UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K10-K/A

(Amendment No.1)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition period from _____ to _____

Commission file number 1-08951

M.D.C. HOLDINGS, INC.

(Exact name of Registrant as specified in its charter) | | | | | | | | |

| Delaware | 84-0622967 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

| 4350 South Monaco Street, Suite 500 | 80237 |

| Denver, Colorado | (Zip code) |

| (Address of principal executive offices) | |

(303) 773-1100

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $.01 par value | MDC | New York Stock Exchange |

| 6% Senior Notes due January 2043 | MDC 43 | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes x No o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and “emerging growth company” in Rule 12b-2 of the Exchange Act. | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☒ | Accelerated Filer | ☐ | Emerging Growth Company | ☐ |

| Non-Accelerated Filer | ☐ | Smaller Reporting Company | ☐ | | |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 726(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2023, the aggregate market value of the Registrant's common stock held by non-affiliates of the Registrant was $2.80 billion based on the closing sales price of $46.77 per share as reported on the New York Stock Exchange on June 30, 2023.

As of DecemberMarch 31, 2023,2024, the number of shares outstanding of Registrant's common stock was 74,661,479.75,047,701.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of part III of this Form 10-K are incorporated by reference from the Registrant's2024definitive proxy statement to be filed with the Securities and Exchange Commission no later than 120 days after the end of the Registrant's fiscal year.None.

EXPLANATORY NOTE

On January 30, 2024, M.D.C. Holdings, Inc. (the "Company," "MDC," "we," or "our,") filed its Annual Report on Form 10-K for the fiscal year ended December 31, 2023, (the "Original Form 10-K"). The Original Form 10-K omitted Part III, Items 10 (Directors, Executive Officers and Corporate Governance), 11 (Executive Compensation), 12 (Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters), 13 (Certain Relationships and Related Transactions, and Director Independence) and 14 (Principal Accounting Fees and Services) in reliance on the General Instructions to Form 10-K, which provides that such information may be either incorporated by reference from the registrant’s definitive proxy statement or included in an amendment to Form 10-K, in either case filed with the Securities and Exchange Commission (the "SEC") not later than 120 days after the end of the fiscal year.

We currently do not expect that a definitive proxy statement for a 2024 annual meeting of stockholders will be filed within 120 days after the end of the last fiscal year. Accordingly, this Amendment No. 1 to Form 10-K (this "Amendment") is being filed solely to:

•amend Part III, Items 10, 11, 12, 13 and 14 of the Original Form 10-K to include the information required by such Items; and

•in accordance with Rule 12b-15 under the Securities Exchange Act of 1934, as amended (the"Exchange Act"), file new certifications of the Company’s principal executive officer and principal financial officer required by Rule 13a-14(a) under the Exchange Act as exhibits to this Amendment under Item 15 of Part IV hereof.

The cover page of the Form 10-K is also amended to delete the reference to incorporation by reference of the Company’s definitive proxy statement.

This Amendment does not otherwise change or update any of the disclosures set forth in the Original Form 10-K and does not otherwise reflect any events relating to the previously announced Agreement and Plan of Merger, dated as of January 17, 2024 (the "Merger Agreement") pursuant to which the Company will become an indirect wholly-owned subsidiary of Sekisui House, Ltd. and any events occurring after the filing of the Original Form 10-K. Accordingly, this Amendment should be read in conjunction with the Original Form 10-K, and our other SEC filings subsequent to the date of the Original Form 10-K.

M.D.C. HOLDINGS, INC.

FORM 10-K10-K/A

For the Year Ended December 31, 2023

M.D.C. HOLDINGS, INC.PART III

FORM

Item 10. Directors,Executive Officers and Corporate Governance.

Directors of the Registrant

The Company's Certificate of Incorporation provides for three classes of directors (“Directors”) with staggered terms of office, to be divided as equally as possible. Directors of each class serve for terms of three years until election and qualification of their successors or until their resignation, death, disqualification or removal from office. Our Board of Directors ("Board") has eleven members, consisting of four Class I Directors whose terms expire in 2025, four Class II Directors whose terms expire in 2026 and three Class III Directors whose terms expire in 2024. The following is a brief description of the names, ages, and business experience during at least the past five years of each Director of the Company. Their experience, qualifications, attributes or skills, set forth below, have led to the Board's conclusion that each person should serve as a Director, in light of the Company’s business and structure. None of the business organizations identified below (excluding HomeAmerican Mortgage Corporation) are affiliates of the Company. None of the Directors holds, or has held during the past five years, any directorship in any company with a class of securities registered pursuant to Section 12 of the Exchange Act, subject to the requirements of Section 15(d) of the Exchange Act or registered as an investment company under the Investment Company Act of 1940. The ages of the directors set forth below are given as of December 31, 2023.

Class I Directors

Michael A. Berman, 73, has over thirty-five years of experience in the financial services industry. He is a member of Applied Capital Management, a private investment management firm located in Scottsdale, Arizona, and has served as its chairman from 2002 to present. From 2005 to 2006, he also served as the chief executive officer of First Ascent Capital, a financial services firm located in New York. From July 2006 until December 2008, he served as president and Chief Executive Officer of Real Estate Equity Exchange, Inc. (Rex & Co.), a financial services firm located in San Francisco, California. From January 1990 to March 1999, Mr. Berman was employed by The Nomura Securities Co., Ltd. (Tokyo) group of companies, where he held several senior executive positions, including that of President and CEO of Nomura Holding America Inc. and Chairman of Capital America, Nomura's commercial real estate lending subsidiary. In April 2006, Mr. Berman became a Director of the Company. Since 2006, he has been a director of HomeAmerican Mortgage Corporation, the Company’s mortgage lending subsidiary. Mr. Berman’s experience as a senior executive in corporate finance, in general, and the residential mortgage market, in particular, provide the Company with a valuable resource.

Herbert T. Buchwald, 92, is a principal in the law firm of Herbert T. Buchwald, P.A. and president and chairman of the Board of Directors of BPR Management Corporation, a property management company located in Denver, Colorado, positions he has held for more than the past five years. Mr. Buchwald has been engaged in the acquisition, development and management of residential and commercial real estate in Florida, Arizona, New Jersey and Colorado, through both publicly and privately held ventures for more than forty years. As an attorney, he has been admitted to practice before federal and state trial and appellate courts in Florida and Colorado. In addition, he holds an accounting degree and formerly was a practicing Certified Public Accountant. He has been a member of the Company's Board of Directors since March 1994. The combination of his knowledge, experience and skills provide the Company with strong oversight of accounting, financial, regulatory and legal matters, as well as the operation of the Company's real estate businesses. Mr. Buchwald is a veteran of the United States Navy.

Larry A. Mizel, 81, founded the Company in 1972 and has served as a Director since its inception. He was appointed Chairman of the Board in 1972 and Chief Executive Officer of the Company in 1988. Then, in October 2020, he was appointed as Executive Chairman. Mr. Mizel has provided the Company with leadership and judgment, previously serving as the Chief Executive Officer and Chairman of the Board of Directors, and now as Executive Chairman, while advancing the long-term interests of the Company's shareholders. One of the most experienced leaders in the homebuilding industry, his knowledge and foresight provide the Board with invaluable guidance.

Janice Sinden, 51, has served as President and Chief Executive Officer of the Denver Center for the Performing Arts since 2016. Past positions include Chief of Staff for Denver Mayor Michael B. Hancock, where she managed 60 appointees and 26 departments. She currently serves on the non-profit boards of Citizens for Arts to Zoo, University of Northern Colorado, VISIT Denver, the American Transplant Foundation, Colorado Inclusive Economy and Denver Preschool Program. Ms. Sinden has been recognized by Titan 100 as one of Colorado's Top 100 CEO's, the Denver Business Journal as an Outstanding Woman in Business, 5280 Magazine as one of the 50 most influential persons in Denver, by the Colorado Women’s Foundation as one of the 25 most influential women in Colorado, by the Girl Scouts of Colorado as a Woman of Distinction, and by the University of Northern Colorado Department of Political Science and International Affairs as Distinguished Alumnus of the Year. Ms. Sinden has been a member of the Company's Board of Directors since January 2022. Her operational and business knowledge, rich

cultural experiences and community involvement provide the Company with a valuable resource and contribute to the business perspectives of the Board.

