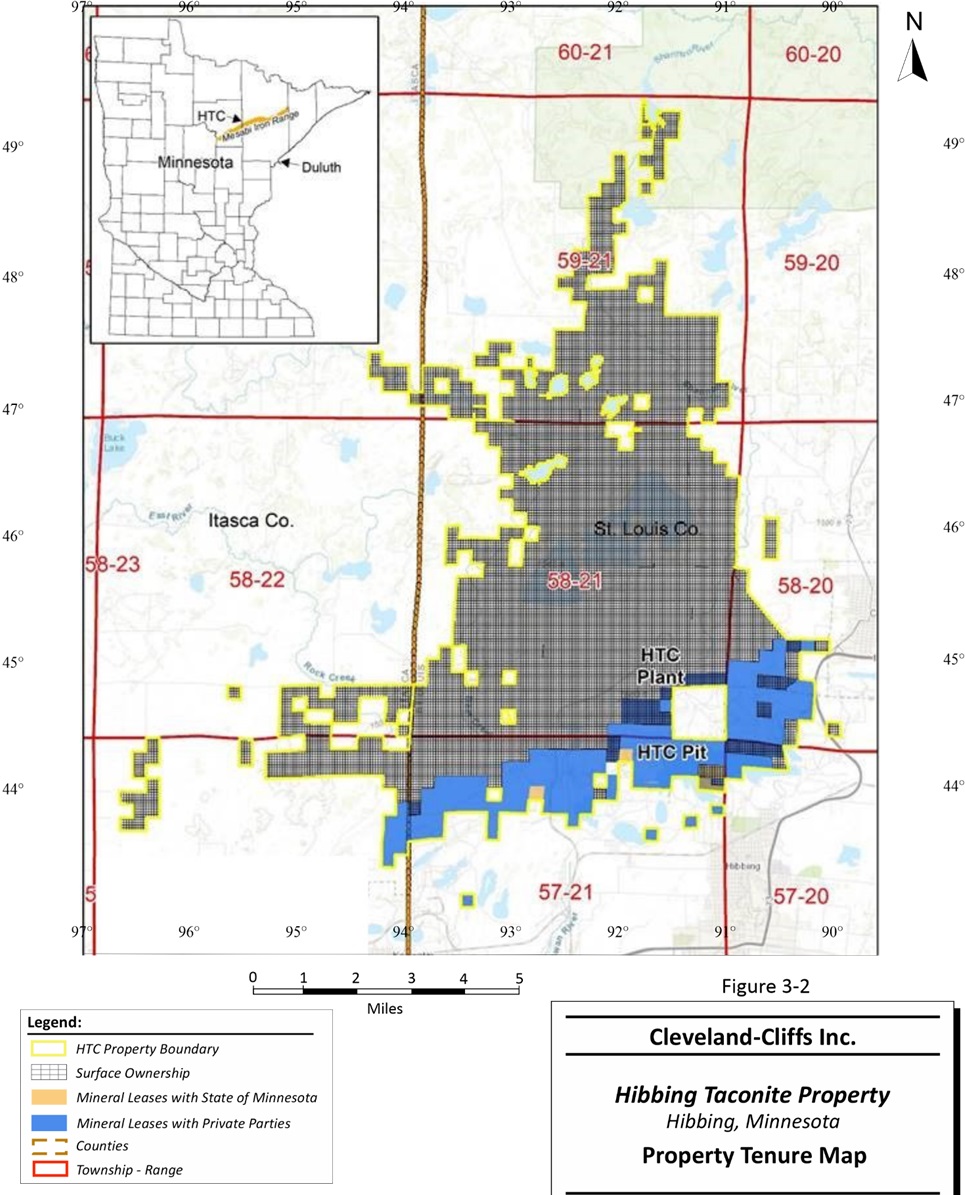

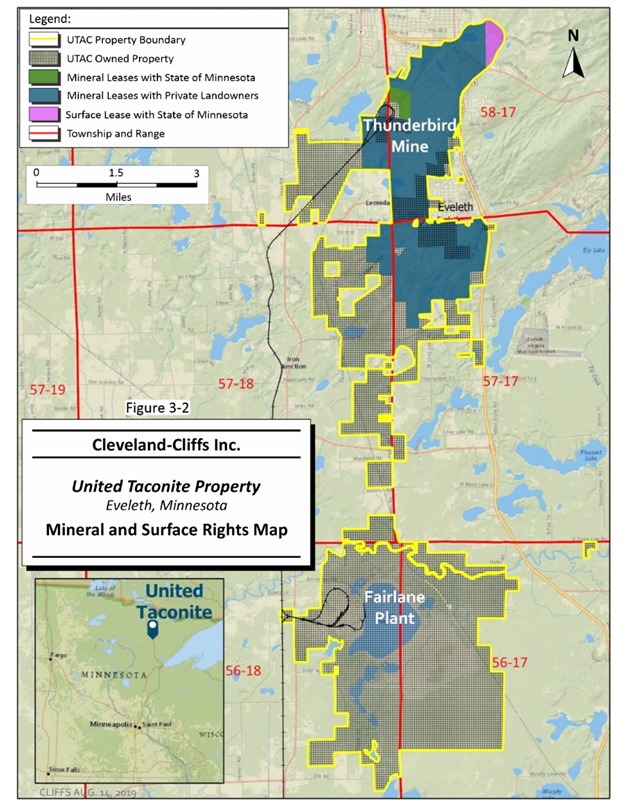

TheUNITED TACONITEUnited Taconite's (100% owned) mine and offices are located on Minnesota's Mesabi Iron Range just north of Eveleth, Minnesota at latitude 47°29'1.62" N, longitude 92°32'23.69" W. The processing facilities are located approximately eight miles to the southeast.

| | | | | |

The property commenced operations as an asset of Eveleth MN at latitude 47°29'1.62" N, longitude 92°32'23.69" W.Taconite Company in 1965 before it was purchased by United Taconite (70% Cliffs and 30% Laiwu Steel) in December 2003. The processing facilities are located approximately eight miles to the southeast. | property has been a wholly owned subsidiary of Cliffs since 2008. United Taconite owns 14,199 acres of surface rights, of which 703 acres are associated with mineral leases. An additional 145 acres of surface rights are leased from the State of Minnesota., We lease 100% of the mineral rights, comprisingcomprised of 4,908 acres expiring between 2037 and 2066, with the exception of the State of Minnesota mineral lease, which expires in 2027. Leases are maintained by making minimum prepaid royalty payments. Mining leases routinely are renegotiated and renewed as they approach their respective expiration dates. | OpenOperations include an open pit truck and shovel mine where two stages of crushing occur before the ore is transported by rail, operated by CN, to the plant site. At the plant site an additional stage of crushing occurs before the ore is sent to the concentrator. The concentrator utilizes rod mills and magnetic separation to produce a magnetite concentrate, which is delivered to the on-site pellet plant. From the plant site, pellets are transported by CN rail to a ship loading port at Duluth, MN,Minnesota, operated by CN. The net book value of United Taconite's property, plant and equipment was $559 million as of December 31, 2023. | The property commenced operations as an asset of Eveleth Taconite Company in 1965 before it was purchased by United Taconite (70% Cliffs and 30% Laiwu Steel) in December 2003. The Property has been a wholly owned subsidiary of Cliffs since 2008. | $567 |

For more information, see Exhibit 96.4, Technical Report Summary on the United Taconite Property, Minnesota, USA, prepared for the Company by the QP, SLR, with an effective date of December 31, 2021.

Mineral ResourcesMINERAL RESOURCES

Mineral resources are defined under Item 1300 of Regulation S-K as a concentration or occurrence of material of economic interest in or on the Earth’s crust in such form, grade or quality, and quantity that there are reasonable prospects for economic extraction. A mineral resource is a reasonable estimate of mineralization, taking into account relevant factors such as cut-off grade, likely mining dimensions, location or continuity that, with the assumed justifiable technical and economic conditions, is likely to, in whole or part, become economically extractable.

A detailed breakdown of the mineral resources exclusive of mineral reserves is presented in the table below. Mineral resources were defined and constrained within open-pit shells, prepared by Cliffs, and based on a US$90.00/WLT pellet price, while meeting defined cut-off grade criteria and existing pellet specifications. All mineral resource estimates were reviewed and validated by the QP, SLR.

