United States

Securities and Exchange Commission

Washington, D.C. 20549

Form 10-K

[X]x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 201127, 2014

Or

[ ]¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission File Number 0-6966

ESCALADE, INCORPORATED

(Exact name of registrant as specified in its charter)

Indiana (State of incorporation) | 13-2739290 (I.R.S. EIN) |

817 Maxwell Ave, Evansville, Indiana | ||

(Address of Principal Executive Office) | 47711 (Zip Code) |

812-467-4449

(Registrant’sRegistrant's Telephone Number)

Securities registered pursuant to Section 12(b) of the Act

Common Stock, No Par Value (Title of Class) | The NASDAQ Stock Market LLC | |

(Name of Exchange on Which Registered) |

Securities registered pursuant to section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities

Yes [ ]¨ No [X]x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act

Yes [ ]¨ No [X]x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X]x No [ ]¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X]x No [ ]¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’sregistrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See the definitions of “Large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | Accelerated filer |

| Non-accelerated filer | Smaller reporting company |

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12 b-2 of the Exchange Act).

Yes [ ]¨ No [X]x

Aggregate market value of common stock held by nonaffiliates of the registrant as of July 9, 201112, 2014 based on the closing sale price as reported on the NASDAQ Global Market: $53,085,149$170,640,965

The number of shares of Registrant’sRegistrant's common stock (no par value) outstanding as of February 6, 2012: 12,891,757.11, 2015: 14,013,809.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’sregistrant's Proxy Statement relating to its annual meeting of stockholders scheduled to be held onApril 27, 201224, 2015 are incorporated by reference into Part III of this Report.

Escalade, Incorporated and Subsidiaries

Table of Contents

General

Escalade, Incorporated (“Escalade”(Escalade, the Company, we, us or “Company”)our) now operates in twoone business segments:segment: Sporting Goods and Information Security and Print Finishing (or “Martin Yale Group”)(Escalade Sports). Escalade and its predecessors have more than 80 years of manufacturing and selling experience in thesethis industry. Previously, we operated in two industries.businesses segments: Sporting Goods (Escalade Sports) and Information Security and Print Finishing (Martin Yale Group). On October 1, 2014, the Company completed the sale of the Information Security business. The sale of the Information Security business, coupled with the previously announced sale of our Print Finishing business on June 30, 2014, represents the Company’s exit from the Information Security and Print Finishing segment. As a result, the Information Security and Print Finishing segment has been classified as discontinued operations for all periods presented and certain assets and liabilities in prior periods are classified as held for sale.

The following table presents the percentages contributed to Escalade’s net sales by each of its business segments:

| 2011 | 2010 | 2009 | 2014 | 2013 | 2012 | |||||||||||||||||||

| Sporting Goods | 72 | % | 71 | % | 66 | % | 87 | % | 81 | % | 76 | % | ||||||||||||

| Information Security and Print Finishing | 28 | % | 29 | % | 34 | % | ||||||||||||||||||

| Discontinued Operations | 13 | % | 19 | % | 24 | % | ||||||||||||||||||

| Total Net Sales | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||||

For additional segment information, see Note 14 – Operating Segment and Geographic Information in the consolidated financial statements.

Sporting Goods

Headquartered in Evansville, Indiana, Escalade Sports manufactures, imports, and distributes widely recognized sporting goods brands in familybasketball goals, archery, indoor and outdoor game recreation fitness, training, and huntingfitness products through major sporting goods retailers, specialty dealers, key on-line retailers, traditional department stores and mass merchandise retailers, and sporting goods specific retailers.merchants. Escalade is the world’s largest producer ofa leader in table tennis tables.tables, residential in-ground basketball goals and in archery bows. Some of the Company’s most recognized brands include:

| Product Segment | Brand Names | |

| Archery | Bear Archery®, Trophy Ridge®, Whisker Biscuit®, Cajun Bowfishing™ | |

| Table Tennis | STIGA®, Ping-Pong®, Prince®, | |

| Basketball | Goalrilla™, Goaliath®, Silverback® | |

| Play Systems | Woodplay®, Childlife® | |

| Fitness | The STEP®, USWeight™ | |

| Game Tables (Hockey and Soccer) | ||

| Darting | Unicorn®, Accudart®, Arachnid®, Nodor®, Winmau® | |

| Outdoor Games | Zume Games®, Pickleball Now |

In 2011,During 2014, 2013 and 2012 the Company hashad one customer, in the Sporting Goods segment, Dick’s Sporting Goods, which accounted for approximately16% 19%, 20% and 23%, respectively, of total consolidated gross revenues.the Company’s revenues from continuing operations.

As of December 27, 2014, the Company had approximately 23% of its total accounts receivable with Dick’s Sporting Goods. As of December 28, 2013 the Company had approximately 27% and 12% of its total accounts receivable with Dick’s Sporting Goods and The Sports Authority, respectively.

Escalade Sports manufactures in the USA and Mexico and imports product from Asia, where the Company utilizes a number of contract manufacturers.

Certain products produced by Escalade Sports are subject to regulation by the Consumer Product Safety Commission. The Company believes it is in material compliance with all applicable regulations.

Information Security and Print Finishing

Martin Yale Group has increasingly expanded its focus on the information security requirements of larger corporate customers, governments, and strategic business partners. The Company is particularly focused on addressing information security issues including the decommissioning or destruction of data stored on optical, solid state, magnetic, and traditional media like paper to meet the increasingly strict security standards set by the National Security Administration, National Institute of Standards and Technology, Deutsches Institut fur Normung (German Institute for Standardization), the European Union, and many other governments and organizations around the world. Martin Yale Group continues to focus on the print finishing sector with a particular focus on digital print applications.

Martin Yale Group has a worldwide presence with manufacturing facilities in Indiana and Germany and joint venture manufacturing facilities in the Czech Republic and Taiwan. Martin Yale Group has sales offices in the USA, Germany, United Kingdom, France, Spain, China, Italy, South Africa and Sweden.

Martin Yale Group products include: shredders, disintegrators, degaussers, paper folders, letter openers, and paper cutters/trimmers. The key Martin Yale Group brands include martin yale®, intimus®, and papermonster®.

Martin Yale Group products and services are sold directly to end-users as well as through retailers, wholesalers, catalogs, specialty dealers, and business partners. No single Martin Yale Group customer accounted for more than 10% of Information Security and Print Finishing sales during 2011.

Marketing and Product Development

The Company makes a substantial investment in product development and brand marketing to differentiate its product line from its competition. Each operating segment conductsWe conduct market research and development efforts to design products which satisfy existing and emerging consumer needs. On a consolidated basis, the Company incurred research and development costs of approximately $1.4$1.7 million, $1.9$1.2 million, and $2.0$1.0 million in 2011, 20102014, 2013 and 2009,2012, respectively.

The Company also makes investments in brand marketing to properly communicate the specific attributes and qualities of its products. The Company advertises directly to the consumer or end-user as well as through its retail partners in the form of advertising and other promotional allowances.

Competition

Escalade is subject to competition with various manufacturers in each product line produced or sold by Escalade.line. The Company is not aware of any other single company that is engaged in both the same industriesproduct lines as Escalade or that produces the same range of products as Escalade within such industries.Escalade. Nonetheless, competition exists for many Escalade products within both the Sporting Goods and Information Security and Print Finishing industries.products. Some competitors are larger and have substantially greater resources than the Company. Escalade believes that its long-term success depends on its ability to strengthen its relationship with existing customers, attract new customers and develop new products that satisfy the quality and price requirements of Sporting Goods and Information Security and Print Finishingsporting goods customers.

