UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 20122013 |

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the transition period from to |

Commission File No. 1-11442

CHART INDUSTRIES, INC.

(Exact Name of Registrant as Specified in its Charter)

|

| | |

| Delaware | | 34-1712937 |

(State or Other Jurisdiction of Incorporation or Organization) | | (IRS Employer Identification No.) |

|

| | |

| One Infinity Corporate Centre Drive, | | |

| Suite 300, Garfield Heights, Ohio | | 44125-5370 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code:

(440) 753-1490

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock, par value $0.01 | | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | |

| Large accelerated filer | | x | | Accelerated filer | | o |

| Non-accelerated filer | | o (Do not check if a smaller reporting company) | | Smaller reporting company | | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting common equity held by non-affiliates computed by reference to the price of $68.7694.09 per share at which the common equity was last sold, as of the last business day of the registrant’s most recently completed second fiscal quarter, was $2,029,029,8322,821,977,295.

As of February 15,17, 20132014, there were 30,074,09430,401,573 outstanding shares of the Company’s common stock, par value $0.01 per share.

Documents Incorporated by Reference

Portions of the following document are incorporated by reference into Part III of this Annual Report on Form 10-K: the definitive Proxy Statement to be used in connection with the Registrant’s Annual Meeting of Stockholders to be held on May 23, 201322, 2014 (the “20132014 Proxy Statement”).

Except as otherwise stated, the information contained in this Annual Report on Form 10-K is as of December 31, 20122013.

CHART INDUSTRIES, INC.

TABLE OF CONTENTS

PART I

THE COMPANY

Overview

Chart Industries, Inc., a Delaware corporation incorporated in 1992 (the “Company,” “Chart” or “we” and as used herein refers to Chart Industries, Inc. and our consolidated subsidiaries, unless the context indicates otherwise), is a leading independent global manufacturer of highly engineered equipment used inthroughout the global liquid gas supply chain for the production, storage and end-use of hydrocarbon and industrial gases, based on our sales and the estimated sales of our competitors. We supply engineered equipment used throughout the global liquid gas supply chain. The largest portion of end-use applications for our products is energy-related, accounting for approximately 54%53% of sales and 56%52% of orders in 20122013, and 77%73% of backlog at December 31, 20122013. We are a leading manufacturer of standardOur equipment and engineered equipmentsystems are primarily used for low-temperature and cryogenic applications. We have developed an expertise in cryogenic systems and equipment, which operate at low temperatures sometimes approaching absolute zero (0 kelvin; -273° Centigrade; -459° Fahrenheit). The majority of ourOur products includinginclude vacuum insulated containment vessels, heat exchangers, cold boxes and other cryogenic components, are used throughout the liquid gas supply chain for the purification, liquefaction, distribution, storage and end-use of hydrocarbon and industrial gases.components.

Our primary customers are large, multinational producers and distributors of hydrocarbon and industrial gases and their suppliers. We sell our products and services to more than 2,000 customers worldwide. We have developed long-standing relationships with leading companies in the gas production, gas distribution, gas processing, liquefied natural gas or LNG, chemical and industrial gas industries, including Air Products, Praxair, Airgas, Air Liquide, The Linde Group or Linde, JGC Corporation or JGC, Bechtel Corporation, ExxonMobil, British Petroleum or BP, ConocoPhillips, Saudi Aramco,PetroChina, The Shaw Group, CB&I Lummus, Uhde, CTCI Corporation or CTCI, Toyo, Samsung, Technip, Daelim, Thomas Russell, Black & Veatch, Chemtex, Enterprise, Exterran,UOP, Shell, Kryopak/Salof and Energy World Corporation or EWC, some of whom have been purchasing our products for over 20 years.

We have attained this position by capitalizing on our low-cost global manufacturing footprint, technical expertise and know-how, broad product offering and reputation for quality, and by focusing on attractive, growing markets. We have an established sales and customer support presence across the globe and low cost manufacturing operations in the United States, Central Europe and China. For the years ended December 31, 2013, 2012 2011 and 20102011, we generated sales of $1,014.21,177.4 million, $794.61,014.2 million, and $555.5794.6 million, respectively.

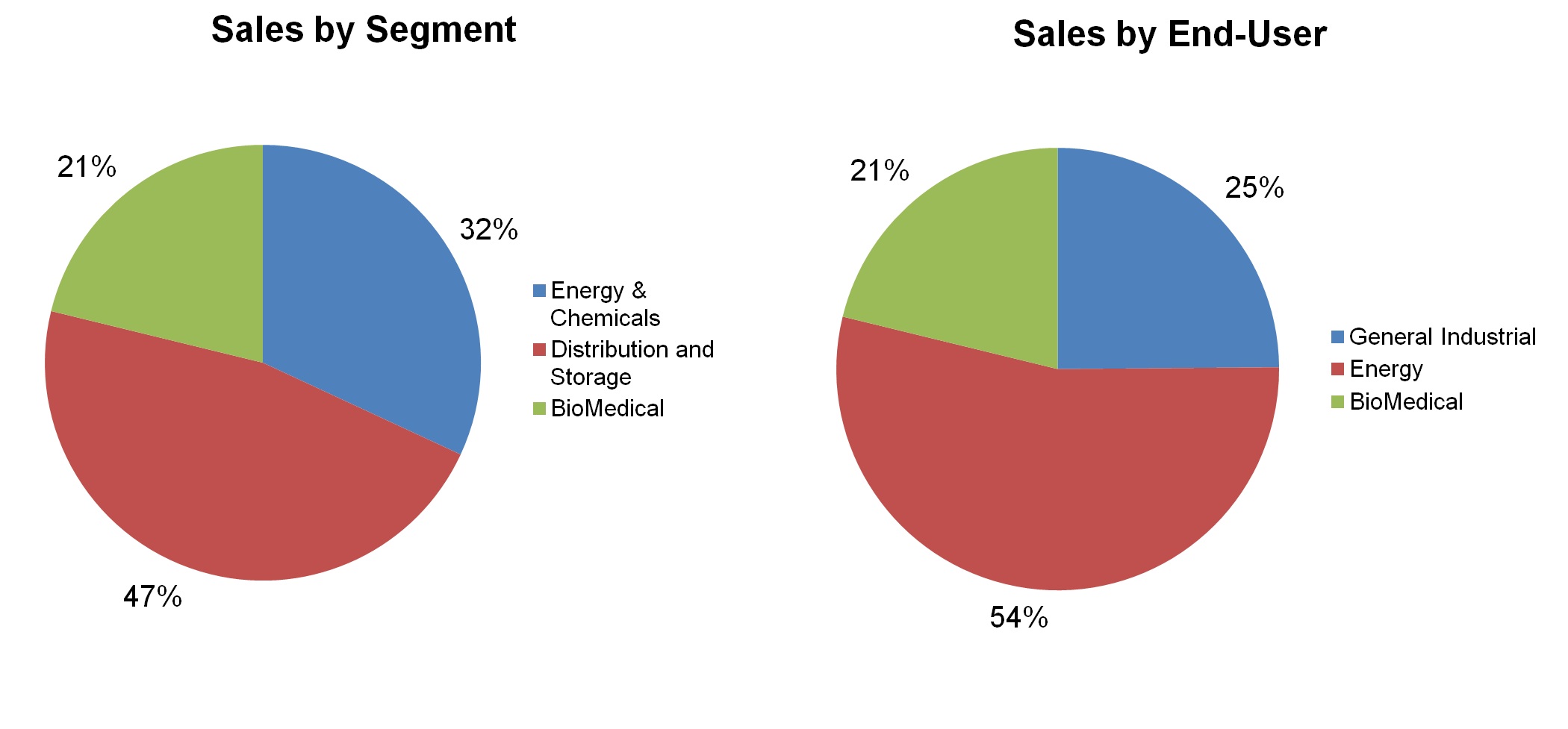

The following charts show the proportion of our revenues generated by each operating segment as well as our estimate of the proportion of revenue generated by end-user for the year ended December 31, 20122013:

