UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 20022003

Commission File Number 0-753

PENN VIRGINIA CORPORATION

Incorporated in VIRGINIA | I.R.S. Employer Identification Number 23-1184320 |

OneThree Radnor Corporate Center, Suite 200230

100 Matsonford Road

Radnor, PA 19087

Registrant’s telephone number, including area code: (610) 687-8900

|

| |

|

|

Securities registered pursuant to section 12(b) of the Act:

None

Securities Registered pursuant to Section 12(g) of the Act:

Title of Each Class | Name of Exchange on which registered | |

Common Stock, $6.25 Par Value | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x¨

Indicate by check mark whether registrant is an accelerated filer (as defined in Rule 12b-2 of the Act). Yes x No ¨

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $348,612,796.$386,346,400.

As of February 27, 2003, 8,947,418March 4, 2004, 9,114,277 shares of common stock of the registrant were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Part Into Which Incorporated | ||

(1) Proxy Statement for Annual Shareholders Meeting on May | Part |

Penn Virginia Corporation and SubsidiariesPENN VIRGINIA CORPORATION AND SUBSIDIARIES

Part I | ||||

1. | 3 | |||

2. | 14 | |||

3. | 18 | |||

4. | 18 | |||

Part II | ||||

5. | Market for the Registrant’s Common Stock and Related Shareholder Matters | 19 | ||

6. | 20 | |||

7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 | ||

8. | 41 | |||

9. | Changes In and Disagreements with Accountants on Accounting and Financial Disclosure | 73 | ||

Part III | ||||

10. | 73 | |||

11. | 73 | |||

12. | Security Ownership of Certain Beneficial Owners and Management | 73 | ||

13. | 73 | |||

14. | 73 | |||

Part IV | ||||

15. | Exhibits, Financial Statement Schedules, and Reports on Form 8-K | 74 |

Page 2

Part 1PART I

ITEM 1 –BUSINESSItem 1—Business

General

Penn Virginia Corporation (“Penn Virginia” or the “Company”) is a Virginia corporation founded in 1882. We are engaged in the exploration, development and production of crude oil and natural gas primarily in the eastern and Gulf Coast onshore areas of the United States. We also collect royalties on various oil and gas properties in which we own a mineral fee interest. At December 31, 2002,2003, we had proved reserves of approximately 5.46.6 million barrels of oil and condensate and 241283 billion cubic feet (Bcf)(“Bcf”) of natural gas, or 273323 billion cubic feet equivalent (“Bcfe”).

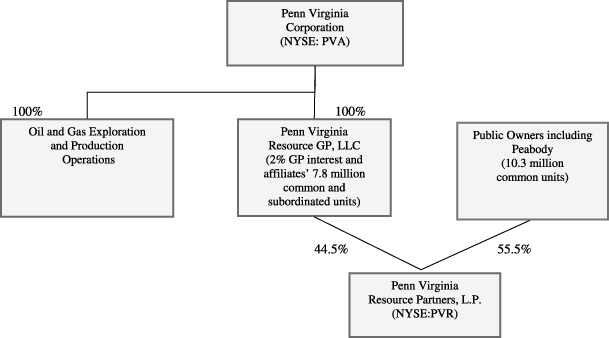

Until October 30, 2001, we also engaged directly in the leasing and management of coal properties in the Centralcentral Appalachian region of the United States. In September 2001, we transferred our coal properties and related assets and liabilities to Penn Virginia Resource Partners, L.P. (the “Partnership” or “PVR”), a newly formed Delaware limited partnership. On October 30, 2001, the Partnership completed its initial public offering (“IPO”) of approximately 7.5 million common units at $21.00 per unit, which are traded on the New York Stock Exchange under the symbol PVR. At December 31, 2002,2003, the Partnership owned approximately 615588 million tons of proven and probable coal reserves including approximately 120 million tons of such reserves that were acquired in December 2002 related to a strategic alliance with Peabody Energy Corporation (“Peabody”). The Partnership’s coal reserves are located on 241,000 acres in Virginia, West Virginia, New Mexico and eastern Kentucky. The Partnership does not operate any mines, but has leased its reserves under 5153 leases to 2829 different operators who mine coal at 6154 mines in exchange for royalty payments to PVR. Lessees other than those which are affiliates of Peabody (the “Peabody Lessees”) are generally required to make royalty payments to the Partnership based on the amount of coal they produce from the Partnership’s properties and the price at which they sell the coal, subject to fixed minimum royalty rates per ton. The Peabody Lessees are required to make payments based on fixed royalty rates which escalate annually. In managing its properties, PVR actively works with its lessees to develop efficient methods to exploit reserves and to maximize production from properties. Additionally, the Partnership provides fee-based coal preparation and transportation facilities to some of its lessees to generate coal service revenues. The Partnership also generates revenues from the sale of standing timber sales from timber owned.on its properties. The Partnership owned approximately 168166 million board feet (“MMbf”) of timber at December 31, 2002.2003.

Our wholly owned subsidiary, Penn Virginia Resource GP, LLC, a Delaware limited liability company, serves as general partner of the Partnership. As of December 31, 2002,2003, we owned approximately 45 percent of the Partnership, consisting of a two percent general partner interest 42and 43 percent subordinated units, and one percent common units.limited partner interest. As part of our ownership of PVR’s general partner, we also own the rights, referred to as Incentive Distribution Rights,“incentive distribution rights”, to receive an increasing percentage of the Partnership’s quarterly distributiondistributions of available cash from operating surplus after certain levels of cash distributions have been achieved. See Item 1 – Business – 1—Business—Corporate and Other for more information on Incentive Distribution Rights.incentive distribution rights.

Financial Information

We operate in two primary business segments. We are in the crude oil and natural gas exploration and production business and, through our interests in PVR, we are in the coal royalty and land management business. For financial statement purposes, the assets, liabilities and earnings of PVR are included in our consolidated financial statements, with the public unitholders’ ownership interest reflected as a minority interest. See Note 19 (Segment Information)20. Segment Information of the Notes to the Consolidated Financial Statements for financial information concerning our business segments.

Oil and Gas Operations

General

Our oil and gas properties are located primarily in the eastern and onshore Gulf Coast onshore areas of the United States. At December 31, 2002,2003, we had 273323 Bcfe of proved reserves, (88of which 88 percent was natural gas) including 226 Bcfe held through various working interests and 47 Bcfe held by royalty interests.gas. Seventy-eight percent or those proved reserves were proved developed reserves. During 2002, 3492003, 625 thousand barrels of oil and condensate and 18.720.1 Bcf of natural gas, net to our interest, were produced from continuing operations compared with 164349 thousand barrels and 13.118.7 Bcf in 2001. In addition, there were approximately 18 thousand barrels of oil and condensate and 16 million cubic feet (“MMcf”) of natural gas produced from properties which were sold in 2002 and reflected as discontinued operations.2002. We received average prices of $23.63$26.91 and $22.94

1

$23.63 per barrel for crude oil and $5.31 and $3.35 and $4.06 per thousand cubic feet (“Mcf”) for crude oil and natural gas sales in 20022003 and 2001,2002, respectively. We also drilled 96

Page 3

180 gross (65.5(132.1 net) wells in 2002,2003, of which 90162 gross (60.9(118.0 net) wells were development and 618 gross (4.6(14.1 net) wells were exploratory. A total of 3 gross (1.6(2.9 net) exploratory wells were not successful.successful and 10 gross (10 net) exploratory wells were under evaluation at December 31, 2003.

Transportation

The majority of our natural gas production is transported to market primarily on threefive major pipeline or transmission systems. NiSource Inc., Dominion Transmission, Inc., Duke Energy Inc., Nisource, Inc.Corporation, Exxon Mobil Corporation and DominionCrosstex Energy Inc.Services LTD transported 3921 percent, 2420 percent, 19 percent, 12 percent and 208 percent, respectively, of our 20022003 natural gas production. The remainder was divided among several pipeline companies in Texas, Louisiana and West Virginia. In almost all cases, our natural gas is sold at the interconnects with the transmission pipelines. For additional information, see Item 1 – 1—Risks Associated with Business Activities – Activities—Oil and Gas – Gas—Transportation.

