UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

Form 10-K

|

| | |

| þ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended July 2, 2011June 29, 2013

or

|

| | |

| o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period fromto

Commission file number 1-4224

Avnet, Inc.

(Exact name of registrant as specified in its charter)

| | |

| |

New York

(State or other jurisdiction of

incorporation or organization) | | 11-1890605

(I.R.S. Employer

Identification No.) |

| | |

2211 South 47th Street,

Phoenix, Arizona

(Address of principal executive offices) | | 85034

(Zip Code) |

Registrant’s telephone number, including area code (480) 643-2000

Securities registered pursuant to Section 12(b) of the Act:

| | |

| | |

| Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesþ Noo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yeso Noþ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesþ Noo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesþ Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.oþ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

| | | | | | |

| | | |

Large accelerated filerþ | | Accelerated filero | | Non-accelerated filero | | Smaller reporting companyo |

| | | | (Do not check if a smaller reporting company) | | Smaller reporting company o |

Indicate by checkmarkcheck mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yeso Noþ

The aggregate market value (approximate) of the registrant’s common equity held by non-affiliates based on the closing price of a share of the registrant’s common stock for New York Stock Exchange composite transactions on January 1, 2011December 28, 2012 (the last business day of the registrant’s most recently completed second fiscal quarter) was $4,995,335,220.$4,058,517,453.

As of July 29, 2011,26, 2013, the total number of shares outstanding of the registrant’s Common Stock was 152,807,450137,153,362 shares, net of treasury shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement (to be filed pursuant to Reg. 14A) relating to the Annual Meeting of Shareholders anticipated to be held on November 4, 20118, 2013 are incorporated herein by reference in Part III of this Report.

TABLE OF CONTENTS

PART I

Avnet, Inc., incorporated in New York in 1955, together with its consolidated subsidiaries (the “Company” or “Avnet”), is one of the world’s largest industrialvalue-added distributors, based on sales, of electronic components, enterprise computer and storage products, IT services and embedded subsystems. Avnet creates a vital link in the technology supply chain that connects more than 300 of the world’s leading electronic component and computer product manufacturers and software developers with a global customer base of more than 100,000 original equipment manufacturers (“OEMs”), electronic manufacturing services (“EMS”) providers, original design manufacturers (“ODMs”), and value-added resellers (“VARs”). Avnet distributes electronic components, computer products and software, as received from its suppliers or withthrough a customized solution, and offers assembly orand other value added by Avnet. Additionally,value-added services. In addition, Avnet provides engineering design, materials management and logistics services, system integration and configuration, and supply chain services that can be customized to meet thespecific requirements of both customers and suppliers.

Organizational Structure

Avnet has two primary operating groups — Electronics Marketing (“EM”) and Technology Solutions (“TS”). Both operating groups have operations in each of the three major economic regions of the world: the Americas; Europe, the Middle East and Africa (“EMEA”); and Asia/Pacific, consisting of Asia, Australia and New Zealand (“Asia” or “Asia/Pac”). Each operating group has its own management team led by a group president and includes regional presidents and senior executives within the operating group who manage the various functions within the businesses. Each operating group also has distinct financial reporting that is evaluated at the corporate level on which operating decisions and strategic planning for the Company as a whole are made. Divisions exist within each operating group that serve primarily as sales and marketing units to further streamline the sales and marketing efforts within each operating group and enhance each operating group’s ability to work with its customers and suppliers, generally along more specific product lines or geographies. However, each division relies heavily on the support services provided by the operating group as well as centralized support at the corporate level.

Avnet’s operating groups and their sales are as follows:

| | | | | | | | | |

| | | Fiscal 2011 | | Percentage |

| Region | | Sales | | of Sales |

| | | (Millions) | | | | | |

| EM Americas | | $ | 5,113.8 | | | | 19.3 | % |

| EM EMEA | | | 4,816.3 | | | | 18.1 | |

| EM Asia | | | 5,136.1 | | | | 19.4 | |

| | | | | | | |

| Total EM | | | 15,066.2 | | | | 56.8 | |

| | | | | | | |

| TS Americas | | | 6,404.7 | | | | 24.1 | |

| TS EMEA | | | 3,577.1 | | | | 13.5 | |

| TS Asia | | | 1,486.4 | | | | 5.6 | |

| | | | | | | |

| Total TS | | | 11,468.2 | | | | 43.2 | |

| | | | | | | |

| Total Avnet | | $ | 26,534.4 | | | | 100.0 | % |

| | | | | | | |

|

| | | | | | |

| Region | Fiscal 2013 Sales | | Percentage of Sales |

| | (Millions) | | |

| EM Americas | $ | 5,263.8 |

| | 20.7 | % |

| EM EMEA | 4,096.0 |

| | 16.1 |

|

| EM Asia | 5,734.6 |

| | 22.5 |

|

| Total EM | 15,094.4 |

| | 59.3 |

|

| TS Americas | 5,452.8 |

| | 21.4 |

|

| TS EMEA | 3,181.9 |

| | 12.5 |

|

| TS Asia | 1,729.8 |

| | 6.8 |

|

| Total TS | 10,364.5 |

| | 40.7 |

|

| Total Avnet | $ | 25,458.9 |

| | 100.0 | % |

A description of each operating group and its businesses is presented below. Further financial information by operating group and geography is provided in Note 16 to the consolidated financial statements appearing in Item 15 of this Report.

Electronics Marketing

EM markets and sells semiconductors, and interconnect, passive and electromechanical devices (“IP&E”) and embedded products for more than 300 of the world’s leading electronic component manufacturers. EM markets and sells its products and services to a diverse customer base serving many end-markets including automotive, communications, computer hardware and peripheral,peripherals, industrial and manufacturing, medical equipment, militaryand defense and aerospace. EM also offers an array of value-added services that help customers evaluate, design-in and procure electronic components throughout the lifecycle of their technology products and systems. By working with EM, from the design phase through new product introduction and throughout the product lifecycle, customers and suppliers can accelerate their time to market and realize cost efficiencies in both the design and manufacturing process.

3

EM Design Chain Services3

EM Design Chain Services

EM offers design chain services that provide engineers a host of technical design solutions in support of the sales process of complex products and technologies. With access to a suite of design tools and engineering services from any point in the design cycle, customers can get product specifications along with evaluation kits and reference designs that enable a broad range of applications from concept through detailed design including new product introduction. EM also offers engineering and technical resources deployed globally to support product design, bill of materials development, design services and technical education and training. By utilizing EM’s Design Chain Services,design chain services, customers can optimize their component selection and accelerate their time to market.

EM Supply Chain Services

EM Supply Chain Services providessupply chain services provide end-to-end solutions focused on OEMs, EMS providers and electronic component manufacturers, enabling them to optimize supply chains on a local, regional or global basis. By combining internal competencies in global warehousing and logistics, finance, information technology and asset management with its global footprint and extensive partner relationships, EM’s Supply Chain Services developssupply chain services develop a deeper level of engagement with its customers. These customers can continuously manage their supply chains to meet the demands of a competitive environment globally without a commensurate investment in physical assets. With proprietary planning tools and a variety of inventory management solutions, EM can provide unique solutions that meet a customer’s just-in-time requirements in a variety of scenarios including lean manufacturing, demand flow and outsourcing.

Embedded Solutions

In the Americas, Avnet Electronics MarketingEmbedded provides embedded computing solutions including technical design, integration and assembly to developers of application-specific computing solutions in the non-PC market. Customers include OEMs targeting the medical, telecommunications, industrial and digital editing markets. The Embedded Solutions group represents the combination of the EM Americas existing embedded business, the acquired Bell Microproducts Inc. embedded business and the TS Americas embedded business that was transferred to EM Americas in the first quarter of fiscal 2011.