Segments and Products

We operate in three operating segments: (i) Energy & Chemicals or E&C, (ii) Distribution and& Storage or D&S, and (iii) BioMedical. While each segment manufactures and markets different cryogenic and gas processing equipment and systems to distinct end-users, they all share a reliance on our heat transfer, low temperature storage and gas processing know-how and expertise. The E&C and D&S segments manufacture products used primarily in energy-related and general industrial applications, such as the separation, liquefaction, distribution and storage of hydrocarbon and industrial gases. Through our BioMedical segment, we supply cryogenic and other equipment used in the storage and distribution of biological materials and oxygen, used primarily in the medical, biological research and animal breeding industries. Further information about these segments is located in Note K19 of the notes to the Company’s consolidated financial statements included in Item 8 of this Annual Report on Form 10-K.

Energy and& Chemicals Segment

Our principal products within the E&C segment, which accounted for 32%27% of sales for the year ended December 31, 20122013, are focused on engineered equipment and systems for the energy and chemicals markets, primarily heat exchangers, Core-in-Kettle® units, cold boxes, and process systems andincluding LNG vacuum insulated pipe.liquefiers. These products are used by major natural gas, petrochemical processing and industrial gas companies in the production of their products. Our products in the E&C segment include the following:

Heat Exchangers and Core-in-Kettles®

We are a leading designer and manufacturer of cryogenic brazed aluminum and air cooled heat exchangers. Brazed aluminum heat exchangers accounted for 14.4%, 11.6%14.4% and 11.3%11.6% of consolidated sales for the years ended December 31, 20122013, 20112012 and 20102011, respectively. Using technology pioneered by us, our brazed aluminum heat exchangers are incorporated into assemblies and cold boxes to facilitate the progressive cooling and liquefaction of air or hydrocarbon mixtures for the subsequent recovery or purification of component gases. In hydrocarbon processing industries, our brazed aluminum heat exchangers allow producers to obtain purified hydrocarbon by-products, such as methane, ethane, propane and ethylene, which are commercially marketable for various industrial or residential uses. In the industrial gas market, our brazed aluminum heat exchangers are used to produce high purity atmospheric gases, such as oxygen, nitrogen and argon, which have diverse industrial applications.

Our air cooled heat exchangers are used in multiple markets to cool fluids to allow for further processing or to provide condensing of fluids, including hydrocarbon, petrochemical, natural gas processing, and power generation. Our compact Core-in-Kettle® heat exchangers are designed to replace shell-and-tube exchangers, offering significantly more heat transfer surface per unit volume and greatly improving the efficiency of chillers, vaporizers, reboilers and condensers in hydrocarbon applications including ethylene, propylene and LNG. Brazed aluminum and air cooled heat exchangers are engineered to the customer’s requirements and range in price from $20,000 to $3.0 million or more depending on the scope and complexity of the project.

Our heat exchanger demand is primarily driven by activity in the LNG and natural gas segments of the hydrocarbon processing market, as well as the global industrial gas market. Other key global drivers involve developing Gas to Liquids, or GTL, clean coal processes including Coal to Liquids, or CTL, and Integrated Gasification and Combined Cycle, or IGCC, power projects. In the future, management believes that continuing efforts by petroleum producing countries to better utilize stranded natural gas and previously flared gases, as well as efforts to broaden their industrial base, and the developing clean coal initiatives globally, present a promising source of demand for our heat exchangers and cold box systems. In addition, demand for heat exchangers and cold boxes in developed countries is expected to continue as firms upgrade their facilities for greater efficiency and regulatory compliance. We believe demand for our heat exchangers has also increased as a result of the natural gas being extracted from the U.S. shale fields.

Our principal competitors for brazed aluminum heat exchangers are Linde, Sumitomo, Kobeinclude several European and Fives,Asian manufacturers, and we face competition from a variety of competitors for air cooled heat exchangers. Management believes we are the only producer of large brazed aluminum heat exchangers in the United States and that we are a leader in the global cryogenic heat exchanger industry. Major customers for our heat exchangers include large companies in the industrial gas industry include Air Liquide, Air Products, Praxair, Hangyang, Kaifeng Air Separation and Sichuan Air Separation. In the hydrocarbon processing industry, major customers andindustries, as well as engineering, procurement and construction (EPC) contractors include BP, Black & Veatch, ExxonMobil, Saudi Aramco, ConocoPhillips, JGC, Bechtel, Chemtex, Kryopak/Salof, Kellogg Brown Root or KBR, Technip, CB&I Lummus, Thomas Russell, Enterprise, Exterran, Toyo, The Shaw Group, Samsung and Shell.(“EPC”) contractors.

Cold Boxes

We are a leading designer and fabricator of cold boxes. Cold boxes are highly engineered systems used to significantly reduce the temperature of gas mixtures to the point where component gases liquefy and can be separated and purified for further use in multiple industrial, scientific and commercial applications. In the hydrocarbon processing industry, our cold box

systems are used in natural gas processing and in the petrochemical industry. In the industrial gas industry, cold box systems are used to separate air into its major atmospheric components, including nitrogen, oxygen and argon, where the gases are used in a diverse range of applications such as metal production and heat treating, enhanced oil and gas production, coal gasification, chemical and oil refining, the quick-freezing of food, wastewater treatment and industrial welding. The construction of a cold box system generally consists of one or more brazed aluminum heat exchangers and other equipment packaged in a “box” consisting of a structural metal frame encasing a complex system of piping, valves and instrumentation. Cold boxes, which are designed and fabricated to order, sell in the price range of $1.0 million to $20.0 million, with the majority of cold boxes priced between $1.0 million and $5.0 million.

We have a number of competitors for fabrication of cold boxes, including Linde, Air Products, Praxair, Air Liquidea number of leading companies in the industrial gas and hydrocarbon processing industries and many smaller fabrication-only facilities around the world. Principal customers for our cold boxes include CB&I Lummus, BP, Black & Veatch, Chemtex, Bechtel, Saudi Aramco, Jacobs, Chevron, ConocoPhillips, Marathon, JGC, Kryopak/Salof, Shell, Technip, Toyo, The Shaw Group, Samsung and KBR.

Process Systems

We are a leader in the design and manufacturing of highly engineered hydrocarbon process systems specifically for those markets requiring cryogenic processing technology. These “Concept-to-Reality” process systems incorporate many of Chart’s core products, including brazed aluminum heat exchangers, Core-in-Kettles®, cold boxes, vessels, pipe work and air cooled heat exchangers. These systems are used for global LNG projects, including potential projects in the United States and China for both domestic LNG production for diesel displacement and in the conversion of LNG import terminals to dual purpose import/export terminals, and also for use in global nitrogen rejection units (NRU)(“NRU”) and propane dehydrogenation (PDH)(“PDH”). These systems, which are custom engineered and manufactured to order, typically sell in the price range of $5.0 million to over $100.0 million, depending on the scope and complexity of the project, with the majority of the systems priced between $5.0 million and $25.0 million.

