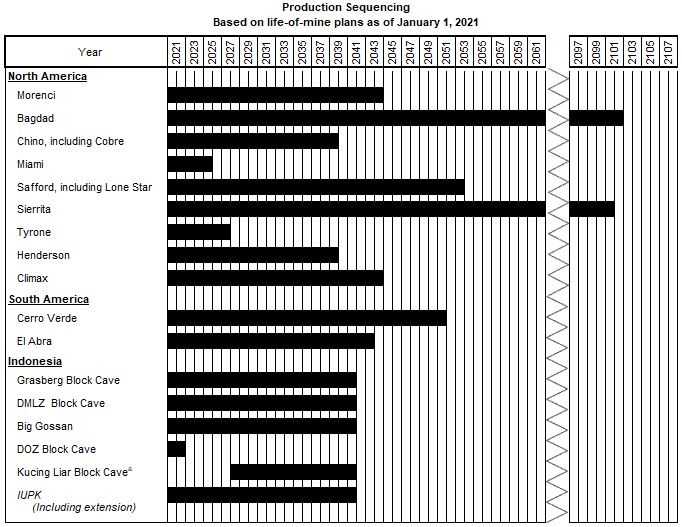

The following chart illustrates our current plans for sequencing and producing our proven and probable reserves at each of our ore bodies and the years in which we currently expect production from each ore body and related stockpiles. Our proven and probable ore reserves in Indonesia reflect estimates of minerals that can be recovered through the end of 2041, and our current mine plan and planned operations are based on the assumption that PT-FI will comply with its obligations under the IUPK and receive the second 10-year extension from 2031 through 2041 (refer to Item 1A. “Risk Factors” and Note 13 for further discussion). Production volumes are typically lower in the first few years for each ore body as development activities are ongoing and as the mine ramps up to full production and production volumes may also be lower as the mine reaches the end of its life. The sequencing dates shown in the chart below include development activity that results in metal production. The ultimate timing of the start of production from our undeveloped mines is dependent upon a number of factors, including the results of our exploration and development efforts, and may vary from the dates shown below. In addition, we develop our mine plans based on maximizing the net present value from the ore bodies. Significant additional capital expenditures will be required at many of these mines in order to achieve the life-of-mine plans reflected below.

Mill and leach stockpiles generally contain lower grade ores that have been extracted from an ore body and are available for metal recovery. Mill stockpiles contain sulfide ores and recovery of metal is through milling, concentrating, smelting and refining or, alternatively, by concentrate leaching. Leach stockpiles contain oxide ores and certain secondary sulfide ores and recovery of metal is through exposure to acidic solutions that dissolve contained copper and deliver it in solution to extraction processing facilities.

Because it is impracticable to determine copper contained in mill and leach stockpiles by physical count, reasonable estimation methods are employed. The quantity of material delivered to mill and leach stockpiles is based on surveyed volumes of mined material and daily production records. Sampling and assaying of blasthole cuttings determine the estimated copper grades of material delivered to mill and leach stockpiles.

Expected copper recovery rates for mill stockpiles are determined by metallurgical testing. The recoverable copper in mill stockpiles, once entered into the production process, can be produced into copper concentrate almost immediately.

Expected copper recovery rates for leach stockpiles are determined using small-scale laboratory tests, small- to large-scale column testing (which simulates the production process), historical trends and other factors, including mineralogy of the ore and rock type. Total copper recovery in leach stockpiles can vary significantly from a low percentage to more than 90 percent depending on several variables, including processing methodology, processing variables, mineralogy and particle size of the rock. For newly placed material on active stockpiles, as much as 80 percent of total copper recovery may be extracted during the first year, and the remaining copper may be recovered over many years. Processes and recovery rates are monitored regularly, and recovery rate estimates are adjusted periodically as additional information becomes available and as related technology changes.

Exploration and Development Activities

Capital expenditures associated with oil and gas properties totaled $2 million in 2018, and we have no plans to incur significant capital expenditures associated with oil and gas properties in future periods. Capital expenditures for our oil and gas operations totaled $34 million in 2017 and $1.2 billion in 2016 (including $0.6 billion incurred for Gulf of Mexico and $0.5 billion for changes in capital expenditure accruals).

Production and Sales Data

Oil and gas sales totaled 3.1 MMBOE in 2018 and 4.6 MMBOE in 2017. Oil and gas production and sales for the year 2016 totaled 47.1 MMBOE, including 34.4 million barrels (MMBbls) of oil, 65.1 billion cubic feet of natural gas and 1.8 MMBbls of natural gas liquids.

Productive Wells

At December 31, 2018 and 2017, the total number of active producing oil and gas wells was not significant. At December 31, 2016, we had working interests in 120 gross (94 net) active producing oil wells and 640 gross (100 net) active producing natural gas wells.

Drilling Activities

As of and for the years ended December 31, 2018 and 2017, there were no exploratory or development wells drilled or in progress. During the year ended December 31, 2016, we drilled 3 gross (2 net) exploratory productive wells and 9 gross (5 net) development productive wells.

Item 1A. Risk Factors.

This report contains “forward-looking statements” within the meaning of United States (U.S.) federal securities laws. Forward-looking statements are all statements other than statements of historical facts, such as plans, projections or expectations relating to ore grades and milling rates; business outlook; production and sales volumes; unit net cash costs; cash flows, capital expenditures, liquidity; operating cash flows; capital expenditures;costs; operating plans; our financial policy; our expectations regarding our share of PT Freeport Indonesia’s (PT-FI) ramp-up of underground mining activities and future cash flows through 2022; PT-FI’s development, financing, construction and completion of a new smelter in Indonesia;Indonesia and possible expansion of the smelter at PT Smelting; our commitments to deliver responsibly produced copper, including plans to implement and validate all of our operating sites under specific frameworks; improvements in operating procedures and technology; exploration efforts and results; development and production activities, rates and costs; liquidity; tax rates; supply ofexport quotas and demand for, andduties; the impact of copper, gold and molybdenum price changes; the impact of deferred intercompany profits on earnings; mineralization and reserve estimates; execution of the settlement agreements associated with the Louisiana coastal erosion cases and talc-related litigation; descriptions of our objectives, strategies, plans, goals or targets, including our net debt target, anticipated improvements in energy efficiency at certain operating sites, and environmental, social and governance (ESG) targets; and future dividend payments; andpayments, share purchases and sales.sales, including under our Board of Director’s (Board’s) financial policy.

We undertake no obligation to update any forward-looking statements. We caution readers that forward-looking statements are not guarantees of future performance and our actual results may differ materially from those anticipated, expected, projected or assumed in the forward-looking statements. Important factors that can cause our actual results to differ materially from those anticipated in the forward-looking statements include the following:

Risk Factor Summary

Investing in our securities involves a high degree of risk and uncertainties. Below is a summary of the material risk factors associated with an investment in our securities. You should read this summary together with the more detailed description of each risk factor that immediately follows this summary.

However, the risk factors described herein are not all of the risks we may face. Other risks not presently known to us or that we currently believe are immaterial may materially affect our business if they occur. Moreover, new risks emerge from time to time. Further, our business may also be affected by additional factors that apply to all companies operating in the U.S. and globally, which have not been included.

In addition to this summary and the more detailed description of the risk factors, you should carefully consider other sections of this annual report on Form 10-K, which may include additional factors that could adversely affect our business, prior to investing in our securities.

Financial risks

•Fluctuations in the market prices of the commodities we produce have caused and may continue to cause significant volatility in our financial performance and in the trading prices of our common stock and debt. Extended declines in the market prices of the commodities we produce could have an adverse effect on our business.

•Our debt and other financial commitments may limit our financial and operating flexibility.

•The ongoing COVID-19 pandemic and any future pandemic, epidemic, endemic or similar public health threats and resulting negative impact on the global economy and financial markets may have an adverse impact on our business and results of operations, the duration and extent of which is highly uncertain and could be material.

•Changes in or the failure to comply with the financial assurance requirements relating to our mine closure reclamation and plugging and abandonment obligations could have a material adverse effect on our business.

•Unanticipated litigation or negative developments in pending litigation or with respect to other contingencies could have a material adverse effect on our business.

•We may be adversely impacted by increased liabilities and costs related to our defined benefit pension plans.

International risks

•Our international operations are subject to, and may be adversely affected by, political, economic, social and regional risks of doing business in countries outside the U.S.

•Our special mining license (IUPK) may not be extended through 2041 if PT-FI fails to abide by the terms and conditions of the IUPK and applicable laws and regulations.

Operational risks

•Our mining operations are subject to operational risks that could adversely affect our business and our underground mining operations can be particularly dangerous.

•Our management of waste rock and tailings are subject to significant environmental, safety and engineering challenges and risks that could adversely affect our business.

•Violence, including shooting incidents, civil and religious strife, and activism could result in loss of life and/or disrupt our operations and may adversely affect our business.

