UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 20202023 |

OR

| | | | | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission File Number 1-10258

TREDEGAR CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Virginia | | 54-1497771 |

(State or other jurisdiction

of incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | | |

| 1100 Boulders Parkway, | | |

Richmond, | Virginia | | 23225 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: 804-330-1000

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock | TG | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | o | Accelerated filer | x | Smaller reporting company | | o |

| | | | | |

| Non-accelerated filer | | o | | Emerging growth company | | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

Aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 20202023 (the last business day of the registrant’s most recently completed second fiscal quarter): $406,328,122*$278,307,771*

Number of shares of Common Stock outstanding as of March 12, 2021:8, 2024: 33,537,89234,430,769

| | | | | |

| * | In determining this figure, an aggregate of 7,133,6347,361,458 shares of Common Stock beneficially owned by Floyd D. Gottwald, Jr., John D. Gottwald, William M. Gottwald, and James T. Gottwald and the members of their immediate families has been excluded because the shares are deemed to be held by affiliates. The aggregate market value has been computed based on the closing price in the New York Stock Exchange on June 30, 2020.2023. |

Documents Incorporated By Reference

Portions of the Tredegar Corporation Proxy Statement for the 20212024 Annual Meeting of Shareholders (the “Proxy Statement”) are incorporated by reference into Part III of this Form 10-K.

Index to Annual Report on Form 10-K

Year Ended December 31, 20202023

PART I

Item 1. BUSINESS

Description of Business

Tredegar Corporation (“Tredegar”) is engaged, through its subsidiaries, in the manufacture of aluminum extrusions, polyethylene (“PE”) plastic films and polyester (“PET”) films. Unless the context requires otherwise, all references herein to “Tredegar,” “the Company,” “we,” “us” or “our” are to Tredegar Corporation and its consolidated subsidiaries.

The Company's reportable business segments are Aluminum Extrusions, PE Films and Flexible Packaging Films.Films (also referred to as “Terphane”).

On October 30, 2020,September 1, 2023, the Company completed the sale of its personal care films business (“Personal Care Films”). The transaction excluded the packaging film lines and related operations located at the Pottsville, Pennsylvania manufacturing site (“Pottsville Packaging”), which are now being reported within the Surface Protection component of PE Films. Commencing in the third quarter of 2020, all historical results for Personal Care Films have been presented as discontinued operations.

In December 2020, the Companyannounced that it had entered into a definitive agreement and completedto sell Terphane to Oben Group (the “Contingent Terphane Sale”). Completion of the sale is contingent upon the satisfaction of Bright View Technologies (“Bright View”). The sale does not represent a strategic shift nor does it have a major effect oncustomary closing conditions, including the Company’s historicalreceipt of certain competition filing approvals by authorities in Brazil and ongoing operations, thus all financial information for Bright View has been presented as continuing operations. Bright View historically has been reported in the PE Films segment.

Columbia. For more information on these transactions, see Note 2 “Discontinued Operations”“Status of Current Corporate Strategic Initiatives - Agreement to the Consolidated Financial Statements includedSell Terphane” in Item 15. “Exhibits7. “Management’s Discussion and Analysis of Financial Statement Schedules”Condition and Results of Operations” of this Annual Report on Form 10-K for the year ended December 31, 2023 (“Item 15”Form 10-K”).

Aluminum Extrusions

Aluminum Extrusions, also referred to as Bonnell Aluminum, produces high-quality, soft-alloysoft and medium-strengthmedium strength alloyed aluminum extrusions, custom fabricated and finished, aluminum extrusions for the building and construction, automotive and transportation, consumer durables goods, machinery and equipment, electrical and renewable energy, and distribution markets. Bonnell Aluminum has manufacturing facilities located in the United States (“U.S.”).

Aluminum Extrusions manufactures mill (unfinished), machined, anodized and painted, (finished) and fabricatedthermally improved aluminum extrusions for sale directly to fabricators and distributors. It also manufactures and sells branded aluminum flooring trims under itsproduct lines: Futura TransitionsTM lineby Bonnell Aluminum (flooring trims) and aluminum framing systems under its TSLOTSTM line.by Bonnell Aluminum (structural aluminum framing systems). Aluminum Extrusions competes primarily on the basis of product quality, service and price. Sales are made predominantly in the U.S. The end-use markets for Aluminum Extrusions are cyclical and seasonal in nature.

The end-uses in each of Aluminum Extrusions’ primary market segments include: | | | | | | | | |

| Major Markets | | End-Uses |

| | |

| Building & construction (“B&C”)- nonresidential | | Commercial windows and doors, curtain walls, storefronts and entrances, automatic entry doors, walkway covers, ducts, louvers and vents, office wall panels, partitions and interior enclosures, acoustical walls and ceilings, point of purchase displays, pre-engineered structures, and flooring trims (Futura TransitionsTM)by Bonnell Aluminum) |

Building & constructionB&C - residential | | Residential windows and doors, shower and tub enclosures, railing and support systems, venetian blinds, and swimming pools |

Automotive and& transportation | | Automotive and light truck structural components, spare parts,battery enclosures for electric vehicles, after-market automotive accessories, grills for heavy trucks, travel trailers and recreation vehicles |

| Consumer durables | | Furniture,Office furniture, pleasure boats, refrigerators and freezers, appliances and sporting goods |

| Machinery & equipment | | Material handling equipment, conveyors and conveyingconveyor systems, medical equipment, industrial fans and aluminum framing systems (TSLOTSTM)by Bonnell Aluminum) |

| Distribution (metal service centers specializing in stock and release programs and custom fabrications to small manufacturers) | | Various custom profiles including storm shutters, pleasure boat accessories, theater set structures and various standard profiles (including rod, bar, tube and pipe) |

Electrical and& renewable energy | | Lighting fixtures, electronic apparatus, solar panel brackets and rigid and flexible conduits |

Aluminum Extrusions’ net sales (sales less freight) by market segment for the three years ended December 31, 20202023, 2022 and 2021 is shown below: | % of Aluminum Extrusions Net Sales by Market Segment | % of Aluminum Extrusions Net Sales1 by Market Segment | | % of Aluminum Extrusions Net Sales1 by Market Segment |

| | | 2020 | | 2019 | | 2018 | | 2023 | | 2022 | | 2021 |

| Building and construction: | |

| B&C: | |

| Nonresidential | |

| Nonresidential | |

| Nonresidential | Nonresidential | 56% | | 51% | | 51% | 56% | | 53% | | 50% |

| Residential | Residential | 9% | | 8% | | 8% | Residential | 8% | | 10% |

| Automotive | Automotive | 8% | | 9% | | 8% | Automotive | 10% | | 8% |

| Specialty: | Specialty: | |

| Consumer durables | Consumer durables | 10% | | 11% | | 12% |

| Consumer durables | |

| Consumer durables | | 8% | | 10% |

| Machinery & equipment | Machinery & equipment | 7% | | 7% | | 7% | Machinery & equipment | 9% | | 10% | | 8% |

| Electrical | Electrical | 4% | | 7% | | 7% | Electrical | 6% | | 4% | | 6% |

| Distribution | Distribution | 6% | | 7% | | 7% | Distribution | 3% | | 5% | | 8% |

| Total | Total | 100% | | 100% | | 100% | Total | 100% | | 100% |

| | | 1. The Company uses net sales as its measure of revenues from external customers at the segment level. For more business segment information, see Note 13 “Business Segments” to the Consolidated Financial Statements included in Item 15. “Exhibits and Financial Statement Schedules” of this Form 10-K (“Item 15”). | | 1. The Company uses net sales as its measure of revenues from external customers at the segment level. For more business segment information, see Note 13 “Business Segments” to the Consolidated Financial Statements included in Item 15. “Exhibits and Financial Statement Schedules” of this Form 10-K (“Item 15”). |

In 2020, 20192023, 2022 and 2018, nonresidential building and construction2021, Aluminum Extrusions net sales accounted for approximately 35%70%, 34%71% and 35%67% of Tredegar’s consolidated net sales, respectively.

Open Orders. Overall open orders in Aluminum Extrusions were approximately $48.0 million, or 14 million pounds, at December 31, 2023 compared to approximately $136.0 million, or 41 million pounds, at December 31, 2022, a decrease of $88.0 million, or approximately 65%. This level is below the quarterly range of 21 to 27 million pounds in 2019 before pandemic-related disruptions that resulted in long lead times, driving a peak in open orders of approximately 100 million pounds during the first quarter of 2022. We believe that current open orders are below pre-pandemic levels due to higher interest rates, tighter lender requirements and the increase in remote working, which particularly impacts the non-residential B&C end-use market. In addition, data indicates that aluminum extrusion imports increased significantly in recent years, especially during the pandemic, and some of Aluminum Extrusions’ customers may have sourced, and continue to source, aluminum extrusions from producers outside the U.S. Sales volume for Aluminum Extrusions, which the Company believes is cyclical and seasonal in nature due to its end-use markets, was 138.5 million pounds in 2023, 174.7 million pounds in 2022 and 183.4 million pounds in 2021.

