Forward-looking statements, which are based on certain assumptions and describe future plans, strategies, and expectations of the Company, are generally identified by use of the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “project,” “seek,” “strive,” “try,” or future or conditional verbs such as “will,” “would,” “should,” “could,” “may,” or similar expressions. Although we believe that our plans, intentions, and expectations as reflected in these forward-looking statements are reasonable, we can give no assurance that they will be achieved or realized.

Our ability to predict results or the actual effects of our plans and strategies is inherently uncertain. Accordingly, actual results, performance, or achievements could differ materially from those contemplated, expressed, or implied by the forward-looking statements contained in this report.

There are a number of factors, many of which are beyond our control, that could cause actual conditions, events, or results to differ significantly from those described in our forward-looking statements. These factors include, but are not limited to:

others;

1

| Term | Definition | Term | Definition | |||||||||||||||||

| ACL | Allowance for Credit Losses | FHLB-NY | Federal Home Loan Bank of New York | |||||||||||||||||

| ADC | Acquisition, development, and construction loan | FOMC | Federal Open Market Committee | |||||||||||||||||

| ALCO | Asset and Liability Management Committee | FRB | Federal Reserve Board | |||||||||||||||||

| AOCL | Accumulated other comprehensive loss | FRB-NY | Federal Reserve Bank of New York | |||||||||||||||||

| ASC | Accounting Standards Codification | FTEs | Full-time equivalent employees | |||||||||||||||||

| ASU | Accounting Standards Update | GAAP | U.S. generally accepted accounting principles | |||||||||||||||||

| BaaS | Banking as a Service | GLBA | The Gramm Leach Bliley Act | |||||||||||||||||

| BOLI | Bank-owned life insurance | GNMA | Government National Mortgage Association | |||||||||||||||||

| BP | Basis point(s) | GSE | Government-sponsored enterprises | |||||||||||||||||

| BTFP | Bank Term Funding Program | HELOC | Home Equity Line of Credit | |||||||||||||||||

| C&I | Commercial and industrial loan | HELOAN | Home Equity Loan | |||||||||||||||||

| CDs | Certificates of deposit | HPI | Housing Price Index | |||||||||||||||||

| CECL | Current Expected Credit Loss | LGG | Loans with government guarantees | |||||||||||||||||

| CFPB | Consumer Financial Protection Bureau | LHFS | Loans Held-for-Sale | |||||||||||||||||

| CMOs | Collateralized mortgage obligations | LIBOR | London Interbank Offered Rate | |||||||||||||||||

| CMT | Constant maturity treasury rate | LTV | Loan-to-value ratio | |||||||||||||||||

| CPI | Consumer Price Index | MBS | Mortgage-backed securities | |||||||||||||||||

| CPR | Constant prepayment rate | MSRs | Mortgage servicing rights | |||||||||||||||||

| CRA | Community Reinvestment Act | NIM | Net interest margin | |||||||||||||||||

| CRE | Commercial real estate loan | NOL | Net operating loss | |||||||||||||||||

| DIF | Deposit Insurance Fund | NPAs | Non-performing assets | |||||||||||||||||

| DFA | Dodd-Frank Wall Street Reform and Consumer Protection Act | NPLs | Non-performing loans | |||||||||||||||||

| DSCR | Debt service coverage ratio | NPV | Net Portfolio Value | |||||||||||||||||

| EPS | Earnings per common share | NYSE | New York Stock Exchange | |||||||||||||||||

| ERM | Enterprise Risk Management | OCC | Office of the Comptroller of the Currency | |||||||||||||||||

| ESOP | Employee Stock Ownership Plan | OREO | Other real estate owned | |||||||||||||||||

| EVE | Economic Value of Equity at Risk | PAA | Purchase accounting adjustments | |||||||||||||||||

| Fannie Mae | Federal National Mortgage Association | PSAs | Performance-Based Restricted Stock Units | |||||||||||||||||

| FASB | Financial Accounting Standards Board | ROU | Right of use asset | |||||||||||||||||

| FDI Act | Federal Deposit Insurance Act | RSAs | Restricted Stock Awards | |||||||||||||||||

| FDIC | Federal Deposit Insurance Corporation | SBA | Small Business Administration | |||||||||||||||||

| FHA | Federal Housing Administration | Signature | Signature Bridge Bank, N.A. | |||||||||||||||||

| FHFA | Federal Housing Finance Agency | SEC | U.S. Securities and Exchange Commission | |||||||||||||||||

| FHLB | Federal Home Loan Bank | SOFR | Secured Overnight Financing Rate | |||||||||||||||||

| Freddie Mac | Federal Home Loan Mortgage Corporation | TDR | Troubled debt restructurings | |||||||||||||||||

2

In addition, the timing and occurrence or non-occurrence of events may be subject to circumstances beyond our control.