The following represents iron ore mineral resources, exclusive of mineral reserves, as of December 31, 2021:2023 and 2022:

| | Iron Ore Mineral Resources | Iron Ore Mineral Resources | Iron Ore Mineral Resources |

as of December 31, 2021 | (In Millions of Long Tons) | | Measured | Indicated | Measured + Indicated | Process | Inferred |

| Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery | Tonnage | % Grade |

| Measured | | | Measured | Indicated | Measured + Indicated | Process | Inferred |

| (In millions of long tons) | | (In millions of long tons) | Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery | Tonnage | % Grade |

| Total Iron Ore | Total Iron Ore | 1,351 | | 22.5 | | 1,483 | | 23.6 | | 2,834 | | 23.1 | | 31% | 420 | | 32.4 | |

| | Michigan | Michigan | — | | — | | 135 | | 35.5 | | 135 | | 35.5 | | 36% | 350 | | 34.7 | |

| Michigan | |

| Michigan | |

| Minnesota | Minnesota | 1,351 | | 22.5 | | 1,348 | | 22.4 | | 2,699 | | 22.4 | | 31% | 70 | | 21.0 | |

| Hibbing1 | |

Hibbing1 | |

Hibbing1 | Hibbing1 | 8 | | 19.2 | | 1 | | 18.7 | | 9 | | 19.2 | | 25% | — | | — | |

| Minorca | Minorca | 484 | | 22.9 | | 317 | | 22.9 | | 801 | | 22.9 | | 33% | 30 | | 21.1 | |

| Northshore | Northshore | 767 | | 22.1 | | 391 | | 22.4 | | 1,158 | | 22.2 | | 26% | 14 | | 19.8 | |

| Tilden | Tilden | — | | — | | 135 | | 35.5 | | 135 | | 35.5 | | 36% | 350 | | 34.7 | |

| United Taconite | United Taconite | 92 | | 23.6 | | 639 | | 22.2 | | 731 | | 22.4 | | 32% | 26 | | 21.5 | |

| 1Hibbing is reported at 85.3% based on our ownership level. | 1Hibbing is reported at 85.3% based on our ownership level. | |

1Hibbing is reported at 85.3% based on our ownership level. | |

1Hibbing is reported at 85.3% based on our ownership level. | |

| Reference point selected is the saleable tons based on the process recovery. | |

| Reference point selected is the saleable tons based on the process recovery. | |

Reference point selected is the saleable tons based on the process recovery. | Process recovery may change based on the required saleable product mix and is reported as wet product percentage. | Mineral resources are estimated using the following cut-off grades: 25% FeT for Tilden hematite; 15% magnetic Fe for Northshore; 16% magnetic Fe for Minorca; 17% magnetic Fe for United Taconite; and 13% magnetic Fe for Hibbing. | | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. |

Mineral resources are reported at a $90.00/LT wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. | | Mineral resources are reported at a $90.00/lt wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. | | Mineral resources are reported at a $90.00/lt wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. |

OurWe did not have any material changes to our mineral resource estimates have not been previously disclosed.resources during 2023. The material assumptions and criteria used for the mineral resource estimates, including but not limited to leases, permits and geotechnical pit design, are covered in more detail in Sections 11 through 13 of the respective Technical Report Summaries filed as Exhibits 96.1 through 96.5 to this Annual Report on Form 10-K.

Mineral ReservesMINERAL RESERVES

Mineral reserves are defined under Item 1300 of Regulation S-K as an estimate of tonnage and grade or quality of indicated and measured mineral resources that, in the opinion of the QP, can be the basis of an economically viable project. More specifically, it is the economically mineable part of a measured or indicated mineral resource, which includes diluting materials and allowances for losses that may occur when the material is mined or extracted.

Proven mineral reserves are defined under Item 1300 of Regulation S-K as the economically mineable part of a measured mineral resource and can only result from conversion of a measured mineral resource. Probable mineral reserves are defined under Item 1300 of Regulation S-K as the economically mineable part of an indicated and, in some cases, a measured mineral resource. All mineral reserves are classified as proven or probable and are supported by LoM plans.

Mineral reserves are based on pricing that does not exceed the three-year trailing average index price of iron pellets adjusted to realized price. We evaluate and analyze, and engage QPs to review and verify, mineral reserves in accordance with our mineral policy and SEC requirements and then complete updated LoM plans. The table below identifies the year in which the latest updated LoM plan was completed.

Mineral reserves estimates for our iron mines are constrained by fully designed open pits developed using three-dimensional modeling techniques. These open pits incorporate design slopes, practical mining shapes and access ramps to assure the accuracy of our mineral reserve estimates. All operations' mineral reserves have been adjusted net of production through year-end 2021.2023. All mineral reservereserves estimates as of December 31, 2021 were reviewed and validated by the QP, SLR.

The following represents iron ore mineral reserves as of December 31, 2021:2023:

| | Iron Ore Mineral Reserves | Iron Ore Mineral Reserves | Iron Ore Mineral Reserves |

as of December 31, 2021 | (In Millions of Long Tons) | | Last LoM Plan | Proven | Probable | Proven & Probable | Process |

| Reserve Analysis | Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery |

| as of December 31, 2023 | | as of December 31, 2023 |

| Last LoM Plan | | | Last LoM Plan | Proven | Probable | Proven & Probable | Process |

| (In millions of long tons) | | (In millions of long tons) | Reserve Analysis | Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery |

| Total Iron Ore | Total Iron Ore | | 638 | | 23.6 | | 1,682 | | 26.6 | | 2,320 | | 25.8 | | 33% | Total Iron Ore | | 539 | | 24.0 | 24.0 | | 1,643 | 1,643 | | 26.4 | 26.4 | | 2,182 | 2,182 | | 25.8 | 25.8 | | 33% | 33% |

| | Michigan | Michigan | | 4 | | 35.3 | | 516 | | 34.7 | | 520 | | 34.7 | | 37% |

| Michigan | |

| Michigan | | | 4 | | 35.3 | | 478 | | 34.7 | | 482 | | 34.7 | | 37% |

| Minnesota | Minnesota | | 634 | | 23.5 | | 1,166 | | 23.0 | | 1,800 | | 23.2 | | 31% | Minnesota | | 535 | | 23.9 | 23.9 | | 1,165 | 1,165 | | 23.0 | 23.0 | | 1,700 | 1,700 | | 23.3 | 23.3 | | 31% | 31% |

| Hibbing1 | |

Hibbing1 | |

Hibbing1 | Hibbing1 | 2021 | 85 | | 18.7 | | 8 | | 18.7 | | 93 | | 18.7 | | 25% | 2021 | 47 | | 18.7 | 18.7 | | 8 | 8 | | 18.7 | 18.7 | | 55 | 55 | | 18.7 | 18.7 | | 26% | 26% |

| Minorca | Minorca | 2021 | 103 | | 23.6 | | 7 | | 25.3 | | 110 | | 23.7 | | 34% | Minorca | 2021 | 86 | | 23.7 | 23.7 | | 7 | 7 | | 25.1 | 25.1 | | 93 | 93 | | 23.8 | 23.8 | | 34% | 34% |

| Northshore | Northshore | 2020 | 303 | | 25.3 | | 519 | | 24.1 | | 822 | | 24.6 | | 29% | Northshore | 2020 | 288 | | 25.3 | 25.3 | | 519 | 519 | | 24.1 | 24.1 | | 807 | 807 | | 24.5 | 24.5 | | 29% | 29% |

| Tilden | Tilden | 2021 | 4 | | 35.3 | | 516 | | 34.7 | | 520 | | 34.7 | | 37% | Tilden | 2021 | 4 | | 35.3 | 35.3 | | 478 | 478 | | 34.7 | 34.7 | | 482 | 482 | | 34.7 | 34.7 | | 37% | 37% |

| United Taconite | United Taconite | 2019 | 143 | | 23.1 | | 632 | | 22.1 | | 775 | | 22.3 | | 33% | United Taconite | 2019 | 114 | | 23.1 | 23.1 | | 631 | 631 | | 22.1 | 22.1 | | 745 | 745 | | 22.3 | 22.3 | | 33% | 33% |

| 1Hibbing is reported at 85.3% based on our ownership level. | 1Hibbing is reported at 85.3% based on our ownership level. | |

1Hibbing is reported at 85.3% based on our ownership level. | |

Reference point selected by the QP is the saleable tons based on the process recovery. | Process recovery may change based on the required saleable product mix and is reported as wet product percentage. | Mineral reserves are estimated using the following cut-off grades: 25% FeT for Tilden hematite; 19% magnetic Fe for Northshore; 16% magnetic Fe for Minorca; 17% magnetic Fe for United Taconite; and 13% magnetic Fe for Hibbing. | | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. | Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. |

| Mineral reserves are classified as probable if not scheduled within the first 20 years. | Mineral reserves are classified as probable if not scheduled within the first 20 years. | Mineral reserves are classified as probable if not scheduled within the first 20 years. |

Mineral reserves are reported at a $90.00/LT wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. | | Mineral reserves are reported at a $90.00/lt wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. | | Mineral reserves are reported at a $90.00/lt wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. |

The material assumptions and criteria used for the mineral reserves estimates, including but not limited to leases, permits and geotechnical pit design, are covered in more detail in Sections 11 through 13 of the respective Technical Report Summaries filed as Exhibits 96.1 through 96.5 to this Annual Report on Form 10-K.