EM Sales and Marketing Divisions

Each of EM’s regions has sales and marketing divisions that generally focus on a specific customer segment, particular product lines or a specific geography. The divisions offer access to one of the industry’s broadest line cards and convenient one-stop shopping with an emphasis on responsiveness, engineering support, on-time delivery and quality. Certain specialty services are made available to the individual divisions through common support service units. Customers are further supported by a sophisticated e-commercee-Commerce platform, Avnet Express, thatwhich includes a host of powerful functions such as parametric parts searches,search capabilities for component part selection, bill of material optimization and partscomponent cross-referencing. The site enables end-to-end online service from part and inventory searches, price checking and ordering to online payment. EM Americas addresses the needs of its customers and suppliers through focused channels to service small- to medium-sized customers, global customers, defense and aerospace customers and contract manufacturers. In EMEA, divisions, which are organized by semiconductors, IP&E products and supply chain services, address customers on both a pan-European and regional basis. EM EMEA does business in over 40 European countries, and over 10 countries in the Middle East and Africa. EM Asia goes to market with sales and marketing divisions within China, South Asia, TaiwanAustralia, New Zealand and Japan.Taiwan. EM Japan has sales and marketing divisions to serve Japanese OEMs in Japan, Southeast Asia and China. All regions within EM provide the Design Chain Servicesdesign chain services and Supply Chain Servicessupply chain services described above.

Technology Solutions

As a leading global IT solutions distributor, TS collaborates with its customers and suppliers to create and deliver services, software and hardware solutions that address the business needs of end-user customers locally and around the world. TS focuses on the global value-added distribution of enterprise computing servers and systems, software, storage, services and complex solutions from the world’s foremost technology manufacturers, marketingmanufacturers. TS partners with its customers and selling themsuppliers to create and throughdeliver effective data center and IT lifecycle solutions that solve the VAR channel.business challenges of end-user customers locally and around the world. TS also serves a number of customer segments, from VARs, system integrators ("SIs") and independent software vendors ("ISVs") to the worldwide OEM market for computing technology system integrators and non-PC OEMs that requirerequiring embedded systems and solutions including engineering, product prototyping, integration and other value-added services. The operating groupTS also provides the latest hard disk drives, microprocessor, motherboard and DRAM module technologies to manufacturers of general-purpose computers and system builders. TS has dedicated sales and marketing divisions dedicated toteams serving these customer segmentssegments.

Customers rely on TS' supplier relationships and experienced sales, marketing, technical and financial experts to help them identify and capitalize on business opportunities in high-growth technology, vertical markets and geographic services to close deals quickly and profitably. Suppliers rely on TS' technology expertise and global scale and scope to broaden their customer base and grow sales in markets around the world. TS has built an ecosystem of highly-trained and knowledgeable VARs who serve as well as independent software vendors.

4

TS enables VARsextensions of suppliers' sales forces to grow faster by helping them understand their customers’ unique business requirements so that they can tailor a completedeliver complex IT solution spanning supplier lines and delivering a higher return on investment.solutions. Unique to Avnet SolutionsPath®is its proven SolutionsPath® methodology, which offers a proven methodology comprisingmarket-specific business analysis and planning, training and enablement, and ongoing support to help partners quickly

and cost effectively attain solution-selling expertise they can use to develop and deploy an array of data center solutions for high-growth market segments. Avnet SolutionsPath® includes practices dedicated to vertical markets such as healthcare, government, energy, banking and retail, as well as technology practices focused on virtualization, storage, networking, security, unified communications, mobility and cloud computing.

TS also provides logistics, sales, marketing, financiala robust portfolio of software, IT lifecycle and technicaleducational service offerings that expand customers' solution delivery capabilities, extend their reach and resources, and enhance project success and return on investment for deployments throughout the IT lifecycle. The TS team sells and delivers complex IT solutions to a variety of channel partners, including VARs, ISVs, SIs and OEMs. Areas of expertise include infrastructure and application management, business commerce and analytics, cloud enablement, aftermarket and IT lifecycle services, including engineering support, systems integration and configurations.multilingual vendor accredited training. To continue to meet customer expectations in an evolving IT ecosystem, TS is also focused on delivering single and multi-vendor converged systems.

In EMEATS continues to invest in geographic, technology and Asia/Pacific,vertical markets with high growth potential via strategic, value-creating acquisitions and organic local market development. These investments ensure that TS provides embedded computing solutions including technical design, integrationhas the critical scale and assemblylocal market expertise in place when and where its customers and suppliers want to developers of application-specific computing solutions in the non-PC market. Developers include OEMs targeting the medical, telecommunications, industrialdo business so that they can capture opportunities quickly and digital editing markets. In these regions, TS also provides the latest hard disk drives, microprocessor, motherboardwith less risk and DRAM module technologies to manufacturers of general-purpose computers and system builders.cost.

Foreign Operations

As noted in the operating group discussions, Avnet has significant operations in all three major economic regions of the world: the Americas, EMEA and Asia/Pacific. The percentage of Avnet’s consolidated sales by region is presented in the following table:

| | | | | | | | | | | | | |

| | | Percentage of Sales for Fiscal Year |

| Region | | 2011 | | 2010 | | 2009 |

| Americas | | | 43 | % | | | 44 | % | | | 47 | % |

| EMEA | | | 32 | | | | 31 | | | | 32 | |

| Asia/Pac | | | 25 | | | | 25 | | | | 21 | |

| | | | | | | | | | | | | |

| | | | 100 | % | | | 100 | % | | | 100 | % |

| | | | | | | | | | | | | |

|

| | | | | |

| | Percentage of Sales for Fiscal Year |

| Region | 2013 | | 2012 | | 2011 |

| Americas | 42% | | 45% | | 43% |

| EMEA | 29 | | 29 | | 32 |

| Asia/Pac | 29 | | 26 | | 25 |

| | 100% | | 100% | | 100% |

Avnet’s foreign operations are subject to a variety of risks. These risks are discussed further underRisk Factorsin Item 1A and underQuantitative and Qualitative Disclosures About Market Riskin Item 7A of this Report. Additionally, the specific translation impacts of foreign currency fluctuations, most notably the Euro, on the Company’s consolidated financial statements are further discussed inManagement’s Discussion and Analysis of Financial Condition and Results of Operationsin Item 7 of this Report.

Acquisitions

Avnet has historically pursued a strategic acquisition program to growfurther its geographicstrategic objectives and market coverage in world markets for electronic components and computer products and solutions.support key business initiatives. This program was a significant factor in Avnet becoming one of the largest industrialvalue-added distributors of suchelectronic components, enterprise computer and storage products, IT services and services worldwide.embedded subsystems. Avnet expects to continue to pursue strategic acquisitions as part of its overall growth strategy, with its focus likely directed primarily at smaller targets in markets where the Company is seeking to expand its market presence, increase its scale and scope, and/orand increase its product or service offerings.

During fiscal 2011,2013, the Company completed seven12 acquisitions the most significant of which was the acquisition of Bell Microproducts Inc. (“Bell”), a value-added distributor of storage and server products and solutions and computer components products, providing integration and support services to OEMs, VARs, system builders and end users in the U.S., Canada, EMEA and Latin America. Bell operated both a distribution and single tier reseller business and generated saleswith aggregate annualized revenue of approximately $3.0$1.18 billion in calendar 2009, of which 42%, 41% and 17% was generated in North America, EMEA and Latin America, respectively. The consideration for the transaction totaled $255 million for the equity of Bell which consisted of $7.00 in cash for each share of Bell common stock outstanding, cash payment for Bell equity awards, and cash payments required under existing Bell change of control agreements, plus the assumption of $323 million of Bell net debt. Of the debt acquired, Avnet repaid approximately $210 million of debt (including associated fees) immediately after closing. As of the end of fiscal 2011, the Company has completed the integration of Bell into both the EM and TS operating groups and expects the full impact of the cost synergies to be realized in the first quarter of fiscal 2012.

5

. See Item 7.Management’s Discussion and Analysis of Financial Condition and Results of Operationsin Part II of this Form 10-K for additional information on acquisitions completed during fiscal 2011, 20102013, 2012 and 2009.2011.