Licenses, Trademarks and Brand Names

The Company has an agreement and contract with STIGA Sports AB, a 50% owned joint venture, for the exclusive right and license to distribute and produce table tennis equipment under the brand name STIGA® for the United States and Canada. The Company also owns several registered trademarks and brand names including but not limited to Ping-Pong®, Bear Archery®, Goalrillaä, The Step®, and Wood Play® which are used in the Sporting Goods business segment and intimus® and papermonster® which are used in the Information Security and Print Finishing business segment..

Backlog and Seasonality

Sales are based primarily on standard purchase orders and in most cases orders are shipped within the same month received. Unshipped orders at the end of the fiscal year (backlog) were not material and therefore are not an indicator of future results. IncreasedDue to diversity in product categories, such as playground and basketball, over the past few years has helped the Company achieve more evenly distributed revenues in Sporting Goods. The Company does not expect Sporting Goods sales to be seasonal in the future. Demand for Information Security and Print Finishing hashave not been seasonal and isare not expected to be so in the future.

| 4 |

Employees

The number of employees at December 31, 201127, 2014 and December 25, 201028, 2013 for each business segment were as follows:

| 2011 | 2010 | 2014 | 2013 | |||||||||||||

| Sporting Goods | ||||||||||||||||

| USA | 281 | 284 | 372 | 356 | ||||||||||||

| Mexico | 105 | 98 | 83 | 106 | ||||||||||||

| Asia | 6 | 8 | 11 | 10 | ||||||||||||

| 392 | 390 | 466 | 472 | |||||||||||||

| Information Security and Print Finishing | ||||||||||||||||

| Discontinued Operations | ||||||||||||||||

| USA | 90 | 89 | — | 68 | ||||||||||||

| Europe | 126 | 121 | — | 91 | ||||||||||||

| Asia | 10 | 8 | — | 10 | ||||||||||||

| Africa | — | 7 | ||||||||||||||

| 226 | 218 | — | 176 | |||||||||||||

| Total | 618 | 608 | 466 | 648 | ||||||||||||

The I.U.E./C.W.A. (United Electrical Communication Workers of America, AFL-CIO) represents hourly rated employees at the Escalade Sports’ Evansville, Indiana distribution center. There are approximately 1318 covered employees at December 31, 2011.27, 2014. A 3-yearthree year labor contract was negotiated and renewed in April 2009; the new agreement2013 and expires on April 30, 2012.2016. Management believes it has satisfactory relations with its employees.

Sources of Supplies

Raw materials for Escalade’sEscalade's various product lines consist of wood, steel, aluminum, plastics, fiberglass and packaging. Escalade relies upon suppliers in various countries and upon various third party Asian manufacturers for certainmany of its game tables and non-security paper shredders.products. The Company believes that these sources will continue to provide adequate supplies as needed and that all other materials needed for the Company’s various operations are available in adequate quantities from a variety of domestic and foreign sources.

SEC Reports

The Company’s Internet site (www.escaladeinc.com) makes available free of charge to all interested parties the Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and all amendments to those reports, as well as all other reports and schedules filed electronically with the Securities and Exchange Commission (the “Commission”)Commission), as soon as reasonably practicable after such material is electronically filed with or furnished to the Commission. Interested parties may also find reports, proxy and information statements and other information on issuers that file electronically with the Commission at the Commission’sCommission's Internet site (http://www.sec.gov).at www.sec.gov.

Sales at Martin Yale Group increased but net loss grew in 2011 and net losses could continue to grow in 2012.

Overall sales in Information Security and Print Finishing increased, but net losses further declined. The increase in lossesOperating results may be impacted by our Martin Yale Group in 2011 over 2010 is due mainly to inefficiencies in bringing new products to the market, customer pricing pressures and high organizational costs. In addition, continued weaknesschanges in the economy that influence business and consumer spending.

Operating results are directly impacted by the health of the North American and to a lesser extent, European and Asian economies. While the global officeeconomy is experiencing some level of recovery from the recent downturn, we cannot predict how robust the recovery will be or whether or not it will be sustained. If the economic recovery slows, or if the economy experiences a prolonged period of decelerating or negative growth, the Company’s results of operations may be negatively impacted. In general, the Company’s sales depend on discretionary spending by consumers. Business and financial performance may be adversely affected by current and future economic conditions, including unemployment levels, energy costs, interest rates, recession, inflation, the impact of natural disasters and terrorist activities, and other matters that influence business and consumer spending.

Fluctuation in economic conditions could prevent the Company from accurately forecasting demand for its products channelwhich could adversely affect its operating results or market share.

Fluctuation in economic conditions and the government sales channel primarilymarket instability in the United States and the United Kingdom and prolonged economic weakness in Spain and certain other European countries continue to provide challenges. Sales in Information Security and Print Finishing may not continue to increase in 2012 and could decline. Improving profitability in the Information Security and Print Finishing segment will prove to be a challenge. The Company cannot provide any assurance thatglobally makes it will be able to maintain or increase sales levels in the future.

Ifdifficult for the Company, would lose significant customers in theand suppliers to accurately forecast future product demand trends, which could cause the Company may haveto produce excess products that can increase inventory carrying costs and result in obsolete inventory. Alternatively, this forecasting difficulty could cause a shortage of products, or materials used in replacing such lost revenues.products, that could result in an inability to satisfy demand for products and a loss of market share.

The Company has several large customers and historically has derived substantial revenues from those customers. The Company needs to continue to expand its customer base to minimize the effects of the loss of any single customer in the future. If sales to one or more significant customers would be lost or materially reduced, there can be no assurance that the Company will be able to replace such revenues, which losses could have a material adverse effect on the Company’s business, results of operations and financial condition.

Markets are highly competitive which could limit the Company’s growth and the Company may not continue to compete successfully.reduce profitability.

The market for sporting goods and information security and print finishing products is highly fragmented and intensely competitive. A majority of the Company’s products are in markets that are experiencing low growth rates. Escalade competes with a variety of regional, national and international manufacturers for customers, employees, products, services and other important aspects of the business. In Sporting Goods, theThe Company has historically sold a large percentage of its sporting goods products to mass merchandisers and has increasingly attempted to expand sales to specialty retailer and dealer markets. Similarly, the Company has traditionally sold information security and print finishing products to office products retailers, specialty machine dealers and government channels. In addition to competition for sales into those distribution channels, vendors also must compete in sporting goods with large format sporting goods stores, traditional sporting goods stores and chains, warehouse clubs, discount stores and department stores, and in information security and print finishing products with office supply superstores, computer and electronics superstores, contract stationers, and others.stores. Competition from on-line retailers may also impact sales. Some of the current and potential competitors are larger than Escalade and have substantially greater financial resources that may be devoted to sourcing, promoting and selling their products, and may discount prices more heavily than the Company can afford.

If the Company is unable to predict or effectively react to changes in consumer demand, it may lose customers and sales may decline.

Success depends in part on the ability to anticipate and respond in a timely manner to changing consumer demand and preferences regarding sporting goods and information security and print finishing products.goods. Products must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to change. The Company often makes commitments to manufacture products months in advance of the proposed delivery to customers. If Escalade misjudges the market for products, sales may decline significantly. The Company may have to take significant inventory markdowns on unpopular products that are overproduced and/or miss opportunities for other products that may rise in popularity, both of which could have a negative impact on profitability. A major shift in consumer demand away from sporting goods or information security and print finishing products could also have a material adverse effect on the Company’s business, results of operations and financial condition.

The Company derives a substantial portion of its revenue from a few significant customers and loss of any of these customers could materially affect our results of operations and financial condition.