Furthermore, on an ongoing basis, we evaluate opportunities to expand through mergers and acquisitions and opportunities for strategic combinations with other banking organizations. Our evaluation of such opportunities involves discussions with other parties, due diligence, and negotiations. As a result, we may decide to enter into definitive arrangements regarding such opportunities at any time.

In addition to the risks and challenges described above, these types of transactions involve a number of other risks and challenges, including:

3

See Part I, Item 1A, “Risk Factors” in this annual report and in our other SEC filings for a further discussion of important risk factors that could cause actual results to differ materially from our forward-looking statements.

Readers should not place undue reliance on these forward-looking statements, which reflect our expectations only as of the date of this report. We do not assume any obligation to revise or update these forward-looking statements except as may be required by law.

4

GLOSSARY

BARGAIN PURCHASE GAIN

CHARGE-OFF

DERIVATIVE

5

6

YIELD

•LIST OF ABBREVIATIONS AND ACRONYMSconditions in the securities markets and real estate markets or the banking industry;

| Business |

| ||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

|

| |||||

PART I

ITEM 1. BUSINESS

General

9

While we continue to originate ADC and C&I loans for investment, such loans represent a small portion of our loan portfolio as compared to multi-family, CRE loans, and specialty finance loans.

10

The 21Parent Company also has four direct subsidiaries of the(including Flagstar Bank, are:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The 12 subsidiaries of Bank-owned entities are:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

N.A). NYB Realty Holding Company, LLC, a subsidiary of the Bank, owns interests in 10 additional active entities organized as indirect wholly-owned subsidiaries to own interests in various real estate properties.

12

See Note 12 “Borrowed- Borrowed Funds,” in Item 8, “Financial Statements and Supplementary Data,” for a further discussion of the Company’s special business trusts. The Parent Company also has one non-banking subsidiary that was established in connection with the acquisition of Atlantic Bank of New York and two non-banking insurance subsidiaries that were acquired in connection with the Flagstar acquisition.

13

14

15

16

17

elements, including board and management oversight and strategic planning, portfolio management, development of underwriting standards, risk assessment and monitoring through market analysis and stress testing, and maintenance of increased capital levels as needed to support the level of CRE lending.

18

Enforcement

We expect an increase in special assessment expense, which is not expected to be material, on or around June 2024 based on the FDIC’s modified loss estimate.

20

evaluate the institution’s record of making loans in its assessment areas; (2) investment, to evaluate the institution’s record of investing in community development projects, affordable housing, and programs benefiting low- or moderate-income individuals and businesses; and (3) service, to evaluate the institution’s delivery of services through its branches, ATMs and other offices. The CRA requires each federal banking agency, in connection with its examination of a financial institution, to assess and assign one of four ratings to the institution’s record of meeting the credit needs of the community and to take such record into account in its evaluation of certain applications by the institution, including applications for charters, branches and other deposit facilities, relocations, mergers, consolidations, acquisitions of assets or assumptions of liabilities, and bank holding company and savings and loan holding company acquisitions. The CRA also requires that all institutions make public disclosure of their CRA ratings.

The final rule (i) encourages banks to expand access to credit, investment and banking services in low- and moderate-income communities, (ii) adapts to changes in the banking industry, including mobile and online banking, (iii) provides greater clarity and consistency in the application of CRA regulations and (iv) tailors CRA evaluations and data collection to bank size and type.Under the final rule, the agencies will evaluate bank performance across the varied activities they conduct and communities in which they operate so that the CRA continues to be an effective tool to address inequities in access to credit and financial services.The final rule also updates existing CRA regulations to evaluate lending outside traditional assessment areas generated by the growth of non-branch delivery systems, such as online and mobile banking, branchless banking, and hybrid models. In addition, the final rule implements a new metrics-based approach to evaluating bank retail lending and community development financing, using benchmarks based on peer and demographic data.Most of the final rule’s requirements will become effective beginning on January 1, 2026 and the remaining requirements, including the final rule’s data reporting requirements, will become effective on January 1, 2027.

