--12-31FY2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K10-K/A

(Amendment No. 1)

ý

☒Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 20062023

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

oTransition Report Pursuant to Section 13 or 15(d) ofFor the Securities Exchange Act of 1934

Commission File No. 0-15057

P.A.M. TRANSPORTATION SERVICES, INC.

(Exact name of registrant as specified in its charter)

Delaware | 0-1507 | 71-0633135 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (I.R.S. Employer Identification No.) |

297 West Henri De Tonti Blvd, Tontitown, Arkansas 72770

(Address of principal executive offices) (Zip Code)

(479) 361-9111

Registrant'sRegistrant’s telephone number, including area codecode: (479) 361-9111

| N/A |

| (Former name, former address and former fiscal year, if changed since last report) |

Securities registered pursuant to section 12(b) of the Act:

| Securities registered pursuant to Section 12(b) of the Act: | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, $.01 par value | PTSI | The NASDAQ StockGlobal Market LLC

|

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark if disclosure of delinquent filerswhether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to ItemRule 405 of Regulation S-K (Section 229.405S-T (§232.405 of this chapter) is not contained herein, and will not be contained,during the preceding 12 months (or for such shorter period that the registrant was required to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. osubmit such files).

Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.filer, a smaller reporting company, or an emerging growth company. See definitionthe definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and large accelerated filer”“emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o ☐ | | Accelerated filer ☑ | |

| Non-accelerated filer ☐ | | Accelerated filer þSmaller reporting company ☑

Emerging growth company ☐ | | Non-accelerated filer o

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b) . ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

The aggregate market value of the common stock of the registrant held by non-affiliates of the registrant computed by reference to the average of the closing bid and askedask prices of the common stock as of the last business day of the registrant's most recently completed second quarter was$130,771,476.160,431,964. Solely for the purposes of this response, the registrant has assumed, without admitting for any purpose, that all executive officers directors and beneficial owners of more than five percentdirectors of the registrant’s common stockregistrant, and no other persons, are considered the affiliates of the registrant at that date.

The number of shares outstanding of the issuer’sregistrant’s common stock, as of March 5, 2007:10,307,607April 19, 2024: 22,034,762 shares of $.01 par value common stock.

AuditorName – Grant Thornton LLP

AuditorFirmID – PCAOB ID Number 248

AuditorLocation – Tulsa, OK

DOCUMENTS INCORPORATED BY REFERENCE

PortionsNone.

EXPLANATORY NOTE

P.A.M. Transportation Services, Inc. (“P.A.M.,” the registrant’s definitive Proxy Statement“Company,” “we,” “our,” or “us”) is filing this Amendment No. 1 on Form 10-K/A (this “Amendment”) to amend the Company’s Annual Report on Form 10-K for its Annual Meetingthe fiscal year ended December 31, 2023, originally filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2024 (the “Original Report”), to include the information required by Items 10 through 14 of Stockholders to be held in 2007 are incorporated by reference in answer to Part III of Form 10-K. This information was previously omitted from the Original Report in reliance on General Instruction G(3) to Form 10-K, which permits the information in the above referenced items to be incorporated in the Form 10-K by reference from the Company’s definitive proxy statement if such statement is filed no later than 120 days after the Company’s fiscal year-end. We are filing this report, withAmendment to provide the exceptioninformation required in Part III of Form 10-K because a definitive proxy statement containing such information regarding executive officers required under Itemwill not be filed by the Company within 120 days after the end of the fiscal year covered by the Original Report.

This Amendment amends and restates in their entirety Items 10, 11, 12, 13, and 14 of Part III of the Original Report. The cover page of the Original Report is also amended to delete the reference to the incorporation by reference of the Company’s definitive proxy statement. In addition, Item 15(a)(3) of Part IV of the Original Report has also been amended and supplemented to include our Certificate of Amendment of our Amended and Restated Certificate of Incorporation, filed with the Secretary of State of the State of Delaware on May 10, 2022, which was inadvertently omitted from the exhibit index in the Original Report, and our 2024 Equity Incentive Plan.

Except as described above, no other changes have been made to the Original Report, and this Amendment does not modify, amend or update in any way any of the financial or other information iscontained in the Original Report. This Amendment does not reflect events occurring after the date of the filing of the Original Report. Accordingly, this Amendment should be read in conjunction with the Original Report and with our filings with the SEC subsequent to the filing of the Original Report. Capitalized terms used in this Amendment and not otherwise defined herein have the meaning ascribed to such terms in the Original Report.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), this Amendment also contains new certifications pursuant to Sections 302 of the Sarbanes-Oxley Act of 2002, which are attached hereto. Because no financial statements have been included in Part I, Item 1.

FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements, including statements about our operatingthis Amendment and growth strategies, our expected financial positionthis Amendment does not contain or amend any disclosure with respect to Items 307 and operating results, industry trends, our capital expenditure308 of Regulation S-K under the Exchange Act, paragraphs 3, 4 and financing plans and similar matters. Such forward-looking statements are found throughout this Report, including under Item 1, Business, Item 1A, Risk Factors, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Item 7A, Quantitative and Qualitative Disclosures About Market Risk. In those and other portions of this Report, the words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “project” and similar expressions, as they relate to us, our management, and our industry are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business. Actual results may differ materially. Some5 of the risks, uncertainties and assumptions about P.A.M. that may cause actual results to differ from these forward-looking statements are described under the headings “Risk Factors,” “Management’s Discussion and Analysiscertifications have been omitted.

All forward-looking statements attributable to us, or to persons acting on our behalf, are expressly qualified in their entirety by this cautionary statement.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. In light of these risks and uncertainties, the forward-looking events and circumstances discussed in this Report might not transpire.

P.A.M. TRANSPORTATION SERVICES, INC.

AMENDMENT NO. 1 ON FORM 10-K10-K/A

For the fiscal year ended December 31, 20062023

TABLE OF CONTENTS

PART III| Item 10 | | | | Item 11 | | | | Item 12 | | | | Item 13 | | | | Item 14 | | | | | PART I

| Page | | Item 115 | | | 1 | | | 8 | | | 11 | | | 11 | | | 11 | | | 11 | | | | | | | PART II

| | | | | 12

|

| | 14 |

| | 15

|

| | 26 |

| | 27 |

| | 54

|

| | 54 |

| | 55 |

| | |

| PART III

| |

| | 56 |

| | 56 |

| | 56

|

| | 57 |

| | 57 |

| | |

| PART IV

| |

| | 58 |

| | |

| | 61 |

| | |

| | 62 |

Item 10. Directors, Executive Officers and Corporate Governance.

PART I

Directors

Our Board of Directors currently consists of nine directors. Members of our Board are elected annually to serve until the next annual meeting of stockholders or until their successors are elected and qualified. The biography of each of our directors and executive officers below contains information regarding the person’s service as director, business experience, director positions held currently or at any time during the last five years, and the experiences, qualifications, attributes or skills that caused the Board to determine that the person should serve as a director.

Unless

Michael D. Bishop, age 56, has been a director and a member of the context otherwise requires, all references in this Annual Report on Form 10-KAudit Committee since 2019. Mr. Bishop is the President and Founder of American General Counsel PLC, a law firm providing general counsel services to “P.A.M.,”businesses. From 2018 to 2020, Mr. Bishop was Co-President of iPSE-US, the “Company,” “we,” “our,” or “us” mean P.A.M. Transportation Services, Inc. and its subsidiaries.

We areAssociation of Independent Workers, an association dedicated to advancing the freedom an interests of America’s independent workers. Mr. Bishop served as a truckload dry van carrier transporting general commodities throughoutmember of the continental United States as well asCongress from 2014 to 2018. During his tenure in Congress, Mr. Bishop was appointed to and served on the Canadian provinces of OntarioHouse Ways and Quebec. We also provide transportation services in Mexico under agreements with Mexican carriers. Our freight consists primarily of automotive parts, consumer goods, such as general retail store merchandise,Means Committee, the Judiciary Committee and manufactured goods, such as heating and air conditioning units.

