Securities registered pursuant to Section 12(b) of the Act:

Name of each exchange | ||

Title of each class | on which registered | |

Common stock, par value $1 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X]x No [ ]o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ]o No [X]x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X]x No [ ]o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant'sregistrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a non-accelerated filer.smaller reporting company. See definitionthe definitions of “large accelerated filer,” “accelerated filerfiler” and large accelerated filer”“smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):Large accelerated filer [X] Accelerated filer [ ] Non-accelerated filer [ ]

Large accelerated filer | x | Accelerated filer | o |

Non-accelerated filer | o | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ]

o Yes [X]x No

The aggregate market value of the voting stock held by non-affiliates of the Registrant as of June 30, 2006,2008, was approximately $1.4$2.0 billion.

The number of shares outstanding of each of the Registrant'sRegistrant’s classes of Common stock as of January 31, 2007:2009:

Class | Number of shares | |

Common stock, par value $1 per share | 45,211,436 |

Page 2

INDEX TO FORM 10-K

Page | |||||

4 | |||||

18 | |||||

25 | |||||

26 | |||||

27 | |||||

27 | |||||

Market for the | |||||

| Purchases of Securities | 27 | ||||

28 | |||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 29 | ||||

49 | |||||

50 | |||||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 94 | ||||

94 | |||||

95 | |||||

96 | |||||

96 | |||||

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 96 | ||||

Certain Relationships and Related Transactions, and Director Independence | 96 | ||||

96 | |||||

96 | |||||

101 | |||||

102 | |||||

Page 3

FORWARD-LOOKING INFORMATIONSTATEMENTS

Except for historical information, this Annual Report on Form 10-K may be deemed to contain "forward-looking" information.“forward-looking” statements within the meaning of the Private Litigation Reform Act of 1995. Examples of forward-looking informationstatements include but are not limited to: (a) projections of or statements regarding return on investment, future earnings, interest income, other income, earnings or loss per share, growth prospects, capital structure, and other financial terms, (b) statements of plans and objectives of management, (c) statements of future economic performance, and (d) statements of assumptions, such as economic conditions underlying other statements. Such forward-looking information maystatement can be identified by the use of forward-looking terminology such as "believes," "expects," "may," "should," "anticipates,"“believes,” “expects,” “may,” “will,” “should,” “could,” “anticipates,” as well as the negative of any of the foregoing or variations of such terms or comparable terminology, or by discussion of strategy. No assurance may be given that the future results described by the forward-looking informationstatements will be achieved. Such statements are subject to risks, uncertainties, and other factors, which could cause actual results to differ materially from future results expressed or implied by such forward-looking information.statements. Such statements in this Annual Report on Form 10-K include, without limitation, those contained in Item 1. Business, Item 7. Management'sManagement’s Discussion and Analysis of Financial Condition and Results of Operations, Item 8. Financial Statements and Supplementary Data including, without limitation, the Notes To Consolidated Financial Statements, and Item 11. Executive Compensation. Important factors that could cause the actual results to differ materially from those in these forward-looking statements include, among other items:

•

the Corporation’s successful execution of internal performance plans and performance in accordance with estimates to complete;

•

performance issues with key suppliers, subcontractors, and business partners;

•

the ability to negotiate financing arrangements with lenders;

•

legal proceedings;

•

changes in the need for additional machinery and equipment and/or in the cost for the expansion of the Corporation’s operations;

•

ability of outside third parties to comply with their commitments;

•

product demand and market acceptance risks;

•

the effect of economic conditions;

•

the impact of competitive products and pricing, product development, commercialization, and technological difficulties;

•

social and economic conditions and local regulations in the countries in which the Corporation conducts its businesses;

•

unanticipated environmental remediation expenses or claims;

•

capacity and supply constraints or difficulties;

•

an inability to perform customer contracts at anticipated cost levels;

•

changing priorities or reductions in the U.S. and Foreign Government defense budgets;

•

contract continuation and future contract awards;

•

the other factors discussed under the caption “Risk Factors” in Item 1A below;

•

and other factors that generally affect the business of companies operating in the Corporation’s markets and/or industries.

These forward-looking statements speak only as of the

Corporation's successful execution of internal performance plans;performance issues with key suppliers, subcontractors,date they were made andbusiness partners;the

ability to negotiate financing arrangements with lenders;legal proceedings;changes in the need for additional machinery and equipment and/or in the cost for the expansion of theCorporation's operations;ability of outside third parties to comply with their commitments;product demand and market acceptance risks;the effect of economic conditions;the impact of competitive products and pricing;product development, commercialization, and technological difficulties;social and economic conditions and local regulations in the countries in which the Corporation conducts itsbusinesses;unanticipated environmental remediation expenses or claims;capacity and supply constraints or difficulties;an inability to perform customer contracts at anticipated cost levels;changing priorities or reductions in the U.S. Government defense budget;contract continuation and future contract awards;U.S. and international military budget constraints and determinations;the factors discussed under the caption “Risk Factors” in Item 1A below;and other factors that generally affect the business of companies operating in the Corporation's marketsand/or industries.

The Corporation assumes no obligation to update forward-looking statements to reflect actual results or changes in or additions to the factors affecting such forward-looking statements.

Page 4

BUSINESS DESCRIPTION

TheCurtiss-Wright Corporation manageswas incorporated in 1929 under the laws of the State of Delaware. We design and evaluates itsmanufacture highly engineered, advanced technologies that perform critical functions in demanding conditions in the defense, energy, commercial aerospace, and general industrial markets, where performance and reliability are essential. Our general industrial markets include high-performance automotive, construction, marine, and simulation and test equipment.

Our core competence is providing advanced technologies with superior reliability for customers operating in harsh environments. In addition to meeting demanding performance requirements, our technologies significantly improve worker safety, minimize environmental impact, and improve operating efficiency. Our products and services include critical-function pumps, valves, motors, generators, and electronics; aircraft flight controls, landing systems, ordnance handling, stabilization and utility actuation; as well as metallurgical enhancement of highly stressed components. We compete globally based on technology and pricing, however, significant engineering expertise is a limiting factor to competition, particularly in the U.S. government market. Our business success is challenged by price pressure, environmental impact, and geopolitical events, such as the global war on terrorism and diplomatic accords. Our ability to provide high-performance, advanced technologies on a cost-effective basis is fundamental to our strategy for meeting customer demand.

We manage and evaluate our operations based on the products and services it offerswe offer and the different markets it serves.we serve. Based on this approach, the Corporation haswe operate through three reportable segments: Flow Control, Motion Control, and Metal Treatment. Our principal manufacturing facilities are located in the United States in New York, North Carolina, and Pennsylvania, and internationally in Canada and the United Kingdom.

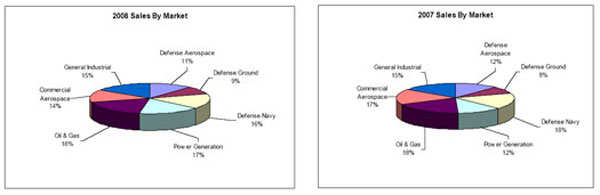

In 2008, we generated $1.8 billion in sales, an increase of 15% over 2007, which is a continuation of our double-digit sales rate growth in recent years. In the five years since 2003, we have attained a cumulative sales increase of 145%, or $1.1 billion, representing a compounded annual growth rate (CAGR) of 20%. This sales growth was achieved primarily through the acquisition of more than 20 businesses, with an aggregate purchase price of approximately $700 million, while producing organic sales growth each year ranging from 6% to 13%. During the same time period, operating income grew at an 17% CAGR, increasing from $89 million in 2003 to $197 million in 2008. We believe our ability to consistently grow operating income during this period of rapid growth illustrates our ability to integrate acquisitions quickly and profitability. We intend to continue to execute our growth strategy which focuses on diversification in complementary markets that demand high performance and highly engineered products and services.