21

Cybersecurity

22

under the Sarbanes-Oxley Act have several requirements, including having those Officers certify that they are responsible for establishing, maintaining and regularly evaluating the effectiveness of our internal controls over financial reporting; that they have made certain disclosures to our auditors and the Audit Committee of the Board of Directors about our internal control over financial reporting; and they have included information in our quarterly and annual reports about their evaluation and whether there have been changes in our internal control over financial reporting or in other factors that could materially affect internal control over financial reporting.

23

to supervision and examination by applicable state regulatory authorities in the jurisdictions in which we may offer consumer financial products or services.

24

own financial requirements. We are also subject to examination by Fannie Mae, FHA and VA to assure compliance with the applicable regulations, policies and procedures. Mortgage origination activities are subject to, among others, the Equal Credit Opportunity Act, the Federal Truth-in-Lending Act, the Fair Housing Act, the Fair Credit Report Act, the National Flood Insurance Act and the Real Estate Settlement Procedures Act and related regulations that prohibit discrimination and require the disclosure of certain basic information to mortgagors concerning credit terms and settlement costs. Our mortgage banking operations are also affected by various state and local laws and regulations and the requirements of various private mortgage investors.

Mortgage Restructuring”), (b) affiliates of funds managed by Hudson Bay Capital Management, LP (“

Legacy Flagstar proactively rightsized its mortgage operation throughout 2022Hudson Bay”), (c) affiliates of funds managed by Reverence Capital Partners L.P. (“Reverence”), and (d) certain other investors (the “Other Investors” and, collectively with Liberty, Reverence and Hudson Bay, the “Investors”, and the investments agreements entered into with each of the Investors on March 7, 2024, collectively, the “Original Investment Agreements”). On March 11, 2024, NYCB entered into separate amendments to adjust for market conditions. The mortgage business is cyclical by naturethe Original Investment Agreements with Liberty (such agreement, as amended, the “Liberty Investment Agreement”), Hudson Bay (such agreements, as amended, the “Hudson Bay Investment Agreements”) and challenging conditions are expectedReverence (such agreement, as amended, the “Reverence Agreement” and, collectively with the Liberty Agreement, the Hudson Bay Agreements and the Original Investment Agreements of the Other Investors, the “Investment Agreements”).

We expect that these actions will optimize our mortgage business and improve profitability duringInvestment Agreements, on March 11, 2024, the current mortgage down cycle, while still allowing us to participateInvestors invested an aggregate of approximately $1.05 billion in the upside onceCompany in exchange for the interest rate cycle becomes favorable. This allows us to maintainsale and issuance by the Company of (a) 76,630,965 shares of our common stock, at a retail presence withinpurchase price per share of $2.00, (b) 192,062 shares of a new series of our nine-state footprint, leveragespreferred stock, par value $0.01 per share, designated as Series B Noncumulative Convertible Preferred Stock (the “Series B Preferred Stock”), at a price per share of $2,000, each share of which is convertible into 1,000 shares of common stock (or, in certain limited circumstances, one share of Series C Preferred Stock (as defined below)), (c) 256,307 shares of a new series of our marketingpreferred stock, par value $0.01 per share, designated as Series C Noncumulative Convertible Preferred Stock (the “Series C Preferred Stock”, together with the Series B Preferred Stock, the “Preferred Stock”), at a price per share of $2,000, each share of which is convertible into 1,000 shares of common stock, and branding spend, and reduces risk. More importantly, it leaves our position within(d) warrants (the “Issued Warrants”), which may not be exercised until 180 days after issuance thereof, affording the mortgage industry intact. We remain oneholder thereof the right, until the seven-year anniversary of the largest bank originators,issuance of such Issued Warrant, to purchase for $2,500 per share, shares of a new class of non-voting, common-equivalent preferred stock of the 6th largest sub-servicerCompany (the “Series D NVCE Stock”), each share of Series D NVCE Stock is convertible into 1,000 shares of common stock (or, in certain limited circumstances, one share of Series C Preferred Stock), and all of which shares of Series D NVCE Stock, upon issuance, will represent the right (on an as converted basis) to receive 315,000,000 million shares of common stock.

ITEM

26

Changes to and replacement of the LIBOR Benchmark Interest Rate may adversely affect our business, financial condition, and results of operations.

