Table of Contents

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

|

Washington, D.C. 20549

|

|

Form 10-K

Table of Contents |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange

Act of 1934 for the fiscal year ended July 31, 20112013 or

☐o Transition Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934

for the transition period from __________ to __________

Commission File Number: 1-7891

DONALDSON COMPANY, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 41-0222640 |

DONALDSON COMPANY, INC.

|

(Exact name of registrant as specified in its charter)

|

| | | | | |

Delaware

| 41-0222640

|

(State or other jurisdiction of | (I.R.S. Employer

|

incorporation or organization)

| (I.R.S. Employer

Identification No.) |

| | | | | |

| |

1400 West 94th Street,

Minneapolis, Minnesota | 55431 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (952) 887-3131

Securities registered pursuant to Section 12(b) of the Act:

| | | | | |

| Title of each class | | | Name of each exchange

on which registered | |

Common Stock, $5 Par Value | New York Stock Exchange |

Preferred Stock Purchase Rights | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.x☒ Yeso☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.o☐ Yesx☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.x☒ Yeso☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such short period that the registrant was required to submit and post such files)x☒ Yeso☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| |

Large accelerated filerx☒ | Accelerated filero☐ |

| |

Non-accelerated filero☐ | Smaller reporting companyo

|

| |

(Do(Do not check if a smaller reporting company)

| Smaller reporting company ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

o☐ Yesx☒ No

As of January 28, 2011,31, 2013, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant was $4,424,036,897$5,466,451,890 (based on the closing price of $58.04$37.61 as reported on the New York Stock Exchange as of that date).

As of August 31, 2011,2013, there were approximately 74,522,228146,109,145 shares of the registrant’s common stock outstanding.

Documents Incorporated by Reference

Portions of the registrant’s Proxy Statement for its 20112013 annual meeting of stockholders (the “2011“2013 Proxy Statement”) are incorporated by reference in Part III, as specifically set forth in Part III.

DONALDSON COMPANY, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

Table of Contents

PART I

Item 1. Business

General

Donaldson Company, Inc. (“Donaldson”(Donaldson or the “Company”)Company) was founded in 1915 and organized in its present corporate form under the laws of the State of Delaware in 1936.

The Company is a worldwide manufacturer of filtration systems and replacement parts. The Company’s product mix includes air and liquid filtration systems and exhaust and emission control products. Products are manufactured at 39 plants around the world and through three3 joint ventures. The Company has two reporting segments: Engine Products and Industrial Products. Products in the Engine Products segment consist of air filtration systems, exhaust and emissions systems, liquid filtration systems, and replacement filters. The Engine Products segment sells to original equipment manufacturers (“OEMs”)(OEMs) in the construction, mining, agriculture, aerospace, defense, and truck markets and to OEM dealer networks, independent distributors, private label accounts, and large equipment fleets. Products in the Industrial Products segment consist of dust, fume, and mist collectors, compressed air purification systems, air filtration systems for gas turbines, PTFE membrane-based products, and specialized air filtration systems for applications including computer hard disk drives.drives and semi-conductor manufacturing. The Industrial Products segment sells to various industrial dealers, distributors, and end-users, OEMs of gas-fired turbines, and OEMs and end-users requiring clean air.

The table below shows the percentage of total net sales contributed by the principal classes of similar products for each of the last three fiscal years:

| | | | | | | | | | | |

| | Year Ended July 31, | | | Year Ended July 31, | |

| | 2011 | | 2010 | | 2009 | | | 2013 | | | 2012 | | | 2011 | |

Engine Products segment | | | | | | | | | | | | | | | | | | | |

Off-Road Products | | 14 | % | | 12 | % | | 13 | % | | | 15% | | | | 15% | | | | 14% | |

Aerospace and Defense Products | | 5 | % | | 6 | % | | 6 | % | |

On-Road Products | | 5 | % | | 4 | % | | 4 | % | | | 5% | | | | 7% | | | | 5% | |

Aftermarket Products* | | 38 | % | | 37 | % | | 30 | % | | | 37% | | | | 36% | | | | 38% | |

Retrofit Emissions Products | | 1 | % | | 1 | % | | 2 | % | | | 1% | | | | 1% | | | | 1% | |

*includes replacement part sales to the Company’s OEMs customers | | | | | | | | |

| | | | | | | | |

| Aerospace and Defense Products | | | | 4% | | | | 4% | | | | 5% | |

| *includes replacement part sales to the Company’s OEM Customers | | | | | | | | | | | | | |

Industrial Products segment | | | | | | | | | | | | | | | | | | | |

Industrial Filtration Solutions Products | | 22 | % | | 22 | % | | 26 | % | | | 22% | | | | 22% | | | | 22% | |

Gas Turbine Products | | 7 | % | | 8 | % | | 11 | % | | | 9% | | | | 7% | | | | 7% | |

Special Applications Products | | 8 | % | | 10 | % | | 8 | % | | | 7% | | | | 8% | | | | 8% | |

FinancialTotal net sales contributed by the principal classes of similar products and financial information about segment operations appearsappear in Note KL in the Notes to Consolidated Financial Statements on page 49.53.

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and amendments to those reports, available free of charge through its website at www.donaldson.com, as soon as reasonably practicable after it electronically files such material with (or furnishes such material to) the Securities and Exchange Commission. Also available on the Company’s website are corporate governance documents, including the Company’s code of business conduct and ethics, corporate governance guidelines, Audit Committee charter, Human Resources Committee charter, and Corporate Governance Committee charter. These documents are also available in print, free of charge to any shareholder who requests them. The information contained on the Company’s website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered to be part of this Form 10-K.

Seasonality

A number of the Company’s end markets are dependent on the construction, agricultural, and power generation industries, which are generally stronger in the second half of the Company’s fiscal year. The first two quarters of the fiscal year also contain the traditional summer and winter holiday periods, which are characterized by more Customer plant closures.

Table of Contents

Competition

Principal methods of competition in both the Engine and Industrial Products segments are technology and innovation, price, geographic coverage, service, and product performance. The Company competes in a number of highly competitive filtration markets in both segments. The Company believes it is a market leader withwithin many of its product lines. The Company believeslines, specifically within the Engine Products segment it is a market leader in its Off-Road Equipment and On-Road Products lines for OEMs and is a significant participant in the aftermarket for replacement filters. The Engine Products segment’s principal competitors include several large global competitors and many regional competitors, especially in the Engine Aftermarket Products business. The Industrial Products segment’s principal competitors vary from country to country and include several large regional and global competitors and a significant number of smaller competitors who compete in a specific geographical region or in a limited number of product applications.

Raw Materials

The principal raw materials that the Company uses are steel, filter media, and plastics. Commodity prices generally increased throughoutpetroleum-based products. Purchased raw materials represent approximately 60 to 65 percent of the year, butCompany’s cost of goods sold. Of that amount, steel, including fabricated parts, represents approximately 25 percent. Filter media represents approximately 15 to 20 percent and the impact was moderated by certain long term supply contracts. The Company anticipates a further impact from rising commodity prices in Fiscal 2012, as compared to Fiscal 2011, specifically for steelremainder is primarily made up of petroleum-based products and media, as these supply contracts expired during the latter half of Fiscal 2011. The Company experienced no significant supply problems in the purchase of its major raw materials.other components. The Company typically has multiple sources of supply for the raw materials essential to its business, andbut does rely primarily on two media suppliers. The Company is not required to carry significant amounts of raw material inventory to secure supplier allotments. However, the Company does stock finished goods inventory at its regional distribution centers in order to meet anticipated Customer demand. The Company has not experienced significant supply problems in the purchase of its major raw materials.

Patents and Trademarks

The Company owns various patents and trademarks, which it considers in the aggregate to constitute a valuable asset, including patents and trademarks for products sold under the Ultra-Web®, PowerCore®, and Donaldson® trademarks. However, it does not regard the validity of any one patent or trademark as being of material importance.

Major Customers

There were no Customers that accounted for over 10 percent of net sales in Fiscal 2011, 20102013, 2012, or 2009.2011. There were no Customers that accounted for over 10 percent of gross accounts receivable in Fiscal 2011 or 2010.2013 and one Customer over 10 percent of gross accounts receivable in Fiscal 2012.

