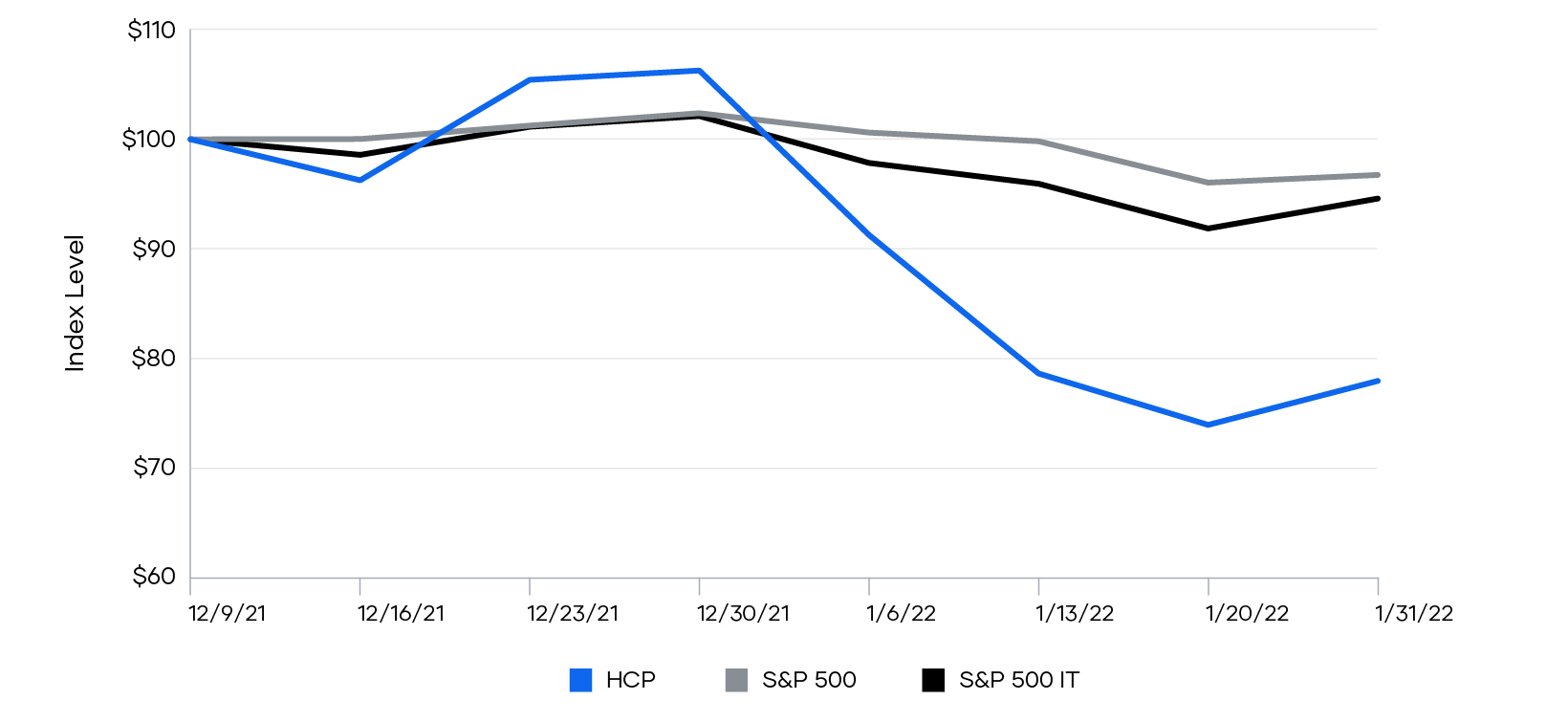

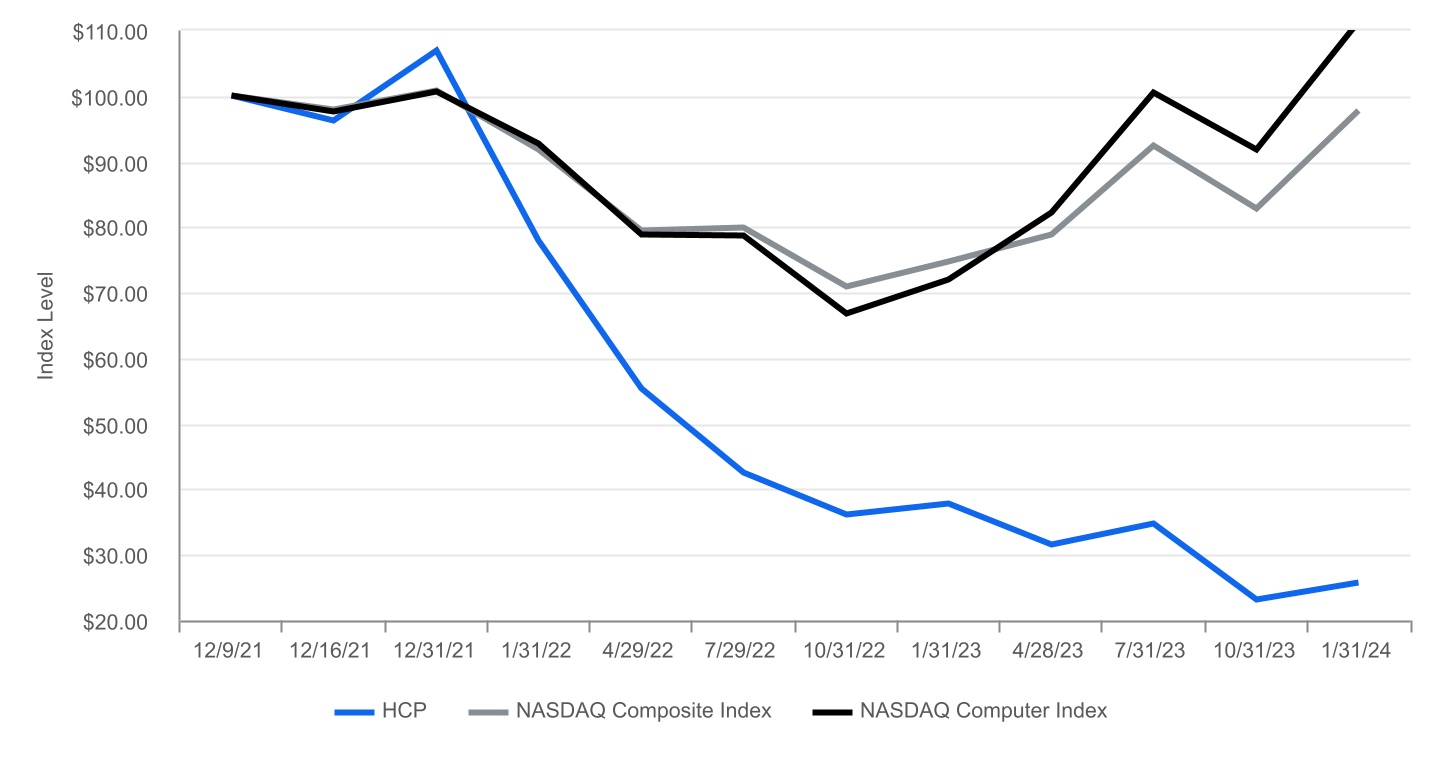

companies for which they work, and this broad community engagement assists our go-to-market strategy by enabling technical knowledge and adoption inside our customers’ organizations. As a result, 2024. continuous integration systems to test code. Once a developer is ready to push a change to production, there is a highly fragmented ecosystem of tools, and organizations often have custom-built solutions to manage the remaining lifecycle. Waypoint provides a standard workflow that is designed to be simple and prescriptive for developers, while being highly extensible to enable platform operators to integrate their existing tools and systems. This enables platform teams to hide the complexity of the underlying infrastructure and enable developers to have a consistent workflow for application delivery across environments. organization. Our business and operations have experienced periods of rapid growth and fluctuation, and if we do not appropriately manage future growth or change, if any, or are unable to improve our systems and processes, our business, financial condition, results of operations, and prospects will be adversely affected. including entry into new markets or growth in lower margin markets; entry into markets with different pricing and cost structures; pricing discounts; and increased price competition. Any one of these factors or the cumulative effects of certain of these factors may result in significant fluctuations in our gross margin and operating results. This variability and unpredictability could result in our failure to meet internal expectations or those of investors for a particular period. features and compliance capabilities to satisfy customer requirements. Our inability to meet those requirements could limit the revenue growth we achieve from our cloud offerings. quarter due to extended sales cycles. results. them. operations. results. the compensation obligations we have to our customers. from changes in gross domestic product growth, financial and credit market fluctuations, uncertain interest rates, inflationary pressures, interest rate increases, recessionary economic cycles, political turmoil, natural catastrophes, warfare, and terrorist attacks on the United States, Europe, the Asia-Pacific region, or elsewhere, could cause a decrease in business investments by our customers and potential customers, including spending on information technology, and negatively affect the growth of our business. For example, rising interest rates and high levels of inflation have affected businesses across many industries, which has significantly constrained and may continue to constrain the budgets of our customers and prospective customers. To the extent our offerings are perceived by customers and potential customers as discretionary, our revenue may be disproportionately affected by delays or reductions in general information technology spending. Also, customers may choose to develop in-house software as an alternative to using our products. Moreover, competitors may respond to market conditions by lowering prices. We cannot predict the timing, strength, or duration of any economic slowdown, instability, or recovery, generally or within any particular industry. If the economic conditions of the general economy or markets in which we operate do not improve, or worsen from present levels, our business, results of operations, and financial condition could be adversely affected. AI in our offerings and in our business may result in reputational harm or liability. receive or deliver the purchased software before the quarter ends. As a result, we may need to prioritize some orders over the United States unless the parties to the transfer have implemented specific safeguards to protect the transferred personal data. The safeguard on which we have primarily relied for such transfers has been implementation of the European Commission’s Standard Contractual Clauses, or SCCs, in our relevant data transfer agreements. We have undertaken certain efforts to conform transfers of personal data from the European Economic Area, or the EEA, to the United States and other jurisdictions based on our understanding of current regulatory obligations and the guidance of data protection authorities. The EU-U.S. Privacy Shield program administered by the U.S. Department of Commerce, to which we have self-certified, was invalidated other claims and penalties, and we could be required to fundamentally change our products or our business practices, which could have an adverse effect on our business. Any inability to adequately address privacy, data protection, and data security concerns, even if unfounded, or any actual or perceived failure to comply with applicable privacy, data protection, and data security laws, regulations, and other obligations, could result in additional cost and liability to us, damage our reputation, inhibit sales, and adversely affect our business. Furthermore, the costs of compliance with, and other burdens imposed by, the laws, regulations, and policies that are applicable to the businesses of our customers may limit the use and adoption of, and reduce the overall demand for, our products. Privacy, data protection, and data security concerns, whether valid or not valid, may inhibit market adoption of our products, particularly in certain industries and countries outside of the United States. If we are not able to adjust to changing laws, regulations, and standards related to the internet, our business may be harmed. procedures to address compliance with such laws, we cannot assure you that all of our employees, representatives, contractors, partners, and agents will not take actions in violation of our policies and applicable law, for which we may be ultimately held responsible. Any allegations or violation of the FCPA or other applicable anti-bribery, anti-corruption laws, and anti-money laundering laws could result in whistleblower complaints, adverse media coverage, investigations, loss of export privileges, severe criminal or civil sanctions, or suspension or debarment from U.S. government contracts, all of which may have an adverse effect on our reputation, business, operating results, and prospects. Responding to any investigation or action will likely result in a materially significant diversion of management’s attention and resources and significant defense costs and other professional fees. have limited experience and expertise regarding acquisitions, and we may devote resources to exploring larger and more complex acquisitions and investments than we have previously attempted. Any such acquisitions or investments may divert the attention of management and cause us to incur various expenses in identifying, investigating, and pursuing suitable opportunities, whether or not the transactions are completed, and may result in unforeseen operating difficulties and expenditures. In particular, we may encounter difficulties assimilating or integrating the businesses, technologies, products, personnel, or operations of any acquired companies, particularly if the key personnel of an acquired company choose not to work for us, their software is not easily adapted to work with our platform, or we have difficulty retaining the customers of any acquired business due to changes in ownership, management, or otherwise. In addition, we have limited experience in acquiring other businesses. If an acquired business fails to meet our expectations, our operating results, and business and financial position may suffer. We may not be able to find and identify desirable acquisition targets, we may incorrectly estimate the value of an acquisition target, and we may not be successful in entering into an agreement with any particular target. Further, any such transactions that we largely remote workforce. wider sanctions and take other actions should the conflict further escalate. It is not possible to predict the broader consequences of this conflict, which could include further sanctions, embargoes, regional instability, prolonged periods of higher inflation, geopolitical shifts, and adverse effects on macroeconomic conditions, currency exchange rates, and financial markets, all of which could have a material adverse effect on our business, financial condition, and results of operations. Our other co-founder Mitchell Hashimoto ceased to be an employee of HashiCorp in fiscal 2024 and has no significant influence on the voting power of our outstanding common stock. Our fiscal year ended January 31, 2023 is referred to as fiscal 2023, and our fiscal year ending January 31, 2024 is referred to as fiscal 2024. We also intend to continue to grow our base of large enterprises around the world. As of January 31, 2022 2021 2020 (dollars in millions) Total customers 2,715 1,473 831 Total customers with $100,000 or greater ARR 655 500 338 Subscription revenue from HCP (and its predecessor cloud offerings) $ 18.5 (1) $ 2.9 (1) $ 0.3 (1) Remaining performance obligations (RPOs) $ 428.8 $ 263.9 $ 152.1 Non-GAAP RPOs(2) $ 452.2 $ 286.1 $ 171.0 As of January 31, 2022 January 31, 2021 GAAP RPOs GAAP short-term RPOs $ 268,911 $ 165,798 GAAP long-term RPOs 159,923 98,131 Total GAAP RPOs $ 428,834 $ 263,929 Add: Customer deposits Customer deposits expected to be recognized within the next 12 months $ 20,324 $ 20,421 Customer deposits expected to be recognized after the next 12 months 3,059 1,798 Total customer deposits $ 23,383 $ 22,219 Non-GAAP RPOs Non-GAAP short-term RPOs $ 289,235 $ 186,219 Non-GAAP long-term RPOs 162,982 99,929 Total Non-GAAP RPOs $ 452,217 $ 286,148 Year Ended January 31, 2022 2021 2020 (in thousands) GAAP net cash used in operating activities $ (56,215 ) $ (39,623 ) $ (28,365 ) Add: purchases of property and equipment (214 ) (4,304 ) (980 ) Add: capitalized internal-use software (6,382 ) (2,920 ) - Free cash flow (used in) $ (62,811 ) $ (46,847 ) $ (29,345 ) GAAP net cash used in operating activities as a percentage of revenue (18 ) % (19 ) % (23 ) % Free cash flow as a % of revenue (20 ) % (22 ) % (24 ) % services and other revenue. Our software subscriptions are currently predominantly self-managed by users and customers who deploy it across public, private, and hybrid cloud environments. We also offer the HCP, our fully-managed cloud platform for multiple products. previous periods. Consequently, increases or decreases in new sales or renewals in any one period may not be immediately reflected as revenue for that period. Any downturn in sales, however, may negatively affect our revenue in future periods. Accordingly, the effect of downturns in sales and market acceptance of our products, and potential changes in our rate of renewals, may not be fully reflected in our results of operations until future periods. losses from foreign currency transactions, and realized gains and losses on short-term investments. Year Ended January 31, 2022 2021 2020 (in thousands) Consolidated Statements of Operations Data: Revenue: License $ 47,504 $ 36,208 $ 18,503 Support 247,566 165,607 96,820 Cloud-hosted services 18,613 4,092 2,339 Total subscription revenue 313,683 205,907 117,662 Professional services 7,086 5,947 3,599 Total revenue 320,769 211,854 121,261 Cost of revenue: Cost of license(1) 221 536 294 Cost of support(1) 38,080 27,194 17,704 Cost of cloud-hosted services(1) 14,031 4,811 1,390 Total cost of subscription revenue(1) 52,332 32,541 19,388 Cost of professional services(1) 11,108 8,511 4,527 Total cost of revenue(1) 63,440 41,052 23,915 Gross profit 257,329 170,802 97,346 Operating expenses: Sales and marketing(1) 269,504 141,018 89,308 Research and development(1) 165,031 65,248 40,118 General and administrative(1) 112,108 48,545 24,137 Total operating expenses 546,643 254,811 153,563 Loss from operations (289,314 ) (84,009 ) (56,217 ) Other income, net 162 756 3,382 Loss before income taxes (289,152 ) (83,253 ) (52,835 ) Provision for income taxes 986 262 535 Net loss $ (290,138 ) $ (83,515 ) $ (53,370 ) Year Ended January 31, 2022 2021 2020 (in thousands) Cost of revenue: Cost of license $ — $ — $ — Cost of support 8,073 1,056 401 Cost of cloud-hosted services 2,482 — — Total cost of subscription revenue 10,555 1,056 401 Cost of professional services 3,367 308 89 Total cost of revenue 13,922 1,364 490 Sales and marketing 64,991 11,286 2,466 Research and development 67,865 5,974 1,507 General and administrative 53,790 20,599 4,998 Total stock-based compensation expense $ 200,568 * $ 39,223 ** $ 9,461 ** Year Ended January 31, 2022 2021 2020 Revenue: License 15 % 17 % 15 % Support 77 78 80 Cloud-hosted services 6 2 2 Total subscription revenue 98 97 97 Professional services 2 3 3 Total revenue 100 100 100 Cost of revenue: Cost of license - - - Cost of support 12 13 15 Cost of cloud-hosted services 4 2 1 Total cost of subscription revenue 16 15 16 Cost of professional services 4 4 4 Total cost of revenue 20 19 20 Gross profit 80 81 80 Operating expenses: Sales and marketing 84 67 73 Research and development 51 31 33 General and administrative 35 23 20 Total operating expenses 170 121 126 Loss from operations (90 ) (40 ) (46 ) Other income, net - 1 2 Loss before income taxes (90 ) (39 ) (44 ) Provision for income taxes - - - Net loss (90 ) % (39 ) % (44 ) % Fiscal 2023 Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Revenue: License $ 47,504 $ 36,208 11,296 31 Support 247,566 165,607 81,959 49 Cloud-hosted services 18,613 4,092 14,521 355 Total subscription revenue 313,683 205,907 107,776 52 Professional services 7,086 5,947 1,139 19 Total revenue $ 320,769 $ 211,854 108,915 51 2024. The increase is offset by a $3.5 million decrease related to revenue recognized from a resale contract commitment in fiscal 2023. Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Cost of revenue: Cost of license $ 221 $ 536 (315 ) (59 ) Cost of support 38,080 27,194 10,886 40 Cost of cloud-hosted services 14,031 4,811 9,220 192 Total cost of subscription revenue 52,332 32,541 19,791 61 Cost of professional services 11,108 8,511 2,597 31 Total cost of revenue $ 63,440 $ 41,052 22,388 55 Year Ended January 31, 2022 2021 Gross margin License 100 % 99 % Support 85 % 84 % Cloud-hosted services 25 % (18 ) % Total subscription margin 83 % 84 % Professional services (57 ) % (43 ) % Total gross margin 80 % 81 % margin profile will change because we have a lower gross margin on cloud-hosted services due to headcount related to our cloud offering operations and cloud hosting fees. service. our professional services and other margin. Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Sales and marketing $ 269,504 $ 141,018 128,486 91 respectively. Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Research and development $ 165,031 $ 65,248 99,783 153 Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) General and administrative $ 112,108 $ 48,545 63,563 131 Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Other income, net $ 162 $ 756 (594 ) (79 ) Year Ended January 31, Change 2022 2021 $ % (in thousands, except percentages) Provision for income taxes $ 986 $ 262 724 276 2024, fiscal Year Ended January 31, 2022 2021 2020 (in thousands) Net cash used in operating activities $ (56,215 ) $ (39,623 ) $ (28,365 ) Net cash provided by (used in) investing activities $ (6,596 ) $ 22,776 $ 46,020 Net cash provided by financing activities $ 1,147,846 $ 177,124 $ 1,071 and $26.4 million of cash inflows from maturities and sales of investments, respectively. equipment. Activities settlement. taxes related to net share settlement. Payment Due By Period Total Less Than 1-3 Years 3-5 Years More Than (in thousands) Operating leases $ 20,603 $ 3,781 $ 8,074 $ 7,471 $ 1,277 Hosting Infrastructure Commitments 29,638 6,569 23,069 - - Non-cancelable purchase obligations 29,883 16,820 13,063 - - Total $ 80,124 $ 27,170 $ 44,206 $ 7,471 $ 1,277 business payments of $10.5 million due in the next 12 months and $1.6 million due thereafter. We expect to fund these obligations with cash flows from operations and cash on our balance sheet. Critical accounting estimates are accounting estimates where the nature of the estimates is material due to the levels of subjectivity and judgment necessary to account for highly uncertain matters or the susceptibility of such matters to change, and the impact of the estimates on financial condition or operating performance is material. recognition. obtaining a contract with a customer. Sales commissions for Year Ended January 31, 2022 2021 2021 Expected volatility 49.0% - 50.2% 50.0% - 51.4% 47.3% - 54.1% Expected term (in years) 6.08 6.08 6.08 Risk-free interest rate 0.9% - 1.04% 0.5% - 0.6% 1.4% - 2.6% Dividend yield 0% 0% 0% pronouncements. There have been no material changes in our market risk exposures during fiscal 2024. Declines in interest rates, however, would reduce our future interest income. Internal Control—Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission and our report dated March 20, 2024, expressed an unqualified opinion on the Company's internal control over financial reporting. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion. 20, 2024 As of January 31, 2022 2021 Assets Current assets Cash and cash equivalents $ 1,355,828 $ 270,793 Accounts receivable, net of allowance of $20 and $36, respectively 126,812 93,462 Deferred contract acquisition costs 32,205 15,275 Prepaid expenses and other current assets 17,744 4,574 Total current assets 1,532,589 384,104 Property and equipment, net 15,897 8,235 Operating lease right-of-use assets 15,420 15,766 Deferred contract acquisition costs, non-current 57,126 34,970 Other assets, non-current 2,643 2,189 Total assets $ 1,623,675 $ 445,264 Liabilities, Redeemable Convertible Preferred Stock, and Stockholders’ Equity (Deficit) Current liabilities: Accounts payable $ 14,267 $ 5,203 Accrued expenses and other current liabilities 4,542 2,138 Accrued compensation and benefits 56,939 19,213 Operating lease liabilities 3,130 2,389 Deferred revenue 206,416 136,091 Customer deposits 23,383 22,219 Total current liabilities 308,677 187,253 Deferred revenue, non-current 16,873 11,206 Operating lease liabilities, non-current 15,483 16,755 Other liabilities, non-current 351 2,741 Total liabilities 341,384 217,955 Commitments and contingencies (note 8) Redeemable convertible preferred stock Redeemable convertible preferred stock; $0.000015 par value; 0 and 94,127,984 shares authorized as of January 31, 2022 and 2021, respectively; 0 and 94,127,984 shares issued and outstanding as of January 31, 2022 and 2021, respectively; aggregate liquidation preference of $0 and $349,760 as of January 31, 2022 and 2021, respectively - 349,113 Stockholders’ equity (deficit) Preferred stock; $0.000015 par value; 100,000,000 and 0 shares authorized as of January 31, 2022 and 2021, respectively; 0 and 0 shares issued and outstanding as of January 31, 2022 and 2021, respectively - - Class A common stock, par value of $0.000015 per share; 1,000,000,000 and 0 shares authorized as of January 31, 2022 and 2021, respectively; 30,596,695 and 0 shares issued and outstanding as of January 31, 2022 and 2021, respectively 1 - Class B common stock, par value of $0.000015 per share; 200,000,000 and 192,000,000 shares authorized as of January 31, 2022 and 2021, respectively; 151,569,865 and 65,577,877 shares issued and outstanding as of January 31, 2022 and 2021, respectively 2 1 Additional paid-in capital 1,788,390 94,159 Accumulated deficit (506,102 ) (215,964 ) Total stockholders’ equity (deficit) 1,282,291 (121,804 ) Total liabilities, redeemable convertible preferred stock, and stockholders’ equity (deficit) $ 1,623,675 $ 445,264 Year Ended January 31, 2022 2021 2020 Revenue: License $ 47,504 $ 36,208 $ 18,503 Support 247,566 165,607 96,820 Cloud-hosted services 18,613 4,092 2,339 Total subscription revenue 313,683 205,907 117,662 Professional services 7,086 5,947 3,599 Total revenue 320,769 211,854 121,261 Cost of revenue: Cost of license 221 536 294 Cost of support 38,080 27,194 17,704 Cost of cloud-hosted services 14,031 4,811 1,390 Total cost of subscription revenue 52,332 32,541 19,388 Cost of professional services 11,108 8,511 4,527 Total cost of revenue 63,440 41,052 23,915 Gross profit 257,329 170,802 97,346 Operating expenses: Sales and marketing 269,504 141,018 89,308 Research and development 165,031 65,248 40,118 General and administrative 112,108 48,545 24,137 Total operating expenses 546,643 254,811 153,563 Loss from operations (289,314 ) (84,009 ) (56,217 ) Other income, net 162 756 3,382 Loss before income taxes (289,152 ) (83,253 ) (52,835 ) Provision for income taxes 986 262 535 Net loss $ (290,138 ) $ (83,515 ) $ (53,370 ) Net loss per share attributable to common stockholders, basic and diluted $ (3.48 ) $ (1.32 ) $ (0.90 ) Weighted-average shares used to compute net loss per share attributable to common stockholders, basic and diluted 83,276,526 63,375,470 59,161,264 COMPREHENSIVE LOSS thousands) Redeemable Convertible Preferred Stock Class A and Class B Additional Paid-in Accumulated Total Stockholders' Shares Amount Shares Amount Capital Deficit Equity (Deficit) Balance as of February 1, 2019 88,076,852 $ 174,389 58,967,390 $ 1 $ 41,509 $ (79,079 ) $ (37,569 ) Issuance of common stock upon exercise of stock options - - 2,289,774 - 1,048 - 1,048 Issuance of common stock related to early exercised stock options - - 190,000 - - - - Vesting of early exercised stock options - - - - 190 - 190 Stock-based compensation - - - - 9,461 - 9,461 Net loss - - - - - (53,370 ) (53,370 ) Balance as of January 31, 2020 88,076,852 $ 174,389 61,447,164 $ 1 $ 52,208 $ (132,449 ) $ (80,240 ) Issuance of Series E redeemable convertible preferred stock, net of issuance costs of $276 6,051,132 174,724 - - - - - Issuance of common stock upon exercise of stock options - - 4,130,713 - 2,629 - 2,629 Vesting of early exercised stock options - - - - 99 - 99 Stock-based compensation - - - - 39,223 - 39,223 Net loss - - - - (83,515 ) (83,515 ) Balance as of January 31, 2021 94,127,984 $ 349,113 65,577,877 $ 1 $ 94,159 $ (215,964 ) $ (121,804 ) Conversion of redeemable convertible preferred stock to common stock upon initial public offering (94,127,984 ) $ (349,113 ) 94,127,984 1 349,112 - 349,113 Issuance of common stock upon initial public offering, net of underwriting discounts and issuance costs - - 16,530,000 1 1,246,924 - 1,246,925 Issuance of common stock for restricted stock awards - - 10,564 - - - - Issuance of common stock upon exercise of stock options - - 2,961,753 - 5,036 - 5,036 Vesting of early exercised stock options - - - - 18 - 18 Issuance of common stock upon settlement of restricted stock units - - 4,355,635 - - - - Tax withholdings on settlement of restricted stock units - - (1,397,253 ) - (110,989 ) - (110,989 ) Stock-based compensation - - - - 204,130 - 204,130 Net loss - - - - - (290,138 ) (290,138 ) Balance as of January 31, 2022 - $ - 182,166,560 $ 3 $ 1,788,390 $ (506,102 ) $ 1,282,291 Year Ended January 31, 2022 2021 2020 Cash flows from operating activities Net loss $ (290,138 ) $ (83,515 ) $ (53,370 ) Adjustments to reconcile net loss to cash from operating activities: Stock-based compensation expense 200,568 39,223 9,461 Depreciation and amortization expense 2,498 888 235 Non-cash operating lease cost 2,382 2,098 1,263 Other 14 57 5 Changes in operating assets and liabilities: Accounts receivable (33,364 ) (41,407 ) (27,698 ) Deferred contract acquisition costs (39,086 ) (19,984 ) (15,920 ) Prepaid expenses and other assets (13,626 ) 2,653 (3,436 ) Accounts payable 8,464 1,093 2,423 Accrued expenses and other liabilities (895 ) 3,277 360 Accrued compensation and benefits 32,379 7,536 6,646 Operating lease liabilities (2,567 ) (1,789 ) (801 ) Deferred revenue 75,992 46,911 45,605 Customer deposits 1,164 3,336 6,862 Net cash used in operating activities (56,215 ) (39,623 ) (28,365 ) Cash flows from investing activities Purchases of property and equipment (214 ) (4,304 ) (980 ) Capitalized internal-use software (6,382 ) (2,920 ) - Purchase of short-term investments - (50,000 ) (120,000 ) Proceeds from maturities of short-term investments - 80,000 167,000 Net cash (used in) provided by investing activities (6,596 ) 22,776 46,020 Cash flows from financing activities Proceeds from initial public offering, net of underwriting discounts and commissions 1,252,974 - - Taxes paid related to net share settlement of equity awards (105,642 ) - - Payments of loan issuance costs - (229 ) - Proceeds from issuance of redeemable convertible preferred stock, net of issuance costs - 174,724 - Proceeds from issuance of common stock upon exercise of stock options 5,036 2,629 1,048 Proceeds from issuance of common stock related to early exercised stock options - - 23 Payments of deferred offering costs (4,522 ) - - Net cash provided by financing activities 1,147,846 177,124 1,071 Net increase in cash, cash equivalents, and restricted cash 1,085,035 160,277 18,726 Cash, cash equivalents, and restricted cash beginning of period 272,576 112,299 93,573 Cash, cash equivalents, and restricted cash end of period $ 1,357,611 $ 272,576 $ 112,299 Supplemental disclosure of cash flow information Cash paid for income taxes $ 739 $ 452 $ 119 Cash paid for operating lease liabilities $ 3,291 $ 2,479 $ 1,379 Supplemental disclosure of noncash investing and financing activities Purchase of property and equipment included in accounts payable $ - $ - $ 1,283 Operating lease right-of-use assets obtained in exchange for new lease obligations $ 2,036 $ - $ 10,829 Tenant allowance included in prepaid expenses and other current assets $ - $ - $ 1,666 Unpaid deferred offering costs $ 1,527 $ - $ - Unpaid taxes related to net share settlement of equity awards $ 5,347 $ - $ - Conversion of convertible preferred stock to common stock upon initial public offering $ 349,113 $ - $ - Capitalized stock-based compensation expense $ 3,562 $ - $ - Vesting of early exercised stock options $ 18 $ 99 $ 190 Basis of Presentation Principles of Consolidation Fiscal Year Foreign Currency Transactions Use of Estimates Cash and Cash Equivalents As of January 31, 2022 2021 2020 Cash and cash equivalents $ 1,355,828 $ 270,793 $ 110,519 Restricted cash included in other assets, non-current 1,783 1,783 1,780 Cash, cash equivalents, and restricted cash $ 1,357,611 $ 272,576 $ 112,299 Accounts Receivable and Allowance for Doubtful Accounts The allowance for credit losses reflects the Company’s best estimate of probable losses inherent in the Company’s receivables portfolio. Activity related to the Company’s allowance for doubtful accounts was as follows (in thousands): Year Ended January 31, 2022 2021 2020 Beginning balance $ 36 $ 6 $ 68 Bad debt expense 14 129 (62 ) Write-offs (30 ) (99 ) - Ending balance $ 20 $ 36 $ 6 Concentrations of Credit Risk and Significant Customers Property and Equipment, net Revenue Recognition services and other revenue. The software subscriptions are currently predominantly self-managed by users and customers who deploy it across public, private, and hybrid cloud environments. The Company also offers the HashiCorp Cloud Platform, or HCP, our fully-managed cloud platform for multiple products. substantial portion of the revenue that we report in each period is attributable to the recognition of deferred revenue relating to agreements that we entered into during previous periods. Consequently, increases or decreases in new sales or renewals in any one period may not be immediately reflected as revenue for that period. Any downturn in sales, however, may negatively affect our revenue in future periods. Accordingly, the effect of downturns in sales and market acceptance of our products, and potential changes in our rate of renewals, may not be fully reflected in our results of operations until future periods. Contract Balances Deferred Contract Acquisition Costs Leases Cost of Revenue Sales and Marketing Research and Development General and Administrative Capitalized Software Development Costs Advertising Costs Impairment of Long-Lived Assets The Company has master netting agreements with each of its counterparties, which permit net settlement of multiple, separate derivative contracts with a single payment. The Company does not have collateral requirements with any of its counterparties. Although the Company is allowed to present the fair value of derivative instruments on a net basis according to master netting arrangements, the Company has elected to present its derivative instruments on a gross basis in the consolidated financial statements. Net Loss per Share Attributable to Common Stockholders outstanding for the period using the treasury stock method or the if-converted method based on the nature of such securities. Diluted net loss per share is the same as basic net loss per share in periods when the effects of potentially dilutive shares of common stock are anti-dilutive. Accumulated Other Comprehensive Segments Fair Value Measurements Employee Benefit Plan Recent Accounting Pronouncements Not Yet Adopted Revenue The following table presents revenue by category (dollars in thousands): Year Ended January 31, 2022 2021 2020 Amount % of Total Amount % of Total Amount % of Total Revenue License $ 47,504 15 % $ 36,208 17 % $ 18,503 15 % Support 247,566 77 165,607 78 96,820 80 Cloud-hosted services 18,613 6 4,092 2 2,339 2 Total subscription revenue 313,683 98 205,907 97 117,662 97 Professional services 7,086 2 5,947 3 3,599 3 Total revenue $ 320,769 100 % $ 211,854 100 % $ 121,261 100 % Year Ended January 31, 2022 2021 2020 Amount % of Total Amount % of Total Revenue Amount % of Total Revenue United States $ 235,428 73 % $ 157,916 75 % $ 92,771 77 % Rest of the world 85,341 27 53,938 25 28,490 23 Total $ 320,769 100 % $ 211,854 100 % $ 121,261 100 % Changes in deferred revenue and unbilled accounts receivable were as follows (in thousands): Year Ended January 31, 2022 2021 2020 Balance, beginning of period $ 147,297 $ 100,386 $ 54,781 Billings, excluding billings for customer deposits 364,365 228,498 149,139 Reclassification to deferred revenue from customer deposits 30,788 29,046 18,331 Recognition of revenue, net of change in unbilled accounts receivable* (319,161 ) (210,633 ) (121,865 ) Balance, end of period $ 223,289 $ 147,297 $ 100,386 * Reconciliation to Revenue Reported per Consolidated Statements of Operations: Revenue billed as of the end of the period $ 319,161 $ 210,633 $ 121,865 Increase (decrease) in total unbilled accounts receivable 1,608 1,221 (604 ) Revenue Reported per Consolidated Statements of Operations $ 320,769 $ 211,854 $ 121,261 The following tables summarize the fair values of the Company’s short-term investments (in thousands): As of January 31, 2022 2021 Within the next 12 months $ 20,324 $ 20,421 After the next 12 months 3,059 1,798 Total $ 23,383 $ 22,219 The Company does not hold any marketable securities that have been in a continuous unrealized loss position for over 12 months. For short-term investments with an unrealized loss at January 31, 2024, the unrealized losses were not due to credit-related factors, the Company does not intend to sell these short-term investments, and it is more likely than not that the Company will hold these short-term investments until maturity or a recovery of the cost basis. Therefore, no allowance for expected credit losses was recorded as of January 31, 2024. Realized gains (losses) were not material during the year ended January 31, 2024. The following table sets forth the financial assets, measured at fair value, by level within the fair value hierarchy on a recurring basis As of January 31, 2022 Level 1 Level 2 Level 3 Total Cash and cash equivalents Money market funds $ 1,129,436 $ 0 $ 0 $ 1,129,436 Total cash and cash equivalents 1,129,436 0 0 1,129,436 Total assets measured at fair value $ 1,129,436 $ 0 $ 0 $ 1,129,436 Included in cash and cash equivalents $ 1,129,436 As of January 31, 2021 Level 1 Level 2 Level 3 Total Cash and cash equivalents Money market funds $ 151,657 $ 0 $ 0 $ 151,657 Total cash and cash equivalents 151,657 0 0 151,657 Total assets measured at fair value $ 151,657 $ 0 $ 0 $ 151,657 Included in cash and cash equivalents $ 151,657 Property and equipment, net are comprised of the following (in thousands): Estimated As of January 31, Useful life 2022 2021 Furniture and fixtures 5 years $ 1,266 $ 1,224 Computers, equipment and software 3 years 532 389 Capitalized internal-use software development costs 5 years 12,209 2,920 Leasehold improvements Shorter of useful life or lease term 5,008 4,979 Construction in progress(1) 655 - Total property and equipment 19,670 9,512 Less: accumulated depreciation and amortization (3,773 ) (1,277 ) Property and equipment - net $ 15,897 $ 8,235 Accrued expenses and other liabilities are comprised of the following (in thousands): As of January 31, 2022 2021 Accrued expenses $ 3,925 $ 569 Accrued income taxes payable 611 354 Liability for early exercise of unvested stock options 6 24 Sales tax payable - 1,191 Total accrued expenses and other liabilities $ 4,542 $ 2,138 Accrued compensation and benefits are comprised of the following (in thousands): As of January 31, 2022 2021 Accrued commissions $ 15,993 $ 9,862 Accrued bonus 2,632 1,725 Accrued vacation 15,970 1,900 Accrued payroll and withholding taxes 18,885 5,296 ESPP employee contribution 2,709 - Other 750 430 Total accrued compensation and benefits $ 56,939 $ 19,213 The following table summarizes the activity of the deferred contract acquisition costs (in thousands): Year Ended January 31, 2022 2021 2020 Beginning balance $ 50,245 $ 30,261 $ 14,341 Capitalization of contract acquisition costs 64,834 33,821 22,668 Amortization of deferred contract acquisition costs (25,748 ) (13,837 ) (6,748 ) Ending balance $ 89,331 $ 50,245 $ 30,261 Deferred contract acquisition costs, current $ 32,205 $ 15,275 $ 8,754 Deferred contract acquisition costs, non-current 57,126 34,970 21,507 Total deferred contract acquisition costs $ 89,331 $ 50,245 $ 30,261 Lease costs were as follows (in thousands): Year Ended January 31, 2022 2021 2020 Short-term lease costs $ 333 $ 227 $ 98 Operating lease costs 3,106 2,898 1,842 Total lease costs $ 3,439 $ 3,125 $ 1,940 Lease term and discount rate information are summarized as follows: As of January 31, 2022 2021 2020 Weighted average remaining lease terms (in years) 5.1 6.3 7.3 Weighted average discount rate 3.8 % 3.9 % 3.9 % Years Ending January 31, Amount 2023 $ 3,781 2024 3,924 2025 4,150 2026 3,734 2027 3,737 Thereafter 1,277 Total minimum lease payments 20,603 Less imputed interest (1,990 ) Present value of future minimum lease payments 18,613 Less current lease liabilities (3,130 ) Operating lease liabilities, non-current $ 15,483 spaces. Litigation Years Ending January 31, Minimum Hosting Other Total (in thousands) 2023 $ 3,781 $ 6,569 $ 7,386 $ 17,736 2024 3,924 9,246 7,076 20,246 2025 4,150 9,656 4,823 18,629 2026 3,734 4,167 - 7,901 2027 3,737 - - 3,737 Thereafter 1,277 - - 1,277 Total $ 20,603 $ 29,638 $ 19,285 $ 69,526 Shares Authorized Issued and Outstanding Carrying Value Liquidation Preference Issue Price per Share Series Seed 8,418,228 8,418,228 $ 560 $ 560 $ 0.07 Series A 23,575,316 23,575,316 10,114 10,200 $ 0.43 Series B 34,434,922 34,434,922 23,927 24,000 $ 0.70 Series C 12,625,844 12,625,844 39,909 40,000 $ 3.17 Series D 9,022,542 9,022,542 99,879 100,000 $ 11.08 Series E 6,051,132 6,051,132 174,724 175,000 $ 28.92 Total 94,127,984 94,127,984 $ 349,113 $ 349,760 The Company reserved shares of common stock for future issuance as As of January 31, 2022 2021 Series Seed convertible preferred stock - 8,418,228 Series A convertible preferred stock - 23,575,316 Series B convertible preferred stock - 34,434,922 Series C convertible preferred stock - 12,625,844 Series D convertible preferred stock - 9,022,542 Series E convertible preferred stock - 6,051,132 2014 Stock Plan: Options outstanding - 15,575,113 Restricted stock units outstanding - 8,616,594 Remaining shares available for future issuance under the 2014 Plan - 637,212 2021 Equity Incentive Plan: Options outstanding 12,381,134 - Restricted stock units outstanding 10,406,294 - Remaining shares available for future issuance under the 2021 Plan 17,560,879 - 2021 Employee Stock Purchase Plan 1,900,000 - Total 42,248,307 118,956,903 As of January 31, 2022 2021 Available at beginning of period 637,212 208,924 Awards authorized 23,051,200 5,654,722 Options granted (69,700 ) (54,500 ) Options cancelled 301,926 269,326 RSUs granted (7,106,578 ) (5,858,686 ) RSUs cancelled 961,243 417,426 Termination of the 2014 Plan (1,611,677 ) - Shares withheld related to net share settlement of RSUs 1,397,253 - Available at end of period 17,560,879 637,212 Stock Options The following table summarizes stock option activity for the Options Outstanding Number of Options Outstanding Weighted- Average Exercise Price Weighted- Average Remaining Contractual Term (in Years) Aggregate Intrinsic Value Balance as of January 31, 2021 15,575,113 $ 1.77 6.7 $ 372,671 Stock options granted 69,700 $ 28.34 Stock options exercised (2,961,753 ) $ 1.68 $ 168,258 Stock options cancelled/forfeited/expired (301,926 ) $ 2.12 Balance as of January 31, 2022 12,381,134 $ 1.93 5.7 $ 798,374 Exercisable as of January 31, 2022 10,536,517 $ 1.39 5.5 $ 684,903 The weighted-average grant-date fair values of option awards granted during fiscal 2022 The Company’s summary of RSUs activity under the 2014 Plan and the 2021 Plan is as Number of Awards Weighted-Average Grant Date Fair Value Outstanding and unvested at January 31, 2021 8,616,594 $ 15.78 RSUs granted 7,106,578 $ 48.88 RSUs released (4,355,635 ) $ 16.32 RSUs cancelled (961,243 ) $ 23.33 Outstanding and unvested at January 31, 2022 10,406,294 $ 37.46 The fair value of the purchase rights granted under the ESPP was estimated on the date of grant using the Black-Scholes option pricing model. The following table summarizes the assumptions used in the Black-Scholes option-pricing model Total stock-based compensation expense recognized in the Company’s consolidated statements of operations is as follows (in thousands): Year Ended January 31, 2022 2021 2020 Cost of license $ - $ - $ - Cost of support 8,073 1,056 401 Cost of cloud-hosted services 2,482 - - Cost of