UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

(Mark One)

|

| |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

xANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934For the fiscal year ended December 31, 20152016

OR

|

| |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

orFORoTRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE TRANSITION PERIOD FROMSECURITIES EXCHANGE ACT OF 1934

For the transition period from TOto

Commission File Number: 001-36373

TRINET GROUP, INC.

(Exact Name of Registrant as Specified in its Charter)

|

| | |

| Delaware | | 95-3359658 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 1100 San Leandro Blvd., Suite 400, San Leandro, CA | | 94577 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (510) 352-5000

Securities registered pursuant to Section 12(b) of the Act: Common Stock, Par Value $0.000025 Per Share; Common stock traded on the New York Stock Exchange.

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

| Large accelerated filer | x | Accelerated filer | o |

| | | | |

| Non-accelerated filer | o (do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of common stock on The New York Stock Exchange on June 30, 2015,2016, was $1,055,737,584.$865,320,029.

The number of shares of Registrant’s Common Stock outstanding as of March 28, 2016February 23, 2017 was 70,711,536.68,268,207.

Portions of the Registrant’s Definitive Proxy Statement to be issued in connection with its Annual Meeting of Stockholders, scheduled to be held on May 26, 2016,18, 2017, are incorporated by reference into Part III of this Form 10-K.

TriNet, Inc.TRINET GROUP, INC.

Form 10-K - Annual Report

For the Fiscal Year End December 31, 20152016

TABLE OF CONTENTS

SpecialCautionary Note Regarding Forward-Looking Statements

For purposes of this Annual Report, the terms “TriNet," "the Company," “we,” “us” and “our" refer to TriNet Group, Inc., and its consolidated subsidiaries. This reportAnnual Report on Form 10-K contains statements that are not historical in nature, are predictive in nature, or that depend upon or refer to future events or conditions or otherwise contain forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E21 of the Securities Exchange Act of 1934, as amended, orand the Exchange Act.Private Securities Litigation Reform Act of 1995. Forward-looking statements are often identified by the use of words such as, but not limited to, “anticipate,” “believe,” “can,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “seek,” “should,” “strategy,” “target,” “will,” “would” and similar expressions or variations intended to identify forward-looking statements. TheseExamples of forward-looking statements include, among others, TriNet’s expectations regarding: the growth of our customer base, our ability to roll out additional product offerings as and when planned, our ability to make enhancements to our technology platform, our ability to remediate the material weaknesses in our internal controls over financial reporting, our ability to execute on our vertical market strategy and penetrate the market for human resources (HR) solutions for small to midsize businesses, and other expectations, outlooks and forecasts on our future business, operational and financial performance.

Forward-looking statements are not guarantees of future performance, but are based on management’s expectations as of the date of this report and assumptions that are inherently subject to uncertainties, risks and changes in circumstances that are difficult to predict. Forward-looking statements are subject toinvolve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from those in forward-looking statements.our current expectations and any past results, performance or achievements. Important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements include, but are not limitedinclude:

risks associated with the market acceptance of outsourcing the HR function, and the anticipated benefits associated with the use of a bundled HR solution;

changes to and our ability to comply with laws and regulations, including both those identified belowapplicable to the co-employment relationship as well as those applicable to our clients’ businesses and thosetheir employees;

the amendment, repeal, replacement or continuing implementation of the Affordable Care Act and other health care reform, which may be more challenging in a changing political environment;

our ability to maintain the security of our information technology (IT) infrastructure against cyber-attacks and security breaches;

our ability to manage unexpected changes in workers’ compensation and health insurance claims by worksite employees;

the unpredictable nature of our costs and operating expenses, in particular our workers’ compensation and health insurance costs;

our ability to remediate the material weaknesses in our internal controls over financial reporting;

our ability to effectively acquire and integrate new businesses;

our ability to gain new clients, and our clients’ ability to grow and gain more employees;

volatility in the financial and economic environment to small and mid-sized businesses;

the effects of increased competition and our ability to compete effectively; and

our ability to comply with the restrictions of our credit facility and meet our debt obligations.

Any of these factors, as well as such other factors as discussed in the section titled “Risk Factors” included under Part I, Item 1A, below.and throughout Part II, Item 7 of this Annual Report on Form 10-K (Form 10-K), as well as in our periodic filings with the Securities and Exchange Commission (SEC), could cause our actual results to differ materially from our anticipated results. The information provided in this Form 10-K is based upon the facts and circumstances known at this time, and any forward-looking statements made by us in this Form 10-K speak only as of the date on which they are made. All information provided in this report is as of the date of this report and we undertake no duty to update this information except as required by law.

PART I

Item 1. Business

Business OverviewGeneral

TriNet Group Inc., or TriNet or the Company, is a leading provider of comprehensive human resources or HR,(HR) solutions for small to midsize businesses or SMBs, under a(SMBs). Under our co-employment model. Our HR solutions are designed to managemodel, we assume many of the complex and burdensome responsibilities of being an increasingly complex set of HR regulations, costs,employer, helping our clients minimize employer-related risks and manage administrative and compliance responsibilities for our clients, allowing them to focus on operatingassociated with employment. We provide an HR technology platform with online and growing their core businesses. Our bundled HR solutions include offerings such as:

multi-state payroll processing and tax administration;

employee benefits programs, including health insurance and retirement plans;

workers compensation insurance and claims management;

federal, state and local labor, employment and benefit law compliance;

risk mitigation, including employment practices claims management;

expense and time management; and

human capital consulting.

Our proprietary, cloud-based HR software systems are used bymobile tools that allow our clients and their employees, whom we refer to as worksite employees or WSEs,(WSEs) to efficiently store, view and manage their core HR-related information and conduct a variety of HR-related transactions anytime and anywhere.

We utilize our size and scale to provide our clients with a broad range of employee benefit and insurance programs generally not available to individual SMBs. In addition, our expertservice teams of in-house HR professionals also provide additional services upon request to support various stages of our clients' growth, includinghelp with talent management, recruiting and training, performance management, consulting or other consultingemployee onboarding and terminations, benefits enrollment and support, claims administration and employment practices risk management. We also monitor employer-related developments and assist clients in complying with applicable local, state and federal regulations.

Our strategy is to provide industry-specific products and services (with an incremental chargeto help clients address their HR needs and allow them to focus on operating and growing their businesses. We believe our industry-oriented (vertical) approach is a key differentiator for such services).

us and delivers significant benefits to our clients. This allows our sales force, product development and service teams to tailor product and service offerings to the specific industry needs of our clients. As of December 31, 2015,2016, we served over 12,700have introduced four verticals - TriNet Financial Services, TriNet Life Sciences, TriNet Nonprofit and TriNet Technology - and we intend to continue to develop and offer new industry vertical products in the future.