Class II Directors

Rafay Farooqui, 47, is the Founder & CEO of Strategic Alternative Funds Group, LLC d/b/a +SUBSCRIBE, a fintech leader providing a unified private markets platform for alternative investment fund investors, fund managers, and service providers. Prior to founding +SUBSCRIBE in 2015, he also co-founded CAIS in 2009, a fintech technology company offering an investable menu of leading alternative investment funds to wealth management firms. Prior to forming CAIS, Mr. Farooqui was the Head of the Middle East & North African Equities division for UBS Investment Bank and was based in Dubai, U.A.E. Between 2003 and 2008, he was Head of UBS Investment Bank's U.S. Institutional Equities Sales Group, based in New York City. Prior to UBS, from 1998 to 2003, Mr. Farooqui was Head of Global Institutional International Sales-Trading in the New York City offices of Goldman Sachs & Co., where he advised alternative investment management clients on research and trading in the global securities markets. Mr. Farooqui began his career in 1998 at Goldman Sachs & Co. within the Equity Division's International Department as a global equity securities sales-trader. He joined the Company's Board of Directors in December 2022. Mr. Farooqui’s focus and experience in technology and finance provide the Company with both technology information architecture and financial expertise.

David D. Mandarich, 76, has been associated with the Company since 1977. He was a Director from September 1980 until April 1989, and has been a Director continuously since March 1994. He was appointed President and Chief Operating Officer of the Company in June 1999. Then, in October 2020, he was appointed President and Chief Executive Officer. A skilled and experienced leader in the homebuilding industry, Mr. Mandarich provides the Board with the benefit of his judgment and his knowledge and understanding of the Company's homebuilding business and operations. Mr. Mandarich is a veteran of the United States Army.

Paris G. Reece III, 69, was formerly the Company’s Chief Financial Officer and Principal Accounting Officer, and retired on August 1, 2008. Since his retirement, Mr. Reece has performed consulting work and served in a volunteer position as the President of Cancer League of Colorado, a leading non-profit organization that was established over fifty years ago to raise money for cancer research and patient care. He joined the Company's Board of Directors in May 2013. As a Certified Public Accountant (Texas, non-practicing), a former Chief Financial Officer and a highly respected person within the homebuilding industry, Mr. Reece is uniquely qualified to provide the Company with strong oversight of accounting and financial matters, as well as the operation of the Company's homebuilding and financial services businesses.

David Siegel, 67, was a partner in the law firm of Irell & Manella LLP for more than thirty years, where he led that firm's securities litigation practice and was the firm's Managing Partner. He retired from the active practice of law in 2019. Mr. Siegel's law practice, for which he is nationally recognized, was concentrated on securities class actions, corporate governance, risk management, SEC reporting standards and regulatory compliance. Mr. Siegel has chaired and has been a frequent speaker at various seminars on securities litigation, class actions, and trial techniques. He has been named by his peers as one of the "Best Lawyers in Commercial Litigation" in The Best Lawyers in America guide. Mr. Siegel has been a member of the Company's Board of Directors since June 2009. Mr. Siegel's knowledge and experience in corporate governance and litigation matters provide the Company with significant guidance and oversight.

Class III Directors

Raymond T. Baker, 73, has served as President of Gold Crown Management Company, a real estate asset management company, from 1978 to 2013, then as Vice President and Secretary from 2013 to present. He is the founder and has served as Co-Director of the Gold Crown Foundation since 1986. He also is a member of the Board of Directors of Alpine Banks of Colorado and Land Title Guarantee Company. Mr. Baker is currently serving as Chairman of the Board of the Metropolitan Football Stadium District (Denver). From February 2004 until May 2007, he served as a director of Central Parking Corporation. He has over thirty-five years of experience in the real estate and banking industries. Mr. Baker became a member of the Company's Board of Directors in January 2012. His experience and knowledge of the real estate and banking industries directly complement and support the Company’s real estate activities and the financing of those activities.

David E. Blackford, 75, has over forty-five years experience in the banking industry. He is employed by California Bank & Trust (CB&T), a leading California banking institution and a division of Zions Bancorporation, National Association. Between 1998 and 2001, he was CB&T’s managing director, serving on the Board of Directors and the Senior Loan Committee for Real Estate Finance. In May 2001 he was appointed chairman, president and chief executive officer of CB&T, and currently serves as executive chairman. He also is an executive vice president of Zions Bancorporation, National Association. Prior to 1998, he served as an executive officer in several financial institutions, including Bank One and Valley National Bank. He joined the

Company's Board of Directors in April 2001. His experience and knowledge of historic and current institutional real estate lending practices, the regulatory process and the volatility of the credit markets provide a unique perspective to the Board.

Courtney L. Mizel, 51, is a Principal at Mizel Consulting where she has worked for over twenty years. In this role, Ms. Mizel consults with companies in various industries on matters relating to their business management and strategy, including operations, business development, marketing, as well as legal matters. She is also a Founding Director of The Counterterrorism Education Learning Lab, an organization dedicated to preventing terrorism through education, empowerment, and engagement. She is active in a number of other non-profit activities, including serving on the Boards of Directors of Zimmer Children’s Museum, Sharsheret National, and JQ International. Ms. Mizel received her Bachelor of Science in Economics with honors from The Wharton School of the University of Pennsylvania and her Juris Doctor from the University of Southern California Gould School of Law. Ms. Mizel became a member of the Company's Board of Directors in June 2017. She is the daughter of the Company’s Executive Chairman, Larry A. Mizel. Ms. Mizel’s professional and business achievements, intellect and diverse experiences contribute to the business, governance and legal perspectives of the Board.

The following table provides the membership of each standing committee of the Board in 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Name | | Audit | | Compensation | | Corporate Governance / Nominating | | Legal | |

| Raymond T. Baker | | | | C | | | | | |

| Michael A. Berman | | | | | | | | | |

| David E. Blackford | | | | | | M | | M | |

| Herbert T. Buchwald | | M | | M | | M | | C | |

| Rafay Farooqui | | | | | | | | | |

| David D. Mandarich | | | | | | | | | |

| Courtney L. Mizel | | | | | | | | M | |

| Larry A. Mizel | | | | | | | | | |

| Paris G. Reece III | | C | | | | | | | |

| David Siegel | | | | | | C | | M | |

| Janice Sinden | | M | | | | | | | |

C = Chair; M = Member

Executive Officers of the Registrant

Set forth below are the names and offices held by the executive officers of the Company as of December 31, 2023. The Board, after reviewing the functions performed by the Company's officers, has determined that, for purposes of Item 401 of SEC Regulation S-K, only these officers are deemed to be executive officers of the Company. These officers also constitute our Named Executive Officers ("NEOs").

The executive officers of the Company hold office until their successors are duly elected and qualified or until their resignation, retirement, death or removal from office. Biographical information on Messrs. Mizel and Mandarich, who serve as Directors and executive officers of the Company, is set forth under "Directors of the Registrant" above. Biographical information for Mr. Martin and Mr. Kaplan is set forth below.

| | | | | | | | | | | |

| Name | | Other Business Experience | |

| David D. Mandarich | | Biographical information regarding Mr. Mandarich is set forth in the section entitled “Directors of the Registrant” above. | |

| President and Chief Executive Officer | | |

| Age: 76 | | |

| | |

| Larry A. Mizel | | Biographical information regarding Mr. Mizel is set forth in the section entitled “Directors of the Registrant” above. | |

| Executive Chairman | | |

| Age: 81 | | |

| | |

| Robert N. Martin | | Robert N. Martin was appointed Senior Vice President and Chief Financial Officer in May 2015. He also served as the principal accounting officer from May 2015 until August 2020 and resumed that role in June 2021 through January 2023. He previously served as Vice President – Finance and Business Development. In April 2013, he was promoted to the position of Vice President of Finance and Corporate Controller. In his current role, Mr. Martin has direct oversight of the Company's division and corporate accounting, tax, treasury, investor relations, information technology and finance, planning and analysis functions. Additionally, he has served on all of the Company’s Asset Management Committees ("AMCs") and has performed a key role in the Company's capital markets activities. He is an officer, director or both of many of the Company’s subsidiaries. Mr. Martin received a bachelor’s degree in Accounting and Computer Applications from the University of Notre Dame and is both a Certified Public Accountant and a CFA charterholder.

| |

| Senior Vice President and Chief Financial Officer | | |

| Age: 45 | | |

| | |

| Michael L. Kaplan | | Michael L. Kaplan joined the Company in October 2022 as Senior Vice President and General Counsel and has direct oversight of the Company’s legal, corporate governance, regulatory compliance, and insurance and risk management functions. From February 2020 until October 2022, Mr, Kaplan was the Executive Vice President, Chief Legal Officer (CLO), Chief Compliance Officer (CCO) and Secretary for Red Robin Gourmet Burgers, Inc. (Nasdaq: RRGB) and from September 2013 until February 2020, he was the Senior Vice President, CLO, CCO and Secretary for that company. Prior to RRGB, Mr. Kaplan was Senior Vice President, General Counsel, Chief Security Officer and Secretary for StandardAero from January 2010 until July 2013, and from January 2000 until January 2010 he was an attorney with Greenberg Traurig, LLP. Mr. Kaplan received an A.B. degree in economics and government from the College of William and Mary and a J.D. degree from the Stanford Law School. | |

| Senior Vice President and General Counsel | | |

| Age: 55 | | |

| | |

Delinquent Section 16(a) Reports

The Company's executive officers and Directors and certain owners of more than ten percent of the Company's common stock are required under Section 16(a) of the Securities Exchange Act, as amended, to file initial reports of ownership and reports of changes in ownership of common stock of the Company with the SEC. Based upon a review of the reports filed electronically with the SEC, and, in certain cases, written representations, the Company believes that during the year ended December 31, 2023, all such reports were filed on a timely basis.