4836 | CLF 2023 FORM 10-K

For comparison purposes, the following represents iron ore mineral reserves as of December 31, 2020: | | | | | | | | | | | | | | | | | | | | | | | |

| Iron Ore Mineral Reserves |

| as of December 31, 2020 |

| (In Millions of Long Tons) |

| Proven | Probable | Proven & Probable | Process |

| Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery |

| Total Iron Ore | 822 | | 26.2 | | 1,596 | | 26.0 | | 2,418 | | 26.0 | | 31% |

| | | | | | | |

| Michigan | 168 | | 35.2 | | 418 | | 34.8 | | 586 | | 34.8 | | 34% |

| Minnesota | 654 | | 23.9 | | 1,178 | | 23.0 | | 1,832 | | 23.3 | | 30% |

| | | | | | | |

Hibbing1 | 65 | | 19.7 | | 21 | | 19.6 | | 86 | | 19.7 | | 27% |

| Minorca | 113 | | 23.6 | | 7 | | 25.3 | | 120 | | 23.7 | | 31% |

| Northshore | 318 | | 25.3 | | 519 | | 24.1 | | 837 | | 24.6 | | 29% |

| Tilden | 168 | | 35.2 | | 418 | | 34.8 | | 586 | | 34.8 | | 34% |

| United Taconite | 158 | | 23.1 | | 631 | | 22.1 | | 789 | | 22.3 | | 31% |

| | | | | | | |

1Hibbing is reported at 85.3% based on our ownership level. |

| Reference point selected was the saleable tons based on the process recovery. |

| Process recovery may change based on the required saleable product mix and is reported as wet product percentage. |

| Mineral reserves are estimated using the following cut-off grades: 25% FeT for Tilden hematite; 19% magnetic Fe for Northshore; 16% magnetic Fe for Minorca; 17% magnetic Fe for United Taconite; and 15% magnetic Fe for Hibbing. |

| Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. |

| Mineral Reserves are classified as probable if not scheduled within the first 20 years. |

| Mineral Reserves are reported at a $90.00/LT wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. |

| | | | | | | | | | | | | | | | | | | | | | | |

| Iron Ore Mineral Reserves |

| as of December 31, 2022 |

| Proven | Probable | Proven & Probable | Process |

| (In millions of long tons) | Tonnage | % Grade | Tonnage | % Grade | Tonnage | % Grade | Recovery |

| Total Iron Ore | 593 | | 23.8 | | 1,665 | | 26.5 | | 2,258 | | 25.8 | | 32% |

| | | | | | | |

| Michigan | 4 | | 35.3 | | 500 | | 34.7 | | 504 | | 34.7 | | 37% |

| Minnesota | 589 | | 23.7 | | 1,165 | | 23.0 | | 1,754 | | 23.2 | | 31% |

| | | | | | | |

Hibbing1 | 67 | | 18.7 | | 8 | | 18.7 | | 75 | | 18.7 | | 26% |

| Minorca | 95 | | 23.7 | | 7 | | 25.1 | | 102 | | 23.8 | | 34% |

| Northshore | 299 | | 25.3 | | 519 | | 24.1 | | 818 | | 24.6 | | 29% |

| Tilden | 4 | | 35.3 | | 500 | | 34.7 | | 504 | | 34.7 | | 37% |

| United Taconite | 128 | | 23.1 | | 631 | | 22.1 | | 759 | | 22.3 | | 33% |

| | | | | | | |

1Hibbing is reported at 85.3% based on our ownership level. |

| Reference point selected by the QP is the saleable tons based on the process recovery. |

| Process recovery may change based on the required saleable product mix and is reported as wet product percentage. |

| Mineral reserves are estimated using the following cut-off grades: 25% FeT for Tilden hematite; 19% magnetic Fe for Northshore; 16% magnetic Fe for Minorca; 17% magnetic Fe for United Taconite; and 13% magnetic Fe for Hibbing. |

| Tonnage is reported in long tons equivalent to 2,240 pounds and has been rounded to the nearest 100,000. |

| Mineral Reserves are classified as probable if not scheduled within the first 20 years. |

| Mineral Reserves are reported at a $90.00/lt wet standard pellet price freight-on-board (FOB) Lake Superior, which is based on the mine planning model's three-year trailing average of the realized product revenue rate. |

Overall, as compared to the mineral reserve estimates as of December 31, 2020, mineral reserves estimates as of December 31, 20212023, as compared to the prior-year period, decreased by 4%3%, which was driven by mining depletion. The mineral reserves of Minorca, Northshore and United Taconite as of December 31, 2021 have decreased mainly due to depletion through mining, the mineral reserves for Tilden as of December 31, 2021 have decreased primarily due to the mine plan changes, and the mineral reserves for Hibbing as of December 31, 2021 have increased primarily due to the mine plan changes.

Internal Controls DisclosureINTERNAL CONTROLS DISCLOSURE

We demonstrated repeated attainment of annual production and quality targets for at least 40 years at each material iron ore mine operated by the Company. Internal controls the Company uses in its industry-standard approach to exploration and mineral resource and reserve estimation efforts are governed by its Mineral Reserve and Mineral Resource Estimation Policy and are detailed in Cliffs’ minimum operating standards for Resource Estimation and Strategic Mine Planning. The controls include: confirmation of drill collar locations and drill hole traces, drill logging and sample collection and security, database verification and security, QA/QC programs, internal and third-party QP statistical analysis, third-party QP model validation, and reconciliation. Modeling and analysis of the Company’s resources has been developed by Company personnel or third-party consultant SLR and reviewed by internal management and the external independent QP, SLR. Reserve estimations have been completed by Company personnel and reviewed by internal management and the QP, SLR.

Drill hole collar surveying methods have evolved with advancements in technology, moving from optical methods to global positioning system, which is currently in use. For the deposit type, all survey methods used for the collar locations are expected to provide adequate accuracy for the drill hole locations. Due to the relatively shallow depth and vertical nature of drill holes at Cliffs’ Minnesota mining operations, downhole deviation surveys are typically not conducted. Drill holes pierce the generally shallow-dipping, tabular iron formation at near perpendicular angles. At the more geologically and structurally complex Tilden mine in Michigan, where drilling deeper than 500 feet is required, downhole surveys have moved from a clay-impression procedure to the gyroscopic method currently in use.

Drill core is transported directly from the drill rig to each site’s core logging facility by either the drilling contractor or Cliffs’ personnel. Temporary core storage is located at each site’s secure logging facility. Depending on the mining operation, unused sample reserves, parts, concentrates and splits are securely stored in labeled boxes or barrels at a Cliffs laboratory facility or logging facility, or via a contracted external laboratory.

CliffsCliffs' QA/QC programs are site-specific and range from in-development to well-developed, long standing protocols that involve formal procedures for the use of crude material standards developed from on-site material, as well as regularly inserted coarse and concentrate duplicate samples, control chart analysis and reporting. Cliffs typically uses internal and external labs for geometallurgical analyses that are accredited with ASQ/ANSI ISO-9001:2015 (American Society for Quality/American National Standards Institute) for their system of quality management. Quality sample results are monitored and enacted on where warranted. Also, Cliffs has implemented a drill campaign reporting practice to ensure results are documented, with defined and illustrated failure metrics, outcomes of investigations, comparisons with previous year’s results and recommendations. The QP, SLR, reviewed CliffsCliffs' QA/QC practices and provided recommendations for further work. Where QA/QC programs are still in

development and prior to resource estimation, Cliffs conducted data verification studies utilizing a suite of blind crude ore standards and blind duplicates from historical sample reserves within the LoM plan. Where unaccredited labs provided data used in resource estimation, check lab studies were initiated to verify analytical results. Cliffs is currently working towardstoward aligning QA/QC protocols at each mine to the Company’s current best practice.

Cliffs maintains exploration drill hole data in an externally-managed, access-controlled acQuire database that is backed up online at regularly scheduled intervals to provide data redundancy and security. Certification of database integrity is accomplished by both visual and statistical inspections comparing geology, assay values and survey locations cross-referenced back to laboratory data and geologic logs. Any discrepancies identified are corrected by referring to hard-copy assay and core log information archived in Cliffs' Mine Engineering department file cabinets.files. Prior to modeling, a secondary validation check is completed using built-in data validation routines in the modeling software.

Cliffs performs routine drill hole database verification with every new drilling program and new block model build, including: check of unique drill hole IDsidentifications and collar coordinates; check of assay or lithology points extending past the specified maximum depth of drill hole; check of abnormal dips and azimuths of downhole drill hole surveys; check of negative, overlapping and missing intervals; and check of incorrect lithologic codes and assay values.

In 2020 and 2021, CliffsCliffs' geologists completed data verification exercises within the LoM plan area for each mining operation. This was audited by the QP, SLR, to assess accuracy and completeness. Database values were checked against source documents including collar surveys, geologic logs and assay certificates. Data verification included collar coordinates, depth intervals of geologic units and assay samples, and results of geometallurgical analyses applied to mineral resource estimation and mine planning.

Cliffs’ mineral resource estimates were validated by the QP, SLR, using standard industry techniques including statistical comparisons with composite samples and parallel nearest neighbor estimates, swath plots, as well as visual reviews in cross-section and plan. A visual review comparing blocks to drill holes for key economic variables, completed after the block modeling work, was performed to ensure general lithologic and analytical conformance. Cliffs’ mining operations have demonstrated good agreement between planned and actual product produced over more than 40 years for each operation.

Cliffs classifies the mineral resources based primarily on drill hole spacing and influenced by geologic continuity, ranges of economic criteria and reconciliation. Some post-processing is undertaken to ensure spatial consistency and remove isolated and fringe blocks. The resource area for each operation is limited by a polygon and subsequent pit shell based on practical mining limits. To ensure that all mineral resource statements satisfy the “reasonable prospects for economic extraction” requirement, in the definition of the mineral resources under Item 1300 of Regulation S-K, factors significant to technical feasibility and potential economic viability are considered (e.g., ability to obtain permits and legal and land tenure considerations). Mineral resources are defined and constrained within optimized, open-pit shells, prepared by Cliffs and reviewed by the QP, SLR, and based on a US$90.00/WLT pellet value and target pellet iron content.

Grade and tonnage reconciliations are run on current production versus modeled production, which provides insight on the accuracy of the modeled assay data versus actual production for each mining operation.

