SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20132015

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

Commission File Number 1-9804

PULTEGROUP, INC.

(Exact name of registrant as specified in its charter)

|

| | |

| MICHIGAN | | 38-2766606 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

100 Bloomfield Hills Parkway,3350 Peachtree Road NE, Suite 300150

Bloomfield Hills, Michigan 48304Atlanta, Georgia 30326

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (248) 647-2750(404) 978-6400

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $0.01 | | New York Stock Exchange |

PulteGroup, Inc. 7.375% Senior Notes due 2046 | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [X] NO [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES [ ] NO [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Act. YES [X] NO [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X][ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [X] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES [ ] NO [X]

The aggregate market value of the registrant’s voting stock held by nonaffiliates of the registrant as of June 30, 20132015, based on the closing sale price per share as reported by the New York Stock Exchange on such date, was $7,299,008,8717,084,534,862.

As of February 1, 20142016, the registrant had 381,299,600349,148,351 shares of common stock outstanding.

Documents Incorporated by Reference

Applicable portions of the Proxy Statement for the 20142016 Annual Meeting of Shareholders are incorporated by reference in Part III of this Form.

PULTEGROUP, INC.

TABLE OF CONTENTS

| | Item No. | | Page No. | | Page No. |

| | | | | |

| | | |

| 1 | | | | |

| | | |

| 1A | | | | |

| | | |

| 1B | | | | |

| | | |

| 2 | | | | |

| | | |

| 3 | | | | |

| | | |

| 4 | | | | |

| | | |

| 4A | | | | |

| | | |

| | | | | |

| | | |

| 5 | | | | |

| | | |

| 6 | | | | |

| | | |

| 7 | | | | |

| | | |

| 7A | | | | |

| | | |

| 8 | | | | |

| | | |

| 9 | | | | |

| | | |

| 9A | | | | |

| | | |

| 9B | | | | |

| | | |

| | | | | |

| | | |

| 10 | | | | |

| | | |

| 11 | | | | |

| | | |

| 12 | | | | |

| | | |

| 13 | | | | |

| | | |

| 14 | | | | |

| | | |

| | | | | |

| | | |

| 15 | | | | |

| | | |

| | | | | |

PART I

ITEM I. BUSINESS

PulteGroup, Inc.

PulteGroup, Inc. is a Michigan corporation organized in 1956. We are one of the largest homebuilders in the United States ("U.S."), and our common stock trades on the New York Stock Exchange under the ticker symbol “PHM”. Unless the context otherwise requires, the terms "PulteGroup", the "Company", "we", "us", and "our" used herein refer to PulteGroup, Inc. and its subsidiaries. While our subsidiaries engage primarily in the homebuilding business, we also have mortgage banking operations, conducted principally through Pulte Mortgage LLC (“Pulte Mortgage”), and title operations.

Homebuilding, our core business, includes the acquisition and development of land primarily for residential purposes within the U.S. and the construction of housing on such land. Homebuilding offers a broad product line to meet the needs of home buyershomebuyers in our targeted markets. Through our brands, which include Pulte Homes, Del Webb, and Centex, (acquired through our merger with Centex Corporation ("Centex") in 2009), we offer a wide variety of home designs, including single-family detached, townhouses, condominiums, and duplexes at different prices and with varying levels of options and amenities to our major customer groups: entry-level,first-time, move-up, and active adult. Over our history, we have delivered over 625,000655,000 homes.

As of December 31, 20132015, we conducted our operations in 4850 markets located throughout 2726 states. For reporting purposes, our Homebuilding operations are aggregated into six reportable segments:

|

| | |

| Northeast: | | Connecticut, Delaware, Maryland, Massachusetts, New Jersey, New York, Pennsylvania,

Rhode Island, Virginia |

| Southeast: | | Georgia, North Carolina, South Carolina, Tennessee |

| Florida: | | Florida |

| Midwest: | | Illinois, Indiana, Kentucky, Michigan, Minnesota, Missouri, Ohio |

| Texas: | | Texas |

North: | | Illinois, Indiana, Michigan, Minnesota, Missouri, Northern California, Ohio, Oregon, Washington |

Southwest:West: | | Arizona, California, Nevada, New Mexico, Southern CaliforniaWashington |

We also have a reportable segment for our financial services operations, which consist principally of mortgage banking and title operations. Our Financial Services segment operates generally in the same geographic markets as our Homebuilding segments.

Financial information for each of our reportable business segments is included in Note 54 to our Consolidated Financial Statements.

Available information

Our internet website address is www.pultegroupinc.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge through our website as soon as reasonably practicable after we electronically file them with or furnish them to the Securities and Exchange Commission. Our code of ethics for principal officers, our code of ethical business conduct, our corporate governance guidelines, and the charters of the Audit, Compensation and Management Development, Nominating and Governance, and Finance and Investment committeesCommittees of our Board of Directors are also posted on our website and are available in print, free of charge, upon request.

Homebuilding Operations

| | | | Years Ended December 31, ($000’s omitted) | Years Ended December 31, ($000’s omitted) |

| | 2013 | | 2012 | | 2011 | | 2010 | | 2009 | 2015 | | 2014 | | 2013 | | 2012 | | 2011 |

| Home sale revenues | $ | 5,424,309 |

| | $ | 4,552,412 |

| | $ | 3,950,743 |

| | $ | 4,419,812 |

| | $ | 3,869,297 |

| $ | 5,792,675 |

| | $ | 5,662,171 |

| | $ | 5,424,309 |

| | $ | 4,552,412 |

| | $ | 3,950,743 |

|

| Home closings | 17,766 |

| | 16,505 |

| | 15,275 |

| | 17,095 |

| | 15,013 |

| 17,127 |

| | 17,196 |

| | 17,766 |

| | 16,505 |

| | 15,275 |

|

Beginning in 2006 and continuing through 2011, the U.S. housing market experienced a significant decline in the demand for new homes as well as a sharp decline in overall residential real estate values. U.S. new home sales in 2011 were the lowest since 1962. As a result of this industry-wide downturn, we suffered net losses in each year between 2007 - 2011 from a combination of reduced operational profitability and significant asset impairments. In response to these market conditions, we restructured our operations, including making significant reductions in employee headcount and overhead costs, and managed our business to generate cash, including curtailing our investments in inventory. We used this positive cash flow to, among other things, increase our cash reserves as well as retire outstanding debt.

In 2012, new home sales in the U.S. increased for the first time since 2005. In 2013, thisThis trend continued in 2015 as new home sales in the U.S. rose 16%15% to approximately 428,000501,000 homes, an approximate 40%64% increase from the bottom of the housing cycle in 2011. Additionally, mortgage interest rates remain near historic lows and the overall inventory of homes available for sale, especially new homes, remains low. Although current industry volume remains low compared with historical levels, the improved environment and the actions we have taken contributed to our return to profitability in 2012 and a significant increaseincreases in our profitabilityincome before income taxes each year in 2013.the period 2013 - 2015. In the long term, we continue to believe that the national publicly-traded builders will have a competitive advantage over local builders through their ability to leverage economies of scale, access to more reliable and lower cost financing through the capital markets, ability to control and entitle large land positions, and greater geographic and product diversification. Among the national publicly-traded peer group, we believe that builders with broad geographic and product diversity, and sustainable capital positions will benefit as market conditions recover. In the short-term, we expect that overall market conditions will continue to improve but that improvements will occur unevenly across our markets. Our strategy to enhance shareholder value is centered around the following operational objectives:

Improving our inventory turns;

More effectivelyEffectively allocating the capital we invest in our business using a risk-based portfolio approach;

Maximizing our inventory turns while maintaining an adequate supply of house and land inventory;

Enhancing revenues by: establishing clear product offerings for each of our brands based on systematic, consumer-driven input, optimizing our pricing through the expanded use of options and lot premiums, and lesseninglimiting our reliance on speculative home sales;

Reducing our house costs through common house plan management, value-engineering our house plans, and working with suppliers to reduce costs; and

Maintaining an efficient overhead structure.