Audit Committee

The Audit Committee of the Board of Directors ("Audit Committee"), which has been established in accordance with Section 3(a)(58)(A) of the Exchange Act, consists of Mr. Reece, who serves as Chairman, Mr. Buchwald and Ms. Sinden. Each member of the Audit Committee is "independent" and "financially literate" in the judgment of the Board, as defined in the listing standards of the NYSE and the rules of the SEC. In addition, the Board has determined that Mr. Buchwald is an "audit committee financial expert" as defined by applicable SEC regulations. The Board believes that his experience and qualifications described above under "Directors of the Registrant" qualify him to act as the Audit Committee's audit committee financial expert. The Audit Committee met eleven times during 2023. The organization, functions and responsibilities of the Audit Committee are described in the restated charter for the Audit Committee, which is posted on the investor relations section of the Company's website, www.mdcholdings.com.

Code of Ethics

We will provide to any shareholders or other person without charge, upon request, a copy of our Corporate Code of Conduct, Corporate Governance Guidelines, code of ethics applicable to our principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions (collectively “senior financial officers”) and the charters for our Audit Committee, The Compensation Committee of the Board of Directors ("Compensation Committee"), The Legal Committee of the Board of Directors ("Legal Committee"), and the Corporate Governance/Nominating Committee of the Board of Directors ("Corporate Governance/Nominating Committee"). You may obtain these documents on our website at www.mdcholdings.com, under our Investor Relations section or by contacting our Investor Relations department at 1-866-424-3395. Our intention is to post on our website any amendments to or waivers from our code of ethics applicable to our senior financial officers if such disclosure is required.

Corporate Governance/Nominating Committee

Procedures for nominating persons for election to the Board are contained in the Company's By-Laws and, accordingly, those procedures constitute the Company's policy with regard to the nomination and consideration of Director candidates recommended by shareholders. The Corporate Governance/Nominating Committee will consider candidates identified by shareholders following the procedures set forth in the By-Laws. There have been no changes to these procedures in the last year.

Item 11. Executive Compensation.

Executive Compensation - Compensation Discussion and Analysis

Executive Summary

For fiscal 2023, our named executive officers were:

| | | | | |

| Named Executive Officers |

| Larry A. Mizel | Executive Chairman |

| David D. Mandarich | President and Chief Executive Officer (“CEO”) |

| Robert N. Martin | Senior Vice President and Chief Financial Officer (“CFO”) |

| Michael L. Kaplan | Senior Vice President and General Counsel (“CLO”) |

Our compensation program is designed to align executive pay with the drivers of long-term value creation and reward execution of our strategic initiatives.

The annual incentive and long-term compensation programs for our Executive Chairman and CEO are 100% performance-based utilizing our annual and long term business goals, predetermined challenging metrics tied to the drivers of long-term shareholder value.

The Compensation Committee aims to design a compensation program that rewards and retains talented executives while motivating them to drive short-term and long-term performance. We believe that our ability to retain and motivate our executive officers with their exceptional skills, experience and capacity to succeed in our competitive industry has been essential to the success of our Company and a significant factor in creating long-term value for our shareholders.

Our compensation program reflects the above philosophy and, additionally, prioritizes the following:

•Attracting and retaining talented executives and encouraging their long-term service and loyalty

•Supporting our long-term business goals and driving performance by closely aligning our compensation metrics and goals with our long-term growth strategy

•Maintaining a firm link between our executives’ and shareholders’ long-term interests

•Prioritizing growth, risk management and financial stability

•Reflecting shareholder feedback in the compensation program design and related considerations, through regular, ongoing shareholder engagement

Compensation Governance Best Practices

In order to continue to provide long-term value to our shareholders, our Compensation Committee is committed to maintaining independent and thorough oversight of our executive compensation program and the following governance best practices are key to achieving this goal. These Compensation Governance best practices include:

•Executive compensation program design and refinements incorporate shareholder feedback

•Significant portion of Executive Chairman and CEO pay is performance based

•Compensation Committee sets rigorous targets and metrics

•Compensation Committee performs thorough assessment of Company and individual performance

•100% of Compensation Committee is independent

•Compensation Committee works with an independent compensation consultant

•Executives are subject to significant stock ownership guidelines

•Company maintains policies prohibiting hedging Company stock

•Clawback policy authorizes Company to recover compensation under specified circumstances

•Vesting of cash remuneration under Executive Chairman and CEO employment agreements is subject to double trigger change-in-control provisions

2023Say-on-Pay Vote

Our Compensation Committee is committed to improving our executive compensation programs and modifying them as necessary to maintain the alignment of our executives and shareholders. We continue to engage investors on executive compensation topics and will continue to seek their feedback. We received a negative vote at the 2023 annual shareholders meeting, where our say-on-pay proposal received 44.8% support. In response to the feedback received, in 2023 the Compensation Committee reduced the bonus opportunity and bonus payment cap by $4 million and $3 million, respectively, for both our Executive Chairman and CEO as further discussed below. In addition, the Compensation Committee granted PSU awards under the Long-Term Incentive Program in 2023, for both our Executive Chairman and CEO, instead of the stock options that were awarded in 2022.

Components of Executive Compensation

The Compensation Committee designed our compensation program to support the drivers of value and shareholder return over the long term. It is comprised of three primary elements: (i) base salary, (ii) annual incentive award; and (iii) long-term incentive award.

| | | | | | | | | | | |

| Compensation Component | Description | Purpose | Key

Characteristic |

| Base Salary | Cash compensation based on executive officer’s role and employment agreement, if any. Salary levels are evaluated annually and may be adjusted for length of service, competitive considerations or recognition of a change in responsibilities. | ● Provide financial certainty and stability

● Attract and retain executive talent

● Recognize experience, length of service, competitive market conditions and individual performance | Fixed |

Annual

Incentive Award | Each year the Compensation Committee approves performance goals for the Executive Chairman and CEO, and establishes Key Performance Indicators (“KPIs”) for the CFO and CLO. The Compensation Committee determines the extent to which an award is earned and the amount of such award is based on individual and Company performance against the pre-established goals. | ● Motivate executive officer to achieve key annual goals and position the Company for long-term success

● Reward executive officer for individual performance and overall Company performance | Performance Based |

Long-Term

Incentive Award | Each executive officer is eligible to receive an award at the discretion of the Compensation Committee based upon long-term performance potential. | ● Provide an incentive for executive officers to achieve long-term sustainable success for the Company and to promote shareholder value

● Attract, motivate, reward and retain executive talent | Performance Based |

The net effect of our pay design is that both for the CEO and the other NEOs, a large majority of total direct compensation is performance based, and dependent on Company, individual, or stock performance.

Fixed Compensation - Base Salary

The Compensation Committee sets executive officer base salaries at a level that reflects the competitive market for these roles as well as each individual’s performance, skills and experience. Base salaries remained unchanged during the year for our Executive Chairman, CEO, CFO and CLO.

Performance-Based Compensation

2023 Executive Chairman and Chief Executive Officer Annual Incentive Bonus

Our annual incentive compensation program is designed to retain, motivate and reward the Executive Chairman and CEO for their respective contributions in achieving the Company’s annual financial goals by focusing their attention on the following key economic drivers: return on equity, home sale revenues, homebuilding operating margin, pre-tax earnings per diluted share and EBITDA. Focus on these key economic drivers is essential to our short-term financial results and, ultimately, our long-term success.

