Securities registered pursuant to Section 12(g) of the Act:

None

None

(Title of Class)

|

Yeso Nox

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yeso Nox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx Noo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesox Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

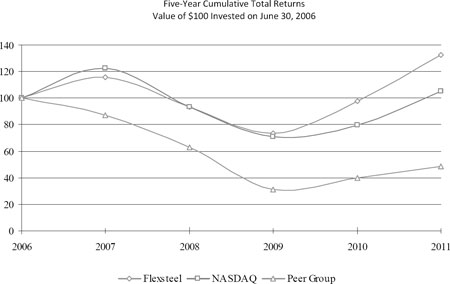

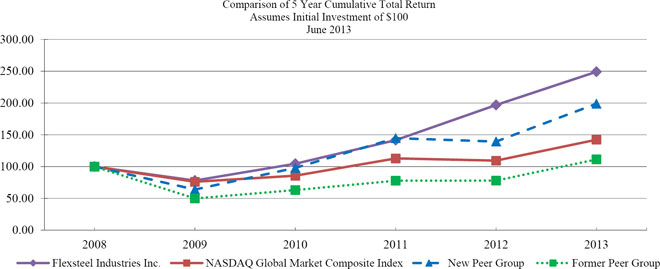

Large accelerated filero Accelerated filerx Non-accelerated filero Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yeso Nox The aggregate market value of the voting stock held by non-affiliates, computed by reference to the last sales price on December 31, Indicate the number of shares outstanding of each of the registrant’s classes of Common Stock, as of the latest practicable date. DOCUMENTS INCORPORATED BY REFERENCE 1 PART I Cautionary Statement Relevant to Forward-Looking Information for the Purpose of “Safe Harbor” Provisions of the Private Securities Litigation Reform Act of 1995 The Company and its representatives may from time to time make written or oral forward-looking statements with respect to long-term goals or anticipated results of the Company, including statements contained in the Company’s filings with the Securities and Exchange Commission and in its reports to stockholders. Statements, including those in this Annual Report on Form 10-K, which are not historical or current facts, are “forward-looking statements” made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. There are certain important factors that could cause our results to differ materially from those anticipated by some of the statements made herein. Investors are cautioned that all forward-looking statements involve risk and uncertainty. Some of the factors that could affect results are the cyclical nature of the furniture industry, supply chain disruptions, litigation, including expenses relating to the Indiana civil litigation, the effectiveness of new product introductions and distribution channels, the product mix of sales, pricing pressures, the cost of raw materials and fuel, retention and recruitment of key employees, actions by governments including laws, regulations, taxes and tariffs, inflation, the amount of sales generated and the profit margins thereon, competition (both U.S. and foreign), credit exposure with customers, participation in multi-employer pension plans and general economic conditions. For further information regarding these risks and uncertainties, see the “Risk Factors” section in Item 1A of this Annual Report on Form 10-K. The Company specifically declines to undertake any obligation to publicly revise any forward-looking statements that have been made to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events. Item 1. Business General The Company has one active wholly-owned subsidiary: DMI Furniture, Inc. (“DMI”), which is a Louisville, Kentucky-based, importer and marketer of residential and commercial office The Company operates in one reportable FOR THE YEARS ENDED JUNE 30, (in thousands) FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 2013 2012 2011 Residential $ 258,095 $ 246,041 $ 230,727 $ 311,214 $ 275,442 $ 258,095 Commercial 81,331 80,425 93,431 74,975 76,647 81,331 $ 339,426 $ 326,466 $ 324,158 $ 386,189 $ 352,089 $ 339,426 Manufacturing and Offshore Sourcing We operate manufacturing facilities that are located in Arkansas, California, Georgia, Iowa, Mississippi and Juarez, Mexico. These manufacturing operations are integral to our product offerings and distribution strategy by offering smaller and more frequent product runs of a wider product selection. We identify and eliminate manufacturing inefficiencies and adjust manufacturing schedules on a daily basis to meet customer requirements. We have established relationships with key suppliers to ensure prompt delivery of quality component parts. Our production includes the use of selected offshore component parts to enhance our value in the marketplace. We integrate our manufactured products with finished products acquired from offshore suppliers who can meet our quality specification and scheduling requirements. We will continue to pursue and refine this blended strategy, offering customers manufactured goods, products manufactured utilizing imported component parts, and ready-to-deliver imported products. The Company believes that it best serves customers by offering products from each of these categories to assist customers in reaching specific consumers with varied price points, styles and product categories. This blended focus on products allows the Company to provide a wide range of options to satisfy customer requirements. Competition Seasonality Foreign Operations Customer Backlog June 30, 2011 June 30, 2010 June 30, 2009 $35,700 $49,000 $35,200 June 30, 2013 June 30, 2012 June 30, 2011 $43,300 $38,700 $35,700 Raw Materials Working Capital Practices Industry Factors Government Regulations Environmental Matters Trademarks and Patents It is not common in the furniture industry to obtain a patent for a furniture design. If a particular design of a furniture manufacturer is well accepted in the marketplace, it is common for other manufacturers to imitate the same design without recourse by the furniture manufacturer who initially introduced the design. Furniture products are designed by the Company’s own design staff and through the services of Fiscal Year Ended June 30, Expenditures Expenditures 2013 $2,520 2012 $2,310 2011 $2,190 $2,190 2010 $2,040 2009 $2,680 Employees Website and Available Information A copy of the Company’s Annual Report on Form 10-K, as filed with the Securities and Exchange Commission (“SEC”), other SEC reports filed or furnished and ourGuidelines for Business Conduct are available, without charge, on the Company’s website atwww.flexsteel.com or by writing to the Office of the Secretary, Flexsteel Industries, Inc., P. O. Box 877, Dubuque, IA 52004-0877. The executive officers of the Company, their ages, positions (in each case as of August 16, 2013), and the year they were first elected or appointed an officer of the registrant, are as follows: Name (age) Position (date first became officer) Karel K. Czanderna (57) President & Chief Executive Officer (2012) Timothy E. Hall (55) Senior Vice President-Finance, Chief Financial Officer, Secretary & Treasurer (2000) Jeffrey T. Bertsch (58) Senior Vice President of Corporate Services (1989) Julia K. Bizzis (56) Senior Vice President Strategic Growth (2013) Donald D. Dreher (63) Senior Vice President (2004), President & CEO of DMI Furniture, Inc. (2003) James R. Richardson (69) Senior Vice President of Residential Sales and Marketing (1979) Item 1A. Risk Factors Our business is subject to a variety of risks. You should carefully consider the risk factors detailed below in conjunction with the other information contained in this Annual Report on Form 10-K. Should any of these risks actually materialize, our business, financial condition, and future prospects could be negatively impacted. These risks are not the only ones we face. There may be additional factors that are presently unknown to us or that we currently believe to be immaterial that could affect our business. Our products are considered highly deferrable purchases for consumers during economic downturns. Prolonged negative economic conditions could impact our business. Home furnishings and commercial products are generally considered a deferrable purchase by most consumers and end-users. Economic downturns and prolonged negative economic conditions could affect consumer spending habits by decreasing the overall demand for home furnishings and commercial products. These events could impact retailers, hospitality, recreational vehicle seating and healthcare businesses resulting in an impact on our business. A recovery in our sales could lag significantly behind a general economic recovery due to the deferrable nature and relatively significant cost of home furnishings and commercial products purchases. Our future success depends on our ability to manage our global supply chain. We acquire raw materials, component parts and certain finished products from external suppliers, both U.S. and foreign. Many of these suppliers are dependent upon other suppliers in countries other than where they are located. This global interdependence within our supply chain is subject to delays in delivery, availability, quality and pricing (including tariffs) of products. The delivery of goods from these suppliers may be delayed by customs, labor issues, changes in political, economic and social conditions, laws and regulations. Unfavorable fluctuations in price, quality, delivery and availability of these products could negatively affect our ability to meet demands of our customers and have a negative impact on product margin. Competition from U.S. and foreign finished product manufacturers may adversely affect our business, operating results or financial condition. The furniture industry is very competitive and fragmented. We compete with U.S. and foreign manufacturers and distributors. As a result, we may not be able to maintain or raise the prices of our products in response to competitive pressures or increasing costs. Also, due to the large number of competitors and their wide range of product offerings, we may not be able to significantly differentiate our products (through styling, finish and other construction techniques) from those of our competitors. Our current and potential customers have the ability to obtain products direct from the manufacturers. As a result, we are continually subject to the risk of losing market share, which may lower our sales and earnings. Business failures of large dealers or a group of customers could impact our future sales and earnings. Our business practice has been to extend payment terms to our customers. As a result, we have a large amount of trade receivables. Although we have no customers that individually represent 10% or more of our annual net sales or accounts receivable, net, balance as of June 30, 2013, business failures of a large customer or a group of customers could require us to record additional receivable reserves, which would decrease earnings. Receivables collection can be significantly impacted by economic conditions. Deterioration of the economy or a lack of economic recovery could cause further business failures of our customers, which could in turn require additional receivable reserves and lower our earnings. Our failure to anticipate or respond to changes in consumer or designer tastes and fashions in a timely manner could adversely affect our business and decrease our sales and earnings. Furniture is a styled product and is subject to rapidly changing consumer and end-user trends and tastes and is highly fashion oriented, and if we are not able to acquire sufficient fabric variety, or if we are unable to predict or respond to changes in fashion trends, we may lose sales and have to sell excess inventory at reduced prices. Our success depends on our ability to recruit and retain key