For a discussion of comprehensive risk inherent in the estimation of mineral reserves, see Part I - Item 1A,1A. Risk Factors - V. Sustainability and Development Risks - We rely on estimates of our recoverable mineral reserves, which isare complex due to the geological characteristics of the properties and the number of assumptions made.

Coal Mining and CokemakingCOAL MINING AND COKEMAKING

Princeton is a coal mining complex located in West Virginia that specializes in surface and underground mining of metallurgical coal to produce coke and pulverized coal injection coal. WeAs of December 31, 2023, we have annual rated metallurgical coal production capacity of 2.31.8 million net tons from our Princeton mine. In 2021,During the years ended December 31, 2023 and 2022, the mine produced 1.41.3 million and 1.5 million net tons of coal.coal, respectively. We own 100% of the Princeton mine, which has been operating since 1995. We own 52%60% of the mineral rights and lease 48%40% via multiple mineral leases having varying expiration dates. Mining leases routinely are renegotiated and renewed as they approach their respective expiration dates. Princeton's operations consist of twothree open-pit surface mines, two underground mines, a preparation plant and two rail loadouts.

In 2021, our cokemakingOur Monessen and Warren facilities produced 2.9 million net tons of coke. Mountain State Carbon produces furnace coke and related by-products from its plant in Follansbee, West Virginia, which consists of four batteries. Monessen producesproduce furnace coke and related by-products in Monessen, Pennsylvania which was temporarily idled due to the COVID-19 pandemic and restarted production during the third quarter of 2021. Warren produces furnace coke and related by-products from its plant in Warren, Ohio, and supplies its coke to the Cleveland facility.respectively. We also operate a cokemaking facilitiesfacility located within Burns HarborHarbor. These facilities have an aggregate annual rated capacity of 2.6 million net tons. During the years ended December 31, 2023 and Middletown Works.

As a result of2022, our internal usage of HBI, coupled with our ongoing evaluationcokemaking facilities produced 2.4 million and 2.1 million net tons of coke, use strategies, we idled our coke facility at Middletown Works during the third quarter of 2021, and we intend to permanently idle our Mountain State Carbon coke plant in the second quarter of 2022.respectively.

Other BusinessesOTHER BUSINESSES

Our Tubular operating segment consists of our subsidiary Tubular Components, which has plants in Walbridge, Ohio and Columbus, Indiana. The Walbridge plant operates six electric resistance welded tube mills.mills on owned property. The Columbus plant operates five electric resistance welded tube mills and four high-speed cold saws on leased property. Tubular Components shut down and ceased tube production at the Queretaro, Mexico plant in April 2021. The high-speed cold saw that was operating at the Queretaro plant was relocated to the Columbus plant and the tube mill returned to the U.S. is replacing an existing, older tube mill currently in operation.

Our Tooling and Stamping operating segment consists of our subsidiary Tooling and Stamping and its related companies, which provides advanced-engineered solutions, tool design and build, hot- and cold-stamped steel components and complex assemblies for the automotive market across ten plants, of which certain of these are under long-term lease agreements, in Ontario, Alabama, Kentucky and Kentucky.Tennessee. Its facilities feature seveneight large-bed, hot-stamping presses, providing 1314 lines of production; 8182 cold-stamping presses ranging from 150 net tons to 3,000 net tons of pressing capacity; 1718 large-bed, high-tonnage tryout presses with

prove-out capabilities for new tool builds; and 149151 multi-axis welding assembly cells. Construction

Our European operating segment consists of our new facility in Tennessee is substantially completea metal distribution company that buys and sells steel, steel products and other materials. We operate out of six different European countries: the Netherlands, Italy, Germany, France, Spain and the facility began producing prototype components in the third quarter of 2021. Commercial start of production at the Tennessee location is expected to begin in the second quarter of 2022.United Kingdom.

| | |

| | |

ItemITEM 3. | Legal Proceedings LEGAL PROCEEDINGS |

Legal Proceedings Relating to our BusinessLEGAL PROCEEDINGS RELATING TO OUR BUSINESS

JSW Steel Litigation. On June 8, 2021, JSW Steel filed a complaint against Cleveland-Cliffs Inc., AK Steel Holding Corporation (now known as Cleveland-Cliffs Steel Holding Corporation), Nucor Corporation and U.S. Steel in the United States District Court for the Southern District of Texas. JSW Steel alleges that the defendants engaged in a group boycott against JSW Steel in violation of federal and Texas antitrust laws by refusing to sell semi-finished steel slabs to JSW Steel, beginning in 2018 and continuing through the present; civil conspiracy among the defendants; and tortious interference with JSW Steel’s contractual rights and business relations involving its vendors and customers. JSW Steel’s allegations involve the tariffs and quotas imposed on steel imports by the U.S. government under Section 232 beginning in March 2018, which JSW Steel alleges raised the price of imported slabs, and statements made to the U.S. government related to exemption requests submitted by JSW Steel in 2018 and 2021. JSW Steel further claims that this alleged anticompetitive conduct negatively impacted JSW Steel’s costs, production and revenues and prevented it from pursuing expansion plans at its Ohio and Texas facilities that would compete with the defendants. JSW Steel is seeking to hold the defendants jointly and severally liable for treble damages in an amount in excess of $500 million and other relief. We filed a MotionOn February 17, 2022, the district court granted the defendants' Motions to Dismiss in their entirety and dismissed all of JSW's claims with prejudice. On March 16, 2022, JSW filed a notice of appeal to the case during 2021,United States Court of Appeals for the Fifth Circuit, and discovery remains stayed untiloral arguments on the court decides our motion.appeal were held on February 6, 2023. We continue to believe the claims asserted against us are without merit, and we are vigorously defending against them.

Mesabi Metallics Adversary Proceeding. On September 7, 2017, Mesabi Metallics Company LLC (f/k/a Essar Steel Minnesota LLC) ("Mesabi Metallics") filed a complaint against Cleveland-Cliffs Inc. in the Essar Steel Minnesota

LLC and ESML Holdings Inc. bankruptcy proceeding that is pending in the United States Bankruptcy Court, District of Delaware. Mesabi Metallics alleges tortious interference with its contractual rights and business relations involving certain vendors, suppliers and contractors, violations of federal and Minnesota antitrust laws through monopolization, attempted monopolization and restraint of trade, violation of the automatic stay, and civil conspiracy with unnamed Doe defendants. Mesabi Metallics amended its complaint to add additional defendants, including, among others, our subsidiary, Cleveland-Cliffs Minnesota Land Development Company LLC ("Cliffs Minnesota Land"), and to add additional claims, including avoidance and recovery of unauthorized post-petition transfers of real estate interests, claims disallowance, civil contempt and declaratory relief. Mesabi Metallics seeks, among other things, unspecified damages and injunctive relief. Cliffs and Cliffs Minnesota Land filed counterclaims against Mesabi Metallics, Chippewa Capital Partners ("Chippewa"), and Thomas M. Clarke ("Clarke") for tortious interference and civil conspiracy, as well as additional claims against Chippewa and Clarke for aiding and abetting tortious interference, for which we seek, among other things, damages and injunctive relief. Our counterclaim against Clarke for libel was dismissed on jurisdictional grounds. The parties filed various dispositive motions on certain of the claims, including a motion for partial summary judgment to settle a dispute over real estate transactions between Cliffs Minnesota Land and Glacier Park Iron Ore Properties LLC ("GPIOP"). A ruling in favor of Cliffs, Cliffs Minnesota Land and GPIOP was issued on July 23, 2018, finding that Mesabi Metallics' leases had terminated and upholding Cliffs' and Cliffs Minnesota Land's purchase and lease of the contested real estate interests. Mesabi Metallics filed a Motion for Leave to File an Interlocutory Appeal, which was denied on September 10, 2019. Discovery is ongoing.has been completed, and we have filed for summary judgment on all claims that Mesabi Metallics has asserted against us. Mesabi Metallics, Chippewa and Clarke have also filed for summary judgment on various claims and issues in the case. We believe the claims asserted against us are without merit, and we intend to continue to vigorously defend against anyall remaining claims in the lawsuit.

Certain Legacy Legal Proceedings Relating to our Steel Operations. Certain of our acquired subsidiaries have been named as defendants, among many other named defendants, in numerous lawsuits filed since 1990 claiming injury allegedly resulting from exposure to asbestos. Similar lawsuits seeking monetary relief continue to be filed in various jurisdictions in the U.S., which cases are vigorously defended. Although predictions about the outcome of pending litigation is subject to uncertainties, based upon present knowledge, we believe it is unlikely that the resolution in the aggregate of these claims will have a materiallymaterial adverse effect on our consolidated results of operations, cash flows or financial condition.

Legal Proceedings Relating to Environmental MattersLEGAL PROCEEDINGS RELATING TO ENVIRONMENTAL MATTERS

SEC regulations require us to disclose certain information about administrative or judicial proceedings involving the environment and to which a governmental authority is a party if we reasonably believe that such proceedings may result in monetary sanctions above a stated threshold. Pursuant to SEC regulations, we use a threshold of $1 million for purposes of determining whether disclosure of any such proceedings is required. We believe that this threshold is reasonably designed to result in disclosure of any such proceedings that are material to our business or financial condition.