The Company has one major customer which accounted for more than ten percent of consolidated gross sales and several other large customers, none of which represent more than ten percent of consolidated gross sales, and historically has derived substantial revenues from these customers. The Company needs to continue to expand its customer base to minimize the effects of the loss of any single customer in the future. If sales to one or more of the large customers would be lost or materially reduced, there can be no assurance that the Company will be able to replace such revenues, which could have a material adverse effect on the Company's business, results of operations and financial condition.

Quarterly operating results are subject to fluctuation.

Operating results have fluctuated from quarter to quarter in the past, and the Company expects that they will continue to do so in the future. Earnings may not recover to historical levels and may fall short of either a prior fiscal period or market expectations. Factors that could cause these quarterly fluctuations include the following:international, national and local general economic and market conditions; the size and growth of the overall Sporting Goods and Information Security and Print Finishingsporting goods markets; intense competition among manufacturers, marketers, distributors and sellers of products; demographic changes; changes in consumer preferences; popularity of particular designs, categories of products and sports; seasonal demand for products; the size, timing and mix of purchases of products; fluctuations and difficulty in forecasting operating results; ability to sustain, manage or forecast growth and inventories; new product development and introduction; ability to secure and protect trademarks, patents and other intellectual property; performance and reliability of products; customer service; the loss of significant customers or suppliers; dependence on distributors; business disruptions; increased costs of freight and transportation to meet delivery deadlines; changes in business strategy or development plans; general risks associated with doing business outside the United States, including, without limitation: exchange rates, import duties, tariffs, quotas and political and economic instability; changes in government regulations; any liability and other claims asserted against the Company; ability to attract and retain qualified personnel; and other factors referenced or incorporated by reference in this Form 10-K and any other filings with the Securities and Exchange Commission.

Operating results may be impacted by changes in the economy that impact business and consumer spending.

In general, the Company’s sales depend on discretionary spending by consumers. The economic downturn experienced in both the United States and the global economy has resulted in reduced consumer demand and reduced selling price and adversely impacted sales. A continuance of this economic downturn could result in further declines in revenues and impair growth in 2012. Severely negative economic conditions could greatly impair the ability and willingness of consumers to buy products. Operating results are directly impacted by the health of the North American, European and Asian economies. Business and financial performance may be adversely affected by current and future economic conditions, including unemployment levels, energy costs, interest rates, recession, inflation, the impact of natural disasters and terrorist activities, and other matters that influence business and consumer spending.

If national and global financial markets do not improve, potential disruptions in the credit markets may adversely affect business, including the availability and cost of short-term funds for liquidity requirements and ability to meet long-term commitments, which could adversely affect results of operations, cash flows and financial condition.

If internal funds are not available from operations, the Company may be required to rely on the banking credit and equity markets to meet financial commitments and short-term liquidity needs. Disruptions in the capital and credit markets could adversely affect the Company’s ability to borrow pursuant to its Credit Agreement with JP Morgan Chase Bank, N.A. (Chase) or to borrow from other financial institutions. Access to funds under the Credit Agreement or pursuant to arrangements with other financial institutions is dependent on Chase’s or other financial institutions’ ability to meet funding commitments. Financial institutions, including Chase, may not be able to meet their funding commitments if they experience shortages of capital and liquidity or if they experience high volumes of borrowing requests from other borrowers within a short period of time. There can be no assurance that the Company would be able to replace its current Credit Agreement on favorable terms, if at all, in the event that replacement would become necessary or desirable.

Longer term disruptions in the capital and credit markets as a result of uncertainty, changing or increased regulation, reduced alternatives or failures of significant financial institutions could adversely affect access to the liquidity needed for business. Any disruption could require the Company to take measures to conserve cash until the markets stabilize or until alternative credit arrangements or other funding for our business needs can be arranged. Such measures could include deferring capital expenditures and reducing or eliminating future share repurchases, dividend payments or other discretionary uses of cash.

Current financial conditions in the United States and globally may have significant effects on customers and suppliers that would result in material adverse effects on business, operating results and stock price.

Current financial conditions in the United States and globally and concern that the worldwide economy may enter into a prolonged recessionary period may materially adversely affect customers’ access to capital or willingness to spend capital on products and/or their levels of cash liquidity with which to pay for products that they will order or have already ordered from the Company. In addition, current financial conditions may materially adversely affect suppliers’ access to capital and liquidity with which to maintain their inventories, production levels and/or product quality could cause them to raise prices, lower production levels or result in their ceasing operations. Continuing adverse economic conditions in the Company’s markets would also likely negatively impact business, which could result in: (1) reduced demand for products; (2) increased price competition for products; (3) increased risk of excess or obsolete inventories; (4) increased risk of collectability of cash from customers; (5) increased risk in potential reserves for doubtful accounts and write-offs of accounts receivable; (6) reduced revenues; and (7) higher operating costs as a percentage of revenues.

All of the foregoing potential consequences of current financial conditions are difficult to forecast and mitigate. As a consequence, operating results for a particular period are difficult to predict, and, therefore, prior results are not necessarily indicative of future results to be expected in future periods. Any of the foregoing effects could have a material adverse effect on the Company’s business, results of operations and financial condition and could adversely affect stock price.

Negative economic conditions could prevent the Company from accurately forecasting demand for its products which could adversely affect its operating results or market share.

The current negative economic conditions and market instability in the United States and globally makes it increasingly difficult for the Company, customers and suppliers to accurately forecast future product demand trends, which could cause the Company to produce excess products that can increase inventory carrying costs and result in obsolete inventory. Alternatively, this forecasting difficulty could cause a shortage of products, or materials used in products, that could result in an inability to satisfy demand for products and a loss of market share.

The Company may pursue strategic acquisitions, whichdivestitures, or investments and the failure of a strategic transaction to produce anticipated results or the inability to fully integrate an acquired company could have an adverse impact on itsthe Company’s business.

In the past, theThe Company has made acquisitions of complementary companies or businesses, which have been part of the strategic plan, and may continue to pursue acquisitions in the future from time to time. Acquisitions may result in difficulties in assimilating acquired companies, and may result in the diversion of capital and management’s attention from other business issues and opportunities. The Company may not be able to successfully integrate operations that it acquires, including personnel, financial systems, distribution, and operating procedures. If the Company fails to successfully integrate acquisitions, the Company’s business could suffer. In addition, acquisitions may result in the integrationincurrence of debt, contingent liabilities, amortization expense or write-offs of goodwill or other intangibles, any acquired business,of which could affect the Company’s financial position. The Company also has sometimes divested or discontinued certain operations, assets, and its financial results, may adversely affect operating results.products that did not perform to the Company’s expectations or no longer fit with the Company’s strategic objectives. Escalade will consider acquisitions, divestitures, and investments in the future, butone or more of which, individually or in the Company currently does not have any agreements with respectaggregate, could be material to any such acquisitions.the Company’s overall business, operations or financial position.

Growth may strain resources, which could adversely affect the Company’s business and financial performance.

Both the Sporting Goods and Information Security and Print Finishing businesses haveThe Company has grown in the past through strategic acquisitions. Growth places additional demands on management and operational systems. If the Company is not successful in continuing to support operational and financial systems, expanding the management team and increasing and effectively managing customers and suppliers, growth may result in operational inefficiencies and ineffective management of the Company’s business, which could adversely affect its business and financial performance.

The Company’s ability to operate and expand business and to respond to changing business and economic conditions will be dependent upon the availability of adequate capital.

