry Regulation Authority |

CITIZENS FINANCIAL GROUP, INC.

|

| | |

| FRB | | Board of Governors of the Federal Reserve System and, as applicable, Federal Reserve Bank(s) |

| Freddie Mac (FHLMC) | | Federal Home Loan Mortgage Corporation |

| FTE | | Fully Taxable Equivalent |

| FTP | | Funds Transfer Pricing |

| GAAP | | Accounting Principles Generally Accepted in the United States of America |

| GDP | | Gross Domestic Product |

| GLBA | | Gramm-Leach-Bliley Act of 1999 |

| Ginnie Mae (GNMA) | | Government National Mortgage Association |

| GSE | | Government-Sponsored Enterprise |

| HELOC | | Home Equity Line of Credit |

| HTM | | Held To Maturity |

| Last-of-Layer | | Last-of-layer is a fair value hedge of the interest rate risk of a portfolio of similar prepayable assets whereby the last dollar amount within the portfolio of assets is identified as the hedged item |

| LCR | | Liquidity Coverage Ratio |

| LHFS | | Loans Held for Sale |

| LGD | | Loss Given Default |

| LIBOR | | London Interbank Offered Rate |

| LIHTC | | Low Income Housing Tax Credit |

| LTV | | Loan-to-Value |

| MBS | | Mortgage-Backed Securities |

| MD&A | | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| Mid-Atlantic | | District of Columbia, Delaware, Maryland, New Jersey, New York, Pennsylvania, Virginia, and West Virginia |

| Midwest | | Illinois, Indiana, Michigan, and Ohio |

| MSA | | Metropolitan Statistical Area |

MSRMSRs | | Mortgage Servicing RightRights |

| New England | | Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont |

| NM | | Not meaningful |

NPR | | Notice of Proposed Rulemaking |

| NSFR | | Net Stable Funding Ratio |

NYSE | | New York Stock Exchange |

| OCC | | Office of the Comptroller of the Currency |

| OCI | | Other Comprehensive Income |

| OFAC | | Office of Foreign Assets Control |

| Parent Company | | Citizens Financial Group, Inc. (the Parent Company of Citizens Bank, of Pennsylvania, Citizens Bank, National Association and other subsidiaries) |

| PD | | Probability of Default |

| peers or peer regional banks | | BB&T, Comerica, Fifth Third, KeyCorp, M&T, PNC, Regions, SunTrust and U.S. BancorpBancorp. Includes Truist for the period subsequent to the merger of BB&T and SunTrust |

| REITs | | Real Estate Investment Trusts |

| ROTCE | | Return on Average Tangible Common Equity |

| RPA | | Risk Participation Agreement |

|

| | |

| | Citizens Financial Group, Inc. | 3 |

|

| | |

| SBA | | Small Business Administration |

| SBO | | Serviced by Others loan portfolio |

| SEC | | United States Securities and Exchange Commission |

| SVaR | | Stressed Value-at-Risk |

| TDR | | Troubled Debt Restructuring |

| Tier 1 capital ratio | | Tier 1 capital, which includes Common Equity Tier 1 capital plus non-cumulative perpetual preferred equity that qualifies as additional tier 1 capital, divided by total risk-weighted assets as defined under the U.S. Basel III Standardized approach |

| Tier 1 leverage ratio | | Tier 1 capital, which includes Common Equity Tier 1 capital plus non-cumulative perpetual preferred equity that qualifies as additional tier 1 capital, divided by quarterly adjusted average assets as defined under the U.S. Basel III Standardized approach |

| Total capital ratio | | Total capital, which includes Common Equity Tier 1 capital, tier 1 capital and allowance for credit losses and qualifying subordinated debt that qualifies as tier 2 capital, divided by total risk-weighted assets as defined under the U.S. Basel III Standardized approach |

| VaR | | Value-at-Risk |

| VIE | | Variable Interest Entities |

|

| | |

| | Citizens Financial Group, Inc. | 4 |

CITIZENS FINANCIAL GROUP, INC.

FORWARD-LOOKING STATEMENTS

FORWARD-LOOKING STATEMENTS

This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Statements regarding potential future share repurchases and future dividends are forward-looking statements. Also, any statement that does not describe historical or current facts is a forward-looking statement. These statements often include the words “believes,” “expects,” “anticipates,” “estimates,” “intends,” “plans,” “goals,” “targets,” “initiatives,” “potentially,” “probably,” “projects,” “outlook” or similar expressions or future conditional verbs such as “may,” “will,” “should,” “would,” and “could.”

Forward-looking statements are based upon the current beliefs and expectations of management, and on information currently available to management. Our statements speak as of the date hereof, and we do not assume any obligation to update these statements or to update the reasons why actual results could differ from those contained in such statements in light of new information or future events. We caution you, therefore, against relying on any of these forward-looking statements. They are neither statements of historical fact nor guarantees or assurances of future performance. While there is no assurance that any list of risks and uncertainties or risk factors is complete, important factors that could cause actual results to differ materially from those in the forward-looking statements include the following, without limitation:

| |

| • | Negative economic and political conditions that adversely affect the general economy, housing prices, the job market, consumer confidence and spending habits which may affect, among other things, the level of nonperforming assets, charge-offs and provision expense; |

| |

| • | The rate of growth in the economy and employment levels, as well as general business and economic conditions, and changes in the competitive environment; |

| |

| • | Our ability to implement our business strategy, including the cost savings and efficiency components, and achieve our financial performance goals; |

| |

| • | Our ability to meet heightened supervisory requirements and expectations; |

| |

| • | Liabilities and business restrictions resulting from litigation and regulatory investigations; |

| |

| • | Our capital and liquidity requirements (including under regulatory capital standards, such as the U.S. Basel III capital rules) and our ability to generate capital internally or raise capital on favorable terms; |

| |

| • | The effect of changes in interest rates on our net interest income, net interest margin and our mortgage originations, mortgage servicing rights and mortgages held for sale; |

| |

| • | Changes in interest rates and market liquidity, as well as the magnitude of such changes, which may reduce interest margins, impact funding sources and affect the ability to originate and distribute financial products in the primary and secondary markets; |

| |

| • | The effect of changes in the level of checking or savings account deposits on our funding costs and net interest margin; |

| |

| • | Financial services reform and other current, pending or future legislation or regulation that could have a negative effect on our revenue and businesses; |

| |

| • | A failure in or breach of our operational or security systems or infrastructure, or those of our third party vendors or other service providers, including as a result of cyber-attacks; and |

| |

| • | Management’s ability to identify and manage these and other risks. |

Negative economic and political conditions that adversely affect the general economy, housing prices, the job market, consumer confidence and spending habits which may affect, among other things, the level of nonperforming assets, charge-offs and provision expense;

The rate of growth in the economy and employment levels, as well as general business and economic conditions, and changes in the competitive environment;

Our ability to implement our business strategy, including the cost savings and efficiency components, and achieve our financial performance goals;

Our ability to meet heightened supervisory requirements and expectations;

Liabilities and business restrictions resulting from litigation and regulatory investigations;

Our capital and liquidity requirements (including under regulatory capital standards, such as the U.S. Basel III capital rules) and our ability to generate capital internally or raise capital on favorable terms;

The effect of changes in interest rates on our net interest income, net interest margin and our mortgage originations, mortgage servicing rights and mortgages held for sale;

Changes in interest rates and market liquidity, as well as the magnitude of such changes, which may reduce interest margins, impact funding sources and affect the ability to originate and distribute financial products in the primary and secondary markets;

The effect of changes in the level of checking or savings account deposits on our funding costs and net interest margin;

Financial services reform and other current, pending or future legislation or regulation that could have a negative effect on our revenue and businesses, including the Dodd-Frank Act and other legislation and regulation relating to bank products and services;

A failure in or breach of our operational or security systems or infrastructure, or those of our third party vendors or other service providers, including as a result of cyber-attacks; and

Management’s ability to identify and manage these and other risks.