Our Homebuilding operations are geographically diverse within the U.S. As of December 31, 2013,2015, we had 577620 active communities.communities spanning 50 markets across 26 states. Sales prices of unit closings during 20132015 ranged from less than $100,000$100,000 to greater than $1,200,000,$1,500,000, with 86%85% falling within the range of $100,000$150,000 to $450,000.$500,000. The average unit selling price in 20132015 was $305,000,$338,000, compared with $276,000$329,000 in 2012, $259,0002014, $305,000 in 2011, $259,0002013, $276,000 in 2010,2012, and $258,000$259,000 in 2009.2011. The increase in average selling price in recent years resulted from a number of factors, including improved market conditions and a shift in our sales mix toward move-up and active adult homebuyers.

Sales of single-family detached homes, as a percentage of total unit sales, were 86% in 2015, compared with 86% in 2014, 85% in 2013, compared with 81% in 2012, and 79% in 2011, 79% in 2010, and 77% in 2009. The increase in the percentage of single-family detached homes can be attributed to a weakened demand for townhouses, condominiums, and other attached housing, as prices forshift in our business toward the move-up buyer, who tends to prefer detached new homes have become more affordable for entry-level and active adult homebuyers.homes.

Ending backlog, which represents orders for homes that have not yet closed, was $1.9$2.5 billion (5,772 (6,731 units) at December 31, 20132015 and $1.9 billion (6,4585,850 units) at December 31, 20122014. For each orderorders in backlog, we have received a signed customer contract and customer deposit, which is refundable in certain instances. Of the orders in backlog at December 31, 20132015, substantially all are scheduled to be closed during 20142016, though all orders are subject to potential cancellation by or final negotiations with the customer. In the event of cancellation, the majority of our sales contracts stipulate that we have the right to retain the customer’s deposit, though we may choose to refund the deposit in certain instances.

Land acquisition and development

We acquire land primarily for the construction of homes for sale to homebuyers. We select locations for development of homebuilding communities after completing a feasibility study, which includes, among other things, soil tests, independent environmental studies and other engineering work, an evaluation of necessary zoning and other governmental entitlements, and extensive market research that enables us to match the location with our product offering to targeted consumer groups. We consider factors such as proximity to developed areas, population and job growth patterns, and, if applicable, estimated development costs. We frequently manage a portion of the risk of controlling our land positions through the use of land option contracts, which enable us to defer acquiring portions of properties owned by land sellers until we have determined whether and when to exercise our option. Our use of land option agreements reduces ourthe financial risksrisk associated with long-term land holdings. We typically acquire land with the intent to complete sales of housing units within 24 to 36 months from the date of opening a community, except in the case of certain Del Webb active adult developments and other large master-planned projects for which the completion of community build-out requires a longer time period. While our overall supply of controlled land is in excess of our short-term needs in many of our markets, some of our controlled land consists of long-term positions that will not be converted to home sales in the near term. Accordingly, we remain active in our pursuit of new land investment. We may also periodically sell select parcels of land to third parties for commercial or other development. Additionally,development if we may determine that certain land assets no longerthey do not fit into our strategic operating plans.

Land is generally purchased after it is properly zoned and developed, or is ready for development.development for our intended use. In the normal course of business, we dispose of owned land not required by our homebuilding operations through sales to appropriate end users.sales. Where we develop land, we engage directly in many phases of the development process, including: land and site planning; obtaining environmental and other regulatory approvals; and constructing roads, sewers, water and drainage facilities, and community amenities, such as parks, pools, and clubhouses. We use our staff and the services of independent engineers and consultants for land development activities. Land development work is performed primarily by independent contractors and local government authorities who construct sewer and water systems in some areas. At December 31, 2013,2015, we controlled 123,478138,079 lots, of which 95,21295,919 were owned and 28,26642,160 were under land option agreements.

Sales and marketing

We are dedicated to improving the quality and value of our homes through innovative architectural and community designs. Analyzing various qualitative and quantitative data obtained through extensive market research, we stratify our potential customers into well-defined buyer groups. Such stratification provides a method for understanding the business opportunities and risks across the full spectrum of consumer groups in each market. Once the demands of potential buyers are understood, we link our home design and community development efforts to the specific lifestyle of each targeted consumer group. Through our portfolioevaluation of brands, each serving unique consumer groups, we are able to provide a distinct experience to potential customers:

|

| | | |

| | Centex | Pulte Homes | Del Webb |

| Targeted consumer group | Entry-level buyers | Move-up buyers | Active adults |

| Portion of 2013 home closings | 25% | 46% | 29% |

|

| | | |

| | First-Time | Move-Up | Active Adult |

| Portion of home closings: | | | |

| 2015 | 32% | 37% | 31% |

| 2011 | 40% | 29% | 31% |

The move-upOur homes targeted to first-time buyers in our Pulte Homes communitiestend to be smaller with product offerings geared toward lower average selling prices or higher density. Move-up buyers tend to place more of a premium on location and amenities. These communities typically offer larger homes at higher price points. Our Centex brand is targeted to entry-level buyers, and these homes tend to be smaller with product offerings geared toward lower average selling prices. Through our Del Webb brand, we are better able to address the needs of active adults. Our Del Webb brand offersadults, to whom we offer both destination communities and “in place” communities, for those buyers who prefer to remain in their current geographic area. TheseMany of these communities are highly amenitized, communities offeroffering a variety of features, including golf courses, recreational centers, and educational classes, to the age fifty-five and over buyer to maintain an active lifestyle. In order to make the cost of these highly amenitized communities affordable to the individual homeowner, Del Webb communities tend to be larger than entry-levelfirst-time or move-up buyer communities. As illustrated in the above table, our sales mix has shifted toward the move-up buyer in recent years. This has occurred primarily due to financial challenges facing the first-time buyer, including a recovering U.S. economy, the overhang of consumer debt, especially student loans related to higher education, and a more restrictive mortgage lending environment.

We market our homes to prospective buyers through media advertising, illustrated brochures, Internetinternet listings and link placements, mobile applications, and other advertising displays. We have made significant enhancements in our tools and business practices to adapt our selling efforts to today's mobile customers. In addition, our websites, www.pulte.com,

www.delwebb.com, and www.centex.com, provide tools to help users find a home that meets their needs, investigate financing alternatives, communicate moving plans, maintain a home, learn more about us, and communicate directly with us. There were approximately 9.29.6 million unique visits to our websites during 20132015, compared with approximately 8.010.4 million in 2012.2014.

To meet the demands of our various customers, we have established design expertise for a wide array of product lines. We believe that we are an innovator in consumer-inspired home design, and we view our design capabilities as an integral aspect of our marketing strategy. Our in-house architectural services teams and management, supplemented by outside consultants, createfollow a 12-step product development process to introduce new features and technologies based on customer-validated data. Following this disciplined process results in distinctive design features, both in exterior facades and interior options and features. We typically offer a variety of potential options and upgrades, such as different flooring, countertop, and appliance choices, and design our base house and option packages to meet the needs of our customers as defined through rigorous market research. Energy efficiency represents an important source of value for new homes compared with existing homes and represents a key area of focus for our home designs, including high efficiency HVAC systems and insulation, low-emissivity windows, solar power in certain geographies, and other energy-efficient features.

Typically, our sales teams, in some cases together with outside sales brokers, are responsible for guiding the customer through the sales process. We are committed to industry-leading customer service through a variety of quality initiatives, including our customer care program, which ensures that homeowners are comfortable at every stage of the building process. Fully furnished and landscaped model homes physically located in our communities are generally used to showcase our homes and their distinctive design features.

Construction

The construction of our homes is conducted under the supervision of our on-site construction field managers. Substantially all of our construction work is performed by independent subcontractors under contracts that, in many instances, cover both labor and materials on a fixed-price basis. Using a selective process, we have teamed up with what we believe are premier subcontractors and suppliers to deliver all aspects of the house construction process.