Annual Bonus Calculation Formula: Links to Key Metrics

The 2023 performance goal included a threshold performance objective that must be met prior to any bonus being earned. The threshold performance objective for 2023 was a 7.0% consolidated adjusted pre-tax return on beginning equity (the “ROE Condition”). This was a decrease compared to the prior year threshold performance objective given the instability of the housing market, but is consistent with 2021 and prior thresholds of 6.0%. The actual consolidated adjusted pre-tax return on beginning equity in 2023 was 18.0%, satisfying the ROE Condition, and as such, the Executive Chairman and CEO earned a $2.0 million bonus.

Once the ROE Condition was met, the Executive Chairman and CEO had the opportunity to earn an additional bonus (the “Additional Bonus Opportunity”) of $6.0 million and $5.0 million, respectively. The Additional Bonus Opportunity is described in more detail below. Both the Executive Chairman and CEO's Additional Bonus Opportunity was decreased compared to 2022 by $4.0 million from $10.0 million and $9.0 million, respectively.

Outcomes Reflect Alignment with Performance

Consistent with prior years and based in part on previous shareholder feedback, the Additional Bonus Opportunity for the Executive Chairman and CEO for 2023 was based on four distinct sets of financial goals, as set forth below. The Compensation Committee believes that achievement of these goals, in concert, is important for long term shareholder value creation.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Home Sale Revenues | Executive Chairman Bonus

(thousands) | CEO Bonus (thousands) | Goal

(millions) | | Adjusted Homebuilding Operating Margin | Executive Chairman Bonus

(thousands) | CEO Bonus (thousands) | Goal |

| Target | $ | 1,500 | | $ | 1,250 | | $ | 3,754 | | | Target | $ | 1,500 | | $ | 1,250 | | 6.2 | % |

| Threshold | $ | 800 | | $ | 800 | | $ | 3,271 | | | Threshold | $ | 800 | | $ | 800 | | 4.5 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Diluted Adjusted

Pre-Tax EPS | Executive Chairman Bonus

(thousands) | CEO Bonus (thousands) | Goal | | Adjusted

EBITDA | Executive Chairman Bonus

(thousands) | CEO Bonus (thousands) | Goal

(millions) |

| Target | $ | 1,500 | | $ | 1,250 | | $ | 4.48 | | | Target | $ | 1,500 | | $ | 1,250 | | $ | 446 | |

| Threshold | $ | 800 | | $ | 800 | | $ | 2.98 | | | Threshold | $ | 1,000 | | $ | 1,000 | | $ | 340 | |

The appropriateness of the categories selected for 2023, along with target and threshold goal amounts, were carefully considered by the Compensation Committee given the Company’s emphasis on prioritizing long-term growth, risk management, financial stability and pursuit of long-term value. Specifically, with respect to the Home Sale Revenues, Adjusted Homebuilding Operating Margin, Adjusted Pre-Tax Diluted EPS and Adjusted EBITDA goals, the Compensation Committee considered prior year results, the 2023 Business Plan as well as current market conditions in setting the threshold and target performance goals.

The 2023 Business Plan was developed by the Executive Chairman, CEO, CFO and other senior leaders from the “ground up” utilizing (i) forecasts submitted by the presidents for each of the Company’s homebuilding divisions detailing their operational projections for each of their divisions’ communities, (ii) the forecast submitted for the mortgage company by its leadership team; and (iii) forecasts from the CFO regarding the insurance companies, any other income producing divisions of the Company, and all the corporate general and administrative departments. The 2023 Business Plan was reviewed by the Board. The process of developing the business plan incorporates a disciplined evaluation of risks identified by management and the Board to establish a reasonable range of potential performance goals for the year including general economic conditions, fluctuations in interest rates, variations in projected mortgage lending programs, the availability and cost of capital, the availability and acquisition cost of land, materials and contractors in the homebuilding operations, potential for shortages and the increased cost of labor, and increased governmental regulation, including the adverse interpretation of tax, labor and environmental laws.

Target performance goals were established to reflect outstanding performance in light of the risks and market conditions anticipated for 2023.

Based on the achievements in these categories, the Executive Chairman and CEO earned an additional bonus of $6.0 million and $5.0 million, respectively, (subject to the bonus cap discussed below) related to the Additional Bonus Opportunity as shown below.

| | | | | | | | | | | | | | | | | |

| 2023 Short-Term Incentive Program |

| Performance Goal | Performance Required at Threshold | Performance Required at Target | Actual Performance | Bonus Earned |

| Executive Chairman | CEO |

| Adjusted pre-tax return* on equity | 7% hurdle achieved at 18.0% | $ | 2,000,000 | | $ | 2,000,000 | |

Additional Bonus Opportunity |

| Home Sales Revenue | $3.27 billion | $3.75 billion | $4.52 billion | $ | 1,500,000 | | $ | 1,250,000 | |

| Adjusted homebuilding operating margin** | 4.5% | 6.2% | 9.0% | $ | 1,500,000 | | $ | 1,250,000 | |

| Diluted adjusted pre-tax EPS* | $2.98 | $4.48 | $7.38 | $ | 1,500,000 | | $ | 1,250,000 | |

| Adjusted EBITDA*** | $340 million | $446 million | $668.6 million | $ | 1,500,000 | | $ | 1,250,000 | |

| Total Additional Bonus | $ | 8,000,000 | | $ | 7,000,000 | |

| | | | | |

| Total Incentive Bonus (Lesser of $7 million and $6 million for the Executive Chairman and CEO, respectively, or the calculated amount) | $ | 7,000,000 | | $ | 6,000,000 | |

* Adjusted pre-tax return / income is a non-GAAP financial measure and is defined as pre-tax income before expenses derived from impairments,executivestock-based compensation expenseabove the budgeted amount, warranty reserve adjustments, non-recurring or out-of-period charges and the effect of changes in laws, regulations or accounting principles divided by diluted weighted shares outstanding.

** Adjusted homebuilding operating margin is a non-GAAPfinancial measure and is defined as gross margin from home sales less homebuilding SG&A expense, before expenses derived from impairments,executivestock-based compensation expenseabove the budgeted amount, warranty reserve adjustments, non-recurring or out-of-period charges and the effect of changes in laws, regulations or accounting principles divided by home sale revenues.

*** Adjusted EBITDA is a non-GAAPfinancial measureand is defined as earnings before interest, taxes, depreciation, amortization, non-cash charges derived from impairments, stock-based compensation expense, abandoned project costs, warranty reserve adjustments, non-recurring or out-of-period charges and the effect of changes in laws, regulations or accounting principles.

Bonus Payment Cap

The 2023 annual incentive bonus for the Executive Chairman and CEO (the ROE Condition Bonus plus the Additional Bonus Opportunity) was subject to a $7.0 million and $6.0 million cap (the “Bonus Cap”), respectively. The Bonus Cap was established by the Compensation Committee based on guidance from its Compensation Consultant taking into account each executive’s historic compensation, reference to executive compensation being awarded to the Company’s peer group and feedback from the Company's shareholders. The Bonus Cap was decreased during 2023 for both the Executive Chairman and CEO, consistent with the decrease in the Additional Bonus Opportunity discussed above.

This year, in light of the Company’s superior performance under the direction of Mr. Mizel and Mr. Mandarich, the Committee determined that an exercise of its discretion under the 2018 Performance-Based Plan was warranted to increase the bonus to be paid to each of Mr. Mizel and Mr. Mandarich by $1.0 million. Accordingly, the Committee awarded a total cash bonus for 2023 to Mr. Mizel of $8.0 million and a total cash bonus for 2023 to Mr. Mandarich of $7.0 million. The Committee made no award of restricted stock.

2023 CFO and General Counsel (CLO) Annual Incentive Bonus

The CFO and CLO positions are primarily responsible for accounting, finance, legal and regulatory compliance and, in the judgment of the Compensation Committee, their incentive compensation should not directly depend on the Company’s financial performance. Instead, the CFO and CLO were awarded a bonus opportunity measured by specific Key Performance Indicators (“KPIs”) established by the Compensation Committee, their attainment and a bonus payment commensurate with a percentage of their base pay. The Compensation Committee consults with the Executive Chairman and CEO with regard to their achievements. For 2023, the Compensation Committee established the following KPIs with the associated weighting:

Chief Financial Officer

•Shareholder relations management and oversight (15%)

•Timely and accurate handling of financial regulatory filings (30%)

•Oversight of accounting, finance, information technology and treasury functions, including capital markets and bank financing transactions, if applicable (40%)

•Successful completion of special projects - including ESG (15%)

General Counsel

•Litigation management (20%)

•Regulatory compliance (20%)

•Successful completion of special projects - including ESG (15%)

•Successful supervision of all real estate transactions (25%)

•Oversight of risk management (20%)

The actual bonus amounts were based on the level of the performance achieved:

•A target bonus of 100% of base salary if the Compensation Committee determined that each KPI was achieved.