In addition to the above factors, we also caution that the amountactual amounts and timing of any future common stock dividends or share repurchases will depend onbe subject to various factors, including our capital position, financial condition, earnings, cash needs,performance, capital impacts of strategic initiatives, market conditions and regulatory constraints, capital requirements (including requirements of our subsidiaries), and accounting considerations, as well as any other factors that our Board of Directors deems relevant in making such a determination. Therefore, there can be no assurance that we will repurchase shares from or pay any dividends to holders of our common stock, or as to the amount of any such repurchases or dividends.

More information about factors that could cause actual results to differ materially from those described in the forward-looking statements can be found under “Risk Factors” in Part I, Item 1A included in this Report.“Risk Factors”.

CITIZENS FINANCIAL GROUP, INC. |

| | |

| | Citizens Financial Group, Inc. | 5 |

PART I

ITEM 1. BUSINESS

Citizens Financial Group, Inc. is the 13th14th largest retail bank holding company in the United States.(1) Headquartered in Providence, Rhode Island, Citizens offerswe offer a broad range of retail and commercial banking products and services to more than five million individuals, small businesses, middle-market companies, large corporations and institutions, largelyinstitutions. Our products and services are offered through approximately 1,100 branches in 11 states in the New England, Mid-Atlantic and Midwest regions and approximately 140135 retail and commercial non-branch offices, located in our branch banking footprint and in other states and the Districtthough certain lines of Columbia, which are contiguous with our footprint.business serve national markets. At December 31, 2018, the Company2019, we had total assets of $160.5$165.7 billion, total deposits of $119.6$125.3 billion and total stockholders’ equity of $20.8$22.2 billion.

Citizens isWe are a bank holding company which was incorporated under Delaware state law in 1984 and whose primary federal regulator is the Board of Governors of the Federal Reserve System (“FRB”). As of December 31, 2018, our primary subsidiaries were Citizens Bank, N.A. (“CBNA”), a national banking association whose primary federal regulator is the Office of the Comptroller of the Currency (“OCC”), and Citizens Bank of Pennsylvania (“CBPA”), a Pennsylvania-chartered savings bank regulated by the Department of Banking of the Commonwealth of Pennsylvania and supervised by the Federal Deposit Insurance Corporation (the “FDIC”) as its primary federal regulator.FRB. On January 2, 2019, we consolidated our banking subsidiaries via a merger of CBPA into CBNA in order to streamline governance and enterprise risk management, improve CBNA’s risk profile and gain operational efficiencies. CBNA is now our primary subsidiary and our sole banking subsidiary.subsidiary, whose primary federal regulator is the OCC.

Business Segments

We manage our business through two reportable business operating segments: Consumer Banking and Commercial Banking. The Company’sFor additional information regarding our business segments see the “Business Operating Segments” section of Item 7 and Note 25 in Item 8. Our activities outside the two business operatingthese segments are classified as “Other” and include treasury activities, wholesale funding activities, securities portfolio, community development assets and other unallocated assets, liabilities, capital, revenues, provision for credit losses and expenses, including income tax expense. The Other classification also includes the financial impact of non-core, liquidating loan portfolios and other non-core assets and liabilities. For a description of non-core assets see “Management’s Discussionthe “Allowance for Credit Losses and AnalysisNonperforming Assets” section of Financial Condition and Results of Operations — Analysis of Financial Condition — Loans and Leases — Non-Core Assets” in Part II, Item 7, of this Report. For additional information regarding our business segments see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results of Operations — 2018 compared with 2017 — Business Operating Segments” in Part II, Item 7 and Note 25 “Business Operating Segments” in the Notes to Consolidated Financial Statements in Part II, Item 8 — Financial Statements and Supplementary Data, of this Report.7.

The following table presents selected financial information for our business operating segments, Other and consolidated:

| | | | For the Year Ended December 31, | For the Year Ended December 31, |

| 2018 | | 2017 | 2019 | | 2018 |

| (in millions) | Consumer Banking | | Commercial Banking | | Other | | Consolidated | | Consumer Banking | | Commercial Banking | | Other | | Consolidated | Consumer Banking | | Commercial Banking | | Other | | Consolidated | | Consumer Banking | | Commercial Banking | | Other | | Consolidated |