•Our business depends on good relations with our workforce and labor disputes or labor unrest could disrupt our operations from time to time, which could adversely affect our financial results.

•Our mining operations depend on the availability of significant quantities of secure water supplies.

•Development projects are inherently risky and may require more capital than anticipated, which could adversely affect our business. The development of our underground mines and operations are also subject to other unique risks.

•We must continually replace reserves depleted by production but exploration is highly speculative and our exploration activities may not result in additional discoveries.

•Estimates of proven and probable reserves and mineralized material are uncertain and the volume and grade of ore actually recovered may vary from our estimates.

•Our operations are subject to extensive laws and regulations, some of which require permits and other approvals, which may increase our costs and may delay or result in a suspension of our operations.

•Our business is dependent upon information technology systems, which may be adversely affected by disruptions, damage, failure and risks associated with implementation and integration.

Environmental and social risks

•Our operations are subject to environmental laws and regulations, and compliance with these laws and regulations involves significant costs and may constrain existing operations or expansion opportunities.

•We incur significant costs for remediating environmental conditions on properties that have not been operated in many years.

•Our Indonesia mining operations create difficult and costly environmental challenges, which could require us to incur increased costs.

•Our operations require significant energy and regulation of greenhouse gas emissions may increase our costs and adversely affect our operations.

•The physical impacts of climate change may adversely affect our copper mining operations.

•Increasing scrutiny and evolving expectations from stakeholders with respect to our environmental, social and governance practices, performance and disclosures may impact our reputation and business and impose additional costs on us.

•Failure or perceived failure to manage our relationships with the communities where we operate, including communities that are adjacent to or near our operations and Indigenous People, could harm our reputation and social license to operate.

Other risks

•Our holding company structure may impact our ability to service debt and our stockholders’ ability to receive dividends.

•Anti-takeover provisions in our charter documents and Delaware law may make an acquisition of us more difficult.

Financial risks

Fluctuations in the market prices of the commodities we produce, primarily copper, gold and molybdenum, have caused and may continue to cause significant volatility in our financial performance and in the trading prices of our debtcommon stock and common stock.debt. Extended declines in the market prices of copper, gold and, to a lesser extent, molybdenum, could adversely affect our earnings, cash flows and asset values and, if sustained, may adversely affect our ability to repay debt.

Our financial results will vary with fluctuations in the market prices of the commodities we produce, primarily copper and gold, and to a lesser extent molybdenum. An extended declineDuring 2020, the COVID-19 pandemic and resulting negative impact on the global economy created significant volatility in the financial markets, including the copper market. In 2020, copper prices ranged from a low of $2.09 per pound in March 2020 and a high of $3.61 per pound in December 2020, and with the ongoing COVID-19 pandemic, significant volatility may continue. Extended declines in market prices of theseour commodities, whether related to the ongoing COVID-19 pandemic or otherwise, could have a material adverse effect on our financial results and the value of our assets, and/ormay depress the price of our common stock, and may have a material adverse effect on our ability to comply with financial and other covenants in our debt agreements, repay our debt and meet our other fixed obligations; and may depress the trading prices of our common stock and of our publicly traded debt securities.obligations.

Additionally, if market prices for our primary commodities decline and remain low for a sustained period of time, we may have to revise our operating plans, including curtailing production, reducing operating costsor modifying some of our mining and capital expenditures and discontinuing certain exploration and development programs.processing operations. We may be unable to decrease our costs in an amount sufficient to offset reductions in revenues, in which case we may incur losses, and those losses may be material. For example, in early 2020, we announced revised operating plans in response to the global COVID-19 pandemic and resulting negative impact on the global economy, which resulted in reductions in (i) operating costs, (ii) capital expenditures, (iii) exploration and administrative costs, and (iv) sales volumes and production from those planned.

Fluctuations in commodities prices are caused by varied and complex factors beyond our control, including global supply and demand balances and inventory levels; global economic and political conditions; international regulatory, trade andand/or tax policies, including national tariffs; commodities investment activity and speculation; interest rates; expectations regarding future inflation rates; the strength of the U.S. dollar compared to foreign currencies; the price and availability of substitute products; and changes in technology. Volatility in global economic growth, particularly in developing economies, has the potential to adversely affect future demand and prices for commodities. Geopolitical uncertainty and protectionism, including the United Kingdom’s plans to exit from the European Union (commonly referred to as Brexit), have the potential to inhibit international trade and negatively impact business confidence, which creates the risk of constraints on our ability to trade in certain markets and has the potential to increase price volatility.

Copper prices may be affected by demand from China, which has becomeis currently the largest consumer of refined copper in the world, and by changes in demand for industrial, commercial and residential products containing copper. Rising trade tensions betweenChina had a major economic shutdown during first-quarter 2020 in connection with its efforts to contain and mitigate the U.S. and China and efforts byspread of COVID-19, which resulted in the Chinese government to reduce debt levels contributed tocountry’s first reported economic contraction in over 40 years. Although our sales during 2020 were not significantly affected, a recent slowdown in China’s growth. A continued slowing in China’s economic growth, and demand and continued trade tensions betweenanother widespread COVID-19 outbreak in China or other pandemic, epidemic or endemic health issues, the U.S. and China could result in lower copper prices which could have a material adverse impact on our business and results of operations, including cash flow. The adoption and expansion of trade restrictions, changes in the state of China-U.S. relations, including the current trade war, or other governmental action related to tariffs or trade agreements or policies are difficult to predict and could adversely affect copper prices, demand for our products, our costs, our customers, our suppliers, and the U.S. economy, which in turn could have a material adverse effect on our business, results of operations, or financial condition.

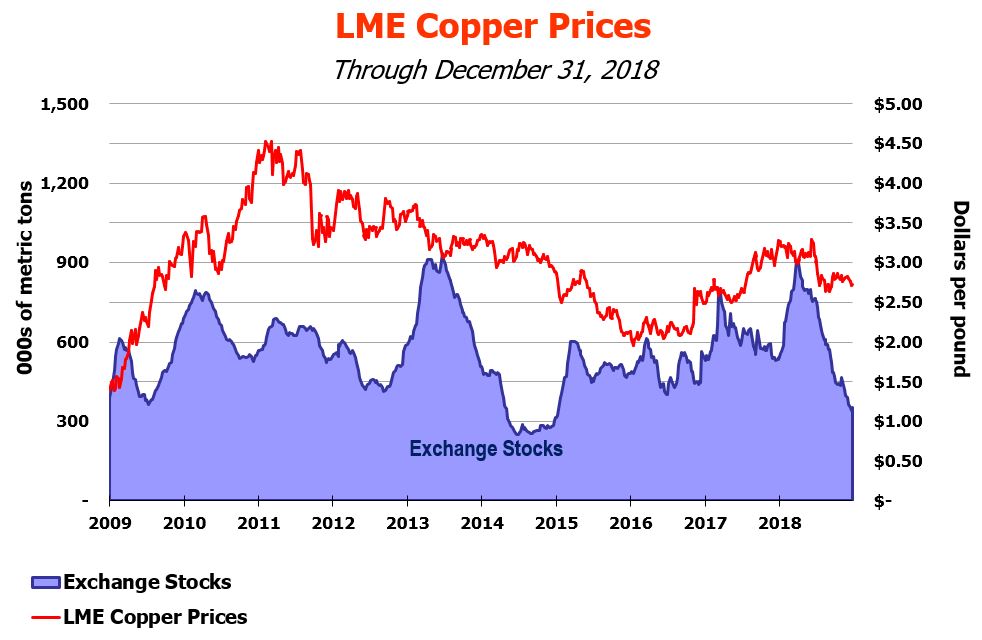

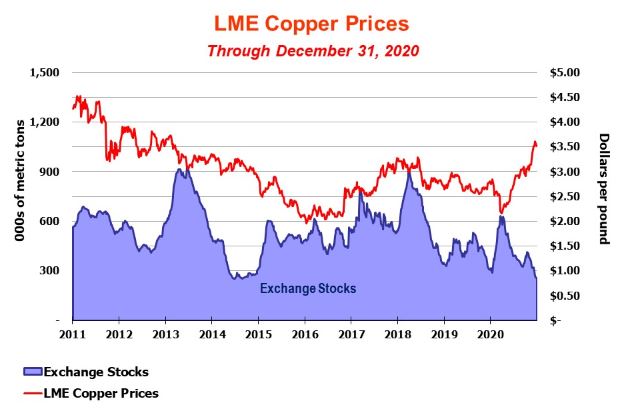

Copper prices have fluctuated historically, with London Metal Exchange (LME) copper settlement prices ranging from $1.96$2.09 per pound to $3.29$3.61 per pound during the three years ended December 31, 2018.2020. LME copper settlement prices averaged $2.80 per pound in 2020, $2.72 per pound in 2019 and $2.96 per pound in 2018, $2.80 per pound in 2017 and $2.21 per pound in 2016.2018. The LME copper settlement price was $2.71$3.51 per pound on December 31, 2018,2020, and $2.79$3.57 per pound on January 31, 2019.29, 2021.