Continuous improvement in our house construction process is a key area of focus. We seek to maintain efficient construction operations by using standard materials and components from a variety of sources and by utilizing standard construction practices. Beginning in 2011, we implemented an intensive effort to improveWe are improving our product offerings and production processes through the following programs:

A 12-step product development process to introduce new features and technologies based on customer-validated data;

Common management of house plans in order to focus on building those house designs that customers value the most and that can be built at the highest quality and at an efficient cost;

Value engineering our house plans to optimize house designs in terms of material content and ease of construction while still providing a clear value to the customer (value engineering eliminates items that add cost but that have little to no value to the customer);

Improving our usage of Pulte Construction Standards, a proprietary system of internally required construction practices, through development of new or revised standards, training of our field leadership and construction personnel, communication with our suppliers, and auditing our compliance; and

Working with our suppliers to establish the "should cost", a data driven, collaborative effort to reduce construction costs to what the associated construction activities or materials “should cost” in the market.

The availability of labor and materials at reasonable prices is becominghas become an increasingincreased concern for certain trades and building materials in some markets as the supply chain respondsadjusts to uneven industry growth. Additionally, the cost of certain building materials, especially lumber, steel, concrete, copper, and petroleum-based materials, is influenced by changes in global commodity prices. To minimize the effects of changes in construction costs, the contracting and purchasing of building supplies and materials generally is negotiated at or near the time when related sales contracts are signed with customers. In addition, we leverage our size by actively negotiating for certain materials on a national or regional basis to minimize production component cost. We are also working to establish a more integrated system that can effectively link suppliers, contractors, and the production schedule. However, we cannot determine the extent to which necessary building materials and labor will be available at reasonable prices in the future.

Competition

The housing industry in the U.S. is fragmented and highly competitive. While we are one of the largest homebuilders in the U.S., our national market share represented only approximately 4%3% of U.S. new home sales in 20132015. In each of our local markets, there are numerous national, regional, and local homebuilders with whom we compete. Additionally, new home sales have traditionally represented less than 15% of overall U.S. home sales (new and existing homes). Therefore, we also compete with sales of existing house inventory and any provider of housing units, for sale or to rent,rental housing units, including apartment operators, may be considered a competitor. Conversion of apartments to condominiums further provides an alternative to traditional housing, as does manufactured housing.operators. We compete primarily on the basis of location, price, quality, reputation, design, community amenities, and our customers' overall sales and homeownership experiences.

Seasonality

OurAlthough significant changes in market conditions have impacted our seasonal patterns in the past and could do so again, we historically experience variability in our quarterly results from operations due to the seasonal nature of the homebuilding operating cycle historically reflected increasedindustry. We generally experience increases in revenues profitability, and cash flow from operations during the fourth quarter based on the timing of home closings. WhileThis seasonal activity increases our working capital requirements in our third and fourth quarters to support our home production and loan origination volumes. As a result of the challenging market conditions experienced in recent years lessened the seasonal variationsseasonality of our operations, our quarterly results we have experienced a return to a more traditional demand pattern as new orders were higher in the first halfof operations are not necessarily indicative of the year and home closings increased in each quarter throughoutresults that may be expected for the full year. If and when the homebuilding industry more fully recovers from the recent downturn, we believe these traditional seasonal patterns will continue.

Regulation and environmental matters

Our operations are subject to extensive regulations imposed and enforced by various federal, state, and local governing authorities. These regulations are complex and include building codes, land zoning and other entitlement restrictions, health and safety regulations, labor practices, marketing and sales practices, environmental regulations, rules and regulations relating to mortgage financing and title operations, and various other laws, rules, and regulations. Collectively, these regulations have a significant impact on the site selection and development of our communities, our house design and construction techniques, our relationships with customers, employees, and suppliers / subcontractors, and many other aspects of our business. The applicable governing authorities frequently have broad discretion in administering these regulations, including inspections of our homes prior to closing with the customer in the majority of municipalities in which we operate.

Financial Services Operations

We conduct our financial services business, which includes mortgage and title operations, through Pulte Mortgage and other subsidiaries. Pulte Mortgage arranges financing through the origination of mortgage loans primarily for the benefit of our homebuyers. We are a lender approved by the FHA and VA and are a seller/servicer approved by Government National Mortgage Association ("Ginnie Mae"), Federal National Mortgage Association ("Fannie Mae"), Federal Home Loan Mortgage Corporation ("Freddie Mac"), and other investors. In our conventional mortgage lending activities, we follow underwriting guidelines established by Fannie Mae, Freddie Mac, and private investors. We believe that our customers’ use of our in-house mortgage and title operations provides us with a competitive advantage by enabling more control over the quality of the overall home buying process for our customers while also helping us align the timing of the house construction process with our customers’ financing needs.

Operating as a captive business model primarily targeted to supporting our Homebuilding operations, the business levels of our Financial Services operations are highly correlated to Homebuilding. During 2013, 2012,2015, 2014, and 2011,2013, we originated mortgage loans for 64%65%, 67%61%, and 61%64%, respectively, of the homes we sold. Such originations represented substantially all of our total originations in each of those years. Our capture rate, which we define as loan originations from our homebuilding business as a percentage of total loan opportunities from our homebuilding business excluding cash settlements, was 82.9% in 2015, 80.2% in 2014, 80.2% in 2013, 81.9% in 2012,, and 78.5% in 2011.2011.

In originating mortgage loans, we initially use our own funds, including funds available pursuant to credit agreements with third parties, and subsequently sell such mortgage loans to third party investors in the secondary market. Substantially all of the loans we originate are sold in the secondary market within a short period of time after origination, generally within 30 days. We also sell the servicing rights for the loans we originate through fixed price servicing sales contracts to reduce the risks and costs inherent in servicing loans. This strategy results in owning the loans and related servicing rights for only a short period of time.

The mortgage industry in the U.S. is highly competitive. We compete with other mortgage companies and financial institutions to provide attractive mortgage financing to our homebuyers. We utilize a centralized fulfillment center staffed with loan consultants to performfor our mortgage operations that performs underwriting, processing, and closing functions. We believe centralizing both the fulfillment and origination of our loans improves the speed, efficiency, and quality of our mortgage operations, improving our profitability and allowing us to focus on providing attractive mortgage financing opportunities for our customers.

In originating and servicing mortgage loans, we are subject to the rules and regulations of the government-sponsored investors and other investors that purchase the loans we originate, as well as to those of other government agencies that have oversight of the government-sponsored investors or consumer lending rules in the U.S. In addition to being affected by changes in these programs, our mortgage banking business is also affected by many of the same factors that impact our homebuilding business.

Our mortgage operations may be responsible for losses associated with mortgage loans originated and sold to investors in the event of errors or omissions relating to representations and warranties made by us that the loans met certain requirements, including representations as to underwriting standards, the existence of primary mortgage insurance, and the validity of certain borrower representations in connection with the loan. If a loan is determined to be faulty, we either repurchase the loan from the investors or reimburse the investors' losses (a "make-whole" payment). Historically, our overall losses related to this risk were not significant. Beginning in 2009, however, we experienced a significant increase in losses as a result of the high level of loan defaults and related losses in the mortgage industry and increasing aggressiveness by investors in presenting such claims to us. To date, the significant majority of these losses relates to loans originated in 2006 and 2007, during which period inherently riskier loan products became more common in the mortgage origination market. Given the volatility in the mortgage industry and the uncertainty regarding the ultimate resolution of these claims, actual costs could differ from our current estimates.

Our subsidiary title insurance companies serve as title insurance agents and underwriters in select markets by providing title insurance policies and examination and closing services to buyers of homes we sell. Historically, we have not experienced significant claims related to our title operations.

Financial Information About Geographic Areas

Substantially all of our operations are located within the U.S. However, weWe have some non-operating foreign subsidiaries and affiliates, which are insignificant to our consolidated financial results.

Organization/Employees

All subsidiaries and operating units operate independently with respect to daily operations. Homebuilding real estate purchases and other significant homebuilding, mortgage banking, financing activities, and similar operating decisions must be approved by the business unit’s management and/or corporate senior management.