Marketing and Hedging

We generally sell our natural gas using the spot market and short-term fixed price physical contracts. For the year ended December 31, 2003, three customers of the oil and gas segment, Dominion Transmission, Inc., El Paso Corporation and Duke Energy Corporation accounted for approximately 19 percent, 13 percent and 12 percent, respectively, of our total revenues. From time to time, we enter into commodity derivative contracts or fixed price physical contracts to mitigate the risk associated with the volatility of natural gas prices. Recently, we have utilized swaps and costless collars in connection with our hedging activities. Gains and losses from hedging activities are included in revenues when the hedged production is sold. We recognized a loss of $1.0$6.1 million on settled hedging activities in 2003, a loss of $1.1 million in 2002 and a gain of $1.9 million in 2001, and no gain or loss in 2000.2001. In 2002,2003, we hedged approximately 4445 percent of our natural gas base production at an average NYMEX Henry Hub floor price of $2.98$3.64 per MMbtu and a ceiling price of $3.53$5.61 per MMbtu.MMbtu for costless collars, and an average $4.70 per MMbtu for swaps. For crude oil, we hedged approximately 7626 percent of our 20022003 crude oil production at an average floor price or $21.31of $23.00 per barrel and a ceiling price of $25.72$28.75 per barrel.barrel for costless collars, and an average $26.82 per barrel for swaps. See Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations –7A.— Quantitative and Qualitative Disclosures about Market Risk for information about our price risk management positions for 2003, 2004 and the first quarter of 2005.

Coalbed Methane Drilling Venture

In August 2002, we entered into an agreement with CDX Gas, LLC (“CDX”), a private owner of proprietary horizontal drilling technology, to explore for and develop coalbed methane (“CBM”) in 16,000 square miles of property located in Central Appalachia as well as in the Devonian Shale formation. Our agreement with CDX is generally for five years and provides that we and CDX will have a 60 percent and 40 percent working interest, respectively, in future CBM projects conducted on property owned by us and subject to the agreement. On future projects conducted on property not owned by us, we and CDX will generally each have a 50 percent working interest.

Coal Royalty and Land Management Operations

OverviewGeneral

At December 31, 2002,2003, the Partnership ownedproperties contained approximately 588 million tons of proven and leased approximatelyprobable coal reserves located on 241,000 acres in Virginia, West Virginia, New Mexico and eastern Kentucky containing approximately 615 million tons of coal reserves.Kentucky. The Partnership earns coal royalty revenue,revenues, based on long-term lease agreements, from 28 coal-mining29 coal mining operators actively mining under 5153 separate leases at 6154 mines. CoalApproximately 72 percent of PVR’s 2003 coal royalty revenues under non-Peabody leases areand 99 percent of its 2002 coal royalty revenues were based on the higher of a percentage of the gross sales price or a fixed price per ton of coal sold, with pre-established minimum monthly or annual payments. Under the Peabody leases,The balance of PVR’s 2003 and 2002 coal royalty revenues arewas based on fixed royalty rates which escalate annually, also with pre-established monthly minimums. The Partnership does not operate coal mines. The Partnership provides fee-based coal preparation and transportation facilities to some of its lessees to enhance their production levels and generate additional coal service revenues.

The Partnership’s timber assets consist of various hardwoods, primarily red oak, white oak, yellow poplar and black cherry. The Partnership owned approximately 168166 million board feet of standing saw timber at December 31, 2002.2003. The Partnership’s timber inventory only includes timber that can be harvested and is greater than 12 inches in diameter.

2

In 2002, the Partnership made two reserve acquisitions as well as an infrastructure acquisition. In December 2002, the Partnership announced the formation of an important strategic alliance withacquired from Peabody Energy Corporation the largest private sector coal company in the world. Central to the transaction was the purchase from and leaseback to Peabody of(“Peabody”) approximately 120 million tons of proven and probable coal reserves located in New Mexico (80 million tons) and northern West Virginia (40 million tons) (the “Peabody Acquisition”). As a result of the Peabody Acquisition, the Partnership’s total reserves increased by approximately 25 percent to 615 million tons. The Peabody Acquisition was funded with $72.5 million in cash and the issuance by the Partnership to

Page 4

Peabody of 1,522,325 common units and 1,240,833 Class B common units. Of the Class B common units issued, 293,700 are currently being held in escrow pending certain approvals from the State of New Mexico and Peabody’s acquisition and transfer to PVR of certain reserves. As a result of the escrow arrangement, approximately five million tons of coal reserves were excluded from reserve totals and 293,700 Class B common units were excluded from units issued in the Partnership’s financial statements for the year ended December 31, 2002.

The alliance with Peabody accomplishes several strategically important goals. It provides geographic diversity by exposing the Partnership to new markets in the western United States and northern Appalachia. The inclusion of affiliates of Peabody as a significant part of the Partnership’s lessee mix adds additional strength and stability to its lessee group. Peabody is incentivized to source additional assets to the Partnership in the future. This incentive is derived not only from Peabody’s ownership of approximately 15 percent of the Partnership’s common units, but also from its right to share in the general partner’s incentive distribution rights if Peabody sells additional coal assets to the Partnership in the future. See Item 1 – Corporate and Other – Partnership Distributions, Incentive Distribution Rights for more information.

In addition to the Peabody Acquisition, in August 2002, the Partnership purchased approximately 16 million tons of proven and probable coal reserves located on the Upshur properties in northern Appalachia for $12 million. This acquisition(the “Upshur Acquisition”). The Upshur Acquisition was the Partnership’sPVR’s first investment outside of central Appalachia. The properties, which include approximately 18,000 mineral acres, contain predominately high sulfur, high BTU coal reserves.

In June 2001, the Partnership acquired the Fork Creek property in West Virginia, purchasing approximately 53 million tons of coal reserves for $33.1 million. In early 2002, the operator at Fork Creek filed for bankruptcy protection under Chapter 11 of the U.S. Bankruptcy Code and operations at the mine were idled on March 4, 2002. The operator continued to pay minimum royalties until the Partnership recovered its lease on August 31, 2002. In November 2002, the Partnership also purchased various infrastructure atlocated on its West Coal River property (formerly know as Fork Creek for $5.1 million plusCreek) including a 900 ton per hour coal preparation plant, a unit train loadout facility and a railroad-granted rebate on coal loaded through the assumption of certain reclamation liabilities and stream mitigation obligations. With control of the reserves, permits and the critical infrastructure, PVR’s management is working diligently to put a new, financially stable operator in place at Fork Creek. As is customary in the Partnership’s operations, PVR intends to assign all related reclamation liabilities to the new operator.facility.

Coal Royalties

The Partnership’s lessees mined approximately 14.326.5 million tons of coal in 20022003 from PVR’s properties and paid an average royalty of $2.20$1.90 per ton, compared with approximately 15.314.3 million tons mined in 20012002 at an average royalty of $2.11$2.20 per ton.

Timber Sales

Timber is harvestedThe Partnership harvests timber in advance of lessee mining to prevent loss of the resource. Timber is sold as individual parcels in competitive bid sales or on a contract basis, where PVR pays independent contractors to harvest timber while PVR directly markets the product. The Partnership sold approximately 5.3 MMbf in 2003, compared with 8.3 MMbf in 2002 at an average price of $187 per thousand board feet (“Mbf”), compared with 8.7 MMbf at an average price of $168 per Mbf in 2001.2002.

Coal Services

The Partnership generates coal service revenues from fees charged to lessees for the use of the Partnership’s coal preparation and transportation facilities. The majority of these fees have been generated by the Partnership’s unit train loadout facility located on its Wise property, which was completed in April 1999 at a cost of $5.2 million. This facility accommodates up to 108-car unit trains, which can be loaded in approximately four hours. Lessees utilize the unit train loadout facility to reduce delivery costs incurred by their customers. The Partnership recognized $1.7$2.1 million in coal service revenues in 2002 and 2001.2003, compared to $1.7 million in 2002. Such amounts are reported inas other revenues in the Consolidated Statements of Income included herein.