| Net interest income |

| $3,064 |

| |

| $1,497 |

| |

| ($29 | ) | |

| $4,532 |

| |

| $2,651 |

| |

| $1,411 |

| |

| $111 |

| |

| $4,173 |

|

| $3,182 |

| |

| $1,466 |

| |

| ($34 | ) | |

| $4,614 |

| |

| $3,064 |

| |

| $1,497 |

| |

| ($29 | ) | |

| $4,532 |

|

| Noninterest income | 973 |

| | 545 |

| | 78 |

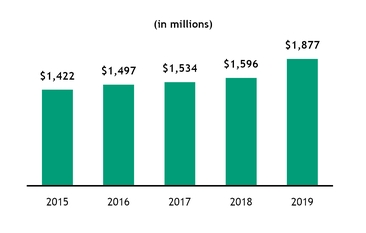

| | 1,596 |

| | 905 |

| | 538 |

| | 91 |

| | 1,534 |

| 1,156 |

| | 607 |

| | 114 |

| | 1,877 |

| | 973 |

| | 545 |

| | 78 |

| | 1,596 |

|

| Total revenue | 4,037 |

| | 2,042 |

| | 49 |

| | 6,128 |

| | 3,556 |

| | 1,949 |

| | 202 |

| | 5,707 |

| 4,338 |

| | 2,073 |

| | 80 |

| | 6,491 |

| | 4,037 |

| | 2,042 |

| | 49 |

| | 6,128 |

|

| Noninterest expense | 2,723 |

| | 813 |

| | 83 |

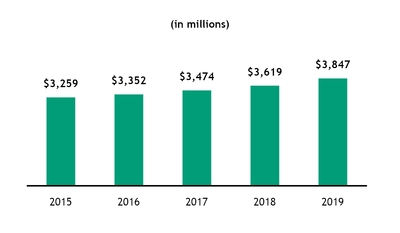

| | 3,619 |

| | 2,593 |

| | 772 |

| | 109 |

| | 3,474 |

| 2,851 |

| | 858 |

| | 138 |

| | 3,847 |

| | 2,723 |

| | 813 |

| | 83 |

| | 3,619 |

|

| Net income |

| $767 |

| |

| $927 |

| |

| $27 |

| |

| $1,721 |

| |

| $452 |

| |

| $774 |

| |

| $426 |

| |

| $1,652 |

| 875 |

| | 870 |

| | 46 |

| | 1,791 |

| | 767 |

| | 927 |

| | 27 |

| | 1,721 |

|

| Total average loans and leases and loans held for sale |

| $60,691 |

| |

| $51,344 |

| |

| $2,446 |

| |

| $114,481 |

| |

| $58,371 |

| |

| $48,655 |

| |

| $2,946 |

| |

| $109,972 |

|

| $63,396 |

| |

| $54,355 |

| |

| $2,089 |

| |

| $119,840 |

| |

| $60,691 |

| |

| $51,344 |

| |

| $2,446 |

| |

| $114,481 |

|

| Total average deposits |

| $77,542 |

| |

| $30,704 |

| |

| $7,611 |

| |

| $115,857 |

| |

| $74,873 |

| |

| $30,005 |

| |

| $6,996 |

| |

| $111,874 |

|

| $84,835 |

| |

| $31,085 |

| |

| $7,381 |

| |

| $123,301 |

| |

| $77,542 |

| |

| $30,704 |

| |

| $7,611 |

| |

| $115,857 |

|

Consumer Banking Segment

Consumer Banking serves retail customers and small businesses with annual revenues of up to $25 million, with products and services that include deposit products, mortgage and home equity lending, credit cards, business loans, wealth management and investment services largely across our 11-state traditional banking footprint. We also offer auto loans, education loans, and unsecured loans and product financing loans in addition to select digital deposit

(1) According to SNL Financial as of September 30, 2018.

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

products nationwide.

Consumer Banking operates a multi-channel distribution network with a workforce of approximately 6,2005,700 branch colleagues, approximately 1,100 branches, including about 310290 in-store locations, and approximately 2,9002,700 ATMs. Our network includes approximately 1,3201,325 specialists covering lending, savings and investment needs as well as a broad range of small business products and services. We serve customers on a national basis through telephone service centers as well as through our online and mobile platforms where we offer customers the convenience of depositing funds, paying bills and transferring money between accounts and from person to person, as well as a host of other everyday transactions.

(1) According to SNL Financial as of September 30, 2019.Based on subsequent peer merger activity.

|

| | |

| | Citizens Financial Group, Inc. | 6 |

We believe our strong retail deposit market share in our core regions, which have relatively diverse economies and affluent demographics, is a competitive advantage. As of June 30, 2018,2019, we ranked second by retail deposit market share in the New England region and ranked in the top five in nine of our ten principal MSAs.(1)

The following table presents information regarding our competitive position in our principal MSAs:

| | | (dollars in billions) | | Total | Deposit | | Total | Deposit |

| MSA | Total Branches | Deposits | Deposit Rank | Market Share | Total Branches | Deposits | Deposit Rank | Market Share |

| Boston, MA | 202 | $22.1 | 2 | 14.0% | 202 | $22.0 | 2 | 13.4% |

| Philadelphia, PA | 171 | 15.0 | 4 | 11.0 | 169 | 14.8 | 4 | 10.1 |

| Pittsburgh, PA | 118 | 8.7 | 2 | 16.2 | 112 | 8.2 | 2 | 13.7 |

| Providence, RI | 93 | 8.6 | 1 | 26.0 | 93 | 8.8 | 1 | 24.9 |

| Detroit, MI | 81 | 5.5 | 6 | 7.0 | 81 | 5.5 | 7 | 6.5 |

| Cleveland, OH | 51 | 3.9 | 4 | 10.1 | 50 | 3.9 | 4 | 7.9 |

| Manchester, NH | 20 | 2.5 | 1 | 30.2 | 19 | 2.5 | 2 | 27.9 |

| Buffalo, NY | 41 | 1.9 | 4 | 8.9 | 40 | 1.9 | 5 | 8.3 |

| Albany, NY | 22 | 1.9 | 3 | 12.3 | 21 | 1.9 | 4 | 9.8 |

| Rochester, NY | 25 | 1.7 | 5 | 9.6 | 25 | 1.7 | 5 | 9.4 |

Source: FDIC, June 2018.2019. Principal MSAs determined by total retail branch count. Deposits capped at $500 million per branch. Includes banks, savings banks and thrifts. Excludes “non-retail banks” as defined by SNL Financial. The scope of “non-retail banks” is subject to the discretion of SNL Financial, but typically includes: industrial bank and non-depository trust charters, institutions with more than 20% brokered deposits (of total deposits), institutions with more than 20% credit card loans (of total loans), institutions deemed not to broadly participate in the banking services market and other nonretail competitor banks. Due to deposit cap, Citizens Access® retail deposits excluded from MSA deposits statistics.

Commercial Banking Segment

Commercial Banking primarily serves companies and institutions with annual revenues of over $25 million to more than $3.0 billion and strives to be our clients’ trusted advisor and preferred provider for their banking needs. We offer a broad complement of financial products and solutions, including lending and leasing, deposit and treasury management services, foreign exchange, and interest rate and commodity risk management solutions, as well as loan syndications, corporate finance, merger and acquisition, and debt and equity capital markets capabilities.

Commercial Banking is structured along business lines and product groups. The business lines, Corporate Banking and Commercial Real Estate, and the product groups, Treasury Solutions and Corporate Finance & Capital Markets, and Treasury Solutions work in teams to understand client needs and provide comprehensive solutions to meet those needs. We acquire new clients through a coordinated approach to the market, leveraging deep industry knowledge in specialized banking groups and a geographic coverage model.

Our Corporate Banking business line servicesserves middle market domestic commercial and industrial clients with annual gross revenues of $25 million to $500 million, and mid-corporate clients with annual revenues of $500 million to more than $3.0 billion.billion in the United States. In several areas, such as Healthcare, Technology, Aerospace and Defense, and Franchise Finance, we offer a more dedicated and tailored approach to better meet the unique needs of these client segments. Smaller commercial clients, with an affinity for local bank branch support, cluster around our 11 state footprint. Larger clients seeking more specialty financial services expertise are covered nationally. Corporate Banking is a general lending business which offers a broad range of products, including secured and unsecured lines of credit, term loans, commercial mortgages, domestic and global treasury management solutions, trade services, interest rate products, foreign exchange services and letters of credit.

(1) According to SNL Financial.

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

Our Commercial Real Estate business line provides customized debt capital solutions for middle market operators, institutional developers, investors, and REITs. Commercial Real Estate provides financing for projects primarily in the office, multi-family, industrial, retail, healthcare and hospitality sectors.