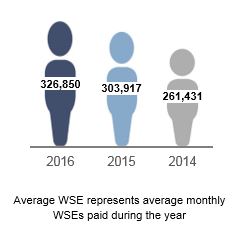

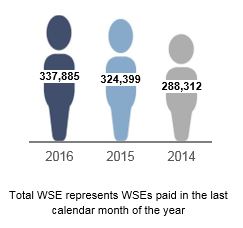

TriNet was founded in 1988 and has significantly grown the number of clients we serve, both organically and through strategic acquisitions, including our acquisitions of SOI Holding, Inc. (SOI) and Park Avenue Holding, Inc. (Accord) in 2012 and Ambrose Employer Group, LLC (Ambrose) in 2013. For the year ended December 31, 2016, we processed $34 billion in payroll payments for approximately 13,900 clients with about 338,000 WSEs in all 50 states, the District of Columbia and Canada, co-employed more than 324,000 WSEsCanada.

Products and had processed over $31 billion in payroll and payroll tax payments for clients on our systems in 2015. Our clients are distributed across a variety of industries, including technology, life sciences, not-for-profit, professional services, financial services, property management, retail, manufacturing, and hospitality. Our sales and marketing, client services and product development teams are increasingly focused on specific industry verticals. This verticalized approach gives us a deeper understanding of the HR needs facing SMBs in particular industries, which better enables us to provide HR solutions and services tailored to the specific needs of clients in these verticals. We conduct our business primarily in the United States, with more than 99% of our total revenues for each of 2015, 2014 and 2013 being attributable to WSEs in the U.S. and the remainder being attributable to WSEs in Canada.

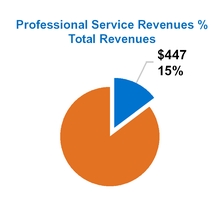

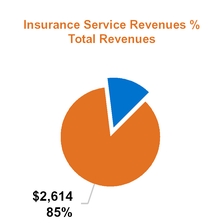

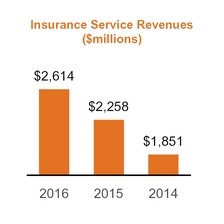

For 2015, 2014 and 2013, our total revenues were $2.7 billion, $2.2 billion and $1.6 billion respectively. Our total revenues consist of professional service revenues and insurance service revenues. For 2015 and 2014, 15% and 16% of our total revenues, respectively, consisted of professional service revenues, and 85% and 84% of our total revenues, respectively, consisted of insurance service revenues.Services

We recognize as professional service revenues the fees we earn for providing our clients withdeliver a comprehensive suite of HR professionalproducts and services but do not include amounts paid to us by clients as payroll that are paid out to WSEs or amounts withheld and remitted to authorities as taxes.

We recognize as insurance service revenues all insurance-related billings and administrative fees collected fromwhich allow our clients and withheld from WSEs. We pay premiumstheir WSEs to third-partyadminister and manage HR-related compensation and benefits, including payroll, health insurance carriers for client and WSE insurance benefits and reimburse the insurance carriers and third-party administrators for claims payments made onworker's compensation programs, through our behalf within our insurance deductible layer, where applicable. These premiums and reimbursements are classified as insurance costs on our statements of operations.

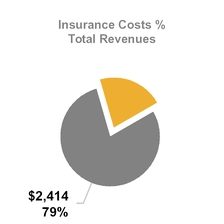

To augment our financial information prepared in accordance with U.S. generally accepted accounting principles, or GAAP, we use internally a non-GAAP financial measure, Net Insurance Service Revenues, which consists of insurance service revenues less insurance costs. We also use a measure of total non-GAAP revenue, or Net Service Revenues, which is the sum of professional service revenues and Net Insurance Service Revenues. For 2015, 2014 and 2013, Net Service Revenues were $546.9 million, $507.2 million and $417.7 million, respectively. For 2015, 73% of our Net Service Revenues consisted of professional service revenues and 27% of our Net Service Revenues consisted of Net Insurance Service Revenues.

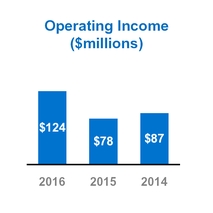

For 2015, 2014 and 2013, our net income was $31.7 million, $15.5 million and $13.1 million, respectively, and our Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization, or Adjusted EBITDA, was $151.3 million, $165.3 million and $136.0 million, respectively.technology platform.

Our Servicescomprehensive HR products and solutions include the following common capabilities:

We provide our clients |

| | | | | | |

| |

| |

| |

|

TECHNOLOGY PLATFORM | | HR EXPERTISE | | BENEFITS | | COMPLIANCE |

| | | | | | |

Technology Platform

Our HR technology platform, with a comprehensive suite of HR professional services that we believe enable SMBs to effectively execute fundamental HR transactions and manage an increasingly complex set of HR regulations, costs, risks and responsibilities.

As part of our professional service offerings, we provide our clients with fundamental HR transactional capabilities, including multi-state payroll processing and tax administration, as well as a cloud-based system of record for all their HR transactions. Our online and mobile self-service tools enableallows our clients for example,and WSEs to store, view and manage effectivelycore HR information and administer a variety of HR transactions, such as payroll processing, tax administration, employee hiringonboarding and termination, administer changescompensation reporting, expense management, and benefits enrollment and administration.

Our strategy is to employee payroll, view real-time benefits datacontinue to invest in product development and create compensation reports. In addition, WSEs are able to access our system to manage their own payroll information, request paid time off (PTO)improve the functionality, experience and view approval status real-time, view paystubs, PTO balances, W-2s and more. This HR functionality is a core componentease of use of our professionalproducts and services for clients and their WSEs. We have transformed the way we deliver our products and services though a full-service online and mobile platform, with standard Application Programming Interfaces (API) for integrating selected third-party software offerings and with an improved client experience for key processes. We will continue to integrate functionality and retire legacy software systems inherited from acquisitions and migrate clients to our primary TriNet software system. We believe the continued improvement of our technology platform and the

consolidation of legacy systems allows us to drive operating efficiencies and improve the user experience by providing a unified view of all pertinent HR service offering.information.

During 2016, 2015 and 2014 we invested approximately $52.7 million, $38.7 million and $32.4 million, respectively, developing our technology solutions.

HR Expertise

We also leverageuse the collective insights and experience that we have gained overof our 27-year operating historyteams of HR, benefits, risk management and compliance professionals to help clients mitigate many of the many administrative, regulatory and practical risks associated with their responsibilities as employers. We continuously monitor changes in the labor, employment and benefit regulatory environment and offer guidanceemployers, including talent management, recruiting and training, to clients to assist them in avoiding or reducing liabilityperformance management, employee onboarding and exposure.terminations, benefits enrollment and support, claims administration and employment practices risk management. Our professional HR services includeteams provide access to HR templates, best practices, employee handbooks, disciplined process management guidelines, employee relations consultation, issue investigation workplace employment posters,support, and compensation practice benchmarking data. In addition,employee communications. Each of our clients are ableand WSEs have access to consult directly withvarying levels of service and support from our HR professionals through a variety of interaction models,experts ranging from call center support for basic questions to pooled specialized resources and dedicated HR professionals,to onsite consulting and services, depending uponon the needs of the client and their WSEs. OurIn addition, our teams of in-house HR teamsprofessionals can also provide additional, incremental consulting and other services upon requestrequest.