The rate of expansion will also depend on the availability of adequate capital, which in turn will depend in large part on cash flow generated by the business and the availability of equity and debt capital. EscaladeThe Company can make no assurances that it will be able to obtain equity or debt capital on acceptable terms or at all, especially consideringall. Our current senior secured revolving credit facility contains provisions that limit our ability to incur additional indebtedness or make substantial asset sales, which might otherwise be used to finance our operations. In the current disruptionsevent of our insolvency, liquidation, dissolution or reorganization, the lenders under our senior secured revolving credit facility would be entitled to payment in the credit markets.full from our assets before distributions, if any, to our stockholders.

FailureThe Company could suffer if it fails to improve operational efficiencyattract and reduce administrative costs could have a material adverse effect on the Company’s liquidity, financial positionretain skilled management and results of operations.key personnel.

The Company’s success depends in large part on its ability to improve profit margins is largely dependent on the success of on-going initiatives to streamline infrastructure, improve operational efficiencyattract and the reduction of administrative costsretain highly qualified management executives and key personnel. Significant competition for qualified candidates exists in certain segments of the Company. Failure to continue to implement these initiatives successfully, or the failure of such initiatives to result in improved profitability, could have a material adverse effect on the Company’s liquidity, results ofbusiness lines and geographic locations. If the Company is not able to hire and retain its executives and key personnel, or if the compensation costs required to attract and retain such individuals becomes more expensive, the Company may suffer adverse consequences to its business, operations, and financial position.

condition.

The Company’s business may be adversely affected by the actions of and risks associated with third-party suppliers.

The raw materials that the Company purchases for manufacturing operations and many of the products that it sells are sourced from a wide variety of third-party suppliers. The Company cannot control the supply, design, function or cost of many of the products that are offered for sale and are dependent on the availability and pricing of key materials and products. Disruptions in the availability of raw materials used in production of these products may adversely affect sales and result in customer dissatisfaction. In addition, global sourcing of many of the products sold is an important factor in the Company’s financial performance. The ability to find qualified suppliers and to access products in a timely and efficient manner is a significant challenge, especially with respect to goods sourced outside the United States. Political instability, financial instability of suppliers, merchandise quality issues, trade restrictions, tariffs, currency exchange rates, transport capacity and costs, inflation and other factors relating to foreign trade are beyond the Company’s control.

Historically, instability in the political and economic environments of the countries in which the Company or its suppliers obtain products and raw materials has not had a material adverse effect on operations. However, the Company cannot predict the effect that future changes in economic or political conditions in such foreign countries may have on operations. In the event of disruptions or delays in supply due to economic or political conditions in foreign countries, such disruptions or delays could adversely affect results of operations unless and until alternative supply arrangements could be made. In addition, products and materials purchased from alternative sources may be of lesser quality or more expensive than the products and materials currently purchased abroad.

Deterioration in relationships with suppliers or in the financial condition of suppliers could adversely affect liquidity, results of operations and financial position.

Access to materials, parts and supplies is dependent upon close relationships with suppliers and the ability to purchase products from the principal suppliers on competitive terms. The Company does not enter into long-term supply contracts with these suppliers, and has no current plans to do so in the future. These suppliers are not required to sell to the Company and are free to change the prices and other terms. Any deterioration or change in the relationships with or in the financial condition of the Company’s significant suppliers could have an adverse impact on its ability to procure materials and parts necessary to produce products for sale and distribution. If any of the significant suppliers terminated or significantly curtailed its relationship with the Company or ceased operations, the Company would be forced to expand relationships with other suppliers, seek out new relationships with new suppliers or risk a loss in market share due to diminished product offerings and availability. Any change in one or more of these suppliers’ willingness or ability to continue to supply the Company with their products could have an adverse impact on the Company’s liquidity, results of operations and financial position.

Disruptions to our supply chain could have an adverse impact on our operations.

Many of the Company’s products are manufactured outside the United States. Those products must be transported by third parties over large geographic distances. Delays in the shipment or delivery of our products could occur due to work stoppages, port strikes, lack of availability of transportation, and other factors beyond the Company’s control. Such delays could impair our ability to timely and efficiently deliver our products, and could adversely impact our operating results.

EscaladeThe Company may be subject to product warranty claims that require the replacement or repair of the product sold. Such warranty claims could adversely affect Escalade’sthe Company’s financial position and relationships with its customers.

The Company manufactures and/or distributes a variety of products in both its Sporting Goods and Information Security and Print Finishing business segments.products. From time to time, such products may contain manufacturing defects or design flaws that are not detected prior to sale, particularly as to new product introductions or upon design changes to existing products. The failure to identify and correct manufacturing defects and product design issues prior to the sale of those products could result in product warranty claims that result in costs to replace or repair any such defective products. Because many of the Company’s products are sold to retailers for broad consumer distribution and/or to customers who buy in large quantities, the costs associated with product warranty claims could have a material adverse effect on the Company’s results of operations and financial position. Product warranty claims also could cause customer dissatisfaction that may have a material adverse effect on the Company’s reputation and on the Company’s relationships with its customers, which may result in lost or reduced sales.

| 8 |

EscaladeThe Company may be subject to product liability claimsvarious types of litigation and the Company’s insurance may not be sufficient to cover damages related to those claims.

From time to time the Company or its subsidiaries may be involved in lawsuits or other claims arising in the course of business, including those related to product liability, consumer protection, employment, intellectual property, torts and other matters, In addition, it may be subject to lawsuits relating to the design, manufacture or distribution of its products. The Company may be subject to lawsuits resulting from injuries associated with the use of sporting goods equipment that it sells and information security and print finishing products that it sells.sold prior to divesting that business. The Company may incur losses relating to these claims or the defense of these claims. There is a risk that claims or liabilities will exceed the Company’s insurance coverage. In addition, the Company may be unable to retain adequate liability insurance in the future. Further, the Company is subject to regulation by the Consumer Product Safety Commission and similar state regulatory agencies. If the Company fails to comply with government and industry safety standards, it may be subject to claims, lawsuits, fines, product recalls and adverse publicity that could have a material adverse effect on the Company’s business, results of operations and financial condition.

Intellectual property rights are valuable, and any inability to protect them could reduce the value of products.

The Company obtains patents, trademarks and copyrights for intellectual property, which represent important assets to the Company. If the Company fails to adequately protect intellectual property through patents, trademarks and copyrights, its intellectual property rights may be misappropriated by others, invalidated or challenged, and our competitors could duplicate the Company’s products or may otherwise limit any competitive design or manufacturing advantages. The Company believes that success is likely to depend upon continued innovation, technical expertise, marketing skills and customer support and services rather than on legal protection of intellectual property rights. However, the Company intends to aggressively assert its intellectual property rights when necessary.

The Company is subject to risks associated with laws and regulations related to health, safety and environmental protection.

Products, and the production and distribution of products, are subject to a variety of laws and regulations relating to health, safety and environmental protection. Laws and regulations relating to health, safety and environmental protection have been passed in several jurisdictions in which the Company operates in the United States and abroad. Although the Company does not anticipate any material adverse effects based on the nature of operations and the thrust of such laws, there is no assurance such existing laws or future laws will not have a material adverse effect on the Company’s business, results of operations and financial condition.

International operations expose the Company to the unique risks inherent in foreign operations.

The Company has operations in Mexico, Europe, S. Africa and Asia.Mexico. Foreign operations encounter risks similar to those faced by U.S. operations, as well as risks inherent in foreign operations, such as local customs and regulatory constraints, control over product quality and content, foreign trade policies, competitive conditions, foreign currency fluctuations and unstable political and economic conditions. The Company’s international operations headquartered in Germany and its business relationships in Asia further increase its exposure to these foreign operating risks, which could have an adverse impact on the Company’s international income and worldwide profitability.