•A maximum bonus of 200% of base salary if the Compensation Committee determined that each KPI has been exceeded at a level doubling the targeted performance.

•Proportionate bonus levels as a percentage of base salary to the extent some KPIs were partially achieved or exceeded.

Based on its evaluation of performance relative to the established KPIs, the Compensation Committee awarded Mr. Martin and Mr. Kaplan annual incentive bonuses for 2023 of $1,500,000 and $475,000, respectively, payable in cash. The Compensation Committee also awarded Mr. Martin $2.0 million in cash in lieu of a restricted stock award, for a total cash payment of $3.5 million.

Long-Term Incentive Compensation

For our Executive Chairman and CEO, the 2023 long-term equity grants were entirely in performance share units in order to objectively align the incentives of the Company’s management team with the interests of our shareholders. This was a change from prior year, based in part on shareholder feedback, where the long-term equity grants were comprised of stock options.

For our CFO, a portion of the 2023 long-term equity grant was delivered in performance share units with the remainder paid in cash in lieu of a restricted stock award as noted above. The Compensation Committee believes this is an appropriate balance of long-term incentive compensation to encourage the continued retention of the CFO and align his interests with the interests of our shareholders.

The long-term incentive program in 2023 includes metrics that measure the Company’s long-term value drivers related to the Company’s core business. The program is performance-based and designed to retain, motivate and reward our executive officers for achieving our strategic and financial long-term objectives through the use of performance share units.

| | | | | | | | | | | |

| Executive | Target | Threshold | Maximum |

| Executive Chairman | 200,000 shares | 50% of Target | 200% of Target |

| CEO | 180,000 shares | 50% of Target | 200% of Target |

| CFO | 17,500 shares | 50% of Target | 200% of Target |

The performance share units vest based on increasing average home sale revenues compared to home sale revenues over a base period, while maintaining a minimum average gross margin from home sales (excluding impairments) of at least fifteen percent (15%).

| | | | | | | | | | | | | | |

| Long-Term Incentive Program |

| Performance Metric | Base | Threshold | Target | Maximum |

| Gross Margin from Home Sales (Excluding Impairments) | 15% Average Gross Margin from Home Sales requirement |

| Home Sale Revenues (in billions) | $4.52 | $4.75* | $4.97* | $5.42* |

* Average over Performance Period

Peer Data

The Compensation Committee utilized peer data as a reference when it considered the incentives and compensation plan design. It was not employed for benchmarking purposes. Rather, the peer group information was considered for broad subjective comparisons and not as an objective metric.

| | | | | | | | |

| Homebuilder Peer Group Companies (the “Peer Group”) |

Beazer Homes USA, Inc.

D.R. Horton, Inc.

Hovnanian Enterprises, Inc.

KB Home | Lennar Corporation

Meritage Homes Corporation

M/I Homes Inc. | NVR, Inc.

PulteGroup, Inc.

Toll Brothers, Inc. |

The Compensation Committee chose these companies for their parallels to MDC's core business and markets, recognizing that their corporate structure, business strategies and risk profile may significantly vary from those of our Company.

The Compensation Committee refers to the Peer Group not only for compensation purposes, but also for business model and risk evaluation purposes, as discussed in more detail, below.

Role of Compensation Committee and Management

The Compensation Committee conducted a series of meetings beginning in March 2023 and continuing into February 2024, at which time the Compensation Committee developed its determinations regarding 2023 executive officer compensation. The following table summarizes the roles of the Compensation Committee, the Consultant and management in formulating their decisions on executive officer compensation:

| | | | | |

| Responsible Party | Roles and Responsibilities |

Compensation Committee of the Board of Directors TheCompensationCommittee currently is comprised of Independent Directors and reports to the Board. | ● Oversees all executive officer compensation levels, including benefits, having a goal to maintain compensation levels that are comparable to the marketplace and in conformity with shareholder interests. ● Administers the Company's current equity and other compensation plans and any additional plans adopted by the Company. ● Reviews and approves corporate goals and objectives relevant to Executive Chairman and CEO compensation. ● Evaluates the Executive Chairman and CEO's performance in light of set goals and objectives, and determines and approves the Executive Chairman and CEO's compensation level based on this evaluation. ● Has authority to determine and approve non-CEO compensation. ● Makes recommendations to the Board with respect to incentive-compensation plans and equity-based plans. ● Develops a compensation committee report on executive compensation as required by the SEC to be included in the Company's annual proxy statement or annual report on Form 10-K filed with the SEC. |

Consultant to the Compensation Committee WealthPoint, LLC, as anindependent Consultant, retained directly by the Compensation Committee, that provides consulting advice on matters of governance and executive compensation. | ● Provides advice and guidance on the appropriateness and competitiveness of our compensation programs relative to Company performance and market practice. ● Performs all functions at the direction of the Compensation Committee. ● Attends Compensation Committee meetings (including executive sessions, as required). ● Provides advice and guidance regarding governance issues bearing on the executive compensation determinations. ● Provides market data, as requested. ● Consults on various compensation matters and compensation program designs and practices. ● Conducts an assessment of the risks arising from our compensation programs. ● Confers with the Executive Chairman and CEO on behalf of the Compensation Committee concerning compensation, incentives and goals for other NEOs. ● Assists in selection of the Company’s peers. |

Executive Chairman and CEO With the support of other members of the management team. | ● Review performance of the CFO and CLO and makes recommendations to the Compensation Committee with respect to their compensation. ● Confer with the Compensation Committee concerning design and development of compensation and benefit plans for Company employees. |

Role of the Independent Compensation Consultant

The Compensation Committee has the authority to retain outside counsel, consultants and other advisors to assist it in evaluating compensation or in otherwise discharging its duties and responsibilities. After consideration of independence factors as required by the NYSE, the Compensation Committee engaged WealthPoint, LLC to advise the Committee in connection with year-end 2023 compensation determinations, the structuring of executive compensation for 2024 and the compensation

disclosures to be included in this Form 10-K/A. This consultant also assisted the Compensation Committee in determining appropriate peers for purposes of comparing (but not benchmarking) market compensation, and provided other related services.

WealthPoint, LLC has not provided any services to the Company or its affiliates other than the services provided to the Compensation Committee. After considering, among other matters, the absence of any business or personal relationship between the consultants and any member of the Compensation Committee or any executive officer of the Company, the Compensation Committee has concluded the consultant's services do not raise any conflicts of interest.

Other Compensation Considerations

Stock Ownership Guidelines

The Company has adopted formal equity ownership guidelines for the executive officers in order to expressly promote their continued short and long term financial alignment with the interests of the shareholders of the Company. Under the guidelines, each executive officer is encouraged to acquire and maintain ownership of common stock of the Company having an acquisition value of not less than the following multiple of the executive officer’s base annual salary:

| | | | | |

| Executive Officer | Multiple |

| Executive Chairman | 5X |

| CEO | 5X |

| All Others | 1X |

To expedite achievement of the goal set forth above, each executive officer who has not yet achieved the goal agrees to retain the shares they acquire through restricted stock awards, performance share units and the future exercise of employee stock options, net of taxes and any option exercise price, up to the number of shares necessary to achieve the goal. Messrs. Mizel, Mandarich and Martin have all achieved and maintain the stock ownership goal.

Anti-Hedging and Anti-Pledging Policies

Our executive officers (but not other employees) and our Directors are prohibited from acquiring an interest in financial instruments intended to hedge or offset any decrease in the market value of the Company’s stock held directly or indirectly by that person. They also are required to inform the Company’s compliance committee and obtain pre-clearance prior to purchasing Company stock on margin, margining Company stock or pledging Company stock as collateral for a loan.

Clawback Policy

On July 24, 2023, our Board adopted a Clawback Recovery Policy in compliance with NYSE listing standard Section 303A.14 and SEC Rule 10D-1. The policy requires the Company to recover the amount of "erroneously awarded" incentive-based compensation received by current or former executive officers in the event that the Company is required to prepare an accounting restatement due to material noncompliance with any financial reporting requirements under the securities laws.

Medical Insurance Benefits

Under the terms of their respective employment agreements, each of the Executive Chairman and CEO is entitled to medical insurance benefits for the duration of his life (described in more detail below under “Employment Agreements”).

Other Compensation

In 2023, our executive officers also received compensation in the form of 401(k) employer contributions, incremental travel expenses incurred by the Company in support of not-for-profit organizations (as approved by the Board), legal expenses associated with employment related matters and cell phone allowances.