professional services 3,367 308 89 Sales and marketing 64,991 11,286 2,466 Research and development 67,865 5,974 1,507 General and administrative 53,790 20,599 4,998 Stock-based compensation expenses $ 200,568 $ 39,223 $ 9,461 Capitalized stock-based compensation 3,562 - - Total stock-based compensation expense $ 204,130 $ 39,223 $ 9,461 Year Ended January 31, 2022 2021 2020 Cost of license $ - $ - $ - Cost of support - 650 - Cost of cloud-hosted services - - - Cost of professional services - 210 - Sales and marketing - 8,895 - Research and development - 4,199 - General and administrative - 18,097 1,524 Stock-based compensation expense $ - $ 32,051 $ 1,524 Capitalized stock-based compensation - - - Total stock-based compensation $ - $ 32,051 $ 1,524 Year Ended January 31, 2022 2021 2020 Cost of license $ - $ - $ - Cost of support 8,073 406 401 Cost of cloud-hosted services 2,482 - - Cost of professional services 3,367 98 89 Sales and marketing 64,991 2,391 2,466 Research and development 67,865 1,775 1,507 General and administrative 53,790 2,502 3,474 Stock-based compensation expense $ 200,568 $ 7,172 $ 7,937 Capitalized stock-based compensation 3,562 - - Total stock-based compensation $ 204,130 $ 7,172 $ 7,937 As of January 31, Year Ended January 31, 2022 2021 2020 Fair value of common stock $28.94 - $47.07 $16.52-$23.37 $5.44 - $10.34 Expected volatility 49.0% - 50.2% 50.0% - 51.4% 47.3% - 54.1% Expected term (in years) 6.08 6.08 6.08 Risk-free interest rate 0.9% - 1.04% 0.5% - 0.6% 1.4% - 2.6% Dividend yield 0% 0% 0% Year Ended January 31, 2022 2021 2020 Numerator: Net loss $ (290,138 ) $ (83,515 ) $ (53,370 ) Denominator: Weighted-average shares used to compute net loss per share attributable to Class A and Class B common stockholders, basic and diluted 83,276,526 63,375,470 59,161,264 Net loss per share attributable to Class A and Class B common stockholders, basic and diluted $ (3.48 ) $ (1.32 ) $ (0.90 ) The following outstanding potentially dilutive shares of common stock were excluded from the computation of diluted net loss per share attributable to common stockholders for the periods presented because the impact of including them would have been Year Ended January 31, 2022 2021 2020 Redeemable convertible redeemable preferred stock - 94,127,984 88,076,852 Stock awards 22,787,428 24,191,707 23,095,986 Share purchase rights under the ESPP 703,862 - - Class A and Class B common stock subject to repurchase 5,250 40,052 397,910 Total 23,496,540 118,359,743 111,570,748 The Company’s loss before income taxes was as follows (in thousands): Year Ended January 31, 2022 2021 2020 Domestic $ (294,299 ) $ (86,845 ) $ (54,236 ) International 5,147 3,592 1,401 Loss before income taxes $ (289,152 ) $ (83,253 ) $ (52,835 ) Year Ended January 31, 2022 2021 2020 Current provisions for income taxes: Federal $ - $ - $ - State 48 9 15 Foreign 1,125 401 520 Total current tax expense 1,173 410 535 Deferred tax expense: Federal - - - State - - - Foreign (187 ) (148 ) - Total deferred tax expense (187 ) (148 ) - Provision for income taxes $ 986 $ 262 $ 535 Year Ended January 31, 2022 2021 2020 U.S. federal tax benefit at statutory rate 21.0 % 21.0 % 21.0 % State income taxes, net of federal benefit 8.2 6.9 4.8 Foreign earnings taxed at different rate 0.6 0.6 (0.4 ) Stock-based compensation 13.1 8.0 (0.7 ) Non-deductible expenses and other (0.7 ) (0.2 ) (1.1 ) Research and development credits 2.9 1.9 2.0 Change in valuation allowance, net (45.4 ) (38.5 ) (26.6 ) Effective tax rate (0.3 ) % (0.3 ) % (1.0 ) % Year Ended January 31, 2022 2021 2020 Deferred tax assets: Net operating losses $ 167,218 $ 62,279 $ 28,920 Deferred revenue 2,687 3,493 3,279 Lease liability 4,772 4,943 5,449 Other accruals 5,542 2,436 479 Stock-based compensation 25,772 1,963 1,459 Credit carryforwards 18,883 6,468 4,829 Total deferred tax assets $ 224,874 $ 81,582 $ 44,415 Year Ended January 31, 2022 2021 2020 Deferred tax liabilities: Fixed assets $ (2,837 ) $ (943 ) $ (489 ) Right-of-use asset (3,953 ) (4,071 ) (4,650 ) Deferred commissions (22,900 ) (12,974 ) (7,877 ) Total deferred tax liabilities $ (29,690 ) $ (17,988 ) $ (13,016 ) Net deferred tax assets $ 195,184 $ 63,594 $ 31,399 Valuation allowance (194,850 ) (63,446 ) (31,399 ) Deferred tax assets, net of valuation allowance $ 334 $ 148 $ - The Company’s reconciliation of the total amounts of unrecognized tax benefits was as follows (in thousands): Year Ended January 31, 2022 2021 Unrecognized tax benefits as of the beginning of the year $ 1,730 $ 1,236 Increases related to prior year tax provisions 475 - Decrease related to prior year tax provisions - (56 ) Increase related to current year tax provisions 2,644 550 Unrecognized tax benefits as of the end of the year $ 4,849 $ 1,730 this Annual Report on Form 10-K. Exhibit Description Form File No. Exhibit Filing Date Number 3.1 Amended and Restated Certificate of Incorporation of the Registrant. 8-K 001-41121 3.1 12/13/2021 3.2 8-K 001-41121 3.2 12/13/2021 4.1 S-1 333-260757 4.1 11/04/2021 4.2 S-1/A 333-260757 4.2 11/17/2021 4.3* 10.1+ S-1 333-260757 10.1 11/4/2021 10.2+ 2014 Stock Plan, as amended, and forms of agreement thereunder. S-1 333-260757 10.2 11/4/2021 10.3+ 2021 Equity Incentive Plan and forms of agreement thereunder. S-1 333-260757 10.3 11/4/2021 10.4+ S-1 333-260757 10.4 11/4/2021 10.5+ Confirmatory Offer Letter between the Registrant and Armon Dadgar. S-1 333-260757 10.5 11/4/2021 10.6+ Confirmatory Offer Letter between the Registrant and Marc Holmes. S-1 333-260757 10.6 11/4/2021 10.7+ Confirmatory Offer Letter between the Registrant and David McJannet. S-1 333-260757 10.7 11/4/2021 10.8+ Confirmatory Offer Letter between the Registrant and Brandon Sweeney. S-1 333-260757 10.8 11/4/2021 10.9+ Confirmatory Offer Letter between the Registrant and Navam Welihinda. S-1 333-260757 10.9 11/4/2021 10.10+ S-1 333-260757 10.10 11/4/2021 10.11+ S-1/A 333-260757 10.10 11/17/2021 10.12+ S-1 333-260757 10.11 11/04/2021 10.13 S-1 333-260757 10.12 11/04/2021 21.1* 23.1* Consent of Deloitte & Touche LLP, independent registered public accounting firm. 31.1* 32.1*† 32.2*† 104 Cover Page Interactive Data File (formatted as inline XBRL with applicable taxonomy extension information contained in Exhibits 101). Date: March By: /s/ Navam Welihinda Navam Welihinda /s/ David McJannet Chief Executive Officer and Chairman of the Board March, David McJannet (Principal Executive Officer) /s/ Navam Welihinda Chief Financial Officer March, Navam Welihinda (Principal Financial and Accounting Officer) /s/ Armon Dadgar Director March, Armon Dadgar /s/ Susan St. Ledger Director March, Susan St. Ledger Todd Ford Director David Henshall Director March, Glenn Solomon /s/ Sigal Zarmi Director March, Sigal ZarmiConsulBoundary is the basis for a complete Zero Trust security architecture with identity-driven controls, offering a full range of authentication, authorization, and access management for human users or machines, like servers or applications. We continue to innovate and deliver additional emerging products to supplement these core capabilities and provide adjacent solutions.thatto further acceleratesaccelerate enterprise cloud migration by addressing resource and skills gaps, improving operational efficiency, and speeding up deployment time for customers.3companies of all sizes and industries use our products which wereare ubiquitous in the largest enterprises. Our products have been downloaded over 250 million times duringand are used in 85% of the fiscal year endedFortune 500 as of January 31, 2022, or fiscal 2022. While we are pleased with this result, we also note that the number of downloads of our open-source products can fluctuate significantly from year-to-year due to various factors, including the timing of new product and feature releases.a key IT deployment decision makermakers at many enterprises, standardize on our platform over time as they build their cloud adoption strategies and programs around their chosen cloud vendors and HashiCorp in concert with their cloud service providers of choice and existing ISVs. Enabling users to work within their existing infrastructure vendors creates a strong network effect with our products. We had over 2,0003,900 providers and integrations and more than 8501060 partners, including over 200320 ISVs, as of January 31, 2022,2024, and thesethese numbers continue to grow as we become mission critical to our customers and increasingly integral to their entire ecosystem.20222024 and January 31, 20212023 our last four quarterfour-quarter average net dollar retention rate wasrates were 115% and 131% and 123%, respectively. We are still in the early stages of our expansion and extension journey with our customers. Our focus on winning lighthouse accounts in the Forbes Global 2000 accelerates our practitioner adoption by adding new users and driving partners to integrate our ecosystem, creating a powerful flywheel helping to drive our business.655, 500897, 798, and 338655 customers with $100,000 or greater annual recurring revenue, or ARR as of January 31, 2024, 2023, and 2022 2021 and 2020, respectively. We served over 375480 of the Forbes Global 2000 companies as of January 31, 2022.2024. Our revenue was $583.1 million, $475.9 million, and $320.8 million $211.9 million,for the fiscal year ended January 31, 2024, or fiscal 2024, the fiscal year ended January 31, 2023, or fiscal 2023, and $121.3 million for the fiscal year ended January 31, 2022, or fiscal 2022, the fiscal year ended January 31, 2021, or fiscal 2021, and the fiscal year ended January 31, 2020, or fiscal 2020, respectively, representing period-over-period growth of 51%23% and 75%48%, respectively. Customers with $100,000 or greater ARR represented 88%89%, 83%88%, and 71%88% of revenue for fiscal 2022, 2021,2024, fiscal 2023, and 2020,fiscal 2022, respectively. We incurred net losses of $290.1$190.7 million, $83.5$274.3 million, and $53.4$290.1 million for fiscal 2022, 2021,2024, fiscal 2023, and 2020,fiscal 2022, respectively. We expect we will incur net losses for the foreseeable future as we continue to invest into the market opportunity ahead of us.industries.industries. Our HashiCorp User Groups, or HUGs, are self-organizing chapters of users that advocate for our products, which include over 38,00051,000 members in more than 140180 chapters across over 5060 countries as of January 31, 2022.2024.516,00055,000 of whom have completed our certification programs as of January 31, 2022.2024. By leveraging our products, customers can more easily hire new employees, train and certify existing employees, and ensure their organizations retain expertise in managing their systems.customers.customers. We served 2,7154,423 total customers as of January 31, 2022,2024, including over 375480 of the Forbes Global 2000. We believe that nearly all organizations will adopt a cloud strategy, resulting in a substantial opportunity to continue growing our customer base. Nearly all of our paid product adoption began with open-source usage. As we continue to cultivate those users and turn them into paid customers, we also intend to drive new paying customer additions by expanding our sales and marketing efforts and our product portfolio.6Consumption-basedThe HashiCorp Flex pricing allowsprogram initially launched in March 2022, offers certain customers consumption-based pricing, which in turn enables them to align spend with usage and also provides an organic way to increase monetization with thenaturally expand their adoption and usage of our products.thethe top systems integrators and resellers around the world, helps accelerate the adoption of our products and platform. In addition, we maintain and manage hundredsthousands of integrations, like our Terraform Providers. These include more than 30 official providers (created by us), more than 180320 verified providers (created by our community and verified by us), and more than 1,6003,500 community providers (created by our community) as of January 31, 2022.2024. We plan to continue investing in building out our partner program to drive more consumption through our platform, broaden our distribution footprint, and create greater awareness of our platform.27% of our revenue30% and 25%27% of our revenue for fiscal 20222024 and 2021,2023, respectively. We plan to make investments in sales and marketing and customer support in geographic areas of focus, and we believe there is a large opportunity to increase our global presence over time.implementadopt a cloud operating model that provides consistent workflows and a standardized approach to automating the critical processes involved in deliveringprovisioning, security, networking, and application delivery to deliver applications to any environment. Our offerings require multiple foundational capabilities that span all environments. We organize our products around four primary functionalities:at scaleat-scale automation by codifying how infrastructure is configured and deployed, along with the security and governance controls that provide guardrails.7not to evolve,be relatively consistent over time, while technology continues to change at a blistering pace. Making the products extensible and pluggable to support new technologies as they evolve keeps our products relevant and increases their utility for customers, who can embrace legacy and modern systems today and hedge against new systems emerging in the future.VaultWaypoint products are available as managed services through HCP, while our Packer product is available as a beta service through HCP. We believe enterprise customers will become increasingly comfortable, over the long term, with infrastructure services being provided by a third party, and SMB customers will benefit from the ease of adopting fully-managed products. Our ability to reduce operational complexity, speed up deployment and adoption times, provide multi-cloud consistency, and address the skills gap will be a critical driver of adoption. The shared identity and unified experience provided by the platform enable us to deeply integrate our products, creating a more powerful experience that drives additional usage of each product, as well as adoption of new products and services.inside sales leadinside-sales led motion to drive high velocity deals. Cloud customers can spend significantly less time focused on product deployment and immediately start product adoption, which enables higher retention and expansion.Nomad,Packer, are earlier in the commercialization process,cycle, while our community products are focused on product development, market maturity, and community adoption. This framework enables us to continue innovating and adding new products to our portfolio while simultaneously executing on a go-to-market strategy for our commercial products. 8infrastructure provisioninginfrastructure-provisioning product and empowers practitioners to create and manage infrastructure at scale for any public cloud andor private cloud environment. Terraform takes an infrastructure-as-code approach to provisioning and lifecycle management, transforming these workflows from ticket-based manual processes into end-to-end self-service infrastructure automation.TheseThe companies that use APIs often build providers for their own technologies to connect with HashiCorp. As of January 31, 2022,2024, Terraform has more than 30 official providers (created by us), more than 180320 verified providers (created by our community and verified by us), and more than 1,6003,500 community providers (created by our community).EnterpriseEnterprise are commercial offerings that provide a centralized way for users to collaborate on infrastructure, define and share reusable modules, provide central visibility, and enforce policy controls. The open-source Terraform product is focused on solving the technical challenge of provisioning, and our HashiCorp community provides thousands of provider integrations and shared blueprints in a public registry, allowing for the advancement of these products. Terraform Cloud and Terraform Enterprise, our commercial offerings, enable enterprises to operationalize Terraform, and pricing is based on the number of workspaces managed by our product. Key use cases include enabling self-service infrastructure, enabling multi-cloud consistency, and enforcing policy and governance.production worthyproduction-worthy artifact. Depending on the environment, that artifact could be a virtual machine, or VM, image for an on-premises infrastructure, a Cloud VM image, a container, or serverless package. Packer provides a consistent way to define the process of transforming the raw source inputs into a production worthy artifact, across any environment or packaging format. This allows for a consistent approach to packaging that handles the nuances and variations in packaging for each environment.9microsegmentation,micro-segmentation, reducing the risk of a network compromise through lateral attacker movement. This focus on identity-based controls reduces the total number of controls that need to be managed and reduces the operational burden of static controls in dynamic cloud environments. Security teams can apply a consistent approach to network segmentation across all their environments regardless of the hardware or network fabric.102022,2024, we had 2,7154,423 total customers, including over 375480 of the Forbes Global 2000. As of January 31, 2022,2024, we had 655897 customers with $100,000 or greater in ARR and 72120 customers with $1.0 million or greater in ARR. For fiscal 2022,2024, no single customer accounted for more than 10% 10% of our total revenue. Our percentage of revenue generated by customers outside of the U.S. was 27%30%, 25%27%, and 23%27% for fiscal 2024, fiscal 2023, and fiscal 2022, 2021, and 2020, respectively.2022,2024, we had more than 38,00051,000 members in our user groups spanning over 5060 countries.32%36% of those who took certification exams stated they were required to by their employer. We also provide experiences,experiences, such as our annual HashiConf and HashiDays community conferences in Europe and the United States, with online viewership of approximately 7,0005,000 participants, including both virtual and in-person attendees, at the Europe event in June 20212023 and approximately 9,00013,000 attendees at the U.S.