The Company could be adversely affected by changes in currency exchange rates and/or the value of the United States dollar.

The Company is exposed to risks related to the effects of changes in foreign currency exchange rates and the value of the United States dollar. Changes in currency exchange rates and the value of the United States dollar can have a significant impact on earnings from international operations.earnings. While the Company carefully watches fluctuations in currency exchange rates, these types of changes can have material adverse effects on the Company’s business, results of operations and financial condition.

Failure to improve and maintain the quality of internal controls over financial reporting could materially and adversely affect the ability to provide timely and accurate financial information, which could harm the Company’s reputation and share price.

Management is responsible for establishing and maintaining adequate internal controls over financial reporting for the Company to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements in accordance with generally accepted accounting principles. Management cannot be certain that weaknesses and deficiencies in internal controls will not arise or be identified or that the Company will be able to correct and maintain adequate controls over financial processes and reporting in the future. Any failure to maintain adequate controls or to adequately implement required new or improved controls could harm operating results or cause failure to meet reporting obligations in a timely and accurate manner. Ineffective internal controls over financial reporting could also cause investors to lose confidence in reported financial information, which could adversely affect the trading price of the Company’s common stock.

Disclosure controls and procedures are designed to provide reasonable assurance of achieving their objectives. However, management, including the Chief Executive Officer and Chief Financial Officer, does not expect that disclosure controls and procedures will prevent all errors and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, have been detected.

Failure to effectively implement the Company’s global integrated information system could cause incorrect information or delays in getting information which could adversely affect the performance of the Company.

The Company converted its Enterprise Risk Planning (ERP) system from the Oracle E-Business suite to Epicor at its Martin Yale North America location at the beginning of 2011 and at its Escalade Sports North Carolina location at the beginning of 2012. The Company is in the process of converting its Enterprise Risk Planning (ERP) systems from legacy system in Germanysystems to Epicor during the second quarter of 2012.Epicor. Implementation has been completed for Raleigh, North Carolina, and Rosarito, Mexico locations. The Company intends to complete the conversion of its remaining sites over the next two years. There can be no assurance the Company will have the necessary funds or the staff to fully avail itself of the control features inherent in the system design. Without such utility, the Company management is faced with cumbersomelegacy systems and time consuming efforts to manually consolidate its financial information.

Problems with the Company’s information system software or hardware could disrupt operations and negatively impact financial results and materially adversely affect the Company’s business operations

The Company relies on a suite of applications and third party software to receive and process customer orders and for the core of its manufacturing, distribution, and accounting systems. These systems, if not functioning properly, could disrupt its operations, including the Company’s ability to receive and ship orders and to process financial information or engage in similar normal business activities. Any material disruption, malfunction or other similar problems in or with these systems could negatively impact our financial results and materially adversely affect our business operations.

The preparation of the Company’s financial statements requires the use of estimates that may vary from actual results.

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States requires management to make significant estimates that may affect financial statements. Due to the inherent nature of making estimates, actual results may vary substantially from such estimates, which could materially adversely affect the Company’s business, results of operations and financial condition. For more information on the Company’s critical accounting estimates, please see the Critical Accounting Estimates section of this Form 10-K.

| 10 |

Changes in accounting standards could impact reported earnings and financial condition.

The accounting standard setters, including the Financial Accounting Standards Board the International Accounting Standards Board,and the Securities and Exchange Commission, and the Public Company Accounting Oversight Board, periodically change the financial accounting and reporting standards that govern the preparation of the Company’s consolidated financial statements. These changes can be hard to predict and apply and can materially affect how the Company records and reports its financial condition and results of operations. In some cases, the Company could be required to apply a new or revised standard retrospectively, which may result in the restatement of prior period financial statements.

EffectiveThe Company’s effective tax rate may fluctuate.

The Company is a multi-national, multi-channel provider of sporting goods and, until October 2014, was a multi-national, multi-channel provider of information security and print finishing products. As a result, the Company’s effective tax rate is derived from a combination of applicable tax rates in the various countries, states and other jurisdictions in which the Company operates. The effective tax rate may be lower or higher than its tax rates have been in the past due to numerous factors, including the sources of income, any agreement with taxing authorities in various jurisdictions, the tax filing positions taken in various jurisdictions and changes in the political environment in the jurisdictions in which the Company operates. The Company bases estimates of an effective tax rate at any given point in time upon a calculated mix of the tax rates applicable to the Company and to estimates of the amount of business likely to be done in any given jurisdiction. The loss of one or more agreements with taxing jurisdictions, a change in the mix of business from year to year and from country to country, changes in rules related to accounting for income taxes, changes in tax laws and any of the multiple jurisdictions in which the Company operates, or adverse outcomes from tax audits that the Company may be subject to in any of the jurisdictions in which the Company operates, could result in an unfavorable change in the effective tax rate which could have an adverse effect on the Company’s business and results of operations.

The market price of Escalade’sthe Company’s common stock is likely to be highly volatile as the stock market in general can be highly volatile.

The public trading of Escalade’sthe Company’s common stock is based on many factors which could cause fluctuation in the Company’s stock price. These factors may include, among other things:

| · | General economic and market conditions; |

| · | Actual or anticipated variations in quarterly operating results; |

| · |

| · | Relatively low market capitalization resulting in low trading volume in the Company’s stock; |

| · | If securities analysts provide coverage, our inability to meet or exceed securities |

| · | Conditions or trends in the Company’s industries; |

| · | Changes in the market valuations of other companies in the Company’s industries; |

| · | Announcements by the Company or the Company’s competitors of significant acquisitions, strategic partnerships, divestitures, joint ventures or other strategic initiatives; |

| · | Capital commitments; |

| · | Additions or departures of key personnel; |

| · | Sales and repurchases of the Company’s common stock; and |

| · | The ability to maintain listing of the Company’s common stock on the NASDAQ Global Market. |

Many of these factors are beyond the Company’s control. These factors may cause the market price of the Company’s common stock to decline, regardless of operating performance.

| 11 |

Information securityIf we are unable to pay quarterly dividends at intended levels, our reputation and stock price may be compromised.harmed.

Our quarterly cash dividend is currently $0.10 per common share. The dividend program requires the use of a portion of our cash flow. Our ability to pay dividends will depend on our ability to generate sufficient cash flows from operations in the future. This ability may be subject to certain economic, financial, competitive and other factors that are beyond our control. Our Board of Directors (Board) may, at its discretion, increase or decrease the intended level of dividends or entirely discontinue the payment of dividends at any time. Any failure to pay dividends after we have announced our intention to do so may negatively impact our reputation, investor confidence in us and negatively impact our stock price.

Unauthorized disclosure of sensitive or confidential customer information could harm the Company’s business and its standing with its customers.

Through sales and marketing activities, the Company collects and stores certain information that customers provide to purchase products or services or otherwise communicate and interact with the Company. Despite instituted safeguards for the protection of such information, the Company cannot be certain that all of its systems are entirely free from vulnerability to attack. Computer hackers may attempt to penetrate the Company’s network security and, if successful, misappropriate confidential customer or business information. In addition, an employee, a contractor or other third party with whom the Company does business may attempt to circumvent the Company’s security measures in order to obtain such information or inadvertently cause a breach involving such information. Loss of customer or business information could disrupt operations, damage the Company’s reputation, and expose the Company to claims from customers, financial institutions, payment card associations and other persons, any of which could have an adverse effect on the Company’s business, results of operations and financial condition. In addition, compliance with tougher privacy and information security laws and standards may result in significant expense due to increased investment in technology and the development of new operational processes.

Terrorist attacks, or acts of war or natural disaster may seriously harm the Company’s business.