The Company has certain loans, interest rate swap agreements, investment securities, and debt obligations whose interest rate is indexed to LIBOR. In 2017, the FCA, which is responsible for regulating LIBOR, announced that the publication of LIBOR is not guaranteed beyond 2021. In December 2020, the administrator of LIBOR announced its intention to (i) cease the publication of the one-week and two-month U.S. dollar LIBOR after December 31, 2021, and (ii) cease the publication of all other tenors of U.S. dollar LIBOR (one, three, six, and 12-month LIBOR) after June 30, 2023, and on March 15, 2021, announced that it will permanently cease to publish most LIBOR settings beginning on January 1, 2022 and cease to publish the overnight, one-month, three-month, six-month, and 12-month U.S. dollar LIBOR settings on July 1, 2023. Accordingly, the FCA has stated that it does not intend to persuade or compel banks to submit to LIBOR after such respective dates. Until such time, however, FCA panel banks have agreed to continue to support LIBOR. In October 2021, the Federal bank regulatory agencies issued a Joint Statement on Managing the LIBOR Transition that offered their regulatory expectations and outlined potential supervisory and enforcement consequences for banks that fail to adequately plan for and implement the transition away from LIBOR. The failure to properly transition away from LIBOR may result in increased supervisory scrutiny. The implementation of a substitute index for the calculation of interest rates under the Company's loan agreements may result in disputes or litigation with counterparties over the appropriateness or comparability to LIBOR of the substitute index, which would have an adverse effect on the Company's results of operations. Even when robust fallback language is included, there can be no assurances that the replacement rate plus any spread adjustment will be economically equivalent to LIBOR, which could result in a lower interest rate being paid to the Company on such assets.

The Alternative Reference Rates Committee (a group of private-market participants convened by the FRB and the FRB-NY) has identified SOFR as the recommended alternative to LIBOR. The use of SOFR as a substitute for LIBOR is voluntary and may not be suitable for all market participants. SOFR is calculated and observed differently than LIBOR. Given the manner in which SOFR is calculated, it is likely to be lower than LIBOR and is less likely to correlate with the funding costs of financial institutions. Market practices related to SOFR calculation conventions continue to develop and may vary. Inconsistent calculation conventions among financial products may expose is to increased basic rate and resultant costs. Other alternatives to LIBOR also exist, but, because of the difference in how those alternatives are constructed, they may diverge significantly from LIBOR in a range of situations and market conditions.

27

repayment of the loans often depends on the successful operation of the properties and the sale of such properties securing the loans. Such loans typically involve larger loan balances to single borrowers or groups of related borrowers compared to one-to-four family residential loans. Also, many of our borrowers have more than one of these types of loans outstanding. Consequently, an adverse development with respect to one loan or one credit relationship can expose us to a significantly greater risk of loss compared to an adverse development with respect to a one-to-four family residential real estate loan. In addition, if loans that are collateralized by real estate become troubled and the value of the real estate has been significantly impaired, then we may not be able to recover the full contractual amount of principal and interest that we anticipated at the time we originated the loan, which could cause us to increase our provision for loan losses and adversely affect our operating results and financial condition.

28

29

30

condition, or results of operations. Penalties for such violations may also include: revocation of licenses; fines and other monetary penalties; civil and criminal liability; substantially reduced payments by borrowers; modification of the original terms of loans, permanent forgiveness of debt, or inability to, directly or indirectly, collect all or a part of the principal of or interest on loans provided by the Bank. Changes in such regulation and supervision, or changes in regulation or enforcement by such authorities, whether in the form of policy, regulations, legislation, rules, orders, enforcement actions, ratings, or decisions, could have a material impact on the Company, our subsidiary bank and other affiliates, and our operations. In addition, failure of the Company or the Bank to comply with such regulations could have a material adverse effect on our earnings and capital. See “Regulation and Supervision” in Part I, Item 1, “Business” earlier in this filing for a detailed description of the federal, state, and local regulations to which the Company and the Bank are subject.

31

In addition, there can be no assurance that we will achieve our anticipated effective tax rate. Unanticipated changes in tax laws or related regulatory or judicial guidance, or an audit assessment that denies previously recognized tax benefits, could result in our recording tax expenses that materially reduce our net income.

Higher inflation could have a negative impact on our financial results and operations.

Inflation can negatively impact the Company by increasing our labor costs, through higher wages and higher interest rates, which may negatively affect the market value of securities on our balance sheet, higher interest expenses on our deposits, especially CDs, and a higher cost of our borrowings. Additionally, higher inflation levels could lead to higher oil and gas prices, which may negatively impact the net operating income on the properties which we lend on and could impair a borrower's ability to repay their mortgage.

