SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended April | ||

| or | ||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period fromto | ||

Commission File Number 1-3385

H. J. HEINZ COMPANY

(Exact name of registrant as specified in its charter)

| PENNSYLVANIA | 25-0542520 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) | |

One PPG Place | 15222 | |

Pittsburgh, Pennsylvania | (Zip Code) | |

| (Address of principal executive offices) | ||

412-456-5700

(Registrant’s telephone number)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes þ No o No þ

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 ofRegulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 ofRegulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of thisForm 10-K or any amendment to thisForm 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” inRule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | Accelerated filer o | Non-accelerated filer (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined inRule 12b-2 of the Exchange Act). Yes o No þ

As of October 27, 201028, 2012, the aggregate market value of the Registrant’s voting stock held by non-affiliates of the Registrant was approximately $15.5 billion.$18.3 billion.

The number of shares of the Registrant’s Common Stock, par value $.25 per share, outstanding as of May 31, 2011,June 20, 2013, was 321,767,370100 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the Annual Meeting of ShareholdersCompany's Amendment to be held on August 30, 2011,Form 10-K, which will be filed with the Securities and Exchange Commission within 120 days after the end of the Registrant’sRegistrant's fiscal year ended April 27, 2011,28, 2013, are incorporated into Part III, Items 10, 11, 12, 13, and 14.

Introductory Note

On June 7, 2013, H. J. Heinz Company (the “Company,” “we,” “us,” and “our”) was acquired by H.J. Heinz Holding Corporation (formerly known as Hawk Acquisition Holding Corporation) (“Parent”), a Delaware corporation controlled by Berkshire Hathaway Inc. (“Berkshire Hathaway”) and 3G Special Situations Fund III, L.P. (“3G Capital,” and together with Berkshire Hathaway, the “Sponsors”), pursuant to the Agreement and Plan of Merger, dated February 13, 2013 (the “Merger Agreement”), as amended by the Amendment to Agreement and Plan of Merger, dated March 4, 2013 (the “Amendment”), by and among the Company, Parent and Hawk Acquisition Sub, Inc., a Pennsylvania corporation and wholly owned subsidiary of Parent (“Merger Subsidiary”), in a transaction hereinafter referred to as the “Merger.” As a result of the Merger, all issued and outstanding shares of our common stock outstanding immediately prior to the effective time of the Merger was converted into the right to receive $72.50 in cash, without interest and less applicable withholding taxes thereon, and the Company continued as the surviving corporation in the Merger, becoming an indirect wholly owned subsidiary of Parent.

The total cash consideration paid in connection with the Merger was approximately $28,750,000,000, which was funded from equity contributions from the Sponsors, as well as proceeds received by Merger Subsidiary in connection with debt financing provided by JPMorgan Chase Bank, N.A., Wells Fargo Bank, National Association and a syndicate of other lenders pursuant to a new senior secured credit facility (the “Senior Credit Facilities”) and upon the issuance of the Notes (as defined and described herein).

As a result of the Merger and the transactions entered into in connection therewith, we have inherited the liabilities and obligations of Merger Subsidiary, including Merger Subsidiary's obligations under the Senior Credit Facilities. The Senior Credit Facilities consist of (i)(a) term B-1 loans in an aggregate principal amount of $2,950,000,000 (the “B-1 Loans”) and (b) term B-2 loans in aggregate principal amount of $6,550,000,000 (the “B-2 Loans”) in each case under the new senior secured term loan facilities (the “Term Loan Facilities”) and (ii) revolving loans of up to $2,000,000,000 (including revolving loans, swingline loans and letters of credit), a portion of which may be denominated in Euro, Sterling, Australian Dollars, Japanese Yen or New Zealand Dollars, under the new senior secured revolving loan facilities (the “Revolving Credit Facilities”). Concurrently with the consummation of the Merger, the full amount of the term loan was drawn, and no revolving loans were drawn.

Also on June 7, 2013, in connection with the Merger, we executed a Joinder Agreement (the “Purchase Agreement Joinder”) to the Purchase Agreement, dated March 22, 2013 (the “Purchase Agreement”), among Merger Subsidiary, Parent and the several initial purchasers named in the schedule thereto (the “Initial Purchasers”), relating to the issuance and sale by Merger Subsidiary to the Initial Purchasers of $3,100,000,000 in aggregate principal amount of Merger Subsidiary's 4.25% Second Lien Senior Secured Notes due 2020 (the “Notes”), pursuant to which the H. J. Heinz Company and certain of its subsidiaries became parties to the Purchase Agreement. On June 7, 2013, the Company entered into a supplemental indenture to the Indenture dated as of April 1, 2013 governing the Notes pursuant to which the Company assumed all of the obligations of Merger Subsidiary as issuer of the Notes.

We refer to the Merger and the related transactions, including the issuance and sale of the Notes, the entering into the Purchase Agreement Joinder and the borrowings under the Senior Credit Facilities, as the “Transactions.”

As a result of the Merger, our common stock is no longer publicly traded.

CAUTIONARY STATEMENT RELEVANT TO FORWARD-LOOKING INFORMATION

Statements about future growth, profitability, costs, expectations, plans, or objectives included in this report, including in management's discussion and analysis, and the financial statements and footnotes, are forward-looking statements based on management's estimates, assumptions, and projections. These forward-looking statements are subject to risks, uncertainties, assumptions and other important factors, many of which may be beyond the Company's control and could cause actual results to differ materially from those expressed or implied in this report and the financial statements and footnotes. Uncertainties contained in such statements include, but are not limited to:

the ability of the Company to retain and hire key personnel and maintain relationships with customers, suppliers and other business partners,

sales, volume, earnings, or cash flow growth,

general economic, political, and industry conditions, including those that could impact consumer spending,

competitive conditions, which affect, among other things, customer preferences and the pricing of products, production, and energy costs,

competition from lower-priced private label brands,

increases in the cost and restrictions on the availability of raw materials including agricultural commodities and packaging materials, the ability to increase product prices in response, and the impact on profitability,

the ability to identify and anticipate and respond through innovation to consumer trends,

the need for product recalls,

the ability to maintain favorable supplier and customer relationships, and the financial viability of those suppliers and customers,

currency valuations and devaluations and interest rate fluctuations,

changes in credit ratings, leverage, and economic conditions, and the impact of these factors on our cost of borrowing and access to capital markets,

our ability to effectuate our strategy, including our continued evaluation of potential opportunities, such as strategic acquisitions, joint ventures, divestitures and other initiatives, our ability to identify, finance and complete these transactions and other initiatives, and our ability to realize anticipated benefits from them,

the ability to successfully complete cost reduction programs and increase productivity,

the ability to effectively integrate acquired businesses,

new products, packaging innovations, and product mix,

the effectiveness of advertising, marketing, and promotional programs,

supply chain efficiency,

cash flow initiatives,

risks inherent in litigation, including tax litigation,

the ability to further penetrate and grow and the risk of doing business in international markets, particularly our emerging markets, economic or political instability in those markets, strikes, nationalization, and the performance of business in hyperinflationary environments, in each case, such as Venezuela; and the uncertain global macroeconomic environment and sovereign debt issues, particularly in Europe,

changes in estimates in critical accounting judgments and changes in laws and regulations, including tax laws,

the success of tax planning strategies,

the possibility of increased pension expense and contributions and other people-related costs,

the potential adverse impact of natural disasters, such as flooding and crop failures, and the potential impact of climate change,

the ability to implement new information systems, potential disruptions due to failures in information technology systems, and risks associated with social media, and

other factors described in "Risk Factors" below.

The forward-looking statements are and will be based on management's then current views and assumptions regarding future events and speak only as of their dates. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by the securities laws.

PART I

| Item 1. | Business. |

H. J. Heinz Company was incorporated in Pennsylvania on July 27, 1900. In 1905, it succeeded to the business of a partnership operating under the same name which had developed from a food business founded in 1869 in Sharpsburg, Pennsylvania by Henry J. Heinz. H. J. Heinz Company and its subsidiaries (collectively, the “Company”) manufacture and market an extensive line of food products throughout the world. The Company’s principal products include ketchup, condiments and sauces, frozen food, soups, beans and pasta meals, infant nutrition and other food products.