At December 31, 20132015, we employed 3,8434,542 people, of which 709749 people were employed in our Financial Services operations. Except for a small group of employees in our St. Louis homebuilding division, our employees are not represented by any union. Contracted work, however, may be performed by union contractors. Our local and corporate management personnel are paid incentive compensation based on a combination of individual performance and the performance of the applicable business unit or the Company. Each business unit is given a level of autonomy regarding employment of personnel, althoughsubject to adherence to our established policies and procedures, and our senior corporate management acts in an advisory capacity in the employment of subsidiary officers. We consider our employee and contractor relations to be satisfactory.

ITEM 1A. RISK FACTORS

Discussion of our business and operations included in this annual report on Form 10-K should be read together with the risk factors set forth below. They describe various risks and uncertainties to which we are, or may become, subject. These risks and uncertainties, together with other factors described elsewhere in this report, have the potential to affect our business, financial condition, results of operations, cash flows, strategies, or prospects in a material and adverse manner.

Downward changes in general economic, real estate construction, or other business conditions could adversely affect our business or our financial results.

The residential homebuilding industry is sensitive to changes in economic conditions and other factors, such as the level of employment, consumer confidence, consumer income, availability of financing, and interest rate levels. Adverse changes in any of these conditions generally, or in the markets where we operate, could decrease demand and pricing for new homes in these areas or result in customer cancellations of pending contracts, which could adversely affect the number of home deliveries we make or reduce the prices we can charge for homes, either of which could result in a decrease in our revenues and earnings and would adversely affect our financial condition.

The homebuilding industry experienced a significant downturn in recent years.from 2006 through 2011. Although industry conditions improved duringbeginning in 2012, and 2013, the overall U.S. economy, while improving, remains challenged and consumer demand in the industry remains volatile. A deterioration in industry conditions could adversely affect our business and results of operations.

Beginning in 2006 and continuing through 2011, the U.S. housing market was unfavorably impacted by severe weakness in new home sales attributable to, among other factors, weak consumer confidence, tightened mortgage standards, significant foreclosure activity, a more challenging appraisal environment, higher than normal unemployment levels, and significant uncertainty in the global economy. These conditions contributed to sharply weakened demand for new homes and heightened pricing pressures on new and existing home sales. As a result of these factors, we experienced significant decreases in our revenues and profitability during the period 2007 - 2011. We also incurred substantial impairments of our land inventory and certain other assets during this period. During 2012 and 2013,Since 2011, overall industry new home sales have increased, and we returned to profitability. However, the overall demand for new homes remains below historical levels. Accordingly, we can provide no assurances that the adjustments we have made in our operating strategy will be successful.

If the market value of our land and homes drops significantly, our profits could decrease.

The market value of land, building lots, and housing inventories can fluctuate significantly as a result of changing market conditions, and the measures we employ to manage inventory risk may not be adequate to insulate our operations from a severe drop in inventory values. We acquire land for expansion into new markets and for replacement of land inventory and expansion within our current markets. If housing demand decreases below what we anticipated when we acquired our inventory, we may not be able to make profits similar to what we have made in the past, we may experience less than anticipated profits, and/or we may not be able to recover our costs when we sell and build homes. When market conditions are such that land values are not appreciating, option arrangements previously entered into may become less desirable, at which time we may elect to forego deposits and pre-acquisition costs and terminate the agreement. In the face of adverse market conditions, we may have substantial inventory carrying costs, we may have to write down our inventory to its fair value, and/or we may have to sell land or homes at a loss.

Supply shortages and other risks related to the demand for skilled labor and building materials could increase costs and delay deliveries.

The homebuilding industry is highly competitive for skilled labor and materials. Labor shortages in certain of our markets have become more acute in recent quarters as the supply chain adjusts to uneven industry growth. Additionally, the cost of certain building materials, especially lumber, steel, concrete, copper, and petroleum-based materials, is influenced by changes in local and global commodity prices. Increased costs or shortages of skilled labor and/or materials could cause increases in construction costs and / or construction delays. We may not be able to pass on increases in construction costs to customers and generally are unable to pass on any such increases to customers who have already entered into sales contracts as those sales contracts generally fix the price of the home at the time the contract is signed, which may be well in advance of the construction of the home. Sustained increases in construction costs may, over time, erode our margins, and pricing competition may restrict our ability to pass on any such additional costs, thereby decreasing our margins.

Our success depends on our ability to acquire land suitable for residential homebuilding at reasonable prices, in accordance with our land investment criteria.

The homebuilding industry is highly competitive for suitable land. The availability of finished and partially finished developed lots and undeveloped land for purchase that meet our internal criteria depends on a number of factors outside our control, including land availability in general, competition with other homebuilders and land buyers for desirable property, inflation in land prices, zoning, allowable housing density, and other regulatory requirements. Should suitable lots or land become less available, the number of homes we may be able to build and sell could be reduced, and the cost of land could be increased, perhaps substantially, which could adversely impact our results of operations.

Our long-term ability to build homes depends on our acquiring land suitable for residential building at reasonable prices in locations where we want to build. In the past, we experienced significant competition for suitable land as a result of land constraints in many of our markets. As competition for suitable land increases, and as available land is developed, the cost of acquiring suitable remaining land could rise, and the availability of suitable land at acceptable prices may decline. Any land shortages or any decrease in the supply of suitable land at reasonable prices could limit our ability to develop new communities or result in increased land costs. We may not be able to pass through to our customers any increased land costs, which could adversely impact our revenues, earnings, and margins.

We are subject to claims related to mortgage loans we sold in the secondary mortgage market that may be significant.

Our mortgage operations may be responsible for losses associated with mortgage loans originated and sold to investors in the event of errors or omissions relating to certain representations and warranties made by us that the loans met certain requirements, including representations as to underwriting standards, the type of collateral, the existence of primary mortgage insurance, and the validity of certain borrower representations in connection with the loan. To date, the significant majority of these losses relate to loans originated in 2006 and 2007, during which period inherently riskier loan products became more common in the origination market. We may also be required to indemnify underwriters that purchased and securitized loans originated by a former subsidiary of Centex for losses incurred by investors in those securitized loans based on similar breaches of representations and warranties.

To date, the significant majority of these losses relate to loans originated in 2006 and 2007, during which period inherently riskier loan products became more common in the origination market. In 2006 and 2007, we originated $39.5 billion of loans, excluding loans originated by Centex's former subprime loan business sold by Centex in 2006.

In addition, we entered into an agreement in conjunction with the wind down of Centex’s mortgage operations, which ceased loan origination activities in December 2009, that provides a guaranty for one major investor of loans originated by Centex. This guaranty provides that we will honor the potential repurchase obligations of Centex’s mortgage operations related to breaches of similar representations in the origination of a certain pool of loans.

The resolution of claims related to alleged breaches of these representations and warranties and repurchase claims could have a material adverse effect on our financial condition, cash flows and results of operations, and could exceed existing estimates and accruals. The repurchase liability we have recorded is estimated based on several factors, includingoperations. Given the level of current unresolved repurchase requests, the volume of estimated probable future repurchase requests, our ability to cure the defects identifiedongoing volatility in the repurchase requests, and the severitymortgage industry, changes in values of the estimated loss upon repurchase. The factors referred to above are subject to change in light of market developments, the economic environment,underlying collateral over time, and other circumstances, someuncertainties regarding the ultimate resolution of which are beyondthese claims, actual costs could differ from our control.current estimates. Accordingly, there can be no assurance that such reserves will not need to be increased in the future.

Future increases in interest rates, reductions in mortgage availability, or other increases in the effective costs of owning a home could prevent potential customers from buying our homes and adversely affect our business and financial results.

