Item 4. |

|

During the quarter ended June 30, 2008 no matter was submitted to a vote of security holders.

PART II

PART II | |

Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

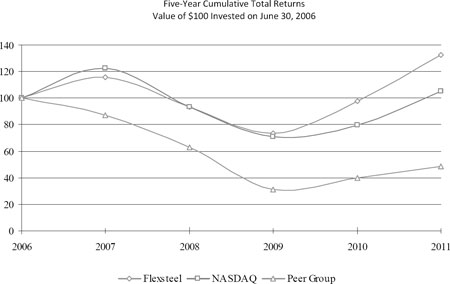

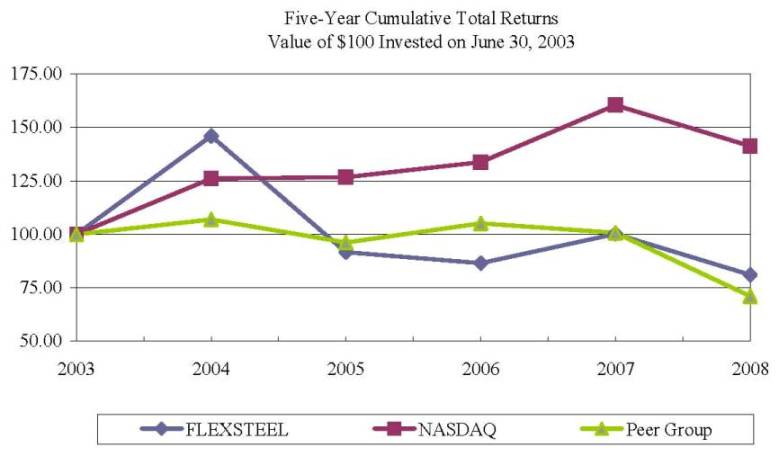

Share Investment Performance

The following graph is based upon the SIC Code #251 Household Furniture Index as a peer group. It shows changes over the past five-year period in the value of $100 invested in: (1) Flexsteel’s common stock; (2) The NASDAQ Global Market; and (3) an industry peer group of the following: Bassett Furniture Ind., Chromcraft Revington Inc., Ethan Allen Interiors, Furniture Brands Intl., Hooker Furniture Corp., InterfaceKimball International, La-Z-Boy Inc., Kimball International, Natuzzi S.P.A., La-Z-Boy Inc., and Stanley Furniture Inc.

| 2003 |

| 2004 |

| 2005 |

| 2006 |

| 2007 |

| 2008 |

Flexsteel | 100.00 |

| 146.06 |

| 91.75 |

| 86.56 |

| 100.25 |

| 81.05 |

Peer Group | 100.00 |

| 106.94 |

| 96.27 |

| 105.22 |

| 100.73 |

| 71.11 |

NASDAQ | 100.00 |

| 126.19 |

| 126.75 |

| 133.85 |

| 160.42 |

| 141.30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2006 |

| 2007 |

| 2008 |

| 2009 |

| 2010 |

| 2011 |

| ||||||

Flexsteel |

| 100.00 |

|

| 115.82 |

|

| 93.64 |

|

| 73.16 |

|

| 97.88 |

|

| 132.62 |

|

|

Peer Group |

| 100.00 |

|

| 87.04 |

|

| 62.64 |

|

| 31.24 |

|

| 39.52 |

|

| 48.76 |

|

|

NASDAQ |

| 100.00 |

|

| 122.72 |

|

| 93.36 |

|

| 71.02 |

|

| 79.93 |

|

| 105.32 |

|

|

The NASDAQ Global Market is the principal market on which the Company’s common stock is traded.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Sale Price of Common Stock * |

| Cash Dividends |

| ||||||||||||||

|

| Fiscal 2011 |

| Fiscal 2010 |

|

| |||||||||||||

|

| High |

| Low |

| High |

| Low |

| Fiscal 2011 |

| Fiscal 2010 |

| ||||||

First Quarter |

| $ | 15.84 |

| $ | 10.08 |

| $ | 8.84 |

| $ | 6.64 |

| $ | 0.075 |

| $ | 0.05 |

|

Second Quarter |

|

| 18.75 |

|

| 14.22 |

|

| 10.34 |

|

| 7.77 |

|

| 0.075 |

|

| 0.05 |

|

Third Quarter |

|

| 19.69 |

|

| 14.11 |

|

| 16.50 |

|

| 9.33 |

|

| 0.075 |

|

| 0.05 |

|

Fourth Quarter |

|

| 16.60 |

|

| 13.80 |

|

| 15.74 |

|

| 10.75 |

|

| 0.075 |

|

| 0.05 |

|

|

| Sale Price of Common Stock * |

| Cash Dividends |

| ||||||||||||||

|

| Fiscal 2008 |

| Fiscal 2007 |

|

| |||||||||||||

|

| High |

| Low |

| High |

| Low |

| Fiscal 2008 |

| Fiscal 2007 |

| ||||||

First Quarter |

| $ | 14.75 |

| $ | 12.92 |

| $ | 13.59 |

| $ | 12.02 |

| $ | 0.13 |

| $ | 0.13 |

|

Second Quarter |

|

| 14.86 |

|

| 11.60 |

|

| 13.26 |

|

| 11.55 |

|

| 0.13 |

|

| 0.13 |

|

Third Quarter |

|

| 14.50 |

|

| 11.00 |

|

| 15.47 |

|

| 12.51 |

|

| 0.13 |

|

| 0.13 |

|

Fourth Quarter |

|

| 13.98 |

|

| 11.01 |

|

| 15.94 |

|

| 12.71 |

|

| 0.13 |

|

| 0.13 |

|

* Reflects the market price as reported on The NASDAQ Global Market.

The Company estimates there were approximately 1,9001,600 holders of common stock of the Company as of June 30, 2008.2011.

There were no repurchases of the Company’s common stock during the quarter ended June 30, 2008.2011.

The payment of future cash dividends is within the discretion of our Board of Directors and will depend, among other factors, on our earnings, capital requirements and operating and financial condition.

Item 6. | Selected Financial Data |

The selected financial data presented below should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in Item 8 of this Annual Report on Form 10-K and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K. The selected consolidated statement of operations data of the Company is derived from the Company’s consolidated financial statements.

Five-Year Review

(Amounts in thousands, except certain ratios and per share data)

|

| FOR THE YEARS ENDED JUNE 30, |

| |||||||||||||

|

| 2008 |

| 2007 |

| 2006 |

| 2005 |

| 2004 (6) |

| |||||

SUMMARY OF OPERATIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

| $ | 405,655 |

| $ | 425,400 |

| $ | 426,408 |

| $ | 410,023 |

| $ | 401,222 |

|

Cost of goods sold |

|

| 327,165 |

|

| 344,177 |

|

| 345,068 |

|

| 334,978 | (1) |

| 318,526 | (1) |

Operating income |

|

| 7,596 |

|

| 14,699 |

|

| 8,561 |

|

| 7,258 | (1) |

| 16,123 | (1) |

Interest and other income |

|

| 469 |

|

| 1,277 |

|

| 775 |

|

| 628 |

|

| 977 |

|

Interest expense |

|

| 1,468 |

|

| 1,491 |

|

| 1,557 |

|

| 990 |

|

| 839 |

|

Income before income taxes |

|

| 6,596 |

|

| 14,484 |

|

| 7,778 |

|

| 6,896 | (1) |

| 16,261 | (1) |

Provision for income taxes (5) |

|

| 2,360 |

|

| 5,150 |

|

| 3,060 |

|

| 1,990 | (1) |

| 6,430 | (1) |

Net income (2) (3) (4) (5) |

|

| 4,236 |

|

| 9,334 |

|

| 4,718 |

|

| 4,906 | (1) |

| 9,831 | (1) |

Earnings per common share: (2) (3) (4) (5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 0.64 |

|

| 1.42 |

|

| 0.72 |

|

| 0.75 | (1) |

| 1.53 | (1) |

Diluted |

|

| 0.64 |

|

| 1.42 |

|

| 0.72 |

|

| 0.74 | (1) |

| 1.51 | (1) |

Cash dividends declared per common share |

| $ | 0.52 |

| $ | 0.52 |

| $ | 0.52 |

| $ | 0.52 |

| $ | 0.52 |

|

SELECTED DATA AS OF JUNE 30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average common shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 6,574 |

|

| 6,568 |

|

| 6,558 |

|

| 6,531 |

|

| 6,440 |

|

Diluted |

|

| 6,611 |

|

| 6,583 |

|

| 6,577 |

|

| 6,601 |

|

| 6,530 |

|

CONSOLIDATED BALANCE SHEET DATA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

| $ | 179,906 |

| $ | 185,014 | (1) | $ | 184,176 | (1) | $ | 165,221 | (1) | $ | 169,220 | (1) |