32

sales for the Bank and for other financial institutions have risen and fallen in response to these and other factors. An increase in interest rates and/or a decrease in our mortgage production volume could have a materially adverse effect on our operating results. The 10-year U.S. Treasury rate was 3.883.97 percent at December 31, 2022,2023, and averaged 2.952.96 percent during 2022, 1512023, 101 basis points higher than average rates experienced during 2021.2022. The sustained higher rates experienced throughout 20222023 negatively impacted the mortgage market including our loan origination volume and refinancing activity. In addition to being affected by interest rates, the secondary mortgage markets are also subject to investor demand for residential mortgage loans and investor yield requirements for these loans. These conditions may fluctuate or worsen in the future. Adverse market conditions, including increased volatility, changes in interest rates and mortgage spreads and reduced market demand, could result in greater risk in retaining mortgage loans pending their sale to investors. A prolonged period of secondary market illiquidity may result in a reduction of our loan mortgage production volume and could have a materially adverse effect on our financial condition and results of operations.

33

provided by Fannie Mae and Freddie Mac or the insurance provided by the FHA could also have broad adverse market implications. The fees that we are required to pay to the Agencies for these guarantees have changed significantly over time and any future increases in these fees would adversely affect our business, financial condition and results of operations.

34

The Parent Company (i.e., the company on an unconsolidated basis) is a separate and distinct legal entity from the Bank, and a substantial portionexpedited nature of the revenuesFDIC-assisted transaction did not allow bidders the Parent Company receives consiststime and access to information customarily associated with preparing for and evaluating a negotiated transaction. As a result, fair value estimates we have made in connection with the Signature transaction may be inaccurate and subject to change, which could adversely impact our financial condition, results of dividendsoperations and future prospects. In addition, we may obtain additional information and evidence during the period of one year from March 20, 2023, the Bank. These dividends aredate we completed the primary funding source forSignature transaction, that may result in changes to the dividends we pay on our common stock and the interest and principal payments on our debt. Various federal and state laws and regulations limitestimated amounts recorded as of December 31, 2023, which could change the amount of dividends that a bank may paythe bargain purchase gain we have recorded. Adjustments to its parent company. In addition, our right to participate in a distribution of assets upon the liquidation or reorganization of a subsidiarythis gain may be subject torecorded based on additional information received after the prior claimsacquisition date that affect the measurement of the subsidiary’s creditors. As a resultassets acquired and liabilities assumed and any decrease in the amount of our acquisition of Flagstar, we are required to seek regulatory approval from the OCC for the payment of any dividend to the Bancorp through at least the period ending November 1, 2024. If the Bank is unable to pay dividends to the Parent Company, we might not be able to service our debt, pay our obligations, or pay dividends on our common stock.

Reduction or elimination of our quarterly cash dividend could have an adverse impact on the market price of our common stock.

Holders of our common stock are only entitled to receive such dividends as our Board of Directors may declare out of funds available for such payments under applicable law and regulatory guidance, and althoughbargain purchase gain we have historically declared cash dividends onrecorded could also adversely impact our common stock, we are not required to do so. Furthermore, the paymentfinancial condition, results of dividends falls under federal regulations that have grown more stringent in recent years. While we pay our quarterly cash dividend in compliance with current regulations, such regulations could change in the future. As a result of our acquisition of Flagstar, we are required to seek regulatory approval from the OCC for the payment of any dividend to the Parent Company through at least the period ending November 1, 2024, which could restrict our ability to pay the common stock dividend. Any reduction or elimination of our common stock dividend in theoperations and future could adversely affect the market price of our common stock.prospects.

35

performance, the models they are based on may prove to be inadequate or inaccurate because of other flaws in their design or implementation. If the models we use in the process of managing our interest rate and other risks prove to be inadequate or inaccurate, we could incur increased or unexpected losses which, in turn, could adversely affect our earnings and capital. Additionally, failure by the Company to maintain compliance with strict capital, liquidity, and other stress test requirements under banking regulations could subject us to regulatory sanctions, including limitations on our ability to pay dividends.