Raw Materials. The primary raw materials used by Aluminum Extrusions consist of aluminum ingot, aluminum scrap and various alloys, which are purchased from domestic and foreign producers in open-market purchases and under annual contracts. Refer to Item 7A. "Quantitative and Qualitative Disclosures About Market Risk” of this Form 10-K (“Item 7A”) for additional information on aluminum price trends. Aluminum Extrusions believes that it has adequate supply agreements for aluminum and other required raw materials and supplies in the foreseeable future.2024.

PE Films

PE Films is composed ofproduces surface protection films, polyethylene overwrap films and films for other markets. Tredegar’s Surface Protection unit produces single- and multi-layer surface protection films sold under the UltraMask®, ForceField™, ForceField PEARL®, Pearl A™ and Pearl A™Obsidian™ brand names. These films, which are manufactured at facilities in the U.S. and China, support manufacturers of optical and other specialty substrates used in high-technology applications, most notably protecting high-value components of flat panel and flexible displays used in televisions, monitors, notebooks, smartphones, tablets, e-readers, automobilesdigital signage, semiconductors and digital signage,automobiles during the manufacturing and transportation process. The Obsidian™ series of products is designed for usage in automotive applications. In 2020, 20192023, 2022 and 2018, surface protection films2021, PE Films accounted for approximately 15%11%, 13%11% and 12%15% of Tredegar’s consolidated net sales, respectively.

In October 2020, the Surface Protection unit assumed responsibility for Pottsville Packaging, which was previously reported within the Personal Care component of PE Films. Pottsville Packaging produces thin-gauge films as overwrap for bathroom tissue and paper towels.

Raw Materials. The primary raw materials used by PE Films are polyethylene and polypropylene resins. These raw materials are obtained from domestic and foreign suppliers at competitive prices. Refer to Item 7A for additional information on resin price trends. PE Films believes that there will be an adequate supply of polyethylene and polypropylene resins in the foreseeable future.

Research and Development. Tredegar’s spending for research and development (“R&D”) activities in 2023, 2022 and 2021 was primarily related to PE Films. During the third quarter of 2023, the Company adopted a plan to close the PE Films technical center in Richmond, VA. Future R&D activities will be performed at the facility in Pottsville, PA. R&D spending by the PE Films was approximately $2.9 million, $5.3 million and $5.7 million in 2023, 2022 and 2021, respectively.

Customers. PE Films’ products are sold primarily in the U.S. and Asia, with the top four customers, collectively, comprising 84%, 86% and 86%87% of its net sales in 2020, 20192023 and 2018, respectively.88% in 2022 and 2021. No single PE Films customer exceeds 10% of Tredegar’s consolidated net sales. For additional information, see Item 1A. “Risk Factors” of this Form 10-K (“Item 1A”).

Flexible Packaging Films

Flexible Packaging Films is comprised of Terphane Holdings LLC (“Terphane”). Flexible Packaging Films produces PET-based films for use in packaging applications that have specialized properties, such as heat resistance, strength, barrier protection and the ability to accept high-quality print graphics. These differentiated, high-value films are primarily manufactured in Brazil and sold in Latin America and the U.S. under the Terphane®, Sealphane® and SealphaneEcophane® brand names. Major end uses include food packaging and industrial applications. Flexible Packaging Films competes in all of its markets on the basis of product quality, service and price. In 2023, 2022 and 2021, Terphane accounted for approximately 19%, 19% and 18% of Tredegar’s consolidated net sales, respectively.

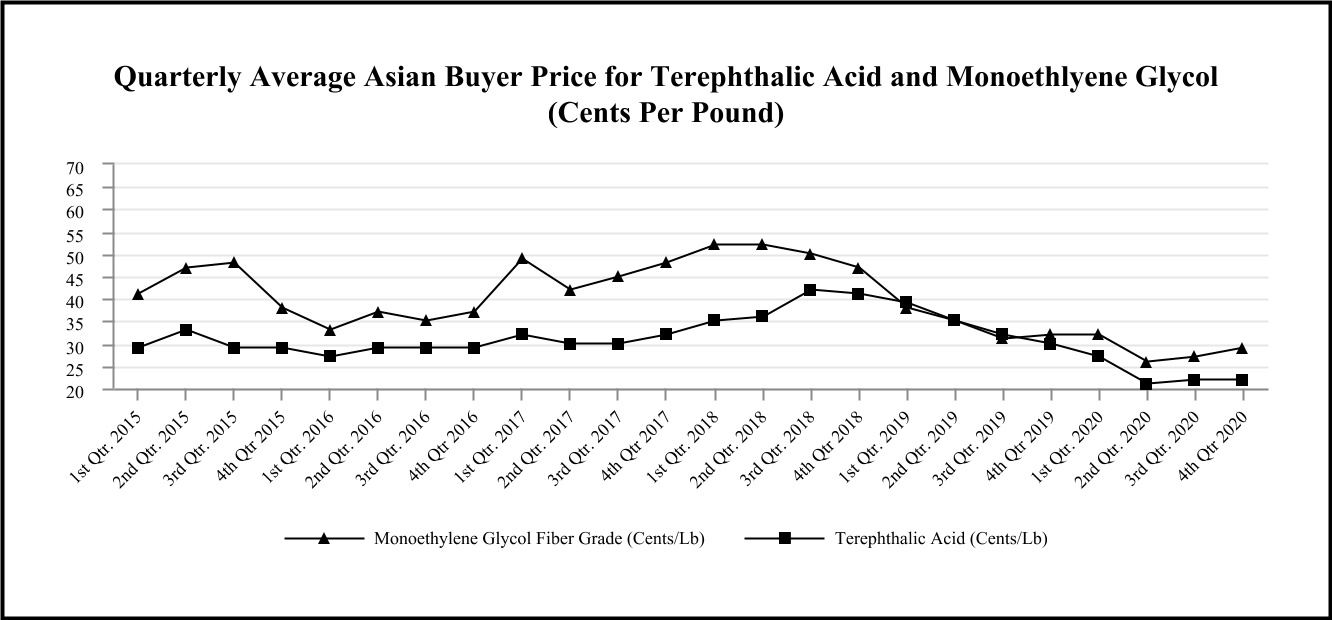

Raw Materials. The primary raw materials used by Flexible Packaging Films to produce polyester resins are purified terephthalic acid (“PTA”) and monoethylene glycol (“MEG”). Flexible Packaging Films also purchases additionalother polyester resins directly from suppliers. These raw materials are obtained from Brazilian and foreign suppliers at competitive prices. Flexible Packaging Films Terphane continues to monitor cost escalations to adjust selling prices as market dynamics permit and believes that there will be an adequate supply of polyester resins, PTA and MEG in the foreseeable future. Refer to Item 7A for additional information on resin price trends.

General

Intellectual Property. Tredegar considers patents, licenses and trademarks to be material to PE Films. On December 31, 2020,2023, PE Films held 5437 patents (including 46 U.S. patents), and 8266 registered trademarks (including 4 U.S. registered trademarks). Flexible Packaging Films held 1 U.S. patent and 1517 registered trademarks (including 24 U.S. registered trademarks). Aluminum Extrusions held no U.S. patents and 43 U.S. registered trademarks. As of December 31, 2020,2023, these patents had remaining terms of 3.50.5 to 15.517 years.

Research and Development. Tredegar’s spending for research and development (“R&D”) activities in 2020, 2019 and 2018 was primarily related to PE Films. R&D spending by the Company was approximately $8.4 million, $7.9 million and $6.7 million in 2020, 2019 and 2018, respectively.

Backlog. Overall backlog in Aluminum Extrusions was approximately $74.2 million at December 31, 2020 compared to approximately $52.8 million at December 31, 2019, an increase of $21.4 million, or approximately 41%. Backlogs are not material to the operations in PE Films or Flexible Packaging Films. Net sales for Aluminum Extrusions, which the Company believes are cyclical in nature, were $455.7 million in 2020, $529.6 million in 2019 and $573.1 million in 2018.

Government Regulation. The Company’s operations are subject to various local, state, federal and foreign government regulations, including environmental, privacy and anti-corruption and anti-bribery laws and regulations.

U.S. laws concerning the environment to which the Company’s domestic operations are or may be subject to include the Clean Water Act, the Clean Air Act, the Resource Conservation and Recovery Act, the Occupational Safety and Health Act, the National Environmental Policy Act, the Toxic Substances Control Act, the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), regulations promulgated under these acts, and other federal, state or local laws or regulations governing environmental matters. Compliance with these laws is an important consideration because Tredegar uses hazardous materials in some of its operations, is a generator of hazardous waste, and wastewater from the Company’s operations is discharged to various types of wastewater management systems. Under CERCLA and other laws, Tredegar may be subject to financial exposure for costs associated with waste management and disposal, even if the Company fully complies with applicable environmental laws.