Property, plant and equipment, net |

|

| 26,372 |

|

| 28,168 |

|

| 24,158 |

|

| 26,141 |

|

| 30,327 |

|

Capital expenditures |

|

| 1,228 |

|

| 10,839 |

|

| 3,411 |

|

| 3,347 |

|

| 6,030 |

|

Long-term debt |

|

| 20,811 |

|

| 21,336 |

|

| 21,846 |

|

| 12,800 |

|

| 17,583 |

|

Working capital (current assets less current liabilities) |

|

| 100,920 |

|

| 97,902 | (1) |

| 95,551 | (1) |

| 83,952 |

| 83,054 | (1) | |

Shareholders’ equity |

| $ | 112,752 |

| $ | 112,679 | (1) | $ | 106,066 | (1) | $ | 103,361 | (1) | $ | 101,313 | (1) |

SELECTED RATIOS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income as percent of sales |

|

| 1.0 | % |

| 2.2 | % |

| 1.1 | % |

| 1.2 | %(1) |

| 2.5 | %(1) |

Current ratio |

|

| 3.5 to | 1 |

| 3.2 to | 1(1) |

| 2.9 to | 1(1) |

| 3.0 to | 1(1) |

| 2.9 to | 1(1) |

Return on ending shareholders’ equity |

|

| 3.8 | % |

| 8.3 | %(1) |

| 4.5 | %(1) |

| 4.8 | %(1) |

| 9.7 | %(1) |

Return on beginning shareholders’ equity |

|

| 3.8 | % |

| 8.8 | %(1) |

| 4.6 | %(1) |

| 4.8 | %(1) |

| 10.5 | %(1) |

Average number of employees |

|

| 2,140 |

|

| 2,290 |

|

| 2,400 |

|

| 2,460 |

|

| 2,610 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2011 |

| 2010 |

| 2009 |

| 2008 |

| 2007 |

| |||||

SUMMARY OF OPERATIONS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net sales |

| $ | 339,426 |

| $ | 326,466 |

| $ | 324,158 |

| $ | 405,655 |

| $ | 425,400 |

|

Cost of goods sold |

|

| 262,124 |

|

| 251,685 |

|

| 263,083 |

|

| 327,165 |

|

| 344,177 |

|

Operating income (loss) |

|

| 15,864 |

|

| 17,529 |

|

| (2,272 | ) |

| 7,596 |

|

| 14,699 |

|

Interest and other income |

|

| 343 |

|

| 361 |

|

| 661 |

|

| 469 |

|

| 1,277 |

|

Interest expense |

|

| — |

|

| 439 |

|

| 968 |

|

| 1,469 |

|

| 1,491 |

|

Income (loss) before income taxes |

|

| 16,207 |

|

| 17,451 |

|

| (2,579 | ) |

| 6,596 |

|

| 14,484 |

|

Income tax provision (benefit) |

|

| 5,790 |

|

| 6,650 |

|

| (1,070 | ) |

| 2,360 |

|

| 5,150 |

|

Net income (loss) (1) (2) (3) |

|

| 10,417 |

|

| 10,801 |

|

| (1,509 | ) |

| 4,236 |

|

| 9,334 |

|

Earnings (loss) per common share: (1) (2) (3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 1.56 |

|

| 1.63 |

|

| (0.23 | ) |

| 0.64 |

|

| 1.42 |

|

Diluted |

|

| 1.50 |

|

| 1.61 |

|

| (0.23 | ) |

| 0.64 |

|

| 1.42 |

|

Cash dividends declared per common share |

| $ | 0.30 |

| $ | 0.20 |

| $ | 0.36 |

| $ | 0.52 |

| $ | 0.52 |

|

SELECTED DATA AS OF JUNE 30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average common shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 6,693 |

|

| 6,608 |

|

| 6,576 |

|

| 6,574 |

|

| 6,568 |

|

Diluted |

|

| 6,929 |

|

| 6,697 |

|

| 6,576 |

|

| 6,611 |

|

| 6,583 |

|

Total assets |

| $ | 164,677 |

| $ | 157,670 |

| $ | 150,971 |

| $ | 179,906 |

| $ | 185,014 |

|

Property, plant and equipment, net |

|

| 21,387 |

|

| 21,614 |

|

| 23,298 |

|

| 26,372 |

|

| 28,168 |

|

Capital expenditures |

|

| 2,573 |

|

| 1,251 |

|

| 1,203 |

|

| 1,228 |

|

| 10,839 |

|

Long-term debt |

|

| — |

|

| — |

|

| — |

|

| 20,811 |

|

| 21,336 |

|

Working capital (current assets less current liabilities) |

|

| 100,683 |

|

| 90,800 |

|

| 78,416 |

|

| 100,920 |

|

| 97,902 |

|

Shareholders’ equity |

| $ | 128,573 |

| $ | 117,612 |

| $ | 106,998 |

| $ | 112,752 |

| $ | 112,679 |

|

SELECTED RATIOS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss), as a percent of sales |

|

| 3.1 |

|

| 3.3 |

|

| (0.5 | ) |

| 1.0 |

|

| 2.2 |

|

Current ratio |

|

| 4.6 to 1 |

|

| 3.9 to 1 |

|

| 3.2 to 1 |

|

| 3.5 to 1 |

|

| 3.2 to 1 |

|

Return on ending shareholders’ equity |

|

| 8.1 |

|

| 9.2 |

|

| (1.4 | ) |

| 3.8 |

|

| 8.3 |

|

Average number of employees |

|

| 1,320 |

|

| 1,400 |

|

| 1,600 |

|

| 2,140 |

|

| 2,290 |

|

| |

(1) |

|

(2) |

|

(3) | Fiscal 2007 net income and per share amounts reflect the net gain (after tax) on sale of building of approximately $2.5 million or $0.37 per share, the gain on life insurance of $0.6 million or $0.08 per share and the net gain (after tax) on the sale of vacant land of approximately $0.2 million or $0.04 per share. |

|

|

|

|

|

|

|

|

|

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

All of the financial information presented in this Item 7 has been revised to reflect the impact of the restatement of the Company’s Consolidated Financial Statements, which is more fully described in Note 19, “Error Corrections” of the Notes to Consolidated Financial Statements in this Annual Report on Form 10-K. The cumulative impact of the unreconciled accounts payable was an increase to accounts payable of $2.3 million, an increase to deferred income taxes-current of $0.9 million and a reduction to Shareholder’s Equity of $1.4 million, as of July 1, 2005.General

General

The following analysis of the results of operations and financial condition of the Company should be read in conjunction with the consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K.

Critical Accounting Policies

The discussion and analysis of the Company’s consolidated financial statements and results of operations are based on consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America. Preparation of these consolidated financial statements requires the use of estimates and judgments that affect the reported results. The Company uses estimates based on the best information available in recording transactions and balances resulting from business operations. Estimates are used for such items as collectibility of trade accounts receivable and inventory valuation, depreciable lives, self-insurance programs, warranty costs and income taxes.valuation. Ultimate results may differ from these estimates under different assumptions or conditions.

