UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

——————————

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 20162018

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM TO

|

| | | | |

Commission File Number | | Registrants, State of Incorporation, Address, and Telephone Number | | I.R.S. Employer Identification No. |

| | | | |

| 001-09120 | | PUBLIC SERVICE ENTERPRISE GROUP INCORPORATED | | 22-2625848 |

| | | (A New Jersey Corporation) | | |

| | | 80 Park Plaza | | |

| | | Newark, New Jersey 07102 | | |

| | | 973 430-7000 | | |

| | | http://www.pseg.com | | |

| 001-00973 | | PUBLIC SERVICE ELECTRIC AND GAS COMPANY | | 22-1212800 |

| | | (A New Jersey Corporation) | | |

| | | 80 Park Plaza | | |

| | | Newark, New Jersey 07102 | | |

| | | 973 430-7000 | | |

| | | http://www.pseg.com | | |

| 001-34232 | | PSEG POWER LLC | | 22-3663480 |

| | | (A Delaware Limited Liability Company) | | |

| | | 80 Park Plaza | | |

| | | Newark, New Jersey 07102 | | |

| | | 973 430-7000 | | |

| | | http://www.pseg.com | | |

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | |

| Registrant | | Title of Each Class | | Name of Each Exchange On Which Registered |

Public Service Enterprise Group Incorporated | | Common Stock without par value | | New York Stock Exchange |

| | | First and Refunding Mortgage Bonds | | |

Public Service Electric and Gas Company | | 9 1/4%4% Series CC, due 2021 | | New York Stock Exchange |

| | 8%, due 2037 | | |

| | | 5%, due 2037 | | |

| PSEG Power LLC | | 8 5/8%8% Senior Notes, due 2031 | | New York Stock Exchange |

(Cover continued on next page)

(Cover continued from previous page)

|

| | |

| Securities registered pursuant to Section 12(g) of the Act: |

| Registrant | | Title of Each Class |

Public Service Electric and Gas Company | | Medium-Term Notes |

| | | |

| PSEG Power LLC | | Limited Liability Company Membership Interest |

Indicate by check mark whether each registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

| | | | |

| Public Service Enterprise Group Incorporated | | Yes x | | No ¨ |

| Public Service Electric and Gas Company | | Yes x | | No ¨ |

| PSEG Power LLC | | Yes x | | No ¨ |

Indicate by check mark if each of the registrants is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether each of the registrants (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrants were required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrants were required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether each registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”filer,” “smaller reporting company,” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | |

| Public Service Enterprise Group Incorporated | | Large accelerated filer x | | Accelerated filer ¨o | | Non-accelerated filer ¨o | Smaller reporting company o | Emerging growth company o |

| | | | | |

| Public Service Electric and Gas Company | | Large accelerated filer ¨o | | Accelerated filer ¨o | | Non-accelerated filer x | Smaller reporting company o | Emerging growth company o |

| | | | | |

| PSEG Power LLC | | Large accelerated filer ¨o | | Accelerated filer ¨o | | Non-accelerated filer x | Smaller reporting company o | Emerging growth company o |

If any of the registrants is an emerging growth company, indicate by check mark if such registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether any of the registrants is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the Common Stock of Public Service Enterprise Group Incorporated held by non-affiliates as of June 30, 20162018 was $23,504,828,537$27,172,268,280 based upon the New York Stock Exchange Composite Transaction closing price.

The number of shares outstanding of Public Service Enterprise Group Incorporated’s sole class of Common Stock as of February 17, 201715, 2019 was 506,217,300.504,999,536.

As of February 17, 2017,15, 2019, Public Service Electric and Gas Company had issued and outstanding 132,450,344 shares of Common Stock, without nominal or par value, all of which were privately held, beneficially and of record, by Public Service Enterprise Group Incorporated.

Public Service Electric and Gas Company and PSEG Power LLC are wholly owned subsidiaries of Public Service Enterprise Group Incorporated and each meet the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K. Each is filing its Annual Report on Form 10-K with the reduced disclosure format authorized by General Instruction I.

DOCUMENTS INCORPORATED BY REFERENCE |

| | |

Part of Form 10-K of Public Service Enterprise Group Incorporated | | Documents Incorporated by Reference |

| III | | Portions of the definitive Proxy Statement for the 20172019 Annual Meeting of Stockholders of Public Service Enterprise Group Incorporated, which definitive Proxy Statement is expected to be filed with the Securities and Exchange Commission on or about March 14, 2017,12, 2019, as specified herein. |

|

| | |

| | Page |

| FORWARD-LOOKING STATEMENTS | |

FILING FORMAT AND GLOSSARY | |

| WHERE TO FIND MORE INFORMATION | |

| PART I | | |

| Item 1. | Business | |

| | Regulatory Issues | |

| | Environmental Matters | |

| Segment Information | |

| | Executive Officers of the Registrant (PSEG) | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

| PART II | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | Selected Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| | Executive Overview of 20162018 and Future Outlook | |

| | Results of Operations | |

| | Liquidity and Capital Resources | |

| | Capital Requirements | |

| | Off-Balance Sheet Arrangements | |

| | Critical Accounting Estimates | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| | Report of Independent Registered Public Accounting Firm | |

| | Consolidated Financial Statements | |

| | Notes to Consolidated Financial Statements | |

| | Note 1. Organization, Basis of Presentation and Summary of Significant Accounting Policies | |

| | Note 2. Recent Accounting Standards | |

| | Note 3. Early Plant RetirementsRevenues | |

| | Note 4. Variable Interest EntitiesEarly Plant Retirements | |

| | Note 5. Variable Interest Entity | |

| Note 6. Property, Plant and Equipment and Jointly-Owned Facilities | |

| Note 6. Regulatory Assets and Liabilities | |

| | Note 7. Long-Term InvestmentsRegulatory Assets and Liabilities | |

| | Note 8. Financing Receivables | |

| Note 9. Available-for-Sale SecuritiesLong-Term Investments | |

| | Note 10. Goodwill and Other Intangibles9. Financing Receivables | |

| Note 10. Trust Investments | |

| | Note 11. Asset Retirement Obligations (AROs)Goodwill and Other Intangibles | |

| | Note 12. Asset Retirement Obligations (AROs) | |

| Note 13. Pension, Other Postretirement Benefits (OPEB) and Savings Plans | |

| Note 13. Commitments and Contingent Liabilities | |

| | Note 14. DebtCommitments and Credit FacilitiesContingent Liabilities | |

| | Note 15. Debt and Credit Facilities | |

| Note 16. Schedule of Consolidated Capital Stock | |

| | Note 16. Financial Risk Management Activities | |

|

| | |

| | | |

| TABLE OF CONTENTS (continued) | |

| | Note 17. Financial Risk Management Activities | |

| | Page |

| | Note 17.18. Fair Value Measurements | |

| | Note 18.19. Stock Based Compensation | |

| | Note 19.20. Other Income and Deductions(Deductions) | |

| | Note 20.21. Income Taxes | |

| | Note 21.22. Accumulated Other Comprehensive Income (Loss), Net of Tax | |

| | Note 22.23. Earnings Per Share (EPS) and Dividends | |

| Note 23. Financial Information by Business Segment | |

| | Note 24. Related-Party TransactionsFinancial Information by Business Segment | |

| | Note 25. Selected Quarterly Data (Unaudited)Related-Party Transactions | |

| | Note 26. Selected Quarterly Data (Unaudited) | |

| Note 27. Guarantees of Debt | |

| Item 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| Item 9B. | Other Information | |

| PART III | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accounting Fees and Services | |

| PART IV | | |

| Item 15. | Exhibits, Financial Statement Schedules | |

| | Schedule II - Valuation and Qualifying Accounts | |

| Glossary of Terms | |

| | Signatures | |

| Exhibit Index | |

FORWARD-LOOKING STATEMENTS

Certain of the matters discussed in this report about our and our subsidiaries’ future performance, including, without limitation, future revenues, earnings, strategies, prospects, consequences and all other statements that are not purely historical constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties, which could cause actual results to differ materially from those anticipated. Such statements are based on management’s beliefs as well as assumptions made by and information currently available to management. When used herein, the words “anticipate,” “intend,” “estimate,” “believe,” “expect,” “plan,” “should,” “hypothetical,” “potential,” “forecast,” “project,” variations of such words and similar expressions are intended to identify forward-looking statements. Factors that may cause actual results to differ are often presented with the forward-looking statements themselves. Other factors that could cause actual results to differ materially from those contemplated in any forward-looking statements made by us herein are discussed in Item 1A. Risk Factors, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A), Item 8. Financial Statements and Supplementary Data—Note 13.14. Commitments and Contingent Liabilities, and other filings we make with the United States Securities and Exchange Commission (SEC), including our subsequent reports on Form 10-Q and Form 8-K. These factors include, but are not limited to:

fluctuations in wholesale power and natural gas markets, including the potential impacts on the economic viability of our generation units;

our ability to obtain adequate fuel supply;

any inability to manage our energy obligations with available supply;

PSE&G’s proposed investment programs may not be fully approved by regulators and its capital investment may be lower than planned;

increases in competition in wholesale energy and capacity markets;

changes in technology related to energy generation, distribution and consumption and customer usage patterns;

economic downturns;

third-party credit risk relating to our sale of generation output and purchase of fuel;

adverse performance of our decommissioning and defined benefit plan trust fund investments and changes in funding requirements;

changes in state and federal legislation and regulations;regulations, and PSE&G’s ability to recover costs and earn returns on authorized investments;

the impact of pendingany future rate case proceedings;

regulatory, financial, environmental, health and safety risks associated with our ownership and operation of nuclear facilities;facilities, including regulatory risks, such as compliance with the Atomic Energy Act and trade control, environmental and other regulations, as well as financial, environmental and health and safety risks;

the impact on our New Jersey nuclear plants of the failure of such plants to be selected to participate in the Zero Emissions Certificate (ZEC) program or adverse changes to the capacity market construct;

adverse changes in energy industry laws, policies and regulations, including market structures and transmission planning;

changes in federal and state environmental regulations and enforcement;

delays in receipt of, or an inability to receive, necessary licenses and permits;

adverse outcomes of any legal, regulatory or other proceeding, settlement, investigation or claim applicable to us and/or the energy industry;

changes in tax laws and regulations;

the impact of our holding company structure on our ability to meet our corporate funding needs, service debt and pay dividends;

lack of growth or slower growth in the number of customers or changes in customer demand;

any inability of Power to meet its commitments under forward sale obligations;

reliance on transmission facilities that we do not own or control and the impact on our ability to maintain adequate transmission capacity;

any inability to successfully develop, obtain regulatory approval for, or construct generation, transmission and distribution projects;

any equipment failures, accidents, severe weather events or other incidents that impact our ability to provide safe and reliable service to our customers;

our inability to exercise control over the operations of generation facilities in which we do not maintain a controlling interest;

any inability to recover the carrying amount of our long-lived assets and leveraged leases;

any inability to maintain sufficient liquidity;

any inability to realize anticipated tax benefits or retain tax credits;

challenges associated with recruitment and/or retention of key executives and a qualified workforce;

the impact of our covenants in our debt instruments on our operations; and

the impact of acts of terrorism, cybersecurity attacks or intrusions.