The Board has determined that it is in the best interests of the Company for its Executive Chairman and its CEO to use the Company's aircraft for non-Company purposes, when the aircraft is not being employed in the ordinary course of Company business. These executive officers reimburse the Company for their non-Company use of the aircraft by paying the incremental cost incurred by the Company for each non-business use, defined as the total variable operating costs directly associated with non-business trips, which include fuel, pilot travel related costs, catering, landing fees, flight communications and trip-related maintenance (the “Incremental Cost”). For their non-business use of the aircraft in 2023, Messrs. Mizel and Mandarich reimbursed the Company for Incremental Cost of$550,291 and $51,631, respectively.

The objective of these benefits is to provide amenities to the Executive Chairman and CEO that allow them to more efficiently utilize their time and to support them in effectively contributing to the success of the Company.

Executive Compensation Tables

Summary Compensation Table

For the fiscal years ended December 31, 2023, 2022 and 2021, the following table summarizes the compensation of the Company’s named executive officers.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Name and

Principal Position | Year | Salary

($) | Bonus

($) | Stock Awards ($) 1 | Option Awards ($) 2 | Non-Equity Incentive Plan Comp ($) 3 | Change in Pension and Nonqualified Deferred Comp Earnings ($) | All Other Comp

($) | Total

($) |

Larry A. Mizel, Executive Chairman | 2023 | $ | 1,000,000 | | N/A | $ | 11,436,609 | | $ | — | | $ | 8,000,000 | | $ | — | | $ | 294,210 | | $ | 20,730,819 | |

| 2022 | $ | 1,000,000 | | N/A | $ | 1,999,966 | | $ | 8,342,900 | | $ | 7,000,000 | | $ | — | | $ | 169,570 | | $ | 18,512,436 | |

| 2021 | $ | 1,000,000 | | N/A | $ | 10,869,266 | | $ | — | | $ | 8,000,000 | | $ | — | | $ | 80,990 | | $ | 19,950,256 | |

David D. Mandarich, President and Chief Executive Officer | 2023 | $ | 1,000,000 | | N/A | $ | 10,592,946 | | $ | — | | $ | 7,000,000 | | $ | — | | $ | 25,939 | | $ | 18,618,885 | |

| 2022 | $ | 1,000,000 | | N/A | $ | 1,999,966 | | $ | 6,674,320 | | $ | 6,000,000 | | $ | — | | $ | 9,060 | | $ | 15,683,346 | |

| 2021 | $ | 1,000,000 | | N/A | $ | 9,982,336 | | $ | — | | $ | 6,000,000 | | $ | — | | $ | 10,279 | | $ | 16,992,615 | |

Robert N. Martin, Senior Vice President and Chief Financial Officer | 2023 | $ | 850,000 | | $ | 3,500,000 | | $ | 2,738,169 | | N/A | N/A | N/A | $ | 9,870 | | $ | 7,098,039 | |

| 2022 | $ | 850,000 | | $ | 1,500,000 | | $ | 1,999,966 | | N/A | N/A | N/A | $ | 9,420 | | $ | 4,359,386 | |

| 2021 | $ | 850,000 | | $ | 1,500,000 | | $ | 1,276,042 | | N/A | N/A | N/A | $ | 9,420 | | $ | 3,635,462 | |

Michael L. Kaplan,, Senior Vice President and General Counsel 4 | 2023 | $ | 475,000 | | $ | 475,000 | | $ | 99,978 | | N/A | N/A | N/A | $ | 727 | | $ | 1,050,705 | |

| 2022 | $ | 91,346 | | $ | 125,000 | | $ | 299,973 | | N/A | N/A | N/A | $ | 136 | | $ | 516,455 | |

1 The amounts shown in the "Stock Awards" column are based on the aggregate grant date fair value computed in accordance with FASB ASC Topic 718 of the following:

2023

–For Messrs. Mizel, Mandarich and Martin, Performance Share Units ("PSUs") were granted to each individual on August 23, 2023. These awards are performance based, and, therefore, the amounts in the table above include $8,436,621, $7,592,959 and $738,204 for Messrs. Mizel, Mandarich and Martin, respectively, reflecting the aggregate grant date fair value of the awards ($42.18) multiplied by the target number of shares. Assuming achievement of the highest level of performance for these awards, the grant date fair value of the performance-based equity awards for Messrs. Mizel, Mandarich and Martin total $16,873,242, $15,185,918 and $1,476,409, respectively.

–For each of Messrs. Mizel and Mandarich, this column includes $2,999,987 in Restricted Stock Awards ("RSAs") that were granted February 3, 2023 pursuant to the 2022 performance goals established under the terms of the 2018 Performance-Based Plan.

–For Mr. Martin and Mr. Kaplan, this column includes $1,999,965 and $99,978, respectively, in RSAs that were granted February 3, 2023 based on their 2022 performance.

2022

–For each of Messrs. Mizel and Mandarich, this column includes $1,999,966 in Restricted Stock Awards ("RSAs") that were granted February 3, 2022 pursuant to the 2021 performance goals established under the terms of the 2018 Performance-Based Plan.

–For Mr. Martin, this column includes $1,999,966 in a RSA that were granted February 3, 2022 based on his 2021 performance.

– For Mr. Kaplan, this column includes $299,973 in a RSA that were granted October 10, 2022 in connection with his hiring.

2021

–For Messrs. Mizel, Mandarich and Martin, Performance Share Units ("PSUs") were granted to each individual on July 14, 2021. These awards are performance based, and, therefore, the amounts in the table above include $8,869,300, $7,982,370 and $776,064 for Messrs. Mizel, Mandarich and Martin, respectively, reflecting the aggregate grant date fair value of the awards ($44.35) multiplied by the target number of shares. Assuming achievement of the highest level of performance for these awards, the grant date fair value of the performance-based equity awards for Messrs. Mizel, Mandarich and Martin total $17,738,601, $15,964,741 and $1,552,128, respectively.

–For each of Messrs. Mizel and Mandarich, this column also includes $1,999,966 in Restricted Stock Awards ("RSAs") that were granted February 4, 2021 pursuant to the 2020 performance goals established under the terms of the 2018 Performance-Based Plan.

–For Mr. Martin this column also includes $499,978 in RSAs that were granted February 4, 2021 based on his 2020 performance.

For a description of assumptions used in valuing the awards, please see Note 22(Stock Based Compensation) to the Consolidated Financial Statements in the Company's Original Form 10-K, for the year ended December 31,2023.

PART I

Forward-Looking2 The amounts shown in the "Option Awards" column are based on the aggregate grant date fair value computed in accordance with FASB ASC Topic 718. For Messrs. Mizel and Mandarich, the option awards granted in 2022 was service based, was assigned a fair value of $8.34 per share on the date of grant using the Black-Scholes option pricing model. For a description of the assumptions used in valuing the awards, please see Note 22 (Stock Based Compensation) to the Consolidated Financial Statements in the Company's Original Form 10-K for the year ended December 31, 2023.

3 These non-equity incentive plan compensation amounts were paid in cash in accordance with the terms of the 2018 Performance-Based Plan, as in effect for the year indicated, as compensation for that year's performance. The amounts were paid in the subsequent year. In the year ended 2023, the Committee determined that the 2023 goal established under the 2018 Performance-Based Plan for each executive had been achieved at the maximum level, thereby qualifying Mr. Mizel for a total bonus of $7.0 million and Mr. Mandarich for a total bonus of $6.0 million. The prior year, in light of economic conditions, the Committee exercised its discretion and reduced the cash awards to Mr. Mizel and Mr. Mandarich. This year, in light of the Company’s superior performance under the direction of Mr. Mizel and Mr. Mandarich, the Committee determined that an exercise of its discretion under the 2018 Performance-Based Plan was warranted to increase the bonus to be paid to each of Mr. Mizel and Mr. Mandarich by $1.0 million. Accordingly, the Committee awarded a total cash bonus for 2023 to Mr. Mizel of $8.0 million and a total cash bonus for 2023 to Mr. Mandarich of $7.0 million. The Committee made no award of restricted stock.

4 Mr. Kaplan was appointed as Senior Vice President and General Counsel effective as of October 10, 2022. On October 24, 2022, Mr. Kaplan was designated as an executive officer and a named executive officer of the Company.