Allowance for doubtful accounts – the Company establishes an allowance for doubtful accounts through review of open accounts, and historical collection and allowances amounts. The allowance for doubtful accounts is intended to reduce trade accounts receivable to the amount that reasonably approximates their net realizable fair value due to their short-term nature.value. The amount ultimately realized from trade accounts receivable may differ from the amount estimated in the consolidated financial statements based on collection experience and actual returns and allowances.experience.

Inventories – the Company values inventory at the lower of cost or market. A large portion of our finished goods inventory is made to order and many of our raw material parts are interchangeable between products. Historically inventory write-downs to market have been in fabric, wood frame and trim, and sourced products purchased for inventory. Management assesses the inventory on hand versus estimated future usage and estimated selling prices and if necessary writes down the obsolete or excess inventory to market. Although, we believe that inventory valuations are reasonable, unexpected changes in sales volume due to economic or competitive conditions may impact inventory valuations. Raw steel, lumber and wood frame parts are valued on the last-in, first-out (“LIFO”) method. Other inventories are valued on the first-in, first-out (“FIFO”) method. Changes in the market conditions could require a write down of inventory.

Self-insurance programs – the Company is self-insured for health care and most workers’ compensation up to predetermined amounts above which third party insurance applies. The Company purchases specific stop-loss insurance for individual health care claims in excess of $150,000 per plan year, with a $1.0 million individual lifetime maximum. For workers’ compensation the Company retains the first $350,000 per claim and purchases excess coverage up to the statutory limits for amounts in excess of the retention limit. The Company is contingently liable to insurance carriers under its comprehensive general, product, and vehicle liability policies, as well as some workers’ compensation. Losses are accrued based upon the Company’s estimates of the aggregate liability of claims incurred using certain actuarial assumptions followed in the insurance industry and based on Company experience. The actual claims experience could differ from the estimates made by the Company based on actual experience.

Income taxes – the Company accounts for income taxes in accordance with the provisions of Statement of Financial Accounting Standards (SFAS) No. 109, Accounting for Income Taxes. In the preparation of the Company’s consolidated financial statements, management calculates income taxes. This includes estimating the Company’s current tax liability as well as assessing temporary differences resulting from different treatment of items for tax and book accounting purposes. These differences result in deferred tax assets and liabilities, which are recorded on the balance sheet. These assets and liabilities are analyzed regularly and management assesses the likelihood that deferred tax assets will be realized from future taxable income. We make judgments regarding the potential tax effects of various transactions including a liability for uncertain tax positions in accordance with FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes an interpretation of FASB Statement No. 109 (“FIN 48”).

Revenue recognition – is upon delivery of product to our customer and when collectibility is reasonably assured. Delivery of product to our customer is evidenced through the shipping terms indicating when title and risk of loss is transferred. Our ordering process creates persuasive evidence of the sale arrangement and the sales amount is determined. The delivery of the goods to our customer completes the earnings process. Net sales consist of product sales and related delivery charge revenue, net of adjustments for returns and allowances. Shipping and handling costs are included in cost of goods sold.

Recently Issued Accounting Pronouncements

See Item 8. Note 1 to the Company’s Consolidated Financial Statements.

Results of Operations

The following table has been prepared as an aid in understanding the Company’s results of operations on a comparative basis for the fiscal years ended June 30, 2008, 20072011, 2010 and 2006.2009. Amounts presented are percentages of the Company’s net sales.

|

|

|

|

|

|

|

|

|

|

|

|

| FOR THE YEARS ENDED JUNE 30, |

| |||||||

|

| 2011 |

| 2010 |

| 2009 |

| |||

Net sales |

|

| 100.0 | % |

| 100.0 | % |

| 100.0 | % |

Cost of goods sold |

|

| (77.2 | ) |

| (77.2 | ) |

| (81.2 | ) |

Gross margin |

|

| 22.8 |

|

| 22.8 |

|

| 18.8 |

|

Selling, general and administrative |

|

| (17.8 | ) |

| (17.5 | ) |

| (18.8 | ) |

Facility consolidation and other charges |

|

| (0.3 | ) |

| — |

|

| (0.8 | ) |

Operating income (loss) |

|

| 4.7 |

|

| 5.3 |

|

| (0.8 | ) |

Other income, net |

|

| 0.1 |

|

| 0.0 |

|

| 0.0 |

|

Income (loss) before income taxes |

|

| 4.8 |

|

| 5.3 |

|

| (0.8 | ) |

Income tax (provision) benefit |

|

| (1.7 | ) |

| (2.0 | ) |

| 0.3 |

|

Net income (loss) |

|

| 3.1 | % |

| 3.3 | % |

| (0.5 | )% |

|

| FOR THE YEARS ENDED JUNE 30, |

| ||||

|

| 2008 |

| 2007 |

| 2006 |

|

Net sales |

| 100.0 | % | 100.0 | % | 100.0 | % |

Cost of goods sold |

| (80.7 | ) | (80.9 | ) | (80.9 | ) |

Gross margin |

| 19.3 |

| 19.1 |

| 19.1 |

|

Selling, general and administrative |

| (17.5 | ) | (16.7 | ) | (17.1 | ) |

Gain on sale of land and building |

| — |

| 1.0 |

| — |

|

Operating income |

| 1.8 |

| 3.4 |

| 2.0 |

|

Other expense, net |

| (0.2 | ) | 0.0 |

| (0.2 | ) |

Income before income taxes |

| 1.6 |

| 3.4 |

| 1.8 |

|

Provision for income taxes |

| (0.6 | ) | (1.2 | ) | (0.7 | ) |

Net income |

| 1.0 | % | 2.2 | % | 1.1 | % |

Fiscal 20082011 Compared to Fiscal 20072010

Net sales for the fiscal year ended June 30, 20082011 were $405.7$339.4 million compared to $425.4$326.5 million in the prior fiscal year, a decreasean increase of 4.6%4%. ResidentialFor the fiscal year June 30, 2011, residential net sales were $258.1 million compared to $259.7$246.0 million infor the fiscal year ended June 30, 2007, a decrease2010, an increase of 0.6%4.9%. Commercial net sales were $91.5$81.3 million for the fiscal year ended June 30, 2008, a decrease2011, an increase of 8.1%1.1% from net sales of $80.5 million for the fiscal year ended June 30, 2007. Recreational vehicle net sales were $56.1 million2010.

Gross margin for the fiscalyears ended June 30, 2011 and 2010 was 22.8%. The gross margin for the year ended June 30, 2008, a decrease of 15.2% from2011, includes the fiscal year ended June 30, 2007. The fiscal year decline in all net sales categories is due to a generally soft market environment.

Net income for the fiscal year ended June 30, 2008 was $4.2 million or $0.64 per share compared to $9.3 million or $1.42 per share in the fiscal year ended June 30, 2007. Results for the fiscal year ended June 30, 2007 were favorably impacted by three significant non-recurring events. The Company sold a commercial property, which resulted in a pre-tax gain of approximately $4.0 million, or $0.37 per share after tax. The Company recognized a pre-tax gain on the sale of vacant land of approximately $0.4 million or $0.04 per share after tax. These gains are reported as “Gain on sale of capital assets” in the Consolidated Statements of Income. The Company also realized a non-taxable gain on life insurance of $0.6 million or $0.08 per share. This gain is included in “Interest and other income” in the Consolidated Statements of Income.inventory write-down related to facility closing offset by operational improvements.

Gross margin forFor the fiscal years ended June 30, 20082011 and 2007 was 19.3% and 19.1%, respectively.

Selling,2010, selling, general and administrative expenses were 17.5 %17.8% and 16.7%17.5% of net sales, for the fiscal years ended June 30, 2008 and 2007, respectively. The percentage increase for the year ended June 30, 2011 reflects higher legal and professional fees.

Operating income decreased by $1.7 million in selling, general and administrative costs comparedfiscal year 2011 in comparison to the prior year. During fiscal year 2011, the Company recorded pre-tax charges of $1.6 million related to closing a manufacturing facility. Of these pre-tax charges, employee separation and other closing costs of $1.0 million are reported as facility closing costs and an inventory write-down of $0.6 million is due primarily to higher marketing and sales support expenses and higher bad debt expensereported as cost of $1.1 million on reduced revenues on a year over year basis.goods sold.