Backlog

At August 31, 2011,2013, the backlog of orders expected to be delivered within 90 days was $423.8$351.7 million. All of thisThis entire backlog is expected to be shipped during Fiscal 2012.2014. The 90-day backlog at August 31, 2010,2012, was $361.1$403.7 million. Backlog is one of many indicators of business conditions in the Company’s markets. However, it is not always indicative of future results for a number of reasons, including short lead times in the Company’s replacement parts businesses and the timing of orders in many of the Company’s Engine OEM and Industrial markets.

Research and Development

During Fiscal 2011,2013, the Company spent $55.3$62.6 million on research and development activities. Research and development expenses include basic scientific research and the application of scientific advances to the development of new and improved products and their uses. The Company spent $44.5$59.6 million and $40.6$55.3 million in Fiscal 20102012 and Fiscal 2009,2011, respectively, on research and development activities. Substantially all commercial research and development is performed in-house.

Environmental Matters

The Company does not anticipate any material effect on its capital expenditures, earnings, or competitive position during Fiscal 20122014 due to compliance with government regulations regulating the discharge of materials into the environment or otherwise relating to the protection of the environment.

Employees

The Company employed over 13,00012,400 persons in worldwide operations as of August 31, 2011.2013.

Geographic Areas

Financial information about geographic areas appears in Note KL of the Notes to Consolidated Financial Statements on page 49.53.

Table of Contents

Item 1A. Risk Factors

There are inherent risks and uncertainties associated with our global operations that involve the manufacturing and sale of products for highly demanding Customer applications throughout the world. These risks and uncertainties could adversely affect our operating performance and financial condition. The following discussion, along with discussions elsewhere in this report, outlines the risks and uncertainties that we believe are the most material to our business. In light of the global economic slowdown in recent years and the continued uncertainty, webusiness at this time. We want to further highlight the risks and uncertainties associated with: world economic factors and conditions, the ongoing global economic uncertainty, that is impacting many regionsthe reduced demand for hard disk drive products with the increased use of the world, the financial condition of our suppliers and Customers,flash memory, the potential for some Customers to increase their reliance on their own filtration capabilities, currency fluctuations, commodity prices, political factors, the Company’sour international operations, the possible reduced demand for hard disk drive products with the increased use of flash memory, highly competitive markets, inability to hire and retain key employees, governmental laws and regulations, including the impact of the various economic stimulus and financial reform measures, being implemented by governments around the world, the implementation of our new information technology systems, failure or breach of information technology and trade secret security, potential global events resulting in market instability, and unpredictability in the world’s markets, including financial bailouts and defaults of sovereign nations, political changes, military and terrorist activities including political unrest in the Middle East, other political changes, health outbreaks, natural disasters, and other factors discussed below. The Company undertakesWe undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Operating internationally carries risks which could negatively affect our financial performance.

We have sales and manufacturing operations throughout the world, with the heaviest concentrations in North America,the Americas, Europe, and Asia. Our stability, growth, and profitability are subject to a number of risks of doing business internationally that could harm our business, including:

| · | |

| •

| political and military events, |

| · | |

| •

| legal and regulatory requirements, including import, export, defense regulations, anti-corruption laws, and foreign exchange controls, |

| · | |

| •

| tariffs and trade barriers, |

| · | |

| •

| potential difficulties in staffing and managing local operations, |

| · | |

| •

| credit risk of local Customers and distributors, |

| · | |

| •

| difficulties in protecting intellectual property, |

| · | |

| •

| local economic, political, and social conditions, specifically in the Middle East, China, Thailand, and Thailandother emerging markets where we have significant investments and do business, |

| · | |

| •

| potential global health outbreaks. outbreaks, and |

Due to the international scope of our operations, we are subject to a complex system of import- and export-related laws and regulations. Any alleged or actual violations may subject us to government scrutiny, investigation, and civil and criminal penalties, and may limit our ability to import or export our products or to provide services outside the United States (U.S.). In addition, the U.S. Foreign Corrupt Practices Act and similar foreign anti-corruption laws generally prohibit companies and their intermediaries from making improper payments or providing anything of value to improperly influence foreign government officials for the purpose of obtaining or retaining business, or obtaining an unfair advantage. Recent years have seen a substantial increase in the global enforcement of anti-corruption laws. Violations of these laws may result in severe criminal or civil sanctions, could disrupt our business, and result in an adverse effect on our reputation, business, and results of operations or financial condition.

Maintaining a competitive advantage requires continuing investment with uncertain returns.

We operate in highly competitive markets and have numerous competitors who may already be well-established in those markets. We expect our competitors to continue improving the design and performance of their products and to introduce new products that could be competitive in both price and performance. We believe that we have certain technological advantages over our competitors, but maintaining these advantages requires us to continually invest in research and development, sales and marketing, and Customer service and support. There is no guarantee that we will be successful in maintaining these advantages. We make investments in new technologies that address increased performance and regulatory requirements around the globe. There is no guarantee that we will be successful in completing development or achieving sales of these products or that the margins on such products will be acceptable. Our financial performance may be negatively impacted if a competitor’s successful product innovation reaches the market before ours or gains broader market acceptance.

A few of our major OEM Customers also manufacture filtration systems. Although these OEM Customers rely on us and other suppliers for some of their filtration systems, they sometimes choose to manufacture additional filtration systems for their own use. There is also a risk that a Customer could acquire one or more of our competitors.

Table of Contents

We may be adversely impacted by changes in technology that could reduce or eliminate the demand for our products. These risks include:

| · | |

| •

| breakthroughs in technology which provide a viable alternative to diesel engines and |

| · | |

| •

| reduced demand for disk drive products by flash memory or a similar technology, which would reduce the use of disk drives and therefore eliminate the need for our filtration solutions in disk drives. drives |

| · | other breakthroughs in filtration technologies that could displace our products |

Difficulties with our information technology systems and security could adversely affect our results.

We have many information technology systems that are important to the operation of its businesses, some of which are managed by third parties. These systems are used to process, transmit, and store electronic information, and to manage or support a variety of business processes and activities. We could encounter difficulties in developing new systems, maintaining and upgrading existing systems, and preventing information security breaches. There may be other challenges and risks as we upgrade and standardize our Enterprise Resource Planning (ERP) system on a worldwide basis. Such difficulties could lead to significant additional expenses and/or disruption in business operations that could adversely affect our results. Additionally, information technology security threats are increasing in frequency and sophistication. These threats pose a risk to the security of our systems and networks and the confidentiality, availability, and integrity of our data. Should such an attack succeed, it could lead to the compromising of confidential information, manipulation and destruction of data, defective products, production downtimes, and operations disruptions. The occurrence of any of these events could adversely affect our reputation, and could result in litigation, regulatory action, potential liability, and increased costs and operational consequences of implementing further data protection matters.

Demand for our products relies on economic and industrial conditions worldwide.

Changes in economic or industrial conditions could impact ourresults of operations or financial condition in any particular period as our business can be sensitive to varying conditions by region across the globe.

While sales to Caterpillar accounted for slightly less than 10 percent of our net sales in Fiscal 2013, 2012, and 2011, an adverse change in Caterpillar’s financial performance or a material reduction in our sales to Caterpillar could negatively impact our operating results.

We participate in highly competitive markets with pricing pressure. If we are not able to compete effectively our margins and results of operations could be adversely affected.

The businesses and product lines in which we participate are very competitive and we risk losing business based on a wide range of factors including technology, price, geographic coverage, product performance, and Customer service. Large Customers continue to seek productivity gains and lower prices from us and their other suppliers. We may lose business or negatively impact our margins if we are unable to deliver the best value to our Customers.

Demand for our products relies on economic and industrial conditions worldwide.

Demand for our products tends to respond to varying levels of economic, construction, agricultural, mining, and industrial activity in the United States and in other industrialized nations.

Sales to Caterpillar accounted for slightly less than 10 percent of our net sales in Fiscal 2011, 2010 and 2009. An adverse change in Caterpillar’s financial performance or a material reduction in our sales to Caterpillar could negatively impact our operating results.

Changes in our product mix impacts our financial performance.

We sell products that have varying profit margins. Our financial performance can be impacted depending on the mix of products we sell during a given period.Our outlook assumes a certain geographic mix of sales as well as a product mix of sales. If actual results vary from this projected geographic and product mix of sales, our results could be negatively impacted.

Unavailable or higher cost materials could impact our financial performance.

We obtain raw materials including steel, filter media, plastics,petroleum-based products, and other components from third-party suppliers and tend to carry limited raw material inventories. An unanticipated delay in delivery by our suppliers could result in the inability to deliver on-time and meet the expectations of our Customers. This could negatively affect our financial performance. An increase in commodity prices could also result in lower operating margins.