The Company’s products are manufactured and packaged to provide safe, wholesome foods for consumers, as well as foodservice and institutional customers. Many products are prepared from recipes developed in the Company’s innovation and research laboratories and experimental kitchens.centers. Ingredients are carefully selected, inspected and passed on to modern factory kitchens where they are processed, after which the intermediate product is filled automatically into containers of glass, metal, plastic, paper or fiberboard, which are then sealed. Products are prepared by sterilization, blending, fermentation, pasteurization, homogenization, chilling, freezing, pickling, drying, freeze drying, baking or extruding, then labeled and cased for market. Quality assurance procedures are designed for each product and process and applied for quality and compliance with applicable laws.

The Company manufactures (and contracts for the manufacture of) its products from a wide variety of raw food materials. Pre-season contracts are made with farmers for certain raw materials such as a portion of the Company’s requirements of tomatoes, cucumbers, potatoes, onions and some other fruits and vegetables. Ingredients, such as dairy products, meat, sugar and other sweeteners, including high fructose corn syrup, spices, flour and fruits and vegetables, are purchased from approved suppliers.

The following table lists the number of the Company’s principal food processing factories and major trademarks by region:

| Factories | ||||||||||

| Owned | Leased | Major Owned and Licensed Trademarks | ||||||||

| North America | 20 | 4 | Heinz, Classico, Quality Chef Foods, Jack Daniel’s*, Catelli*, Wyler’s, Heinz Bell ’Orto, Bella Rossa, Chef Francisco, Dianne’s, Ore-Ida, Tater Tots, Bagel Bites, Weight Watchers* Smart Ones, Poppers, T.G.I. Friday’s*, Delimex, Truesoups, Alden Merrell, Escalon, PPI, Todd’s, Nancy’s, Lea & Perrins, Renee’s Gourmet, HP, Diana, Bravo, Arthur’s Fresh | |||||||

| Europe | 21 | — | Heinz, Orlando, Karvan Cevitam, Brinta, Roosvicee, Venz, Weight Watchers*, Farley’s, Sonnen Bassermann, Plasmon, Nipiol, Dieterba, Bi-Aglut, Aproten, Pudliszki, Ross, Honig, De Ruijter, Aunt Bessie*, Mum’s Own, Moya Semya, Picador, Derevenskoye, Mechta Hoziajki, Lea & Perrins, HP, Amoy*, Daddies, Squeezme!, Wyko, Benedicta | |||||||

| Asia/Pacific | 25 | 2 | Heinz, Tom Piper, Wattie’s, ABC, Chef, Craig’s, Bruno, Winna, Hellaby, Hamper, Farley’s, Greenseas, Gourmet, Nurture, LongFong, Ore-Ida, SinSin, Lea & Perrins, HP, Classico, Weight Watchers*, Cottee’s, Rose’s*, Complan, Glucon D, Nycil, Golden Circle, La Bonne Cuisine, Original Juice Co., The Good Taste Company, Master, Guanghe | |||||||

| Rest of World | 7 | 2 | Heinz, Wellington’s, Today, Mama’s, John West, Farley’s, Complan, HP, Lea & Perrins, Classico, Banquete, Wattie’s, Quero | |||||||

| 73 | 8 | * Used under license | ||||||||

| Factories | |||||||

| Owned | Leased | Major Owned and Licensed Trademarks | |||||

| North America | 15 | 4 | Heinz, Classico, Quality Chef Foods, Jack Daniel’s*, Catelli*, Wyler’s, Heinz Bell ’Orto, Bella Rossa, Chef Francisco, Ore-Ida, Tater Tots, Bagel Bites, Weight Watchers* Smart Ones, Poppers, T.G.I. Friday’s*, Delimex, Truesoups, Escalon, PPI, Todd’s, Nancy’s, Lea & Perrins, Renee’s Gourmet, HP, Diana, Bravo, Arthur’s Fresh | ||||

| Europe | 17 | — | Heinz, Orlando, Karvan Cevitam, Brinta, Roosvicee, Venz, Weight Watchers*, Farley’s, Plasmon, Nipiol, Dieterba, Bi-Aglut, Aproten, Pudliszki, Ross, Honig, De Ruijter, Aunt Bessie*, Mum’s Own, Moya Semya, Picador, Derevenskoye, Lea & Perrins, HP, Amoy*, Daddies, Squeezme!, Wyko, Benedicta | ||||

| Asia/Pacific | 24 | — | Heinz, Tom Piper, Wattie’s, ABC, Chef, Craig’s, Winna, Hellaby, Hamper, Farley’s, Greenseas, Gourmet, Nurture, Ore-Ida, SinSin, Lea & Perrins, HP, Classico, Weight Watchers*, Cottee’s, Rose’s*, Complan, Glucon D, Nycil, Golden Circle, La Bonne Cuisine, Original Juice Co., The Good Taste Company, Master, Guanghe | ||||

| Rest of World | 7 | 2 | Heinz, Wellington’s, Today, Mama’s, John West, Farley’s, Complan, HP, Lea & Perrins, Classico, Banquete, Wattie’s, Quero | ||||

| 63 | 6 | * Used under license | |||||

The Company also owns or leases office space, warehouses, distribution centers and research and other facilities throughout the world. The Company’s food processing factories and principal properties are in good condition and are satisfactory for the purposes for which they are being utilized.

The Company has developed or participated in the development of certain of its equipment, manufacturing processes and packaging, and maintains patents and has applied for patents for some of those developments. The Company regards these patents and patent applications as important but does not consider any one or group of them to be materially important to its business as a whole.

Although crops constituting some of the Company’s raw food ingredients are harvested on a seasonal basis, most of the Company’s products are produced throughout the year. Seasonal factors inherent in the business have always influenced the quarterly sales, operating income and cash flows of the Company. Consequently, comparisons between quarters have always been more meaningful when made between the same quarters of prior years.

The products of the Company are sold under highly competitive conditions, with many large and small competitors. The Company regards its principal competition to be other manufacturers of prepared foods, including branded retail products, foodservice products and private label products, that compete with the Company for consumer preference, distribution, shelf space and merchandising support. Product quality and consumer value are important areas of competition.

2

The Company’s products are sold through its own sales organizations and through independent brokers, agents and distributors to chain, wholesale, cooperative and independent grocery accounts, convenience stores, bakeries, pharmacies, mass merchants, club stores, foodservice distributors and institutions, including hotels, restaurants, hospitals, health-care facilities, and certain government agencies. For Fiscal 2011,2013 and 2012, one customer, Wal-Mart Stores Inc., represented approximately 11%10% of the Company’s sales. We closely monitor the credit risk associated with our customers and to date have not experienced material losses.

Compliance with the provisions of national, state and local environmental laws and regulations has not had a material effect upon the capital expenditures, earnings or competitive position of the Company. The Company’s estimated capital expenditures for environmental control facilities for the remainder of Fiscal 20122014 and the succeeding fiscal year are not material and are not expected to materially affect the earnings, cash flows or competitive position of the Company.

The Company’s factories are subject to inspections by various governmental agencies in the U.S. and other countries where the Company does business, including the United States Department of Agriculture, and the Occupational Health and Safety Administration, and its products must comply with the applicable laws, including food and drug laws, such as the Federal Food and Cosmetic Act of 1938, as amended, and the Federal Fair Packaging or Labeling Act of 1966, as amended, of the jurisdictions in which they are manufactured and marketed.

The Company employed, on a full-time basis as of April 27, 2011,28, 2013, approximately 34,80031,900 people around the world.

Segment information is set forth in this report on pages 8378 through 8580 in Note 15,16, “Segment Information” in Item 8—“Financial Statements and Supplementary Data.”

Income from international operations is subject to fluctuation in currency values, export and import restrictions, foreign ownership restrictions, economic controls and other factors. From time to time, exchange restrictions imposed by various countries have restricted the transfer of funds between countries and between the Company and its subsidiaries. To date, such exchange restrictions have not had a material adverse effect on the Company’s operations.