Information for this item relating to certain other environmental proceedings may be found under the heading Burns Harbor Water Issues Issues.in NOTE 20 - COMMITMENTS AND CONTINGENCIES In August 2019, ArcelorMittal Burns Harbor LLC (n/k/a Cleveland-Cliffs Burns Harbor LLC) suffered a loss of the blast furnace cooling water recycle system, which led to the discharge of cyanide and ammonia in excess of the Burns Harbor plant's NPDES permit limits. Since that time, the facility has taken numerous steps to prevent recurrence and maintain compliance with its NPDES permit. We engaged in settlement discussions with the U.S. Department of Justice, the EPA and the State of Indiana to resolve any alleged violations of environmental laws or regulations arising out of the August 2019 event. Later

stages of the settlement discussions included the Environmental Law and Policy Center (ELPC) and Hoosier Environmental Council (HEC), which had filed a lawsuit on December 20, 2019 in the U.S. District Court for the Northern District of Indiana alleging violations resulting from the August 2019 event and other Clean Water Act claims. On February 14, 2022, the United States and the State of Indiana filed a complaint and a proposed consent decree, and on April 21, 2022, the United States, with the consent of all of the parties, filed a motion seeking final approval of the consent decree from the court. The consent decree was approved by the court with an effective date of May 6, 2022. The consent decree requires specified enhancements to the mill's wastewater treatment systems and required us to pay a $3 million civil penalty, along with other terms and conditions. Other parties to the consent decree include the United States, the State of Indiana, ELPC and HEC. The ELPC/HEC civil litigation was dismissed with prejudice on May 12, 2022. In addition, ArcelorMittal Burns Harbor LLC was served with a subpoena on December 5, 2019, from the United States District Court for the Northern District of Indiana, relating to the August 2019 event. We responded to the subpoena requests, including follow-up requests, and we have been informed that the government has now closed its investigation. With the resolution of monetary sanctions and injunctive relief requirements under the consent decree, we do not believe that the costs to resolve any other third-party claims that arise out of the August 2019 event, including natural resource damages claims pending final resolution, are likely to have, individually or in the aggregate, a material adverse effect on our consolidated financial statements in Part II – Item 8. Financial Statements and Supplementary Data, which information is incorporated herein by reference.condition, results of operations or cash flows.

| | |

| | |

ItemITEM 4. | Mine Safety Disclosures MINE SAFETY DISCLOSURES |

We are committed to protecting the occupational health and well-being of each of our employees. Safety is one of our core values and we strive to ensure that safe production is the first priority for all employees. Our internal objective is to achieve zero injuries and incidents across the Company by focusing on proactively identifying needed prevention activities, establishing standards and evaluating performance to mitigate any potential loss to people, equipment, production and the environment. We have implemented intensive employee training that is geared toward maintaining a high level of awareness and knowledge of safety and health issues in the work environment through the development and coordination of requisite information, skills and attitudes. We believe that through these policies, we have developed an effective safety management system.

Under the Dodd-Frank Act, each operator of a coal or other mine is required to include certain mine safety results within its periodic reports filed with the SEC. As required by the reporting requirements included in §1503(a) of the Dodd-Frank Act and Item 104 of Regulation S-K, the requiredinformation concerning mine safety results regarding certain mining safety and health or other regulatory matters for each of our mine locations that are covered under the scope of the Dodd-Frank Act areis included in Exhibit 95 of Part IV – Item 15. Exhibits and Financial Statement Schedules of this Annual Report on Form 10-K.

5240 | CLF 2023 FORM 10-K

PART II

| | |

| | |

ItemITEM 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Stock Exchange InformationSTOCK EXCHANGE INFORMATION

Our common shares (ticker symbol CLF) are listed on the NYSE.NYSE (New York Stock Exchange).

HoldersHOLDERS

At February 10, 2022,8, 2024, we had 2,5322,526 shareholders of record.

Shareholder Return PerformanceSHAREHOLDER RETURN PERFORMANCE

The following graph shows changes over the past five-year period in the value of $100 invested in: (1) Cliffs' common shares; (2) S&P 500 Index; (3) S&P SmallCap 600Metals and Mining Select Industry Index; and (4) S&P MidCap 400 Index; and (5) S&P Metals and Mining Select Industry Index. Due to the increased market capitalization of the Company, we were included within the S&P MidCap 400 Index and removed from the S&P SmallCap 600 Index during the year ended December 31, 2021. The values of each investment are based on price change plus reinvestment of all dividends reported to shareholders, based on monthly granularity.

| | 2016 | | 2017 | | 2018 | | 2019 | | 2020 | | 2021 |

| | | 2018 | | | | | 2018 | | 2019 | | 2020 | | 2021 | | 2022 | | 2023 |

| Cleveland-Cliffs Inc. | Cleveland-Cliffs Inc. | Return % | | — | | | (14.27) | | 6.66 | | 12.60 | | 77.46 | | 49.52 |

| Cum $ | | 100.00 | | 85.73 | | 91.44 | | 102.96 | | 182.71 | | 273.19 |

| Cumulative $ | | | Cumulative $ | | 100.00 | | 112.60 | | 199.82 | | 298.77 | | 221.09 | | 280.23 |

| S&P 500 Index | S&P 500 Index | Return % | | — | | | 21.80 | | (4.39) | | 31.48 | | 18.39 | | 28.68 |

| Cum $ | | 100.00 | | 121.80 | | 116.45 | | 153.11 | | 181.27 | | 233.25 |

| S&P SmallCap 600 Index | Return % | | — | | | 13.15 | | (8.52) | | 22.74 | | 11.24 | | 26.74 |

| Cum $ | | 100.00 | | 113.15 | | 103.51 | | 127.05 | | 141.33 | | 179.12 |

| Cumulative $ | | | Cumulative $ | | 100.00 | | 131.48 | | 155.66 | | 200.30 | | 163.99 | | 207.05 |

| S&P Metals and Mining Select Industry Index | |

| Cumulative $ | | | Cumulative $ | | 100.00 | | 114.70 | | 133.02 | | 179.50 | | 203.05 | | 246.73 |

| S&P MidCap 400 Index | S&P MidCap 400 Index | Return % | | — | | | 16.23 | | (11.10) | | 26.17 | | 13.65 | | 24.73 |

| Cum $ | | 100.00 | | | 116.23 | | 103.33 | | 130.37 | | 148.16 | | 184.80 |

| S&P Metals and Mining Select Industry Index | Return % | | — | | | 20.61 | | (26.76) | | 14.70 | | 15.97 | | 34.94 |

| Cum $ | | 100.00 | | 120.61 | | 88.33 | | 101.32 | | 117.50 | | 158.56 |

| Cumulative $ | | | Cumulative $ | | 100.00 | | | 126.17 | | 143.39 | | 178.85 | | 155.42 | | 180.89 |

5341 | CLF 2023 FORM 10-K

Issuer Purchases of Equity Securities

The following table presents information with respect to repurchases by the Company of our common shares during the periods indicated:

ISSUER PURCHASES OF EQUITY SECURITIES

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Period | | Total Number of Shares (or Units) Purchased1 | | Average Price Paid per Share

(or Unit) | | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet be Purchased Under the Plans or Programs2 |

| October 1 - 31, 2021 | | 534 | | | $ | 19.66 | | | — | | | $ | — | |

| November 1 - 30, 2021 | | — | | | — | | | — | | | — | |

| December 1 - 31, 2021 | | — | | | — | | | — | | | — | |

| Total | | 534 | | | $ | 19.66 | | | — | | | $ | — | |

| | | | | | | | |

1 All shares were delivered to us to satisfy tax withholding obligations due upon the vesting or payment of stock awards. |

2 On February 10, 2022, our Board of Directors authorized a program to repurchase our outstanding common shares in the open market or in privately negotiated transactions, which may include purchases pursuant to Rule 10b5-1 plans or accelerated share repurchases, up to a maximum of $1 billion. We are not obligated to make any purchases, and the program may be suspended or discontinued at any time. The share repurchase program does not have a specific expiration date. |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Period | | Total Number of Shares (or Units) Purchased1 | | Average Price Paid per Share

(or Unit) | | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet be Purchased Under the Plans or Programs2 |

| October 1 - 31, 2023 | | 7,796 | | | $ | 18.33 | | | — | | | $ | 608,285,509 | |

| November 1 - 30, 2023 | | 3,165 | | | 16.79 | | | — | | | 608,285,509 | |

| December 1 - 31, 2023 | | 601 | | | 17.30 | | | — | | | 608,285,509 | |

| Total | | 11,562 | | | $ | 17.85 | | | — | | | |

| | | | | | | | |

1 All shares were delivered to us to satisfy tax withholding obligations due upon the vesting or payment of stock awards. |

2 On February 10, 2022, our Board of Directors authorized a program to repurchase our outstanding common shares in the open market or in privately negotiated transactions, which may include purchases pursuant to Rule 10b5-1 plans or accelerated share repurchases, up to a maximum of $1 billion. We are not obligated to make any purchases, and the program may be suspended or discontinued at any time. The share repurchase program does not have a specific expiration date. |

| | |

| | |

ItemITEM 6. | [Reserved] [Reserved] |

| | |

| | |

ItemITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Management's Discussion and Analysis of Financial Condition and Results of Operations is designed to provide a reader of our financial statements with a narrative from the perspective of management on our financial condition, results of operations, liquidity and other factors that may affect our future results. The following discussion should be read in conjunction with the consolidated financial statements and related notes that appear in Part II – Item 8. Financial Statements and Supplementary Data of this Annual Report on Form 10-K.