Corporate and Other

Partnership Distributions

Cash Distributions. The Partnership paid cash distributions of $2.06 per common and subordinated unit during the year ended December 31, 2003. In 2004, the Partnership expects to make distributions of $2.08 or more per common and subordinated unit.

We are entitled, through our wholly owned subsidiaries, to receive certain cash distributions payable with respect to the subordinated and common units of PVR held by such subsidiaries as well as certain cash distributions payable with respect to general partner incentive distribution rights held by our general partner subsidiary.

Page 5

Cash Distributions. The Partnership made its first cash distributionCompany received distributions from PVR of $0.34 per common$16.8 million and subordinated unit$14.9 million in February2003 and 2002, for the period October 30, 2001 through December 31, 2001. For 2002, the Partnership made quarterly cash distributions of $0.50 per common unit and subordinated unit. The Partnership intends to increase quarterly cash distributions to $0.52 per common unit and subordinated unit beginning with the distribution payable in May 2003 with respect to the first quarter of 2003.respectively.

Incentive Distribution Rights. Our wholly owned subsidiary is the general partner of PVR and, as such, holds certain incentive distribution rights which represent the right to receive an increasing percentage of quarterly distributions of available cash from operating surplus after the Partnership has paid minimum quarterly distributions and certain target distribution levels have been achieved. The minimum quarterly distribution is $0.50 per unit ($2.00 per unit on an annual basis). The incentive distributions rights are payable as follows:

If for any quarter:

3

then, PVR will distribute any additional available cash from operating surplus for that quarter among the unitholders and our general partner subsidiary in the following manner:

In each case, the amount of the target distribution set forth above is exclusive of any distributions to common unitholders to eliminate any cumulative arrearages in payment of the minimum quarterly distribution on the common units. In conjunction with the Peabody Acquisition, and if PVR purchases additional assets from Peabody in the future, our general partner subsidiary has issued a special membership interest which entitles Peabody to receive increased percentages, starting at zero and increasing up to 40 percent, of payments PVR makes to our general partner subsidiary with respect to incentive distribution rights if PVR purchases additional assets from Peabody in the future.rights.

Investments

During 2001, we sold 3,307,200 shares of Norfolk Southern Corporation (NYSE: NSC) common stock. The shares were sold in open market transactions on the New York Stock Exchange at an average price of $17.39 per share. Our 3,307,200 common shares of Norfolk Southern Corporation generated dividends of $0.2 million in 2001 and $2.6 million in 2000.2001. We received a quarterly dividend of $0.06 per share in 2001, which was a reduction from the $0.20 per share realized in 2000.2001. We had no available-for-sale securities at December 31, 20022003 and 2001.2002. See Note 5 (Investments5. Investments and Dividend Income)Income of the Notes to the Consolidated Financial Statements for additional information.

Page 6

Risks Associated with Business Activities

Oil and Gas

Oil and Gas

Competition

The oil and natural gas industry is very competitive. Competition is particularly intense in the acquisition of prospective oil and natural gas properties and oil and gas reserves. Our competitive position depends on our geological, geophysical and engineering expertise, our financial resources, our ability to develop properties and our ability to select, acquire and develop proved reserves. We compete with a substantial number of other companies having larger technical staffs and greater financial and operational resources. Many such companies not only engage in the acquisition, exploration, development and production of oil and natural gas reserves, but also carry on refining operations, electricity generation and the marketing of refined products. We also compete with major and independent oil and gas companies in the marketing and sale of oil and natural gas, and the oil and natural gas industry in general competes with other industries supplying energy and fuel to industrial, commercial and individual consumers. We compete with other oil and natural gas companies in attempting to secure drilling rigs and other equipment necessary for drilling and completion of wells. Such equipment may be in short supply from time to time.

4

Price Volatility

Historically, natural gas and crude oil prices have been volatile. These prices rise and fall based on changes in market demand and changes in the political, regulatory and economic climate and other factors that affect commodities markets that are generally outside of our control. Some of our projections and estimates are based on assumptions as to the future prices of natural gas and crude oil. These price assumptions are used for planning purposes. We expect our assumptions will change over time and that actual prices in the future may differ from our estimates. Any substantial or extended decline in the actual prices of natural gas and/or crude oil could have a material adverse effect on the Company’s financial position and results of operations (including reduced cash flow and borrowing capacity), the quantities of natural gas and crude oil reserves that we can economically produce, the quantity of estimated proved reserves that may be attributed to our properties and our ability to fund our capital program.

Drilling and Operating Risks

Our drilling operations are subject to various risks common in the industry, including cratering, explosions, fires and uncontrollable flows of oil, gas or well fluids. Our drilling operations are also subject to the risk that no commercially productive natural gas or oil reserves will be encountered. The cost of drilling, completing and operating wells is often uncertain, and drilling operations may be curtailed, delayed or canceled as a result of a variety of factors, including drilling conditions, high pressure or irregularities in formations, equipment failures or accidents and adverse weather conditions.

Transportation

We transport our natural gas to market on various gathering and transmission pipeline systems owned by third parties. Gathering fees are primarily paid by the purchaser of the natural gas. The majority of natural gas sales contracts are one year or less in duration and contain relevant monthly index pricing provisions. Interruptible gathering rates have increased over the years as pipelines have implemented the mandatory unbundling of gathering services (Federal Energy Regulatory Commission Order 636) from other transportation services. In 2002, Duke Energy,2003, NiSource Inc. gathered and transported approximately 3921 percent of our natural gas, Nisource,Dominion Transmission, Inc. (formerly Columbia Gas Transmission) approximately 2420 percent, Duke Energy Corporation approximately 19 percent, Exxon Mobil Corporation approximately 12 percent, and DominionCrosstex Energy Inc.Services LTD approximately 208 percent, with the remainder divided among several pipeline companies in Texas, Louisiana and West Virginia and Louisiana.Virginia. Production could be adversely affected by shutdownsdisruptions or curtailments of the operations of pipelines for maintenance or replacement as transportation options are limited.

Regulation

State Regulatory MattersMatters.. Various aspects of our oil and natural gas operations are regulated by administrative agencies under statutory provisions of the states where such operations are conducted. All of the jurisdictions in which we own or operate producing crude oil and natural gas properties have statutory provisions regulating the exploration for and production of crude oil and natural gas. These provisions include the permitting for the drilling of wells, maintaining bonding requirements in order to drill or operate wells, provisions relating to the location of wells, the method of drilling and casing wells, the surface use and restoration of properties upon which wells are drilled, and the plugging and abandoning of wells. Our operations are also subject to various conservation laws and regulations. These include the regulation of the size of drilling and spacing units or proration units, the number of wells that may be

Page 7

drilled in an area, and the unitization or pooling of crude oil and natural gas properties. In addition, state conservation laws establish maximum rates of production from crude oil and natural gas wells, generally prohibit the venting or flaring of natural gas, and impose certain requirements regarding the ratability or fair apportionment of production from fields and individual wells. The effect of these regulations is to limit the amounts of crude oil and natural gas we can produce from our wells, and to limit the number of wells or the locations at which we can drill.

5

Federal Energy Regulatory Commission. The Federal Energy Regulatory Commission (“FERC”) regulates the transportation and sale for resale of natural gas in interstate commerce under the Natural Gas Act of 1938 (“NGA”) and the Natural Gas Policy Act of 1978 (“NGPA”). In the past, the Federal government has regulated the prices at which oil and gas could be sold. The Natural Gas Wellhead Decontrol Act of 1989 (the “Decontrol Act”) removed all NGA and NGPA price and nonprice controls affecting producers’ wellhead sales of natural gas effective January 1, 1993. While sales by producers of their own natural gas production, and all sales of crude oil, condensate and natural gas liquids can currently be made at market prices, Congress could reenact price controls in the future.