Our strategy, initiated in 2000, was to minimize our dependence on the commercial aerospace market and expand into other key markets. The rebalancing of our business portfolio was the result of focusing growth initiatives in two robust markets: energy and defense. As a result of our growth, we have achieved a balanced business portfolio with revenues generated from defense, energy, commercial aerospace and general industrial markets. While we have diversified our business portfolio, we have also developed a new core competence in electronics technology. We believe our ability to design and develop future generations of advanced electronics systems is a strategic growth area for the high performance platforms in our served markets.

Flow Control

Our Flow Control segment primarily designs, manufactures, and distributes and services a broad rangeportfolio of highly engineered, flow-controlcritical-function products used in severe serviceincluding valves, pumps, motors, generators, instrumentation, and control electronics. These products manage the flow of liquids and gases, generate power, provide electronic operating systems, and monitor critical functions. Our primary markets are naval defense, and commercial markets including power generation, oil and gas and general industrial. The Motion Control segment primarily designs, develops, and manufactures high-performance mechanical systems, drive systems, embedded computing solutions, and electronic controls and sensors for the defense, aerospace,processing, and general industrial markets. Metal Treatment providesapplications. In the naval defense market, we are a variety of metallurgical services, principally shot peening, laser peening, heat treating, and specialty coatings, for various markets, including military and commercial aerospace, automotive, construction equipment, oil and gas, power generation, and general industrial.

Flow Control

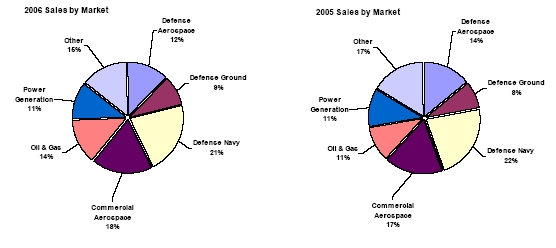

Curtiss-Wright Flow Control specializesglobal leader in the design and manufacture of highly engineered valves, pumps, motors, generators, electronics, and related products for the commercial nuclear power industry, oil and gas processing facilities,propulsion technologies and a range of critical national defense programs. Flow control products are mainly used bypreferred supplier to the U.S. Navy nuclear power plants, the oilfor their aircraft carrier and gas industry, and other commercial applications. While our markets are defined by advanced technology and significant engineering expertise, competition, especially in the U.S. governments’ market, is increasingly impacted by price concerns and geopolitical events, such as the war on terrorism. The ability to provide quality products with excellent performance coupled with our response to downward pricing pressure have become integral to meeting customer demand.submarine programs. Government sales, primarily to the U.S. Navy as a subcontractor, comprised 43%23%, 48%29%, and 50%43% of segment sales in 2008, 2007, and 2006, 2005,respectively. Revenues derived from the sales of valves during 2008, 2007 and 2004, respectively.2006 represented 20%, 22%, and 18%, respectively, of our consolidated revenue.

The Flow Control segment is made upconsists of 19 companies that are organized and21 business units managed through fourfive operating divisions: Electro-Mechanical Systems, Valve Systems, Control Systems, Commercial Power and Services, Electromechanical Systems, and ControlsOil and Gas Systems. The segment has a global customer base with principal manufacturing operations in the United States, Canada, and the United Kingdom.

The ValvePage 5

Our Electro-Mechanical Systems division produces high performance, specialized valveadvanced electro-mechanical solutions for the defense,U.S. Navy, Army, Coast Guard, commercial nuclear power generation, oil and gas processing, and other general industrial markets. The division designs and manufactures advanced critical function pumps, motors, generators, ship propulsors, mechanical seals, control rod drive mechanisms, power conditioning electronics, pulse power supplies, integrated motor-controls, composite materials applications, and protection technologies solutions.

This division develops, designs, manufactures, and performs qualification testing of critical-function, electro-dynamic solutions for its primary customer, the U.S. Nuclear Navy, including main coolant pumps, various other critical-function pumps, extremely power-dense compact motors, main and ship service generators, secondary propulsion systems, and design engineering and testing services. The division has served the U.S. Navy for over 60 years and is a sole source provider for various products. The division also overhauls and provides critical spares for units serving the fleet on operational platforms. Current platforms include the Nimitz and Ford class aircraft carriers, and Virginia, Los Angeles, Seawolf, and Ohio class submarines.

In addition, the division provides propulsion motors and main generators to the non-nuclear U.S. Navy, including the DDG1000 destroyer program. We are strengthening our relationship with the U.S. Navy by participating in the design and development of major subsystems for the U.S. Navy’s Electro-Mechanical Aircraft Launch System (EMALS), Advanced Arresting Gear (AAG) for installation in its future aircraft carrier fleet, and advanced condensate and feed systems designs for the next generation submarine fleet. We expanded our offerings to the military to now include advanced electro-magnetic product development for the U.S. Army as pulsed power technology continues to advance in the military weapons segment.

Electro-Mechanical Systems’ products are also sold to complementary commercial markets, primarily power generation and oil and gas. We have been a supplier to the nuclear power market since its inception more than 50 years ago. We provide reactor coolant pumps, pump seals, and control rod drive mechanisms for commercial nuclear power plants. In 2008, we announced our first domestic new construction contract for three Westinghouse AP1000 power plants to be built in the United States. In 2007, we announced our first award for reactor coolant pumps for for four new AP1000 nuclear power plants to be built in China. Combined, these awards are a significant milestone for both the nuclear power renaissance and the globalization of nuclear power technology. While the nuclear power supply base dwindled considerably during the last two decades due to limited new construction projects, we believe this new ramp up will result in increased competition from other nuclear component suppliers globally. We believe awards will be based on a combination of preferred systems designs, historical performance, and price.

In the oil and gas market, we are utilizing our canned motor and pumping system expertise and partnering with industry leaders to develop advanced systems for offshore recovery, production, and transmission. Current programs encompass sub-sea pumping and power-dense motors for compact, integrated compressor systems. This division has also expanded its offerings to include hazardous waste pumps for the Department of Energy (DOE) and in-line pumps for the hydrocarbon processing industry.

In the general industrial market, this division is a market leader in the design, development, and manufacture of integrated motor-controls and protection technologies solutions for leading original equipment manufacturers (OEMs) and industrial customers. We engineer and manufacture a full range of rugged, reliable, and internationally compliant products that smoothly control the amount of electrical current provided to motors. Custom panel solutions include a variety of low and medium voltage components, such as starters, drives, contactors, breakers, and other related devices. While this is a highly competitive market, our installed base of over 100,000 control units with hundreds of custom designed systems support customers in the industrial heating, ventilation, and air conditioning (HVAC) market, as well as providing engineering, testing, repair,in the energy processing market, including petrochemicals, power generation, mining, and consulting services throughout the world. Thetransportation.

Our Valve Systems division offers a diverse line of products and servicesproduces high-performance specialized valve solutions that control the flow of liquids and gases and provide safety relief in high-pressure, severe-service applications. Becauseprevent over-pressurization of the critical nature of these applications, our products are highly engineered to meet stringent performancevessels, pipelines, and reliability requirements. These products and services include customized critical valve components for the defense industry, a unique and revolutionary coker unheading device, boltless slide valves, fluidic catalytic cracking unit (FCCU) devices, and web-enabled software for the management of pressure relief systems. Revenues derived from the sales of valves during 2006, 2005, and 2004 represented 18%, 16%, and 14%, respectively, of the Corporation’s consolidated revenue.equipment. This division operates facilities in the U.S., Canada, and the U.K. To enhance our global competitiveness, we have made a small investment in Korea and Russia and plan to establish a manufacturing facility in China in the near future.