The effective income tax rate for the fiscal year ended June 30, 20082011 was 35.8%, reflecting lower net income35.7% compared to the prior year.38.1% for fiscal year 2010. The change in effective income tax rate was 35.6% for the fiscal year ended June 30, 2007. The 2007 rate was reduced by approximately 1.4%is primarily due to the non-taxable life insurance gain.change in provision for uncertain tax positions related to various state taxing jurisdictions, stock-based compensation and the benefit of the Domestic Manufacturing Deduction under Internal Revenue Code Section 199 (DMD), which provides a tax benefit on U.S. based manufacturing. The DMD tax benefit available in previous years was being phased in by statute and was therefore lower than the full DMD tax benefit for 2011.

The above factors resulted in net income for the fiscal year ended June 30, 20082011 of $4.2$10.4 million or $0.64$1.50 per share compared to $9.3$10.8 million or $1.42$1.61 per share for thein fiscal year ended June 30, 2007.2010.

All earnings per share amounts are on a diluted basis.

Fiscal 20072010 Compared to Fiscal 20062009

Net sales for the fiscal year ended June 30, 20072010 were $425.4$326.5 million compared to $426.4$324.2 million in the prior fiscal year.year, an increase of 1%. Residential net sales were $259.7$246.0 million a decreasecompared to $230.7 million in fiscal 2009, an increase of 3% from the fiscal year ended June 30, 2006.7%. Commercial net sales were $99.5$80.5 million for the fiscal year ended June 30, 2007, an increase of 15% from the fiscal year ended June 30, 2006. This increase in commercial net sales for the fiscal year ended June 30, 2007 is primarily due to expanded commercial office product offerings and improved industry performance of hospitality products. Recreational vehicle net sales were $66.2 million for the fiscal year ended June 30, 2007,2010, a decrease of 8%14% from thenet sales of $93.5 million for fiscal 2009.

The Company’s operating income improved by $19.8 million in fiscal year ended June 30, 2006.2010 in comparison to the prior year. The Company benefited from strategies implemented and actions taken during fiscal year decline2009 including consolidation of manufacturing operations and workforce reductions that brought production capacity and fixed overhead more in recreational vehicle net sales isline with current product demand. During the prior fiscal year, the Company recorded pre-tax charges of approximately $2.6 million related to facility consolidation and employee separation costs. Company-wide employment was reduced approximately 30% through plant closures and workforce reductions and remains at these reduced levels. These factors contributed significantly to gross margin improvements and selling, general and administrative expense reductions.

Gross margin for fiscal year 2010 was 22.8% compared to 18.8% for the prior year period. The gross margin improvements for the year were greatly impacted by the operational changes discussed above. In addition, gross margin improved due to a generally soft wholesale market environment for recreational vehicles.stability in material and product costs and lower ocean freight costs.

Net income for the fiscal year ended June 30, 2007 was $9.3 million or $1.42 per share. Results for the fiscal year ended June 30, 2007 were favorably impacted by three significant non-recurring events. The Company sold a commercial property, which resulted in a pre-tax gain of approximately $4.0 million, or $0.37 per share after tax. The Company recognized a pre-tax gain on the sale of vacant land of approximately $0.4 million or $0.04 per share after tax. These gains are reported as “Gain on sale of capital assets” in the Consolidated Statements of Income. The Company also realized a non-taxable gain on life insurance of $0.6 million, or $0.08 per share. This gain is included in “Interest and other income” in the Consolidated Statements of Income.

Gross margin forFor the fiscal years ended June 30, 20072010 and 2006 was 19.1%.

Selling,2009, selling, general and administrative expenses were 16.7%17.5% and 17.1%18.8% of net sales, for the fiscal year ended June 30, 2007 and 2006, respectively. The decrease in selling, general and administrative costs of approximately $1.9 million comparedThese percentage improvements are due to the prior fiscal year is due primarily to lower marketing and sales support expenses andoperational changes discussed above, as well as, lower bad debt expense of $0.8 million.and advertising costs.

Interest expense decreased $0.6 million to $0.4 million for fiscal year 2010 due to lower borrowings.

The effective income tax rate for the fiscal year ended June 30, 20072010 was 35.6%38.1%. The rate was reduced by approximately 1.4% due to the non-taxable life insurance gain. The effective income tax benefit rate was 39.3%41.5% for the fiscal year ended June 30, 2006.2009 due to losses or low level of earnings in various tax jurisdictions.

The above factors resulted in net income for the fiscal year ended June 30, 20072010 of $9.3$10.8 million or $1.42$1.61 per share compared to $4.7a net loss of $1.5 million or $0.72$0.23 per share for thein fiscal year ended June 30, 2006.2009.

All earnings per share amounts are on a diluted basis.

Liquidity and Capital Resources

Working capital (current assets less current liabilities) at June 30, 2011 was $100.7 million as compared to $90.8 million at June 30, 2010. Significant changes in working capital from June 30, 2010 to June 30, 2011 included increased cash of $9.6 million and decreased accruals of $2.4 million offset by decreased accounts receivable of $4.3 million. The decrease in receivables is due to timing of collections and lower shipment volume in the fourth fiscal quarter.

Net cash provided by operating activities was $8.7$13.8 million for the fiscal year ended June 30, 2011 reflecting net income of $10.4 million, changes in operating assets and liabilities of $1.3 million and non-cash charges of $4.7 million. The change in net cash provided by operating activities of $19.1 million in fiscal year 2008 compared to $10.32010 was comprised primarily of net income of $10.8 million, changes in fiscal year 2007. Significant working capital changes fromoperating assets and liabilities of $4.4 million and non-cash charges of $3.9 million. Depreciation expense was $2.7 million and $3.0 million for the years ended June 30, 2007 to June 30, 2008 included: decreased accounts receivables of $12.5 million, increased inventory levels of $7.0 million2011 and decreased accounts payable of $1.3 million. The decrease in receivables is related to timing of shipments and related payment terms, collection efforts and lower net sales. The increase in inventory is due primarily to timing of inventory purchases to meet our forecasted customer demands especially sourced products where there are longer lead times for international shipments. The decrease in accounts payable is due to the timing of payments. The Company expects that due to the nature of our operations that there will continue to be significant fluctuations in inventory levels, the related accounts payable, and cash flows from operations due to the following: we purchase a significant amount of inventory in large orders from overseas suppliers with significant lead times and depending on the timing of those large orders inventory levels can be significantly impacted, we have various large customers that purchase significant quantities of inventory at a time and the timing of those purchases can significantly impact inventory levels, accounts receivable, accounts payable and short-term borrowings. As discussed below the Company believes it has adequate financing arrangements and access to capital to absorb these fluctuations in operating cash flow. 2010, respectively.

Net cash used in investing activities was $1.0$2.7 million in fiscal year 20082011 compared to $5.1cash used by investing activities of $1.6 million in fiscal year 2007. The significant change in investing activities is related to the large amount2010. Net purchases of capital expenditures made in 2007 somewhat offset by a sale of land and commercial property.investments were $0.3 million. Capital expenditures were $1.2$2.6 million $10.8during fiscal year 2011.

Net cash used in financing activities was $1.5 million in fiscal year 2011, primarily for the payment of dividends of $1.8 million, compared to $11.0 million in fiscal year 2010. For fiscal year 2010, the cash was used primarily to reduce borrowings by $10.0 million and $3.4 million (of which $2.6 million was a non-cash purchasepay dividends of equipment by assumption of a note payable) in fiscal years 2008, 2007 and 2006, respectively. Fiscal 2008 expenditures were primarily for manufacturing equipment. Depreciation and amortization expense was $4.4 million and $5.3 million for the fiscal years ended June 30, 2008 and 2007, respectively.$1.3 million.

