FORM 10-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

| | | | | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended | December 31, 20222023 |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ______ to ______ |

| Commission file number | 1-10816 |

MGIC Investment Corporation

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | |

| Wisconsin | | 39-1486475 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 250 E. Kilbourn Avenue | | |

| Milwaukee, | Wisconsin | | 53202 |

| (Address of principal executive offices) | | (Zip Code) |

| (414) | | 347-6480 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common stock, par value $1 per share | | MTG | | New York Stock Exchange |

| | | | |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒

| Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐ |

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If the securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements the required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

MGIC Investment Corporation 2023 Form 10-K | 1

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter. : Approximately $4.6$4.4 billion*

MGIC Investment Corporation 2022 Form 10-K | 1

* Solely for purposes of computing such value and without thereby admitting that such persons are affiliates of the Registrant, shares held by directors and executive officers of the Registrant are deemed to be held by affiliates of the Registrant. Shares held are those shares beneficially owned for purposes of Rule 13d-3 under the Securities Exchange Act of 1934 but excluding shares subject to stock options.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: As of February 17, 2023,16, 2024, there were 290,428,422269,669,667 shares of common stock of the registrant, par value $1.00 per share, outstanding.

The following documents have been incorporated by reference in this Form 10-K, as indicated:

| | | | | | | | |

| Document | | Part and Item Number of Form 10-K Into Which Incorporated* |

Proxy Statement for the 20232024 Annual Meeting of Shareholders, provided such Proxy Statement is filed within 120 days after December 31, 2022.2023. If not so filed, the information provided in Items 10 through 14 of Part III will be included in an amended Form 10-K filed within such 120 day period. | | Items 10 through 14 of Part III |

* In each case, to the extent provided in the Items listed.

MGIC Investment Corporation 20222023 Form 10-K | 2

MGIC Investment Corporation and Subsidiaries

| | | | | | | | | | | |

| Table of Contents |

| | Page No. |

| PART I | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | Cybersecurity | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| PART II | | |

| Item 5. | | |

| Item 6. | Reserved. | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| PART IV | | |

| Item 15. | | |

| Item 16. | | |

| | |

| | |

MGIC Investment Corporation 20222023 Form 10-K | 3

Glossary of terms and acronyms

/ A

ARMs

Adjustable rate mortgages

ABS

Asset-backed securities

Annual Persistency

The percentage of our insurance remaining in force from one year prior. As of September 30, 2023, we refined our methodology for calculating our Annual Persistency by excluding the amortization of the principal balance. All prior periods have been revised

ASC

Accounting Standards Codification

Available Assets

Assets, as designated under the PMIERs, that are readily available to pay claims, and include the most liquid investments

/ B

Book or book year

A group of loans insured in a particular calendar year

BPMI

Borrower-paid mortgage insurance

BPS

Basis Points

/ C

CECL

Current expected credit losses covered under ASC 326

CFPB

Consumer Financial Protection Bureau

CLO

Collateralized loan obligations

CMBS

Commercial mortgage-backed securities

COVID-19 Pandemic

An outbreak of the novel coronavirus disease, later named COVID-19. The outbreak of COVID-19 was declared a pandemic by the World Health Organization and a national emergency in the United States in March 2020

CRT

Credit risk transfer. The transfer of a portion of mortgage credit risk to the private sector through different forms of transactions and structures

/ D

DAC

Deferred insurance policy acquisition costs

Debt-to-income ("DTI") ratio

The ratio, expressed as a percentage, of a borrower's total debt payments to gross income

Delinquent Loan

A loan that is past due on a mortgage payment. A delinquent loan is typically reported to us by servicers when the loan has missed two or more payments. A loan will continue to be reported as delinquent until it becomes current or a claim payment has been made. A delinquent loan is also referred to as a default

Delinquency Rate

The percentage of insured loans that are delinquent

Direct

Before giving effect to reinsurance

/ E

EPS

Earnings per share

/ F

Fannie Mae

Federal National Mortgage Association

FCRA

Fair Credit Reporting Act

FHA

Federal Housing Administration

FHFA

Federal Housing Finance Agency

FHLB

Federal Home Loan Bank of Chicago, of which MGIC is a member

MGIC Investment Corporation 2023 Form 10-K | 4

MGIC Investment Corporation and Subsidiaries

FICO score

A measure of consumer credit risk provided by credit bureaus, typically produced from statistical models by Fair Isaac Corporation utilizing data collected by the credit bureaus

Freddie Mac

Federal Home Loan Mortgage Corporation

/ G

GAAP

Generally Accepted Accounting Principles in the United States

GSEs

Government Sponsored Enterprise. Collectively, Fannie Mae and Freddie Mac

MGIC Investment Corporation 2022 Form 10-K | 4

MGIC Investment Corporation and Subsidiaries

/ H

HAMP

Home Affordable Modification Program

HARP

Home Affordable Refinance Program

Home Re Entities

Unaffiliated special purpose insurers domiciled in Bermuda that participate in our aggregate XOL transactionsTransactions through the ILN market.

Home Re Transactions

Excess-of-loss reinsurance transactions with the Home Re Entities

HOPA

Homeowners Protection Act

HUD

Housing and Urban Development

/ I

IBNR Reserves

Loss reserves established on loans we estimate are delinquent, but for which the delinquency has not been reported to us

IIF

Insurance in force, which for loans insured by us, is equal to the unpaid principal balance, as reported to us

ILN

Insurance-linked notes

/ L

LAE

Loss adjustment expenses, which includes the costs of settling claims, including legal and other expenses and general expenses of administering the claims settlement process.

Loan-to-value ("LTV") ratio

The ratio, expressed as a percentage, of the dollar amount of the first mortgage loan to the value of the property at the time the loan became insured and does not reflect subsequent housing price appreciation or depreciation. Subordinate mortgages may also be present

Long-term debt:

5.75% Notes

5.75% Senior Notes

5.25% Notes

5.25% Senior Notes due on August 15, 2028, with interest payable semi-annually on February 15 and August 15 of each year

9% Debentures

9% Convertible Junior Subordinated Debentures due on April 1, 2063, with interest payable semi-annually on April 1 and October 1 of each year

FHLB Advance or the Advance

1.91% Fixed rate advance from the FHLB

Loss ratio

The ratio, expressed as a percentage, of the sum of net incurred losses and loss adjustment expensesincurred to net premiums earned

Low down payment loans or mortgages

Loans with less than 20% down payments

LPMI

Lender-paid mortgage insurance

/ M

MBS

Mortgage-backed securities

MD&A

Management's discussion and analysis of financial condition and results of operations

MGIC

Mortgage Guaranty Insurance Corporation, a subsidiary of MGIC Investment Corporation

MAC

MGIC Assurance Corporation, a subsidiary of MGIC

Minimum Required Assets

The minimum amount of Available Assets that must be held under the PMIERs, which is based on an insurer's book of RIF and is calculated from tables of factors with several risk dimensions, reduced for credit given for risk ceded under reinsurance transactions, and subject to a floor of $400 million

MGIC Investment Corporation 2023 Form 10-K | 5

MGIC Investment Corporation and Subsidiaries

MPP

Minimum Policyholder Position, as required under certain state requirements. The “policyholder position” of a mortgage insurer is its net worth or surplus, contingency reserve and a portion of the reserves for unearned premiums

MGIC Investment Corporation 2022 Form 10-K | 5

MGIC Investment Corporation and Subsidiaries

/ N

N/A

Not applicable for the period presented

NAIC

The National Association of Insurance Commissioners

NIW

New Insurance Written, is the aggregate original principal amount of the mortgages that are insured during a period

N/M

Data, or calculation, deemed not meaningful for the period presented

NPL Settlement

Non-performing loan,The commutation of coverage on non-performing loans, which is aare delinquent loan,loans, at any stage in its delinquency

/ O

OCI

Office of the Commissioner of Insurance of the State of Wisconsin

/ P

Persistency

The percentage of our insurance remaining in force from one year prior

PMI

Private Mortgage Insurance (as an industry or product type)

PMIERs

Private Mortgage Insurer Eligibility Requirements issued by each of Fannie Mae and Freddie Mac to set forth requirements that an approved insurer must meet and maintain to provide mortgage guaranty insurance on loans delivered to or acquired by Fannie Mae or Freddie Mac, as applicable