Any failure, breach, or interruption in service involving our systems or those

36

our customers, to adequately process and account for our customers’ transactions, or otherwise conduct our business could be adversely impacted by any disruption in the services provided by these third parties; their failure to handle current or higher volumes of usage; or any difficulties we may encounter in communicating with them. Replacing these third-party providers also could entail significant delay and expense. Our third-party providers may be vulnerable to unauthorized access, computer viruses, phishing schemes, and other security breaches. Threats to information security also exist in the processing of customer information through various other third-party providers and their personnel. We may be required to expend significant additional resources to protect against the threat of such security breaches and computer viruses, or to alleviate problems caused by such security breaches or viruses. To the extent that the activities of our third-party providers or the activities of our customers involve the storage and transmission of confidential information, security breaches and viruses could expose us to claims, regulatory scrutiny, litigation, and other possible liabilities. These types of third-party relationships are subject to increasingly demanding regulatory requirements and oversight by federal bank regulators (such as the Federal Reserve Board, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation) and the CFPB. As a result, if our regulators conclude that we have not exercised adequate oversight and control over vendors and subcontractors or other ongoing third-party business relationships or that such third-parties have not performed appropriately, we could be subject to enforcement actions, including civil money penalties or other administrative or judicial penalties or fines, as well as requirements for consumer remediation. In addition, the Company may not be adequately insured against all types of losses resulting from third-party failures, and our insurance coverage may be inadequate to cover all losses resulting from systems failures or other disruptions to our banking services.

37

institution. Further, as servicer or subservicer of loans, we have certain contractual obligations, including foreclosing on defaulted mortgage loans or, to the extent applicable, considering alternatives to foreclosure. If we commit a material breach of our obligations as servicer, we may be subject to termination if the breach is not cured within a specified period of time following notice, causing us to lose servicing income.

38

burden and the system requirements associated with complying with these rules or potential changes to these rules could impact our mortgage volume and increase costs. These arrangements with third-party mortgage originators and the fees payable by us to such third parties could also be subject to future regulatory scrutiny and restrictions.

39

requiring the payment of interest on escrow balances or if we would be required to retroactively credit interest on escrow funds, the Company’s earnings could be adversely affected.

| Item 1B. | Unresolved Staff Comments | ||||

| Item 1C. | Cybersecurity | ||||

| Item 2. | Properties | ||||

| Item 3. | Legal Proceedings | ||||

40

ITEM 3. LEGAL PROCEEDINGS

Not applicable.Lemm, Jr. v. New York Community Bancorp, Inc., et al., Case No. 1:24-cv-00903, filed on February 6, 2024 in the United States District Court for the Eastern District of New York. This action, which seeks unspecified compensatory damages to be proven at trial, alleges violations of the federal securities laws, including Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 (the “Exchange Act”) and SEC Rule 10b-5, with respect to disclosures concerning the Company’s business, operations and prospects, particularly regarding the impact of the Flagstar and Signature transactions and the Bank’s commercial real estate loan portfolio and related matters, that were made in the Company’s public SEC filings and press releases during the period beginning on March 1, 2023 and ending on January 30, 2024. The Company intends to vigorously defend this action and any related actions.

| Item 4. | Mine Safety Disclosures | ||||

| Item 5. | Market For the Registrant's Common Equity, Related Stockholder Matters, and Issuer Purchases | ||||

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

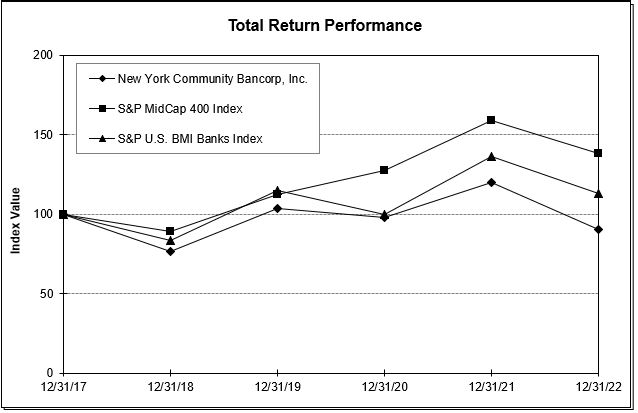

Comparison of 5-Year Cumulative Total Return

Among New York Community Bancorp, Inc.,

S&P Mid-Cap 400 Index, and S&P U.S. BMI Banks Index*

r

ASSUMES $100 INVESTED ON

| 12/31/2018 | 12/31/2019 | 12/31/2020 | 12/31/2021 | 12/31/2022 | 12/31/2023 | |||||||||||||||

| New York Community Bancorp, Inc. | $ | 100.00 | $ | 135.38 | $ | 127.51 | $ | 156.41 | $ | 118.03 | $ | 149.75 | ||||||||