Our principal industry segments include natural gas processing, LNG, nitrogen rejection,NRUs, ammonia purification, propane dehydrogenation or PDH, HYCO/hydrogen recovery, and Ryan-Holmes CO2 bulk removal technology for enhanced oil recovery and CO2 sequestration.

We have a number of competitors for our process systems including Linde, Air Products,leading industrial gas companies and other smaller engineering, procurement and construction, or EPC, firms to whom we also act as a supplier of equipment including heat exchangers and cold boxes. Principal customers and end-users for our process systems include EWC, CB&I Lummus, Fluor, ExxonMobil, JGC, The Shaw Group, CTCI, Samsung, Uhde and KBR.

Distribution and Storage Segment

Through our D&S segment, which accounted for 47%50% of our sales for the year ended December 31, 20122013, we are a leading supplier of cryogenic equipment to the global bulk and packaged industrial gas industry as well as for energy-related applications.applications including the distribution and storage of LNG. Demand for the products supplied by this segment is driven primarily by the significant installed base of users of cryogenic liquids as well as new applications and distribution technologies for cryogenic liquids. Our products span the entire spectrum of industrial gas demand from small customers requiring cryogenic packaged gases to large users requiring custom engineered cryogenic storage systems. Our products in the D&S segment include the following:

Cryogenic Bulk Storage Systems

We are a leading supplier of cryogenic bulk storage systems (stationary tanks, trailers, and ISO tanks) of various sizes ranging from 500 gallons to 250,000265,000 gallons. Cryogenic bulk storage systems accounted for 15.1%14.9%, 19.3%15.1% and 18.5%19.3% of consolidated sales for the years ended December 31, 20122013, 20112012 and 20102011, respectively. Using sophisticated vacuum insulation systems placed between inner and outer vessels, these bulk storage systems are able to store and transport liquefied industrial gases and hydrocarbon gases at temperatures from -100°0° Fahrenheit to temperatures nearing absolute zero. End useEnd-use customers for our cryogenic storage equipment include industrial gas producers and distributors, chemical producers, manufacturers of electrical components, health care organizations, food processors and businesses in the oil and natural gas industries. Prices for our cryogenic bulk storage systems range from $10,000 to $1.0 million. Global industrial gas producers and distributors including Air Products, Air Liquide, Linde, Airgas, Praxair and Messer, are significant customers for our cryogenic bulk storage systems. OnOur competitors tend to be regionally focused while Chart is able to supply a broad range of systems on a worldwide basis, we compete primarily with Taylor-Wharton International or Taylor-Wharton and CVA/INOX

in this product area. In Europe and Asia, webasis. We also compete with several suppliers owned by the global industrial gas producers as well as independent regional suppliers such as VRV, Aritas and Sanctum.producers.

Cryogenic Packaged Gas Systems

We are a leading supplier of cryogenic packaged gas systems of various sizes ranging from 160 liters to 3,000 liters. Cryogenic packaged gas systems accounted for 14.2%13.0%, 17.9%14.2% and 17.6%17.9% of consolidated sales for the years ended December 31, 20122013, 20112012 and 20102011, respectively. Cryogenic liquid cylinders are used extensively in the packaged gas industry to allow smaller quantities of liquid to be easily delivered to the customers of industrial gas distributors on a full-for-empty or fill-on-site basis. Principal customers for our liquid cylinders are the same global industrial gas producers and the North

American industrial gas distributors who purchase our cryogenic bulk storage systems. We competeOur competitors tend to be regionally focused while Chart is able to supply a broad range of systems on a worldwide basis primarily with Taylor-Wharton and Beijing Tenhai Industrial Cylinders in this product area.basis. We have developed two technologies in the packaged gas product area: ORCA™ Micro-BulkMicroBulk systems and Tri-fectaTrifecta® Laser Gas assist systems. ORCA™ Micro-BulkMicroBulk systems bring the ease of use and distribution economics of bulk gas supply to customers formerly supplied by high pressure or cryogenic liquid cylinders. The ORCA™ Micro-BulkMicroBulk system is the leader in this growing product line. The Tri-fectaTrifecta® Laser Gas assist system was developed to meet the “assist gas” performance requirements for new high powered lasers being used in the metal fabrication industry.

Cryogenic Systems and Components

Our line of cryogenic components, including VIP,Vacuum Insulated Pipe ("VIP"), engineered bulk gas installations, specialty liquid nitrogen, or LN2, end-use equipment and cryogenic flow meters are recognized in the market for their reliability, quality and performance. These products are sold to industrial gas producers, as well as to a diverse group of distributors, resellers and end users.end-users. We compete with a number of suppliers of cryogenic systems and components, including Acme Cryogenics, Vacuum Barrier Corporation and others. Additionally, incomponents. In 2010 we completed the acquisition of Cryotech which is a manufacturer of LN2 dosing systems for food and beverage packaging applications located in San Jose, California. Cryotech expands our expertise in LN2 end useend-use applications and distributes its products globally.

LNG Applications

We supply cryogenic solutions for the storage, distribution, vaporization, and application of LNG. LNG applications accounted for 16.4%, 10.6% and 4.5% of consolidated sales for the years ended December 31, 2013, 2012 and 2011, respectively. LNG may be utilized as a primary source of heat or power at industrial or residential complexes located away from a natural gas pipeline. LNG may also be used for peak shaving or as a backup supply at remote locations. We refer to our LNG distribution products as a “Virtual Pipeline” as the natural gas pipeline is replaced with cryogenic distribution to deliver the gas to the end user. We supply cryogenic trailers, bulk storage tanks, tap-offloading facilities, and vaporization equipment specially configured for LNG into Virtual Pipeline applications. LNG may also be used as a fuel to power on-road vehicles, or ships.off-road vehicles, drill rigs, ships and rail locomotives. LNG vehicle fueling applications consist of LNG and liquid/compressed natural gas refueling systems for centrally fueled fleets of vehicles, trucks,heavy-duty truck and ships powered by natural gas, such as fleets operated by metropolitan transportation authorities, refuse haulers and heavy-duty truckbus fleets. We sell LNG applications around the world from all D&S facilities to numerous end users, energy companies, and gas distributors. Competition for LNG applications is based primarily on product design, customer support and service, dependability and price. Our competitors tend to be regionally focused or product specific while Chart is able to supply a broad range of solutions required by LNG applications.

Beverage Liquid CO2 Systems

This product line consists primarily of vacuum insulated, bulk liquid CO2 containers used for beverage carbonation in restaurants, convenience stores and cinemas, in sizes ranging from 100 pounds to 7501,000 pounds of liquid CO2 storage. We also manufacture and market non-insulated, bulk fountain syrup containers for side-by-side installation with our CO2 systems. Our beverage systems are sold to national restaurant chains, soft drink companies and CO2 distributors. Our primary competitors for bulk liquid CO2 beverage delivery systems are Taylor-Wharton and other producers of cryogenic systems and high-pressure gaseous CO2 cylinders.

Cryogenic Services

We operate locations in the United States and Europe providing installation, service, repair and maintenance of cryogenic products including storage tanks, liquid cylinders, cryogenic trailers, cryogenic railcars, cryogenic pumps, cryogenic flow meters and VIP. In 2010, we opened a comprehensive service facility in McCarran, Nevada that allows us to provide a full range of repair services for equipment located west of the Rocky Mountains.

