CHARGE-OFF

DERIVATIVE

GOODWILL

YIELD

•LIST OF ABBREVIATIONS AND ACRONYMSconditions in the securities markets and real estate markets or the banking industry;

| Business |

| ||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

PART I

ITEM 1. BUSINESS

General

(ii) New York Community Bank

Established in 1859, was merged with and into Flagstar Bank N.A., with Flagstar Bank N.A. continuing as the Bank is a surviving entity.

We are a leading producer of multi-family loans inthe New York City market area, where it specializes in rent-regulated, non-luxury apartment buildings. Flagstar Mortgage is the 7th largest bank originator of residential mortgages for the 12-months ended December 31, 2023, while we are the industry’s 5th largest sub-servicer of mortgage loans nationwide, servicing 1.4 million accounts with an emphasis$382.2 billion in unpaid principal balances as of December 31, 2023. Additionally, the Company is the 2nd largest mortgage warehouse lender nationally based on non-luxury residential apartment buildings with rent-regulated units that feature rents that are below non-regulated units. In addition to multi-family loans, which are our principal asset, we originate CRE loans (primarily in New York City), specialty finance loans and leases, and, to a much lesser extent, ADC loans, and C&I loans (typically made to small and mid-size business in Metro New York).total commitments.

Our current market for deposits consists of the 26 counties

9

The combined population of the 26 counties where our branches are located is approximately 31.7 million, and the number of banks and thrifts we compete with currently exceeds 350. With total deposits of $35.1 billion at December 31, 2021, we ranked in the top 20 among all bank and thrift depositories serving these 26 counties. We also ranked third among all banks and thrifts in Richmond County in New York, fifth among all banks and thrifts in Queens County in New York, and second among all banks and thrifts in Nassau County in New York (market share information was provided by S&P Global Market Intelligence).

One of our competitive advantages is our strong community presence and commitment to providing a high level of customer service in each of our markets. In 2021, the Bank was named the number one bank in the country for best overall customer experience based on a survey conducted by American Banker and creative experience firm Monigle.

10

finance loans that we originate are sourced from larger financial institutions who have many customers for these loans. Some of these customers are larger and have more capital and liquidity than the Company.

While

11

The 11Parent Company also has four direct subsidiaries of the(including Flagstar Bank, are:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The eight subsidiaries of Bank-owned entities are:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

N.A). NYB Realty Holding Company, LLC, a subsidiary of the Bank, owns interests in ten10 additional active entities organized as indirect wholly-owned subsidiaries to own interests in various real estate properties.

12

The health and safety of our employees is also of critical importance. In response to the ongoing COVID-19 pandemic, we have implemented a flexible response plan that includes the transitioning of certain back office employees to a remote work model, as conditions warrant while implementing additional safety protocols for employees who, due to the nature of their positions, continue to work on-site. We maintain strict compliance with federal, state and local requirements that enhance workplace safety, such as masking and social distancing, and we provide employees who either contract or are exposed to COVID-19 with appropriate leave.

Federal Reserve. The Bank is requiredalso subject to file reports with the NYSDFS,supervision of the CFPB, which regulates the offering and provision of consumer financial products or services under federal consumer financial laws. The OCC, FDIC and the CFPB concerning itsmay take regulatory enforcement actions if we do not operate in accordance with applicable regulations, policies and directives. Proceedings may be instituted against us, or any "institution-affiliated party", such as a director, officer, employee, agent or controlling person, who engages in unsafe and unsound practices, including violations of applicable laws and regulations. The FDIC has additional authority to terminate insurance of accounts, if after notice and hearing, we are found to have engaged in unsafe and unsound practices, including violations of applicable laws and regulations. The federal system of regulation and supervision establishes a comprehensive framework of activities and financial condition,in which to operate and is periodically examined byprimarily intended for the NYSDFS, the FDIC,protection of depositors and the CFPB to assess compliance with various regulatory requirements, including with respect to safety and soundness and consumer financial protection regulations. The regulatory structure gives the regulatory authorities extensive discretion in connection with their supervisory and enforcement activities and examination policies, including policies with respect to the classificationFDIC's DIF rather than our shareholders.

of assets and the establishment of an adequate allowance for credit losses on loans and leases for regulatory purposes. Changes in such regulations or in banking legislation could have

The Company is subject to examination, regulation, and periodic reporting under the Bank Holding Company Act of 1956, as amended (the “BHCA”) by the FRB. Furthermore, the Company would be required to obtain the prior approval of the FRB to acquire all, or substantially all, of the assets of any bank or bank holding company.

In addition, the Company is periodically examined by the FRB-NY, and iscompany, we are required to file certain reports under, and otherwise comply with the rules and regulations of the SEC underFederal Reserve. We are required to file certain reports, and we are subject to examination by, and the enforcement authority of, the Federal Reserve. Under the federal securities laws. Certainlaws, we are also subject to the rules and regulations of the regulatory requirements applicableSEC.

On June 14,

14

15

the Capital section of the MD&A and Note 17 - Capital. As of December 31, 2021,2023, each of the Bank’s capital ratios exceeded those required for an institution to be considered “well capitalized” under these regulations.

the preceding two calendar years, less any required transfer to paid-in capital. The FDIC has authorityterm “net profits” is defined as net income for a given period less any dividends paid during that period. As a result of our acquisition of Flagstar, we are also required to use its enforcement powers to prohibit a savings bank or commercial bankseek regulatory approval from paying dividends if, in its opinion,the OCC for the payment of any dividend to the Parent Company through at least the period ending November 1, 2024. In 2023, dividends would constitute an unsafe or unsound practice. Federal law prohibitsof $580 million were paid by the paymentBank to the Parent Company.

Investment Activities

Since the enactment of the FDICIA, all state-chartered financial institutions, including savings banks, commercial banks,OCC's regulations in conducting such investment activities. A bank must consider, as appropriate, the interest rate, credit, liquidity, price, foreign exchange, transaction, compliance, strategic, and their subsidiaries, have generally been limitedreputation risks presented by a proposed activity, and the particular activities undertaken by the bank must be appropriate for that bank. If the OCC determines for safety and soundness reasons that a bank should calculate its investment limits more frequently than required by the OCC's Investment Securities regulations, the OCC may provide written notice to such activities as principalthe bank

17

In 1993,

Enforcement

The FDIC has extensive enforcement authority over insured banks, includingof the Bank. ThisFederal Reserve. The enforcement authority of these regulatory agencies includes, among other things, the ability to assess civil money penalties, to issue cease and desist orders, and to remove directors and officers. In general, these enforcement actions may be initiated in response to violations of laws and regulations and unsafe or unsound practices.

We expect an increase in special assessment expense, which is not expected to be material, on or around June 2024 based on the FDIC’s modified loss estimate.

The Company is currently subject to examination, regulation, and periodic reporting under the BHCA, as administered by the FRB.

FRB regulations generally prohibitacquiring us if that company is engaged directly or indirectly in activities that are not permissible for a bank holding company from engagingor financial holding company.

18

The FRB has issued a policy statement regardingOCC for the payment of dividends by bank holding companies. In general, the FRB’s policies provide that dividends should be paid only out of current earnings, and only if the prospective rate of earnings retention by the bank holding company appears consistent with the organization’s capital needs, asset quality, and overall financial condition. The FRB’s policies also require that a bank holding company serve as a source of financial strength to its subsidiary bank by standing ready to use available resources to provide adequate capital fundsany dividend to the bank during periods of financial stress or adversity, and by maintainingParent Company through at least the financial flexibility and capital-raising capacity to obtain additional resources for assisting its subsidiary bank where necessary.