Overview

OVERVIEW

Throughout 2023, we continued to position the Company for long-term success as wellwe had record steel shipments, with particular strength in automotive; significantly reduced our operational costs with greater emphasis on throughput and productivity; dramatically improved our balance sheet; reached our stated net debt target of $3.0 billion; returned substantial capital to shareholders through share repurchases; and continued to focus on our goal of reducing GHG emissions, all with an eye toward the future and in line with our consistent strategic objectives. As of December 31, 2023, we have a record level of liquidity of $4.5 billion. Our strong balance sheet and operational achievements further strengthens our position as an American leader in the immediate benefitssteel industry as we continue to create value for all stakeholders of the transformational acquisitions we completed in 2020 were on full display during the year as we achieved these phenomenal results. Our commercial actions, along with a healthy demand environment for steel, drove substantially higher selling prices for the majorityCompany.

2023 HIGHLIGHTS

•Net income of products we sell, and we adjusted production to meet the needs of our order book. Combined with this, we believe we were able to manage costs better than our peers due to our vertically integrated footprint, which reduces the impact of material price inflation on our major cost inputs. As a result, we produced record revenues, record net income, record $450 million

•Adjusted EBITDA of $1.9 billion

•Revenues of $22 billion and third consecutive year of revenues over $20 billion

•Significantly reduced unit costs year-over-year

•Record steel shipments of 16.4 million net tons

•Record automotive shipments

•Reduced total outstanding long-term debt by $1.1 billion to $3.2 billion

•Net debt of $2.9 billion below stated target of $3.0 billion and lowest net debt level since becoming a steel company

•Reached record operating cash flow in 2021.

The HRC index averaged $1,573 per net ton for 2021, a record year that was also 174% higher than 2020. The record prices for steel products in 2021 resulted from both supply and demand factors, each driven by a rapid recovery from the impactsliquidity of the COVID-19 pandemic. Stay-at-home mandates and fiscal stimulus drove strong demand for consumer goods, such as HVAC products and appliances. Demand from machinery and equipment producers has also been robust. The demand for light vehicles was also strong; however, automotive supply chain difficulties have limited the demand for steel from automotive manufacturers. On the supply side, spot steel availability was limited throughout the year.

We expect healthy demand to continue into 2022 as we start to see the impacts of the Infrastructure and Jobs Act of 2021, growing environmentally-focused capital projects, healthy economic conditions and pent-up automotive demand, as supply chain issues begin to show signs of waning. With strong demand and steel prices in the U.S. reaching all-time highs in 2021, we were well positioned to negotiate our fixed price contracts, which represent approximately 45% of our volumes, at favorable levels, which should enable us to deliver strong financial results and free cash flow in 2022, even if HRC pricing falls considerably.$4.5 billion

5442 | CLF 2023 FORM 10-K

As•Returned $152 million in capital to shareholders through share repurchase program

•Net pension and OPEB liabilities of $586 million are lowest since becoming a resultsteel company

•Successfully implemented Cliffs H surcharge for steel melted with HBI

•Continued focus on our goal of our healthy free cash flow in 2021, we were able to complete several strategic and financial transactions, including the FPT Acquisition. FPT is onereducing GHG emissions

•Secured award of the largest processors of prime scrap in the country, representing approximately 15% of the entire U.S. merchant market. We believe this acquisition is a complementary addition to our footprint, as prime scrap demandNashwauk state mineral leases, which is expected to grow with new flat-rolled EAF capacity set to come online over the next five years and as the worldwide focus on decarbonization continues. We expect to be able to leverage our long-standing flat-rolled automotive and other customer relationships into recycling partnerships to further grow our prime scrap presence. Additionally, FPT allows us to optimize productivity at our existing EAFs and BOFs and furthers our commitment to environmentally-friendly, low-carbon intensity steelmaking with a cleaner materials mix.

Another use of our robust cash flow was the complete redemption of our Series B Participating Redeemable Preferred Stock for $1,343 million during the third quarter of 2021. This transaction reduced our diluted share count by approximately 10%, providing a meaningful return to our shareholders. During February 2021, we executed a series of favorable debt and equity capital market transactions in an effort to extend our average debt maturity profile and increase our ratio of unsecured debt to secured debt. We also completedprovide additional financing transactions, including the redemption of all $396 million aggregate principal amount of our 5.750% 2025 Senior Notes in June 2021, and provided notice of our election to redeem all remaining $294 million aggregate principal amount of our 1.500% 2025 Convertible Senior Notes in December 2021, which was completed in January 2022.

In 2021, we reached full run-rate nameplate annual capacity at our state-of-the-art direct reduction plant in Toledo, Ohio. This facility produces high-quality HBI and is the first of its kind in the Great Lakes region. While we originally expected to be a merchant seller of HBI, following the 2020 Acquisitions, we have instead maximized the value of our HBI by utilizing it primarily in our blast furnaces, which allows us to improve costs and productivity while reducing our coke rates and reducing our carbonlong-term iron ore reservesemissions. As a result of our internal usage of HBI, coupled with our ongoing evaluation of coke use strategies, we idled our coke facility at Middletown Works in 2021 and we intend to permanently idle our Mountain State Carbon coke plant in 2022.

Along with these notable accomplishments, we have been able to continue successfully navigating through the COVID-19 pandemic while preserving the health and safety of both our workforce and our Company for the long term. The health and safety of our employees has always been our top priority. In an effort to best protect our workforce and our Company, we launched a vaccine incentive program in July 2021 that was developed in partnership with our labor unions. Throughout the 45 days the program was in place, the vaccination rate more than doubled, and we achieved a total vaccination rate of over 75% throughout our workforce. The initiative resulted in a payout of $45 million in total cash incentives to our vaccinated workforce. The successful vaccination program allowed us to operate efficiently and safely throughout the remainder of 2021 and into 2022.

We also continued our best practices from both a safety and environmental standpoint. During 2021,2023, our safety TRIRTotal Reportable Incident Rate (including contractors) was 1.371.22 per 200,000 hours worked. Throughout 2021,2023, we made continued progress towardsto focus on our goal of reducing GHG emissions with our increased usageoptimal utilization of HBI and scrap inthroughout our facilities, as well as more efficient power generation through recycling of gases at certain facilities.off-gases. We arehave also partneringcontinued our partnership with the U.S. Department of EnergyDOE as part of the Better Climate Challenge initiative, which was established in December 2021. We continue to pursue opportunities such as we aim to build oncarbon capture and the use of hydrogen within our GHG emission reduction progress.

Recent Developments

Acquisition of FPT

On November 18, 2021, we completed the acquisition of FPT, a leading prime ferrous scrap processor infacilities. With the U.S. These operations consistgovernment awarding funding for the development of 22 scrap processingregional hydrogen hubs throughout the country, including near our largest facilities, primarily inwe expect to dramatically increase our use of hydrogen gas as both a reducing agent and energy source as the Midwest regionclean hydrogen production facilities come online. Additionally, we have continued forming partnerships to develop renewable and clean energy sources - such as wind, solar and hydrogen - which will benefit our own environmental footprint while combating the global impacts of the U.S. Refer to NOTE 3 - ACQUISITIONS for additional information.climate change.

Financing TransactionsFINANCIAL SUMMARY

On December 1, 2021, we issued a notice of redemption for all $294 million in aggregate principal amount outstanding of the 1.500% 2025 Convertible Senior Notes. The 1.500% 2025 Convertible Senior Notes were redeemed on January 18, 2022, through a combination settlement, with the aggregate principal amount of $294 million paid in cash, and 24 million common shares delivered to noteholders, with a fair value of $499 million in settlement of the premium due per the terms of the indenture, plus cash in respect of the accrued and unpaid interest of the 1.500% 2025 Convertible Senior Notes to, but not including, the redemption date per the terms of the indenture.

On December 17, 2021, we entered into the Third ABL Amendment. The Third ABL Amendment modified our ABL Facility to, among other things, increase the amount of tranche A revolver commitments available thereunder by an additional $1 billion and exchange $150 million of tranche B revolver commitments available thereunder for tranche

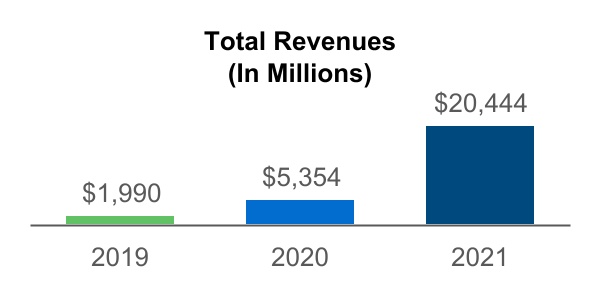

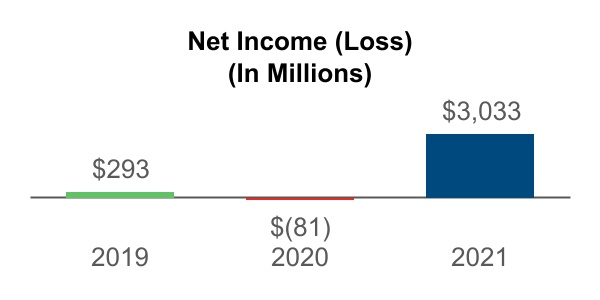

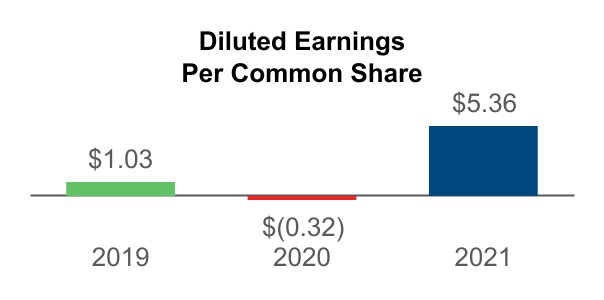

A revolver commitments. After giving effect to the Third ABL Amendment, the aggregate principal amount of tranche A revolver commitments under our ABL Facility is $4.5 billion and there are no longer any tranche B revolver commitments. This action increased our liquidity by $1.0 billion. The increasefollowing is a resultsummary of a larger projected borrowing base driven by more favorable market conditions.our consolidated results for the years ended December 31, 2023, 2022 and 2021 (in millions, except for diluted EPS):