A large majority of our customers finance their home purchases through mortgage loans, many through our mortgage bank. Interest rates have been near historical lows for several years, which has made new homes more affordable. Increases in interest rates or decreases in the availability of mortgage financing however, could adversely affect the market for new homes. Potential homebuyers may be less willing or able to pay the increased monthly costs or to obtain mortgage financing. Lenders may increase the qualifications needed for mortgages or adjust their terms to address any increased credit risk. Even if potential customers do not need financing, changes in interest rates and mortgage availability could make it harder for them to sell their current homes to potential buyers who need financing. These factors could adversely affect the sales or pricing of our homes and could also reduce the volume or margins in our financial services business. Our financial services business could also be impacted to the extent we are unable to match interest rates and amounts on loans we have committed to originate through the various hedging strategies we employ. These developments have had, and may continue to have, a material adverse effect on the overall demand for new housing and thereby on the results of operations for our homebuilding business.

We also believe that the availability of FHA and VA mortgage financing is an important factor in marketing some of our homes. The FHA has and may continue to impose stricter loan qualification standards, raise minimum down payment requirements, impose higher mortgage insurance premiums and other costs, and/or limit the number of mortgages it insures. The liquidity provided by Fannie Mae and Freddie Mac to the mortgage industry is also critical to the housing market. The impact of the federal government’s conservatorship of Fannie Mae and Freddie Mac on the short-term and long-term demand for new housing remains unclear. Any limitations or restrictions on the availability of financing by these agencies could adversely affect interest rates, mortgage financing, and our sales of new homes and mortgage loans.

Significant costs of homeownership include mortgageMortgage interest expense and real estate taxes represent significant costs of homeownership, both of which are generally deductible for an individual’s federal and, in some cases, state income taxes. Any changes to income tax laws by the

federal government or a state government to eliminate or substantially reduce these income tax deductions, as has been considered from time to time, would increase the after-tax cost of owning a home. Increases in real estate taxes by local governmental authorities also increase the cost of homeownership. Any such increases to the cost of homeownership could adversely impact the demand for and sales prices of new homes.

Adverse capital and credit market conditions may significantly affect our access to capital and cost of capital.

The capital and credit markets have experiencedcan experience significant volatility in recent years. In many cases, the markets have exerted downward pressure on the availability of liquidity and credit capacity for issuers.volatility. We may need credit-related liquidity for the future growth and development of our business. Without sufficient liquidity, we may not be able to purchase additional land or develop land, which could adversely affect our financial results. At December 31, 2013,2015, we had cash and equivalents of $1.6 billion as well as$754.2 million, restricted cash totaling $72.7$21.3 million,. and $308.7 million available under our revolving credit facility, net of outstanding letters of credit. However, our internal sources of liquidity may prove to be insufficient, and in such case, we may not be able to successfully obtain additional financing on terms acceptable to us, or at all.

Another source of liquidity includes our ability to use letters of credit and surety bonds pursuant to certain performance-related obligations and as security for certain land option agreements and under various insurance programs. The majority of these letters of credit and surety bonds are in support of our land development and construction obligations to various municipalities, other government agencies, and utility companies related to the construction of roads, sewers, and other infrastructure. At December 31, 20132015, we had outstanding letters of credit and surety bonds totaling $183.1$191.3 million and $958.3 million,$1.0 billion, respectively. Of these amounts outstanding, $58.7 million of theThese letters of credit were subject to cash-collateralized agreements while the remaining letters ofare issued via our unsecured revolving credit facility, which contains certain financial covenants and surety bonds were unsecured.other limitations. If we are unable to obtain letters of credit or surety bonds when required, or the conditions imposed by issuers increase significantly, our financial condition and results of operations could be adversely affected.

Competition for homebuyers could reduce our deliveries or decrease our profitability.

The U.S. housing industry in the U.S. is highly competitive. We compete primarily on the basis of location, price, quality, reputation, design, community amenities, and our customers' overall sales and homeownership experiences. We compete in each of our markets with numerous national, regional, and local homebuilders. This competition with other homebuilders could reduce the number of homes we deliver or cause us to accept reduced margins in order to maintain sales volume.

We also compete with resales of existing or foreclosed homes, housing speculators, and available rental housing. Increased competitive conditions in the residential resale or rental market in the regions where we operate could decrease demand for new homes or unfavorably impact pricing for new homes.

Supply shortages and other risks related to the demand for skilled labor and building materials could increase costs and delay deliveries.

The homebuilding industry is highly competitive for skilled labor and materials. Additionally, the cost of certain building materials, especially lumber, steel, concrete, copper, and petroleum-based materials, is influenced by changes in global commodity prices. Increased costs or shortages of skilled labor and/or materials could cause increases in construction costs and construction delays. We may not be able to pass on increases in construction costs to customers and generally are unable to pass on any such increases to customers who have already entered into sales contracts as those sales contracts generally fix the price of the home at the time the contract is signed, which may be well in advance of the construction of the home. Sustained increases in construction costs may, over time, erode our margins, and pricing competition may restrict our ability to pass on any such additional costs, thereby decreasing our margins.

Our income tax provision and tax reserves may be insufficient if a taxing authority is successful in asserting positions that are contrary to our interpretations and related reserves, if any.

Significant judgment is required in determining our provision for income taxes and our reserves for federal, state, and local taxes. In the ordinary course of business, there may be matters for which the ultimate outcome is uncertain. Our evaluation of our tax matters is based on a number of factors, including changes in facts or circumstances, changes in tax law, correspondence with tax authorities during the course of audits, and effective settlement of audit issues. Although we believe our approach to determining the tax treatment for such items is appropriate, no assurance can be given that the final tax authority review will not be materially different than that which is reflected in our income tax provision and related tax reserves. Such differences could have a material adverse effect on our income tax provision in the period in which such determination is made and, consequently, on our financial position, cash flows, or net income for such period.

We are periodically audited by various federal, state, and local authorities regarding tax matters. Our current audits are in various stages of completion; however, no outcome for a particular audit can be determined with certainty prior to the conclusion of the audit, appeal, and, in some cases, litigation process. As each audit is concluded, adjustments, if any, are recorded in our financial statements in the period determined. To provide for potential tax exposures, we maintain tax reserves based on reasonable estimatesconsider a variety of potentialfactors, including changes in facts or circumstances, changes in law, correspondence with taxing authorities, and effective settlement of audit results.issues. If these reserves are insufficient upon completion of an audit, there could be an adverse impact on our financial position, cash flows, and results of operations.

We may not realize our deferred income tax assets.

As of December 31, 20132015, we had deferred income tax assets, net of deferred tax liabilities, of $2.2$1.5 billion, against which we provided a valuation allowance of $157.3 million.$109.1 million. The ultimate realization of our deferred income tax assets is dependent upon generating future taxable income and executing tax planning strategies. While we have recorded valuation allowances against certain of our deferred income tax assets, the valuation allowances are subject to change as facts and circumstances change.

Our ability to utilize net operating losses (“NOLs”), built-in losses (“BILs”), and tax credit carryforwards to offset our future taxable income would be limited if we were to undergo an “ownership change” within the meaning of Section 382 of the Internal Revenue Code (the “IRC”). In general, an “ownership change” occurs whenever the percentage of the stock of a corporation owned by “5-percent shareholders” (within the meaning of Section 382 of the IRC) increases by more than 50 percentage points over the lowest percentage of the stock of such corporation owned by such “5-percent shareholders” at any time over the testing period.

An ownership change under Section 382 of the IRC would establish an annual limitation to the amount of NOLs, BILs, and tax credit carryforwards we could utilize to offset our taxable income in any single year. The application of these limitations might prevent full utilization of the deferred tax assets attributable to our NOLs, BILs, and tax credit carryforwards. We have not experienced an ownership change as defined by Section 382. To preserve our ability to utilize NOLs, BILs, and other tax benefits in the future without a Section 382 limitation, we adopted a shareholder rights plan, which is triggered upon certain transfers of our securities, and amended our by-laws to prohibit certain transfers of our securities. Our shareholder rights plan expires June 1, 2016, unless our board of directors and shareholders approve an amendment to extend the term prior thereto. Notwithstanding the foregoing measures, there can be no assurance that we will not undergo an ownership change within the meaning of Section 382.