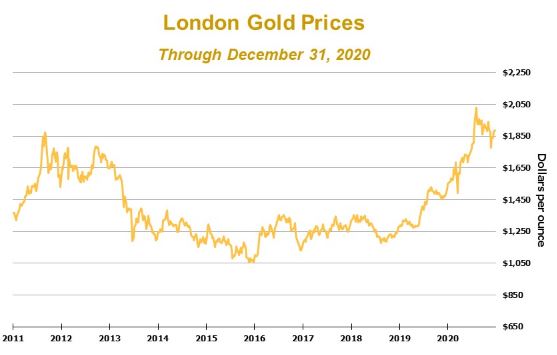

Factors affecting gold prices may include the relative strength of the U.S. dollar to other currencies, inflation and interest rate expectations, purchases and sales of gold by governments and central banks, demand from China and India, two of the world’s largest consumers of gold, and global demand for jewelry containing gold. The London Bullion Market Association (London) PM gold price averaged $1,770 per ounce in 2020, $1,393 per ounce in 2019 and $1,268 per ounce in 2018, $1,257 per ounce in 2017 and $1,250 per ounce in 2016.2018. The London PM gold price was $1,279$1,888 per ounce on December 28, 201830, 2020 (there was no London PM gold price quote on December 31, 2018)2020), and $1,323$1,864 per ounce on January 31, 2019.29, 2021.

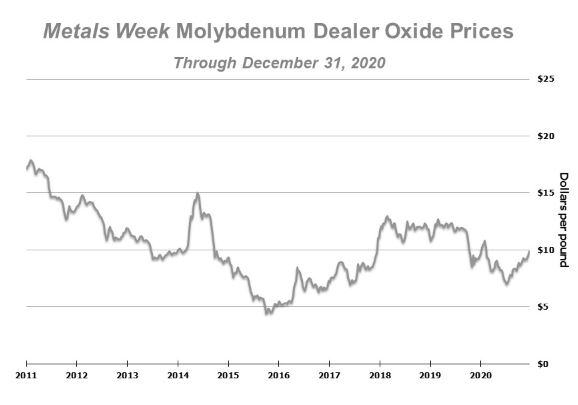

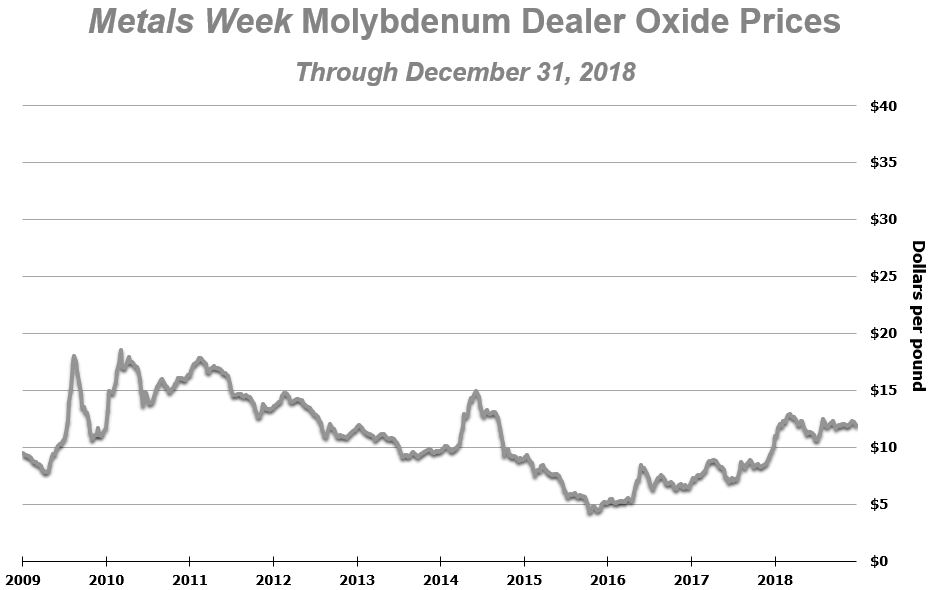

The Metals Week Molybdenum Dealer Oxide weekly average price averaged $8.69 per pound in 2020, $11.37 per pound in 2019 and $11.93 per pound in 2018, $8.21 per pound in 2017 and $6.47 per pound in 2016.2018. The Metals Week Molybdenum Dealer Oxide weekly average price was $11.88$9.86 per pound on December 31, 2018,2020, and $10.95$10.38 per pound on January 31, 2019.29, 2021.

Declines in prices of commodities we sell could result in metals inventory adjustments and impairment charges for our long-lived assets.During 2020, we recorded unfavorable metals inventory adjustments totaling $96 million associated with lower market prices for copper and molybdenum. Refer to Note 4 for additional information regarding metals inventory adjustments. Other events that could result in impairment of our long-lived assets include, but are not limited to, decreases in estimated proven and probable mineral reserves and any event that might have a material adverse effect on current and future expected mine production costs.

Our debt and other financial commitments may limit our financial and operating flexibility.

At December 31, 2018,2020, our total consolidated debt was $11.1$9.7 billion (see Note 8) and our total consolidated cash was $4.2$3.7 billion. We also have various other financial commitments, including reclamation and environmental obligations, take-or-pay contracts and leases. For further information, refer to thesee risk factor below relating to mine closure and reclamation regulations, and plugging and abandonment obligations related to our remaining oil and gas properties. Although we have been successful in repaying debt in the past, refinancing our bank facilities, and issuing new debt securities in capital markets transactions, there can be no assurance that we can continue to do so. In addition, we may incur additional debt in future periods or reduce our holdings of cash and cash equivalents in connection with funding existing operations, capital expenditures, dividends, share repurchases or in pursuing other business opportunities.

Our level of indebtedness and other financial commitments could have important consequences to our business, including the following:

•Limiting our flexibility in planning for, or reacting to, changes in the industry in which we operate;

•Increasing our vulnerability to general adverse economic, industry and industryregulatory conditions;

•Limiting our ability to fund future working capital, capital expenditures, general corporate requirements and/or material contingencies, to engage in future development activities, or to otherwise realize the value of our assets and opportunities fully because of the need to dedicate a substantial portion of our cash flows from operations to payments on our debt;

•Requiring us to sell assets to reduce debt; or

•Placing us at a competitive disadvantage compared to our competitors that have less debt and/or fewer financial commitments.

Any failure to comply with the financial andand/or other covenants in our debt agreements may result in an event of default that would allow the creditors to accelerate maturities of the related debt, which in turn may trigger cross-acceleration or cross-default provisions in other debt agreements. Our available cash and liquidity may not be sufficient to fully repay borrowings under our debt instruments that aremay be accelerated upon an event of default.

From August 2015 through November 2016, we sold 326.5 million shares of our common stock under registered at-the-market equity programs, which generated $3.5 billion in gross proceeds (refer to Note 10). In addition, during 2016, we issued 48.1 million shares of our common stock in connection with the settlement of two drilling rig contracts (refer to Note 13) and 27.7 million shares of our common stock in exchange for $369 million of FCX senior notes (refer to Note 10). Any additional issuance of equity capital to fund operations, reduce debt, improve our financial position or for other purposes, may have a negative impact on our stock price.

As of January 31, 2019,29, 2021, our senior unsecured debt was rated “BB“ with a stablepositive outlook by Standard & Poor’s, (S&P), “BB+” with a negativestable outlook by Fitch Ratings, (Fitch), and “Ba2”“Ba1” with a stable outlook by Moody’s Investors Service (Moody’s). ThereService. If we are unable to maintain our indebtedness and financial ratios at levels acceptable to these credit rating agencies, or should our business prospects deteriorate, our current credit ratings could be downgraded, which could adversely affect the value of our outstanding securities and existing debt and our ability to obtain new financing on favorable terms and could increase our borrowing costs.

The ongoing COVID-19 pandemic and any future pandemic, epidemic, endemic or similar public health threats and resulting negative impact on the global economy and financial markets may have an adverse impact on our business and results of operations, the duration and extent of which is highly uncertain and could be material.

The ongoing COVID-19 pandemic continues to adversely impact the global economy and is creating significant volatility in the financial markets, including the copper markets. The duration and scope of and uncertainties associated with, the ongoing COVID-19 pandemic and the related impact on commodity prices, our business and the global economy are evolving and beyond our control. The extent and duration of adverse impacts that the COVID-19 pandemic may have on supply, demand and prices of the commodities we produce, on our suppliers, vendors, customers and employees and on global financial markets is unknown at this time, but could be both material and prolonged. Prolonged unfavorable economic conditions, and any resulting slowed global economic growth, including the current U.S. recession, may result in lower demand for the commodities we produce, as well as the inability of various customers, contractors, suppliers and other business partners to fulfill their obligations, which could have a material adverse effect on our business and results of operations.