All of the forward-looking statements made in this report are qualified by these cautionary statements and we cannot assure you that the results or developments anticipated by management will be realized or even if realized, will have the expected consequences to, or effects on, us or our business, prospects, financial condition, results of operations or cash flows. Readers are cautioned not to place undue reliance on these forward-looking statements in making any investment decision. Forward-looking statements made in this report apply only as of the date of this report. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so, even in light of new information or future events, unless otherwise required by applicable securities laws.

The forward-looking statements contained in this report are intended to qualify for the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

FILING FORMAT AND GLOSSARY

This combined Annual Report on Form 10-K is separately filed by Public Service Enterprise Group Incorporated (PSEG), Public Service Electric and Gas Company (PSE&G) and PSEG Power LLC (Power). Information relating to any individual company is filed by such company on its own behalf. PSE&G and Power are each only responsible for information about itself and its subsidiaries.

Discussions throughout the document refer to PSEG and its direct operating subsidiaries, PSE&G and Power. Depending on the context of each section, references to “we,” “us,” and “our” relate to PSEG or to the specific company or companies being discussed. In addition, certain key acronyms and definitions are summarized in a glossary beginning on page 193.

WHERE TO FIND MORE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. You may read and copy any document that we file at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. You may also obtain our filed documents from commercial document retrieval services, the SEC’s internet website at www.sec.gov or our website at www.pseg.com. Information on our website should not be deemed incorporated into or as a part of this report. Our Common Stock is listed on the New York Stock Exchange under the tickertrading symbol PEG. You can obtain information about us at the offices of the New York Stock Exchange, Inc., 20 Broad11 Wall Street, New York, New York 10005.

PART I

ITEM 1. BUSINESS

We were incorporated under the laws of the State of New Jersey in 1985 and our principal executive offices are located at 80 Park Plaza, Newark, New Jersey 07102. We conduct our business through two direct wholly owned subsidiaries, PSE&G and Power, each of which also has its principal executive offices at 80 Park Plaza, Newark, New Jersey 07102.

We are an energy company with a diversified business mix. Our operations are located primarily in the Northeastern and Mid- Atlantic United States. Our business approach focuses on operational excellence, financial strength and disciplined investment. As a holding company, our profitability depends on our subsidiaries’ operating results. Below are descriptions of our two principal direct operating subsidiaries.

|

| | | | |

| | PSE&G | | Power | |

| | | | |

| | A New Jersey corporation, incorporated in 1924, which is a franchised public utility in New Jersey. It is also the provider of last resort for gas and electric commodity service for end users in its service territory. Earns revenues from its regulated rate tariffs under which it provides electric transmission and electric and gas distribution to residential, commercial and industrial customers in its service territory. It also offers appliance services and repairs to customers throughout its service territory. Has also implementedAlso invests in regulated demand responsesolar generation projects and regulated energy efficiency and related programs and invested in solar generation within New Jersey.

| | A Delaware limited liability company formed in 1999 as a result of the deregulation and restructuring of the electric power industry in New Jersey. It integrates the operations of its merchant nuclear and fossil generating assets with its wholesale power marketing businesses and fuel supply functions through competitive energy sales in well-developed energy markets and fuel supply functions.markets. Earns revenues from the generation and marketing of power and natural gas to hedge business risks and optimize the value of its portfolio of power plants, other contractual arrangements and oil and gas storage facilities. This is achieved primarily by selling power and transacting in natural gas and other energy-related products, on the spot market or using short-term or long-term contracts for physical and financial products. Also earns revenues from solar generation facilities under long-term sales contracts for power and environmental products.

| |

| | | | | |

Our other direct wholly owned subsidiaries are: PSEG Long Island LLC (PSEG LI), which operates the Long Island Power Authority’s (LIPA) electric transmission and distribution (T&D) system under a contractual agreement; PSEG Energy Holdings L.L.C. (Energy Holdings), which earns its revenues primarily from its portfolio of lease investments; PSEG Long Island LLC (PSEG LI), which operates the Long Island Power Authority’s (LIPA) transmission and distribution (T&D) system under a contractual agreement; and PSEG Services Corporation (Services), which provides us and our operating subsidiaries with certain management, administrative and general services at cost.

The following is a more detailed description of our business, including a discussion of our:

Business Operations and Strategy

Competitive Environment

Employee Relations

Regulatory Issues

Environmental Matters

BUSINESS OPERATIONS AND STRATEGY

PSE&G

Our regulated transmission and distribution (T&D) public utility, PSE&G, distributes electric energy and gas to customers within a designated service territory running diagonally across New Jersey where approximately 6.2 million people, or about 70% of

New Jersey’s population resides.

.

Products and Services

Our utility operations primarily earn margins through the transmission and distributionT&D of electricity and the distribution of gas.

Transmission—the movement of electricity at high voltage from generating plants to substations and transformers, where it is then reduced to a lower voltage for distribution to homes, businesses and industrial customers. Our

revenues for these services are based upon tariffs approved by the Federal Energy Regulatory Commission (FERC).

Distribution—the delivery of electricity and gas to the retail customer’s home, business or industrial facility. Our revenues for these services are based upon tariffs approved by the New Jersey Board of Public Utilities (BPU).

The commodity portion of our utility business’ electric and gas sales is managed by basic generation service (BGS) and basic gas supply service (BGSS) suppliers. Pricing for those services areis set by the BPU as a pass-through, resulting in no margin for our utility operations.

We also earn margins through competitive services, such as appliance repair.repair, in our service territory.

In addition to our current utility products and services, we have implemented several programs to invest in regulated solar generation within New Jersey, including:

programs to help finance the installation of solar power systems throughout our electric service area, and

programs to develop, own and operate solar power systems.

We have also implemented a set of energy efficiency and demand response programs to encourage conservation and energy efficiency by providing energy and cost savingcost-saving measures directly to businesses and families. For additional information concerning these programs and the components of our tariffs, see Regulatory Issues—State Regulation and Item 8. Financial Statements and Supplementary Data—Note 6. Regulatory Assets and Liabilities.

How PSE&G Operates

We are a transmission owner in PJM Interconnection, L.L.C. (PJM) and we provide distribution service to 2.22.3 million electric customers and 1.8 million gas customers in a service area that covers approximately 2,600 square miles running diagonally across New Jersey. We serve the most heavilydensely populated, commercialized and industrialized territory in New Jersey, including its six largest cities and approximately 300 suburban and rural communities.

Transmission

We use formula rates for our transmission cost of service and investments. Formula-type rates provide a method of rate recovery where the transmission owner annually determines its revenue requirements through a fixed formula that considers Operation and Maintenance expenditures, rate base and capital investments and applies an approved return on equity (ROE) in developing the weighted average cost of capital. Under this formula, rates are put into effect in January of each year based upon our internal forecast of annual expenses and capital expenditures. Rates are subsequently trued up to reflect actual annual expenses and capital expenditures. Our current approved rates provide for a base ROE of 11.68% on existing and new transmission investment, while certain investments are entitled to earn an additional incentive rate. For more information, see Regulatory Issues—Federal Regulation.

We continue to invest in transmission projects that are included for review in the FERC-approved PJM transmission expansion process. These projects focus on reliability improvements and replacement of aging infrastructure with anticipatedplanned capital spendspending of $4.1$3.4 billion for transmission in 2017-20192019-2021 as disclosed in Item 7. MD&A—Capital Requirements.