Commencing in April 1992, the FERC issued Order Nos. 636, 636-A, 636-B and 636-C (“Order No. 636”), which require interstate pipelines to provide transportation separate, or “unbundled,” from the pipelines’ salessale of gas. Also, Order No. 636 requires pipelines to provide open-access transportation on a basis that is equal for all gas supplies. Although Order No. 636 does not directly regulate gas producers like Penn Virginia, Corporation, the FERC has stated that it intends for Order No. 636 to foster increased competition within all phases of the natural gas industry. The courts have largely affirmed the significant features of Order No. 636 and numerous related orders pertaining to the individual pipelines, although certain appeals remain pending and the FERC continues to review and modify its open access regulations. In particular, the FERC has issued Order No.Nos. 637, 637-A and 637-B which, among other things, (i) permitspermit pipelines to charge different maximum cost-based rates for peak and off-peak times,periods, (ii) encouragesencourage auctions for pipeline capacity, (iii) requiresrequire pipelines to implement imbalance management services, and (iv) restrictsrestrict the ability of pipelines to impose penalties for imbalances, overruns, and non-compliance with operational flow orders. In addition, the FERC has implemented regulations governingin place that govern the procedure for obtaining authorization to construct new pipeline facilities and has issued a policy statement, which it largely affirmed in a recent order on rehearing, establishing a presumption in favor of requiring owners of newnewly constructed pipeline facilities to charge rates based solely on the incremental costs associated with such new pipeline facilities.

While any additional FERC action on these matters would affect us only indirectly, these changes are intended to further enhance competition in natural gas markets. We cannot predict what further action the FERC will take on these matters, nor can we predict whether the FERC’s actions will achieve its stated goal of increasing competition in natural gas markets. However, we do not believe that we will be treated materially differently than other natural gas producers and markets with which we compete.

Environmental Matters. Extensive federal, state and local laws govern oil and natural gas operations, regulate the discharge of materials into the environment or otherwise relate to the protection of the environment. Numerous governmental departments issue rules and regulations to implement and enforce such laws that are often difficult and costly to comply with and which carry substantial administrative, civil and even criminal penalties for failure to comply. Some laws, rules and regulations relating to protection of the environment may, in certain circumstances, impose “strict liability” for environmental contamination, rendering a person liable for environmental and natural resource damages and cleanup costs without regard to negligence or fault on the part of such person. Other laws, rules and regulations may restrict the rate of oil and natural gas production below the rate that would otherwise exist or even prohibit exploration or production activities in sensitive areas. In addition, state laws often require some form of remedial action to prevent pollution from former operations, such as closure of inactive pits and plugging of abandoned wells. The regulatory burden on the oil and natural gas industry increases its cost of doing business and consequently affects its profitability. These laws, rules and regulations affect our operations, as well as the oil and gas exploration and production industry in general. We believe that we are in substantial compliance with current applicable environmental laws, rules and regulations and that continued compliance with existing requirements will not have a material adverse impact on us. Nevertheless, changes in existing environmental laws or the adoption of new environmental laws have the potential to adversely affect our operations.

Page 86

Coal Royalty and Land Management

Although the Partnership intendsexpects to make quarterly cash distributions of $0.52 or more per common unit, it can only do so to the extent it has sufficient cash from operations after payment of fees and expenses. In addition, quarterly distributions are payable on our subordinated units only after each common unit has received a distribution of $0.52$0.50 plus any arrearages due from prior quarters. Incentive distributions are payable to our general partner subsidiary after cash distributions per unit exceed $0.55 in any quarter. The Partnership’s revenues and its ability to make quarterly and incentive distributions are subject to several risks, including those described below.

Competition

The coal industry is intensely competitive primarily as a result of the existence of numerous producers. The Partnership’s lessees compete with coal producers in various regions of the U.S. for domestic sales. The industry has undergone significant consolidation that has led to some of the competitors of the Partnership’s lessees located in Appalachia to have significantly larger financial and operating resources than the Partnership’s lessees do. The Partnership’s lessees primarily compete with both large and small producers in Appalachia as well as the western United States. They compete on the basis of coal price at the mine, coal quality (including sulfur content), transportation cost from the mine to the customer and the reliability of supply. Continued demand for the Partnership’s coal and the prices that the Partnership’s lessees obtain are also affected by demand for electricity, environmental and government regulations, technological developments and the availability and price of alternative fuel supplies, including nuclear, natural gas, oil and hydroelectric power. Demand for the Partnership’s low sulfur coal and the prices the Partnership’s lessees will be able to obtain for it will also be affected by the price and availability of high sulfur coal, which can be marketed in tandem with emissions allowances in order to meet federal Clean Air Act requirements.

Operating Risks

General Regulation. The Partnership’s lessees are obligated to conduct mining operations in compliance with all applicable federal, state and local laws and regulations. These laws and regulations include matters involving the discharge of materials into the environment, employee health and safety, mine permits and other licensing requirements, reclamation and restoration of mining properties after mining is completed, management of materials generated by mining operations, surface subsidence from underground mining, water pollution, legislatively mandated benefits for current and retired coal miners, air quality standards, protection of wetlands, plant and wildlife protection, limitations on land use, storage of petroleum products and substances which are regarded as hazardous under applicable laws, and management of electrical equipment containing polychlorinated biphenyls, or PCBs. Because of extensive and comprehensive regulatory requirements, violations during mining operations are not unusual in the industry and, notwithstanding compliance efforts, we do not believe violations by the Partnership’s lessees can be eliminated completely. However, none of the violations to date, or the monetary penalties assessed, have been material to us, to the Partnership or, to our knowledge, to the Partnership’s lessees. We do not currently expect that future compliance will have a material adverse effect on us or the Partnership.

While it is not possible to quantify the costs of compliance by the Partnership’s lessees with all applicable federal and state laws, those costs have been and are expected to continue to be significant. The lessees post performance bonds pursuant to federal and state mining laws and regulations for the estimated costs of reclamation and mine closing, including the cost of treating mine water discharge when necessary. The Partnership does not accrue for such costs because its lessees are contractually liable for all costs relating to their mining operations, including the costs of reclamation and mine closure. However, the Partnership does require some smaller lessees to deposit certain funds into escrow for reclamation and mine closure costs or post performance bonds for these costs. Although the lessees typically accrue adequate amounts for these costs, their future operating results wouldmight be adversely affected if they later determined these accruals to be insufficient. Compliance with these laws has substantially increased the cost of coal mining for all domestic coal producers.

7

In addition, the electric utility industry, which is the most significant end-user of coal, is subject to extensive regulation regarding the environmental impact of its power generation activities which could affect demand for the Partnership’s lessees’ coal. The possibility exists that new legislation or regulations may be adopted which may have a significant impact on the mining operations of the Partnership’s lessees or their customers’ ability to use coal and may require the Partnership, its lessees or their customers to change operations significantly or incur substantial costs.

Page 9

RegulationCertain Regulatory and Legal Matters.

Clean Air Act. The Clean Air Act affects the end-users of coal and could significantly affect the demand for the Partnership’s coal and reduce the Partnership’s coal royalty revenues. The Clean Air Act and corresponding state and local laws extensively regulate the amount of sulfur dioxide, particulate matter, nitrogen oxides and other compounds emitted from industrial boilers and power plants, including those that use the Partnership’s coal. These regulations together constitute a significant burden on coal customers and stricter regulation could further adversely impact the demand for and price of the Partnership’s coal, resulting in lower coal royalty revenues.

In July 1997, the U.S. Environmental Protection Agency (“EPA”) adopted more stringent ambient air quality standards for particulate matter and ozone. Particulate matter includes small particles that are emitted during the combustion process. In a February 2001 decision, the U.S. Supreme Court largely upheld the EPA’s position, although it remanded the EPA’s ozone implementation policy for further consideration. Details regarding the new particulate standard itself are still subject to judicial challenge. These ozone restrictions will require electric power generators to further reduce nitrogen oxide emissions. Nitrogen oxides are naturally occurring byproducts of coal combustion that lead to the formation of ozone. Further reduction in the amount of particulate matter that may be emitted by power plants could also result in reduced coal consumption by electric power generators. Future regulations regarding ozone, particulate matter and other ambient air standards could restrict the market for coal and the development of new mines by the Partnership’s lessees. This in turn may result in decreased production by the Partnership’s lessees and a corresponding decrease in the Partnership’s coal royalty revenues. These decreases could adversely effectaffect the distributions we receive from the Partnership.