Major Products

One of Avnet’s competitive strengths is the breadth and quality of the suppliers whose products it distributes. IBM products accounted for approximately 12%, 15%11% and 15%12% of the Company’s consolidated sales during fiscal 2011, 20102013, 2012 and 2009, 2011,

respectively, and was the only supplier from which sales of its products exceeded 10% of consolidated sales. Listed in the table below are the major product categories and the Company’s approximate sales of each during the past three fiscal years:

| | | | | | | | | | | | | |

| | | Years Ended | |

| | | July 2, | | | July 3, | | | June 27, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | (Millions) | |

| Semiconductors | | $ | 14,149.3 | | | $ | 10,098.7 | | | $ | 8,324.0 | |

| Computer products | | | 10,284.6 | | | | 7,302.8 | | | | 6,393.4 | |

| Connectors | | | 1,041.4 | | | | 841.4 | | | | 735.2 | |

| Passives, electromechanical and other | | | 1,059.1 | | | | 917.3 | | | | 777.3 | |

| | | | | | | | | | |

| | | $ | 26,534.4 | | | $ | 19,160.2 | | | $ | 16,229.9 | |

| | | | | | | | | | |

|

| | | | | | | | | | | |

| | Years Ended |

| | June 29, 2013 | | June 30, 2012 | | July 2, 2011 |

| | (Millions) |

| Semiconductors | $ | 13,720.8 |

| | $ | 13,461.6 |

| | $ | 14,149.3 |

|

| Computer products | 9,346.0 |

| | 9,984.4 |

| | 10,284.6 |

|

| Connectors | 687.6 |

| | 667.5 |

| | 1,041.4 |

|

| Passives, electromechanical and other | 1,704.5 |

| | 1,594.0 |

| | 1,059.1 |

|

| | $ | 25,458.9 |

| | $ | 25,707.5 |

| | $ | 26,534.4 |

|

Competition & Markets

Avnet is one of the world’s largest industrial distributors, based on sales, of electronic components and computer products and services. The Company has more than 300 locations worldwide as well as a limited number of instances where Avnet-owned product is stored in customer facilities. Some of these locations contain sales, warehousing and administrative functions for multiple sales and marketing units.

The electronic components and computer products industries continue to be extremely competitive and are subject to rapid technological advances. The Company’s major competitors include Arrow Electronics, Inc., Future Electronics and World Peace Group.Group, and, to a lesser extent, Ingram Micro, Inc. and Tech Data Corp. There are also certain smaller, specialized competitors who generally focus on narrower markets, products or particular sectors. As a result of these factors, Avnet must remain competitive in its pricing of goods and services.

AnotherA key competitive factor in the electronic component and computer product distribution industry is the need to carry a sufficient amount of inventory to meet customers’ rapid delivery requirements. However, toTo minimize its exposure related to valuation of inventory on hand, the majority of the Company’s products are purchased pursuant to non-exclusive distributor agreements. These agreements, which typically provide certain protections for product obsolescence and price erosion anderosion. These agreements are generally cancelable upon 30 to 180 days’ notice. Innotice and, in most cases, these agreements provide for inventory return privileges upon cancellation. In addition, the Company enhances its competitive position by offering a variety of value-added services, which entail the performance of services and/or processes tailored to individual customer specifications and business needs such as point of use replenishment, testing, assembly, supply chain management and materials management. For the year ended June 29, 2013, sales of services constituted less than 10% of our total revenues.

AnotherA competitive advantage is the size of the supplier base. Because of the number of Avnet’s suppliers, many customers can simplify their procurement process and make all of their required purchases from Avnet, rather than purchasing from several different vendors.

Seasonality

Historically, Avnet’s business has not been materially impacted by seasonality, with the exception of a relatively minor impact on consolidated results from the growth in revenues in the Technology SolutionsTS business during the December quarter primarily driven by the fiscalcalendar year end of a key supplier.suppliers and customers.

6

Number of Employees

At July 2, 2011,June 29, 2013, Avnet had approximately 17,60018,500 employees.

Available Information

The Company files its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other documents with the U.S. Securities and Exchange Commission (“SEC”) under the Securities Exchange Act of 1934. A copy of any document the Company files with the SEC is available for review at the SEC’s public reference room, 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the public reference room by calling the SEC at 1-800-SEC-0330. The Company’s SEC filings are also available to the public on the SEC’s website athttp://www.sec.gov and through the New York Stock Exchange (“NYSE”), 20 Broad Street, New York, New York 10005, on which the Company’s common stock is listed.

A copy of any of the Company’s filings with the SEC, or any of the agreements or other documents that constitute exhibits to those filings, can be obtained by request directed to the Company at the following address and telephone number:

Avnet, Inc.

2211 South 47th Street

Phoenix, Arizona 85034

(480) 643-2000

Attention: Corporate Secretary

The Company also makes these filings available, free of charge, through its website (see “Avnet Website” below).

Avnet Website

In addition to the information about Avnet contained in this Report, extensive information about the Company can be found atwww.avnet.com, including information about its management team, products and services and corporate governance practices.

The corporate governance information on the website includes the Company’s Corporate Governance Guidelines, the Code of Conduct and the charters for each of the committees of Avnet’s Board of Directors. In addition, amendments to the Code of Conduct, committee charters and waivers granted to directors and executive officers under the Code of Conduct, if any, will be posted in this area of the website. These documents can be accessed atwww.avnet.com under the “Investor Relations — Corporate Governance” caption. Printed versions of the Corporate Governance Guidelines, Code of Conduct and charters of the Board committees can be obtained, free of charge, by writing to the Company at the address listed above in “Available Information.”

In addition, the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports, if any, filed or furnished pursuant to Section 13(a) or 15(d) of Securities Exchange Act of 1934, as well as Section 16 filings made by any of the Company’s executive officers or directors with respect to Avnet common stock, are available on the Company’s website (www.avnet.com under the “Investor Relations — SEC Filings” caption) as soon as reasonably practicable after the report is electronically filed with, or furnished to, the Securities and Exchange Commission.

These details about Avnet’s website and its content are only for information. The contents of the Company’s website are not, nor shall they be deemed to be, incorporated by reference in this Report.

Item 1A. Risk Factors

Forward-Looking Statements Andand Risk Factors

This Report contains forward-looking statements with respect to the financial condition, results of operations and business of Avnet. These statements are generally identified by words like “believes,” “expects,” “anticipates,” “should,” “will,” “may,” “estimates” or similar expressions. Forward-looking statements are subject to numerous assumptions, risks and uncertainties.

7

Except as required by law, Avnet does not undertake any obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Factors that may cause actual results to differ materially from those contained in the forward-looking statements include the following:

Economic weakness and uncertainty could adversely affect our revenuesresults and gross margins.prospects.

The Company’s revenuesCompany's results, operations and gross profit marginsprospects depend significantly on worldwide economic conditions, the demand for its products and services, and the financial condition of its customers.customers and suppliers. Economic weakness and uncertainty, including ongoing macroeconomic issues in many countries, have in the past resulted, and may result in the future, in decreased revenues, margins, earnings and gross profit margins.impairments to long-lived assets, including goodwill and other intangible assets. Economic weakness and uncertainty also make it more difficult for the Company to forecast with a great deal of confidence the overall supplymanage inventory levels and/or collect customer receivables, which may result in reduced access to liquidity and demand throughout the IT supply chain.higher financing costs.

While the Company’s operating results over the past four quarters would suggest that the business has experienced a significant recovery, there can be no assurance that the recovery to date will continue at the current pace or at all; nor can there be any assurance that such economic volatility experienced recently will not reoccur or continue.

The electronics component and computer industries are highly competitive and if the Company fails to compete effectively, its revenues, gross profit margins and prospects may decline.