Distribution

PSE&G distributes gas and electricity to end users in our respective franchised service territories. Our approved rates, established inIn October 2018, the BPU issued an Order approving the settlement of our most recent gas and electricdistribution base rate proceeding completed in mid-2010, providewith new rates effective November 1, 2018. The Order provides for a ROE of 10.3% on distribution rate base. We are required to filebase of $9.5 billion, a 9.60% ROE for our next distribution base rate case proceeding no later than November 1, 2017.business and a 54% equity component of our capitalization structure. The BPU has also approved a series of PSE&G infrastructure, energy efficiency and renewable energy investment programs with cost recovery through various clause mechanisms, with approved ROEs ranging from 9.75% to 10.3%.mechanisms. Our load requirements are split among residential, commercial and industrial customers, as described in the following table for 2016:2018:

|

| | | | | | |

| | | | | | | |

| | | | % of 2018 Sales | |

| | Customer Type | | Electric | | Gas | |

| | Commercial | | 58% | | 38% | |

| | Residential | | 33% | | 58% | |

| | Industrial | | 9% | | 4% | |

| | Total | | 100% | | 100% | |

| | | | | | | |

|

| | | | | | |

| | | | | | | |

| | | | % of 2016 Sales | |

| | Customer Type | | Electric | | Gas | |

| | Commercial | | 58% | | 37% | |

| | Residential | | 33% | | 59% | |

| | Industrial | | 9% | | 4% | |

| | Total | | 100% | | 100% | |

| | | | | | | |

While ourOur customer base has modestly increased since 2012,2014, with electric load has declined and gas load has increasedloads increasing as illustrated below:

|

| | | | | | | | | | | |

| | | | | | | | | | |

| | Electric and Gas Distribution Statistics | |

| | | | | | | |

| | | December 31, 2016 | | | |

| | | Number of Customers | | Electric Sales and Gas Firm Sales (A) | | Historical Annual Load Growth 2012-2016 | |

| | Electric | 2.2 |

| Million | | 41,580 |

| Gigawatt hours (GWh) | | (0.4)% | |

| | Gas | 1.8 |

| Million | | 2,360 |

| Million Therms | | 0.7% | |

| | | | | | | | | | |

|

| | | | | | | | | | | |

| | | | | | | | | | |

| | Electric and Gas Distribution Statistics | |

| | | | | | | |

| | | December 31, 2018 | | | |

| | | Number of Customers | | Electric Sales and Firm Gas Sales (A) | | Historical Annual Load Growth 2014-2018 | |

| | Electric | 2.3 |

| Million | | 41,889 |

| Gigawatt hours (GWh) | | 0.3% | |

| | Gas | 1.8 |

| Million | | 2,630 |

| Million Therms | | 1.7% | |

| | | | | | | | | | |

| |

| (A) | Excludes sales from Gas rate classes that do not impact margin, specifically Contract, Non-Firm Transportation, Cogeneration Interruptible and Interruptible Services. |

The declineElectric sales were essentially flat with increases due to growth in electric sales is the resultnumber of changes in customer usage patterns, includingcustomers and improved economic conditions offset by conservation and more energy efficient appliances. Gas firmFirm gas sales increased as a result of lowergrowth in the number of customers and customer response to continued low gas prices. Only firm gas firm sales impact margin.

During 2016, PSE&G as part ofcompleted its BPU-approved $1.2 billion Energy Strong Program I (ES I) in 2018. Under ES I, PSE&G, at an investment of $1 billion, completed the replacement and modernization of 240 miles of low-pressure cast iron gas mains in or near flood areas. PSE&G continues to execute the Energy Strong Program to (1) upgradeupgraded all of its electric substations that were damaged by water in recent storms; makemade investments that will create redundancy in the electric distribution system, reducing outages when damage occurs; and deploydeployed technologies to better monitor system operations, enabling PSE&G to restore customers more quickly in the event of an electric outage, and (2) with respect tooutage. Concerning PSE&G’s gas system, upgradePSE&G upgraded five natural gas metering stations, two liquefied propane stations and a liquefied natural gas station recently affected by severe weather or located in flood zones.

In 2018, PSE&G also commenced modernizingessentially completed its gas distribution system as part of our Gas System Modernization Program (GSMP)(GSMP I), which was approved by the BPU in late 2015. TheBy June 2019, through GSMP through whichI, we will invest $905have invested approximately $900 million over three years, willto replace approximately 510450 miles of cast iron and unprotected steel gas mains and about 38,00040,000 unprotected steel service lines to homes and businesses, including the uprating of the mains to higher pressure. The mains and service lines will bewere replaced with stronger, more durable plastic piping, reducing the potential for leaks and release of methane gas. The new elevated pressure systemssystem also enableincludes the installation of excess flow valves on each gas service that automatically shut off gas flow if a service line is abruptly damaged, and better supportsupports the use of high-efficiency appliances.

In May 2018, PSE&G received approval for the Gas System Modernization Program II (GSMP II), an expanded, five-year program to invest $1.9 billion over five years beginning in 2019 to replace approximately 875 miles of cast iron and unprotected steel mains in addition to other improvements to the gas system.

In June 2018, we filed for our Energy Strong Program II (ES II), a proposed five-year $2.5 billion program to harden, modernize and make our electric and gas distribution systems more resilient. The size and duration of ES II, as well as certain other elements of the program, are subject to BPU approval. A procedural schedule has been issued with the review process expected to conclude in mid-2019.

In October 2018, we filed our proposed Clean Energy Future (CEF) program with the BPU, a six-year estimated $3.6 billion investment program covering four programs; (i) an Energy Efficiency (EE) program totaling $2.5 billion of investment designed to achieve energy efficiency targets required under New Jersey’s Clean Energy law; (ii) an Electric Vehicle (EV) infrastructure program; (iii) an Energy Storage (ES) program and (iv) an Energy Cloud (EC) program which will include installing approximately two million electric smart meters and associated infrastructure. The procedural process for the CEF-EE program is expected to conclude by the third quarter of 2019. The CEF-EV/ES and CEF-EC programs will have separate procedural schedules. For additional information regarding the New Jersey Division of Rate Counsel’s motions related to these programs, see Item 7. MD&A—Executive Overview of 2018 and Future Outlook.

Solar Generation

In order toTo support New Jersey’s Energy Master Plan and the state’s renewable energy goals, we have undertaken two major solar initiatives at PSE&G, the Solar Loan Program and the Solar 4 All and Solar 4 All ExtensionAll® Programs. Our Solar Loan Program provides solar system financing to our residential and commercial customers. The loans are repaid with cash or solar renewable energy certificates (SRECs). We sell the SRECs received through periodic auctions and use the proceeds to offset program costs. Our Solar 4 All® Programs invest in utility-owned solar photovoltaic (PV) centralized solar systems installed on PSE&G property and third-party sites, including landfill facilities, and solar panels installed on distribution system poles in our electric service territory. We sell the energy and capacity from the systems in the PJM wholesale electricity market. In addition, we sell SRECs generated by the projects through the same periodic auction used in the loan program, the proceeds of which are used to offset program costs.

Supply

Although commodity revenues make up almost 41%39% of our revenues, we make no margin on the default supply of electricity and gas since the actual costs are passed through to our customers.

All electric and gas customers in New Jersey have the ability to choose their own electric energy and/or gas supplier. Pursuant to BPU requirements, we serve as the supplier of last resort for two types of electric and gas customers within our service territory that are not served by another supplier. The first type, which represents about 80% of PSE&G’s load requirements, provides default supply service for smaller commercial and industrial and commercial(C&I) customers and residential customers at seasonally-adjusted fixed prices for a three-year term (BGS-Residential Small Commercial Pricing (RSCP)). These rates change annually on June 1 and are based on the average price obtained at auctions in the current year and two prior years. The second type provides default supply for larger customers, with energy priced at hourly PJM real-time market prices for a contract term of 12 months (BGS-Commercial Industrial Energy Pricing (CIEP))Pricing).

We procure the supply to meet our BGS obligations through auctions authorized by the BPU for New Jersey’s total BGS requirement. These auctions take place annually in February. Results of these auctions determine which energy suppliers are authorized to supply BGS to New Jersey’s electric distribution companies (EDCs). Once validated by the BPU, electricity prices for BGS service are set. Approximately one-third of PSE&G’s total BGS-RSCP eligible load is auctioned each year for a three-year term. For information on current prices, see Item 8. Financial Statements and Supplementary Data—Note 13.14. Commitments and Contingent Liabilities.

PSE&G procures the supply requirements of its default service BGSS gas customers through a full-requirements contract with Power. The BPU has approved a mechanism designed to recover all gas commodity costs related to BGSS for residential customers. BGSS filings are made annually by June 1 of each year, with an effective date of October 1. PSE&G’s revenues are matched with its costs using deferral accounting, with the goal of achieving a zero cumulative balance by September 30 of each year. In addition, we have the ability to put in place two self-implementing BGSS increases on December 1 and February 1 of up to 5% and also may reduce the BGSS rate at any time and/or provide bill credits. See Item 8. Financial Statements and Supplementary Data—Note 6.7. Regulatory Assets and Liabilities for information on recent self-implementing credits.Liabilities. Any difference between rates charged under the BGSS contract and rates charged to our residential customers is deferred and collected or refunded through adjustments in future rates. Commercial and industrialC&I customers that do not select third-party suppliers are also supplied under the BGSS arrangement. These customers are charged a market-based price largely determined by prices for commodity futures contracts.

Markets and Market Pricing

Historically, there has been significant volatility in commodity prices. Such volatilityfluctuations can have a considerable impact on us since a rising commodity price environment results in higher delivered electric and gas rates for customers. This could result in decreased demand for electricity and gas, increased regulatory pressures and greater working capital requirements as the collection of higher commodity costs from our customers may be deferred under our regulated rate structure. A declining commodity price, on the other hand, would be expected to have the opposite effect. For additional information, including the impact of natural gas commodity prices on electricity prices such as BGS, see Item 7. MD&A—Executive Overview of 2016 and Future Outlook.

Power

Through Power, we seek to produce low-cost electricity by efficiently operating our nuclear, coal, gas, oil-fired and renewable generation assets while balancing generation output, fuel requirements and supply obligations through energy portfolio management. Our commitments for load, such as BGS in New Jersey and other bilateral supply contracts, are backed by the generation we own and may be combined with the use of physical commodity purchases and financial instruments from the market to optimize the economic efficiency of serving the load. Power is a public utility within the meaning of the Federal Power Act (FPA) and the payments it receives and how it operates are subject to FERC regulation.

Power is also subject to certain regulatory requirements imposed by state utility commissions such as those in New York and Connecticut.