The COVID-19 pandemic disrupted our 2020 operating plans. In April 2020, we announced revised operating plans in response to the global COVID-19 pandemic and resulting negative impact on the global economy. Our revised operating plans focused on safeguarding our business in an uncertain public health and economic environment, advancing the ramp-up of underground production at Grasberg, and advancing initiatives in North America and South America. The ongoing COVID-19 pandemic or any future pandemic, epidemic, endemic or other similar public health threats could disrupt or change our future operating plans. For additional information, refer to Part 1, Item 2. herein.

Our business and results of operations could be adversely affected if significant portions of our workforce are unable to work effectively, including because of illness, quarantines, government actions or other restrictions in connection with the COVID-19 pandemic. We have proactively implemented operating protocols at each of our operating sites to contain and mitigate the risk of spread of COVID-19, including but not limited to, physical distancing, travel restrictions, sanitizing, and frequent health screening and monitoring. COVID-19 cases have been confirmed through testing at our operating sites, including PT-FI’s remote operating site in Papua, Indonesia. Despite our efforts to manage these impacts, there can be no assurance that our credit ratingsactions will be effective in containing and mitigating the risk of spread or a major outbreak of COVID-19 at our operating sites. Additionally, although several vaccines for COVID-19 have been approved, there are risks that these vaccines will not be downgradedeffective against variants of the virus and that these vaccines may not be accepted or widely available in the future.

Certainareas in which we operate due to shortages or other issues with distribution. A major outbreak of COVID-19 at any of our debt agreements, includingoperating sites, and particularly at PT-FI’s remote operating site, could have a material adverse effect on our revolving credit facility, usebusiness and results of operations.

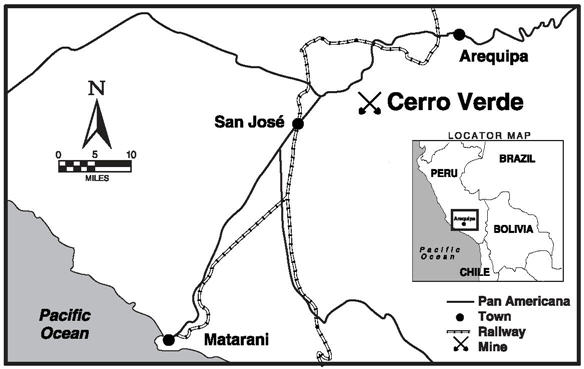

Actions taken by governmental authorities and third parties to contain and mitigate the London Interbank Offered Rate (LIBOR) asrisk of spread of COVID-19 may have an adverse impact on our business. For example, in mid-March 2020, the Peru government issued a reference rate. In July 2017,Supreme Decree and declaration of a National Emergency in its efforts to contain the United Kingdom’s Financial Conduct Authority, which regulates LIBOR, announced that it intendsoutbreak of COVID-19, and subsequently extended the order through May 10, 2020. The Peru government also extended the quarantine measures instituted in mid-March 2020 through August 31, 2020, for certain cities in Peru (including Arequipa, where our Cerro Verde mine is located). To comply with the government’s requirements, we temporarily transitioned our Cerro Verde mine to phase out LIBORcare and maintenance status and adjusted operations to prioritize critical activities. Strict health protocols have been implemented and a plan for Cerro Verde to restore operations was approved by the endPeru government in second-quarter 2020. Cerro Verde continued to increase milling rates while operating consistent with our April 2020 revised operating plans and under strict COVID-19 restrictions and protocols. Cerro Verde expects mill rates to average approximately 360,000 metric tons of 2021. If LIBORore per day in 2021 with the potential to ramp-up to pre-COVID-19 levels approximating 400,000 metric tons of ore per day as COVID-19 restrictions are lifted.

These and other impacts of COVID-19 or other pandemic, epidemic, endemic or similar public health threats could also have the effect of heightening many of the other risks described in these “Risk Factors.” The ultimate impact of COVID-19 on our business is unavailable after 2021, our debt with interest ratesdifficult to predict and depends on factors that are indexedevolving and beyond our control, including the scope and duration of the outbreak and recovery, including any future resurgences, as well as actions taken by governmental authorities and third parties, including the distribution, effectiveness and acceptance of

vaccines, to LIBOR willcontain its spread and mitigate its public health effects. Any of these disruptions could continue to adversely impact our business and results of operations, and such adverse impacts could be determined using various alternative methods to the extent provided for in our agreements, which could result in increases in interest rates on such debt. Further, we may need to renegotiate our debt agreements and the loans that utilize LIBOR to replace LIBOR with the new standard that is established by the U.S. Alternative Rate Reference Committee, which is currently expected to be the Secured Overnight Bank Financing Rate.material.

Mine closure and reclamation regulations impose substantial costs on our operations and include requirements that we provide financial assurance supporting those obligations. We also have plugging and abandonment obligations related to our remaining oil and gas properties, and are required to provide bonds or other forms of financial assurance in connection with those properties.Changes in or the failure to comply with these requirements could have a material adverse effect on us.our business.

We are required by U.S. federal and state laws and regulations to provide financial assurance sufficient to allow a third party to implement approved closure and reclamation plans for our mining properties if we are unable to do so. Most of our financial assurance obligations are imposed by state laws that vary significantly by jurisdiction, depending on how each state regulates land use and groundwater quality. The U.S. Environmental Protection Agency (EPA) and state agencies may also require financial assurance for investigation and remediation actions that are required under settlements of enforcement actions under the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (CERCLA) or similar state laws. Refer to Note 12 for additional information regarding our financial assurance obligations.

With respect to our mining operations, most of our financial assurance obligations are imposed by state laws that vary significantly by jurisdiction, depending on how each state regulates land use and groundwater quality. Although Section 108(b) of CERCLA has required EPA to identify classes of facilities that must establish evidence of financial responsibility since CERCLA was adopted in 1980, currently, there are no financial assurance requirements for

active mining operations under CERCLA. In response to litigation initiated by several environmental organizations against EPA and a subsequent settlement, EPA proposed financial assurance regulations for the hard rock mining industry in January 2017, which were vigorously opposed by us and others in the mining industry. As proposed, the rules would have imposed financial responsibility obligations on U.S. hard rock mining operations that are unnecessary, duplicative of existing state and other federal requirements, and unreasonable. Our initial calculations suggested that the financial responsibility amounts would be difficult, if not impossible, for us and others to meet with corporate resources, and would be extremely expensive, if not impossible, to finance with third-party financial instruments such as letters of credit, bonds or insurance. In December 2017, EPA withdrew its proposed rules and in February 2018, EPA published its final decision that additional financial assurance regulations for the hard rock mining industry would not be needed given the existing state and federal regulatory programs that became effective in March 2018. In May 2018, environmental organizations filed a petition for review with the U.S. Court of Appeals for the District of Columbia. We and others in the mining industry intervened in the case. If the court remands the rule back to EPA for reconsideration, a re-proposal of rules similar in nature to EPA’s 2017 proposed rules would severely harm the international competitiveness of the U.S. hard rock mining industry and would materially and adversely affect our cash flows, results of operations and financial condition.

We are also subject to financial assurance requirements in connection with our remaining oil and gas properties and certain of our previously sold oil and gas properties under both state and federal laws, including financial responsibility required under the Oil Pollution Act of 1990 to cover containment and cleanup costs resulting from an oil spill. As a result of a significant increase in the number of oil and gas companies experiencing financial distress, especially those operating in the Outer Continental Shelf, we may have additional exposure if our partners or buyers of our previously owned properties file for bankruptcy and/or default on their share of the abandonment obligations. In 2016, the U.S. Bureau of Ocean Energy Management (BOEM) issued revised requirements for lessees operating in federal waters to secure the cost of plugging, abandoning, decommissioning and/or removing wells, platforms and pipelines at the end of production. The revised requirements eliminate previously provided waivers from requirements to post security. In early 2017, the BOEM announced a delay in the implementation of certain aspects of the rules pending further review and in June 2017, BOEM further extended the start date for implementation indefinitely. This extension currently remainsOn October 16, 2020, BOEM issued a Notice of Proposed Rulemaking and Request for Comments that proposed to limit the circumstances in effect. If implemented,which it will require supplemental bonding so that it will apply more narrowly than the new requirements could require us2016 requirements. However, we may still be subject to post security in the formsignificant levels of bonds or similar assurances.supplemental bonding. The cost for bonds or other forms of assurances can be substantial, and there is no assurance that they can be obtained in all cases.