The Clean Air Act also imposes standards on sources of hazardous air pollutants. These standards have not yet been extended to coal mining operations, or by-productsbut in January 2004, EPA proposed regulations to control emissions of coal combustion, but consideration is now being given to regulating certainmercury, a hazardous air pollutant componentsfrom power plants that combust coal, as well as nitrogen oxides and sulfur dioxide, which are found in coal combustion exhaust, including mercury.also power plant pollutants, Like other environmental regulations, these standards and future standards could result in a decreased demand for coal.

Surface Mining Control and Reclamation Act of 1977. The Surface Mining Control and Reclamation Act of 1977 (“SMCRA”) and similar state statutes impose on mine operators the responsibility of restoring the land to its original state or compensating the landowner for types of damages occurring as a result of mining operations, and require mine operators to post performance bonds to ensure compliance with any reclamation obligations. Regulatory authorities may attempt to assign the liabilities of the Partnership’s lessees to the Partnership if any of the lessees are not financially capable of fulfilling those obligations. In conjunction with mining the property, the Partnership’s lessees are contractually obligated under the terms of their leases to comply with all laws, including SMCRA and equivalent state and local laws, which obligations include reclaiming and restoring the mined areas by grading, shaping and reseeding the soil. Upon completion of the mining, reclamation generally is completed by seeding with grasses or planting trees for use as pasture or timberland, as specified in the approved reclamation plan.

CERCLA. The Partnership could become liable under federal and state Superfund and waste management statutes if its lessees are unable to pay environmental cleanup costs. The Comprehensive Environmental Response, Compensation and Liability Act, known as CERCLA or “Superfund,” and similar state laws create liabilities for the investigation and remediation of releases and threatened releases of hazardous substances to the environment and damages to natural resources. As a landowner, the Partnership is potentially subject to liability for these investigation and remediation obligations.

8

Mountaintop Removal LitigationSurface Mining Valley Fills.. On January 29, 2003, Over the United States Fourth Circuit Court of Appeals (the “Circuit Court”) vacated an injunction issued in May 2002 by the United States District Court for the Southern District of West Virginia (the “District Court”). This injunction had prohibited the Huntington, West Virginia officecourse of the U.S. Army Corpslast several years, opponents of Engineers (the “Corps”) from issuingsurface mining have filed three lawsuits challenging the legality of permits under Section 404 of the Clean Water Act forauthorizing the construction of valley fills for the disposal of coal mining overburden. These valleys typically contain steamsoverburden under federal and state laws applicable to surface mining activities. Although two of these challenges were successful in the United States District Court for the southern District of West Virginia (the “District Court”), the United States Court of Appeals for the Fourth Circuit overturned both of those decisions in Bragg v. Robertson in 2001 and in Kentuckians For The Commonwealth v. Rivenburgh in 2003.

On October 23, 2003, a third lawsuit involving the disposal of coal mining overburden was filed under the name of Ohio Valley Environmental Coalition v. Bulen. In this case, which was also filed in the District Court, several public interest group plaintiffs have alleged that underthe Army Corps of Engineers violated the Clean Water Act are considered navigable waters of the United States. The District Court had found that the Corp’s permitting of overburden valley fills under Section 404 was(“CWA”) and other federal regulations when it issued Nationwide Permit 21, a violation of the Clean Water Act since Section 404 allows only the permitting of fill material depositedgeneral permit for a beneficial purpose and not for mere waste disposal such as the disposal of coal overburden. The Circuit Court reversedmining overburden into United States waters. This most recent suit also challenges certain individual discharge authorizations in West Virginia, including several involving the mining activities of the Partnership’s lessees. If the plaintiffs prevail in this finding, concluding, instead, that overburden valley fillslatest lawsuit, lessees who have received authorization for discharges pursuant to Nationwide Permit 21 could be prevented from undertaking future discharges until they receive individual CWA permits, and future operations could require individual permits. Obtaining these individual permits is likely to substantially increase both the time and the costs of obtaining CWA permits for our lessees and other coal mining operators throughout the industry where any such unfavorable ruling may be permitted under Section 404 and remandedapplied. These increases could adversely affect our coal royalty revenues. Although the case backPartnership expects that any ruling for the plaintiffs would be appealed to the Fourth Circuit, the coal mining industry, including the operations of our lessees, could be significantly adversely impacted by the initial effects of an adverse decision while any appeal is pending.

West Virginia Anti-degradation Policy.As a result of a September 2003 decision by the District Court for further proceedingsin Ohio Valley Environmental Coalition v. Whitman, the State of West Virginia is currently implementing the CWA without an EPA-approved anti-degradation implementation policy, which would apply in cases of pollutant discharges into waters that have been designated as high quality waters by the State. In this case, the District Court vacated EPA’s previous approval of the West Virginia anti-degradation policy after the District Court determined that the State’s policy did not inconsistentcomply with the Circuit Court’s opinion.requirements of the CWA. The West Virginia anti-degradation policy had included a number of exceptions, including one for parties holding general CWA permits, from anti-degradation review requirements. The EPA has reportedly decided not to appeal this decision and is instead proceeding with a policy review. Were PVA’s lessees to seek permits to discharge coal overburden into high quality waters under a new policy which does not include such an exception, permit applications will likely be required to undergo the public and intergovernmental scrutiny associated with an anti-degradation review, which may either delay the issuance or reissuance of CWA permits, require the use of more costly control measures or lead to the denial of these permits. The delay, denial or added costs of complying with these permits may increase the costs of coal production, potentially reducing PVR’s royalty revenues and adversely affecting our Partnership distributions.

Mine Health and Safety Laws.Stringent safety and health standards have been imposed by federal legislation since the adoption of the Mine Health and Safety Act of 1969. The Mine Health and Safety Act of 1969 resulted in increased operating costs and reduced productivity. The Mine Safety and Health Act of 1977, which significantly expanded the enforcement of health and safety standards of the Mine Health and Safety Act of 1969, imposes comprehensive safety and health standards on all mining operations. In addition, as part of the Mine Health and Safety Acts of 1969 and 1977, the Black Lung Acts require payments of benefits by all businesses conducting current mining operations to coal miners with black lung and to some survivors of a miner who dieshas died from this disease.

Page 10

Mining Permits and Approvals.Numerous governmental permits or approvals are required for mining operations. In connection with obtaining these permits and approvals, the Partnership’s lessees may be required to prepare and present to federal, state or local authorities data pertaining to the effect or impact that any

9

proposed production of coal may have upon the environment. The requirements imposed by any of these authorities may be costly and time consuming and may delay commencement or continuation of mining operations.

In order to obtain mining permits and approvals from state regulatory authorities, mine operators, including the Partnership’s lessees, must submit a reclamation plan for restoring, upon the completion of mining operations, the mined property to its prior condition, productive use or other permitted condition. Typically, lessees submit the necessary permit applications between 12 and 18 months before they plan to begin mining a new area. In the Partnership’s experience, permits generally are approved within 12 months after a completed application is submitted. In the past, lessees have generally obtained their mining permits without significant delay. The Partnership’s lessees have obtained or applied for permits to mine a majority of the reserves that are currently planned to be mined by lesseesthem over the next five years. The Partnership’s lessees are also in the planning phase for obtaining permits for the remainingadditional reserves planned to be mined over the nextfollowing five years. However, they cannot makegive any assurances that they will not experience difficulty in obtaining mining permits in the future.

Timber Regulations.The Partnership’s timber operations are subject to federal, state and local laws and regulations, including those related to the environment, protection of endangered species, foresting activities and health and safety. The Partnership believes it is managing its timberlands in substantial compliance with applicable federal and state regulations.

Employees

We had 104116 employees at December 31, 2002,2003, including 3032 employees who directly provide services for PVR through its general partner. We consider our relations with our employees to be good.

Available Information

The Company’s Internet address is www.pennvirginia.com. We make available free of charge on or through our Internet website our Governance Principles, Code of Business Conduct and Ethics, Executive and Financial Officer Code of Ethics and the charters of each of our Audit Committee, Nominating and Governance Committee, Compensation and Benefits Committee and Oil and Gas Committee. We also make available free of charge on or through our Internet website our annual report on Form 10-K, quarterly reports on Form 10-Q, reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. To date, we have inadvertently not made so available on our website any current reports on Form 8-K. We will provide, free of charge upon request, electronic or paper copies of all current reports on Form 8-K which were filed from November 15, 2002 to February 15, 2003. We will make available, free of charge, on or through our internet website, all reports on Form 8-K and amendments to those reports filed after February 15, 2003 as soon as reasonably practicable after we electronically file such reports with, or furnish them to, the Securities and Exchange Commission.