Premium Rate

The contractual rate charged for coverage under our insurance policies

Premium Yield

The ratio of premium earned divided by the average IIF outstanding for the period measured

Primary Insurance

Insurance that provides mortgage default protection on individual loans. Primary insurance may be written on a "flow" basis, in which loans are insured in individual, loan-by-loan transactions, or on a "bulk" basis, in which each loan in a portfolio of loans is individually insured in a single bulk transaction

Profit Commission

Payments we receive from reinsurers under each of our quota share reinsurance transactions if the annual loss ratio is below levels specified in the quota share reinsurance transaction

/ Q

QSR Transaction

Quota share reinsurance transaction with a group of unaffiliated reinsurers

20152020 QSR

Our QSR transaction that provided coverage on eligible NIW written prior to 2017

2017 QSR

Our QSR transaction that provided coverage on eligible NIW in 2017

2018 QSR

Our QSR transaction that provided coverage on eligible NIW in 2018

2019 QSR

Our QSR transaction that provided coverage on eligible NIW in 2019

2020 QSR

Our QSR transactions that provide coverage on eligible NIW in 2020

2021 QSR

Our QSR transactions that provideprovides coverage on eligible NIW in 2021

2022 QSR

Our QSR transactions that provide coverage on eligible NIW in 2022

2023 QSR

Our QSR transactionstransaction that provideprovides coverage on eligible NIW in 2023

2024 QSR

Our QSR transaction that provides coverage on eligible NIW in 2024

Credit Union QSR

Our QSR transaction that provides coverage on eligible NIW from credit union institutions originated from April 1, 2020 through December 31, 2025

/ R

RESPA

Real Estate Settlement Procedures Act

MGIC Investment Corporation 2022 Form 10-K | 6

MGIC Investment Corporation and Subsidiaries

RIF

Risk in force, which for an individual loan insured by us, is equal to the unpaid loan principal balance, as reported to us, multiplied by the insurance coverage percentage. RIF is sometimes referred to as exposure

Risk-to-capital

Under certain state regulations, the ratio of RIF, net of reinsurance and exposure on policies currently in default and for which loss reserves have been established, to the level of statutory capital

RMBS

Residential mortgage-backed securities

MGIC Investment Corporation 2023 Form 10-K | 6

MGIC Investment Corporation and Subsidiaries

/ S

State Capital Requirements

Under certain state regulations, the minimum amount of statutory capital relative to risk in force (or similar measure)

/ T

TILA

Truth in Lending Act

Traditional XOL Transaction

Excess-of-loss reinsurance transaction with a group of unaffiliated reinsurers

2022 Traditional XOL

Our XOL transaction that provides coverage on eligible NIW in 2022

2023 Traditional XOL

Our XOL transaction that provides coverage on eligible NIW in 2023

/ U

Underwriting expense ratio

The ratio, expressed as a percentage, of the other underwriting and operating expenses, net and amortization of DAC of our combined insurance operations (which excludes underwriting and operating expenses of our non-insurance subsidiaries) to net premiums written

Underwriting profit

Net premiums earned minus losses incurred, lossesnet and other underwriting and operating expenses, net

USDA

U.S. Department of Agriculture

/ V

VA

U.S. Department of Veterans Affairs

VIE

Variable interest entity

/ X

XOL Transactions

Excess-of-loss reinsurance transactions executed through the Home Re Transactions and the Traditional XOL TransactionTransactions

MGIC Investment Corporation 20222023 Form 10-K | 7

Item 1. Business

A. General

We are a holding company and through wholly-owned subsidiaries we provide private mortgage insurance, other mortgage credit risk management solutions, and ancillary services. In 2022,2023, our total revenues were $1.2 billion and our primary NIW was $76.4$46.1 billion. As of December 31, 2022,2023, our direct primary IIF was $295.3$293.5 billion and our direct primary RIF was $76.5$77.2 billion. For further information about our results of operations, see our consolidated financial statements in Item 8 and our MD&A in Item 7. As of December 31, 2022,2023, our principal mortgage insurance subsidiary, MGIC, was licensed in all 50 states of the United States, the District of Columbia, Puerto Rico and Guam. During 2022,2023, we wrote new insurance in each of those jurisdictions.

20232024 BUSINESS STRATEGIES

Our business strategies continue to be to 1) maximize the value we create through our mortgage credit enhancement activities; 2) differentiate ourselves through our customer experience; 3) establish a competitive advantage through our digital and analytical capabilities; 4) excel at acquiring, managing and distributing mortgage credit risk and the related capital; 5) maintain financial strength through economic cycles; and 6) foster an environment that embraces diversity and best positions our people to succeed.

20222023 ACCOMPLISHMENTS

Following are several of our 20222023 accomplishments that furthered our business strategies.

•Earned $865$713 million of net income ($2.792.49 per diluted share) for the year, compared to $635$865 million ($1.852.79 per diluted share) in 2021.

•Increased primary IIF by more than 7.6% year-over-year.2022.

•Expanded our reinsurance program by securing quota share reinsurance covering the majority of our 2022 and 20232024 NIW, and executingentered into a $330 million excess of loss reinsurance agreement executed through an ILNa mortgage insurance linked notes transaction in the capital market, and the traditionalplaced a forward-commitment excess of loss reinsurance market.agreement covering 2023 NIW. These transactions allow us to better manage our risk profile, and they provide an alternative source of capital.

•Conducted tender offers on certain tranches of our Home Re 2019-1 Ltd., Home Re 2021-1 Ltd., and Home Re 2021-2 Ltd insurance linked notes that were not providing efficient PMIERs benefit. The tender offers resulted in the reduction in the insurance-linked notes of $187.1 million for the Home Re 2019-1 Ltd, $91.1 million for the Home Re 2021-1 Ltd., and $106.7 million for the Home Re 2021-2 Ltd.

•Paid $800$600 million of cash dividends from MGIC to our holding company.

•Maintained financial strength and capital flexibility while returning approximately $497$465 million in capital to shareholders:

◦Repurchased 8.7%7.4% of our shares outstanding at the beginning of the year.

◦Increased cash dividends to shareholders by 25%15% in the second half of 2022.2023.

•Repurchased $89 million of our 2063 Junior Convertible Debentures, which eliminated approximately 6.8 million potentially dilutive shares.

•Redeemed the outstanding principal balance of the 5.75% Senior Notes at a purchase price$21.1 million on our 9% Convertible Junior Subordinated Debentures ("9% Debentures) for cash of $248$28.6 million plus accrued interest.

•Repaid the outstanding principal balancein lieu of the FHLB advance at a prepayment priceissuing shares of $156 million.common stock.

•Established a Transformationan Enterprise Project Management Office to prioritize and Senior Leadership Team (the "SLT") to overseemonitor the progress of our technological investment governanceinitiatives and lead an enterprise-wide business prioritization process.investments. Continued to transform our business processes along a number of dimensions, including modelling, pricing, data and analytics, application programming interfaces, salesmodeling, and underwriting.data management.

•Continued work on our Affordable Housing Strategy through ongoing participation in the Affordable Housing Advisory Board of the Mortgage Bankers Associationsponsored research, partnerships, and support offor local and national organizations including the Urban Institute's Housing Finance Innovation Forum, the National Housing Conference, the Coalition of Community Development Financial Institutions theCoalition, National Association of Hispanic Real Estate Professionals, theNational Association of Local Housing Financing Agencies, National Association of Real Estate Brokers, theand National Conference of State Housing Agencies, and the National Association of Local Housing Finance Agencies.

•Made significantContinued to make progress in our diversity, equity and inclusion ("DEI") work, including the formationlaunch of our "DEI Compass" webinar series, co-worker learning and development opportunities, and a DEI Council, leadership participation in DEI Workshops,community grant program whereby co-workers nominated non-profit organizations to which the Company made donations.

MGIC Investment Corporation 2023 Form 10-K | 8

MGIC Investment Corporation and the creation of a DEI site on the Company's intranet page.Subsidiaries

OVERVIEW OF THE PRIVATE MORTGAGE INSURANCE INDUSTRY AND ITS OPERATING ENVIRONMENT

We established the modern PMI industry in 1957 to provide a private market alternative to federal government insurance programs. PMI covers losses from homeowner defaults on residential mortgage loans, reducing, and in some instances eliminating, the loss to the insured institution.