As a result of theour merger with Centex in August 2009, our ability to use certain of Centex’s pre-ownership change NOLs, BILs, and deductions is limited under Section 382 of the Internal Revenue Code. The applicable Section 382 limitation is approximately $67.4 million per year for NOLs, losses realized on built-in loss assets that are sold within 60 months of the ownership change (i.e. before August 2014), and certain deductions.IRC. We do not believe that the Section 382 limitation will prevent the Companyus from using Centex's pre-ownership change NOL carryforwards and built-in lossesfederal NOLs, BILs, or deductions.deductions, however, no assurance can be given that any such limitation will not occur, which could be material.

The value of our deferred tax assets is also dependent upon the tax rates expected to be in effect at the time taxable income is expected to be generated. A decrease in enacted corporate tax rates in our major jurisdictions, especially the U.S. federal corporate tax rate, would decrease the value of our deferred tax assets, which could be material.

We have significant intangible assets. If these assets become impaired, then our profits and shareholders’ equity may be reduced.

We have significant intangible assets related to prior business combinations. We evaluate the recoverability of intangible assets whenever facts and circumstances indicate the carrying amount may not be recoverable. If the carrying value of intangible assets is deemed impaired, the carrying value is written down to fair value. This would result in a charge to our operating earnings. If management’s expectations of future results and cash flows decrease significantly, impairments of the remaining intangible assets may occur.

Government regulations could increase the cost and limit the availability of our development and homebuilding projects or affect our related financial services operations and adversely affect our business or financial results.

Our operations are subject to building, environmental, and other regulations imposed and enforced by various federal, state, and local governing authorities. New housing developments may also be subject to various assessments for schools, parks, streets, and other public improvements. These can cause an increase in the effective cost of our homes.

We also are subject to a variety of local, state, and federal laws and regulations concerning protection of health, safety, and the environment. The impact of environmental laws varies depending upon the prior uses of the building site or adjoining properties and may be greater in areas with less supply where undeveloped land or desirable alternatives are less available. These matters may result in delays, may cause us to incur substantial compliance, remediation and other costs, and can prohibit or severely restrict development and homebuilding activity in environmentally sensitive regions or areas. More stringent requirements could be imposed in the future on homebuilders and developers, thereby increasing the cost of compliance.

Our financial services operations are also subject to numerous federal, state, and local laws and regulations. These include eligibility requirements for participation in federal loan programs and compliance with consumer lending and similar

requirements such as disclosure requirements, prohibitions against discrimination, and real estate settlement procedures. They also subject our operations to examination by applicable agencies, pursuant to which those agencies may limit our ability to provide mortgage financing or title services to potential purchasers of our homes. For our homes to qualify for FHA or VA mortgages, we must satisfy valuation standards and site, material, and construction requirements of those agencies.

In January 2013, the Consumer Financial Protection Bureau ("CFPB") adopted new rules regarding the origination of mortgages, including the criteria for “qualified mortgages”, rules for lender practices regarding assessing borrowers’ ability to repay, and limitations on certain fees and incentive arrangements. Such rules went into effect in January 2014. The CFPB also issued the TILA-RESPA Integrated Disclosure ("TRID") rules, which combined the mortgage disclosures consumers receive under the Truth in Lending Act ("TILA") and the Real Estate Settlement and Procedures Act ("RESPA"). Such rules went into effect in October 2015. While we have adjusted our operations to comply with the new rules, the impact such rules will have on our business remains unclear. Additionally, manycertain other rules required by the Dodd-Frank Act of 2010 have not yet been completed or implemented, which has created uncertainty in the overall U.S. financial services and mortgage industries as to their long-term impact.

Homebuilding is subject to warranty and other claims in the ordinary course of business that can be significant.

As a homebuilder, we are subject to home warranty, construction defect, and other claims arising in the ordinary course of business. We record warranty and other reserves for the homes we sell based on historical experience in our markets and our judgment of the qualitative risks associated with the types of homes built. We have, and require our subcontractors to have, general liability, property, errors and omissions, workers compensation, and other business insurance. These insurance policies protect us against a portion of our risk of loss from claims, subject to certain self-insured per occurrence and aggregate retentions, deductibles, and available policy limits. In certain instances, we may offer our subcontractors the opportunity to purchase insurance through one of our captive insurance subsidiaries or participate in a project-specific insurance program provided by us. Policies issued by our captive insurance subsidiaries represent self-insurance of these risks by us. We reserve for costs to cover our self-insured and deductible amounts under these policies and for any costs of claims and lawsuits based on an analysis of our historical claims, which includes an estimate of claims incurred but not yet reported. Because of the uncertainties inherent in these matters, we cannot provide assurance that our insurance coverage, our subcontractor arrangements, and our reserves will be adequate to address all our warranty and construction defect claims in the future. Contractual indemnities can be difficult to enforce, we may be responsible for applicable self-insured retentions, and some types of claims may not be covered by insurance or may exceed applicable coverage limits. Additionally, the coverage offered by and the availability of general liability insurance for construction defects are currently costly and limited. We have responded to increases in insurance costs and coverage limitations by increasing our self-insured retentions and claim reserves. There can be no assurance that coverage will not be further restricted andor become more costly. Additionally, we are exposed to counterparty default risk related to our subcontractors, and our insurance carriers, and our subcontractors’ insurance carriers.

Natural disasters and severe weather conditions could delay deliveries, increase costs, and decrease demand for new homes in affected areas.

Our homebuilding operations are located in many areas that are subject to natural disasters and severe weather. The occurrence of natural disasters or severe weather conditions can delay new home deliveries, increase costs by damaging inventories, reduce the availability of materials, and negatively impact the demand for new homes in affected areas. Furthermore, if our insurance does not fully cover business interruptions or losses resulting from these events, our earnings, liquidity, or capital resources could be adversely affected.

Inflation may result in increased costs that we may not be able to recoup.

Inflation can have a long-term impact on us because increasing costs of land, materials, and labor may require us to increase the sales prices of homes in order to maintain satisfactory margins. However, we may not be able to raise home prices sufficiently to keep up with the rate of inflation and our margins could decrease. In addition, inflation is often accompanied by higher interest rates, which could have a negative impact on housing demand.

Information technology failures or data security breaches could harm our business.

We use information technology and other computer resources to carry out important operational activities and to maintain our business records. Our computer systems, including our back-up systems, are subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, security breaches (through cyber-attackscyberattacks from computer hackers and sophisticated organizations), catastrophic events such as fires, tornadoes and hurricanes, and usage

errors by our associates. If our computer systems and our back-up systems are damaged, breached, or cease to function properly, we could suffer interruptions in our operations or unintentionally allow misappropriation of proprietary or confidential information (including information about our homebuyers and business partners), which could require us to incur significant costs to remediate or otherwise resolve these issues.

Future terrorist attacks against the U.S. or increased domestic and international instability could have an adverse effect on our operations.

A future terrorist attack against the U.S. could cause a sharp decrease in the number of new contracts signed for homes and an increase in the cancellation of existing contracts. Accordingly, adverse developments in the war on terrorism, future terrorist attacks against the U.S., or increased domestic and international instability could adversely affect our business.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our homebuilding and corporate headquarters are located in leased office facilities at 100 Bloomfield Hills Parkway, Bloomfield Hills, Michigan 48304.3350 Peachtree Road NE, Suite 150, Atlanta, GA 30326. Pulte Mortgage leases its primary office facilities in Englewood, Colorado. We also maintain various support functions in leased facilities near Phoenix,in Tempe, Arizona and Atlanta, Georgia.Bloomfield Hills, Michigan. Our homebuilding divisions and financial services branches lease office space in the geographic locations in which they conduct their day-to-day operations.

Because of the nature of our homebuilding operations, significant amounts of property are held as inventory in the ordinary course. Such properties are not included in response to this Item.

ITEM 3. LEGAL PROCEEDINGS

We are involved in various legal and governmental proceedings incidental to our continuing business operations, many involving claims related to certain construction defects. The consequences of these matters are not presently determinable but, in our opinion, after consulting with legal counsel and taking into account insurance and reserves, the ultimate liability is not expected to have a material adverse impact on our results of operations, financial position, or cash flows. However, to the extent the liability arising from the ultimate resolution of any matter exceeds our estimates reflected in the recorded reserves relating to such matter, we could incur additional charges that could be significant.