Share Repurchase Program | | | | | | | | | | | | | | | | | | | | |

| Total Revenue | | Net Income | | Adjusted EBITDA | | Diluted EPS |

On February 10, 2022, our Board of Directors authorized a program to repurchase our outstanding common shares in the open market or in privately negotiated transactions, which may include purchases pursuant to Rule 10B5-1 plans or accelerated share repurchases, up to a maximum of $1 billion. We are not obligated to make any purchases and the program may be suspended or discontinued at any time. The share repurchase program does not have a specific expiration date.

Results of Operations

Overview

Our total revenues, net income (loss), diluted EPS and Adjusted EBITDA were as follows:

See "— Results of Operations — Adjusted EBITDA"Non-GAAP Financial Measures" below for a reconciliation of our Net Income (loss)income to Adjusted EBITDA.

ECONOMIC OVERVIEW

STEEL MARKET OVERVIEW

Steel market conditions in 2023 were marked by notable volatility, driven by both improved light vehicle production but also inconsistent service center buying behavior. The resultsprice for 2021 includedomestic HRC, the FPT operations subsequentmost significant index impacting our revenues and profitability, averaged $906 per net ton for 2023, which was 10% lower than 2022. Demand for steel from automotive manufacturers improved in 2023 as supply chain issues continued to ease and light vehicle sales increased. North American light vehicle production of 15.6 million units in 2023 was the highest since 2019. Demand for steel from service centers was adversely impacted at certain points of the year due to recessionary fears and the anticipation of, and ultimate occurrence of, the UAW strike at certain domestic automotive producers. During 2023, service center inventories were as low as 1.6 months of inventory on hand, significantly lower than the prior ten-year average of 2.2 months of inventory on hand. Low inventory levels generated significant demand for steel toward the end of 2023 as the UAW strike concluded and service centers needed to meet the continued healthy demand from their end-use customers. Additionally, steel imports remained unattractive for the majority of 2023 due to low pricing spreads between the U.S. and other regions. Looking forward, we expect domestic steel demand to remain healthy as automotive production continues to improve, service centers restock inventory and incremental steel demand stimulated by government legislation is realized.

The Infrastructure and Jobs Act, the CHIPS Act and Inflation Reduction Act should continue to provide meaningful support for overall domestic steel demand in the coming years. Our extensive portfolio of products should result in increased steel demand from some of our end markets. The Infrastructure and Jobs Act was signed into law in November 18, 2021 and full-year resultsincludes approximately $550 billion of authorized spending for allnew investments and programs. This legislation provides direct spending support for roads, bridges and other operations. The results for 2020 include AK Steel operations subsequent to March 13, 2020, ArcelorMittal USA operations subsequent to December 9, 2020, and our results from operations previously reported as part of our historical Mining and Pelletizing segment.

Revenues

During the year ended December 31, 2021, our consolidated Revenues increased by $15,090 million, compared to 2020. The increase was primarily dueinfrastructure projects, including upgrades to the additiondomestic power grid and building out a national network of 12.1 million net tons of steel shipmentsEV chargers. We expect to continue to benefit from our Steelmaking segment resulting from the 2020 Acquisitions, along with an increasethese steel-intensive projects in the averagecoming years as they will consume our hot-rolled, plate, electrical, rail and other steel product selling priceproducts. The CHIPS Act promotes semiconductor manufacturing in the U.S., which should help support non-residential construction as well as machinery and equipment. Additionally, the on-shoring of $240 per net ton.manufacturing in the U.S. should reduce risk of supply chain issues in the future. The Inflation Reduction Act provides a tax credit for consumers who buy new EVs, which further incentivizes consumers to purchase vehicles in an environment where pent-up

5643 | CLF 2023 FORM 10-K

Revenues by Product Line

demand is still very strong from a low unemployment rate, recent supply chain issues and lower than historical dealer inventory levels. The following represents our consolidated Revenues by product lineInflation Reduction Act also provides incentives for the use of domestic steel for investments in clean energy projects, including wind and solar projects, which consume a substantial amount of steel. We expect to benefit from the spending related to this legislation for years ended:to come.

The change in product mix for 2021, compared to 2020, is due primarily to the inclusion of full-period results for the 2020 Acquisitions. The results for 2020 include AK Steel operations subsequent to March 13, 2020, ArcelorMittal USA operations subsequent to December 9, 2020, and our results from operations previously reported as part of our historical Mining and Pelletizing segment.

Revenues by Market

The following table represents our consolidated Revenues and percentage of revenues attributable to each of the markets we supply:

| | | | | | | | | | | | | | | | | | | | | | | |

| (In Millions) |

| Year Ended December 31, |

| 2021 | | 2020 |

| Revenue | | % | | Revenue | | % |

| Automotive | $ | 5,152 | | | 25 | % | | $ | 2,391 | | | 45 | % |

| Infrastructure and Manufacturing | 5,427 | | | 27 | % | | 818 | | | 15 | % |

| Distributors and Converters | 7,741 | | | 38 | % | | 722 | | | 13 | % |

| Steel producers | 2,124 | | | 10 | % | | 1,423 | | | 27 | % |

| Total revenues | $ | 20,444 | | | | | $ | 5,354 | | | |

The change in percentages of net revenues to each market in 2021 compared to 2020 was driven primarily by the AM USA Transaction, which increased overall sales to automotive customers, but reduced the total percentage exposure, increased exposure to infrastructure and manufacturing and distributors and converters customers, and drove more in-house iron ore sales, which reduced the percentage of sales to steel producers.

Automotive MarketOTHER KEY DRIVERS

The largest end usermarket for our steel products is the automotive industry in North America, which makes light vehicle production a key driver of demand. During 2021,2023, North American light vehicle production was approximately 13.015.6 million units, the same as the prior year. Production the past two years has been down approximately 3.0up from 14.3 million units compared to the prior ten-year average, primarily due to the global semiconductor shortage, as well as other material shortages and supply chain disruptions resulting from the COVID-19 pandemic. This has caused several outages amongst light vehicle manufacturers despite strong consumer demand. In light of these production outages, we have been able to redirect certain volumes originally intended for this end market to the spot market, where demand has been strong and pricing has reached all-time highs. The percentage of sales to the automotive market should increase in 2022, as fixed price contract prices increase and volumes expand as the material shortage issues ease.

highest level since 2019. During 2021,2023, light vehicle sales in the U.S. were 15.1saw an average seasonally adjusted annualized rate of 15.5 million units sold, representing a 3%13% increase over the prior year. These improved sales, combined with continued production difficulties, broughtcompared to 2022. North American light vehicle inventoriesproduction in 2024 is estimated to exceed 2023 units, indicating continued strength from the automotive industry. Additionally, the average age of light vehicles on the road in the U.S. reached an all-time lowhigh during 2023, surpassing the previous record set in 2022, which should support demand as older vehicles need to be replaced. As a leading supplier of 22 days' supply during the third quarter of 2021.

Infrastructure and Manufacturing

We sell a variety of our steel products, including plate, carbon, stainless, electrical, tinplate and rail, to the infrastructure and manufacturing market. This market includes sales to manufacturers of HVAC, appliances, power transmission and distribution transformers, storage tanks, ships and railcars, wind towers, machinery parts, heavy equipment, military armor, food preservation, and railway lines. Domestic construction activity and the replacement of aging infrastructure directly affects sales of steel to this market. Residential construction spending surged in 2021 due to overwhelming demand for new houses. Nonresidential construction spending was slightly down in 2021; however, the sector saw a surge in spending in the second half of the year that will likely continue into 2022 with the passing of the Infrastructure and Jobs Act of 2021. The Infrastructure and Jobs Act of 2021 is also expected to increase demand for steel products related to renewable energy as well as the modernization of the U.S. electrical grid. Our plate products can be used in windmills, which we estimate contain 130 metric tons of steel per megawatt of electrical generating capacity. Additionally, we estimate solar panels consume 40 metric tons of steel per megawatt of electrical generating capacity. We also expect to see an increase in charging stations for EVs, which we will benefit from as we are the sole producer of electricalautomotive-grade steel in the U.S., we expect to benefit from increased vehicle production over the coming years.