-based global event in October 2021.2023. We also support our HUGs and other community efforts globally.generation,generation, due to the mission-critical nature of our platform. On our platform, users naturally demonstrate the value of our products to their organizations, as use of our platform scales with their cloud-adoption journeys. In this process, users drive further11programsprograms based on their chosen cloud vendors and HashiCorp in concert with their cloud service providers of choice and existing ISVs.2022,2024, we had more than 850 employees860 employees in our sales and marketing organizations.2022,2024, we had more than 500680 employees in our research and development organization. We intend to continue to invest in our research and development capabilities to extend our platform. Research and development expenses totaled $165.0$222.6 million, $65.2$195.4 million, and $40.1$165.0 million for fiscal 2024, fiscal 2023, and fiscal 2022, 2021, and 2020, respectively. Red Hat, CyberArk, VMware, and IBM. We also compete with alternative open-source projects such as Google Istio.12principalprincipal purpose of our share incentive plans is to attract, retain, and reward personnel through the granting of share-based compensation awards in order to increase stockholder value and the success of our company by motivating such individuals to perform to the best of their abilities and achieve our objectives.2022,2024, we had over 1,8502200 employees operating across the world. We recognize that everyone deserves respect and equal treatment, regardless of gender, race, ethnicity, age, disability, sexual orientation, gender identity, cultural background, or religious belief and we strive to emphasize this equality as part of our core values to create a diverse,diverse, equitable, and inclusive work environment. We believe that kindness should be extended at every opportunity, to our peers, users, partners, and customers. An internal environment that is friendly, kind, and forgiving of mistakes is positive and productive. None of our employees are represented by a labor union. In certain countries in which we operate, such as France, we are subject to, and comply with, local labor law requirements, which may automatically make our employees subject to industry-wide collective bargaining agreements. We have not experienced any work stoppages, and we consider our relations with our employees to be good.2022,2024, we held six18 issued U.S. patents, had onethree other U.S. patent applicationapplications allowed, and had at least 22eight pending U.S. patent applications, with several more patent applications in the pipeline. We have no pending or issued patents in any jurisdiction outside of the United States. Our issued patents are scheduled to expire between 2039-2040.2022,2024, we held ninetwelve registered trademarks in the United States, and also held 5785 registered trademarks in foreign jurisdictions. As of January 31, 2022,2024, we held threeno pending U.S. trademark applications and 283 pending foreign trademark applications. We continually review our development efforts to assess the existence and patentability of new intellectual property.1314Risk Factorsfactorfactors summary contains a high-level summary of risks associated with our business. It does not contain all of the information that may be important to you, and you should read this risk factorfactors summary together with the more detailed discussion of risks and uncertainties set forth following this summary. A summary of our risks includes, but is not limited to, the following:Because ofThe license for our free community edition products places certain limits on competitive use, but the permissive rights accorded tounder our legacy open-source licenses makes it possible for third parties underto offer and build upon older open-source versions of our open-source and source available licenses, there are limited technological barriers to entry into the markets in which we compete andproducts. Those competing versions could make it is, and may continue to be, relatively easy for competitors including public cloud operators, to enter our markets and compete with us.to useusing our products and renewrenewing their subscriptions, it could have an adverse effect on our business and results of operations.•ability to increase salescustomers’ usage of our products is highly dependent on the quality of our customer support, and our failure to offer high-quality support would have an adverse effect on our business, reputation, and results of operations.•If we do not effectively focus our product development efforts, our business, results of operations, and financial condition could be adversely affected.•We have limited experience with respect to determining the optimal prices for our products.•We target enterprise customers, and sales to these customers involve risks that differ from risks associated with sales to smaller entities.•The length of our sales cycles can be unpredictable, and our sales effortsrenewal rates may require considerable time and expense.15•Our revenue growth depends in part on the success of our strategic relationships with our ecosystem of partners and the continued performance of these partners.•The estimates of market opportunity and forecasts of market growth included in our public disclosures may prove to be inaccurate, and even if the market in which we compete achieves the forecasted growth, our business could fail to grow at similar rates, if at all.•The markets for some of our products are new, unproven, and evolving, and our future success depends on the growth and expansion of these markets and our ability to adapt and respond effectively to evolving markets.•We face competition that we expect to become more intense over time, and which could adversely affect our business, financial condition, and results of operations.•Problems with our internal systems, networks,decline or data, including actual or perceived breaches or failures by us or our partners, could cause our products to be perceived as insecure, underperforming, or unreliable, our reputation to be damaged, and our financial results to be negatively impacted.•If our self-managed offerings do not meet our customers’ performance or support expectations or if we fail to meet service-level availability commitments made to our cloud platform customers, we could face subscription terminations and a reduction in renewals, which could significantly affect our current and future revenue.•If we are not able to keep pace with technological and competitive developments or fail to integrate our products with a variety of technologies that are developed by others, our products may become less marketable, less competitive, or obsolete, and our results of operations may be adversely affected.•Failure of our products to satisfy customer demands or to achieve increased market acceptance could adversely affect our business, results of operations, financial condition, and growth prospects.•Unfavorable conditions in our industry or the global economy or reductions in spending for products like ours could limit our ability to grow our business and negatively affect our results of operations.•Uncertainty regarding ongoing hostility between Russia and Ukraine and the related impact on macroeconomic conditionsfluctuate as a result of such conflict.•not ableunable to maintainmake our paid products sufficiently compelling to business customers as compared to our free community versions, we may have limited success selling paid subscriptions and enhanceretaining our brand, especially among practitioners, our business and operating results may be adversely affected.•We depend on cooperating with public cloud operators. Changes to arrangements with such operators may significantly harm our customer retention, new customer acquisition, and product extension or expansion, or require us to change our business models, operations, practices, or advertising activities, which could restrict our ability to maintain our platform through these clouds and would adversely impact our business.•We rely upon public cloud operators to operate our platform and any disruption of or interference with our use of these operators’ services would adversely affect our business, results of operations, and financial condition.•Interruptions or performance problems associated with our technology and infrastructure, and our reliance on technologies from third parties, may adversely affect our business operations and financial results.16Risks Related to Our Business and Operations2021, and 2020 were $320.8$583.1 million, $211.9$475.9 million and $121.3$320.8 million, respectively, representing an annual growth rate of 51%23% from fiscal 20212023 to fiscal 2022,2024, and 75%48% from fiscal 20202022 to fiscal 2021.2023. In addition, we have experienced fluctuation in our growth rates over time. You should not rely on the revenue growth of any prior quarterly or annual period or combined periods as an indication of our future performance. Even if our revenue continues to increase, we expect our revenue growth rate to decline in future periods. We expect to continue growing our headcount significantly forin the near future. The growth and expansion of our business and products place a continuous significant strain on our management, operational, and financial resources. In addition, as customers use more of our products for an increasing number of use cases, we have had to support more complex commercial relationships. We must continue to improve and expand our information technology and financial infrastructure, our operating and administrative systems, our relationships withrapid growth and the complexity of our multi-product business may make it difficult to evaluate our future prospects. Our ability to forecast our future results of operations is subject to a number of uncertainties, including our ability to effectively plan for and model future growth. We have encountered in the past, and may encounter in the future, risks and uncertainties frequently experienced by growing companies in rapidly changing industries. If we fail to achieve the necessary level of efficiency in our organization as it grows, or if we are not able to accurately forecast future growth, our business wouldwill be harmed. Moreover, if the assumptions that we use to plan our business are incorrect or change in reaction to changes in our market or business, or we are unable to maintain consistent revenue or revenue growth, our share price could be volatile, and it may be difficult to achieve and maintain profitability.future.future, or as quickly as we expect. If we cannot achieve or sustain profitability or positive cash flows, or are slow to do so, our business, financial condition, and results of operations may suffer.$290.1$190.7 million, $83.5$274.3 million, and $53.4$290.1 million in fiscal 2022, 2021,2024, fiscal 2023, and 2020,fiscal 2022, respectively. We had an accumulated deficit of $506.1$971.1 million as of January 31, 20222024, and $216.0$780.4 million as of January 31, 2021.2023. We anticipate that our operating expenses will increase in the foreseeable future as we continue to enhance our products, grow our relationships with existing customers, broaden our customer base, expand our sales and marketing activities, expand our operations, hire additional employees, and continue to develop our technology. These efforts may prove more expensive than we currently anticipate, and we may not succeed in increasing our revenue sufficiently, or at all, to offset these higher expenses. Because the markets for our products are rapidly evolving, it is difficult for us to predict our future results of operations. Revenue growth may slow or revenue may decline for a number of possible reasons, including slowing demand for our products or increasing competition. Any failure to increase our revenue as we grow our business could prevent us from achieving consistent profitability or positive cash flow at all, or on a consistent basis,in the time frame we expect, which could cause our business, financial condition, and results of operations to suffer.2013. We2013, but only began commercializing our software in 2016, so2016. Consequently, much of our growth has occurred in recent years. Our limited operating history makes it difficult to evaluate our current business and our future prospects, including our ability to plan for and model future growth. We have encountered and will continue to encounter risks and difficulties frequently experienced by rapidly growing companies in evolving industries. If we do not address these risks successfully, our business and results of operations will be adversely affected.17introduceenter our markets with new products or services, that compete with ours, we may be unable to attract new customers or convert open-sourcecommunity users to paying customers on terms or based on pricing models that we have used historically. In the future, we may be required to reduce our prices or be unable to increase our prices, or it may be necessary for us to increase ourprovide more products without additional revenue to remain competitive, all of which could harm our results of operations and financial condition.and retain new customers;18Because ofaccorded to third parties under our open-source licenses prior to the change makes it possible for third parties to offer and source available licenses, there are limited technological barriers to entry intobuild upon open-source versions of our products as they existed before the markets in which we compete andlicense change. Those competing versions could make it is, and may continue to be, relatively easy for competitors, including public cloud operators, to enter our markets and compete with us.One ofcharacteristics of open-source is that the governing license terms generally allow liberal modifications of the code and distribution thereof to a wide group of companies and/or individuals. Our open-source licenses allowMozilla Public License, which allows anyone, subject to compliance with the conditions of the applicable license, to redistribute our software and share certain source code components in modified or unmodified form and use it to build products that compete in our markets. Such competition can develop without the degree of overhead and lead time required by traditional proprietary software companies, due to the rights granted to licensees of open-source and source available software. ItUnder our historical Mozilla Public License, it is possible for competitors and new entrants to develop their own software, including software based on open-source or our products, and for public cloud operators to expand their offerings to compete directly with ours, potentially reducing the demand for our products and putting pricing pressure on our subscriptions. For example, a new or existing competitor may dedicate its developers to building competing offerings based on open-source and source-availablesource available software provided by us or third parties, and such offerings may reduce the demand for our offerings. be able to compete successfully against current and future competitors that use the open-sourcesource available nature of our products to compete against us,develop competitive offerings, or that we will be able to effectively enforce licensing restrictions on the competitive use of our community versions, or that competitive pressure or the availability of new software will not result in price reductions, reduced operating margins, andor loss of market share, any one of which would harm our business, financial condition, results of operations, and cash flows.a number ofseveral factors, including the mix of our subscriptions for different products and our professional services and other revenue. For example, while Terraform and Vault are our most established products with commercial offerings at scale and make up the majority of our revenues, generating collectively over 88% and 85% of our revenues for each of fiscal 20222024 and 2021,fiscal 2023, respectively, we believe that our emerging and community products represent a significant growth opportunity. Currently, our self-managed offerings represent the majority of our revenues. However, weWe also believe that HCP, our fully managed cloud platform, represents a significant growth opportunity for our business, particularly as an increasing number of our customers look for a fully managed offering. Shifts in our business mix from quarter to quarter could produce substantial variation in the revenue wemixcomposition and costs as we shift further to cloud models,managed offerings, together with numerous other factors,19If we are unable to increase sales of subscriptions to our products to new customers, sell additional subscriptions to our products to our existing customers, or expand the value of our existing customers’ subscriptions to our products, our future revenue and results of operations will be harmed.We offer certain features of our products as open-source software with no payment required. Customers purchase subscriptions to our products in order to gain access to additional functionality and support. Our future success depends on our ability to sell our subscriptions to new customers and to extend the deployment of our products with existing customers by selling paid subscriptions to our existing users and expanding the value and number of existing customers’ subscriptions. Our ability to sell new subscriptions depends on a number of factors, including the prices of our products, prices offered by our competitors, and the budgets of our customers, as well as their desire and ability to create new features and perform their own support relying on our publicly available open-source software products. We also face competition from public cloud operators, who may use our open-source software products to provide and support hosted offerings that compete with our own. We rely in large part on our customers to identify new use cases for our products and new products to meet a broader set of their needs in order to expand such deployments and grow our business. If our customers do not recognize the potential of our products, our business would be materially and adversely affected. If our efforts to sell subscriptions to new customers and to expand deployments at existing customers are not successful, our total revenue and revenue growth rate may decline and our business will suffer.If our existing customers do not continue to use our products and renew their subscriptions, it could have an adverse effect on our business and results of operations.We expect to derive a significant portion of our revenue from renewals of existing subscriptions for our products. As a result, achieving a high renewal rate of our subscriptions will be critical to our business. Our customers have no contractual obligation to renew their subscriptions after the completion of their subscription term. Terms of our subscriptions typically range from one to three years.Our customers’ usage of our products and renewal rates may decline or fluctuate as a result of a number of factors, including their satisfaction with our products and our customer support, our products’ ability to integrate with new and changing technologies, the frequency and severity of product outages, our product uptime or latency, the pricing of our, or competing, products, and our customers’ own budget priorities and fluctuations in spending. Even if our customers renew their subscriptions, they may renew for shorter subscription terms or on other terms that are less economically beneficial to us. We have limited historical data with respect to rates of customer renewals, so we may not accurately predict future renewal trends. If our customers do not renew their subscriptions, or renew on less favorable terms, our revenue may grow slower than expected or decline and our net expansion rate may decline.grow