Difficulties with the Company’s information technology systems could adversely affect our results.

The Company has many information technology systems that are important to the operation of its businesses. The Company could encounter difficulties in developing new systems or maintaining and upgrading existing systems. Such difficulties could lead to significant expenses due to disruption in business operations and could adversely affect the Company’s results.

Unfavorable fluctuations in foreign currency exchange rates could negatively impact our results and financial position.

We have operations in many countries. Each of our subsidiaries reports its results of operations and financial position in its relevant foreignfunctional currency, which is then translated into U.S. dollars. This translated financial information is included in our consolidated financial statements. The strengthening of the U.S. dollar in comparison to the foreign currencies of our subsidiaries could have a negative impact on our results and financial position.

Acquisitions may have an impact on our results.

We have made and continue to pursue acquisitions. We cannot guarantee that these acquisitions will have a positive impact on our results. These acquisitions could negatively impact our profitability due to operating and integration inefficiencies, the incurrence of debt, contingent liabilities, and amortization expenses related to intangible assets. There are also a number of other risks involved in acquisitions. We could lose key existing Customers, have difficulties in assimilating the acquired operations, assume unanticipated legal liabilities, or lose key employees.

ComplianceCosts associated with environmental and product laws and regulations can be costly.lawsuits or investigations may have an adverse effect on our results of operations.

We are subject to many environmental laws and regulations in the jurisdictions in which we operate. We routinely incur costs in order to comply with these laws and regulations. We may be adversely impacted by new or changing laws and regulations that affect both our operations and our ability to develop and sell products that meet our Customers’ requirements. We are involved in various product liability, product warranty, intellectual property, environmental claims, and other legal proceedings that arise in and outside of the ordinary course of our business. It is not possible to predict the outcome of investigations and lawsuits, and we could incur judgments, fines, or penalties or enter into settlements of lawsuits and claims that could have an adverse effect on our business, results of operations, and financial condition in any particular period.

Additional tax expense or tax exposure could impact our financial performance.

We are subject to income taxes in various jurisdictions in which we operate. Our tax liabilities are dependent upon the location of Contents

earnings among these different jurisdictions. Our provision for income taxes and cash tax liability could be adversely affected by numerous factors, including income before taxes being lower than anticipated in countries with lower statutory tax rates and higher than anticipated in countries with higher statutory tax rates, changes in the valuation of deferred tax assets and liabilities, and changes in tax laws and regulations. We are also subject to the continuous examination of our income tax returns tax authorities. The results of audit and examination of previously filed tax returns and continuing assessments of our tax exposures may have an adverse effect on the Company’s provision for income taxes and cash tax liability.

Compliance with environmental and product laws and regulations can be costly.

We are subject to many environmental and product laws and regulations in the jurisdiction we operate. We routinely incur costs in order to comply with these laws and regulations. We may be adversely impacted by new or changing laws and regulations that affect both our operations and our ability to develop and sell products that meet our Customers’ requirements.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company’s principal administrative office and research facilities are located in Bloomington, a suburb of Minneapolis, Minnesota. The Company’s principal European administrative and engineering offices are located in Leuven, Belgium. The Company also has extensive operations in the Asia-Pacific region.

The Company’s principal manufacturing and distribution activities are located throughout the world. The following is a summary of the principal plants and other materially important physical properties owned or leased by the Company.

| Americas | |

Americas

| Europe / Middle East / Africa |

Auburn, Alabama (E) | Kadan, Czech Republic (I) |

Riverbank, California (I)* | Klasterec, Czech Republic |

Valencia, California (E)* | Domjean, France (E) |

Dixon, Illinois | Paris, France (E)* |

Frankfort, Indiana | Dulmen, Germany (E) |

Cresco, Iowa | Flensburg,Haan, Germany (I)

|

Grinnell, Iowa (E) | Haan, Germany (I)

Ostiglia, Italy (E) |

Nicholasville, Kentucky | Ostiglia, Italy

|

Bloomington, Minnesota

| Cape Town, South Africa |

Chillicothe, Missouri (E)

Bloomington, Minnesota | Johannesburg, South Africa* |

Chesterfield, Missouri (E)* | Hull, United Kingdom |

Philadelphia, Pennsylvania (I)

Chillicothe, Missouri (E) | Leicester, United Kingdom (I) |

Greeneville, Tennessee

Philadelphia, Pennsylvania (I) | |

Baldwin, Wisconsin

Greeneville, Tennessee | Australia |

Baldwin, Wisconsin | Wyong, Australia |

| Stevens Point, Wisconsin | Wyong, Australia

|

Sao Paulo, Brazil (E)* | Asia |

Brockville, Canada (I)(E)* | Asia

Wuxi, China |

Aguascalientes, Mexico | Hong Kong, China*

New Delhi, India |

Monterrey, Mexico (I) | Wuxi, China

Gunma, Japan |

| New Delhi, India

Rayong, Thailand (I) |

Joint Venture Facilities | Gunma, Japan

Third-Party Logistics Providers |

Champaign, Illinois (E) | Rayong, Thailand (I)

Santiago, Chile |

Jakarta, Indonesia | Wuxi, China |

Dammam, Saudi Arabia (I) | Third-Party Logistics Providers

Mumbai, India |

| Santiago, Chile

Chennai, India |

Distribution Centers | Wuxi, China

|

Wyong, Australia

| Mumbai, India

|

Brugge, Belgium

| Plainfield, Indiana (I) |

Rensselaer, Indiana

Wyong, Australia | Gunma, Japan |

Ostiglia, Italy

Brugge, Belgium | Singapore |

Aguascalientes, Mexico

Sao Paulo, Brazil* | Greeneville, Tennessee (I) |

Johannesburg, South Africa

Rensselaer, Indiana | |

| Jakarta, Indonesia | |

| Aguascalientes, Mexico | |

The Company’s properties are utilized for both the Engine and Industrial Products segments except as indicated with an (E) for Engine or (I) for Industrial. The Company leases certain of its facilities, primarily under long-term leases. The facilities denoted with an asterisk (*) are leased facilities. In Wuxi, China, and Bloomington, Minnesota a portion of the activities are conducted in leased facilities. The Company uses third-party logistics providers for some of its product distribution and neither leases nor owns the facilities. The Company considers its properties to be suitable for their present purposes, well-maintained, and in good operating condition.

Table of Contents

Item 3. Legal Proceedings

The Company records provisions with respect to identified claims or lawsuits when it is probable that a liability has been incurred and the amount of the loss can be reasonably estimated. Claims and lawsuits are reviewed quarterly and provisions are taken or adjusted to reflect the status of a particular matter. The Company believes the recorded reserves in its consolidated financial statements are adequate in light of the probable and estimable outcomes. Any recorded liabilities were not material to the Company’s financial position, results of operationoperations or liquidity, and the Company does not believe that any of the currently identified claims or litigation will materially affect its financial position, results of operation or liquidity.

The Company has reached a preliminary agreement to settle the class action lawsuits that were previously disclosed in its SEC filings, including most recently the Form 10-Q for the quarter ending April 30, 2011. On March 31, 2008, S&E Quick Lube, a filter distributor, filed a lawsuit alleging that 12 filter manufacturers, including the Company, engaged in a conspiracy to fix prices, rig bids, and allocate U.S. Customers for aftermarket automotive filters. The U.S. cases have been consolidated into a single multi-district litigation in the Northern District of Illinois. The Company denies any liability and has vigorously defended the claims raised in these lawsuits. The settlement will fully resolve all claims brought against the Company in the lawsuits and the Company does not admit any liability or wrongdoing. The settlement is still subject to Court approval and will not have a material impact on the Company’s financial position, results of operations or liquidity.

The Company has reached a preliminary agreement with the Air Resources Board for the State of California (“ARB”) to settle regulatory claims brought by ARB in connection with the sales of our Diesel Multi-Stage Filter System (“DMF”) for an immaterial amount. On May 19, 2010, ARB revoked its verification of the Company’s DMF for use with on-road diesel engines, for which verification was originally issued on December 16, 2005. The Company denies that any sales were made in California without ARB verification. The Company is not currently selling any DMF product and is working with the Environmental Protection Agency to verify the product for any future sales.

Item 4. (Removed and Reserved)Mine Safety Disclosures

Not applicable.

Executive Officers of the Registrant

Current information regarding executive officers is presented below. All terms of office are for one year. There are no arrangements or understandings between individual officers and any other person pursuant to which the officer was selected as an executive officer.

| | | | | | | |

Name | | Age | | Positions and Offices Held | | First Fiscal Year

Appointed as an

Executive Officer | | Age | | Positions and Offices Held | | First Fiscal Year

Appointed as an

Executive Officer |

Tod E. Carpenter | Tod E. Carpenter | | 52 | | Vice President, Europe and Middle East | | 2008 | | 54 | | Senior Vice President, Engine Products | | 2008 |

| | | | | |

William M. Cook | William M. Cook | | 58 | | Chairman, President and Chief Executive Officer | | 1994 | | 60 | | Chairman, President and Chief Executive Officer | | 1994 |

| | | | | |

Sandra N. Joppa | Sandra N. Joppa | | 46 | | Vice President, Human Resources | | 2005 | | 48 | | Vice President, Human Resources | | 2006 |

| | | | | |

Norman C. Linnell | Norman C. Linnell | | 52 | | Vice President, General Counsel and Secretary | | 1996 | | 54 | | Vice President, General Counsel and Secretary | | 1996 |

| | | | | |

Charles J. McMurray | Charles J. McMurray | | 57 | | Senior Vice President, Industrial Products | | 2003 | | 59 | | Senior Vice President, Chief Administrative Officer | | 2003 |

| | | | | |

Mary Lynne Perushek | Mary Lynne Perushek | | 53 | | Vice President and Chief Information Officer | | 2006 | | 55 | | Vice President and Chief Information Officer | | 2007 |

| | | | | |

David W. Timm | | 58 | | Vice President, Asia-Pacific | | 2007 | |

| | | | | |

Thomas R. VerHage | | 58 | | Vice President and Chief Financial Officer | | 2004 | |

| | | | | |

| James F. Shaw | | | 44 | | Vice President and Chief Financial Officer | | 2012 |

| Wim Vermeersch | | | 47 | | Vice President, Europe and Middle East | | 2012 |

Jay L. Ward | Jay L. Ward | | 47 | | Senior Vice President, Engine Products | | 2006 | | 49 | | Senior Vice President, Industrial Products | | 2006 |

| | | | | |

Debra L. Wilfong | | 56 | | Vice President and Chief Technology Officer | | 2007 | |

| | | | | |

| Eugene X. Wu | | | 45 | | Vice President, Asia Pacific | | 2012 |

Mr. Carpenter joined the Company in 1996 and has held various positions, including Gas Turbine Systems General Manager from 2002 to 2004; General Manager, Industrial Filtration Systems (“IFS’)(IFS) Sales from 2004 to 2006; General Manager, IFS Americas in 2006; and Vice President, Global IFS from 2006 to 2008. Mr. Carpenter was appointed2008; and Vice President, Europe and Middle East in August 2008.from 2008 to 2011. In October 2011, Mr. Carpenter has beenwas appointed Senior Vice President, Engine Products, effective October 1, 2011.Products.

Mr. Cook joined the Company in 1980 and has held various positions, including CFO and Senior Vice President, International from 2001 to 2004 and President and CEO from 2004 to 2005. Mr. Cook was appointed Chairman, President and CEO in July 2005.

Table of Contents

Ms. Joppa was appointed Vice President, Human Resources and Communications in November 2005. Prior to that time, Ms. Joppa held various positions at General Mills, a consumer food products company, from 1989 to 2005, including service as Director of Human Resources for several different operating divisions from 1999 to 2005.

Mr. Linnell joined the Company in 1996 as General Counsel and Secretary and was appointed Vice President, General Counsel and Secretary in 2000.

Mr. McMurray joined the Company in 1980 and has held various positions, including Director, Global Information Technology from 2001 to 2003; Vice President, Human Resources from 2004 to 2005; and Vice President, Information Technology, Europe, South Africa, and Mexico from 2005 to 2006. Mr. McMurray became2006; and Senior Vice President Industrial Products in September 2006.from 2006 to 2011. In 2011, Mr. McMurray has beenwas appointed Senior Vice President and Chief Administrative Officer, effective October 1, 2011.Officer.

Ms. Perushek was appointed Vice President and Chief Information Officer in November 2006. Prior to that time, Ms. Perushek was Vice President of Global Information Technology at H.B. Fuller Company, a worldwide manufacturer of adhesive products, from 2005 to 2006 and Chief Information Officer for Young America Corporation, a marketing company, from 1999 to 2004.

Mr. TimmShaw joined the Company in 19832004 and has held various positions, including General Manager, Disk Drive from 1995 to 2005Director, Corporate Compliance/Internal Audit, and General Manager, Gas Turbine Systems Products from 2005 to 2006. Mr. Timm was appointed Vice President, Asia-Pacific in December 2006. The Company has announced that Mr. Timm will retire from the Company at the end of 2011, with his replacement to be announced at a later date.

Mr. VerHage was appointed Vice President and Chief Financial Officer in March 2004. Prior to that time, Mr. VerHage was a partner for Deloitte & Touche, LLP, an international accounting firm, from 2002 to 2004. The Company has announced that Mr. VerHage is leaving the Company on October 31, 2011 and that James F. Shaw, age 42, currentlyCorporate Controller and Principal Accounting Officer for the Company, has beenfrom 2004 to 2011. Mr. Shaw was appointed Vice President and Chief Financial Officer effective November 1, 2011. Prior to joining Donaldson, Mr. Shaw held various positions at Deloitte & Touche, LLP and Arthur Andersen, LLP.

Mr. Vermeersch joined the Company in 1992 and has held various positions, including Director, Gas Turbine Systems, Asia Pacific from 2000 to 2005; Manager, Aftermarket and Service IFS, Belgium from 2005 to 2006; Manager, IFS, Belgium from 2006 to 2007; Director, Gas Turbine Systems, Europe, Middle East and North Africa, from 2007 to 2010; and Director, Engine, Europe, Middle East and North Africa from 2010 to 2011. Mr. Vermeersch was appointed Vice President, Europe and Middle East in January 2012.

Mr. Ward joined the Company in 1998 and has held various positions, including Director, Operations from 2001 to 2003; Director, Product and Business Development, IFS Group from 2003 to 2004; Managing Director, Europe from 2004 to 2006; and Vice President, Europe and Middle East from 2006 to 2008. Mr. Ward was appointed Senior Vice President, Engine Products in August 2008. Mr. Ward has been2008 and was appointed Senior Vice President, Industrial Products, effectivein October 1, 2011.

Ms. WilfongMr. Wu was appointed Vice President, and Chief Technology OfficerAsia Pacific in May 2007.January 2012. Prior to that time, Ms. WilfongMr. Wu was Director, Researchthe Global Vice President and DevelopmentPresident of Asia Pacific at 3M Company, an international consumerGreif, Inc., a global leader in industrial packaging products company,and services, from 20002005 to 2007, most recently as Director, Research2010; and Development forChief Advisor to Chairman of the 3M Automotive DivisionBoard of Wanhua Industrial Group, a global chemical industry leader, from 20062010 to 2007.2011.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The common shares of the Company are traded on the New York Stock Exchange under the symbol DCI. The amount and frequency of all cash dividends declared on the Company’s common stock for Fiscal 20112013 and 20102012 appear in Note PQ of the Notes to Consolidated Financial Statements on page 54.56. The Company’s dividend payout ratio target is 20approximately 30 percent to 40 percent of the average earnings per share of the last three years. This is a change from the previous target of 25 percent to 30 percent of the average earnings per share of the last three years. This guidance is expected to be used for future dividend payouts. As of September 22, 2011,25, 2013, there were 1,9501,862 shareholders of record of common stock.

The low and high sales prices for the Company’s common stock for each full quarterly period during Fiscal 20112013 and 20102012 were as follows:

| | | | | | | | |

| | First Quarter | | Second Quarter | | Third Quarter | | Fourth Quarter |

Fiscal 2011 2013 | $30.90 - 38.18 | | $40.8631.83 - 50.1938.30 | | $48.5134.26 - 60.28 38.08 | | $54.5934.35 - 62.90 | | $54.62 - 63.04

39.36 |

| Fiscal 2012 | $23.19 - 33.33 | | $30.48 - 36.52 | | $34.02 - 38.89 | | | |

Fiscal 2010

| | $32.6030.51 - 39.82 | | $35.24 - 45.19

| | $37.24 - 47.38

| | $40.51 - 48.21

36.82 |

Table of Contents

The following table sets forth information in connection with purchases made by, or on behalf of, the Company or any affiliated purchaser of the Company, of shares of the Company’s common stock during the quarterly period ended July 31, 2011.2013.

| | | | | | | | | | | | | |

Period | | Total Number of

Shares Purchased

(1) | | Average Price

Paid per Share | | Total Number of

Shares Purchased as

Part of Publicly

Announced Plans or

Programs | | Maximum Number

of Shares that May

Yet Be Purchased

Under the Plans or

Programs | |

May 1 - May 31, 2011 | | | — | | $ | — | | | — | | | 6,187,240 | |

June 1 - June 30, 2011 | | | 900,000 | | $ | 56.35 | | | 900,000 | | | 5,287,240 | |

July 1 - July 31, 2011 | | | 291,558 | | $ | 59.23 | | | 256,648 | | | 5,030,592 | |

Total | | | 1,191,558 | | $ | 57.06 | | | 1,156,648 | | | 5,030,592 | |

The Company initiated the purchase of an additional 162,900 shares for $9.2 million in July 2011 that are not included in Fiscal 2011 repurchases as the transactions did not settle until after fiscal year end. These repurchases will be included in Fiscal 2012 activity.

| Period | | | Total Number of

Shares Purchased

(1) | | | Average Price

Paid per Share | | | Total Number of

Shares Purchased as

Part of Publicly

Announced Plans or

Programs | | | Maximum Number

of Shares that May

Yet Be Purchased

Under the Plans or

Programs | |

| May 1 - May 31, 2013 | | | | — | | | $ | — | | | | — | | | | 3,737,155 | |

| June 1 - June 30, 2013 | | | | 1,037,194 | | | $ | 35.69 | | | | 1,031,318 | | | | 2,705,837 | |

| July 1 - July 31, 2013 | | | | 152,067 | | | $ | 35.53 | | | | 135,034 | | | | 2,570,803 | |

| | Total | | | | 1,189,261 | | | $ | 35.67 | | | | 1,166,352 | | | | 2,570,803 | |

_________________

| (1) | |

| (1)

| On March 26, 2010, the Company announced that the Board of Directors authorized the repurchase of up to 8.016.0 million shares of common stock. This repurchase authorization which is effective until terminated by the Board of Directors, replaced the existing authority that was authorized on March 31, 2006.Directors. There were no repurchases of common stock made outside of the Company’s current repurchase authorization during the quarter ended July 31, 2011.2013. However, the “Total Number of Shares Purchased” column of the table above includes 34,91022,909 previously owned shares tendered by option holders in payment of the exercise price of options during the quarter. While not considered repurchases of shares, the Company does at times withhold shares that would otherwise be issued under equity-based awards to cover the withholding taxes due as a result of exercising stock options or payment of equity-based awards. |

TableOn January 27, 2012, the Company announced that its Board of ContentsDirectors declared a two-for-one stock split effected in the form of a 100 percent stock dividend. The stock split was distributed March 23, 2012, to stockholders of record as of March 2, 2012. Earnings and dividends per share and weighted average shares outstanding are presented in this Form 10-K after the effect of the 100 percent stock dividend. The two-for-one stock split is reflected in the share amounts in all periods presented in the table above and elsewhere in this annual Form 10-K.

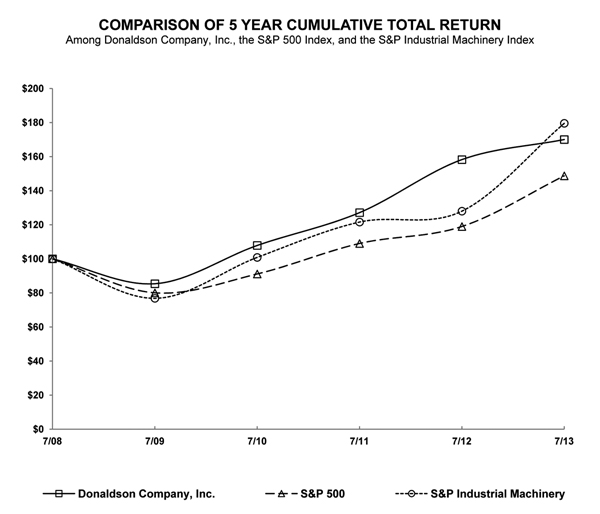

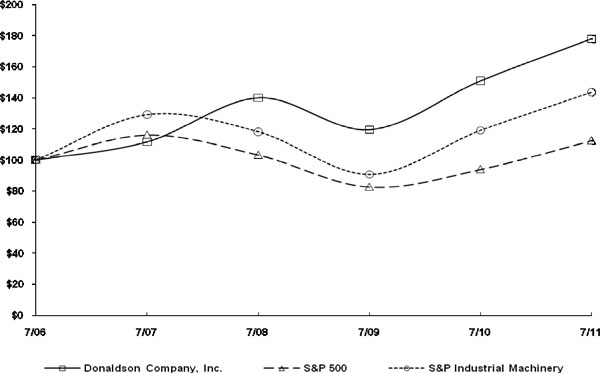

The graph below compares the cumulative total stockholder return on the Company’s common stock for the last five fiscal years with the cumulative total return of the Standard & Poor’s 500 Stock Index and the Standard & Poor’s Industrial Machinery Index. The graph and table assume the investment of $100 in each of the Company’s common stock and the specified indexes at the beginning of the applicable period, and assume the reinvestment of all dividends.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN

Among Donaldson Company, Inc., the S&P 500 Index

and the S&P Industrial Machinery Index

| | | | | | | | | | | | | | | | | | | |

| | Year Ended July 31, | |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 | | 2006 | |

Donaldson Company, Inc. | | $ | 177.91 | | $ | 150.95 | | $ | 119.50 | | $ | 139.95 | | $ | 111.77 | | $ | 100.00 | |

S&P 500 | | | 112.56 | | | 94.07 | | | 82.64 | | | 103.25 | | | 116.13 | | | 100.00 | |

S&P Industrial Machinery | | | 143.55 | | | 119.05 | | | 90.70 | | | 118.06 | | | 129.23 | | | 100.00 | |

Table of Contents

| | | Year Ended July 31, | |

| | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| Donaldson Company, Inc. | | $ | 170.03 | | | $ | 158.25 | | | $ | 127.12 | | | $ | 107.86 | | | $ | 85.39 | | | $ | 100.00 | |

| S&P500 | | | 148.71 | | | | 118.97 | | | | 109.02 | | | | 91.11 | | | | 80.04 | | | | 100.00 | |

| S&P Industrial Machinery | | | 179.57 | | | | 127.98 | | | | 121.59 | | | | 100.84 | | | | 76.83 | | | | 100.00 | |

Item 6. Selected Financial Data

The following table sets forth selected financial data for each of the fiscal years in the five-year period ended July 31, 20112013 (in millions, except per share data):

| | | | | | | | | | | | | | | | | |

| | Year Ended July 31, | | | Year Ended July 31, | |

| | 2011 | | 2010 | | 2009 | | 2008 | | 2007 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | | | 2009 | |

Net sales | | $ | 2,294.0 | | $ | 1,877.1 | | $ | 1,868.6 | | $ | 2,232.5 | | $ | 1,918.8 | | | $ | 2,436.9 | | | $ | 2,493.2 | | | $ | 2,294.0 | | | $ | 1,877.1 | | | $ | 1,868.6 | |

Income from continuing operations | | 225.3 | | 166.2 | | 131.9 | | 172.0 | | 150.7 | | |

| Net earnings | | | | 247.4 | | | | 264.3 | | | | 225.3 | | | | 166.2 | | | | 131.9 | |

Diluted earnings per share | | 2.87 | | 2.10 | | 1.67 | | 2.12 | | 1.83 | | | | 1.64 | | | | 1.73 | | | | 1.43 | | | | 1.05 | | | | 0.83 | |

Total assets | | 1,726.1 | | 1,499.5 | | 1,334.0 | | 1,548.6 | | 1,319.0 | | | | 1,743.6 | | | | 1,730.1 | | | | 1,726.1 | | | | 1,499.5 | | | | 1,334.0 | |

Long-term obligations | | 205.7 | | 256.2 | | 253.7 | | 176.5 | | 129.0 | | | | 102.8 | | | | 203.5 | | | | 205.7 | | | | 256.2 | | | | 253.7 | |

Cash dividends declared per share | | 0.560 | | 0.480 | | 0.460 | | 0.430 | | 0.370 | | | | 0.450 | | | | 0.335 | | | | 0.280 | | | | 0.240 | | | | 0.230 | |

Cash dividends paid per share | | 0.535 | | 0.470 | | 0.455 | | 0.420 | | 0.360 | | | | 0.410 | | | | 0.320 | | | | 0.268 | | | | 0.235 | | | | 0.228 | |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of OperationOperations

Results of OperationOperations

The following discussion of the Company’s financial condition and results of operations should be read in conjunction with the Consolidated Financial Statements and Notes thereto and other financial information included elsewhere in this report.

Overview

The Company is a worldwide manufacturer of filtration systems and replacement parts. The Company’s core strengths are leading filtration technology, strong Customer relationships, and its global presence. The Company operates through two reporting segments, Engine Products and Industrial Products, and has a product mix including air and liquid filtration systems and exhaust and emission control products. As a worldwide business, the Company’s results of operations are affected by conditions in the global economic environment. Under normalmost economic conditions, the Company’s market diversification between its OEM and replacement parts Customers, its diesel engine and industrial end markets, and its North American and international end markets has helped to limit the impact of weakness in any one product line, market, or geography on the consolidated results of the Company.

The Company reported record sales in Fiscal 20112013 of $2,294.0$2,436.9 million, up 22.2down 2.3 percent from $1,877.1$2,493.2 million in the prior year. The Company’s results were positivelynegatively impacted by foreign currency translation, which increaseddecreased sales by $49.8$32.2 million. Excluding the current year impact of foreign currency translation, worldwide sales increased 19.6decreased 1.0 percent.

Although net sales excluding foreign currency translation is not a measure of financial performance under GAAP,generally accepted accounting principles in the United States of America (U.S.) (U.S. GAAP), the Company believes it is useful in understanding its financial results and provides a comparable measure for understanding the operating results of the Company between different fiscal periods excluding the impact of foreign currency translation. The following is a reconciliation to the most comparable U.S. GAAP financial measure of this non-GAAP financial measure (in millions):

| | | | | | | |

| | Year Ended July 31, | |

| | 2011 | | 2010 | |

Net sales, excluding foreign currency translation | | $ | 2,244.2 | | $ | 1,833.9 | |

Foreign currency translation impact | | | 49.8 | | | 43.2 | |

Net sales | | $ | 2,294.0 | | $ | 1,877.1 | |

| | | Net Sales | | | Percent

Change in

Net Sales | |

| Year ended July 31, 2011 | | $ | 2,294.0 | | | | NA | |

| Net sales change, excluding foreign currency translation impact | | | 237.9 | | | | 10.4 | % |

| Foreign currency translation impact | | | (38.7 | ) | | | (1.7 | )% |

| Year ended July 31, 2012 | | $ | 2,493.2 | | | | 8.7 | % |

| Net sales change, excluding foreign currency translation impact | | | (24.1 | ) | | | (1.0 | )% |

| Foreign currency translation impact | | | (32.2 | ) | | | (1.3 | )% |

| Year ended July 31, 2013 | | $ | 2,436.9 | | | | (2.3 | )% |

The Company also reported record net earnings in Fiscal 20112013 of $225.3$247.4 million, an increasea decrease of 35.66.4 percent from $166.2$264.3 million in the prior year. The Company’s net earnings were also positivelynegatively impacted by foreign currency translation, which increaseddecreased net earnings by $6.1$2.1 million. Excluding the current year impact of foreign currency translation, net earnings increased 31.9decreased 5.6 percent.

Table of Contents

Although net earnings excluding foreign currency translation is not a measure of financial performance under U.S. GAAP, the Company believes it is useful in understanding its financial results and provides a comparable measure for understanding the operating results of the Company between different fiscal periods excluding the impact of foreign currency translation. The following is a reconciliation to the most comparable U.S. GAAP financial measure of this non-GAAPnon-U.S. GAAP financial measure (in millions):

| | | | | | | |

| | Year Ended July 31, | |

| | 2011 | | 2010 | |

Net earnings, excluding foreign currency translation | | $ | 219.2 | | $ | 162.6 | |

Foreign currency translation impact, net of tax | | | 6.1 | | | 3.6 | |

Net earnings | | $ | 225.3 | | $ | 166.2 | |

| | | Net Earnings | | | Percent

Change in

Net Earnings | |

| Year ended July 31, 2011 | | $ | 225.3 | | | | NA | |

| Net earnings change, excluding foreign currency translation impact | | | 43.0 | | | | 19.1 | % |

| Foreign currency translation impact | | | (4.0 | ) | | | (1.8 | )% |

| Year ended July 31, 2012 | | $ | 264.3 | | | | 17.3 | % |

| Net earnings change, excluding foreign currency translation impact | | | (14.8 | ) | | | (5.6 | )% |

| Foreign currency translation impact | | | (2.1 | ) | | | (0.8 | )% |

| Year ended July 31, 2013 | | $ | 247.4 | | | | (6.4 | )% |

The Company reported diluted earnings per share of $2.87,$1.64, a 36.75.2 percent increasedecrease from $2.10$1.73 in the prior year.

As discussed above, the Company recorded full year records forFollowing are net sales and net earnings. In addition, operating margin was a record of 13.7 percent for the year. The Company’s manufacturing plants and distribution centers executed very well and continued to make both capital and operating investments which, along with the Company’s Continuous Improvement initiatives, resulted in a record year and puts the Company in a position to profitably support its Customers’ global growth plans. These improvements were slightly offset by increases in purchased raw material and freight costs.

Following is financial information forproduct within the Company’s Engine and Industrial Products segments.segments and a comparison of earnings before income taxes. Corporate and Unallocated includes corporate expenses determined to be non-allocable to the segments and interest income and expense. See further discussion of segment information in Note KL of the Company’s Notes to Consolidated Financial Statements.

| | | | | | | | | | | | | |

| | Engine

Products | | Industrial

Products | | Corporate &

Unallocated | | Total

Company | |

| | (thousands of dollars) | |

2011 | | | | | | | | | | | | | |

Net sales | | $ | 1,440,495 | | $ | 853,534 | | $ | — | | $ | 2,294,029 | |

Earnings before income taxes | | | 211,255 | | | 123,871 | | | (22,863 | ) | | 312,263 | |

| | | | | | | | | | | | | |

2010 | | | | | | | | | | | | | |

Net sales | | $ | 1,126,007 | | $ | 751,057 | | $ | — | | $ | 1,877,064 | |

Earnings before income taxes | | | 155,833 | | | 91,084 | | | (16,741 | ) | | 230,176 | |

| | | | | | | | | | | | | |

2009 | | | | | | | | | | | | | |

Net sales | | $ | 1,027,685 | | $ | 840,944 | | $ | — | | $ | 1,868,629 | |

Earnings before income taxes | | | 85,896 | | | 87,427 | | | (11,898 | ) | | 161,425 | |

| | | 2013 | | | 2012 | | | 2011 | |

| | | (thousands of dollars) | |

| Engine Products segment: | | | | | | | | | | | | |

| Off-Road Products | | $ | 358,834 | | | $ | 376,870 | | | $ | 327,557 | |

| On-Road Products | | | 128,446 | | | | 163,934 | | | | 127,107 | |

| Aftermarket Products* | | | 900,419 | | | | 907,306 | | | | 861,393 | |

| Retrofit Emissions Products | | | 12,298 | | | | 15,354 | | | | 19,555 | |

| Aerospace and Defense Products | | | 104,191 | | | | 106,676 | | | | 104,883 | |

| Total Engine Products segment | | | 1,504,188 | | | | 1,570,140 | | | | 1,440,495 | |

| Industrial Products segment: | | | | | | | | | | | | |

| Industrial Filtration Solutions Products | | | 529,751 | | | | 553,453 | | | | 507,646 | |

| Gas Turbine Products | | | 232,922 | | | | 180,669 | | | | 154,726 | |

| Special Applications Products | | | 170,087 | | | | 188,986 | | | | 191,162 | |

| Total Industrial Products segment | | | 932,760 | | | | 923,108 | | | | 853,534 | |

| Total Company | | $ | 2,436,948 | | | $ | 2,493,248 | | | $ | 2,294,029 | |

For_________________

* Includes replacement part sales to the twelve months ended July 31, 2010 and 2009, net sales reflect the reclassification of $31,636 and $25,724, respectively, earnings before income taxes reflect a reclassification of $5,360 and $2,099, respectively, as a result of an internal reorganization of Industrial Hydraulics from Industrial Products to Engine Products, which became effective August 1, 2010.Company’s OEM Customers

| | | Engine | | | Industrial | | | Corporate & | | | Total | |

| | | Products | | | Products | | | Unallocated | | | Company | |

| | | (thousands of dollars) | |

| 2013 | | | | | | | | | | | | |

| Net sales | | $ | 1,504,188 | | | $ | 932,760 | | | $ | — | | | $ | 2,436,948 | |

| Earnings before income taxes | | | 220,892 | | | | 139,108 | | | | (11,819 | ) | | | 348,181 | |

| 2012 | | | | | | | | | | | | | | | | |

| Net sales | | $ | 1,570,140 | | | $ | 923,108 | | | $ | — | | | $ | 2,493,248 | |

| Earnings before income taxes | | | 227,941 | | | | 149,249 | | | | (6,410 | ) | | | 370,780 | |

| 2011 | | | | | | | | | | | | | | | | |

| Net sales | | $ | 1,440,495 | | | $ | 853,534 | | | $ | — | | | $ | 2,294,029 | |

| Earnings before income taxes | | | 211,255 | | | | 123,871 | | | | (22,863 | ) | | | 312,263 | |

Many factors contributed to the Company’s results for each of the Company’s reportingreportable segments for Fiscal 2011,2013, including an improvementa weakening in global economic conditions in many of the Company’s end markets, partially offset by the Company’s program of Continuous Improvement initiatives new product introductions,and emerging market growth, and the expansion of the Company’s distribution capabilities.growth.

In the Engine Products segment, the Company experienced increaseddecreased sales in all end-markets and regions withmost end-markets. Earnings before income taxes as a percentage of Engine Products segment sales of 14.7 percent increased slightly from 14.5 percent in the exception of Aerospace and Defense Products.prior year. The percentage earnings improvementincrease for the current fiscal yeartwelve months ended July 31, 2013, was primarily driven by better absorption of fixed costs due to improved volumes at our manufacturing plants, andbenefits from the Company’s ongoing Continuous Improvement initiatives. Theinitiatives and a higher percentage of sales coming from replacement filters, partially offset by increased incremental expenses related to the Company’s Strategic Business Systems project (which is the Company’smulti-year implementation of a global enterprise resource planning system), higher pension and insurance costs, and lower fixed cost absorption as a result of lower production volumes (primarily in the first half of the year). In addition, the Engine Products segment incurred $1.7 million in restructuring expenses compared to none in the prior year. These expenses related to employee severance costs associated with a reduction in workforce. Off-Road Product sales decreased by 4.8 percent driven by a decline in the mining equipment markets and weakness in the construction equipment markets, which were partially offset by strength in the agriculture equipment markets across the globe. On-Road Products sales decreased by 21.6 percent as a result of reduced truck builds by the Company’s OEM Customers in the U.S., Europe, and Japan. Aftermarket Products sales increasesdecreases were driven by continued improvement inlower equipment utilization rates in the mining, construction, and transportation industries globally. The Off-Road Product sales increase is driven by higher demand for agriculture and mining equipment, due to continued strong commodity prices and improved sales of heavy construction equipment, which was due to increased global infrastructure spending, especially in developing economies. On-Road Products sales improved as North America and Europe heavy truck build rates continued rebounding.

Table of Contentsindustries.

In the Industrial Products segment, where many product lines are later economic cycle businesses, sales increased primarily due to improvingstrong global economies leading to greater Customer demand. Indemand for Gas Turbine Systems products. Earnings before income taxes as a percentage of Industrial Filtration Solutions Products segment sales of new dust collection equipment14.9 percent decreased from 16.2 percent in the prior year. The decline in earnings as a percentage of sales over the prior year was driven by a shift in product mix to large first fit Gas Turbine projects which generally utilize outside subcontractors, less absorption of fixed manufacturing costs in businesses other than Gas Turbine Systems, increased incremental expenses related to the Company’s Strategic Business Systems project, and replacement filters continuedhigher pension and insurance costs, partially offset by benefits from the Company’s ongoing Continuous Improvement initiatives. In addition, the Industrial Products segment incurred $2.3 million in restructuring expenses compared to grow.none in the prior year. These expenses related to employee severance costs associated with a reduction in workforce. Gas Turbine Products sales remained slowincreased by 28.9 percent due to staticstrong Customer demand for large gas turbine power generation projects as a result of unchangedincreased global power generationelectricity requirements. The increase inIn Industrial Filtration Solutions Products, sales declined due to reduced capital investment by manufacturers. Sales in Special Applications Products isdecreased by 10.0 percent due to strong sales in certain product linesreduced demand for filtration products serving the electronics industries and weakness in industrial end markets resulting in lower sales of the Company’s membrane semiconductor, imaging, and venting end markets.products.

Following are net sales by product within both the Engine and Industrial Products segments:Outlook

| | | | | | | | | | |

| | 2011 | | 2010 | | 2009 | |

| | (thousands of dollars) | |

Engine Products segment: | | | | | | | | | | |

Off-Road Products | | $ | 327,557 | | $ | 222,329 | | $ | 243,691 | |

Aerospace and Defense Products | | | 104,883 | | | 111,977 | | | 119,094 | |

On-Road Products | | | 127,107 | | | 81,874 | | | 71,958 | |

Aftermarket Products* | | | 861,393 | | | 691,899 | | | 561,846 | |

Retrofit Emissions Products | | | 19,555 | | | 17,928 | | | 31,096 | |

Total Engine Products segment | | | 1,440,495 | | | 1,126,007 | | | 1,027,685 | |

Industrial Products segment: | | | | | | | | | | |

Industrial Filtration Solutions Products | | | 507,646 | | | 423,050 | | | 477,908 | |

Gas Turbine Products | | | 154,726 | | | 150,131 | | | 206,760 | |

Special Applications Products | | | 191,162 | | | 177,876 | | | 156,276 | |

Total Industrial Products segment | | | 853,534 | | | 751,057 | | | 840,944 | |

|

Total Company | | $ | 2,294,029 | | $ | 1,877,064 | | $ | 1,868,629 | |

| · | |

| *

| Includes replacement part sales to the Company’s OEM Customers.

|

Outlook

The Company forecasts continued expansion in many of its end markets, with higher growth in emerging economies. The Company forecasts its full year Fiscal 2012 EPS to be between $3.15 and $3.45.

| | |

| •

| The Company is planning its total Fiscal 20122014 sales to be between $2.45 and $2.60$2.55 billion, or up about 7an increase of 1 to 155 percent from Fiscal 2011.2013. Foreign currency translation is based on the Company’s plannedforecasted rates for the Euro at US$1.421.32 and 8197 Yen to the US$.

|

| · | |

| •

| The Company’s full year Fiscal 20122014 operating margin is forecasted to be 13.714.1 to 14.514.9 percent. Included in this forecast is approximately $30 million in expense increases for our Strategic Business Systems project and incentive compensation. |

| · | |

| •

| The Company’s full year Fiscal 20122014 tax rate is projected to be between 28 and 3031 percent. |

| · | The Company forecasts its full year Fiscal 2014 EPS to be between $1.65 and $1.85. |

| •

· | The Company projects that cash generated by operating activities will be between $275 and $305 million in Fiscal 2012.million. Capital spending in Fiscal 2012 is estimated to be approximately $100$90 million. |

Engine Products – The Company forecasts full year sales to increase 8 to 15 percent, including the impact of foreign currency translation.

| | |

| •

| The Company anticipates sales torepurchasing between 2 and 4 percent of its agricultural, mining, and construction equipment OEM Customers to grow at a more moderate pacediluted outstanding shares in Fiscal 2012 compared to Fiscal 2011’s growth rate. The Company also expects to continue to benefit from increased market share on their Customers’ new Tier IV equipment platforms. |

| | |

| •

| In the On-Road Products’ business, the Company believes build rates for heavy and medium duty trucks at their OEM Customers will be higher than Fiscal 2011, but are expected to grow at a more normal rate.

|

| | |

| •

| Sales of the Company’s Aftermarket Products are expected to remain strong based on current utilization rates for both off-road equipment and on-road heavy trucks. The Company should also benefit as its distribution

FY14. |

Table of Contents

| | |

| | networks continue to expand in the emerging economies and from the increasing number of systems installed in the field with their proprietary filtration systems.

|

| | |

| •

| The Company forecasts modest sales gains in Aerospace and Defense Products for Fiscal 2012 as the continued slowdown in military spending is anticipated to be offset by increased commercial aerospace sales.

13 |

Industrial Products - The Company forecasts full year FY12 sales to increase 7 to 15 percent, including the impact of foreign currency translation.

| | |

| •

| The Company’s Industrial Filtration Solutions Products’ sales are projected to increase 7 to 14 percent, assuming demand for new filtration equipment and replacement filters both continue to improve as general industrial capital activity and spending increase globally.

|

| | |

| •

| The Company anticipates its Gas Turbine Products’ sales to increase 14 to 22 percent due to improvement in the power generation market and ongoing strength in the oil and gas market segment.

|

| | |

| •

| Special Applications Products’ sales are projected to increase 2 to 9 percent primarily due to growing salesTable of their membranes products.

Contents |

Fiscal 20112013 Compared to Fiscal 20102012

Engine Products SegmentThe Engine Products segment sells to OEMs in the construction, mining, agriculture, aerospace, defense, and truck markets and to independent distributors, OEM dealer networks, private label accounts, and large equipment fleets. Products include air filtration systems, exhaust and emissions systems, liquid filtration systems including hydraulics, fuel, lube, and replacement filters.

Sales for the Engine Products segment were $1,440.5$1,504.2 million, an increasea decrease of 27.94.2 percent from $1,126.0$1,570.1 million in the prior year.year with decreases across all businesses. Fiscal 2013 Engine Products sales decreased by 11.3 percent in Asia, 3.6 percent in the United States increased by 25.9 percentAmericas, and were flat in Fiscal 2011Europe compared to Fiscal 2010. International Engine Products sales increased 29.8 percent from the prior year.2012. The impact of foreign currency increaseddecreased total sales by $31.5$23.8 million, or 2.81.6 percent. Earnings before income taxes as a percentage of Engine Products segment sales of 14.7 percent increased from 13.8 percent in the prior year. The earnings improvement for the current fiscal year was driven by better absorption of fixed costs due to improved volumes and the Company’s ongoing Continuous Improvement initiatives, partially offset by increased commodity costs compared to the prior year. There were $1.9 million in restructuring expenses for the Engine Products segment in the prior year.

Worldwide sales of Off-Road Products were $327.6$358.8 million, an increasea decrease of 47.34.8 percent from $222.3$376.9 million in the prior year. Sales declined 18.5 percent in Asia and 7.7 percent in the Americas, partially offset by growth of 3.0 percent in Europe. The sales decreases were driven by a decline in the mining equipment markets as commodity prices moderated and reductions in mining investments kept production of new mining equipment below prior year levels. Reductions in large non-residential construction and non-building infrastructure projects lead to lower demand for larger construction equipment. These decreases were partially offset by strength in the agriculture equipment market globally.

Worldwide sales of On-Road Products were $128.4 million, a decrease of 21.6 percent from $163.9 million in the prior year. Sales decreased 31.4 percent in the Americas, 19.7 percent in Asia, and 6.7 percent in Europe. Sales decreases were a result of a decrease in global truck builds, especially in the U.S, as well as OEM Customer initiatives to reduce inventory. According to published industry data, North American Class 8 truck build rates decreased 19.0 percent and medium-duty truck build rates increased 4.9 percent over the prior year.

Worldwide sales of Aftermarket Products were $900.4 million, a decrease of 0.8 percent from $907.3 million in the prior year. Sales in the United States increased 35.8 percent over the prior fiscal year. Internationally, sales of Off-Road Products were up 56.0 percent from the prior year, with sales increasing in Asia and Europe by 58.2decreased 4.4 percent and 55.61.8 percent, respectively. The Company’s overall increase was driven by higher demand for agriculture, construction, and mining equipment due to continued strong commodity prices and improved sales of heavy construction equipment, which was due to increased global infrastructure spending, especially in developing economies. Off-Road Productsrespectively, while sales in the U.S. also benefited from market share gains on new platforms that began production during calendar year 2011. These increases were slightly offset by U.S. residential and non-residential construction markets, which showed continued weakness, resulting in lower sales of the Company’s products into those markets.

Worldwide sales of Aerospace and Defense Products were $104.9 million, a 6.3 percent decrease from $112.0 million in the prior year. Sales in the United States decreased 8.7 percent over the prior year as a result of slowdowns in U.S. military activity, which is causing an associated slowdown in government procurement spending for major programs. Internationally, sales of Aerospace and Defense Products increased 3.0 percent over the prior year. The international sales increased primarily due to market share gains resulting from improving the Company’s Aerospace distribution capabilities in Europe.

Worldwide sales of On-Road Products were $127.1 million, an increase of 55.2 percent from $81.9 million in the prior year. On-Road Products sales in the United States increased 86.0 percent from the prior year. Class 8 build rates increased 47.8 percent and medium duty truck build rates increased 37.1 percent over the prior year. International On-Road Products sales increased 27.4 percent from the prior year, driven by increased sales in Europe of 45.6Americas grew 4.1 percent. This increase is consistent with the increase in European build rates. The overall sales increase was a result of an increase in Customer truck build rates, higher content per truck, and a slightly higher market share.

Worldwide Engine Aftermarket Products sales of $861.4 million increased 24.5 percent from $691.9 million in the prior year. Sales in the United States increased 26.3 percent over the prior year. International sales increased 23.1

Table of Contents

percent from the prior year,decreases were primarily driven by sales increases in Asia, Latin America and Europe of 37.8 percent, 25.7 percent, and 13.5 percent, respectively. The sales increases in the U.S. and internationally were attributable to improved On-Road and Off-Road equipmentlower utilization rates from a year ago, the Company’s increased distribution and market share growth, and the continued increase in the percentage of equipment inacross the field that useson-road and off-road equipment markets along with the Company’s proprietary filtration systems.negative impacts of foreign currency translation.

Worldwide sales of Retrofit Emissions Products were $19.6$12.3 million, an increasea decrease of 9.119.9 percent from $17.9$15.4 million in the prior year. The Company’s Retrofit Emissions Products sales are solely in the United States.U.S. The sales of these products are highly dependent on government regulations. Sales were impacted by a lack of government funding availability and delayed government verification of new products throughout Fiscal 2013.

Worldwide sales of Aerospace and Defense Products were $104.2 million, a decrease of 2.3 percent from $106.7 million in the prior year. Sales of Retrofit EmissionsAerospace and Defense Products increased overall, but challenges still remainwere relatively flat over the prior year in Europe, while sales decreased 2.2 percent in the supply chain for certain components and delaysAmericas. The sales decrease was due to a continued slowdown in regulatory approval for certain of the Company’s products have impacted the Company’s sales.U.S. military spending, which is forecasted to continue in Fiscal 2014.

Industrial Products SegmentThe Industrial Products segment sells to various industrial distributors, dealers, and end-users, OEMs of gas-fired turbines, and OEMs and end-users requiring clean air. Products include dust, fume, and mist collectors, compressed air purification systems, air filtration systems for gas turbines, PTFE membrane basedmembrane-based products, and specialized air and gas filtration systems for various applications including computer hard disk drives.drives and other electronic equipment.

Sales for the Industrial Products segment were $853.5$932.8 million, an increase of 13.61.0 percent from $751.1$923.1 million in the prior year. Internationalyear driven by 28.9 percent sales growth in Gas Turbine Products, partially offset by sales decreases in Special Applications Products and Industrial Filtration Solutions Products of 10.0 percent and 4.3 percent, respectively. Fiscal 2013 Industrial Products sales increased 8.5by 2.9 percent and salesin Asia, 0.9 percent in the United States increased 27.2 percent from the prior year.Americas, and were flat in Europe compared to Fiscal 2012. The impact of foreign currency increaseddecreased sales by $18.3$8.4 million, or 2.40.9 percent. Earnings before income taxes as a percentage of Industrial Products segment sales of 14.5 percent increased from 12.1 percent in the prior year. The improvement in earnings as a percent of sales over the prior year was driven by better leverage of fixed operating costs and better plant utilization. Restructuring expenses in Fiscal 2011 were $0.7 million, a decrease from $8.3 million in Fiscal 2010.