Under FRB regulations, banks must adopt and maintain written policies that establish appropriate limits and standards for extension of credit secured by liens or interests in real estate or are made for the purpose of financing permanent improvements to real estate. These policies must establish loan portfolio diversification standards; prudent underwriting standards, including loan-to-value limits that are clear and measurable; loan administration procedures; and documentation, approval, and reporting requirements. A bank's real estate lending policy must reflect consideration of the Interagency Guidelines for Real Estate Lending Policies (the "Interagency Guidelines") adopted by the federal bank regulators. The Interagency Guidelines, among other things, call for internal loan-to-value limits for real estate loans that are not in excess of the limits specified in the guidelines. The Interagency Guidelines state, however, that it may be appropriate in individual cases to originate or purchase loans with loan-to-value ratios in excess of the supervisory loan-to-value limits.

Interchange fees, or "swipe" fees, are fees that merchants pay to credit card companies and debit card-issuing banks such as the Bank for processing electronic payment transactions on their behalf. The maximum permissible interchange fee that a non-exempt issuer may receive for an electronic debit transaction is the sum of 21 cents per transaction and five bps multiplied by the value of the transaction, subject to an upward adjustment of one cent if an issuer certifies that it has implemented policies and procedures reasonably designed to achieve the fraud-prevention standards set forth by the FRB. In addition, card issuers and networks are prohibited from entering into agreements requiring that debit card transactions be processed on a single network or only two affiliated networks, and allows merchants to determine transaction routing.

The DFA codified the source of financial strength policy and required regulations to facilitate its application. Under the prompt corrective action laws, theperiod ending November 1, 2024, which could restrict our ability of a bank holding company to pay dividends may be restricted if a subsidiary bank becomes undercapitalized. These regulatory policies could affect the ability of the Company to pay dividends or otherwise engage in capital distributions.common stock dividend.

19

New York State Regulation

The Bank is also subject to provisions of the New York State Banking Law that impose continuing and affirmative obligations upon a banking institution organized in New York State to servemeeting the credit needs of the community and to take such record into account in its local community. Such obligations are substantially similar to those imposedevaluation of certain applications by the CRA.institution, including applications for charters, branches and other deposit facilities, relocations, mergers, consolidations, acquisitions of assets or assumptions of liabilities, and bank holding company and savings and loan holding company acquisitions. The latest New York State CRA rating receivedalso requires that all institutions make public disclosure of their CRA ratings.

Federal

activities. The Financial Crimes Enforcement Network ("Fin CEN"), a bureau of the U.S. Treasury, has the authority to implement, administer, and enforce compliance with the USA PATRIOTPatriot Act requires banks and other BSA legislation. Fin CEN has adopted regulations that require financialdepository institutions, brokers, dealers and certain other businesses involved in the transfer of money to among other things, obtain beneficial ownership information with respect to legal entities with which such institutions conduct business, subject to certain exemptions and exclusions.

The Anti-Money Laundering Act of 2020 ("AMLA"), which amends the BSA, was enacted in January 2021. The AMLA is intended to comprehensively reform and modernize U.S. bank secrecy andestablish anti-money laundering laws. Among other things, it codifiesprograms, including employee training and independent audit requirements meeting minimum standards specified by the Patriot Act, to follow standards for customer identification and maintenance of customer identification records, and to compare customer lists against lists of suspected terrorists, terrorist organizations and money launderers. The Patriot Act also requires federal bank regulators to evaluate the effectiveness of an applicant in combating money laundering in determining whether to approve a risk-based approach toproposed bank acquisition.

20

by prohibiting transfers of property subject to U.S. jurisdiction (including property in the possession or control of U.S. persons). Blocked assets (e.g., property and bank deposits) cannot be paid out, withdrawn, set off, or transferred in any manner without a license from OFAC. Failure to comply with these sanctions could have serious legal and reputational consequences.

New York State Law

The Bank derives its lending, investment,stock and other authority primarily from the applicable provisions$329 million of New York State Banking Law and the regulations of the NYSDFS, as limited by FDIC regulations. Under these laws and regulations, banks, including the Bank, may invest in real estate mortgages, consumer and commercial loans, certain types of debt securities (including certain corporate debt securities, and obligations of federal, state, and local governments and agencies), certain types of corporate equity securities, and certain other assets.FHLB-Indianapolis shares.

New York State Banking Law gives the Superintendent authority to issue an order to a New York State-chartered banking institution to appear and explain an apparent violation of law, to discontinue unauthorized or unsafe practices, and to keep prescribed books and accounts. Upon a finding by the NYSDFS that any director, trustee, or officer of any banking organization has violated any law, or has continued unauthorized or unsafe practices in conducting the business of the banking organization after having been notified by the Superintendent to discontinue such practices, such director, trustee, or officer may be removed from office after notice and an opportunity to be heard. The

21

Superintendent also has authority to appoint a conservator or a receiver for a savings or commercial bank under certain circumstances.

Interstate Branching

Federal law allows the FDIC, and New York State Banking Law allows the Superintendent, to approve an application by a state banking institution to acquire interstate branches by merger, unless, in the case of the FDIC, the state of the target institution has opted out of interstate branching. New York State Banking Law authorizes savings banks and commercial banks to open and occupy de novo branches outside the state of New York. Pursuant to the DFA, the FDIC is authorized to approve a state bank’s establishment of a de novo interstate branch if the intended host state allows de novo branching by banks chartered by that state. The Bank currently maintains 40 branches in New Jersey, 26 branches in Florida, 28 branches in Ohio, and 14 branches in Arizona, in addition to its 129 branches in New York State.

Acquisition of the Holding Company

Federal Restrictions

Under the Federal Change in Bank Control Act (“CIBCA”), a notice must be submitted to the FRB if any person (including a company), or group acting in concert, seeks to acquire 10% or more of the Company’s shares of outstanding common stock, unless the FRB has found that the acquisition will not result in a change in control of the Company. Under the CIBCA, the FRB generally has 60 days within which to act on such notices, taking into consideration certain factors, including the financial and managerial resources of the acquirer; the convenience and needs of the communities served by the Company, the Bank; and the anti-trust effects of the acquisition. Under the BHCA, any company would be required to obtain approval from the FRB before it may obtain “control” of the Company within the meaning of the BHCA. Control generally is defined to mean the ownership or power to vote 25% or more of any class of voting securities of the Company, the ability to control in any manner the election of a majority of the Company’s directors, or the power to exercise a controlling influence over the management or policies of the Company. Under the BHCA, an existing bank holding company would be required to obtain the FRB’s approval before acquiring more than 5% of the Company’s voting stock. See “Holding Company Regulation” earlier in this report.

New York State Change in Control Restrictions

New York State Banking Law generally requires prior approval of the New York State Banking Board before any action is taken that causes any company to acquire direct or indirect control of a banking institution which is organized in New York.

22

Information (Regulation P), Margin Stock Loans (Regulation U), Right To Financial Privacy Act, Flood Disaster Protection Act, Homeowners Protection Act, Servicemembers Civil Relief Act, Real Estate Settlement Procedures Act (Regulation X), Telephone Consumer Protection Act, CAN-SPAM Act, Children’s Online Privacy Protection Act, the Military Lending Act, and the Homeownership Counseling Act. Additionally, we are subject to Section 5 of the Federal Trade Commission Act, which prohibits unfair and deceptive acts or practices in or affecting commerce, and Section 1031 of the Dodd-Frank Act, which prohibits unfair, deceptive, or abusive acts or practices (“UDAAP”) in connection with any consumer financial product or service.

President Biden's Executive Order on Promoting Competition in CFPB Interpretive Rule regarding Section 1042 of the American EconomyConsumer Financial Protection Act of 2010 (87 FR 31940, May 26, 2022).

Current Operating Environment

COVID-19 Pandemic

The Company's business, financial condition, and results of operation have been and may continue to be affected by the outbreak of COVID-19. Both globally and within the United States, the pandemic continues to have various effects on economic and commercial activity and financial markets, both nationally and locally. Due to its high rate of contagion and mortality, state and local governments enacted numerous safeguards to contain the spread of the virus. These included, the shut-down of all businesses considered to be “non-essential,” restrictions on gatherings, social distancing requirements were put in place. Businesses continue to observe and modify their activities and behaviors to remain in compliance with the jurisdictional directives while concurrently providing consumers with goods and services. Certain actions taken by U.S. or other governmental authorities, including the Federal Reserve, that are intended to ameliorate the macroeconomic effects of COVID-19 may adversely impact our business.