The Company expects that capital expenditures will be approximately $3.0$15.0 million in fiscal year 2009.2012. The significant fiscal year 2007 capital expenditure cash outflows were offset byCompany plans to invest approximately $12 million to construct, furnish and equip a significant sale of commercial property resultingcorporate office building in total cash proceeds of $5.5 millionDubuque, Iowa, and a sale of vacant land of approximately $0.4 million. The commercial property was previously leased to a non-related third party and used as retail space. Neither the salebalance of the commercial property or vacant land is expected to significantly impact future operations.

Net cash used in financing activities was $5.8 million in fiscal year 2008 compared to $6.3 million in fiscal year 2007. For fiscal years 2008expenditures on delivery and 2007, repayment of debt and the payment of dividends were the primary financing activities utilizing cash. For fiscal year 2006, borrowings were used to pay for the expansion of inventory programs and accounts receivable and the payment of dividends. Cash dividends were $3.4 million in 2008 and in 2007.

manufacturing equipment. Management believes that the Company has adequate cash cash equivalents, and credit arrangements to meet its operating and capital requirements for fiscal year 2009.2012, including the construction of a corporate office. In the opinion of management, the Company’s liquidity and credit resources provide it with the ability to react to opportunities as they arise, the ability to pay quarterly dividends to its shareholders, and ensures thatto purchase productive capital assets that enhance safety and improve operationsoperations.

At June 30, 2011, the Company has no long-term debt obligations and therefore, no contractual interest payments are purchased as needed.

included in the table below. The following table summarizes the Company’s contractual obligations at June 30, 20082011 and the effect these obligations are expected to have on the Company’s liquidity and cash flow in the future (in thousands):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total |

| Less than |

| 1 - 3 |

| 3 - 5 |

| More than |

| |||||

Operating lease obligations |

| $ | 4,082 |

| $ | 1,851 |

| $ | 2,231 |

| $ | — |

| $ | — |

|

|

| Total |

| Less than |

| 1 – 3 |

| 3 – 5 |

| More than |

| |||||

Long-term debt obligations |

| $ | 25,954 |

| $ | 5,143 |

| $ | 811 |

| $ | 20,000 |

| $ | — |

|

Interest on long-term debt obligations |

|

| 3,252 |

|

| 1,030 |

|

| 2,060 |

|

| 162 |

|

| — |

|

Operating lease obligations |

|

| 6,244 |

|

| 2,601 |

|

| 3,359 |

|

| 284 |

|

| — |

|

Total contractual cash obligations |

| $ | 35,450 |

| $ | 8,774 |

| $ | 6,230 |

| $ | 20,446 |

| $ | — |

|

Contractual obligations associated with the Company’s deferred compensation plans were excluded from the table above as the Company cannot predict when the events that trigger payment will occur. Total accumulated deferred compensation liabilities were $5.3 million at June 30, 2008.2011. At June 30, 20082011 the Company had no capital lease obligations, and no purchase obligations for raw materials or finished goods. The purchase price on all open purchase orders was fixed and denominated in U.S. dollars. Additionally, the Company has excluded the FIN 48tax contingency reserve from the above table, as the timing of payments, if any, payments cannot be reasonably estimated.

Financing Arrangements

See Note 76 to the Consolidated Financial Statements on page 28 of this Annual Report on Form 10-K.

Outlook

The fiscalWe had modest gains in sales for the current year ended June 30, 2008 began well with the first two quarters showing improved earnings over fiscal year 2007 on only slightly lower net sales. Beginning in the third fiscal quarter net sales dropped more rapidly, and although net earnings were only about 55% of the prior year quarterly amount, our net income forpartially due to a strong backlog entering the nine-months was still ahead of the prior year nine-month total. The fourth quarter 12% decrease in net sales hampered the ability to absorb fixed costs and that, combined with additional bad debt and selling expenses, contributed negatively toyear. We enter fiscal year 2008 results. Normally, at least one2012 with lower backlogs and anticipate that first quarter fiscal year 2012 sales will be lower than first quarter fiscal year 2011. Macroeconomic conditions, such as, high unemployment, minimal job growth, a weak housing market and low levels of the markets in which we sell products is doing well. However, residential net sales were off 1%, commercial net sales were down 8%, and recreational vehicle seating net sales were down 15%. We do not believe that we are losing market share in these categories.

The U.S. economy, where most of our products are sold, has been greatly impacted by the credit crisis in the home mortgage sector, a fall in the value of the U.S. dollar versus most other major currencies, volatile high-cost fuel, increasing food prices and a changing political landscape. These factors have contributed to the lowest consumer confidence levels since 1981.

We have been negatively impacted by price increases incontinue to adversely impact our business. The macroeconomic environment tempers expectations of top line growth through the raw materials and component parts, such as steel, poly foam and fabrics, as well as increases in the cost to transport those materials to our manufacturing facilities and products to our customers. Our overseas manufacturers have also increased prices and the cost to transport those products to the U.S. has increased with the pricefirst part of fuel. We see no near term improvement in macro-economic operating conditions.

Thisfiscal year Flexsteel Industries, Inc. will complete it’s 115th year doing business in the furniture industry.2012. The commercial office industry is reporting improving order trends. While we have seen challenging business conditions before, they are never comfortable or reassuringbenefited minimally from those improvements to date, we believe we will see increased sales volume during fiscal year 2012. We anticipate increased orders for hospitality products during fiscal year 2012 resulting from pent up demand caused by delays in typical refurbishing cycles for hotel properties.

We remain committed to our shareholders. In response to these challenges, we have:

implemented price increases to offset cost increases where possible,

commenced the closing of two manufacturing operations, Lancaster, PA and New Paris, IN, to more closely match our manufacturing capacity with our expected demand for residential and recreational vehicle seating products and we anticipate annual pre-tax savings in the range of $3.5 million to $4.0 million from this manufacturing consolidation,

focused attention on our credit risk exposure,

maintained a close relationship with our customers to offer products and services they need to operate effectively and profitability, and

continued to focus on profitability and cash flow over top line growth to maintain a strong balance sheet.

While we expect that current business conditions will persist for most, if not all, of fiscal year 2009, we remain optimistic that our strategy ofcore strategies, which include a wide range of quality product offerings and price points to the residential recreational vehicle and commercial markets, combined with oura conservative approach to businessbusiness. We will be rewarded overmaintain our focus on a strong balance sheet through emphasis on cash flow and improving profitability. We believe these core strategies are in the longer-term.best interest of our shareholders.

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk |

General– Market risk represents the risk of changes in the value of a financial instrument, derivative or non-derivative, caused by fluctuations in interest rates, foreign exchange rates and equity prices. As discussed below, management of the Company does not believe that changes in these factors could cause material fluctuations in the Company’s results of operations or cash flows. The ability to import furniture products can be adversely affected by political issues in the countries where suppliers are located, disruptions associated with shipping distances and negotiations with port employees. Other risks related to furniture product importation include government imposition of regulations and/or quotas; duties and taxes on imports; and significant fluctuation in the value of the U.S. dollar against foreign currencies. Any of these factors could interrupt supply, increase costs and decrease earnings.

Impairment of long-lived assets – InflationAccounting rules require that long-lived assets be evaluated for impairment whenever events or changes in circumstances indicate that its carrying value may not be recoverable. We have substantial long-lived assets, consisting mainly of property, plant and equipment, which based upon such events or changes in circumstances, there could be a write-down of all or a portion of these assets and a corresponding reduction in our earnings and net worth. At June 30, 2008, no impairment of long-lived assets has been identified.

Foreign Currency Risk – During fiscal years 2008, 2007 and 2006, the Company did not have sales, purchases, or other expenses denominated in foreign currencies. As such, the Company is not exposed to market risk associated with currency exchange rates and prices.