Among the chief uncertainties facing the nation and the world and, as a result, the business is the instability and conflict in the Middle East. Obviously, no one can predict with certainty what the overall economic impact will be as a result of these circumstances. Terrorist attacks may cause damage or disruption to the Company, employees, facilities and customers, which could significantly impact net sales, costs and expenses and financial condition. The potential for future terrorist attacks, the national and international responses to terrorist attacks, and other acts of war and hostility may cause greater uncertainty and cause business to suffer in ways the Company currently cannot predict.

In addition, any natural disaster or other serious disruption to one of the Company’s manufacturing or distribution sights due to fire, tornado, earthquake or any other causes could damage a material portion of inventory or impair our ability to provide product to our customers and could negatively affect our sales and profitability.

These risks are not exhaustive.

Other sections of this Form 10-K may include additional factors which could adversely impact the Company’s business and financial performance. Moreover, the Company operates in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for management to predict all risk factors, nor can the Company assess the impact of all factors on business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results.

ITEM 1B—UNRESOLVED STAFF COMMENTS

None.

| 12 |

At December 31, 2011,27, 2014, the Company owned or operated from the following locations:

| Location | Square Footage | Owned or Leased | Use | |||||

| Evansville, Indiana, USA | 380,200 | Owned | Distribution; sales and marketing; administration | |||||

| Rosarito, Mexico | 174,700 | Owned | Manufacturing and distribution | |||||

| Olney, Illinois, USA | 108,500 | Leased | Manufacturing and distribution | |||||

| Gainesville, Florida, USA | 154,200 | Owned | Manufacturing and distribution | |||||

| Raleigh, N. Carolina, USA | 88,800 | Leased | Manufacturing and distribution | |||||

| Jacksonville, Florida, USA | 31,800 | |||||||

| Leased | Distribution; sales and marketing | |||||||

| 1,130 | Leased | Sales and | ||||||

| 141,000 | Owned | |||||||

At the end of 2010, the Company had one idle facility in Reynosa, Mexico. The sale of the Reynosa facility was completed in 2011. The Company believes that its remaining facilities are in satisfactory and suitable condition for their respective operations. The Company also believes that it is in material compliance with all applicable environmental regulations and is not subject to any proceeding by any federal, state or local authorities regarding such matters. The Company provides regular maintenance and service on its plants and machinery as required.

The Company is involved in litigation arising in the normal course of its business, but the Company does not believe that the disposition or ultimate resolution of such claims or lawsuits will have a material adverse affect on the business or financial condition of the Company.

The Company is not aware of any probable or levied penalties against the Company relating to the American Jobs Creation Act.

ITEM 4—MINE SAFETY DISCLOSURES

Not applicable.

| 13 |

ITEM 5—MARKET FOR THE REGISTRANT’SREGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company’sCompany's common stock is traded under the symbol “ESCA” on the NASDAQ Global Market. The following table sets forth, for the calendar periods indicated, the high and low sales prices of the Common Stock as reported by the NASDAQ Global Market:

| Prices | High | Low | ||||||

| 2011 | ||||||||

| Fourth quarter ended December 31, 2011 | $ | 5.60 | $ | 4.26 | ||||

| Third quarter ended October 1, 2011 | 6.22 | 4.30 | ||||||

| Second quarter ended July 9, 2011 | 6.43 | 5.00 | ||||||

| First quarter ended March 19, 2011 | 7.10 | 5.30 | ||||||

| 2010 | ||||||||

| Fourth quarter ended December 25, 2010 | $ | 6.65 | $ | 4.27 | ||||

| Third quarter ended October 2, 2010 | 5.80 | 4.14 | ||||||

| Second quarter ended July 10, 2010 | 5.52 | 2.46 | ||||||

| First quarter ended March 20, 2010 | 3.00 | 2.21 | ||||||

| 2009 | ||||||||

| Fourth quarter ended December 26, 2009 | $ | 3.07 | $ | 1.96 | ||||

| Third quarter ended October 3, 2009 | 3.44 | 0.72 | ||||||

| Second quarter ended July 11, 2009 | 1.48 | 0.43 | ||||||

| First quarter ended March 21, 2009 | 1.15 | 0.30 | ||||||

| Prices | High | Low | ||||||

| 2014 | ||||||||

| Fourth quarter ended December 27, 2014 | $ | 14.47 | $ | 11.18 | ||||

| Third quarter ended October 4, 2014 | 16.77 | 11.78 | ||||||

| Second quarter ended July 12, 2014 | 16.83 | 12.58 | ||||||

| First quarter ended March 22, 2014 | 12.77 | 10.61 | ||||||

| 2013 | ||||||||

| Fourth quarter ended December 28, 2013 | $ | 12.41 | $ | 8.18 | ||||

| Third quarter ended October 5, 2013 | 8.70 | 6.32 | ||||||

| Second quarter ended July 13, 2013 | 6.48 | 5.72 | ||||||

| First quarter ended March 23, 2013 | 6.20 | 5.21 | ||||||

| 2012 | ||||||||

| Fourth quarter ended December 29, 2012 | $ | 5.54 | $ | 4.67 | ||||

| Third quarter ended October 6, 2012 | 6.09 | 5.05 | ||||||

| Second quarter ended July 14, 2012 | 6.10 | 5.15 | ||||||

| First quarter ended March 24, 2012 | 6.06 | 4.31 | ||||||

The closing market price on February 6, 201211, 2015 was $4.88$15.79 per share.

DependingDuring 2013, the Company’s Board of Directors adopted a dividend policy under which the Company intends to pay quarterly cash dividends on profitability and cash flows from operations,its common stock. At the August 2014 meeting of the Board of Directors, issues dividends. Based on the Company’s 2010 performance,Company established the Board declared a dividend in 2010 ofannual rate to be $0.40 per share, or $0.10 per share. As a result of the 2011 performance, the Board declared a dividend in August 2011 of $0.25 per share and in November 2011 of $0.07 per share.quarterly. Dividends issued/declared during 20102013 and 20112014 are as follows:

| Record Date | Payment Date | Amount per Common Share | ||||

| March 14, 2013 | March 20, 2013 | $ | 0.08 | |||

| June 13, 2013 | June 20, 2013 | $ | 0.08 | |||

| September 13, 2013 | September 20, 2013 | $ | 0.09 | |||

| December 13, 2013 | December 20, 2013 | $ | 0.09 | |||

| March 13, 2014 | March 20, 2014 | $ | 0.09 | |||

| June 12, 2014 | June 19, 2014 | $ | 0.09 | |||

| September 14, 2014 | September 21, 2014 | $ | 0.10 | |||

| December 12, 2014 | December 19, 2014 | $ | 0.10 | |||

There were approximately 186158 holders of record of the Company’sCompany's Common Stock at February 9, 2012.11, 2015. The approximate number of stockholders, including those held by depository companies for certain beneficial owners, was 1,250.1,931.

| 14 |

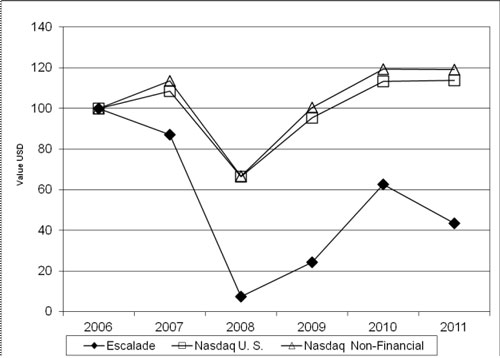

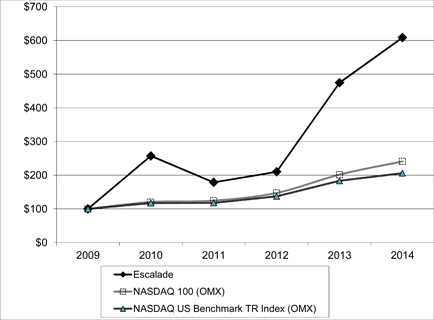

SHAREHOLDER RETURN PERFORMANCE GRAPH

Set forth below is a line graph comparing the yearly percentage change in the cumulative total shareholder return on the Company’s common stock with that of the cumulative total return on the NASDAQ US Stock Market Index100 and the NASDAQ Non-Financial StocksUS Benchmark TR Index for the five year period ended December 31, 2011.2014. The following information is based on an investment of $100, on December 31, 2006,2009, in the Company’s common stock, the NASDAQ US Stock Market Index100 and the NASDAQ Non-Financial StocksUS Benchmark TR Index, with dividends reinvested.