The U.S. Environmental Protection Agency has adopted regulations under the Clean Air Act relating to emissions of carbon dioxide and other greenhouse gases (“GHG”), including mandatory reporting and permitting requirements. Several of the Company’s manufacturing operations result in emissions of carbon dioxide or GHG and are subject to the current GHG regulations. The Company’s compliance with theseenvironmental regulations has yet to require significant capital expenditures; however, environmental standards tend to become more stringent over time. Therefore, in order to comply with current or future environmental legislation or regulations, the Company may be subject to additional capital expenditures, operating expenses or other compliance costs, the amounts and timing of which are not presently determinable, but which could be significant, including constructing new facilities or modifying existing facilities.

For further discussion regarding certain privacy and anti-corruption and anti-bribery laws and regulations to which the Company is subject, see Item 1A. Risk Factors below. Like environmental regulations, current or future privacy and anti-corruption and anti-bribery legislation or regulations may subject the Company to additional capital expenditures, operating expenses or other compliance costs, the amounts and timing of which are not presently determinable but could be significant. Finally, anyAny failure to comply with current or future laws and regulations, including environmental, privacy and anti-corruption and anti-bribery laws and regulations, could subject Tredegar to substantial penalties, fines, costs and expenses. For further discussion regarding certain environmental, privacy and anti-corruption and anti-bribery laws and regulations to which the Company is subject, see Item 1A below.

Human Capital Management.

Overview

Tredegar employed approximately 2,4001,900 people at December 31, 20202023 located in the U.S., Brazil, and Asia.Asia, of which 75% are located in the U.S. Approximately 34%15% of the Company’s employees are represented by labor unions located in the U.S. and Brazil under various collective bargaining agreements with varying durations and expiration dates.dates, none of which expire before 2025. All of Tredegar’s Brazilian employees are represented by a national labor union. Generally, the total number of employees of Tredegar does not significantly fluctuate throughout the year. However, acquisition or divestiture activity, or changes in the level of business activity may impact employee levels.

Health and Safety

Tredegar has continuously exceeded the industry standards for safety in each of its respective manufacturing sectors. The Company uses various forms of employee safety metrics to assess the health and safety performance of its Aluminum Extrusions, PE Films and Flexible Packaging operations, including employee safety data which is available on the Company’s website at www.tredegar.com/about-tredegar/our-broader-commitments/committed-to-our-employees/.

Additionally, Aluminum Extrusions has on-site health clinics at its Carthage and Clearfield facilities. These clinics allow Aluminum Extrusions to invest in its people, provide more personal and more thorough healthcare to employees, and enhance the employer-employee relationship. Collectively, the Carthage and Clearfield clinics serve over 600 employees.

Talent and Development

The Company believes its employees are its most valuable asset and are critical to the success of the Company. The Company seeks to retain employees by offering competitive wages, benefits and training opportunities. To assess and monitor employee retention and engagement, the Company surveys employees and takes actions to address areas of employee concern. The annual employee engagement survey results are presented to Tredegar’s Board of Directors (“Board”). Additionally, the objectives of our executive compensation programs are to attract, motivate and retain highly qualified executive officers. To accomplish these objectives, the Company relies on a pay strategy that emphasizes performance-based compensation through annual and long-term incentives. The Company believes that this pay strategy creates a strong link between pay and performance and aligns with our business strategy of generating strong operating results and shareholder value creation while controlling fixed costs.

The Company is committed to holistically supporting our employees both at work and in their communities by:

•Strictly following all applicable health, safety and non-discrimination laws in each country;

•Promoting the highest standards for employee health and safety through innovative programs; and

•Providing opportunities for community outreach and supporting programs that enhance the lives of children and families.

Inclusion and Diversity

Tredegar strictly complies with all applicable state, local and international laws governing nondiscrimination in employment in every location where Tredegar and its businesses have facilities to ensure healthy and positive working conditions. This applies to all terms and conditions of employment, including recruiting, hiring, job assignments, promotion, termination, layoff, recall, transfer, leaves of absence, compensation and training. All applicants and employees are treated with the same high level of respect regardless of their race, creed, color, religion, sex, sexual orientation, gender identity, age, pregnancy, national origin, ethnicity, political affiliation, union membership, marital status, citizenship status, veteran status, disability or other protected category. Employees who experience or witness discriminatory behavior are encouraged to report such behavior to their supervisor, Human Resources or Tredegar’s toll-free anonymous reporting hotline. Additionally, the Company spends significant resources in developing its employees. Among the five core principles of the “The Tredegar Way” that the Company uses to guide its organization, the “Leadership” principle is focused on building a team of motivated and engaged leaders at every level of the Company. Each business unit has identified specific action plans to promote the Leadership

principle among its employees. Action plans include talent development, skills training, reinforcement of strong cultural values, and robust systems to ensure a safe working environment.

The Company seeks to retain employees by offering competitive wages, benefits and training opportunities. To assess and monitor employee retention and engagement, the Company surveys employees and takes actions to address areas of employee concern. The annual employee engagement survey results are presented to Tredegar’s Board of Directors (“Board”). Additionally, the objectives of our executive compensation programs are to attract, motivate and retain highly qualified executive officers. To accomplish these objectives, we rely on a pay strategy that emphasizes performance-based compensation through annual and long-term incentives. We believe that this pay strategy creates a strong link between pay and performance and aligns with our business strategy of generating strong operating results and shareholder value creation while controlling fixed costs.

We are committed to holistically supporting our employees both at work and in their communities by:

•Strictly following all applicable health, safety and non-discrimination laws in each country;

•Promoting the highest standards for employee health and safety through innovative programs; and

•Providing opportunities for community outreach and supporting programs that enhance the lives of children and families.

The Company uses various forms of employee safety metrics to assess the health and safety performance of its Aluminum Extrusions, PE Films and Flexible Packaging operations, including employee safety data which is available on its website at https://tredegar.com/about-tredegar/committed-to-our-employees. Tredegar has also instituted additional safety precautions during the ongoing COVID-19 pandemic as described in "The Impact of COVID-19" included in Item 7. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" of this Form 10-K (“Item 7”).

Information About Our Executive Officers. See Item 10. “Directors, Executive Officers and Corporate Governance” of this Form 10-K.

Available Information and Corporate Governance Documents. Tredegar’s website address is www.tredegar.com. The Company makes available, through its website, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). Information filed electronically with the SEC can be accessed on its website at www.sec.gov. In addition, the Company’s Corporate Governance Guidelines, Code of Conduct, the

charters of the Audit, Executive Compensation, and Nominating and Governance Committees and Climate Change Risk Assessment and many other corporate policies are available on Tredegar’s website and are available in print to any shareholder upon request by contacting Tredegar’s Corporate Secretary at 1100 Boulders Parkway, Richmond, Virginia 23225. The information on or that can be accessed through the Company’s website is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K for the year ended December 31, 2020 (“Form 10-K”) or incorporated into other filings it makes with the SEC.

Forward-looking and Cautionary Statements

Some of the information contained in this Form 10-K may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. When the Company uses the words “believe,” “estimate,” “anticipate,” “appear to,” “expect,” “project,” “plan,” “likely,” “may” and similar expressions, it does so to identify forward-looking statements. Such statements are based on the Company's then current expectations and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those addressed in the forward-looking statements. It is possible that the Company's actual results and financial condition may differ, possibly materially, from the anticipated results and financial condition indicated in or implied by these forward-looking statements. Accordingly, you should not place undue reliance on these forward-looking statements. For risks and important factors that could cause actual results to differ from expectations, refer to the reports that Tredegar files with or furnishes the SEC from time-to-time, including the risks and important factors set forth in Item 1A. Readers are urged to review and consider carefully the disclosures Tredegar makes in the reports Tredegar files with or furnishes to the SEC. Tredegar does not undertake, and expressly disclaims any duty, to update any forward-looking statement to reflect any change in management’s expectations or any change in conditions, assumptions or circumstances on which such statements are based, except as required by applicable law.

Item 1A. RISK FACTORS

There are a number of risks and uncertainties that could have a material adverse effect on the Company’s businesses and its consolidated financial condition, results of operations or cash flows. The following risk factors should be considered, in addition to the other information included in this Form 10-K, when evaluating Tredegar and its businesses.