Under our vertical strategy, we continue to tailor our product and service offerings to specific industries by identifying common needs and leveraging scale and shared experience to provide more efficient, relevant offerings. For example, our fourth vertical product, TriNet Technology, is specifically targeted to help support stages of our clients’ growth, includingthe talent recruiting, orequity compensation and foreign employee immigration needs with applicant tracking systems, immigration services for employees requiring work visas and online tools to help clients manage equity compensation plans that SMBs in other services (with an incremental charge for such services).industries do not face. We now offer four industry specific product offerings: TriNet Technology, TriNet Financial Services, TriNet Life Sciences and TriNet Nonprofit.

Insurance ServicesBenefits

We offer our clients and WSEs access to a broad range of TriNet-sponsored benefitsbenefit and insurance programs that many of our clients may be unable to obtain for their WSEs on their own and that are compliant with state, local, and federal regulations. We believe access to our fully-insured, Affordable Care Act compliant group health insurance plans is one of the

most important benefits we provide to our clients and WSEs. In addition, ourOur insurance services offerings include plan design and administration, enrollment management, and WSE and client communications relating to our sponsored benefits and insurance programs. As described below,

We pay premiums to third-party insurance carriers for WSE insurance benefits and reimburse the principal components ofinsurance carriers and third-party administrators for claims payments made on our behalf within our insurance services offerings are employee benefit plans, workers compensation insurance and employment practices liability insurance.deductible layer, where applicable.

Employee Benefit Plans

Plans: We sponsor and administer a number ofseveral fully-insured, risk based employee benefit plans, including group health, dental, vision and life insurance as an employer plan sponsor under Section 3(5) of the Employee Retirement Income Security Act or ERISA.(ERISA). We also offer other benefit programs to our clients and WSEs, including flexible spending accounts, retirement plans, Consolidated Omnibus Budget Reconciliation Act (COBRA) benefits, individual life insurance, a legal services plan, commuter benefits, home insurance, critical illness insurance, pet insurance and auto insurance. We provide group insurance coverage to our WSEs through a national network of carriers including Aetna, Blue Shield of California, Florida Blue, BlueCross BlueShield of North Carolina, Tufts, Kaiser Permanente, MetLife United Healthcare, EyeMed, Delta Dental and Vision Service Plan.

Approximately 38%For further discussion of our 2015 group health insurance premiums were for fully insuredfully-insured programs including policies with respect to which our carriers set the premiums and for whichwhere we were not responsible for any deductible, which are referred to as ‘guaranteed cost’ policies. The remaining 62% of our 2015 group health insurance premiums were for fully insured policies with respect to which we agree to pay additional amounts toreimburse our carriers for anycertain amounts relating to claims, paid within an agreed-upon deductible layer. Our agreements with our health insurance carriers with respect to these non-'guaranteed cost' policies typically include limits to our exposure for individual claims, which we refer to as ‘pooling’ limits, and limits to our maximum aggregate exposure for claimsNote 1 in a given policy year, which we refer to as ‘stop loss’ limits. We have experienced variability, and may experience variability in the future, in the amounts that we are required to pay our health insurance carriers for group health insurance expenses incurred by WSEs within our deductible layer under non-'guaranteed cost' policies, based on continually changing trends in the frequency and severityPart II, Item 8 of claims. These historical trends may change, and other seasonal trends and variability may develop, which may make it more difficult for us to manage this aspect of our business.Form 10-K.

Workers Compensation Insurance

Workers' Compensation: We provide fully-insured workersworkers' compensation insurance coverage for our clients and WSEs through agreementsinsurance policies that we negotiate with our third-party insurance providers. These agreements typically include a deductible layercarriers. Additionally, we help clients manage their risk by providing risk management services, including performing workplace assessment, safety consultation, accident investigation and other risk management services at our client locations to help prevent workplace accidents that obligates uscould lead to reimburse our carriers upclaims. We also provide services to $1 million per claim occurrence. help remediate such claims when they occur.

We manage the deductible risk that we assume in connection with these policies by being selective in the types of businesses that we take on as new clients, by monitoring claims data and the performance of our carriers and third-party claims management services and vendors and by providing risk management services for existing clients. These services include performing workplace assessment, safety consultation, accident investigation and other risk management services at our client locations to help prevent situations that could lead to claims and services to help remediate claims when they occur.

Employment Practices Liability Insurance

(EPLI): We provide employment practices liability insurance (EPLI)EPLI coverage for our clients through agreementsinsurance policies that we negotiate withobtain from our third-party EPLI insurance provider.carrier. These EPLI policies provide coverage for certain claims that arise in the course of the employment relationship such as discrimination, harassment, and certain other employee claims,

with a per-claim retention amount. For most of our clients, the retention amount is split between the client and TriNet, with the client paying its portion of the retention amount first.

While we do not provide legal representation to our clients, our clients can benefit from the extensive experience of our employment law specialists in our legal department who support ourand HR professionals in their efforts towho assist clients in avoidingimplementing HR best practices to avoid employment practices liability claims and in managing, processing and responding to such claims. For claims covered by theour EPLI insurance, actual litigation defense is conducted by one of several outside employment law firms chosen by the EPLI carrier with whom we and our EPLI carriers have previously negotiated rates, established billing guidelines and invoice review processes andprocesses. We have also developed a case management protocol to efficiently and effectively defend such claims.

Seasonality and Insurance VariabilityCompliance

Our business is affected by cyclicalityproducts and services are designed to help our clients comply with local, state and federal employment and benefit laws. Often these changes are staggered and require additional guidance from a variety of local, state or federal agencies, making compliance a continuous challenge. We monitor employer-related developments and assist clients in business activitycomplying with changing regulations and WSE behavior. Historically, we have experienced our highest monthly addition of WSEs,requirements at all levels, from changes in local minimum wage and family leave ordinances to sweeping reforms such as well as our highest monthly levels of client attrition, in the month of January, primarily because clients that change their payroll service providers tend to do so at the beginning of a calendar year. We also experience higher levels of client attrition in connection with renewals of the health insurance we sponsor for our WSEs, in the event that such renewals result in higher costs to our clients. We have also historically experienced higher insurance claim volumes in the secondPatient Protection and third quarters of a fiscal year than in the first and fourth quarters of a fiscal year, as WSEs typically access their health care providers more often in the second and third quarters of a fiscal year, which has negatively impacted our insurance

costs in these quarters. We have also experienced variability on a quarterly basis in the amountAffordable Care Act (ACA). Each component of our healthHR solutions is designed with compliance in mind, whether it is payroll processing and workers compensation insurance costs due to the number and severity of insurance claims being unpredictable. These historical trends may change, and other seasonal trends and variability may develop which would make it more difficult for us to manage our business.tax administration, HR services focused on creating a compliant workplace, or offering ACA-compliant benefit plans.