The concentration and severity of COVID-19 infection in the New York City metro region, during the early stages of the pandemic, led it to be considered the epicenter of the pandemic in the country. This region is also the Company’s largest service area, having over 100 branches and 72% of the loan portfolio.

The Company has been very proactive throughout all stages of the pandemic, supporting employees, customers, and its communities. As an essential business, the Company implemented business continuity plans and continued to provide our financial services to customers, while taking health and safety measures into account.

In response to the pandemic and to ensure that the Company’s operations, during the term of the pandemic runs smoothly, senior management formed two committees: the COVID-19 Resiliency Committee and the COVID-19 Lending Committee. The COVID-19 Resiliency Committee meets as needed and is primarily focused on operational issues including employee safety and well-being, branch closings, PPE procurement, IT sustainability, and continuous monitoring of the COVID-19 pandemic. The COVID-19 Lending Committee meets weekly and focuses on our credit quality trends and our deferral program. Management continually monitors developments, evaluates strategic and tactical initiatives and solutions and allocates the necessary resources to mitigate the negative impact of this significant market disruption caused by the pandemic. For a description of the potential impacts of COVID-19 on the Company, see "Item 1A. Risk Factors".

Pending Acquisition of Flagstar Bancorp, Inc.

On April 26, 2021,2024, the Company announced it hadthat future quarterly cash dividends on shares of the Company’s common stock would be further reduced to $0.01 per share.

24

Community Pledge Agreement with the National Community Reinvestment Coalition

On January 24, 2022, the Company and the National Community Reinvestment Coalition ("NCRC") announced the Company's commitment to provide $28 billion in loans, investments, and other financial support to communities and people of color, low- and moderate-income ("LMI") families and communities, and small businesses. The Company's Community Pledge Agreement was developed with NCRC and its members in conjunction with the Company's pending merger with Flagstar Bancorp, Inc. The agreement includes $22 billion in community lending and affordable housing commitments and $6 billion of residential mortgage originations to underserved and LMI borrowers, and in LMI and majority-minority neighborhoods over a five-year period. NYCB will also provide $542 million in loans to small businesses with less than $1 million in revenues and in LMI and majority-minority communities; $16.5 million in philanthropic support to nonprofit organizations that meet the needs of LMI and majority-minority communities and individuals; greater access to banking products and services; and the continuation of NYCB's responsible multi-family lending practices. The agreement is subject to the closing of the Flagstar merger. Absent the closing of the merger, the Company will continue to work with its community groups to provide financial and other support within its markets.

USDF Stablecoin Program Initiative

Part

The Company has also engaged its regulators, including the NYSDFS and the FDIC, throughout this process and intends to request non-objection from the Superintendentapproval of the NYSDFS to engage in USDF Stablecoin Program activities, and any additional non-objection required by the FDIC. Assuming that timely non-objection is received, the Company expects to launch the USDF Stablecoin Program in late first-quarter 2022. At which point, the Bank's customers would be able to conduct USDF transactions upon demand, including (i) minting USDF stablecoin; (ii) transmitting and receiving USDF stablecoin; (iii) redeeming USDF stablecoin; and (iv) conducting any and all activities necessary or incidental to the USDF Stablecoin Program.reverse stock split).

ITEM

COVID-19 Related Risk

COVID-19 has caused a significant global economic downturn which has adversely affectedChanges in interest rates could reduce our net interest income and is expected to continue to adversely affect many business.

25

Our business is dependent uponnegatively impact the ability and willingnessvalue of our customers to conduct bankingloans, securities, and other assets and have a material adverse effect on our cash flows, financial transactions, including the paymentcondition, results of their loan obligations. Specifically,operations, and capital.

The COVID-19 pandemic has also ledcould result in, additional expenses, exposure to an increase in the numbercivil litigation, increased regulatory scrutiny, losses, and a loss of deferred loans the Company entered intocustomers.

26

reduction in our earnings. Our net interest income and earnings would be similarly impacted were the interest rates on our interest-earning assets to decline more quickly than the interest rates on our interest-bearing liabilities.

In addition, such changes in interest rates could affect our ability to originate loans and attract and retain deposits; the fair values of our securities and other financial assets; the fair values of our liabilities; and the average lives of our loan and securities portfolios. Changes in interest rates also could have an effect on loan refinancing activity, which, in turn, would impact the amount of prepayment income we receive on our multi-family and CRE loans. Because prepayment income is recorded as interest income, the extent to which it increases or decreases during any given period could have a significant impact on the level of net interest income and net income we generate during that time.

Also, changes in interest rates could have an effect on the slope of the yield curve. If the yield curve were to invert or become flat, our net interest income and net interest margin could contract, adversely affecting our net income and cash flows, and the value of our assets. Moreover, higher inflation could lead to fluctuations in the value of our assets and liabilities and off-balance sheet exposures, and could result in lower equity market valuations of financial services companies.

Changes to and replacement of the LIBOR Benchmark Interest Rate may adversely affect our business, financial condition, and results of operations.

The Company has certain loans, interest rate swap agreements, investment securities, and debt obligations whose interest rate is indexed to LIBOR. In 2017, the FCA, which is responsible for regulating LIBOR, announced that the publication of LIBOR is not guaranteed beyond 2021. In December 2020, the administrator of LIBOR announced its intention to (i) cease the publication of the one-week and two-month U.S. dollar LIBOR after December 31, 2021, and (ii) cease the publication of all other tenors of U.S. dollar LIBOR (one, three, six, and 12-month LIBOR) after June 30, 2023, and on March 15, 2021, announced that it will permanently cease to publish most LIBOR settings beginning on January 1, 2022 and cease to publish the overnight, one-month, three-month, six-month, and 12-month U.S. dollar LIBOR settings on July 1, 2023. Accordingly, the FCA has stated that it does not intend to persuade or compel banks to submit to LIBOR after such respective dates. Until such time, however, FCA panel banks have agreed to continue to support LIBOR. In October 2021, the Federal bank regulatory agencies issued a Joint Statement on Managing the LIBOR Transition that offered their regulatory expectations and outlined potential supervisory and enforcement consequences for banks that fail to adequately plan for and implement the transition away from LIBOR. The failure to properly transition away from LIBOR may result in increased supervisory scrutiny. The implementation of a substitute index for the calculation of interest rates under the Company's loan agreements may result in disputes or litigation with counterparties over the appropriateness or comparability to LIBOR of the substitute index, which would have an adverse effect on the Company's results of operations. Even when robust fallback language is included, there can be no assurances that the replacement rate plus any spread adjustment will be economically equivalent to LIBOR, which could result in a lower interest rate being paid to the Company on such assets.

The Bank established a sub-committee of ALCO to address issues related to the phase out and transition from LIBOR. This sub-committee is led by our Chief Financial Officer and consists of personnel from various departments through the Bank including lending, loan administration, credit risk management, finance/treasury, including interest rate risk and liquidity management, information technology, and operations. The Company has LIBOR-based contracts that extend beyond June 20, 2023 included in loans and leases, securities, wholesale borrowings, derivative financial instruments, and long-term debt. The sub-committee has reviewed contract fallback language and noted that certain contracts will need updated provisions for the transition and is coordinating with impacted business lines. In complying with industry requirements, the Bank will not offer new LIBOR-based products after December 31, 2021.

The Alternative Reference Rates Committee (a group of private-market participants convened by the FRB and the FRB-NY) has identified SOFR as the recommended alternative to LIBOR. The use of SOFR as a substitute for LIBOR is voluntary and may not be suitable for all market participants. SOFR is calculated and observed differently than LIBOR. Given the manner in which SOFR is calculated, it is likely to be lower than LIBOR and is less likely to correlate with the funding costs of financial institutions. Market practices related to SOFR calculation conventions continue to develop and may vary. Inconsistent calculation conventions among financial products may expose is to increased basic rate and resultant costs.