COMPARISON OF FIVE YEAR CUMULATIVE TOTAL RETURN

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||||||

| Escalade Common Stock | 100 | 87 | 7 | 24 | 63 | 43 | ||||||||||||||||||

| NASDAQ US Stock Index | 100 | 108 | 66 | 95 | 113 | 114 | ||||||||||||||||||

| NASDAQ Non-Financial Stock Index | 100 | 113 | 67 | 101 | 119 | 119 | ||||||||||||||||||

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||||||||

| Escalade Common Stock | 100 | 257 | 179 | 210 | 475 | 608 | ||||||||||||||||||

| NASDAQ 100 (OMX) | 100 | 120 | 125 | 147 | 202 | 241 | ||||||||||||||||||

| NASDAQ US Benchmark TR Index (OMX) | 100 | 118 | 118 | 137 | 183 | 206 | ||||||||||||||||||

The above performance graph does not constitute soliciting material and should not be deemed filed or incorporated by reference into any other Company filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent the Company specifically incorporates the performance graph by reference therein.

| 15 |

ISSUER PURCHASES OF EQUITY SECURITIES

| Period | (a) Total Number of Shares (or Units) Purchased | (b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs |

| Share purchases prior to 10/01/2011 under the current repurchase program. | 982,916 | $8.84 | 982,916 | $ 2,273,939 |

Fourth quarter purchases: | ||||

| 10/02/2011 – 10/29/2011 | None | None | None | No Change |

| 10/30/2011 – 11/26/2011 | None | None | None | No Change |

| 11/27/2011 – 12/31/2011 | None | None | None | No Change |

| Total share purchases under the current program | 982,916 | $8.84 | 982,916 | $2,273,939 |

| Period | (a) Total Number of Shares (or Units) Purchased | (b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

| Share purchases prior to 10/4/2014 under the current repurchase program. | 982,916 | $ | 8.84 | 982,916 | $ | 2,273,939 | ||||||||||

| Fourth quarter purchases: | ||||||||||||||||

| 10/5/2014 – 11/01/2014 | None | None | None | No Change | ||||||||||||

| 11/2/2014 – 11/29/2014 | None | None | None | No Change | ||||||||||||

| 11/30/2014 – 12/27/2014 | None | None | None | No Change | ||||||||||||

| Total share purchases under the current program | 982,916 | $ | 8.84 | 982,916 | $ | 2,273,939 | ||||||||||

The Company has one stock repurchase program which was established in February 2003 by the Board of Directors and which initially authorized management to expend up to $3,000,000 to repurchase shares on the open market as well as in private negotiated transactions. In each of February 2005 and 2006, August 2007 and February 2008 the Board of Directors increased the remaining balance on this plan to its original level of $3,000,000. The repurchase plan has no termination date and there have been no share repurchases that were not part of a publicly announced program.

| 16 |

ITEM 6—SELECTED FINANCIAL DATA

(In thousands, except per share data)

| At and For Years Ended | December 31, 2011 | December 25, 2010 | December 26, 2009 | December 27, 2008 | December 29, 2007 | December 27, 2014 | December 28, 2013 | December 29, 2012 | December 31, 2011 | December 25, 2010 | ||||||||||||||||||||||||||||||

| Income Statement Data | ||||||||||||||||||||||||||||||||||||||||

| Net revenue | ||||||||||||||||||||||||||||||||||||||||

| Sporting Goods | $ | 96,971 | $ | 85,815 | $ | 76,807 | $ | 98,039 | $ | 129,788 | $ | 137,975 | $ | 132,991 | $ | 112,599 | $ | 96,971 | $ | 85,815 | ||||||||||||||||||||

| Information Security and Print Finishing | 37,279 | 34,841 | 39,192 | 50,647 | 55,788 | |||||||||||||||||||||||||||||||||||

| Discontinued Operations | 20,865 | 30,686 | 34,990 | 37,279 | 34,841 | |||||||||||||||||||||||||||||||||||

| Total net sales | 134,250 | 120,656 | 115,999 | 148,686 | 185,576 | 158,840 | 163,677 | 147,589 | 134,250 | 120,656 | ||||||||||||||||||||||||||||||

| Net income (loss) | 4,441 | 6,059 | 1,657 | (7,496 | ) | 9,255 | 11,817 | 9,805 | (4,930 | ) | 4,441 | 6,059 | ||||||||||||||||||||||||||||

| Weighted-average shares | 12,849 | 12,726 | 12,632 | 12,684 | 12,901 | 13,853 | 13,506 | 13,244 | 12,849 | 12,726 | ||||||||||||||||||||||||||||||

| Per Share Data | ||||||||||||||||||||||||||||||||||||||||

| Basic earnings (loss) per share | $ | 0.35 | $ | 0.48 | $ | 0.13 | $ | (0.59 | ) | $ | 0.72 | $ | 0.85 | $ | 0.73 | $ | (0.37 | ) | $ | 0.35 | $ | 0.48 | ||||||||||||||||||

| Cash dividends | $ | 0.32 | $ | 0.10 | $ | — | $ | 0.25 | $ | 0.22 | $ | 0.38 | $ | 0.34 | $ | 0.31 | $ | 0.32 | $ | 0.10 | ||||||||||||||||||||

| Balance Sheet Data | ||||||||||||||||||||||||||||||||||||||||

| Working capital | 29,496 | 24,132 | 9,688 | 4,842 | 31,442 | 37,105 | 37,537 | 32,656 | 29,496 | 24,132 | ||||||||||||||||||||||||||||||

| Total assets | 130,115 | 127,553 | 127,238 | 147,701 | 152,016 | 127,881 | 141,974 | 125,740 | 130,115 | 127,553 | ||||||||||||||||||||||||||||||

| Short-term bank debt | 16,947 | 11,407 | 27,644 | 46,525 | 13,033 | |||||||||||||||||||||||||||||||||||

| Long-term bank debt | 5,000 | 7,500 | — | — | 19,135 | |||||||||||||||||||||||||||||||||||

| Total stockholders’ equity | 87,565 | 87,030 | 82,764 | 78,790 | 91,742 | |||||||||||||||||||||||||||||||||||

| Short-term debt | 17,786 | 23,263 | 19,070 | 16,947 | 11,407 | |||||||||||||||||||||||||||||||||||

| Long-term debt | 3,360 | 4,946 | 3,500 | 5,000 | 7,500 | |||||||||||||||||||||||||||||||||||

| Total stockholders' equity | 89,779 | 87,955 | 80,457 | 87,565 | 87,030 | |||||||||||||||||||||||||||||||||||

Fiscal year 2014 was positively impacted by increased sales in the Sporting Goods segment. Net income was negatively impacted by the divestiture of the Information Security and Print Finishing segment of $9.6 million partially off-set by a tax benefit of $6.1 million.