Our Co-Employment Model

We operate under a co-employment model business model, under which employment-related responsibilities are contractually allocated between us and our clients, which affords us a close relationship with ourclients. This model allows clients and their WSEs.WSEs to receive the full benefit of our employee benefit plan offerings. Each of our clients enters into a client service agreement with us that defines the suite of professional and insurance services and benefits to be provided by us, the fees payable to us, and the division of responsibilities between us and our clientclients as co-employers. The division of responsibilities under our client service agreements is typically as follows:

TriNet Responsibilities

We assume responsibility for, and manage certain risks associated with:

remittance to WSEs of salaries, wages and certain other compensation, as reported and paid to us by the client, related tax reporting and remittance to tax authorities and processing of garnishment and wage deduction orders. Unlike a payroll service provider, we issue each WSE a payroll check drawn on our bank accounts;accounts,

report the wages, withhold and deposit the associated payroll taxes as the employer on information reporting and payroll tax returns,

maintenance of workersworkers' compensation insurance and workersworkers' compensation claims processing;processing,

provision and administration of group health, welfare, and retirement benefits to WSEs based on our clients’ elections, under TriNet-sponsored insurance plans;plans,

compliance with applicable law for employee benefits offered to WSEs;WSEs,

processing of unemployment claims;claims, and

provision of certain HR policies, including an employee handbook describing the co-employment relationship.

Client Responsibilities

Our clients are responsible for employment-related responsibilities that we do not assume, including:

day-to-day management of their worksites and WSEs;WSEs,

compliance with laws associated with the classification of employees as exempt or non-exempt, such as overtime pay and minimum wage law compliance;compliance,

accurate and timely reporting to TriNet of compensation and deduction information, including information relating to hours worked, rates of pay, salaries, wages and certain other compensation;compensation,

accurate and timely reporting to TriNet of information relating to workplace injuries, employee hires and termination, and certain other information relevant to TriNet’s services;services,

provision and administration of any employee benefits not provided by TriNet (e.g., equity incentive plans);,

compliance with all laws and regulations applicable to the client’sclients' workplace and business, including work eligibility laws, laws relating to workplace safety or the environment, laws relating to family and medical leave, laws pertaining to employee organizing efforts and collective bargaining and employee termination notice requirements;requirements,

payment of TriNet invoices which include wages to WSEs and applicable employment taxes and service fees;fees, and

all other matters for which TriNet does not assume responsibility under the client service agreement, such as intellectual property ownership and protection and liability for products produced and/or services provided.

As a result of our co-employment relationship with each of our WSEs, we are liable for payment of salary, wages and certain other compensation to the WSEs as reported and paid to us by the client and are responsible for providing specified employee benefits to such persons to the extent provided in each client service agreement and under federal and state law. In most instances, clients are required to remit payment prior to the applicable payroll date by wire transfer or automated clearinghouse transaction. Although we may become liable, as the employer for payroll purposes, to pay certain amounts for work previously performed, we are not obligated to continue to provide services to the client if payment has not been made. For the year ended December 31, 2015, our bad debt expense relating to such obligations was approximately $2.0 million.transaction (ACH).

We also assume responsibility for payment and liability for the withholding and remittance of federal and state income and employment taxes with respect to salaries, wages and certain other compensation paid to WSEs, although we reserve the right to seek recourse against our clients for any liabilities arising out of their conduct. We perform these functions as the employer for federal employment tax purposes, since our clients transfer legal control over these payroll functions to us. Except to the extent applicable federal legislation and applicable state lawlaws otherwise provide, the client may be held ultimately liable for those obligations if we fail to remit taxes and the bonding security provided by the Employer Services Assurance Corporation (ESAC) is not sufficient to satisfy the obligation. We also secure insurance in the event that we fail to meet these obligations.

Our Technology Platform

We provide our clients and WSEs with fundamental HR transactional capabilities, as well as a cloud-based system of record for all their HR transactions. Our online and mobile self-service tools allow our clients and WSEs 24/7 access to their core HR information. On our systems, clients can effectively manage employee hiring and termination, administer employee payroll, view real-time benefits data and create compensation reports. WSEs can also manage their own payroll information, request paid time off (PTO) and view approval status real-time, enroll in benefits, and view paystubs, PTO balances, and W-2s, among other things. We also offer human capital management software offerings, including talent management and development, applicant tracking, expense management, and performance management. These modules can be either bundled into the product offering or purchased as add-ons for certain of our verticals. We have also made significant investments to integrate our software offerings with those of certain third-party technology and benefits services providers to allow clients and WSEs to access a unified view of all of their pertinent HR information.

By offering a proprietary, cloud-based HR system, our clients gain the efficiencies of an enterprise-level software solution without the significant cost of in-house installation or ongoing maintenance. Features include:

multi-tenant system enabling multiple clients and WSEs to share one version of our system while isolating each client’s and WSE’s data;

rule-based provisioning ensuring that all users are authenticated, authorized and validated before they can access our systems;

redundant processing centers to protect client data from loss;

integrated benefits and payroll processing for faster, more accurate data; and

flexible and extensible platform architecture.

From 2013 through 2015, we invested approximately $111.3 million in our technology systems. We plan to continue to invest to upgrade and improve our technology offerings, including enhancements of our solutions to address specific needs of clients in our key vertical markets, as we believe the continued improvement of our technology provides TriNet with the ability to drive operating efficiencies while improving our clients’ experience. We will leverage our existing online technology offerings to build additional products and features, including a full-service mobile platform, standard APIs for selected third party offerings, improved client experience for key processes, and retirement of legacy software systems from acquisitions and migration of clients to the primary TriNet software system.

Competition

We face significant competition on a national and regional level from a number of companies purporting to deliver a range of bundled services that are generally similar to the services we provide. The National Association of Professional Employer Organizations, or NAPEO, estimates that there are between 780 and 980 such entities currently operating in the United States. We are one of only five PEOs accredited by the Employer Services Assurance Corporation that offers services in all 50 states and believe that we are one of the largest PEOs in the industry. Our competitors include large PEOs such as the TotalSource unit of Automatic Data Processing, Inc. and Insperity, Inc., as well as specialized and smaller PEOs and similar service providers. If and to the extent that we and other companies providing these services are successful in growing our businesses, we anticipate that future competitors will enter this industry.

In addition to competition from other professional employer organizations, we also face significant competition in the form of companies serving their HR needs in both traditional and non-traditional manners. These forms of competition include:

HR and information systems departments and personnel of companies that perform their own administration of employee benefits, payroll and HR;

providers of certain endpoint HR services, including payroll, employee benefits and business process outsourcers with high-volume transaction and administrative capabilities, such as Automatic Data Processing, Inc., Paychex, Inc. and other third-party administrators;

employee benefit exchanges that provide benefits administration services over the Internet to companies that otherwise maintain their own employee benefit plans; and

insurance brokers who allow third party HR systems to integrate with their platform.