Risks Related to Tredegar’s Corporate Strategic Initiatives and Indebtedness

•The planned divestiture of Terphane to Oben Group is subject to a number of conditions beyond our control. On September 1, 2023, the Company announced that it had entered into a definitive agreement to sell Terphane to Oben Group. Completion of the sale is contingent upon the satisfaction of customary closing conditions, including the receipt of certain competition filing approvals by authorities in Brazil and Colombia. On October 27, 2023, the Company filed the requisite competition forms with the Administrative Council for Economic Defense (“CADE”) in Brazil, which the Company views as the primary competition authority regarding this matter. This filing followed a pre-filing phase for CADE’s initial review. CADE’s maximum deadline for completing its review is no later than November 18, 2024. The merger review regarding the transaction was cleared by the Colombian authority in early February 2024.

As usual, it cannot be predicted with certainty whether all of the required closing conditions will be satisfied, waived or if other uncertainties may arise. While the regulatory review process is ongoing and in line with the Company’s expectations, regulators could impose additional requirements or obligations as conditions for their approval, which may be burdensome. If such closing conditions are not met or additional obligations are imposed, the proposed sale may not be consummated, encounter delays, or experience other issues that are not currently anticipated.

•The Company’s failure to successfully transition to the reporting requirements for its asset-based revolving credit facility (“ABL Facility”), which matures on June 30, 2026, or an unexpected downturn in the markets could adversely impact the Company’s financial position and results of operations. On December 27, 2023, the Company entered into the ABL Facility, which provides the Company with $180 million senior secured asset-based revolving credit facility that will expire on June 30, 2026. The ABL Facility amended the Company’s existing $200 million revolving, secured credit facility that was cash flow-based. Availability under the ABL Facility is governed by a borrowing base, determined by the application of specified advance rates against eligible assets, including a portion of trade accounts receivable, inventory, cash and cash equivalents, owned real properties, and owned machinery and equipment.

A number of factors could affect the Company’s ability to successfully complete its transition from its prior cash flow-based revolving credit facility to the current asset-based facility. These factors include:

•Failure to establish processes associated with the ABL Facility’s reporting requirements, which are currently on a monthly basis but could change to a weekly cadence if at any time the borrowing availability falls below 10% of the maximum aggregate principal amount. Failure to timely report could result in an Event of Default (as defined in the ABL Facility), which if not waived, would permit the lenders, at their option, to accelerate all outstanding debt under the ABL Facility. Should the lenders elect to accelerate the debt under the ABL Facility,

a cross-default would be triggered under the Terphane Brazil Loan (as defined below in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Form 10-K (“Item 7”)).

•Because the Company is currently subject to a Cash Dominion Period (as defined in Item 7), it is required to borrow cash to fund working capital, capital expenditures, business development activity, and other general corporate purposes, which limits its financial flexibility;

•Advances on accounts receivable and inventory are subject to change based on periodic commercial finance examinations and appraisals, and the real property, machinery and equipment values included in the borrowing base are subject to change based on periodic appraisals, which could reduce borrowing availability under the ABL Facility; and

•If a Material Adverse Effect (as defined in the ABL Facility) has occurred, the Company will not be able to continue to borrow under the ABL Facility.

In addition, a significant deterioration in the Company’s accounts receivable or inventory levels due to depressed economic conditions, weak consumer spending, turmoil in the credit markets or other factors, could restrict its ability to service its indebtedness or borrow additional funds.

Upon the earlier of March 31, 2025 or the date the Company receives the proceeds from the Contingent Terphane Sale (the “ABL Adjustment Date”), borrowing availability under the ABL Facility will be reduced from $180 million to $125 million. If the Contingent Terphane Sale is not completed by the ABL Adjustment Date, the Company may have to undertake alternative financing plans, subject to the limitations imposed by the ABL Facility, including limitations on its ability to:

•refinance or restructure its indebtedness;

•sell assets; and

•raise additional capital.

The Company may be unable to implement alternative financing plans on commercially reasonable terms or at all, and any such alternative financing plans might be insufficient to allow it to make principal and interest payments on its indebtedness required as a result of the ABL Adjustment Date and the reduction of borrowing availability under the ABL Facility to $125 million. The Company’s ability to restructure or refinance its indebtedness will depend on, among other things, its existing financial condition, projections of business conditions, sales, Credit EBITDA, net cash flow, net leverage and the condition of the capital markets at such time. Any refinancing of the Company’s indebtedness could be at higher interest rates and could require it to comply with additional covenants, which could further restrict the Company’s business operations.

Noncompliance with any of the covenants of the ABL Facility could result int an Event of Default, which if not cured or waived, would permit the lenders, at their option, to accelerate all outstanding debt under the ABL Facility.

Risks Related to All Tredegar’s Businesses

•Recent macroeconomic factors, including inflation, high interest rates, recession risks and other lagging effects of the COVID-19 pandemic, have caused downturns in key markets and created other commercial disruptions, which have and could further adversely impact our businesses.Products sold to key end-use markets, including the B&C and consumer electronics markets, represent a significant portion of our revenue. Because these markets are tied closely to overall economic performance, macroeconomic factors have and could further cause changes to demand for our products. These factors include: (i) inflation; (ii) high interest rates; (iii) recession risks; (iv) disruptions to supply chains; (v) other interruptions of international and regional commerce; and (vi) other lagging effects of the COVID-19 pandemic. Price erosion may occur as competitors become more aggressive in pricing practices. To the extent that these factors reduce demand for our products, our business, financial position, results of operations and cash flows could be adversely impacted.