The market for the Company’sCompany's products and services is very competitive and subject to rapid technological advances.advances, new market entrants, changes in industry standards and changes in customer needs. Not only does the Company compete with other global distributors, it also competes for customers with regional distributors and some of the Company’sCompany's own suppliers.suppliers that maintain direct sales efforts. The Company’sCompany's failure to maintain and enhance its competitive position could adversely affect its business and prospects. Furthermore, the Company’sCompany's efforts to compete in the marketplace could cause deterioration of gross profit margins and, thus, overall profitability.

The size of the Company’sCompany's competitors vary across market sectors, as do the resources the Company has allocated to the sectors and geographic areas in which it does business. Therefore, some of the competitors may have greater financial, personnel, capacity and other resources or a more extensive customer base than the Company has in one or more of its market sectors and geographic areas.areas, which may result in the Company not being able to effectively compete in certain markets which could impact the Company's profitability and prospects.

An industry down-cycle in semiconductors could significantly affect the Company’sCompany's operating results as a large portion of revenues comescome from sales of semiconductors, which is a highly cyclical industry.

The semiconductor industry historically has experienced periodic fluctuations in product supply and demand, often associated with changes in technology and manufacturing capacity, and is generally considered to be highly cyclical. During each of the last three fiscal years, sales of semiconductors represented over 50% of the Company’sCompany's consolidated sales, and the Company’sCompany's revenues, particularly those of EM, closely follow the strength or weakness of the semiconductor market. Future downturns in the technology industry, particularly in the semiconductor sector, could negatively affect the Company’sCompany's operating results and negatively impact the Company’sCompany's ability to maintain its current profitability levels.

Failure to maintain its relationships with key suppliers could adversely affect the Company’s sales.

One of the Company’sCompany's competitive strengths is the breadth and quality of the suppliers whose products the Company distributes. However, sales of products and services from one of the Company’sCompany's suppliers, IBM, accounted for approximately 12% of the Company’sCompany's consolidated sales in fiscal year 2011.2013. Management expects IBM products and services to continue to account for roughly a similar percentage of the Company’sCompany's consolidated sales in fiscal year 2012.2014. The Company’sCompany's contracts with its suppliers, including those with IBM, vary in duration and are generally terminable by either party at will upon notice. To the extent IBM or other primary suppliers significantly reduce their volume of business with the Company in the future, because of a product shortage, an unwillingness to do business with Avnet, or otherwise, the Company’sCompany's business and relationships with its customers could be materially and adversely affected because its customers depend on the Company’sCompany's distribution of electronic components and computer products from the industry’sindustry's leading suppliers. In addition, to the extent that any of the Company’sCompany's key suppliers modify the terms of their contracts including, without limitation, the terms regarding price protection, rights of return, rebates or other terms that protect or enhance the Company’sCompany's gross margins, it could materially and adversely affect the Company’sCompany's results of operations, financial condition or liquidity.

8

The Company's non-U.S. locations represent a significant portion of its revenue, and consequently, the Company is increasingly exposed to risks associated with operating internationally.

During fiscal year 2013, 2012 and 2011, approximately 63%, 61% and 62%, respectively, of the Company's sales came from its operations outside the United States. As a result of the Company's foreign sales and locations, in particular those in emerging and developing economies, the Company's operations are subject to a variety of risks that are specific to international operations, including, but not limited to, the following:

potential restrictions on the Company's ability to repatriate funds from its foreign subsidiaries;

foreign currency and interest rate fluctuations and the impact on the Company's reported results of operations;

import and export duties and value-added taxes;

compliance with foreign and domestic import and export regulations, data privacy regulations, business licensing requirements, environmental regulations and anti-corruption laws, the failure of which could result in severe penalties including monetary fines, criminal proceedings and suspension of import or export privileges;

changing tax laws and regulations;

regulatory requirements and prohibitions that differ between jurisdictions;

economic and political instability, terrorism and potential military conflicts or civilian unrest;

fluctuations in freight costs, limitations on shipping and receiving capacity, and other disruptions in the transportation and shipping infrastructure;

natural disasters and health concerns;

differing environmental regulations and employment practices and labor issues; and

the risk of non-compliance with local laws.

In addition to the cost of compliance, the potential criminal penalties for violations of export regulations and anti-corruption laws by the Company or its third-party agents create heightened risks for the Company's international operations. In the event that a governing regulatory body determined that the Company had violated applicable import or export regulations or anti-corruption laws, the Company could be fined significant sums, incur sizable legal defense costs and/or its import or export capabilities could be restricted, which could have a material and adverse effect on the Company's business. Additionally, allegations that the Company has violated a governmental regulation may negatively impact the Company's reputation, which may result in customers or suppliers being unwilling to do business with the Company. While the Company has adopted measures designed to ensure compliance with these laws, the Company cannot be assured that such measures will be adequate or that its business will not be materially and adversely impacted in the event of an alleged violation.

The Company's acquisition strategy may not produce the expected benefits, which may adversely affect the Company's results of operations.

Avnet has made, and expects to continue to make, strategic acquisitions or investments in companies around the world to further its strategic objectives and support key business initiatives. Acquisitions and investments involve risks and uncertainties, some of which may differ from those associated with Avnet's historical operations. The risks relating to such transactions include, but are not limited to, risks relating to expanding into emerging markets and business areas, adding additional product lines and services, incurring unanticipated costs or liabilities associated with the companies acquired and diverting management's attention from existing business operations. As a result, the Company's profitability may be negatively impacted. In addition, the Company may not be successful in integrating the acquired businesses or the integration may be more difficult, costly or time-consuming than anticipated. Further, any litigation relating to a potential acquisition will result in an increase in the expenses associated with the acquisition or cause a delay in completing the acquisition, thereby impacting the Company's profitability. The Company may experience disruptions that could, depending on the size of the acquisition, have a material adverse effect on its business, especially where an acquisition target may have pre-existing non-compliance or pre-existing deficiencies or material weaknesses in internal controls as those terms are defined under relevant SEC rules and regulations. Furthermore, the Company may not realize all of the anticipated benefits from its acquisitions, which could materially and adversely affect the Company's financial performance.

Major disruptions to the Company’s logistics capability could have a material adverse impact on the Company’s operations.

The Company's global logistics services are operated through specialized, centralized or outsourced distribution centers around the globe. The Company also depends almost entirely on third-party transportation service providers for the delivery of products to its customers. A major interruption or disruption in service at one or more of its distribution centers for any reason (such as natural disasters, pandemics, or significant disruptions of services from our third-party providers) could cause cancellations or delays in a significant number of shipments to customers and, as a result, could have a severe impact on the Company's business, operations and financial performance.

If the Company’s internal information systems fail to function properly, or if the Company is unsuccessful in the integration or upgrade of information systems, its business operations could suffer.

The Company's expanding operations put increasing pressure on the Company's information systems to facilitate the day-to-day operations of the business and to produce timely, accurate and reliable reports on financial and operational results. Currently, the Company's global operations are tracked with multiple information systems, some of which are subject to ongoing IT projects designed to streamline or optimize the Company's global information systems. There is no guarantee that the Company will be successful at all times in these efforts or that there will not be integration difficulties that will adversely affect the Company's ability to complete business transactions timely or the accurate and timely recording and reporting of financial data. In addition, the Company's information technology is subject to cybersecurity breaches, computer hacking or other general system failures. Maintaining and operating these systems requires continuous investments. A security breach could result in sensitive data being manipulated or exposed to unauthorized persons or to the public. A failure of any of these information systems in a way described above or material difficulties in upgrading these information systems could have material adverse effects on the Company's business and its compliance with reporting obligations under federal securities laws.

Declines in the value of the Company’sCompany's inventory or unexpected order cancellations by the Company’sCompany's customers could materially and adversely affect its business, results of operations, financial condition and liquidity.