This division’s sales to the U.S. Government, primarily the U.S. Navy, include valves that are installed on every nuclear submarine and aircraft carrier commissioned by the U.S. Navy. It also currently supplies all the relief valves utilized by the Navy’s nuclear propulsion systems. Key programs include the Virginia class submarine and CVN aircraft carriers. Other programs include various Navy submarine classes, such as Los Angeles and Trident, as well as the Nimitz aircraft carriers. Additional growth in this sector has been generated through development programs for aircraft launch and arrest systems and non-nuclear control valves for aircraft carriers and ball valves for submarines. Valve Systems continues to leverage its long-standing relationship and proven engineering expertise with the U.S. Navy to identify new opportunities for additional products on all of its platforms.

Page 5

The Valve Systems division also provides products for the commercial markets, mainly nuclear power. The Valve Systems Group provides its valves to owners and operators of commercial power utilities who use them in new and existing nuclear and fossil fuel power plants. Recently, the product line has been enhanced to include instrumentation accessories for air operated valves. The division expects a resurgence of demand for commercial nuclear power both in the U.S. and abroad and is positioning itself to participate in the new construction for both domestic and international nuclear power plants. In recent years, all newly built nuclear power plants have been outside the U.S., and segment sales for such plants have been mainly to South Korea and Taiwan. As the nuclear market picks up momentum, we expect increased competition in the market. However, we believe our long standing reputation, strong customer relationships, and proven technologies should provide us with good opportunities.

Within the petroleum, petrochemical, chemical, and oil and gas processing markets, the Valve Systems division designs, engineers, and manufactures spring-loaded, pilot-operated pressure-relief valves and pilot operated pressure-reliefsolenoid-operated valves, as well as metal-seated industrial gate, butterfly boltless slide, plug, angle, diverter, and ball valves used in standard and advanced applications, including high-cycle, high-pressure, extreme temperature, and corrosive plant environments. Included in this portfolio of products is the recent commercializationBecause of the DeltaGuard™ coke-drum unheading device, which represents a significant advancement in coke-drum unheading technology. This patented technology is remotely operated, therefore inherently safe, easycritical nature of these applications, our products are highly engineered to operate, reliable, cost effective,meet stringent performance and can be configured for any coke-drum application. There are patents for The DeltaGuard coke-drum which are significant to the sales ofreliability requirements. In addition, this product as they require new entrants to develop new technological approaches in order to enter the market. The division also provides inspection, installation,engineering support, testing, repair, and maintenance, and other fieldconsulting services for harsh environment flow control systems.

Enhancing ourglobally. Key markets include defense, power generation, oil and gas market position, this division recently purchased Enpro Systemsprocessing, and general industrial markets.

Page 6

This division’s valves are utilized in April 2006the nuclear propulsion system of every nuclear submarine and subsequently integrated it with an existing business, Tapco International, creating TapcoEnpro International. The acquisition expanded our product portfolio toaircraft carrier commissioned by the U.S. Navy. Current programs include engineered pressure vessels, FCCUs, ethylene cracking processing equipment,the Virginia class submarine and related field services. TapcoEnpro International offers custom-designed valvesFord class aircraft carriers. In addition, we provide spares and complementary components that operate in industrial process applications including fluid, residual,repair work for various submarine classes, such as Los Angeles and millisecond catalytic cracking unitsTrident, as well as the Nimitz class aircraft carriers. Despite a relatively flat naval defense budget in recent years, growth has been generated in this market through long-standing customer relationships and successful development programs for non-nuclear control valves and flight critical applications aboard the nation’s aircraft carriers. Although there is strong competition for these awards, competition is limited by significant qualifications and performance requirements. In commercial markets, this division provides valves to commercial nuclear power generation, steel manufacture,plants, oil and ore reduction. TapcoEnpro International also manufactures, repairs,gas refineries, production platforms and modifies orifice chambers, hydrotreaters,pipelines, and American Society of Mechanical Engineers (ASME) code pressure vessels.general processing industries worldwide. In addition, TapcoEnpro International can provide a wide array of field services, including equipment repair, modification or replacement, inspection of valves, controls, pipeswe are integrating our core hardware technology with engineering software to enhance product selection and refractory linings, maintenance planning and scheduling for valves or control systems, diagnostic assistance with troubleshooting problems in critical components, and on-site system training.

inventory management. General industryindustrial products within the Valve Systems division include hydraulic power units and components primarily for the automotive and entertainment industries, specialty hydraulic and pneumatic valves, air-driven pumps, gas boosters, and directional control valves used in various industrial applications includingsuch as truck transmissiontransmissions and car transport carriers. Competition is based upon quality of technology, price, installed base, and delivery times.

The Commercial Power and Services division designs, manufactures, distributes, and qualifies flow control products for nuclear power plants, hydroelectric energy producers, the Department of Energy (DOE), and the Department of Defense. This division offers a wide range of fasteners, fastening systems, specialized containment doors, airlock hatches, electrical units, bolting solutions, machined products, consulting, and enterprise resource planning for the nuclear power. In addition, this division provides distribution and servicing of original equipment manufacturers (OEM) spare parts and valve components, training, on-site services, staff augmentation, and engineering programs relating to nuclear power plants, as well as diamond wire cutting services used to create large, thick cuts from concrete structures.

During the last decade, numerous competitors have exited this market due the stringent qualification requirements. Our operations have maintained all of the regulatory certifications required to provide and /or qualify value-added representations and certification of nuclear-grade products and are well positioned to benefit from a commercial nuclear power renaissance both domestically and internationally. The key will be to remain competitive and continue to offer excellent performance and quality products. This division has locations in Brea, California, Middleburgh, Ohio and Cincinnati, Ohio.

Page 6

The Electro-Mechanical Systems division produces advanced electro-mechanical solutions for the U.S. Navy, commercial nuclear power, and the oil and gas processing markets. The division designs and manufactures advanced pumps, motors, generators, propulsors, mechanicals seals, control rod drive mechanisms, and power conditioning electronics. This division develops, designs, manufactures, and performs qualification testing of critical-function, electro-dynamic solutions for their main customer, the U.S. Nuclear Navy, including reactor and main coolant pumps, other critical-function pumps, various advanced motors, generators, secondary propulsion systems, and design engineering services. Specific applications include the Los Angeles, Virginia, Trident, Ohio, and Seawolf class submarines, and the CVN aircraft carrier.

In addition, the segment provides ship service generators and secondary propulsion systems to the non-nuclear U.S. Navy, including the Destroyer program. The division is strengthening its relationship with the Navy by participating in the design and development of major subsystems for the Navy’s Electro-Mechanical Aircraft Launch System (EMALS) as well as the Advanced Arresting Gear (AAG) for installation in its aircraft carrier fleet. This division expanded its offerings to the military to now include advanced electromagnetic product development to the U.S. Army as pulsed power supply continues to advance in the military weapons segment.

The Electro-Mechanical Systems’ products are also sold to complementary commercial markets, primarily nuclear power generation and oil and gas. We provide reactor coolant pumps, advanced motors, control rod drive mechanisms to the nuclear power markets. In the oil and gas market, we are partnering with industry leaders to develop advanced systems for exploration and production. Current programs encompass subsea pumping and power-dense motors for compact, integrated compression systems. This division has also expanded its offerings to include hazardous waste pumps to the DOE.

