0000874766 hig:OtherInvestmentsandOtherLiabilitiesMember us-gaap:DerivativeFinancialInstrumentsAssetsMember 2018-12-31 0000874766 hig:HomeownersMember us-gaap:ShortdurationInsuranceContractsAccidentYear2009Member 2013-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

| | |

| þ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20172018

or

|

| | |

| o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-13958

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 13-3317783 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

One Hartford Plaza, Hartford, Connecticut 06155

(Address of principal executive offices) (Zip Code)

(860) 547-5000

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12 (b) OF THE ACT

(ALL OF WHICH ARE LISTED ON THE NEW YORK STOCK EXCHANGE INC.):

Common Stock, par value $0.01 per share

Warrants (expiring June 26, 2019)

6.10% Notes due October 1, 2041

7.875% Fixed-to-Floating Rate Junior Subordinated Debentures due 2042

Depositary Shares, Each Representing a 1/1,000th Interest in a Share of 6.000% Non-Cumulative Preferred Stock, Series G, par value $0.01 per share

SECURITIES REGISTERED PURSUANT TO SECTION 12 (g) OF THE ACT:

None

|

| | | |

| Indicate by check mark: | Yes | No |

| • | if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | þ | |

| • | if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. | | þ |

| • | whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | þ | |

| • | whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | þ | |

| • | if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | þ | |

| • | whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | | |

| | Large accelerated filer þ Accelerated filer o Non-accelerated filer o Smaller reporting company o Emerging growth company o | | |

| • | whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) | | þ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

The aggregate market value of the shares of Common Stock held by non-affiliates of the registrant as of June 30, 201729, 2018 was approximately $19$18 billion, based on the closing price of $52.57$51.13 per share of the Common Stock on the New York Stock Exchange on June 30, 2017.29, 2018.

As of February 21, 2018,20, 2019, there were outstanding 356,981,387359,470,401 shares of Common Stock, $0.01 par value per share, of the registrant.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement for its 20182019 annual meeting of shareholdersstockholders are incorporated by reference in Part III of this Form 10-K.

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 20172018

TABLE OF CONTENTS

| | | Item | Description | Page | Description | Page |

| | | | | |

| 1 | | | | |

| 1A. | | | | |

| 1B. | | None | | None |

| 2 | | | | |

| 3 | | | | |

| 4 | | Not Applicable | | Not Applicable |

| | | | | |

| 5 | | | | |

| 6 | | | | |

| 7 | | | | |

| 7A. | | [a] | | [a] |

| 8 | | [b] | | [b] |

| 9 | | None | | None |

| 9A. | | | | |

| 9B. | | None | | None |

| | | | | |

| 10 | | | | |

| 11 | | [c] | | [c] |

| 12 | | | | |

| 13 | | [d] | | [d] |

| 14 | | [e] | | [e] |

| | | | | |

| 15 | | | | |

| | EXHIBITS INDEX |

| EXHIBITS INDEX | |

| 16 | FORM 10-K SUMMARY | Not Applicable | FORM 10-K SUMMARY | Not Applicable |

| | | | | |

[a] The information required by this item is set forth in the Enterprise Risk Management section of Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations and is incorporated herein by reference.

[b] See Index to Consolidated Financial Statements and Schedules elsewhere herein.

[c] The information called for by Item 11 will be set forth in the Proxy Statement under the subcaptions "Compensation Discussion and Analysis", "Executive Compensation", "Director Compensation", "Report of the Compensation and Management Development Committee", and "Compensation and Management Development Committee Interlocks and Insider Participation" and is incorporated herein by reference.

[d] Any information called for by Item 13 will be set forth in the Proxy Statement under the caption and subcaption "Board and Governance Matters" and "Director Independence" and is incorporated herein by reference.

[e] The information called for by Item 14 will be set forth in the Proxy Statement under the caption "Audit Matters" and is incorporated herein by reference.

Forward-Looking Statements

Certain of the statements contained herein are forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects,” “projects,” and similar references to future periods.

Forward-looking statements are based on management's current expectations and assumptions regarding future economic, competitive, legislative and other developments and their potential effect upon The Hartford Financial Services Group, Inc. and its subsidiaries (collectively, the “Company” or “The Hartford”). Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Actual results could differ materially from expectations, depending on the evolution of various factors, including the risks and uncertainties identified below, as well as factors described in such forward-looking statements or in Part I, Item 1A. Risk Factors, in Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations, and those identified from time to time in our other filings with the Securities and Exchange Commission.

Risks Relating to Economic, Political and Global Market Conditions:

| |

| ◦ | challenges related to the Company’s current operating environment, including global political, economic and market conditions, and the effect of financial market disruptions, economic downturns, changes in trade regulation including tariffs and other barriers or other potentially adverse macroeconomic developments on the demand for our products and returns in our investment portfolios; |

| |

◦ | financial risk related to the continued reinvestment of our investment portfolios; |

| |

| ◦ | market risks associated with our business, including changes in credit spreads, equity prices, interest rates, inflation rate, and market volatility and foreign exchange rates;volatility; |

| |

| ◦ | the impact on our investment portfolio if our investment portfolio is concentrated in any particular segment of the economy; |

| |

| ◦ | the impacts of changing climate and weather patterns on our businesses, operations and investment portfolio including on claims, demand and pricing of our products, the availability and cost of reinsurance, our modeling data used to evaluate and manage risks of catastrophes and severe weather events, the value of our investment portfolios and credit risk with reinsurers and other counterparties; |

| |

| ◦ | the risks associated with the change in or replacement of the London Inter-Bank Offered Rate ("LIBOR") on the securities we hold or may have issued, other financial instruments and any other assets and liabilities whose value is tied to LIBOR; |

Insurance Industry and Product-Related Risks:

| |

| ◦ | the possibility of unfavorable loss development, including with respect to long-tailed exposures; |

| |

| ◦ | the significant uncertainties that limit our ability to estimate the ultimate reserves necessary for asbestos and environmental claims |

| |

| ◦ | the possibility of a pandemic, earthquake, or other natural or man-made disaster that may adversely affect our businesses; |

| |

| ◦ | weather and other natural physical events, including the severityintensity and frequency of storms, hail, wildfires, flooding, winter storms, hurricanes and tropical storms, as well as climate change and its potential impact on weather patterns; |

| |

| ◦ | the possible occurrence of terrorist attacks and the Company’s inability to contain its exposure as a result of, among other factors, the inability to exclude coverage for terrorist attacks from workers' compensation policies and limitations on reinsurance coverage from the federal government under applicable laws; |

| |

| ◦ | the Company’s ability to effectively price its property and casualty policies, including its ability to obtain regulatory consents to pricing actions or to non-renewal or withdrawal of certain product lines; |

| |

| ◦ | actions by competitors that may be larger or have greater financial resources than we do; |

| |

| ◦ | technological changes, such as usage-based methods of determining premiums, advancements in automotive safety features, the development of autonomous vehicles, and platforms that facilitate ride sharing, which may alter demand for the Company's products, impact the frequency or severity of losses, and/or impact the way the Company markets, distributes and underwrites its products; |

| |

| ◦ | the Company's ability to market, distribute and provide insurance products and investment advisory services through current and future distribution channels and advisory firms; |

| |

| ◦ | the uncertain effects of emerging claim and coverage issues; |

Financial Strength, Credit and Counterparty Risks:

| |

| ◦ | risks to our business, financial position, prospects and results associated with negative rating actions or downgrades in the Company’s financial strength and credit ratings or negative rating actions or downgrades relating to our investments; |

| |

| ◦ | the impact on our statutory capital of various factors, including many that are outside the Company’s control, which can in turn affect our credit and financial strength ratings, cost of capital, regulatory compliance and other aspects of our business and results; |

| |

| ◦ | losses due to nonperformance or defaults by others, including sourcing partners, derivativecredit risk with counterparties associated with investments, derivatives, premiums receivable, reinsurance recoverables and otherindemnifications provided by third parties;parties in connection with previous dispositions; |

| |

| ◦ | the potential for losses due to our reinsurers' unwillingness or inability to meet their obligations under reinsurance contracts and the availability, pricing and adequacy of reinsurance to protect the Company against losses; |

| |

| ◦ | regulatory limitations on the ability of the Company and certain of its subsidiaries to declare and pay dividends; |

Risks Relating to Estimates, Assumptions and Valuations:

| |

| ◦ | risk associated with the use of analytical models in making decisions in key areas such as underwriting, pricing, capital management, hedging, reserving, investments, reinsurance and catastrophe risk management; |

| |

| ◦ | the potential for differing interpretations of the methodologies, estimations and assumptions that underlie the Company’s fair value estimates for its investments and the evaluation of other-than-temporary impairments on available-for-sale securities; |

| |

| ◦ | the significant uncertainties that limitpotential for further impairments of our ability to estimategoodwill or the ultimate reserves necessarypotential for asbestos and environmental claims;changes in valuation allowances against deferred tax assets; |