As of December 31, 2018,2020, our financial assurance obligations totaled $1.2$1.5 billion for closure and reclamation/restoration costs of U.S. mining sites, and $0.5 billion for plugging and abandonment obligations of our remaining oil and gas properties. A substantial portion of our financial assurance obligations are satisfied by FCXFreeport-McMoRan Inc. (FCX) and subsidiary guarantees and financial capability demonstrations. Our ability to continue to provide guarantees and financial capability demonstrations depends on state and other regulatory requirements, our financial performance and our financial condition. Other forms of assurance, such as letters of credit and surety bonds, are costly to provide and, depending on our financial condition and market conditions, may be difficult or impossible to obtain. Failure to provide the required financial assurance could result in the closure of the affected properties.

The laws and regulations governing mine closure and remediation in a particular jurisdiction and oil and gas properties plugging and abandonment obligations are subject to review at any time and may be amended to impose additional requirements and conditions, which may cause our provisions for environmental and asset retirement obligations to be underestimated and could materially affect our financial position or results of operations. Similarly, our implementation of the Global Industry Standard for Tailings Management (the Tailings Standard) (discussed below) could require changes to our closure and reclamation plans, although it is uncertain if these changes would result in material capital or operating cost increases. In addition, climate change could lead to changes in the physical risks posed to our operations, which could result in changes in our closure and reclamation plans to address such risks. Any modifications to our closure and reclamation plans that may be required to address physical climate risks may materially increase the costs associated with implementing closure and reclamation at any or all of our active or inactive mine sites and the financial assurance obligations related to the same. Refer to Notes 1 and 12, for further discussion of our environmental and asset retirement obligations.

Unanticipated litigation or negative developments in pending litigation or with respect to other contingencies could have a material adverse effect on our cash flows, results of operations and financial condition.

We are involved in numerous legal proceedings and subject to other contingencies that have arisen or may arise in the ordinary course of our business or are associated with environmental issues, including those described in Note 12 and in Item 3. “Legal Proceedings” involving matters such as remediation, restoration and reclamation of environmental contamination, claims of personal injury or property damage arising from such contamination or from exposure to substances such as lead, arsenic, asbestos, talc, uranium and other allegedly toxic substances, disputes over water rights, and disputes with foreign governments or regulatory authorities over royalties, taxes, rights and obligations under concession or other agreements, or other matters. We are also involved periodically in other reviews, inquiries,investigations and other proceedings initiated by or involving government agencies, some of which may result in adverse judgments, settlements, fines, penalties, injunctions or other relief. In addition, fromFrom time to time we are involved in disputes over the allocation of environmental remediation obligations at Superfund“superfund” and other sites. In addition, we may be held responsible for the costs of addressing contamination at the site of current or former activities or at third party sites, or be held liable to third parties for exposure to hazardous substances should those be identified in the future. The outcome of litigation is inherently uncertain and adverse developments or outcomes can result in significant monetary damages, penalties, other sanctions or injunctive relief against us, limitations on our property rights, or regulatory interpretations that increase our operating costs. Management does not believe, based on currently available information, that the outcome of any individual legal proceeding will have a material adverse effect on our financial condition, although individual or cumulative outcomes could be material to our operating

results for a particular period, depending on the nature and magnitude of the outcome and the operating results for the period.

With respect to the asbestos and talc exposure cases described in Note 12, there has been a recent significant increase in the number of cases alleging the presence of asbestos contamination in talc-based personal care products and in cases alleging exposure to talc products that are not alleged to be contaminated with asbestos. In these cases, plaintiffs allege serious health risks and often fatal diseases, including mesothelioma and ovarian cancer, allegedly caused by long-term use of talc-based cosmetic and personal care products. Nationwide trial results in these cases have ranged from outright dismissals to very large jury awards of both compensatory and punitive damages. The primary targets have been the producers of those products, but defendants in many of these cases also include talc miners. Cyprus Amax Minerals Company (CAMC), an indirect wholly owned subsidiary of FCX is one of those targets. One of CAMC’s wholly owned subsidiaries, Cyprus Mines Corporation, was involved in talc mining until 1992 when it exited that business. CAMC has contractual indemnification rights, subject to limited reservations, against the ultimate successor to the business, which has acknowledged those indemnification obligations and has taken responsibility for all cases tendered to it to date. However, on February 13, 2019, the indemnitor filed for Chapter 11 bankruptcy protection, and CAMC is in the very early stages of evaluating the potential implications of that filing.

We may be adversely impacted by increased liabilities and costs related toour defined benefit pension plans.

We sponsor two defined benefit pension plans for certain current and former employeeemployees in the U.S. and a few pension plans for non-U.S. locations which provide for specified payments after retirement. The major defined benefit pension plans are funded with trust assets invested in a diversified portfolio of securities and other investments. Changes in regulatory requirements or the market value of plan assets, investment returns, interest rates and mortality rates may affect the funded status of our defined benefit pension plans and may cause volatility in the net periodic benefit cost, future funding requirements of the plans and the funded status as recorded on the balance sheet. A sustained period of low or insufficient investment returns or low interest rates could require us to fund our pension plans to a greater extent than anticipated. Refer to Note 9 for further discussion.

International risks

Our international operations are subject to political, economic, social and regional risks of doing business in countries outside the U.S.

We are a U.S.-based mining company with substantial assets located outside of the U.S. We conduct international mining operations in Indonesia, Peru and Chile and exploration activities in various foreign jurisdictions. Accordingly, in addition to the usual risks associated with conducting business in countries outside the U.S., our business may be adversely affected by political, economic, social and regional uncertainties in each of these countries. Risks of conducting business in countries outside the U.S. include:

•Delays in obtaining or renewing, or the inability to obtain, maintain or renew, or the renegotiation, cancellation, revocation or forced modification of existing contracts, leases, licenses, permits or other agreements and/or approvals;

•Expropriation or nationalization of property, protectionism, or restrictions on repatriation of earnings or capital, or other currency controls;capital;

•Changes in the host country’s laws, regulations and policies (which may be applied retroactively), including, but not limited to, those relating to labor, taxation, royalties, duties, tariffs, divestment, imports, exports (including restrictions on the export of copper concentrates, copper and/or gold), trade regulations, immigration, currency and environmental matters (including land use and water use), which because of rising “resource nationalism” in countries around the world, may impose increasingly onerous requirements on foreign operations and investment;investment, and/or result in fines, fees, and sanctions imposed for failure to comply with the laws and regulations of the jurisdictions in which we operate;

•Political, social and economic instability, bribery, extortion, corruption, civil unrest, acts of war, guerrilla activities, insurrection and terrorism;

Changes in the aspirations and expectations of local communities in which we operate with respect to our contributions to employee health and safety, infrastructure and community development and other factors that may affect our social license to operate, allterrorism, certain of which leadmay result in, among other things, an inability to increased costs;access our property;

•Risk of loss associated with trespass, local artisanal or illegal mining, theft and vandalism;vandalism or due to potential pandemic, epidemic and endemic health issues;

•Changes in U.S. trade, tariff, tax, immigration or other policies that may harm relations with foreign countries or result in retaliatory policies, including the U.S.-China trade war that began in 2018 which, if prolonged, could have a significant adverse effect on global trade and the global economy;policies;

•Increases in training and other costs and challenges relating to requirements by governmental entities to employ the nationals of the country in which a particular operation is located;

•Foreign exchange controls, fluctuations in foreign currency exchange rates and inflation;

•Reduced protection for intellectual property rights; and

•The risk of having to submit to the jurisdiction of an international court or arbitration panel or having to enforce the judgment of an international court or arbitration panel against a sovereign nation within its own territory.nation.

Our insurance does not cover most losses caused by the above described risks. Accordingly, our exploration, development and production activities outside of the U.S. may be substantially affected by many unpredictable factors beyond our control, some of which could have a material adverse effect on our cash flows, results of operations and financial condition.

Our international operations must comply with the U.S. Foreign Corrupt Practices Act and similar anti-corruption and anti-bribery laws of the other jurisdictions in which we operate. There has been a substantial increase in the global enforcement of these laws in recent years. We operate in certain jurisdictions that have experienced governmentalpublic and private sector corruption to some degree, and in certain circumstances, compliance withwhere significant anti-corruption enforcement activities, prosecutions, and anti-bribery laws and heightened expectations of enforcement authorities may be in tension with certain local customs and practices.settlements have occurred. There can be no assurance that our internal control policies and procedures will always protect us from misinterpretation of or noncompliance with applicable laws and internal policies, recklessness, fraudulent behavior, dishonesty or other inappropriate acts committed by our affiliates, employees, agents or contractors. As such, our corporate policies and processes may not prevent or detect all potential breaches of law or other governance practices. Any violation of thoseanti-corruption or anti-bribery laws could result in significant criminal or civil fines and penalties, litigation, and loss of operating licenses or permits, and may damage our reputation, which could have a material adverse effect on our cash flows, results of operations and financial condition.