salesretain them or expand our relationship with them.20the significant number of our currentmultiple products and advancing theour new product pipeline may overextend our workforce and negatively affect product quality and development schedules. Enhancements and new products that we develop may not be introduced in a timely or cost-effective manner, may contain errors or defects, may require reworking features and capabilities, may have interoperability difficulties with our platform or other products, or may not achieve the broad market acceptance necessary to generate significant revenue. Not allSome new products we develop may becomefail commercially, successful, and we may incorrectly prioritize the development of products that do not become commercially successful over products which may have had a better chance of attaining commercial success. Workforce productivity spent on theseunsuccessful product development efforts may not be recouped in the form of sales to customers.recovered. Furthermore, our ability to increase the usage of our products depends, in part, on the development of new use cases for our products, which is typically driven by our developer community and may be outside of our control. In addition, adoption of new products or enhancements may put additional strain on our customer support team, which could shift the team’s resources away from supporting our current products or require us to make additional expenditures related to further hiring and training. If we are unable to timely and successfully enhance our existing products to meet evolving customer requirements, increase adoption and usage of our products, develop new products, or if our efforts do not render the outcomes we expect, then our business, results of operations, and financial condition wouldwill be adversely affected.products.products ormodel,models, which could adversely affectmaterially harm our business, results of operations, and financial condition.involvecarry risks that may not be present or that are present to a lesser extentexceed those associated with sales to smaller entities, such as longer sales cycles, more complex and demanding customer requirements and contract negotiations, substantial upfront sales costs, and less predictability in completing some of our sales. For example, enterprise customers may require considerable time to evaluate and test our solutions and those of our competitors prior tobefore making a purchase decision and placing an order. A number ofMultiple factors influence the length and variability of our sales cycle, including the need to educate potential customers about the uses and benefits of our solutions, economic pressure or uncertainty that prompts customers to seek cost savings on software purchases, the discretionary nature of purchasing and budget cycles, and the competitive nature of evaluation and purchasing approval processes. As a result, the length of our sales cycle, from identification of the opportunity to deal closure, may vary significantly from customer to customer, with sales to large enterprises typically taking longer to complete. Moreover, large enterprise customers often begin to deploy our products on a limited basis, but nevertheless demand integration services and pricing negotiations, with no guarantee that they will deploy our products widely across their organization.21Contentssubsequent to thosethan we anticipated,expected, or have not occurred at all. The loss or delay of one or more large transactions in a quarter could affect our cash flows and results of operations for that quarter and for future quarters. Customers often view a subscription to our products as a strategic decision and significant investment and, as a result, frequently require considerable time to evaluate, test, and qualify our products before entering intopurchasing or expanding a subscription. During the sales cycle, we expend significant time and money on sales and marketing and contract negotiation activities which may not result in a sale. Because a substantial proportion of our expenses are relatively fixedwillmay suffer if revenue falls below our expectations in a particular quarter. with our partners are generally non-exclusive, meaning our partners may offer customers the offerings of several different companies, including offerings that compete with ours, or may themselves be or become competitors. If our partners do not effectively market and sell our offerings, choose to use greater efforts to market and sell their own offerings or those of our competitors, or fail to meet the needs of our customers, our ability to grow our business and sell our offerings may be harmed. Our partners may cease marketing our offerings with limited or no notice and with little or no penalty. The loss of a substantial number of our partners, our possible inability to replace them, or the failure to recruit additional partners could harm our results of operations. Likewise, because the success of our products depends on integrations with partners’ technologies, if partners decide to no longer implement or support such integrations, or if they partner with our competitors and devote greater resources to implement and support the products of competitors, our business may be harmed.achieve revenue growth in the future will depend in partacquire and retain customers depends heavily on our success in developing and maintaining successful relationships with our partners and in helping our partners enhance their ability to marketoffer effective professional services to customers, and sell our subscriptions.effectiveness in cultivating a sufficient network of partners to provide high quality professional services for our products. At times we have had trouble meeting customer demand for professional services. If we are unable to build and maintain enough professional services capacity to meet customer demand, either directly or through our relationships with these partners, we will be at risk of increased customer attrition, slowing sales, and reputational damage from failed implementations, all of which could materially damage our business results of operations,and our financial condition, or cash flows could be harmed. to be inaccurate, and even if the market in which we compete achieves the forecasted growth, our business could fail to grow at similar rates, if at all.not prove to be accurate,inaccurate, including the risks described herein. Even if the market in which we compete achieves the forecasted growth, our business could fail to grow at similar rates, if at all.any particular number or percentageestimates of addressable users or companies covered by our market opportunity estimates will purchasecorrespond to actual sales of our products at all or generate any particular level of revenue for us.revenue. For example, negative conditions in the general economy both in the United States and abroad, including conditions resulting from uncertain interest rates, inflation, and geopolitical tensions, could diminish growth expectations in the U.S. economy and our market opportunity estimates. Any expansion in our market depends on a number ofmultiple factors, including the cost, performance, and perceived value associated with our products and the products provided by our competitors. Even if the market in which we compete meets the size estimates and growth forecastedforecasts included in our public disclosures, our business could fail to grow at similar rates, if at all.rates. Our growth is subject to many factors,variables, including our success in implementing our business strategy, which is subject tocarries many assumptions, risks and uncertainties. Accordingly, the forecasts of market growth included in our public disclosures shouldmay not be taken as indicative of our future growth.evolving markets. for these products, customers’ demand for these products, the size, growth rate, expansion, and longevity of these markets, the entry of competitive products, or the success of existing competitive products. Our ability to penetrate these new and evolving markets depends on a number of factors, including the cost, performance, and perceived value associated with our products. If these markets do not continue to grow as expected, or if we are unable to anticipate or react to changes in these markets, our competitive position would weaken, which would adversely affect our business and results of operations.become more intenseintensify over time, and which could adversely affect our business, financial condition, and results of operations.ourwe expect competition is expected to increase over time. Our business is impacted by rapid changes in technology, customer needs, frequent introductions of new offerings, and improvements to existing offerings, all of which may increase the competitive pressures that we face. We provide offerings to address the needs of a wide variety of prospective customers that compete with other approaches and solutions. For example, internal IT teams sometimes attempt to “do it themselves” using open-sourcesource available software. While individuals and small teams can sometimes use our open-sourcecommunity products to solve their technical problems, larger enterprises face more complex needs that require our commercial products. For select companies adopting a single-cloud solution, we compete with the well-established public cloud providers such as Amazon Web Services, or AWS, and their in-house offerings. We also compete with similar in-house offerings from Microsoft Azure, Google Cloud Platform, and other cloud providers; legacy providers with point products such as Red Hat, CyberArk, VMware, and IBM; and alternative open-source projects, such as Google Istio.cases supported;cases; ability to integrate with existing IT infrastructure, cloud platforms, and on-premises environments; offering consistency of offerings across clouds; ability to implement multi-cloud provisioning, security, networking, and application deployment; speed of implementation and time to achieving value; ability to scale up and down dynamically on demand; robustness of professional services and customer support; price and total cost of ownership; adherence to certifications; size of customer base and level of user adoption; strength of sales and marketing efforts; offering anscope of vendor ecosystem of vendors integrated with the products; creatingability to create new products and expanding the existing platform; ability to innovate around a cloud-delivered architecture; brand awareness, recognition, and reputation, particularly within the open-sourcedeveloper community; and ability to engage the community of open-source users and partners. If we fail to innovate and improve our products and professional services to address these factors, we may become vulnerable to increased competition and therefore fail to attract new customers or lose or fail to renew existing customers, which would causeharm our business and results of operations to suffer.our offerings.ours. These companies may have advantages over us, such as longer operating histories, more established relationships with current and potential customers and commercial partners, significantly greater financial, technical, marketing, or other resources, stronger brand recognition, larger intellectual property portfolios, and broader global distribution and presence. OurIn addition, our business model alsolargely assumes that our customers are committed to a multi-cloud strategy and will not bundle their cloud services.services with a single provider. However, if this assumption does not accurately reflectinaccurately reflects the decisions of our customers, our business maywill suffer. Some of our larger potential competitors and other cloud providers have substantially greater resources than we do and therefore may afford to bundle competitively priced related products and services, which may allow them to leverage existing commercial relationships, incorporate functionality into existing products, sell products with which we compete at zero or negative margins, offer fee waivers and reductions or other economic and non-economic concessions, maintain closed technology platforms, or render our products unable to interoperate with such platforms. Our actual or potential customers may prefer to bundle their cloud services with one of our potential competitors even if such competitors’ individual products have more limited functionality compared to our software. These larger potential competitors are also often in a better position to withstand any significant reduction in technology spending and will therefore not be as susceptible to competition or economic downturns. Our potential competitors may also be able to respond more quickly and effectively than we can to new or changing opportunities, technologies, standards, or customer requirements. In addition, some potential competitors may offer products or services that address one or a limited number of functions at lower prices, with greater depth than our products or in geographies23of these reasons, we may not be able to compete successfully against our current or potential competitors. to be damaged, and our financial results to be negatively impacted.our or our customers’ or other third parties’ highly sensitive, proprietary, and confidential information.information we receive from our customers, our employees, and other third parties. In addition to threats from traditional attackers and insider threats, we also face security threats from malicious third parties, including individual hackers, sophisticated criminal groups, nation states, and state-sponsored organizations, that could disrupt or interrupt, or introduce ransomware, viruses, or other malicious code into our products, services, systems, or networks, obtain unauthorized access to our internal systems, networks, and data, as well as systems of organizations using our cloud products and services, and the information they store and process. Users and organizations using our services may also disclose or leak their passwords, API keys, or secrets that could lead to unauthorized access to their accounts and data within our products. Such incidents have become more prevalent in our industry, particularly against cloud services, and may in the future result in unauthorized, unlawful, or inappropriate access to, inability to access, disclosure of, or loss or other unauthorized processing of the sensitive, proprietary, and confidential information that we own, process, or control, such as customer information and proprietary data and information, including source code and trade secrets. In addition, the risks of data security failures has increased significantly based upon the growing number of new data protection laws throughout the world and intensive scrutiny from regulatory bodies. It is virtually impossible for us to entirely mitigate the risk of these security threats. While we have implemented security measures internally and have integrated security measures into our products, these measures may not function as expected and may not detect or prevent all unauthorized activity, prevent all security breaches and incidents, mitigate all security breaches or incidents, or protect against all attacks or incidents. Moreover, our products incorporate a variety of third-party components (including open-sourcesource available software components) which may expose us to additional security threats, and vulnerabilities in those components may be difficult or impossible to detect, control, and manage. We may also experience security breaches and other incidents that may remain undetected for an extended period and, therefore, may have a greater impact on our products, the networks and systems used in our business, and the proprietary and other confidential data contained on such networks and systems. We expect to incur significant costs in our efforts to detect and prevent security breaches and other security-related incidents, and we may face increased costs in the event of an actual or perceived security breach or other security-related incident. These cybersecurity risks pose a particularly significant risk to a business like ours that is focused on providing highly secure products to customers. Additionally, as a remote-firsthybrid remote company, much of our workforce functions in a remote work environment that requires remote access to our corporate network, which in turn imposes additional risks to our business, including increased risk of industrial espionage, theft of assets, phishing, and other cybersecurity attacks, and inadvertent or unauthorized access to or dissemination of sensitive, proprietary, or confidential information.24ContentsOurour offerings, and may continue to incorporate additional AI features into our offerings in the future. The use of AI may result in security incidents and our integration of AI and the use of AI features by our customers, and the use of AI solutions and offerings by our personnel, may create additional cybersecurity risks or increase cybersecurity risks, including risks of security breaches and incidents. Further, AI technologies may be used in connection with certain cybersecurity attacks, resulting in heightened risks of security breaches and incidents. In addition, our products may experience errors, failures, vulnerabilities, or bugs that cause our products not to perform as intended. Any such errors, failures, vulnerabilities, or bugs may not be found until after they are deployed to our customers and may create the perception that our platform and products are insecure, underperforming, or unreliable. We also provide frequent updates and fundamental enhancements to our platform and products, which increase the possibility of errors. Our quality assurance procedures and efforts to report, track, and monitor issues with our products may not be sufficient to ensure we detect any such defects in a timely manner. There can be no assurance that our software code is or will remain free from actual or perceived errors, failures, vulnerabilities, or bugs.our Vault and our other products, we believe that such products could be targets for hackers and others, and that an actual or perceived breach of, or security incident affecting, our security products and customers, could be especiallyparticularly detrimental to our reputation, customer confidence in our security products, and our business. The potential for an attack is compounded now that our Vault product is includedoffered as a cloud offering.service. Additionally, our products are designed to operate with little or no downtime. If a breach or security incident were to impact the availability of our products, our business, results of operations, and financial condition, as well as our reputation, could be adversely affected.increasingly largeincreasing amounts of data.Additionally, we cannot be certain that our insurance coverage will be adequate or otherwise protect us with respect to claims, expenses, fines, penalties, business loss, data loss, litigation, regulatory actions, or other impacts arising from security breaches, or that such