P.A.M. Transportation Services, Inc. is a holding company organized under the laws of the State of Delaware in June 1986 which conducts operations through the following wholly owned subsidiaries: P.A.M. Transport, Inc., T.T.X., Inc., P.A.M. Dedicated Services, Inc., P.A.M. Logistics Services, Inc., Choctaw Express, Inc., Choctaw Brokerage, Inc., Transcend Logistics, Inc., Allen Freight Services, Inc., Decker Transport Co., Inc., East Coast Transport and Logistics, LLC, S & L Logistics, Inc., P.A.M. International, Inc., P.A.M. Canada, Inc. and McNeill Express, Inc. Our operating authorities are held by P.A.M. Transport, Inc., P.A.M. Dedicated Services, Inc., Choctaw Express, Inc., Choctaw Brokerage, Inc., Allen Freight Services, Inc., T.T.X., Inc., Decker Transport Co., Inc., East Coast Transport and Logistics, LLC, and McNeill Express, Inc.

We are headquartered and maintain our primary terminal and maintenance facilities and our corporate and administrative offices in Tontitown, Arkansas, which is located in northwest Arkansas, a major center for the trucking industry and where the support services (including warranty repair services) for most major tractor and trailer equipment manufacturers are readily available.

In order to conform to industry practice, the Company began to classify fuel surcharges charged to customers as revenue rather than as a reduction of operating supplies expense as had been presented in reports prior to the period ended June 30, 2004. During 2006, the Company began to separately display as a line item “Fuel expense” for amounts paid for fuel which previously had been aggregated with other operating supplies and included in the line item “Operating supplies”. These reclassifications have had no effect on operating income, net income or earnings per share. The Company has made corresponding reclassifications to comparative periods shown.

Segment Financial Information

The Company's operations are all in the motor carrier segment and are aggregated into a single operating segment in accordance with the aggregation criteria presented in SFAS 131.

Operations

Our operations can generally be classified into truckload services or brokerage and logistics services. Truckload services include those transportation services in which we utilize company owned tractors or owner-operator owned tractors for the pickup and delivery of freight. The brokerage and logistics services consists of services such as transportation scheduling, routing, mode selection, transloading and other value added services related to the transportation of freight which may or may not involve the usage of company owned or owner-operator owned equipment. Both our truckload operations and our brokerage and logistics operations have similar economic characteristics and are impacted by virtually the same economic factors as discussed elsewhere in this Report. Truckload services operating revenues, before fuel surcharges represented 87.8%, 88.0%, and 86.4% of total operating revenues for the years ended December 31, 2006, 2005, and 2004, respectively. The remaining operating revenues, before fuel surcharge for the same periods were generated by brokerage and logistics services, representing 12.2%, 12.0%, and 13.6%, respectively. Approximately 99% of the Company's revenues are generated by operations conductedHigher Education Committee. Preceding his service in the United States Congress, Mr. Bishop was the Chief Legal Officer and allGeneral Counsel of International Bancard Company, a nation-wide financial services technology company. Prior to his role at International Bancard, Mr. Bishop was a Senior Attorney with Clark Hill PLC, an international law firm, where he concentrated in the areas of Public Policy and Business Law. Before joining Clark Hill PLC, Mr. Bishop was elected to and served in the Michigan State legislature from 1998 to 2010. During his tenure in the Michigan State legislature, Mr. Bishop was chosen to serve as the Senate Majority Leader and also served on various committees including chairing the Senate Banking and Financial Institutions Committee and the Constitutional Law and Ethics Committee. Mr. Bishop is a licensed real estate broker and an attorney licensed to practice law in the state of Michigan, the District of Columbia, and before the U.S. Supreme Court. He also serves as an Adjunct Professor of Law at the Thomas M. Cooley Law School. His thorough understanding of legal matters, public policy, financial analytics, and budgeting qualify him for service on the Board of PTSI.

Frederick P. Calderone, age 73, has been a director since 1998. Mr. Calderone retired in 2016 after over 20 years of service as a Vice President of a diversified holding company headquartered in Warren, Michigan. During his career, Mr. Calderone was widely recognized for his expertise in corporate, partnership and individual income tax matters; estate planning; tax planning for multinational businesses; mergers, acquisitions and commercial transactions; tax controversies and litigation; and corporate accounting. Prior to this time, Mr. Calderone was a partner with Deloitte, Haskins, & Sells, a predecessor to Deloitte LLP. Mr. Calderone is a certified public accountant, attorney and tax specialist with a long history of advising and providing executive oversight to transportation companies. Mr. Calderone has served as a director of Universal Logistics Holdings, Inc. (NASDAQ: ULH) since 2009. With his thorough understanding of financial reporting, generally accepted accounting principles, financial analytics, taxation and budgeting, Mr. Calderone brings to the Board a unique combination of expertise in accounting, strategic planning and finance.

W. Scott Davis, age 61, is Director of Partner Relations of Circumference Group, LLC, an investment management partnership, where he is responsible for business development and client relations. Prior to that, he served as Vice Chairman and Chief Financial Officer of Clearview International, LLC, a data center business headquartered in Dallas, Texas, until the company was sold in April 2016. He had been an investor in Clearview since June 2009. Mr. Davis was a Partner and Senior Managing Director of Rock Financial Partners, LLC from April 2009 to December 2013. From August 2006 to April 2009, he served as the President and sole owner of WS Davis, Inc., the company through which he performed his consulting work. From 1987 to 2006, Mr. Davis worked for Stephens Inc., an investment banking firm, including serving as an Executive Vice President of Stephens Inc. from 2002 to 2006. Mr. Davis has served as a director of PTSI since August 2007. He has extensive experience in the investment banking industry. He currently serves as Chairman of our Audit Committee. His extensive experience in financial statement analysis and review qualifies him to serve on the Board and as Chairman of the Company's assets areAudit Committee of PTSI.

Edwin J. Lukas, age 56, is the founder of Vistula PLC, a business law firm located orin Saint Clair Shores, Michigan. He is also a Strategic Partner with Aquila Equity Partners, a private investment firm located in Bloomfield Hills, Michigan. From 2016 to March 2020, Mr. Lukas served in an executive-level capacity with a diversified holding company based in Warren, Michigan, including as its Executive Vice President and General Counsel. Prior to this time, Mr. Lukas was a partner at Bodman PLC in Detroit, Michigan. Mr. Lukas is a graduate of the University of Pennsylvania and the University of Detroit School of Law, where he served as Editor-in-Chief of the University of Detroit Law Review. He has served as a director of PTSI since 2018. Mr. Lukas brings to our Board extensive experience in representing both public and private companies in corporate law, mergers and acquisitions, and capital markets transactions. His expertise in organizations, processes, strategies, and risk management supports our goal of strong Board and management accountability, transparency, and protection of stakeholder interests.