We believe that our services are attractive to many SMBs in part because of the quality and breadth of our workers compensation, group health insurance and other employee benefits programs. We compete with insurance brokers and other providers of this coverage in this regard.

We believe the principal competitive factors in our market include the following:

level of client satisfaction;

ease of client setup and on-boarding;

breadth and depth of benefit plans;

vertical market expertise;

total cost of service;

brand awareness and reputation;

ability to innovate and respond to client needs rapidly;

online and mobile functionality; and

subject matter expertise.

We believe that we compete favorably on the basis of each of these factors.

Sales and Marketing

We sell our solutions primarily through our direct sales organization. We have aligned our sales organization by industry vertical with the goal of drivinggrowing profitable market share in our targeted industries. This vertical approach deepens our network of relationships and gives us an understanding of the unique HR needs facing SMBs in those industries. As part of our vertical approach, we conduct industry-specific client marketing programs, including industry and geographic focus groups, to foster a sense of community through the sharing of best practices, while also collecting valuable information about the unique requirements of companies in particular industries. This knowledge then allows our sales team to work with our product development and client service teams to build bundled solutions of services that are tailored to the specific needs of clients in these industries.

The number of sales representatives in the field has grown substantially in recent years, through both internal hiring and through onboarding sales representatives from acquired businesses, from 80224 sales representatives as of December 31, 20112012 to 481452 sales representatives as of December 31, 2015. In our direct sales organization, we2016. We recruit and seek to hire sales professionals who have experience in a specific industry vertical market,markets, and with a background in selling business services such as accounting, HR or sales solutions. As of December 31, 2015,2016, we had approximately 5049 regional field sales offices.

Our sales team’s primary focus and goal is to win new accounts as opposed to mining our installed base of business for incremental revenue. In order to drive the most effective cost of acquisition for this new business, we continually fine-tune our lead generation and marketing efforts and our initiatives to attempt to drive higher productivity per sales representative.

Our marketing, inside sales, lead generation, and lead incubation efforts support the success of our direct sales representatives. We employ a broad range of vertically focused awareness and demand-generation marketing programs, including digital and print advertising, e-mail, direct mail and social media. We have an internal public relations team that works with an external agency to promote relevant content to target media outlets. We sponsor and participate in associations and events around the country and utilize these forums to target specific vertical and geographic markets. We also generate

sales opportunities and deepen our relationships within key industry verticals, through marketing alliances and other indirect channels, such as existing clients, certified public accountants,accounting firms, venture capital firms, incubators, insurance brokers, and other vertical market industry associations. Additionally, we utilize digital marketing programs, including digital advertising, search and email marketing, to create awareness and interest in our products.

We drive sales representative productivity in a number of ways, including by improving the quality of leads generated by our marketing and inside sales teams, and through the development of a sales operations team that offloads sales process work. We believe our focus on specific verticals, and the expertise gained through this focus, makes our sales representatives increasingly relevant to their target audience. Recently, we have expanded our focus on various channel relationships and alliances that drive warm leadsreferrals to our direct sales force. Finally, our sales representatives benefit from building strong relationships with prospects during the sales process,and client service processes, resulting in referrals to new prospects as well as direct support through providing reference calls in regardsregard to our products and services.

Legal and Regulatory

Our business operates in a complex environment created by the numerous federal, state and local laws and regulations relating to labor and employment matters, benefit plans and income and employment taxes. The following summarizes what we believe are the most important legal and regulatory aspects of our business:

Federal Regulations

Employer Status

We sponsor our employee benefit plan offerings as the “employer” of our WSEs under the Internal Revenue Code of 1986 (the Code), and ERISA. The multiple definitions of “employer” under both the Code and ERISA are not clear and most are defined in part by complex multi-factor tests under common law. We believe that we qualify as an “employer” of our WSEs in the U.S. under both the Code and ERISA, as well as various state regulations, but this status could

be subject to challenge by various regulators. For additional information on employer status and its impact on our business and results of operations, refer to Item 1A of this Form 10-K, under the heading - If we are not recognized as an employer of worksite employees under federal and state regulations, or are deemed to be an insurance agent or third-party administrator, we and our clients could be adversely impacted.

Affordable Care Act and Health Care Reform

The Patient Protection and Affordable Care Act (ACA) was signed into law in March 2010. The ACA implemented sweeping health care reforms with staggered effective dates from 2010 through 2020, and many provisions in the Act require the issuance of additional guidance from the U.S. Department of Labor (DOL), the Internal Revenue Service (IRS), the U.S. Department of Health and Human Services and the states. There could be significant changes to the ACA and health care in general in 2017 and beyond, including the potential modification, amendment or repeal of the ACA. For additional information on the ACA and its impact on our business and results of operations, refer to Item 1A of this Form 10-K, under the heading - Our business is subject to numerous complex state and federal laws, and changes in, uncertainty regarding, or adverse application of these laws could adversely affect our business.

Health Insurance Portability and Accountability Act

Maintaining the security of our WSEs information is important to TriNet as we sponsor employee benefit plans and may have access to personal health information of our WSEs. The manner in which we manage protected health information (PHI) is subject to the Health Insurance Portability and Accountability Act of 1996 (HIPAA), and the Health Information Technology for Economic and Clinical Health Act of 2009 (HITECH Act). HIPAA contains substantial restrictions and health data privacy, security and breach notification requirements with respect to the use and disclosure of PHI. Further, under the HITECH Act there are steep penalties and fines for HIPAA violations. Our health plans are covered entities under HIPAA, and we are therefore required to comply with HIPAA's portability, privacy, and security requirements.

However, only our Flexible Spending Accounts and SOI dental plans come into direct contact with PHI. The other health information we possess is anonymized and accessed through a secured third-party database. For additional information on how we maintain the confidentiality of our clients' and WSEs' personal data and PHI and the potential impact to our business if we fail to protect our WSEs' PHI, refer to Item 1A of this Form 10-K, under the heading - Cyber-attacks or security breaches could result in reduced revenue, increased costs, liability claims or damage to our reputation.

Certified Professional Employer Organization (PEO)

With passage of the Small Business Efficiency Act in 2014, the U.S. Congress clarified the employer status of PEOs who voluntarily become certified under this law for federal tax purposes under the Code. The IRS has started accepting applications for certification under the Code, and we intend to apply for certification, even though final regulations for the certification program have not yet been issued.

State Regulations

Forty-two states have adopted provisions for licensing, registration, certification or recognition of co-employers, and others are considering such regulation. Such laws vary from state to state but generally provide for monitoring or ensuring the fiscal responsibility of PEOs, and in some cases codify and clarify the co-employment relationship for unemployment, workers' compensation and other purposes under state laws. We believe we are in compliance in all material respects with the requirements in all 42 states.