employees. Our success depends on our ability to recruit and retain key employees. If we are not successful in recruiting and retaining key employees or experience the unexpected loss of key employees, our operations may be negatively impacted. Future costs of complying with various laws and regulations may adversely impact future operating results. Our business is subject to various laws and regulations Terms of collective bargaining agreements and labor disruptions could adversely impact our results of operations. We employ approximately Due to our participation in multi-employer pension plans, we may have exposures under those plans that could extend beyond what our obligations would be with respect to our employees. We participate in, and make periodic contributions to, three multi-employer pension plans that cover Our future results may be affected by various legal proceedings and compliance risk, including those involving product liability, environmental, or other matters. We face the business risk of exposure to product liability claims in the event that the use of any of our products results in personal injury or property damage. In the event any of our products prove to be defective, we may be required to recall or redesign such products. We are also subject to various laws and regulations relating to environmental protection and the discharge of materials into the Item 1B. Unresolved Staff Comments Item 2. Properties The Company owns the following facilities as of June 30, Location Approximate Principal Operations 221,000 Manufacturing Riverside, California Manufacturing and Distribution Dublin, Georgia 300,000 Manufacturing New Paris, Indiana 168,000 Held for sale Huntingburg, Indiana 691,000 Distribution Dubuque, Iowa Manufacturing and Distribution Dubuque, Iowa 40,000 Corporate Office Starkville, Mississippi 349,000 Manufacturing Lancaster, Pennsylvania 216,000 Distribution The Company leases the following facilities as of June 30, Location Approximate Principal Operations 32,000 Ferdinand, Indiana 101,000 Distribution Louisville, Kentucky 15,000 Administrative Offices Juarez, Mexico Manufacturing The Company’s operating plants are well suited for their manufacturing purposes and have been updated and expanded from time to time as conditions warrant. Management believes there is adequate production and distribution capacity at the Company’s facilities to meet present market demands. The Company leases showrooms for displaying its products in the furniture markets in High Point, North Carolina and Las Vegas, Nevada. Item 3. Legal Proceedings Indiana Civil Litigation – A Complaint for Damages and Injunctive Relief and Request for Jury Trial was filed on March 3, 2011 in Elkhart, Indiana Superior Court by Leo VanNorman, et al, plaintiffs vs. Flexsteel Industries, Inc., et al, defendants. The Plaintiffs have not identified a dollar amount of their alleged Other Item 4. PART II Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities Share Investment Performance The following graph 2006 2007 2008 2009 2010 2011 2008 2009 2010 2011 2012 2013 Flexsteel 100.00 115.82 93.64 73.16 97.88 132.62 100.00 78.13 104.53 141.64 196.86 249.18 Peer Group 100.00 87.04 62.64 31.24 39.52 48.76 New Peer Group 100.00 63.84 97.91 144.69 139.38 198.91 NASDAQ 100.00 122.72 93.36 71.02 79.93 105.32 100.00 76.07 85.62 112.80 109.34 142.31 Former Peer Group 100.00 49.87 63.09 77.84 77.96 111.35 The NASDAQ Global Select Market is the principal market on which the Company’s common stock is traded. Sale Price of Common Stock * Cash Dividends Sale Price of Common Stock * Cash Dividends Fiscal 2011 Fiscal 2010 Fiscal 2013 Fiscal 2012 High Low High Low Fiscal 2011 Fiscal 2010 High Low High Low Fiscal 2013 Fiscal 2012 First Quarter $ 15.84 $ 10.08 $ 8.84 $ 6.64 $ 0.075 $ 0.05 $ 23.28 $ 18.68 $ 15.91 $ 13.04 $ 0.15 $ 0.10 Second Quarter 18.75 14.22 10.34 7.77 0.075 0.05 23.44 19.01 15.00 13.26 0.15 0.10 Third Quarter 19.69 14.11 16.50 9.33 0.075 0.05 26.29 21.15 18.39 13.82 0.15 0.10 Fourth Quarter 16.60 13.80 15.74 10.75 0.075 0.05 25.43 18.56 22.00 18.28 0.15 0.15 * Reflects the market price as reported on The NASDAQ Global The Company estimates there were approximately 2013. There were no repurchases of the Company’s common stock during the quarter ended June 30, 2013. The payment of future cash dividends is within the discretion of our Board of Directors and will depend, among other factors, on our earnings, capital requirements and operating and financial condition. Item 6. Selected Financial Data The selected financial data presented below should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in Item 8 of this Annual Report on Form 10-K and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K. The selected consolidated 2011 2010 2009 2008 2007 SUMMARY OF OPERATIONS Net sales $ 339,426 $ 326,466 $ 324,158 $ 405,655 $ 425,400 Cost of goods sold 262,124 251,685 263,083 327,165 344,177 Operating income (loss) 15,864 17,529 (2,272 ) 7,596 14,699 Interest and other income 343 361 661 469 1,277 Interest expense — 439 968 1,469 1,491 Income (loss) before income taxes 16,207 17,451 (2,579 ) 6,596 14,484 Income tax provision (benefit) 5,790 6,650 (1,070 ) 2,360 5,150 Net income (loss) (1) (2) (3) 10,417 10,801 (1,509 ) 4,236 9,334 Earnings (loss) per common share: (1) (2) (3) Basic 1.56 1.63 (0.23 ) 0.64 1.42 Diluted 1.50 1.61 (0.23 ) 0.64 1.42 Cash dividends declared per common share $ 0.30 $ 0.20 $ 0.36 $ 0.52 $ 0.52 SELECTED DATA AS OF JUNE 30 Average common shares outstanding: Basic 6,693 6,608 6,576 6,574 6,568 Diluted 6,929 6,697 6,576 6,611 6,583 Total assets $ 164,677 $ 157,670 $ 150,971 $ 179,906 $ 185,014 Property, plant and equipment, net 21,387 21,614 23,298 26,372 28,168 Capital expenditures 2,573 1,251 1,203 1,228 10,839 Long-term debt — — — 20,811 21,336 Working capital (current assets less current liabilities) 100,683 90,800 78,416 100,920 97,902 Shareholders’ equity $ 128,573 $ 117,612 $ 106,998 $ 112,752 $ 112,679 SELECTED RATIOS Net income (loss), as a percent of sales 3.1 3.3 (0.5 ) 1.0 2.2 Current ratio 4.6 to 1 3.9 to 1 3.2 to 1 3.5 to 1 3.2 to 1 Return on ending shareholders’ equity 8.1 9.2 (1.4 ) 3.8 8.3 Average number of employees 1,320 1,400 1,600 2,140 2,290 2013 2012 2011 2010 2009 SUMMARY OF OPERATIONS Net sales $ 386,189 $ 352,089 $ 339,426 $ 326,466 $ 324,158 Cost of goods sold 295,720 266,810 262,124 251,685 263,083 Operating income (loss) 20,271 20,246 15,864 17,529 (2,272 ) Interest and other income 610 422 343 361 661 Interest expense — — — 439 968 Income (loss) before income taxes 20,881 20,668 16,207 17,451 (2,579 ) Income tax provision (benefit) 7,730 7,600 5,790 6,650 (1,070 ) Net income (loss) (1) (2) (3) 13,151 13,068 10,417 10,801 (1,509 ) Earnings (loss) per common share: (1) (2) (3) Basic 1.87 1.93 1.56 1.63 (0.23 ) Diluted 1.80 1.86 1.50 1.61 (0.23 ) Cash dividends declared per common share $ 0.60 $ 0.45 $ 0.30 $ 0.20 $ 0.36 SELECTED DATA AS OF JUNE 30 Average common shares outstanding: Basic 7,041 6,781 6,693 6,608 6,576 Diluted 7,326 7,008 6,929 6,697 6,576 Total assets $ 192,539 $ 181,672 $ 164,677 $ 157,670 $ 150,971 Property, plant and equipment, net 32,145 29,867 21,387 21,614 23,298 Capital expenditures 6,225 10,939 2,573 1,251 1,203 Working capital (current assets less current liabilities) 113,699 103,744 100,683 90,800 78,416 Shareholders’ equity $ 151,237 $ 139,442 $ 128,573 $ 117,612 $ 106,998 SELECTED RATIOS Net income (loss), as a percent of sales 3.4 3.7 3.1 3.3 (0.5 ) Current ratio 4.2 to 1 4.3 to 1 4.6 to 1 3.9 to 1 3.2 to 1 Return on ending shareholders’ equity 8.7 9.4 8.1 9.2 (1.4 ) Average number of employees 1,320 1,300 1,320 1,400 1,600 (1) Fiscal 2013 net income and per share amounts include executive transition costs of $0.8 million (after tax) or $0.11 per share. (2) Fiscal 2011 net income and per share amounts include charges consisting of employee separation costs and inventory write down related to closing a manufacturing facility of $1.0 million (after tax) or $0.15 per share. Fiscal 2009 net loss and per share amounts reflect facility consolidation and other costs (after tax) of $1.5 million or $0.23 Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations General The following analysis of the results of operations and financial condition of the Company should be read in conjunction with the consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K. Critical Accounting Policies The discussion and analysis of the Company’s consolidated financial statements and results of operations are based on consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America. Preparation of these consolidated financial statements requires the use of estimates and judgments that affect the reported results. The Company uses estimates based on the best information available in recording transactions and balances resulting from business operations. Estimates are used for such items as Allowance for doubtful accounts – the Company establishes an allowance for doubtful accounts through review of open accounts, historical collections and historical Inventories – the Company values inventory at the lower of cost or Revenue recognition – is Recently Issued Accounting Pronouncements See Item 8. Note 1 to the Company’s Consolidated Financial Statements. Results of Operations The following table has been prepared as an aid in understanding the Company’s results of operations on a comparative basis for the fiscal years ended June 30, FOR THE YEARS ENDED JUNE 30, FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 2013 2012 2011 Net sales 100.0 % 100.0 % 100.0 % 100.0 % 100.0 % 100.0 % Cost of goods sold (77.2 ) (77.2 ) (81.2 ) (76.6 ) (75.8 ) (77.2 ) Gross margin 22.8 22.8 18.8 23.4 24.2 22.8 Selling, general and administrative (17.8 ) (17.5 ) (18.8 ) (18.2 ) (18.4 ) (17.8 ) Facility consolidation and other charges (0.3 ) — (0.8 ) — — (0.3 ) Operating income (loss) 4.7 5.3 (0.8 ) Operating income 5.2 5.8 4.7 Other income, net 0.1 0.0 0.0 0.2 0.1 0.1 Income (loss) before income taxes 4.8 5.3 (0.8 ) Income tax (provision) benefit (1.7 ) (2.0 ) 0.3 Net income (loss) 3.1 % 3.3 % (0.5 )% Income before income taxes 5.4 5.9 4.8 Income tax provision (2.0 ) (2.2 ) (1.7 ) Net income 3.4 % 3.7 % 3.1 % Fiscal Net sales for fiscal Gross margin for the fiscal year ended June 30, 2013 was 23.4% compared to 24.2% for the prior fiscal year. During fiscal year 2013 the Company’s expenses related to workers compensation and health insurance programs were approximately $1.5 million higher than in fiscal 2012, impacting gross margin by 0.4%. Selling, general and administrative expenses for the fiscal year ended June 30, 2013 were 18.2% of net sales compared to 18.4% in the prior fiscal year. The current year includes executive transition costs of $1.3 million or 0.4% of net sales. The effective tax rate for the fiscal year ended June 30, 2013 was 37.0% compared to 36.8% for fiscal year 2012. The change in effective tax rate is primarily due to the lower benefit of the Domestic Manufacturing Deduction under Internal Revenue Code Section 199 (DMD), which provides