Franklin H. McLarty, age 49, is the Chairman and CEO of McLarty Diversified Holdings, a diversified holding company with investments in professional services, transportation, real estate, and media. Mr. McLarty founded McLarty Diversified Holdings in 2020. He also leads Coastal Automotive Group, an automotive retail operation that focuses on dealerships in Southern California and South Florida. He was previously the Executive Chairman and Director of MDH Acquisition Corp (NYSE: MDH.U) prior to its liquidation in 2022. Mr. McLarty was the co-founder of McLarty Capital Partners, now named Firmament, a private markets investment manager founded in June 2012; CapRocq, a real estate investment firm founded in September 2012 with significant experience as an owner-operator of high-quality office, mixed-use properties and automotive retail properties located in secondary and tertiary markets across the Southeast, Southcentral and Midwest regions otherwise known as the Heartland; and Southern United Auto Group, a growing automotive retail platform founded in June 2016 focused on the southeastern U.S. In addition, he was a founding executive of RML Automotive, where he served a tenure as CEO. Earlier in his career, Mr. McLarty worked in hotel-related private equity with McKibbon Hotel Group and The Seaway Group. Mr. McLarty has served on numerous advisory boards and boards of directors including Tire Group International, Palo Verde Holdings, The McLarty Companies and The Seaway Group. He also served on the board of, and was lead investor in, XTR, a premium documentary production company in Los Angeles. In 2007, he was appointed by then Governor Mike Beebe to the Arkansas Economic Development Commission and served as its Chairman in 2009. Mr. McLarty has served as a director and member of the Audit Committee of PTSI since 2014. Mr. McLarty’s extensive financial and transportation-related experience as an executive in the automotive industry and his insight into the Company’s customer base qualify him to serve on the Board of PTSI.

H. Pete Montaño, age 64, retired in 2018 as Vice President of Sales of Contract Freighters, Inc. (“CFI”), a trucking and logistics company which formerly operated as a division of Con-way, Inc. and XPO Logistics, Inc. As Vice President of Sales and Revenue Management for CFI, he oversaw sales in the United States.States, Canada and Mexico and was responsible for the strategic sales planning, account growth and training for all sales in the United States, Mexico and Canada as well as the pricing and bid departments. Mr. Montaño served over 28 years in various capacities with CFI, starting as Director of Sales for Mexico. Mr. Montaño brings significant industry experience and cross-border expertise to our board. Prior to his time at CFI, Mr. Montaño worked for Roadway Express, where he was in charge of sales for regions of the United States and Mexico. He currently serves as an advisory director of The Hawthorne Group, parent company of Melton Truck Lines, Inc., a private flatbed and step-deck carrier serving the United States, Canada, and Mexico. Mr. Montaño has served as a director and a member of the Audit Committee of PTSI since 2019. He is a dual citizen of the United States and Mexico and brings extensive sales and operational experience to the board and particular knowledge and insight relating to the Company’s Mexico operations. Mr. Montaño’s comprehensive cross-border and transportation-related experience qualify him to serve on the Board of PTSI.

Matthew J. Moroun, age 24, has been a director since 2020. He is also employed in other Moroun family-owned businesses engaged in transportation and business services. Mr. Moroun obtained a Bachelor of Business Administration in Finance from the Mendoza College of Business at the University of Notre Dame in December 2021. Mr. Moroun has served as a director of Universal Logistics Holdings, Inc. (NASDAQ: ULH) since 2020. Matthew J. Moroun is the son of our Chairman, Matthew T. Moroun. We believe Mr. Moroun offers the Board a unique perspective on the Company’s strategic challenges and opportunities and will advance the long-term interests of our shareholders.

Matthew T. Moroun, age 50, is Chairman of our Board of Directors. He currently serves as Chairman and President of a diversified holding company based in Warren, Michigan. He is also Chairman of an insurance and real estate holding company based in Sterling Heights, Michigan. Mr. Moroun owns or controls other privately-held businesses engaged in transportation services and real estate acquisition, development, and management. Mr. Moroun has served as a director of the Company since 1992 and as our Chairman since 2007. He is currently Chairman of our Executive Committee and Chairman of our Compensation and Stock Option Committee and served as our interim President and Chief Executive Officer from May 2020 to August 2020. Mr. Moroun has served as a director and as Chairman of the Board of Universal Logistics Holdings, Inc. (NASDAQ: ULH) since 2004. Matthew T. Moroun is the father of Matthew J. Moroun, a member of our Board of Directors. Mr. Moroun’s long-term, substantive leadership experience allows him to provide operational, financial, business, capital markets, and strategic expertise to our Board. He possesses first-hand knowledge of the best practices and trends for our industry. His perspective and practical insight on transportation, automotive, real estate development, infrastructure, and government relations enhance the Board’s ability to oversee and direct our strategy, business planning, and execution.

Business

Joseph A. Vitiritto, age 53, has served as President and Growth StrategyChief Executive Officer since August 2020. Prior to his employment with the Company, Mr. Vitiritto served as Senior Vice President of Pricing and Network Design for Knight-Swift Transportation Holdings, Inc. (“Knight-Swift”) since May 2019. Prior to assuming that role, Mr. Vitiritto served in various managerial capacities for Knight-Swift and its predecessor, Knight Transportation, Inc., beginning in 2003, including most recently as Senior Vice President of Operations – Swift Transition Team and Senior Vice President of Human Resources. These experiences and his knowledge of the day-to-day operations and management of the Company qualify him to serve on the Board of PTSI.

Executive Officers

Our strategy focuses on the following elements:current executive officers are Joseph A. Vitiritto and Lance K. Stewart.

Maintaining Dedicated Fleets in High Density Lanes. We strive to maximize utilizationLance K. Stewart, age 55, has served as Vice President of Finance, Chief Financial Officer and increase revenue per tractor while minimizing our time and empty miles between loads. In this regard, we seek to provide dedicated equipment to our customers where possible and to concentrate our equipment in defined regions and disciplined traffic lanes. Dedicated fleets in high density lanes enable us to:

·maintain more consistent equipment capacity;

·provide a high level of service to our customers, including time-sensitive delivery schedules;

·attract and retain drivers; and

·maintain a sound safety record as drivers travel familiar routes.

Providing Superior and Flexible Customer Service. Our wide range of services includes dedicated fleet services, logistics services, “just-in-time” delivery, two-man driving teams, cross-docking and consolidation programs, specialized trailers, and Internet-based customer access to delivery status. These services, combined with a decentralized regional operating strategy, allow us to quickly and reliably respond to the diverse needs of our customers, and provide an advantage in securing new business. We also maintain ISO 9002 certification to ensure that we operate in accordance with approved quality assurance standards.

Many of our customers depend on us to make delivery on a “just-in-time” basis, meaning that parts or raw materials are scheduled for delivery as they are needed on the manufacturer’s production line. The need for this service is a product of modern manufacturing and assembly methods that are designed to drastically decrease inventory levels and handling costs. Such requirements place a premium on the freight carrier’s delivery performance and reliability.

Employing Stringent Cost Controls. We focus intently on controlling our costs while not sacrificing customer service. We maintain this balance by scrutinizing all expenditures, minimizing non-driver personnel, operating a late-model fleet of tractors and trailers to minimize maintenance costs, and adopting new technology only when proven and cost justified.

Making Strategic Acquisitions. We continually evaluate strategic acquisition opportunities, focusing on those that complement our existing business or that could profitably expand our business or services. Our operational integration strategy is to centralize administrative functions of acquired businesses at our headquarters, while maintaining the localized operations of acquired businesses. We believe that allowing acquired businesses to continue to operate under their pre-acquisition names and in their original regions allows such businesses to maintain driver loyalty and customer relationships.

Industry

The U.S. market for truck-based transportation services is estimated to be approximately $600 billion in annual revenue. The truckload industry is highly fragmented and is impacted by several economic and business factors, many of which are beyond the control of individual carriers. The stateTreasurer of the economy, coupled with equipment capacity levels, can impact freight rates. VolatilityCompany since April 2023. Mr. Stewart served as interim Chief Financial Officer and Treasurer in March 2023 and served as Vice President of various operating expenses, such as fuel and insurance, make the predictability of profit levels unclear. Availability, attraction, retention and compensation for drivers affect operating costs, as well as equipment utilization. In addition, the capital requirements for equipment, coupled with potential uncertainty of used equipment values, impact the ability of many carriers to expand their operations. The current operating environment is characterized by the following:

·Price increases by tractor and trailer equipment manufacturers, rising fuel costs, and intense competition for drivers.

·In the last few years, many less profitable or undercapitalized carriers have been forced to consolidate or to exit the industry.