Fiscal year 2013 was positively impacted by increased sales in the Sporting Goods segment, as well as improved margins resulting from higher sales volumes.

Fiscal year 2012 was positively impacted by increased sales in the Sporting Goods segment. Net income was negatively impacted by goodwill and intangible asset impairment in Martin Yale Group, which reduced net income by $13.4 million.

Fiscal year 2011 was positively impacted by increased sales in the Sporting Goods and Information Security and Print Finishing segments. Net income was negatively impacted by the accelerated write-off of the Oracle ERP system, which reduced net income by $2.7 million.

Fiscal year 2010 was positively impacted by increased sales in the Sporting Goods segment, as well as continued efforts at cost reduction, and improved margins resulting from higher sales volumes.

Fiscal year 2009 was positively impacted by significant cost reductions and consolidation of certain manufacturing and distributions facilities.

Fiscal year 2008 was negatively impacted by loss of sales to Sears, a major sporting goods retailer, impairment of certain long-lived assets and a general economic downturn.

Fiscal year 2007 was positively impacted by the sale of rights to license potential future intellectual property.

ITEM 7—MANAGEMENT’SMANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following section should be read in conjunction with Item 1: Business; Item 1A: Risk Factors; Item 6: Selected Financial Data; and Item 8: Financial Statements and Supplementary Data.

Forward-Looking Statements

This report contains forward-looking statements relating to present or future trends or factors that are subject to risks and uncertainties. These risks include, but are not limited to, the impact of competitive products and pricing, product demand and market acceptance, new product development, Escalade’s ability to achieve its business objectives, especially with respect to its Sporting Goods business on which it has chosen to focus, Escalade’s ability to successfully achieve the anticipated results of strategic transactions, including the integration of the operations of acquired assets and businesses and the divestiture of its Information Security and Print Finishing segment, the continuation and development of key customer and supplier relationships, disruptions or delays in our supply chain, Escalade’s ability to control costs, general economic conditions, fluctuation in operating results, changes in foreign currency exchange rates, changes in the securities market, Escalade’s ability to obtain financing and to maintain compliance with the terms of such financing and other risks detailed from time to time in Escalade’s filings with the Securities and Exchange Commission. Escalade’s future financial performance could differ materially from the expectations of management contained herein. Escalade undertakes no obligation to release revisions to these forward-looking statements after the date of this report.

Overview

Escalade, Incorporated (“Escalade”(Escalade, the Company, we, us or “Company”) manufacturesour) has historically manufactured and distributesdistributed products for two industries: Sporting GoodsGoods; and Information Security and Print Finishing. Sporting Goods has expandedOn June 30, 2014, the Company announced the sale of its product offerings to include team training products.Print Finishing business. On October 1, 2014, the Company announced the sale of its Information Security business. The divestiture of these two divisions accomplishes the Company’s complete exit from the Information Security and Print Finishinghas increasingly focused its strategy on expanding segment.

Due to the securityplanned exit from the Information Security and Print Finishing segment, effective as of its second quarter ended July 12, 2014, the Company began reporting results of its Information Security and Print Finishing business as discontinued operations, which are excluded from the results of continuing operations. Under terms of the final agreement of the Information Security business divestiture, the Company contributed to assistits international Information Security operations, all claims related to intercompany debt of this operation prior to the divestiture. The Company also assumed the foreign tax liability related to this gain. The Company was able to utilize previously reserved net operating loss carry-forwards to offset the majority of this tax liability.

As a result of the divestiture of the Information Security and Print Finishing segment, the Company incurred a loss on disposal of assets of $9.6 million, income from reclassification of accumulated other comprehensive income from foreign currency translation adjustments of $2.6 million and a tax benefit of $6.1 million. For more information relating to the Information Security and Print Finishing segment, see Note 11 – Discontinued Operations, and Note 14 – Segment Information, to the financial statements included under Item 1 of this Form 10-K.

The Company is solely focused on growing its Sporting Goods segment through organic growth of existing categories, strategic acquisitions, and new product development now that the businesses comprising the Information Security and governments with their high security needsPrint Finishing segment have been divested. The Sporting Goods segment competes in a variety of categories including basketball goals, archery, indoor and outdoor game recreation and fitness products. Strong brands and on-going investment in product development provide a solid foundation for handling sensitivebuilding customer employeeloyalty and business documents and information, in addition to Martin Yale’s traditional product offerings.continued growth.

Within these industriesthe sporting goods industry, the Company has successfully built a robust market presence in several niche markets. This strategy is heavily dependent on expanding theour customer base, barriers to entry, brand recognition andstrong brands, excellent customer service.service and a commitment to innovation. A key strategic advantage is the Company’s established relationships with major customers that allow the Company to bring new products to market in a cost effective manner while maintaining a diversified product line and wide customer base.portfolio of products to meet the demands of consumers. In addition to strategic customer relations, the Company has substantial manufacturing and import experience that enable it to be a low cost supplier. Concentrated focus on the sporting goods industry will allow the Company to leverage its strength in these markets.

A majority of the Company’sCompany's products are in markets that are currently experiencing low growth rates. Where the Company enjoys a commanding market position, such as table tennis tables, in the Sporting Goods segment and paper folding machines in the Information Security and Print Finishing segment, revenue growth is expected to be roughly equal to general growth/decline in the economy. However, in markets that are fragmented and wheremacro-economic consumer trends.

To enhance growth opportunities, the Company is not the dominant leader, such as archery in the Sporting Goods segmenthas focused on promoting new product innovation and data security shredders in the Information Securitydevelopment and Print Finishing segment,brand marketing. In addition, the Company anticipates growth. To enhance internal growth, the Company has embarked on a strategy of acquiring companies or product lines that complement or expand the Company’sCompany's existing product lines.lines or provide expansion into new or emerging categories in sporting goods. A key objective is the acquisition of product lines with barriers to entry that the Company can take to market through its established distribution channels or through new market channels. Significant synergies are achieved through assimilation of acquired product lines into the existing companyCompany structure. The Company also sometimes divests or discontinues certain operations, assets, and products that do not perform to the Company's expectations or no longer fit with the Company's strategic objectives.

The Company’s decision to exit the Information Security and Print Finishing segment was influenced by low performance in this segment and lack of strategic fit. Management believes it can better achieve earnings growth through a more concentrated focus within the sporting goods equipment industry, including the traditional sports and emerging outdoor categories.

Management believes that key indicators in measuring the success of this strategythese strategies are revenue growth, earnings growth, new product introductions, and the expansion of channels of distribution. The following table sets forth the annual percentage change in revenues and net income (loss) over the past three years:

| 2011 | 2010 | 2009 | 2014 | 2013 | 2012 | |||||||||||||||||||

| Net revenue | ||||||||||||||||||||||||

| Sporting Goods | 13.0 | % | 11.7 | % | -21.7 | % | 3.7 | % | 18.1 | % | 16.1 | % | ||||||||||||

| Information Security and Print Finishing | 7.0 | % | -11.1 | % | -22.6 | % | ||||||||||||||||||

| Discontinued Operations | (32.0 | )% | (12.3 | )% | (6.1 | )% | ||||||||||||||||||

| Total | 11.3 | % | 4.0 | % | -22.0 | % | (3.0 | )% | 10.9 | % | 9.9 | % | ||||||||||||

| Net income | -26.7 | % | 265.6 | % | 122.1 | % | ||||||||||||||||||

| Net income (loss) | ||||||||||||||||||||||||