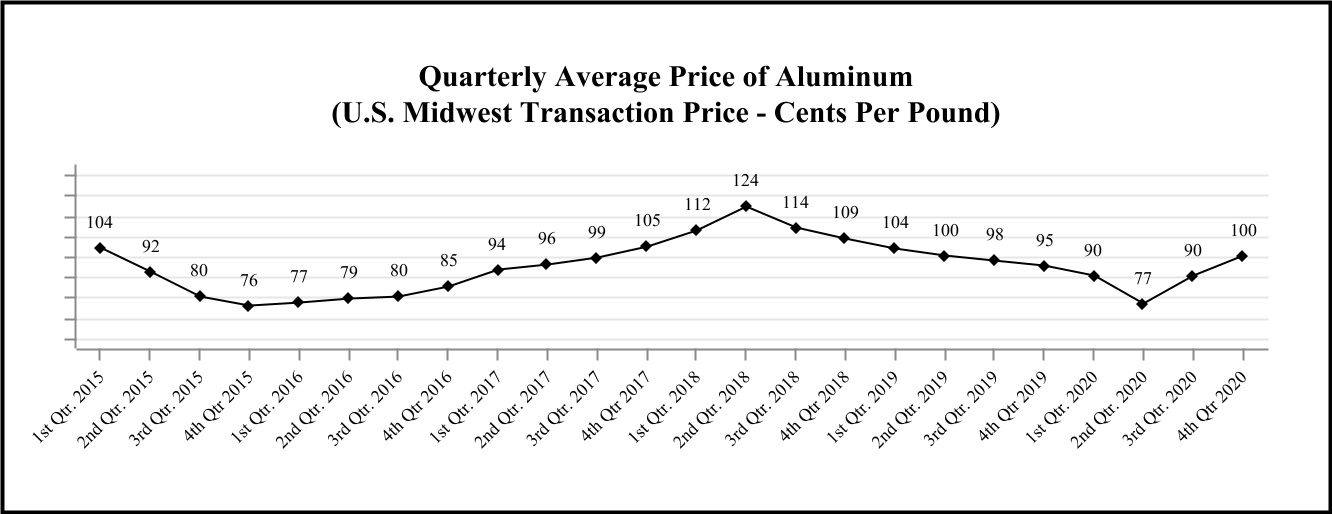

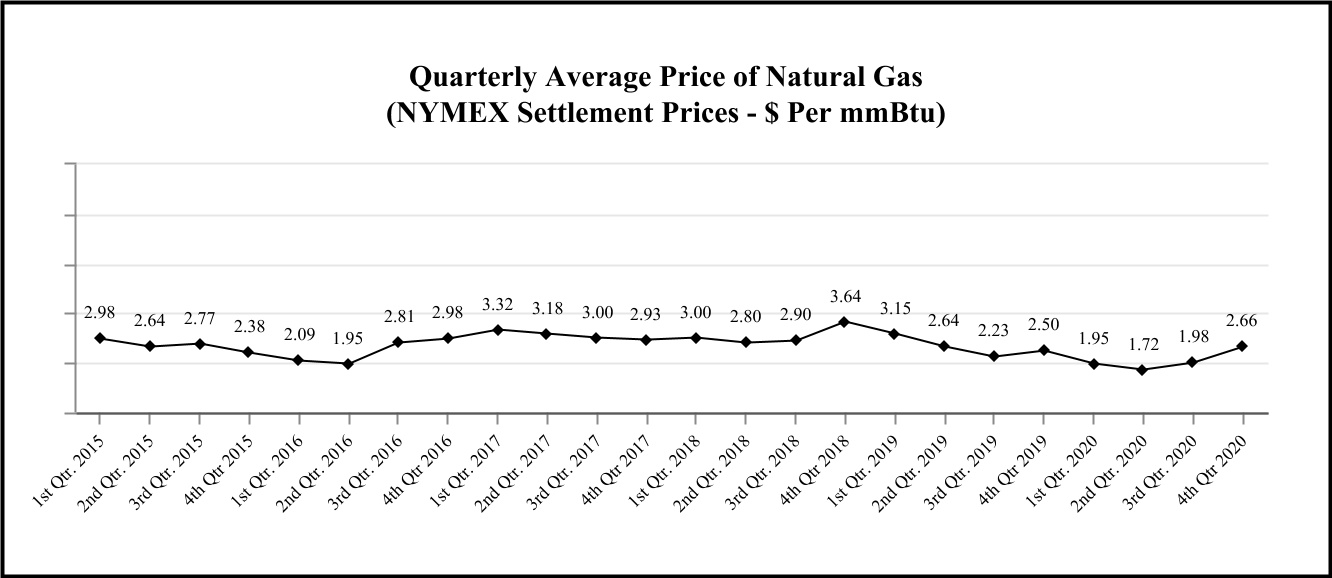

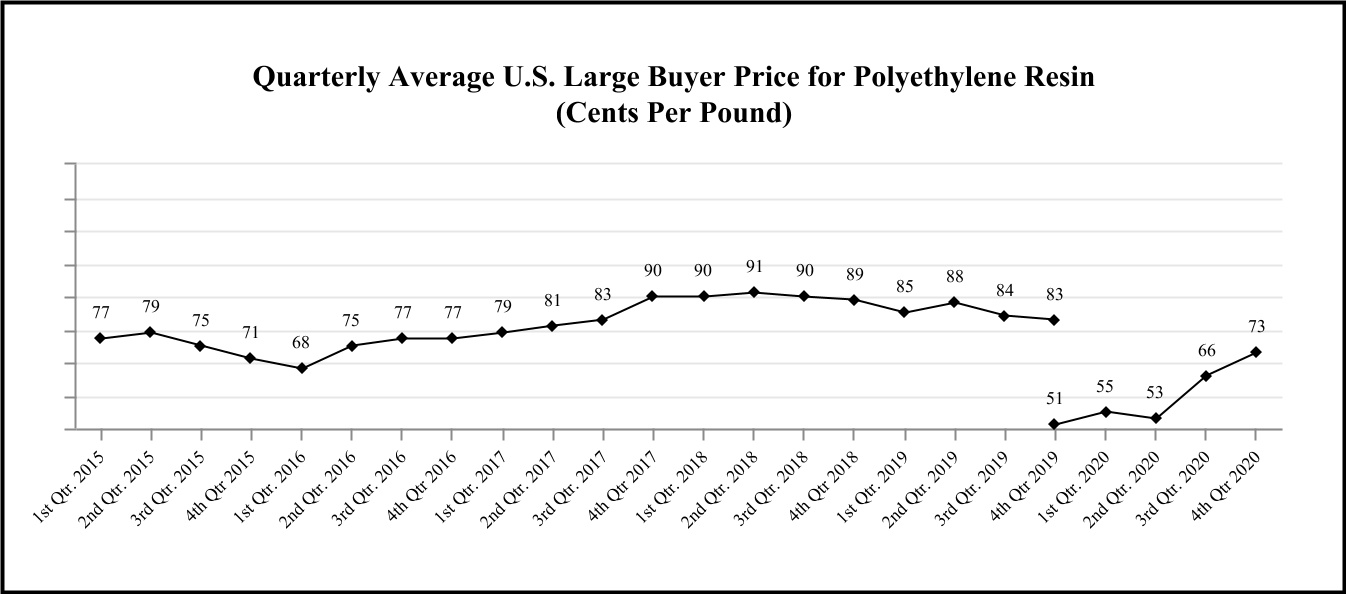

•Tredegar’s performance is influenced by costs incurred by its operating companies, including the cost of raw materials and energy. These costs include the cost of aluminum (the raw material on which Aluminum Extrusions primarily depends), resin (the raw material on which PE Films primarily depends), PTA and MEG (the raw materials on which Flexible Packaging Films primarily depends), natural gas (the principal fuel necessary for Aluminum Extrusions’ plants to operate), electricity, diesel fuel and paint. Aluminum, resin and natural gas prices are volatile as shown in the charts in Item 7A. The Company attempts to mitigate the effects of increased costs through price increases and contractual pass-through provisions, but there are no assurances that higher prices can effectively be passed through to customers or that Tredegar will be able to offset fully or on a timely basis the effects of higher costs. Further, the Company’s cost control efforts may not be sufficient to offset any increases in raw materials, energy or other costs.

•Our failure to continue to attract, develop and retain certain key officers or employees could adversely affect our businesses. Our success depends upon the efforts and abilities of key personnel, many of whom are longstanding employees. The loss of any of these key personnel could deplete our institutional knowledge base and negatively affect our ability to efficiently operate our businesses. Certain roles have experienced high turnover in recent years, and we are experiencing an increasingly competitive labor market. Increased employee turnover could hinder our ability to execute our business strategy and adversely affect our business, financial condition, results of operations and cash flows.

•Disruptions at one of the Company’s major manufacturing facilities could negatively impact financial results. Tredegar believes it has implemented measures to minimize the risks of disruption at its facilities. However, a disruption could occur as a result of any number of events: an equipment failure with repairs requiring long lead times, labor stoppages or shortages, cybersecurity attacks, utility disruptions, constraints on the supply or delivery of critical raw materials, and severe weather conditions, including potential flooding at the Aluminum Extrusions facility located in Carthage, TN, which is located in a 50-year flood plain. A material disruption in one of the Company’s operating locations could negatively impact production and the Company’s consolidated financial condition, results of operations and cash flows.

Risks Related to Aluminum Extrusions

•Sales volume and profitability of Aluminum Extrusions is cyclical and seasonal and highly dependent on economic conditions of end-use markets in the U.S., particularly in the construction sector. Aluminum Extrusions’ end-use markets can be cyclical and subject to seasonal swings in volume, and have been adversely impacted duringvolume. In addition, changes in architectural design, demographic, and/or remote work trends could negatively impact the coronavirus pandemic (“COVID-19”).overall commercial construction industry. Because of the capital intensivecapital-intensive nature and level of fixed costs inherent in the aluminum extrusions business, the percentage drop in earnings before interest, taxes, depreciation and amortization (“EBITDA”) from ongiongongoing operations in a cyclical downturn will likely exceed the percentage drop in volume. In addition, during an economic slowdown, excess industry capacity often drives increased pricing pressure in many end-use markets as competitors seek to protect their position with key customers. Any benefits associated with cost reductions and productivity improvements may not be sufficient to offset the adverse effects on profitability from pricing and margin pressure and higher bad debts (including a greater chance of loss associated with customers defaulting on fixed-price forward sales contracts) that usually accompany a downturn. In addition, higher energy costs can reduce profits unless offset by price increases or cost reductions and productivity improvements.

•Failure to prevent competitors from evading anti-dumping and countervailing duties, or a reduction in such duties, could adversely impact Aluminum Extrusions. Effective April 25, 2017, the anti-dumping duty and countervailing duty orders onUnfairly traded imports of aluminum extrusions were extended for a period of five years. The orders will be reviewed again beginning in

March 2022. Chinese and other overseas manufacturers continue to try to evade the anti-dumping and countervailing orders to avoid duties. A failure by,could injure or the inability of, U.S. trade officials to curtail the evasion of these duties, or the potential reduction of applicable duties pursuant to annual administrative reviews of the orders by the Department of Commerce,threaten with injury America’s domestic aluminum extrusions industry, which could have a materialan adverse effect on the financial condition, results of operations and cash flows of Aluminum Extrusions.

•1.Failure to prevent foreign competitors from evading anti-dumping and countervailing duties, or failure to reinstate the Aluminum Tariff on aluminum extrusions, could adversely impact Aluminum Extrusions. In 2018, the U.S. imposed tariffs of 10% on aluminum ingot and semi-finished aluminum imported into the U.S. from certain countries; however, in December 2020, the Department of Commerce (“DOC”) introduced a tariff exclusion process, granting applicants with tariff exclusions. In response to large and increasing volumes of unfairly traded imports of extrusions associated with these tariff exclusions, a coalition of U.S. domestic producers filed petitions with the DOC and U.S. International Trade Commission (“ITC”). In November 2023, the ITC found that there is a reasonable indication that the American aluminum extrusions industry is materially injured or threatened with injury due to imports from 14 countries, including China. The ITC’s preliminary determination found that subject import volumes were significant and increasing, and that with regard to pricing, subject imports predominantly undersold the domestic product by volume in each year of the period of investigation. On March 5, 2024, the DOC announced its preliminary finding that the governments of China, Indonesia, Mexico and Turkey unfairly subsidize their aluminum extrusion industries. The DOC calculated a range of affirmative preliminary countervailing duties from each country. A preliminary anti-dumping determination for these four countries and the 10 other countries included in the initial petition is expected in May 2024. The Company expects the final ITC vote to occur in late 2024. A failure by, or the inability of, U.S. trade officials to restore the import tariff in its full format could have an adverse effect on the businesses, financial condition, results of operations and cash flows of Aluminum Extrusions.