Competition

The trucking industry is highly competitive and includes thousands of carriers, none of which dominates the market in which the Company operates. The Company's market share is less than 1% and we compete primarily with other irregular route medium- to long-haul truckload carriers, with private carriage conducted by our existing and potential customers, and, to a lesser extent, with the railroads. Increased competition has resulted from deregulation of the trucking industry. We compete on the basis of quality of service and delivery performance, as well as price. Many of the other irregular route long-haul truckload carriers have substantially greater financial resources, own more equipment or carry a larger total volume of freight.

Marketing and Significant Customers

Our marketing emphasis is directed to that portion of the truckload market which is generally service-sensitive, as opposed to being solely price competitive. We seek to become a “core carrier” for our customers in order to maintain high utilization and capitalize on recurring revenue opportunities. Our marketing efforts are diversified and designed to gain access to dedicated fleet services (including those in Mexico and Canada), domestic regional freight traffic, and cross-docking and consolidation programs.

Our marketing efforts are conducted by a sales staff of seven employees who are located in our major markets and supervised from our headquarters. These individuals work to improve profitability by maintaining an even flow of freight traffic (taking into account the balance between originations and destinations in a given geographical area) and high utilization, and minimizing movement of empty equipment.

Our five largest customers, for which we provide carrier services covering a number of geographic locations, accounted for approximately 59%, 57% and 62% of our total revenues in 2006, 2005 and 2004, respectively. General Motors Corporation accounted for approximately 41%, 39% and 44%of our revenues in 2006, 2005 and 2004, respectively.

We also provide transportation services to other manufacturers who are suppliers for automobile manufacturers. Approximately 52%, 52% and 56% of our revenues were derived from transportation services provided to the automobile industry during 2006, 2005 and 2004, respectively. This portion of our business, however, is spread over 19 assembly plants and over 60 suppliers/vendors located throughout North America, which we believe reduces the risk of a material loss of business.

Revenue Equipment

At December 31, 2006, we operated a fleet of 1,998 tractors and 4,540 trailers. We operate late-model, well-maintained premium tractors to help attract and retain drivers, promote safe operations, minimize maintenance and repair costs, and improve customer service by minimizing service interruptions caused by breakdowns. We evaluate our equipment decisions based on factors such as initial cost, useful life, warranty terms, expected maintenance costs, fuel economy, driver comfort, customer needs, manufacturer support, and resale value. Our current policy is to replace most of our tractors at 500,000 miles, which normally occurs 30 to 48 months after purchase.

We historically have contracted with owner-operators to provide and operate a small portion of our tractor fleet. Owner-operators provide their own tractors and are responsible for all associated expenses, including financing costs, fuel, maintenance, insurance, and taxes. We believe that a combined fleet complements our recruiting efforts and offers greater flexibility in responding to fluctuations in shipper demand. At December 31, 2006 the Company's tractor fleet included 49 owner-operator tractors.

During 1999, the U.S. Environmental Protection Agency (“EPA”) proposed a three-phase strategy to reduce engine emissions from heavy-duty vehicles through a combination of advanced emissions control technologies and diesel fuel with a reduced sulfur content. Each phase and its effect on the Company’s operations, if known, are described below.

The first phase mandated new engine emission standards for all model year 2004 heavy-duty trucks, however, through agreements with heavy-duty diesel engine manufacturers, the effective date was accelerated to October 1, 2002. Therefore, effective October 1, 2002, all newly manufactured truck engines had to comply with the new engine emission standards. All truck engines manufactured prior to October 1, 2002 were not subject to these new standards. As of December 31, 2006, substantially allof our Company-owned truck fleet consisted of trucks with engines that comply with these emission standards. The Company has experienced a reduction in fuel efficiency and increased depreciation expense due to the higher cost of tractors with these new engines.

In the second phase, effective January 1, 2007, the EPA mandated a new set of more stringent emissions standards for vehicles powered by diesel fuel engines manufactured in 2007 through 2009. These new engines have been designed for and require the use of a more costly type of fuel known as ultra-low-sulfur-diesel (“ULSD”) which, according to EPA estimates, will cost from $.04 to $.05 more per gallon due to increased refining costs. The EPA has also mandated that refiners and importers nationwide must ensure that at least 80% of the volume of the highway diesel fuel they produce or import is ULSD-compliant by June 1, 2006, however, the EPA does not require service stations and truck stops to sell ULSD fuel. Therefore, it is possible that ULSD fuel might not be available in a particular area in which the Company operates. The Company’s current tractor fleet can be fueled with either ULSD or low-sulfur diesel (“LSD”) but future purchases of tractors which contain 2007 or later diesel engines will require the use of ULSD fuel which may result in lower fuel economy as the process that removes sulfur can also reduce the energy content of the fuel. During 2007, the Company expects to take delivery of its remaining 2006 tractor orders of approximately 350 tractors which will contain the 2006 diesel engines and does not expect to purchase tractors with the 2007 diesel engines until the second half of 2007. Compared to our current tractor fleet, we expect that tractors powered by the 2007 diesel engines will have an increased purchase price of approximately 10% and as a result, we expect that depreciation expense will increase as we replace older tractors with tractors powered by the 2007 diesel engines. We also expect that these engines will result in higher maintenance costs and be less fuel efficient. To the extent we are unable to offset these anticipated increased costs with rate increases charged to customers or offsetting cost savings in other areas, our results of operations would be adversely affected.

During the third phase, effective in 2010, final emission standards become effective and LSD fuel will no longer be available for highway use. The EPA requires that by June 1, 2010 all diesel fuel imported or produced must be ULSD-compliant as it phases out low-sulfur-diesel fuel availability by December 1, 2010 when all highway diesel fuel must be ULSD fuel. We are unable at this time to determine the increase in acquisition and operating costs of the final 2010 EPA-compliant engines but we expect that the engines produced under the final standards will be less fuel-efficient and have higher acquisition and maintenance costs than either the 2002 or 2007 engines.

Technology

We have installed Qualcomm Omnitracs™ display units in all of our tractors. The Omnitracs system is a satellite-based global positioning and communications system that allows fleet managers to communicate directly with drivers. Drivers can provide location status and updates directly to our computer which increases productivity and convenience. The Omnitracs system provides us with accurate estimated time of arrival information, which optimizes load selection and service levels to our customers. In order to optimize our tractor-to-trailer ratio, we have also installed Qualcomm TrailerTracs™ tracking units in all of our trailers. The TrailerTracs system is a trailer tracking product that enables us to more efficiently track the location of trailers in our inventory. During 2006, the Company began replacing its current tethered TrailerTracs units, which were unable to transmit data unless connected to Qualcomm-equipped tractors, with more advanced untethered TrailerTracs units which are able to operate and transmit data independent of a tractor connection. At December 31, 2006, approximately one-halfOperations of the Company’s trailer fleet has been fitted with these new untethered devicesprimary operating subsidiary, P.A.M. Transport, Inc., from 2020 to April 2023. He served as Vice President of Accounting of P.A.M. Transport from 2016 until 2020. Mr. Stewart previously served as Vice President of Finance, Chief Financial Officer, Secretary and Treasurer of the Company intends to install these new devices on its remaining trailer fleet during 2007.from 2010 until 2013 and as Vice President of Accounting and Controller of P.A.M. Transport from 2002 until 2010. He began his career with P.A.M. Transport in 1989 and served in various capacities before becoming Vice President of Accounting in 2002.

Our computer system manages the information provided by the Qualcomm devices to provide us real-time information regarding the location, status and load assignment of all of our equipment, which permits us to better meet delivery schedules, respond to customer inquiries and match equipment with the next available load. Our system also provides electronically to our customers real-time information regarding the status of freight shipments and anticipated arrival times. This system provides our customers flexibility and convenience by extending supply chain visibility through electronic data interchange, the Internet and e-mail.Delinquent Section 16(a) Reports

Maintenance

We have a strictly enforced comprehensive preventive maintenance program for our tractors and trailers. Inspections and various levels of preventive maintenance are performed at set mileage intervals on both tractors and trailers. A maintenance and safety inspection is performed on all vehicles each time they return to a terminal.