We must also comply with state unemployment tax requirements where our clients are located. State unemployment taxes are based on taxable wages and tax rates assigned by each state. The tax rates vary by state and are determined, in part, based on our prior years’ compensation and unemployment claims experience in each state. Certain rates are also determined, in part, by each client’s own compensation and unemployment claims experience. In addition, states have the ability under law to increase unemployment tax rates, including retroactively, to cover deficiencies in the unemployment tax funds.

Strategic Acquisitions

Historically, we have pursued strategic acquisitions to both expand our product capabilities and supplement our growth across geographies and certain industry verticals. Our acquisition targets have included other bundled HR providers as well as technology companies or technology product offerings to supplement or enhance our existing HR solutions. We intend to continue to pursue strategic acquisitions that will enable us to add new clients and WSEs, expand our presence in certain geographies or industry verticals and offer our clients and WSEs more comprehensive and attractive products and services.

ClientsClient Industries and Geographies

We approach the market with a vertical, or industry-based, focus. Our clients spanare distributed across a variety of industries including technology, life sciences, not-for-profit, professional services, financial services, property management, retail, manufacturing, and hospitality. We have grownOur clients execute annual service contracts with us that automatically renew. Generally, our number of clients from approximately 4,500 as of December 31, 2011may cancel these contracts with thirty to over 12,700 clients as of December 31, 2015. We have also grown our number of WSEs from approximately 83,000 as of December 31, 2011 to approximately 324,000 in all 50 states, the District of Columbianinety days' notice and Canada as of December 31, 2015.

U.S. Legal and Regulatory Environment

The complex environment created by the numerous federal, state and local laws and regulations relating to labor and employment matters, benefit plans and income and employment taxes creates a significant demand for our HR solutions. Many of those laws and regulations also significantly affect how we are able to provide our HR solutions to our clients. Many ofmay cancel these laws, such as ERISA, were enacted before the development of the co-employment relationship and other non-traditional employment relationships, such as temporary employment and other employment-related outsourcing arrangements. Therefore, many of these laws do not specifically address the obligations and responsibilities of professional employer organizations utilizing a co-employment model like ours, creating uncertainty about their interpretation and application to our industry. In addition, other federal and state laws and regulations, such as the Affordable Care Act, are relatively new and administrative agencies and federal and state courts have only begun to interpret and apply these regulations to our industry. The development of additional regulations and interpretation of these laws and regulations can be expected over time.contracts with thirty days' notice.

We believe thatconduct our operations are currently in compliance in all material respects with applicable federal and state statutes and regulations. The sections discussed below summarize what we believe are the most important regulatory aspects of our business:

Employer Status

In order for clients and WSEs to receive the full benefit of our employee benefit plan offerings, it is important that we constitute the “employer” of the WSEs under the Internal Revenue Code of 1986, or the Code, and ERISA. The definitions of “employer” under both the Code and ERISA are not clear and are defined in part by complex multi-factor tests under common law. We believe that we qualify as an “employer” of our WSEsbusiness primarily in the United States under bothof America (U.S.), with more than 99% of our total revenues being attributable to WSEs in the CodeU.S. and ERISA,the remainder being attributable to WSEs in Canada. Substantially all our long-lived assets are located in the U.S.

Seasonality

Our business is affected by seasonality in business activity and we implement processes to protect and preserve this status. With Congressional passageWSE behavior. Clients generally change their payroll service providers at the beginning of the Small Business Efficiency Act in December 2014, the Code clarified the employer status of professional employer organizations, or PEOs, for federalpayroll tax purposes, for those PEOs who voluntarily become certified under this law. The IRS is expected to begin accepting applications for certification in July 2016year and we currently intend to apply for certification.

Tax Qualified Plans. In order to qualify for favorable tax treatment under the Code, certain employee benefit plans such as 401(k) retirement plans and cafeteria plans must be established and maintained by an employer for the exclusive benefit of its employees. Generally, an entity is an “employer” of certain workers for federal employment tax purposes if an employment

relationship exists between the entity and the workers under the common law test of employment. The common law test of employment, as applied by the IRS, involves an examination of many factors to ascertain whether an employment relationship exists between a worker and a purported employer. Our 401(k) retirement plans are operated pursuant to guidance provided by the IRS for the operation of defined contribution plans maintained by co-employers that benefit WSEs. This guidance provides qualification standards for such plans. All of our 401(k) retirement plans have received favorable determination letters from the IRS confirming the qualified status of the plans. The IRS 401(k) guidance and qualification requirements are not applicable to the operation of our cafeteria plans.

ERISA Regulation. Employee pension and welfare benefit plans are also governed by ERISA. ERISA defines an “employer” as “any person acting directly as an employer, or indirectly in the interest of an employer, in relation to an employee benefit plan.” ERISA defines the term “employee” as “any individual employed by an employer.” The courts have held that the common law test of employment must be applied to determine whether an individual is an employee or an independent contractor under ERISA. However, in applying that test, control and supervision are less important for ERISA purposes when determining whether an employer has assumed responsibility for providing employee benefits. A definitive judicial interpretation of “employer” in the context of a professional employer organization has not been established, and the U.S. Department of Labor has issued guidance that certain entities in the HR outsourcing industry do not qualify as common law employers for ERISA purposes. If we were found not to be an employer for ERISA purposes, it could affect the manner in which we are able to provide employee benefits to our WSEs.

Affordable Care Act

The Affordable Care Act, or the Act, implemented sweeping health care reforms with staggered effective dates from 2010 through 2020, and many provisions in the Act require the issuance of additional guidance from the U.S. Department of Labor, the IRS, the U.S. Department of Health and Human Services and the states. The Act imposed a number of new mandates on the coverage required to be provided under health insurance plans beginning in 2010, with additional requirements staged in subsequent years. We believe that our group health insurance plans comply with existing mandates. However, the guidance issued to date by the IRS and the U.S. Department of Health and Human Services has not addressed, or in some instances is unclear, as to its application in the co-employer context. As a result, we are not yet able to predict allhave historically experienced our highest volumes of new and exiting clients in the impacts to our business,month of January. Other periods of client changes coincide with a client's benefit program renewal.

Competition

Our competitors include large PEOs such as the TotalSource unit of Automatic Data Processing, Inc. and Insperity, Inc., as well as specialized and smaller PEOs and similar HR service providers with PEO operations. If and to the extent that we and other companies providing these services are successful in growing our clients, resulting from the Act.businesses, we anticipate that future competitors will enter this industry.