Products and Services

As a merchant generator and power marketer, our profit is derived from selling a range of products and services under contract to an array of customers including utilities, other power marketers, such as retail energy providers, or counterparties in the open market. These products and services may be transacted bilaterally or through exchange markets and include but are not limited to:

Energy—the electrical output produced by generation plants that is ultimately delivered to customers for use in lighting, heating, air conditioning and operation of other electrical equipment. Energy is our principal product and is priced on a usage basis, typically in cents per kilowatt hour (kWh) or dollars per megawatt hour (MWh).

Capacity—distinct from energy, capacity is a market commitment that a given generation unit will be available to an Independent System Operator (ISO) for dispatch to produce energy when it is needed to meet system demand. Capacity is typically priced in dollars per MW for a given sale period (e.g. day or month).

Ancillary Services—related activities supplied by generation unit owners to the wholesale market that are required by the ISO to ensure the safe and reliable operation of the bulk power system. Owners of generation units may bid units into the ancillary services market in return for compensatory payments. Costs to pay generators for ancillary services are recovered through charges collected from market participants.

Congestion and Renewable Energy Credits—Congestion credits (or Financial Transmission Rights) are financial instruments that entitle the holder to a stream of revenues (or charges) based on the hourly congestion price differences across a transmission path. Renewable Energy Credits (RECs) are obtained through Power’s owned renewable generation or purchased in the open market. Electric suppliers of load are required to deliver a certain amount or percentage of their delivered power from renewable resources as mandated by applicable regulatory requirements.

Power also sells wholesale natural gas, primarily through a full-requirements BGSS contract with PSE&G to meet the gas supply requirements of PSE&G’s customers. On March 19,In 2014, the BPU approved an extension of the long-term BGSS contract to March 31, 2019, and then year-to-year thereafter the contract remains in effect unless terminated by either party with a two yeartwo-year notice.

Approximately 45% of PSE&G’s peak daily gas requirements is provided from Power’s firm gas transportation capacity, which is available every day of the year. Power satisfies the remainder of PSE&G’s requirements from storage contracts, liquefied natural gas, seasonal purchases, contract peaking supply and propane. Based upon the availability of natural gas beyond PSE&G’s daily needs, Power sells gas to others and uses it for its generation fleet.

In addition to its nuclear and fossil generation fleet, Power also owns and operates 326414 MW direct current (dc) of PV solar generation facilities and has an additional 7052 MW dc of PV solar generation in construction. Power also has a 50% ownership interest in a 208 MW oil-fired generation facility in Hawaii.

The remainder of this section about Power covers our nuclear and fossil fleet in the Mid-Atlantic and Northeast regions which comprises the vast majority of Power’s operations and financial performance.

How Power’s Generation Operates

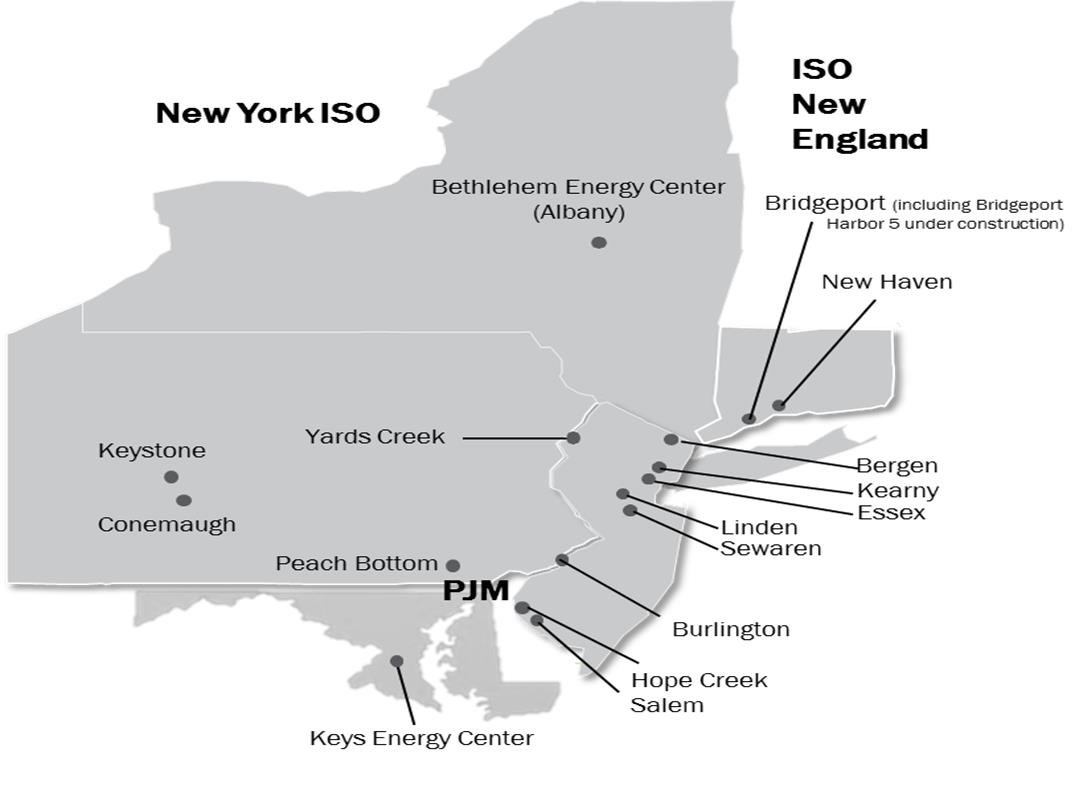

Nearly all of our generation capacity consists of nuclear and fossil generation (11,681(11,458 MW) that is located in the Northeast and Mid-Atlantic regions of the United States in some of the country’s largest and most developed electricity markets. For additional information see Item 2. Properties.

The map below shows the locations of our Northeast and Mid-Atlantic nuclear and fossil generation facilities, and projectsincluding theBridgeport Harbor 5 (BH5) project currently under construction:

Generation Capacity

Our nuclear and fossil installed capacity utilizes a diverse mix of fuels. As of December 31, 2016,2018, our fuel mix was comprised of 41%51% gas, 32% nuclear, 20%10% coal, 5% oil and 2% pumped storage. This fuel mix does not give effect to our previously announced decision to cease generation operations of the existing coal/gas units at our Hudson and Mercer generating stations on June 1, 2017. This fuel diversity helps to mitigate risks associated with fuel price volatility and market demand cycles. Our total generating output in 20162018 was approximately 52,000 GWh.55,800 gigawatt hours (GWh). The generation mix by fuel type in recent years has reflected the relatively more favorable price of natural gas compared to coal, making it more economical to run certain of our gas units in place of our coal units.coal. The following table indicates the proportionate share of generating output by fuel type in 2016.2018.

|

| | | | | |

| | | | | | |

| | Generation by Fuel Type (A) | | Actual 20162018 | | |

| | Nuclear: | | | | |

| | New Jersey facilities | | 36%37% | | |

| | Pennsylvania facilities | | 21%19% | | |

| | Fossil: | | | | |

| Coal: | | | | |

| Pennsylvania facilities | | 9% | | |

| Connecticut facilities | | —% | (B) | |

| Coal and Natural Gas: | | | | |

| New Jersey facilities | | —% | (B) | |

| | Natural Gas and Oil: | | | | |

| | New Jersey facilities | | 24%21% | | |

| | New York facilities | | 9% | | |

| Maryland facilities | | 4% | | |

| Connecticut facilities | | —% | (B) | |

| Coal: | | | | |

| Pennsylvania facilities | | 10% | | |

| | Connecticut facilities | | —% | (B) | |

| | Total | | 100% | | |

| | | | | | |

| |

| (A) | Excludes pumped storage, solar facilities and fossil generation in Hawaii which account for less than two2.5 percent of total generation. |

(B) Less than one percent.

WeIn mid-2018, we commenced commercial operations of our Keys Energy Center (Keys), a 761 MW gas-fired combined cycle generating station in Maryland and Sewaren 7, a 538 MW dual-fueled combined cycle generating station in New Jersey.

In July 2018, Exelon, co-owner of the Peach Bottom nuclear facilities in Pennsylvania, submitted a second 20-year license renewal application with the Nuclear Regulatory Commission (NRC) for Peach Bottom Units 2 and 3. It is anticipated that the NRC’s review process will take approximately two years from submission of the application. Peach Bottom Units 2 and 3 are also executingcurrently licensed to operate through 2033 and 2034, respectively.

In February 2016, the

following growth projectsproposed generating facility, BH5, a 485 MW dual-fueled combined cycle generation project, was awarded a capacity obligation. Construction continues on BH5, which

are includedis targeted for commercial operation in

the 2017-2019 capital spend of $1.3 billion for Fossil Growth Opportunities disclosed in Item 7. MD&A—Capital Requirements. |

| | | | | | |

| | | | | | |

| Major Growth Projects | |

| As of December 31, 2016 | |

| Project | | Location | | Expected In-Service Date | |

| | | | | | |

| Keys Energy Center gas-fired combined cycle generating station (755 MW) | | Maryland | | 2018 | |

| Sewaren 7 dual-fueled combined cycle generating station (540 MW) | | New Jersey | | 2018 | |

| Bridgeport Harbor 5 gas-fired combined cycle generating station (485 MW) | | Connecticut | | 2019 | |

| Bethlehem Energy Center (BEC) combined cycle uprate (58 MW) | | New York | | 2017/2018 | |

| | | | | | |

mid-2019.Generation Dispatch

Our generation units have historically been characterized as serving one or more of three general energy market segments: base load; load following; and peaking, based on their operating capability and performance.