Our tractors carry full warranty coverage for at least three years or 350,000 miles. Extended warranties are negotiated with the tractor manufacturer and manufacturers of major components, such as engine, transmission and differential manufacturers, for up to four years or 500,000 miles. Trailers carry full warranties by the manufacturer and major component manufacturers for up to five years.

Employees

At December 31, 2006, we employed 3,062 persons, of whom 2,550 were drivers, 136 were maintenance personnel, 224 were employed in operations, 17 were employed in marketing, 66 were employed in safety and personnel, and 69 were employed in general administration and accounting. None of our employees are represented by a collective bargaining unit and we believe that our employee relations are good.

Drivers

At December 31, 2006, we utilized 2,550 company drivers in our operations. We also had 49 owner-operators under contract compensated on a per mile basis. Our drivers are compensated on the basis of miles driven, loading and unloading, extra stops and layovers in transit. Drivers can earn bonuses by recruiting other qualified drivers who become employed by us and both cash and non-cash prizes are awarded for consecutive periods of safe, accident-free driving. All of our drivers are recruited, screened, drug tested and trained and are subject to the control and supervision of our operations and safety departments. Our driver training program stresses the importance of safety and reliable, on-time delivery. Drivers are required to report to their driver managers daily and at the earliest possible moment when any condition en route occurs that might delay their scheduled delivery time.

In addition to strict application screening and drug testing, before being permitted to operate a vehicle our drivers must undergo classroom instruction on our policies and procedures, safety techniques as taught by the Smith System of Defensive Driving, the proper operation of equipment, and must pass both written and road tests. Instruction in defensive driving and safety techniques continues after hiring, with seminars at several of our terminals. At December 31, 2006, we employed 66 persons on a full-time basis in our driver recruiting, training and safety instruction programs.

Intense competition in the trucking industry for qualified drivers over the last several years, along with difficulties and added expense in recruiting and retaining qualified drivers, has had a negative impact on the industry. Our operations have also been impacted and from time to time we have experienced under-utilization and increased expenses due to a shortage of qualified drivers. We place a high priority on the recruitment and retention of an adequate supply of qualified drivers.

Executive Officers of the Registrant

Our executive officers are as follows:

Name | Age | Position with Company | Years of Service With P.A.M. |

| Robert W. Weaver | 57 | President and Chief Executive Officer | 24 |

| W. Clif Lawson | 53 | Executive Vice President and Chief Operating Officer | 22 |

| Larry J. Goddard | 48 | Vice President - Finance, Chief Financial Officer, Secretary and Treasurer | 19 |

Each of our executive officers has held his present position with the Company for at least the last five years. The Company has entered into an employment agreement with Robert W. Weaver that expires on July 10, 2009. The Company has the option to extend the employment agreement for two consecutive years following the July 10, 2009 expiration date for an additional one year at a time. The Company has also entered into employment agreements with both W. Clif Lawson and Larry J. Goddard which each expire on June 1, 2010. The Company has the option to extend these employment agreements for one additional year following the June 1, 2010 expiration date.

Internet Web Site

The Company maintains a web site where additional information concerning its business can be found. The address of that web site is www.pamt.com. The Company makes available free of charge on its Internet web site its Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d)16(a) of the Securities Exchange Act of 1934 (the “Exchange Act”) as soon as reasonably practicable after it electronically files or furnishes such materials to the Securitiesrequires our directors, executive officers and Exchange Commission.

Seasonality

Our revenues do not exhibit a significant seasonal pattern due primarily to our varied customer mix. Operating expenses can be somewhat higher in the winter months primarily due to decreased fuel efficiency and increased maintenance costs associated with inclement weather. In addition, the automobile plants for which we transport a large amount of freight typically utilize scheduled shutdowns of two weeks in July and one week in December and the volume of freight we ship is reduced during such scheduled plant shutdowns.

Regulation

We are a common and contract motor carrier regulated by various federal and state agencies. We are subject to safety requirements prescribed by the U.S. Department of Transportation (“DOT”). Such matters as weight and dimension of equipment are also subject to federal and state regulations. Allpersons who own more than 10% of our drivers are requiredoutstanding common stock to obtain national driver’s licenses pursuant to the regulations promulgated by the DOT. Also, DOT regulations impose mandatory drug and alcohol testing of drivers. We believe that we are in compliance in all material respects with applicable regulatory requirements relating to our trucking business and operate with a “satisfactory” rating (the highest of three grading categories) from the DOT.

Our motor carrier operations are also subject to environmental laws and regulations, including laws and regulations dealing with underground fuel storage tanks, the transportation of hazardous materials and other environmental matters, and our operations involve certain inherent environmental risks. We maintain four bulk fuel storage and fuel islands. Our operations involve the risks of fuel spillage or seepage, environmental damage, and hazardous waste disposal, among others. We have instituted programs to monitor and control environmental risks and assure compliance with applicable environmental laws. As part of our safety and risk management program, we periodically perform internal environmental reviews so that we can achieve environmental compliance and avoid environmental risk. We transport a minimum amount of environmentally hazardous substances and, to date, have experienced no significant claims for hazardous materials shipments. If we should fail to comply with applicable regulations, we could be subject to substantial fines or penalties and to civil and criminal liability.

Company operations conducted in industrial areas, where truck terminals and other industrial activities are conducted, and where groundwater or other forms of environmental contamination have occurred, potentially expose us to claims that we contributed to the environmental contamination.

We believe we are currently in material compliance with applicable laws and regulations and that the cost of compliance has not materially affected results of operations.

In addition to environmental regulations directly affecting our business, we are also subject to the effects of new tractor engine design requirements implemented by the EPA. See "Revenue Equipment", above.

The Federal Motor Carrier Safety Administration ("FMCSA") issued a final rule on April 24, 2003 that made several changes to the regulations that govern truck drivers' hours of service ("HOS"). These new federal regulations became effective on January 4, 2004. On July 16, 2004, the U.S. Circuit Court of Appeals for the District of Columbia rejected these new hours of service rules for truck drivers that had been in place since January 2004 because it said the FMCSA had failed to address the impact of the rules on the health of drivers as required by Congress. In addition, the judge's ruling noted other areas of concern including the increase in driving hours from 10 hours to 11 hours, the exception that allows drivers in trucks with sleeper berths to split their required rest periods, the new rule allowing drivers to reset their 70-hour clock to 0 hours after 34 consecutive hours off duty, and the decision by the FMCSA not to require the use of electronic onboard recorders to monitor driver compliance. On September 30, 2004, the extension of the Federal highway bill signed into law by the President of the United States extended the current hours of service rules for one year or until the FMCSA developed a new set of regulations, whichever came first. On January 24, 2005, the FMCSA re-proposed its April 2003 HOS rules, adding references to how the rules would affect driver

health, but making no changes to the regulations. The FMCSA sought public comments by March 10, 2005 on what changes to the rule, if any, were necessary to respond to the concerns raised by the court, and to provide data or studies that would support changes to, or continued use of, the 2003 rule. Effective October 1, 2005, the April 2003 HOS rules became effective with the most significant change requiring drivers that utilize the sleeper berth provision to take at least eight consecutive hours in the sleeper berth during their ten hours off-duty. Under previous regulations, drivers were allowed to split their ten hour off-duty time in the sleeper berth into two periods, provided neither period was less than two hours. This more restrictive sleeper berth provision may impact multiple-stop shipments and those shipments incurring delays in loading or unloading. Improper planning on such shipments could result in delivery delays and equipment utilization inefficiencies.