27

Other alternatives to LIBOR also exist, but, because of the difference in how those alternatives are constructed, they may diverge significantly from LIBOR in a range of situations and market conditions.

A decline in the quality of our assets could result in higher losses and the need to set aside higher loan loss provisions, thus reducing our earnings and our stockholders’ equity.

The inability of our borrowers to repay their loans in accordance with their terms would likely necessitate an increase in our provision for credit losses, and therefore reduce our earnings.

The loans we originate for investment are primarily multi-family loans, CRE loans, and specialty finance loans and leases. Such loans are generally larger, and have higher risk-adjusted returns and shorter maturities, than the other loans we produce for investment. Our credit risk would ordinarily be expected to increase with the growth of our multi-family and CRE loan portfolios.

Payments on multi-family and CRE loans generally depend on the income generated by the underlying properties which, in turn, depends on their successful operation and management. The ability of our borrowers to repay these loans may be impacted by adverse conditions in the local real estate market and the local economy. While we seek to minimize these risks through our underwriting policies, which generally require that such loans be qualified on the basis of the collateral property’s cash flows, appraised value, and debt service coverage ratio, among other factors, there can be no assurance that our underwriting policies will protect us from credit-related losses or delinquencies.

To minimize the risks involved in our specialty finance lending and leasing, we participate in syndicated loans that are brought to us, and equipment loans and leases that are assigned to us, by a select group of nationally recognized sources, and generally are made to large corporate obligors, many of which are publicly traded, carry investment grade or near-investment grade ratings, and participate in stable industries nationwide. Each of our credits is secured with a perfected first security interest in the underlying collateral and structured as senior debt or as a non-cancelable lease.

We seek to minimize the risks involved in our other C&I lending by underwriting such loans on the basis of the cash flows produced by the business; by requiring that such loans be collateralized by various business assets, including inventory, equipment, and accounts receivable, among others; and by requiring personal guarantees. However, the capacity of a borrower to repay such a C&I loan is substantially dependent on the degree to which his or her business is successful. In addition, the collateral underlying other C&I loans may depreciate over time, may not be conducive to appraisal, or may fluctuate in value, based upon the results of operations of the business.

We also originate ADC loans, although to a far lesser degree than we originate multi-family and CRE loans. ADC financing typically involves a greater degree of credit risk than longer-term financing on multi-family and CRE properties. Risk of loss on an ADC loan largely depends upon the accuracy of the initial estimate of the property’s value at completion of construction or development, compared to the estimated costs (including interest) of construction. If the estimate of value proves to be inaccurate, the loan may be under-secured. While we seek to minimize these risks by maintaining consistent lending policies and procedures, and rigorous underwriting standards, an error in such estimates, among other factors, could have a material adverse effect on the quality of our ADC loan portfolio, thereby resulting in losses or delinquencies.

The ability of our borrowers to repay their loans could be adversely impacted by a decline in real estate values and/or an increase in unemployment, which not only could result in our experiencing losses, but also could necessitate our recording a provision for credit losses. Either of these events would have an adverse impact on our net income. Although losses on the loans we produce have been comparatively limited, even during periods of economic weakness in our markets, we cannot guarantee that this will be our experience in future periods.

In addition to loan losses due to borrowers’ inability to repay their loans, downgrades in our internal loan classifications may result in a higher provision for credit losses and the ACL, a higher level of net charge-offs, and/or higher non-interest expenses.

28

If the judgments and assumptions we make with regard to the allowance are incorrect, our allowance for losses on such loans might not be sufficient, and an additional provision for credit losses might need to be made. Depending on the amount of such loan loss provisions, the adverse impact on our earnings could be material.

In addition,

Our current business strategy is to continue to originate multi-family loans and to a lesser extent CRE loans.

29

Accordingly, the ability of our borrowers to repay their loans, and the value of the collateral securing such loans, may be significantly affected by economic conditions in this region, including changes in the local real estate market. A significant decline in general economic conditions caused by inflation, recession, unemployment, acts of terrorism, extreme weather, or other factors beyond our control, could therefore have an adverse effect on our financial condition and results of operations. In addition, because multi-family and CRE loans represent the majority of the loans in our portfolio, a decline in tenant occupancy or rents, due to such factors, or for other reasons, such as new legislation, could adversely impact the ability of our borrowers to repay their loans on a timely basis, which could have a negative impact on our net income.

Furthermore, economic or market turmoil could occur in the near or long term. This could negatively affect our business, our financial condition, and our results of operations, as well as our ability to maintain or increase the level of cash dividends we currently pay to our stockholders.

Changes in accounting standards or interpretation of new or existing standards may affect how we report our financial condition and results of operations.

From time to time the FASB and the SEC change accounting regulations and reporting standards that govern the preparation of our financial statements. In addition, the FASB, SEC, and bank regulators, may revise their previous interpretations regarding existing accounting regulations and the application of these accounting standards. These changes can be difficult to predict and can materially impact how to record and report our financial condition and results of operations. In some cases, there could be a requirement to apply a new or revised accounting standard retroactively, resulting in the restatement of prior period financial statements.

Deposit flows, calls of investment securities and wholesale borrowings, and the prepayment of loans and mortgage-related securities are strongly influenced by such external factors as the direction of interest rates, whether actual or perceived; local and national economic conditions; and competition for deposits and loans in the markets we serve. Deposit outflows can occur for a number of reasons, including clients seeking higher yields, clients with uninsured deposits may seek greater financial security or clients may simply prefer to do business with our competitors, or for other reasons. The withdrawal of more deposits than we anticipate could have an adverse impact on our profitability as this source of funding, if not replaced by similar deposit funding, would need to be

A downgrade Downgrades of the credit ratings of the Company and the Bank, such as those announced by certain credit rating agencies in both February and March 2024, could alsoresult in an acceleration in deposit outflows and additional collateral needs, which this far have been modest. They could adversely affect our access to liquidity and capital, and could significantly increase our cost of funds, trigger additional collateral or funding requirements, and decrease the number of investors and counterparties willing to lend to us or to purchase our securities. This could affect our growth, profitability, and financial condition, including our liquidity.

31

If the non-payment of dividends on Series A Preferred Stock, Series B Preferred Stock and Series C Preferred Stock for any dividend period would cause the Company to fail to comply with any applicable law or regulation, or any agreement we may enter into with our regulators from time to time, then we would not be able to declare or pay a dividend for such dividend period. In such a case,

Furthermore, it is possible that future regulatory changes could result in more stringent capital or liquidity requirements, including increases in the levels of regulatory capital we are required to maintain and changes in the way capital or liquidity is measured for regulatory purposes, either of which could adversely affect our business and our ability to expand. For example, federal banking regulations adopted under Basel III standards require bank holding companies and banks to undertake significant activities to demonstrate compliance with higher capital requirements. Any additional requirements to increase our capital ratios or liquidity could necessitate our liquidating certain assets, perhaps on terms that are unfavorable to us or that are contrary to our business plans. In addition, such requirements could also compel us to issue additional securities, thus diluting the value of our common stock.