| S&P Mid-Cap 400 Index | $ | 100.00 | $ | 126.20 | $ | 143.44 | $ | 178.95 | $ | 155.58 | $ | 181.15 | ||||||||

| S&P U.S. BMI Banks Index | $ | 100.00 | $ | 137.36 | $ | 119.83 | $ | 162.92 | $ | 135.13 | $ | 147.41 | ||||||||

|

| 12/31/2017 |

| 12/31/2018 |

| 12/31/2019 |

| 12/31/2020 |

| 12/31/2021 |

| 12/31/2022 |

| ||||||

New York Community Bancorp, Inc. |

| $ | 100.00 |

| $ | 76.76 |

| $ | 103.92 |

| $ | 97.88 |

| $ | 120.07 |

| $ | 90.61 |

|

S&P Mid-Cap 400 Index |

| $ | 100.00 |

| $ | 88.92 |

| $ | 112.21 |

| $ | 127.54 |

| $ | 159.12 |

| $ | 138.34 |

|

S&P U.S. BMI Banks Index |

| $ | 100.00 |

| $ | 83.54 |

| $ | 114.74 |

| $ | 100.10 |

| $ | 136.10 |

| $ | 112.89 |

|

| (dollars in millions, except share data) | ||||||||||||||||||||||||||

| Period | Total Shares of Common Stock Repurchased | Average Price Paid per Common Share | Total Allocation | Total Shares of Common Stock Purchased as Part of Publicly Announced Plans or Programs | ||||||||||||||||||||||

| First Quarter 2023 | 976,454 | $ | 9.33 | $ | 9 | 0 | ||||||||||||||||||||

| Second Quarter 2023 | 190,177 | 10.36 | 2 | 0 | ||||||||||||||||||||||

| Third Quarter 2023 | 33,956 | 12.50 | 0 | 0 | ||||||||||||||||||||||

| Fourth Quarter 2023 | ||||||||||||||||||||||||||

| October 1 - 31, 2023 | 1,525 | 10.29 | 0 | — | ||||||||||||||||||||||

| November 1 - 30, 2023 | 4,897 | 9.34 | — | — | ||||||||||||||||||||||

| December 1 - 31, 2023 | 50,526 | 9.92 | 1 | — | ||||||||||||||||||||||

| Total Fourth Quarter 2023 | 56,948 | $ | 16.57 | 1 | — | |||||||||||||||||||||

| 2023 Total | 1,257,535 | $ | 9.59 | $ | 12 | — | ||||||||||||||||||||

| Item 6. | Reserved | ||||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

(dollars in millions, except per share data) |

| Total Shares |

|

| Average Price |

|

| Total |

|

| Total Shares of Common Stock Purchased as Part of Publicly Announced Plans or Programs |

| ||||

First Quarter 2022 |

|

| 901,934 |

| $ |

| 12.93 |

| $ |

| 11 |

|

|

| — |

|

Second Quarter 2022 |

|

| 809,996 |

|

|

| 8.88 |

|

|

| 7 |

|

|

| 791,101 |

|

Third Quarter 2022 |

|

| 107,022 |

|

|

| 9.16 |

|

|

| 1 |

|

|

| 80,609 |

|

Fourth Quarter 2022 |

|

|

|

|

|

|

|

|

|

|

|

| ||||

October 1-31, 2022 |

|

| 236 |

|

|

| 8.54 |

|

|

| — |

|

|

| — |

|

November 1-30, 2022 |

|

| 2,173 |

|

|

| 9.90 |

|

|

| — |

|

|

| — |

|

December 1-31, 2022 |

|

| 515,574 |

|

|

| 8.72 |

|

|

| 5 |

|

|

| — |

|

Total Fourth Quarter 2022 |

|

| 517,983 |

|

|

| 8.72 |

|

|

| 5 |

|

|

| — |

|

2022 Total |

|

| 2,336,935 |

|

|

| 10.42 |

| $ |

| 24 |

|

|

| 871,710 |

|

44

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

EXECUTIVE SUMMARY

For the twelve monthsyear ended December 31, 2022,2023, net loss was $79 million as compared to net income wasof $650 million an increase of $54 million or 9 percent compared to the $596 million the Company reported for the twelve monthsyear ended December 31, 2021.2022. Net incomeloss available to common stockholders for the twelve monthsyear ended December 31, 20222023 was $112 million, compared to net income $617 million also up $54 million and 10 percent compared tofor the twelve monthsyear ended December 31, 2021. On a per share basis, this translates into diluted2022. Diluted (loss) earnings per share of $1.26 in full-year 2022, up 5 percenttotaled $(0.16) for the year ended December 31, 2023 compared to the $1.20 we reported in full-year 2021. In terms of profitability, our full-year 2022 results reflect a return on average assets of 1.01 percent compared to 1.04 percent in full-year 2021 and a return on average common stockholders' equity of 9.38 percent$1.26 for the full-year 2022 versus 8.75 percentyear ended December 31, 2022.