State Unemployment Taxes

State unemployment taxes are based on taxable wages and tax rates assigned by each state. The tax rates vary by state and are determined, in part, based on our prior years’ compensation and unemployment claims experience in each state. Certain rates are also determined, in part, by each client’s own compensation and unemployment claims experience. In addition statesto competition from other PEOs, we also face significant competition from companies that serve part of a clients’ HR needs. These forms of competition include providers of endpoint HR services, employee benefit exchanges that provide benefits administration services and insurance brokers who allow third-party HR systems to integrate with their insurance services platform. Such competitors may have the ability under law to increase unemployment tax rates, including retroactively, to cover deficiencies in the unemployment tax funds. Due to the adverse U.S. economic conditions during recent yearsgreater marketing and the associated reductions in employment levels, the state unemployment tax fundsfinancial resources than we have, experienced a significant increase in the number of unemployment claims. Accordingly, state unemployment tax rates increased substantially over the past few years. Employers in certain states are also experiencing higher federal unemployment tax rates as a result of certain states not repaying their unemployment loans from the federal government in a timely manner. We have taken steps to mitigate the risk of fluctuations in state and federal unemployment tax rates, including reporting and remitting unemployment insurance taxes or contributions at the client level and/or under the client’s own account number in approximately 40 states, and we will continue to evaluate such reporting relationships in the future.

State Regulation of Co-Employers

Forty-two states have adopted provisions for licensing, registration, certification or recognition of co-employers, and others are considering such regulation. Such laws vary from state to state but generally provide for monitoring or ensuring the fiscal responsibility of professional employer organizations, and in some cases codify and clarify the co-employment relationship for unemployment, workers compensation and other purposes under state law. We believemay be better positioned than we are in compliance in all material respects with the requirements in all 42 states. Regardless of whether a state has licensing, registration or certification requirements for co-employers, we must comply with a number of other state and local regulations that could impact our operations, such as state and local taxes, licensing and business regulations.

Intellectual Property

Our success depends in part on intellectual property rights to the services that we develop. We rely on a combination of contractual rights, including non-disclosure agreements, trade secrets, copyrights and trademarks, to establish and protect our

intellectual property rightscertain markets. Increased competition in our names, services, methodologies and related technologies. If we lose intellectual property protectionindustry could result in price reductions or the ability to secure intellectual property protection on anyloss of our names, confidential information or technology, this could harm our business. Our intellectual property rights may not prevent competitors from independently developing services and methodologies similar to ours, and the steps we take might be inadequate to deter infringement or misappropriation of our intellectual property by competitors, former employees or other third parties,market share, any of which could harm our business. We expect that we will continue to experience competitive pricing pressure.

We believe the principal competitive factors in our market include client satisfaction, ease of client setup and on-boarding, breadth and depth of benefit plans, vertical market expertise, total cost of service, brand awareness and reputation, ability to innovate and respond to client needs rapidly, online and mobile solutions, and subject matter expertise. We believe that we compete favorably on the basis of each of these factors.

Intellectual Property

We own or license from third parties' various computer software, as well as other intellectual property rights, used in our business. Generally, we protect our intellectual property rights through the use of confidentiality and non-disclosure agreements and policies with our employees and third-party partners and vendors, although we currently have one pending U.S. patent application covering our technology. We also own registered trademarks in the United States,U.S., Canada and the European Union that have various expiration dates unless renewed through customary processes. Our trademark registrations may be unenforceable or ineffective in protectingcovering our trademarks. Ourname and other trademarks may be unenforceable in countries outside of the United States, which may adversely affect our ability to build our brand outside of the United States.

Althoughand logos that we believe thatare materially important to our conduct of our business does not infringe on the intellectual property rights of others, third parties may nevertheless assert infringement claims against us in the future. We may be required to modify our products, services, internal systems or technologies, or obtain a license to permit our continued use of those rights. We may be unable to do so in a timely manner, or upon reasonable terms and conditions, which could harm our business. In addition, future litigation over these matters could result in substantial costs and resource diversion. Adverse determinations in any litigation or proceedings of this type could subject us to significant liabilities to third parties and could prevent us from using some of our services, internal systems or technologies.operations.

Corporate Employees

We refer to our employees excluding employees that we do not co-employ on behalf ofwith our clients as our corporate employees. We had approximately 2,5002,600 corporate employees as of December 31, 2015.2016. None of our corporate employees isare covered by a collective bargaining agreement.

Corporate and Other Available Information

We were incorporated in 1988 as TriNet Employer Group, Inc., a California corporation. We reincorporated as TriNet Merger Corporation, a Delaware corporation, in 2000 and during that year changed our name to TriNet Group, Inc. Our principal executive offices are located at 1100 San Leandro Blvd., Suite 400, San Leandro, CA 94577 and our telephone number is (510) 352-5000. Our website address is www.trinet.com. Information contained in or accessible through our website is not a part of this report.

On the Investor Relations page of our Internet website at http://www.trinet.com, we make available, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Information contained in or accessible through our website isThe public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov. The contents of these websites are not incorporated into this report and isare not a part of this report.

Item 1A. Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully consider the following risks and all of the other information contained in this report, including the section of this report titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes. Any of the following risks could materially and adversely affect our business, financial condition and results of operations and cause a decline in the trading price of our common stock, and you may lose some or all of your investment.

Risks Related to Our Business and Industry

Our co-employment relationship with our worksite employees exposes us to business risks.

Under our agreements with our clients, we are a co-employer of our WSEs and assume certain obligations, including the responsibility to pay salaries, wages and related payroll taxes of our WSEs, and to do so, to the extent required by law, regardless of whether our client timely remits payments to us. In addition, we provide benefits to our WSEs, even if the cost of providing such benefits is greater than fees received from our clients. Although our client agreements require clients to pay these amounts or indemnify us for failure to make such payments, we may not be able to effectively enforce or collect on these contractual obligations. Accordingly, our ultimate liability for payroll and benefits expenses for our WSEs could exceed the amounts we receive from our clients, which could have a material adverse effect on our financial condition or results of operations.

Moreover, as a co-employer of our WSEs, there is a possibility that we may be subject to liability for violations of employment laws and other acts and omissions by our clients or WSEs, who may be deemed to be our agents, even if we do not participate in any such acts or violations. Such laws include, but are not limited to, laws relating to payment of wages, employment discrimination, labor relations and whistleblower protection. Although our client agreements establish the contractual division of responsibilities between us and our clients for various personnel management matters, including compliance with and liability under various governmental regulations, as well as providing for clients to indemnify us for any liability attributable to clients’ or their employees’ conduct, we may not be able to effectively enforce or collect on these contractual obligations, which could have a material adverse effect on our financial condition or results of operations.

We maintain employment practices liability insurance coverage (often including coverage for our clients) to manage our and our clients’ exposure for various WSE-related claims and are responsible (often together with our clients) for any deductible layer under such coverage. Furthermore, employment practices liability insurance generally excludes coverage for claims relating to compliance with laws associated with the classification of employees as exempt or non-exempt, such as overtime pay and minimum wage law compliance. We cannot assure you that our insurance will be sufficient in amount or scope to cover all claims that may be asserted against us and for which we are unable to obtain indemnification from our clients. If judgments or settlements or defense costs exceed our insurance coverage, it could harm our results of operations and financial condition. We cannot assure you that we will be able to obtain appropriate types and levels of insurance in the future, that we will be able to replace existing policies on acceptable terms, or at all, or that our insurers will be able to pay all claims that we may make under our policies, any of which could have a material adverse effect on our financial condition or results of operations.