The Company’s annual report onForm 10-K, quarterly reports onForm 10-Q, current reports onForm 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge on the Company’s websiteweb site atwww.heinz.com, as soon as

3

reasonably practicable after being filed or furnished to the Securities and Exchange Commission (“SEC”). Our reports filed with the SEC are also made available on its website atwww.sec.gov. www.sec.gov.

Recent Developments

Completion of Acquisition by Berkshire Hathaway and 3G Capital

The total cash consideration paid in connection with the Merger was approximately $28.75 billion, which was funded from equity contributions from the Sponsors, as well as proceeds received by Merger Subsidiary from the Senior Credit Facilities and upon the issuance of the Notes (as defined and described herein). The Senior Credit Facilities consist of:

$9.5 billion in senior secured term loans, with tranches of 6 and 7 year maturities and fluctuating interest rates based on, at the Company's election, base rate or LIBOR plus a spread on each of the tranches, with respective spreads ranging from 125-150 basis points for base rate loans with a 2% base rate floor and 225-250 basis points for LIBOR loans with a 1% LIBOR floor, and

$2.0 billion senior secured revolving credit facility with a 5 year maturity and a fluctuating interest rate based on, at the Company's election, base rate or LIBOR, with respective spreads ranging from 50-100 basis points for base rate loans and 150-200 basis points for LIBOR loans, on which nothing is currently drawn.

On June 7, 2013, this indebtedness was assumed by the Company, substantially increasing the Company's overall level of debt.

On April 1, 2013, in connection with the Merger, Merger Subsidiary completed the private placement of $3.1 billion aggregate principal amount of 4.25% Second Lien Senior Secured Notes due 2020 (the “Notes”) to initial purchasers for resale by the Initial Purchasers to qualified institutional buyers pursuant to Rule 144A under the Securities Act and to persons outside the United States

3

under Regulation S of the Securities Act. The Notes were issued pursuant to an indenture (the “Indenture”), dated as of April 1, 2013, by and among Merger Subsidiary, Hawk Acquisition Intermediate Corporation II and Wells Fargo Bank, National Association, as trustee (in such capacity, the “Trustee”) and as collateral agent (in such capacity, the “Collateral Agent”). On June 7, 2013, the Company, certain of its direct and indirect wholly owned domestic subsidiaries (the “Guarantors”), the Trustee and the Collateral Agent entered into a supplemental indenture (the “Supplemental Indenture”) to the Indenture pursuant to which the Company assumed all of the obligations of Merger Subsidiary as issuer of the Notes. The Notes mature in 2020 and are required, within one year of consummation of the Merger Agreement, to be exchanged for notes registered with the SEC.

In addition, in connection with the Merger, Parent issued to Berkshire Hathaway 80,000 shares of its 9% Cumulative Perpetual Series A Preferred Stock for $8 billion.

In the Merger, (i) each outstanding share of Company common stock (other than shares owned by the Company, Parent, Merger Sub or any other direct or indirect wholly owned subsidiary of Parent, and in each case not held on behalf of third parties) was cancelled and automatically converted into the right to receive $72.50 in cash, without interest and less applicable withholding taxes thereon (the “Merger Consideration”), (ii) each outstanding stock option, whether vested or unvested, was cancelled and automatically converted into the right to receive, with respect to each share subject to the option, the Merger Consideration less the exercise price per share, (iii) each outstanding Company phantom unit, whether vested or unvested, was cancelled and automatically converted into the right to receive the Merger Consideration, and (iv) each outstanding Company restricted stock unit (other than retention restricted stock units, which will remain subject to the vesting schedule pursuant to the existing terms of the applicable award agreements and that the general timing of payment would be in accordance with such terms), whether vested or unvested, was cancelled and automatically converted into the right to receive, with respect to each share subject to the restricted stock unit, the Merger Consideration plus any accrued and unpaid dividend equivalents, except that payment in respect of Company restricted stock units that have been deferred will be made in accordance with the terms of the award and the applicable deferral election made by the holder.

At the effective time of the Merger, each holder of a certificate formerly representing any shares of Company common stock or of book-entry shares no longer had any rights with respect to the shares, except for the right to receive the Merger Consideration upon surrender thereof.

The acquisition will be accounted for as a purchase business combination. The application of purchase accounting as of the closing date is expected to have a material effect on the Company's results of operations for periods after the acquisition. The Company has begun the process to determine the purchase accounting allocation to the Company's assets and liabilities including estimating fair values of the Company's intangible and tangible assets. While these estimates have not been completed, management expects that a substantial portion of the purchase price will be allocated to indefinite-lived intangible assets (principally brands) and goodwill.

Financing implications of the acquisition on our existing debt

A substantial portion of the Company's indebtedness was subject to acceleration upon a change of control or required the Company to offer holders the option to repurchase such indebtedness from such holders (assuming such change of control triggered certain downgrades in the ratings of the Company's debt). Certain of the Company's outstanding indebtedness at April 28, 2013 that was not subject to acceleration upon a change of control and that either did not contain change of control repurchase obligations or where the holders did not elect to have such indebtedness repurchased in a change of control offer remain outstanding.

On March 13, 2013, the Company launched a consent solicitation relating to the 7.125% Notes due 2039 seeking a waiver of the change of control provisions as applicable to the Merger Agreement. As of March 21, 2013, the Company received the required consents to waive such provisions and as a result those notes remain outstanding.

Changes in the Directors and Officers of the RegistrantCompany

Also in accordance with the Merger and related transactions, in accordance with the terms of the Merger Agreement, as of the effective time of the Merger, each of William R. Johnson, Charles E. Bunch, Leonard S. Coleman Jr., John G. Drosdick, Edith E. Holiday, Candace Kendle, Franck J. Moison, Dean R. O'Hare, Nelson Peltz, Dennis H. Reilley, Lynn C. Swann, Thomas J. HeinzUsher and Michael F. Weinstein (the “Former Directors”) ceased serving as members of the board of directors of the Company indicating all

4

and, in connection therewith, the Former Directors also ceased serving on any committees of which such Former Directors were members. Information on the positions and offices held by each such personthe Former Directors on any committee of the board of directors of the Company at the time of the Former Directors' resignation is set forth under the caption “Board of Directors and each such person’s principal occupations or employment duringCommittees of the past five years. AllBoard” in the executive officers have beenCompany's definitive Proxy Statement filed with the Securities and Exchange Commission on June 15, 2012 and is incorporated herein by reference.

Warren Buffett, Alexandre Behring, Gregory Abel, Jorge Paulo Lemann, Marcel Herrmann Telles and Tracy Britt were elected to serve untilas new members of the next annual electionboard of officers, until their successors are elected, or until their earlier resignation or removal. The next annual electiondirectors of officers is scheduled to occurthe Company on August 30, 2011.June 7, 2013.

4

| Item 1A. | Risk |

In addition to the factors discussed elsewhere in this report, the following risks and uncertainties could materially and adversely affect the Company’s business, financial condition, and results of operations. Additional risks and uncertainties that are not presently known to the Company or are currently deemed by the Company to be immaterial also may impair the Company’s business operations and financial condition.

Risks Related to Our Business

Competitive product and pricing pressures in the food industry and the financial condition of customers and suppliers could adversely affect the Company’s ability to gain or maintain market share and/or profitability.

The Company operates in the highly competitive food industry, competing with other companies that have varying abilities to withstand changing market conditions. Any significant change in the Company’s relationship with a major customer, including changes in product prices, sales volume, or contractual terms may impact financial results. Such changes may result because the Company’s competitors may have substantial financial, marketing, and other resources that may change the competitive environment. Private label brands sold by retail customers, which are typically sold at lower prices, are a source of competition for certain of our product lines. Such competition could cause the Company to reduce pricesand/or increase capital, marketing, and other expenditures, or could

5

result in the loss of category share. Such changes could have a material adverse impact on the Company’s net income. As the retail grocery trade continues to consolidate, the larger retail customers of the Company could seek to use their positions to improve their profitability through lower pricing and increased promotional programs. If the Company is unable to use its scale, marketing expertise, product innovation, and category leadership positions to respond to these changes, or is unable to increase its prices, its profitability and volume growth could be impacted in a materially adverse way. The success of our business depends, in part, upon the financial strength and viability of our suppliers and customers. The financial condition of those suppliers and customers is affected in large part by conditions and events that are beyond our control. A significant deterioration of their financial condition could adversely affect our financial results.