In addition, failure to meet established capital requirements could result in the FRB and/or OCC placing limitations or

Such regulation and supervision govern the activities in which a bank holding company and its banking subsidiaries may engage, and are intended primarily for the protection of the DIF, the banking system in general, and

32

bank customers, rather than for the benefit of a company’s stockholders. These regulatory authorities have extensive discretion in connection with their supervisory and enforcement activities, including with respect to the imposition of restrictions on the operation of a bank or a bank holding company, the imposition of significant fines, the ability to delay or deny merger or other regulatory applications, the payment of dividends, the classification of assets by a bank, and the adequacy of a bank’s allowance for loan losses, among other matters. Failure to comply (or to ensure that our agents and third-party service providers comply) with laws, regulations, or policies, including our failure to obtain any necessary state or local licenses, could result in enforcement actions or sanctions by regulatory agencies, civil money penalties, and/or reputational damage, which could have a material adverse effect on our business, financial condition, or results of operations. Penalties for such violations may also include: revocation of licenses; fines and other monetary penalties; civil and criminal liability; substantially reduced payments by borrowers; modification of the original terms of loans, permanent forgiveness of debt, or inability to, directly or indirectly, collect all or a part of the principal of or interest on loans provided by the Bank. Changes in such regulation and supervision, or changes in regulation or enforcement by such authorities, whether in the form of policy, regulations, legislation, rules, orders, enforcement actions, ratings, or decisions, could have a material impact on the Company, our subsidiary bank and other affiliates, and our operations. In addition, failure of the Company or the Bank to comply with such regulations could have a material adverse effect on our earnings and capital.

See “Regulation and Supervision” in Part I, Item 1, “Business” earlier in this filing for a detailed description of the federal, state, and local regulations to which the Company and the Bank are subject.

For example, economic and market conditions, heightened legislative and regulatory scrutiny of the financial services industry, and increases in the overall complexity of our operations, among other developments, have resulted in the creation of a variety of risks that were previously unknown and unanticipated, highlighting the intrinsic limitations of our risk monitoring and mitigation techniques. As a result, the further development of previously unknown or unanticipated risks may result in our incurring losses in the future that could adversely impact our financial condition and results of operations. Furthermore, an ineffective ERM framework, as well as other risk factors, could result in a material increase in our FDIC insurance premiums.

33

audit, and application of financial accounting standards. We may take tax return filing positions for which the final determination of tax is uncertain, and our net income and earnings per share could be reduced if a federal, state, or local authority were to assess additional taxes that have not been provided for in our consolidated financial statements. In addition, there can be no assurance that we will achieve our anticipated effective tax rate. Unanticipated changes in tax laws or related regulatory or judicial guidance, or an audit assessment that denies previously recognized tax benefits, could result in our recording tax expenses that materially reduce our net income.

Furthermore, declines in the value of our investment securities could result in our having to record losses based on the other-than-temporary impairment of securities, which would reduce our earnings and also could reduce our capital. In addition, continued economic weakness could reduce the demand for our products and services, which would adversely impact our liquidity and the revenues we produce.

Higher inflationDecember 31, 2023, and averaged 2.96 percent during 2023, 101 basis points higher than average rates experienced during 2022. The sustained higher rates experienced throughout 2023 negatively impacted the mortgage market including our loan origination volume and refinancing activity. In addition to being affected by interest rates, the secondary mortgage markets are also subject to investor demand for residential mortgage loans and investor yield requirements for these loans. These conditions may fluctuate or worsen in the future. Adverse market conditions, including increased volatility, changes in interest rates and mortgage spreads and reduced market demand, could result in greater risk in retaining mortgage loans pending their sale to investors. A prolonged period of secondary market illiquidity may result in a reduction of our loan mortgage production volume and could have a materially adverse effect on our financial condition and results of operations.

Inflation can negativelyrisk management strategies, which rely on assumptions or projections, may not adequately mitigate the impact the Company by increasing our labor costs, through higher wages and higherof changes in interest rates, which may negatively affectinterest rate volatility, convexity, credit spreads, or prepayment speeds, and, as a result, the marketchange in the fair value of securities on our balance sheet, higher interest expenses on our deposits, especially CDs, and a higher cost of our borrowings. Additionally, higher inflation levels could lead to higher oil and gas prices, whichMSRs may negatively impact the net operating incomeearnings.

Recent supply chain constraints have led to higher inflation, which if sustained couldmay have a negativematerially adverse effect on our results of operations or could cause us to take other actions that would be materially detrimental. Fannie Mae and Freddie Mac remain in conservatorship and a path forward for them to emerge from conservatorship is unclear. Their roles could be reduced, modified or eliminated as a result of regulatory actions and the nature of their guarantees could be limited or eliminated relative to historical measurements. The elimination or modification of the traditional roles of Fannie Mae or Freddie Mac could create additional competition in the market and significantly and adversely affect our business, financial condition and results of operations.

Longer-lasting supply chain constraintsother servicing practices, the servicing and ancillary fees that we may charge, modification standards and procedures, and the amount of non-reimbursable advances. We cannot negotiate these terms, which are subject to change at any time, with the Agencies. A significant change in various productsthese guidelines, which decreases the fees we charge or requires us to expend additional resources in providing mortgage services, could decrease our revenues or increase our costs, adversely affecting our business, financial condition, and labor marketsresults of operations. In addition, changes in the nature or extent of the guarantees provided by Fannie Mae and Freddie Mac or the insurance provided by the FHA could potentially exacerbate inflationalso have broad adverse market implications. The fees that we are required to pay to the Agencies for these guarantees have changed significantly over time and sustain it at elevated levels, even as growth slows. The riskany future increases in these fees would adversely affect our business, financial condition and results of sustained high inflation would likely be accompanied by monetary policy tightening with potential negative effects on various elevated asset classes.operations.

The market price and liquidity

Thethe exercise of warrants issued by us may dilute existing holders of our common stock and other securities, decrease the value of our common stock and other securities and adversely affect the market price of our common stock could beand other securities.

34

Economic or market turmoil could occur in the near or long term, which could negatively affect our business, governmental activities, and on our financial condition and our results of operations, as well as volatilityperformance.

Although we also originate C&I and ADC loans, and invest in securities, our

If we are unable to engage in or complete a desired acquisition or merger transaction, our financial condition and results of operations could be adversely impacted. As acquisitions have been a significant source of deposits, the inability to complete a business combination could require that we increase the interest rates we pay on deposits in order to attract such funding through our current branch network, or that we increase our use of wholesale funds. Increasing our cost of funds could adversely impact our net interest income and our net income. Furthermore, the absence of acquisitions could impact our ability to fulfill our loan demand.

In addition, mergers and acquisitions can lead to uncertainties about the future on the part of customers and employees. Such uncertainties could cause customers and others to consider changing their existing business relationships with the company to be acquired, and could cause its employees to accept positions with other companies before the merger occurs. As a result, the ability of a company to attract and retain customers, and to attract, retain, and motivate key personnel, prior to a merger’s completion could be impaired.

Furthermore, no assurance can be given that acquired operations would not adversely affect our existing profitability; that we would be able to achieve results in the future similar to those achieved by our existing banking business; that we would be able to compete effectively in the market areas served by acquired branches; or that we would be able to manage any growth resulting from a transaction effectively. In particular, our ability to compete effectively in new markets would be dependent on our ability to understand those markets and their competitive

35

dynamics, and our ability to retain certain key employees from the acquired institution who know those markets better than we do.

The failure to receive the necessary regulatory approvals for the Company's acquisition of Flagstar Bancorp, Inc. in a timely manner, would have a material negative impact on our financial results, operations, and reputation.

On April 26, 2021, the Company entered into a definitive merger agreement under which it will acquire Flagstar Bancorp, Inc. in a 100% stock transaction. On August 4, 2021, both sets of shareholders approved the merger. Completion of the proposed merger remains subject to the receipt of required approvals from NYSDFS, the FDIC, and the FRB.

While both companies remain committed to continuing to seek all such approvals, the aforementioned regulatory approvals could be delayed or not obtained at all, including due to: an adverse development in either company's regulatory standing or in any other factors considered by regulators when granting such approvals, including factors not known at the present time.

If the merger is not completed for any reason, there

Additionally, NYCB has incurred and will continue to incur substantial expenses in connection with the negotiation and completion of the transaction completed by the merger agreement, as well as the costs and expenses incurred in connection with the merger. If the merger is not completed, NYCB would have incurred these expenses without realizingachieving the expected benefits from our merger and acquisition activities.