BioMedical Segment

The BioMedical segment, which accounted for 21%23% of our sales for the year ended December 31, 20122013, consists of various product lines built around our core competencies in cryogenics and pressure swing adsorption, but with a focus on the respiratory and biological users of the liquids and gases instead of the large producers and distributors of cryogenic liquids. Our products in the BioMedical segment include the following:

Respiratory Products

Medical respiratory products accounted for 14.8%14.9%, 17.4%14.2% and 17.2%17.4% of consolidated sales for the years ended December 31, 20122013, 20112012 and 20102011, respectively. Our respiratory oxygen product line is comprised of a range of medical respiratory products, including liquid oxygen systems and ambulatory oxygen systems, both of which are used primarily for the in-home supplemental oxygen treatment of patients with chronic obstructive pulmonary diseases, such as bronchitis,

emphysema and asthma. We further expanded our respiratory product offering in 2010 and 2012 by acquiring SeQual Technologies, Inc. and AirSep Corporation, respectively, which design, manufacture, and service stationary, transportable, and portable oxygen concentrators.

Individuals for whom supplemental oxygen is prescribed generally receive an oxygen system from a home healthcare provider, medical equipment dealer, or gas supplier. The provider or physician usually selects which type of oxygen system that is providedto provide to its customers: liquid oxygen systems, transportable oxygen concentrators, portable oxygen concentrators, stationary concentrators or high-pressure oxygen cylinders. Physicians generally believe that increased patient ambulation offers greater long-term therapeutic benefits which can be provided by liquid oxygen and transportable and portable oxygen concentrators.

We believe that competition for our respiratory productproducts is based primarily upon product quality, performance, reliability, ease-of-use and price, and we focus our marketing strategies on these considerations. Furthermore, competition also includes the impact of other modalities in the broader respiratory industry.

Cold Storage Systems

This product line consists of vacuum insulated containment vessels for the storage of biological materials. The primary applications for this product line include medical laboratories, biotech/pharmaceutical, research facilities, blood and tissue banks, veterinary laboratories, large-scale repositories and artificial insemination, particularly in the beef and dairy industry.

The significant competitors for biological storage systems include a fewnumber of large companies worldwide, such as Taylor-Wharton, Air Liquide and Ind-Burma Petroleum Company, or IBP.worldwide. These products are sold through multiple channels of distribution specifically applicable to each industry sector. The distribution channels range from highly specialized cryogenic storage systems providers to general supply and catalogue distribution operations to breeding service providers. Historically, competitionCompetition in this field has beenis focused on design, reliability and price. Alternatives to vacuum insulated containment vessels include mechanical, electrically powered refrigeration.

Commercial Oxygen Generation Systems

This product line includes self-contained generators, standard generators, and packaged systems for industrial and medical oxygen generating systems. These generators produce oxygen from compressed air and provide an efficient and cost-effective alternative to the procurement of oxygen from third party cylinder or liquid suppliers. Applications include mining operations, industrial plants, ozone generation, hospital medical oxygen, and wastewater sites, among other commercial applications. The primary competitors include OGSI, Onsite Gas, OxymatManagement expects demand for this product line to increase over the long-term with competition focused on design, reliability and Novair.price.

Domestic and Foreign Operations

Financial and other information regarding domestic and foreign operations is located in Note K19 of the notes to the Company's consolidated financial statements included in Item 8 of this Annual Report on Form 10-K. Additional information regarding risks attendant to foreign operations is set forth in Item 7A of this Annual Report on Form 10-K under the caption “Quantitative and Qualitative Disclosures About Market Risk” and Item 7 under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Engineering and Product Development

Our engineering and product development activities are focused primarily on developing new and improved solutions and equipment for the users of cryogenic liquids and hydrocarbon and industrial gases. Our engineering, technical and marketing employees actively assist customers in specifying their needs and in determining appropriate products to meet those needs.

Portions of our engineering expenditures typically are charged to customers, either as separate items or as components of product cost.

Competition

We believe we can compete effectively around the world and that we are a leading competitor in the industries we serve. Competition is based primarily on performance and the ability to provide the design, engineering and manufacturing capabilities required in a timely and cost-efficient manner. Contracts are usually awarded on a competitive bid basis. Quality, technical expertise and timeliness of delivery are the principal competitive factors within the industry. Price and terms of sale are also important competitive factors. Because independent third-party prepared market share data is not available, it is difficult to know for certain our exact position in our markets, although we believe we rank among the leaders in each of the markets we serve. We base our statements about industry and market positions on our reviews of annual reports and published investor presentations of our competitors and augment this data with information received by marketing consultants conducting

competition interviews and our sales force and field contacts. For information concerning competition within a specific segment of the Company's business, see descriptions provided under segment captions herein.in this Annual Report on Form 10-K.

Marketing

We market our products and services throughout the world primarily through direct sales personnel and independent sales representatives and distributors. The technical and custom design nature of our products requires a professional, highly trained sales force. While each salesperson and sales representative is expected to develop a highly specialized knowledge of one product or group of products within one of our segments, each salesperson and certain sales representatives are able to sell many products from different segments to a single customer. We use independent sales representatives and distributors to market our products and services in certain foreign countries and in certain North American markets.regions. These independent sales representatives supplement our direct sales force in dealing with language and cultural matters. Our domestic and foreign independent sales representatives earn commissions on sales, which vary by product type.

Backlog

The dollar amount of our backlog as of December 31, 2013, 2012 2011 and 20102011 was $617.4728.8 million, $489.1617.4 million and $236.4489.1 million, respectively. Approximately 10%8.6% of the December 31, 20122013 backlog is expected to be filled beyond 20132014. Backlog is comprised of the portion of firm signed purchase orders or other written contractual commitments received from customers that we have not recognized as revenue under the percentage of completion method or based upon shipment. Backlog can be significantly affected by the timing of orders for large products, particularly in the E&C segment, and the amount of backlog at December 31, 20122013 described above is not necessarily indicative of future backlog levels or the rate at which backlog will be recognized as sales. Orders included in our backlog may include customary cancellation provisions under which the customer could cancel all or part of the order, potentially subject to the payment of certain costs and/or penalties. For further information about our backlog, including backlog by segment, see Item 7.7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Customers

We sell our products primarily to gas producers, distributors and end-users across the industrial gas, hydrocarbon and chemical processing and biomedical industries in countries throughout the world. Sales to our top ten customers accounted for 38%37%, 36%38% and 38%36% of consolidated sales in 2013, 2012 2011 and 20102011, respectively. No single customer exceeded 10% of consolidated sales in 20122013. Our sales to particular customers fluctuate from period to period, but the global producers and distributors of hydrocarbon and industrial gases and their suppliers tend to be a consistently large source of revenue for us. Our supply contracts are generally contracts for “requirements” only. While our customers may be obligated to purchase a certain percentage of their supplies from us, there are generally no minimum requirements. Also, many of our contracts may be canceled on as little as one month’s notice. To minimize credit risk from trade receivables, we review the financial condition of potential customers in relation to established credit requirements before sales credit is extended and monitor the financial condition of customers to help ensure timely collections and to minimize losses. In addition, for certain domestic and foreign customers, particularly in the E&C segment, we require advance payments, letters of credit and other such guarantees of payment. Certain customers also require us to issue letters of credit or performance bonds, particularly in instances where advance payments are involved, as a condition of placing the order. We believe our relationships with our customers are generally good.

Intellectual Property

Although we have a number of patents, trademarks and licenses related to our business, no one of them or related group of them is considered by us to be of such importance that its expiration or termination would have a material adverse effect on

our business. In general, we depend upon technological capabilities, manufacturing quality control and application of know-how, rather than patents or other proprietary rights, in the conduct of our business.