The electronic components and computer products industries are subject to rapid technological change, new and enhanced products, changes in customer needs and evolvingchanges in industry standards, which can contribute to a decline in value or obsolescence of inventory. Regardless of the general economic environment, it is possible that prices will decline due to a decrease in demand or an oversupply of products and, as a result of the price declines, there may be greater risk of declines in inventory value. Although

it is the policy of many of the Company’sCompany's suppliers to offer distributors like Avnet certain protections from the loss in value of inventory (such as price protection and limited rights of return), the Company cannot be assured that such policies will fully compensate for the loss in value, or that the vendors will choose to, or be able to, honor such agreements, some of which are not documented and, therefore, subject to the discretion of the vendor. In addition, the Company’smajority of the Company's sales are typically made pursuant to individual purchase orders, and the Company generally does not have long-term supply arrangements with its customers. Generally, the Company’sCompany's customers may cancel orders 30 days prior to shipment with minimal penalties. The Company cannot be assured that unforeseen new product developments, declines in the value of the Company’sCompany's inventory or unforeseen order cancellations by its customers will not materially and adversely affect the Company’sCompany's business, results of operations, financial condition or liquidity.

Substantial defaults by the Company’sCompany's customers on its accounts receivable or the loss of significant customers could have a significant negative impact on the Company’sCompany's business, results of operations, financial condition or liquidity.

A significant portion of the Company’sCompany's working capital consists of accounts receivable from customers. If customers responsible for a significant amount of accounts receivable were to become insolvent or otherwise unable to pay for products and services,the amount they owe the Company, or were to become unwilling or unable to make such payments in a timely manner, the Company’sCompany's business, results of operations, financial condition or liquidity could be adversely affected. An economic or industry downturn could adversely and materially affect the servicing of these accounts receivable, which could result in longer payment cycles, increased collection costs and defaults in excess of management’smanagement's expectations. A significant deterioration in the Company’sCompany's ability to collect on accounts receivable could also impact the cost or availability of financing under its accounts receivable securitization program (seeFinancingTransactionsappearing in Item 7 of this Report).

The Company’s non-U.S. locations represent a significantCompany may not have adequate or cost-effective liquidity or capital resources.

The Company's ability to satisfy its cash needs depends on its ability to generate cash from operations and growing portionto access the financial markets, both of its revenue, and consequently, the Company is increasingly exposed to risks associated with operating internationally.

During fiscal year 2011, 2010 and 2009, approximately 62%, 60% and 58%, respectively, of the Company’s sales came from its operations outside the United States. As a result of the Company’s foreign sales and locations, in particular those in emerging and developing economies, the Company’s operationswhich are subject to a variety of risksgeneral economic, financial, competitive, legislative, regulatory and other factors that are specificbeyond the Company's control.

The Company may need to international operations, including, but not limited to, the following:

potential restrictions on the Company’s ability to repatriate funds fromsatisfy its foreign subsidiaries;

foreign currency and interest rate fluctuations and the impact on the Company’s reported results of operations;

import and export duties and value-added taxes;

compliance with foreign and domestic import and export regulations, business licensing requirements and anti-corruption laws, the failure of which could result in severe penalties including monetary fines, criminal proceedings and suspension of export privileges;

changing tax laws and regulations;

regulatory requirements and prohibitions that differ between jurisdictions;

political instability, terrorism and potential military conflicts or civilian unrest;

fluctuations in freight costs, limitations on shipping and receiving capacity, and other disruptions in the transportation and shipping infrastructure;

| • | | differing environmental regulations and employment practices and labor issues; and |

|

| • | | the risk of non-compliance with local laws. |

9

The potential criminal penalties for violations of export regulations and anti-corruption laws, particularly anti-bribery, data privacy laws and environmental laws and regulations in many jurisdictions, create heightened risks for the Company’s international operations. In the event that a governing regulatory body determined that the Company had violated applicable export regulations or anti-corruption laws, the Company could be fined significant sums, incur sizable legal defense costs and/or its export capabilities could be restricted, which could have a material and adverse effect on the Company’s business. While the Company has and will continue to adopt measures designed to ensure compliance with these laws, the Company cannot be assured that such measures will be adequate or that its business willcash needs through external financing. However, external financing may not be materiallyavailable on acceptable terms or at all. As of June 29, 2013, Avnet had total debt outstanding of approximately $2.05 billion under various notes and adversely impacted in the eventcommitted and uncommitted lines of an alleged violation.

credit with financial institutions. The Company’s acquisition strategy may not produce the expected benefits, which may adversely affect the Company’s results of operations.

Avnet historically has pursued a strategic acquisition programCompany needs cash to grow its global businessmake interest payments on, and to refinance, this indebtedness and for electronic and computer products, thereby enabling Avnet to solidify and maintain its leadership position in the marketplace. Acquisitions involve risks and uncertaintiesgeneral corporate purposes, such as expansion into new geographic marketsfunding its ongoing working capital and business areas and diversioncapital expenditure needs. Under the terms of management’s attention from existing business operations. In addition,any external financing, the Company may not be successfulincur higher than expected financing expenses and become subject to additional restrictions and covenants. Any material increase in integrating the acquired businesses or the integration may be more difficult, costly or time-consuming than anticipated. Consequently, the Company may experience disruptions thatCompany's financing costs could depending on the size of the acquisition, have a material adverse effect on its profitability.

Under certain of its credit facilities, the Company is required to maintain certain specified financial ratios and meet certain tests. If the Company fails to meet these financial ratios and/or tests, it may be unable to continue to utilize these facilities. If the Company is unable to utilize these facilities, it may not have sufficient cash available to make interest payments on and refinance indebtedness and for general corporate needs. General economic or business especially where an acquisition targetconditions, domestic and foreign, may have pre-existing non-compliancebe less favorable than management expects and could adversely impact the Company's sales or pre-existing deficienciesits ability to collect receivables from its customers, which may impact access to the Company's securitization program.

The agreements governing some of the Company's financings contain various covenantsand restrictions that limit the discretion of management in operating its businessand could prevent us from engaging in some activities that may be beneficial to theCompany's business.

The agreements governing the Company's financing, including its credit facility and the indentures governing the Company's outstanding notes, contain various covenants and restrictions that, in certain circumstances, limit the Company's ability, and the ability of certain subsidiaries, to:

grant liens on assets;

make restricted payments (including paying dividends on capital stock or material weaknesses as those terms are defined under relevant SEC rulesredeeming or repurchasing capital stock);

make investments;

merge, consolidate or transfer all or substantially all of the Company’s assets;

incur additional debt; or

engage in certain transactions with affiliates.

As a result of these covenants and regulations. Furthermore,restrictions, the Company may be limited in the future in how it conducts its business and may be unable to raise additional debt, compete effectively or make further investments.

The Company may become involved in intellectual property disputes that could cause it to incur substantial costs, divert the efforts of management or require it to pay substantial damages or licensing fees.

From time to time, the Company receives notifications alleging infringements of intellectual property rights allegedly held by others relating to the Company's business or the products or services it sells. Litigation with respect to patents or other intellectual property matters could result in substantial costs and diversion of management and other resources and could have an adverse effect on the Company's operations. Further, the Company may be obligated to indemnify and defend its customers if the products or services the Company sells are alleged to infringe any third-party's intellectual property rights. While the Company may be able to seek indemnification from its suppliers for itself and its customers against such claims, there is no assurance that it will be successful in obtaining such indemnification or that the Company will be fully protected against such claims. If an infringement claim is successful, the Company may be required to pay damages or seek royalty or license arrangements, which may not realizebe available on commercially reasonable terms. The Company may have to stop selling certain products or services, which could affect its ability to compete effectively.

Failure to comply with the requirements of environmental regulations could adversely affect its business.

The Company is subject to various federal, state, local and foreign laws and regulations addressing environmental and other impacts from product disposal, use of hazardous materials in products, recycling of products at the end of their useful life and other related matters. While the Company strives to ensure it is in full compliance with all applicable regulations, certain of these regulations impose liability without fault. Additionally, the Company may be held responsible for the prior activities of an entity it acquired. Failure to comply with these regulations could result in substantial costs, fines and civil or criminal sanctions, as well as third-party claims for property damage or personal injury. Further, environmental laws may become more stringent over time, imposing greater compliance costs and increasing risks and penalties associated with violations.