Set forth below and elsewhere in this Report and in other documents we file with the SEC initial reports of ownership and reports of changes in ownership of our common stock. Executive officers, directors and greater than 10% stockholders are risksalso required to furnish us with copies of the reports that they file. To our knowledge, based solely on a review of the copies of the reports furnished to us and uncertaintiesrepresentations received from our directors and executive officers, we believe that could causeall reports required to be filed under Section 16(a) for 2023 were timely filed, except that one Form 4 each for Joseph A. Vitiritto and Allen W. West were not filed timely, each reporting an award of restricted shares.

Code of Ethics

We have adopted a written code of ethics that applies to all our actual resultsdirectors, officers and employees, including our CEO and our chief financial and accounting officer. We have posted a copy of our Code of Ethics on our website at www.pamtransport.com under the caption “Investors.” In addition, we intend to differ materially from the results contemplated by the forward-looking statements contained in this Report.

Our business is subject to general economic and business factorspost on our website all disclosures that are largely outrequired by law or NASDAQ listing standards concerning any amendments to, or waivers from, any provision of our control, any of which could have a material adverse effect on our operating results.the code.

These factors include significant increases or rapid fluctuations in fuel prices, excess capacity in the trucking industry, surpluses in the market for used equipment, interest rates, fuel taxes, license and registration fees, insurance premiums, self-insurance levels, and difficulty in attracting and retaining qualified drivers and independent contractors.

We are also affected by recessionary economic cycles and downturns in customers’ business cycles, particularly in market segments and industries, such as the automotive industry, where we have a significant concentration of customers. Economic conditions may adversely affect our customers and their ability to pay for our services.

We operate in a highly competitive and fragmented industry, and our business may suffer if we are unable to adequately address downward pricing pressures and other factors that may adversely affect our ability to compete with other carriers.

Numerous competitive factors could impair our ability to maintain our current profitability. These factors include, but are not limited to, the following:

·we compete with many other truckload carriers of varying sizes and, to a lesser extent, with less-than-truckload carriers and railroads, some of which have more equipment and greater capital resources than we do;

·some of our competitors periodically reduce their freight rates to gain business, especially during times of reduced growth rates in the economy, which may limit our ability to maintain or increase freight rates, maintain our margins or maintain significant growth in our business;

·many customers reduce the number of carriers they use by selecting so-called “core carriers” as approved service providers, and in some instances we may not be selected;

·many customers periodically accept bids from multiple carriers for their shipping needs, and this process may depress freight rates or result in the loss of some of our business to competitors;

·the trend toward consolidation in the trucking industry may create other large carriers with greater financial resources and other competitive advantages relating to their size and with whom we may have difficulty competing;

·advances

Director Nominating Process

Our Board does not have a nominating committee that nominates candidates for election to our Board. That function is performed by our Board of Directors. Each member of our Board participates in technology require increased investmentsthe consideration of director nominees. Our Board of Directors believes that it can adequately fulfill the functions of a nominating committee without having to remain competitive,appoint an additional committee to perform that function. Our Board of Directors believes that not having a separate nominating committee saves the administrative expense that would be incurred in maintaining such a committee, and saves time for directors who would serve on a nominating committee if it were established. As there is no nominating committee, we do not have a nominating committee charter.

At least a majority of our customers may notindependent directors participate in the consideration of director nominees. These directors are independent, as independence for nominating committee members is defined in the NASDAQ listing standards. However, so long as the Company continues to be willing to accept higher freight rates to covera controlled company (within the costmeaning of these investments;

·competition from Internet-based and other logistics and freight brokerage companies may adversely affect our customer relationships and freight rates; and

·economiesNASDAQ Rule 5615(c)(1)), the Board of scale thatDirectors may be passed onguided by the recommendations of the Company’s controlling stockholders in its nominating process. After discussion and evaluation of potential nominees, the full Board of Directors selects the director nominees.

Our Board will consider as potential nominees persons recommended by stockholders. Recommendations should be submitted to smaller carriersour Board of Directors in care of our Secretary, Tyler Majors, at Post Office Box 188, Tontitown, Arkansas 72770. Each recommendation should include a personal biography of the suggested nominee, a description of the background or experience that qualifies the person for consideration, and a statement that the person has agreed to serve if nominated and elected. If a stockholder desires to nominate a director candidate for election at the Annual Meeting but does not intend to recommend the candidate for consideration as part of the Board’s slate of director nominees, such stockholder must comply with the procedural and informational requirements described in Section 1.11 of our Bylaws. A copy of our Bylaws may be obtained upon written request to our Secretary.

Our Board has used an informal process to identify potential candidates for nomination as directors. Candidates for nomination have been recommended by procurement aggregation providers may improve their abilityan executive officer or director, and considered by our Board of Directors. Generally, candidates have been known to compete with us.

We are highly dependent on our major customers, the loss of one or more of which could haveour Board members. Our Board of Directors has not adopted specific minimum qualifications that it believes must be met by a material adverse effect on our business.

A significant portion of our revenue is generated from our major customers. For 2006, our top five customers, based on revenue, accountedperson it recommends for approximately 59% of our revenue, and our largest customer, General Motors Corporation, accounted for approximately 41% of our revenue. We also provide transportation services to other manufacturers who are suppliers for automobile manufacturers. As a result, concentration of our business within the automobile industry is greater than the concentration in a single customer. Approximately 52% of our revenues for 2006 were derived from transportation services provided to the automobile industry.

Generally, we do not have long-term contractual relationships with our major customers, and we cannot assure that our customer relationships will continue as presently in effect. A reduction in or termination of our services by our major customers could have a material adverse effect on our business and operating results.

Ongoing insurance and claims expenses could significantly reduce our earnings.

Our future insurance and claims expenses might exceed historical levels, which could reduce our earnings. The Company is self insured for health and workers compensation insurance coverage up to certain limits. If medical costs continue to increase, or if the severity or number of claims increase, and if we are unable to offset the resulting increases in expenses with higher freight rates, our earnings could be materially and adversely affected.

We may be unable to successfully integrate businesses we acquire into our operations.

Integrating businesses we acquire may involve unanticipated delays, costs or other operational or financial problems. Successful integration of the businesses we acquire depends on a number of factors, including our ability to transition acquired companies to our management information systems. In integrating businesses we acquire, we may not achieve expected economies of scale or profitability or realize sufficient revenues to justify our investment. We also face the risk that an unexpected problem at one of the companies we acquire will require substantial time and attention from senior management, diverting management’s attention from other aspects of our business. We cannot be certain that our management and operational controls will be able to support us as we grow.

Difficulty in attracting drivers could affect our profitability and ability to grow.

Periodically, the transportation industry experiences difficulty in attracting and retaining qualified drivers, including independent contractors, resulting in intense competition for drivers. We have from time to time experienced under-utilization and increased expenses due to a shortage of qualified drivers. If we are unable to continue to attract drivers and contract with independent contractors, we could be required to further adjust our driver compensation package or let trucks sit idle, which could adversely affect our growth and profitability.

If we are unable to retain our key employees, our business, financial condition and results of operations could be harmed.

We are highly dependent upon the services of the following key employees: Robert W. Weaver, our President and Chief Executive Officer; W. Clif Lawson, our Executive Vice President and Chief Operating Officer; and Larry J. Goddard, our Vice President and Chief Financial Officer. We do not maintain key-man life insurance on any of these executives. The loss of any of their services could have a material adverse effect on our operations and future profitability. We must continue to develop and retain a core group of managers if we are to realize our goal of expanding our operations and continuing our growth. We cannot assure that we will be able to do so.

We have significant ongoing capital requirements that could affect our profitability if we are unable to generate sufficient cash from operations.

The trucking industry is very capital intensive. If we are unable to generate sufficient cash from operations in the future, we may have to limit our growth, enter into financing arrangements, or operate our revenue equipment for longer periods, any of which could have a material adverse affect on our profitability.