Interest Rate Risk – The Company’s primary market risk exposure with regard to financial instruments is changes in interest rates. At June 30, 2008, a hypothetical 100 basis point increase in short-term interest rates would decrease annual pre-tax earnings by approximately $150,000, assuming no change in the volume or composition of debt. As of June 30, 2008, the Company has effectively fixed the interest rates at 4.5% on approximately $15.0 million of its long-term debt through the use of interest rate swaps, and the above estimated earnings reduction takes these swaps into account. On July 31, 2008, a $5.0 million swap matured. As of the date of this Annual Report on Form 10-K, the Company has effectively fixed its interest rate at 5.0% on approximately $10.0 million of it long-term debt through the use of interest rate swaps. As of June 30, 2008, the fair value of these swaps is a liability of approximately $0.3 million and is included in other liabilities. As of June 30, 2007, the fair value of these swaps were an asset of approximately $0.1 million and was included in other assets.

Tariffs – The Company has exposure to actions by governments, including tariffs. Tariffs are a possibility on any imported or exported products.

Inflation – Increased operating costs are reflected in product or services pricing with any limitations on price increases determined by the marketplace. TheInflation or other pricing pressures could impact of inflation on the Company has not been significant during the past three years because of the relatively low rates of inflation experienced in the United States. Rawraw material costs, labor costs and interest rates which are important components of costs for the Company. Inflation or other pricing pressuresCompany and could impact any or all of these components, with a possiblehave an adverse effect on our profitability, especially where increases in these costs exceed price increases on finished products. In recent

Foreign Currency Risk – During fiscal years 2011, 2010 and 2009, the Company has faced strong inflationarydid not have sales, purchases, or other expenses denominated in foreign currencies. As such, the Company is not directly exposed to market risk associated with currency exchange rates and other pricing pressuresprices.

Interest Rate Risk –The Company’s primary market risk exposure with respectregard to steel, fuel and health care costs, whichfinancial instruments is changes in interest rates. At June 30, 2011, the Company does not have been partially mitigated by pricing adjustments.any debt outstanding.

Item 8. | Financial Statements and Supplementary Data |

|

|

|

Page(s) | ||

|

| |

Consolidated Balance Sheets at June 30, |

|

|

|

| |

|

| |

|

| |

|

|

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the ShareholdersBoard of Directors and Stockholders of Flexsteel Industries, Inc.

We have audited the accompanying consolidated balance sheets of Flexsteel Industries, Inc. and subsidiaries (the "Company"“Company”) as of June 30, 20082011 and 2007,2010, and the related consolidated statements of income,operations, changes in stockholders'shareholders’ equity, and cash flows for each of the three years in the period ended June 30, 2008.2011. Our audits also included the financial statement schedulesschedule listed in the Index at Item 15. These financial statements and financial statement schedule are the responsibility of the Company'sCompany’s management. Our responsibility is to express an opinion on the financial statements and financial statement schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includesstatements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such consolidated financial statements present fairly, in all material respects, the financial position of Flexsteel Industries, Inc. and subsidiaries atas of June 30, 20082011 and June 30, 2007,2010, and the results of their operations and their cash flows for each of the three years in the period ended June 30, 2008,2011, in conformity with accounting principles generally accepted in the United States of America. Also, in our opinion, such financial statement schedule, when considered in relation to the basic consolidated financial statements taken as a whole, presentpresents fairly, in all material respects, the information set forth therein.

| |

DELOITTE & TOUCHE LLP | |

Minneapolis, Minnesota | |

August 19, 2011 |

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES |

(Amounts in thousands, except share and per share data) |

|

|

|

|

|

|

|

|

|

| JUNE 30, |

| ||||

|

| 2011 |

| 2010 |

| ||

| |||||||

ASSETS |

|

|

|

|

| ||

| |||||||

CURRENT ASSETS: |

|

|

|

|

|

|

|

Cash |

| $ | 17,889 |

| $ | 8,278 |

|

Trade receivables – less allowance for doubtful accounts: 2011, $2,000; 2010, $2,020 |

|

| 31,451 |

|

| 35,748 |

|

Inventories |

|

| 73,680 |

|

| 72,637 |

|

Deferred income taxes |

|

| 3,700 |

|

| 4,050 |

|

Other |

|

| 1,633 |

|

| 1,076 |

|

Total current assets |

|

| 128,353 |

|

| 121,789 |

|

NONCURRENT ASSETS: |

|

|

|

|

|

|

|

Property, plant and equipment, net |

|

| 21,387 |

|

| 21,614 |

|

Deferred income taxes |

|

| 2,560 |

|

| 3,010 |

|

Other assets |

|

| 12,377 |

|

| 11,257 |

|

TOTAL |

| $ | 164,677 |

| $ | 157,670 |

|

|

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES: |

|

|

|

|

|

|

|

Accounts payable – trade |

| $ | 9,899 |

| $ | 10,815 |

|

Accrued liabilities: |

|

|

|

|

|

|

|

Payroll and related items |

|

| 6,922 |

|

| 7,023 |

|

Insurance |

|

| 5,645 |

|

| 6,192 |

|

Other |

|

| 5,204 |

|

| 6,959 |

|

Total current liabilities |

|

| 27,670 |

|

| 30,989 |

|

LONG-TERM LIABILITIES: |

|

|

|

|

|

|

|

Deferred compensation |

|

| 5,270 |

|

| 5,096 |

|

Other liabilities |

|

| 3,164 |

|

| 3,973 |

|

Total liabilities |

|

| 36,104 |

|

| 40,058 |

|

|

|

|

|

|

|

|

|

COMMITMENTS AND CONTINGENCIES (Note 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SHAREHOLDERS’ EQUITY: |

|

|

|

|

|

|

|

Cumulative preferred stock – $50 par value; authorized 60,000 shares; outstanding – none |

|

|

|

|

|

|

|

Undesignated (subordinated) stock – $1 par value; authorized 700,000 shares; outstanding – none |

|

|

|

|

|

|

|

Common stock – $1 par value; authorized 15,000,000 shares; outstanding 2011, 6,710,612 shares; 2010, 6,645,532 shares |

|

| 6,711 |

|

| 6,646 |

|

Additional paid-in capital |

|

| 6,698 |

|

| 5,425 |

|

Retained earnings |

|

| 115,699 |

|

| 107,293 |

|

Accumulated other comprehensive loss |

|

| (535 | ) |

| (1,752 | ) |

Total shareholders’ equity |

|

| 128,573 |

|

| 117,612 |

|

TOTAL |

| $ | 164,677 |

| $ | 157,670 |

|

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

|

| JUNE 30, |

| ||||

ASSETS |

| 2008 |

| 2007 |

| ||

|

|

|

|

|

|

|

|

CURRENT ASSETS: |

|

|

|

|

|

|

|

Cash and cash equivalents |

| $ | 2,841,323 |

| $ | 900,326 |

|

Investments |

|

| 1,160,066 |

|

| 976,180 |

|

Trade receivables – less allowance for doubtful |

|

| 43,783,224 |

|

| 56,273,874 |

|

Inventories |

|

| 85,791,400 |

|

| 78,756,985 |

|

Deferred income taxes |

|

| 4,210,000 |

|

| 4,700,000 |

|

Other |

|

| 2,853,634 |

|

| 1,759,045 |

|

Total current assets |

|

| 140,639,647 |

|

| 143,366,410 |

|

NONCURRENT ASSETS: |

|

|

|

|

|

|

|

Property, plant and equipment, net |

|

| 26,372,392 |

|

| 28,168,244 |

|

Deferred income taxes |

|

| 1,392,187 |

|

| 1,270,000 |

|

Other assets |

|

| 11,501,992 |

|

| 12,209,528 |

|

TOTAL |

| $ | 179,906,218 |

| $ | 185,014,182 |

|

|

|

|

|

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES: |

|

|

|

|

|

|

|

Accounts payable – trade |

| $ | 14,580,275 |

| $ | 15,893,964 |

|

Notes payable and current maturities on long-term debt |

|

| 5,142,945 |

|

| 7,030,059 |

|

Accrued liabilities: |

|

|

|

|

|

|

|

Payroll and related items |

|

| 6,759,941 |

|

| 7,530,083 |

|

Insurance |

|

| 7,176,799 |

|

| 7,615,532 |

|

Other |

|

| 6,059,575 |

|

| 7,394,448 |

|

Total current liabilities |

|

| 39,719,535 |

|

| 45,464,086 |

|

LONG-TERM LIABILITIES: |

|

|

|

|

|

|

|

Long-term debt |

|

| 20,810,597 |

|

| 21,336,352 |

|

Deferred compensation |

|

| 5,343,545 |

|

| 5,535,113 |

|

Other liabilities |

|

| 1,280,154 |

|

| — |

|

Total liabilities |

|

| 67,153,831 |

|

| 72,335,551 |

|

|

|

|

|

|

|

|

|

COMMITMENTS AND CONTINGENCIES (Note 14) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SHAREHOLDERS’ EQUITY: |