Fannie Mae and Freddie Mac ("the GSEs") have been the major purchasers of the mortgage loans underlying new insurance written by private mortgage insurers. The GSEs purchase residential mortgage loans as part of their governmental mandate to provide liquidity in the secondary mortgage market. The GSEs cannot buy low down payment mortgage loans without certain forms of credit enhancement. Private mortgage insurance has generally been purchased by lenders in primary mortgage market transactions to satisfy this credit enhancement requirement. Therefore, PMI facilitates the sale of low down payment mortgages in the secondary mortgage market to the GSEs and plays an important role in the housing finance system by assisting consumers, especially first-time and low- and medium-wealth homebuyers, to finance homes with low down payment mortgages. PMI also reduces the regulatory capital that depository institutions are required to hold against certain low down payment mortgages that they hold as assets.

Because the GSEs have been the major purchasers of the mortgages underlying new insurance written by private mortgage insurers, the PMI industry in the U.S. is defined in large part by the requirements and practices of the GSEs. These requirements and practices, as well as those of the federal regulators that oversee the GSEs and lenders, impact the operating results and financial performance of private mortgage insurers. In 2008, the federal

MGIC Investment Corporation 2022 Form 10-K | 8

MGIC Investment Corporation and Subsidiaries

government took control of the GSEs through a conservatorship process. The FHFA is the conservator of the GSEs and has the authority to control and direct their operations.

In 2022 the GSEs submittedeach published Equitable Housing Finance Plans to the FHFA.("Plans"). Updated Plans were subsequently published by each GSE in April 2023. The Plans seek to advance equity in housing finance over a three yearthree-year period and include potential changes to the GSEs’ business practices and policies. Specifically relating to mortgage insurance, (1) Fannie Mae’s Plan contemplatesincludes the creation of special purchasepurpose credit program(s) ("SPCPs") targeted to historically underserved borrowers with a goal of lowering costs for such borrowers through lower than standard mortgage insurance requirements; and (2) Freddie Mac’s Plan contemplatesincludes plans to work with mortgage insurers to look for ways to lower mortgage costs, the creation of SPCPs targeted to historically underserved borrowers, withand the goalsplanned purchase of (a) working with mortgage insurers to reduce costs for high LTV borrowers, and (b) updating mortgage insurance cancellation requirements.loans originated through lender-created SPCPs. To the extent the business practices and policies of the GSEs regarding mortgage insurance coverage, costs and cancellation change, including more broadly than through SPCPs, such changes may negatively impact the mortgage insurance industry.

It is uncertain what role the GSEs, FHA and private capital, including private mortgage insurance, will play in the residential housing finance system in the future. The timing and impact on our business of any resulting changes is uncertain. Some changes would require Congressional action to implement and it is difficult to estimate when any action would be final and how long any associated phase-in period may last.

The GSEs have private mortgage insurer eligibility requirements, or "PMIERs", for private mortgage insurers that insure loans delivered to or purchased by the GSEs. The financial requirements of the PMIERs require a mortgage insurer’s Available Assets to equal or exceed its Minimum Required Assets. MGIC is in compliance with the PMIERs and eligible to insure loans purchased by the GSEs. In calculating Minimum Required Assets, we receiveMGIC receives significant credit for risk ceded under our reinsurance transactions. See "Reinsurance" in this Item 1 for information about our reinsurance transactions and "Regulation – Direct Regulation" in this Item 1 for information about our compliance with the financial requirements of the PMIERs.

The private mortgage insurance industry is greatly impacted by macroeconomic conditions that affect home loan originations and credit performance of home loans, including unemployment rates, home prices, restrictions on mortgage credit due to underwriting standards, interest rates, household formations and homeownership rates. During the years leading up to the financial crisis of the 2000s, the mortgage lending industry increasingly made home loans with higher risk profiles. In certain sections of this Annual Report, we discuss our insurance written in 2005-2008 separately from our insurance written in earlier and later years. Beginning in 2007, job creation slowed and the housing markets began slowing in certain areas, with declines in certain other areas. In 2008 and 2009, employment in the U.S. decreased substantially and nearly all geographic areas in the U.S. experienced home price declines. Together, these conditions resulted in significant adverse developments for us and our industry. The operating environment for private mortgage insurers materially improved after the financial crisis, as the economy recovered.

The COVID-19 pandemic had a material impact on our 2020 financial results. The increased level of unemployment and

economic uncertainty resulted in an increase in the number of mortgage delinquenciesour delinquency inventory for which we recorded increased loss reserves. After reaching 14.7% in April 2020,Since that time, our mortgage delinquency inventory has decreased significantly and is below the unemployment rate declined throughlevels seen immediately before the endonset of 2021, and remained below 4% for most of 2022.the pandemic. The number of delinquent mortgages that we insure has also declined through the end of 2022, after reaching its recent peak in June 2020. Theoverall decline in delinquent mortgages that we insure,the delinquency inventory, along with favorable loss reserve development in 2022recent years has resulted in ourdecreased losses incurred significantly decreasing in 2022 compared to 2021, and ourincreased net income significantly increasing. For a discussion of the various ways the COVID-19 pandemic may impact us in the future, see our Risk Factor titled "The COVID-19 pandemic may materially impact our business and future financial condition" in Item 1A.income.

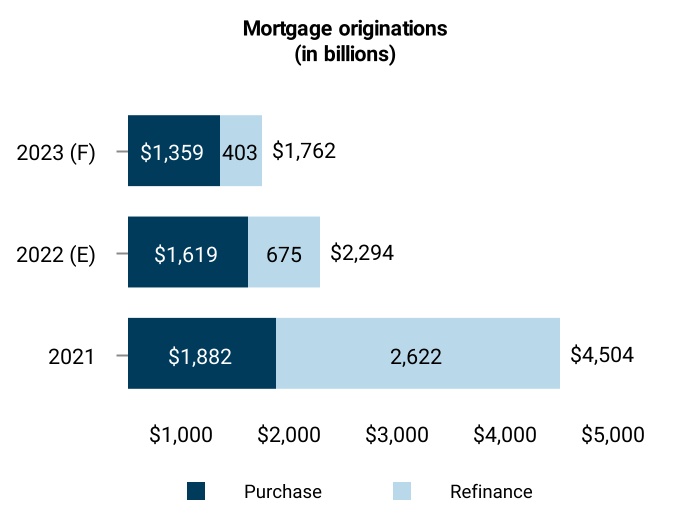

In 2022, $4052023, $284 billion of mortgages were insured with primary coverage by private mortgage insurers, compared to $585$405 for the full year of 2021,2022, and $600$585 billion for full year 2020. The 2022 and 2021 volumes were significantly greater than the recent low in 2010 of $70 billion and greater than the volumes of 2001 through 2007 when, on average, approximately $311 billion of mortgages were insured with primary coverage by private mortgage insurers.2021. The high 2021 and 2020 volumesvolume resulted, in part, from historically low interest rates driving sustained borrower demand, including for refinances, and the effect that the COVID-19 pandemic had on demand for homes.

For most of our business, we and other private mortgage insurers compete directly with federal and state governmental and quasi-governmental agencies that sponsor government-backed mortgage insurance programs, principally the FHA, VA and USDA. The publication Inside Mortgage Finance estimates that in 2022,2023, the FHA accounted for 26.7%33.2% of low down payment residential mortgages

MGIC Investment Corporation 2023 Form 10-K | 9

MGIC Investment Corporation and Subsidiaries

that were subject to FHA, VA, USDA or primary private mortgage insurance, compared to 26.7% in 2022 and 24.7% in 2021 and 23.4% in 2020.2021. Since 2012, the FHA’s market share has been as low as 23.4% (2020) and as high as 42.1% (in 2012). Factors that influence the FHA’s market share include relative rates and fees, underwriting guidelines and loan limits of the FHA, VA, private mortgage insurers and the GSEs; lenders' perceptions of legal risks under FHA versus GSE programs; flexibility for the FHA to establish new products as a result of federal legislation and programs; returns expected to be obtained by lenders for Ginnie Mae securitization of FHA-insured loans compared to those obtained from selling loans to the GSEs for securitization; and differences in policy terms, such as the ability of a borrower to cancel insurance coverage under certain circumstances. The focus ofOn February 22, 2023, the Presidential Administration on equitable housing finance and sustainable housing opportunities increases the likelihood ofFHA announced a reduction30-basis point decrease in the FHA’sits mortgage insurance premium rates. Such aThis rate reduction wouldhas negatively impactimpacted our NIW; however, given the many factors that influence the FHA's market share, it is difficultNIW. We are unable to predict the impact. In addition, we also cannot predictextent of any further impact on our NIW or how the factors that affect the FHA’sFHA's share of NIW will change in the future.