coverage will continue to be available on acceptable terms or at all. Any of these results could adversely affect our business, financial condition, and results of operations. self-managed offerings do not meet our customers’ performance or support expectations or if we fail to meet service-level availability commitments made to our cloud platform customers, we could face subscription terminations and a reduction in renewals, which could significantly affect our current and future revenue.self-managed customers have for our products, or the service-level availability commitments we have made to our cloud platform customers, then we may not retain our customers or renew them expected rates. With respect to service-level availability commitments, we may be obligated to pay monetary penalties to the impacted cloud customers. Additionally, we may be contractually obligated to provide cloud customers with additional capacity and reputationally obligated to provide self-managed customers with additional support, each of which could significantly affect our revenue.interruptions.25Tableinterruptions, or we may have limited rights that fall short of Contentsnot ableunable to keep pace with technological and competitive developments or fail to integrate our products with a variety of technologies that are developed by others, our products may become less marketable, less competitive, or obsolete, and our results of operations may be adversely affected.cost-effectivecost-open-sourcedeveloper community, and growth or contraction in our market or the overall economy. We expect the growth and proliferation of data to lead to an increase in the data analyses demands of our customers and we may not be able to scale and perform to meet those demands or may not be chosen by users for those needs. If we are unable to continue to meet customer demands or to achieve more widespread market acceptance of our products, our business operations, financial results, and growth prospects will be materially and adversely affected.2627%30% and 25%27% of our revenue outside of the United States in fiscal 20222024 and 2021,fiscal 2023, respectively. Our ability to expand internationally involves various risks, including the need to invest significant resources in such expansion, and the possibility that returns on such investments will not be achieved in the near future or at all in these less familiar competitive environments. We may also choose to conduct our international business through partnerships. If we are unable to identify partners or negotiate favorable terms, our international growth may be limited. In addition, we have incurred and may continue to incur significant expenses in advance of generating material revenue as we attempt to establish our presence in particular international markets. Additional risks associated with our international operations include:conditions;27Failure by usOur failure to effectively provide training and implementation services to our customers could result in lost opportunities for follow-on sales to these customers and decrease subscriptions by new customers, and adversely affect our business and growth prospects.cooperatingcooperation with public cloud operators. Changes to arrangements with such operators may significantly harm our customer retention, new customer acquisition, and product extension or expansion, or require us to change our business models, operations, practices, or advertising activities, which could restrict our ability to maintain our platform through these clouds and would adversely impact our business. our products to our customers. Because of the significant use of our platform on public clouds, our solutions must remain interoperable with them. Further, we are subject to the standard agreements, policies, and terms of service of these public clouds, as well as agreements, policies, and terms of service of the various application stores that make our solutions available to our developers, creators, customers, and users. These agreements, policies, and terms of service govern the availability, promotion, distribution, content, and operation generally of applications and experiences on such public clouds. As a result, we may not successfully cultivate relationships with key industry participants or develop products that operate effectively with these technologies, systems, networks, regulations, or standards. If it becomes more difficult for our customers or users to access and engage with our platform on the public clouds they are already using, if our customers choose not to access or use our platform application on their cloud accounts, or if our customers or users choose to use public clouds that do not offer or discontinue access to our platform, our business and customer retention, new customer acquisition, and product extension or expansion could be significantly harmed.28have experienced that it takescan take significant time to adjust such technologies to function with these public clouds, impacting the adoption of our new technologies and features, and we expect this trend to continue. be able to access our platform at any time, without interruption or degradation of performance. Public cloud operators run their own platforms that we access, and we are, therefore, vulnerable to service interruptions of these platforms. We have experienced, and expect that in the future we may experience, interruptions, delays, and outages in service and availability from time to time due to a variety of factors, including infrastructure changes, human or software errors,for are cloud-based server capacity and, to a lesser extent, storage and other optimization offerings. Public cloud operators allow us to order and reserve server capacity in varying amounts and sizes distributed across multiple regions. We access public cloud operator infrastructure through standard IP connectivity. Public cloud operators provide us with computing and storage capacity pursuant to an agreementunder agreements that continuescontinue until terminated by either party. Public cloud operators may terminate the agreementagreements by providing 30 days’a set amount of prior written notice and may in some cases may terminate the agreementagreements immediately for cause upon notice. Although we expect that we could receive similar services from other third parties, if any of our arrangements with public cloud operators are terminated, we could experience interruptions on our platform and in our ability to make our products available to customers, as well as delays and additional expenses in arranging alternative cloud infrastructure services.29open-sourcesource available software and reliance on other third-party services may increase this risk. For example, we are dependentdepend on our relationship with a third-party processor for installation and packaging solutions in one of our products. If our website is unavailable or our users are unable to download our products or order subscriptions or services within a reasonable amount of time or at all, our business could be harmed. We expect to continue to make significant investments to maintain and improve website performance and to enable rapid releases of new features and applications for our products. To the extent that we do not effectively upgrade our systems as needed and continually develop our technology to accommodate actual and anticipated changes in technology, our business and results of operations may be harmed.wouldmay be similarly be interrupted. An interruption in our services to our customers could cause our customers’ internal and consumer-facing applications to fail to function properly, which could have a material adverse effect on our business, operations, financial results, customer relationships, and reputation. In addition, we rely on cloud technologies from third parties in order to operate critical functions of our business, including financial management services, customer relationship management services, and lead generation management services. Accordingly, if these services become unavailable due to extended outages or interruptions or because they are no longer available on commercially reasonable terms or prices, our expenses could increase, our ability to manage our finances could be interrupted, our processes for managing sales of our products and supporting our customers could be impaired, and our ability to generate and manage sales leads could be weakened until equivalent services, if available, are identified, obtained, and implemented, all of which could harm our business and results of operations.that we carry may be insufficient to cover all liabilities incurred by uswe incur in connection with any privacy or cybersecurity incidents or may not cover the kinds of incidents for which we submit claims. For example, insurers may consider cyberattacks by a nation-state as an “act of war” and any associated damages as uninsured. We also cannot be certain that our insurance coverage will be adequate for data handling or data security liabilities actually incurred, that insurance will continue to be available to us on economically reasonable terms, or at all, or that any insurer will not denyaccept coverage as to any future claim. The successful assertion of one or more large claims against us that exceed available insurance coverage, or the occurrence of changes in our insurance policies, including premium increases or the imposition of large deductible or co-insurance requirements, could have a material adverse effect on our business, results of operations, and financial condition, as well as our reputation.30Contentsplanplans and to identify and pursue new opportunities and product innovations. The loss of services of senior management could significantly delay or prevent the achievement of our development and strategic objectives, which could adversely affect our business, financial condition, and results of operations.Both thein which we operate and the San Francisco Bay Area, where our headquarters is located, are generally characterized by significant competition for skilled personnel as well as high employee attrition. Additionally, many of the companies with which we compete for experienced personnel have greater resources than we have and may provide higher levels of compensation. We have from time to time experienced, and we expect to continue to experience,experiencing, difficulty in hiring and retaining employees with appropriate qualifications. Also, to the extent we hire personnel from competitors, we may be subject to allegations that they have been improperly solicited, that they have divulged proprietary or other confidential information, or that their former employers own their inventions or other work product.a large percentage of our sales force is new to our company. New hiresnewly hired employees require significant training and may take significant time before theyto achieve full productivity. Our recent hires and planned hires may not become productive as quickly as we expect, and we may be unable to hire or retain sufficient numbers of qualified individuals in the markets where we do business or plan to do business. In addition,at which we may prove unsuccessful.not manage successfully. If we are unable to hire and train a sufficient number of effective sales personnel, we are ineffective at overseeing a growing sales force, or the sales personnel we hire are otherwise unsuccessful in obtaining new customers or increasing sales to our existing customer base, our business will be adversely affected.Any failure to successfully attract, integrate, train, or retain qualified personnel to fulfill our current or future needs could materially and adversely affect our business, results of operations, and financial condition. that our culture has been and will continue to be a key contributor to our success. If we do not continue to maintain our corporate culture as we grow, we may be unable to foster the innovation, creativity, and entrepreneurial spirit we believe we need to support our growth. Any failure to preserve our culture also could further harm our ability to retain and recruit personnel, innovate and create new products, operate effectively, and execute on our business strategy.remote-firsthybrid remote company may make it difficult for us to preserve our corporate culture, have a negative impact on workforce morale and productivity, and harm our future success, including our ability to retain and recruit personnel, innovate and operate effectively, and execute on our business strategy.remote-firsthybrid remote company since incorporation. This subjects us to heightened operational risks. For example, technologies in our employees’ and service providers’ homes may not be as robust as in our offices and could cause the networks, information systems, applications, and other tools available to employees and service providers to be more limited or less reliable than in our offices. Further, because the security systems in place at our employees’ and service providers’ homes may be less secure than those used in our offices, we may be subject to increased cybersecurity risk, which could expose us to risks of data or financial loss and disrupt our business operations. There is no guarantee that our data security and privacy safeguards will be completely effective or that we will not encounter risks associated with employees and service providers accessing company data and systems remotely.31as a remote-first company as an increasing number of our employees choose tohybrid work remotely due to the COVID-19 pandemicenvironment may make it more difficult for us to preserve our corporate culture, and our employees may have decreased opportunities to collaborate in meaningful ways. Further, we cannot guarantee that an increasing number working remotely will not have a negative impact ondamage workforce morale and productivity. Any failure to preserve our corporate culture and foster collaboration could harm our future success, including our ability to retain and recruit personnel, innovate and operate effectively, and execute on our business strategy.providing services toworking in a remote-firsthybrid remote company allows employees to move freely while undertaking their work responsibilities. On occasion, employees have and may continue to fail to inform us of changes to their work location in a timely manner. Conducting business in certain geographies may expose use to risks associated with that location, including compliance with local laws and regulations or exposure to compromised internet infrastructure. If employees fail to inform us of changes in their work location, we may be exposed to various risks without our knowledge. For example, if employees create intellectual property on our behalf while residing in a jurisdiction with weak or uncertain intellectual property laws, our ownership of such intellectual property may be questioned. Similarly, if employees access our resources through unsecured internet infrastructure, they may expose us to a heightened risk of data theft or cyberattack.COVID-19 pandemic and uncertainties about the future,macroeconomic environment, including the effectiveness of vaccines against various strains of the virus and macroeconomic impacts of the Russia/Ukraineglobal military conflict.conflicts, inflationary pressures, or recessionary economic cycles. Episodic experiences may also contribute to fluctuations in our quarterly results of operations. As our business matures, other seasonal trends may develop, or existing seasonal trends may become more extreme.pre-requisiteprerequisite to recognizing revenue under applicable software accounting rules. If we are unable to deliver our software to a new customer before the quarter ends, we cannot recognize any revenue from the sale during the quarter in which the customer placed its order. Instead, we must wait until the quarter in which we actually delivered the software to begin recognizing revenue. In quarters where we have a high volume of late-quarter sales, we may be unable to sign or process a significant number of the orders we32have recently started sellingsell to U.S. federal governmental agency customers. Sales to such entities currently constitute a small portion of our revenue. Selling to such entities can be highly competitive, expensive, and time-consuming, often requiring significant upfront time and expense without any assurance that these efforts will generate meaningful sales. Government certification or other requirements for products like ours may change, thereby restricting our ability to sell into the government sector until we have attained such revised certification or certifications.updated the necessary certifications or satisfy other applicable requirements. Government demand and payment for our products may be affected by public sector budgetary cycles and funding authorizations, with funding reductions or delays adversely affecting public sector demand for our products. Additionally, any actual or perceived privacy, data protection, or data security incident, or even any perceived defect with regard toregarding our practices or measures in these areas, may negatively impact public sector demand for our products.in doing socould restrict our ability to sell into the government sector until we have met government-mandated requirements, which may require significant upfront cost, time, and resources. If we do not achieve and maintain government requirements, it may harm our competitive position against larger enterprises whose competitive offerings are able to meet these requirements. ThereWe also can also beprovide no assurance that we will secure commitments or contracts with government entities even following efforts toif we meet government requirements, which could harm our margins, business, financial condition, and results of operations. Further, government demand and payment for our offerings are affected by public sector budgetary cycles and funding authorizations, with funding reductions or delays adversely affecting public sector demand for our offering.open-sourcesource available and proprietary technologies incorporate third-party open-source software, and we expect to continue to incorporateusing third-party open-source software in our products in the future, and itwhich may be necessary to utilizerequire using new and upgraded versions of these software applications. There can be no assurance that new versions of the third-party open-source projects we currently use will continue to be licensed under open-source licenses, or that necessarynew versions will not contain different open-source licenses will be availablethat carry unacceptable limitations on distribution. In addition, where buying proprietary licenses is they only way to avoid onerous open-source distribution limitations, we may not succeed in obtaining those proprietary licenses on acceptable terms or under open-source licenses permitting redistribution in our open-source and proprietary offerings, if at all. Theterms. Our inability to obtain certain licenses or other rights or to obtain such licenses or rights on favorable