Page 11

Executive Officers of the Company

The following table sets forth information concerning our executive officers. Each officer is elected annually by the Board of Directors and serves at the pleasure of the Board of Directors.

Name | Age | Position with the Company | ||

A. James Dearlove |

| President and Chief Executive Officer | ||

Frank A. Pici |

| Executive Vice President and Chief Financial Officer | ||

|

| Executive Vice President | ||

|

| Executive Vice President | ||

Nancy M. Snyder |

| Senior Vice President, General Counsel and Secretary | ||

Dana |

| Vice President and Controller | ||

Ronald K. Page | 53 | Vice President, Corporate Development |

10

A. James Dearlove – Dearlove—Mr. Dearlove has served in various capacities with the Company since 1977, including as President and Chief Executive Officer and a Director of the Company since May 1996, President and Chief Operating Officer of the Company from 1994 to May 1996, Senior Vice President of the Company form 1992 to 1994 and Vice President of the Company from 1986 to 1992. He is also Chief Executive Officer and Chairman of the Board of Penn Virginia Resource GP, LLC, the general partner of Penn Virginia Resource Partners, L.P. He also serves as director of the Powell River Project and the National Council of Coal Lessors.

Frank A. Pici – Pici—Mr. Pici is the Executive Vice President and Chief Financial Officer of the Company, which he joined in September 2001. Mr. Pici is also the Vice President and Chief Financial Officer and a Director of Penn Virginia Resource, GP LLC. From 1996 to August 2001, Mr. Pici was Vice President of Finance and Chief Financial Officer of Mariner Energy, Inc., an oil and gas exploration and production company. Prior to 1996, he served in various capacities with Cabot Oil & Gas Corporation, including Corporate Controller from 1994 to 1996, Director, Internal Audit from 1992 to 1994, and regional accounting manager from 1989 to 1992. From 1982 to 1989, he held financial management positions with companies in the oil and gas and coal industries.

Keith D. Horton – Mr. Horton has served in various capacities with the Company since 1981, including Executive Vice President and a Director of the Company since December 2000, Vice President – Eastern Operations of the Company from May 1996 to May 1997, President of Penn Virginia Coal Company from April 1996 to October 2001, Vice President of Penn Virginia Coal Company from March 1994 to February 1996, Vice President from January 1990 to December 1998, and Manager, Coal Operations from July 1982 to December 1989, of Penn Virginia Resources Corporation. He is also the President and Chief Operating Officer and a Director of Penn Virginia Resource, GP LLC. Additionally, Mr. Horton is Chairman of the Central Appalachian Section of the Society of Mining Engineers. He also serves as a director of the Virginia Mining Association, Powell River Project and Virginia Coal Council.

H. Baird Whitehead – Whitehead—Mr. Whitehead is an Executive Vice President of the Company, which he joined in January 2001. Prior to joining Penn Virginia, Mr. Whitehead served in various positions with Cabot Oil & Gas Corporation. From 1998 to 2001, he served as Senior Vice President during which time he oversaw Cabot’s drilling, production, and exploration activity in the Appalachia, Rocky Mountains, Mid-Continent and the Texas and Louisiana Gulf Coast areas. From 1992 to 1998, he was Vice President and Regional Manager of Cabot’s Appalachian business unit and from 1989 to 1992, he was Vice President and Regional Manager of Cabot’s Anadarko business unit. From 1987 to 1989, he served as Vice President of Engineering for Cabot. From 1972 to 1987, he held various engineering and supervisory positions with Texaco, Columbia Gas Transmission and Cabot.

Keith D. Horton—Mr. Horton has served in various capacities with the Company since 1981, including Executive Vice President and a Director of the Company since December 2000, Vice President—Eastern Operations of the Company from February 1999 to December 2000, President of Penn Virginia Coal Company from February 1996 to October 2001, Vice President of Penn Virginia Coal Company from March 1994 to February 1996, Vice President from January 1990 to December 1998, and Manager, Coal Operations from July 1982 to December 1989, of Penn Virginia Resources Corporation. He is also the President and Chief Operating Officer and a Director of Penn Virginia Resource, GP LLC. Additionally, Mr. Horton is Chairman of the Central Appalachian Section of the Society of Mining Engineers. He also serves as a director of the Virginia Mining Association, Powell River Project and Virginia Coal Council.

Nancy M. Snyder – Snyder—Ms. Snyder has served as Senior Vice President of the Company since February 2003 as Vice President since December 2000 and as General Counsel and Corporate Secretary of the Company since 1997. She was a Vice President of the Company from December 200 to February 2003. Ms. Snyder is also the Vice President, General Counsel and a Director of Penn Virginia Resource GP, LLC. From 1993 to 1997, Ms. Snyder was a solo practitioner representing clients generally in connection with mergers and acquisitions and general corporate matters. From 1990 to 1993, Ms. Snyder served as general counsel to Nan Duskin, Inc. and its affiliated companies, which were in the businesses of womens’women’s’ retail fashion and real estate. From 1983 to 1989, Ms. Snyder was an associate at the law firm of Duane Morris, where she practiced securities, banking and general corporate law.

Dana G. Wright – G Wright—Mr. Wright joined the Company in July 2002 and serves as Vice President and Controller. Prior to joining Penn Virginia, he was employed for 26 years with Atlantic Richfield Company, and most recently with its publicly traded subsidiary, Vastar Resources, Inc. During that time he held a variety of financial, accounting and treasury related positions.

Ronald K. Page—Mr. Page 12has served as Vice President, Corporate Development since joining the Company in July 2003. From January 1998 to May 2003, Mr. Page served in various positions with El Paso Field Services Company, including Vice President of Commercial Operations—Texas Pipelines and Processing, Vice

11

President of Business Development, Director of Business Development and Consultant. From October 1995 through December 1997, Mr. Page was employed as Vice President of Business Development by TPC Corporation (formerly Texas Power Corporation). For 17 years prior to 1995, Mr. Page served in various positions at Seagull Energy Corporation, including Vice President of Operations at Seagull’s Enstar Natural Gas Company, Vice President of Pipelines and Marketing and Manager of Engineering.

The following terms have the meanings indicated below when used in this report.

| means a standard barrel of 42 U.S. gallons liquid volume | |

| means one billion cubic feet | |

| means one billion cubic feet equivalent with one barrel of oil or condensate converted to six thousand cubic feet of natural gas based on the estimated relative energy content | |

| acre or well means an acre or well in which a working interest is owned | |

| means one thousand barrels | |

| means one thousand board feet | |

| means one thousand cubic feet | |

| means one million board feet | |

| means one million British thermal units | |

| means one million cubic feet | |

| acres or wells is determined by multiplying the gross acres or wells by the owned working interest in those gross acres or wells | |

| New York Mercantile Exchange | |

Present value of proved | means the present value (discounted at 10%) of estimated future cash flows from proved oil and natural gas reserves, as estimated by our independent engineers, reduced by additional estimated future operating expenses, development expenditures and abandonment costs (net of salvage value) associated therewith (before income taxes). | |

Probable Coal | means those reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation. | |

Proved | means those estimated quantities of crude oil, condensate and natural gas that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known oil and gas reservoirs under existing economic and operating | |

Proven Coal | means those reserves for which: (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; |

12

grade and/or quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely, and the geologic character is so well defined, that the size, shape, depth and mineral content of reserves are well-established. | |

Standardized | means present value of proved reserves further reduced by the present value (discounted at 10%) of estimated future income taxes on cash | |

Working | means a cost-bearing interest under an oil and gas lease that gives the holder the right to develop and produce the minerals under the |

Page 13

ITEM 2 –PROPERTIESItem 2—Properties

Facilities

We are headquartered in Radnor, Pennsylvania with additional offices in Kingsport, Tennessee, Houston, Texas and Charleston, West Virginia. All of our office facilities are leased. We believe that our properties are adequate for our current needs.