The commercial nuclear power markets and the oil and gas processing industries are experiencing pricing increases of materials due to increase in the demand. The increase in the pricing of the materials as well as pricing concerns and the effect of the war remain key competitive factors. As a renaissance is expected both domestically and in the increasing market overseas, the key will be to remain competitive and continue to offer excellent performance and quality products. This division has locations in Cheswick, Pennsylvania, and Phillipsburg, New Jersey.

The Controls Systems division develops, manufactures, tests, and services specialized electronic instrumentation and control equipment which includes instrumentation for primary and secondary controls, steam generator control equipment, valve actuators, and valve and heater controls. This division provides custom designed and commercial-off-the-shelf (COTS) electronic circuit boards and systems to the U.S. Nuclear Navy. Sales toThere is strong competition in the U.S. Navy are madeCOTS market, but competition is limited by responding directly to requests for proposals from customers. significant qualification and performance requirements.

The Controls Systems division also designs and manufactures advanced valve controllers and predictive maintenance systems for the oil and gas and general industrial markets.

The Controls Systems division’s products also include plant instrumentation, primary and secondary controls, steam generator control equipment, valve actuators, valve and heater controls, calorimetric instrumentation, generic digital signal processor cards, digital and numeric readout meters, response time test instrumentation, reactor plant control equipment, Stress Wave Analysis (SWAN) technology, and COTS power supply units. The division also provides engineering and support services which include embedded system design, shipboard automation and valve networking, microprocessor, Field Programmable Gate Arrayfield programmable gate array (FPGA), and analog design, system integration, software design and qualification, and factory acceptance testing. The

Our Commercial Power and Services division encounters strong competitiondesigns, manufactures, distributes, and qualifies flow control products for nuclear power plants, nuclear equipment manufacturers, hydroelectric energy producers, the DOE, and the Department of Defense (DoD). This division offers a wide range of critical hardware, including fastening systems, specialized containment doors, airlock hatches, electrical units, bolting solutions, machined products, valves, pumps, and enterprise resource planning, as well as plant process controls, including electrical instrumentation, specialty hardware and proprietary database solutions, aimed at improving safety and plant performance, efficiency, reliability, and reducing costs. In addition, the division provides distribution and servicing of OEM spare parts and valve components, training, on-site services, staff augmentation, and engineering programs relating to nuclear power plants.

As new construction of nuclear power plants continues to ramp up, we anticipate a growing number of new customers and some increased competition. We are already beginning to receive requests for newly designed components for next-generation plants expected to be built, and we are currently providing third-party nuclear-grade certification of other suppliers’ components. Many of the suppliers that participated in the Navyconstruction of first and second generation nuclear power plants retired their nuclear Quality Assurance (QA) programs and exited the business during the past twenty years. More recently, some suppliers have announced plans to re-establish their nuclear manufacturing and QA programs. As an established provider of these services, these companies represent a new market from a limited number of competitors. This division is located in East Farmingdale, New York.opportunity for us to provide nuclear QA program start-up, harsh environment qualification, innovative installation technologies, such as HydraNut and PlasmaBond, and inventory management software.

This division acquired Techswan, Inc., which conducted business as Swantech, in September 2006has maintained all of the regulatory certifications required to enhance its portfolioprovide and/or qualify value-added representations and certification of advanced electronicsnuclear-grade products and are well positioned to benefit from a commercial nuclear renaissance both domestically and internationally. Our continued success will require us to remain competitive and continue to offer excellent performance and quality products. We believe we maintain a competitive advantage by virtue of our breadth of nuclear technology, industry-benchmarked QA programs, large

Page 7

installed base, strategic alliances, resident expertise, and customer recognition of the important nature of our long-term commitment to servicing the unique challenges of the nuclear market.

Our Oil and Gas Systems division designs and manufactures valves and vessel products for the oil and gas refining market. Primary products include coke deheading systems, fluidic catalytic cracking unit (FCCU) components, and generalweb-enabled software for the FCCU process control.

This division is a leader in turnkey coker systems globally, as well as oil production platforms and storage facilities, liquefied natural gas (LNG) terminals and storage facilities, natural gas pipeline operations, and power generation facilities. Our coke deheading system, which includes top and bottom un-heading valves, isolation valves, cutting tools, and valve automation, process control, and protection systems, enable safe coke drums operation during the refining process. Included in this portfolio of products is the DeltaGuard™ coke-drum unheading valve, a revolutionary advancement in coke-drum unheading technology. Our patented technology is remotely operated, therefore inherently safe, easy to operate, reliable, cost effective, and can be configured for any coke-drum application.

We also offer a delayed coker operations optimization system featuring process control, interlocks, valve control solutions, batch process data acquisition, interactive operator batch sequence procedures, batch scheduler, batch sequence editor, risk management, asset protection, and predictive maintenance capabilities. In addition, we provide inspection, installation, repair and maintenance, and other field services for harsh environment flow control systems. Competition is mitigated by our superior technical expertise, proven technology and extraordinary service.

Our FCCU product portfolio includes custom-designed valves, engineered pressure vessels, and complementary components that operate in industrial markets. Swantech has patentedprocess applications including fluid, residual, and catalytic cracking units as well as power generation, steel manufacture, and ore reduction. We manufacture, repair, and modify orifice chambers, hydrotreaters, and American Society of Mechanical Engineers (ASME) code pressure vessels. In addition, we provide a unique technology called Stress Wave Analysis (SWAN) that provides vibrationwide array of field services, including equipment repair, modification or replacement, inspection of valves, controls, pipes and oil/lubrication analysis solutions. SWAN has shownrefractory linings, maintenance planning and scheduling for valves or control systems, diagnostic assistance with troubleshooting problems in critical components, and on-site system training. Due to be an effective, non-invasive methodthe critical and severe service applications requiring highly engineered solutions, competition is limited to identify early stage mechanical damagea few major competitors. While we face price competition on most major projects, our large installed base product suite, integrated systems capability, and equipment setup issues, such as imbalance and alignment, far sooner than the existing technologies. SWAN is an order of magnitude more sensitive than the presently installed technologies and provides the only continuous measurement of machine condition. The technology acquired in the purchase will enhance our existing product line.aftermarket service attracts a significant customer base.

Page 7

The following list defines our principle products and the markets served by the Flow Control segment.

Naval Defense | |||

• | Nuclear propulsion system components | ||

Valves (butterfly, globe, gate, control, safety, relief, solenoid, hydraulic operated gate) | |||

Pumps | |||

Motors | |||

Instrumentation and controls | |||

• | Non-nuclear products | ||

Smart leakless valves | |||

Sub-safe ball valves | |||

Jet-fuel pumping valves | |||

Steam generator control equipment | |||

Air driven fluid pumps | |||

Engineering, inspection, and testing services | |||

• | Aircraft carrier launch and retrieval equipment | ||

Advanced electromagnetic systems | |||

Flight critical components (aircraft shuttle components, holdback bars, capacity selector valves) | |||