All Other Compensation

The table below provides a breakdown of all other compensation for 2023 for the named executive officers:

| | | | | | | | | | | | | | | | | |

| Name | Non-

Business

Use of

Aircraft | | 401(k) Match 2 | Other 3 | Total |

| Larry A. Mizel | — | | 1 | $ | 9,150 | | $ | 285,060 | | $ | 294,210 | |

| David D. Mandarich | — | | 1 | $ | 9,150 | | $ | 16,789 | | $ | 25,939 | |

| Robert N. Martin | N/A | | $ | 9,150 | | $ | 720 | | $ | 9,870 | |

| Michael L. Kaplan | N/A | | $ | — | | $ | 727 | | $ | 727 | |

1The incremental costs of non-business use of the Company's aircraft are calculated as the total variable operating costs directly associated with non-business trips, which include fuel, pilot travel related costs, catering, landing fees, flight communications and trip-related maintenance (the “Incremental Cost”). For theirnon-businessuse of the aircraft in 2023, Messrs.Mizeland Mandaricheachreimbursed the Companyfor the Incremental Cost.

2401(k) match represents amounts paid in 2024based on 2023401(k) deferrals.

3For Mr. Mizel, the amounts shown for “Other” consists of $267,911of Incremental Costs incurred by the Company in support of Mr. Mizel's service to not-for-profit organizations, consistent with the Company’s commitment to sustainability andas approved by the Company's Board. For both Mr. Mizel and Mr. Mandarich, "Other" also consists of $16,429 for legal

expenses in connection with employment related matters. The remainder of the amount shown for Mr. Mizel and Mr. Mandarich and all of the amounts shown for the other NEOs represent cell phone allowances.

Grants of Plan-Based Awards in 2023

The following table sets forth certain information with respect to awards granted during 2023 to our named executive officers. All equity awards were made under the 2021 Equity Incentive Plan.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Estimated possible payouts under non-equity incentive plan awards | | Estimated payouts under equity incentive plan awards 3 | | All other stock

awards: Number

of shares of stock or units

(#) | | Exercise or

Base Price

of Option Awards

($/Sh) | Grant Date

Fair Value of

Stock and Option Award

($) |

| Name | Grant Date | Threshold ($) | Target ($) | Threshold (#) | Target (#) | Maximum (#) | |

| Larry A. Mizel | — | 5,400,000 | | 7,000,000 | | 1 | | | | | | | | $ | — | |

| Larry A. Mizel | 2/3/2023 | | | | | | | | 74,386 | | 2 | | $ | 2,999,987 | |

| Larry A. Mizel | 8/23/2023 | | | | 100,000 | 200,000 | 400,000 | | | | | $ | 8,436,621 | |

| David D. Mandarich | — | 5,400,000 | 6,000,000 | 1 | | | | | | | | $ | — | |

| David D. Mandarich | 2/3/2023 | | | | | | | | 74,386 | 2 | | $ | 2,999,987 | |

| David D. Mandarich | 8/23/2023 | | | | 90,000 | 180,000 | 360,000 | | | | | $ | 7,592,959 | |

| Robert N. Martin | 2/3/2023 | | | | | | | | 49,590 | | 2 | | $ | 1,999,965 | |

| Robert N. Martin | 8/23/2023 | | | | 8,750 | 17,500 | 35,000 | | | | | $ | 738,204 | |

| Michael L. Kaplan | 2/3/2023 | | | | | | | | 2,479 | 2 | | $ | 99,978 | |

1Messrs. Mizel and Mandarich had the opportunity to earn a threshold award of up to $5,400,000 based on specified performance criteria, and to receive a total cash bonus up to $7,000,000 and $6,000,000, respectively, based on the Company's outperformance of goals. As discussed above, the Committee determined that an exercise of its discretion under the 2018 Performance-Based Plan was warranted to increase the bonus to be paid to each of Mr. Mizel and Mr. Mandarich by $1.0 million. Accordingly, the Committee awarded a total cash bonus for 2023 to Mr. Mizel of $8.0 million and a total cash bonus for 2023 to Mr. Mandarich of $7.0 million. The Committee made no award of restricted stock.

2The restricted stock award vests equally over three years, starting with February 3, 2024. Dividends are paid on the restricted stock. The restricted stock granted in 2023 was based on 2022 performance.

3The PSUs will be earned based upon the Company’s performance, over a three year period commencing January 1, 2023 and ending December 31, 2025 (the “Performance Period”), measured by increasing average home sale revenues over the Base Period. The “Base Period” for the awards is January 1, 2023 to December 31, 2023. The awards are conditioned upon the Company achieving a minimum average gross margin from home sales percentage (excluding impairments) of at least fifteen percent (15%) over the Performance Period. If average home sale revenues over the Performance Period ("Performance Revenues") exceed the Base Revenues by at least 5% but less than 10% (“Threshold Goals”), 50% of the Target Goals will be earned. If Performance Revenues exceed the Base Revenues by at least 20%, 200% of the Target Goals will be earned (“Maximum Goals”). The number of PSUs earned under these grants shall be adjusted to be proportional to the partial performance between the Threshold Goals, Target Goals and Maximum Goals.

Outstanding Equity Awards at December 31, 2023

The table below sets forth information with respect to all unexercised options, unvested restricted stock and unvested performance share units awarded to our named executive officers that were outstanding as of December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Option Awards | | Stock Awards |

| Name | Number of

Securities Underlying Unexercised

Options (#) Exercisable | Number of

Securities Underlying Unexercised

Options (#) Unexercisable | | Option

Exercise

Price

($) | Option

Expiration

Date | | Number of

Shares or

Units of

Stock

That Have

Not Vested

(#) | | Market

Value of

Shares or

Units of

Stock That

Have Not

Vested

($) | Equity

Incentive

Plan

Awards:

Number of

Unearned

Units That

Have Not

Vested

(#) | | Equity

Incentive

Plan

Awards:

Market

Value of

Unearned

Units That

Have Not

Vested ($) |

| Larry A. Mizel | 233,280 | | — | | | 26.40 | | 5/23/2028 | | — | | | — | | — | | | — | |

| | 216,000 | | — | | | 32.92 | | 8/5/2029 | | — | | | — | | — | | | — | |

| | 216,000 | | — | |

| 23.90 | | 4/27/2030 | | — | | | — | | — | | | — | |

| | 333,400 | | 666,600 | | 1 | 28.78 | | 9/28/2032 | | — | | | — | | — | | | — | |

| | — | | — | | | — | | — | | | 12,770 | | 2 | 705,543 | | — | | | — | |

| | — | | — | | | — | | — | | | 28,556 | | 3 | 1,577,719 | | — | | | — | |

| | — | | — | | | — | | — | | | 74,386 | | 4 | 4,109,827 | | — | | | — | |

| | — | | — | | | — | | — | | | — | | | — | | 400,000 | | 5 | 22,100,000 | |

| | — | | — | | | — | | — | | | — | | | — | | 100,000 | | 6 | 5,525,000 | |

| David D. Mandarich | 233,280 | | — | | | 26.40 | | 5/23/2028 | | — | | | — | | — | | | — | |

| | 216,000 | | — | | | 32.92 | | 8/5/2029 | | — | | | — | | — | | | — | |

| | 216,000 | | — | | | 23.90 | | 4/27/2030 | | — | | | — | | — | | | — | |

| | 266,720 | | 533,280 | | 1 | 28.78 | | 9/28/2032 | | — | | | — | | — | | | — | |

| | — | | — | | | — | | — | | | 12,770 | | 2 | 705,543 | | — | | | — | |

| | — | | — | | | — | | — | | | 28,556 | | 3 | 1,577,719 | | — | | | — | |

| | — | | — | | | — | | — | | | 74,386 | | 4 | 4,109,827 | | — | | | — | |

| | — | | — | | | — | | — | | | — | | | — | | 360,000 | | 5 | 19,890,000 | |

| | — | | — | | | — | | — | | | — | | | — | | 90,000 | | 6 | 4,972,500 | |

| Robert N. Martin | — | | — | | | — | | — | | | — | | | — | | — | | | — | |

| — | | — | | | — | | — | | | — | | | — | | — | | | — | |

| — | | — | | | — | | — | | | 3,193 | | 2 | 176,413 | | — | | | — | |

| — | | — | | | — | | — | | | 28,556 | | 3 | 1,577,719 | | — | | | — | |

| — | | — | | | — | | — | | | 49,590 | | 4 | 2,739,848 | | — | | | — | |

| — | | — | | | — | | — | | | — | | | — | | 35,000 | | 5 | 1,933,750 | |

| — | | — | | | — | | — | | | — | | | — | | 8,750 | | 6 | 483,438 | |

| Michael L. Kaplan | — | | — | | | — | | — | | | 6,879 | | 7 | 380,065 | | — | | | — | |

| — | | — | | | — | | — | | | 2,479 | | 4 | 136,965 | | — | | | — | |

1 This option vested immediately and will become exercisable as to 50% of the shares on each of September 28, 2024 and 2025.