Inside Mortgage Finance estimates that in 2022,2023, the VA accounted for 24.5%21.5% of all low down payment residential mortgages that were subject to FHA, VA, USDA or primary private mortgage insurance, compared to 24.5% in 2022 and 30.2% in 2021 and 30.9% in 2020.2021. Since 2012, the VA's market share has been as lowhigh as 22.8% (in 2013) and as high a 30.9% (in 2020). The VA's 2023 market share was the lowest since 2013 (22.8%). We believe that the VA’s market share grows as the number of borrowers that are eligible for the VA’s program increases and when eligible borrowers opt to use the VA program when refinancing their

MGIC Investment Corporation 2022 Form 10-K | 9

MGIC Investment Corporation and Subsidiaries

mortgages. The VA program offers 100% LTV loans and charges a one-time funding fee that can be included in the loan amount.

The private mortgage insurance industry also competes with alternatives to mortgage insurance, such as investors using risk mitigation and credit risk transfer techniques other than PMI, including capital market transactions entered into by the GSEs and banks; lenders and other investors holding mortgages in portfolio and self-insuring; and “piggyback loans,” which combine a first lien loan with a second lien loan. In 2018, the GSEs initiated secondary mortgage market programs with loan level mortgage default coverage provided by various (re)insurers that are not mortgage insurers governed by PMIERs, and that are not selected by the lenders. While we view these programs as competing with traditional private mortgage insurance, we participate in them through an affiliate of MGIC.

The GSEs (and other investors) have also used other forms of credit enhancement that did not involve traditional private mortgage insurance, such as engaging in credit-linked note transactions executed in the capital markets, orand using other forms of debt issuances or securitizations that transfer credit risk directly to other investors, including competitors and an affiliate of MGIC; and using other risk mitigation techniques in conjunction with reduced levels of private mortgage insurance coverage.

In addition to the FHA, VA, other governmental agencies and the alternatives to mortgage insurance discussed above, we compete with other mortgage insurers. The level of competition, including price competition, within the private mortgage insurance industry has remained intense over the past several years. See "Our Products and Services – Sales and Marketing and Competition – Competition" below for more information about the impact on our business of competition in the private mortgage insurance industry.

In addition to being subject to the requirements and practices of the GSEs, private mortgage insurers are subject to comprehensive, detailed regulation by state insurance departments. The insurance laws of 16 jurisdictions, including Wisconsin, MGIC's domiciliary state, require a mortgage insurer to maintain a minimum amount of statutory capital relative to the RIF (or a similar measure) in order for the mortgage insurer to continue to write new business. The NAIC previously announced plans to revise the minimum capital and surplus requirements for mortgage insurers that are provided forAdditionally, in its Mortgage Guaranty Insurance Model Act. In December 2019, a working group of state regulators released an exposure draft of2023 a revised Mortgage Guaranty Insurance Model Act and a risk-based capital framework to establish capital requirements for mortgage insurers, although certain items were not completely addressedwas adopted by the framework, including the treatment of ceded riskNAIC. The revised Model Act includes requirements relating to, among other things: (i) capital and minimum capital floors. In October 2022,requirements, and contingency reserves; (ii) restrictions on mortgage insurers’ investments in notes secured by mortgages; (iii) prudent underwriting standards and formal underwriting guidelines; (iv) the NAIC working group released a revised exposure draftestablishment of the Mortgageformal, internal “Mortgage Guaranty Insurance Model Act that does not include changesQuality Control Programs” with respect to the capital requirements of the existing Model Act.in-force business; and (v) reinsurance and prohibitions on captive reinsurance arrangements.

GENERAL INFORMATION ABOUT OUR COMPANY

We are a Wisconsin corporation organized in 1984. Our principal office is located at MGIC Plaza, 250 East Kilbourn Avenue, Milwaukee, Wisconsin 53202 (telephone number (414) 347-6480). As used in this annual report, “we,” “our” and “us” refer to MGIC Investment Corporation’s consolidated operations or to MGIC Investment Corporation, as a separate

entity, as the context requires, and “MGIC” refers to Mortgage Guaranty Insurance Corporation.

Our revenues and losses may be materially affected by the risk factors that are included in Item 1A of this annual report and are an integral part of this annual report. These risk factors may also cause actual results to differ materially from the results contemplated by forward looking statements that we may make. Forward looking statements consist of statements that relate to matters other than historical fact. Among others, statements that include words such as we “believe,” “anticipate” or “expect,” or words of similar import, are forward looking statements. We are not undertaking any obligation to update any forward looking statements or other statements we may make even though these statements may be affected by events or circumstances occurring after the forward looking statements or other statements were made. No reader of this annual report should rely on these statements being current at any time other than the time at which this annual report was filed with the Securities and Exchange Commission.

MGIC Investment Corporation 2023 Form 10-K | 10

MGIC Investment Corporation and Subsidiaries

B. Our Products and Services

MORTGAGE INSURANCE

In general, there are two principal types of private mortgage insurance: “primary” and “pool.”

Primary Insurance.Insurance

Primary insurance provides mortgage default protection on individual loans and covers a percentage of the unpaid loan principal, delinquent interest and certain expenses associated with the default and subsequent foreclosure on the mortgage or sale of the underlying property (collectively, the “claim amount”). In addition to the loan principal, the claim amount is affected by the mortgage note rate and the time necessary to complete the foreclosure or sale process. The insurer generally pays the coverage percentage of the claim amount specified in the primary policy but has the option to pay 100% of the claim amount and acquire title to the property. Primary insurance is generally written on first mortgage loans secured by owner occupied "single-family" homes, which are one-to-four family homes and condominiums. Primary insurance can be written on first liens secured by non-owner occupied single-family homes, which are referred to in the home mortgage lending industry as investor loans, and on vacation or second homes. Primary coverage can be used on any type of residential mortgage loan instrument approved by the mortgage insurer.

References in this document to amounts of insurance written or in force, risk written or risk in force, and other historical data related to our insurance refer only to direct (before giving effect to reinsurance) primary insurance, unless otherwise indicated. Primary insurance may be written on a flow basis, in which loans are insured in individual, loan-by-loan transactions, or may be written on a bulk basis, in which each loan in a portfolio of loans is individually insured in a single, bulk transaction. Our new primary insurance written was $46.1 billion in 2023, compared to $76.4 billion in 2022 compared toand $120.2 billion in 2021 and $112.1 billion in 2020.2021. The 20222023 decrease compared to 20212022 reflects a decrease insmaller purchase mortgage originations we insured, as well as a decrease in refinance mortgage originations we insured.market.

MGIC Investment Corporation 2022 Form 10-K | 10

MGIC Investment Corporation and Subsidiaries

The following charts show, on a direct basis, our primary IIF and primary RIF as of December 31 for the years indicated.

| | Primary insurance and risk in force | Primary insurance and risk in force | Primary insurance and risk in force |

| (In billions) | (In billions) | | 2022 | | 2021 | | 2020 | | 2019 | | 2018 | (In billions) | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 |

| Primary IIF | Primary IIF | | $ | 295.3 | | | $ | 274.4 | | | $ | 246.6 | | | $ | 222.3 | | | $ | 209.7 | |

| Primary RIF | Primary RIF | | 76.5 | | | 69.3 | | | 61.8 | | | 57.2 | | | 54.1 | |

For loans sold to a GSE, the coverage percentage must comply with the requirements established by the particular GSE to which the loan is delivered. The GSEs have different loan purchase programs that allow different levels of mortgage insurance coverage. Under the “charter coverage” program, on certain loans lenders may choose a mortgage insurance coverage percentage that is less than the GSEs’ “standard coverage” and only the minimum required by the GSEs’ charters, with the GSEs paying a lower price for such loans. In 2022,2023, a substantial majority of our volume was on loans with GSE standard or higher coverage.