The Company’s performance may be adversely affected by economic and political conditions in the U.S. and in various other nations where it does business.

The Company’s performance has been in the past and may continue in the future to be impacted by economic and political conditions in the United States and in other nations. Such conditions and factors include changes in applicable laws and regulations, including changes in food and drug laws, accounting standards and critical accounting estimates, taxation requirements and environmental laws. Other factors impacting our operations in the U.S., Venezuela and other international locations where the Company does business include export and import restrictions, currency exchange rates, currency devaluation, recessionary conditions, foreign ownership restrictions, nationalization, the impact of hyperinflationary environments, and terrorist acts, and political unrest. Such factors in either domestic or foreign jurisdictions could materially and adversely affect our financial results.

Increases in the cost and restrictions on the availability of raw materials could adversely affect our financial results.

The Company sources raw materials including agricultural commodities such as tomatoes, cucumbers, potatoes, onions, other fruits and vegetables, dairy products, meat, sugar and other sweeteners, including high fructose corn syrup, spices, and flour, as well as packaging materials such as glass, plastic, metal, paper, fiberboard, and other materials and inputs such as water, in order to manufacture products. The availability or cost of such commodities may fluctuate widely due to government policy and regulation, crop failures or shortages due to plant disease or insect and other pest infestation, weather conditions, potential impact of climate change, increased demand for biofuels, or other unforeseen circumstances. Additionally, the cost of raw materials and finished products may fluctuate due to movements in cross-currency transaction rates. To the extent that any of the foregoing or other unknown factors increase the prices of such commodities or materials and the Company is unable to increase its prices or adequately hedge against such changes in a manner that offsets such changes, the results of its operations could be materially and adversely affected. Similarly, if supplier arrangements and relationships result in increased and unforeseen expenses, the Company’s financial results could be materially and adversely impacted.

6

5

Disruption of our supply chain could adversely affect our business.

Damage or disruption to our manufacturing or distribution capabilities due to weather, natural disaster, fire, terrorism, pandemic, strikes, the financialand/or operational instability of key suppliers, distributors, warehousing and transportation providers, or brokers, or other reasons could impair our ability to manufacture or sell our products. To the extent the Company is unable to, or cannot, financially mitigate the likelihood or potential impact of such events, or to effectively manage such events if they occur, particularly when a product is sourced from a single location, there could be a materially adverse affect on our business and results of operations, and additional resources could be required to restore our supply chain.

Higher energy costs and other factors affecting the cost of producing, transporting, and distributing the Company’s products could adversely affect our financial results.

Rising fuel and energy costs may have a significant impact on the cost of operations, including the manufacture, transportation, and distribution of products. Fuel costs may fluctuate due to a number of factors outside the control of the Company, including government policy and regulation and weather conditions. Additionally, the Company may be unable to maintain favorable arrangements with respect to the costs of procuring raw materials, packaging, services, and transporting products, which could result in increased expenses and negatively affect operations. If the Company is unable to hedge against such increases or raise the prices of its products to offset the changes, its results of operations could be materially and adversely affected.

The results of the Company could be adversely impacted as a result of increased pension, labor, and people-related expenses.

Inflationary pressures and any shortages in the labor market could increase labor costs, which could have a material adverse effect on the Company’s consolidated operating results or financial condition. The Company’s labor costs include the cost of providing employee benefits in the U.S. and foreign jurisdictions, including pension, health and welfare, and severance benefits. Any declines in market returns could adversely impact the funding of pension plans, the assets of which are invested in a diversified portfolio of equity and fixed income securities and other investments. Additionally, the annual costs of benefits vary with increased costs of health care and the outcome of collectively-bargained wage and benefit agreements.

The impact of various food safety issues, environmental, legal, tax, and other regulations and related developments could adversely affect the Company’s sales and profitability.

The Company is subject to numerous food safety and other laws and regulations regarding the manufacturing, marketing, and distribution of food products. These regulations govern matters such as ingredients, advertising, taxation, relations with distributors and retailers, health and safety matters, and environmental concerns. The ineffectiveness of the Company’s planning and policies with respect to these matters, and the need to comply with new or revised laws or regulations with regard to licensing requirements, trade and pricing practices, environmental permitting, or other food or safety matters, or new interpretations or enforcement of existing laws and regulations, as well as any related litigation, may have a material adverse effect on the Company’s sales and profitability. Influenza or other pandemics could disrupt production of the Company’s products, reduce demand for certain of the Company’s products, or disrupt the marketplace in the foodservice or retail environment with consequent material adverse effects on the Company’s results of operations.

7

The need for and effect of product recalls could have an adverse impact on the Company’s business.

If any of the Company’s products become misbranded or adulterated, the Company may need to conduct a product recall. The scope of such a recall could result in significant costs incurred as a result of the recall, potential destruction of inventory, and lost sales. Should consumption of any product cause injury, the Company may be liable for monetary damages as a result of a judgment against it. A significant product recall or product liability case could cause a loss of consumer confidence in the Company’s food products and could have a material adverse effect on the value of its brands and results of operations.

The failure of new product or packaging introductions to gain trade and consumer acceptance and changes in consumer preferences could adversely affect our sales.

The success of the Company is dependent upon anticipating and reacting to changes in consumer preferences, including health and wellness. There are inherent marketplace risks associated with new product or packaging introductions, including uncertainties about trade and consumer acceptance. Moreover, success is dependent upon the Company’s ability to identify and respond to consumer trends through innovation. The Company may be required to increase expenditures for new product development. The Company may not be successful in developing new products or improving existing products, or its new products may not achieve consumer acceptance, each of which could materially and negatively impact sales.

6

The failure to successfully integrate acquisitions and joint ventures into our existing operations or the failure to gain applicable regulatory approval for such transactions or divestitures could adversely affect our financial results.

The Company’s ability to efficiently integrate acquisitions and joint ventures into its existing operations also affects the financial success of such transactions. The Company may seek to expand its business through acquisitions and joint ventures, and may divest underperforming or non-core businesses. The Company’s success depends, in part, upon its ability to identify such acquisition, joint venture, and divestiture opportunities and to negotiate favorable contractual terms. Activities in such areas are regulated by numerous antitrust and competition laws in the U. S., the European Union, and other jurisdictions, and the Company may be required to obtain the approval of acquisition and joint venture transactions by competition authorities, as well as satisfy other legal requirements. The failure to obtain such approvals could materially and adversely affect our results.

The Company’s operations face significant foreign currency exchange rate exposure, which could negatively impact its operating results.

The Company holds assets and incurs liabilities, earns revenue, and pays expenses in a variety of currencies other than the U.S. dollar, primarily the British Pound, Euro, Australian dollar, Canadian dollar, and New Zealand dollar. The Company’s consolidated financial statements are presented in U.S. dollars, and therefore the Company must translate its assets, liabilities, revenue, and expenses into U.S. dollars for external reporting purposes. Increases or decreases in the value of the U.S. dollar relative to other currencies may materially and negatively affect the value of these items in the Company’s consolidated financial statements, even if their value has not changed in their original currency. In addition, the impact of fluctuations in foreign currency exchange rates on transaction costs ( i.e., the impact of foreign currency movements on particular transactions such as raw material sourcing), most notably in the U.K., could materially and adversely affect our results.

8

The failure to implement our growth plans could adversely affect the Company’s ability to increase net income and generate cash.