• | Instrumentation and control systems | ||

Ground Defense | |||

• | Electromagnetic gun | ||

Page 8

Oil & Gas Processing | |||||

• | Critical process valves | ||||

DeltaGuard coker unheading valve | |||||

Boltless catalyst control slide valves | |||||

Butterfly and triple offset butterfly valves | |||||

Pilot-operated relief valves | |||||

Pressure relief valves | |||||

Safety valves | |||||

Solenoid, gate, and globe valves | |||||

Steam valves | |||||

• |

| ||||

Air grids and cyclones | |||||

Risers, headers, and wye sections | |||||

• | Engineered process vessels | ||||

Cat cracker reactors and | |||||

Hydrotreators | |||||

• | Advanced | ||||

Digital valve controller with redundant technology | |||||

Signature recognition for fault and leak detection | |||||

Integrated valve, automation, safety, and control systems | |||||

• | Web-enabled process control software | ||||

| |||||

• | |||||

Advanced motors and generators | |||||

• |

| ||||

Reactor coolant and process | |||||

• | Valves | ||||

Solenoid, ball, butterfly, check, pressure relief, safety and | |||||

• | Control rod drive mechanisms | ||||

• | Design, fabrication of nuclear facility airlocks, doors, hatches | ||||

• | Instrumentation | ||||

• | Diagnostic and test equipment | ||||

• | Fluid sealing technologies | ||||

• | Actuators | ||||

Pneumatic and hydraulic | |||||

• | Plate heat exchangers | ||||

• | Separation technologies | ||||

• | Fasteners | ||||

• | Advanced bolting technologies | ||||

• | Diamond wire concrete cutting | ||||

• | Engineering services | ||||

Page 8

• | Equipment qualification, commercial grade dedication | ||||

• | Inventory management systems | ||||

General Industrial | |||||

• | Valves | ||||

Directional control and pneumatic | |||||

• | Power Control Systems | ||||

Integrated motor-control systems | |||||

Variable frequency drives | |||||

Pump control panels | |||||

Low voltage solid state starters | |||||

Medium voltage controls | |||||

Protective technology solutions | |||||

• | Critical machinery fault detection and prognostics systems | ||||

Page 9

The Flow Control segment experiences strong competition from a large number of domestic and foreign sources. Competition occurscompetes globally on the basis of technical expertise, price, delivery, contractual terms, previous installation history, and globally renowned reputation for quality. Delivery speed and the proximity of service centers are important with respect to aftermarket products. Sales to commercial end users are accomplished primarily by a combination of direct sales employees and, in certain instances, by manufacturers’ representatives located in the segment’s primary market areas. This representation provides sales coverage ofareas, such as nuclear power utilities, principal boiler and reactor builders, processing plants, and architectural engineers, and hydrocarbon processing industry and chemical processing industry plants worldwide.engineers. For its military contracts, the segment receives requests for quotes from prime contractors as a result of being an approved supplier for naval propulsion system pumps and valves. SalesIn addition, sales engineers support non-nuclear sales activities. The segment uses the direct distribution basis for military and commercial valves and associated spare parts. In addition, the sales associated with the power plants follow the cycles associated with the power outages that are more prevalent in the spring and fall and bi-annual plant updates.

Backlog for this segment at December 31, 2006,2008, was $434.9$1,102 million, of which 22%44% will be shipped after one year, compared with $429.3$776 million at December 31, 2005. Additionally, 38%2007. Approximately 50% of this segment'ssegment’s backlog as of December 31, 2008 is comprised of commercial nuclear orders with Westinghouse Electric Company LLC (“Westinghouse”). Sales to Westinghouse represented approximately 12%, 6%, and 10% of total segment sales in 2008, 2007, and 2006, respectively. Additionally, 22% of this segment’s backlog as of December 31, 2008 is comprised of orders with the U.S. Navy, the majority of which is through itsa prime contractor, Bechtel Group, Inc. Sales by this segment to Bechtel accounted for 21%11%, 24%15%, and 33%21% of this segment’s total segment sales in 2006, 2005,2008, 2007, and 2004,2006, respectively, or 9%5%, 10%, and 13% of the Corporation’s consolidated revenue. Additionally, sales to one of the segment’s commercial customers represented approximately 10%, 8%7%, and 9% of total segment sales in 2006, 2005, and 2004, respectively.our consolidated revenue. The loss of these customers would have a material adverse effect on the business of this segment and the Corporation.in total. None of thethis segment’s business of this segment is seasonal. Raw materials are generally available in adequate quantities.quantities, although pricing of raw materials is impacted by commodity prices.

Motion Control

Curtiss-Wright’sOur Motion Control segment designs, develops, manufactures, and maintains sophisticated, high-performance mechanical actuation and drive systems, mission-critical electronic component and control systems, and sensors for the aerospace, defense, and general industrial equipment markets. This segment consists of 1422 business units that are organized and managed as three core technology groups: Engineered Systems, Integrated Sensing, and Embedded Computing.

Our Engineered Systems division’s product offerings to the commercial and defense aerospace industrymarkets consist of electro-mechanical and hydro-mechanical actuation control components and systems that are designed to position aircraft control surfaces or to operate flaps, slats, and utility systems such as canopies, cargo doors, weapons bay doors, or other moving devices used on aircraft. Aircraft applications include actuators and electronic control systems and sensors for the Boeing 737, 747, 757, 767, 777, Airbus A320, A330, A340, and future Boeing 787 civil air transports, Airbus A320, A330, A340, A380, the Lockheed Martin F-16 Falcon fighter jet, the Boeing F/A-18 Hornet fighter jet, the F-22 Raptor fighter jet, the Bell Boeing V-22 Osprey, and the Sikorsky Black Hawk and Seahawk helicopters. The Engineered Systems division is also developing flight control actuators and weapons handling systems for the engineering and manufacturing development phase of Lockheed Martin'sMartin’s F-35 Lightning II Joint Strike Fighter (JSF)(F-35 JSF) program. The F-35 JSF is the next-generation fighter aircraft being designed for use by all three branches of the U.S. military as well as by several foreign governments. The division also provides electric motors, rotary sensors, controllers, and smaller electromechanical actuation subsystems for flight, engine, and environmental control applications on various commercial transports, regional aircraft, business aircraft, military aircraft, and spacecraft.

As a related service within the Engineered Systems division, we also provide commercial airlines, the military, and general aviation customers with component overhaul and repair services.services in support of our manufactured products. These services include the overhaul and repair of hydraulic, pneumatic, mechanical, electro-mechanical, and electronic components, aircraft parts sourcing, and component exchange services for a wide array of aircraft.

Page 9

In addition, Engineered Systems designs, manufactures, and distributes electro-mechanical and electro-hydraulic actuation components and systems, and electronic controls for military tracked and wheeled vehicles and, high-speed tilting trains, andwithin the ground defense market as well as for commercial markets utilizing drive technology. These products consist of turret aiming and stabilization, weapons handling systems, suspension systems for armored military vehicles sold to foreign defense equipment manufacturers, tilting systems for high-speed train applications, fuel control valves for large commercial transport ships, camera head stabilization for the entertainment industry, and a variety of commercial servo valves.

Through its marine defenseMarine Defense unit, the Engineered Systems division designs and manufactures electro-mechanical and hydro-mechanical systems for landing helicopters aboard naval vessels. The shipboard helicopter handling systems are used by the U.S. Navy, U.S. Coast Guard, and more than ten other navies around the world. The

Page 10

division also designs and builds the elements of the ship’s aircraft storage structures, including telescopic hangars and hangar doors. Specialized handling systems are provided for towing sonar and mine sweep systems for submarines and surface ships.

Engineered Systems products are sold primarily through both a domestic sales force and international sales force. In addition, we have a marketing distribution facility in Singapore.network of representatives. A direct sales force is utilized with assistance from commissioned agents. Sales to Japan are made through Mitsubishi Trading Corporation, and certain sales to the U.S. Navy are made through the Canadian Commercial Corporation. All other sales are made directly to OEM’s,OEMs, airlines, and government agencies as well as to aircraft and ship builders around the world.