Strategic and Operational Risks:

| |

| ◦ | the Company’s ability to maintain the availability of its systems and safeguard the security of its data in the event of a disaster, cyber or other information security incident or other unanticipated event; |

| |

| ◦ | the potential for difficulties arising from outsourcing and similar third-party relationships; |

| |

| ◦ | the risks, challenges and uncertainties associated with capital management plans, expense reduction initiatives and other actions, which may include acquisitions, divestitures or restructurings; |

| |

| ◦ | failure to complete our proposed acquisition of The Navigators Group, Inc. may cause volatility in our securities; |

| |

| ◦ | risks associated with acquisitions and divestitures including the potential for difficulties arisingchallenges of integrating acquired companies or businesses or separating from outsourcingour divested businesses that may result in our not being able to achieve the anticipated benefits and similar third-party relationships;synergies and may result in unintended consequences; |

| |

| ◦ | difficulty in attracting and retaining talented and qualified personnel including key employees, such as executives, managers and employees with strong technological, analytical and other specialized skills; |

| |

| ◦ | the Company’s ability to protect its intellectual property and defend against claims of infringement; |

Regulatory and Legal Risks:

| |

| ◦ | the cost and other potential effects of increased regulatory and legislative developments, including those that could adversely impact the demand for the Company’s products, operating costs and required capital levels; |

| |

| ◦ | unfavorable judicial or legislative developments; |

| |

| ◦ | the impact of changes in federal or state tax laws; |

| |

| ◦ | regulatory requirements that could delay, deter or prevent a takeover attempt that shareholdersstockholders might consider in their best interests; and |

| |

| ◦ | the impact of potential changes in accounting principles and related financial reporting requirements; |

Risks Related to the Company's Life and Annuity Business in Discontinued Operations

| |

◦ | the risks related to the Company's ability to close its previously announced sale of its life and annuity run-off book of business, which is subject to several closing conditions, including many that are outside of the Company's control; |

| |

◦ | the risks related to political, economic and global economic conditions, including interest rate, equity and credit spread risks; |

| |

◦ | the impact on our investment portfolio if our investment portfolio is concentrated in any particular segment of the economy; |

| |

◦ | risks related to negative rating actions or downgrades in the financial strength and credit ratings of Hartford Life Insurance Company or Hartford Life and Annuity Insurance Company or negative rating actions or downgrades relating to our investments; |

| |

◦ | the volatility in our statutory and United States ("U.S.") Generally Accepted Accounting Principles ("GAAP") earnings and potential material changes to our results resulting from our risk management program to emphasize protection of economic value; |

| |

◦ | the potential for losses due to our reinsurers’ unwillingness or inability to meet their obligations under reinsurance contracts; |

| |

◦ | the potential for differing interpretations of the methodologies, estimations and assumptions that underlie the fair value estimates for investments and the evaluation of other-than-temporary impairments on available for sale securities; |

| |

◦ | the potential for further acceleration of deferred policy acquisition cost amortization and an increase in reserves for certain guaranteed benefits in our variable annuities; |

| |

◦ | changes in federal or state tax laws that would impact the tax-favored status of life and annuity contracts; and |

| |

◦ | changes in accounting and financial reporting of the liability for future policy benefits, including how the life and annuity businesses account for deferred acquisition costs and market risk benefits on variable annuity contracts and the discounting of life contingent fixed annuities.requirements. |

Any forward-looking statement made by the Company in this document speaks only as of the date of the filing of this Form 10-K. Factors or events that could cause the Company’s actual results to differ may emerge from time to time, and it is not possible for the Company to predict all of them. The Company undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise.

Part I - Item 1. Business

Item 1. BUSINESS

(Dollar amounts in millions, except for per share data, unless otherwise stated)

GENERAL

The Hartford Financial Services Group, Inc. (together with its subsidiaries, “The Hartford”, the “Company”, “we”, or “our”) is a holding company for a group of subsidiaries that provide property and casualty insurance, group benefits, and mutual funds and exchange-traded products to individual and business customers in the United States. In December 2017, the Company announced the signing of a definitive agreement to sell its life and annuity operating subsidiaries and, accordingly, the assets and liabilities of those subsidiaries have been presented as held for sale with results of operations from that business reflected as discontinued operations. See Note 20 - Business Dispositions and Discontinued Operations of Notes to Consolidated Financial Statements. The Hartford is headquartered in Connecticut and its oldest subsidiary, Hartford Fire Insurance Company, dates back to 1810. At December 31, 2017,2018, total assets and total stockholders’ equity of The Hartford were $225.362.3 billion and $13.513.1 billion, respectively.

ORGANIZATION

The Hartford strives to maintain and enhance its position as a market leader within the financial services industry. The Company sells diverse and innovative products through multiple distribution channels to individuals and businesses and is considered a leading property and casualty and employee group benefits insurer. The Company endeavors to expand its insurance product offerings and distribution and capitalize on the strength of the Company's brand. The Hartford Stag logo is one of the most recognized symbols in the financial services industry. The Company is also working to increase efficiencies through investments in technology.

As a holding company, The Hartford Financial Services Group, Inc. is separate and distinct from its subsidiaries and has no significant business operations of its own. The Companyholding company relies on the dividends from its insurance companies and other subsidiaries as the principal source of cash flow to meet its obligations, pay dividends and repurchase common stock. Information regarding the cash flow and liquidity needs of The Hartford Financial Services Group, Inc. may be found in Part II, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) — Capital Resources and Liquidity.

REPORTING SEGMENTS

The Hartford conducts business principally in five reporting segments including Commercial Lines, Personal Lines, Property & Casualty ("P&C") Other Operations, Group Benefits and MutualHartford Funds (previously referred to as "Mutual Funds"), as well as a Corporate category. The HartfordCompany includes in itsthe Corporate category discontinued operations ofrelated to the Company's life and annuity run-off business accounted for as held for sale,sold in May 2018, reserves for run-off structured settlement and terminal funding agreement liabilities, retained, capital raising activities (including debt financing and related interest expense), purchase accounting adjustments related to goodwill and other expenses not allocated to the reporting segments. Corporate also includes investment management fees and expenses related to managing third party business, including management of the invested assets of Talcott Resolution Life, Inc. and its subsidiaries ("Talcott Resolution"). Talcott Resolution is the new holding company of the life and annuity business that we

2017sold in May 2018. In addition, Corporate includes a 9.7% ownership interest in the legal entity that acquired the life and annuity business sold.

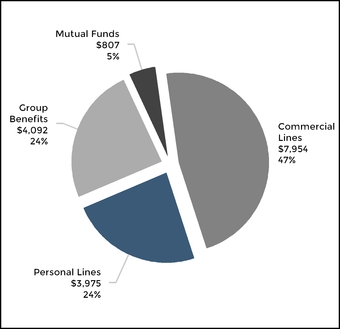

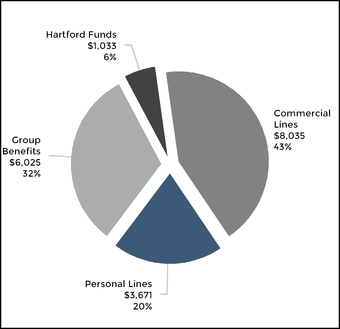

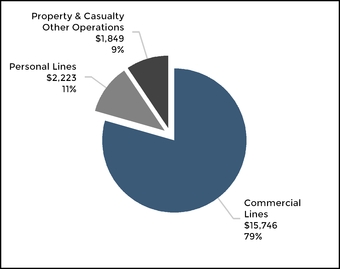

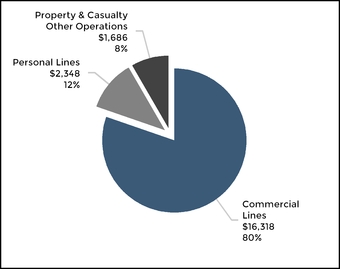

2018 Revenues of $16,974$18,955 [1] by Segment

[1]Includes Revenue of $120$86 for P&C Other Operations and $26$105 for Corporate.

The following discussion describes the principal products and services, marketing and distribution, and competition of The Hartford's reporting segments. For further discussion of the reporting segments, including financial disclosures of revenues by product line, net income (loss), and assets for each reporting segment, see Note 4 - Segment Information of Notes to Consolidated Financial Statements.