The success of the Company could be impacted by its inability to continue to execute on its growth plans regarding product innovation, implementing cost-cutting measures, improving supply chain efficiency, enhancing processes and systems, including information technology systems, on a global basis, and growing market share and volume. The failure to fully implement the plans, in a timely manner or within our cost estimates, could materially and adversely affect the Company’s ability to increase net income. Additionally, the Company’s ability to pay cash dividends will depend upon its ability to generate cash and profits, which, to a certain extent, is subject to economic, financial, competitive, and other factors beyond the Company’s control.

The Sponsors control us and may have conflicts of interest with us in the future.

Our business could be adversely impacted as a result of the Merger and significant costs, expenses and fees.

The Merger could cause disruptions to our business or business relationships, which could have an adverse impact on our financial condition, results of operations and cash flows. For example:

• the attention of our management may be directed to transaction-related considerations or activities and may be diverted from the day-today operations of our business;

• our associates may experience uncertainty about their future roles with us, which might adversely affect our ability to retain and hire key personnel and other employees; and

• vendors or other parties with which we maintain business relationships may experience uncertainty about our future and seek alternative relationships with third parties or seek to alter their business relationships with us.

7

In addition, we incurred significant costs, expenses and fees for professional services and other transaction costs in connection with the Merger.

The Company is increasingly dependent on information technology, and potential disruption, cyber attacks, security problems, and expanding social media vehicles present new risks.

The inappropriate use of certain media vehicles could cause brand damage or information leakage. Negative posts or comments about usthe Company on any social networking web site could seriously damage ourits reputation. In addition, the disclosure of non-public company sensitive information through external media channels could lead to information loss. Identifying new points of entry as social media continues to expand presents new challenges. Any business interruptions or damage to the Company’sCompany's reputation could negatively impact the Company’sCompany's financial condition and results of operation,operation.

The Company's operating results may be adversely affected by the current sovereign debt crisis in Europe and elsewhere and by related global economic conditions.

The current European debt crisis, particularly most recently in Greece, Italy, Ireland, Portugal and Spain, and related European financial restructuring efforts may cause the value of the European currencies, including the Euro, to further deteriorate, thus reducing the purchasing power of European customers. One potential extreme outcome of the European financial situation is the re-introduction of individual currencies in one or more Eurozone countries or the dissolution of the Euro entirely. Should the Euro dissolve entirely, the legal and contractual consequences for holders of Euro-denominated obligations would be determined by laws in effect at such time. The potential dissolution of the Euro, or market perceptions concerning this and related issues, could adversely affect the value of the Company's Euro-denominated assets and obligations. In addition, the European crisis is contributing to instability in global credit markets. The world has recently experienced a global macroeconomic downturn, and if global economic and market conditions, or economic conditions in Europe, the United States or other key markets, remain uncertain, persist, or deteriorate further, consumer purchasing power and demand for Company products could decline, and the market priceCompany may experience material adverse impacts on its business, operating results, and financial condition.

Risks Related to Our Indebtedness and Certain Other Obligations

Our indebtedness could adversely affect our ability to raise additional capital to fund our operations and make strategic acquisitions, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under our indebtedness, including the Company’s common stock.Notes.

Our high degree of indebtedness could have important consequences for our creditors, including holders of the Notes. For example, they could:

•limit our ability to obtain additional financing for working capital, capital expenditures, research and development, debt service requirements, acquisitions and general corporate or other purposes;

•restrict us from making strategic acquisitions or cause actual resultsus to differ materiallymake non-strategic divestitures;

•limit our ability to adjust to changing market conditions and place us at a competitive disadvantage compared to our competitors who are not as highly leveraged;

•increase our vulnerability to general economic and industry conditions;

8

•expose us to the risk of increased interest rates as the borrowings under our Senior Credit Facilities will be at variable rates of interest;

•make it more difficult for us to make payments on our indebtedness; and

•require a substantial portion of cash flow from those expressed or impliedoperations to be dedicated to the payment of principal and interest on our indebtedness, thereby reducing our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities.

For the fiscal year ended April 28, 2013, on a pro forma basis after giving effect to the Merger and related financing transactions as if they had closed at the beginning of fiscal 2013, our cash interest expense would have been approximately $603 million. As of April 28, 2013, on a pro forma basis after giving effect to the Transactions as if they had closed on such date, we would have had approximately $14.5 billion of debt outstanding.

Despite current indebtedness levels and restrictive covenants, we and our subsidiaries may incur additional indebtedness in this reportthe future. This could further exacerbate the risks associated with our substantial financial leverage.

The terms of the indenture governing our Notes and the financial statementscredit agreements governing our Senior Credit Facilities permit us to incur a substantial amount of additional debt, including secured debt. Any additional borrowings under our Senior Credit Facilities, and footnotes. Uncertainties contained incertain other secured debt, would be senior to the Notes and the guarantees thereto to the extent of the value of the assets securing such statements include, but are not limited to:

9

10

Our debt agreements contain restrictions that limit our flexibility in operating our business.

The credit agreement governing our Senior Credit Facilities and the indenture governing our Notes contain various covenants that limit our ability to engage in specified types of transactions. These covenants limit our, our immediate parent's and our restricted subsidiaries' ability to, among other things, incur or guarantee additional indebtedness, pay dividends on, or redeem or repurchase, our capital stock, make certain acquisitions or investments, materially change our business, incur or permit to exist certain liens, enter into transactions with affiliates or sell our assets to, or merge or consolidate with or into, another company, in each case with customary exceptions.

Upon the occurrence of an event of default under our Senior Credit Facilities, the lenders thereunder could elect to declare all amounts outstanding under our Senior Credit Facilities to be immediately due and payable and terminate all commitments to extend further credit. If we were unable to repay those amounts, the lenders under our Senior Credit Facilities could proceed against the collateral granted to them to secure that indebtedness. We have pledged a significant portion of our assets as collateral under our Senior Credit Facilities. If the lenders under our Senior Credit Facilities accelerate the repayment of borrowings, we cannot assure you that we will have sufficient assets to repay our Senior Credit Facilities, as well as our other secured and unsecured indebtedness, including our outstanding Notes.

To service our indebtedness, we will require a significant amount of cash and our ability to generate cash depends on many factors beyond our control.

Our ability to make cash payments on and to refinance our indebtedness and to fund planned capital expenditures will depend on our ability to generate significant operating cash flow in the future. This ability is, to a significant extent, subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

Our business may not generate sufficient cash flow from operations, and future eventsborrowings may not be available under our Senior Credit Facilities, in an amount sufficient to enable us to pay our indebtedness, including the outstanding Notes, or to fund our other liquidity needs. In any such circumstance, we may need to refinance all or a portion of our indebtedness, including our Senior Credit Facilities and the Notes, on or before maturity. We may not be able to refinance any of our indebtedness, including our Senior Credit Facilities and the Notes, on commercially reasonable terms or at all. If we cannot service our indebtedness, we may have to take actions such as selling assets, seeking additional equity or reducing or delaying capital expenditures, strategic acquisitions and investments. Any such action, if necessary, may not be effected on commercially reasonable terms or at all. The credit agreements governing our Senior Credit Facilities and the indenture governing the Notes restrict our ability to sell assets and use the proceeds from such sales.

9

If we are unable to generate sufficient cash flow or are otherwise exceptunable to obtain funds necessary to meet required payments of principal, premium, if any, and interest on our indebtedness, or if we otherwise fail to comply with the various covenants in the instruments governing our indebtedness (including covenants in the credit agreement governing our Senior Credit Facilities and the indenture governing the Notes), we could be in default under the terms of the agreements governing such indebtedness. In the event of such default, the holders of such indebtedness could elect to declare all the funds borrowed thereunder to be due and payable, together with accrued and unpaid interest, the lenders under our Senior Credit Facilities could elect to terminate their commitments thereunder, cease making further loans and institute foreclosure proceedings against our assets, and we could be forced into bankruptcy or liquidation. If our operating performance declines, we may in the future need to obtain waivers from the required lenders under our Senior Credit Facilities to avoid being in default. If we breach our covenants under the credit agreements governing our Senior Credit Facilities and seek a waiver, we may not be able to obtain a waiver from the required lenders. If this occurs, we would be in default under our Senior Credit Facilities, the lenders could exercise their rights, as required by the securities laws.described above, and we could be forced into bankruptcy or liquidation.

| Item 1B. | Unresolved Staff Comments. |

Nothing to report under this item.

| Item 2. | Properties. |

See table in Item 1.

| Item 3. | Legal Proceedings. |

Nothing to report under this item.

| Item 4. |

Nothing to report under this item.