For loans that are not sold to the GSEs, the lender determines the coverage percentage from those that we offer. Higher coverage percentages generally result in increased severity, which is the amount paid on a claim. We charge higher premium rates for higher coverage percentages. However, there can be no assurance that the higher premium rates adequately reflect the risks associated with higher coverage percentages. In accordance with GAAP for the mortgage insurance industry, loss reserves are only established for policies covering delinquent loans. Historically, because relatively few delinquencies occur in the early years of a book of business, the higher premium revenue from higher coverage has been recognized before any significant higher losses resulting from that higher coverage may be incurred. For more information, see “Exposure to Catastrophic Loss; Delinquencies; Claims; Loss Mitigation.”

In general, mortgage insurance coverage cannot be terminated by the insurer. However, subject to certain restrictions on our rescission rights as specified in our insurance policy, we may terminate or rescind coverage for, among other reasons, non-payment of premium, certain material misrepresentations and fraud in connection with the application for the insurance policy. Mortgage insurance coverage isunder monthly or annual premium plans are renewable at the option of the insured lender, at the renewal rate fixed when the loan was initially insured. Lenders may cancel insurance written on a flow basis at any time at their option or because of mortgage repayment, which may be accelerated because of the refinancing of mortgages.

In the case of a loan purchased by a GSE, a borrower may request termination of insurance based on the home’s current value if certain LTV ratio and seasoning requirements are met and the borrowers have an acceptable payment history. For loans seasoned between two and five years, the LTV ratio must be 75% or less, and for loans seasoned more than five years the LTV ratio must be 80% or less. If the borrower has made substantial improvements to the property, the GSEs allow for cancellation once the LTV ratio reaches 80% or less with no minimum seasoning requirement.

Mortgage insurance for loans secured by one-family, primary residences can be canceled under the Homeowners Protection Act (“HOPA”). In general, HOPA requires a servicer to cancel the mortgage insurance if a borrower requests cancellation when the principal balance of the loan is first scheduled to reach 80% of

the original value of the property, or reaches that percentage through payments, if 1) the borrower is current on the loan and has a “good payment history” (as defined by HOPA), 2) if required by the mortgage owner, the borrower provides evidence that the value of the property has not declined below the original value, and 3) if required by the mortgage owner, the borrower certifies that the borrower’s equity in the property is not subject to a subordinate lien. Additionally, HOPA requires mortgage insurance to terminate automatically when the principal balance of the loan is first scheduled to reach 78% of the original

MGIC Investment Corporation 2023 Form 10-K | 11

MGIC Investment Corporation and Subsidiaries

value of the property and the borrower is current on loan payments or thereafter becomes current. Annually, servicers must inform borrowers of their right to cancel or terminate mortgage insurance. The provisions of HOPA described above apply only to borrower paid mortgage insurance, which is described below.

Coverage tends to continue for borrowers experiencing economic difficulties or living in areas experiencing home price depreciation. The persistency of coverage for those borrowers, coupled with cancellation of coverage for other borrowers, can increase the percentage of an insurer’s portfolio covering loans with more credit risk. This development can also occur during periods of heavy mortgage refinancing because borrowers experiencing property value appreciation are less likely to require mortgage insurance at the time of refinancing, while borrowers not experiencing property value appreciation are more likely to continue to require mortgage insurance at the time of refinancing or not qualify for refinancing at all (including if they have experienced economic difficulties) and thus remain subject to the mortgage insurance coverage.

The percentage of NIW on loans representing refinances was 2% for 2023, compared to 3% for 2022 compared toand 20% for 2021 and 36% for 2020.2021. When a borrower refinances a mortgage loan insured by us by paying it off in full with the proceeds of a new mortgage that is also insured by us, the insurance on that existing mortgage is cancelled, and insurance on the new mortgage is considered to be NIW. Therefore, continuation of our coverage from a refinanced loan to a new loan results in both a cancellation of insurance and NIW. When a lender and borrower modify a loan rather than replace it with a new one or enter into a new loan pursuant to a loan modification program, our insurance continues without being cancelled, assuming that we consent to the modification or new loan. As a result, such modifications or new loans are not included in our NIW.

In addition to varying with the coverage percentage, our premium rates for insurance have varied depending upon the perceived risk of a claim on the insured loan and thus have taken into account, among other things, the LTV ratio, the borrower’s credit score and DTI ratio, the number of borrowers, the property location, the mortgage term and whether the property is the borrower’s primary residence. In recent years, the mortgage insurance industry has materially reduced its use of standard rate cards, which were fairly consistent among competitors, and correspondingly increased its use of (i)"risk based pricing systemssystems" that use a spectrum of filed rates to allow for formulaic, risk-based pricing based on multiple attributes that may be quickly adjusted within certain parameters, and (ii) customized rate plans, both of which typically have rates lower than the standard rate card.plans.

The borrower’s mortgage loan instrument may require the borrower to pay the mortgage insurance premium. Our industry refers to the related mortgage insurance as “borrower-paid” or BPMI. If the borrower is not required to pay the premium and

MGIC Investment Corporation 2022 Form 10-K | 11

MGIC Investment Corporation and Subsidiaries

mortgage insurance is required in connection with the origination of the loan, then the premium is paid by the lender, who may recover the premium through an increase in the note rate on the mortgage or higher origination fees. Our industry refers to the related mortgage insurance as “lender-paid” or LPMI. Most of our primary IIF is BPMI.

There are several payment plans available to the borrower, or lender, as the case may be. Under the single premium plan, the borrower or lender pays us in advance a single payment covering a specified term exceeding twelve months. Under the monthly premium plan, the borrower or lender pays us a monthly premium payment to provide only one month of coverage. Under the annual premium plan, an annual premium is paid to us in advance, with annual renewal premiums paid in advance thereafter.

During 2023, 2022 2021 and 2020,2021, the single premium plan represented approximately 4%, 7%4% and 9%7%, respectively, of our NIW. The monthly premium plan represented approximately 96%, 93%96% and 91%93%, respectively. The annual premium plan represented less than 1% of NIW in each of those years. Depending upon the actual life of a single premium policy and its premium rate relative to that of a monthly premium policy, a single premium policy may generate more or less premium than a monthly premium policy over its life.

Pool and Other Insurance.Insurance

Pool insurance is generally used as an additional “credit enhancement” for certain secondary market mortgage transactions. Pool insurance generally covers the amount of the loss on a defaulted mortgage loan that exceeds the claim payment under the primary coverage, if primary insurance is required on that mortgage loan, as well as the total loss on a defaulted mortgage loan which did not require primary insurance. Pool insurance may have a stated aggregate loss limit for a pool of loans and may also have a deductible under which no losses are paid by the insurer until losses on the pool of loans exceed the deductible. We have written no new pool insurance since 2008; however, for a variety of reasons, including responding to capital market alternatives to PMI and customer demands, we may write pool risk in the future. As of December 31, 2022,2023, our direct pool RIF was $276$256 million ($196186 million on pool policies with aggregate loss limits and $80$70 million on pool policies without aggregate loss limits).

In connection with the GSEs' credit risk transfer programs, we provide insurance and reinsurance covering portions of the credit risk related to certain reference pools of mortgages acquired by the GSEs. The amount of risk associated with these transactions is currently $310 million.

MGIC Investment Corporation 2023 Form 10-K | 12

MGIC Investment Corporation and Subsidiaries

MORTGAGE INSURANCE PORTFOLIO

Geographic Dispersion.Dispersion

The following tables reflect the percentage of primary RIF in the top 10 jurisdictions and top 10 core-basedmetropolitan statistical areas at December 31, 2022.2023.

| | | | | |

| Top 10 jurisdictions – RIF |

| |

| California | 8.38.6 | % |

| Texas | 7.67.7 | % |

| Florida | 6.7 | % |

| Pennsylvania | 4.95.1 | % |

| Illinois | 4.24.1 | % |

| Virginia | 3.9 | % |

| North Carolina | 3.83.7 | % |

| Ohio | 3.73.6 | % |

| Georgia | 3.73.5 | % |

| New York | 3.5 | % |

| Total | 50.350.4 | % |

| | | | | |

Top 10 core-basedmetropolitan-based statistical areas – RIF |

| |

| New York-Newark-Jersey City | 4.3 | % |

| Washington-Arlington-Alexandria | 3.24.1 | % |

| Chicago-Naperville-Arlington Heights | 3.3 | % |

| Atlanta-Sandy Springs-Roswell | 2.72.6 | % |

| Philadelphia-Camden-Wilmington | Chicago-Naperville-Arlington Heights2.6 | 2.7% |

| Dallas-Fort Worth | 2.4 | % |

| Los Angeles-Long Beach-Anaheim | 2.3 | % |

| Houston-Woodlands-Sugar Land | 2.32.2 | % |

| Minneapolis-St. Paul-Bloomington | 1.9 | % |

Los Angeles-Long Beach-Glendale | 1.7 | % |

| Phoenix-Mesa-Scottsdale | 1.7 | % |

Dallas-Plano-Irving | 1.6 | % |

Philadelphia | 1.6 | % |

Riverside-San Bernardino | 1.51.8 | % |

| Total | 20.927.5 | % |

The percentages shown above for various core-basedmetropolitan-based statistical areas can be affected by changes, from time to time, in the federal government’s definition of a core-based statistical area.