ITEM 4. MINE SAFETY DISCLOSURES

This Item is not applicable.

ITEM 4A. EXECUTIVE OFFICERS OF THE REGISTRANT

Set forth below is certain information with respect to our executive officers.

| | | Name | | Age | | Position | | Year Became An Executive Officer | | Age | | Position | | Year Became An Executive Officer |

| Richard J. Dugas, Jr. | | 48 | | Chairman, President and Chief Executive Officer | | 2002 | | 50 | | Chairman, President and Chief Executive Officer | | 2002 |

| Robert T. O'Shaughnessy | | 48 | | Executive Vice President and Chief Financial Officer | | 2011 | | 50 | | Executive Vice President and Chief Financial Officer | | 2011 |

| James R. Ellinghausen | | | 57 | | Executive Vice President, Human Resources | | 2005 |

| Harmon D. Smith | | 50 | | Executive Vice President - Homebuilding Operations and Area President, Texas | | 2011 | | 52 | | Executive Vice President, Field Operations | | 2011 |

| James R. Ellinghausen | | 55 | | Executive Vice President, Human Resources | | 2005 | |

| Ryan R. Marshall | | | 41 | | Executive Vice President, Homebuilding Operations | | 2012 |

| Steven M. Cook | | 55 | | Senior Vice President, General Counsel and Secretary | | 2006 | | 57 | | Executive Vice President, Chief Legal Officer and Corporate Secretary | | 2006 |

| Stephen P. Schlageter | | 43 | | Area President, Northeast | | 2012 | |

| Ryan R. Marshall | | 39 | | Area President, Southeast | | 2012 | |

| Patrick J. Beirne | | 50 | | Area President, Central | | 2011 | |

| John J. Chadwick | | 52 | | Area President, Southwest | | 2012 | |

| James L. Ossowski | | 45 | | Vice President, Finance and Controller | | 2013 | | 47 | | Vice President, Finance and Controller | | 2013 |

The following is a brief account of the business experience of each officer during the past five years:

Mr. Dugas was appointed Chairman in August 2009 and President and Chief Executive Officer in July 2003. Previously, he was appointed Chief Operating Officer in May 2002 and Executive Vice President in December 2002. Since joining our company in 1994, he has served in a variety of management positions.

Mr. O'Shaughnessy was appointed Executive Vice President and Chief Financial Officer in May 2011. Prior to joining our company, he held a number of financial roles at Penske Automotive Group from 1997 to 2011, most recently as Executive Vice President and Chief Financial Officer.

Mr. Ellinghausen was appointed Executive Vice President, Human Resources in December 2006.

Mr. Smith was appointed Executive Vice President, -Field Operations in May 2014 and previously held the position of Executive Vice President, Homebuilding Operations and Area President, Texas insince May 2012, and previously held the position of Area President, Gulf Coast since 2008.2012. He has served as an Area President over various geographical markets since 2006.

Mr. EllinghausenMarshall was appointed Executive Vice President, Human ResourcesHomebuilding Operations in December 2006.

Mr. Cook was appointed Senior Vice President, General Counsel and Secretary in December 2008 and previously held the position of Vice President, General Counsel and Secretary since February 2006.

Mr. Schlageter was appointed Area President, Northeast in November 2012 and previouslyMay 2014. Previously he held the positions of Vice President, Strategic Planning since October 2010 and Division President, Raleigh since November 2003.

Mr. Marshall was appointed Area President, Southeast insince November 2012, and previously held the positions of Area President, Florida since May 2012, and Division President, South Florida since 2006.

Mr. BeirneCook was appointed AreaExecutive Vice President, CentralChief Legal Officer and Corporate Secretary in 2012 and has served as an Area President over various geographical markets since 2006.

Mr. Chadwick was appointed Area President, Southwest in 2012September 2015 and previously served as Division President, Arizona. Since 2006, Mr. Chadwick has held the positionpositions of AreaSenior Vice President, or DivisionGeneral Counsel and Secretary since December 2008 and Vice President, over various geographical markets.General Counsel and Secretary since February 2006.

Mr. Ossowski was appointed Vice President, Finance and Controller in February 2013 and previously held the position of Vice President, Finance - Homebuilding Operations since August 2010. Since 2002, Mr. Ossowski has held various finance positions of increasing responsibility with the Company.our company.

There is no family relationship between any of the officers. Each officer serves at the pleasure of the Board of Directors.

PART II

| |

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common shares are listed on the New York Stock Exchange (Symbol: PHM).

Related Stockholder Matters

The table below sets forth, for the quarterly periods indicated, the range of high and low closingintraday sales prices for our common shares and dividend per share information:

| | | | December 31, 2013 | | December 31, 2012 | December 31, 2015 | | December 31, 2014 |

| | High | | Low | | Declared

Dividend | | High | | Low | | Declared

Dividend | High | | Low | | Declared

Dividend | | High | | Low | | Declared

Dividend |

| 1st Quarter | $ | 21.67 |

| | $ | 18.02 |

| | $ | — |

| | $ | 9.61 |

| | $ | 6.52 |

| | $ | — |

| $ | 23.24 |

| | $ | 20.56 |

| | $ | 0.08 |

| | $ | 21.65 |

| | $ | 18.21 |

| | $ | 0.05 |

|

| 2nd Quarter | 24.25 |

| | 17.54 |

| | — |

| | 10.70 |

| | 7.69 |

| | — |

| 22.78 |

| | 18.85 |

| | 0.08 |

| | 20.47 |

| | 18.01 |

| | 0.05 |

|

| 3rd Quarter | 20.39 |

| | 15.11 |

| | 0.10 |

| | 16.98 |

| | 10.02 |

| | — |

| 22.02 |

| | 18.72 |

| | 0.08 |

| | 20.64 |

| | 17.47 |

| | 0.05 |

|

| 4th Quarter | 20.37 |

| | 15.54 |

| | 0.05 |

| | 18.61 |

| | 15.24 |

| | — |

| 20.21 |

| | 17.18 |

| | 0.09 |

| | 22.03 |

| | 16.56 |

| | 0.08 |

|

At February 1, 20142016, there were 2,8682,617 shareholders of record.

Issuer Purchases of Equity Securities

|

| | | | | | | | | | | | | | |

| | (a) Total number of shares purchased (1) | | (b) Average price paid per share (1) | | (c) Total number of shares purchased as part of publicly announced plans or programs | | (d) Approximate dollar value of shares that may yet be purchased under the plans or programs ($000’s omitted) | |

| October 1, 2013 to October 31, 2013 | — |

| | $ | — |

| | — |

| | $ | 269,321 |

| (2) |

| November 1, 2013 to November 30, 2013 | 894,286 |

| | 16.77 |

| | 886,509 |

| | $ | 254,467 |

| (2) |

| December 1, 2013 to December 31, 2013 | 1,238,872 |

| | 18.34 |

| | 1,100,000 |

| | $ | 234,290 |

| (2) |

| Total | 2,133,158 |

| | $ | 17.68 |

| | 1,986,509 |

| | | |

|

| | | | | | | | | | | | | | |

| | (a) Total number of shares purchased | | (b) Average price paid per share | | (c) Total number of shares purchased as part of publicly announced plans or programs | | (d) Approximate dollar value of shares that may yet be purchased under the plans or programs ($000’s omitted) | |

| October 1, 2015 to October 31, 2015 | — |

| | $ | — |

| | — |

| | $ | 304,765 |

| (1) |

| November 1, 2015 to November 30, 2015 | — |

| | — |

| | — |

| | $ | 304,765 |

| (1) |

| December 1, 2015 to December 31, 2015 | — |

| | — |

| | — |

| | $ | 604,765 |

| (1) |

| Total | — |

| | $ | — |

| | — |

| | | |

| |

| (1) | During the fourth quarter of 2013, a total of 146,649 shares were surrendered by employees for payment of minimum tax obligations upon the vesting or exercise of previously granted stock-based compensation awards. Such shares were not repurchased as part of our publicly-announced stock repurchase programs. |

| |

(2) | Pursuant to the two $100 million share repurchase programs authorized and announced by ourThe Board of Directors in October 2002 and October 2005, the $200 million share repurchase authorized and announced in February 2006, and the $250 million share repurchase authorized and announced in July 2013 (for a total share repurchase authorization of $650 million), we have repurchased a total of 16,925,409 shares for a total of $415.8 million. We have fully utilized the authorizations provided by the 2002, 2005, and 2006approved share repurchase authorizations totaling $750.0 million and will no longer conduct share repurchases under these programs. The July 2013 share repurchase authorization has $234.3$300.0 million remainingin October 2014 and December 2015, respectively, of which $604.8 million remained available as of December 31, 2013.2015. There isare no expiration datedates for this program.these programs. During 2015, we repurchased 21.2 million shares under these programs. |

The information required by this item with respect to equity compensation plans is set forth under Item 12 of this annual report on Form 10-K and is incorporated herein by reference.