a tax benefit on U.S. based manufacturing, and the limitation on executive compensation deduction. The fiscal year 2013 net income increased $0.1 million to $13.2 million, the highest ever reported for the Company. The number of diluted shares increased during fiscal 2013 due to additional shares outstanding and the impact of the Company’s higher stock trading price on outstanding options, resulting in the Company reporting diluted earnings per share of $1.80 for fiscal year 2013 versus $1.86 for fiscal year 2012. All earnings per share amounts are on a diluted basis. Fiscal 2012 Compared to Fiscal 2011 Net sales for fiscal 2012 were $352.1 million compared to $339.4 million in the prior fiscal year, an increase of 3.7%. For the fiscal year ended June 30, 2012, residential net sales were $275.4 million compared to $258.1 million for the year ended June 30, 2011, an increase of Gross margin for the year ended June 30, Operating income The effective tax rate for the fiscal year ended June 30, The above factors resulted in net income for the fiscal year ended June 30, 2011. All earnings per share amounts are on a diluted basis. Liquidity and Capital Resources Working capital (current assets less current liabilities) at June 30, The Company’s main source of liquidity is cash and cash flows from operations. As of June 30, 2013 and 2012, the Company had cash totaling $10.9 million and $14.0 million, respectively. The Company maintains a credit agreement which provides short-term working capital financing up to $10.0 million with interest of LIBOR plus 1%, including up to $4.0 million of letters of credit. Letters of credit outstanding at June 30, 2013 totaled $2.3 million, leaving borrowing availability of $7.7 million. The Company did not utilize any borrowing availability under the credit facility during the period other than the aforementioned letters of credit. The credit agreement expires June 30, 2014. At June 30, 2013, the Company was in compliance with all of the financial covenants contained in the credit agreement. An officer of the Company is a director at a bank where the Company maintains an unsecured $8.0 million line of credit, with interest at prime minus 1%, and where its routine banking transactions are processed. The Company did not utilize any borrowing availability during the period and no amount was outstanding on the line of credit at June 30, 2013. In addition, the supplemental retirement plans assets, held in a Rabbi Trust, of $5.8 million are administered by this bank’s trust department. The Company receives no special services or pricing on the services performed by the bank due to the directorship of this officer. Cash decreased Net cash provided by operating activities Net cash used in investing activities was During fiscal year Net cash used in financing activities was The Company expects that capital expenditures for fiscal year 2014 will be approximately At June 30, Total Less than 1 - 3 3 - 5 More than Operating lease obligations $ 4,082 $ 1,851 $ 2,231 $ — $ — Total 1 Year 2 - 3 4 - 5 More than Operating lease obligations $ 10,087 $ 2,617 $ 3,897 $ 1,588 $ 1,985 Supplemental retirement plans 5,403 2,989 — — 2,414 Total contractual obligations 15,490 5,606 3,897 1,588 4,399 Financing Arrangements See Note 6 to the Consolidated Financial Statements of this Annual Report on Form 10-K. Outlook Item 7A. Quantitative and Qualitative Disclosures About Market Risk General– Market risk represents the risk of changes in the value of a financial instrument, derivative or non-derivative, caused by fluctuations in interest rates, foreign exchange rates and equity prices. As discussed below, management of the Company does not believe that changes in these factors could cause material fluctuations in the Company’s results of operations or cash flows. The ability to import furniture products can be adversely affected by political issues in the countries where suppliers are located, disruptions associated with shipping distances and negotiations with port employees. Other risks related to furniture product importation include government imposition of regulations and/or quotas; duties and taxes on imports; and significant fluctuation in the value of the U.S. dollar against foreign currencies. Any of these factors could interrupt supply, increase costs and decrease earnings. Inflation – Increased operating costs are reflected in product or services pricing with any limitations on price increases determined by the marketplace. Inflation or other pricing pressures could impact raw material costs, labor costs and interest rates which are important components of costs for the Company and could have an adverse effect on our profitability, especially where increases in these costs exceed price increases on finished products. Foreign Currency Risk – During fiscal years Interest Rate Risk –The Company’s primary market risk exposure with regard to financial instruments is changes in interest rates. At June 30, Item 8. Financial Statements and Supplementary Data REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM To the Board of Directors and We have audited the accompanying consolidated balance sheets of Flexsteel Industries, Inc. and subsidiaries (the “Company”) as of June 30, We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. In our opinion, such consolidated financial statements present fairly, in all material respects, the financial position of Flexsteel Industries, Inc. and subsidiaries as of June 30, (Amounts in thousands, except share and per share data) JUNE 30, June 30, 2011 2010 2013 2012 ASSETS CURRENT ASSETS: Cash $ 17,889 $ 8,278 $ 10,934 $ 13,970 Trade receivables – less allowance for doubtful accounts: 2011, $2,000; 2010, $2,020 31,451 35,748 Trade Receivables - less allowances: 2013, $1,560; 2012, $1,910 36,075 33,601 Inventories 73,680 72,637 92,417 82,689 Deferred income taxes 3,700 4,050 4,970 3,750 Other 1,633 1,076 Other current assets 4,805 1,583 Total current assets 128,353 121,789 149,201 135,593 NONCURRENT ASSETS: Property, plant and equipment, net 21,387 21,614 32,145 29,867 Deferred income taxes 2,560 3,010 1,190 3,160 Other assets 12,377 11,257 10,003 13,052 TOTAL $ 164,677 $ 157,670 $ 192,539 $ 181,672 LIABILITIES AND SHAREHOLDERS’ EQUITY CURRENT LIABILITIES: Accounts payable – trade $ 9,899 $ 10,815 Accounts payable - trade $ 13,927 $ 12,973 Accrued liabilities: Payroll and related items 6,922 7,023 7,836 8,037 Insurance 5,645 6,192 4,667 4,440 Other 5,204 6,959 Other current liabilities 9,072 6,399 Total current liabilities 27,670 30,989 35,502 31,849 LONG-TERM LIABILITIES: Deferred compensation 5,270 5,096 Supplemental retirement plans 2,414 5,613 Other liabilities 3,164 3,973 3,386 4,768 Total liabilities 36,104 40,058 41,302 42,230 COMMITMENTS AND CONTINGENCIES (Note 12) SHAREHOLDERS’ EQUITY: Cumulative preferred stock – $50 par value; authorized 60,000 shares; outstanding – none Undesignated (subordinated) stock – $1 par value; authorized 700,000 shares; outstanding – none Common stock – $1 par value; authorized 15,000,000 shares; outstanding 2011, 6,710,612 shares; 2010, 6,645,532 shares 6,711 6,646 Cumulative preferred stock - $50 par value; authorized 60,000 shares; outstanding - none Undesignated (subordinated) stock - $1 par value; authorized 700,000 shares; outstanding - none Common stock - $1 par value; authorized 15,000,000 shares; outstanding 2013, 7,106,723 shares; 2012, 6,905,534 shares 7,107 6,906 Additional paid-in capital 6,698 5,425 10,615 8,476 Retained earnings 115,699 107,293 134,606 125,699 Accumulated other comprehensive loss (535 ) (1,752 ) (1,091 ) (1,639 ) Total shareholders’ equity 128,573 117,612 151,237 139,442 TOTAL $ 164,677 $ 157,670 $ 192,539 $ 181,672 See accompanying Notes to Consolidated Financial Statements. FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES For the years ended June 30, 2013 2012 2011 Net sales $ 386,189 $ 352,089 $ 339,426 Cost of goods sold (295,720 ) (266,810 ) (262,124 ) Gross margin 90,469 85,279 77,302 Selling, general and administrative (70,198 ) (65,033 ) (60,422 ) Facility closing costs — — (1,016 ) Operating income 20,271 20,246 15,864 Interest and other income 610 422 343 Income before income taxes 20,881 20,668 16,207 Income tax provision (7,730 ) (7,600 ) (5,790 ) Net income $ 13,151 $ 13,068 $ 10,417 Weighted average number of common shares outstanding: Basic 7,041 6,781 6,693 Diluted 7,326 7,008 6,929 Earnings per share of common stock: Basic $ 1.87 $ 1.93 $ 1.56 Diluted $ 1.80 $ 1.86 $ 1.50 Cash dividends declared per common share $ 0.60 $ 0.45 $ 0.30 CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME For the years ended June 30, 2013 2012 2011 Net income $ 13,151 $ 13,068 $ 10,417 Unrealized gains (losses) on securities in supplemental retirement plans 96 (5 ) 562 Income tax (expense) benefit related to securities in supplemental retirement plans gains (losses) (36 ) 2 (214 ) Net unrealized gains (losses) on securities in supplemental retirement plans (1) 60 (3 ) 348 Minimum pension liability 787 (1,771 ) 1,401 Income tax (expense) benefit related to minimum pension liability (299 ) 670 (532 ) Net minimum pension liability 488 (1,101 ) 869 Other comprehensive income (loss), net of tax 548 (1,104 ) 1,217 Comprehensive income $ 13,699 $ 11,964 $ 11,634 See Note 9 to the Consolidated Financial Statements See accompanying Notes to Consolidated Financial Statements. FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 NET SALES $ 339,426 $ 326,466 $ 324,158 COST OF GOODS SOLD (262,124 ) (251,685 ) (263,083 ) GROSS MARGIN 77,302 74,781 61,075 SELLING, GENERAL AND ADMINISTRATIVE (60,422 ) (57,252 ) (60,792 ) FACILITY CLOSING COSTS (1,016 ) — (2,555 ) OPERATING INCOME (LOSS) 15,864 17,529 (2,272 ) OTHER INCOME (EXPENSE): Interest and other income 343 361 661 Interest expense — (439 ) (968 ) Total 343 (78 ) (307 ) INCOME (LOSS) BEFORE INCOME TAXES 16,207 17,451 (2,579 ) INCOME TAX (PROVISION) BENEFIT (5,790 ) (6,650 ) 1,070 NET INCOME (LOSS) $ 10,417 $ 10,801 $ (1,509 ) WEIGHTED AVERAGE NUMBER OF COMMON SHARES OUTSTANDING: Basic 6,693 6,608 6,576 Diluted 6,929 6,697 6,576 EARNINGS (LOSS) PER SHARE OF COMMON STOCK: Basic $ 1.56 $ 1.63 $ (0.23 ) Diluted $ 1.50 $ 1.61 $ (0.23 ) CASH DIVIDENDS DECLARED PER COMMON SHARE $ 0.30 $ 0.20 $ 0.36 FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES Total Par Additional Retained Accumulated Total Balance at June 30, 2010 $ 6,646 $ 5,425 $ 107,293 $ (1,752 ) $ 117,612 Issuance of common stock: Stock options exercised, net 65 259 — — 324 Unrealized gain on available for sale investments, net of tax — — — 348 348 Long-term incentive compensation — 590 — — 590 Stock-based compensation — 424 — — 424 Minimum pension liability adjustment, net of tax — — — 869 869 Cash dividends declared — — (2,011 ) — (2,011 ) Net income — — 10,417 — 10,417 Balance at June 30, 2011 $ 6,711 $ 6,698 $ 115,699 $ (535 ) $ 128,573 Issuance of common stock: Stock options exercised, net 156 761 — — 917 Unrealized gain on available for sale investments, net of tax — — — (3 ) (3 ) Long-term incentive compensation 39 761 — — 800 