Base Load Units run the most and typically are called to operate whenever they are available. These units generally derive revenues from both energy and capacity sales. Variable operating costs are low due to the combination of highly efficient operations and the use of relatively lower-cost fuels. Performance is generally measured by the unit’s “capacity factor,” or the ratio of the actual output to the theoretical maximum output. In 2016, our2018, the base load capacity factors were as follows:for the following units were:

|

| | | | |

| | | | | |

| | Unit | | 20162018

Capacity Factor | |

| | Nuclear | | | |

| | Salem Unit 1 | | 67.0%97.9% | |

| | Salem Unit 2 | | 84.3%84.6% | |

| | Hope Creek | | 89.8%88.8% | |

| | Peach Bottom Unit 2 | | 91.7%93.4% | |

| | Peach Bottom Unit 3 | | 100.0%94.2% | |

| | Coal | | | |

| | Keystone | | 68.4%83.4% | |

| | Conemaugh | | 61.7%76.9% | |

| | | | | |

Load Following Units’ operating costs are generally higher per unit of output than for base load units due to the use of higher-cost fuels such as oil, natural gas and, in some cases, coal or lower overall unit efficiency. These units usually have more flexible operating characteristics than base load units which enable them to more easily follow fluctuations in load. They operate less frequently than base load units and derive revenues from energy, capacity and ancillary services.

Peaking Units run the least amount of time and in some cases may utilize higher-priced fuels. These units typically start very quickly in response to system needs. Costs per unit of output tend to be higher than for base load units given the combination of higher heat rates and fuel costs. The majority of revenues are from capacity and ancillary service sales. The characteristics of these units enable them to capture energy revenues during periods of high energy prices.

In the energy markets in which we operate, owners of power plants specify to the ISO prices at which they are prepared to generate and sell energy based on the marginal cost of generating energy from each individual unit. The ISOs will generally dispatch in merit order, calling on the lowest variable cost units first and dispatching progressively higher-cost units until the point that the entire system demand for power (known as the system “load”) is satisfied reliably. Base load units are dispatched first, with load following units next, followed by peaking units. It should be noted that the sustained lower pricing of natural gas over the past several years has resulted in changes in relative operating costs compared to historical norms, whereinenabling some gas-fired generation is now able to displace some coal-fired generation.generation by other fuel types. This change, combined with the addition of new, more efficient generation capacity, has altered the historical dispatch order of certain plants in the markets where we operate.

During periods when one or more parts of the transmission grid are operating at full capability, thereby resulting in a constraint on the transmission system, it may not be possible to dispatch units in merit order without violating transmission reliability standards. Under such circumstances, the ISO may dispatch higher-cost generation out of merit order within the congested area, and power suppliers will be paid an increased Locational Marginal Price (LMP) in congested areas, reflecting the bid prices of those higher-cost generation units.

Typically, the bid price of the last unit dispatched by an ISO establishes the energy market-clearing price. After considering the market-clearing price and the effect of transmission congestion and other factors, the ISO calculates the LMP for every location in the system. The ISO pays all units that are dispatched their respective LMP for each MWh of energy produced, regardless of their specific bid prices. Since bids generally approximate the marginal cost of production, units with lower marginal costs typically generate higher operating profitsgross margins than units with comparatively higher marginal costs.