10

PART II

| Item 5. | Market for |

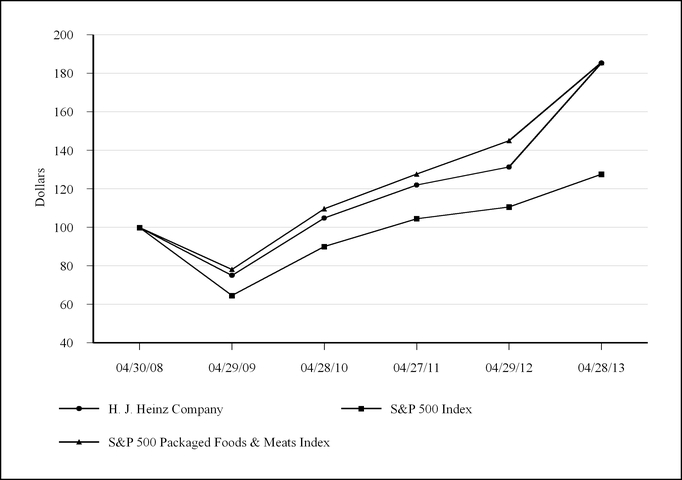

Information relating to the Company’s common stock is set forth in this report on page 3632 under the caption “Stock Market Information” in Item 7—“Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and on page 86pages 80 and 81 in Note 16,17, “Quarterly Results” in Item 8—“Financial Statements and Supplementary Data.”

| Maximum | ||||||||||||||||

| Total | Total Number of | Number of Shares | ||||||||||||||

| Number of | Average | Shares Purchased as | that May Yet Be | |||||||||||||

| Shares | Price Paid | Part of Publicly | Purchased Under | |||||||||||||

| Period | Purchased | per Share | Announced Programs | the Programs | ||||||||||||

| January 27, 2011— | ||||||||||||||||

| February 23, 2011 | — | $ | — | — | — | |||||||||||

| February 24, 2011— | ||||||||||||||||

| March 23, 2011 | — | — | — | — | ||||||||||||

| March 24, 2011— | ||||||||||||||||

| April 27, 2011 | 1,425,000 | 49.12 | — | — | ||||||||||||

| Total | 1,425,000 | $ | 49.12 | — | — | |||||||||||

| Item 6. | Selected Financial Data. |

The following table presents selected consolidated financial data for the Company and its subsidiaries for each of the five fiscal years 20072009 through 2011.2013. All amounts are in thousands except per share data.

| Fiscal Year Ended | ||||||||||||||||||||

| April 27, | April 28, | April 29, | April 30, | May 2, | ||||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

| (52 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | ||||||||||||||||

| Sales(1) | $ | 10,706,588 | $ | 10,494,983 | $ | 10,011,331 | $ | 9,885,556 | $ | 8,800,071 | ||||||||||

| Interest expense(1) | 275,398 | 295,711 | 339,635 | 364,808 | 333,037 | |||||||||||||||

| Income from continuing operations(1) | 1,005,948 | 931,940 | 944,400 | 858,176 | 794,398 | |||||||||||||||

| Income from continuing operations per share attributable to H.J. Heinz Company common shareholders—diluted(1) | 3.06 | 2.87 | 2.91 | 2.62 | 2.34 | |||||||||||||||

| Income from continuing operations per share attributable to H.J. Heinz Company common shareholders—basic(1) | 3.09 | 2.89 | 2.95 | 2.65 | 2.37 | |||||||||||||||

| Short-term debt and current portion of long- term debt | 1,534,932 | 59,020 | 65,638 | 452,708 | 468,243 | |||||||||||||||

| Long-term debt, exclusive of current portion(2) | 3,078,128 | 4,559,152 | 5,076,186 | 4,730,946 | 4,413,641 | |||||||||||||||

| Total assets | 12,230,645 | 10,075,711 | 9,664,184 | 10,565,043 | 10,033,026 | |||||||||||||||

| Cash dividends per common share | 1.80 | 1.68 | 1.66 | 1.52 | 1.40 | |||||||||||||||

| Fiscal Year Ended | |||||||||||||||||||

| April 28, 2013 | April 29, 2012 | April 27, 2011 | April 28, 2010 | April 29, 2009 | |||||||||||||||

| (52 Weeks) | (52 1/2 Weeks) | (52 Weeks) | (52 Weeks) | (52 Weeks) | |||||||||||||||

Sales(1) | $ | 11,528,886 | $ | 11,507,572 | $ | 10,558,636 | $ | 10,323,968 | $ | 9,826,298 | |||||||||

Interest expense(1) | 283,607 | 293,009 | 272,660 | 293,574 | 336,509 | ||||||||||||||

Income from continuing operations attributable to H.J. Heinz Company common shareholders(1) | 1,087,615 | 974,374 | 1,029,067 | 945,389 | 954,297 | ||||||||||||||

Income from continuing operations per share attributable to H.J. Heinz Company common shareholders—diluted(1) | 3.37 | 3.01 | 3.18 | 2.96 | 2.99 | ||||||||||||||

Income from continuing operations per share attributable to H.J. Heinz Company common shareholders—basic(1) | 3.39 | 3.03 | 3.21 | 2.99 | 3.03 | ||||||||||||||

| Short-term debt and current portion of long-term debt | 2,160,393 | 246,708 | 1,534,932 | 59,020 | 65,638 | ||||||||||||||

Long-term debt, exclusive of current portion(2) | 3,848,339 | 4,779,981 | 3,078,128 | 4,559,152 | 5,076,186 | ||||||||||||||

| Total assets | 12,939,007 | 11,983,293 | 12,230,645 | 10,075,711 | 9,664,184 | ||||||||||||||

| Cash dividends per common share | 2.06 | 1.92 | 1.80 | 1.68 | 1.66 | ||||||||||||||

| (1) | Amounts exclude the operating results as well as any associated impairment charges and losses on sale related to the Company’s Shanghai LongFong Foods business in China and U.S. Foodservice frozen desserts business, which were divested in Fiscal 2013, as well as the private label frozen desserts business in the U.K. |

| (2) | Long-term debt, exclusive of current portion, includes |

Fiscal 2013 results include the following special items:

•As a result of the Merger, the Company incurred $44.8 million pre-tax ($27.8 million after-tax) of transaction-related costs, including legal, accounting and other professional fees, during the fourth quarter of Fiscal 2013. See Note 21, “Subsequent Events” in Item 8- “Financial Statements and Supplementary Data” for further explanation. The Company expects to incur additional costs related to the Merger including costs associated with changing our debt and equity structure, additional professional fees, gains and losses on derivative instruments, acceleration of stock based compensation expense, and potential tax costs associated with changes in plans with respect to earnings invested outside of the United States.

11

•Also during the fourth quarter of Fiscal 2013, the Company closed a factory in South Africa resulting in a $3.5 million pre-tax charge ($2.6 million million after-tax) primarily related to asset write-downs.

•On February 8, 2013, the Venezuelan government announced the devaluation of its currency relative to the U.S. dollar, changing the official exchange rate from 4.30 to 6.30, resulting in a $42.7 million pre-tax ($39.1 million after-tax) currency translation loss during the fourth quarter of Fiscal 2013. See Note 20, "Venezuela- Foreign Currency" in Item 8—"Financial Statement and Supplementary Data" for further explanation.

•During the third quarter of Fiscal 2013, the Company renegotiated the terms of the Foodstar Holdings Pte earn-out that was due in Fiscal 2014 resulting in a $12.1 million pre-tax and after-tax charge. See Note 11, "Fair Value Measurements" in Item 8—"Financial Statement and Supplementary Data" for further explanation.