Raw Materials and Suppliers

We manufacture most of the products we sell. The raw materials used in manufacturing include aluminum products (including sheets, bars, plate and piping), stainless steel products (including sheets, plates, heads and piping), palladium oxide, carbon steel products (including sheets, plates and heads), valves and gauges and fabricated metal components. Most raw materials are available from multiple sources of supply. We believe our relationships with our raw material suppliers and other vendors are generally good. Raw material prices were fairly stable during 2012,2013, and we expect them to remain stable during 2013.2014. Subject to certain risks related to our suppliers as discussed under Item 1A. “Risk Factors,” we foresee no acute shortages of any raw materials that would have a material adverse effect on our operations.

Employees

As of January 31, 20132014, we had 4,8425,086 employees, including 2,0182,826 domestic employees and 2,8242,260 international employees. These employees consisted of 2,1392,280 salaried, 433473 bargaining unit hourly and 2,2702,333 non-bargaining unit hourly.

We are a party to one collective bargaining agreement with the International Association of Machinists and Aerospace Workers ("IAM") covering 433473 employees at our La Crosse, Wisconsin heat exchanger facility. On October 31, 2012,Effective February 3, 2013, we entered into a new five-year agreement with the IAM which replaced the previous agreement that had an expiration date of February 2, 2013. The five-year term will extend from February 3, 2013 toexpires on February 3, 2018.

Environmental Matters

Our operations have historically included and currently include the handling and use of hazardous and other regulated substances, such as various cleaning fluids used to remove grease from metal, that are subject to federal, state and local environmental laws and regulations. These regulations impose limitations on the discharge of pollutants into the soil, air and water, and establish standards for their handling, management, use, storage and disposal. We monitor and review our procedures and policies for compliance with environmental laws and regulations. Our management is familiar with these regulations and supports an ongoing program to maintain our adherence to required standards.

We are involved with environmental compliance, investigation, monitoring and remediation activities at certain of our owned or formerly owned manufacturing facilities and at one owned facility that is leased to a third party. We believe that we are currently in substantial compliance with all known environmental regulations. We accrue for certain environmental remediation-related activities for which commitments or remediation plans have been developed or for which costs can be reasonably estimated. These estimates are determined based upon currently available facts regarding each facility. Actual costs incurred may vary from these estimates due to the inherent uncertainties involved. Future expenditures relating to these environmental remediation efforts are expected to be made over the next 14 years as ongoing costs of remediation programs. We do not believe that these regulatory requirements have had a material effect upon our capital expenditures, earnings or competitive position. We are not anticipating any material capital expenditures in 20132014 that are directly related to regulatory compliance matters. Although we believe we have adequately provided for the cost of all known environmental conditions, additional contamination, the outcome of disputed matters or changes in regulatory posture could result in more costly remediation measures than budgeted, or those we believe are adequate or required by existing law. We believe that any additional liability in excess of amounts accrued which may result from the resolution of such matters will not have a material adverse effect on our financial position, liquidity, cash flows or results of operations.

Available Information

Additional information about the Company is available at www.chartindustries.com. On the Investor Relations page of the website, the public may obtain free copies of the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable following the time that they are filed with, or furnished to, the Securities and Exchange Commission (SEC)(“SEC”). Additionally, the Company has posted its Code of Ethical Business Conduct and Officer Code of Ethics on its website, which are also available free of charge to any shareholder interested in obtaining a copy. This Form 10-K and reports filed with the SEC are also accessible through the SEC’s website at www.sec.gov. References to our website or the SEC’s website do not constitute incorporation by reference of the information contained on such websites, and such information is not part of this Form 10-K.

Investing in our common stock involves risk. You should carefully consider the risks described below as well as the other information contained in this Annual Report on Form 10-K in evaluating your investment in us. If any of the following risks actually occur, our business, financial condition, operating results or cash flows could be harmed materially. Additional risks, uncertainties and other factors that are not currently known to us or that we believe are not currently material may also adversely affect our business, financial condition, operating results or cash flows. In any of these cases, you may lose all or part of your investment in us.

Risks Related to Our Business

The markets we serve are subject to cyclical demand and vulnerable to economic downturn, which could harm our business and make it difficult to project long-term performance.

Demand for our products depends in large part upon the level of capital and maintenance expenditures by many of our customers and end users,end-users, in particular those customers in the global hydrocarbon and industrial gas markets. These customers’ expenditures historically have been cyclical in nature and vulnerable to economic downturns. Decreased capital and maintenance spending by these customers could have a material adverse effect on the demand for our products and our business, financial condition and results of operations. In addition, this historically cyclical demand limits our ability to make accurate long-term predictions about the performance of our company. Even if demand improves, it is difficult to predict whether any improvement represents a long-term improving trend or the extent or timing of improvement. There can be no assurance that historically improving cycles are representative of actual future demand.

While we experienced growth in demand from 2003 until mid-2008 in the global hydrocarbon and industrial gas markets, we experienced a significant decline in orders from mid-2008 until mid-2009. Since that time there has been improvement in orders for our businesses, particularly throughout 2011 and early 2012, and more recently in 2013, but we cannot predict whether business performance may be better or worse in the future.

The loss of, or significant reduction or delay in, purchases by our largest customers could reduce our sales and profitability.

A small number of customers has accounted for a substantial portion of our historical net sales. For example, sales to our top ten customers accounted for 38%37%, 36%38% and 38%36% of consolidated sales in 2013, 2012 2011 and 20102011, respectively. We expect that a limited number of customers will continue to represent a substantial portion of our sales for the foreseeable future. While our sales to particular customers fluctuate from period to period, the global producers and distributors of hydrocarbon and industrial gases and their suppliers tend to be a consistently large source of our sales.

The loss of any of our major customers or a decrease or delay in orders or anticipated spending by such customers could materially reduce our sales and profitability. For example, a delay in the anticipated timing of LNG infrastructure build out or respiratory therapy demand recovery could materially reduce the demand for our products. Our largest customers could also engage in business combinations, which could increase their size, reduce their demand for our products as they recognize synergies or rationalize assets and increase or decrease the portion of our total sales concentration to any single customer.

Decreases in energy prices may decrease demand for some of our products and cause downward pressure on the prices we charge, which could harm our business, financial condition and results of operations.

A significant amount of our sales are to customers in the energy production and supply industry. We estimate that 54%53% of our sales for the year ended December 31, 20122013 were generated by end-users in the energy industry. Accordingly, demand for a significant portion of our products depends upon the level of capital expenditures by companies in the oil and gas industry, which depends, in part, on energy prices. While some applications for our products could see greater demand if prices for natural gas remain relatively low compared to oil prices, a sustained decline in energy prices generally and a resultant downturn in energy production activities could negatively affect the capital expenditures of our customers. Any significant decline in the capital expenditures of our customers, whether due to a decrease in the market price of energy or otherwise, may decrease demand for our products and cause downward pressure on the prices we charge. Accordingly, if there is a downturn in the energy production and supply industry, our business, financial condition and results of operations could be adversely affected.

Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing and the potential for related regulatory action or litigation could result in increased costs and additional operating restrictions or delays for our customers, which could negatively impact our business, financial condition and results of operations.