Our operations are subject to various environmental laws and regulations, the violation of which could result in substantial fines or penalties.

We are subject to various environmental laws and regulations dealing with the handling of hazardous materials, underground fuel storage tanks, and discharge and retention of stormwater. We operate in industrial areas, where truck terminals and other industrial activities are located, and where groundwater or other forms of environmental contamination could occur. We also maintain bulk fuel storage and fuel islands at four of our facilities. Our operations involve the risks of fuel spillage or seepage, environmental damage, and hazardous waste disposal, among others. If we are involved in a spill or other accident involving hazardous substances, or if we are found to be in violation of applicable laws or regulations, it could have a materially adverse effect on our business and operating results. If we should fail to comply with applicable environmental regulations, we could be subject to substantial fines or penalties and to civil and criminal liability.

We operate in a highly regulated industry and increased costs of compliance with, or liability for violation of, existing or future regulations could have a material adverse effect on our business.

The U.S. Department of Transportation and various state agencies exercise broad powers over our business, generally governing such activities as authorization to engage in motor carrier operations, safety, and financial reporting. We may also become subject to new or more restrictive regulations relating to fuel emissions, drivers’ hours in service, and ergonomics. Compliance with such regulations could substantially impair equipment productivity and increase our operating expenses.

The EPA adopted new emissions control regulations, which require progressive reductions in exhaust emissions from diesel engines through 2010, for engines manufactured in October 2002 and thereafter. In part to offset the costs of compliance with the new EPA engine design requirements, some manufacturers have significantly increased new equipment prices and eliminated or sharply reduced the price of repurchase or trade-in commitments. If new equipment prices were to increase, or if the price of repurchase commitments by equipment manufacturers were to decrease, more than anticipated, we may be required to increase our depreciation and financing costs and/or retain some of our equipment longer, with a resulting increase in maintenance expenses. To the extent we are unable to offset any such increases in expenses with rate increases or cost savings, our results of operations would be adversely affected. If our fuel or maintenance expenses were to increasenomination as a result of our use of the new, EPA-compliant engines, and we are unable to offset such increases with fuel surcharges or higher freight rates, our results of operations would be adversely affected. Further, our business and operations could be adversely impacted if we experience problems with the reliability of the new engines. We began operating tractors with engines meeting the EPA guidelines during 2003. Although we have not experienced any significant reliability issues with these engines to date, the expenses associated with the tractors containing these engines have been slightly elevated, primarily as a result of lower fuel efficiency and higher depreciation.

None.

Our executive offices and primary terminal facilities, which we own, are located in Tontitown, Arkansas. These facilities are located on approximately 49.3 acres and consist of 114,403 square feet of office space and maintenance and storage facilities.

Our subsidiaries lease facilities in Jacksonville, Florida; Breese and Effingham, Illinois; Parsippany and Paulsboro, New Jersey; North Jackson, Ohio; Oklahoma City, Oklahoma; and Laredo and El Paso, Texas. Our terminal facilities in Columbia, Mississippi; Irving, Texas; North Little Rock, Arkansas; and Willard, Ohio are owned. The leased facilities are leased primarily on contractual terms ranging from one to five years. The following provides a summary of the ownership and types of activities conducted at each location:

Location

| Own/

Lease

| Dispatch

Office

| Maintenance

Facility

| Safety

Training

|

Tontitown, Arkansas | Own | Yes | Yes | Yes |

North Little Rock, Arkansas | Own | Yes | Yes | No |

Jacksonville, Florida | Lease | Yes | Yes | Yes |

Breese, Illinois | Lease | Yes | No | No |

Effingham, Illinois | Lease | No | Yes | No |

Columbia, Mississippi | Own | No | No | No |

Parsippany, New Jersey | Lease | Yes | Yes | Yes |

Paulsboro, New Jersey | Lease | Yes | No | No |

North Jackson, Ohio | Lease | Yes | Yes | Yes |

Willard, Ohio | Own | Yes | Yes | Yes |

Oklahoma City, Oklahoma | Lease | Yes | Yes | Yes |

El Paso, Texas | Lease | Yes | Yes | No |

Irving, Texas | Own | Yes | Yes | Yes |

Laredo, Texas | Lease | Yes | Yes | No |

We also have access to trailer drop and relay stations in various other locations across the country. We lease certain of these facilities on a month-to-month basis from an affiliate of our largest shareholder.

We believe that all of the properties that we own or lease are suitabledirector. In evaluating candidates for their purposes and adequate to meet our needs.

The nature of our business routinely results in litigation, primarily involving claims for personal injuries and property damage incurred in the transportation of freight. We believe that all such routine litigation is adequately covered by insurance and that adverse results in one or more of those cases would not have a material adverse effect on our financial condition.

No matters were submitted to a vote of our security holders during the fourth quarter ended December 31, 2006.

PART II

Our common stock is traded on the NASDAQ Global Market under the symbol PTSI. The following table sets forth, for the quarters indicated, the range of the high and low sales prices per share for our common stock as reported on the NASDAQ Global Market.

Calendar Year Ended December 31, 2006

| | | High | | Low | |

| First Quarter | | $ | 25.18 | | $ | 17.51 | |

| Second Quarter | | | 28.96 | | | 23.24 | |

| Third Quarter | | | 31.50 | | | 23.78 | |

| Fourth Quarter | | | 26.68 | | | 20.90 | |

Calendar Year Ended December 31, 2005

| | | High | | Low | |

| First Quarter | | $ | 19.49 | | $ | 16.47 | |

| Second Quarter | | | 17.35 | | | 13.43 | |

| Third Quarter | | | 17.90 | | | 15.71 | |

| Fourth Quarter | | | 18.85 | | | 15.16 | |

As of March 5, 2007, there were approximately 178 holders of record of our common stock.

Dividends

We have not declared or paid any cash dividends on our common stock for the two most recent fiscal years. The policy ofnomination, our Board of Directors iswill consider the factors it believes to retain earnings forbe appropriate, which would generally include the expansioncandidate’s independence, personal and development of ourprofessional integrity, business judgment, relevant experience and the payment of our debt service obligations. Future dividend policyskills, including those related to transportation services, and the payment of dividends, if any, willpotential to be determined by the Board of Directors in light of circumstances then existing, including our earnings, financial condition and other factors deemed relevant by the Board of Directors.

Repurchases of Common Stock

On October 24, 2003, the Company announced the approval by the Board of Directors of a stock repurchase program in which the Company was authorized to purchase 300,000 shares of its common stock at prevailing market prices over a twelve month period. The stock repurchase program expired during the fourth quarter of 2004 with no purchases by the Company during the authorized twelve month period.

On April 11, 2005, the Company announced that the Board of Directors had authorized the Company to repurchase up to 600,000 shares of its common stock during the six month period ending October 11, 2005. These 600,000 shares were all repurchased by September 30, 2005. On September 6, 2005, the Company announced that its Board of Directors had authorized the Company to extend the stock repurchase program until September 6, 2006 and to include up to an additional 900,000 shares of its common stock. The Company repurchased 458,600 shares of these additional shares prior to the September 6, 2006 program expiration date. There were no repurchases during the fourth quarter of 2006.

See Part III, Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of this Annual Report for a presentation of compensation plans under which equity securities of the Company are authorized for issuance.