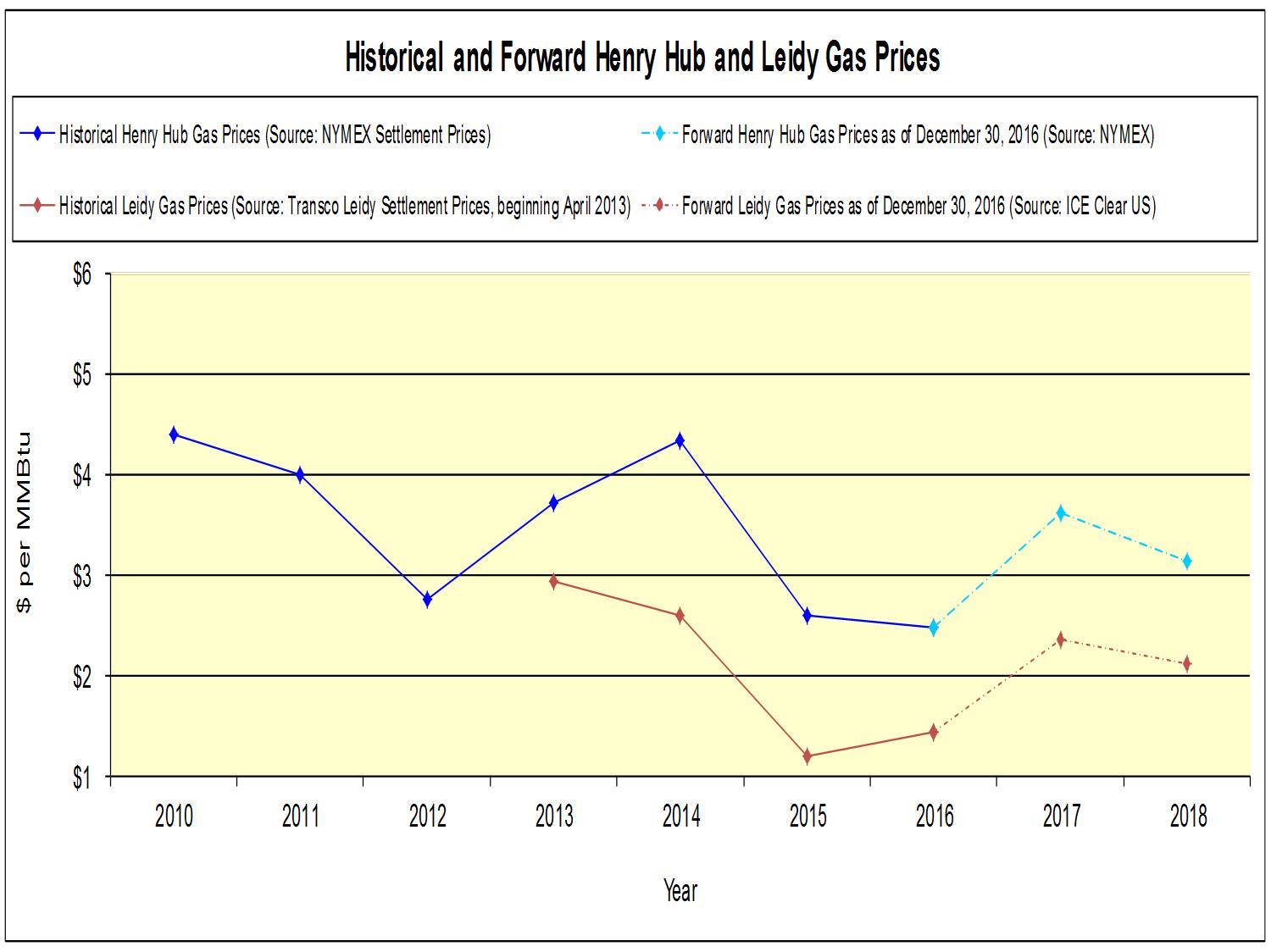

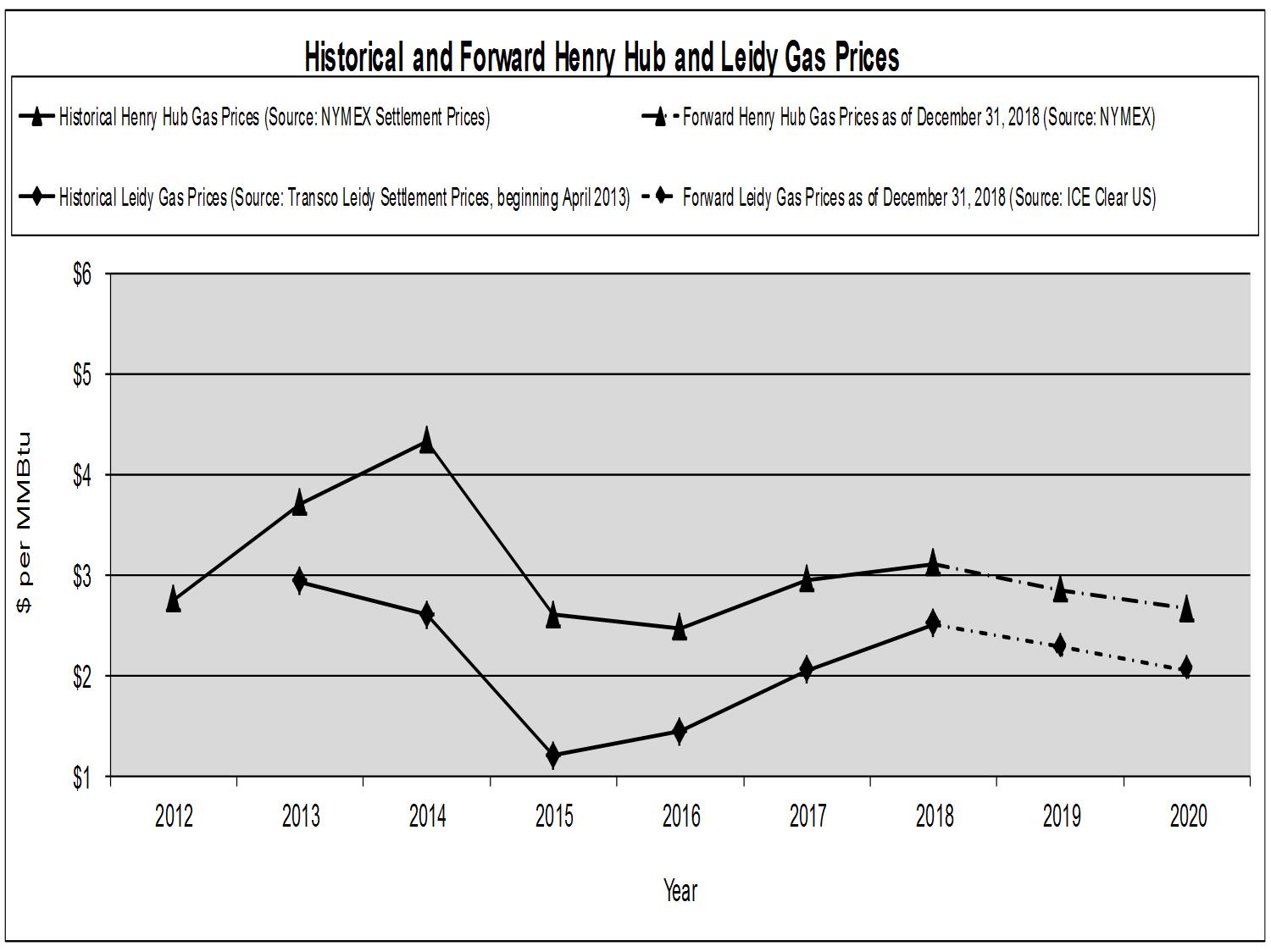

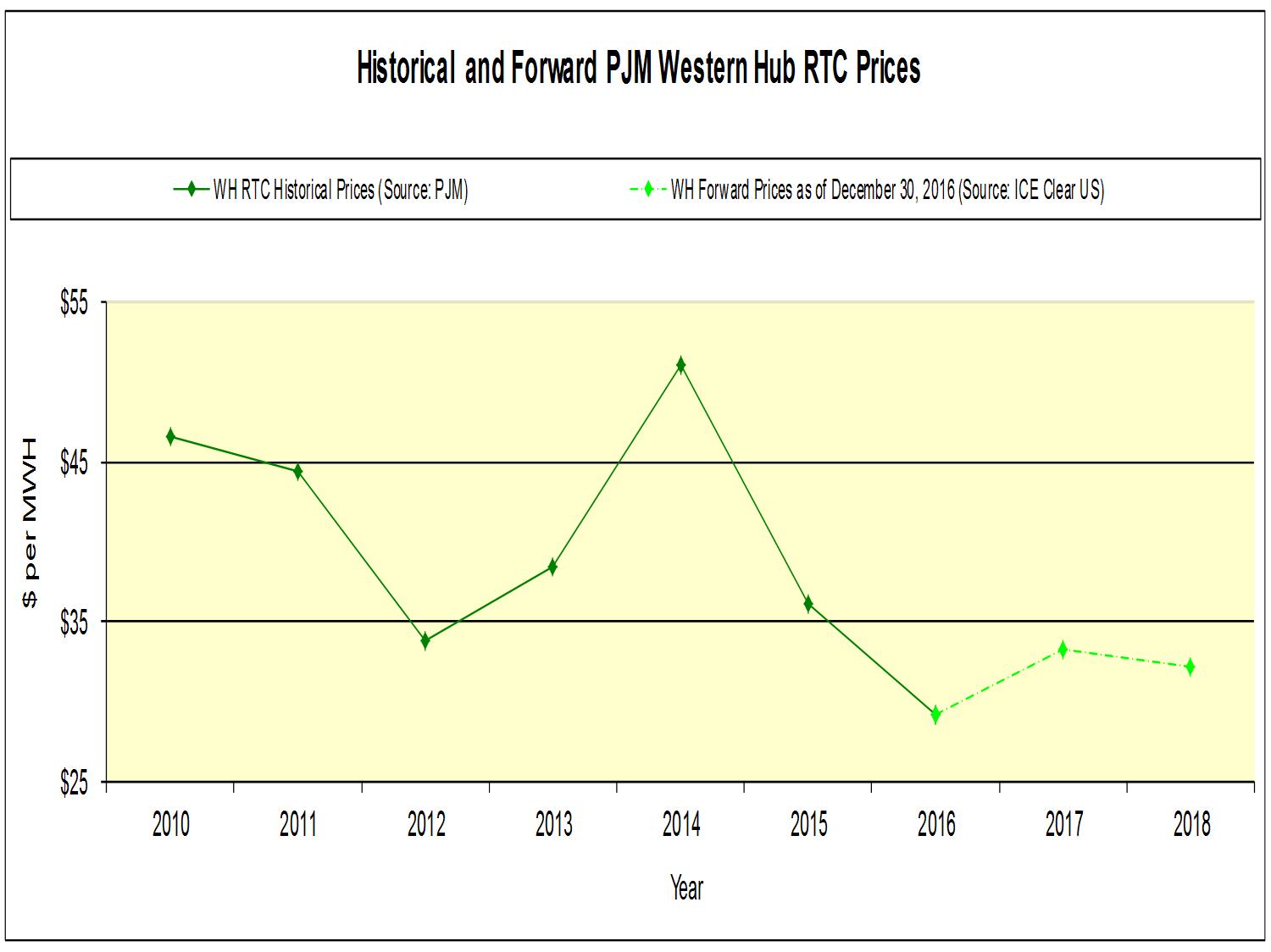

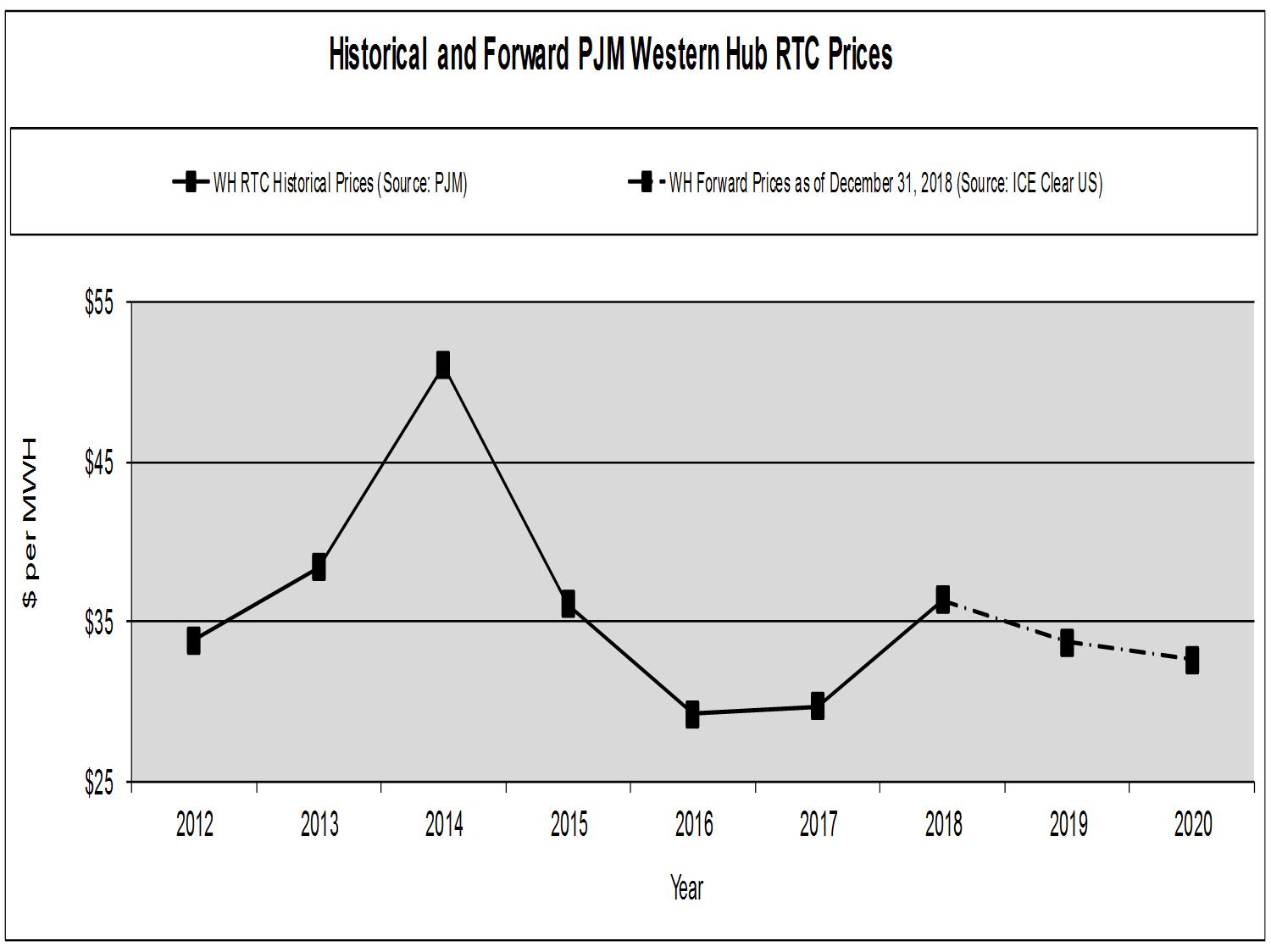

This method of determining supply and pricing creates a situation where natural gas prices often have a major influence on the price that generators will receive for their output, especially in periods of relatively strong or weak demand. Therefore, changes in the price of natural gas will often translate into changes in the wholesale price of electricity. This can be seen in the following graphs which present historical annual spot prices and forward calendar prices as averaged over each year at two liquid trading hubs.

Historical data implies that the price of natural gas will continue to have a strong influence on the price of electricity in the primary markets in which we operate.

The prices reflected in the preceding graphs above do not necessarily illustrate our contract prices, but they are representative of market prices at relatively liquid hubs, with nearer-term forward pricing generally resulting from more liquid markets than pricing for later years. As shown above, prices may vary by location resulting from congestion or other factors, such as the availability of natural gas from the Marcellus (Leidy) and other shale-gas regionsregions. These variations can be considerable. Concurrent with the development of regional shale gas, we have been increasing our purchases from the Marcellus/Utica shale gas regions and in 20162018 they accounted for approximately 90%70% of the gas we procured. While these prices provide some perspective on past and future prices, the forward prices are volatile and there can be no assurance that such prices will remain in effect or that we will be able to contract output at these forward prices.

Fuel Supply

Nuclear Fuel Supply—We have long-term contracts for nuclear fuel. These contracts provide for:

purchase of uranium (concentrates and uranium hexafluoride),

conversion of uranium concentrates to uranium hexafluoride,

enrichment of uranium hexafluoride, and

fabrication of nuclear fuel assemblies.