We supply equipment to companies that process, transport and utilize natural gas, many of which benefit from increased natural gas production resulting from hydraulic fracturing in the oil and natural gas industry. As a result, increased regulation

of hydraulic fracturing may adversely impact our business, financial condition and results of operations. If additional levels of

regulation are implemented with respect to hydraulic fracturing, it may make it more difficult to complete natural gas wells in shale formations and discourage exploration of new wells. This could increase our customers' costs of compliance and doing business or otherwise adversely affect the hydraulic fracturing services they perform, which may negatively impact natural gas production and demand for our equipment used in the natural gas industry.

In addition, heightened political, regulatory and public scrutiny of hydraulic fracturing practices could potentially expose our customers to increased legal and regulatory proceedings, which could negatively impact natural gas production and demand for our equipment used in the natural gas industry. Any such developments could have a material adverse effect on our business, financial condition and results of operations, whether directly or indirectly.

We may be unable to compete successfully in the highly competitive markets in which we operate.

Although many of our products serve niche markets, a number of our direct and indirect competitors in these markets are major corporations, some of which have substantially greater technical, financial and marketing resources than Chart, and other competitors enter these markets from time to time. Any increase in competition may cause us to lose market share or compel us to reduce prices to remain competitive, which could result in reduced sales and earnings. We compete with several suppliers owned by global industrial gas producers or large industrial companies and many smaller fabrication-only facilities around the world. Increased competition with these companies could prevent the institution of price increases or could require price reductions or increased spending on research and development, and marketing and sales, any of which could materially reduce our sales, profitability or both. Moreover, during an industry downturn, competition in some of the product lines we serve increases as a result of over-capacity, which may result in downward pricing pressure. Further, customers who typically outsource their need for cryogenic systems to us may use their excess capacity to produce such systems themselves. We also compete in the sale of a limited number of products with certain of our major customers. If we are unable to compete successfully, our results of operations, cash flows and financial condition could be negatively affected.

Governmental energy policies could change, or expected changes could fail to materialize, which could adversely affect our business or prospects.

Energy policy can develop rapidly in the markets we serve, including the United States. Within the last few years, significant developments have taken place, primarily in international markets that we serve with respect to energy policy and related regulations. We anticipate that energy policy will continue to be an important regulatory priority globally as well as on a national, state and local level. As energy policy continues to evolve, the existing rules and incentives that impact the energy-related segments of our business may change. It is difficult, if not impossible, to predict whether changes in energy policy might occur in the future and the timing of potential changes and their impact on our business. The elimination or reduction of favorable policies for our energy-related business, or the failure to adopt expected policies that would benefit our business, could negatively impact our sales and profitability. For example, China’s 12th Five-Year Plan promotes the use of natural gas by mandating an increase of gas as a percentage of energy consumption from less thatthan 4% to over 8%. Our business prospects in China could be harmed if China changed this policy or the mandate is not otherwise achieved.

We may be unable to compete successfully in the highly competitive markets in which we operate.

Although many of our products serve niche markets, a number of our direct and indirect competitors in these markets are major corporations, some of which have substantially greater technical, financial and marketing resources than Chart, and other competitors enter these markets from time to time. Any increase in competition may cause us to lose market share or compel us to reduce prices to remain competitive, which could result in reduced sales and earnings. Companies, or their divisions, that operate in our industry include Air Products, Kobe, Linde, Fives, Sumitomo, CVA and Taylor-Wharton. Additionally, we compete with several suppliers owned by global industrial gas producers and many smaller fabrication-only facilities around the world. Increased competition with these companies could prevent the institution of price increases or could require price reductions or increased spending on research and development, and marketing and sales, any of which could materially reduce our sales, profitability or both. Moreover, during an industry downturn, competition in some of the product lines we serve increases as a result of over-capacity, which may result in downward pricing pressure. Further, customers who typically outsource their need for cryogenic systems to us may use their excess capacity to produce such systems themselves. We also compete in the sale of a limited number of products with certain of our major customers. If we are unable to compete successfully manage our resultsplanned operational expansions, it may place a significant strain on our management and administrative resources and lead to increased costs and reduced profitability.

We expect to continue to expand our operations, particularly in China and the United States, in markets where we perceive the opportunity for profitable expansion. Our ability to operate our business successfully and implement our strategies depends, in part, on our ability to allocate our resources optimally in each of our facilities in order to maintain efficient operations cash flowsas we expand. Ineffective management of our growth could cause manufacturing inefficiencies, increase our operating costs, place significant strain on our management and financial conditionadministrative resources and prevent us from implementing our business plan.

For example, we have invested or plan to invest approximately $60 to $90 million in new capital expenditures in 2014 related to the expected growth of selective parts of each of the E&C, D&S and BioMedical segments. If we fail to implement these projects in a timely and effective manner, we may lose the opportunity to obtain some new customer orders. Even if we effectively implement these projects, the orders needed to support the capital expenditure may not be obtained, may be delayed, or may be less than expected, which may result in sales or profitability at lower levels than anticipated. For example, while we invested in the expansion of our E&C segment in past years, we experienced delay in some of the orders initially anticipated to support the cold box portion of that expansion, which resulted in the underutilization of some of our capacity. In addition, potential cost overruns, delays or unanticipated problems in any capital expansion could be negatively affected.make the expansions more costly than originally predicted or cause us to miss windows of opportunity.

Downturns in economic and financial conditions have had and may have in the future a negative effect on our business, financial condition and results of operations.

Demand for our products depends in large part upon the level of capital and maintenance expenditures by many of our customers and end users. While general economic conditions improved throughout 2011 and early 2012 and continue to improve in many parts of the world, there has been continued economic weakness in Europe and aend-users. A downturn in economic conditions there or elsewherein markets in which we operate may reduce the willingness or ability of our customers and prospective customers to commit funds to purchase our products and services, and may reduce their ability to pay for our products and services after purchase. Economic conditions that could impact our business include, but are not limited to, recessionary conditions, slow or negative economic growth rates, the impact of state and sovereign debt defaults or the impact of U.S. budgetary pressures. Similarly, our suppliers may not be able to supply us with needed raw materials or components on a timely basis, may increase prices or go out of business, which could result in our inability to meet customer demand, or fulfill our contractual obligations or could affect our gross margins. See “We depend on the availability of certain key suppliers; if we experience difficulty with a supplier, we may have difficulty finding alternative sources of supply” below. We cannot predict the timing or duration of negative market conditions. If the economy or markets in which we operate deteriorate or financial markets weaken, our business, financial condition and results of operations could be adversely impacted.

Our exposure to fixed-price contracts, including exposure to fixed pricing on long-term customer contracts, could negatively impact our financial results.

A substantial portion of our sales has historically been derived from fixed-price contracts for large system projects, which may involve long-term fixed price commitments to customers and which are sometimes difficult to execute. We have experienced difficulties in executing large contracts of this kind in the past, including cost overruns, storm damage, supplier failures and customer disputes.

To the extent that any of our fixed-price contracts are delayed, our subcontractors fail to perform, contract counterparties successfully assert claims against us, the original cost estimates in these or other contracts prove to be inaccurate or the contracts do not permit us to pass increased costs on to our customers, profitability from a particular contract may decrease or project losses may be incurred, which, in turn, could decrease our sales and overall profitability. The uncertainties associated with our fixed-price contracts make it more difficult to predict our future results and exacerbate the risk that our results will not match expectations, which has happened in the past.

If we are unable to successfully manage our planned operational expansions, it may place a significant strain on our management and administrative resources and lead to increased costs and reduced profitability.

We expect to continue to expand our operations, particularly in China and the United States, in markets where we perceive the opportunity for profitable expansion. Our ability to operate our business successfully and implement our strategies depends, in part, on our ability to allocate our resources optimally in each of our facilities in order to maintain efficient operations as we expand. Ineffective management of our growth could cause manufacturing inefficiencies, increase our operating costs, place significant strain on our management and administrative resources and prevent us from implementing our business plan.