Tax legislation initiatives or challenges to the Company's tax positions could impact the Company's results of operations and financial condition.

As a multinational corporation, the Company is subject to the tax laws and regulations of the anticipated benefits from its acquisitions, whichUnited States federal, state and local governments and of many international jurisdictions. From time to time, legislation may be enacted that could materially and adversely affect the Company’s financial performance.Company's tax positions. There can be no assurance that our effective tax rate and the resulting cash flow will not be adversely affected by these potential changes in regulations. The tax laws and regulations of the various countries where the Company has operations are extremely complex and subject to varying interpretations. Although the Company believes that its historical tax positions are sound and consistent with applicable laws, regulations and existing precedent, there can be no assurance that these tax positions will not be challenged by relevant tax authorities or that the Company would be successful in any such challenge.

If the Company fails to maintain effective internal controls, it may not be able to report its financial results accurately or timely or prevent or detect fraud, which could have a material adverse effect on the Company’s business or stock price.the market price of the Company's securities.

Effective internal controls are necessary for the Company to provide reasonable assurance with respect to its financial reports and to effectively prevent or detect fraud. If the Company cannot provide reasonable assurance with respect to its financial reports and effectively prevent or detect fraud, its brand and operating results could be harmed. Pursuant to the Sarbanes-Oxley Act of 2002, the Company is required to furnish a report by management on internal control over financial reporting, including management’smanagement's assessment of the effectiveness of such control. Internal control over financial reporting may not prevent or detect misstatements because of its inherent limitations, including the possibility of human error, the circumvention or overriding of controls, or fraud. Therefore, even effective internal controls cannot provide absolute assurance with respect to the preparation and fair presentation of financial statements. In addition, projections of any evaluation of effectiveness of internal control over financial reporting to future periods are subject to the risk that the control may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. If the Company fails to maintain the adequacy of its internal controls, including any failure to implement required new or improved controls, or if the Company experiences difficulties in their implementation, the Company’sCompany's business and operating results could be harmed, and the Company could fail to meet its reporting obligations, which could have a material adverse effect on its business andor the market price of the Company’sCompany's securities.

If the Company’s internal information systems fail to function properly, or if the Company is unsuccessful in the integration or upgrade11

The Company’s expanding operations put increasing pressure on the Company’s information systems to produce timely, accurate and reliable reports on financial and operational results. Currently, the Company’s global operations are tracked with multiple information systems, some of which are subject to on-going IT projects designed to streamline or optimize its global information systems. There is no guarantee that the Company will be successful at all times in these efforts or that there will not be integration difficulties that will adversely affect the Company’s operations or the accurate and timely recording and reporting of financial data. In addition, these systems are subject to computer hacking or other general system failure. Maintaining and operating these systems requires continuous investments. Failure of any of these information systems or material difficulties in upgrading these information systems could have material adverse effects on the Company’s business and its compliance with reporting obligations under federal securities laws.

10

Major disruptions to the Company’s logistics capability could have a material adverse impact on the Company’s operations.

The Company’s global logistics services are operated through specialized and centralized distribution centers around the globe. The Company also depends almost entirely on third party transportation service providers for the delivery of products to its customers. A major interruption or disruption in service at one or more of our distribution centers for any reason (such as natural disasters, pandemics, or significant disruptions of services from our third party providers) could cause cancellations or delays in a significant number of shipments to customers and, as a result, could have a severe impact on the Company’s business, operations and financial performance.

The Company may not have adequate or cost-effective liquidity or capital resources.

The Company’s ability to satisfy its cash needs depends on its ability to generate cash from operations and to access the financial markets, both of which are subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond the Company’s control.

The Company may need to satisfy its cash needs through external financing. However, external financing may not be available on acceptable terms or at all. As of July 2, 2011, Avnet had total debt outstanding of $1.517 billion under various notes and committed and uncommitted lines of credit with financial institutions. The Company needs cash to make interest payments on, and to refinance, this indebtedness and for general corporate purposes, such as funding its ongoing working capital and capital expenditure needs. Under the terms of any external financing, the Company may incur higher than expected financing expenses and become subject to additional restrictions and covenants. Any material increase in the Company’s financing costs could have a material adverse effect on its profitability.

Under some of its credit facilities, the Company is required to maintain certain specified financial ratios and meet certain tests. If the Company fails to meet these financial ratios and tests, it may be unable to continue to utilize these facilities. If the Company is unable to utilize these facilities, it may not have sufficient cash available to make interest payments on and refinance indebtedness and for general corporate needs.

The agreements governing some of the Company’s financings contain various covenants and restrictions that limit the discretion of management in operating its business and could prevent us from engaging in some activities that may be beneficial to the Company’s business.

The agreements governing the Company’s financing, including its credit facility and the indentures governing the Company’s outstanding notes, contain various covenants and restrictions that, in certain circumstances, limit the Company’s ability and the ability of certain subsidiaries to:

grant liens on assets;Contents

make restricted payments (including paying dividends on capital stock or redeeming or repurchasing capital stock);

merge, consolidate or transfer all or substantially all of the Company’s assets;

incur additional debt; or

engage in certain transactions with affiliates.

As a result of these covenants and restrictions, the Company may be limited in the future in how it conducts its business and may be unable to raise additional debt, compete effectively or make further investments.

In addition to the specific factors described above, general economic or business conditions, domestic and foreign, may be less favorable than management expected and, if such conditions persist for a sustained period of time, could eventually adversely impact the Company’s sales or its ability to collect receivables from some of its customers.

11

| | |

Item 1B. | | Unresolved Staff Comments

|

Item 1B. Unresolved Staff CommentsNot applicable.

Item 2. Properties

The Company owns and leases approximately 1,151,0001,558,000 and 5,523,0006,391,000 square feet of space, respectively, of which approximately 36%42% is located in the United States. The following table summarizes certain of the Company’s key facilities.

| | | | | | | | |

| | Sq. | | | Leased or | | |

| Location | | Sq. Footage | | | Leased or Owned | | Primary Use |

| Poing, Germany | | 423,000 | 427,000 |

| | Leased | | EM warehousing, value-added operations and offices |

| Chandler, Arizona | | | 399,000 |

| | Owned | | EM warehousing and value-added operations |

| Tongeren, Belgium | | | 388,000 |

| | Owned | | EM and TS warehousing and value-added operations |

Chandler, ArizonaGrove City, Ohio | | 297,000 | 231,000

| | Leased | | EM warehousing, integration and value-added operations |

| Poing, Germany | | 296,000 |

| | Owned | | EM warehousing, value-added operations and offices |

| Groveport, Ohio | | 266,000 |

| | Leased | | TS warehousing, integration and value-added operations |

Tsuen Wan, Chandler, Arizona | | 231,000 |

| | Leased | | EM warehousing, integration and value-added operations |

| Atlanta, Georgia | | 195,000 |

| | Leased | | TS warehousing, integration and value-added operations |

| Hong Kong, | China | | 181,000 |

| | Leased | | EM warehousing and value-added operations |

| Phoenix, Arizona | | | 176,000 |

| | Leased | | Corporate and EM headquarters |

| Coppell, Texas | | 174,000 |

| | Leased | | EM warehousing, integration and value-added operations |

| Nettetal, Germany | | 137,000 |

| | Owned | | EM warehousing, value-added operations and offices |

| Tempe, Arizona | | | 132,000 |

| | Leased | | TS headquarters |

| Nettetal, Germany | | 126,000 |

| | Owned | | TS warehousing, value-added operations and offices |

| Nogales, Mexico | | | 124,000 |

| | Leased | | EM warehousing and value-added operations |

Doral, Florida | | | 120,000 | | | Leased | | TS warehousing and value-added operations |

Loyang, Singapore | | | 116,000 | | | Leased | | TS warehousing and value-added operations |

| | |

Item 3. | | Item 3. Legal Proceedings |

As a result primarily of certain former manufacturing operations, Avnet has incurred and may have future liability under various federal, state and local environmental laws and regulations, including those governing pollution and exposure to, and the handling, storage and disposal of, hazardous substances. For example, under the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended (“CERCLA”) and similar state laws, Avnet is and may be liable for the costs of cleaning up environmental contamination on or from certain of its current or former properties, and at off-site locations where the Company disposed of wastes in the past. Such laws may impose joint and several liability. Typically, however, the costs for cleanup at such sites are allocated among potentially responsible parties based upon each party’s relative contribution to the contamination, and other factors.