We conduct international mining operations in Indonesia, Peru and Chile and exploration activities in various foreign jurisdictions. Accordingly, in addition to the usual risks associated with conducting business in countries outside the U.S., our business may be adversely affected by political, economic, social and regional uncertainties in each of these countries. For example, we are involved in several significant tax proceedings and other tax disputes with IndonesianIndonesia and PeruvianPeru tax authorities (refer to Note 12 for further discussion of these matters). Other risks specific to certain countries in which we operate are discussed in more detail below.

Because our mining operationoperations in Indonesia isare a significant operating asset, our business may be adversely affected by political, economic and social uncertainties in Indonesia.

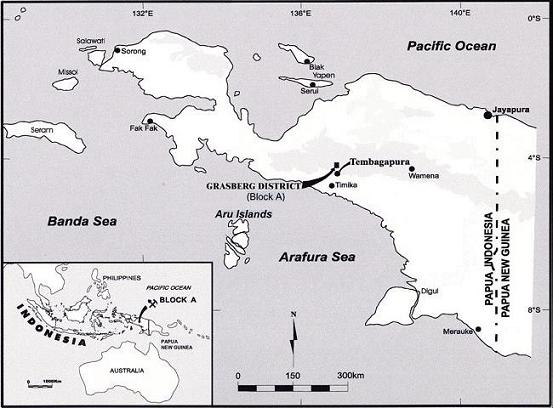

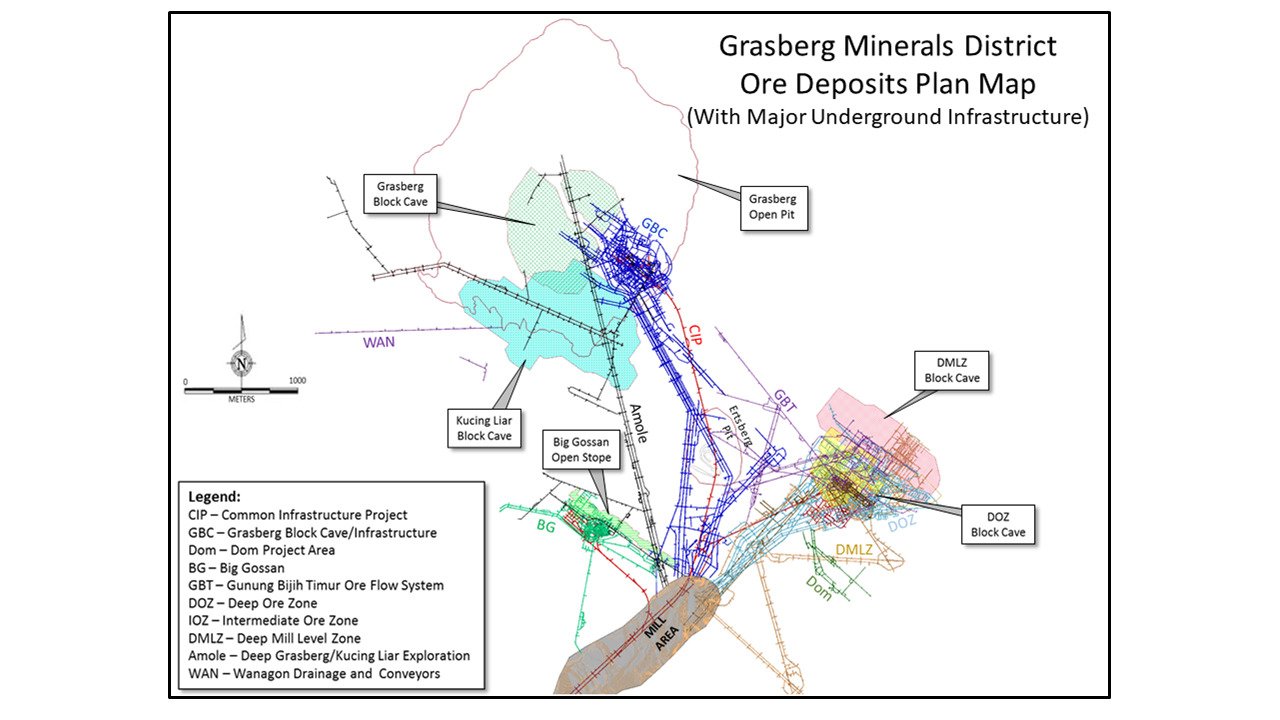

Our Indonesia mining operations include the Grasberg minerals district, one of the world’s largest copper and gold deposits. These operations are conducted by our subsidiary PT-FI pursuant to a special mining license (IUPK) issued by the Indonesian government on December 21, 2018, which replaced PT-FI’s former Contract of Work (COW) entered into in December 1991. Under the terms of the IUPK, PT-FI has been granted an extension of mining rights through 2031, with rights to extend its mining rights through 2041, subject to, among other things, PT-FI completing the construction of a new smelter in Indonesia by December 21, 2023, and fulfilling its defined fiscal obligations to the Indonesian government. Refer to Note 13 for a summary of the IUPK’s key fiscal terms.

PT-FI has applied for a one-year extension of its export license, which currently expires on February 16, 2019. Export licenses are valid for one year periods, subject to review and approval by the Indonesian government every six months, depending on smelter construction progress.

Maintaining a good working relationship with the IndonesianIndonesia government is important because of the significance of our Indonesia operations to our business, and because our mining operations there are among Indonesia’s most significant business enterprises. The Grasberg minerals district has been designated by the IndonesianIndonesia government as one of Indonesia’s vital national assets. Partially because of its significance to Indonesia’s economy, the environmentally sensitive area where it is located, and the number of people employed, our Indonesia operations have been the subject of political debates and of criticism in the IndonesianIndonesia press, and have been the target of

protests and occasional violence. Improper management of our working relationship with the IndonesianIndonesia government could lead to a disruption of operations and/or impact our reputation in Indonesia and in the region where we operation, operate,

which could adversely affect our business. In addition, PT Indonesia Asahan Aluminium (Persero) (PT Inalum)Inalum, also known as MIND ID), a shareholder in PT-FI, is an IndonesianIndonesia state-owned enterprise. Disputes between us and PT Inalum may result in litigation or arbitration, which could increase our expenses and distract our officers and directors from focusing their time and effort on our business.business and could create tensions with the Indonesia government.

The IndonesianIndonesia mining industry is subject to extensive regulation within Indonesia, and there have been major developments in laws and regulations applicable to mining concession holders, some of which have conflicted with PT-FI’s contractual rights in the past. In particular, the enactment of Law No. 4 of 2009 on Coal and Mineral Mining on January 12, 2009 (the Mining Law) replaced the previous regulatory framework which allowed concession holders, including PT-FI, to conduct mining activities in Indonesia under a contract of work system. The Mining Law, which sets out the regulatory framework for the mining industry in Indonesia, only contains substantive principles and leaves many specific issues to be addressed in implementing regulations, some of which have conflicted with PT-FI’s contractual rights in the past, including, but not limited to, regulations that imposed a progressive export duty on copper concentrate, restricted exports of copper concentrate and anode slimes, increased royalty rates, and required payment of a smelter assurance bond to support a commitment to construct a new smelter in Indonesia (refer to Note 13 for further discussion of the smelter assurance bond). In January 2017, PT-FI suspended exports through April 2017 in response to these Mining Law regulations.

The Mining Law stipulated that previously granted mining rights (through a contract of work) would continue to be valid until expiry, subject to certain adjustments. PT-FI’s former COW was concluded pursuant to the 1967 Foreign Capital Investment Law, which provided basic guarantees of remittance rights and protection against nationalization, a framework for economic incentives and basic rules regarding other rights and obligations of foreign investors. The initial term of PT-FI’s former COW was scheduled to expire in 2021 and explicitly provided that it could be extended for two 10-year periods subject to Indonesian government approval, which could not be withheld or delayed unreasonably. Prior to the issuance of the IUPK to PT-FI in December 2018, PT-FI had been engaged in discussions with the Indonesian government since 2012 regarding various provisions of its former COW, including extending its term. Notwithstanding provisions in PT-FI’s former COWContract of Work (COW) prohibiting it from doing so, the IndonesianIndonesia government sought to modify PT-FI’s former COW to address provisions contained in the Mining Law and implementing regulations adopted thereunder, some of which were not required under or conflicted with PT-FI’s former COW, including, but not limited to (i) restrictions on PT-FI’s basic right to export mining products; (ii) imposition of additional export duties;duties and higher royalty rates; (iii) imposition of excess surface water taxes (refer to Note 12); (iv) imposition of new requirement to build additional smelter capacity in Indonesia; (v) unreasonable withholding and delay in granting approval of two successive ten-year extensions of the term of the former COW; and (vi) imposition of new divestment requirements.