terms, could result in delays in product releases until equivalent technology can be identified, licensed, or developed, if at all, and integrated into our products, andwhich may have a material adverse effect on our business, resultsthat these licenses could be construed in a manner that could adversely impact our interests and the interests of our customers, both with respect to our use of third-party open-source as well as our distribution of our own software under open-sourcesource available licenses, including by imposing unanticipated conditions or restrictions on our ability to commercialize our products, or limiting our ability to enforce our rights in the manner we had anticipated. Moreover, we cannot ensure that our software does not include open-source software that we are unaware of, or that we have not incorporated additional open-source software in our software in a manner that is inconsistent with the terms of the applicable license or our current policies and procedures, including requiring us to make some or all of our software available under an open-source license that is unacceptable to us or to our customers. If we incorporate third-party open-source software into our software products, then in certain circumstances, we and our customers may be subject to certain requirements, including requirements that we offer our solutions that incorporate such third-party open-source software under license terms that are inconsistent with our intended license, such as requiring portions of our products we create based upon, derived from, incorporating, or using such open-source software (and in turn, portions of our customers’ products that they create which are based upon, derived from, incorporating, or using our products) be made available for no cost and for the purpose of making and redistributing such software (including in source code form) and derivatives thereof. If an author or other third party that distributes such open-source software were to allege that we had not complied with the conditions of one or more of these licenses, we could be required to incur significant legal expenses defending against such allegations and could be subject to significant damages, enjoined from the sale of our products that contained the open-source software, and required to comply with onerous conditions or restrictions on these products, which could disrupt the distribution and sale of these products.wereis made with respect to a third-party open-source component included in our products, we and our customers could be required to seek licenses from third parties in order to continue offering our products, and to re-engineer our respective products or discontinue the sale of our respective products in the event re-engineering cannot be accomplished on a timely basis. We and our customers may also be subject to suits by parties claiming infringement, misappropriation or violation due to the reliance by our solutions on certain open-source software, and such litigation could be costly for us to defend or subject us to certain types of equitable remedies, such as an injunction. Some open-source projects have known vulnerabilities and architectural instabilities and are provided on an as-is basis, which, if not properly addressed, could negatively affect the performance of our product. Any of the foregoing could require us to devote additional research and development resources to re-engineer our solutions, provide an advantage to our competitors or other entrants to the market, create new security vulnerabilities, or highlight existing security vulnerabilities in products, result in customer dissatisfaction, and may adversely affect our business, results of operations, and financial condition. We cannot ensure that our processes for identifying and controlling our use of open-source software in our platform and products will be effective.use third-party open-sourcedevelop our products in a source available software environment, which could negatively affect our ability to sell our offerings, or make it easier for competitors, some of whom may have greater resources than we have, to enter our markets and compete with us.is developed in open-source,has its source code available, allowing our partners and third parties to give feedback directly, report issues, contribute features, and fix bugs, which we may accept and integrate into our products. Our partners are able to integrate their technology solutions and validate their integrations with continuous development. We plan to continue to develop our products in this open-sourcesource available environment, and enabling third-party contributions, and the integration of open-source software from third parties into our codebase. While these open-source software licenses state that any work of authorship licensed under it may be reproduced and distributed provided that certain conditions are met, we may nevertheless be subject to suits by parties claiming ownership rights in what we believe to be permissively licensed open-source software or claiming non-compliance with the applicable open-source licensing terms.34 patents, contractual restrictions, and other intellectual property laws and confidentiality procedures to establish and protect our proprietary rights. However, the steps we take to obtain, maintain, protect, and enforce our intellectual property rights may be inadequate. Our intellectual property rights may not protect our competitive position if we are unable to enforce our rights or if we do not detect unauthorized use of our intellectual property rights, or if others are successful in designing around the protections our intellectual property rights afford. If we fail to protect our intellectual property rights adequately, our competitors may gain access to our proprietary technology, develop and commercialize substantially identical products, services, or technologies, and our business may be harmed. In addition, defending our intellectual property rights might entail significant expense.No assurance can be given thatWe cannot assure these agreements will be effective in controlling access to and distribution of our proprietary information. Further, these agreements may not prevent our competitors from independently developing technologies that are substantially equivalent or superior to our products. These agreements may be breached, and we may not have adequate remedies for any such breach.35 For example, recently we and a number of other companies were sued by a non-practicing entity in Delaware federal court alleging patent infringement with respect to certain patents relating to power savings in data centers and cloud networking management, and we are vigorously defending against this lawsuit. Further, the software industry is characterized by the existence of a large number of patents, copyrights, trademarks, trade secrets, and other intellectual and proprietary rights. Companies in the software industry are often required to defend against litigation claims based on allegations of infringement, misappropriation, or other violations of intellectual property rights. Our technologies may not be able to withstand any third-party claims against their use. In addition, many companies have the capability to dedicate substantially greater resources to enforce their intellectual property rights and to defend claims that may be brought against them.and thiswhich could further exhauststrain our financial and management resources.as a result of anydue to intellectual property infringement, misappropriation, or violation claims against us or any obligation to indemnify our customers for such claims, such payments or actions could harm our business.36gainsell more traction with our cloud offerings. We process certain personal data as part of our business operations, and our Vault product is specifically designed to assist our customers with management of their private and sensitive information. As we develop our cloud offerings and are able to process more data in the cloud, these issues become more significant. The regulatory frameworks for privacy, data protection, and data security issues worldwide are rapidly evolving and are likely to remain uncertain for the foreseeable future, particularly for data processed in the cloud. Federal, state, and non-U.S. government bodies or agencies have in the past adopted, and may in the future adopt, new laws and regulations or may make amendments to existing laws and regulations affecting data protection, data privacy, and/or data security and/or regulating the use of the internet as a commercial medium. Industry organizations also regularly adopt and advocate for new standards in these areas, and we are bound by certain contractual obligations relating to our use, storage, security, and other processing of personal data and other personally identifiable information. We also post privacy policies and have made, and may make, other representations regarding our privacy and data security practices. If we fail to comply with any of these laws, regulations, standards, or other obligations, or such public representations, or are alleged to have done so, we may be subject to investigations, enforcement actions, civil litigation, fines, and other penalties, all of which may generate negative publicity and have a negative impact on our business.adoptedamended and expanded the CCPA with a new law, the California Privacy Rights Act of 2020, or CPRA, that will substantially expand the CCPA effectivewhich came into effect as of January 1, 2023. Additionally, other U.S. states continue to propose, and in certain cases adopt, privacy-focused legislation. For example, Virginia, Colorado, Utah, and Connecticut have enacted comprehensive privacy legislation such as Coloradothat has gone into effect in 2023; Florida, Montana, Oregon, and Virginia.Texas have enacted similar legislation that will go into effect in 2024; Delaware Iowa, New Jersey, and Tennessee have enacted similar legislation that will go into effect in 2025; and Indiana has enacted similar legislation that will go into effect in 2026. Aspects of these state laws remain unclear, resulting in further uncertainty and potentially requiring us to modify our data practices and policies and to incur substantial additional costs and expenses in an effort to comply. A patchwork of differing state privacy and data security requirements wouldwill increase the cost and complexity of operating our business and increase our exposure to liability. Similarly, regulatory37in the “Schrems II” decision issued by the Court of Justice of the European Union, or CJEU, on July 16, 2020. On September 8, 2020, theThe Swiss Federal Data Protection and Information Commissioner invalidated the Swiss-U.S. Privacy Shield on similar grounds. In its July 16, 2020 opinion, the CJEU imposed additional obligations on companies when relying on SCCs to transfer personal data. The CJEU decision may result in European data protection regulators applying differing standards for, and requiring ad hoc verification of, transfers of personal data from Europe to the U.S. The European Commission has published revised SCCs addressing the CJEU concerns on June 4, 2021, that are required to be implemented over time.implemented. The United Kingdom also has adopted new standard contractual clauses, or the UK SCCs, that are anticipated to becomebecame effective as of March 21, 2022, and which are required to be implemented over time.implemented. The United States and European Union announced an “agreement in principle” to replace the EU-U.S. Privacy Shield transfer framework with the Trans-Atlantic Data Privacy Framework, or EU-U.S. DPF, on March 25, 2022. On July 10, 2023, the European Commission adopted an adequacy decision in relation to the EU-U.S. DPF, allowing the EU-U.S. DPF to be utilized as a means of legitimizing EU-U.S. personal data transfers for participating entities, including us. We also have self-certified under a UK Extension to the EU-U.S. DPF and the Swiss-U.S. Data Privacy Framework, or the Swiss-U.S. DPF. The EU-U.S. DPF already has faced legal challenges, and the CJEU’s Schrems II decision, the revised SCCs and UK SCCs, guidance and opinions of regulators, and other developments relating to cross-border data transfer, including the EU-U.S. DPF, the UK Extension to the EU-U.S. DPF, and the Swiss-U.S. DPF may be subject to challenges, future reviews, suspension, amendment, repeal, or limitations, and may require us to implement additional contractual and technical safeguards for any personal data transferred out of Europe, which may increase compliance costs, lead to increased regulatory scrutiny or liability, and which may adversely impact our business, financial condition and operating results. in May 2018 that substantially implements the GDPR, and has implemented legislation referred to as the “UK GDPR”GDPR,” that generally provides forsubstantially implements the GDPR to be implemented in the United Kingdom following Brexit and the transition period that ended on December 31, 2020. This legislation provides for substantial penalties for noncompliance of up to the greater of £17.5 million or four percent of worldwide revenues. While the EU has deemed the United Kingdom an “adequate country” to which personal data could be exported from the EEA, this decision is required to be renewed after four years of being in effect and may be modified, revoked, or challenged in the interim, creating uncertainty regarding transfers of personal data to the United Kingdom from the EEA. Some countries also are considering or have passed legislation requiring local storage and processing of data, or similar requirements, which could increase the cost and complexity of delivering our products.38softwareproducts and services may be subject to U.S. export control laws and regulations including the Export Administration Regulations, or EAR, and trade and economic sanctions maintained by the Office of Foreign Assets Control, or OFAC. As such, an export license may be required to export or re-export our products and services to certain countries, end-users, and end-uses. Because we incorporate encryption functionality into some of our products, we also are subject to certain U.S. export control laws that apply to encryption items. If we were to fail to comply with such U.S. export controls laws and regulations, U.S. economic sanctions, or other similar laws, we could be subject to both civil and criminal penalties, including substantial fines, possible incarceration for employees and managers for willful violations, and the possible loss of our export or import privileges. Obtaining the necessary export license for a particular sale or offering may not be possible and may be time-consuming and may result in the delay or loss of sales opportunities. Furthermore, U.S. export control laws and economic sanctions prohibit the export of products and services to certain U.S. embargoed or sanctioned countries governments and persons, as well as for prohibited end-uses. For example, following Russia’s invasion of Ukraine, the United States and other countries imposed economic sanctions and severe export control restrictions against Russia and Belarus and could impose wider sanctions and export restrictions and take other actions should the conflict continue to escalate. While we currently do not have any significant exposure, any exports or sales of our software or services into Russia and Belarus may be impacted by these restrictions. Monitoring and ensuring compliance with these complex U.S. export control laws is particularly challenging because our offerings are widely distributed throughout the world and are available for download without registration. Even though we take precautions to ensure that we and our partners comply with all relevant export control laws and regulations, any failure by us or our partners to comply with such laws and regulations could have negative consequences for us, including reputational harm, government investigations, and penalties.Additionally, export restrictions recently imposed on Russia and Belarus limit the export of encryption software and related source code and technology to these locations which limits our ability to provide our software and, in some cases services, to these countries. Changes in our products and services or changes in export and import regulations in such countries may create delays in the introduction of our products into international markets, prevent our end-customers with international operations from deploying our products globally, or, in some cases, prevent or delay the export or import of our products to certain countries, governments, or persons altogether. Any change in export or import laws or regulations, economic sanctions, or related legislation, shift in the enforcement or scope of existing export, import, or sanctions laws or regulations, or change in the countries, governments, persons, or technologies targeted by such export, import, or sanctions laws or regulations, could result in decreased use of our products by, or in our decreased ability to export or sell our products and services to, existing or potential end-customers with international operations. Any decreased use of our products or services or limitation on our ability to export to or sell our products and services in international markets could adversely affect our business, financial condition, and operating results.39the use of the internet is reduced as a result ofby these or other issues, then demand for our products could decline, which could adversely affect our business, results of operations, and financial condition.torts,employment, securities, employment, contractual rights, torts, or other legal claims. Such matters can be time-consuming, divert management’s attention and resources, cause us to incur significant expenses or liability, or require us to change our business practices.agreeing toentering into settlement agreements. Any of the foregoing could adversely affect our business, financial condition, and results of operations.402022,2024, we had U.S. federal and state net operating loss carryforwards of $647.8$690.4 million and $498.3$602.2 million, respectively, which may be utilized against future income taxes and beginrespectively. The Federal NOL does not expire since all balances relate to expire in 2034 and 2025 for federal andlosses incurred after January 1, 2018, whereas state purposes,NOL will start expiring from 2026, respectively. Limitations imposed by the applicable jurisdictions on our ability to utilize net operating loss carryforwards could cause income taxes to be paid earlier than would be paid if such limitations were not in effect and could cause such net operating loss carryforwards to expire unused, in each case reducing or eliminating the benefit of such net operating loss carryforwards. Furthermore, we may not be able to generate sufficient taxable income to utilize our net operating loss carryforwards before they expire. If any of these events occur, we may not derive some or all of the expected benefits from our net operating loss carryforwards.utilize the aforementioneduse our net operating loss carryforwards and other tax attributes may be limited.utilize suchuse those carryforwards in tax years beginning after December 31, 2020, to 80% of taxable income for the tax years beginning after December 31, 2020.year. Net operating loss carryforwards generated before January 1, 2018, (which represent the substantial majority of our net operating losses as of January 31, 2021) will not be subject to the Tax Act’s 80% taxable income limitation, andbut will continue to have a twenty-year carryforward period. Nevertheless,As such, our net operating loss carryforwards and other tax assets could expire before utilization and could be subject to limitations, which could harm our business, revenue, and financial results.as a result ofdue to changes in the applicable tax principles, including increased tax rates, new tax laws, or revised interpretations of existing tax laws and precedents. In addition, the authorities in the jurisdictions in which we operate through our subsidiaries could review our tax returns or require us to file tax returns in jurisdictions in which we are not currently filing, and could impose additional tax, interest, and penalties. These authorities could also claim that various withholding requirements apply to us or our subsidiaries, assert that benefits of tax treaties are not available to us or our subsidiaries, or challenge our methodologies for valuing developed technology or intercompany arrangements, including our transfer pricing. The relevant taxing authorities may determine that the manner in which we operate our business does not achieve the intended tax consequences. If such a disagreement was to occur, and our position was not sustained, we could be required to pay additional taxes, and interest, and penalties. Such authorities could claim that various withholding requirements apply to us or our subsidiaries or assert that benefits of tax treaties are not available to us or our subsidiaries. Any increase in the amount of taxes we pay or that are imposed on us could increase our worldwide effective tax rate and harm our business and results of operations.41of taxation of international business activitiesand other jurisdictions or the adoption of other tax reform policies could materially impact our financial position and results of operations.U.S. tax laws including those that increaseof the U.S. corporate tax rate,United States and other jurisdictions could impact the tax treatment of our earnings. For example, the Tax Act has eliminated the option to deduct research and development expenditures currently and instead requires taxpayers to capitalize and amortize such expenditures over five or fifteen years, for U.S.