For example, we have invested or plan to invest approximately $70 to $80 million in new capital expenditures in 2013 related to the expected growth of selective parts of each of the E&C, D&S and BioMedical segments. If we fail to implement these projects in a timely and effective manner, we may lose the opportunity to obtain some new customer orders. Even if we effectively implement these projects, the orders needed to support the capital expenditure may not be obtained, may be delayed, or may be less than expected, which may result in sales or profitability at lower levels than anticipated. For example, while we invested in the expansion of our E&C segment in recent years, we experienced delay in some of the orders initially anticipated to support the cold box portion of that expansion, which resulted in the underutilization of some of our capacity. In addition, potential cost overruns, delays or unanticipated problems in any capital expansion could make the expansions more costly than originally predicted or cause us to miss windows of opportunity.

We depend on the availability of certain key suppliers; if we experience difficulty with a supplier, we may have difficulty finding alternative sources of supply.

The cost, quality and availability of raw materials and certain specialty metals used to manufacture our products are critical to our success. The materials and components we use to manufacture our products are sometimes custom made and may be available only from a few suppliers, and the lead times required to obtain these materials and components can often be significant. We rely on sole suppliers or a limited number of suppliers for some of these materials, including special grades of aluminum used in our brazed aluminum heat exchangers. While we have not historically encountered problems with availability, this does not mean that we will continue to have timely access to adequate supplies of essential materials and components in the future or that supplies of these materials and components will be available on satisfactory terms when needed. If our vendors for these materials and components are unable to meet our requirements, fail to make shipments in a timely manner or ship defective materials or components, we could experience a shortage or delay in supply or fail to meet our contractual requirements, which would adversely affect our results of operations and negatively impact our cash flow and profitability.

Our backlog is subject to modification or termination of orders, which could negatively impact our sales.

Our backlog is comprised of the portion of firm signed purchase orders or other written contractual commitments received from customers that we have not recognized as sales. The dollar amount of backlog as of December 31, 20122013 was $617.4728.8 million. Our backlog can be significantly affected by the timing of orders for large products,projects, particularly in our E&C segment, and the amount of our backlog at December 31, 20122013 is not necessarily indicative of future backlog levels or the rate at which backlog will be recognized as sales. Although historically the amount of modifications and terminations of our orders has not been material compared to our total contract volume and is partially offset by cancellation penalties, customers can, and sometimes do, terminate or modify these orders. We cannot predict whether cancellations will accelerate or diminish in the future. Cancellations of purchase orders or reductions of product quantities in existing contracts could substantially and

materially reduce our backlog and, consequently, our future sales. Our failure to replace canceled or reduced backlog could negatively impact our sales and results of operations.

Health care reform or other changes in government and other third-party payor reimbursement levels and practices could negatively impact our sales and profitability.

Acquisitions by our BioMedical segment have significantly increased the size and impact on our financial results of our respiratory products business. Many of our BioMedical segment’s customers are reimbursed for products and services by third-party payors, such as government programs, including Medicare and Medicaid, private insurance plans and managed care programs in the U.S, and by similar programs and entities in the other countries in which we operate or sell our equipment. In the United States, the Centers for Medicare & Medicaid Services (CMS), the agency responsible for administering the Medicare program, implemented a number of payment rules that reduced Medicare payments for oxygen and oxygen equipment, including a competitive bidding program effective January 1, 2011. Under the competitive bidding program, CMS selected contract suppliers that agreed to receive as payment the “single payment amount” calculated by CMS in certain geographic regions. If third-party payors deny coverage, make the reimbursement process or documentation requirements more uncertain or reduce levels of reimbursement, it could negatively affect our sales and profitability.

In March 2010, health care reform legislation known as the Affordable Care Act was adopted in the United States. The new law includes provisions that, among other things, reduce and/or limit Medicare reimbursement, require all individuals to have health insurance (with limited exceptions) and impose new and/or increased taxes. In addition, the Affordable Care Act requires CMS to nationalize the competitive bidding process or adjust the prices in non-competitive bidding areas to match competitive bidding prices. The Affordable Care Act could impact the demand for our products or the prices at which we sell our products. The impact of this law and these proposals could have a material adverse effect on our business, results of operations and/or financial condition.

As a global business, we are exposed to economic, political and other risks in different countries which could materially reduce our sales, profitability or cash flows, or materially increase our liabilities.

Since we manufacture and sell our products worldwide, our business is subject to risks associated with doing business internationally. In 2012, 2011 and 2010, 56%, 58% and 57%, respectively, of our sales were made in international markets. Our future results could be harmed by a variety of factors, including:

changes in foreign currency exchange rates;

exchange controls and currency restrictions;

changes in a specific country’s or region’s political, social or economic conditions, particularly in emerging markets;

civil unrest, turmoil or outbreak of disease in any of the countries in which we operate or sell our products;

tariffs, other trade protection measures and import or export licensing requirements;

potentially negative consequences from changes in U.S. and international tax laws;

difficulty in staffing and managing geographically widespread operations;

differing labor regulations;

requirements relating to withholding taxes on remittances and other payments by subsidiaries;

different regulatory regimes controlling the protection of our intellectual property;

restrictions on our ability to own or operate subsidiaries, make investments or acquire new businesses in these jurisdictions;

restrictions on our ability to repatriate dividends from our foreign subsidiaries;

difficulty in collecting international accounts receivable;

difficulty in enforcement of contractual obligations under non-U.S. law;

transportation delays or interruptions;

changes in regulatory requirements; and

the burden of complying with multiple and potentially conflicting laws.

For example, the continuing European sovereign debt crisis has negatively affected economic conditions in Europe and globally. If the European sovereign debt crisis continues or deepens, economic conditions in Europe may further deteriorate. In that case, our business in Europe and elsewhere, as well as the businesses of our customers and suppliers, may be adversely affected.

Our international operations and sales also expose us to different local political and business risks and challenges. For example, we are faced with potential difficulties in staffing and managing local operations and we have to design local solutions to manage credit and legal risks of local customers and distributors, which may not be effective. In addition, because some of our international sales are to suppliers that perform work for foreign governments, we are subject to the political risks associated with foreign government projects. For example, certain foreign governments may require suppliers for a project to obtain products solely from local manufacturers or may prohibit the use of products manufactured in certain countries.

International growth and expansion into emerging markets, such as China, Central and Eastern Europe, India, the Middle East and Latin America, may cause us difficulty due to greater regulatory barriers than in the United States, the necessity of adapting to new regulatory systems, problems related to entering new markets with different economic, social and political systems and conditions, and significant competition from the primary participants in these markets, some of which may have substantially greater resources than us. For example, unstable political conditions or civil unrest, including political instability in North Africa and the Middle East, could negatively impact our order levels and sales in a region or our ability to collect receivables from customers or operate or execute projects in a region.

Our international operations and transactions also depend upon favorable trade relations between the United States and those foreign countries in which our customers and suppliers have operations. A protectionist trade environment in either the United States or those foreign countries in which we do business or sell products, such as a change in the current tariff structures, export compliance, government subsidies or other trade policies, may adversely affect our ability to sell our products or do business in foreign markets. Our overall success as a global business depends, in part, upon our ability to succeed in differing economic, social and political conditions. We may not succeed in developing and implementing policies and strategies to counter the foregoing factors effectively in each location where we do business and the foregoing factors may cause a reduction in our sales, profitability or cash flows, or cause an increase in our liabilities.