2 Therestrictions on these shares lapse as to 100% of the remaining shares on February 4, 2024.

3The restrictions on these shares lapse as to 50% of the remaining shares on each of February 3, 2024 and 2025.

4The restrictions on these shares lapse as to 33-1/3% of the shares on each of February 3, 2024, 2025 and 2026.

5The PSUs will be earned based upon the Company’s performance, over a three year period commencingJanuary 1, 2021and endingDecember31, 2023. For more detail of the vesting terms see Note 22(Stock Based Compensation) to the Consolidated Financial Statements in the Company's Original Form 10-K for the year ended December 31, 2023.

6 The PSUs will be earned based upon the Company’s performance, over a three year period commencingJanuary 1, 2023and endingDecember31, 2025. For more detail of the vesting terms see Note 22(Stock Based Compensation) to the Consolidated Financial Statements in the Company's Original Form 10-K for the year ended December 31, 2023.

7 The restrictions on these shares lapse as to50%of theremainingshareson each of October 10, 2024 and 2025.

Option Exercises and Stock Vested in 2023

The following table provides additional information about value realized by the named executive officers on option award exercises and restricted stock award vestings during the year ended December 31, 2023.

| | | | | | | | | | | | | | | | | | | | | | | |

| | Option Awards | | Stock Awards |

| | Number of

Shares Acquired

on Excercise

(#) | | Value

Realized on

Exercise

($) | | Number of

Shares Acquired

on Vesting

(#) | | Value

Realized on

Vesting

($) |

| Larry A. Mizel | 1,322,697 | | | 30,090,166 | | | 302,774 | | | 12,210,875 | |

| David D. Mandarich | — | | | — | | | 302,774 | | | 12,210,875 | |

| Robert N. Martin | 33,065 | | | 805,453 | | | 85,369 | | | 3,442,932 | |

| Michael L. Kaplan | — | | | — | | | 3,440 | | | 138,873 | |

Pension Benefits at December 31, 2023

The following table shows, as of December 31, 2023, the present value of accumulated post-retirement medical insurance benefits under the current employment agreements of Mr. Mizel and Mr. Mandarich.

| | | | | | | | | | | | | | | | | | | | | | | |

| Name | Plan Name | | Number of

Years Credited

Service (#) | | Present Value of

Accumulated

Medical Insurance

Benefits

($) | | Payments During

Last Fiscal Year

($) |

| Larry A. Mizel | Employment Agreement 1 | | N/A | | $ | 222,032 | | | N/A |

| David D. Mandarich | Employment Agreement 1 | | N/A | | $ | 297,968 | | | N/A |

| Robert N. Martin | N/A | | N/A | | N/A | | N/A |

| Michael L. Kaplan | N/A | | N/A | | N/A | | N/A |

1 Mr. Mizel is eligible to receive a Termination Payment, as described below under "Employment Agreements" upon Retirement, as described in his Employment Agreement, as his original Employment Term has been successfully completed. Mr. Mandarich will be eligible to receive a Termination Payment, as described below under "Employment Agreements" upon Retirement, as described in his Employment Agreement, following the successful completion of his current Employment Term.

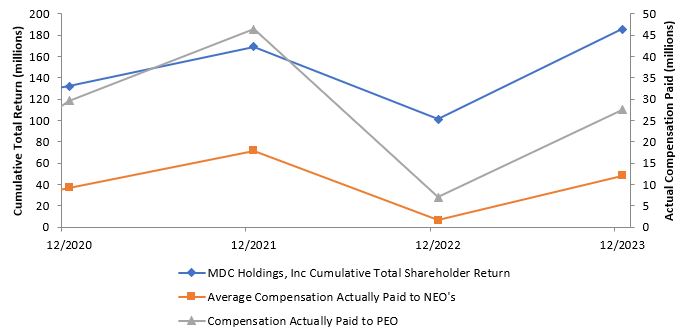

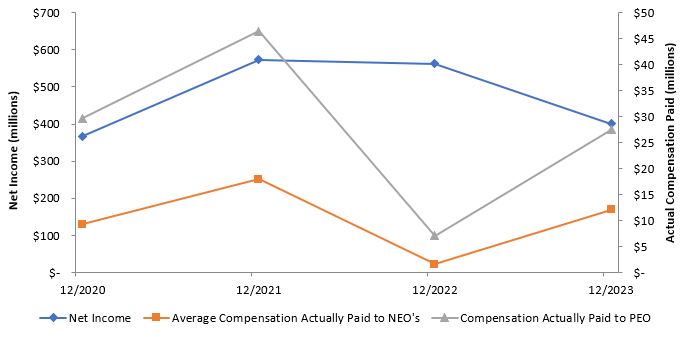

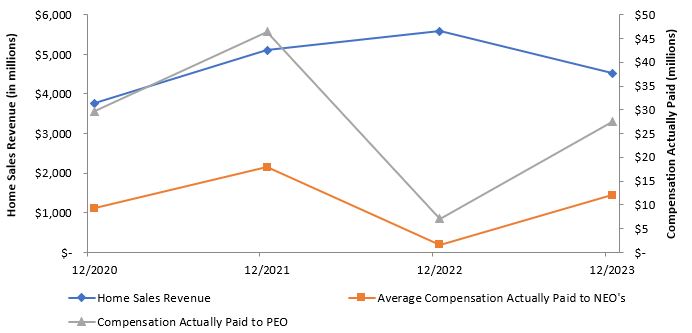

Pay Versus Performance

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year | Summary Compensation Table total For PEO 1 | Compensation Actually Paid to PEO 12 | Average Summary Compensation Table Total for Non-PEO NEOs 1 | Average Compensation Actually Paid to Non-PEO NEOs 12 | Value of Initial Fixed $100 Investment Based On: 11 | Net Income (Dollars in thousands) | Home Sale Revenues (Dollars in thousands) |

| Total Shareholder Return | Peer Group Total Shareholder Return 10 |

| 2023 | $ | 20,730,819 | | $ | 27,508,707 | | 2 | $ | 8,922,543 | | $ | 12,061,539 | | 6 | $ | 186 | | $ | 279 | | $ | 401,005 | | $ | 4,520,296 | |

| 2022 | $ | 18,512,436 | | $ | 7,050,930 | | 3 | $ | 5,207,073 | | $ | 1,591,502 | | 7 | $ | 101 | | $ | 151 | | $ | 562,139 | | $ | 5,586,264 | |

| 2021 | $ | 19,950,256 | | $ | 46,427,292 | | 4 | $ | 7,212,486 | | $ | 17,912,881 | | 8 | $ | 169 | | $ | 190 | | $ | 573,657 | | $ | 5,102,456 | |

| 2020 | $ | 14,150,011 | | $ | 29,684,799 | | 5 | $ | 4,762,382 | | $ | 9,243,394 | | 9 | $ | 132 | | $ | 124 | | $ | 367,582 | | $ | 3,765,379 | |

1The PEO for each of the years presented within this table is Larry A. Mizel, Executive Chairman. The NEO's for 2023 were David D. Mandarich, CEO; Robert N. Martin, CFO; Michael L. Kaplan, CLO. The NEO's for 2022 were David D. Mandarich, CEO; Robert N. Martin, CFO; Michael L. Kaplan, CLO (hired in 2022); and Rebecca B. Givens, CLO (resigned in 2022). The NEO's for 2021 were David D. Mandarich, CEO; Robert N. Martin, CFO; and Rebecca B. Givens, CLO. The NEO's for 2020 were David D. Mandarich, CEO; Robert N. Martin, CFO; Rebecca B. Givens, CLO (hired in 2020); and Michael Touff, CLO (retired in 2020).

2 For compensation actually paid to the PEO in 2023, the Summary Compensation Table total for the PEO is adjusted to reflect the changes in the value of equity awards and pension benefits, described in the following: (1) $11,436,609 was deducted from the total, representing the amount reported in the Stock Awards and Option Awards columns of the Summary Compensation Table; (2) $4,109,827 was added representing the year-end 2023 valuation of the equity awards granted in 2023 that remained outstanding and unvested as of December 31, 2023; (3) $11,218,458 was added representing the increase in fair value between the year end 2023 and 2022 for equity awards granted in prior years that remain outstanding and unvested at the end of 2023; (4) $2,643,217 was added representing the increase in fair value for equity awards granted in prior years that vested during 2023, and; (5) $242,995 was added related to dividends paid on outstanding and unvested RSA awards in 2023.