Our specialty finance portfolio increased $912 million or 26 percent to $4.4 billion at December 31, 2022. Total commitments for the specialty finance portfolio stood at $7.4$12.3 billion at December 31, 2022. The remainingmajority of the increase is attributable to the $9.9 billion of C&I loans acquired in the Signature Transaction along with continued growth through new originations.

Loans held for sale were $1.1 billion at December 31, 2022, resulting from the Flagstar acquisition. These loans consisted of one-to-four family residential mortgage loans pending sale for which we have elected the fair value option.

At December 31, 2022, multi-family loans represented 55 percent of total loans, compared to 76 percent at December 31, 2021, commercial loans (including specialty financeSignature transaction, and CRE loans) represented 33 percent compared to less than 25 percent at December 31, 2021, while residential loans represented 8 percent.

Deposit Base

Total deposits at December 31, 2022 were $58.7 billion, up $23.7 billion or 67 percent compared to $35.1 billion at December 31, 2021. Deposit growth was driven by the addition of $16.0 billion of deposits from the Flagstar acquisition and $7.6 billion growth in loan-related deposits and BaaS deposits. Non-interest-bearing deposits were $12.1 billion at December 31, 2022 and represented 21 percent of total deposits, compared to $4.5 billion, or 13 percent as of December 31, 2021. Excluding the impact of the Flagstar acquisition, deposits increased $7.6 billion or 22 percent during 2022. Loan-related deposits totaled $4.4 billion at December 31, 2022 up $389 million or 10 percent as compared to $4.0 billion at December 31, 2021.

45

In addition, our BaaS deposits totaled $11.5 billion at December 31, 2022, up $10.5 billion compared to $1.0 billion at December 31, 2021. Our BaaS deposits fall into three verticals: traditional BaaS, banking as a service for government agencies and states, which includes the U.S. Treasury's prepaid debit card program, and mortgage as a service, which caters to mortgage companies and consists primarily of escrow deposit accounts for principal, interest, and tax payments. The majority of the year-over-year growth was in the government banking as a service vertical and related to certain prepaid debit card programs.

Net Interest Income

During the twelve months ended December 31, 2022, our net interest income grew driven by our higher asset base. Net interest income for full-year 2022 was $1.4 billion, up $107 million or 8 percent compared to $1.3 billion for the twelve months ended December 31, 2021. Average interest-earning assets increased $7.0 billion or 13 percent over the course of the year to $59.3 billion primarily due to organic loan growth, and the Flagstar acquisition. The average yield increased 30 basis points to 3.53 percent. Average interest-bearing liabilities totaled $51.4 billion, up $6.2 billion or 14 percent, while the average cost of funds rose 47 basis points to 1.35 percent.

For the twelve months ended December 31, 2022, the NIM declined 12 basis points to 2.35 percent compared to 2.47 percent for the twelve months ended December 31, 2021 primarily driven byalong with the impact of higher interest rates on the liability sensitive balance sheet through November 30, 2022. With the Flagstar acquisition we remain slightly liability sensitive. See Item 7A, “Quantitative and Qualitative Disclosures About Market Risk,”. Prepayment income contributed eight basis pointsrates.

Asset Quality

Asset quality remained strong during 2022 as increases in NPAs were substantially due to changes in asset mix related to the Flagstar acquisition and centered on non-performing one-to-four family residential and home equity loans. Total NPAs0.17 percent at December 31, 2022 were $153 millionwhile NPL to total loans equaled 0.51 percent compared to $41 million0.20 percent at December 31, 2021,2022. The increase in NPLs was primarily driven by NPLsa $125 million increase in multi-family loans and a $108 million in commercial real estate loans. Repossessed assets acquiredof $14 million were slightly higher compared to $12 million in the Flagstar acquisition. At December 31, 2022, NPAsprior year.

In this capacity, Mr. DiNello serves as the most senior executive officer of the Company.

46

Year-Over-Year Comparison

The following factors contributed to the year-over-year increase in net interest income: