UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended DECEMBER 31, 20112014

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 1-12252 (Equity Residential)

Commission File Number: 0-24920 (ERP Operating Limited Partnership)

EQUITY RESIDENTIAL

ERP OPERATING LIMITED PARTNERSHIP

(Exact Namename of Registrantregistrant as Specifiedspecified in Its Charter)its charter)

|

| |

| Maryland (Equity Residential) | 13-3675988 (Equity Residential) |

| Illinois (ERP Operating Limited Partnership) | 36-3894853 (ERP Operating Limited Partnership) |

(State or Other Jurisdictionother jurisdiction of Incorporationincorporation or Organization)organization) | (I.R.S. Employer Identification No.) |

| | |

| Two North Riverside Plaza, Chicago, Illinois 60606 | (312) 474-1300 |

(Address of Principal Executive Offices)principal executive offices) (Zip Code) | (Registrant's Telephone Number, Including Area Code)telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

| |

| Common Shares of Beneficial Interest, $0.01 Par Value (Equity Residential) | New York Stock Exchange |

Preferred Shares of Beneficial Interest, $0.01 Par Value (Equity Residential) | New York Stock Exchange |

| 7.57% Notes due August 15, 2026 (ERP Operating Limited Partnership) | New York Stock Exchange |

(Title of Each Class)each class) | (Name of Each Exchangeeach exchange on Which Registered)which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None (Equity Residential)

Units of Limited Partnership Interest (ERP Operating Limited Partnership)

(Title of Each Class)each class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

| |

Equity Residential Yes x No ¨ | ERP Operating Limited Partnership Yes x No o |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

|

| |

Equity Residential Yes ¨ No x | ERP Operating Limited Partnership Yes ¨ No x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

| |

Equity Residential Yes x No ¨ | ERP Operating Limited Partnership Yes x No ¨ |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

| |

Equity Residential Yes x No ¨ | ERP Operating Limited Partnership Yes x No ¨ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

|

| |

Equity Residential ¨x | ERP Operating Limited Partnership ¨x |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

| |

| Equity Residential: | |

Large accelerated filer x | Accelerated filer ¨ |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

|

| |

| ERP Operating Limited Partnership: | |

Large accelerated filer ¨ | Accelerated filer ¨ |

Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

|

| |

Equity Residential Yes ¨ No x | ERP Operating Limited Partnership Yes ¨ No x |

The aggregate market value of Common Shares held by non-affiliates of the Registrant was approximately $17.4$22.3 billion based upon the closing price on June 30, 20112014 of $60.00$63.00 using beneficial ownership of shares rules adopted pursuant to Section 13 of the Securities Exchange Act of 1934 to exclude voting shares owned by Trustees and Executive Officers, some of who may not be held to be affiliates upon judicial determination.

The number of Common Shares of Beneficial Interest, $0.01 par value, outstanding on February 17, 201220, 2015 was 300,240,671.363,798,297.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates by reference certain information that will be contained in Equity Residential's Proxy Statement relating to its 20122015 Annual Meeting of Shareholders, which Equity Residential intends to file no later than 120 days after the end of its fiscal year ended December 31, 2011,2014, and thus these items have been omitted in accordance with General Instruction G(3) to Form 10-K. Equity Residential is the general partner and 95.7%96.2% owner of ERP Operating Limited Partnership.

EXPLANATORY NOTE

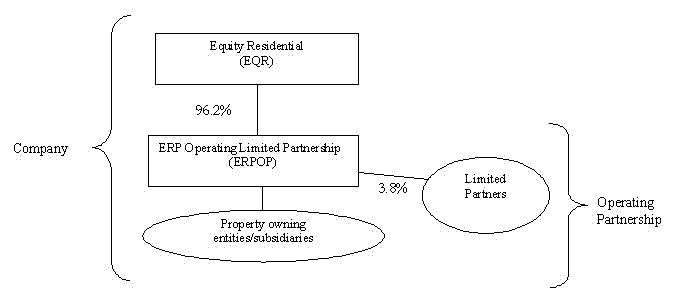

This report combines the annual reports on Form 10-K for the year ended December 31, 20112014 of Equity Residential and ERP Operating Limited Partnership. Unless stated otherwise or the context otherwise requires, references to “EQR” mean Equity Residential, a Maryland real estate investment trust (“REIT”), and references to “ERPOP” mean ERP Operating Limited Partnership, an Illinois limited partnership. References to the “Company,” “we,” “us” or “our” mean collectively EQR, ERPOP and those entities/subsidiaries owned or controlled by EQR and/or ERPOP. References to the “Operating Partnership” mean collectively ERPOP and those entities/subsidiaries owned or controlled by ERPOP. The following chart illustrates the Company's and the Operating Partnership's corporate structure:

EQR is the general partner of, and as of December 31, 20112014 owned an approximate 95.7%96.2% ownership interest in, ERPOP. The remaining 4.3%3.8% interest is owned by limited partners. As the sole general partner of ERPOP, EQR has exclusive control of ERPOP's day-to-day management.

The Company is structured as an umbrella partnership REIT (“UPREIT”) and contributes all net proceeds from its various equity offerings to the Operating Partnership. In return for those contributions, the Company receives a number of OP Units (see definition below) in the Operating Partnership equal to the number of Common Shares it has issued in the equity offering. Contributions of properties to the Company can be structured as tax-deferred transactions through the issuance of OP Units in the Operating Partnership, which is one of the reasons why the Company is structured in the manner shown above. Based on the terms of ERPOP's partnership agreement, OP Units can be exchanged with Common Shares on a one-for-one basis. The Company maintains a one-for-one relationship between the OP Units of the Operating Partnership issued to EQR and the Common Shares issued to the public.Shares.

The Company believes that combining the reports on Form 10-K of EQR and ERPOP into this single report provides the following benefits:

enhances investors' understanding of the Company and the Operating Partnership by enabling investors to view the business as a whole in the same manner as management views and operates the business;

eliminates duplicative disclosure and provides a more streamlined and readable presentation since a substantial portion of the disclosure applies to both the Company and the Operating Partnership; and

creates time and cost efficiencies through the preparation of one combined report instead of two separate reports.

Management operates the Company and the Operating Partnership as one business. The management of EQR consists of the same members as the management of ERPOP.

The Company believes it is important to understand the few differences between EQR and ERPOP in the context of how EQR and ERPOP operate as a consolidated company. All of the Company's property ownership, development and related business operations are conducted through the Operating Partnership and EQR has no material assets or liabilities other than its investment in ERPOP. EQR's primary function is acting as the general partner of ERPOP. EQR also issues public equity from time to time and guarantees certain debt of ERPOP, as disclosed in this report. EQR does not have any indebtedness as all debt is incurred by the Operating Partnership. The Operating Partnership holds substantially all of the assets of the Company, including the Company's ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a

partnership with no publicly traded equity. Except for the net proceeds from equity offerings by the Company, which are contributed

to the capital of the Operating Partnership in exchange for additional limited partnership interests in the Operating Partnership (“OP Units”) (on a one-for-one Common Share per OP Unit basis), the Operating Partnership generates all remaining capital required by the Company's business. These sources include the Operating Partnership's working capital, net cash provided by operating activities, borrowings under its revolving credit facility, the issuance of secured and unsecured debt and equity securities including additional OP Units, and proceeds received from disposition of certain properties and joint ventures.

Shareholders' equity, partners' capital and noncontrolling interests are the main areas of difference between the consolidated financial statements of the Company and those of the Operating Partnership. The limited partners of the Operating Partnership are accounted for as partners' capital in the Operating Partnership's financial statements and as noncontrolling interests in the Company's financial statements. The noncontrolling interests in the Operating Partnership's financial statements include the interests of unaffiliated partners in various consolidated partnerships and development joint venture partners. The noncontrolling interests in the Company's financial statements include the same noncontrolling interests at the Operating Partnership level and limited partner OP Unit holders of the Operating Partnership. The differences between shareholders' equity and partners' capital result from differences in the equity issued at the Company and Operating Partnership levels.

To help investors understand the significant differences between the Company and the Operating Partnership, this report provides separate consolidated financial statements for the Company and the Operating Partnership; a single set of consolidated notes to such financial statements that includes separate discussions of each entity's debt, noncontrolling interests and shareholders' equity or partners' capital, as applicable; and a combined Management's Discussion and Analysis of Financial Condition and Results of Operations section that includes discrete information related to each entity.

This report also includes separate Part I,II, Item 4.9A. Controls and Procedures sections and separate Exhibits 31 and 32 certifications for each of the Company and the Operating Partnership in order to establish that the requisite certifications have been made and that the Company and the Operating Partnership are compliant with Rule 13a-15 or Rule 15d-15 of the Securities Exchange Act of 1934 and 18 U.S.C. §1350.

In order to highlight the differences between the Company and the Operating Partnership, the separate sections in this report for the Company and the Operating Partnership specifically refer to the Company and the Operating Partnership. In the sections that combine disclosure of the Company and the Operating Partnership, this report refers to actions or holdings as being actions or holdings of the Company. Although the Operating Partnership is generally the entity that directly or indirectly enters into contracts and joint ventures and holds assets and debt, reference to the Company is appropriate because the Company is one business and the Company operates that business through the Operating Partnership.

As general partner with control of the Operating Partnership, the Company consolidates the Operating Partnership for financial reporting purposes, and EQR essentially has no assets or liabilities other than its investment in ERPOP. Therefore, the assets and liabilities of the Company and the Operating Partnership are the same on their respective financial statements. The separate discussions of the Company and the Operating Partnership in this report should be read in conjunction with each other to understand the results of the Company on a consolidated basis and how management operates the Company.

EQUITY RESIDENTIAL

ERP OPERATING LIMITED PARTNERSHIP

TABLE OF CONTENTS

|

| | | |

| | | | PAGE |

| PART I. | | | |

| Item 1. | | | |

| Item 1A. | | | |

| Item 1B. | | | |

| Item 2. | | | |

| Item 3. | | | |

| Item 4. | | | |

| PART II. | | | |

| Item 5. | | | |

| Item 6. | | | |

| Item 7. | | | |

| Item 7A. | | | |

| Item 8. | | | |

| Item 9. | | | |

| Item 9A. | | | |

| Item 9B. | | | |

| PART III. | | | |

| Item 10. | | | |

| Item 11. | | | |

| Item 12. | | | |

| Item 13. | | | |

| Item 14. | | | |

| PART IV. | | | |

| Item 15. | | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

PART I

Item 1. Business

General

Equity Residential (“EQR”), a Maryland real estate investment trust (“REIT”) formed in March 1993, is an S&P 500 company focused on the acquisition, development and management of high quality apartment properties in top United States growth markets. ERP Operating Limited Partnership (“ERPOP”), an Illinois limited partnership, was formed in May 1993 to conduct the multifamily residential property business of Equity Residential. EQR has elected to be taxed as a REIT. References to the “Company,” “we,” “us” or “our” mean collectively EQR, ERPOP and those entities/subsidiaries owned or controlled by EQR and/or ERPOP. References to the “Operating Partnership” mean collectively ERPOP and those entities/subsidiaries owned or controlled by ERPOP.

EQR is the general partner of, and as of December 31, 20112014 owned an approximate 95.7%96.2% ownership interest in, ERPOP. All of the Company's property ownership, development and related business operations are conducted through the Operating Partnership and EQR has no material assets or liabilities other than its investment in ERPOP. EQR issues public equity from time to time but does not have any indebtedness as all debt is incurred by the Operating Partnership. The Operating Partnership holds substantially all of the assets of the Company, including the Company's ownership interests in its joint ventures. The Operating Partnership conducts the operations of the business and is structured as a partnership with no publicly traded equity.

As of December 31, 2011,2014, the Company, directly or indirectly through investments in title holding entities, owned all or a portion of 427391 properties located in 1512 states and the District of Columbia consisting of 121,974109,225 apartment units. The ownership breakdown includes (table does not include various uncompleted development properties):

| | | | | Properties | | Apartment Units | | Properties | | Apartment Units |

| Wholly Owned Properties | | 404 |

| | 113,157 |

| | 364 |

| | 98,287 |

|

| Master-Leased Properties – Consolidated | | | 3 |

| | 853 |

|

| Partially Owned Properties – Consolidated | | 21 |

| | 3,916 |

| | 19 |

| | 3,771 |

|

| Partially Owned Properties – Unconsolidated | | | 3 |

| | 1,281 |

|

| Military Housing | | 2 |

| | 4,901 |

| | 2 |

| | 5,033 |

|

| | | 427 |

| | 121,974 |

| | 391 |

| | 109,225 |

|

The Company's corporate headquarters are located in Chicago, Illinois and the Company also operates property management offices in each of its core markets. As of December 31, 20112014, the Company had approximately 3,8003,500 employees who provided real estate operations, leasing, legal, financial, accounting, acquisition, disposition, development and other support functions.

Certain capitalized terms used herein are defined in the Notes to Consolidated Financial Statements. See also Note 17 in the Notes to Consolidated Financial Statements for additional discussion regarding the Company’s segment disclosures.

Available Information

You may access our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and any amendments to any of those reports we file with the SEC free of charge at our website, www.equityresidential.com. These reports are made available at our website as soon as reasonably practicable after we file them with the SEC. The information contained on our website, including any information referred to in this report as being available on our website, is not a part of or incorporated into this report.

Business Objectives and Operating and Investing Strategies

The Company invests in high quality apartment communities located in strategically targeted markets with the goal of maximizing our risk adjusted total return (operating income plus capital appreciation) on invested capital.

We seek to maximize the income and capital appreciation of our properties by investing in markets that are characterized by conditions favorable to multifamily property operations and appreciation. We are focused primarily on the six core coastal, high barrier to entry markets of Boston, New York, Washington DC, Southern California (including Los Angeles, Orange County and San Diego), San Francisco and Seattle. These markets generally feature one or more of the following characteristics that allow us to increase rents:

| |

| ▪ | High barriers to entry where, because of land scarcity or government regulation, it is difficult or costly to build new apartment properties, creating limits on new supply; |

| |

| ▪ | High home ownership costs; |

| |

| ▪ | Strong economic growth leading to job growth and household formation, which in turn leads to high demand for our apartments; |

| |

| ▪ | Urban core locations with an attractive quality of life and higher wage job categories leading to high resident demand and retention; and |

| |

| ▪ | Favorable demographics contributing to a larger pool of target residents with a high propensity to rent apartments. |

Our operating focus is on balancing occupancy and rental rates to maximize our revenue while exercising tight cost control to generate the highest possible return to our shareholders. Revenue is maximized by attracting qualified prospects to our properties, cost-effectively converting these prospects into new residents and keeping our residents satisfied so they will renew their leases upon expiration. While we believe that it is our high-quality, well-located assets that bring our customers to us, it is the customer service and superior value provided by our on-site personnel that keeps them renting with us and recommending us to their friends.

We use technology to engage our customers in the way that they want to be engaged. Many of our residents utilize our web-based resident portal which allows them to sign and renew their lease,leases, review their accountaccounts and make payments, provide feedback and make service requests on-line.

We seek to maximize capital appreciation of our properties by investing in markets that are characterized by conditions favorable to multifamily property appreciation. These markets generally feature one or more of the following:

| |

▪ | High barriers to entry where, because of land scarcity or government regulation, it is difficult or costly to build new apartment properties, creating limits on new supply; |

| |

▪ | High single family home prices making our apartments a more economical housing choice; |

| |

▪ | Strong economic growth leading to household formation and job growth, which in turn leads to high demand for our apartments; and |

| |

▪ | An attractive quality of life leading to high demand and retention that allows us to increase rents. |

Acquisitions and developments may be financed from various sources of capital, which may include retained cash flow, issuance of additional equity and debt, sales of properties and joint venture agreements. In addition, the Company may acquire properties in transactions that include the issuance of limited partnership interests in the Operating Partnership (“OP Units”) as consideration for the acquired properties. Such transactions may, in certain circumstances, enable the sellers to defer, in whole or in part, the recognition of taxable income or gain that might otherwise result from the sales. The Company may acquire land parcels to hold and/or sell based on market opportunities.opportunities as well as options to buy more land in the future. The Company may also seek to acquire properties by purchasing defaulted or distressed debt that encumbers desirable properties in the hope of obtaining title to property through foreclosure or deed-in-lieu of foreclosure proceedings. The Company has also, in the past, converted some of its properties and sold them as condominiums but is not currently active in this line of business.

Over the past several years, the Company has done an extensive repositioning of its portfolio from low barrier to entry/non-core markets to high barrier to entry/core markets. Since 2005, the Company has sold over 124,000166,000 apartment units primarily in its non-core markets for an aggregate sales price of approximately $10.0$16.1 billion, acquired over 42,00067,000 apartment units primarily in its core markets for approximately $9.4$19.5 billion and began approximately $2.7$5.3 billion of development projects primarily in its core markets. We are currently seeking to acquire and develop assets primarily in the following targetedsix core coastal metropolitan areas: Boston, New York, Washington DC, South Florida,D.C., Southern California, San Francisco and Seattle. We also have investments (in the aggregate about 19.2%12.1% of our NOI at December 31, 2011)2014) in otherthe two core markets includingof South Florida and Denver Atlanta, Phoenix, New England (excluding Boston), Orlando and Jacksonville but do not currently intend to acquire or develop new assets in these markets. Further, we are in the process of exiting Phoenix and Orlando and will use sales proceeds from these markets to acquire and/or develop new assets and for other corporate purposes.

As part of its strategy, the Company purchases completed and fully occupied apartment properties, partially completed or partially occupied properties and takes options on land or acquires land on which apartment properties can be constructed. We intend to hold a diversified portfolio of assets across our target markets. As of December 31, 2011,2014, no single market/metropolitan area accounted for more than 15.3%17.5% of our NOI, though no guarantee can be made that NOI concentration may not increase in the future.

We endeavor to attract and retain the best employees by providing them with the education, resources and opportunities to succeed. We provide many classroom and on-line training courses to assist our employees in interacting with prospects and residents as well as extensively train our customer service specialists in maintaining theour properties and improvements, equipment and appliances on our property sites.appliances. We actively promote from within and many senior corporate and property leaders have risen from entry level or junior positions. We monitor our employees' engagement by surveying them annually and have consistently received high engagement scores.

We have a commitment to sustainability and consider the environmental impacts of our business activities. Sustainability and social responsibility are key drivers of our focus on creating the best apartment communities for residents to live, work and play. We have a dedicated in-house team that initiates and applies sustainable practices in all aspects of our business, including transactions,investment activities, development, property operations and property management activities. With its high density, multifamily housing is, by its nature, an environmentally friendly property type. Our recent acquisition and development activities have been

primarily concentrated in pedestrian-friendly urban locations near public transportation. When developing and renovating our properties, we strive to reduce energy and water usage by investing in energy saving technology while positively impacting the experience of our residents and the value of our assets. We continue to implement a combination of irrigation, lighting, HVAC and HVACrenewable energy improvements at our properties that will reduce energy and water consumption. The Company was recently named as the 2014 North American Residential – Large Cap Sector Leader by the Global Real Estate Sustainability Benchmark ("GRESB") survey, a globally recognized analysis of the sustainability indicators of approximately 650 real estate portfolios worldwide. For additional information regarding our sustainability efforts, see our December 2014 Corporate Social Responsibility and Sustainability Report at our website, www.equityresidential.com.

Competition

All of the Company's properties are located in developed areas that include other multifamily properties. The number of competitive multifamily properties in a particular area could have a material effect on the Company's ability to lease apartment units at the properties or at any newly acquiredits properties and on the rents charged. The Company may be competing with other entities that have greater resources than the Company and whose managers have more experience than the Company's managers. In addition, other forms of rental properties and single family housing provide housing alternatives to potential residents of multifamily properties. See Item 1A. Risk Factorsfor additional information with respect to competition.

Archstone Transaction

TableOn February 27, 2013, the Company, AvalonBay Communities, Inc. (“AVB”) and certain of Contentstheir respective subsidiaries completed their previously announced acquisition (the “Archstone Acquisition” or the "Archstone Transaction") from Archstone Enterprise LP (“Enterprise”) (which subsequently changed its name to Jupiter Enterprise LP), an affiliate of Lehman Brothers Holdings Inc. (“Lehman”) and its affiliates, of all of the assets of Enterprise (including interests in various entities affiliated with Enterprise), constituting a portfolio of apartment properties and other assets (the “Archstone Portfolio”). As a result of the Archstone Acquisition, the Company owns assets representing approximately 60% of the Archstone Portfolio. The consideration paid by the Company in connection with the Archstone Acquisition consisted of cash of approximately $4.0 billion (inclusive of $2.0 billion of Archstone secured mortgage principal paid off in conjunction with the closing), 34,468,085 Common Shares (which shares had a total value of $1.9 billion based on the February 27, 2013 closing price of EQR common shares of $55.99 per share) issued to the seller and the assumption of approximately $3.1 billion of mortgage debt (inclusive of a net mark-to-market premium of $127.9 million) and approximately 60% of all of the other assets and liabilities related to the Archstone Portfolio. See Note 4 in the Notes to Consolidated Financial Statements for further discussion.

Debt and Equity Activity

EQR issues public equity from time to time and guarantees certain debt of ERPOP. EQR does not have any indebtedness as all debt is incurred by the Operating Partnership. In addition, ERPOP issues OP Units and preference interests ("Preference Units") from time to time.

Please refer to Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations,, for the Company’s and the Operating Partnership's Capital Structure charts as of December 31, 2011.2014.

Major Debt and Equity Activities for the Years Ended December 31, 2011, 20102014, 2013 and 20092012

During 20112014:

| |

| ▪ | The Company redeemed $482.5 million of its 3.85% unsecured notes with a final maturity of 2026 at par and no premium was paid and repaid $93.1assumed $28.9 million of 6.95% unsecured notes at maturity. mortgage debt on one property. |

| |

| ▪ | The Company repaid $100.7 million of mortgage debt. |

| |

| ▪ | The Company repaid $500.0 million of 5.250% unsecured notes at maturity. |

| |

| ▪ | The Company repaid its $750.0 million unsecured term loan facility in conjunction with the note issuances discussed below. |

| |

| ▪ | The Company issued $1.0 billion$450.0 million of ten-year 4.625%five-year 2.375% fixed rate public notes, in a public offering, receiving net proceeds of $996.2$449.6 million before underwriting fees and other expenses. The notes haveexpenses, at an all-in effective interest rate of approximately 6.2%2.52% and swapped the notes to a floating interest rate in conjunction with the issuance (see Note 9 in the Notes to Consolidated Financial Statements for further discussion). |

| |

| ▪ | The Company issued $750.0 million of thirty-year 4.50% fixed rate public notes, receiving net proceeds of $744.7 million before underwriting fees, hedge termination costs and other expenses, at an all-in effective interest rate of 4.57% after termination of various forward starting swaps in conjunction with the issuance (see Note 89 in the Notes to Consolidated Financial Statements for further discussion). |

| |

| ▪ | The Company issued 2,086,380 Common Shares pursuant to its Share Incentive Plans and received net proceeds of approximately $82.6 million. |

| |

| ▪ | The Company issued 68,807 Common Shares pursuant to its Employee Share Purchase Plan and received net proceeds of approximately $3.4 million. |

| |

| ▪ | The Company repurchased and retired 31,240 of its Common Shares at a price of $56.87 per share for total consideration of $1.8 million (all related to the vesting of employee restricted shares). See Note 3 in the Notes to Consolidated Financial Statements for further discussion. |

During 2013:

| |

| ▪ | The Company assumed as part of the Archstone Transaction $2.2 billion of mortgage debt held in two Fannie Mae loan pools, consisting of $1.2 billion collateralized by 16 properties with an interest rate of 6.256% and a maturity date of November 1, 2017 ("Pool 3") and $963.5 million collateralized by 15 properties with an interest rate of 5.883% and a maturity date of November 1, 2014 ("Pool 4"). |

| |

| ▪ | The Company paid down $825.0 million of Pool 3 mortgage debt and repaid $963.5 million of Pool 4 mortgage debt. |

| |

| ▪ | The Company assumed as part of the Archstone Transaction $346.6 million of tax-exempt bonds on four properties with interest rates ranging from SIFMA plus 0.860% to SIFMA plus 1.402% and maturity dates through November 15, 2036. |

| |

| ▪ | The Company assumed as part of the Archstone Transaction $339.0 million of other mortgage debt on three properties with fixed interest rates ranging from 0.100% to 5.240% and maturity dates through May 1, 2061. |

| |

| ▪ | The Company assumed as part of the Archstone Transaction $34.1 million of other mortgage debt on one property with a variable rate of LIBOR plus 1.75% and a maturity date of September 1, 2014. |

| |

| ▪ | The Company obtained an $800.0 million secured loan from a large insurance company which matures on November 10, 2023, is interest only and carries a fixed interest rate of 4.21% and was used in part to pay down Pool 3. |

| |

| ▪ | The Company repaid $400.0 million of 5.200% unsecured notes at maturity. |

| |

| ▪ | The Company issued 3,866,666$500.0 million of ten-year 3.00% fixed rate public notes, receiving net proceeds of $495.6 million before underwriting fees and other expenses, at an all-in effective interest rate of 3.998%. |

| |

| ▪ | The Company entered into a senior unsecured $750.0 million delayed draw term loan facility which was fully drawn on February 27, 2013 in connection with the Archstone Acquisition. The maturity date of January 11, 2015 was subject to a one-year extension option exercisable by the Company. The interest rate on advances under the term loan facility generally was LIBOR plus a spread (1.20%), which was dependent on the credit rating of the Company's long-term debt. The facility was paid off in the second quarter of 2014. |

| |

| ▪ | The Company issued 34,468,085 Common Shares to an affiliate of Lehman having a value of $1.9 billion (based on the February 27, 2013 closing price of EQR Common Shares of $55.99 per share) as partial consideration for the portion of the Archstone Portfolio acquired by the Company. Lehman has since sold all of these Common Shares. |

| |

| ▪ | The Company issued 586,017 Common Shares pursuant to its Share Incentive Plans and received net proceeds of approximately $17.3 million. |

| |

| ▪ | The Company issued 73,468 Common Shares pursuant to its Employee Share Purchase Plan and received net proceeds of approximately $3.4 million. |

During 2012:

The Company repaid $253.9 million of 6.625% unsecured notes and $222.1 million of 5.500% unsecured notes, both at maturity.

The Company repaid its $500.0 million term loan at maturity.

In connection with the Archstone Transaction, the Company issued 21,850,000 Common Shares at a price of $54.75 per share for total consideration of approximately $1.2 billion, after deducting underwriting commissions of $35.9 million. See Note 3 in the Notes to Consolidated Financial Statements for further discussion.

| |

| ▪ | The Company issued 3,173,919 Common Shares at an average price of $52.23$60.59 per share for total consideration of $201.9$192.3 million pursuant to its At-The-Market (“ATM”) share offering program. See Note 3 in the Notes to Consolidated Financial Statements for further discussion. |

| |

| ▪ | The Company issued 2,945,9481,608,427 Common Shares pursuant to its Share Incentive Plans and received net proceeds of approximately $95.3$49.0 million. |

| |

| ▪ | The Company issued 113,1071,081,797 OP Units having a value of $66.6 million (based on the closing price for Common Shares of $61.57 on such date) as partial consideration for the acquisition of one rental property. |

| |

| ▪ | The Company issued 110,054 Common Shares pursuant to its Employee Share Purchase Plan and received net proceeds of approximately $5.3 million. |

During 2010:

| |

▪ | The Company issued $600.0 million of ten-year 4.75% fixed rate public notes in a public offering at an all-in effective interest rate of 5.09%, receiving net proceeds of $595.4 million before underwriting fees and other expenses. |

| |

▪ | The Company issued 6,151,198 Common Shares at an average price of $47.45 per share for total consideration of $291.9 million pursuant to its ATM share offering program. See Note 3 in the Notes to Consolidated Financial Statements for further discussion. |

| |

▪ | The Company issued 2,506,645 Common Shares pursuant to its Share Incentive Plans and received net proceeds of approximately $71.6$5.4 million. |

| |

| ▪ | The Company issued 157,363 Commonredeemed its Series N Cumulative Redeemable Preferred Shares pursuant to its Employee Share Purchase Plan and received net proceeds of approximately $5.1 million. |

| |

▪ | The Company repurchased and retired 58,130 of its Common Shares at an average price of $32.46 per share for totalcash consideration of $1.9$150.0 million (all related toplus accrued dividends through the vesting of employee restricted shares). See Note 3 in the Notes to Consolidated Financial Statements for further discussion.redemption date. |

During 2009:

| |

▪ | The Company obtained $500.0 million of mortgage loan proceeds through the issuance of an 11 year (stated maturity date of July 1, 2020) cross-collateralized loan with an all-in fixed interest rate for 10 years at approximately 5.6% secured by 13 properties. |

| |

▪ | The Company issued 3,497,300 Common Share at an average price of $35.38 per share for total consideration of $123.7 million pursuant to its ATM share offering program. See Note 3 in the Notes to Consolidated Financial Statements for further discussion. |

| |

▪ | The Company issued 422,713 Common Shares pursuant to its Share Incentive Plans and received net proceeds of approximately $9.1 million. |

| |

▪ | The Company issued 324,394 Common Shares pursuant to its Employee Share Purchase Plan and received net proceeds of approximately $5.3 million. |

| |

▪ | The Company repurchased and retired 47,450 of its Common Shares at an average price of $23.69 per share for total consideration of $1.1 million (all related to the vesting of employee restricted shares). See Note 3 in the Notes to Consolidated Financial Statements for further discussion. |

| |

▪ | The Company repurchased $75.8 million of its 5.20% fixed rate tax-exempt notes. |

| |

▪ | The Company repurchased at par $105.2 million of its 4.75% fixed rate public notes due June 15, 2009. In addition, the Company repaid the remaining $122.2 million of its 4.75% fixed rate public notes at maturity. |

| |

▪ | The Company repurchased $185.2 million at par and $21.7 million at a price of 106% of par of its 6.95% fixed rate public notes due March 2, 2011. |

| |

▪ | The Company repurchased $146.1 million of its 6.625% fixed rate public notes due March 15, 2012 at a price of 108% of par. |

| |

▪ | The Company repurchased $127.9 million of its 5.50% fixed rate public notes due October 1, 2012 at a price of 107% of par. |

| |

▪ | The Company repurchased $17.5 million of its 3.85% convertible fixed rate public notes due August 15, 2026 (putable in 2011) at a price of 88.4% of par. In addition, the Company repurchased $48.5 million of these notes at par. |

EQR contributed all of the net proceeds of the above equity offerings to ERPOP in exchange for OP Units or preference units.

During the first quarter of 2012 through February 17, 2012, the Company has issued approximately 2.1 million Common Shares at an average price of $59.47 per share for total consideration of approximately $123.6 million through the ATM share offering program.

An unlimited amount of equity and debt securities remains available for issuance by EQR and ERPOP under effective shelf registration statements filed with the SEC. Most recently, EQR and ERPOP filed acurrently have an active universal shelf registration statement for an unlimited amountthe issuance of equity and debt securities that automatically became automatically effective upon filing with the SEC in October 2010on July 30, 2013 and expires on October 15, 2013. However, asJuly 30, 2016. In July 2013, the Board of February 17, 2012, issuancesTrustees also approved an increase to the amount of shares which may be offered under the ATM share offering program are limited to 7.113.0 million additional shares.Common Shares and extended the program maturity to July 2016. Per the terms of ERPOP's partnership agreement, EQR contributes the net proceeds of all equity offerings to the capital of ERPOP in exchange for additional OP Units (on a one-for-one Common Share per OP Unit basis) or preference units (on a one-for-one preferred share per preference unit basis).

On June 16, 2011, the shareholders of EQR approved the Company's 2011 Share Incentive Plan (the "2011 Plan") and the Company has filed a Form S-8 registration statement to register 12,980,741 Common Shares under this plan. As of December 31, 2011, 12,473,580 shares were available for future issuance. See Note 12 in the Notes to Consolidated Financial Statements for further discussion.

Credit Facilities

EQR does not have any indebtedness as all debt is incurred by the Operating Partnership. EQR guarantees the Operating Partnership'sPartnership’s revolving credit facility up to the maximum amount and for the full term of the facility.

In July 2011,On January 11, 2013, the Company replaced its then existing unsecured revolving credit$1.75 billion facility with a new $1.25$2.5 billion unsecured revolving credit facility maturing on July 13, 2014, subject to a one-year extension option exercisable by the Company.April 1, 2018. The Company has the ability to increase available borrowings by an additional $500.0$500.0 million by adding additional banks to the facility or obtaining the agreement of existing banks to increase their commitments. The interest rate on advances under the new credit facility will generally be LIBOR plus a spread (currently 1.15%1.05%) and the Company pays an annual facility fee of 0.2%(currently 15 basis points). Both the spread and the facility fee are dependent on the credit rating of the Company's long-term debt. This

In July 2011, the Company replaced its then existing unsecured revolving credit facility with a new $1.25 billion unsecured revolving credit facility maturing on July 13, 2014, subject to a one-year extension option exercisable by the Company. The Company had the ability to increase available borrowings by an additional $500.0 million by adding additional banks to the facility or obtaining the agreement of existing banks to increase their commitments. On January 6, 2012, the Company amended this credit facility to increase available borrowings by an additional $500.0 million to $1.75 billion with all other terms, including the July 13, 2014 maturity date, remaining the same. The interest rate on advances under the credit facility was generally LIBOR plus a spread (1.15%) and the Company paid an annual facility fee of 0.2%. Both the spread and the facility fee were dependent on the credit rating of the Company's long-term debt. The facility had replaced the Company's existing $1.425previous $1.425 billion facility which was scheduled to mature in February 2012.2012.

As of December 31, 2011,February 20, 2015, the amount available on the new credit facility was $1.22$1.94 billion (net of $31.8$43.8 million which was restricted/dedicated to support letters of credit)credit, net of $300.0 million outstanding on the credit facility and there was no amount outstanding. Duringnet of $220.0 million outstanding on the year ended December 31, 2011,commercial paper program) (see Note 18 in the weighted average interest rate was 1.42%Notes to Consolidated Financial Statements for additional discussion of the commercial paper program). As of December 31, 2010,2014, the amount available on the old credit facility was $1.28$2.12 billion (net of $147.3$43.8 million which was restricted/dedicated to support letters of credit and net of $75.0$333.0 million which had been committed by a now bankrupt financial institution and was not available for borrowing) and there was no amount outstanding. outstanding). During the year ended December 31, 2010,2014, the weighted average interest rate was 0.66%0.95%.

See Note 18 for discussion As of December 31, 2013, the amount available on the increase of available borrowings on the new $1.25 billion unsecured revolving credit facility was $2.35 billion (net of $34.9 million which was restricted/dedicated to support letters of credit and net of $115.0 million outstanding). During the new senior unsecured $500.0 million delayed draw term loan facility.year ended December 31, 2013, the weighted average interest rate was 1.26%.

Environmental Considerations

See Item 1A. Risk Factorsfor information concerning the potential effects of environmental regulations on our operations.

Item 1A. Risk Factors

General

References to "EQR" mean Equity Residential, a Maryland real estate investment trust ("REIT"), and references to "ERPOP" mean ERP Operating Limited Partnership, an Illinois limited partnership. Unless otherwise indicated, when used in this section, the terms “Company,” “we,” “us” or “our” mean collectively EQR, ERPOP and those entities/subsidiaries owned or controlled by EQR and/or ERPOP and the term “Operating Partnership” means collectively ERPOP and those entities/subsidiaries owned or controlled by ERPOP. This Item 1A. includes forward-looking statements. You should refer to our discussion of the qualifications and limitations on forward-looking statements included in Item 7.

The occurrence of the events discussed in the following risk factors could adversely affect, possibly in a material manner, our business, financial condition or results of operations, which could adversely affect the value of our common shares of beneficial interest or preferred shares of beneficial interest (which we refer to collectively as “Shares”), preferencePreference Units, OP Units, restricted units limited partnership interests in the Operating Partnership (“OP Units”),(formerly known as Long-Term Incentive Plan Units (“LTIP Units”("LTIP") Units) and our public unsecured debt. In this section, we refer to the Shares, preference units,Preference Units, OP Units, LTIP Unitsrestricted units and public unsecured debt together as our “securities” and the investors who own Shares/Units, OP/LTIP Units and public unsecured debtsuch securities as our “security holders”.

Our Performanceperformance and Securities Valuesecurities value are Subjectsubject to Risks Associatedrisks associated with the Real Estate Industryreal estate industry.

General

Real property investments are subject to varying degrees of risk and are relatively illiquid. Numerous factors may adversely affect the economic performance and value of our properties and the ability to realize that value. These factors include changes in the global, national, regional and local economic climates, local conditions such as an oversupply of multifamily properties or a reduction in demand for our multifamily properties, the attractiveness of our properties to residents, competition from other multifamily properties and single family homes and changes in market rental rates. Our performance also depends on our ability to collect rent from residents and to pay for adequate maintenance, insurance and other operating costs, including real estate taxes, all of which could increase over time. These operating expenses could rise faster than our revenues causing our income to decline. Sources of labor and materials required for maintenance, repair, capital expenditure or development may be more expensive than anticipated. Also, the expenses of owning and operating a property are not necessarily reduced when circumstances such as market factors and competition cause a reduction in income from the property.

We May Not Have Sufficient Cash Flows From Operations After Capital Expenditures to Cover Our Distributions and Our Dividend Policy May Lead to Quicker Dividend Reductions

We generally consider our cash flows provided by operating activities after capital expenditures to be adequate to meet operating requirements and payment of distributions to our security holders. However, there may be times when we experience shortfalls in our coverage of distributions, which may cause usunable to consider reducing our distributions and/renew leases or using the proceeds from property dispositions or additional financing transactions to make up the difference. Should these shortfalls occur for lengthy periods of time or be material in nature, our financial condition may be adversely affected and we may not be able to maintain our current distribution levels. While our dividend policy makes it less likely we will over distribute, it will also lead to a dividend reduction more quickly than a fixed dividend policy should operating results deteriorate. See Item 7 for additional discussion regarding our dividend policy.

We May Be Unable to Renew Leases or Relet Apartment Unitsrelet units as Leases Expireleases expire.

When our residents decide to leave our apartments, whether because they decide not to renew their leases or they leave prior to their lease expiration date, we may not be able to relet their apartment units. Even if the residents do renew or we can relet the apartment units, the terms of renewal or reletting may be less favorable than current lease terms. If we are unable to promptly renew the leases or relet the apartment units, or if the rental rates upon renewal or reletting are significantly lower than expected rates, then our results of operations and financial condition will be adversely affected. If residents do not experience increases in their income, we may be unable to increase rent and/or delinquencies may increase. Occupancy levels and market rents may be adversely affected by national and local economic and market conditions including, without limitation, new construction and excess inventory of multifamily and single family housing, increasing portions of single family housing stock being converted to rental use, rental housing subsidized by the government, other

government programs that favor single family rental housing or owner occupied housing over multifamily rental housing, governmental regulations, slow or negative employment growth and household formation, the availability of low interestlow-interest mortgages or the availability of mortgages requiring little or no down payment for single family home buyers, changes in social preferences and the potential for geopolitical instability, all of which are beyond the Company's control. In addition, various state and local municipalities are considering and may continue to consider rent control legislation or take other actions which could limit our ability to raise rents. Finally, the federal government's policies, many of which may encourage home ownership, can increase competition and possibly limit our ability to raise rents. Consequently, our cash flow and ability to service debt and make distributions to security holders could be reduced.

The retail/commercial space at our properties primarily serves as an additional amenity for our residents. The long term nature of our retail/commercial leases (generally five to ten years with market based renewal options) and the characteristics of many of our tenants (generally small, local businesses) may subject us to certain risks. We may not be able to lease new space for rents that are consistent with our projections or for market rates. Also, when leases for our existing retail/commercial space expire, the space may not be relet or the terms of reletting, including the cost of allowances and concessions to tenants, may be less favorable than the current lease terms. Our properties compete with other properties with retail/commercial space. The presence

of competitive alternatives may affect our ability to lease space and the level of rents we can obtain. If our retail/commercial tenants experience financial distress or bankruptcy, they may fail to comply with their contractual obligations, seek concessions in order to continue operations or cease their operations which could adversely impact our results of operations and financial condition. The revenues from our retail/commercial space represent approximately 4% of our total rental income.

We have increased our concentration of properties in certain core markets, which could have an adverse effect on our operations if a particular market is adversely affected by economic or other conditions.

We have increased our concentration of properties in certain core markets as a result of our strategy to reposition our portfolio from low barrier to entry/non-core markets to high barrier to entry/core markets. If any one or more of our core markets (Boston, New AcquisitionsYork, Washington D.C., Southern California, San Francisco, Seattle, South Florida and Denver) is adversely affected by local or regional economic conditions (such as business layoffs, industry slowdowns, changing demographics and other factors) or local real estate conditions (such as oversupply of or reduced demand for multifamily properties), such conditions may have an increased adverse impact on our results of operations than if our portfolio was more geographically diverse.

Because real estate investments are illiquid, we may not be able to sell properties when appropriate.

Real estate investments generally cannot be sold quickly. We may not be able to reconfigure our portfolio promptly in response to economic or other conditions. This inability to reallocate our capital promptly could adversely affect our financial condition and ability to make distributions to our security holders.

New acquisitions, development projects and/or Development Projects May Failrehabs may fail to Performperform as Expectedexpected and Competitioncompetition for Acquisitions May Resultacquisitions may result in Increased Pricesincreased prices for Propertiesproperties.

We intend to actively acquire, and/or develop and rehab multifamily properties for rental operations as market conditions dictate. We may also acquire multifamily properties that are unoccupied or in the early stages of lease up. We may be unable to lease up these apartment properties on schedule, resulting in decreases in expected rental revenues and/or lower yields due to lower occupancy and rates as well as higher than expected concessions.concessions or higher than expected operating expenses. We may not be able to achieve rents that are consistent with expectations for acquired, developed or rehabbed properties. We may underestimate the costs necessary to bring an acquired property up to standards established for its intended market position, to complete a development property or to complete a development property.rehab. Additionally, we expect that other real estate investors with capital will compete with us for attractive investment opportunities or may also develop properties in markets where we focus our development and acquisition efforts. This competition (or lack thereof) may increase (or depress) prices for multifamily properties. We may not be in a position or have the opportunity in the future to make suitable property acquisitions on favorable terms. We have acquired in the past and intend to continue to pursue the acquisition of properties and portfolios of properties, including large portfolios, that could increase our size and result in alterations to our capital structure. The total number of apartment units under development, costs of development and estimated completion dates are subject to uncertainties arising from changing economic conditions (such as the cost of labor and construction materials), competition and local government regulation.

In connection with such government regulation, we may incur liability if our properties are not constructed and operated in compliance with the accessibility provisions of the Americans with Disabilities Act, the Fair Housing Act or other federal, state or local requirements. Noncompliance could result in fines, subject us to lawsuits and require us to remediate or repair the noncompliance.

Risks Involved in Real Estate Activity Through Joint VenturesDevelopment and construction risks could affect our profitability.

We intend to continue to develop multifamily properties. These activities can include long planning and entitlement timelines and can involve complex and costly activities, including significant environmental remediation or construction work in high-density urban areas. We may abandon opportunities that we have already begun to explore for a number of reasons, including changes in local market conditions or increases in construction or financing costs, and, as a result, we may fail to recover expenses already incurred in exploring those opportunities. The occupancy rates and rents at a property may fail to meet our original expectations for a number of reasons, including changes in market and economic conditions beyond our control and the pastdevelopment by competitors of competing properties. We may be unable to obtain, or experience delays in obtaining, necessary zoning, occupancy, or other required governmental or third party permits and authorizations, which could result in increased costs or the delay or abandonment of opportunities.

Our investments in joint ventures could be adversely affected by our lack of sole decision-making authority regarding major decisions, our reliance on our joint venture partners' financial condition, any disputes that may arise between us and our joint venture partners and our exposure to potential losses from the actions of our joint venture partners.

We currently do and may continue in the future to develop and acquire properties in joint ventures with other persons or entities when we believe circumstances warrant the use of such structures. A portion of the assets acquired in the Archstone Transaction were acquired through joint ventures with AVB that neither we nor AVB control solely. We have several joint ventures with other real estate investors. Joint venture investments, including the joint ventures with AVB, involve risks not present with respect to our wholly owned properties, including the possibility that following:

our joint venture partners might refuseexperience financial distress, become bankrupt or fail to makefund their share of required capital contributions, when due; that which may delay construction or development of a property or increase our financial commitment to the joint venture;

we may be responsible to our partners for indemnifiable losses; that

our joint venture partners might at any timemay have business interests or economicgoals with respect to a property that conflict with our business interests and goals, which could increase the likelihood of disputes regarding the ownership, management or disposition of the property;

we may be unable to take actions that are inconsistent with ours;opposed by our joint venture partners under arrangements that require us to share decision-making authority over major decisions affecting the ownership or operation of the joint venture and that any property owned by the joint venture, such as the sale or financing of the property or the making of additional capital contributions for the benefit of the property;

our joint venture partners may betake actions that we oppose;

our ability to sell or transfer our interest in a positionjoint venture to take actiona third party may be restricted without prior consent of our joint venture partners;

we may disagree with our joint venture partners about decisions affecting a property or withhold consent contrarythe joint venture, which could result in litigation or arbitration that increases our expenses, distracts our officers and disrupts the day-to-day operations of the property, including by delaying important decisions until the dispute is resolved; and

we may suffer losses as a result of actions taken by our joint venture partners with respect to our instructions or requests.joint venture investments.

At times we have entered into agreements providing for joint and several liability with our partners. Frequently, we and our partners may each have the right to trigger a buy-sell arrangement, which could cause us to sell our interest, or acquire our partners' interest, at a time when we otherwise would not have initiated such a transaction. In some instances,Any of these risks could materially and adversely affect our ability to generate and recognize attractive returns on our joint venture partners mayinvestments, which could have competinga material adverse effect on our results of operations, financial condition and distributions to our shareholders.

Several of the assets we acquired in the Archstone Transaction along with certain preferred interests acquired in our markets that could create conflicts of interest. Further, the Company's joint venture partners may experience financial distress, including bankruptcy, and to the extent they do not meet their obligations to us or our joint ventures with them,AVB as part of the Archstone Transaction are subject to tax protection agreements, which could limit our flexibility with respect to our ownership of such assets or cause us to incur material costs.

Several of the assets we acquired in the Archstone Transaction were contributed to Archstone subject to various agreements limiting the ability of the owner of the property to take actions that would trigger income tax liability for the contributing owner of the property, including a taxable disposition of the property. In addition, we will also be required to maintain a certain amount of qualified nonrecourse financing on the tax protected properties during their respective restricted periods. Our obligations relating to the tax protected properties may be adversely affected.

Because Real Estate Investments Are Illiquid, We May Not Be Able to Sell Properties When Appropriate

Real estate investments generally cannot be sold quickly. Weaffect the way in which we conduct our business, including whether, when and under what circumstances we sell properties or interests therein and the timing and nature of our financings and refinancing transactions. As a result, we may not be able to reconfiguredispose of or refinance the tax protected properties when to do so may have otherwise been favorable to us and our portfolio promptlyshareholders, which could have a material adverse effect on our results of operations and financial condition. Certain preferred interests acquired in responsejoint ventures with AVB as part of the Archstone Transaction have complex tax requirements that, if violated, may cause us to economic or other conditions. This inabilitybe required to reallocate our capital promptlyindemnify the preferred stockholders for certain tax protection costs.

Changes in market conditions and volatility of share prices could adversely affect the market price of our financial condition and ability to make distributions to our security holders.

The Value of Investment Securities Could Result In Losses to the Company

From time to time, the Company holds investment securities and/or cash investments that have a higher risk profile than the government obligations and bond funds, money market funds or bank deposits in which we generally invest. On occasion we may purchase securities of companies in our own industry as a means to invest funds. There may be times when we experience declines in the value of these investment securities, which may result in losses to the Company and our financial condition or results of operations could be adversely affected. Sometimes the cash we deposit at a bank exceeds the FDIC insurance limit resulting in risk to the Company of loss of funds if these banks fail.

Changes in Market Conditions and Volatility of Share Prices Could Adversely Affect the Market Price of Our Common SharesShares.

The stock markets, including the New York Stock Exchange, on which we list our Common Shares, have experienced significant price and volume fluctuations.fluctuations over time. As a result, the market price of our Common Shares could be similarly volatile, and investors in our Common Shares may experience a decrease in the value of their shares, including decreases unrelated to our

operating performance or prospects. The market price of our Common Shares may decline or fluctuate significantly in response to many factors, including but not limited to the following:

general market and economic conditions;

actual or anticipated variations in our guidance, quarterly operating results or dividends;

changes in our funds from operations, normalized funds from operations or earnings estimates;

difficulties or inability to access capital or extend or refinance debt;

large portfolio acquisitions or dispositions;

decreasing (or uncertainty in) real estate valuations;

rising crime rates in markets where our increasingly urban portfolio is concentrated;

a change in analyst and/or credit ratings;

adverse market reaction to any additional debt we incur in the future;

governmental regulatory action, including changes or proposed changes to the mandates of Fannie Mae or Freddie Mac, and changes in tax laws; and

the issuance of additional Common Shares, or the perception that such issuances might occur, including under EQR's ATM program.program; and

the resale of substantial amounts of our common shares, or the anticipation of the resale of such shares, by large holders of our securities.

We may not have sufficient cash flows from operations after capital expenditures to cover our distributions and our dividend policy may lead to quicker dividend reductions.

We generally consider our cash flows provided by operating activities after capital expenditures to be adequate to meet operating requirements and payment of distributions to our security holders. However, there may be times when we experience shortfalls in our coverage of distributions, which may cause us to consider reducing our distributions and/or using the proceeds from property dispositions or additional financing transactions to make up the difference. Should these shortfalls occur for lengthy periods of time or be material in nature, our financial condition may be adversely affected and we may not be able to maintain our current distribution levels. While our current dividend policy makes it less likely we will over distribute, it will also lead to a dividend reduction more quickly should operating results deteriorate. See Item 7 for additional discussion regarding our dividend policy.

The value of investment securities could result in losses to the Company.

From time to time, the Company holds investment securities and/or cash investments that have various levels of repayment and liquidity risk, including government obligations and bond funds, money market funds or bank deposits. On occasion we also may purchase securities of companies in our own industry as a means to invest funds. There may be times when we experience declines in the value of these investment securities, which may result in losses to the Company and our financial condition or results of operations could be adversely affected. Sometimes the cash we deposit at a bank substantially exceeds the FDIC insurance limit or we invest cash in money market or similar type funds with investment management institutions that may be subject to, now or in the future, liquidity restrictions, resulting in risk to the Company of loss or lack of immediate availability of funds if these banks or institutions fail to meet their obligations.

Any weaknesses identified in our internal control over financial reporting could have an adverse effect on our share price.

Section 404 of the Sarbanes-Oxley Act of 2002 requires us to evaluate and report on our internal control over financial reporting. If we identify one or more material weaknesses in our internal control over financial reporting, we could lose investor confidence in the accuracy and completeness of our financial reports, which in turn could have an adverse effect on our share price.

The occurrence of cyber incidents, or a deficiency in our cybersecurity, could negatively impact our business by causing a disruption to our operations, a compromise or corruption of our confidential information, and/or damage to our reputation and business relationships, all of which could negatively impact our financial results.

A cyber incident is considered to be any adverse event that threatens the confidentiality, integrity or availability of our information resources. More specifically, a cyber incident is an intentional attack or an unintentional event that can include gaining unauthorized access to systems to disrupt operations, corrupt data or steal confidential information, including information regarding our residents and employees. As our reliance on technology has increased, so have the risks posed to our systems, both internal and those we have outsourced to third party service providers. In addition, information security risks have generally increased in recent years due to the rise in new technologies and the increased sophistication and activities of perpetrators of cyber attacks. Our primary risks that could directly result from the occurrence of a cyber incident include operational interruption, damage to our reputation, damage to our business relationships with our residents/tenants and private data exposure. We have implemented processes, procedures and controls to help mitigate these risks, but these measures, as well as our increased awareness of a risk of a cyber incident, do not guarantee that our financial results will not be negatively impacted by such an incident.

Changes in Lawslaws and Litigation Risk Could Affect Our Businesslitigation risk could affect our business.

We are generally not able to pass through to our residents under existing leases any real estate or other federal, state or local taxes. Consequently, any such tax increases may adversely affect our financial condition and limit our ability to make distributions to our security holders.

We may become involved in legal proceedings, including but not limited to, proceedings related to consumer, shareholder, employment, environmental, development, condominium conversion, tort and commercial legal issues that, if decided adversely to or settled by us, could result in liability material to our financial condition or results of operations.

Any Weaknesses Identified in Our Internal Control Over Financial Reporting Could Have an Adverse Effect on Our Share Price

Section 404 of the Sarbanes-Oxley Act of 2002 requires us to evaluateEnvironmental problems are possible and report on our internal control over financial reporting. If we identify one or more material weaknesses in our internal control over financial reporting, we could lose investor confidence in the accuracy and completeness of our financial reports, which in turn could have an adverse effect on our share price.

Environmental Problems Are Possible and Can Be Costlycan be costly.

Federal, state and local laws and regulations relating to the protection of the environment may require a current or previous owner or operator of real estate to investigate and clean up hazardous or toxic substances or petroleum product releases at such property. The owner or operator may have to pay a governmental entity or third parties for property damage and for investigation and clean-up costs incurred by such parties in connection with the contamination. These laws typically impose clean-up responsibility and liability without regard to whether the owner or operator knew of or caused the presence of the contaminants. Even if more than one person may have been responsible for the contamination, each person covered by the environmental laws may be held responsible for all of the clean-up costs incurred. In addition, third parties may sue the owner or operator of a site for damages and costs resulting from environmental contamination emanating from that site.

Substantially all of our properties have been the subject of environmental assessments completed by qualified independent environmental consulting companies. While these environmental assessments have not revealed, nor are we aware of, any environmental liability that our management believes would have a material adverse effect on our business, results of operations, financial condition or liquidity, there can be no assurance that we will not incur such liabilities in the future.

TableWe are aware that some of Contentsour properties have lead paint and have implemented an operations and maintenance program at each of those properties. While we do not currently anticipate that we will incur any material liabilities as a result of the presence of lead paint at our properties, there can be no assurance that we will not incur such liabilities in the future.There have been an increasinga number of lawsuits against owners and managers of multifamily properties alleging personal injury and property damage caused by the presence of mold in residential real estate. As some of these lawsuits have resulted in substantial monetary judgments or settlements, insurance carriers have reacted by excluding mold-related claims from standard policies and pricing mold endorsements at prohibitively high rates. While we have adopted programs designed to minimize the existence of mold in any of our properties as well as guidelines for promptly addressing and resolving reports of mold to minimize any impact mold might have on our residents or the property, should mold become an issue in the future, our financial condition or results of operations may be adversely affected.

We cannot be assured that existing environmental assessments of our properties reveal all environmental liabilities, that any prior owner of any of our properties did not create a material environmental condition not known to us, or that a material environmental condition does not otherwise exist as to any of our properties.

Climate Changechange

To the extent that climate change does occur, we may experience extreme weather and changes in precipitation and temperature, all of which may result in physical damage or a decrease in demand for properties located in these areas or affected by these conditions. Should the impact of climate change be material in nature, including destruction of our properties, or occur for lengthy periods of time, our financial condition or results of operations may be adversely affected.

In addition, changes in federal and state legislation and regulation on climate change could result in increased capital expenditures to improve the energy efficiency of our existing properties and could also require us to spend more on our new development properties without a corresponding increase in revenue.

Insurance Policy Deductibles, Exclusionspolicy deductibles, exclusions and Counterpartiescounterparties

As of December 31, 2011,2014, the Company's property insurance policy providespolicies provide for a per occurrence deductible of $250,000 and self-insured retention of $5.0 million per occurrence, subject to a maximum annual aggregate self-insured retention of $7.5 million, with approximately 80% of any excess losses being covered by insurance.$250,000. Any earthquake and named windstorm losses in critical areas are subject to a deductible of 5% of the values of the buildings involved in the losses. The Company also typically self-insures a substantial portion of the first $50 million of a property loss in excess of these base deductibles. Should a claim exceed these amounts, it would be 100% covered by insurance. Furthermore, the Company purchased additional coverage in the event that the Company suffers multiple non-catastrophic occurrences with losses and are not subjectfrom $25 million to $50 million within the aggregate self-insured retention.same policy year. The Company's general liability and worker's compensation policies at December 31, 20112014 provide for a $2.0 million and $1.0 million per occurrence deductible, respectively. These higher deductible and self-insured retention amounts do expose the Company to greater potential for uninsured losses. The Company also has become more susceptible to large losses but managementas it has reviewedtransformed its claims historyportfolio, becoming more concentrated in fewer, more valuable assets over the years and believes the savings in insurance premium expense justify this potential increased exposure over the long-term. However,a smaller geographical footprint. Furthermore, the potential impact of climate change, and increased severe weather or earthquakes could cause a significant increase in insurance premiums and deductibles, particularly for our coastal properties, or a decrease in the availability of coverage, either of which could expose the Company to even greater uninsured losses which may adversely affect our financial condition or results of operations.

As a result of the terrorist attacks of September 11, 2001, property insurance carriers created exclusions for losses from terrorism from our “all risk” property insurance policies. As of December 31, 2011, under a separate terrorism insurance policy, the

The Company was insured for $500.0also has $750.0 million in terrorism insurance coverage, with a $100,000 deductible. This coverage excludes losses from nuclear, biological and chemical attacks. In the event of a terrorist attack impacting one or more of our properties, we could lose the revenues from the property, our capital investment in the property and possibly face liability claims from residents or others suffering injuries or losses. The Company has become more susceptible to large losses as it has transformed its portfolio, becoming more concentrated in fewer, more valuable assets over a smaller geographical footprint.