We may fail to successfully acquire or integrate companies that provide complementary products or technologies.

A component of our business strategy is the acquisition of businesses that complement our existing products and services. Such a strategy involves the potential risks inherent in assessing the value, strengths, weaknesses, contingent or other liabilities and potential profitability of acquisition candidates and in integrating the operations of acquired companies. In addition, any acquisitions of businesses with foreign operations or sales may increase our exposure to risks inherent in doing business outside the United States.

From time to time, we may have acquisition discussions with potential target companies both domestically and internationally. If a large acquisition opportunity arises and we proceed, a substantial portion of our cash and surplus borrowing capacity could be used for the acquisition or we may seek additional debt or equity financing. For example, in August 2012 we used a substantial portion of our available cash to acquire AirSep Corporation.

Potential acquisition opportunities become available to us from time to time, and we engage periodically in discussions or negotiations relating to potential acquisitions, including acquisitions that may be material in size or scope to our business. Any acquisition may or may not occur and, if an acquisition does occur, it may not be successful in enhancing our business for one or more of the following reasons:

Any business acquired may not be integrated successfully and may not prove profitable;

The price we pay for any business acquired may overstate the value of that business or otherwise be too high;

Liabilities we take on through the acquisition may prove to be higher than we expected;

We may fail to achieve acquisition synergies; or

The focus on the integration of operations of acquired entities may divert management’s attention from the day-to-day operation of our businesses.

Inherent in any future acquisition is the risk of transitioning company cultures and facilities. The failure to efficiently and effectively achieve such transitions could increase our costs and decrease our profitability.

If we lose our senior managementHealth care reform or other key employees,changes in government and other third-party payor reimbursement levels and practices could negatively impact our business may be adversely affected.sales and profitability.

Our ability to successfully operateAcquisitions by our BioMedical segment have significantly increased the size and growimpact on our business and implementfinancial results of our strategies is largely dependent on the efforts, abilitiesrespiratory products business. Many of our BioMedical segment’s customers are reimbursed for products and services of our senior management and other key employees. Our future success will also depend on, among other factors, our ability to attract and retain qualified personnel,by third-party payors, such as engineersgovernment programs, including Medicare and Medicaid, private insurance plans and managed care programs in the U.S, and by similar programs and entities in the other skilled labor, either through direct hiringcountries in which we operate or sell our equipment. In the acquisitionUnited States, the Centers for Medicare & Medicaid Services (“CMS”), the agency responsible for administering the Medicare program, implemented a number of other businesses employing such professionals. Our products, manypayment rules that reduced Medicare payments for oxygen and oxygen equipment, including a competitive bidding program effective January 1, 2011. Under the competitive bidding program, CMS selected contract suppliers that agreed to receive as payment the “single payment amount” calculated by CMS in certain geographic regions. In addition, CMS has increased the level of audit activity involving the sales practices of intermediaries in the health care field, some of which are highly engineered, represent specialized applicationscustomers of cryogenic low temperatureours for respiratory products we sell. If third-party payors deny coverage, make the reimbursement process or gas processing technologiesdocumentation requirements more burdensome or uncertain, or reduce levels of reimbursement, it could negatively affect our sales and know-how,profitability.

In March 2010, the Affordable Care Act was adopted in the United States. The law includes provisions that, among other things, reduce and/or limit Medicare reimbursement, require all individuals to have health insurance (with limited exceptions) and manyimpose new and/or increased taxes. In addition, the Affordable Care Act requires CMS to nationalize the competitive bidding process or adjust the prices in non-competitive bidding areas to match competitive bidding prices. There remains a significant amount of uncertainty regarding the implementation of the marketsAffordable Care Act, and the potential impact of such policies on the demand for our products or the prices at which we serve represent niche markets for these specialized applications. Accordingly,sell our products. Any such negative impact in demand or product prices associated with the Affordable Care Act could have a material adverse effect on our business, results of operations and/or financial condition.

As a global business, we rely heavilyare exposed to economic, political and other risks in different countries which could materially reduce our sales, profitability or cash flows, or materially increase our liabilities.

Since we manufacture and sell our products worldwide, our business is subject to risks associated with doing business internationally. In 2013, 2012 and 2011, 59%, 56% and 58%, respectively, of our sales were made in international markets. Our future results could be harmed by a variety of factors, including:

changes in foreign currency exchange rates;

exchange controls and currency restrictions;

changes in a specific country’s or region’s political, social or economic conditions, particularly in emerging markets;

civil unrest, turmoil or outbreak of disease in any of the countries in which we operate or sell our products;

tariffs, other trade protection measures and import or export licensing requirements;

potentially negative consequences from changes in U.S. and international tax laws;

difficulty in staffing and managing geographically widespread operations;

differing labor regulations;

requirements relating to withholding taxes on engineers, salespersons, business unit leaders, senior managementremittances and other key employees who have experiencepayments by subsidiaries;

different regulatory regimes controlling the protection of our intellectual property;

restrictions on our ability to own or operate subsidiaries, make investments or acquire new businesses in these specialized applicationsjurisdictions;

restrictions on our ability to repatriate dividends from our foreign subsidiaries;

difficulty in collecting international accounts receivable;

difficulty in enforcement of contractual obligations under non-U.S. law;

transportation delays or interruptions;

changes in regulatory requirements; and

the burden of complying with multiple and potentially conflicting laws.

Our international operations and sales also expose us to different local political and business risks and challenges. For example, we are knowledgeable aboutfaced with potential difficulties in staffing and managing local operations and we have to design local solutions to manage credit and legal risks of local customers and distributors, which may not be effective. In addition, because some of our international sales are to suppliers that perform work for foreign governments, we are subject to the political risks associated with foreign government projects. For example, certain foreign governments may require suppliers for a project to obtain products solely from local manufacturers or may prohibit the use of products manufactured in certain countries.

International growth and expansion into markets such as China, Central and Eastern Europe, India, the Middle East and Latin America, may cause us difficulty due to greater regulatory barriers than in the United States, the necessity of adapting to new regulatory systems, problems related to entering new markets with different economic, social and political systems and conditions, and significant competition from the primary participants in these niche markets, some of which may have substantially greater resources than us. For example, unstable political conditions or civil unrest, including political instability in North Africa, the Middle East or elsewhere, could negatively impact our order levels and sales in a region or our ability to collect receivables from customers or operate or execute projects in a region.

Our international operations and transactions also depend upon favorable trade relations between the United States and those foreign countries in which our customers and suppliers have operations. A protectionist trade environment in either the United States or those foreign countries in which we do business or sell products, such as a change in the current tariff structures, export compliance, government subsidies or other trade policies, may adversely affect our ability to sell our products or do business in foreign markets. Our overall success as a global business depends, in part, upon our ability to succeed in differing economic, social and political conditions. We may not succeed in developing and implementing policies and strategies to counter the foregoing factors effectively in each location where we do business and the foregoing factors may cause a reduction in our company. Additionally, we may modifysales, profitability or cash flows, or cause an increase in our management structure from time to time or substantially reduce our overall workforce as we did in certain sectors of our business during the recent economic downturn, which may create marketing, operational and other business risks. The loss of the services of these senior managers or other key employees or the failure to attract or retain other qualified personnel could reduce the competitiveness of our business or otherwise impair our business prospects.liabilities.

Due to the nature of our business and products, we may be liable for damages based on product liability and warranty claims.