Stock-based compensation — 256 — — 256 Minimum pension liability adjustment, net of tax — — — (1,101 ) (1,101 ) Cash dividends declared — — (3,068 ) — (3,068 ) Net income — — 13,068 — 13,068 Balance at June 30, 2012 $ 6,906 $ 8,476 $ 125,699 $ (1,639 ) $ 139,442 Issuance of common stock: Stock options exercised, net 92 1,197 — — 1,289 Unrealized gain on available for sale investments, net of tax — — — 60 60 Long-term incentive compensation 109 442 — — 551 Stock-based compensation — 500 — — 500 Minimum pension liability adjustment, net of tax — — — 488 488 Cash dividends declared — — (4,244 ) — (4,244 ) Net income — — 13,151 — 13,151 Balance at June 30, 2013 $ 7,107 $ 10,615 $ 134,606 $ (1,091 ) $ 151,237 See accompanying Notes to Consolidated Financial Statements. Total Par Additional Retained Accumulated Total Balance at July 1, 2008 $ 6,576 $ 4,256 $ 101,692 $ 228 $ 112,752 Unrealized loss on available for sale investments, net of tax — — — (1,022 ) (1,022 ) Stock-based compensation — 114 — — 114 Interest rate swaps valuation adjustment, net of tax — — — (1 ) (1 ) Minimum pension liability adjustment, net of tax — — — (969 ) (969 ) Cash dividends declared — — (2,367 ) — (2,367 ) Net loss — — (1,509 ) — (1,509 ) Balance at June 30, 2009 6,576 4,370 97,816 (1,764 ) 106,998 Issuance of common stock: Stock options exercised, net 70 274 — — 344 Unrealized gain on available for sale investments, net of tax — — — 39 39 Long-term incentive compensation — 510 — — 510 Stock-based compensation — 271 — — 271 Interest rate swaps valuation adjustment, net of tax — — — 177 177 Minimum pension liability adjustment, net of tax — — — (204 ) (204 ) Cash dividends declared — — (1,324 ) — (1,324 ) Net income — — 10,801 — 10,801 Balance at June 30, 2010 6,646 5,425 107,293 (1,752 ) 117,612 Issuance of common stock: Stock options exercised, net 65 259 — — 324 Unrealized gain on available for sale investments, net of tax — — — 348 348 Long-term incentive compensation — 590 — — 590 Stock-based compensation — 424 — — 424 Minimum pension liability adjustment, net of tax — — — 869 869 Cash dividends declared — — (2,011 ) — (2,011 ) Net income — — 10,417 — 10,417 Balance at June 30, 2011 $ 6,711 $ 6,698 $ 115,699 $ (535 ) $ 128,573 FOR THE YEARS ENDED JUNE 30, 2013 2012 2011 OPERATING ACTIVITIES: Net income $ 13,151 $ 13,068 $ 10,417 Adjustments to reconcile net income to net cash provided by (used in) operating activities: Depreciation 3,803 2,835 2,690 Deferred income taxes 414 23 54 Stock-based compensation expense 1,051 1,056 1,014 Excess tax benefit from stock-based payment arrangements (182 ) — — Provision for losses on accounts receivable (215 ) (150 ) 870 Other non-cash, net 69 7 224 Gain on disposition of capital assets (18 ) (34 ) (185 ) Changes in operating assets and liabilities: Trade receivables (2,260 ) (2,000 ) 3,427 Inventories (9,728 ) (9,009 ) (1,043 ) Other current assets 58 50 (557 ) Other assets (307 ) (308 ) (270 ) Accounts payable - trade 1,082 2,699 (841 ) Accrued liabilities (138 ) 572 (2,541 ) Other long-term liabilities (665 ) (174 ) 367 Supplemental retirement plans (210 ) 342 174 Net cash provided by operating activities 5,905 8,977 13,800 INVESTING ACTIVITIES: Purchases of investments (1,086 ) (777 ) (698 ) Proceeds from sales of investments 1,273 405 410 Proceeds from sale of capital assets 21 34 187 Capital expenditures (6,225 ) (10,939 ) (2,573 ) Net cash used in investing activities (6,017 ) (11,277 ) (2,674 ) FINANCING ACTIVITIES: Dividends paid (4,213 ) (2,535 ) (1,839 ) Proceeds from issuance of common stock 1,107 916 324 Excess tax benefit from stock-based payment arrangements 182 — — Net cash used in financing activities (2,924 ) (1,619 ) (1,515 ) (Decrease) increase in cash and cash equivalents (3,036 ) (3,919 ) 9,611 Cash at beginning of year 13,970 17,889 8,278 Cash at end of year $ 10,934 $ 13,970 $ 17,889 FOR THE YEARS ENDED JUNE 30, 2013 2012 2011 SUPPLEMENTAL INFORMATION CASH PAID DURING THE PERIOD FOR: Income taxes paid $ 7,250 $ 6,237 $ 7,647 Capital expenditures in accounts payable $ 261 $ 389 $ 14 See accompanying Notes to Consolidated Financial Statements. FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 OPERATING ACTIVITIES: Net income (loss) $ 10,417 $ 10,801 $ (1,509 ) Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: Depreciation 2,690 2,986 3,733 Deferred income taxes 54 (963 ) 449 Stock-based compensation expense 1,014 781 114 Provision for losses on accounts receivable 870 920 1,240 Other non-cash, net 224 218 14 Gain on disposition of capital assets (185 ) (9 ) (252 ) Gain on sale of investments — — (462 ) Impairment of long-lived assets — — 138 Changes in operating assets and liabilities: Trade receivables 3,427 (5,386 ) 11,261 Inventories (1,043 ) 1,207 11,947 Other current assets (557 ) 2,837 (781 ) Other assets (270 ) (18 ) (288 ) Accounts payable – trade (841 ) 994 (4,849 ) Accrued liabilities (2,541 ) 3,618 (2,918 ) Other long-term liabilities 367 1,028 (178 ) Deferred compensation 174 105 (352 ) Net cash provided by operating activities 13,800 19,119 17,307 INVESTING ACTIVITIES: Purchases of investments (698 ) (721 ) (520 ) Proceeds from sales of investments 410 359 1,460 Proceeds from sale of capital assets 187 34 676 Capital expenditures (2,573 ) (1,251 ) (1,203 ) Net cash (used in) provided by investing activities (2,674 ) (1,579 ) 413 FINANCING ACTIVITIES: (Repayments of) proceeds from short-term borrowings, net — (10,000 ) 4,857 Repayment of long-term borrowings — — (20,811 ) Dividends paid (1,839 ) (1,320 ) (2,893 ) Proceeds from issuance of common stock 324 344 — Net cash used in financing activities (1,515 ) (10,976 ) (18,847 ) Increase (decrease) in cash and cash equivalents 9,611 6,564 (1,127 ) Cash and cash equivalents at beginning of year 8,278 1,714 2,841 Cash and cash equivalents at end of year $ 17,889 $ 8,278 $ 1,714 FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 SUPPLEMENTAL INFORMATION CASH PAID DURING THE PERIOD FOR: Interest $ — $ 439 $ 979 Income taxes paid (refunded) $ 7,647 $ 3,587 $ (62 ) FLEXSTEEL INDUSTRIES, INC. AND SUBSIDIARIES 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES DESCRIPTION OF BUSINESS – Flexsteel Industries, Inc. and subsidiaries (the “Company”) is one of the oldest and largest PRINCIPLES OF CONSOLIDATION – the consolidated financial statements include the accounts of Flexsteel Industries, Inc. and its wholly owned subsidiaries. All intercompany transactions and accounts have been eliminated in consolidation. USE OF ESTIMATES – the preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Ultimate results could differ from those estimates. FAIR VALUE – the Company’s cash, accounts receivable, other current assets, accounts payable and certain accrued liabilities are carried at amounts which reasonably approximate their fair value due to their short-term nature. Generally accepted accounting principles on fair value measurement for certain financial assets and liabilities INVENTORIES – are stated at the lower of cost or PROPERTY, PLANT AND EQUIPMENT – is stated at cost and depreciated using the straight-line method over the estimated useful lives of the assets. For internal use software, the Company’s policy is to capitalize external direct costs of materials and services, directly related internal payroll and payroll-related costs, and interest costs. These costs are amortized using the straight-line method over the useful lives. VALUATION OF LONG–LIVED ASSETS – the Company periodically reviews the carrying value of long-lived assets and estimated depreciable or amortizable lives for continued appropriateness. This review is based upon projections of anticipated future cash flows and is performed whenever events or changes in circumstances indicate that asset carrying values may not be recoverable or that the estimated depreciable or amortizable lives may have changed. No impairments of long-lived assets or changes in depreciable or amortizable lives were incurred during fiscal year 2013. WARRANTY – the Company estimates the amount of warranty claims on sold product that may be incurred based on current and historical data. The actual warranty expense could differ from the estimates made by the Company based on product performance. REVENUE RECOGNITION – is ADVERTISING COSTS – are charged to selling, general and administrative expense in the periods incurred. The Company conducts no direct-response advertising programs and there are no assets related to advertising recorded on the consolidated balance sheet. Advertising expenditures, primarily shared customer advertising in which an identifiable benefit is received and national trade-advertising programs, were approximately DESIGN, RESEARCH AND DEVELOPMENT COSTS – are charged to selling, general and administrative expense in the periods incurred. Expenditures for design, research and development costs were approximately INSURANCE – the Company is self-insured for health care and most workers’ compensation up to predetermined amounts above which third party insurance applies. The Company purchases specific stop-loss insurance for individual health care claims in excess of $150,000 per plan year. For workers’ compensation the Company retains the first INCOME TAXES – the Company uses the liability method of accounting for income taxes. Under this method, deferred tax assets and liabilities are determined based on differences between the financial reporting and tax bases of assets and liabilities and are measured using the enacted tax rates and laws that will be in effect when the differences are expected to reverse. The Company recognizes in its financial statements the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. EARNINGS In computing EPS for the fiscal years ended 2013, 2012 and 2011, net income as reported for each respective period is divided by the fully diluted weighted average number of June 30, (in thousands) 2013 2012 2011 Basic shares 7,041 6,781 6,693 Potential common shares: Stock options 253 142 147 Long-term incentive plan 32 85 89 285 227 236 Diluted shares 7,326 7,008 6,929 Anti-dilutive shares 10 300 424 STOCK–BASED COMPENSATION – the Company recognizes compensation expense related to the cost of employee services received in exchange for Company equity interests based on the award’s fair value at the date of grant. See Note 8 Stock-Based Compensation. ACCOUNTING DEVELOPMENTS – In 2. INVENTORIES Inventories valued on a LIFO basis (steel) would have been approximately June 30, (in thousands) June 30, 2011 2010 2013 2012 Raw materials $ 9,235 $ 9,696 $ 10,684 $ 10,410 Work in process and finished parts 3,951 4,943 5,410 5,288 Finished goods 60,494 57,998 76,323 66,991 Total $ 73,680 $ 72,637 $ 92,417 $ 82,689 3. PROPERTY, PLANT AND EQUIPMENT (in thousands) Estimated June 30, Estimated June 30, Life (Years) 2011 2010 2013 2012 Land $ 3,984 $ 3,984 $ 4,233 $ 4,150 Buildings and improvements 5-39 39,851 40,248 5-39 49,147 39,978 Machinery and equipment 3-7 26,513 28,251 3-7 27,048 26,449 Delivery equipment 3-5 18,180 18,269 3-5 18,689 18,113 Furniture and fixtures 3-7 4,000 4,291 3-7 6,265 