Title to Properties

We believe that we have satisfactory title to all of our properties and the associated oil and gas reserves in accordance with standards generally accepted in the oil and natural gas and coal royalty and land management industries.

As is customary in the oil and gas industry, we make only a cursory review of title to farmout acreage and to undeveloped oil and gas leases upon execution of any contracts. Prior to the commencement of drilling operations, a thorough title examination is conducted and curative work is performed with respect to significant defects. To the extent title opinions or other investigations reflect defects, we cure such title defects. If we were unable to remedy or cure any title defect of a nature such that it would not be prudent to commence drilling operations on a property, we could suffer a loss of our investment in the property. Prior to completing an acquisition of producing oil and gas assets, we obtain title opinions on all material leases. Our oil and gas properties are subject to customary royalty interests, liens for current taxes and other burdens that we believe do not materially interfere with the use or materially affect the value of such properties.

Of the 615588 million tons of proven and probable coal reserves to which the Partnership hashad rights as of December 31, 2002,2003, PVR owned the mineral rightsinterests and the majority of related surface rights to 572544 million tons, or 93 percent, and leased the remaining 4344 million tons, or 7 percent, from unaffiliated third parties. In addition to the revenues the Partnership receives from its coal business, it also earns revenues from the sale of timber. At December 31, 2002, the Partnership owned 114,500 surface acres of timberland containing 168 million board feet of inventory.

Page 1413

Information Regarding Oil and Gas Properties

Production and Pricing

The following table sets forth production, average sales prices and production costs with respect to our properties for the years ended December 31, 2003, 2002 2001 and 2000.2001.

2002 | 2001 | 2000 | 2003 | 2002 | 2001 | ||||||||||||||||

Production | |||||||||||||||||||||

Oil and condensate (Mbbls)* |

| 349 |

|

| 164 |

| 31 | 625 | 349 | 164 | |||||||||||

Natural gas (MMcf)* |

| 18,697 |

|

| 13,130 |

| 11,645 | 20,094 | 18,697 | 13,130 | |||||||||||

Total production (MMcfe)* |

| 20,791 |

|

| 14,114 |

| 11,831 | 23,844 | 20,791 | 14,114 | |||||||||||

Average sales price | |||||||||||||||||||||

Oil and condensate ($/Bbl) | $ | 23.63 |

| $ | 22.94 | $ | 26.84 | $ | 26.91 | $ | 23.63 | $ | 22.94 | ||||||||

Natural gas ($/Mcf) | $ | 3.35 |

|

| 4.06 |

| 3.95 | $ | 5.31 | $ | 3.35 | $ | 4.06 | ||||||||

Production cost ($/Mcfe) | |||||||||||||||||||||

Lease operating expense | $ | 0.45 |

| $ | 0.40 | $ | 0.38 | $ | 0.51 | $ | 0.45 | $ | 0.40 | ||||||||

Taxes other than income |

| 0.27 |

|

| 0.31 |

| 0.24 | 0.40 | 0.27 | 0.31 | |||||||||||

General and Administrative Expense |

| 0.40 |

|

| 0.38 |

| 0.22 | ||||||||||||||

General and administrative expense | 0.33 | 0.40 | 0.38 | ||||||||||||||||||

Total production cost | $ | 1.12 |

| $ | 1.09 | $ | 0.84 | $ | 1.24 | $ | 1.12 | $ | 1.09 | ||||||||

Hedging Summary | |||||||||||||||||||||

Natural gas prices ($/Mcf): | |||||||||||||||||||||

Actual price received for production | $ | 3.39 |

| $ | 3.92 | $ | 3.95 | $ | 5.59 | $ | 3.39 | $ | 3.92 | ||||||||

Effect of derivative hedging activities |

| (0.04 | ) |

| 0.14 |

| — | (0.28 | ) | (0.04 | ) | 0.14 | |||||||||

Average realized price | $ | 3.35 |

| $ | 4.06 | $ | 3.95 | $ | 5.31 | $ | 3.35 | $ | 4.06 | ||||||||

Crude oil prices ($/Bbl): | |||||||||||||||||||||

Actual price received for production | $ | 24.39 |

| $ | 22.45 | $ | 26.84 | $ | 27.77 | $ | 24.39 | $ | 22.45 | ||||||||

Effect of derivative hedging activities |

| (0.76 | ) |

| 0.49 |

| — | (0.86 | ) | (0.76 | ) | 0.49 | |||||||||

Average realized price | $ | 23.63 |

| $ | 22.94 | $ | 26.84 | $ | 26.91 | $ | 23.63 | $ | 22.94 | ||||||||

| * | Production for 2002 does not include approximately 16 Mbbls of oil condensate and 18 MMcf of natural gas production, or 114 MMcfe, related to discontinued operations. Production volumes for the related properties sold were insignificant in 2001. |

*Production for 2002 does not include approximately 16 Mbbls of oil condensate and 18 MMcf of natural gas production, or 114 MMcfe, related to discontinued operations. 2001 production volumes for properties sold were insignificant.

Page 1514

Proved Reserves

We hadThe following table presents certain information regarding our proved reserves as of 241 BcfDecember 31, 2003, 2002 and 2001. The proved reserve estimates presented below were prepared by Wright and Company, Inc., independent petroleum engineers. For additional information regarding estimates of natural gasproved reserves, the preparation of such estimates by Wright and 5.4 million barrels of crudeCompany, Inc. and other information about our oil and condensate at December 31, 2002. The present valuegas reserves, see Note 23. Supplemental Information on Oil and Gas Producing Activities (Unaudited) of the estimated future cash flows discounted at 10 percent (pre-tax SEC PV10 Value) at December 31, 2002, was $481 million. At December 31, 2002, we had 195 gross (128.3 net)Notes to the Consolidated Financial Statements. Our estimates of proved undeveloped drilling locations.reserves in the table above are consistent with those filed by us with other federal agencies.

Oil and Condensate (MMbbls) | Natural Gas (Bcf) | Natural Gas Equivalents (Bcfe) | Pre-tax SEC PV10Value ($MM) | Year-end Weighted Average Prices Used | ||||||||||||||||||||||||||

$ / Bbl | $ / Mmbtu | Oil and Condensate | Natural Gas | Natural Equivalents | Pre-tax SEC PV10 Value | Year-end Prices Used | ||||||||||||||||||||||||

| (MMbbls) | (Bcf) | (Bcfe) | ($ millions) | $ / Bbl | $ /MMbtu | |||||||||||||||||||||||||

2003 | ||||||||||||||||||||||||||||||

Developed | 3.3 | 231 | 251 | $ | 570 | |||||||||||||||||||||||||

Undeveloped | 3.3 | 52 | 72 | 126 | ||||||||||||||||||||||||||

Total | 6.6 | 283 | 323 | $ | 696 | $ | 32.52 | $ | 5.97 | |||||||||||||||||||||

2002 | ||||||||||||||||||||||||||||||

Developed | 2.9 | 199 | 216 | $ | 404 | 2.9 | 199 | 216 | $ | 404 | ||||||||||||||||||||

Undeveloped | 2.5 | 42 | 57 |

| 77 | 2.5 | 42 | 57 | 77 | |||||||||||||||||||||

Total | 5.4 | 241 | 273 | $ | 481 | $ | 31.13 | $ | 4.74 | 5.4 | 241 | 273 | $ | 481 | $ | 31.13 | $ | 4.74 | ||||||||||||

2001 | ||||||||||||||||||||||||||||||

Developed | 2.2 | 183 | 196 | $ | 202 | 2.2 | 183 | 196 | $ | 202 | ||||||||||||||||||||

Undeveloped | 1.7 | 46 | 56 |

| 40 | 1.7 | 46 | 56 | 40 | |||||||||||||||||||||

Total | 3.9 | 229 | 252 | $ | 242 | $ | 20.40 | $ | 2.65 | 3.9 | 229 | 252 | $ | 242 | $ | 20.40 | $ | 2.65 | ||||||||||||

2000 | ||||||||||||||||||||||||||||||

Developed | 0.1 | 146 | 147 | $ | 540 | |||||||||||||||||||||||||

Undeveloped | — | 28 | 28 |

| 104 | |||||||||||||||||||||||||

Total | 0.1 | 174 | 175 | $ | 644 | $ | 23.31 | $ | 9.91 | |||||||||||||||||||||

The standardized measure of discounted future net cash flows, which represents the present value of future net revenues after income taxes discounted at ten percent, was $512 million, $355 million and $189 million and $467 million atas of December 31, 2003, 2002 2001 and 2000,2001, respectively. For information on the changes in standardized measure of discounted future net cash flows. Seeflows, see Note 22 (Supplementary23. Supplemental Information on Oil and Gas Producing Activities (Unaudited)) of the Notes to the Consolidated Financial Statements, for more information.Statements.