Fiscal 2012 results from continuing operations include expenses of $205.4 million pre-tax ($144.0 million after-tax or $0.45 per share) for productivity initiatives. See Note 4, "Fiscal 2012 Productivity Initiatives" in Item 8—"Financial Statement and Supplementary Data" for further explanation of these initiatives.

Fiscal 2010 results from continuing operations include expenses of $37.7$35.9 million pretax ($27.826.0 million after tax) for upfront productivity charges and a gain of $15.0 million pretax ($11.1 million after tax) on a property disposal in the Netherlands. The upfront productivity charges include costs associated with targeted workforce reductions and asset write-offs, that were part of a corporation-wide initiative to improve productivity. The asset write-offs related to two factory closures and the exit of a formula business in the U.K. See “Discontinued Operations and Other Disposals” in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 15 through 16 for further explanation of the property disposal in the Netherlands.

13

12

| Item 7. |

Executive Overview- Fiscal 20112013

The H.J. Heinz Company has been a pioneer in the food industry for over 140 years and possesses one of the world’s best and most recognizable brands—Heinz®. The Company has a global portfolio of leading brands focused in three core categories, Ketchup and Sauces, Meals and Snacks, and Infant/Nutrition.

The Company's Fiscal 2013 results reflect strong organic sales growth(1) of 3.1% comprised of a 1.0% volume improvement and a 2.1% increase in net pricing. Overall reported recordsales improved slightly by 0.2% as product line divestitures reduced sales 0.3% and foreign currency decreased sales 2.5%. Organic sales growth was led by our trio of growth engines comprised of emerging markets, the Company's top 15 brands and global ketchup. The emerging markets posted organic sales growthof 16.8% for the fiscal year (14.3% reported) and represented 23.6% of total Company sales. The Company's top 15 brands generated organic sales growth of 3.6% (0.8% reported) driven by the Heinz®, ABC®, Quero®, and Master® brands. Global ketchup grew organically 4.6% (2.8% reported) mainly driven by improvements in Russia, Brazil and the U.S.

Fiscal 2013 results include the following special, non-recurring items:

•As a result of the Merger, the Company incurred $45 million pre-tax ($28 million after-tax) of transaction-related costs, including legal, accounting and other professional fees, during the fourth quarter of Fiscal 2013. These costs were recorded in selling, general and administrative expenses ("SG&A") on the consolidated income statement and in the Non-Operating segment. The Company expects to incur additional costs related to the Merger including costs associated with changing our debt and equity structure, additional professional fees, gains and losses on derivative instruments, acceleration of stock based compensation expense, and potential tax costs associated with changes in plans with respect to earnings invested outside of the United States.

•Also during the fourth quarter of Fiscal 2013, the Company closed a factory in South Africa resulting in a $3.5 million pre-tax charge ($2.6 million after-tax) primarily related to asset write-downs that were recorded in costs of products sold on the consolidated income statement and in the Non-Operating segment.

•On February 8, 2013, the Venezuelan government announced the devaluation of its currency relative to the U.S. dollar, changing the official exchange rate from 4.30 to 6.30. As a result, the Company recorded a $43 million pre-tax currency translation loss during the fourth quarter of Fiscal 2013, which was reflected within other expense, net, on the consolidated statement of income ($39 million after-tax loss). See the “Venezuela - Foreign Currency and Inflation” section below for further discussion.

•During the third quarter of Fiscal 2013, the Company renegotiated the terms of the Foodstar Holdings Pte ("Foodstar") earn-out that was due in Fiscal 2014 in order to give the Company additional flexibility in the future for growing its business in China, one of its largest and most important emerging markets. This renegotiation resulted in a cash payment of $60 million and a $12 million charge, which represents the difference between the settlement amount and carrying value of the earn-out on the Company's balance sheet at the date of this transaction. This charge was recorded in SG&A on the consolidated income statement and in the Non-Operating segment.

On a reported basis, gross margin for Fiscal 2013 improved 170 basis points to 36.4%, compared to prior year. Excluding charges for special items in the current year(2) as well as charges for productivity initiatives in Fiscal 2012(3), gross margin for the year improved 60 basis points driven by higher pricing and productivity improvements which more than offset higher commodity costs.

13

Operating income for the fiscal year increased 10.6% to $1.66 billion on a reported basis. Excluding charges for special items in the current yearas well as charges for productivity initiatives in the prior year, operating income increased 0.8% versus prior year to $1.72 billion despite increased investments in the business, including higher marketing (+2.5%), enhanced selling capabilities in emerging markets and incremental spending on Project Keystone.

Reported diluted earnings per share from continuing operations of $3.06,were $3.37 for Fiscal 2013, compared to $2.87$3.01 in the prior year. Excluding charges for special items, current year diluted earnings per share from continuing operations were $3.62 in the current year compared to $3.45 in the prior year an increase of 6.6%, overcoming a $0.06excluding charges for productivity initiatives. Earnings per share unfavorable impact from currency translation and translation hedges and a $0.02 per share unfavorable impact for acquisition costs from our recent acquisition in Brazil. Given that almost two-thirds of the Company’s sales and net income are generated outside of the U.S., foreign currency movements can have a significant impact on the Company’s financial results.

| (1) | Organic sales growth is defined as volume plus price or total sales growth excluding the impact of foreign exchange, acquisitions and divestitures. See “Non-GAAP Measures” section below for the reconciliation of all of these organic sales growth measures to the reported GAAP measure. |

| (2) |

| (3) | All Fiscal 2012 results excluding charges for productivity initiatives are non-GAAP measures used for management reporting and incentive compensation purposes. See “Non-GAAP Measures” section below for the reconciliation of all Fiscal 2012 non-GAAP measures to the reported GAAP measures. |

| (4) | ||

Discontinued Operations and Other Disposals

During the first quarter of Fiscal 2013, the Company completed the sale of its Appetizers And, Inc. frozen hors d’oeuvres business which was previously reported within the U.S. Foodservice segment,frozen desserts business, resulting in a $14.5$32.7 million pre-tax ($10.4($21.1 million after-tax) loss. Also during the third quarter of Fiscal 2010, the Company completed the sale of its private label frozen desserts business in the U.K., resulting in a $31.4 million pre-tax ($23.6 million after-tax) loss. During the second quarter of Fiscal 2010, the Company completed the sale of its Kabobs frozen hors d’oeuvres businessloss which was previously reported within the U.S. Foodservice segment, resulting in a $15.0 million pre-tax ($10.9 million after-tax) loss. The losses on each of these transactions havehas been recorded in discontinued operations.

| Fiscal Year Ended | ||||||||

| April 28, | April 29, | |||||||

| 2010 | 2009 | |||||||

| FY 2010 | FY 2009 | |||||||

| (Millions of Dollars) | ||||||||

| Sales | $ | 63.0 | $ | 136.8 | ||||

| Net after-tax losses | $ | (4.7 | ) | $ | (6.4 | ) | ||

| Tax benefit on losses | $ | 2.0 | $ | 2.4 | ||||

| Fiscal Year Ended | |||

| April 28, 2013 FY 2013 | April 29, 2012 FY 2012 | April 27, 2011 FY 2011 | |

| (In millions) | |||

| Sales | $47.7 | $141.5 | $148.0 |

| Net after-tax losses | $(17.6) | $(51.2) | $(39.6) |

| Tax benefit on losses | $0.6 | $1.4 | $2.6 |

Fiscal 2010,2012 Productivity Initiatives

On May 26, 2011, the Company received cash proceedsannounced that it would invest in productivity initiatives during Fiscal 2012 designed to increase manufacturing effectiveness and efficiency as well as accelerate overall productivity on a global scale. The Company recorded costs related to these productivity initiatives of $95$205.4 million from pre-tax ($144.0 million after-tax or $0.45 per share) during the governmentfiscal year ended April 29, 2012, all of the Netherlands for property the government acquired through eminent domain proceedings. The transaction includes the purchase by the government of the Company’s factory located in Nijmegen, which produces soups, pasta and cereals. The cash proceeds are intended to compensate the Company for costs, both capital and expense, the Company will incur three years from the date of the transaction, which is the length of time the Company has to exit the current