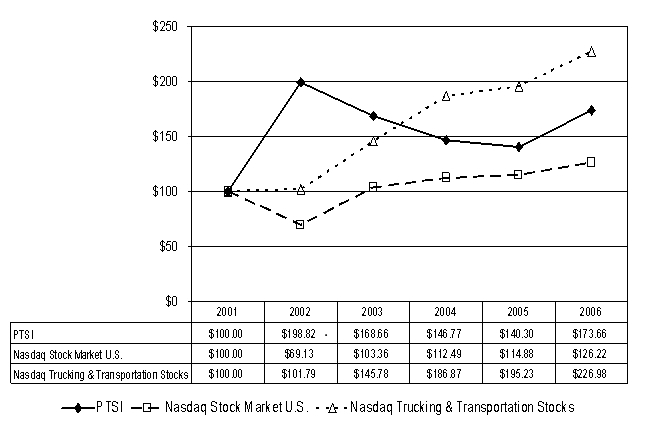

Performance Graph

Set forth below is a line graph comparing the yearly percentage change in the cumulative total stockholder return on our common stock against the cumulative total return of the CRSP Total Return Index for the Nasdaq Stock Market (U.S. companies) and the CRSP Total Return Index for the Nasdaq Trucking and Transportation Stocks for the period of five years commencing December 31, 2001 and ending December 31, 2006. The graph assumes that the value of the investment in our common stock and in each index was $100 on December 31, 2001 and that all dividends were reinvested.

The following selected financial and operating data should be readeffective director in conjunction with the Consolidated Financial Statements and notes thereto included elsewhere in this Report.

| | | Year Ended December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | | (in thousands, except earnings per share amounts) | |

Statement of Operations Data: | | | | | | | | | | | |

| Operating revenues: | | | | | | | | | | | | | | | | |

| Operating revenues, before fuel surcharge | | $ | 351,373 | | $ | 326,353 | | $ | 309,475 | | $ | 293,547 | | $ | 264,012 | |

| Fuel surcharge (1) | | | 48,896 | | | 34,527 | | | 15,591 | | | 7,491 | | | 2,042 | |

| Total operating revenues | | | 400,269 | | | 360,880 | | | 325,066 | | | 301,038 | | | 266,054 | |

| | | | | | | | | | | | | | | | | |

| Operating expenses: | | | | | | | | | | | | | | | | |

| Salaries, wages and benefits | | | 127,539 | | | 122,005 | | | 119,519 | | | 119,350 | | | 115,432 | |

| Fuel expense (2) | | | 97,286 | | | 81,017 | | | 55,645 | | | 42,883 | | | 35,103 | |

| Rent and purchased transportation | | | 43,844 | | | 39,074 | | | 38,938 | | | 35,287 | | | 9,780 | |

| Depreciation and amortization | | | 33,929 | | | 31,376 | | | 30,016 | | | 26,601 | | | 24,715 | |

| Operating supplies (1)(2) | | | 25,682 | | | 23,114 | | | 21,718 | | | 20,358 | | | 18,100 | |

| Operating taxes and licenses | | | 16,421 | | | 15,776 | | | 15,488 | | | 14,710 | | | 13,467 | |

| Insurance and claims | | | 16,389 | | | 15,992 | | | 15,820 | | | 13,500 | | | 12,786 | |

| Communications and utilities | | | 2,642 | | | 2,648 | | | 2,690 | | | 2,540 | | | 2,284 | |

| Other | | | 5,426 | | | 6,205 | | | 5,131 | | | 4,755 | | | 4,620 | |

| Loss on sale or disposal of property | | | 47 | | | 147 | | | 915 | | | 368 | | | 127 | |

| Total operating expenses | | | 369,205 | | | 337,354 | | | 305,880 | | | 280,352 | | | 236,414 | |

| Operating income | | | 31,064 | | | 23,526 | | | 19,186 | | | 20,686 | | | 29,640 | |

| Non-operating income | | | 448 | | | 477 | | | 464 | | | 276 | | | - | |

| Interest expense | | | (1,475 | ) | | (1,881 | ) | | (1,758 | ) | | (1,667 | ) | | (1,985 | ) |

| Income before income taxes | | | 30,037 | | | 22,122 | | | 17,892 | | | 19,295 | | | 27,655 | |

| Income taxes | | | 12,073 | | | 8,983 | | | 7,304 | | | 7,805 | | | 11,062 | |

| Net income | | $ | 17,964 | | $ | 13,139 | | $ | 10,588 | | $ | 11,490 | | $ | 16,593 | |

| Earnings per common share: | | | | | | | | | | | | | | | | |

| Basic | | $ | 1.74 | | $ | 1.20 | | $ | 0.94 | | $ | 1.02 | | $ | 1.56 | |

| Diluted | | $ | 1.74 | | $ | 1.20 | | $ | 0.94 | | $ | 1.01 | | $ | 1.55 | |

| Average common shares outstanding - Basic | | | 10,296 | | | 10,966 | | | 11,298 | | | 11,291 | | | 10,669 | |

| Average common shares outstanding - Diluted(3) | | | 10,302 | | | 10,976 | | | 11,324 | | | 11,326 | | | 10,715 | |

__________

(1) | In order to conform to industry practice, during 2004 the Company began to classify fuel surcharges charged to customers as revenue rather than as a reduction of operating supplies expense. This reclassification has no effect on net operating income, net income or earnings per share. The Company has made corresponding reclassifications to comparative periods shown. |

(2) | Because of the increased impact of fuel costs on the Company’s results of operations in recent years, during 2006 the Company began to separately display as a line item “Fuel expense” for amounts paid for fuel which had previously been aggregated with other operating supplies and included in the line item “Operating supplies”. This reclassification has no effect on net operating income, net income or earnings per share. The Company has made corresponding reclassifications to comparative periods shown. |

(3) | Diluted income per share for 2006, 2005, 2004, 2003 and 2002 assumes the exercise of stock options to purchase an aggregate of 55,738, 22,297, 62,224, 77,758 and 87,984 shares of common stock, respectively. |

| | | At December 31, | |

| | | 2006 | | 2005 | | 2004 | | 2003 | | 2002 | |

Balance Sheet Data: | | (in thousands) | |

| Total assets | | $ | 314,246 | | $ | 293,441 | | $ | 285,349 | | $ | 264,849 | | $ | 228,320 | |

| Long-term debt, excluding current portion | | | 21,205 | | | 39,693 | | | 23,225 | | | 26,740 | | | 20,175 | |

| Stockholders' equity | | | 185,028 | | | 164,762 | | | 168,543 | | | 156,875 | | | 144,452 | |

| | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | | | 2006 | | | 2005 | | | 2004 | | | 2003 | | | 2002 | |

Operating Data: | | | | | | | | | | | | | | | | |

| Operating ratio (1) | | | 91.2 | % | | 92.8 | % | | 93.8 | % | | 92.9 | % | | 88.7 | % |

| Average number of truckloads per week | | | 7,200 | | | 6,946 | | | 7,278 | | | 7,105 | | | 6,463 | |

| Average miles per trip | | | 659 | | | 680 | | | 664 | | | 701 | | | 755 | |

| Total miles traveled (in thousands) | | | 229,810 | | | 228,624 | | | 235,894 | | | 242,890 | | | 238,256 | |

| Average miles per tractor | | | 123,156 | | | 125,479 | | | 127,124 | | | 131,934 | | | 136,772 | |

| Average revenue, before fuel surcharge per tractor per day | | $ | 778 | | $ | 740 | | $ | 684 | | $ | 653 | | $ | 621 | |

| Average revenue, before fuel surcharge per loaded mile | | $ | 1.43 | | $ | 1.33 | | $ | 1.19 | | $ | 1.13 | | $ | 1.15 | |

| Empty mile factor | | | 5.9 | % | | 5.5 | % | | 4.7 | % | | 4.5 | % | | 4.0 | % |

| | | | | | | | | | | | | | | | | |

At end of period: | | | | | | | | | | | | | | | | |

| Total company-owned/leased tractors | | | 1,998(2 | ) | | 1,792(3 | ) | | 1,857(4 | ) | | 1,913(5 | ) | | 1,781(6 | ) |

| Average age of tractors (in years) | | | 1.55 | | | 1.43 | | | 1.70 | | | 1.94 | | | 2.12 | |

| Total trailers | | | 4,540 | | | 4,406 | | | 4,257 | | | 4,175 | | | 3,973 | |