In early 2017, the Indonesia government issued new regulations to address exports of unrefined metals, including copper concentrate and anode slimes, and other matters related to the mining sector. PT-FI’s export license for copper concentrate is valid for one year periods, subject to review and approval by the Indonesia government every six months, depending on smelter construction progress. PT-FI’s export license expires on March 15, 2021. Refer to MD&A and Note 12 for further discussion of the administrative fine levied by the Indonesia government on PT-FI for failing to achieve physical development progress on the new smelter, and ongoing discussions with the Indonesia government regarding a deferred schedule for the completion of the new smelter project as well as other alternatives in light of the ongoing COVID-19 pandemic and volatile global economic conditions. The 2017 regulations also permit the export of anode slimes, which is necessary for PT Smelting (PT-FI’s 25-percent-owned copper smelter and refinery located in Gresik, Indonesia) to continue operating. PT Smelting’s export license for anode slimes expires on July 18, 2021. In addition to a delay in the renewal of its export license for anode slimes in 2017, PT Smelting’s operations were shut down from mid-January 2017 until early March 2017 as a result of labor disturbances. Copper concentrate sales to PT Smelting totaled over 10 percent of our consolidated revenues for each of the years ended December 31, 2020, 2019 and 2018. We cannot predict when PT-FI’s copper concentrate license and PT Smelting’s anode slimes export license may be renewed. PT-FI’s sale of concentrates could be interrupted if either of these export license is not timely renewed or if PT Smelting is unable to operate either due to other operational or financial constraints, which would adversely impact our revenues and operations.

We cannot assure you that future regulatory changes affecting the mining industry in Indonesia will not be introduced or unexpectedly repealed, or that new interpretations of existing laws and regulations will not be issued, which could adversely affect our business, financial condition and results of operations.

In 2019, Indonesia will hold national legislative elections. The presidential election will be held in April 2019, with a run-off in August 2019, if required. Political considerations leading up to these elections could affect the country’s policies pertaining to foreign investment, which could adversely affect our Indonesia mining operations.

We will not mine all of PT-FI’s ore reserves in the Grasberg minerals district before the initial term of PT-FI’s IUPK expires in 2031 and the IUPK may not be extended through 2041 if PT-FI fails to abide by the terms and conditions of the IUPK and applicable laws and regulations.

As discussed in the above risk factor, “Because our mining operation in Indonesia is a significant operating asset, our business may be adversely affected by political, economic and social uncertainties in Indonesia”, onOn December 21, 2018, PT-FI was granted a newan IUPK to replace its former COW, enabling PT-FI to conduct operations in the Grasberg minerals district through 2041. Under the terms of the IUPK, PT-FI has been granted mining rights through 2031, with rights to extend its mining rights through 2041, subject to, among other things, PT-FI completing the construction of a new smelter in Indonesia by December 21, 2023 (an extension of which has been requested due to COVID-19 mitigation measures subject to the approval of the Indonesia government), and

fulfilling its defined fiscal obligations to the IndonesianIndonesia government. Refer to Note 13 for a summary of the IUPK’s key fiscal terms.

The IUPK also requires PT-FI to pay duties on concentrate exports of 5 percent, declining to 2.5 percent when smelter development progress exceeds 30 percent, and eliminated when smelter development progress exceeds 50 percent. SmelterRefer to MD&A and Note 12 for further discussion of the administrative fine levied by the Indonesia government on PT-FI for failing to achieve physical development progress will be determined by an independent verifier appointed byon the Ministrynew smelter, and ongoing discussions with the Indonesia government regarding a deferred schedule for the completion of Energythe new smelter project as well as other alternatives in light of the ongoing COVID-19 pandemic and Mineral Resources (MEMR)volatile global economic conditions. Engineering and subject to approval by the MEMR. PT-FI is initiating front-end engineering and design and intends to pursue financing, commercial and potential partner arrangements for this project, which has athe selected process technology are ongoing. The preliminary estimated capital cost inestimate for the project approximates $3 billion, range.and PT-FI plans to arrange financing for the project. The economics of the new smelter will be borne by PT-FI’s shareholders according to their respective long-term share ownership percentages. PT-FI’s ability to raise and service significant new sources of capital will be a function of macroeconomic conditions, future market prices as well as PT-FI’s operational performance, cash flow and debt position, among other factors. Financing may not be available when needed or, if available, the terms of such financing may not be favorable to PT-FI.

Our proven and probable ore reserves in Indonesia reflect estimates of minerals that can be recovered through the end of 2041, and PT-FI’s current long-term mine plan and planned operations are based on the assumption that PT-FI will abide by the terms and conditions of the IUPK and will be granted the 10-year extension from 2031 through 2041. As a result, we will not mine all of these ore reserves during the initial term of the IUPK. Prior to the end of 2031, we expect to mine 5350 percent of aggregate proven and probable recoverable ore at December 31, 2018,2020, representing 57 percent of our net equity share of recoverable copper reserves and 6459 percent of our net equity share of recoverable gold reserves.

If PT-FI does not complete the construction of a new smelter in Indonesia by December 21, 2023 (an extension of which has been requested due to COVID-19 mitigation measures subject to the approval of the Indonesia government), or fulfill its defined fiscal obligations to the IndonesianIndonesia government as set forth in the IUPK, the IUPK will likely not be extended from 2031 to 2041, and we would be unable to mine all of PT-FI’s ore reserves in the Grasberg minerals district, which would adversely affect our business, results of operations and financial position.

Operational risks

Our mining operations are subject to operational risks that could adversely affect our business and our underground mining operations can be particularly dangerous.

Our mines are very large in scale and, by their nature are subject to significant operational risks, some of which are outside of our control, and many of which are not covered fully, or in some cases even partially, by insurance. These operational risks, which could materially and adversely affect our business, operating results and cash flow, include earthquakes, rainstorms, floods, and other natural disasters; environmental hazards, including discharge of metals, concentrates, pollutants or hazardous chemicals; surface or underground fires; equipment failures; accidents;accidents, including in connection with mining equipment, milling equipment or conveyor systems, transportation of chemicals, explosives or other materials and in the transportation of employees and business partners to and from sites; wall failures and rock slides in our open-pit mines, and structural collapses of our underground mines or tailings impoundments; and lower than expected ore grades or recovery rates.rates; and unexpected geological formations or conditions (whether in mineral or gaseous form).

Since late JanuaryFor a discussion of risks specific to our tailings management, see below “Our management of waste rock and tailings are subject to significant environmental, safety and engineering challenges and risks that could adversely affect our business.”

We are facing continued geotechnical challenges due to the older age of some of our open-pit mines and a trend toward mining deeper pits and more complex deposits. No assurances can be given that unanticipated geotechnical and hydrological conditions may or may not occur, nor whether these conditions may lead to events such as landslides and pit wall failures, in the future or that such events will be detected in advance. Geotechnical instabilities can be difficult to predict and are often affected by risks and hazards outside of our control, such as seismic activity or severe weather, which may lead to floods, mudslides, pit-wall instability, and possibly even slippage of material. During the first quarter of 2019, our El Abra operation in Chile has experienced heavy rainfall and electrical storms, resulting instorms. As a result, our operating results for 2019 were impacted by a suspension of El Abra’s crushed

leach stacking operations since February 4, 2019.for approximately 35 days. We have been unablecannot predict whether similar events will occur in the future or the extent to assess damages becausewhich any such event would affect this, or any of poor road conditions and inaccessible areas and we do not currently know when normal operations will resume. We estimate the impact on 2019 production will approximate 8 million pounds of copper through mid-February 2019, and additional impacts of approximately 600 thousand pounds of copper per day are expected until normal operations resume.our other operations.

Underground mining operations can be particularly dangerous, and in May 2013, a tragic accident, which resulted in 28 fatalities and 10 injuries, occurred at PT-FI when the rock structure above the ceiling of an underground training facility collapsed. PT-FI temporarily suspended mining and processing activities at the Grasberg complex to conduct inspections and resumed open-pit mining and concentrating activities in June 2013, and underground operations in July 2013. No assurance can be given that similar events will not occur in the future.

In addition to the usual risks encountered in the mining industry, our Indonesia mining operations involve additional

risks given that such operations are locatedtheir location in steep mountainous terrain in a remote area of Indonesia. These

conditions have required us to overcome special engineering difficulties and develop extensive infrastructure facilities. The area also receives considerableextreme rainfall, which has led to periodic floods and mudslides. Further, the

mine site is also in an active seismic area and has experienced earth tremors from time to time. Our

We maintain insurance at amounts we believe to be reasonable to cover some of these risks and hazards; however, our insurance may

not sufficiently cover an unexpectedlosses from certain natural or operating disaster.disasters. No assurance can be given that such insurance will continue to be available, or that it will be available at economically feasible premiums, or that we will be able to obtain or maintain such insurance. We may elect to not purchase insurance for certain risks due to the high premium costs associated with insuring such risk or for various other reasons. We do not have coverage for certain environmental losses and other risks, as such coverage generally cannot be purchased at a commercially reasonable cost by us or other companies within the mining industry. The lack of, or insufficiency of, insurance coverage could adversely affect our cash flow and overall profitability.