Our nuclear fuel contracts cover approximately 100% of our estimated uranium, enrichment and fabrication requirements through 2018 and a significant portion through 2021.

Coal Supply—OurThe Keystone, Conemaugh and Bridgeport Harbor 3 (BH3) stations operate on coal. Coal is delivered to ourthese units through a combination of rail, truck, barge and ocean shipments.

In order toTo control emissions levels, our Bridgeport 3BH3 unit uses a specific type of coal obtained from Indonesia. We currently have a coal supply contract from Indonesia under contract through 2017 forinventory at the Bridgeport facility and believe that additional coal would be available after 2017BH3 station as required.well as off-site storage to meet the plant’s projected requirements.

Gas Supply—Natural gas is the primary fuel for the bulk of our load following and peaking fleet. We purchase gas directly from natural gas producers and marketers. These supplies are transported to New Jersey by four interstate pipelines with which we have contracted. In addition, we have firm gas transportation contracted for this winter season to serve a portion of the gas requirements for our BEC stationBethlehem Energy Center (BEC) in New York.York and hold year-round firm gas transportation to serve the majority of the requirements of Keys in Maryland.

We have 1.3 billion cubic feet-per-day of firm transportation capacity and 0.9 billion cubic feet-per-day of firm storage delivery under contract to meet our obligations under the BGSS contract. This volume includes capacity from the Pennsylvania and Ohio shale gas regions where we purchase the majority of our natural gas. On an as-available basis, this firm transportation capacity may also be used to serve the gas supply needs of our New Jersey generation fleet.

Power has contracted for approximately 125 million cubic feet-per-day125,000 dekatherms/day of delivery capability on the PennEast Pipeline from eastern Pennsylvania to New Jersey with a targeted in-service date in the latter half of 2018.Jersey. This additional delivery capability will be used to supplement the BGSS contract.contract when it becomes operational.

Oil—Oil is used as the primary fuel for one load following steam unit and four combustion turbine peaking units and can be used as an alternate fuel by several load following and peaking units that have a dual-fuel capability. Oil for operations is drawn from on-site storage and is generally purchased on the spot market and delivered by truck or barge.

We expect to be able to meet the fuel supply demands of our customers and our own operations. However, the ability to maintain an adequate fuel supply could be affected by several factors not within our control, including changes in prices and demand, curtailments by suppliers, severe weather, environmental regulations, and other factors. For additional information and a discussion of risks, see Item 1A. Risk Factors, Item 7. MD&A—Executive Overview of 20162018 and Future Outlook and Item 8. Financial Statements and Supplementary Data—Note 13.14. Commitments and Contingent Liabilities.

Markets and Market Pricing

The vast majority of Power’s generation assets are located in three centralized, competitive electricity markets operated by ISO organizations all of which are subject to the regulatory oversight of FERC:

PJM Regional Transmission Organization—PJM conducts the largest centrally dispatched energy market in North America. It serves over 6165 million people, nearly 19%20% of the total United States population, and has a record peak demand of 165,492 MW. The PJM Interconnection coordinates the movement of electricity through all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia. The majority of our generating stations operate in PJM.

New York—The New York ISO (NYISO) is the market coordinator for New York State and is responsible for managing the New York Power Pool and for administering its energy marketplace. This service area has a population of about 19 million and a record peak demand of 33,956 MW. Our BEC station operates in New York.

New England—The ISO-New England (ISO-NE) is the market coordinator for the New England Power Pool and for administering its energy marketplace which covers Maine, New Hampshire, Vermont, Massachusetts, Connecticut and Rhode Island. This service area has a population of about 15 million and a record peak demand of 28,130 MW. Our Bridgeport and New Haven stations operate in Connecticut.

The price of electricity varies by location in each of these markets. Depending uponon our production and our obligations, these price differentials may increase or decrease our profitability.

Commodity prices, such as electricity, gas, coal, oil and environmental products, as well as the availability of our diverse fleet of generation units to operate, also have a considerable effect on our profitability. Over the long-term, the higher the forward prices are, the more attractive an environment exists for us to contract for the sale of our anticipated output. However, higher prices also increase the cost of replacement power; thereby placing us at greater risk should our generating units fail to operate effectively or otherwise become unavailable.

Over the past fewseveral years, lower wholesale natural gas prices have resulted in lower electric energy prices. One of the reasons for the lower natural gas prices is greater supply from more recently-developed sources, such as shale gas, much of which is

produced in states adjacent statesto New Jersey (e.g. Pennsylvania). This trend has reduced margin on forward sales as we re-contract our expected generation output.

In addition to energy sales, we earn revenue from capacity payments for our generating assets. These payments are compensation for committing our generating units to the ISO for dispatch at its discretion. Capacity payments reflect the value to the ISO of assurance that there will be sufficient generating capacity available at all times to meet system reliability and energy requirements. Currently, there is sufficient capacity in the markets in which we operate. However, in certain areas of these markets, there are transmission system transfer limitations which raise concerns about reliability and create a more acute need for capacity.

In PJM and ISO-NE, where we operate most of our generation, the market design for capacity payments provides for a structured, forward-looking, transparent capacity pricing mechanism. This is through the Reliability Pricing Model (RPM) in PJM and the Forward Capacity Market (FCM) in ISO-NE. These mechanisms provide greater transparency regarding the value of capacity and provide a pricing signal to prospective investors in new generating facilities so as to encourage expansion of capacity to meet future market demands. For additional information regarding FERC actions related to the capacity market construct, see Regulatory Issues—Federal Regulation.

The prices to be received by generating units in PJM for capacity have been set through RPM base residual and incremental auctions and depend upon the zone in which the generating unit is located. For each delivery year, the prices differ in the various areas of PJM, depending on the transfer limitations of the transmission system in each area. Keystone and Conemaugh in Pennsylvania receive lower capacity prices than the majority of our PJM generating units since there are fewer constraints in that region and our generating units in New Jersey usually receive higher pricing.

Our PJM generating units are located in several zones andzones. The average capacity prices that Power expects to realize the following average capacity pricesreceive from the base and incremental auctions which have been completed:

|

| | | | |

| | | | |

| Delivery Year | | MW-day | |

| June 2016 to May 2017 | | $172 | |

| June 2017 to May 2018 | | $177 | |

| June 2018 to May 2019 | | $215 | |

| June 2019 to May 2020 | | $116 | |

| | | | |

completed are disclosed in Item 8. Note 3. Revenues. The price that must be paid by an entity serving load in the various zones is also set through these auctions. These prices can be higher or lower than the prices noteddisclosed in the table aboveNote 3. Revenues due to the import and export capability to and from lower-priced areas. Prices in the most recent auction reflect PJM’s downwardly-revised demand forecast, changes in the emergency transfer limits due to transmission expansion and the effects of both the new generation and uncleared generation from the prior year’s auction.

We have obtained price certainty for our PJM capacity through May 20202022 and New England capacity through May 20212026 forBH5 and May 2022 for New Haven through the RPM and FCM pricing mechanisms, respectively.

Like PJM and ISO-NE, the NYISO provides capacity payments to its generating units, but unlike the other two markets, the New York market does not provide a forward price signal beyond a six monthsix-month auction period.

On a prospective basis, many factors may affect the capacity pricing, including but not limited to:

load and demand,

availability of generating capacity (including retirements, additions, derates and forced outage rates),

capacity imports from external regions,

transmission capability between zones,

available amounts of demand response resources,

pricing mechanisms, including potentially increasing the number of zones to create more pricing sensitivity to changes in supply and demand, as well as other potential changes that PJM and the other ISOs may propose over time, and

legislative and/or regulatory actions impacting the capacity auction or that permit subsidized local electric power generation.

For additional information on the RPM and FCM markets, as well as on state subsidization through various mechanisms, see Regulatory Issues—Federal Regulation.

Hedging Strategy

To mitigate volatility in our results, we seek to contract in advance for a significant portion of our anticipated electric output, capacity and fuel needs. We seek to sell a portion of our anticipated lower-cost generation over a multi-year forward horizon, normally over a period of two to three years. We believe this hedging strategy increases the stability of earnings.

Among the ways in which we hedge our output are: (1) sales at PJM West or other nodes within PJM corresponding to our generation portfolio and (2) BGS and similar full-requirements contracts. Sales atin PJM Westgenerally reflect block energy sales at the liquid PJM Western Hub or other basis locations when available and other transactions that seek to secure price certainty for our generation related products. The BGS-RSCP contract, a full-requirements contract that includes energy and capacity, ancillary and other services, is awarded for three-year periods through an auction process managed by the BPU. The volume of

BGS contracts and the mix of electric utilities that our generation operations serve will vary from year to year. Pricing for the BGS contracts, including a capacity component, for recent and future periods by purchasing utility is as follows:

|

| | | | | | | | | | |

| | | | | | | | | | | |

| | Load Zone ($/MWh) | | 2014-2017 | | 2015-2018 | | 2016-2019 | | 2017-2020 | |

| | PSE&G | | $97.39 | | $99.54 | | $96.38 | | $90.78 | |

| | Jersey Central Power & Light Company (JCP&L) | | $84.44 | | $80.42 | | $74.85 | | $69.08 | |

| | Atlantic City Electric Company | | $87.80 | | $86.06 | | $82.14 | | $75.49 | |

| | Rockland Electric Company | | $95.61 | | $90.66 | | $85.02 | | $80.50 | |

| | | | | | | | | | | |

|

| | | | | | | | | | |

| | | | | | | | | | | |

| | Load Zone ($/MWh) | | 2016-2019 | | 2017-2020 | | 2018-2021 | | 2019-2022 | |

| | PSE&G | | $96.38 | | $90.78 | | $91.77 | | $98.04 | |

| | Jersey Central Power & Light Company (JCP&L) | | $74.85 | | $69.08 | | $73.11 | | $77.15 | |

| | Atlantic City Electric Company | | $82.14 | | $75.49 | | $81.23 | | $87.40 | |

| | Rockland Electric Company | | $85.02 | | $80.50 | | $85.94 | | $88.03 | |

| | | | | | | | | | | |

Although we enter into these hedges in an effort to provide price certainty for a large portion of our anticipated generation, there is variability in both our actual output as well as in the effectiveness of our hedges. Actual output will vary based upon total market demand, the relative cost position of our units compared to other units in the market and the operational flexibility of our units. Hedge volume can also vary, depending on the type of hedge into which we have entered. The BGS auction, for example, results in a contract that provides for the supplier to serve a percentage of the default load of a New Jersey EDC, that is, the load that remains after some customers have chosen to be served directly either by third-party suppliers or through municipal aggregation. The amount of power supplied through the BGS auction varies based on the level of the EDC’s default load, which is affected by the number of customers who are served by third-party suppliers, as well as by other factors such as weather and the economy.