The inabilityacquisitions. We may also lose key personnel from the acquired entity as a result of an acquisition. We may not discover all known and unknown factors when examining a company for acquisition or merger during the due diligence period. These factors could produce unintended and unexpected consequences for us including, but not limited to, receive dividendsincreased compliance and legal risks, including increased litigation or regulatory actions such as fines or restrictions related to the business practices or operations of the combined business. Undiscovered factors as a result of an acquisition or merger could bring civil, criminal, and financial liabilities against us, our management, and the management of those entities we acquire or merge with. In addition, if difficulties arise with respect to the integration process, we may incur higher integration expenses than anticipated and the economic benefits expected to result from the acquisition, including revenue growth and cost savings, might not occur or might not occur to the extent we expected. Failure to successfully integrate businesses that we acquire or merge with could have an adverse effect on our subsidiary bankprofitability, return on equity, return on assets, or our ability to implement our strategy, any of which in turn could have a material adverse effect on our business, financial condition orand results of operations.

The Parent Company (i.e., the company on an unconsolidated basis) is a separate and distinct legal entity from the Bank, and a substantial portionexpedited nature of the revenuesFDIC-assisted transaction did not allow bidders the Parent Company receives consiststime and access to information customarily associated with preparing for and evaluating a negotiated transaction. As a result, fair value estimates we have made in connection with the Signature transaction may be inaccurate and subject to change, which could adversely impact our financial condition, results of dividendsoperations and future prospects. In addition, we may obtain additional information and evidence during the period of one year from March 20, 2023, the Bank. These dividends aredate we completed the primary funding source forSignature transaction, that may result in changes to the dividends we pay on our common stock and the interest and principal payments on our debt. Various federal and state laws and regulations limitestimated amounts recorded as of December 31, 2023, which could change the amount of dividends that a bank may paythe bargain purchase gain we have recorded. Adjustments to its parent company. In addition, our right to participate in a distribution of assets upon the liquidation or reorganization of a subsidiarythis gain may be subject torecorded based on additional information received after the prior claimsacquisition date that affect the measurement of the subsidiary’s creditors. Ifassets acquired and liabilities assumed and any decrease in the Bank is unable to pay dividends to the Parent Company, we might not be able to service our debt, pay our obligations, or pay dividends on our common stock.

Reduction or eliminationamount of our quarterly cash dividend could have an adverse impact on the market price of our common stock.

Holders of our common stock are only entitled to receive such dividends as our Board of Directors may declare out of funds available for such payments under applicable law and regulatory guidance, and althoughbargain purchase gain we have historically declared cash dividends onrecorded could also adversely impact our common stock, we are not required to do so. Furthermore, the paymentfinancial condition, results of dividends falls under federal regulations that have grown more stringent in recent years. While we pay our quarterly cash dividend in compliance with current regulations, such regulations could change in the future. Any reduction or elimination of our common stock dividend in theoperations and future could adversely affect the market price of our common stock.prospects.

36

be inadequate or inaccurate, we could incur increased or unexpected losses which, in turn, could adversely affect our earnings and capital. Additionally, failure by the Company to maintain compliance with strict capital, liquidity, and other stress test requirements under banking regulations could subject us to regulatory sanctions, including limitations on our ability to pay dividends.

In addition, breaches of security have in the past and may in the future occur through intentional or unintentional acts by those having authorized or unauthorized access to our confidential or other information, or that of our customers, clients, or counterparties. If one or more ofCertain previously identified cyber incidents have resulted, and future such events were to occur,could result, in the breach of confidential and other information processed and stored in and transmitted through, our computer systems and networksnetworks. These events could potentially be jeopardized, or could otherwise cause interruptions or malfunctions in our operations or the operations of our customers, clients, or counterparties. Further, we may not know that an attack occurred until well after the event. Even after discovering an attempt or breach occurred, we may not know the extent of the impact of the attack for some period of time. This could cause us significant reputational damage or result in our experiencing significant losses.

Furthermore, we We may also be required to expend significant additional resources to modify our protective measures or investigate and remediate vulnerabilities or other exposures arising from operational and security risks. Additional expenditures may be requiredrisks, including expenses for third-party expert consultants or outside counsel. We are currently subject to litigation regarding cyber incidents, and we also may be subject to future litigation and financial losses that either are not insured against or not fully covered through any insurance we maintain.maintain or any third-party indemnification or insurance. We believe that the impact of any previously identified cyber incidents, including those subject to ongoing investigation and remediation, will not have a material financial impact.

While we have established information security policies, procedures and procedures,controls, including an Incident Response Plan, to prevent or limit the impact of systems failures and interruptions, we may not be able to anticipate all possible security breaches that could affect our systems or information and there can be no assurance that such events will not occur or will be adequately prevented or mitigated by our policies, procedures and controls if they do.

37

Our third-party providers may be vulnerable to unauthorized access, computer viruses, phishing schemes, and other security breaches. Threats to information security also exist in the processing of customer information through various other third-party providers and their personnel. We may be required to expend significant additional resources to protect against the threat of such security breaches and computer viruses, or to alleviate problems caused by such security breaches or viruses. To the extent that the activities of our third-party providers or the activities of our customers involve the storage and transmission of confidential information, security breaches and viruses could expose us to claims, regulatory scrutiny, litigation, and other possible liabilities.

These types of third-party relationships are subject to increasingly demanding regulatory requirements and oversight by federal bank regulators (such as the Federal Reserve Board, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation) and the CFPB. As a result, if our regulators conclude that we have not exercised adequate oversight and control over vendors and subcontractors or other ongoing third-party business relationships or that such third-parties have not performed appropriately, we could be subject to enforcement actions, including civil money penalties or other administrative or judicial penalties or fines, as well as requirements for consumer remediation. In addition, the Company may not be adequately insured against all types of losses resulting from third-party failures, and our insurance coverage may be inadequate to cover all losses resulting from systems failures or other disruptions to our banking services.

10 owners of MSRs, excluding ourselves, for which we act as subservicer for the mortgage loans they own. Due to the limited number of relationships, discontinuation of existing agreements with those third parties or adverse changes in contractual terms could have a significant negative impact to our mortgage servicing revenue. The terms and conditions in which a master servicer may terminate subservicing contracts are broad and could be exercised at the discretion of the master servicer without requiring cause. Additionally, the master servicer directs the oversight of custodial deposits associated with serviced loans and, to the extent allowable, could choose to transfer the oversight of the Bank's custodial deposits to another depository institution. Further, as servicer or subservicer of loans, we have certain contractual obligations, including foreclosing on defaulted mortgage loans or, to the extent applicable, considering alternatives to foreclosure. If we commit a material breach of our obligations as servicer, we may be subject to termination if the breach is not cured within a specified period of time following notice, causing us to lose servicing income.

in turn, on our financial condition and results of operations. Claims asserted against us can be highly complicated and slow to develop, making the outcome of such proceedings difficult to predict or estimate early in the process. As a public company,participant in the financial services industry, it is likely that we arewill be exposed to a high level of litigation and regulatory scrutiny relating to our business and operations. Although we establish accruals for legal or regulatory proceedings when information related to the loss contingencies represented by those matters indicates both that a loss is probable and that the amount of loss can be reasonably estimated, we do not have accruals for all legal or regulatory proceedings where we face a risk of loss. Due to the inherent subjectivity of the assessments and unpredictability of the outcome of legal and regulatory proceedings, amounts accrued may not represent the ultimate loss to us from the legal and regulatory proceedings in question. As a result, our ultimate losses may be significantly higher than the amounts accrued for legal loss contingencies. For further information, see Note 19 - Commitments and Contingencies and Item 3 - Legal Proceedings.

38

cannot assure you that our internal control over financial reporting will be effective in the future may enact, statutes requiring the payment of interest on escrow balances or if we would be required to retroactively credit interest on escrow funds, the Company’s earnings could be adversely affected.