In accordance with the Securities and Exchange Commission’s guidelines, the engineers’ estimates of future net revenues from our properties and the pre-tax SEC PV10 value thereof are made using oil and natural gas sales prices in effect as of December 31, 2002.2003. The prices are held constant throughout the life of the properties except where such guidelines permit alternate treatment, including the use of fixed and determinable contractual price escalations. Net proved oil and gas reserves for the three years ended December 31, 2002 were estimated by Wright and Company, Inc. Prices for oil and gas are subject to substantial seasonal fluctuations and prices for each are subject to substantialas well as fluctuations as a result ofresulting from numerous other factors. See Item 7 – 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Proved reserves are the estimated quantities of natural gas, crude oil and condensate that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. Proved developed reserves are proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods. There are numerous uncertainties inherent in estimating quantities of proved reserves and in projecting future rates of production and timing of development expenditures, including many factors beyond our control. Reserve engineering is a subjective process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact manner, and the accuracy of any reserve estimate is a function of the quality of available data and of engineering and geological interpretation and judgment. The quantities of crude oil and natural gas

15

that are ultimately recovered, production and operating costs, the amount and timing of future development expenditures and future crude oil and natural gas sales prices may all differ from those assumed in these estimates. Therefore, neither the pre-tax nor after-tax SEC PV10 value amounts shown above should not be

construed as the current market value of the estimated oil and natural gas reserves attributable to our properties. The information set forth in the foregoing tables includes revisions of certain volumetric reserve estimates attributable to proved properties included in the preceding year’s estimates. Such revisions are the result of additional information from subsequent completions and production history from the

Page 16

properties involved or the result of a decrease (or increase) in the projected economic life of such properties resulting from changes in production prices.

Acreage

The following table sets forth our developed and undeveloped acreage at December 31, 2002.2003. The acreage is located in the eastern and southern portionsGulf Coast areas of the United States.

Gross Acreage | Net Acreage | Gross Acreage | Net Acreage | |||||

(in thousands) | (in thousands) | |||||||

Developed | 611 | 487 | 669 | 531 | ||||

Undeveloped | 246 | 131 | 408 | 231 | ||||

Total | 857 | 618 | 1,077 | 762 | ||||

Wells Drilled

The following table sets forth the gross and net number of exploratory and development wells drilled during the last three years. The number of wells drilled refers to the number of wells spud at any time during the respective year. Net wells equal the number of gross wells multiplied by our working interest in each of the gross wells. Productive wells represent either wells which were producing or which were capable of commercial production.

2002 | 2001 | 2000 | 2003 | 2002 | 2001 | |||||||||||||||||||

Gross | Net | Gross | Net | Gross | Net | Gross | Net | Gross | Net | Gross | Net | |||||||||||||

Development | ||||||||||||||||||||||||

Productive | 87 | 58.4 | 125 | 96.1 | 99 | 75.3 | 161 | 117.0 | 87 | 58.4 | 125 | 96.1 | ||||||||||||

Non-productive | 3 | 2.5 | 5 | 5.0 | 1 | 0.9 | 1 | 1.0 | 3 | 2.5 | 5 | 5.0 | ||||||||||||

90 | 60.9 | 130 | 101.1 | 100 | 76.2 | 162 | 118.0 | 90 | 60.9 | 130 | 101.1 | |||||||||||||

Exploratory | ||||||||||||||||||||||||

Productive | 3 | 3.0 | 19 | 14.5 | 1 | 0.2 | 5 | 1.2 | 3 | 3.0 | 19 | 14.5 | ||||||||||||

Non-productive | 3 | 1.6 | 5 | 3.5 | 5 | 1.3 | 3 | 2.9 | 3 | 1.6 | 5 | 3.5 | ||||||||||||

Under evaluation | — | — | — | — | 3 | 1.4 | 10 | 10.0 | — | — | — | — | ||||||||||||

6 | 4.6 | 24 | 18.0 | 9 | 2.9 | 18 | 14.1 | 6 | 4.6 | 24 | 18.0 | |||||||||||||

Total | 96 | 65.5 | 154 | 119.1 | 109 | 79.1 | 180 | 132.1 | 96 | 65.5 | 154 | 119.1 | ||||||||||||

The ten exploratory wells under evaluation represent coalbed methane (“CBM”) wells drilled and completed in the Cherokee Basin in Chase County, Kansas. The Company expects to determine the commercial viability of the Cherokee basin program during the first half of 2004.

16

Productive Wells

The number of productive oil and gas wells in which we had a working interest at December 31, 20022003 is set forth below. Productive wells are producing wells or wells capable of commercial production.

Operated Wells | Operated Wells | Non-Operated Wells | Total | Operated Wells | Non-Operated Wells | Total | ||||||||||||||

Gross | Net | Gross | Net | Gross | Net | Net | Gross | Net | Gross | Net | ||||||||||

692 | 668 | 430 | 63 | 1,122 | 731 | |||||||||||||||

794 | 769.7 | 493 | 77.7 | 1,287 | 847.4 | |||||||||||||||

In addition to the above working interest wells, Penn Virginia owns royalty interests in 2,346 gross wells.

Page 17

Information Regarding Coal Royalty and Land Management Properties

The Partnership’s coal reserves at December 31, 20022003 covered 241,000 acres, including fee and leased acreage, in Virginia, West Virginia, New Mexico and eastern Kentucky. The coal reserves are in various surface and underground seams.

The Partnership’s As of December 31, 2003, the Partnership had approximately 588 million tons of proven and probable coal reserves, which are estimated at 615 million tons as of December 31, 2002. found in the following six separate properties:

Reserves are coal tons that can be economically extracted or produced at the time of determination considering legal, economic and technical limitations. Proven coal reserves are reserves for which (a) the quantity is computed from dimensions revealed in outcrops, trenches, working or drill holes; grade and/orand quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely, and the geologic character is so well defined,well-defined, that the size, shape, and depth and mineral content of reserves are well-established. Probable coal reserves are reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

In areas where geologic conditions indicate potential inconsistencies related to coal reserves, the Partnership performs additional drilling to ensure the continuity and mineablility of coal reserves. Consequently, sampling in those areas involves drill holes that are spaced closer together than those distances cited above.

Reserve estimates are adjusted annually for production, unmineable areas, acquisitions and sales of coal in place. The majority of PVR’s reserves are high in energy content, low in sulfur and suitable for either the steam or metallurgical markets.market.

The amount of coal a lessee can profitably mine at any given time is subject to several factors and may be substantially different from “proven and probable reserves.” Included among the factors that influence profitability are the existing market price, coal quality and operating costs.

17

The following table sets forth production data and reserve information with respect to each of the Partnership’s six properties:

Production Year Ended December | Proven and Probable December 31, 2003 | |||||||||||

Property | 2003 | 2002 | 2001 | Under- ground | Surface | Total | ||||||

| (tons in millions) | ||||||||||||

Wise | 9.3 | 8.9 | 9.0 | 186.5 | 25.2 | 211.7 | ||||||

Coal River | 3.9 | 2.5 | 4.0 | 128.0 | 73.2 | 201.2 | ||||||

New Mexico | 6.3 | 0.2 | — | — | 73.3 | 73.3 | ||||||

Northern Appalachia | 5.1 | 0.5 | — | 46.5 | 2.5 | 49.0 | ||||||