15

14

million were recorded in the leased factory while commencing to execute its plans for closure and relocation of the operations. The Company has accountedlosses from discontinued operations for the proceeds on a cost recovery basis. In doing so, the Company has made its estimates of cost, both of a capital and expense nature, to be incurred and recovered and to which proceeds from the transaction will be applied. Of the proceeds received, $81 million was deferred based on management’s total estimated future costs to be recovered and incurred and recorded in other non-current liabilities, other accrued liabilities and accumulated depreciation in the Company’s consolidated balance sheet as of April 28, 2010. These deferred amounts are recognized as the related costs are incurred. If estimated costs differ from what is actually incurred, these adjustments are reflected in earnings. As of April 27, 2011, the remaining deferred amount on the consolidated balance sheet was $63 million and was recorded in other non-current liabilities, other accrued liabilities and accumulated depreciation. No significant adjustments were reflected in earnings in Fiscal 2011. The excess of the $95 million of proceeds received over estimated costs to be recovered and incurred was $15 million which has been recorded as a reduction of cost of products sold in the consolidated statement of income for thefiscal year ended April 28, 2010.29, 2012 . See Note 4, "Fiscal 2012 Productivity Initiatives" in Item 8- "Financial Statements and Supplementary Data" and the "Liquidity and Financial Position" section below for additional information on these productivity initiatives.

Results of Continuing Operations

On March 14, 2012 the Company's Board of Directors authorized a change in the Company's fiscal year end from the Wednesday nearest April 30 to the Sunday nearest April 30. The change in the fiscal year end resulted in Fiscal 2012 changing from a 53 week year to a 52 1/2 week year and was intended to better align the Company's financial reporting period with its business partners and production schedules. This change did not have a material impact on the Company's financial statements.

The Company’s revenues are generated via the sale of products in the following categories:

| Fiscal Year Ended | ||||||||||||

| April 27, | April 28, | April 29, | ||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (52 Weeks) | (52 Weeks) | (52 Weeks) | ||||||||||

| (Dollars in thousands) | ||||||||||||

| Ketchup and sauces | $ | 4,607,971 | $ | 4,446,911 | $ | 4,251,583 | ||||||

| Meals and snacks | 4,282,318 | 4,289,977 | 4,225,127 | |||||||||

| Infant/Nutrition | 1,175,438 | 1,157,982 | 1,105,313 | |||||||||

| Other | 640,861 | 600,113 | 429,308 | |||||||||

| Total | $ | 10,706,588 | $ | 10,494,983 | $ | 10,011,331 | ||||||

| Fiscal Year Ended | |||||||||||

| April 28, 2013 | April 29, 2012 | April 27, 2011 | |||||||||

| (52 Weeks) | (52 1/2 Weeks) | (52 Weeks) | |||||||||

| (In thousands) | |||||||||||

| Ketchup and Sauces | $ | 5,375,788 | $ | 5,232,607 | $ | 4,607,326 | |||||

| Meals and Snacks | 4,240,808 | 4,337,995 | 4,134,836 | ||||||||

| Infant/Nutrition | 1,189,015 | 1,232,248 | 1,175,438 | ||||||||

| Other | 723,275 | 704,722 | 641,036 | ||||||||

| Total | $ | 11,528,886 | $ | 11,507,572 | $ | 10,558,636 | |||||

Fiscal 2013 Company Results- Fiscal Year Ended April 28, 2013 compared to Fiscal Year Ended April 29, 2012

Sales for Fiscal 2013 increased $21 million, or 0.2%, to $11.53 billion. Volume increased 1.0%, as volume gains in emerging markets were partially offset by declines in the U.S., Continental Europe, Australia and Italy. Emerging markets volume included an extra month of results for Brazil, which was more than offset by the Company's decision to exit the T.G.I Friday's® frozen meals business in the U.S. Emerging markets, the Company's top 15 brands and global ketchup continued to be the Company's primary growth drivers, with organic sales growth of 16.8%, 3.6% and 4.6%, respectively (reported sales growth of 14.3%, 0.8%, and 2.8%, respectively). Net pricing increased sales by 2.1%, driven by price increases across the emerging markets, as well as in Continental Europe and U.S. Foodservice. Divestitures decreased sales by 0.3%, and unfavorable foreign exchange rates decreased sales by 2.5%.

Gross profit increased $201 million, or 5.0%, to $4.20 billion, and gross profit margin increased 170 basis points to 36.4%. Current year gross profit includes the previously discussed $3.5 million charge related to the closure of a factory in South Africa. Excluding this charge and charges for productivity initiatives in Fiscal 2012, gross profit margin increased 60 basis points, and gross profit increased $74 million, or 1.8%, as the benefits from higher pricing, volume and productivity initiatives were offset by a $104 million unfavorable impact from foreign exchange and higher commodity costs.

SG&A increased $41 million, or 1.7%, to $2.53 billion, and increased as a percentage of sales to 22.0% from 21.7%. Current year SG&A includes the previously discussed special items of $12 million for the Foodstar earn-out settlement and $45 million in transaction-related costs associated with the Merger Agreement. Excluding these current year special items and charges for productivity initiatives in Fiscal 2012, SG&A increased $60 million, or 2.5%, to $2.48 billion and increased as a percentage of sales to 21.5% from 21.0%. The increase in aggregate spending reflects higher marketing spending, incremental investments in Project Keystone, and strategic investments to drive growth in emerging markets partially offset by a $66 million impact from foreign exchange translation rates, reduced pension expense and effective cost management in developed markets.

Operating income increased $159 million, or 10.6%, to $1.66 billion Excluding the special items in the current year and charges for productivity initiatives in Fiscal 2012, operating income increased $14 million, or 0.8%, to $1.72 billion.

Net interest expense decreased $3 million, to $256 million, reflecting a $9 million decrease in interest expense and a $7 million decrease in interest income, both of which are driven by lower interest rates. Other expense, net, increased $54 million, to $62 million in the current year, primarily due to a $43 million currency translation loss previously discussed recorded during the fourth quarter of Fiscal 2013 resulting from the devaluation of the Venezuelan currency relative to the U.S. dollar, changing the official

15

exchange rate from 4.30 to 6.30. The remaining increase is due to other currency losses this year compared to currency gains last year.

The effective tax rate for Fiscal 2013 decreased to 18.0% from 19.8% in the prior year on a reported basis. Excluding special items in the current year and productivity initiatives last year, the effective rate was 18.2% compared to 21.3% last year. The decrease in the effective tax rate is primarily the result of increased benefits from the revaluation of the tax basis of certain foreign assets, which includes our Fiscal 2013 reorganization, and reduced charges for the repatriation of current year foreign earnings. See below in "Liquidity and Financial Position" for further explanation.These amounts were partially offset by lower current year benefits from tax free interest and tax on income of foreign subsidiaries. The prior year also contained a benefit from the resolution of a foreign tax case. Both periods contained a benefit of approximately $15 million from the reversal of an uncertain tax position liability due to the expiration of the statute of limitations in a foreign tax jurisdiction as well as benefits in each year related to 200 basis point statutory tax rate reductions in the United Kingdom.

Income from continuing operations attributable to H. J. Heinz Company was $1.09 billion, an increase of 11.6% compared to $974 million in the prior year on a reported basis. Excluding special items, income from continuing operations was $1.17 billion, an increase of 4.5% compared to $1.12 billion in the prior year excluding charges for productivity initiatives. Diluted earnings per share from continuing operations of $3.37 were up 12.0% compared to $3.01 in the prior year on a reported basis. Excluding special items, diluted earnings per share was $3.62, an increase of 4.9% compared to $3.45 in the prior year excluding charges for productivity initiatives. EPS movements were unfavorably impacted by $0.09 from currency translation and translation hedges.

The impact of fluctuating translation exchange rates in Fiscal 2013 has had a relatively consistent impact on all components of operating income on the consolidated statement of income.

FISCAL YEAR 2013 OPERATING RESULTS BY BUSINESS SEGMENT

North American Consumer Products