Part I - Item 1. Business

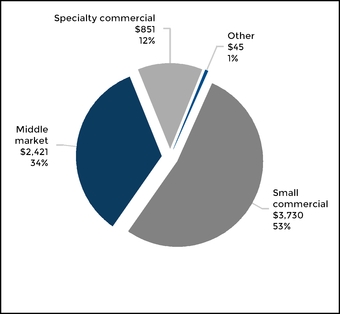

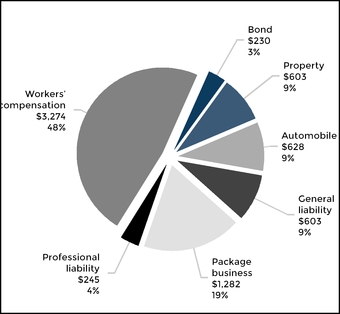

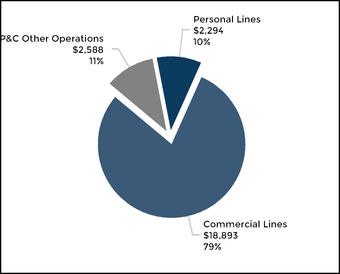

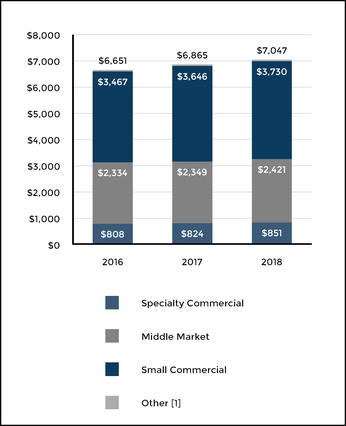

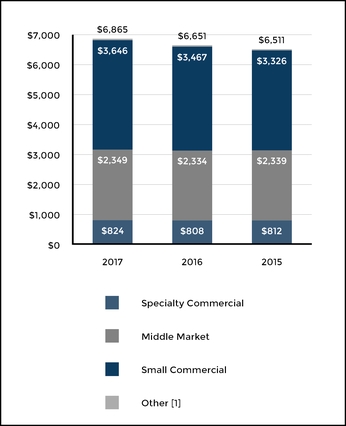

20172018 Earned Premiums of $6,865$7,047 by Line of Business

20172018 Earned Premiums of $6,865$7,047 by Product

Principal Products and Services |

| |

| Automobile | Covers damage to a business's fleet of vehicles due to collision or other perils (automobile physical damage). In addition to first party automobile physical damage, commercial automobile covers liability for bodily injuries and property damage suffered by third parties and losses caused by uninsured or under-insured motorists. |

| Property | Covers the building a business owns or leases as well as its personal property, including tools and equipment, inventory, and furniture. A commercial property insurance policy covers losses resulting from fire, wind, hail, earthquake, theft and other covered perils, including coverage for assets such as accounts receivable and valuable papers and records. Commercial property may include specialized equipment insurance, which provides coverage for loss or damage resulting from the mechanical breakdown of boilers and machinery, and ocean and inland marine insurance, which provides coverage for goods in transit and unique, one-of-a-kind exposures. |

| General Liability | Covers a business in the event it is sued for causing harm to a person and/or damage to property. General liability insurance covers third-party claims arising from accidents occurring on the insured’s premises or arising out of their operations. General liability insurance may also cover losses arising from product liability and provide replacement of lost income due to an event that interrupts business operations. |

| Package Business | Covers both property and general liability damages. |

| Workers' Compensation | Covers employers for losses incurred due to employees sustaining an injury, illness or disability in connection with their work. Benefits paid under workers’ compensation policies may include reimbursement of medical care costs, replacement income, compensation for permanent injuries and benefits to survivors. Workers’ compensation is provided under both guaranteed cost policies (coverage for a fixed premium) and loss sensitive policies where premiums are adjustable based on the loss experience of the employer. |

| Professional Liability | Covers liability arising from directors and officers acting in their official capacity and liability for errors and omissions committed by professionals and others. Coverage may also provide employment practices insurance relating to allegations of wrongful termination and discrimination. |

| Bond | Encompasses fidelity and surety insurance, including commercial surety, contract surety and fidelity bonds. Commercial surety includes bonds that insure non-performance by contractors, license and permit bonds to help meet government-mandated requirements and probate and judicial bonds for fiduciaries and civil court proceedings. Contract surety bonds may include payment and performance bonds for contractors. Fidelity bonds may include ERISA bonds related to the handling of retirement plan assets and bonds protecting against employee theft or fraud. The Company also provides credit and political risk insurance offered to clients with global operations. |

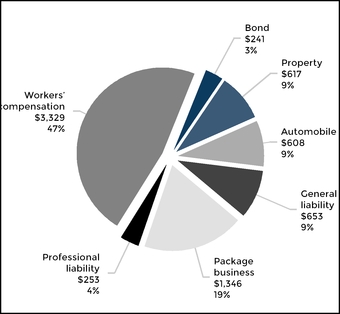

Through its three lines of business of small commercial, middle market and specialty, Commercial Lines principally provides workers’ compensation, property, automobile and general liability insurance products to businesses, primarily throughout the

United States. In addition, the specialty line of business provides

professional liability, bond, credit and political risk, loss-sensitive workers compensation, general liability, automobile liability and automobile physical damage.damage coverages. The majority of

Part I - Item 1. Business

Commercial Lines written premium is generated by small commercial and middle market, which provide coverage options and customized pricing based on the

Part I - Item 1. Business

policyholder’s individual risk characteristics. Within small commercial, both property and general liability coverages are offered under a single package policy, marketed under the Spectrum name. Specialty provides a variety of customized insurance products and services.

Small commercial provides coverages for small businesses, which the Company considers to be businesses with an annual payroll under $12, revenues under $25 and property values less than $20 per location. Through Maxum Specialty Insurance Group ("Maxum"), small commercial also provides excess and surplus lines coverage to small businesses including umbrella, general liability, property and other coverages. Middle market provides insurance coverages to medium-sized businesses, which are companies whose payroll, revenue and property values exceed the small business definition. The Company has a small amount of property and casualty business written internationally. For U.S. exporters and other U.S. companies with international exposures, the Company covers property, marine and liability risks outside the U.S. as the assuming reinsurer under a reinsurance agreementagreements with a third party.parties.

In addition to offering standard commercial lines products, middle market includes program business which provides tailored programs, primarily to customers with common risk characteristics. Within specialty, a significant portion of the business is written through large deductible programs for national accounts. Other programs written within specialty are retrospectively-rated where the premiums are adjustable based on loss experience. Also within specialty, the Company writes captive programs business, which provides tailored programs to those seeking a loss sensitive solution where premiums are adjustable based on loss experience. On August 22, 2018, the Company entered into a definitive agreement to acquire The Navigators Group, Inc., a global specialty underwriter. This acquisition could change the way we go to market as a commercial lines carrier.

Marketing and Distribution

Commercial Lines provides insurance products and services through the Company’s regional offices, branches and sales and policyholder service centers throughout the United States. The products are marketed and distributed nationally using independent agents, brokers and wholesalers. The independent agent and broker distribution channel is consolidating and this trend is expected to continue. This will likely result in a larger proportion of written premium being concentrated among fewer agents and brokers. In addition, the Company offers insurance products to customers of payroll service providers through its relationships with major national payroll companies and to members of affinity organizations.

Competition

Small Commercial

In small commercial, The Hartford competes against large national carriers, regional carriers and direct writers. Competitors include stock companies, mutual companies and other underwriting organizations. The small commercial market remains highly competitive and fragmented as carriers seek to differentiate themselves through product expansion, price

reduction, enhanced service and leading technology. Larger carriers such as The Hartford continually advance their pricing sophistication and ease of doing business with agents and customers through the use of technology, analytics and other capabilities that improve the process of evaluating a risk, quoting new business and servicing customers. The Company also hascontinuously enhances digital capabilities as customers and distributors demand more

access and convenience, and expandingexpands product and underwriting capabilities to accommodate both larger accounts and a broader risk appetite.

The small commercial market has experienced low written premium growth rates due to current economic conditions. Competitors seek Existing competitors and new business by increasing their underwriting appetite, and deepening their relationships with distribution partners. Also, carriers serving middle market-sized accounts are more aggressively competing for small commercial accounts, which are generally less price-sensitive. Some carriers,entrants, including start-up and non-traditional carriers, are actively looking to expand sales of business insurance products to small commercial market insuredsbusinesses through increasing their underwriting appetite, deepening their relationships with distribution partners, and through on-line and direct-to-consumer marketing.