MGIC Investment Corporation 2022 Form 10-K | 12

MGIC Investment Corporation and Subsidiaries

Policy Year.Year

The following table sets forth the dispersion and certain statistics associated with our primary IIF and RIF as of December 31, 2022,2023, by year(s) of policy origination since we began operations in 1985.

| | Primary insurance in force and risk in force by policy year | Primary insurance in force and risk in force by policy year | Primary insurance in force and risk in force by policy year |

| ($ in millions) | Insurance in Force | | Risk In Force | | Weighted Avg. Interest Rate | Delinquency Rate % | Cede Rate % | % of Original Remaining |

| ($ in billions) | | ($ in billions) | Insurance in Force | | Risk In Force | | Weighted Avg. Interest Rate | Delinquency Rate % | Cede Rate % | % of Original Remaining IIF |

| Policy Year | Policy Year | Total | % of Total | | Total | % of Total | | Weighted Avg. Interest Rate | Delinquency Rate % | Cede Rate % | % of Original Remaining |

| 2004 and prior | 2004 and prior | $ | 1,475 | | 0.5 | % | | $ | 411 | | 0.5 | % | |

| 2004 and prior | |

| 2004 and prior | | $ | 1.2 | | 0.4 | % | | $ | 0.3 | | 0.4 | % | | 7.4 | % | 12.7 | % | — | % | N.M. |

| 2005-2008 | 2005-2008 | 11,610 | | 3.9 | % | | 3,083 | | 4.0 | % | | 6.9 | % | 10.9 | % | — | % | 4.8 | % | 2005-2008 | $ | 9.9 | | 3.4 | 3.4 | % | | $ | 2.6 | | 3.4 | 3.4 | % | | 7.0 | % | 10.6 | % | — | % | 4.1 | % |

| 2009-2015 | 6,457 | | 2.2 | % | | 1,754 | | 2.3 | % | | 4.3 | % | 4.7 | % | — | % | 3.6 | % |

| 2016 | 6,527 | | 2.2 | % | | 1,749 | | 2.3 | % | | 3.9 | % | 3.2 | % | — | % | 13.6 | % |

| 2017 | 7,839 | | 2.7 | % | | 2,059 | | 2.7 | % | | 4.2 | % | 3.8 | % | — | % | 15.9 | % |

| 2018 | 8,106 | | 2.7 | % | | 2,081 | | 2.8 | % | | 4.8 | % | 4.4 | % | — | % | 16.2 | % |

| 2019 | 17,285 | | 5.9 | % | | 4,447 | | 5.8 | % | | 4.1 | % | 2.2 | % | 1.5 | % | 26.6 | % |

| 2009-2019 | | 2009-2019 | $ | 35.6 | | 12.1 | % | | $ | 9.4 | | 12.1 | % | | 4.3 | % | 3.5 | % | — | % | 9.1 | % |

| 2020 | 2020 | 64,659 | | 21.9 | % | | 16,204 | | 21.2 | % | | 3.2 | % | 1.0 | % | 28.7 | % | 56.6 | % | 2020 | $ | 50.8 | | 17.3 | 17.3 | % | | $ | 13.2 | | 17.2 | 17.2 | % | | 3.2 | % | 1.2 | % | 5.0 | % | 44.4 | % |

| 2021 | 2021 | 100,796 | | 34.1 | % | | 26,004 | | 34.0 | % | | 3.1 | % | 0.9 | % | 29.2 | % | 85.5 | % | 2021 | $ | 86.5 | | 29.5 | 29.5 | % | | $ | 22.8 | | 29.6 | 29.6 | % | | 3.1 | % | 1.4 | % | 29.7 | % | 73.4 | % |

| 2022 | 2022 | 70,545 | | 23.9 | % | | 18,680 | | 24.4 | % | | 4.8 | % | 0.4 | % | 30.4 | % | 96.4 | % | 2022 | $ | 66.3 | | 22.6 | 22.6 | % | | $ | 17.6 | | 22.8 | 22.8 | % | | 4.9 | % | 1.2 | % | 30.5 | % | 89.3 | % |

| Total | $ | 295,298 | | 100.0 | % | | $ | 76,472 | | 100.0 | % | | |

| 2023 | | 2023 | $ | 43.3 | | 14.7 | % | | $ | 11.2 | | 14.5 | % | | 6.6 | % | 0.2 | % | 26.5 | % | 96.0 | % |

Total (1) | |

MGIC Investment Corporation 20222023 Form 10-K | 13

MGIC Investment Corporation and Subsidiaries

Product Characteristics.Characteristics

The following table reflects, at the dates and by the categories indicated, the total dollar amount of primary RIF and the percentage of that primary RIF, as determined on the basis of information available on the date of mortgage origination.

| | Characteristics of primary risk in force | Characteristics of primary risk in force | Characteristics of primary risk in force |

| | December 31, 2022 | | December 31, 2021 |

Primary RIF (In millions): | $ | 76,472 | | | $ | 69,337 | |

| December 31, 2023 | |

| December 31, 2023 | |

| December 31, 2023 | | | December 31, 2022 |

Primary RIF (In billions): | |

| Loan-to-value ratios: | Loan-to-value ratios: | |

| 95.01% and above | |

| 95.01% and above | |

| 95.01% and above | 95.01% and above | 15.2 | % | | 14.7 | % | 15.7 | % | | 15.2 | % |

| 90.01 - 95.00% | 90.01 - 95.00% | 52.0 | % | | 50.4 | % | 90.01 - 95.00% | 52.4 | % | | 52.0 | % |

| 85.01 - 90.00% | 85.01 - 90.00% | 27.2 | % | | 28.1 | % | 85.01 - 90.00% | 27.2 | % | | 27.2 | % |

| 80.01 - 85.00% | 80.01 - 85.00% | 5.4 | % | | 6.4 | % | 80.01 - 85.00% | 4.5 | % | | 5.4 | % |

| 80% and below | 80% and below | 0.2 | % | | 0.4 | % | 80% and below | 0.2 | % | | 0.2 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Debt-to-income ratios: | Debt-to-income ratios: | |

| 45.01% and above | 45.01% and above | 15.6 | % | | 13.6 | % |

| 45.01% and above | |

| 45.01% and above | | 17.5 | % | | 15.6 | % |

| 38.01% - 45.00% | 38.01% - 45.00% | 31.6 | % | | 31.5 | % | 38.01% - 45.00% | 31.8 | % | | 31.6 | % |

| 38% and below | 38% and below | 52.8 | % | | 54.9 | % | 38% and below | 50.7 | % | | 52.8 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Loan Type: | Loan Type: | |

Fixed(1) | Fixed(1) | 99.5 | % | | 99.4 | % |

Fixed(1) | |

Fixed(1) | | 99.6 | % | | 99.5 | % |

ARMs(2) | ARMs(2) | 0.5 | % | | 0.6 | % | ARMs(2) | 0.4 | % | | 0.5 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