If we are not able to maintaindetect or document effective internal control over financial reporting, our independent registered public accounting firm will not be able to certify as to the effectiveness of our internal control over financial reporting. Matters impacting our internal control over financial reporting may cause us to be unable to report our financial information onmitigate fraud risks in a timely basis, or may cause usmanner. We are committed to restate previously issued financial information,ongoing investments and thereby subject usattention to adverse regulatory consequences, including sanctions or investigations by the SEC, or violations of applicable stock exchange listing rules.

There could also be a negative reaction in the financial markets duecombat fraud and enhance our security measures to a loss of investor confidence in us and the reliability of our financial statements. Confidence in the reliability of our financial statements is also likely to suffer if we or our independent registered public accounting firm reports a material weakness in the effectiveness of our internal control over financial reporting. This could materially adversely affect us by, for example, leading to a decline in our stock price and impairing our ability to raise capital.protect against these risks.

Our actual or perceived failure to identify and address various issues also could give rise to reputational risk that could significantly harm us and our business prospects, including failure to properly address operational risks. These issues include legal and regulatory requirements; consumer protection, fair lending, and privacy issues; properly maintaining customer and associated personal information; record keeping; protecting against money laundering; sales and trading practices; and ethical issues.

Additionally, concerns over the long-term impacts of climate change have led and will continue to lead to governmental efforts around the world to mitigate those impacts. Investors, consumers, and businesses also may change their behavior on their own as a result of these concerns. The Company and its customers will need to respond to new laws and regulations as well as investor, consumer and business preferences resulting from climate change concerns. The Company and its customers may face cost increases, asset value reductions, and operating process changes, among other impacts. The impact on the Company’s customers will likely vary depending on their specific attributes, including reliance on or role in carbon intensive activities. In addition, the Company would face reductions in credit worthiness on the part of some customers or in the value of assets securing loans. Investors could determine

39

not to invest in the Company’s securities due to various climate change related considerations. The Company’s efforts to take these risks into account in making lending and other decisions may not be effective in protecting the Company from the negative impact of new laws and regulations or changes in investor, consumer or business behavior.

| Item 1B. | Unresolved Staff Comments | ||||

| Item 1C. | Cybersecurity | ||||

| Item 2. | Properties | ||||

| Item 3. | Legal Proceedings | ||||

ITEM 3. LEGAL PROCEEDINGS

Following

| Item 4. | Mine Safety Disclosures | ||||

40

| Item 5. | Market For the Registrant's Common Equity, Related Stockholder Matters, and Issuer Purchases | ||||

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

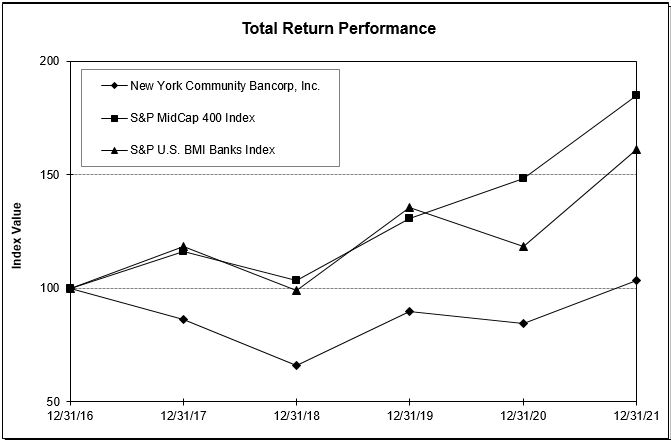

Comparison of 5-Year Cumulative Total Return

Among New York Community Bancorp, Inc.,

S&P Mid-Cap 400 Index, and S&P U.S. BMI Banks Index*

ASSUMES $100 INVESTED ON

| 12/31/2018 | 12/31/2019 | 12/31/2020 | 12/31/2021 | 12/31/2022 | 12/31/2023 | |||||||||||||||

| New York Community Bancorp, Inc. | $ | 100.00 | $ | 135.38 | $ | 127.51 | $ | 156.41 | $ | 118.03 | $ | 149.75 | ||||||||

| S&P Mid-Cap 400 Index | $ | 100.00 | $ | 126.20 | $ | 143.44 | $ | 178.95 | $ | 155.58 | $ | 181.15 | ||||||||

| S&P U.S. BMI Banks Index | $ | 100.00 | $ | 137.36 | $ | 119.83 | $ | 162.92 | $ | 135.13 | $ | 147.41 | ||||||||

|

| 12/31/2016 |

| 12/31/2017 |

| 12/31/2018 |

| 12/31/2019 |

| 12/31/2020 |

| 12/31/2021 |

| ||||||

New York Community Bancorp, Inc. |

| $ | 100.00 |

| $ | 86.12 |

| $ | 66.11 |

| $ | 89.50 |

| $ | 84.30 |

| $ | 103.41 |

|

S&P Mid-Cap 400 Index |

| $ | 100.00 |

| $ | 116.24 |

| $ | 103.36 |

| $ | 130.44 |

| $ | 148.26 |

| $ | 184.97 |

|

S&P U.S. BMI Banks Index |

| $ | 100.00 |

| $ | 118.21 |

| $ | 98.75 |

| $ | 135.64 |

| $ | 118.33 |

| $ | 160.89 |

|

*The SNL U.S. Bank & Thrift Index was renamed to the S&P U.S. BMI Banks Index.

| (dollars in millions, except share data) | ||||||||||||||||||||||||||

| Period | Total Shares of Common Stock Repurchased | Average Price Paid per Common Share | Total Allocation | Total Shares of Common Stock Purchased as Part of Publicly Announced Plans or Programs | ||||||||||||||||||||||

| First Quarter 2023 | 976,454 | $ | 9.33 | $ | 9 | 0 | ||||||||||||||||||||

| Second Quarter 2023 | 190,177 | 10.36 | 2 | 0 | ||||||||||||||||||||||

| Third Quarter 2023 | 33,956 | 12.50 | 0 | 0 | ||||||||||||||||||||||

| Fourth Quarter 2023 | ||||||||||||||||||||||||||

| October 1 - 31, 2023 | 1,525 | 10.29 | 0 | — | ||||||||||||||||||||||

| November 1 - 30, 2023 | 4,897 | 9.34 | — | — | ||||||||||||||||||||||

| December 1 - 31, 2023 | 50,526 | 9.92 | 1 | — | ||||||||||||||||||||||

| Total Fourth Quarter 2023 | 56,948 | $ | 16.57 | 1 | — | |||||||||||||||||||||

| 2023 Total | 1,257,535 | $ | 9.59 | $ | 12 | — | ||||||||||||||||||||

| Item 6. | Reserved | ||||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||

|

|

|

|

|

|

|

|

|

| |||

(dollars in millions, except per share data) |

| Total Shares |

|

| Average Price |

|

| Total |

| |||

First Quarter 2021 |

|

| 1,343,366 |

| $ |

| 11.55 |

| $ |

| 16 |

|

Second Quarter 2021 |

|

| 17,422 |

|

|

| 11.99 |

|

|

| - |

|

Third Quarter 2021 |

|

| 36,163 |

|

|

| 11.58 |

|

|

| - |

|

Fourth Quarter 2021 |

|

|

|

|

|

|

|

|

| |||

October |

|

| 579 |

|

|

| 13.85 |

|

|

| - |

|

November |

|

| 2,246 |

|

|

| 12.51 |

|

|

| - |

|

December |

|

| 2,331 |

|

|

| 11.96 |

|

|

| - |

|

Total Fourth Quarter 2021 |

|

| 5,156 |

|

|

| 12.41 |

|

|

| - |

|

2021 Total |

|

| 1,402,107 |

|

|

| 11.56 |

| $ |

| 16 |

|

ITEM 6. RESERVED

43

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

For the purpose of this discussion and analysis, the words “we,” “us,” “our,” and the “Company” are used to refer to New York Community Bancorp, Inc. and our consolidated subsidiaries, including New York Community Bank (the “Bank”).