3,843 Construction in progress 366 — — 9,333 Total 92,894 95,043 105,382 101,866 Less accumulated depreciation (71,507 ) (73,429 ) (73,237 ) (71,999 ) Net $ 21,387 $ 21,614 32,145 29,867 4. OTHER NONCURRENT ASSETS (in thousands) June 30, June 30, 2011 2010 2013 2012 Cash value of life insurance $ 6,815 $ 6,560 $ 7,337 $ 7,072 Rabbi Trust assets (see Note 9) 5,533 4,683 2,529 5,900 Other 29 14 137 80 Total $ 12,377 $ 11,257 $ 10,003 $ 13,052 5. ACCRUED LIABILITIES – OTHER (in thousands) June 30, June 30, 2011 2010 2013 2012 Dividends $ 504 $ 332 $ 1,067 $ 1,036 Income taxes — 1,445 299 562 Advertising 1,873 2,200 2,220 1,899 Warranty 970 980 1,000 1,010 Supplemental retirement plans - current 2,989 — Other 1,857 2,002 1,497 1,892 Total $ 5,204 $ 6,959 $ 9,072 $ 6,399 6. CREDIT ARRANGEMENTS The Company maintains a credit agreement which provides short-term working capital financing up to An officer of the Company is a director at a bank where the Company maintains an 7. INCOME TAXES In determining the provision for income taxes, the Company uses an estimated annual effective tax rate that is based on the annual income, The components of the gross liabilities related to unrecognized tax benefits and the related deferred tax assets are as June 30, (in thousands) June 30, 2011 2010 2013 2012 Gross unrecognized tax benefits $ 970 $ 995 $ 1,085 $ 1,000 Accrued Interest and penalties 340 215 Accrued interest and penalties 425 365 Gross liabilities related to unrecognized tax benefits $ 1,310 $ 1,210 $ 1,510 $ 1,365 Deferred tax assets $ 330 $ 230 $ 440 $ 350 A reconciliation of the beginning and ending amount of unrecognized tax benefits is as Balance at June 30, 2009 $ 404 Additions for tax positions of prior years 591 Balance at June 30, 2010 995 Reduction for tax positions of prior years (25 ) Balance at June 30, 2011 $ 970 (in thousands) 2013 2012 2011 Balance at July 1 $ 1,000 $ 970 $ 995 Additions based on tax positions related to the current year 265 207 193 Additions for tax positions of prior years 100 — 41 Reductions for tax positions of prior years (280 ) (177 ) (259 ) Balance at June 30 $ 1,085 $ 1,000 $ 970 The Company records interest and penalties related to income taxes as income tax expense in the The income tax provision (benefit) is as follows for the years ended June 2011 2010 2009 Federal – current $ 5,313 $ 6,630 $ (1,410 ) State – current 423 975 (110 ) (in thousands) 2013 2012 2011 Federal- current $ 6,750 $ 6,969 $ 5,313 State - current 566 608 423 Deferred 54 (955 ) 450 414 23 54 Total $ 5,790 $ 6,650 $ (1,070 ) $ 7,730 $ 7,600 $ 5,790 A reconciliation between the U.S. federal statutory tax rate and the effective tax rate is as follows for the years ended June 30: 2011 2010 2009 2013 2012 2011 Federal statutory tax rate 35.0 % 35.0 % 34.0 % 35.0 % 35.0 % 35.0 % State taxes, net of federal effect 2.6 3.7 2.7 2.6 2.9 2.6 Other (1.9 ) (0.6 ) 4.8 (0.6 ) (1.1 ) (1.9 ) Effective tax rate 35.7 % 38.1 % 41.5 % 37.0 % 36.8 % 35.7 % The effective tax rate for the fiscal The primary components of deferred tax assets and (liabilities) are as June 30, 2011 June 30, 2010 (in thousands) June 30, 2013 June 30, 2012 Current Long-term Current Long-term Current Long-term Current Long-term Accounts receivable $ 740 $ — $ 750 $ — $ 590 $ — $ 710 $ — Inventory 1,360 — 1,100 — 1,530 — 1,390 — Self insurance 620 — 690 — Self-insurance 500 — 480 — Employee benefits 360 — 680 — 800 — 480 — Accrued expenses 620 — 830 — 550 — 690 — Property, plant and equipment — (760 ) — (340 ) — (1,150 ) — (860 ) Deferred compensation — 2,520 — 2,280 Supplemental retirement plans 1,000 810 — 2,430 Other — 800 — 1,070 — 1,530 — 1,590 Total $ 3,700 $ 2,560 $ 4,050 $ 3,010 $ 4,970 $ 1,190 $ 3,750 $ 3,160 The Company is subject to U.S. federal income tax as well as income tax of multiple state and foreign jurisdictions. Generally, tax years 8. STOCK-BASED COMPENSATION The Company has two stock-based compensation methods available when determining employee compensation. (1) Long-Term Management Incentive Compensation Plan – The plan provides for shares of common stock and cash to be awarded to officers and key employees based on performance targets set by the Nominating and Compensation Committee of the Board of Directors (the “Committee”). The Company’s shareholders approved 500,000 shares to be issued under the plan. As of June 30, 2013, 148,213 shares have been issued. The Committee selected consolidated operating results for organic net sales growth and fully-diluted earnings per share for the three-year performance periods beginning July 1, The aggregate number of shares and cash that could be awarded to key executives if the minimum, target and maximum performance goals are met, based upon the fair market value at June 30, Minimum Target Maximum Performance Period Shares Cash Shares Cash Shares Cash Fiscal Year 2009 – 2011 16 $ 152 45 $ 435 71 $ 696 Fiscal Year 2010 – 2012 20 $ 198 58 $ 567 93 $ 907 Fiscal Year 2011 – 2013 17 $ 162 48 $ 463 76 $ 741 (in thousands) Minimum Target Maximum Performance Period Shares Cash Shares Cash Shares Cash Fiscal Year 2011 - 2013 12 $ 198 35 $ 566 56 $ 905 Fiscal Year 2012 - 2014 11 $ 179 32 $ 512 50 $ 819 Fiscal Year 2013 - 2015 10 $ 168 30 $ 481 47 $ 769 If the target performance goals would be achieved, the total amount of compensation cost recognized over the requisite service periods would be $0.9 million Stock Option Plans – The stock option plans for key employees and directors provide for the granting of incentive and nonqualified stock options. Under the plans, options are granted at an exercise price equal to the fair market value of the underlying common stock at the date of grant, and may be exercisable for up to 10 years. All options are exercisable when granted. In fiscal years The fair value of each option grant is estimated on the date of grant using the Black-Scholes option-pricing model with the following weighted-average assumptions used for grants in fiscal The weighted-average grant date fair value of stock options granted during fiscal years 2013, 2012 and 2011 At June 30, A summary of the status of the Company’s stock option plans as of June 30, Shares Weighted Average Aggregate Shares Weighted Average Aggregate Outstanding and exercisable at June 30, 2009 1,020 $ 12.94 $ 407 Outstanding and exercisable at June 30, 2011 1,046 13.56 2,271 Granted 165 8.43 83 13.87 Exercised (99 ) 7.52 (306 ) 12.57 Canceled (34 ) 13.40 (5 ) 17.12 Outstanding and exercisable at June 30, 2010 1,052 12.70 1,168 Outstanding and exercisable at June 30, 2012 818 $ 13.94 $ 4,783 Granted 88 17.23 89 20.31 Exercised (91 ) 7.41 (109 ) 13.38 Canceled (3 ) 17.30 (11 ) 16.09 Outstanding and exercisable at June 30, 2011 1,046 $ 13.56 $ 2,271 Outstanding and exercisable at June 30, 2013 787 $ 14.71 $ 7,609 The following table summarizes information for options outstanding and exercisable at June 30, Weighted Average Range of Options Outstanding Remaining Exercise $ 6.81 – 10.75 254 8.0 $ 7.71 12.35 – 12.74 230 6.0 12.51 14.40 – 16.52 352 3.4 15.54 17.23 – 20.27 210 5.3 18.46 $ 6.81 – 20.27 1,046 5.4 $ 13.56 Range of Options Weighted Average Remaining Exercise $ 6.81 - 8.55 129 5.9 $ 7.62 12.35 - 13.90 216 5.1 12.86 14.40 – 17.23 245 3.5 16.02 19.21 – 22.82 197 4.3 19.77 $ 6.81 – 22.82 787 4.6 14.71 9. BENEFIT AND RETIREMENT PLANS Defined Contribution and Retirement Plans The Company sponsors various defined contribution pension and retirement plans, which cover substantially all employees, other than employees covered by multi-employer pension plans under collective bargaining agreements. Total pension and retirement plan expense was The Company contributes to • Assets contributed to the multi-employer plan by • If a participating employer stops contributing to the plan, the unfunded obligations of the plan may be shared by the remaining participating employers. • If a participating employer chooses to stop participating in The Company’s participation in these plans for the annual period ended June 30, 2013, is outlined in the following table. Unless otherwise noted, the most recent Pension Protection Act zone status available in 2013 and 2012 is for the plan’s year-end at December 31, 2012 and 2011, Pension Protection Company Contributions Expiration Date Number of EIN/Pension June 30, Rehabilitation Surcharge Pension Fund 2013 2012 2013 2012 2011 Central States SE and SW Areas Pension Fund 36-6044243 Red Red Implemented $ 243 $ 254 $ 249 Yes 03/28/2015 18 Steelworkers Pension Trust 23-6648508 Green Green No 347 285 283 No 10/31/2015 194 Central Pension Fund 36-6052390 Green Green No 7 7 7 No 05/31/2017 3 $ 597 $ 546 $ 539 The cumulative cost to exit the Company’s multi-employer plans was approximately $8.6 million, $7.8 million and $7.2 million on June 30, Supplemental Retirement Plans The Company has unfunded 10. ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS) 2011 2010 2009 Net income (loss) $ 10,417 $ 10,801 $ (1,509 ) Other comprehensive income (loss) (OCI): Change in fair value of derivatives, net of income taxes of $0, $(109) and $5, respectively — 177 (1 ) Change in fair value of available-for-sale, Securities, net of income taxes of $(214), $(24), $631, respectively 348 39 (1,022 ) Change in minimum pension liability, net of income taxes of $(532), $124 and $595, respectively 869 (204 ) (969 ) Total other comprehensive income (loss) 1,217 12 (1,992 ) Total comprehensive income (loss) $ 11,634 $ 10,813 $ (3,501 ) The components of accumulated other comprehensive loss, net of income taxes, are as June 30, June 30, 2011 2010 (in thousands) 2013 2012 2011 Available-for-sale securities $ 337 $ (11 ) $ 394 $ 334 $ 337 Pension and other post-retirement benefit adjustments (872 ) (1,741 ) (1,485 ) (1,973 ) (872 ) Total accumulated other comprehensive loss $ (535 ) $ (1,752 ) $ (1,091 ) $ (1,639 ) $ (535 ) 11. LITIGATION Indiana Civil Litigation – A Complaint for Damages and Injunctive Relief and Request for Jury Trial was filed on March 3, 2011 in Elkhart, Indiana Superior Court by Leo VanNorman, et al, plaintiffs vs. Flexsteel Industries, Inc., et al, defendants. The Plaintiffs have not identified a dollar amount of their alleged Other Proceedings– From time to time, the Company is subject to various other legal proceedings, including lawsuits, which arise out of, and are incidental to, the conduct of the Company’s business. The Company does not consider any of such other proceedings that are currently pending, individually or in the aggregate, to be material to its business or likely to result in a material effect on its consolidated operating results, financial condition, or cash flows. 12. COMMITMENTS AND CONTINGENCIES FACILITY LEASES – the Company leases certain facilities and equipment under various operating leases. These leases require the Company to pay the lease cost, operating costs, including property taxes, insurance, and maintenance. Total lease expense related to the various operating leases was approximately Expected future minimum commitments under operating leases as of June 30, (in thousands) Fiscal Year Ended June 30, Fiscal Year Ended June 30, Fiscal Year Ended June 30, 2012 $ 1,851 2013 1,315 2014 751 $ 2,617 2015 165 2,218 2016 — 1,679 2017 794 2018 794 Thereafter — 1,985 $ 4,082 $ 10,087 13. SEGMENT REPORTING The Company operates in one reportable Set forth below is information for the past three fiscal years showing the Company’s net sales attributable to each of the areas of FOR THE YEARS ENDED JUNE 30, (in thousands) FOR THE YEARS ENDED JUNE 30, 2011 2010 2009 2013 2012 2011 Residential $ 258,095 $ 246,041 $ 230,727 $ 311,214 $ 275,442 $ 258,095 Commercial 81,331 80,425 93,431 74,975 76,647 81,331 $ 339,426 $ 326,466 $ 324,158 $ 386,189 $ 352,089 $ 339,426 SUPPLEMENTARY QUARTERLY FINANCIAL INFORMATION– UNAUDITED (in thousands, except per share amounts) FOR THE QUARTER ENDED FOR THE QUARTER ENDED September 30 December 31 March 31 June 30 September 30 December 31 March 31 June 30 Fiscal 2011: Fiscal 2013: Net sales $ 87,230 $ 82,821 $ 85,175 $ 84,200 $ 91,237 $ 94,590 $ 98,351 $ 102,010 Gross margin 19,606 18,825 18,207 20,664 21,101 22,747 22,839 23,781 Net income 2,343 2,131 2,455 3,488 2,872 2,922 3,118 4,240 Earnings per share: Basic $ 0.35 $ 0.32 $ 0.37 $ 0.52 $ 0.41 $ 0.42 $ 0.44 $ 0.60 Diluted $ 0.34 $ 0.31 $ 0.35 $ 0.50 $ 0.40 $ 0.40 $ 0.42 $ 0.57 (in thousands, except per share amounts) FOR THE QUARTER ENDED September 30 December 31 March 31 June 30 FOR THE QUARTER ENDED Fiscal 2010: September 30 December 31 March 31 June 30 Fiscal 2012: Net sales $ 75,941 $ 83,524 $ 81,451 $ 85,550 $ 81,520 $ 85,001 $ 91,631 $ 93,936 Gross margin 16,556 20,041 18,033 20,151 18,964 20,458 22,098 23,759 Net income 1,380 2,964 2,320 4,137 2,378 2,948 3,343 4,399 Earnings per share: Basic $ 0.21 $ 0.45 $ 0.35 $ 0.62 $ 0.35 $ 0.44 $ 0.49 $ 0.64 Diluted $ 0.21 $ 0.45 $ 0.34 $ 0.61 $ 0.34 $ 0.42 $ 0.48 $ 0.61 Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure None. Item 9A. Controls and Procedures Evaluation of disclosure controls and procedures – Based on their evaluation as of the end of the period covered by this Annual Report on Form 10-K, the Company’s Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”) have concluded that the Company’s disclosure controls and procedures (as defined in Rules 13a-15(e) or 15d-15(e)) under the Securities Act of 1934, as amended) were effective as of June 30, Changes in internal control over financial reporting – During the Management’s Annual Report on Internal Control Over Financial Reporting – Management is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Rules 13a-15(f) or 15d-15(f) of the Securities Exchange Act of 1934, as amended. We performed an evaluation under the supervision and with the participation of our management, including the CEO and CFO, to assess the effectiveness of the design and operation of our disclosure controls and procedures under the Exchange Act as of June 30, Item 9B. Other Information None. PART III Item 10. Directors, Executive Officers and Corporate Governance The information contained in the Company’s The Company has adopted a code of ethics called theGuidelines for Business Conduct that applies to the Company’s employees, including the principal executive officer, principal financial officer, principal accounting officer or controller, and persons performing similar functions. A copy of the code of ethics is posted on our website at www.flexsteel.com. Item 11. Executive Compensation The information contained in the Company’s Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters The information contained in the Company’s Item 13. Certain Relationships and Related Transactions, and Director Independence Item 14. Principal Accountant Fees and Services 2011 2010 Audit Fees (1) $ 357,500 $ 376,000 Tax Fees (2) 15,000 — $ 372,500 $ 376,000 PART IV Item 15. Exhibits, Financial Statement Schedules, and Reports on Form 8-K (a) (1) Financial Statements The financial statements of the Company are set forth above in Item 8. (2) Schedules Description Balance at Additions Deductions Balance at Allowance for Doubtful Accounts: 2011 $ 2,020,000 $ 870,000 $ (890,000 ) $ 2,000,000 2010 $ 1,760,000 $ 920,000 $ (660,000 ) $ 2,020,000 2009 $ 2,110,000 $ 1,240,000 $ (1,590,000 ) $ 1,760,000 The following financial statement schedules for the years ended June 30, 2013, 2012 and 2011 are submitted herewith: SCHEDULE II VALUATION AND QUALIFYING ACCOUNTS For the Years Ended June 30, 2013, 2012 and 2011 (in thousands) Balance at (Additions) Reductions to Income Additions to (Deductions from) Balance at Accounts Receivable Allowances: 2013 $ 1,910 $ (215 ) $ (135 ) $ 1,560 2012 $ 2,000 $ (150 ) $ 60 $ 1,910 2011 $ 2,020 $ 870 $ (890 ) $ 2,000 Other schedules are omitted because they are not required or are not applicable or because the required information is included in the financial statements. (3) Exhibit No. 3.1 Amended and Restated Articles of Incorporation of the Company 3.2 Amended and Restated Bylaws of the Company 10.1 1995 Stock Option Plan 10.2 1999 Stock Option Plan 10.3 Flexsteel Industries, Inc. Voluntary Deferred Compensation Plan (incorporated by reference to Exhibit No. 10.5 to the Annual Report on Form 10-K for the fiscal year ended June 30, 2001). * 10.4 Flexsteel Industries, Inc. Restoration Retirement Plan (incorporated by reference to Exhibit No. 10.6 to the Annual Report on Form 10-K for the fiscal year ended June 30, 2001). * 10.5 Flexsteel Industries, Inc. Senior Officer Supplemental Retirement Plan (incorporated by reference to Exhibit No. 10.7 to the Annual Report on Form 10-K for the fiscal year ended June 30, 2001). * 10.6 2002 Stock Option Plan (incorporated by reference to Appendix A from the 2002 Flexsteel definitive proxy statement). * 10.7 Agreement and Plan of Merger, dated as of August 12, 2003, by and among Flexsteel, Churchill Acquisition Corp. and DMI (incorporated by reference to Exhibit 99(d)(1) of Flexsteel Industries, Inc.’s Tender Offer Statement on Schedule TO filed with the Securities and Exchange Commission on August 20, 2003). 10.8 Flexsteel Industries, Inc. 2006 Stock Option Plan (incorporated by reference to Appendix C from the 2006 Flexsteel Proxy Statement filed with the Securities and Exchange Commission on October 31, 2006). 10.9 Employment Agreement dated October 1, 2006 between Flexsteel Industries, Inc. and Donald D. Dreher (incorporated by reference to Exhibit 10.1 to Flexsteel’s Form 8-K filed with the Securities and Exchange Commission on October 5, 2006). * 10.10 Amendment to Employment Agreement dated June 27, 2008 between Flexsteel Industries, Inc. and Donald D. Dreher (incorporated by reference to Exhibit 10.3 to Flexsteel’s Form 8-K filed with the Securities and Exchange Commission on June 27, 2008).* 10.11 Flexsteel Industries, Inc. 2007 Long-Term Management Compensation Plan (incorporated by reference to Appendix C to the Definitive Proxy Statement on Schedule 14A filed with the Commission on November 1, 2007). * 10.12 2009 Stock Option Plan (incorporated by reference to Appendix A from the 2009 Flexsteel definitive proxy statement). * 10.13 Credit Agreement dated 10.14 Revolving Line of Credit Note dated April 14, 2010 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 8-K filed with the Securities and Exchange Commission on April 19, 2010). 10.15 First Amendment dated June 7, 2011 to Credit Agreement dated April 14, 2010 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 8-K filed with the Securities and Exchange Commission on June 9, 2011). Revolving Line of Credit Note dated June 7, 2011 between Flexsteel Industries, Inc. and Wells Fargo Bank, 10.17 Second Amendment dated May 11, 2012 to Credit Agreement dated April 14, 2010 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 10-Q for the period ended March 31, 2013 filed with the Securities and Exchange Commission on April 18, 2013). 10.18 Revolving Line of Credit Note dated May 11, 2012 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 10-Q for the period ended March 31, 2013 filed with the Securities and Exchange Commission on April 18, 2013). 10.19 Third Amendment dated June 28, 2013 to Credit Agreement dated April 14, 2010 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 8-K filed with the Securities and Exchange Commission on July 5, 2013). 10.20 Revolving Line of Credit Note dated June 28, 2013 between Flexsteel Industries, Inc. and Wells Fargo Bank, N.A. (incorporated by reference to Form 8-K filed with the Securities and Exchange Commission on July 5, 2013). 10.21 One-Year Incentive Compensation Award for Karel K. Czanderna, dated July 1, 2012 (incorporated by reference to Exhibit 4.1 of Flexsteel’s Form S-8 filed with the Securities and Exchange Commission on August 20, 2012.)* 10.22 Restricted Stock Unit Award Agreement for Karel K. Czanderna, dated July 1, 2012 (incorporated by reference to Exhibit 4.1 of Flexsteel’s Form S-8 filed with the Securities and Exchange Commission on August 20, 2012.)* 21.1 Subsidiaries of the Company. Filed herewith. 23 Consent of Independent Registered Public Accounting Firm. Filed herewith. 31.1 Certification. Filed herewith. 31.2 Certification. Filed herewith. 32 Certification by Chief Executive Officer and Chief Financial Officer Pursuant to 18 U.S.C. Section 1350 as Adopted Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. Filed herewith. 101.INS XBRL Instance Document. 101.SCH XBRL Taxonomy Extension Schema Document. 101.CAL XBRL Taxonomy Extension Calculation Linkbase Document. 101.LAB XBRL Taxonomy Extension Labels Linkbase Document. 101.DEF XBRL Taxonomy Extension Definition Linkbase Document. 101.PRE XBRL Taxonomy Extension Presentation Linkbase Document. *Management contracts, compensatory plans and arrangements required to be filed as an exhibit to this report. SIGNATURES Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized. Date: August FLEXSTEEL INDUSTRIES, INC. By: /S/ Chief Executive Officer and Principal Executive Officer By: /S/ Timothy E. Hall Timothy E. Hall Chief Financial Officer and Principal Financial and Accounting Officer Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated. Date: August /S/ Chairman of the Board of Directors Date: August /S/ Karel K. Czanderna �� Karel K. Czanderna Director Date: August 23, 2013 /S/ Jeffrey T. Bertsch Jeffrey T. Bertsch Director Date: August 23, 2013 /S/ Mary C. Bottie Mary C. Bottie Director Date: August 23, 2013 /S/ Patrick M. Crahan Patrick M. Crahan Director Date: August 23, 2013 /S/ Robert E. Deignan Robert E. Deignan Director Date: August 23, 2013 /S/ Thomas M. Levine Thomas M. Levine Director Date: August 23, 2013 /S/ Ronald J. Klosterman Ronald J. Klosterman Director Date: August /S/ Robert J. Maricich Robert J. Maricich Director Date: August /S/ Eric S. Rangen Eric S. Rangen Director Date: August /S/ James R. Richardson James R. Richardson Director Date: August /S/ Nancy E. Uridil Nancy E. Uridil Director 33o Accelerated filero Non-accelerated fileroSmaller reporting companyx20102012 (which was the last business day of the registrant’s most recently completed second quarter) was $74,061,443.$96,762,452.6,715,6127,107,723 Common Shares ($1 par value) as of August 15, 2011.9, 2013.

In Part III, portions of the registrant’s 20112013 Proxy Statement to be filed with the Securities and Exchange Commission within 120 days of the Registrant’s fiscal year end.

Flexsteel Industries, Inc. and Subsidiaries (the “Company”) was incorporated in 1929 and is one of the oldest and largest manufacturers, importersmanufacturer, importer and marketersmarketer of residential and commercial upholstered and woodenwood furniture products in the United States. Product offerings include a wide variety of upholstered and wood furniture such as sofas, loveseats, chairs, reclining and rocker-reclining chairs, swivel rockers, sofa beds, convertible bedding units, occasional tables, desks, dining tables and chairs and bedroom furniture. The Company’s products are intended for use in home, office, hotel, healthcare and other commercial applications. Featured as a basicA featured component in most of the upholstered furniture is a unique steel drop-in seat spring from which our name “Flexsteel” is derived. The Company distributes its products throughout the United States through the Company’s sales force and various independent representatives. The Company’s products are also sold to several national and regional chains, some of which sell on a private label basis. No single customer accounted for more than 10% of net sales.furniture with warehouses in Indiana and manufacturing sources in Asia;furniture. DMI’s divisionsbrands are WYNWOOD, HomestylesHome Styles and DMI Commercial Office Furniture. operating segment, furniture products. Our furniture products business involves the distribution of manufactured and imported products consisting of a broad line of upholstered and wooden furniture for residential and commercial markets. Set forth below is information for the past three fiscal years showing the Company’s net sales attributable to each of the areas of application (in thousands):application: We operate manufacturing facilities that are located in Arkansas, California, Georgia, Iowa, Mississippi and Juarez, Mexico. These manufacturing operations are integral to our product offerings and distribution strategy by offering smaller and more frequent product runs of a wider product selection. We identify and eliminate manufacturing inefficiencies and adjust manufacturing schedules on a daily basis to meet customer requirements. We have established relationships with key suppliers to ensure prompt delivery of quality component parts. Our production includes the use of selected offshore component parts to enhance our product quality and value in the marketplace.