Our Engineered Systems products are sold in competition with a number of other suppliers, some of whom have broader product lines and greater financial, technical, and human resources. The competitive environment for these products is focused on a short list of companies, with recent strategic trends at the prime contractor level resulting in a smaller market of vertically integrated suppliers, while prime contractors specialize in integration and final assembly. Price, technical capability, performance, service, investment, and “overall value” are the primary forces of competition together with an ability to offer solutions to perform control and actuation functions on a limited number of new production programs. Our overhaul and repair services are sold in competition with a number of other overhaul and repair providers with a focus on quality, delivery, and price. The division provides these services from facilities in Gastonia and Shelby, North Carolina, Miami, Florida, and Stratford, Ontario.

Our Integrated Sensing division develops and manufactures a range of sensors, controllers, and electronic control units for militarycommercial and commercialdefense aerospace and general industrial markets. These products include position, pressure, and temperature sensors, solenoids and solenoid valves, smoke detection sensors, torque sensing, ice detection and protection equipment, air data computers, flight data recorders, joysticks, and electronic signal conditioning and control equipment. We sell this division’s products primarily to prime contractors and system integrators, both directly and through a network of independent sales representatives on a worldwide basis. Position sensors are used on primary flight control systems and engine controls on Airbus and Boeing aircraft, regional and business aircraft, and on many U.S. and European military aircraft. Air data, flight recorder, and ice detection and protection equipment are supplied to many helicopter applications. We also sell our products for use in a wide range of industrial applications such as off-highway vehicles, powered wheelchairs, process control,controls, and motorsport.motorsports.

Competition within the IntegratedCompetitive discriminators for Integrating Sensing division, especially in the aerospace market, is increasingly being driven byinclude technical support and product price concerns. The ability to service the customer with superior performanceas well as quality and quality is expected of all vendors, but downward pricing pressure is emerging as a key discriminator.delivery. For that reason Integrated Sensing products are marketed through facilities in the United Kingdom, Germany and the United States.States, and manufacturing facilities have now been established in Mexico and China.

In 2008, this division acquired Mechetronics Ltd., a United Kingdom supplier of solenoids and solenoid valves for global general industrial markets. A solenoid is an electromagnetic actuator used as a mechanical switch or integrated with a valve to provide control in pneumatic or hydraulic systems. Mechetronics products are supplied to OEMs and are used in a variety of applications including business machines, switchgear and vehicle braking systems. Originally founded in 1918, today Mechetronics is a leading industrial solenoid supplier with headquarters in Bishop Auckland, United Kingdom, and a new production facility in Zhuhai, China which opened in 2007. Mechetronics employs 72 people.

Our Embedded Computing division designs, develops, and manufactures rugged embedded computing board-level modules and integrated subsystems primarily for the aerospace and ground defense markets. Using standard, commercially available electronics technologies, coupled with application domain specific knowledge, this division offers COTS hardware and software modules based on open industry standards, referred to as COTS.standards. Our advanced subsystems are integrated subsystems include both in-houseusing our standard modules and third party modules as well as custom modules based on in-house intellectual property content.content as well as third-party technology. We also offer a supportingbroad array of support services that include:include life-cycle management, technical support, training, and developmentcustom engineering of custom module variants based on COTS modules.modules and fully integrated subsystems. Our Embedded Computing division is considered one of the embedded computing industry’s most comprehensive and experienced single sourcesources for processing, data communications, digital signal processing, and video and graphics, computing solutions.recording and storage, analog acquisition and reconstruction, radar, and integrated subsystems. Our COTS modules and integrated subsystems are designed to perform reliably in harsh conditions where space, weight, and power constraints are critical. Our rugged conditions, such asproducts excel in extreme temperatures terrain and/or speed which result inand environments, enduring high shock and vibration, as well as in commercial environments for use in laboratory and benign environment applications.

Page 10

Embedded Computing’s subsystem products are used in a wide variety of mission-critical military applications, including fire control, aiming and stabilization, munitions loading, and environmental processors for military ground vehicles. These products are used on demanding combat platforms such as the Bradley fighting vehicle, the Abrams M1A2/A3 tank, and the Brigade Combat Team Interim Armored Vehicle, which is part of the U.S.

Page 11

Army’s modernization and transformation efforts. This division also provides the mission management, flight control computers, and the sensor management units for advanced aerospace platforms including Global Hawk, the U.S. Air Force Global Hawk, which is aForce’s high-altitude and high-endurance unmanned aerial vehicle.

Embedded Computing’s modules are used in hundreds ofnumerous active programs today, including leading-edge military platforms such as the Improved Bradley Acquisition System and the Improved Tow Acquisition System. The modules feature highthe highest performance chipscommercial processors on open standard board architectures. The division has taken a leadership position in the drafting and definition of the newest embedded standards, which are designed to address the more demanding performance and data bandwidth requirements of emerging applications. Embedded Computing is frequently the first embedded computingCOTS vendor to announce forthcoming boards and systems based on these new architectures. Embedded Computing is also committedhas been selected to supply technology for some of the most advanced future military platforms including the F-22, F-35 JSF, P-8 Poseidon, and Future Combat System.

This division’s products are manufactured at its operations located in North America and the United Kingdom. Our products are sold primarily to prime contractors and subsystem suppliers located primarily in the United States, United Kingdom, and Canada, both directly and through a network of independent sales representatives. In recent years, competition in the embedded electronic systems market has migrated away from traditional board competitors toward fully integrated subsystem and system providers selling to prime and second-tier defense and aerospace companies. Competition in this market is based on quality of technology, price, and delivery times.time to market.

In 2008, this division enhanced its portfolio of high-performance embedded computing products with the acquisition of VMETRO ASA. Founded in 1986, VMETRO is a leading supplier of COTS board- and system-level embedded computing products for applications in aerospace, defense, and industrial markets. Key products provide real-time computing capabilities, high-density radar processing, data recording, and network storage systems. Application of these products as components or subsystems enables improved response time and critical protection in server and storage appliances, utility mapping, and ground penetrating radar. VMETRO operates globally with headquarters and principal engineering in Oslo, Norway. Additional sales, engineering and distribution networks are established in the United States, Europe, and Asia. VMETRO employs approximately 200 people.

The following list defines our principle products and the markets served by the Motion Control segment.

Commercial Aerospace | |||

• | Commercial Jet Transports | ||

Secondary flight control actuation systems and electromechanical trim actuators | |||