|

|

|

|

|

|

|

Cumulative preferred stock – $50 par value; authorized 60,000 shares; |

|

|

|

|

|

|

|

Undesignated (subordinated) stock – $1 par value; authorized |

|

|

|

|

|

|

|

Common stock – $1 par value; authorized 15,000,000 shares; |

|

| 6,575,633 |

|

| 6,570,467 |

|

Additional paid-in capital |

|

| 4,255,996 |

|

| 4,013,456 |

|

Retained earnings |

|

| 101,692,431 |

|

| 100,984,577 |

|

Accumulated other comprehensive income |

|

| 228,327 |

|

| 1,110,131 |

|

Total shareholders’ equity |

|

| 112,752,387 |

|

| 112,678,631 |

|

TOTAL |

| $ | 179,906,218 |

| $ | 185,014,182 |

|

See accompanying Notes to Consolidated Financial Statements.

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES

Consolidated Statements of Income

|

| FOR THE YEARS ENDED JUNE 30, |

| |||||||

|

| 2008 |

| 2007 |

| 2006 |

| |||

|

|

|

|

|

|

|

|

|

|

|

NET SALES |

| $ | 405,654,829 |

| $ | 425,399,951 |

| $ | 426,407,585 |

|

COST OF GOODS SOLD |

|

| (327,165,396 | ) |

| (344,176,763 | ) |

| (345,068,305 | ) |

GROSS MARGIN |

|

| 78,489,433 |

|

| 81,223,188 |

|

| 81,339,280 |

|

SELLING, GENERAL AND ADMINISTRATIVE |

|

| (70,893,485 | ) |

| (70,895,260 | ) |

| (72,778,577 | ) |

GAIN ON SALE OF CAPITAL ASSETS |

|

| — |

|

| 4,370,712 |

|

| — |

|

OPERATING INCOME |

|

| 7,595,948 |

|

| 14,698,640 |

|

| 8,560,703 |

|

OTHER INCOME (EXPENSE): |

|

|

|

|

|

|

|

|

|

|

Interest and other income |

|

| 468,933 |

|

| 1,276,857 |

|

| 774,783 |

|

Interest expense |

|

| (1,468,476 | ) |

| (1,491,510 | ) |

| (1,557,303 | ) |

Total |

|

| (999,543 | ) |

| (214,653 | ) |

| (782,520 | ) |

INCOME BEFORE INCOME TAXES |

|

| 6,596,405 |

|

| 14,483,987 |

|

| 7,778,183 |

|

PROVISION FOR INCOME TAXES |

|

| (2,360,000 | ) |

| (5,150,000 | ) |

| (3,060,000 | ) |

NET INCOME |

| $ | 4,236,405 |

| $ | 9,333,987 |

| $ | 4,718,183 |

|

|

|

|

|

|

|

|

|

|

|

|

WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING: |

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 6,573,999 |

|

| 6,567,522 |

|

| 6,558,440 |

|

Diluted |

|

| 6,611,136 |

|

| 6,582,558 |

|

| 6,577,278 |

|

|

|

|

|

|

|

|

|

|

|

|

EARNINGS PER SHARE OF COMMON STOCK: |

|

|

|

|

|

|

|

|

|

|

Basic |

| $ | 0.64 |

| $ | 1.42 |

| $ | 0.72 |

|

Diluted |

| $ | 0.64 |

| $ | 1.42 |

| $ | 0.72 |

|

|

|

|

|

|

|

|

|

|

|

|

CASH DIVIDENDS DECLARED PER COMMON SHARE |

| $ | 0.52 |

| $ | 0.52 |

| $ | 0.52 |

|

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES |

(Amounts in thousands, except per share data) |

|

|

|

|

|

|

|

|

|

|

|

|

| FOR THE YEARS ENDED JUNE 30, |

| |||||||

|

| 2011 |

| 2010 |

| 2009 |

| |||

|

|

|

|

|

|

|

|

|

|

|

NET SALES |

| $ | 339,426 |

| $ | 326,466 |

| $ | 324,158 |

|

COST OF GOODS SOLD |

|

| (262,124 | ) |

| (251,685 | ) |

| (263,083 | ) |

GROSS MARGIN |

|

| 77,302 |

|

| 74,781 |

|

| 61,075 |

|

SELLING, GENERAL AND ADMINISTRATIVE |

|

| (60,422 | ) |

| (57,252 | ) |

| (60,792 | ) |

FACILITY CLOSING COSTS |

|

| (1,016 | ) |

| — |

|

| (2,555 | ) |

OPERATING INCOME (LOSS) |

|

| 15,864 |

|

| 17,529 |

|

| (2,272 | ) |

OTHER INCOME (EXPENSE): |

|

|

|

|

|

|

|

|

|

|

Interest and other income |

|

| 343 |

|

| 361 |

|

| 661 |

|

Interest expense |

|

| — |

|

| (439 | ) |

| (968 | ) |

Total |

|

| 343 |

|

| (78 | ) |

| (307 | ) |

INCOME (LOSS) BEFORE INCOME TAXES |

|

| 16,207 |

|

| 17,451 |

|

| (2,579 | ) |

INCOME TAX (PROVISION) BENEFIT |

|

| (5,790 | ) |

| (6,650 | ) |

| 1,070 |

|

NET INCOME (LOSS) |

| $ | 10,417 |

| $ | 10,801 |

| $ | (1,509 | ) |

|

|

|

|

|

|

|

|

|

|

|

WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING: |

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 6,693 |

|

| 6,608 |

|

| 6,576 |

|

Diluted |

|

| 6,929 |

|

| 6,697 |

|

| 6,576 |

|

|

|

|

|

|

|

|

|

|

|

|

EARNINGS (LOSS) PER SHARE OF COMMON STOCK: |

|

|

|

|

|

|

|

|

|

|

Basic |

| $ | 1.56 |

| $ | 1.63 |

| $ | (0.23 | ) |

Diluted |

| $ | 1.50 |

| $ | 1.61 |

| $ | (0.23 | ) |

|

|

|

|

|

|

|

|

|

|

|

CASH DIVIDENDS DECLARED PER COMMON SHARE |

| $ | 0.30 |

| $ | 0.20 |

| $ | 0.36 |

|

See accompanying Notes to Consolidated Financial Statements.