Our business is subject to numerous state and federalcomplex laws, and changes in, uncertainty as to theregarding, or adverse application of these laws or adverse applications of these laws, as well as changes in applicable laws, could adverselynegatively affect our business.

Our operationsThe products and services we provide to our clients are governed by numerous complex federal, state and local laws relating to labor, tax, employee benefits, insurance and employment matters. However, manyregulations, including those described under the heading "Legal and Regulatory" in Item 1 of this Form10-K. Many of these laws (such as ERISA and federal and state employment tax laws)laws, wage and hour laws, anti-discrimination laws, etc.) may not result in a consistent approach at the federal, state and local level, do not specifically address the obligationsPEOs and responsibilitiesco-employment relationships or may allow significant regulatory interpretation and discretion in enforcement. As a result, there is uncertainty in how they might be applied to our operations and those of a professional employer organization providing outsourced HR services in a co-employment relationship, and the definition of employer under these laws is not uniform. In addition, many states have not addressed the co-employment relationship for purposes of compliance with applicable state laws governing the relationship between employers and employees and state insurance laws. We are not able to predict whether broader federal or state regulation governing our business and the co-employment relationship with our WSEs will be implemented, or if it is, how it will affect us, our clients and WSEs.

New laws, changes in existing laws, or our WSEs. Any adverse application or interpretation (in courts, agencies or otherwise) of new or existing federal or state laws to theregarding our co-employment relationship with our clients and WSEs could reduce or eliminate the need for, or benefit provided by, some or all of the services we provide or require us to make significant changes in our methods of doing business and providing services, which could have a material adverse effect on our financial condition and results of operations. If federal, state or local jurisdictions were to change their regulatory framework related to outsourced HR services, or introduce new laws governing our industry that were materially different from existing laws, thoseRegulatory changes could reduce or eliminate the need for some of our services, or could require that we make significant changes in our methods of doing business, which could increase our cost of doing business. Changes in regulations could also affect the extent and type of employee benefits employers can or must provide employees, the amount and type of taxes employers and employees are required to pay or the time within which employers must remit taxes to the applicable tax authority. These changesFor example, continued uncertainty regarding the implementation and future of health care reform in the U.S. under the ACA, any successor to the ACA, related or similar state laws, and the regulations adopted or to be adopted thereunder, has the potential to substantially change the health insurance market for SMBs and how such employers provide health insurance to their employees, which could substantially decrease our revenues and substantially increase our cost of doing business and have a materialmaterially adverse effect on our financial conditionability to attract and resultsretain our clients. In addition, there could be significant changes to the ACA in 2017 and beyond, including the potential modification, amendment or repeal of the ACA. Changes to the ACA could also result in new or amended regulations being introduced at the state or local level. Changes in, or uncertainty regarding, the ACA and other health care reforms could impact our business and we are not able to predict the direction or ultimate impact of health care reform on our business operations.

Although some statesSimilarly, state regulatory authorities generally impose licensing requirements on companies acting as insurance agents or third-party administrators, such as those that handle health or retirement plan funding and claim processing. We do not explicitly regulate professional employer organizations, 42 states have passed lawsbelieve that haveour current activities require such licensing, certificationbut if regulatory authorities in any state determine that we are acting as an insurance agent or registration requirements applicable to professional employer organizations or recognize the professional employer organization model, and other states may implement such requirements in the future. Laws regulating professional employer organizations vary from state to state, but generally provide for oversight of the fiscal responsibility of professional employer organizations, and in some cases codify and clarify the co-employment relationship for processing unemployment claims, workers compensation and other purposes under state law. We may be required to spend significant time and resources to satisfy licensing requirements or other applicable regulations in some states, andas a third-party administrator, we may not be ableneed to satisfy these requirements or regulations in all states, which could prohibit us from doing business in such states,hire additional personnel to manage regulatory compliance and become obligated to pay annual regulatory fees, which could have a material adverse effect on our financial condition and results of operations.

Our co-employment relationship with our worksite employees exposes us to business risks.

We are the co-employer of our WSEs. As the co-employer of our WSEs, we assume certain obligations and responsibilities of an employer. For instance, we are responsible for providing benefits to our WSEs regardless of whether the cost of providing benefits exceeds the fees received from our clients. Under certain circumstances, it could be argued that we are, or we may be found to be, responsible for paying salaries, wages and related payroll taxes of our WSEs, regardless of whether our client timely remits payments to us.

We co-employ people in our clients' workplaces. Our ability to control the workplace environment of our clients is limited. As a co-employer of our WSEs, there is a possibility that we may be subject to liability for violations of employment or other laws and other acts and omissions by our clients or WSEs, who may be deemed to be our agents, even if we do not participate in any such acts or violations.

We seek to mitigate these risks through our client agreements and with employment practices liability insurance coverage. Our agreements with our clients establish the contractual division of responsibilities between us and our clients and that they will indemnify us for any liability attributable to their own or our WSEs' conduct, however, we may not be able to effectively enforce or collect on these contractual obligations. In addition, we maintain employment practices insurance to limit our and our clients' exposure to various WSE related claims, but we are still responsible for any deductible layer under such insurance and such insurance generally excludes coverage for claims relating to the classification of employees as exempt or non-exempt, other wage and hour issues, and employment contract disputes, among other things. We cannot assure you that our insurance will be sufficient in amount or scope to cover all claims that may be asserted against us and for which we are unable to obtain indemnification from our clients. Negative publicity relating to events or activities attributed to us, our corporate employees, our WSEs, or others associated with any of these parties, whether or not justified, may tarnish our reputation and reduce the value of our

brand. In addition, if our brand is negatively impacted, it may have a material adverse effect on our business, including creating challenges in retaining clients or attracting new clients and hiring and retaining employees.

If we are not recognized as an employer of worksite employees under federal and state regulations, or are deemed to be an insurance agent or third-party administrator, we and our clients could be adversely impacted.

In order for WSEs to receive the full benefit ofsponsor our employee benefitsbenefit plan offerings it is important thatfor our WSEs, we act andmust qualify as an employer of theour WSEs for certain purposes under the Code and ERISA. In addition, our status as an employer is important for purposes of ERISA’s preemption of certain state laws. The definition of employer under various laws is not uniform, and under both the Code and ERISA, the term is defined in part by complex multi-factor tests. We believe

Generally, these tests are designed to evaluate whether an individual is an independent contractor or employee and they provide substantial weight to whether a purported employer has the right to direct and control the details of an individual's work. Some factors that we