Pursuant to SEC regulations, including but not limited to Item 103 of Regulation S-K, the Company regularly assesses the status of and developments in pending environmental legal proceedings to determine whether any such proceedings should be identified specifically in this discussion of legal proceedings, and has concluded that no particular pending environmental legal proceeding requires public disclosure. Based on the information known to date, management believes that the Company has appropriately accrued in its consolidated financial statements for its share of the estimated costs associated with theof environmental clean-up of sites in which the Company is participating.matters.

The Company and/or its subsidiaries areis also partiesparty to various other lawsuits, claims, investigations and other legal proceedings arising from time to time in the normal course of business. While litigation is subject to inherent uncertainties, management currently believes that the ultimate outcome of these proceedings, individually and in the aggregate, will not have a material adverse effect on the Company’s financial position, cash flowliquidity or results of operations.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

| | |

Item 5. | | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

Market price per share

The Company’s common stock is listed on the New York Stock Exchange under the symbol AVT. Quarterly high and low sales closing prices (as reported for the New York Stock Exchange composite transactions) for the last two fiscal years were:

| | | | | | | | | | | | | | | | | |

| | | 2011 | | | 2010 | |

| Fiscal Quarters | | High | | | Low | | | High | | | Low | |

| 1st | | $ | 27.08 | | | $ | 22.86 | | | $ | 27.33 | | | $ | 20.31 | |

| 2nd | | | 33.34 | | | | 26.61 | | | | 30.42 | | | | 23.67 | |

| 3rd | | | 36.97 | | | | 31.88 | | | | 30.53 | | | | 26.35 | |

| 4th | | | 37.81 | | | | 29.97 | | | | 33.49 | | | | 23.93 | |

|

| | | | | | | | | | | | | | | |

| | 2013 | | 2012 |

| Fiscal Quarters | High | | Low | | High | | Low |

| 1st | $ | 33.51 |

| | $ | 28.91 |

| | $ | 32.86 |

| | $ | 24.19 |

|

| 2nd | 31.62 |

| | 27.01 |

| | 31.73 |

| | 24.77 |

|

| 3rd | 36.86 |

| | 30.61 |

| | 36.83 |

| | 31.02 |

|

| 4th | 35.39 |

| | 31.54 |

| | 36.65 |

| | 29.23 |

|

The Company hasdid not paidpay any dividends sinceon its common stock during the last two fiscal 2002years. Any future decision to declare or pay dividends will be at the discretion of the Board of Directors and does not currently contemplate any future dividend payments.will be dependent upon the Company's financial condition, results of operations, capital requirements, and such other factors as the Board of Directors deems relevant. In addition, certain of the Company's debt facilities contain restrictions on the declaration and payment of dividends.

Record Holders

As of July 29, 2011,26, 2013, there were 3,1523,330 registered holders of record of Avnet’s common stock.

Equity Compensation Plan Information as of July 2, 2011

| | | | | | | | | | | | |

| | | | | | | | | | | Number of Securities | |

| | | Number of Securities | | | | | | | | Remaining Available for | |

| | | to be Issued Upon | | | | Weighted-Average | | | Future Issuance Under Equity | |

| | | Exercise of | | | | Exercise Price of | | | Compensation Plans | |

| | | Outstanding Options, | | | | Outstanding Options, | | | (Excluding Securities | |

| Plan Category | | Warrants and Rights | | | | Warrants and Rights | | | Reflected in Column (a)) | |

| | | (a) | | | | (b) | | | (c) | |

| Equity compensation plans approved by security holders | | 5,320,709 | (1) | | | $ | 21.79 | | | 6,694,816 | (2) |

|

| | | | | | | | |

| Plan Category | Number of Securities

to be Issued Upon

Exercise of

Outstanding Options, Warrants and Rights | | Weighted-Average

Exercise Price of

Outstanding Options, Warrants and Rights | | Number of Securities

Remaining Available for

Future Issuance Under Equity

Compensation Plans

(Excluding Securities Reflected in Column (a)) | |

| | (a) | | (b) | | (c) | |

| Equity compensation plans approved by security holders | 5,559,753 |

| (1) | $26.65 | | 2,995,588 |

| (2) |

______________________

| | |

| (1) | | Includes 3,059,2152,579,188 shares subject to options outstanding and 1,414,7842,009,510 stock incentive shares and 846,710971,055 performance shares awarded but not yet delivered. Included in the performance shares is the number of shares anticipated to be issued in the first quarter of fiscal 20122014 relating to the level of achievement reached under the 2009 performance share program, whichthat ended July 2, 2011on June 29, 2013 (see Note 12 in theNotes to Consolidated Financial Statementsincluded in Item 15 of this Report) |

| |

|

| (2) | | Does not include 58,707432,789 shares available for future issuance under the Employee Stock Purchase Plan, which is a non-compensatory plan. |