Middle Market

Middle market business is considered “high touch” and involves individual underwriting and pricing decisions. The pricing of middle market accounts is prone to significant volatility over time due to changes in individual account characteristics and exposure, as well as legislative and macro-economic forces. National and regional carriers participate in the middle market insurance sector, resulting in a competitive environment where pricing and policy terms are critical to securing new business and retaining existing accounts. Within this competitive environment, The Hartford is working to deepen its product and underwriting capabilities, and leverage its sales and underwriting talent with tools it has introduced in recent years. Through advanced training and expand its use of data analytics the Company’s field underwriters are working to improvemake risk selection and pricing decisions. In product development and related areas such as claims and risk engineering, the Company is extending its capabilities in industry verticals, such as energy, construction, automobile parts manufacturing, food processing and hospitality. Through a partnership with AXA Corporate Solutions,business partner, the Company offers business insurance coverages to exporters and other U.S. companies with a physical presence overseas. The Company has also added newHartford’s middle market underwritersbusiness will leverage the investments in product, underwriting, and technology to better match price to individual risk as the Midwest and Western U.S.firm pursues responsible growth strategies to deepen relationships with its distribution partners.deliver target returns.

Specialty Commercial

Specialty commercial competes on an account-by-account basis due to the complex nature of each transaction. Competition in this market includes stock companies, mutual companies, alternative risk sharing groups and other underwriting organizations.

For specialty casualty businesses, pricing competition continues to be significant, particularly for the larger individual accounts. As a means to mitigate the cost of insurance on larger accounts, more insureds may opt for the loss-sensitive products offered in our national accounts segment, including retrospectively rated contracts, in lieu of guaranteed cost policies. Under a retrospectively-rated contract, the ultimate premium collected from the insured is adjusted based on how incurred losses for the policy year develop over time, subject to a minimum and maximum premium. Within national accounts, the Company is implementing a phased roll out ofimplemented a new risk management platform, allowing customers better access to claims data and other information needed by corporate risk managers. This investment will allowsystem allows the Company to work more closely with customers to improve long-term account performance.

Part I - Item 1. Business

In the bond business, favorable underwriting results in recent years has led to increased competition for market share, setting the stage for potential written price decreases.share.

In professional liability, large and medium-sized businesses are in differing competitive environments. Large public director &

officers coverage, specifically excess layers, is under significant competitive price pressure. The middle market private management liability segment is in a more stable competitive and pricing environment.

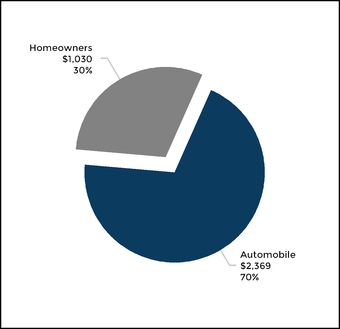

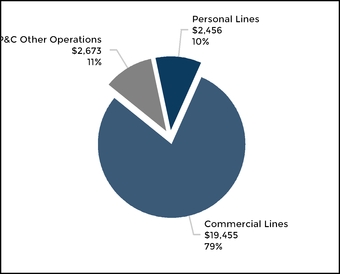

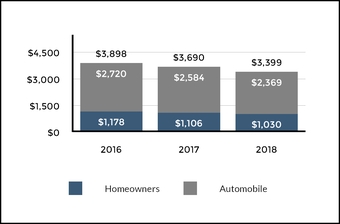

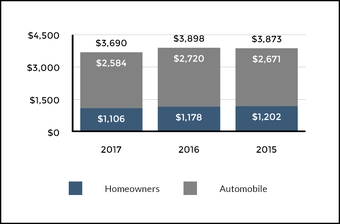

20172018 Earned Premiums of $3,690$3,399 by Line of Business

20172018 Earned Premiums of $3,690$3,399 by Product

Principal Products and Services |

| |

| Automobile | Covers damage to an individual insured’s own vehicle due to collision or other perils and is referred to as automobile physical damage. In addition to first party automobile physical damage, automobile insurance covers liability for bodily injuries and property damage suffered by third parties and losses caused by uninsured or underinsured motorists. Also, under no-fault laws, policies written in some states provide first party personal injury protection. Some of the Company’s personal automobile insurance policies also offer personal umbrella liability coverage for an additional premium. |

| Homeowners | Insures against losses to residences and contents from fire, wind and other perils. Homeowners insurance includes owned dwellings, rental properties and coverage for tenants. The policies may provide other coverages, including loss related to recreation vehicles or watercraft, identity theft and personal items such as jewelry. |

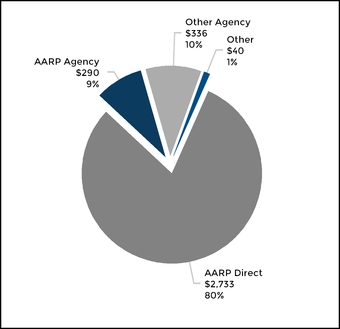

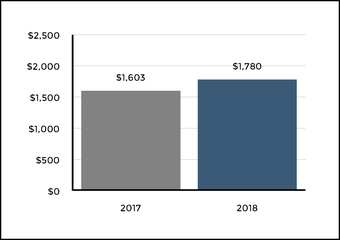

Personal Lines provides automobile, homeowners and personal umbrella coverages to individuals across the United States, including a program designed exclusively for members of AARP (“AARP Program”). The Hartford's automobile and homeowners products provide coverage options and pricing tailored to a customer's individual risk. The Hartford has individual customer relationships with AARP Program policyholders and, as a group, they represent a significant portion of the total Personal Lines' business. Business sold to AARP members, either direct or through independent agents, amounted to earned premiums of $3.0 billion, $3.2 billion and $3.3 billion in 2018, 2017 and $3.2 billion in 2017, 2016, and 2015, respectively.

During 2017,2018, Personal Lines continued to refine its automobile and home product offerings i.e., itsmarketed under the Open Road Auto and Home Advantage products.names. Overall rate

levels, price segmentation, rating factors

and underwriting procedures were examined and updated to reflect the company’s actual experience with these products. In addition, Personal Lines also continued working with carrier partners to provide risk protection options for AARP members with needs beyond the company’s current product offering.

Marketing and Distribution

Personal Lines reaches diverse customers through multiple distribution channels, including direct-to-consumer and independent agents. In direct-to-consumer, Personal Lines markets its products through a mix of media, including direct mail, digital marketing, television as well as digital and print advertising. Through the agency channel, Personal Lines provides products and services to customers through a network of independent agents in the standard personal lines market,

Part I - Item 1. Business

independent agents in the standard personal lines market, primarily serving mature, preferred consumers. These independent agents are not employees of the Company.

Personal Lines has made significant investments in offering direct and agency-based customers the opportunity to interact with the company online, including via mobile devices. In addition, its technology platform for telephone sales centers enables sales representatives to provide an enhanced experience for direct-to-consumer customers, positioning Thethe Company to offer unique capabilities to AARP’s member base.

Most of Personal Lines' sales are associated with its exclusive licensing arrangement with AARP, with the current agreement in place through January 1, 2023, to market automobile, homeowners and personal umbrella coverages to AARP's approximately 3837 million members, primarily direct but also through independent agents. This relationship with AARP, which has been in place since 1984, provides Personal Lines with an important competitive advantage given the expected growth ofincrease in the population of those over age 50 and the strength of the AARP brand. The Company has expanded its relationship withIn most states, auto and home policies issued to AARP to enable its members whoinclude a lifetime continuation agreement endorsement, providing that the policies will be renewed as long as certain terms are small business owners to purchase the Company's industry-leading small business products offered by Commercial Lines.met, such as timely payment of premium and maintaining a driver’s license in good standing.

In addition to selling to AARP members, Personal Lines offers its automobile and homeowners products to non-AARP customers, primarily through the independent agent channel within select underwriting markets where we believe we have a competitive advantage. Personal Lines leverages its agency channel to target AARP members and other customer segments that value the advice of an independent agent and recognize the differentiated experience the Company provides. In particular, the Company has taken action to distinguish its brand and improve profitability in the independent agent channel with fewer and more highly partnered agents.

Competition

The personal lines automobile and homeowners insurance

markets are highly competitive. Personal lines insurance is written by insurance companies of varying sizes that compete principally on the basis of price, product, service, including claims handling, the insurer's ratings and brand recognition. Companies with strong ratings, recognized brands, direct sales capability and economies of scale will have a competitive advantage. In recent years, insurers have increased their advertising in the direct-to-consumer market, in an effort to gain new business and retain profitable business. The growth of direct-to-consumer sales continues to outpace sales in the agency distribution channel.

Insurers that distribute products principally through agency channels compete by offering commissions and additional incentives to attract new business. To distinguish themselves in the marketplace, top tier insurers are offering online and self service capabilities that make it easier for agents and consumers to do business with the insurer. A large majority of agents have been using “comparative rater” tools that allow the agent to compare premium quotes among several insurance companies. The use of comparative rater tools increases price competition. Insurers that are able to capitalize on their brand and reputation, differentiate their products and deliver strong customer service are more likely to be successful in this market.

The use of data mining and predictive modeling is used by more and more carriers to target the most profitable business, and carriers have further segmented their pricing plans to expand market share in what they believe to be the most profitable segments. The Company is investingcontinues to invest in capabilities to better utilize data and analytics, and thereby, refine and manage underwriting and pricing.

Also, new automobile technology advancements, including lane departure warnings, backup cameras, automatic braking and active collision alerts, are being deployed rapidly and are expected to improve driver safety and reduce the likelihood of vehicle collisions. However, these features include expensive parts, potentially increasing average claim severity.

|

|

| PROPERTY & CASUALTY OTHER OPERATIONS |

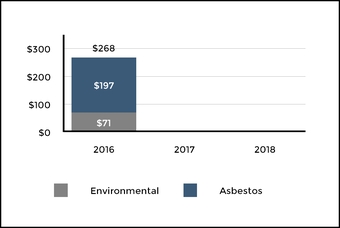

Property & Casualty Other Operations includes certain property and casualty operations, managed by the Company, that have discontinued writing new business and includes substantially all of the Company's asbestos and environmental ("A&E") exposures.

For a discussion of coverages provided under policies written with exposure to A&E, assumed reinsurance and all other non-A&E, see Part II, Item 7, MD&A - Critical Accounting Estimates, Property & Casualty Insurance Product Reserves.

Part I - Item 1. Business

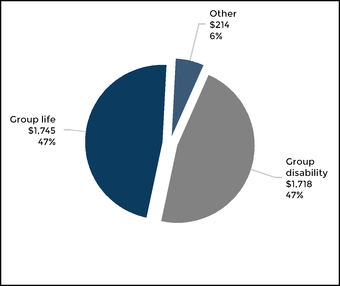

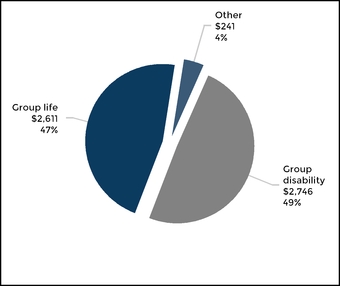

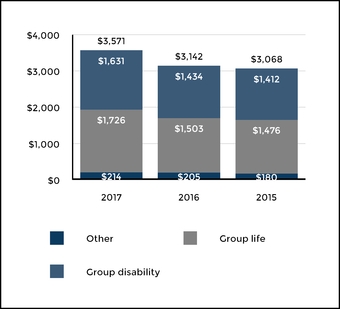

20172018 Premiums and Fee Income of $3,677$5,598

Principal Products and Services

|

| |

| Group Life | Typically is term life insurance provided in the form of yearly renewable term life insurance. Other life coverages in this category include accidental death and dismemberment and travel accident insurance. |

| Group Disability | Typically comprised of both short-term and long-term disability coverage that pays a percentage of an employee’s salary for a period of time if they are ill or injured and cannot perform the duties of their job. Short-term and long-term disability policies have elimination periods that must be satisfied prior to benefit payments. In addition to premiums, administrative service fees are paid by employers forThe Company also earns fee income from leave management services and the administration of underwriting, enrollment and claims processing for employer self-funded plans. |

| Other Products | Includes other group coverages such as retiree health insurance, critical illness, accident, hospital indemnity and participant accident coverages. |

Group insurance typically covers an entire group of people under a single contract, most typically the employees of a single employer or members of an association.

Group Benefits provides group life, disability and other group coverages to members of employer groups, associations and affinity groups through direct insurance policies and provides reinsurance to other insurance companies. In addition to employer paid coverages, Group Benefitsthe segment offers voluntary product coverages which are offered through employee payroll deductions. Group Benefits also offers disability underwriting, administration, and claims processing to self-funded employer plans. In addition, Group Benefitsthe segment offers a single-company leave management solution,The Hartford Productivity Advantage, which integrates work absence data from the insurer’s short-term and long-term group disability and workers’ compensation insurance with its leave management administration services.

Group Benefits generally offers term insurance policies, allowing for the adjustment of rates or policy terms in order to minimize the adverse effect of market trends, loss costs, declining interest rates and other factors. Policies are typically sold with one, two or three-year rate guarantees depending upon the product and market segment.

On November 1, 2017, the Company's group benefits subsidiary, Hartford Life and Accident Insurance Company ("HLA") acquired Aetna's U.S. group life and disability business through a reinsurance transaction. Revenues and earnings of the Aetna U.S. group life and disability business are included in operating results of the Company's Group Benefits segment since the acquisition date. For discussion of this transaction, see Note 2- Business Acquisitions of Notes to Consolidated Financial Statements.

Marketing and Distribution

The Group Benefits distribution network is managed through a regional sales office system to distribute its group insurance products and services through a variety of distribution outlets including brokers, consultants, third-party administrators and trade associations. Additionally, Group Benefitsthe segment has relationships with several private exchanges which offer its products to employer groups.

The acquisition of Aetna's U.S. group life and disability business further enhancesenhanced Group Benefit's distribution footprint by increasing its sales force. The acquisition also providesprovided Group Benefits an exclusive, multi year collaboration to sell it's group life and disability products through Aetna's medical sales team.

Part I - Item 1. Business

Competition

Group Benefits competes with numerous insurance companies and financial intermediaries marketing insurance products. In order to differentiate itself, Group Benefits uses its risk management expertise and economies of scale to derive a competitive advantage. Competitive factors include the extent of products offered, price, the quality of customer and claims handling services, and the Company's relationship with third-party distributors and private exchanges. Active price competition continues in the marketplace, resulting in multi-year rate guarantees being offered to customers. Top tier insurers in the marketplace also offer on-line and self service capabilities to third party distributors and consumers. The relatively large size and underwriting capacity of the Group Benefits business provides a competitive advantage over smaller companies.competitors.

Group Benefits' recent acquisition of Aetna's U.S. group life and disability business further increasesincreased its market presence and

competitive capabilities through the addition of industry-leading digital technology and an integrated absence management and claims platform.

Additionally, as employers continue to focus on reducing the cost of employee benefits, we expect more companies to offer voluntary products paid for by employees. Competitive factors affecting the sale of voluntary products include the breadth of products, product education, enrollment capabilities and overall customer service.

The Company has expanded its employer group product offerings, including the voluntary product suite, including coverages for short term absences from work, critical illness and accident coverages. The Company's enhanced enrollment and marketing tools, such as My Tomorrow©, are providing additional opportunities to educate individual participants about supplementary benefits and deepen their knowledge about product selection.

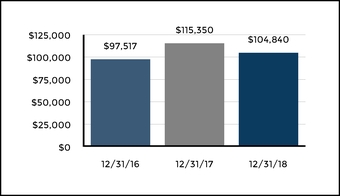

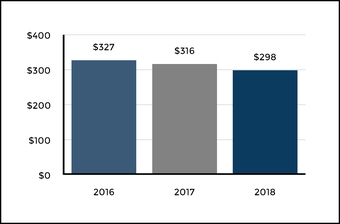

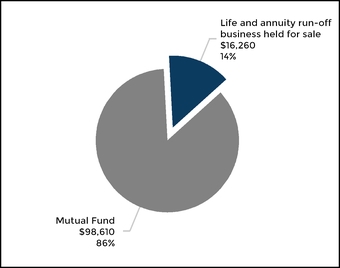

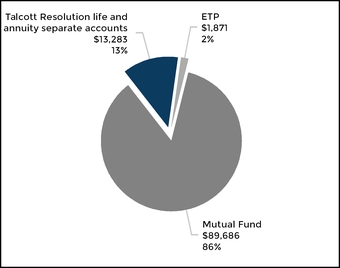

MutualHartford Funds Segment AUM of $115,350 [1]$104,840 as of December 31, 2017

[1] Includes Mutual Fund Segment AUM for ETPs of $480.2018

Mutual Fund AUM as of December 31, 20172018

Principal Products and Services

|

| |

Mutual FundFunds | Includes over 7570 actively managed open-ended mutual funds across a variety of asset classes including domestic and international equity, fixed income, and multi-strategy investments, principally subadvised by two unaffiliated institutional asset management firms that have comprehensive global investment capabilities. |

| ETP | Includes a suite of exchange-traded products (“ETP”) traded on the New York Stock Exchange that is comprised of strategic beta and actively managed fixed income of exchange-traded funds ("ETF"). Strategic beta ETF’s are designed to track indices using both active and passive investment techniques that strive to improve performance relative to traditional capitalization weighted indices.

|

LifeTalcott Resolution life and annuity run-offseparate accounts | Relates to assets of the life and annuity business held for sale | Includes assets heldsold in separate accounts classified as assets held for sale, which support legacy run-off variable insurance contracts.May 2018 that are still managed by the Company's Hartford Funds segment. |

The MutualHartford Funds segment provides investment management, administration, product distribution and related services to investors through a diverse set of investment products in domestic and international markets. Our comprehensive range ofHartford Funds'

comprehensive range of products and services assist clients in achieving their desired investment objectives. Our assetsAssets under management are separated into three distinct categories referred to as mutual funds, (“Funds”), ETP and Talcott Resolution life and annuity run-off business held for

Part I - Item 1. Business

sale (formerly referredseparate accounts, which relate to as “Talcott Resolution”).the life and annuity business sold in May 2018. The MutualHartford Funds segment expectswill continue to continue managingmanage the mutual fund assets of the life and annuity run-off business after the Company closes the sale during 2018,Talcott Resolution, though thosethese assets are expected to continue to decline over time.

Marketing and Distribution

Our Fundsfunds and ETPs are sold through national and regional broker-dealer organizations, independent financial advisers, defined contribution plans, financial consultants, bank trust groups and registered investment advisers. Our distribution team is organized to sell primarily in the United States. The investment products for the life and annuity run-off business held for saleTalcott Resolution are not actively distributed.

Competition

The investment management industry is mature and highly competitive. Firms are differentiated by investment performance, range of products offered, brand recognition, financial strength, proprietary distribution channels, quality of service and level of fees charged relative to quality of investment products. The MutualHartford Funds segment competes with a large number of asset management firms and other financial institutions and differentiates itself through superior fund performance, product breadth, strong distribution and competitive fees. In recent years demand for lower cost passive investment strategies has outpaced demand for actively managed strategies and has taken market share from active managers.

The Company includes in the Corporate category discontinued operations frominvestment management fees and expenses related to managing third party business, including management of the Company's life and annuity run-off business accounted for as held for sale,invested assets of Talcott Resolution, reserves for run-off structured settlement and terminal funding agreement liabilities, retained, capital raising

activities (including debt financing and related interest expense), purchase accounting adjustments related to goodwill and other expenses not allocated to the reporting segments.

Additionally, included in the Corporate category are discontinued operations from the Company's life and annuity business sold in May 2018 and a 9.7% ownership interest in the legal entity that acquired this business. The assets and liabilities of this business had been accounted for as held for sale until closing and operating results of the life and annuity business are included in discontinued operations for all periods prior to the closing date.

RESERVES

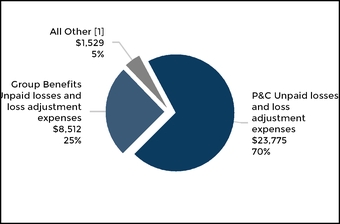

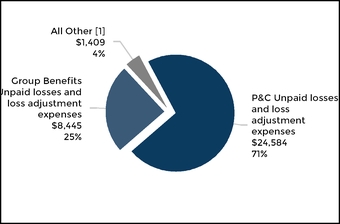

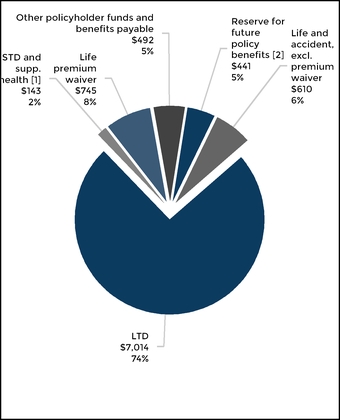

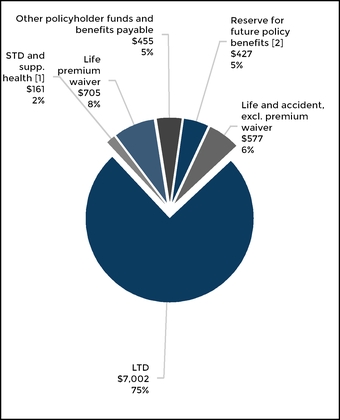

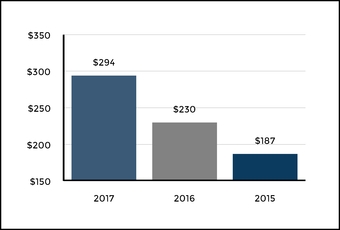

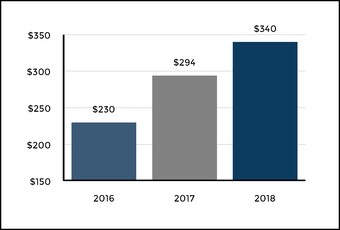

Total Reserves as of December 31, 20172018

| |

| [1] | Includes reserves for future policy benefits and other policyholder funds and benefits payable of $713642 and $816767, respectively, of which $441427 and $492455, respectively, relate to the Group Benefits segment with the remainder related to retained liferun-off structured settlement and annuity run-off business reservesterminal funding agreements within Corporate. |

Total Property & Casualty Reserves as of December 31, 20172018

The reserve for unpaid losses and loss adjustment expenses includes a liability for unpaid losses, including those that have been incurred but not yet reported, as well as estimates of all expenses associated with processing and settling these insurance claims, including reserves related to both Property & Casualty and Group Benefits.

Further discussion of The Hartford’s property and casualty insurance product reserves, including asbestos and environmental claims reserves within P&C Other Operations,

Part I - Item 1. Business

may be found in Part II, Item 7, MD&A — Critical Accounting Estimates — Property and Casualty Insurance Product Reserves. Additional discussion may be found in Notes to Consolidated

Part I - Item 1. Business

Financial Statements, including in the Company’s accounting policies for insurance product reserves within Note 1 - Basis of Presentation and Significant Accounting Policies and in Note 11 - Reserve for Unpaid Losses and Loss Adjustment Expenses of Notes to Consolidated Financial Statements.

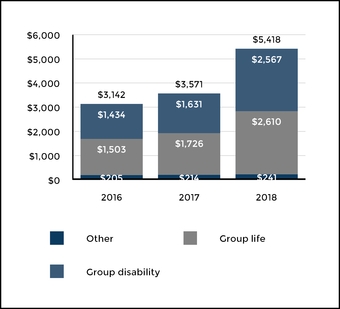

Total Group Benefits Reserves as of December 31, 20172018

[1]Includes $104$118 of short-term disability ("STD") reserves and $39$43 of supplemental health reserves.

[2]Includes $320$311 of paid up life reserves $110and policy reserves on life policies, $107 of reserves for conversions to individual life and $11$9 of other reserves.

Other policyholder funds and benefits payable represent deposits from policyholders where the company does not have insurance risk but is subject to investment risk. Reserves for future policy benefits represent life-contingent reserves for which the company is subject to insurance and investment risk.

Further discussion of The HartfordHartford's Group Benefits long-term disability reserves may be found in Part II, Item 7, MD&A — Critical Accounting Estimates — Group Benefits Long-term Disability ("LTD") Reserves, Net of Reinsurance. Additional discussion may be found in Note 11 - Reserve for Unpaid Losses and Loss Adjustment Expenses of Notes to Consolidated Financial Statements.

UNDERWRITING FOR P&C AND GROUP BENEFITS

The Company underwrites the risks it insures in order to manage exposure to loss through favorable risk selection and diversification. Risk modeling is used to manage, within specified limits, the aggregate exposure taken in each line of business and across the Company. For property and casualty business, aggregate exposure limits are set by geographic zone and peril. Products are priced according to the risk characteristics of the insured’s exposures. Rates charged for Personal Lines products are filed with the states in which we write business. Rates for Commercial Lines products are also filed with the states but the premium charged may be modified based on the insured’s relative risk profile and workers’ compensation policies may be subject to modification based on prior loss experience. Pricing for Group Benefits products, including long-term disability and life insurance, is also based on an underwriting of the risks and a projection of estimated losses, including consideration of investment income.

Pricing adequacy depends on a number of factors, including the ability to obtain regulatory approval for rate changes, proper evaluation of underwriting risks, the ability to project future loss cost frequency and severity based on historical loss experience adjusted for known trends, the Company’s response to rate actions taken by competitors, its expense levels and expectations about regulatory and legal developments. The Company seeks to price its insurance policies such that insurance premiums and future net investment income earned on premiums received will cover underwriting expenses and the ultimate cost of paying claims reported on the policies and provide for a profit margin.

Geographic Distribution of Earned Premium (% of total)

|

| | | | | | | | |

| Location | Commercial Lines | Personal Lines | Group Benefits | Total |

| California | 8 | % | 2 | % | 3 | % | 13 | % |

| New York | 5 | % | 1 | % | 3 | % | 9 | % |

| Texas | 3 | % | 2 | % | 2 | % | 7 | % |

| Florida | 2 | % | 2 | % | 2 | % | 6 | % |

| New Jersey | 3 | % | — | % | 2 | % | 5 | % |

| All other [1] | 23 | % | 15 | % | 22 | % | 60 | % |

| Total | 44 | % | 22 | % | 34 | % | 100 | % |

|

| | | | | | | | |

| Location | Commercial Lines | Personal Lines | Group Benefits | Total |

| California | 8 | % | 3 | % | 2 | % | 13 | % |

| Texas | 4 | % | 2 | % | 1 | % | 7 | % |

| New York | 5 | % | 2 | % | 1 | % | 8 | % |

| Florida | 2 | % | 2 | % | 1 | % | 5 | % |

| All other [1] | 30 | % | 17 | % | 20 | % | 67 | % |

| Total | 49 | % | 26 | % | 25 | % | 100 | % |

| |

| [1] | No other single state or country accounted for 5% or more of the Company's consolidated earned premium written in 2017.2018. |

Part I - Item 1. Business

CLAIMS ADMINISTRATION FOR P&C AND GROUP BENEFITS

Claims administration includes the functions associated with the receipt of initial loss notices, claims adjudication and estimates,

Part I - Item 1. Business

legal representation for insureds where appropriate, establishment of case reserves, payment of losses and notification to reinsurers. These activities are performed by approximately 6,6006,720 claim professionals located in 49 states, organized to meet the specific claim service needs for our various product offerings. Our combined Workers’ Compensation and Group Benefits units enable us to leverage synergies for improved outcomes.

Claim payments for benefit, loss and loss adjustment expenses are the largest expenditure for the Company.

REINSURANCE

For discussion of reinsurance, see Part II, Item 7, MD&A — Enterprise Risk Management and Note 8 - Reinsurance of Notes to Consolidated Financial Statements.

INVESTMENT OPERATIONS

Hartford Investment Management Company (“HIMCO”) is an SEC registered investment advisor and manages the Company's investment operations. HIMCO provides customized investment strategies primarily for The Hartford's investment portfolio, as well as for The Hartford's pension plan certain investment options in Hartford Life Insurance Company's corporate owned life insurance products, a variable insurance trust and institutional clients. In connection with the pending sale of the Company’s life and annuity run-off business sold in May 2018, HIMCO will continue to manage a significant majority of the assetsentered into an agreement for an initial five year term.term to manage the invested assets of Talcott Resolution.

As of December 31, 20172018 and 20162017, the fair value of HIMCO’s total assets under management was approximately $89.6 billion and $98.6 billion and $98.3 billion, respectively, of which $40.2 billion and $2.1 billion and $2.2 billion, respectively, were held in HIMCO managed third party accounts and of which $29.6 billion and $30.9 billion, respectively, relate to assets of the life and annuity run-off business accounted for as held for sale.accounts.

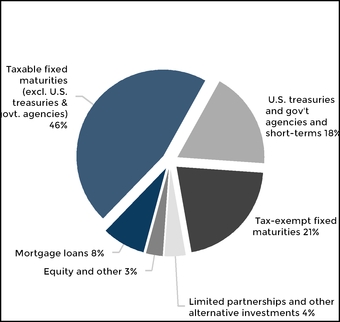

Management of The Hartford's Investment Portfolio

HIMCO manages the Company's investment portfolios to maximize economic value and generate the returns necessary to support the Hartford’s various product obligations, within internally established objectives, guidelines and risk tolerances. The portfolio objectives and guidelines are developed based upon the asset/liability profile, including duration, convexity and other characteristics within specified risk tolerances. The risk tolerances considered include, but are not limited to, asset sector, credit issuer allocation limits, and maximum portfolio limits for below investment grade holdings. The Company attempts to minimize adverse impacts to the portfolio and the Company’s results of operations from changes in economic conditions

through asset diversification, asset allocation limits, asset/liability duration matching and the use of derivatives. For further discussion of HIMCO’s portfolio management approach, see Part II, Item 7, MD&A — Enterprise Risk Management.

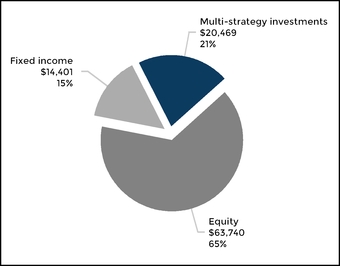

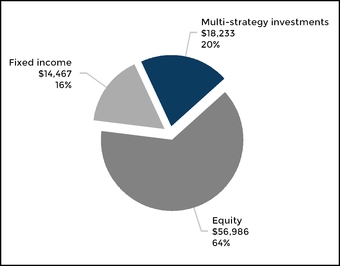

The Hartford's Investment Portfolio of $46.8 billion as of December 31, 20172018

ENTERPRISE RISK MANAGEMENT

The Company has insurance, operational and financial risks. For discussion on how The Hartford manages these risks, see Part II, Item 7, MD&A - Enterprise Risk Management.

REGULATION

State Insurance Laws

State insurance laws are intended to supervise and regulate insurers with the goal of protecting policyholders and ensuring the solvency of the insurers. As such, the insurance laws and regulations grant broad authority to state insurance departments (the “Departments”) to oversee and regulate the business of insurance. The Departments monitor the financial stability of an insurer by requiring insurers to maintain certain solvency standards and minimum capital and surplus requirements; invested asset requirements; state deposits of securities; guaranty fund premiums; restrictions on the size of risks which may be insured under a single policy; and adequate reserves and other necessary provisions for unearned premiums, unpaid losses and loss adjustment expenses and other liabilities, both reported and unreported. In addition, the Departments perform periodic market and financial examinations of insurers and require insurers to file annual and other reports on the financial condition of the companies. Policyholder protection is also regulated by the Departments through licensing of insurers, sales employees, agents and brokers and others; approval of premium rates and

Part I - Item 1. Business

policy forms; claims administration requirements; and maintenance of minimum rates for accumulation of surrender values.

Many states also have laws regulating insurance holding company systems. These laws require insurance companies, which are

Part I - Item 1. Business

formed and chartered in the state (referred to as “domestic insurers”), to register with the state department of insurance (referred to as their “domestic state or regulator”) and file information concerning the operations of companies within the holding company system that may materially affect the operations, management or financial condition of the insurers within the system. Insurance holding company regulations principally relate to (i) state insurance approval of the acquisition of domestic insurers, (ii) prior review or approval of certain transactions between the domestic insurer and its affiliates, and (iii) regulation of dividends made by the domestic insurer. All transactions within a holding company system affecting domestic insurers must be determined to be fair and equitable.

The National Association of Insurance Commissioners (“NAIC”), the organization that works to promote standardization of best practices and assists state insurance regulatory authorities and insurers, conducted the “Solvency Modernization Initiative” (the “Solvency Initiative” ).). The effort focused on reviewing the U.S. financial regulatory system and financial regulation affecting insurance companies including: (1) capital requirements; (2) corporate governance and risk management; (3) group supervision; (4) statutory accounting and financial reporting; and (5) reinsurance. As a result of the Solvency Initiative, among other items, the NAIC adopted the Corporate Governance Annual Disclosure Model Act, , which was enacted by the Company’s lead domestic state of Connecticut. The model law requires insurers to make an annual confidential filing regarding their corporate governance policies commencing in 2016. In addition, the NAIC adopted the Risk Management and Own Risk and Solvency Assessment Model Act (“ORSA”), which also has been adopted by Connecticut. ORSA requires insurers to maintain a risk management framework and conduct an internal risk and solvency assessment of the insurer’s material risks in normal and stressed environments. Many state insurance holding company laws, including those of Connecticut, have also been amended to require insurers to file an annual confidential enterprise risk report with their lead domestic regulator, disclosing material risks within the entire holding company system that could pose an enterprise risk to the insurer.

Federal and State Securities and Financial Regulation Laws

Certain subsidiaries of theThe Company soldsells and distributed the Company’s retaildistributes its mutual funds variable annuitiesthrough a broker dealer subsidiary, and other securities as broker-dealers and areis subject to regulation promulgated and enforced by the Financial Industry Regulatory Authority (“FINRA”), the SEC and/or, in some instances, state securities administrators. Other subsidiaries operate as investment advisers registered with the SEC under the Investment Advisers’ Act of 1940, as amended, and are registered as investment advisers under certain state laws, as applicable. Because federal and state laws and regulations are primarily intended to protect investors in securities markets, they generally grant regulators broad rulemaking and enforcement authority. Some of these regulations include, among other things, regulations impacting sales methods, trading practices, suitability of investments, use

and safekeeping of customers’ funds, corporate governance, capital, record keeping,recordkeeping, and reporting requirements.

The Hartford operates in limited foreign jurisdictions. The extent of financial services regulation on business outside the United

States varies significantly among the countries in which The Hartford operates. Some countries have minimal regulatory requirements, while others regulate financial services providers extensively. Foreign financial services providers in certain countries are faced with greater restrictions than domestic competitors domiciled in that particular jurisdiction.

Failure to comply with federal and state laws and regulations may result in fines, the issuance of cease-and-desist orders or suspension, termination or limitation of the activities of our operations and/or our employees.

INTELLECTUAL PROPERTY

We rely on a combination of contractual rights and copyright, trademark, patent and trade secret laws to establish and protect our intellectual property.

We have a trademark portfolio that we consider important in the marketing of our products and services, including, among others, the trademarks of The Hartford name, the Stag Logo and the combination of these two trademarks. The duration of trademark registrations may be renewed indefinitely subject to country-specific use and registration requirements. We regard our trademarks as highly valuable assets in marketing our products and services and vigorously seek to protect them against infringement. In addition, we own a number of patents and patent applications relating to on-line quoting, insurance related processing, insurance telematics, proprietary interface platforms, and other matters, some of which may be important to our business operations. Patents are of varying duration depending on filing date, and will typically expire at the end of their natural term.

EMPLOYEES

The Hartford has approximately 16,40018,500 employees as of December 31, 20172018.

AVAILABLE INFORMATION

The Company’s Internet address is www.thehartford.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available, without charge, on the investor relations section of our website, https://ir.thehartford.com, as soon as reasonably practicable after they are filed electronically with the SEC. Reports filed with the SEC may be viewed at www.sec.gov or obtained at the SEC’s Public Reference Room at 100 F Street, N.E., Washington D.C. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.www.sec.gov. References in this report to our website address are provided only as a convenience and do not constitute, and should not be viewed as, an incorporation by reference of the information contained on, or available through, the website. Therefore, such information should not be considered part of this report.

Part I - Item 1A. Risk Factors

Item 1A. RISK FACTORS

In deciding whether to invest in The Hartford, you should carefully consider the following risks, any of which could have a material adverse effect on our business, financial condition, results of operation or liquidity and could also impact the trading price of our securities. These risks are not exclusive, and additional risks to which we are subject include, but are not limited to, the factors mentioned under “Forward-Looking Statements” above and the risks of our businesses described elsewhere in this Annual Report on Form 10-K.

The following risk factors have been organized by category for ease of use, however many of the risks may have impacts in more than one category. The occurrence of certain of them may, in turn, cause the emergence or exacerbate the effect of others. Such a combination could materially increase the severity of the impact of these risks on our business, results of operations, financial condition or liquidity.

As noted below under “Risks Relating to the Pending Sale of Our Life and Annuity Business," the assets and liabilities of the life and annuity run-off business, consisting primarily of the operations of Hartford Life Insurance Company and Hartford Life and Annuity Insurance Company (formerly known as Talcott Resolution), have been accounted for as held for sale as of December 31, 2017, with the operating results of that business included in discontinued operations for all periods presented. The Company expects the sale to close by June 30, 2018, subject to regulatory approval and other closing conditions. Apart from interest expense on debt issued and outstanding of Hartford Life, Inc., the holding company of the life and annuity run-off business, and certain tax benefits to be retained by The Hartford, the results from the discontinued operations inure to the buyer. Accordingly, any earnings or losses of the life and annuity run-off business up until closing will not change the Company's results. If the sale of the business does not close, we would retain the risks associated with the life and annuity run-off business.

Risks Relating to Economic, Political and Global Market Conditions

Unfavorable economic, political and global market conditions may adversely impact our business and results of operations.

The Company’s investment portfolio and insurance liabilities are sensitive to changes in economic, political and global capital market conditions, such as the effect of a weak economy and changes in credit spreads, equity prices, interest rates and inflation. Weak economic conditions, such as high unemployment, low labor force participation, lower family income, a weak real estate market, lower business investment and lower consumer spending may adversely affect the demand for insurance and financial products and lower the Company’s profitability in some cases. In addition, a deterioration in global economic conditions, including due to a trade war, tariffs or other actions with respect to international trade agreements or policies, has the potential to, among other things, reduce demand for our products, reduce exposures we insure, drive higher inflation that could increase the Company’s loss costs and result in increased incidence of claims, particularly for workers’ compensation and disability claims. The Company’s investment portfolio includes limited partnerships and other alternative investments and equity securities for which

changes in value are reported in earnings. These investments may be adversely impacted by political turmoil and economic volatility, including real estate market deterioration, which could impact our net investment returns and result in an adverse impact on operating results.

Below are several key factors impacted by changes in economic, political, and global market conditions and their potential effect on the Company’s business and results of operation:

| |

| • | Credit Spread Risk - Credit spread exposure is reflected in the market prices of fixed income instruments where lower |

Credit Spread Risk- Credit spread exposure is reflected in the market prices of fixed income instruments where lower rated securities generally trade at a higher credit spread. If issuer credit spreads increase or widen, the market value of our investment portfolio may decline. If the credit spread widening is significant and occurs over an extended period of time, the Company may recognize other-than-temporary impairments, resulting in decreased earnings. If credit spreads tighten, significantly, the Company’s net investment income associated with new purchases of fixed maturities may be reduced. In addition, the value of credit derivatives under which the Company assumes exposure or purchases protection are impacted by changes in credit spreads, with losses occurring when credit spreads widen for assumed exposure or when credit spreads tighten if credit protection has been purchased.

Equity Markets Risk - A decline in equity markets may result in unrealized capital losses on investments in equity securities recorded against net income and lower earnings from Mutual Funds where fee income is earned based upon the fair value of the assets under management. Equity markets are unpredictable. In early 2018, the equity markets were more volatile than in the months prior, which could be indicative of a greater risk of a decline.

Interest Rate Risk -Global economic conditions may result in the persistence of a low interest rate environment which would continue to pressure our net investment income and could result in lower margins on certain products.

| |

| • | Equity Markets Risk - A decline in equity markets may result in unrealized capital losses on investments in equity securities recorded against net income and lower earnings from Hartford Funds where fee income is earned based upon the fair value of the assets under management. Equity markets are unpredictable. During 2018, the equity markets were more volatile than in prior periods, which could be indicative of a greater risk of a decline. For additional information on equity market sensitivity, see Part II, Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operation (MD&A), Enterprise Risk Management, Financial Risk- Equity Risk. |

| |

| • | Interest Rate Risk -Global economic conditions may result in the persistence of a low interest rate environment which would continue to pressure our net investment income and could result in lower margins on certain products. For additional information on interest rate sensitivity, see Part II, Item 7, MD&A, Enterprise Risk Management, Financial Risk - Interest Rate Risk |

New and renewal business for our property and casualty and group benefits products is priced based onconsidering prevailing interest rates. As interest rates decline, in order to achieve the same economic return, we would have to increase product prices to offset the lower anticipated investment income earned on invested premiums. Conversely, as interest rates rise, pricing targets will tend to decrease to reflect higher anticipated investment income. Our ability to effectively react to such changes in interest rates may affect our competitiveness in the marketplace, and in turn, could reduce written premium and earnings. For additional information on interest rate sensitivity, see Part II, Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operation (MD&A), Enterprise Risk Management, Financial Risk - Interest Rate Risk.

In addition, due to the long-term nature of the liabilities within our Group Benefits operations, particularly for long-term disability, declines in interest rates over an extended period of time would result in our having to reinvest at lower yields. On the other hand, a rise in interest rates, in the absence of other countervailing changes, would reduce the market value of our investment portfolio. A decline in market value of invested assets due to an increase in interest rates could also limit our ability to realize tax benefits from previously recognized capital losses.

Part I - Item 1A. Risk Factors

Inflation Risk - Inflation is a risk to our property and casualty business because, in many cases, claims are paid out many years after a policy is written and premium is collected for the risk. Accordingly, a greater than expected increase in inflation related to the cost of medical services and repairs over the claim settlement period can result in higher claim costs than what was estimated at the time the policy was written. Inflation can also affect consumer spending and business investment which can reduce the demand for our products and services.

| |