Original Insured Loan Amount:(3) | Original Insured Loan Amount:(3) | |

| Conforming loan limit and below | |

| Conforming loan limit and below | |

| Conforming loan limit and below | Conforming loan limit and below | 97.3 | % | | 97.5 | % | 97.3 | % | | 97.3 | % |

| Non-conforming | Non-conforming | 2.7 | % | | 2.5 | % | Non-conforming | 2.7 | % | | 2.7 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Mortgage Term: | Mortgage Term: | |

| 15-years and under | 15-years and under | 1.1 | % | | 1.7 | % |

| 15-years and under | |

| 15-years and under | | 0.7 | % | | 1.1 | % |

| Over 15 years | Over 15 years | 98.9 | % | | 98.3 | % | Over 15 years | 99.3 | % | | 98.9 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Property Type: | Property Type: | |

| Single-family detached | |

| Single-family detached | |

| Single-family detached | Single-family detached | 86.9 | % | | 86.9 | % | 86.7 | % | | 86.9 | % |

| Condominium/Townhouse/Other attached | Condominium/Townhouse/Other attached | 12.5 | % | | 12.4 | % | Condominium/Townhouse/Other attached | 12.6 | % | | 12.5 | % |

Other(4) | Other(4) | 0.6 | % | | 0.7 | % | Other(4) | 0.7 | % | | 0.6 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Occupancy Status: | Occupancy Status: | |

| Owner occupied | Owner occupied | 97.8 | % | | 97.4 | % |

| Owner occupied | |

| Owner occupied | | 98.1 | % | | 97.8 | % |

| Second home | Second home | 2.1 | % | | 2.4 | % | Second home | 1.8 | % | | 2.1 | % |

| Investor property | Investor property | 0.1 | % | | 0.2 | % | Investor property | 0.1 | % | | 0.1 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

| Documentation: | Documentation: | |

Reduced:(5) | Reduced:(5) | |

Reduced:(5) | |

Reduced:(5) | |

| Stated | |

| Stated | |

| Stated | Stated | 0.6 | % | | 0.7 | % | 0.5 | % | | 0.6 | % |

| No | No | 0.2 | % | | 0.3 | % | No | 0.2 | % | | 0.2 | % |

| Full documentation | Full documentation | 99.2 | % | | 99.0 | % | Full documentation | 99.3 | % | | 99.2 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

MGIC Investment Corporation 20222023 Form 10-K | 14

MGIC Investment Corporation and Subsidiaries

| | Characteristics of primary risk in force | Characteristics of primary risk in force | Characteristics of primary risk in force |

| | December 31, 2022 | | December 31, 2021 |

| December 31, 2023 | |

| December 31, 2023 | |

| December 31, 2023 | | | December 31, 2022 |

FICO Score:(6) | FICO Score:(6) | |

| 760 and greater | |

| 760 and greater | |

| 760 and greater | 760 and greater | 42.2 | % | | 42.1 | % | 43.1 | % | | 42.2 | % |

| 740 - 759 | 740 - 759 | 17.7 | % | | 17.2 | % | 740 - 759 | 17.9 | % | | 17.7 | % |

| 720 - 739 | 720 - 739 | 14.1 | % | | 13.7 | % | 720 - 739 | 14.1 | % | | 14.1 | % |

| 700 - 719 | 700 - 719 | 11.1 | % | | 11.1 | % | 700 - 719 | 10.8 | % | | 11.1 | % |

| 680 - 699 | 680 - 699 | 7.7 | % | | 7.9 | % | 680 - 699 | 7.3 | % | | 7.7 | % |

| 660 - 679 | 660 - 679 | 3.3 | % | | 3.3 | % | 660 - 679 | 3.2 | % | | 3.3 | % |

| 640 - 659 | 640 - 659 | 1.9 | % | | 2.2 | % | 640 - 659 | 1.8 | % | | 1.9 | % |

| 639 and less | 639 and less | 2.0 | % | | 2.5 | % | 639 and less | 1.8 | % | | 2.0 | % |

| Total | Total | 100.0 | % | | 100.0 | % | Total | 100.0 | % | | 100.0 | % |

(1)Includes fixed rate mortgages with temporary buydowns (where in effect, the applicable interest rate is typically reduced by one or two percentage points during the first two years of the loan and then increased thereafter to the original interest rate), ARMs in which the initial interest rate is fixed for at least five years, and balloon payment mortgages (a loan with a maturity, typically five to seven years, that is shorter than the loan’s amortization period).

(2)Includes ARMs where payments adjust fully with interest rate adjustments. Also includes pay option ARMs and other ARMs with negative amortization features, which collectively at each of December 31, 20222023 and 2021,2022, represented and 0.1%, respectively, of primary RIF. As indicated in note (1), does not include ARMs in which the initial interest rate is fixed for at least five years. For both December 31, 20222023 and 2021,2022, ARMs with LTV ratios in excess of 90% represented 0.1%, of primary RIF, respectively.

(3)Loans within the conforming loan limit have an original principal balance that does not exceed the maximum original principal balance of loans that the GSEs will purchase. The conforming loan limit for one unit properties was $510,400 for 2020, $548,250 for 2021, and $647,200 for 2022, and is $726,200 for 2023.2023, and is $766,550 for 2024. The limit for high cost communities has been higher and is $1,089,300$1,149,825 for 2023.2024. Non-conforming loans are loans with an original principal balance above the conforming loan limit.

(4)Includes cooperatives and manufactured homes deemed to be real estate.

(5)Reduced documentation loans were originated prior to 2009 under programs in which there was a reduced level of verification or disclosure compared to traditional mortgage loan underwriting, including programs in which the borrower’s income and/or assets were disclosed in the loan application but there was no verification of those disclosures ("stated" documentation) and programs in which there was no disclosure of income or assets in the loan application ("no" documentation). In accordance with industry practice, loans approved by GSE and other automated underwriting (AU) systems under “doc waiver” programs that did not require verification of borrower income are classified by us as “full documentation.” We understand that the GSEs terminated their “doc waiver” programs in the second half of 2008.

(6)Represents the FICO score at loan origination. The weighted average “decision FICO score” at loan origination for NIW in 20222023 was 747753 compared to 749747 in 2021.2022. The FICO score for a loan with multiple borrowers is the lowest of the borrowers’ decision FICO scores. A borrower’s “decision FICO score” is determined as follows: if there are three FICO scores available, the middle FICO score is used; if two FICO scores are available, the lower of the two is used; if only one FICO score is available, it is used. A FICO score is a score based on a borrower’s credit history generated by a model developed by Fair Isaac Corporation.

MGIC Investment Corporation 2022 Form 10-K | 15

MGIC Investment Corporation and Subsidiaries

OTHER PRODUCTS AND SERVICES

Contract Underwriting.

A non-insurance subsidiary of ours provides contract underwriting services for lenders, pursuant to which loans are underwritten to conform to prescribed guidelines. The guidelines might be the lender's own guidelines or the guidelines of Fannie Mae, Freddie Mac or a non-GSE investor. These services are provided for loans that require private mortgage insurance as well as for loans that do not require private mortgage insurance.

Other. We provide insurance and reinsurance related to certain mortgages under GSE credit risk transfer programs. The amount of risk associated with these transactions is currently $226 million.

CUSTOMERS

Originators of residential mortgage loans such as savings institutions, commercial banks, mortgage brokers, credit unions, mortgage bankers and other lenders have historically determined the placement of mortgage insurance written on a flow basis and as a result are our customers. To obtain primary insurance from us, written on a flow basis, a mortgage lender must first apply for and receive a mortgage guaranty master policy from us. Our top 10 customers generated 33%37% of our NIW on a flow basis in 2022, 36%2023 and 33% in 2021 and 41% in 2020.2022. Our relationships with our customers could be adversely affected by a variety of factors, including if our premium rates are higher than those of our competitors, our underwriting requirements are more restrictive than those of our competitors, or our customers are dissatisfied with our claims-paying practices (including insurance policy rescissions and claim curtailments). Information about some of the other factors that can affect a mortgage insurer’s relationship with its customers can be found in our risk factor titled “Competition or changes in our relationships with our customers could reduce our revenues, reduce our premium yields and/or increase our losses” in Item 1A.

MGIC Investment Corporation 2023 Form 10-K | 15

MGIC Investment Corporation and Subsidiaries

SALES AND MARKETING AND COMPETITION

Sales and Marketing.Marketing

Our employees sell our insurance products throughout all regions of the United States, Puerto Rico, and Guam.

Competition.Competition

Our competition includes other mortgage insurers, governmental agencies and products designed to eliminate the need to purchase private mortgage insurance. For flow business, weWe and other private mortgage insurers compete directly with federal and state government and quasi-governmental agencies, principally the FHA and the VA. The FHA, VA and USDA sponsor government-backed mortgage insurance programs, and it is estimated that during 2022,2023, they accounted for a combined approximately 52.8%55.9% of the total low down payment residential mortgages which were subject to FHA, VA, USDA or primary private mortgage insurance, compared to 56.8% and 56.1%52.8% in 2021 and 2020, respectively.2022. For more information about the market share of the FHA and the VA, see “Overview of the Private Mortgage Insurance Industry and its Operating Environment” above.