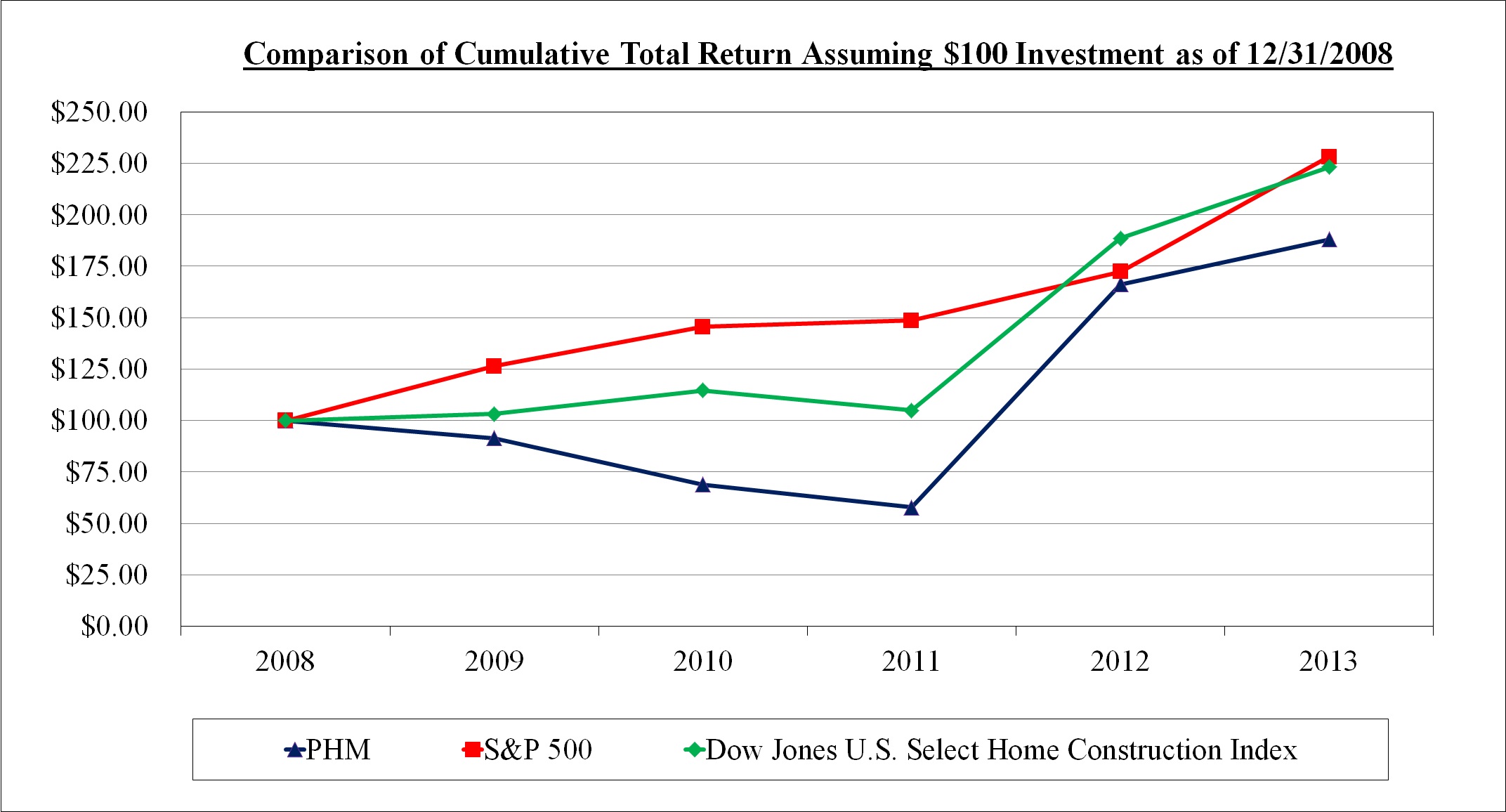

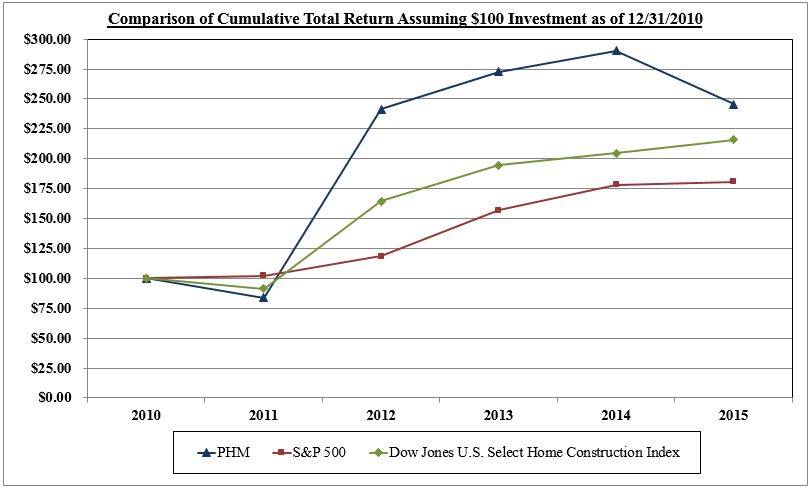

Performance Graph

The following line graph compares for the fiscal years ended December 31, 2009, 2010, 2011, 2012, 2013, 2014, and 20132015 (a) the yearly cumulative total shareholder return (i.e., the change in share price plus the cumulative amount of dividends, assuming dividend reinvestment, divided by the initial share price, expressed as a percentage) on PulteGroup’s common shares, with (b) the cumulative total return of the Standard & Poor’s 500 Stock Index, and with (c) the Dow Jones U.S. Select Home Construction Index. The Dow Jones U.S. Select Home Construction Index is a widely-recognized index comprised primarily of large national homebuilders. We believe comparison of our shareholder return to this index represents a meaningful analysis for investors.

COMPARISON OF FIVE YEAR CUMULATIVE TOTAL RETURN*

AMONG PULTEGROUP, INC., S&P 500 INDEX, AND PEER INDEX

Fiscal Year Ended December 31, 20132015

| | | | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 | | 2013 | | 2010 | | 2011 | | 2012 | | 2013 | | 2014 | | 2015 |

| PULTEGROUP, INC. | | 100.00 |

| | 91.49 |

| | 68.80 |

| | 57.73 |

| | 166.15 |

| | 187.99 |

| | 100.00 |

| | 83.91 |

| | 241.49 |

| | 272.87 |

| | 290.55 |

| | 245.74 |

|

| S&P 500 Index - Total Return | | 100.00 |

| | 126.47 |

| | 145.52 |

| | 148.59 |

| | 172.37 |

| | 228.17 |

| | 100.00 |

| | 102.11 |

| | 118.45 |

| | 156.82 |

| | 178.28 |

| | 180.75 |

|

Dow Jones U.S. Select Home Construction Index | | 100.00 |

| | 103.13 |

| | 114.65 |

| | 104.90 |