The Corporate Finance & GlobalCapital Markets product group serves clients through key product groups including Corporate Finance, Capital Markets, and Global Markets. Corporate Finance provides advisory services to middle market and mid-corporate clients, including mergers and acquisitions and capital structure advice. The team works closely with industry-sector specialists within debt capital markets to advise our clients. Corporate Finance also provides acquisition and follow-on financing for new and recapitalized portfolio companies of key sponsors, services meeting the unique and time-sensitive needs of private equity firms, management companies and funds, and underwriting and portfolio management expertise for leveraged transactions and relationships. Capital Markets originates, structures and underwrites multi-bank syndicated credit facilities targeting middle market, mid-corporate and private equity sponsors with a focus on offering value-added ideas to optimize their capital structures. Citizens Capital Markets, Inc. (“CCMI”), our commercial broker-dealer, advisesstructures, including advising on and facilitatesfacilitating mergers and acquisitions, valuations, tender offers, financial restructurings, asset sales,

(1) According to SNL Financial.

|

| | |

| | Citizens Financial Group, Inc. | 7 |

divestitures and other corporate reorganizations and business combinations. Global Markets provides foreign exchange, and interest rate and commodities risk management services.

The Treasury Solutions product group supports Commercial Banking and certain small business clients with treasury management solutions, including domestic and international products and services related to receivables, payables, information reporting and liquidity management as well as commercial credit cards and trade finance.

Business Strategy

Our mission is to help each of our customers, colleagues and communities reach their potential, and our vision is to bebecome a top-performing bank distinguished by our customer-centric culture, mindset of continuous improvement, and excellent capabilities. It is embedded in our cultureWe strive to make sure we understand our customers’customers and targeted client needs, so we can tailor advice and solutions to help make our customersthem more successful. Our business strategy is designed to maximize the full potential of our business andbusinesses, drive sustainable growth, and enhanced profitability, and ourenhance profitability. Our success rests on our ability to distinguish ourselves as follows:

Maintain a high-performing, customer-centric organization:To accomplish this, we are embedding acontinually strive to enhance our “customer-first” culture among our managers and colleaguesin order to deliver the best possible banking experience forexperience. Recently, we launched a new company-wide branding campaign ‘Made Ready,’ which is centered around our customers.focus on delivering personalized and distinctive experiences. For our colleagues, we are drivingtaking talent management to the next level, with a focus ongoal of attracting, developing and retaining great people, andwhile ensuring strong leadership, teamwork, and a sense of empowerment, accountability and urgency.

Develop differentiated value propositions to acquire, deepen, and retain core customer segments: We have focused on certain customer segments where we believe we are well positioned to compete. In Consumer Banking, we focus on mass market andserving mass affluent and affluent customers, and small business customers. In Commercial Banking, we focus on serving customers in the middle market, mid-corporate, and certain industry vertical areas. By developing differentiated and targeted value propositions, we believe we can attract new customers, deepen relationships with existing customers, and deliver an enhanced customer experience.

Build excellent capabilities that will allowdesigned to help us to stand out from our competitors:Across our businesses we strive to deliver seamless, multi-channel experiences andthat allow customers to interact with us when, where and how they want.choose. We are buildingcontinue to build out enhanced data analytics and capabilities to provide timely, insight-driven, and tailored advice and continuein order to add new capabilities that help deliver solutions for ourto consumer and business customers throughout their lifecycles. We are also focused on expanding our digital capabilities and related strategies in order to satisfy rapidly changing customer preferences.

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

Operate with financial discipline and a mindset of continuous improvement to self-fund investments: We believe that continued focus on operational efficiency is critical to ourfuture profitability and the ability to continue to reinvest to drive future growth. We launched the first Tapping our Potential (“TOP”) initiative in late 2014 which wasand have launched additional programs in each subsequent year. The programs are designed to improve the effectiveness, efficiency, and competitiveness of the franchise, and we commenced the fifth phase of this initiative infranchise. In the second half of 2018.2019, we launched the sixth TOP program, which is a multi-year program consisting of traditional TOP initiatives (similar in nature to prior programs), and a Transformation Program designed to redefine how we operate across the organization and deliver for customers and colleagues.

Prudently grow and optimize our balance sheet:We operate with a strong balance sheet with regard to capital, liquidity and funding, coupled with a well-defined and prudent risk appetite. We are prudentlycontinue to focus on thoughtfully growing our balance sheet and we strive to delivergenerate attractive risk-adjusted returns by making goodactively managing capital and resource allocation decisions through our balance sheet optimization initiatives, beinginitiatives. Our goal is to be good stewards of our resources, and we continue to rigorously evaluatingevaluate our execution.

Modernize our technology and operational models to improve delivery, organizational agility and speed to market:We are continuing to modernize our technology environment so that we can accelerateand operating models to improve our speed-to-market, deliver innovative products and take advantage of technology opportunities in the marketplace. We are also investing in new technologiesservices, strengthen collaboration across teams, and leveraging those technologies to deliver better customer outcomes efficiently in order to deliver on our overallmeet financial objectives. We havewill also engagedcontinue to engage in FinTech partnerships that help deliver differentiated value-added digital experiences for our customers.

Embed risk management within our culture and our operations:We are continuing to strengthen our risk management culture and processes asGiven that the quality of our risk management program directly affects our ability to execute our strategy deliver valuewe continue to work to further strengthen our stakeholders and become a top-performing bank.risk management culture. Moreover, our continuous and disciplined enhancementswe are committed to continuously enhancing our processes and talent, as well as ourand to making improvements in the platform including ongoing investments in risk technology and frameworks, serveframeworks. These actions are designed to support and bolster our risk management capabilities and our regulatory profile.

|

| | |

| | Citizens Financial Group, Inc. | 8 |

Competition

The financial services industry is highly competitive. Our branch footprint is in the New England, Mid-Atlantic and Midwest regions, though certain lines of business serve national markets. Within these markets we face competition from community banks, super-regional and national financial institutions, credit unions, savings and loan associations, mortgage banking firms, consumer finance companies, securities brokerage firms, insurance companies, money market funds, hedge funds and private equity firms. Some of our larger competitors may make available to their customers a broader array of product,products, pricing and structure alternatives while some smaller competitors may have more liberal lending policies and processes. Competition among providers of financial products and services continues to increase, with consumers having the opportunity to select from a growing variety of traditional and nontraditional alternatives. The ability of non-banking financial institutions, including FinTech companies, to provide services previously limited to commercial banks has also intensified competition.

In Consumer Banking, the industry has become increasingly dependent on and oriented toward technology-driven delivery systems, permitting transactions to be conducted through telephone, online and mobile channels. In addition, technology has lowered barriers to entry and made it possible for non-bank institutions to attract funds and provide lending and other financial services in our footprint, despite not having a physical presence there.products and services. The emergence of digital-only banking models has increased and we expect this trend to continue. Given their lower cost structure, these institutionsmodels are often, on average, able to offer on average higher rates on deposit products than retail banking institutions with a traditional branch footprint. The primary factors driving competition for loans and deposits are interest rates, fees charged, tailored value propositions to different customer segments, customer service levels, convenience, including branch locationlocations and hours of operation, and the range of products and services offered.

In Commercial Banking, there is intense competition for quality loan originations from traditional banking institutions, particularly large regional banks, as well as commercial finance companies, leasing companies and other non-bank lenders, and institutional investors including CLO managers, hedge funds and private equity firms. Some larger competitors, including certain national banks that compete in our market area, may offer a broader array of products and due to their asset size, may sometimes be in a position to hold more exposure on their own balance sheet. We compete on a number of factors including providing innovative corporate finance solutions, quality of customer service and execution, range of products offered, price and reputation.

Regulation and Supervision

Our operations are subject to extensive regulation, supervision and examination under federal and state laws.laws and regulations. These laws and regulations cover all aspects of our business, including lending practices, safeguarding deposits,deposit insurance, customer privacy and information security,cybersecurity, capital structure,adequacy and planning, liquidity, conductsafety and qualifications of personnelsoundness, consumer protection and disclosure, permissible activities and investments, and certain transactions with affiliates. These laws and regulations are intended primarily for the protection of depositors,

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

the Deposit Insurance Fund and the banking system as a whole and not for the protection of shareholders or other investors. The discussion below outlines the material elements of selected laws and regulations applicable to us and our subsidiaries. Changes in applicable law or regulation, and in their interpretation and application by regulatory agencies and other governmental authorities, cannot be predicted, but may have a material effect on our business, financial condition or results of operations.

We and our subsidiaries and affiliates are subject to numerous examinations by federal and state banking regulators, as well as the SEC, FINRA and various state insurance and securities regulators. In some cases, regulatory agencies may take supervisory actions that may not be publicly disclosed, and such actions may restrict or limit our activities or activities of our subsidiaries. As part of our regular examination process, our and CBNA’s respective regulators may advise us or CBNA to operate under various restrictions as a prudential matter. We and CBNA have periodically received requests for information from regulatory authorities at the federal and state level, including from statebanking, securities and insurance commissions,regulators, state attorneys general, federal agencies or law enforcement authorities, securities regulators and other regulatory authorities, concerning theirour business practices. Such requests are considered incidental to the normal conduct of business. For a further discussion of how regulatory actions may impact our business, see “Risk Factors” in Part I, Item 1A included in this Report.“Risk Factors.” For additional information regarding regulatory and supervisory matters, see Note 18 “Commitments and Contingencies”24 in the notes to our Consolidated Financial Statements in Part II, Item 8 of this Report.8.

Overview

We are a bank holding company under the Bank Holding Company Act of 1956 (“Bank Holding Company Act”).Act. We have elected to be treated as a financial holding company under amendments to the Bank Holding Company Act as effected by Gramm-Leach-Bliley Act of 1999 (“GLBA”).GLBA. As such, we are subject to the supervision, examination and reporting requirements of the Bank Holding Company Act and the regulations of the FRB, including through the Federal Reserve Bank of Boston. Under the system of “functional regulation” established under the Bank Holding Company Act, the FRB serves as the primary regulator of our

|

| | |

| | Citizens Financial Group, Inc. | 9 |

consolidated organization, and the SEC serves as the primary regulator of our broker-dealer and investment advisory subsidiaries and directly regulates the activities of those subsidiaries, with the FRB exercising a supervisory role. The Dodd-Frank Act amendments to the Bank Holding Company Act require the FRB to examine the activities of non-depository institution subsidiaries of bank holding companies (that are not functionally regulated) that are engaged in depository institution-permissible activities and provide the FRB with back-up examination and enforcement authority for such activities. The FRB also has the authority to require reports of and examine any subsidiary of a bank holding company.

On July 3, 2018, we received regulatory approval from the OCC to consolidate our two banking subsidiaries via a merger of CBPA into CBNA. We completed this consolidation on January 2, 2019, such that CBNA is now our sole banking subsidiary. CBNA is a national banking association. As such, it is subject to regulation, examination and supervision by the OCC as its primary federal regulator and by the FDIC as the insurer of its deposits.

The federal banking regulators have authority to approve or disapprove mergers, acquisitions, consolidations, the establishment of branches and similar corporate actions. These banking regulators also have the power to prevent the continuance or development of unsafe or unsound banking practices or other violations of law. Federal law governs the activities in which CBNA engages, including the investments it makes and the aggregate amount of loansavailable credit that it may grant to one borrower. Various consumer and compliance laws and regulations also affect its operations. The actions the FRB takes to implement monetary policy also affect CBNA.

In addition, CBNA is subject to regulation, supervision and examination by the CFPB with respect to consumer protection laws and regulations. The CFPB has broad authority to among other things, regulate the offering and provision of consumer financial products by depository institutions, such as CBNA, with more than $10 billion in total assets. The CFPB may promulgate rules under a variety of consumer financial protection statutes, including the Truth in Lending Act, the Electronic Funds Transfer Act and the Real Estate Settlement Procedures Act.

Financial Regulatory ReformTailoring of Prudential Requirements

The Dodd-Frank Act regulates many aspects ofIn October 2019, the financial services industryFRB and addresses amongthe other things, systemic risk, capital adequacy, deposit insurance assessments, consumer financial protection, derivatives and securities markets, restrictions on an insured bank’s transactions with its affiliates, lending limits and mortgage-lending practices. Moreover, as a general matter, in recent years, the federal banking regulators (the FRB,finalized rules that tailor the OCCapplication of the enhanced prudential standards to bank holding companies and the FDIC) as well as the CFPB have taken a more stringent approachdepository institutions to supervising and regulating the financial institutions and financial products and services over which the regulators exercise their respective supervisory authorities, including with respect to enforcement matters. CBNA’s and our products and services have been subject

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

to greater supervisory scrutiny and enhanced supervisory requirements and expectations in recent years, and we expect this scrutiny to continue for the foreseeable future.

Prior to amendment byimplement the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 (“EGRRCPA”), which was signed into law on May 24, 2018, Section 165 of amendments to the Dodd-Frank Act directed the FRB to establish enhanced prudential standards applicable to systemically important financial institutions (“SIFIs”Tailoring Rules”),. The Tailoring Rules assign each U.S. bank holding companiescompany with $100 billion or more in total consolidated assets, as well as its bank subsidiaries, to one of $50four categories based on its size and five other risk-based indicators:

i.cross-jurisdictional activity,

ii.weighted short-term wholesale funding (“wSTWF”),

iii.non-bank assets,

iv.off-balance sheet exposure, and

v.status as a U.S. globally systematically important bank.

Under the Tailoring Rules, we are subject to “Category IV standards,” which apply to banking organizations with at least $100 billion or more. The FRB has adopted final rules implementing three aspectsin total consolidated assets that do not meet any of Section 165: liquiditythe thresholds specified for Categories I through III. Accordingly, Category IV firms, such as us,

| |

| i. | are no longer subject to any LCR requirement (or in certain cases, are subject to reduced requirements), |

ii.remain not subject to advanced approaches capital requirements,

| |

| iii. | remain eligible to opt-out of the requirement to recognize most elements of Accumulated Other Comprehensive Income in regulatory capital, |

iv.remain not subject to the supplementary leverage ratio,

v.remain not subject to the countercyclical capital buffer,

vi.are no longer subject to company-run stress testing requirements,

vii.became subject to supervisory stress testing on a biennial instead of annual basis,

viii.remain subject to requirements to develop and maintain a capital plan on an annual basis, and overall

ix.remain subject to certain liquidity risk management and risk committee requirements.

We discuss other elements of the Tailoring Rules where relevant below. The current rules’ liquidity requirements are described below under “—Liquidity Requirements”,Requirements,” and their stress testing requirements are described below under “—Capital Planning and Stress Testing Requirements.” In addition, the resolution planning requirements implemented by the FRB and FDIC are described below under “—Resolution Planning”.

EGRRCPA amended the Dodd-Frank Act by increasing the asset threshold for application of these enhanced prudential standards from $50 billion to $250 billion. EGRRCPA’s increased asset threshold took effect immediately for bank holding companies with total consolidated assets less than $100 billion. The increased asset threshold generally will become effective 18 months after the date of enactment (that is, in November 2019) for bank holding companies with total consolidated assets of $100 billion or more but less than $250 billion, including Citizens. The FRB is authorized, however, during the 18-month period to exempt, by order, any bank holding company with assets between $100 billion and $250 billion from any enhanced prudential standard requirement. The FRB is also authorized to apply any enhanced prudential standard requirement to any bank holding company with between $100 billion and $250 billion in total consolidated assets that would otherwise be exempt under EGRRCPA, if the FRB determines that such action is appropriate to address risks to financial stability and promote safety and soundness, taking into consideration certain factors including the bank holding company’s capital structure, riskiness, complexity, financial activities (including financial activities of subsidiaries), size, and any other risk-related factors that the FRB deems appropriate. U.S. global systemically important bank holding companies (“G-SIBs”) and bank holding companies with $250 billion or more in total consolidated assets remain fully subject to the Dodd-Frank Act’s enhanced prudential standards requirements.

In October 2018, the FRB and the other federal banking regulators proposed rules that would tailor the application of the enhanced prudential standards to bank holding companies and depository institutions to implement the EGRRCPA amendments (“Tailoring NPRs”). The proposed rules would assign each U.S. bank holding company with $100 billion or more in total consolidated assets, as well as its bank subsidiaries, to one of four categories based on its size and five risk-based indicators: (i) cross-jurisdictional activity, (ii) weighted short-term wholesale funding, (iii) nonbank assets, (iv) off-balance sheet exposure, and (v) status as a U.S. G-SIB. Under the Tailoring NPRs, “Category IV standards” would apply to banking organizations with at least $100 billion in total consolidated assets that do not meet any of the thresholds specified for Categories I through III. Category I standards would be applicable to U.S. G-SIBs; Category II standards would be applicable to non-G-SIBs with $700 billion or more in total consolidated assets or at least $100 billion in total consolidated assets and $75 billion or more in cross-jurisdictional activity; and Category III standards would be applicable to banking organizations that are not subject to Category I or Category II standards and that have at least $250 billion in total consolidated assets or at least $100 billion in total consolidated assets and $75 billion or more in any of three indicators: (i) nonbank assets, (ii) weighted short-term wholesale funding, or (iii) off-balance sheet exposures.

In connection with the release of the proposed rules, FRB staff indicated which firms would fall into each of the four categories based on data for the second quarter of 2018. According to the FRB staff’s projections, Citizens would be a “Category IV” firm under the proposed rules. Firms subject to Category IV standards would generally be subject to the same capital and liquidity requirements as firms with under $100 billion in total consolidated assets, but would also be required to monitor and report certain risk-based indicators. Accordingly, under the Tailoring NPRs, Category IV firms would (i) no longer be subject to any LCR or proposed NSFR requirement, (ii) remain not subject to advanced approaches capital requirements, (iii) remain eligible to opt-out of the requirement to recognize most elements of Accumulated Other Comprehensive Income in regulatory capital, (iv) remain not subject to the supplementary leverage ratio, (v) remain not subject to the countercyclical capital buffer, (vi) no longer be subject to company-run stress testing requirements and (vii) become subject to supervisory stress testing on a biennial instead of annual basis. We discuss other elements of the proposed rules where relevant below. The Tailoring NPRs are subject to modification through the federal rulemaking process in accordance with the Administrative Procedures Act.

The U.S. Basel III rules, summarized briefly in the “—Capital” section below, have impacted our level of capital, and may influence the types of business we may pursue and how we pursue business opportunities. Among other things, the U.S. Basel III rules raised the required minimums for certain capital ratios, added a common equity

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

ratio, included capital buffers, and restricted what constitutes capital. The capital and risk weighting requirements became effective for us on January 1, 2015.Planning.”

Many of the provisions of the Dodd-Frank Act, EGRRCPA and other laws are subject to further rulemaking, guidance and interpretation by the applicable federal regulators. The ultimate effects of EGRRCPA and the Tailoring NPRsRules on Citizens, CBNAus and their respective subsidiaries andour activities will be subject to the final form of the Tailoring NPRs andany additional rulemakingsrule making issued by the FRB and other federal regulators. We will continue to evaluate the impact of any changes in law and any new regulations promulgated, including changes

|

| | |

| | Citizens Financial Group, Inc. | 10 |

in regulatory costs and fees, modifications to consumer products or disclosures required by the CFPB and the requirements of the enhanced supervision provisions, among others.

Financial Holding Company Regulation

The Bank Holding Company Act generally restricts bank holding companies from engaging in business activities other than (i) banking, managing or controlling banks, (ii) furnishing services to or performing services for subsidiaries and (iii) activities that the FRB has determined to be so closely related to banking as to be a proper incident thereto.banking. For so long as they continue to meet the eligibility requirements for financial holding company status, financial holding companies may engage in a broader range of activities, including among other things, securities underwriting and dealing, insurance underwriting and brokerage, merchant banking and other activities that are determined by the FRB, in coordination with the Treasury Department, to be “financial in nature or incidental thereto” or that the FRB determines unilaterally to be “complementary” to financial activities. In addition, a financial holding company may conduct permissible new financial activities or acquire permissible non-bank financial companies with after-the-fact notice to the FRB.

As noted above, we currently have elected to be treated as a financial holding company under amendments to the Bank Holding Company Act as effected by GLBA. To maintain financial holding company status, a financial holding company and all of its insured depository institution subsidiaries must remain well capitalized and well managed (as described below under “Federal Deposit Insurance Act”), and maintain a CRA rating of at least “Satisfactory.”“Satisfactory” (see “Community Reinvestment Act Requirements” below). If a financial holding company ceases to meet the capital and management requirements, the FRB’s regulations provide that the financial holding company must enter into an agreement with the FRB to comply with all applicable capital and management requirements. Until the financial holding company returns to compliance, the FRB may impose limitations or conditions on the conduct of its activities, and the company may not commence any of the broader financial activities permissible for financial holding companies or acquire a company engaged in such financial activities without prior approval of the FRB. In addition, the failure to meet such requirements could result in other material restrictions on the activities of the financial holding company, may also adversely affect the financial holding company’s ability to enter into certain transactions, including acquisition transactions, or obtain necessary approvals in connection therewith, and may result in the bank holding company losing financial holding company status. Any restrictions imposed on our activities by the FRB may not necessarily be made known to the public. If the company does not return to compliance within 180 days, which period may be extended, the FRB may require the financial holding company to divest its subsidiary depository institutions or to discontinue or divest investments in companies engaged in activities permissible only for a bank holding company electing to be treated as a financial holding company. If any insured depository institution subsidiary of a financial holding company fails to maintain a CRA rating of at least “Satisfactory,” the financial holding company would be subject to restrictions on certain new activities and acquisitions. Bank holding companies and banks must also be both well capitalized and well managed in order to acquire banks located outside their home state.

Capital

We must comply with the FRB’sThe U.S. Basel III rules apply to us. These rules establish risk-based and leverage capital adequacy rules, and CBNA must comply with similar capital adequacy rules of the OCC.requirements. The capital adequacy rules of both agenciesrisk-based requirements are based on a banking organization’s risk-weighted assets, also known as RWA, which reflect the Basel III framework.organization’s on- and off-balance sheet exposures, subject to risk weights. The leverage requirements are based on a banking organization’s average consolidated on-balance sheet assets. For more detail on our regulatory capital, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Capitalthe “Capital and Regulatory Matters” in Part II,section of Item 7, included7.

We calculate RWA using the standardized approach and have made the one-time election to opt-out of AOCI. As a result, we are not required to recognize in this Report.

The U.S. Basel III rules, among other things, (i) impose a capital measure called common equity tier 1 capital, or “CET1 capital”, (ii) specify that tier 1 capital consists of CET1 capital and “additional tier 1 capital” instruments meeting certain revised requirements, (iii) define CET1 capital narrowly by requiring that most deductions/adjustments to regulatory capital measures be madethe impacts of net unrealized gains and losses included within AOCI for debt securities that are available for sale or held to CET1maturity, accumulated net gains and not to the other components of capital,losses on cash flow hedges and (iv) expand the scope of the deductions/adjustments to capital as compared to previous regulations. certain defined benefit pension plan assets.

Under the U.S. Basel III rules, the minimum capital ratios are:

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

•4.5% CET1 capital to risk-weighted assets;

•6.0% tier 1 capital (that is, CET1 capital plus additional tier 1 capital) to risk-weighted assets;

•8.0% total capital (that is, tier 1 capital plus tier 2 capital) to risk-weighted assets; and

•

|

| | |

| | Citizens Financial Group, Inc. | 11 |

4.0% tier 1 capital to total average consolidated assets as defined under U.S. Basel III Standardized

approach (known as the “leverage ratio”).

The U.S. Basel III rules also impose a capital conservation buffer (“CCB”) of 2.5% on top of each of the three minimum risk-weighted asset ratios listed above. The implementation of the CCB began on January 1, 2016 at 0.625% and increased by 0.625% annually over a three year phase-in period, which ended January 1, 2019. The CCB for 2018 was 1.875%, and increased to its fully phased-in level of 2.5% as of January 1, 2019. Banking institutions that fail to meet the effective minimum ratios oncewith the fully phased-in CCB is taken into account (that is, 7.0% for CET1 capital to risk-weighted assets, 8.5% for tier 1 capital to risk-weighted assets and 10.5% for total capital to risk-weighted assets) will be subject to constraints on capital distributions, including dividends and share repurchases, and certain discretionary executive compensation. The severity of the constraints depends on the amount of the shortfall and the institution’s “eligible retained income” (that is,, defined as four quarter trailing net income, net of distributions and tax effects not reflected in net income).income. For more details, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Capitalthe “Capital and Regulatory Matters” in Part II,section of Item 7, included in this Report. On7.

In April 10, 2018, the FRB issued a proposal designed to create a single, integrated capital requirement by combining the quantitative assessment of firms’ capital plans with the CCB requirement. Details of this proposal are discussed under “—Capital Planning and Stress Testing Requirements” below. Although the proposal, if adopted, would change the way in which the minimum capital ratios are calculated, firms would continue to be subject to progressively more stringent constraints on capital actions as they approach the minimum ratios.

We are also subject to the FRB's risk-based capital requirements for market risk. See “Management’s Discussion and Analysisthe “Market Risk” section of Financial Condition and Results of Operations — Market Risk — Market Risk Regulatory Capital” in Part II, Item 7, included in this Report, for further discussion.

The U.S. Basel III rules also provide for a number of deductions from, and adjustments to, CET1 capital. For example, certain deferred tax assets (“DTAs”), mortgage servicing assets, and significant investments in non-consolidated financial entities must be deducted from CET1 capital to the extent that any one such category exceeds 10% of CET1 capital or all such items, in the aggregate, exceed 15% of CET1 capital. The deductions and other adjustments to CET1 capital generally became fully phased-in on January 1, 2018, although, as discussed below, the federal banking regulators have extended the transitional treatment for certain items.7.

In November 2017,July 2019, the FRB and the other federal banking regulators issued a final rule that extendedto simplify regulatory capital treatment for MSRs, certain DTAs and significant investments in the 2017 transition provisionscapital of unconsolidated financial institutions, pursuant to EGRRCPA. Effective for certain U.S. Basel III capital rules for non-advanced approaches banking organizations, including us. Effective Januaryus on April 1, 2018,2020, the final rule retainswill change the 2017 U.S. Basel III transitional treatmentindividual CET1 deduction threshold for these assets from 10% to 25%, eliminate the aggregate deduction threshold for these assets of certain15%, assign a 250% risk weight for any MSRs or DTAs mortgage servicing assets,not deducted from CET1 capital, and assign an exposure category risk weight for investments in the capital of unconsolidated financial institutions and minority interests. As a result, since January 1, 2018, our mortgage servicing assets have retained their 2017 risk weight treatment, which will continue until the federalnot deducted from CET1 capital.

Liquidity Requirements

The Federal banking regulators revise the extended transitional treatment under the November 2017 final rule, which may occur in connection with the finalization of the related September 2017 proposal to simplify the capital treatment of certain DTAs, mortgage servicing assets, significant investments in unconsolidated financial institutions and minority interests.

The U.S. Basel III rules prescribe a standardized approach for risk weighting many categories of assets. These categories generally range from 0% for U.S. government and agency securities, to 600% for certain equity exposures, to 1,250% for certain securitization exposures.

With respect to CBNA, the U.S. Basel III rules also revise the “prompt corrective action” regulations pursuant to Section 38 of the Federal Deposit Insurance Act, as discussed below in “Federal Deposit Insurance Act.”

In December 2017, the Basel Committee published standards that it described as the finalization of the Basel III post-crisis regulatory reforms (the standards are commonly referred to as “Basel IV”). Among other things, these standards revise the Basel Committee’s standardized approach for credit risk (including recalibrating risk weights and introducing new capital requirements for certain “unconditionally cancellable commitments,” such as unused credit card and home equity lines of credit) and provide a new standardized approach for operational risk capital. Under the Basel framework, these standards will generally be effective on January 1, 2022, with an aggregate output floor phasing in through January 1, 2027. Under the current U.S. Basel III rules, operational risk capital requirements and a capital floor apply only to advanced approaches institutions, and not to CFG or CBNA. The impact of Basel IV on CFG and CBNA will depend on the manner in which it is implemented by the FRB and the OCC.

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

Liquidity Requirements

We are currently subject tohave adopted the Basel III-based U.S. LCR rule, which is a quantitative liquidity metric designed to ensure that a covered bank or bank holding company maintains an adequate level of unencumbered high-quality liquid assets to cover expected net cash outflows over a 30-day time horizon under an acute liquidity stress scenario; however, asscenario. As noted above, under the Tailoring NPRs,Rules, Category IV firms with less than $50 billion in wSTWF, including Citizens, wouldus, are no longer be subject to any LCR requirement. The LCR rule currently applies in its most comprehensive form only to advanced approaches bank holding companies (that is, those with $250 billion or more in total consolidated assets or $10 billion or more in on-balance sheet foreign exposures) and depository institution subsidiaries of such bank holding companies with $10 billion or more in total consolidated assets. The LCR rule, following the threshold amendments under EGRRCPA, currently applies in a modified form to bank holding companies such as the Parent Company that have $100 billion or more but less than $250 billion in total consolidated assets and less than $10 billion in total on-balance sheet foreign exposure. The U.S. version of the LCR differs in certain respects from the Basel Committee’s version; the U.S. version includes a narrower definition of high-quality liquid assets, different prescribed cash inflow and outflow assumptions for certain types of instruments and transactions, and a shorter phase-in schedule that began on January 1, 2015 and is now complete. The modified LCR currently requires us to maintain a ratio of high-quality liquid assets to net cash outflows of 70% (compared to 100% in the comprehensive LCR applicable to advanced approaches bank holding companies). At December 31, 2018, our LCR on the modified basis was above the minimum requirement.

Until the changes to the LCR requirement contained in the Tailoring NPRs are adopted, as a modified LCR company, we are required to calculate our LCR on a monthly basis. If a covered company fails to meet the minimum required LCR, it must promptly notify its primary federal banking regulator and may be required to take remedial actions. In December 2016, the FRB issued a final rule that requires bank holding companies currently subject to the LCR rule to disclose publicly, on a quarterly basis, quantitative and qualitative information about certain components of their LCR. For modified LCR bank holding companies, this disclosure requirement began with the fourth quarter of 2018 and is required to be disclosed by March 1, 2019. We will publish the required information on quantitative and qualitative components of our LCR on our regulatory filings and disclosures page on our Investor Relations website at http://investor.citizensbank.com.

The Basel III framework also includes a second liquidity standard, the NSFR, which is designed to promote more medium- and long-term funding of the assets and activities of banks over a one-year time horizon. In May 2016, the federal banking regulators issued a proposed rule that would implement the NSFR for large U.S. banking organizations, including Citizens; however, as noted above, under the Tailoring NPRs, Category IV firms, including Citizens, would not be subject to any NSFR requirement.organizations. Under the 2016 proposal, the most stringent requirements would apply to advanced approaches bank holding companies, and would have required such organizations to maintain a minimum NSFR of 1.0 on an ongoing basis, calculated by dividing the organization’s available stable funding (“ASF”) by its required stable funding (“RSF”). Bank holding companies with $50 billion or more in total consolidated assets but that are not advanced approaches bank holding companies, including Citizens,us, would have been subject to a modified, less stringent NSFR requirement. Although the NSFR has not been finalized, it is expected that the framework for applying any finalized NSFR will be consistent with the approach for the LCR requirement which would have required such bank holding companies to maintain a minimum NSFR of 0.7 on an ongoing basis. Underunder the 2016 proposal, a banking organization’s ASF would have been calculated by applying specified standard weightings to its equity and liabilities based on their expected stability over a one-year time horizon and its RSF would be calculated by applying specified standardized weightings to its assets, derivative exposures and commitments based on their liquidity characteristics over the same one-year time horizon.Tailoring Rules.

Finally, per the liquidity rules included in the FRB’s enhanced prudential standards adopted pursuant to Section 165 of the Dodd-Frank Act (referred to above under “—Financial Regulatory Reform”Tailoring of Prudential Requirements”), we are also required to maintain a buffer of highly liquid assets based on projected funding needs for 30 days. The liquidity buffer is in addition to the federal banking regulators’ LCR rule and is described by the FRB as being “complementary” to the LCR. Under the Tailoring NPRs,Rules, the liquidity buffer requirements forcontinue to apply to Category IV firms, such as Citizens, would not change,us, and Category IV firms would remain subject to liquidity risk management requirements; however,requirements. However, these requirements would beare now tailored such that these firms would bewe required to: (i)

i.calculate collateral positions monthly, as opposed to weekly as is currently required; (ii) weekly;

ii.establish a more limited set of liquidity risk limits than are currentlywas previously required; and (iii)

iii.monitor fewer elements of intraday liquidity risk exposures than were previously monitored.

We are currently monitored. Category IV firms would also benow subject to liquidity stress testing quarterly, rather than monthly, and would beare required to report liquidity data on a monthly basis.

Capital Planning and Stress Testing Requirements

Under the CCAR process, bank holding companiesfinal Tailoring Rules implementing the EGRRCPA, Category IV firms with $100 billion or moreto $250 billion in total consolidated assets, including us, are no longer required to conduct and publicly disclose results of the company-run stress tests and are subject to supervisory stress testing on a two-year rather than an annual basis. Category IV firms continue to be subject to the requirement to submit an annual capital plan that must be reviewed and approved

|

| | |

| | Citizens Financial Group, Inc. | 12 |

by the firm’s Board of Directors (or one of its committees) at least annually, as well as FR Y-14 reporting requirements. In connection with the final Tailoring Rules, the FRB noted that it intends to propose changes to the capital plan rule, including providing firms subject to Category IV standards additional flexibility to develop their annual plans.

In February 2019, the FRB provided relief to a number of BHCs with assets between $100 billion and maintain$250 billion in assets, including us, from certain regulatory requirements related to supervisory stress testing and company-run stress testing, and related disclosure requirements for the 2019 stress test cycle. As a result, we were not required to participate in the supervisory stress test or CCAR, conduct company-run stress tests, or submit a capital plan and to submit the plan to the FRB for review. CCAR is designed to

CITIZENS FINANCIAL GROUP, INC.

BUSINESS

evaluate a bank holding company’s capital adequacy, capital adequacy process and2019. As required, we submitted our planned capital distributions, such as dividend payments and common stock repurchases. As part of CCAR, the FRB evaluates whether a bank holding company has sufficient capital to continue operations under various hypothetical scenarios of economic and financial market stress. These scenarios currently include both bank holding company- and FRB-developed scenarios, including an “adverse” and a “severely adverse” stress scenario (although the FRB, on January 8, 2019, proposed amendments that, among other things, would eliminate the adverse scenario). The FRB also evaluates whether the bank holding company has robust, forward-looking capital planning processes that accounts for the bank holding company’s unique risks.

Due to the importance and intensity of the stress tests and the CCAR process, we have dedicated significant resources to comply with stress testing and capital planning requirements and may continue to do so in the future.