2.The duty-free importation of goods allowed under the United States-Mexico-Canada Agreement (“USMCA”), or other free trade agreements or duty-preference regimes, could result in lower demand for aluminum extrusions made in the U.S., which could materially and negatively affect Bonnell Aluminum’s business and results of operations. InAs noted above, in March 2018, the U.S. imposed tariffs of 10% on aluminum ingot and semi-finished aluminum imported ininto the U.S. from certain countries, including countries from which Bonnell Aluminum Extrusions has historically sourced aluminum products. In September 2019, the U.S., Canada and Mexico entered into the USMCA. As a result of the 10% tariffs on aluminum ingot imported to the U.S. and the duty-free importation of goods allowed under USMCA, aluminum extrusions made in Canada and Mexico that are able to take advantage of duty-preference programs upon importation into the United States are free of the

10% tariff and can now be imported into and sold in the U.S. at very competitive prices. This could result in lower demand for aluminum extrusions made in the U.S., which could materially and negatively affect Bonnell Aluminum’s business and results of operations.

•Competition from China could increase significantly if China is granted market economy status by the World Trade Organization. China launched a formal complaint to the World Trade Organization (“WTO”) challenging its non-market economy status, claiming that as of December 11, 2016, China’s transition period as a non-market economy under its Accession Protocol to the WTO ended. China believes with respect to all Chinese-made products that it should receive market economy status and the rights attendant to that status under WTO rules. The U.S. and the European Union have each rejected that interpretation. If China is granted market economy status by the WTO, the extent to which the U.S. anti-dumping laws will be able to limit unfair trade practices from China will likely be limited because the U.S. government will be forced to utilize Chinese prices and costs that do not reflect market principles in anti-dumping duty investigations involving China, which could ultimately limit the level of anti-dumping duties applied to unfairly traded Chinese imports. The volume of unfairly traded imports of Chinese aluminum extrusions could increase as a result and this, in turn, would likely create substantial pricing pressure on Aluminum Extrusions’ products and could have a material adverse effect on the financial condition,business, results of operations, financial condition and cash flows of Aluminum Extrusions. In June 2019, at China’s request, after certain preliminary rulings in the case went against the Chinese position, the WTO indefinitely suspended the proceedings on the Chinese WTO complaint.flows.

•The markets for Aluminum Extrusions’ products are highly competitive with product quality, service, delivery performance and price being the principal competitive factors. Aluminum Extrusions has approximately 1,4501,100 customers that are in a variety of end-use markets within the broad categories of building and construction, distribution, automotive and other transportation, machinery and equipment, electrical and consumer durables. No single Aluminum Extrusions’ customer exceeds 4% of consolidated net sales. Future success and prospects depend on Aluminum Extrusions’ ability to provide superior service, high quality products, timely delivery and competitive pricing to retain existing customers and participate in overall industry cross-cycle growth. Failure in any of these areas could lead to a loss of customers, which could have an adverse material effect on the business, financial condition, results of operations and cash flows of Aluminum Extrusions.

•The failure to successfully implement the new enterprise resource planning and manufacturing execution systems could adversely impact the Aluminum Extrusions business and results of operations. InJanuary 2022, Aluminum Extrusions commenced the implementation of new enterprise resource planning and manufacturing execution systems (“ERP/MES”) across all locations of the Aluminum Extrusions business. The implementation of these systems is a major undertaking from a financial, management, and personnel perspective. The implementations have been more difficult, time consuming and costly (approximately $21 million of spending to date) than expected. This project, which was expected to be completed in 2024, has been reorganized with an extended implementation period, due to the implementation of stringent spending measures to control financial leverage. As a result, the earliest “go-live” date for the new ERP/MES is 2025. There can be no assurance that these systems will be beneficial to the extent anticipated. Any additional disruptions, delays or deficiencies in the design and implementation of the new systems could adversely affect our financial position, results of operations and cash flows.

Risks Related to PE Films

•PE Films is highly dependent on sales associated with relatively few large customers. PE Films’ top four customers comprised approximately 16%10%, 14%10% and 13% of Tredegar’s consolidated net sales in 2020, 20192023, 2022 and 2018,2021, respectively. The loss or significant reduction of sales associated with one or more of these customers without replacement by new business could have a materialan adverse effect on the Company.

Additionally, PE Films anticipates that a portion Surface Protection sales have been adversely impacted by weak market demand and competitive pricing. Customer demand for electronics has continued to deteriorate since the third quarter of its film products used2022, causing manufacturers in surface protection applications could be made obsolete by possible future customer product transitionsthe supply chain to less costly alternative processes or materials. These transitions principally relate to one customer. The Company believes that previously reported delays in this customer's transitions were recently resolved by the customerexperience reduced capacity utilization and muchinventory corrections. Consequently, results of the remaining transitions could occur by the end of 2021. Under this scenario, the Company estimates that the contribution to EBITDA from ongoing operations for PE Films could decline due to the remaining customer product transitionshave been adversely impacted by $18 million in 2021 versus 2020 and $4 million in 2022 versus 2021. To offset the expected adverse impact, the Company is aggressively pursuing and making progress in generating contribution from sales from new surface protection products, applications and customers and implementing cost savings measures. Annual contribution to EBITDA from ongoing operationsweak demand for PE Films on surface protection products unrelated to the customer product transitions has increased since 2018 by approximately $12 million.Surface Protection products.

While PE Films is undertaking efforts to expand its customer base, there can be no assurance that such efforts will be successful, or that they will offset any loss of sales and profits associated with customer transitions and other large customer declines.

•FailureThe failure of PE Films’ customers who are subject to cyclical downturns, to achieve success or maintain market share could adversely impact PE Films’ sales and operating margins. PE Films’ plastic films are used in the production of various consumer products sold worldwide. A customer’sOur customers’ ability to successfully develop, manufacture and market those products is integral to PE Films’ success. Cyclical downturns and changing consumer preferences, particularly those driven by changes in technology, may negatively affect businesses that use PE Films’ plastic film products, which could adversely affect sales and operating margins. Other factors that could adversely affect the business include (i) failure by a key customer to achieve success or maintain share in markets in which they sell products containing PE Films’ materials, including as a result of customer preferences for products other than plastics, (ii) key customers using products developed by others that replace PE Films’ business with such customers, (iii) delays in a key customer rolling out products utilizing new technologies developed by PE Films, and (iv) operational decisions by a key customer that result in component substitution, inventory reductions and similar changes.

•The Company’s inability to protect its intellectual property rights or its infringement of the intellectual property rights of others could have a materialan adverse impact on PE Films. The continued success of the PE Films’ business depends on its ability not only to protect its own technologies and trade secrets, but also to develop and sell new products that do not infringe upon existing patents. Intellectual property litigation is very costly and could result in substantial expense and diversions of Company resources, both of which could adversely affect its consolidated financial condition, results of operations and cash flows. In addition, there may be no effective legal recourse against infringement of the Company’s intellectual property by third parties, whether due to limitations on enforcement of rights in foreign jurisdictions or as a result of other factors.

•Disruptions to PE Films’ supply chain could have a material adverse impact on PE Films. Certain raw materials used in manufacturing PE Films’ products are sourced from single suppliers, and PE Films may not be able to quickly or inexpensively re-source from other suppliers. The risk of damage or disruption to its supply chain may increase if and when different suppliers consolidate their product portfolios, experience financial distress or disruption of manufacturing operations (such as, for example, the impact of hurricanes on petrochemical production). Failure to take adequate steps to effectively manage such events, which are intensified when a product is procured from a single supplier or location, could adversely affect PE Films’ consolidated financial condition, results of operations and cash flows, and also require additional resources to restore its supply chain.

•Rising trade tensions could cause an increase in the cost of PE Films’ products or otherwise negatively impact the Company. A portion of PE Film’s business involves imports to and from the U.S. and other countries where the

Company produces and sells its products. Trade tensions have been rising between the U.S. and other countries, particularly China. An increase in tariffs and other trade barriers between the U.S. and China, or between the U.S. and other countries, could cause an increase in the cost of PE Films’ products or otherwise negatively impact the production and sale of the Company’s products in world markets.

•Further impairment of the Surface Protection reporting unit’s goodwill could have a non-cash adverse impact on our results of operations. The Company assesses goodwill for impairment when events or circumstances indicate that the carrying value may not be recoverable, or, at a minimum, on an annual basis (December 1st of each year). The valuation of goodwill depends on a variety of factors, including macroeconomic conditions, industry and market considerations, cost factors and overall financial performance, as well as Company and reporting unit factors, and goodwill impairment valuations can be sensitive to assumptions associated with such factors. Failure to successfully achieve projections could result in future impairments.