13

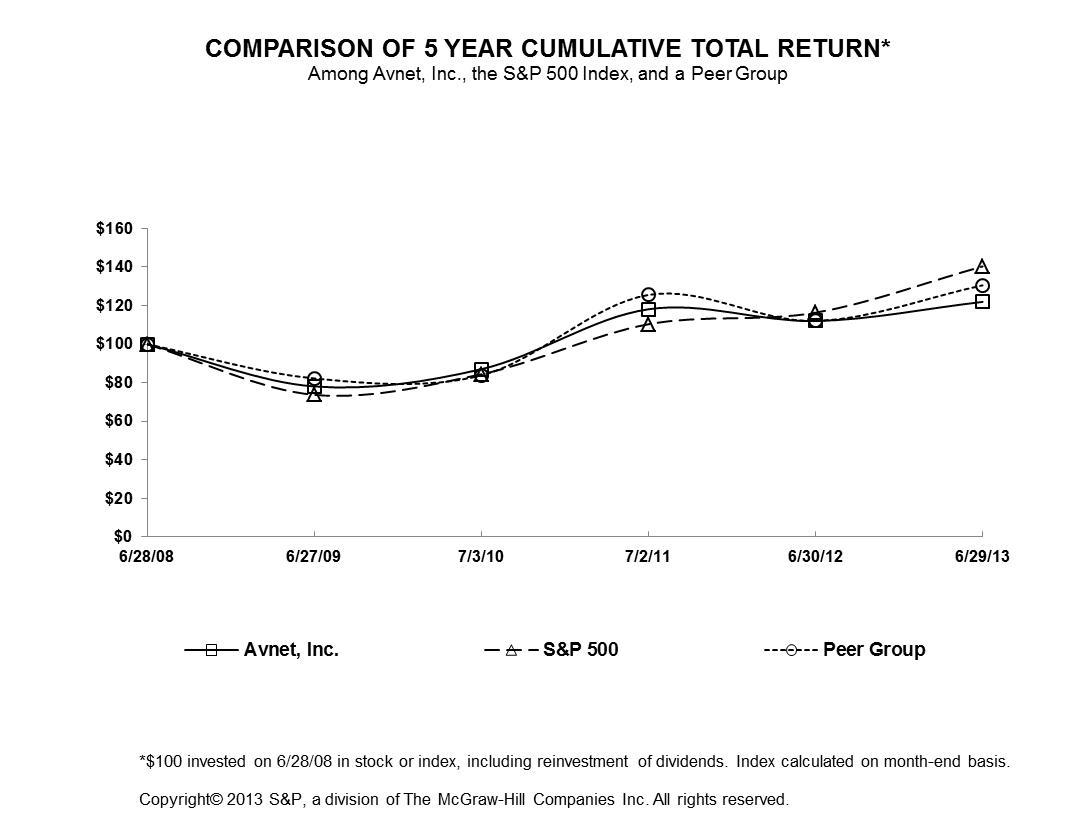

Stock Performance Graphs and Cumulative Total Returns

The graph below compares the cumulative 5-year total return of holders of Avnet, Inc.’s common stock with the cumulative total returns of the S&P 500 index and certain of Avnet’s peer companies in the electronics distribution industry. The graph tracks the performance of a $100 investment in Avnet’s common stock, in the peer group, and the index (with the reinvestment of all dividends) from July 1, 2006June 28, 2008 to July 2, 2011. During fiscal 2011, two ofJune 29, 2013. The companies comprising the companies included in the Company’s fiscal 2010 peer group (Bell Microproducts Inc. and Nu Horizons Electronics Corp) terminated their respective registrations with the SEC. The Company’s new peer group consists ofthat Avnet has historically used are: Agilysys, Inc., Anixter International, Inc., Arrow Electronics, Inc., Brightpoint, Inc., Ingram Micro, Inc., Insight Enterprises, Inc., Scansource, Inc., Synnex Corp. and Tech Data Corp. The Company’s old peer group, whichBrightpoint, Inc. terminated its registration with the SEC as a result of it being acquired and, therefore, is also included below for comparative purposes, consisted of Arrow Electronics, Inc., Ingram Micro, Inc., and Tech Data Corp. Bell Microproducts Inc. and Nu Horizons Electronics Corp are not included in the old peer groupgraph below.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 07/1/06 | | 06/30/07 | | 06/28/08 | | 06/27/09 | | 07/3/10 | | 07/2/11 | | 6/28/2008 | | 6/27/2009 | | 7/3/2010 | | 7/2/2011 | | 6/30/2012 | | 6/29/2013 |

| Avnet, Inc. | | 100.00 | | 198.00 | | 137.61 | | 107.49 | | 119.78 | | 162.59 | | 100.00 | | 78.11 | | 87.04 | | 118.15 | | 112.01 | | 121.96 |

| S&P 500 | | 100.00 | | 120.59 | | 104.77 | | 77.30 | | 88.46 | | 115.61 | | 100.00 | | 73.79 | | 84.43 | | 110.35 | | 116.36 | | 140.32 |

| Old Peer Group | | 100.00 | | 115.02 | | 94.26 | | 80.93 | | 79.40 | | 119.43 | | |

| New Peer Group | | 100.00 | | 120.11 | | 94.66 | | 78.10 | | 79.95 | | 118.59 | | |

| Peer Group | | 100.00 | | 82.26 | | 83.84 | | 125.55 | | 112.07 | | 130.55 |

The stock price performance included in this graph is not necessarily indicative of future stock price performance. The Company does not make or endorse any predictions as to future stock performance. The performance graph is furnished solely to accompany this Report and is not being filed for purposes of the Securities Exchange Act of 1934, as amended, and is not to be incorporated by reference into any filing of the Company, whether made before or after the date hereof, regardless of any general incorporation language in such filing.

14

Issuer Purchases of Equity Securities

In August 2011, the Company's Board of Directors (the "Board") approved the repurchase of up to $500.0 million of the Company's common stock through a share repurchase program. During August 2012, the Board approved an additional $250.0 million for the share repurchase program. With this increase, the Company may repurchase up to a total of $750.0 million of the Company's common stock under the share repurchase program. The following table presentsincludes, if any, the Company’sCompany's monthly purchases of Avnet's common stock during the fourth quarter ended June 29, 2013 under the share repurchase program, which is

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Maximum Number (or | |

| | | | | | | | | | | Total Number of | | | Approximate Dollar | |

| | | Total | | | | | | | Shares Purchased as | | | Value) of Shares That | |

| | | Number of | | | | | | | Part of Publicly | | | may yet be Purchased | |

| | | Shares | | | Average Price | | | Announced Plans or | | | Under the Plans or | |

| Period | | Purchased | | | Paid per Share | | | Programs | | | Programs | |

| April | | | 4,100 | | | $ | 34.80 | | | | — | | | | — | |

| May | | | 6,700 | | | $ | 37.07 | | | | — | | | | — | |

| June | | | 4,300 | | | $ | 31.74 | | | | — | | | | — | |

The purchasespart of Avnet common stock noted above werea publicly announced plan, and purchases made on the open market to obtain shares for purchase under the Company’sCompany's Employee Stock Purchase Plan.Plan (“ESPP”), which is not part of a publicly announced plan:

In August 2011, the Board of Directors approved the repurchase of up to an aggregate of $500 million of shares of the Company’s common stock through a share repurchase program. The Company plans to repurchase stock from time to time at the discretion of management in open market or privately negotiated transactions or otherwise, subject to applicable laws, regulations and approvals, strategic considerations, market conditions and other factors. The Company may terminate or limit the stock repurchase program at any time without prior notice. |

| | | | | | | | | | |

| Period | | Total Number of Shares Purchased(1) | | Average Price Paid per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | | Approximate Dollar Value of Shares That May Yet Be Purchased Under the Plans or Programs |

| | | |

| April | | 5,600 |

| | $33.86 | | — |

| | $224,475,000 |

| May | | 5,500 |

| | $32.82 | | — |

| | $224,475,000 |

| June | | 4,400 |

| | $33.05 | | — |

| | $224,475,000 |

______________________

| | |

Item 6.(1) | | Selected Financial Data

Consists entirely of purchases of Avnet’s common stock associated with the Company’s ESPP. |

Item 6. Selected Financial Data

| | | | | | | | | | | | | | | | | | | | | |

| | | Years Ended | |

| | | July 2, | | | July 3, | | | June 27, | | | June 28, | | | June 30, | |

| | | 2011 | | | 2010 | | | 2009 (a) | | | 2008 (a) | | | 2007 (a) | |

| | | (Millions, except for per share and ratio data) | |

| Income: | | | | | | | | | | | | | | | | | | | | |

| Sales | | $ | 26,534.4 | | | $ | 19,160.2 | | | $ | 16,229.9 | | | $ | 17,952.7 | | | $ | 15,681.1 | |

| Gross profit | | | 3,107.8 | | | | 2,280.2 | | | | 2,023.0 | | | | 2,313.7 | | | | 2,048.6 | |

| Operating income (loss) | | | 930.0 | (b) | | | 635.6 | (c) | | | (1,019.0 | )(d) | | | 710.8 | (e) | | | 678.7 | (f) |

| Income tax provision | | | 201.9 | (b) | | | 174.7 | (c) | | | 34.7 | (d) | | | 203.8 | (e) | | | 187.9 | (f) |

| Net income (loss) | | | 669.1 | (b) | | | 410.4 | (c) | | | (1,129.7 | )(d) | | | 489.6 | (e) | | | 384.4 | (f) |

| Financial Position: | | | | | | | | | | | | | | | | | | | | |

| Working capital(g) | | | 3,749.5 | | | | 3,190.6 | | | | 2,688.4 | | | | 3,191.3 | | | | 2,711.2 | |

| Total assets | | | 9,905.6 | | | | 7,782.4 | | | | 6,273.5 | | | | 8,195.2 | | | | 7,343.7 | |

| Long-term debt | | | 1,273.5 | | | | 1,243.7 | | | | 946.6 | | | | 1,169.3 | | | | 1,127.9 | |

| Shareholders’ equity | | | 4,056.1 | | | | 3,009.1 | | | | 2,760.9 | | | | 4,141.9 | | | | 3,417.4 | |

| Per Share: | | | | | | | | | | | | | | | | | | | | |

| Basic earnings (loss) | | | 4.39 | (b) | | | 2.71 | (c) | | | (7.49 | )(d) | | | 3.26 | (e) | | | 2.60 | (f) |