The occurrence of one or more of these events in connection with our exploration activities and development of and production from mining operations may result in the death of, or personal injury to, our employees, other personnel or third parties, the loss of mining equipment, damage to or destruction of mineral properties or production facilities, significant repair costs, monetary losses, deferral or unanticipated fluctuations in production, extensive community disruption, loss of licenses, permits or necessary approvals to operate, loss of infrastructure and services, disruption to essential supplies or delivery of our products, environmental damage and potential legal liabilities, all of which may adversely affect our reputation, business, prospects, results of operations and financial position.

Our management of waste rock and tailings are subject to significant environmental, safety and engineering challenges and risks that could adversely affect our business.

The waste rock (including overburden) and tailings produced in our mining operations represent our largest volume of waste material. Managing the volume of waste rock and tailings presents significant environmental, safety and

engineering challenges and risks primarily relating to structural stability, geochemistry, water quality and dust generation. Management of this waste is regulated in the jurisdictions where we operate and our programs are designed to be in compliancecomply with applicable national, state and local laws, permits and approved environmental impact studies.

We maintain large leach pads and tailings impoundments containing viscous material, which are effectivelymaterial. Tailings impoundments include large damsembankments that must be engineered, constructed and monitored to ensure structural stability and avoid leakages or structural collapse. Our tailings impoundments in arid areas must have effective programs to suppress fugitive dust emissions, and we must effectively monitor and treat acid rock drainage at all of our operations. In Indonesia, we use a river transport system for tailings management, which presents other risks as discussed below.in more detail below under Environmental and social risks - “Our Indonesia mining operations create difficult and costly environmental challenges, and future changes in environmental laws, or unanticipated environmental impacts from those operations, could require us to incur increased costs.”

WeAffiliates of our company currently operate 1917 tailings storage facilities, 15 in the U.S. and 2 in Peru; and manage 5556 tailings storage facilities in the U.S. that are inactive or closed (approximately three-fourths of the inactive facilities have been reclaimed (approximately two-thirdsclosed). Our inventory of these have been reclaimed).tailings storage facilities comprises 12 active and 51 inactive or closed facilities with an upstream design and 5 active and 5 inactive with a centerline design. In 2020, we produced approximately 259 million metric tons of tailings. The failure of tailings and other impoundmentsembankments at any of our mining operations could cause severe, and in some cases catastrophic, property and environmental damage and loss of life, as well as adverse effects on our business and reputation. Many of our tailings storage facilities are located in areas where a failure has the potential to impact individual dwellings and a limited number of impoundments are in areas where a

failure has the potential to impact nearby communities or mining infrastructure. As a result, our programs take into account the significant consequences resulting from a potential failure, and we apply significantsubstantial financial resources and both internal and external technical resources to pursue the safe management of all those facilities. The importance of careful design, management and monitoring of large impoundments has been emphasized in recent years, including as recently as January 2019, by large scale tailings dam failures at unaffiliated mines, which resulted in numerous fatalities and caused extensive property and environmental damage. Our tailings management and stewardship program, which involves qualified external Engineers of Record and periodic oversight by independent External Tailingstailings Technical Review Boards at numerous operations,and our Tailings Stewardship Team, complies with the tailings governance framework on preventing catastrophic failure of tailings storage facilities adopted in December 2016 by the International Council on Mining and Metals (ICMM), an industry group of which we are a founding member, and required to be implemented by ICMM members. We continue to enhance our existing practices and work with ICMM members on additional initiatives to strengthen critical controls for the design, operation and closure of tailings storage facilities in an effort to reduce the risk of severe or catastrophic failure of tailings storage facilities butthose facilities. However, no assurance can be given that these events will not occur in the future.

Labor unrest, violence, activismThe importance of careful design, management and monitoring of large impoundments has been emphasized in recent years by large scale tailings dam failures at unaffiliated mines, which resulted in numerous fatalities and caused extensive property and environmental damage. As a result of failures at unaffiliated mines, in 2019, international groups initiated the drafting of standards for the safe management of tailings facilities. In August 2020, the co-conveners of the Global Tailings Review, which included ICMM, published the Tailings Standard. The Tailings Standard includes 77 requirements across 6 key areas including the design, construction, operation and monitoring of tailings facilities, management and governance, emergency response and long-term recovery, and public disclosure. ICMM has committed that members will implement the Tailings Standard within three years for certain facilities and within five years for all others. ICMM members have prepared a guidance document focused on practices that drive safe tailings management and prepared a conformance protocol document to be used by companies on demonstrating implementation of the Tailings Standard; both documents are expected to be published in early 2021. As an ICMM member, management has committed to implement the Tailings Standard at our tailings storage facilities, including providing required public disclosures regarding our facilities and efforts. We are evaluating changes to our tailings stewardship and management programs and approaches that may be needed to demonstrate conformance with the Tailings Standard, although it is uncertain if changes would result in material capital or operating cost increases.

In addition, changes in physical risks to our facilities resulting from climate change could lead to changes in our plans for managing tailings and waste rock in order to address such risks, which may materially increase the costs associated with managing waste rock and tailings at any or all of our active or inactive mine sites. Addressing the effects of climate change on tailings facilities is a requirement under the Tailings Standard.

Based on observations from such tailings failures at unaffiliated mines, in addition to fatalities and severe personal, property and environmental damages, these events could result in limited or restricted access to mine sites, suspension of operations, decrease in reserves, legal liability (possibly involving the freezing of assets), government investigations, additional regulations and restrictions on mining operations in response to any such failure, increased monitoring costs and production costs, increased insurance costs or inability to obtain insurance, increased costs and/or limited access to capital, remediation costs, inability to comply with any additional safety requirements or obtain necessary certifications, evacuation or relocation of communities or other emergency action, and other impacts, which could have a material adverse effect on our operations and financial position.

Violence, including shooting incidents, civil and religious strife, and activism could result in loss of life and/or disrupt our operations and may adversely affect our business, financial condition, results of operations and prospects.

Indonesia has long faced separatist movements and civil and religious strife in a number of provinces. Several separatist groups have sought increased political independence for the province of Papua, where our Grasberg minerals district is located. In Papua, there have been sporadic attacks on civilians by separatists and sporadic but highly publicized conflicts between separatists and the Indonesia military and police. In addition, illegal miners have periodically clashed with police who have attempted for years to move them away from our facilities. Social, economic and political instability in Papua could materially and adversely affect us if it results in damage to our property or interruption of our Indonesia operations.

In 2009, a series of shooting incidents occurred within the PT-FI project area, including along the road leading to our mining and milling operations. The shooting incidents continued on a sporadic basis through January 2020. During this time, there were 22 fatalities and more than 75 injuries to our employees, contractor employees, government

security personnel and civilians. In addition, in December 2018, a mass shooting incident targeting a highway construction crew occurred in a remote mountain area approximately 100 miles east of the PT-FI project area, resulting in at least 19 fatalities and several reported as missing. During first-quarter 2020 and April 2020, there was an escalation in shooting incidents in PT-FI’s area of operations. In late March 2020, a shooting incident occurred near PT-FI’s administrative offices in the lowlands in Papua, Indonesia, resulting in the death of one PT-FI employee and injuries to two other workers. In January 2021, another shooting incident occurred when a helicopter operating under contract to PT-FI was struck by a single gunshot. Separatist security incidents, including shootings, continue to be sporadically reported, and PT-FI continues to monitor the occurrence of incidents in the region.

The safety of our workforce is a critical concern, and PT-FI continues to work with the Indonesia government to enhance security and address security issues within the PT-FI project area and in nearby areas. We continue to limit the use of the road leading to our mining and milling operations to secured convoys, including transport of personnel by armored vehicles in designated areas.

We cannot predict whether additional incidents will occur that could result in loss of life, disrupt or suspend our operations. If other disruptive incidents occur, they could adversely affect our results of operations and financial condition in ways that we cannot predict at this time.

South America countries have historically experienced uneven periods of economic growth, as well as recession, periods of high inflation and general economic and political instability. During 2019 and 2020, both Peru and Chile experienced significant and prolonged civil unrest unrelated to our operations. Production and sales for the third quarter and first nine months of 2019 were impacted by protests associated with an unaffiliated copper development project in Peru that blocked access to the shipping ports and main transportation routes. Although the civil unrest did not significantly impact our results for 2019, similar events in the future could cause, our South America operations to be materially impacted, in which case, we may not be able to meet our production and sales targets. We cannot predict whether similar or more significant incidents of civil unrest will occur in the future in Peru or Chile.

Our business depends on good relations with our workforce and labor disputes or labor unrest could disrupt our operations from time to time, which could adversely affect our financial results.