Risks Related to Flexible Packaging Films

•Overcapacity in Latin American polyester film production and governmental failure to extend anti-dumping duties in Brazil on imported products or prevent competitors from circumventing such duties could adversely impact Flexible Packaging Films. In recent years, excess global capacity in the industry has led to increased competitive pressures from imports into Brazil. The Company believes that these conditions have shifted the competitive environment from a regional to a global landscape and have driven price convergence and lower product margins for Flexible Packaging Films. Favorable anti-dumping rulings or countervailing duties are in effect for products imported from China, Egypt, India, Mexico, United Arab Emirates, Peru and Bahrain. Competitors not currently subject to anti-dumping duties may choose to utilize their excess capacity by selling product in Brazil, which may result in pricing pressures that Flexible Packaging Films may not be able to offset with cost savings measures and/or manufacturing efficiency initiatives.

In May 2021, the Brazilian authorities concluded the sunset review relating to the anti-dumping process for polyester film imported from China, India and Egypt, and decided to extend duties for another five years. However, due to its doubts that films would continue to be imported from China and Egypt, the government immediately suspended the implementation of the tariffs for those countries but agreed that if in the future there were volumes imported from China or Egypt which were harming the Brazilian market, authorities may promptly reinstate tariffs. Importing from Egypt increased in Brazil during 2023; therefore, Terphane requested the application of anti-dumping tariffs for Egypt, which was accepted by the Brazilian Government. These tariffs went into effect starting in November 2023. For films imported from India, the Brazilian authorities also reviewed measures against countervailing duties and extended those for five years as well.

In February 2024, the Brazilian Government determined that the anti-dumping measures against Mexico and United Arab Emirates should be extended for a five-year period and anti-dumping measures against Turkey should be removed.

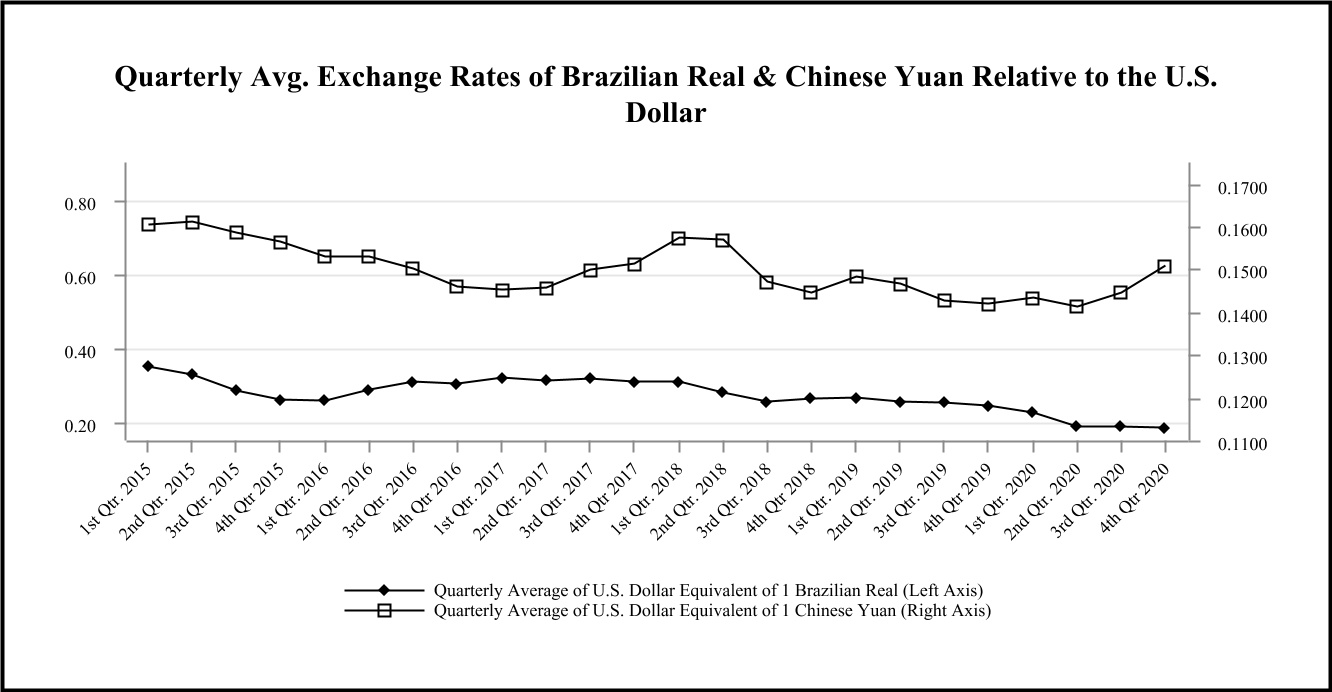

•A history of uncertain economic conditions in Brazil could adversely impact the financial condition, results of operations and cash flows of Flexible Packaging Films. For flexible packaging films produced in Brazil, selling prices and key raw material costs are principally determined in U.S. Dollars and are impacted by local economic conditions and local and global competitive dynamics. Flexible Packaging Films is exposed to foreign exchange translation risk (its functional currency is the Brazilian Real) because almost 90% of the sales of Flexible Packaging Films business unit in Brazil (“Terphane Ltda.”) and substantially all of its related raw material costs are quoted or priced in U.S. Dollars while its variable conversion, fixed conversion and sales, general and administrative costs before depreciation & amortization (collectively “Terphane Ltda. Operating Costs”) are quoted or priced in Brazilian Real. This mismatch, together with a variety of economic variables impacting currency exchange rates, causes volatility that could negatively or positively impact EBITDA from ongoing operations for Flexible Packaging Films. While Flexible Packaging Films hedges this exposure on a short-term basis with foreign exchange forward rate contracts, the exposure continues to exist beyond the hedging periods.

Other Business Risks

•GovernmentalA failure to extend anti-dumping duties in Brazil on imported products or prevent competitors from circumventing such duties could adversely impact Flexible Packaging Films. In recent years, excess global capacity in the industry has led to increased competitive pressures from imports into Brazil. Company’s information technology systems as a result of cybersecurity attacks or other causes could negatively affect Tredegar’s business. The Company believes that these conditions have shifteddepends on information technology (“IT”) to record and process customer orders, manufacture and ship products in a timely manner, secure its production processes and know-how, maintain the competitive environmentfinancial accuracy of its business records and maintain personally identifiable information of its employees. An IT system failure due to computer viruses, internal or external security breaches, cybersecurity attacks or other malicious causes could disrupt our operations and prevent us from a regional to a global landscape and have driven price convergence and lower product margins for Flexible Packaging Films. Favorable anti-dumping rulings or countervailing duties are in effect for products imported from China, Egypt, India, Mexico, United Arab Emirates, Turkey, Peru and Bahrain. Competitors not currently subject to anti-dumping duties may choose to utilize their excess capacity by selling product in Brazil, which may result in pricing pressures that Flexible Packaging Films may not bebeing able to offsetprocess transactions with cost savings measures and/our customers, operate our manufacturing facilities and properly report transactions in a timely manner. Increased global IT security threats and cyber-crime pose a potential risk to the security and availability of the Company’s IT systems, networks and services, including those that are managed, hosted, provided or manufacturing efficiency initiatives. Brazilian authorities initiated an investigation for sunset review on anti-dumping rulings against China, Indiaused by third parties, as well as to the confidentiality, availability and Egyptintegrity of the Company’s data. Additionally, increased cybersecurity risk arises due to certain employees working remotely. To date, interruptions of the Company’s IT systems have been infrequent, and extended duties that would have expired in 2020 forTredegar

one year. There can be no assurance that effortshas not experienced a material cybersecurity incident. A significant prolonged failure of or security breach of the IT systems, networks or service providers the Company relies upon, or a loss or disclosure of business or other sensitive information, or personally identifiable information, as a result of a cybersecurity incident or other cause, could result in substantial costs to extend anti-dumping duties beyond 2021 on products imported from China, India, Egyptthe Company, damage to the Company’s reputation, regulatory enforcement actions and other countries will be successful.

Risks Related to all Tredegar Businesseslawsuits and could adversely affect the Company’s business, results of operations, financial condition or cash flows.

•The Company has identified material weaknesses in its internal control overCompany’s results of operations, financial reporting. The Company’s failure to establishcondition and maintain effective internal control over financial reportingcash flows have been and to maintain effective disclosure controls and procedures increasescould be impacted by the riskmacroeconomic effects of a material misstatement in its consolidated financial statements,pandemic.The COVID-19 pandemic had multiple adverse effects on the global economy, including short-term impacts affecting labor supply and its failurecausing supply chain disruptions which led to meet its reporting and financial obligations, could, in turn, have a negative impact on its financial condition. Maintaining effective internal control over financial reporting is an integral part of producing reliable financial statements. As discussed in Item 9A. “Controls and Procedures” of this Form 10-K (“Item 9A”), the Company’s management concluded that the Company’s internal control over financial reporting was not effective for the periods referred to therein as a result of certain deficiencies that were determined to constitute material weaknesses in the Company’s internal control over financial reporting.