Executive Summary

New York Community Bancorp, Inc. is the holding company for New York Community Bank, with 237 branches in Metro New York, New Jersey, Ohio, Florida, and Arizona.

Chartered in the Statebusiness of New York, theSignature Bridge Bank, is subject to regulation byfrom the FDIC the CFPB, and the NYSDFS. In addition, the holding company is subject to regulation by the FRB, the SEC, andas receiver for Signature Bridge Bank (the “Signature Transaction”). See Note 3 - Business Combinations to the requirements ofConsolidated Financial Statements for further information regarding the NYSE, where shares of our common stock are traded under the symbol “NYCB” and shares of our preferred stock trade under the symbol “NYCB PA.” As a publicly traded company, our mission is to provide our stockholders with a solid return on their investment by producing a strong financial performance, maintaining a solid capital position, and engaging in corporate strategies that enhance the value of their shares.Signature Transaction.

Strong Year-Over-Year Growth In Our Loan Portfolio

| For the Years Ended December 31, | |||||||||||||||||||||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||||||||||||||||||||

| (dollars in millions) | Average Balance | Interest | Average Yield/Cost | Average Balance | Interest | Average Yield/Cost | Average Balance | Interest | Average Yield/Cost | ||||||||||||||||||||||||||

| ASSETS: | |||||||||||||||||||||||||||||||||||

| Interest-earning assets: | |||||||||||||||||||||||||||||||||||

Mortgage and other loans and leases , net (1) | $ | 81,855 | $ | 4,509 | 5.51 | % | $ | 49,376 | $ | 1,848 | 3.74 | % | $ | 43,200 | $ | 1,525 | 3.53 | % | |||||||||||||||||

Securities (2) (3) | 10,611 | 444 | 4.18 | % | 7,448 | 200 | 2.69 | % | 6,625 | 156 | 2.35 | % | |||||||||||||||||||||||

| Reverse repurchase agreements | 388 | 22 | 5.77 | % | 460 | 15 | 3.24 | % | 430 | 4 | 1.05 | % | |||||||||||||||||||||||

| Interest-earning cash and cash equivalents | 10,025 | 516 | 5.14 | % | 1,988 | 29 | 1.47 | % | 2,016 | 4 | 0.17 | % | |||||||||||||||||||||||

| Total interest-earning assets | $ | 102,879 | $ | 5,491 | 5.34 | % | $ | 59,272 | $ | 2,092 | 3.53 | % | $ | 52,271 | $ | 1,689 | 3.23 | % | |||||||||||||||||

| Non-interest-earning assets | 7,616 | 5,130 | 5,275 | ||||||||||||||||||||||||||||||||

| Total assets | $ | 110,495 | $ | 64,402 | $ | 57,546 | |||||||||||||||||||||||||||||

| LIABILITIES AND STOCKHOLDERS' EQUITY: | |||||||||||||||||||||||||||||||||||

| Interest-bearing deposits: | |||||||||||||||||||||||||||||||||||

| Interest-bearing checking and money market accounts | $ | 29,286 | $ | 943 | 3.22 | % | $ | 17,910 | $ | 226 | 1.26 | % | $ | 12,829 | $ | 31 | 0.24 | % | |||||||||||||||||

| Savings accounts | 9,941 | 169 | 1.70 | % | 9,336 | 60 | 0.64 | % | 7,612 | 28 | 0.36 | % | |||||||||||||||||||||||

| Certificates of deposit | 17,097 | 646 | 3.78 | % | 8,772 | 97 | 1.11 | % | 9,094 | 55 | 0.60 | % | |||||||||||||||||||||||

| Total interest-bearing deposits | $ | 56,324 | $ | 1,758 | 3.12 | % | $ | 36,018 | $ | 383 | 1.06 | % | $ | 29,535 | $ | 114 | 0.38 | % | |||||||||||||||||

| Short term borrowed funds | 7,263 | 305 | 4.20 | % | 2,408 | 56 | 2.32 | % | 2,343 | 8 | 0.34 | % | |||||||||||||||||||||||

| Other borrowed funds | 10,671 | 351 | 3.29 | % | 12,982 | 257 | 1.99 | % | 13,366 | 278 | 2.08 | % | |||||||||||||||||||||||

| Total borrowed funds | $ | 17,934 | $ | 656 | 3.66 | % | $ | 15,390 | $ | 313 | 2.04 | % | $ | 15,709 | $ | 286 | 1.82 | % | |||||||||||||||||

| Total interest-bearing liabilities | $ | 74,258 | $ | 2,414 | 3.25 | % | $ | 51,408 | $ | 696 | 1.35 | % | $ | 45,244 | $ | 400 | 0.88 | % | |||||||||||||||||

| Non-interest-bearing deposits | 21,583 | 5,124 | 4,578 | ||||||||||||||||||||||||||||||||

| Other liabilities | 4,073 | 787 | 790 | ||||||||||||||||||||||||||||||||

| Total liabilities | $ | 99,914 | $ | 57,319 | $ | 50,612 | |||||||||||||||||||||||||||||

| Stockholders’ equity | 10,581 | 7,083 | 6,934 | ||||||||||||||||||||||||||||||||

| Total liabilities and stockholders’ equity | $ | 110,495 | $ | 64,402 | $ | 57,546 | |||||||||||||||||||||||||||||

| Net interest income/interest rate spread | $ | 3,077 | 2.09 | % | $ | 1,396 | 2.17 | % | $ | 1,289 | 2.35 | % | |||||||||||||||||||||||

| Net interest margin | 2.99 | % | 2.35 | % | 2.47 | % | |||||||||||||||||||||||||||||

| Ratio of interest-earning assets to interest-bearing liabilities | 1.39 | x | 1.15 | x | 1.16 | x | |||||||||||||||||||||||||||||

| For the Years Ended December 31, | ||||||||||||||||||||||||||

| 2023 compared to Year Ended 2022 Increase/(Decrease) Due to: | 2022 compared to Year Ended 2021 Increase/(Decrease) Due to: | |||||||||||||||||||||||||

| (in millions) | Volume | Rate | Net | Volume | Rate | Net | ||||||||||||||||||||

| INTEREST-EARNING ASSETS: | ||||||||||||||||||||||||||

| Mortgage and other loans and leases, net | $ | 1789 | $ | 872 | $ | 2661 | $ | 231 | $ | 92 | $ | 323 | ||||||||||||||

| Securities | 132 | 112 | 244 | 22 | 22 | 44 | ||||||||||||||||||||

| Reverse repurchase agreements | (4) | 11 | 7 | 1 | 10 | 11 | ||||||||||||||||||||

| Interest Earning cash and cash equivalents | 413 | 74 | 487 | — | 25 | 25 | ||||||||||||||||||||

| Total interest-earnings assets | 2,327 | 1,072 | 3,399 | 247 | 156 | 403 | ||||||||||||||||||||

| INTEREST-BEARING LIABILITIES: | ||||||||||||||||||||||||||

| Interest-bearing checking and money market accounts | 366 | 351 | 717 | 64 | 131 | 195 | ||||||||||||||||||||

| Savings accounts | 10 | 99 | 109 | 11 | 21 | 32 | ||||||||||||||||||||

| Certificates of deposit | 315 | 234 | 549 | (4) | 46 | 42 | ||||||||||||||||||||

| Short term borrowed funds | 204 | 45 | 249 | 2 | 46 | 48 | ||||||||||||||||||||

| Other borrowed funds | (76) | 170 | 94 | (8) | (13) | (21) | ||||||||||||||||||||

| Total interest-bearing liabilities | 743 | 975 | 1,718 | 83 | 213 | 296 | ||||||||||||||||||||

| Change in net interest income | $ | 1,584 | $ | 97 | $ | 1,681 | $ | 164 | $ | (57) | $ | 107 | ||||||||||||||

| For the Years Ended December 31, | |||||||||||||||||