The PMI industry is highly competitive. We believe that we currently compete with other private mortgage insurers based on premium rates, underwriting requirements, financial strength (including based on credit or financial strength ratings), customer relationships, name recognition, reputation, strength of management teams and field organizations, the ancillary products and services provided to lenders, and the effective use

of technology and innovation in the delivery and servicing of our mortgage insurance products.

The U.S. PMI industry currently consists of six active mortgage insurers and their affiliates, including MGIC. Our market share (as measured by NIW) was 16.3% in 2023, compared to 18.9% in 2022, compared to 20.6% in 2021 and 18.7% in 2020, in each case excluding HARP refinances.2022. (source: Inside Mortgage Finance).

If we are unable to compete effectively in the current or any future markets as a result of the financial strength ratings assigned to our insurance subsidiaries, our future new insurance written could be negatively affected. Our ability to participate in the non-GSE residential mortgage-backed securities market (the size of which has been limited since 2008, but may grow in the future), could depend on our ability to maintain and improve our investment grade ratings for our insurance subsidiaries. Although the current PMIERs of each of the GSEs do not require an insurer to maintain minimum financial strength ratings, the GSEs consider financial strength ratings to be important when using forms of credit enhancement other than traditional mortgage insurance.

In assigning financial strength ratings, in addition to considering the adequacy of the mortgage insurer’s capital to withstand very high claim scenarios under assumptions determined by the rating agency, we believe rating agencies review a mortgage insurer’s historical and projected operating performance, franchise risk, business outlook, competitive position, management, corporate strategy, enterprise risk management and other factors. The rating agency issuing the financial strength rating can withdraw or change its rating at any time. At the time that this annual report was finalized, the financial strength of MGIC was rated A- (with a stablepositive outlook) by A.M. Best, A3 (with a stable outlook) by Moody’s Investors Service and BBB+A- (with a stable outlook) by Standard & Poor’s Rating Services.

MGIC Investment Corporation 2022 Form 10-K | 16

MGIC Investment Corporation MGIC's Standard and SubsidiariesPoor's Rating was upgraded to A- in January of 2024.

C. Risk Management

ENTERPRISE RISK MANAGEMENT

The Company has an enterprise risk management (“ERM”) framework that it believes is commensurate with the size, nature and complexity of the Company’s business activities (all of which relate to insuring or reinsuring mortgage credit risk) and strategies. Among the key objectives of the ERM framework are to have a clear and well documented shared understanding, by senior management and the Board, of the Company’s risk management philosophy and overall appetite for risk, and that there are appropriate monitoring, management and reporting mechanisms to support the framework.

Risk Governance.

The Company maintains a Senior Management Oversight Committee (“SMOC”) that, at the management level, serves as its primary risk management governance organization. The SMOC oversees the Company’s ERM framework; maintains an enterprise view of risk across a set of identified key risks that may exist from time to time (see “Risk Identification and Assessment” below); and provides support and reporting to the Risk Management Committee of the Company’s Board of Directors (“RMC”). The SMOC, of which the CEO is a member, is chaired by the Company’s Executive Vice President and Chief Risk Officer, who is the principal management liaison to the RMC.

The Board implements its risk oversight function as a whole and through delegation to its Committees which meet regularly and report back to the full Board. The Risk Management Committee coordinates with the Board and other Board Committees regarding the assignment to the Board and Committees of oversight responsibilities for all risks considered to have the greatest impact on the Company's ability to accomplish its strategic goals. Each Committee's charter describes its principal responsibilities, including its oversight responsibility for applicable key risks.

Corporate Sustainability Risk Governance.

The Company maintains a Corporate Sustainability Executive Council that, at the management level, supports the Company's on-going commitment to environmental, health and safety, corporate social responsibility, corporate governance, sustainability, and other public

MGIC Investment Corporation 2023 Form 10-K | 16

MGIC Investment Corporation and Subsidiaries

policy matters relevant to the Company. In performing this general responsibility, the Council has discretion to: adopt the Company’s general strategy with respect to sustainability matters; identify current and emerging sustainability issues that may affect the Company’s business, strategy, operations, performance, or public image; make recommendations regarding policies, practices, procedures, or disclosures to address sustainability matters; oversee the Company’s internal and external reporting and disclosures surrounding sustainability matters; and advise on material concerns of shareholders or stakeholders regarding sustainability matters. The Corporate Sustainability Executive Council will make regular reports to the SLT and to the relevant Committee(s) of the Board of Directors of the Company.

The Board has delegated oversight for the following ESGsustainability matters to the following committees, who regularly report their actions to the Board:

•Risk Management Committee: Mortgage Credit Risk, including risks associated with climate change.

•Management Development, Nominating and Governance Committee: Corporate governance and human capital

management policies such as executive compensation; succession planning; recruitment, retention and development of management resources; workforce planning, recruitment morale and talent; diversity and inclusion initiatives; and work environment, including health and safety.

•Securities Investment Committee: Our investment portfolio; such oversight may include consideration of ESGsustainability factors.

•Audit Committee: Disclosure controls and procedures relating to financial reports made to the SEC as well as ESGand corporate sustainability reports.

•Business Transformation and Technology Committee: Cybersecurity and business continuity.

Risk Management and Controls.

The Company has established enterprise-wide policies, procedures and processes to allow it to identify, assess, monitor and manage the Company’s various risks. Management of these risks is an interdepartmental endeavor, with oversight by the Chief Risk Officer and the SMOC. The Company’s Internal Audit function, which reports to the Audit Committee of the Board of Directors, provides independent ongoing assessments of the Company’s management of certain enterprise risks and reports its findings to the Audit Committee.

Risk Identification and Assessment.

On a regular basis, the Company monitors key risks with a focus on identifying risks or changes to risks with the greatest impact on the Company's ability to accomplish its strategic goals. In addition to the ongoing monitoring, the Company also identifies key risks in a bottom up process facilitated through questionnaires and discussions during an annual compliance and risk forum with co-workers across all business functions. The results of the identification process are reported to and reviewed annually by the SMOC and presented to the RMC and/or the full Board.

Risk Reporting and Communication. The Company's Risk Management department produces various analyses, reports and key risk indicators (“KRIs”) that are reported to the SMOC, the RMC and the Board quarterly. For our largest risk exposure, mortgage credit risk, these KRIs include risk factors for the Company’s NIW, IIF, quality control and claim activity, and the quarterly reports include performance relative to metrics and thresholds. Each of the other Board Committees also receive regular reporting concerning the risks they oversee.

Although the Company has in place the ERM framework discussed above, it may not be effective in identifying, or adequate in controlling or mitigating, the risks we face. For more information, see our Risk Factor titled "If our risk management programs are not effective in identifying, or adequate in controlling or mitigating, the risks we face, or if the models used in our businesses are inaccurate, it could have a material adverse impact on our business, results of operations and financial condition" in Item 1A.

MORTGAGE CREDIT RISK

We believe that mortgage credit risk is materially affected by:

•the condition of the economy, including the direction of change in home prices and employment, in the area in which the property is located;

•the borrower’s credit profile, including the borrower’s credit history, DTI ratio and cash reserves, and the

MGIC Investment Corporation 2022 Form 10-K | 17

MGIC Investment Corporation and Subsidiaries

willingness of a borrower with sufficient resources to make mortgage payments when the mortgage balance exceeds the value of the home;

•the loan product, which encompasses the LTV ratio, the type of loan instrument, including whether the instrument provides for fixed or variable payments and the amortization schedule, the type of property and the purpose of the loan;

•origination practices of lenders and the percentage of coverage on insured loans; and

•the size of insured loans.

We believe that, excluding other factors, claim incidence increases:

MGIC Investment Corporation 2023 Form 10-K | 17

MGIC Investment Corporation and Subsidiaries

•during periods of economic contraction and home price depreciation, including when these conditions may not be nationwide, compared to periods of economic expansion and home price appreciation;

•for loans to borrowers with lower FICO scores compared to loans to borrowers with higher FICO scores;