Under standards established by the Public Company Accounting Oversight Board, a material weakness is defined as a deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the annual or interim financial statements will not be prevented or detected on a timely basis. Under the criteria set forth in Internal Control - Integrated Framework 2013 issued by the Committee of Sponsoring Organizations of the Treadway Commission, a material weakness in the design of monitoring controls indicates that the Company has not sufficiently developed and/or documented internal controls by which management can review and oversee the Company’s financial information to detect and correct material errors or that the personnel responsible for performing the review did not have the sufficient skill set or knowledge of the subject matter to perform a proper assessment.

As discussed in Item 9A to remediate the material weaknesses, the Company, with the assistance of its outside consultant, is in the process of implementing certain changes to its internal controls and reviewing the entire control environment to help ensure that there are no other material weaknesses. The Company believes that its remediation plan will be sufficient to remediate the identified material weaknesses and strengthen its internal control over financial reporting. The Company’s remediation efforts are ongoing, and it will continue its initiatives to implement and document policies and procedures. Remediation of the identified material weaknesses and strengthening the Company’s internal control environment have extended into 2021.inflationary pressures. In addition, the Company is monitoringpandemic resulted in certain after-shocks and structural shifts, which have adversely impacted Tredegar’s markets.

In the impactevent of COVID-19 on its remediation plan. Depending on the severitya future pandemic, Tredegar’s businesses, our suppliers, contractors and length of the pandemic, the remediation timelinethird-party logistic providers could be negatively impacted because of inefficiencies caused by COVID-related limitations on travel, meetings, on-site work and close collaboration and the related increase in time necessaryexperience conditions similar to complete remediation projects.

As the Company continues to evaluate and work to improve its internal control over financial reporting and disclosure controls and procedures, management may determine to take additional measures to address control deficiencies or modify the remediation plan. The Company cannot provide assurance, however, as to when it will remediate all such weaknesses, nor can it be certain of whether additional actions will be required or the costs of any such actions. Moreover, the Company cannot provide assurance that additional material weaknesses will not arise in the future.

While the material weaknesses discussed in Item 9A did not result in material misstatements of the Company’s financial statements as of and for the years ended December 31, 2020, 2019, 2018 and 2017 or in the intervening interim periods during those respective years, any failure to remediate the material weaknesses, or the development of new material weaknesses in its internal control over financial reporting, could result in material misstatements in the Company’s consolidated financial statements and cause it to fail to meet its reporting and financial obligations, which in turn could have a negative impact on its financial condition.

•Tredegar has an underfunded defined benefit (pension) plan. Tredegar sponsors a pension plan that covers certain hourly and salaried employees in the U.S. The plan was closed to new participants in 2007, and substantially frozen to benefit accruals for active participants in 2014. As of January 31, 2018, the plan no longer accrued benefits associated with crediting employees for service, thereby freezing all future benefits under the plan. As of December 31, 2020, the plan was underfunded under U.S. generally accepted accounting principles (“GAAP”) measures by $103.1 million. Tredegar expects that it will be requiredCOVID-19 pandemic, including facility closures, labor constraints, supply chain disruptions and other challenges. These challenges could impact our ability to make a cash contribution of approximately $11.7 millionmaintain sufficient inventory and to its underfunded pension plan in 2021, and may be required to make higher cash contributions in future periods depending on the level of interest rates and investment returns on plan assets.

•Noncompliance with any of the covenants in the Company’s $375 million revolving credit facility, as amended on December 1, 2020, which matures in June 2024, could result in all debt under the agreement outstanding at such time becoming due and limiting the Company’s borrowing capacity,accurately predict demand or lead times, which could haveinhibit our ability to service customer demand. Additionally, a material adverse effect on its consolidated financial condition and liquidity. The credit agreement governing Tredegar’s revolving credit facility contains restrictions and financial covenants that, if violated,future pandemic could restrict the Company’s operational and financial

flexibility. Failure to comply with these covenants could result in an event of default, which if not cured or waived, would result in all outstanding debt under the credit facility at such time becoming due, which could have a material adverse effect on the Company’s consolidated financial condition and liquidity.

•Tredegar’s performance is influenced by costs incurred by its operating companies, including, for example, the cost of raw materials and energy. These costs include the cost of aluminum (the raw material on which Aluminum Extrusions primarily depends), resin (the raw material on which PE Films primarily depends), PTA and MEG (the raw materials on which Flexible Packaging Films primarily depends), natural gas (the principal fuel necessary for Aluminum Extrusions’ plants to operate), electricity and diesel fuel. Aluminum, resin and natural gas prices are volatile as shown in the charts in Quantitative and Qualitative Disclosures in Item 7. The Company attempts to mitigate the effects of increased costs through price increases and contractual pass-through provisions, but there are no assurances that higher prices can effectively be passed through to customers or that Tredegar will be able to offset fully or on a timely basis the effects of higher raw material and energy costs through price increases or pass-through arrangements. Further, the Company’s cost control efforts may not be sufficient to offset any increases in raw material, energy orheighten other costs.risks described above.

•Tredegar is subject to current and future governmental regulation,regulations, including environmental laws and regulations, and could become exposed to material liabilities and costs associated with such regulation. The Company is subject to regulation by local, state, federal and foreign governmental authorities. New laws and regulations, or changes to existing laws, including those relating to environmental matters (including global climate change and plastic products), and privacy matters, could subject Tredegar to significant additional capital expenditures, operating expenses or other compliance costs. Moreover, future developments in federal, state, local and international laws and regulations, including environmental laws, are difficult to predict. Environmental laws and privacy restrictions have become and are expected to continue to become increasingly strict. As a result, Tredegar expects to be subject to new environmental and privacy laws and regulations. However, any such changes are uncertain and, therefore, it is not possible for the Company to predict with certainty the amount of additional capital expenditures or operating expenses that could be necessary for compliance with respect to any such changes. See Government Regulation in Item 1. “Business” of this Form 10-K for a further discussion of this risk factor.

We areThe Company is subject to the U.S. Foreign Corrupt Practices Act, Brazilian anti-corruption laws and similar anti-bribery laws in other jurisdictions, which generally prohibit companies and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or retaining business. Although we have policies and procedures designed to facilitate compliance with these laws and regulations, our employees, contractors and agents may take actions in violation of our policies. Any such violation, even if prohibited by our policies, could adversely affect our business and/or our reputation.

•Material disruptions at one of the Company’s major manufacturing facilities could negatively impact financial results. Tredegar believes it has implemented measures to minimize the risks of disruption at its facilities. However, a disruption could occur as a result of any number of events: an equipment failure with repairs requiring long lead times, labor stoppages or shortages, cybersecurity attacks, utility disruptions, constraints on the supply or delivery of critical raw materials, and severe weather conditions. A material disruption in one of the Company’s operating locations could negatively impact production and the Company’s consolidated financial condition, results of operations and cash flows.

•An inability to renegotiate the Company’s collective bargaining agreements could adversely impact its consolidated financial condition, results of operations and cash flows. Approximately 34% of the Company’s employees are represented by labor unions located in the U.S. and Brazil under various collective bargaining agreements with varying durations and expiration dates. Tredegar may not be able to satisfactorily renegotiate collective bargaining agreements when they expire, which could result in strikes or work stoppages or higher labor costs. In addition, existing collective bargaining agreements may not prevent a strike or work stoppage at the Company’s facilities in the future. Any such work stoppages (or potential work stoppages) could negatively impact Tredegar’s ability to manufacture its products and adversely affect its consolidated financial condition, results of operations and cash flows. None of Tredegar’s collective bargaining agreements expire before the fourth quarter of 2021.

•Our business and operations, and the operations of our customers, suppliers and others we do business with, may be adversely affected by epidemics such as the recent COVID-19 pandemic, which could adversely affect our financial condition, results of operations and cash flows. We may face risks related to health epidemics or outbreaks of communicable diseases. The outbreak of such a communicable disease could result in a widespread health crisis that could adversely affect general commercial activity and the economies and financial markets of many countries. For example, COVID-19 has spread across the globe to every country in which the Company does business and is impacting worldwide economic activity. A public health epidemic, including COVID-19, poses the risk that we or our contractors, suppliers, customers and other business partners may be prevented or otherwise adversely affected in the conduct of business activities for an indefinite period of time, including due to shutdowns that may be requested or mandated by governmental authorities and by other government mandates or policy changes. We may also face staffing issues if our employees