-based and non-U.S. based research expenditures, respectively, beginning in 2022. However, recently proposed tax legislation, if enacted, would restore the ability to deduct currently U.S.-based research expenditures through 2025 and would retroactively restore this benefit for 2022 and 2023. Further, the United States recently enacted the Inflation Reduction Act of 2022, or the IRA, which introduced a 15% minimum tax on adjusted book income over one billion, and a 1% excise tax on stock buybacks. We do not currently expect the IRA will have a material impact on our income tax liability. Further, the Organization for Economic Cooperation and Development has proposed implementing a global minimum tax of 15%, which has been agreed to by over 136 countries. The Council of the European Union has adopted this proposed 15% global minimum tax, which has been implemented into the domestic laws of some jurisdictions, effective for fiscal years beginning on or after December 31, 2023. Due to expansion of our international business activities, such proposed changes, as well as regulations and legal decisions interpreting and applying these changes may increase our worldwide effective tax rate and adversely affect our financial position and results of operations.could affect the reporting of transactions completed before the announcement of a change. Additionally, if there are changes to certain of our facts-and-circumstances or if regulators changed their interpretation, we might be required to change the way we report our financial results. seek to acquire or invest in businesses, joint ventures, and platform technologies that we believe could complement or expand our platform, enhance our technology, or otherwise offer growth opportunities. We42are able to completeclose may not result in the synergies or other benefits we expect to achieve, including the introduction of new products or enhancements to existing products, which could result in substantial impairment charges. These transactions could also result in dilutive issuances of equity securities or the incurrence of debt, which could adversely affect our results of operations.or prevent fraud, or comply with applicable regulations, and investor confidence may, therefore, be adversely affected.Our credit facility provides our lender with a first-priority lien against substantially all of our assets and contains restrictive covenants which could limit our operational flexibility and otherwise adversely affect our financial condition.Our revolving credit facility allows us to borrow up to $50.0 million, and we have not borrowed any amounts under this agreement. In the event we borrow amounts under our credit facility, we will become subject to a number of covenants that may limit our ability to, among other things, transfer or dispose of assets, pay dividends or make distributions, incur additional indebtedness, create liens, make investments, loans and acquisitions, engage in transactions with affiliates, merge or consolidate with other companies, and sell substantially all of our assets. Our credit facility is secured by substantially all of our assets. The terms of our credit facility may restrict our current and future operations and could adversely affect our ability to finance our future operations or capital needs, execute preferred business strategies, make it more difficult for us to successfully execute our business strategy, and compete against companies who are not subject to such restrictions. Additionally, any obligations to repay principal and interest on our indebtedness make us vulnerable to economic or market downturns.43Our failure to comply with the covenants or payment requirements, or other events specified in our credit facility, could result in an event of default and our lender may accelerate our obligations under our credit facility and foreclose upon the collateral, or we may be forced to sell assets, restructure our indebtedness, or seek additional equity capital, which would dilute our stockholders’ interests. Our failure to comply with any covenant could result in an event of default under the agreement and the lender could make the entire debt immediately due and payable. If this occurs, we might not be able to repay our debt or borrow sufficient funds to refinance it. Even if new financing is available, it may not be on terms that are acceptable to us. According to the U.S. Department of Labor, the annual inflation rate for the United States was approximately 7.0% for the 12 months ended December 31, 2021. If the inflation rate continues to increase, such as increases in the costs of labor and supplies, it will affect our expenses, such as employee compensation which accounts for a significant portion of our operating expenses. Additionally, the United States is experiencing an acute workforce shortage,historically low unemployment rates, which in turn, has createdcreates a hyper-competitivecompetitive wage environment that may increase our operating costs. To the extent inflation results inleads to rising interest rates, resulting in higher borrowing costs to us, and has other adverse effects on the market, it may adversely affect our consolidated financial condition and results of operations.result of the COVID-19 pandemic.the aforementionedthese risks may beincrease further increased if our course of action in response to catastrophic events prove to beproves inadequate.44 including the COVID-19 pandemic, have had, and could in the future have an adverse impact on our business, operations, and the markets and communities in which we, our partners, and customers operate. including the COVID-19 pandemic, impacting the markets and communities in which we, our partners, and customers operate. The ongoing global COVID-19 pandemic has adversely impacted, and may continue to adversely impact, certain parts of our business. In industries that were heavily impacted by the pandemic, such as travel and hospitality, we experienced a slowdown in customer spending on our products. Additionally, we also took responsive measures to the pandemic that impacted our business. For example, we suspended non-essential travel by our employees, required events to be held virtually, and temporarily closed our offices. These responsive measures negatively impacted our in-person conferences, the length and variability of our sales cycles, the rate of sales to new customers, our international operations, and the hiring and onboarding of new employees across the organization.The pandemic wasalso ledcould lead to existing and potential customers accelerating transitions for some customers to the cloud. As a result, we believe the value of our offering has become increasingly relevant during the course of the pandemic, which may result in a positive impact on our business over the long term. However, if customers do not transition to the cloud at anticipated rates, we may not experience these anticipated benefits.the COVID-19 pandemichealth epidemics on our customers and our customers’ response to the COVID-19 pandemicepidemics is difficult to assess or predict, and we may be unable to accurately forecast our revenues or financial results, especially given thatwhen the long-term impact of the pandemic remainsepidemic is uncertain. Our results of operations could be materially above or below our forecasts, which could adversely affect our results of operations, disappoint analysts and investors, and/or cause our stock price to decline.The global impact of COVID-19 continues to evolve, and we will continue to monitor the situation closely. the COVID-19 pandemic or a similar health epidemicepidemics is highly uncertain and subject to change. We do not yet know the full extent of potential delays or impacts on our business, operations, ability to access capital, or the global economy as a whole. While the spread of COVID-19 may be contained or mitigated, thereThere is also no guarantee that a future outbreak of this or any other widespread epidemics will not occur, or that the global economy will recover, either of which could harm our business.45the expiration of contractual lock-up agreements and sales of shares of our Class A common stock by us or our stockholders;•2022,2024, our executive officers and directors and their affiliates together hold and/or control approximately 37.6%43% of the voting power of our outstanding common stock, and Armon Dadgar, and Mitchell Hashimoto, our co-founders, together holdco-founder, holds and/or controlcontrols approximately 22.4%18% of the voting power of our outstanding common stock. As a result, our executive officers, directors, and other affiliates have significant influence over our management and affairs and over all matters requiring stockholder approval, including election of directors and significant corporate transactions, such as a merger or other sale of the company or our assets, for the foreseeable future.46and Standard & Poor’s dodoes not allow most newly public companies utilizingwith dual or multi-class capital structures to be included in their indices. Affected indices include the Russell 2000 and the S&P 500, S&P MidCap 400, and S&P SmallCap 600, which together make up the S&P Composite 1500. Also, in 2017, MSCI, a leading stock index provider, opened public consultations on its treatment of no-vote and multi-class structures and temporarily barred new multi-class listings from certain of its indices; however, in October 2018, MSCI announced its decision to include equity securities “with unequal voting structures” in its indices and to launch a new index that specifically includes voting rights in its eligibility criteria. Under the announced policies, our dual-class capital structure makes us ineligible for inclusion in certain indices, and as a result, mutual funds, exchange-traded funds, and other investment vehicles that attempt to passively track these indices will not be investing in our stock. In addition, we cannot assure you that other stock indices will not take similar actions. Given the sustained flow of investment funds into passive strategies that seek to track certain indices, exclusion from certain stock indices would likely preclude investment by many of these funds and would make our Class A common stock less attractive to other investors. As a result, the trading price, volume, and liquidity of our Class A common stock could be adversely affected.theour initial public offering, or IPO, have substantial unrecognized gains on the value of the equity they hold based on recent market prices of our shares of Class A common stock, and therefore, they may take steps to sell their shares or otherwise secure the unrecognized gains on those shares. We are unable to predict the timing of or the effect that such sales may have on the prevailing market price of our Class A common stock.2022,2024, up to 7,017,9204,484,297 shares of our Class B common stock and up to 15,769,50813,945,779 shares of our Class A common stock may be issued upon exercise of outstanding stock options or vesting and settlement of outstanding restricted stock units, or RSUs, and 17,560,87929,058,446 shares of our Class A common stock are available for future issuance under our 2021 Equity Incentive Plan and 2021 Employee Stock Purchase Plan, and 2014 Stock Plan, and will become eligible for sale in the public market to the extent permitted by the provisions of various vesting schedules, exercise limitations, and Rule 144 and Rule 701 under the Securities Act of 1933, as amended, or the Securities Act. We have registered all of the shares of Class A common stock issuable upon exercise of outstanding options and all of the shares of Class A common stock issuable upon vesting and settlement of RSUs, as well as other equity incentive awards we may grant in the future for public resale under the Securities Act. Shares of Class A common stock will become eligible for sale in the public market to the extent such options are exercised and RSUs settle, subject to compliance with applicable securities laws. If these additional shares of Class A common stock are sold, or if it is perceived that they will be sold, in the public market, the trading price of our Class A common stock could decline.47We are an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our Class A common stock less attractive to investors.We are an “emerging growth company,” as defined in the JOBS Act, and have the option to utilize certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We may take advantage of these reporting exemptions until we are no longer an emerging growth company. We will remain an emerging growth company until the earlier of (i) the last day of the fiscal year (A) following the fifth anniversary of our IPO, (B) in which we have total annual revenue of at least $1.07 billion, or (C) in which we are deemed to be a large accelerated filer, with at least $700 million of equity securities held by non-affiliates as of the prior June 30th, and (ii) the date on which we have issued more than $1 billion in non-convertible debt during the prior three-year period.Under the JOBS Act, emerging growth companies can also delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards and, therefore, we will be subject to the same new or revised49accounting standards as other public companies that are not emerging growth companies. However, we may take advantage of some of the other reduced regulatory and reporting requirements that will be available to us so long as we qualify as an emerging growth company.Among other things, this means that our independent registered public accounting firm will not be required to provide an attestation report on the effectiveness of our internal control over financial reporting so long as we qualify as an emerging growth company, which may increase the risk that weaknesses or deficiencies in our internal control over financial reporting go undetected. Likewise, so long as we qualify as an emerging growth company, we may elect not to provide you with certain information, including certain financial information and certain information regarding compensation of our executive officers, that we would otherwise have been required to provide in filings we make with the SEC, which may make it more difficult for investors and securities analysts to evaluate our company. As a result, investor confidence in our company and the market price of our Class A common stock may be adversely affected. Further, we cannot predict if investors will find our Class A common stock less attractive because we will rely on these exemptions. If some investors find our Class A common stock less attractive as a result, there may be a less active trading market for our Class A common stock and our stock price may be more volatile.Comments.CommentsNoneThis includes the deployment of technical security monitoring and alerting measures to identify potential incidents. In the event of a cybersecurity incident, the Security organization and relevant teams throughout the company follow a formalized, documented incident response plan. This plan includes immediate actions to assess and mitigate the impact of an incident, as well as subsequent actions to remediate and help prevent future incidents of a similar nature.remote-firsthybrid remote company with a global distributed workforce.7,11, "Commitments and Contingencies" each included elsewhere in this Annual Report on Form 10-K.21, 2022,14, 2024, there were 59785 stockholders of record of our common stock, and the closing price of our common stock was $48.44$25.74 per share as reported on the Nasdaq Global Select Market. Because many shares of our Class A common stock are held by brokers and other institutions as record holders and on behalf of stockholders, we are unable to estimate the total number of stockholders represented by these record holders.S&P 500NASDAQ Composite Index and the S&P 500 Information TechnologyNASDAQ Computer Index. The graph assumes $100 was invested at the market close on December 9, 2021, which was our initial trading day, in our Class A common stock.stock through January 31, 2024. Data for the S&P 500NASDAQ Composite Index and the S&P 500 Information TechnologyNASDAQ Computer Index assume reinvestment of dividends. Our offering price of our Class A common stock in our IPO, which had a closing stock price of $85.19 on December 9, 2021, was $80.00 per share.Comparison of Cumulative Total Returns