In recent years, as market prices declined from previous levels, there was an incentive for more of the smaller commercial and industrialC&I electric customers to switch to third-party suppliers. In a falling price environment, this has a negative impact on our margins, as the anticipated BGS pricing is replaced by lower spot market pricing. As average BGS rates have declined to a level that more closely resembles current market prices, customers may see less of an incentive to switch to third-party suppliers. We are unable to determine the degree to which this switching, or “migration,” will continue, but the impact on our results could be material should market prices fall or rise significantly.

In 2016, Power announced its intention to develop a retail energy platform to sell physical electricity and natural gas directly to commercial and industrial customers. We believe a retail energy platform would complement our existing wholesale generation-to-load marketing business and is intended to hedge our generation at improved margins inReflecting February 2019 BGS auction results, the geographic areas where we have generation facilities. Power was granted licenses in 2016 to sell both electricity and gas in the states of New Jersey and Pennsylvania and expects to begin its marketing efforts in 2017.

As of February 9, 2017, we had contracted for the following percentages of our anticipated base load generation output for the next three years with modest amounts beyond 20192021. are as follows:

|

| | | | | | | | |

| | | | | | | | | |

| | Base Load Generation | | 2017 | | 2018 | | 2019 | |

| | Generation Sales | | 100% | | 80%-85% | | 35%-40% | |

| | | | | | | | | |

|

| | | | | | | | |

| | | | | | | | | |

| | Base Load Generation | | 2019 | | 2020 | | 2021 | |

| | Generation Sales | | 100% | | 95%-100% | | 30%-35% | |

| | | | | | | | | |

In a changing market environment, this hedging strategy may cause our realized prices to differ materially from current market prices. In a rising price environment, this strategy normally results in lower margins than would have been the case had no hedging activity been conducted. Alternatively, in a falling price environment, this hedging strategy will tend to create margins higher than those implied by the then-current market.

Our fuel strategy is to maintain certain levels of uranium in inventory and to make periodic purchases to support such levels. Our nuclear fuel commitments cover approximately 100% of our estimated uranium, enrichment and fabrication requirements through 20182020 and a significant portion through 2021.

We also have various long-term fuel purchase commitments for coal to support our Keystone Conemaugh and Bridgeport HarborConemaugh stations. These purchase obligations are consistent with our strategy, in general, to enter into contracts for our fuel supply in comparable volumes to our sales contracts.

We take a more opportunistic approach in hedging both the fuel for and the anticipated output of our natural gas-fired generation. The generation from thesemore efficient load following units iscan be estimated with a moderate degree of certainty. The peaking units are less predictable, as a significant portion of these units will only dispatch when aggregate market demand has exceeded the supply provided by lower-cost units. The natural gas-fired units are hedged based on their expected generation; however, at much lower thresholds than baseload generation. Additionally, the recent development of low-cost gas supplies in the Marcellus region presents opportunities during certain portions of the year to procure gas for our generating units at attractive prices.

More than half of Power’s expected gross margin in the upcoming year2019 relates to our hedging strategy, our expected revenues from the capacity market mechanisms described above and certain ancillary service payments such as reactive power.

Other

Energy Holdings Lease Investments

Energy Holdings primarily owns and manages a portfolio of domestic lease investments. The majority of Energy Holdings’ $649$540 million of domestic lease investments are primarily energy-related leveraged leases. As of December 31, 2016,2018, the counterparties for 66%55% of our total leveraged lease investments were rated below investment grade by Standard & Poor’s (S&P). See Item 8. Financial Statements and Supplementary Data—Note 8.9. Financing Receivables for additional information.

Energy Holdings’ leveraged leasing portfolio is designed to provide a fixed rate of return. Leveraged lease investments involve three parties: an owner/lessor, a creditor and a lessee. In a typical leveraged lease financing, the lessor purchases an asset to be leased. The purchase price is typically financed 80% with debt provided by the creditor and the balance comes from equity funds provided by the lessor. The creditor provides long-term financing to the transaction secured by the property subject to the lease. Such long-term financing is non-recourse to the lessor and, with respect to our lease investments, is not presented on our Consolidated Balance Sheets.

The lessor acquires economic and tax ownership of the asset and then leases it to the lessee for a period of time no greater than 80% of its remaining useful life. As the owner, the lessor is entitled to depreciate the asset under applicable federal and state tax guidelines. The lessor receives income from lease payments made by the lessee during the term of the lease and from tax benefits associated with interest and depreciation deductions with respect to the leased property. Our ability to realize these tax benefits is dependent on operating gains generated by our other operating subsidiaries and allocated pursuant to the consolidated tax sharing agreement between us and our operating subsidiaries.

Lease rental payments are unconditional obligations of the lessee and are set at levels at least sufficient to service the non-recourse lease debt. The lessor is also entitled to any residual value associated with the leased asset at the end of the lease term. An evaluation of the after-tax cash flows to the lessor determines the return on the investment. Under accounting principles generally accepted in the United States (GAAP), the leveraged lease investment is recorded net of non-recourse debt and income is recognized as a constant return on the net unrecovered investment.

For additional information on leases, including the credit, tax and accounting risks, see Item 1A. Risk Factors, Item 7A. Quantitative and Qualitative Disclosures About Market Risk—Credit Risk, and Item 8. Financial Statements and Supplementary Data—Note 8.9. Financing Receivables.

LIPA Operating Services Agreement (OSA)

In accordance with a twelve year Amended and Restated Operations Services Agreement (OSA)OSA entered into by PSEG LI and the LIPA, PSEG LI commenced operating LIPA’s electric T&D system in Long Island, New York on January 1, 2014. As required by the OSA, PSEG LI also provides certain administrative support functions to LIPA. PSEG LI uses its brand in the Long Island T&D service area. Pursuant toUnder the OSA, PSEG LI acts as LIPA’s agent in performing many of its obligations and in return (a) receives reimbursement for pass-through operating expenditures, (b) receives a fixed management fee and (c) is eligible to receive an incentive fee contingent on meeting established performance metrics. In addition,Also, there is thean opportunity for the parties to extend the contract for an additional eight years subject to the achievement by PSEG LI of certain performance levels during the initial term of the OSA. Also, as ofFurther, since January 2015, Power began providingprovides fuel procurement and power management services to LIPA under separate agreements.

COMPETITIVE ENVIRONMENT

PSE&G

Our transmission and distributionT&D business is minimally impacted when customers choose alternate electric or gas suppliers since we earn our return by providing transmission and distribution service, not by supplying the commodity. Increased reliance by customers on net-metered generation, including solar, and changes in customer behaviors can result in decreased reliance on our system and impact our revenues and investment opportunities. The demand for electric energy and gas by customers is affected by customer conservation, economic conditions, weather and other factors not within our control. Construction of new local generation and changing customer usage patterns also have the potential to reduce the need for the construction of new transmission to transport remote generation and alleviate system constraints.

Changes in the current policies for building new transmission lines, such as those ordered by FERC and being implemented by PJM and other ISOs to eliminate contractual provisions that previously provided us a “right of first refusal” (ROFR) to construct projects in our service territory, could result in third-party construction of transmission lines in our area in the future

and also allow us to seek opportunities to build in other service territories. These implementing rules within the regions are still in fluxcontinue to evolve so both the extent of the risk within our service territory and the opportunities for our transmission business elsewhere remain difficult to assess. For additional information, see the discussion in Regulatory Issues—Federal Regulation—Transmission Regulation, below.

Construction

Power

Various market participants compete with us and one another in buying and sellingtransacting in the wholesale energy markets, entering into bilateral contracts and selling to individual and aggregated retail customers. Our competitors include:

merchant generators,

domestic and multi-national utility generators,

energy marketers and retailers,

private equity firms, banks funds and other financial entities,

fuel supply companies, and

affiliates of other industrial companies.

New additions of lower-cost or more efficient generation capacity could make our plants less economic in the future. Although it is not clear if this capacity will be built or, if so, what the economic impact will be, such additions would impact market prices and our competitiveness.

Our business is also under competitive pressure due to demand sidedemand-side management (DSM) and other efficiency efforts aimed at changing the quantity and patterns of usage by consumers which could result in a reduction in load requirements. A reduction in load requirements can also be caused by economic cycles, weather, municipal aggregation and other customer migration and other factors. In addition, how resources such as demand response and capacity imports are permitted to bid into the capacity markets also affects the prices paid to generators such as Power in these markets. It is also possible that advances in technology, such as distributed generation and micro grids, will reduce the cost of alternative methods of producing electricity to a level that is competitive with that of most central station electric production. To the extent that additions to the electric transmission system relieve or reduce limitations and constraints in eastern PJM where most of our plants are located, our revenues could be adversely affected. Changes in the rules governing what types of transmission will be built, who is selected to build transmission and who will pay the costs of future transmission could also impact our generation revenues.