Distributors and Converters

Virtually all ofSince 2021, the grades of steel we produce are sold to the steel distributors and converters market. This market generally represents downstream steel service centers, which source various types of steel from us and fabricate it according to their customers' needs, which also includes automotive customers. Our steel is typically sold to this market onprice for busheling scrap, a spot basis or under short-term contracts linked to steel pricing indices. Demand and pricingnecessary input for this market can be highly dependent on a variety of factors outside our control, including global and domestic commodityflat-rolled steel production in EAFs in the U.S., has continued to average well above the prior annual ten-year average of approximately $390 per long ton. The busheling price averaged $488 per long ton during 2023. We expect the supply of busheling scrap to further tighten due to decreasing prime scrap generation from original equipment manufacturers and the growth of EAF capacity in the relative healthU.S., reduced metallics import availability, and a push for expanded scrap use globally. As we are fully integrated and have primarily a blast furnace footprint, increased prices for busheling scrap in the U.S. bolster our competitive advantage, as we source the majority of countries’ economiesour iron feedstock from our stable-cost mining and whether they are consuming or exporting excess steel production,pelletizing operations in Minnesota and Michigan.

As for iron ore, the provisions of international trade agreements and fluctuationsPlatts 62% price averaged $120 per metric ton in international currencies and, therefore, are subject to market changes in steel prices.

The price for domestic HRC,2023, which is an important attribute in the profitability of this end market, averaged $1,573 per net ton for the year ended December 31, 2021, 174%24% higher than the prior year. The record prices for steel products in 2021 resulted from both supply and demand factors, each driven by a rapid recovery since the onset of the COVID-19 pandemic in 2020.

Steel Producers Market

The steel producers market represents third-party sales to other steel producers, including those who operate blast furnaces and EAFs. It includes sales of raw materials and semi-finished and finished goods, including iron ore pellets, coal, coke, HBI, scrap and steel products.

The increase in revenues from the steel producers market for 2021, as compared to 2020, is primarily due to the inclusion of full-period results for the AK Steel and ArcelorMittal USA operations. This was partially offset by a decrease in iron ore product revenues during 2021, as compared to 2020, primarily as a result of the 2020 Acquisitions, as our iron ore pellet production is now predominately consumed internally and the respective intercompany revenue is eliminated in consolidation.

The largest component of sales to this market during the year ended December 31, 2021 was third-party slab sales, which are primarily made under a long-term supply agreement that was initiated in connection with the closing of the AM USA Transaction. Additionally, while it has fallen from peak 2021 levels in recent months, the price of iron ore has also risen dramatically over the past year, which, along with strong demand, has been an important factor in rising steel prices globally. The Platts 62% Price averaged $159 per metric ton during 2021, a 46% increase compared to the prior year.annual ten-year average. While higher iron ore prices play a role in increased steel prices, we also directly benefit from higher iron ore prices for the portion of iron ore pellets we sell to third parties.

Operating CostsOTHER FACTORS

CostOn September 14, 2023, the UAW announced a simultaneous labor strike against three domestic automotive manufacturers, as each of goods soldthe individual companies were unable to come to terms on a new labor agreement. The strike originally impacted one assembly plant at each company and was further expanded to additional facilities, including certain parts-distribution centers for each company. Steel demand remained strong from the automotive industry as the strike was limited to certain facilities, allowing the automotive manufacturers to continue production at other facilities within their footprint. On October 30, 2023, the UAW strike concluded after the UAW reached tentative labor deals with each of the three domestic automotive manufacturers. The conclusion of the strike led to increased demand in the fourth quarter of 2023 from automotive customers as well as service centers who had significantly reduced their inventory levels in anticipation of a broader strike.

In January 2023, we announced that we partnered with the USW and filed antidumping and countervailing duty petitions against eight countries related to unfairly traded tin and chromium coated sheet steel products. Tin mill products are used primarily for packaging applications, particularly canned food. We produce tin mill products at our Weirton, West Virginia operating facility and sell approximately 300,000 net tons per year, representing approximately two percent of total Company steel sales volumes. The U.S. Department of Commerce determined that imports of tin mill products from Canada, China, Germany and South Korea are being unfairly priced and dumped into the United States and that imports from China are being unfairly subsidized. On January 5, 2024, the U.S. Department of Commerce announced its final countervailing and antidumping determination of tin mill products. The U.S. Department of Commerce imposed countervailing subsidy rates on China ranging from 331.88% to 649.98%, based on the exporter. Final antidumping duty rates on tin and chromium-coated sheet steel products were imposed on Canada, China, Germany and South Korea ranging from 2.69% to 122.52%. However, on February 6, 2024, the U.S. International Trade Commission terminated the investigation on South Korea and reached negative determinations in the investigations on Canada, China and Germany. As a result, countervailing duties and antidumping duties will not be imposed on imports of tin and chromium-coated steel sheet products from these four countries.

During 2023, we significantly reduced costs compared to the prior year as we had higher production volume, normalized repair and maintenance spending, and inflationary pressures on input and energy costs eased. We expect to benefit further from reduced costs in 2024 as we have worked through higher cost inventory, production volumes should remain similar, and reductions in coal and alloy costs should mitigate any cost increases.

STEELMAKING RESULTS

COMPARISON OF 2023 TO 2022

The following is a summary of the Steelmaking segment operating results for the years ended December 31, 2023 and 2022 (dollars in millions, except for average selling price and shipments in thousands of net tons):

| | | | | | | | | | | | | | | | | | | | |

| Total Revenue | | Gross Margin | | Adjusted EBITDA | | Steel Shipments (nt) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2022 | 2023 | | 2022 | 2023 | | 2022 | 2023 | | 2022 | 2023 |

| | | | | | |

| STEEL PRODUCT REVENUE: | | GROSS MARGIN %: | | ADJUSTED EBITDA %: | | AVERAGE SELLING PRICE PER TON OF STEEL PRODUCTS: |

| $20,054 | $19,237 | | 11% | 6% | | 14% | 9% | | $1,360 | $1,171 |

REVENUE

The following tables represent our steel shipments by product and total revenues by market:

| | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, | | |

| (In thousands of net tons) | 2023 | | 2022 | | % Change |

| Steel shipments by product: | | | | | | | |

| Hot-rolled steel | 5,899 | | | | 4,326 | | | | 36 | % |

| Cold-rolled steel | 2,389 | | | | 2,286 | | | | 5 | % |

| Coated steel | 4,791 | | | | 4,730 | | | | 1 | % |

| Stainless and electrical steel | 682 | | | | 763 | | | | (11) | % |

| Plate | 899 | | | | 880 | | | | 2 | % |

| Slab and other steel products | 1,772 | | | | 1,766 | | | | — | % |

| Total steel shipments by product | 16,432 | | | | 14,751 | | | | 11 | % |

| | | | | | | |

| Year Ended December 31, | | |

| (In millions) | 2023 | | 2022 | | % Change |

| Steelmaking revenues by market: | | | | | | | |

| Direct automotive | $ | 7,440 | | | | $ | 6,661 | | | | 12 | % |

| Infrastructure and manufacturing | 5,612 | | | | 5,869 | | | | (4) | % |

| Distributors and converters | 5,330 | | | | 6,388 | | | | (17) | % |

| Steel producers | 2,949 | | | | 3,465 | | | | (15) | % |

| Total Steelmaking revenues by market | $ | 21,331 | | | | $ | 22,383 | | | | (5) | % |

CostRevenues decreased by 5% during the year ended December 31, 2023, as compared to the prior year, primarily due to:

•A decrease in revenues from the distributors and converters market of goods sold $1,058 million, or 17%, predominantly due to the average HRC price declining, which was partially offset by increased hot-rolled steel shipments; and

•A decrease in revenues from the steel producers market of $516 million, or 15%, which was primarily due to the decrease in pricing indices for slabs and busheling scrap.

•These decreases were partially offset by an increase in revenues from the direct automotive market of $779 million, or 12%, predominantly due to increases in selling prices as a result of favorable renewals of annual fixed price contracts and an increase in shipments.

GROSS MARGIN

Gross margin decreased by $1,117 million, or 45%, during the year ended December 31, 2023, as compared to the prior year, primarily due to:

•A decrease in selling prices (approximately $2.4 billion impact) predominantly due to lower spot prices, which was partially offset by favorable renewals of annual sales contracts.

•This decrease was partially offset by a decrease in costs of production (approximately $700 million impact) driven by lower raw materials and utility costs, including natural gas, coal, coke, alloys and scrap, coupled with decreased maintenance costs; and

•An increase in sales volumes (approximately $500 million impact).

ADJUSTED EBITDA

Adjusted EBITDA from our Steelmaking segment for the year ended December 31, 2023, decreased by $1,216 million, as compared to 2022, primarily due to the decreased gross margin from our operations. Additionally, our Steelmaking Adjusted EBITDA included $549 million and $439 million of Selling, general and administrative expenses for the years ended December 31, 2023 and 2022, respectively.

CONSOLIDATED RESULTS

COMPARISON OF 2023 TO 2022

REVENUES AND GROSS MARGIN

During the year ended December 31, 2023, our consolidated Revenues decreased by $993 million, compared to 2022. The decrease was primarily due to the decrease in the average steel product selling price of $189 per net ton, partially offset by the increase of 1.7 million net tons of steel shipments from our Steelmaking segment.

During the year ended December 31, 2023, our consolidated gross margin decreased by $1,127 million, as compared to 2022. See "— Steelmaking Results" above for further detail on our operating results.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES

Selling, general and administrative expensesincreased by $10,808$112 million during the year ended December 31, 2023, as compared to 2022. The increase primarily relates to employment-related costs, including higher incentive compensation, and external service costs.