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES |

(Amounts in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Par |

| Additional |

| Retained |

| Accumulated |

| Total |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at July 1, 2008 |

| $ | 6,576 |

| $ | 4,256 |

| $ | 101,692 |

| $ | 228 |

| $ | 112,752 |

|

Unrealized loss on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| (1,022 | ) |

| (1,022 | ) |

Stock-based compensation |

|

| — |

|

| 114 |

|

| — |

|

| — |

|

| 114 |

|

Interest rate swaps valuation adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| (1 | ) |

| (1 | ) |

Minimum pension liability adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| (969 | ) |

| (969 | ) |

Cash dividends declared |

|

| — |

|

| — |

|

| (2,367 | ) |

| — |

|

| (2,367 | ) |

Net loss |

|

| — |

|

| — |

|

| (1,509 | ) |

| — |

|

| (1,509 | ) |

Balance at June 30, 2009 |

|

| 6,576 |

|

| 4,370 |

|

| 97,816 |

|

| (1,764 | ) |

| 106,998 |

|

Issuance of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock options exercised, net |

|

| 70 |

|

| 274 |

|

| — |

|

| — |

|

| 344 |

|

Unrealized gain on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| 39 |

|

| 39 |

|

Long-term incentive compensation |

|

| — |

|

| 510 |

|

| — |

|

| — |

|

| 510 |

|

Stock-based compensation |

|

| — |

|

| 271 |

|

| — |

|

| — |

|

| 271 |

|

Interest rate swaps valuation adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| 177 |

|

| 177 |

|

Minimum pension liability adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| (204 | ) |

| (204 | ) |

Cash dividends declared |

|

| — |

|

| — |

|

| (1,324 | ) |

| — |

|

| (1,324 | ) |

Net income |

|

| — |

|

| — |

|

| 10,801 |

|

| — |

|

| 10,801 |

|

Balance at June 30, 2010 |

|

| 6,646 |

|

| 5,425 |

|

| 107,293 |

|

| (1,752 | ) |

| 117,612 |

|

Issuance of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock options exercised, net |

|

| 65 |

|

| 259 |

|

| — |

|

| — |

|

| 324 |

|

Unrealized gain on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| 348 |

|

| 348 |

|

Long-term incentive compensation |

|

| — |

|

| 590 |

|

| — |

|

| — |

|

| 590 |

|

Stock-based compensation |

|

| — |

|

| 424 |

|

| — |

|

| — |

|

| 424 |

|

Minimum pension liability adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| 869 |

|

| 869 |

|

Cash dividends declared |

|

| — |

|

| — |

|

| (2,011 | ) |

| — |

|

| (2,011 | ) |

Net income |

|

| — |

|

| — |

|

| 10,417 |

|

| — |

|

| 10,417 |

|

Balance at June 30, 2011 |

| $ | 6,711 |

| $ | 6,698 |

| $ | 115,699 |

| $ | (535 | ) | $ | 128,573 |

|

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES

Consolidated Statements of Changes in Shareholders’ Equity

|

| Total Par |

| Additional |

| Retained |

| Accumulated |

| Total |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at June 30, 2005 (as previously reported) |

| $ | 6,541,436 |

| $ | 2,954,398 |

| $ | 95,196,022 |

| $ | 105,864 |

| $ | 104,797,720 |

|

Restatement adjustment (see Note 19) |

|

| — |

|

| — |

|

| (1,436,479 | ) |

| — |

|

| (1,436,479 | ) |

Balance at July 1, 2005 (as restated) |

|

| 6,541,436 |

|

| 2,954,398 |

|

| 93,759,543 |

|

| 105,864 |

|

| 103,361,241 |

|

Issuance of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock options exercised, net |

|

| 2,000 |

|

| 20,500 |

|

| — |

|

| — |

|

| 22,500 |

|

401(k) plan and management incentive shares |

|

| 20,314 |

|

| 268,254 |

|

| — |

|

| — |

|

| 288,568 |

|

Unrealized loss on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| (221 | ) |

| (221 | ) |

Stock-based compensation |

|

| — |

|

| 427,000 |

|

| — |

|

| — |

|

| 427,000 |

|

Interest rate swaps valuation adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| 116,910 |

|

| 116,910 |

|

Minimum pension liability adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| 543,559 |

|

| 543,559 |

|

Cash dividends declared |

|

| — |

|

| — |

|

| (3,411,894 | ) |

| — |

|

| (3,411,894 | ) |

Net income |

|

| — |

|

| — |

|

| 4,718,183 |

|

| — |

|

| 4,718,183 |

|

Balance at June 30, 2006 (as restated) |

|

| 6,563,750 |

|

| 3,670,152 |

|

| 95,065,832 |

|

| 766,112 |

|

| 106,065,846 |

|

Issuance of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock options exercised, net |

|

| 1,566 |

|

| 10,891 |

|

| — |

|

| — |

|

| 12,457 |

|

401(k) plan |

|

| 5,151 |

|

| 58,413 |

|

| — |

|

| — |

|

| 63,564 |

|

Unrealized gain on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| 301,611 |

|

| 301,611 |

|

Stock-based compensation |

|

| — |

|

| 274,000 |

|

| — |

|

| — |

|

| 274,000 |

|

Interest rate swaps valuation adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| (168,137 | ) |

| (168,137 | ) |

SFAS No. 87 minimum pension liability |

|

| — |

|

| — |

|

| — |

|

| 254,638 |

|

| 254,638 |

|

SFAS No. 158 transition adjustment |

|

| — |

|

| — |

|

| — |

|

| (44,093 | ) |

| (44,093 | ) |

Cash dividends declared |

|

| — |

|

| — |

|

| (3,415,242 | ) |

| — |

|

| (3,415,242 | ) |

Net income |

|

| — |

|

| — |

|

| 9,333,987 |

|

| — |

|

| 9,333,987 |

|

Balance at June 30, 2007 (as restated) |

|

| 6,570,467 |

|

| 4,013,456 |

|

| 100,984,577 |

|

| 1,110,131 |

|

| 112,678,631 |

|

Adoption of FIN 48 |

|

|

|

|

|

|

|

| (110,000 | ) |

|

|

|

| (110,000 | ) |

Issuance of common stock: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stock options exercised, net |

|

| 1,642 |

|

| 13,314 |

|

| — |

|

| — |

|

| 14,956 |

|

401(k) plan shares |

|

| 3,524 |

|

| 43,226 |

|

| — |

|

| — |

|

| 46,750 |

|

Unrealized loss on available for sale investments, net of tax |

|

| — |

|

| — |

|

| — |

|

| (84,342 | ) |

| (84,342 | ) |

Stock-based compensation |

|

| — |

|

| 186,000 |

|

| — |

|

| — |

|

| 186,000 |

|

Interest rate swaps valuation adjustment, net of tax |

|

| — |

|

| — |

|

| — |

|

| (273,062 | ) |

| (273,062 | ) |

Minimum pension liability, net of tax |

|

| — |

|

| — |

|

| — |

|

| (524,400 | ) |

| (524,400 | ) |

Cash dividends declared |

|

| — |

|

| — |

|

| (3,418,551 | ) |

| — |

|

| (3,418,551 | ) |

Net income |

|

| — |

|

| — |

|

| 4,236,405 |

|

| — |

|

| 4,236,405 |

|

Balance at June 30, 2008 |

| $ | 6,575,633 |

| $ | 4,255,996 |

| $ | 101,692,431 |

| $ | 228,327 |

| $ | 112,752,387 |

|

See accompanying Notes to Consolidated Financial Statements.

FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES |

(Amounts in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

| FOR THE YEARS ENDED JUNE 30, |

| |||||||

|

| 2011 |

| 2010 |

| 2009 |

| |||

|

|

|

|

|

|

|

|

|

|

|

OPERATING ACTIVITIES: |

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

| $ | 10,417 |

| $ | 10,801 |

| $ | (1,509 | ) |

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: |

|

|

|

|

|

|

|

|

|

|

Depreciation |

|

| 2,690 |

|

| 2,986 |

|

| 3,733 |

|

Deferred income taxes |

|

| 54 |

|

| (963 | ) |

| 449 |

|

Stock-based compensation expense |

|

| 1,014 |

|

| 781 |

|

| 114 |

|

Provision for losses on accounts receivable |

|

| 870 |

|

| 920 |

|

| 1,240 |

|

Other non-cash, net |

|

| 224 |

|

| 218 |

|

| 14 |

|

Gain on disposition of capital assets |

|

| (185 | ) |

| (9 | ) |

| (252 | ) |

Gain on sale of investments |

|

| — |

|

| — |

|

| (462 | ) |

Impairment of long-lived assets |

|

| — |

|

| — |

|

| 138 |

|

Changes in operating assets and liabilities: |

|

|

|

|

|

|

|

|

|

|

Trade receivables |

|

| 3,427 |

|

| (5,386 | ) |

| 11,261 |

|

Inventories |

|