The furniture industry is highly competitive and includes a large number of U.S. and foreign manufacturers and distributors, none of which dominates the market. Our competition includes foreign manufacturers, in countries such as China, and customers who obtain products directly from foreign manufacturers. The markets in which we compete include a large number of relatively small manufacturers; however, certain competitors have substantially greater sales volumes than we have. Our products compete based on style, quality, price, delivery, service and durability. We believe that our manufacturing and sourcing capabilities, facility locations, commitment to customers, product quality, delivery, service and value and experienced production, sales, marketing and management teams, aided by offshore sourced components and finished product, are our competitive advantages.

The Company’s business is not considered seasonal.

The Company makes minimal export sales. At June 30, 2011,2013, the Company had approximately 90 employees located in Asia to inspect and coordinate the delivery of purchased products.

The approximate backlog of customer orders believed to be firm as of the end of the current fiscal year and the prior two fiscal years were as follows (in thousands):

The Company utilizes various types of wood, fabrics, leathers, upholsteredfabric, leather, filling material, high carbon spring steel, bar and wire stock, polyurethane and other raw materials in manufacturing furniture. While the Company purchases these materials from numerous outside suppliers, both U.S. and foreign, it is not dependent upon any single source of supply. The costs of certain raw materials fluctuate, but all continue to be readily available.

For a discussion of the Company’s working capital practices, see “Liquidity and Capital Resources” in Item 7 of this Annual Report on Form 10-K.

The Company has exposure to actions by governments, including tariffs, see “Risk Factors” in Item 1A of this Annual Report on Form 10-K.

The Company is subject to various local, state, and federal laws, regulations and agencies that affect businesses generally, see “Risk Factors” in Item 1A of this Annual Report on Form 10-K.

The Company is subject to environmental laws and regulations with respect to product content and industrial waste, see “Risk Factors” in Item 1A and “Legal Proceedings” in Item 3 of this Annual Report on Form 10-K.

The Company owns the American and Canadian improvement patents to its Flexsteel seat spring, as well as patents on convertible beds. The Company has patents and owns certain trademarks in connection with its furniture products, which are due to expire on dates ranging from 20112013 to 2025.2026. The Company does not consider its trademarks and patents material to its business.independentthird-party designers. New models and designs of furniture, as well as new fabrics, are introduced continuously. In the last three fiscal years, these design activities involved the following expenditures (in thousands):

The Company had 1,3001,360 employees as of June 30, 20112013, including 250285 employees that are covered by collective bargaining agreements. Management believes it has good relations with employees.

Our website is located atwww.flexsteel.com. www.flexsteel.com. Information on the website does not constitute part of this Annual Report on Form 10-K.such as the California Transparency in Supply Chains Act of 2010, Patient Protection and Affordable Care Act of 2010, the Pension Protection Act of 2006, the Lacey Act, as amended in 2008 to cover plants and trees, the Consumer Product Safety Improvement Act of 2008, the Security and Accountability for Every (SAFE) Port Act of 2006 and the Maritime Transportation Security Act of 2002 as well as many others. Partially in response to the financial markets crises and the global economic recession, regulatory initiatives have accelerated. These initiativeswhich could have a significant impact on our operations and the cost to comply with such laws and regulations could adversely impact our financial position, results of operations and cash flows. In addition, failure to comply with such laws and regulations, even inadvertently, could produce negative consequences which could adversely impact our operations.1,3001,360 people, 250285 of whom are covered by collective bargaining agreements. Terms of collective bargaining agreements that prevent us from competing effectively could adversely affect our financial condition, results of operations and cash flows. We are committed to working with those groups to avert or resolve conflicts as they arise. However, there can be no assurance that these efforts will be successful.200215 of our union employees. Multi-employer pension plans are managed by trustee boards comprised of participating employer and labor union representatives, and the employers participating in a multi-employer pension plan are jointly responsible for maintaining the plan’s funding requirements. Based on the most recent information available to us, we believe that the present value of actuarially accrued liabilities in the multi-employer pension plans substantially exceeds the value of the assets held in trust to pay benefits. As a result of our participation, we could experience greater volatility in our overall pension funding obligations. Our obligations may be impacted by the funded status of the plans, the plans’ investment performance, changes in the participant demographics, financial stability of contributing employers and changes in actuarial assumptions.environment and weenvironment. We could incur substantial costs, including legal expenses, as a result of the noncompliance with, or liability for cleanup or other costs or damages under, environmental laws. See Note 11, “Litigation” within the Notes to Consolidated Financial Statements for a description of an existing environmental claim against the Company. Additionally, the Company is involved in various other kinds of commercial disputes. Given the inherent uncertainty of litigation, these various legal proceedings and compliance matters could have a material impact on our business, operating results or financial condition. None.2011:2013:Approximate

Size (square feet)Dubuque, IowaHarrison, Arkansas719,000 Distribution and Corporate OfficesLancaster, Pennsylvania216,000Distribution236,000305,00069,000DistributionManufacturingHarrison, Arkansas221,000ManufacturingStarkville, Mississippi349,000691,000719,0002011:2013:Approximate