Aircraft cargo door and utility actuation systems | |||

Fire detection and suppression control systems | |||

Position sensors | |||

Solenoids and solenoid valves | |||

• | Business/Regional Jets | ||

Throttle quadrants | |||

Position Sensors | |||

• | Helicopters | ||

Rotor Ice Protection Systems | |||

• | Repair & Overhaul Services | ||

Component overhaul and logistics support services | |||

Defense Aerospace | |||

• | Transport and fighter aircraft | ||

Weapons bay door actuation systems | |||

Secondary flight control actuation | |||

Rotary actuation for environmental control systems | |||

Weapons handling systems | |||

• | Helicopters | ||

Radar warning systems | |||

Acoustic processing systems | |||

Flight data recorders | |||

Air data computers | |||

Position Sensors | |||

Page 12

• | Unmanned aerial vehicles | ||

Integrated mission management and flight control computers | |||

Weapons handling systems | |||

Page 11

Ground Defense | |||

• | Tanks and light armored vehicles | ||

Digital electromechanical aiming and stabilization systems | |||

Fire control, sight head, and environmental control processors | |||

Single Board Computers for target acquisition systems | |||

Hydropneumatic suspension systems | |||

Ammunition handling systems | |||

Naval Defense | |||

• | Surface ships | ||

Helicopter handling and traverse systems | |||

Tie-down components | |||

• | Marine Propulsion | ||

Marine engine diesel valve injection systems | |||

• | Submarines | ||

Cable handling systems for towed arrays | |||

Other Military & Government | |||

• | High performance data communication products | ||

Power conversion products | |||

• | Space programs | ||

Control electronics and sensors | |||

• | Security systems | ||

Perimeter intrusion detection equipment | |||

• | FAA | ||

Airport surface detection equipment radar video processing | |||

General Industrial Markets | |||

• | Automated industrial equipment | ||

Air, sea, and ground simulation | |||

Fractional horse power (HP) specialty motors | |||

Force transducers | |||

Joysticks | |||

Sensors | |||

Sales by our Motion Control segment to its largest customer in 2006, 2005,2008, 2007, and 20042006 accounted for 10% of Motion Control revenue and 4% of our consolidated revenue for each year. The loss of this customer would have a material adverse effect on Motion Control. Direct and end use sales of this segment to government agencies, primarily the U.S. Government, in 2006, 2005,2008, 2007, and 2004,2006, accounted for 63%66%, 64%62%, and 62%63%, respectively, of total Motion Control sales. Although the loss of this business would also have a material adverse affect on Motion Control, no single prime contractor to the U.S. Government to which we are a subcontractor provided greater than 10% of Motion Control revenue during any of the last three years.

Backlog for our Motion Control segment at December 31, 2006,2008, was $438.6$575 million, of which 33%64% is expected to be shipped after one year, compared with $374.5$526 million at December 31, 2005.2007. None of the businesses of our Motion Control segment is seasonal. Raw materials are generally available in adequate quantities from a number of suppliers. However, we utilize sole source suppliers in this segment. Thus, the failure and/or inability of a sole source supplier to provide product to Motion Control could have an adverse impact on our financial performance. While alternatives could be identified to replace a sole source supplier, a transition could result in increased costs and manufacturing delays.

Page 13

Metal Treatment

Curtiss-Wright’sOur Metal Treatment segment provides various metallurgical processes that are used principallyprimarily to improve the service life, strength, and durability of highly stressed, critical-function metal parts. Metal Treatment provides these services to a broad spectrum of customers in various industries, includingcommercial and defense aerospace, automotive, construction equipment, oil and gas, power generation, and general industrial markets, including automotive/transportation, construction equipment, and metal working.

Page 12

This segment consists of several business units that are organized into three principal services that the segment offers which include peening, specialty coatings, and heat treating.

Shot peening is a process by which the durability of metal parts is enhanced by the bombardment of the part’s surface with spherical media, such as steel shot or ceramic or glass beads, to compress the outer layer of the metal. In addition, shot peen forming enables metal panels to be shaped with aerodynamic curvatures that are assembled as wing skins of commercial and military aircraft. Revenue of shot peening services in 2006, 2005,2008, 2007, and 20042006 accounted for 10%8%, 10%9%, and 12%10%, respectively, of our consolidated revenues.

Laser peening is an advanced metal surface treatment process that utilizes a unique high energy laser developed by the Lawrence Livermore National Laboratory. The laser peening process is being used in production to extend the life of critical industrial and flight turbine engine components. Laser peening is also utilized to form the wing skins of the Boeing 747-8 aircraft in an on-site facility within the Boeing Frederickson, Washington complex. Future applications include high value, extreme service components in aircraft structures, oil and gas, medical implant, and marine applications. We retain the exclusive worldwide rights to the intellectual property necessary for the use of this laser architecture on laser peening of commercial products. Currently, the patents associated with the laser peening technology are not material to our operations. However, we believe that this technology has significant potential and, thus, these patents may become material to our future operations.

Specialty coatings primarily consist of the application of solid film lubricant coatings, which are designed to enhance the performance of metal components used in high-stress applications for a broad range of industries. We apply our coatings by air spray or by a dipping and spinning process for bulk applications. We have diversified this service with the acquisition of new capabilities, such as the ability to manufacture our own bulk coatings, and new international facilities in Canada and United Kingdom.

Heat treating is a metallurgical process of subjecting metal objects to heat and/or cold or otherwise treating the material to change the physical and/or chemical characteristics or properties of the material. In addition to shot peening, heat treating, and specialty coatings, other metal treatment services that are provided on a job shop basis include shot peen forming, laser peening, wet finishing, chemical milling, and feedreed valve manufacturing.

Working in conjunction with Lawrence Livermore National Laboratory, Metal Treatment has developed an advanced metal surface treatmentIn 2008, we acquired Parylene Coating Services (“PCS”) which further expands our coating services business into the growing medical market. PCS utilizes a vapor deposition process utilizing laser technology. The laser peening process is beingto apply parylene coatings to medical devices, including coronary artery stents, rubber/silicone seals and wire forming mandrels used in productionthe manufacture of catheters. The conformal coating provides lubricity; resistance to extend the life of critical turbine engine components. Futuresolvents, radiation and bacteria; and is also biocompatible. In addition to medical applications, include additional turbine engine components as well as other high value, extreme service componentsparylene coatings are uniquely suited for use in aircraft structures,niche electronic, oil and gas, medical implant, and marinegeneral industrial applications. Laser peening also shows potential to augment the segment’s wing skin forming capabilities, allowing for placement of more extreme aerodynamic curvatures of wing skins of greater thickness. We operate a laser peeningPCS’s facility in the United StatesKaty, Texas is ISO 9001 registered and another in the United Kingdom. We currently have seven operational lasers and are in the process of building two additional lasers, with mobile capability. We retain the exclusive worldwide rights to the intellectual property necessary for the use of this laser architecture on laser peening of commercial products. Currently, the patents associated with the laser peening technology are not material to our operations. However, we believe that this technology has significant potential and, thus, these patents may become material to our future operations.

In May, 2006 we acquired, two coating application facilities of Diversified Coatings, Inc. (Allegheny), located in Fremont, Indiana and Ingersoll, Ontario. These additions provided an entry into the Ontario, Canada coatings market and increased the segment’s number of coating facilities to ten. During 2004, we increased Metal Treatment’s coatings capabilities with the acquisitions of selected assets of Evesham and Everlube, located in Evesham, United Kingdom and Peachtree City, Georgia, respectively. These acquisitions provided an entry into the European coatings market and added the capability to manufacture our own bulk coatings.18 employees.

The following list defines our principle products and the markets served by the Metal Treatment segment.

Commercial Aerospace | |||

• | Shot peen forming | ||

Wing skins | |||

• | Shot peening | ||

Aircraft structural components | |||

Landing gear components | |||

Turbine engine rotating components | |||

• | Laser peening | ||

Turbine engine rotating components | |||

• | Coatings | ||

Fasteners | |||

Sliding components | |||

Page 1314

• | Heat Treating | ||

Aluminum structural components | |||

General Industrial | |||

• | Shot Peening | ||

Highly stressed metal components susceptible to fatigue | |||

Welded components subject to distortion | |||

Architectural structures | |||

Engine and transmission components | |||

• | Heat Treating | ||

Miscellaneous engine, transmission and structural components | |||

Miscellaneous aluminum and steel components | |||

• | Coatings | ||

Fasteners | |||

Brake and suspension components | |||

Sliding components | |||

Miscellaneous components subject to corrosion and sliding wear | |||

Defense | |||

• | Shot Peening | ||

Helicopter and fighter aircraft structural and turbine engine components | |||

Through a combination of acquisitions and new plant openings, we continue to increase Metal Treatment’s network of regional facilities. Metal Treatment operations are now conducted from 5965 facilities located in the United States, Canada, United Kingdom, France, Germany, Sweden, Belgium, Italy, Spain, Austria, and Italy, with new facilities in Spain, Sweden, and France scheduled to open in the second half of 2007.China. Our Metal Treatment services are marketed directly by our employees. Although numerous companies compete in this field and many customers have the resources to perform such services themselves, we believe that our technical knowledge and quality of workmanship provide a competitive advantage. We compete in this segment on the basis of quality, service, and price.

The business of this segment is not seasonal. Raw materials are generally available in adequate quantities from a number of suppliers, and we are not materially dependent upon any single source of supply in this segment. We have no significant working capital requirements outside of normal industry accounts receivable and inventory turnover. Our largest customer in this segment accounted for 9%, 10%, and 8% of Metal Treatment sales during 2006, 2005,2008, 2007, and 2004, respectively.2006. Although the active customer base is in excess of 5,000, the loss of this customer would have a material adverse effect on our Metal Treatment segment.

The backlog of Metal Treatment was $2 million as of December 31, 2006, was $2.1 million,2008 and 2007, all of which is expected to be recognized in the first quarter of 2007, compared with $1.9 million as of December 31, 2005.2009. Due to the nature of our metal treatment services, we operate with a very limited backlog of orders and services that are provided primarily on newlynew manufactured parts. Thus, the backlog of this segment is not indicative of our future sales, and as a result, this segment’s sales and profitability are closely aligned with general industrial economic conditions and, in particular, the commercial aerospace market.

OTHER INFORMATION

Certain Financial Information

For information regarding sales by geographic region, see Note 16 to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

In 2006, 2005,2008, 2007, and 2004,2006, our foreign operations generated 37%57%, 35%42%, and 33%37%, respectively, of our pre-tax earnings. We do not regard the risks associated with these foreign operations to be materially greater than those applicable to our U.S. businesses.

Government Sales

Our direct sales to the U.S. Government and sales for U.S. Government and foreign government end use represented 45%36%, 48%38%, and 47%45% of consolidated revenue during 2006, 2005,2008, 2007, and 2004,2006, respectively. U.S.

Page 15

Government sales, both direct and indirect, are generally made under standard types of government contracts, including fixed price, fixed price-redeterminable, and fixed price-redeterminable.cost plus.

In accordance with normal practice in the case of U.S. Government business, contracts and orders are subject to partial or complete termination at any time, at the option of the customer. In the event of a termination for convenience by the government, there generally are provisions for recovery by us of our allowable incurred costs and a proportionate share of the profit or fee on the work completed, consistent with regulations of the U.S.

Page 14

Government. Fixed-price redeterminable contracts, generally on naval programs, usually provide that we absorb the majority of any cost overrun. In the event that there is a cost underrun, the customer recoups a portion of the underrun based upon a formula in which the customer'scustomer’s portion increases as the underrun exceeds certain established levels.

Generally, long-term contracts with the U.S. Government require us to invest in and carry significant levels of inventoriable costs. However, where allowable, we utilize progress payments and other interim billing practices on nearly all of these contracts, thus reducing the overall working capital requirements. It is our policy to seek customary progress payments on certain of our contracts. Where we obtain such payments under U.S. Government prime contracts or subcontracts, the U.S. Government has either title to or a secured interest in the materials and work in process allocable or chargeable to the respective contracts. (See Notes 1.F, 3, and 4 to the Consolidated Financial Statements, contained in Part II, Item 8, of this Annual Report on Form 10-K). In the case of most motion controlMotion Control and flow controlFlow Control segment products for U.S. Government end use, the contracts typically provide for the retention by the customer of stipulated percentages of the contract price, pending completion of contract closeout conditions.

Patents

We own and are licensed under a number of United States and foreign patents and patent applications, which have been obtained or filed over a period of years. We also license intellectual property to and from third parties. Specifically, the U.S. Government has licenses in our patents that are developed in performance of government contracts, and it may use or authorize others to use the inventions covered by such patents for government purposes. Additionally, unpatented research, development, and engineering skills, some of which have been acquired by us through business acquisitions, make an important contribution to our business. While our intellectual property rights in the aggregate are important to the operation of our business, we do not consider the successful conduct of our business or business segments to be materially dependent upon the protection of any one of the patents, patent applications, or patent license agreements under which we now operate.

Research and Development

We conduct research and development activities under customer-sponsored contracts, shared development contracts, and our own independent research and development activities. Customer-sponsored research and development costs are charged to costs of goods sold when the associated revenue has been recognized, fundsrecognized. Funds received under shared development contracts are a reduction of the total development expenditures under the shared contract and are shown net as research and development costs, while corporation-sponsoredcosts. Corporation-sponsored research and development costs are charged to expense when incurred. Customer-sponsored research and development activity amounted to $35.7$32 million, $28.3$45 million, and $26.5$36 million, in 2006, 2005,2008, 2007, and 2004,2006, respectively, and were attributed to customers within our Flow Control and Motion Control segments. Research and development expenses incurred by the Corporationus amounted to $38.8$50 million in 20062008 as compared with $39.7$48 million in 20052007 and $33.8$39 million in 2004.2006.

Environmental Protection

We are subject to federal, state, local, and foreign laws, regulations, and ordinances that govern activities or operations that may have adverse environmental effects, such as discharges to air and water. These laws, regulations, and ordinances may also apply to handling and disposal practices for solid and hazardous waste and impose liability for the costs of cleaning up and for certain damages resulting from sites of past spills, disposals, or other releases of hazardous substances.

At various times, we have been identified as a potentially responsible party pursuant to the Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA), and analogous state environmental laws, for the cleanup of contamination resulting from past disposals of hazardous wastes at certain current and former facilities and at sites to which we, among others, sent wastes in the past. CERCLA requires potentially responsible persons to pay for cleanup of sites from which there has been a release or threatened release of hazardous substances. Courts have interpreted CERCLA to impose strict joint and several liability on

Page 16

all persons liable for cleanup costs. As a practical matter, however, at sites where there are multiple potentially responsible persons, the costs of cleanup typically are allocated among the parties according to a volumetric or other standard.

Information concerning our specific environmental liabilities is described in Notes 1.M1.N and 13 to the Consolidated Financial Statements contained in Part II, Item 8, of this Annual Report on Form 10-K.

Page 15

Executive Officers

Martin R. Benante, age 54,56, has served as the Chairman of the Board of Directors and Chief Executive Officer of the Corporation since April 2000; President and Chief Operating Officer of the Corporation from April 1999 to April 2000; Vice President of the Corporation from April 1996 to April 1999; and President of Curtiss-Wright Flow Control Corporation from March 1995 to April 1999.2000. He has been a Director of the Corporation since 1999.

B. Parker Miller III, age 61, has served as Senior Vice President – Government Relations of the Corporation since June 2005 and was elected an officer of the Corporation in February 2006; Director of Business and Strategic Development, Northrop Grumman from January 2005 to June 2005; Director of Business and Strategic Development, Unmanned Systems Group, Integrated Systems Sector, Northrop Grumman from June 2003 to January 2005; Manager, Legislative Affairs, Northrop Grumman from January 1997 to June 2003. In February 1994, after 25 years of service Mr. Miller retired from the Marine Corps with the rank of Colonel.

Edward Bloom, age 65,67, has served as Vice President of the Corporation and President of Metal Improvement Company, LLC since June 2002; Executive Vice President of Metal Improvement Company, Inc. from December 1995 to June 2002.