UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K/A

Amendment No. 1

| x | ANNUAL REPORT PURSUANT TO SECTION 13 |

For the fiscal year ended December 31, 2017

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ____________to ______________. | |

Commission File Number | Exact name of registrant as specified in its charter and principal office address and telephone number | State of Incorporation | I.R.S. Employer Identification No. | Name of exchange on which registered | Securities registered pursuant to Section 12(b) of the Act: | Securities registered pursuant to Section 12(g) of the Act: |

| 1-6364 | South Jersey Industries, Inc. 1 South Jersey Plaza Folsom, NJ 08037 (609) 561-9000 | New Jersey | 22-1901645 | New York Stock Exchange | Common Stock - $1.25 par value per share (Title of each class) | None |

| 000-22211 | South Jersey Gas Company 1 South Jersey Plaza Folsom, NJ 08037 (609) 561-9000 | New Jersey | 21-0398330 | |||

| None | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act:

South Jersey Industries, Inc.: Yes x No o

South Jersey Gas Company: Yes oNo x

Indicate by check mark if theeach registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Act: Yes oNo x

Indicate by check mark whether theeach registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that theeach registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes xNo o

Indicate by check mark whether theeach registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that theeach registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’sregistrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

South Jersey Industries, Inc.: o

South Jersey Gas Company: x

Indicate by check mark whether theeach registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.filer, smaller reporting company, or an emerging growth company. See definitionthe definitions of “accelerated filer” and “large accelerated filer”filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| South Jersey Industries, Inc.: | ||

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o |

Smaller reporting company o | Emerging growth company o | |

| South Jersey Gas Company: | ||

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer x | ||

Smaller reporting company o | Emerging growth company o | |

Indicate by check mark whether any of the registrant isregistrants are a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes oNo x

Documents Incorporated by Reference: None

In Part III of Form 10-K: Portions of South Jersey Industries, Inc.'s definitive proxy statement for its 2018 annual meeting of shareholders to be filed with the Securities and Exchange Commission are incorporated by reference into Part III of this Form 10-K.

EXPLANATORY NOTE:

South Jersey Industries, Inc. (the “Company”) filed its Annual Report on Form 10-K for the fiscal year ended December 31, 2017 (the “Original Filing”) with the U.S. Securities and Exchange Commission (the “SEC”) on February 26, 2018 as part of a combined report also filed separately by its wholly-owned subsidiary, South Jersey Gas Company. The Company is filing this Amendment No. 1 (this “Amendment”) to the Original Filing solely to correct three typographical errors as follows:

1) A date contained in the REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM related to its Opinion on the Financial Statements of the Company and its subsidiaries, as shown on page 145 of the Original Filing. In that report, the date cross-referencing the accounting firm’s Opinion on Internal Control over Financial Reporting was inadvertently referenced as February 23, 2018. The correct date of the Opinion on Internal Control over Financial Reporting is February 26, 2018. That error has been corrected in this Amendment.

2) A date contained in the REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM related to its Opinion on Internal Control over Financial Reporting of the Company and its subsidiaries, as shown on page 150 of the Original Filing. In that report, the date cross-referencing the accounting firm’s Opinion on the Financial Statements was inadvertently referenced as February 23, 2018. The correct date of the Opinion on the Financial Statements is February 26, 2018. That error has been corrected in this Amendment.

3) A date contained in the REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM related to its Opinion on the Financial Statement Schedules of the Company, as shown on page 159 of the Original Filing. In that report, the date cross-referencing the accounting firm’s Opinion on the Financial Statements as well as its Opinion on Internal Control over Financial Reporting was inadvertently referenced as February 23, 2018. The correct date of the Opinion on the Financial Statements as well as the Opinion on Internal Control over Financial Reporting is February 26, 2018. That error has been corrected in this Amendment.

In addition, pursuant to the rules of the SEC, the exhibit list included in Item 15 of Part IV of the Original Filing has been amended to contain currently-dated certifications from the Principal Executive Officer and Chief Financial Officer of each of the Company and South Jersey Gas Company, as required by Sections 302 and 906 of the Sarbanes-Oxley Act of 2002. The certifications of the Company's Chief Executive Officer and Chief Financial Officer are attached as exhibits to this Amendment.

Except as described above, this Amendment does not amend or update any other information contained in the Original Filing. For ease of reference, the Company has included a complete copy of the Original Filing, amended as described above, in this Amendment.

TABLE OF CONTENTS

| Page No. | ||

| PART I | ||

| Item 4A. | ||

| PART II | ||

| South Jersey Industries, Inc. | ||

| South Jersey Gas Company | ||

| Item 9. | ||

| PART III | ||

| PART IV | ||

INTRODUCTION

FILING FORMAT

This Annual Report on Form 10-K is a combined report being filed separately by two registrants: South Jersey Industries, Inc. (SJI) and South Jersey Gas Company (SJG). Information relating to SJI or any of its subsidiaries, other than SJG, is filed by SJI on its own behalf. SJG is only responsible for information about itself.

Except where the content clearly indicates otherwise, any reference in the report to "SJI," "the Company," "we," "us" or "our" is to SJI and all of its subsidiaries, including SJG, which is a wholly-owned subsidiary of SJI.

Management's Discussion and Analysis of Financial Condition and Results of Operations (Management's Discussion) included under Item 7 is divided into two major sections: SJI and SJG. Financial information in this Annual Report on Form 10-K included in Item 8 includes separate financial statements (i.e., statements of income, statements of comprehensive income, statements of cash flows, balance sheets, and statements of changes in equity and comprehensive income) for SJI and SJG. The Notes to Consolidated Financial Statements are presented on a combined basis for both SJI and SJG.

Forward Looking Statements

Certain statements contained in this Annual Report on Form 10-K may qualify as “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements in this Report other than statements of historical fact, included in this Reportincluding statements regarding future results of operations or financial position, expected sources of incremental margin, strategy, financing needs, future capital expenditures and the outcome or effect of ongoing litigation, should be considered forward-looking statements made in good faith by South Jersey Gas Company (SJGIndustries (SJI or the Company) and South Jersey Gas Company (SJG), as applicable, and are intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. When used in this Report, or any other of the Company’s documents or oral presentations, words such as “anticipate,” “believe,” "estimate," “expect,” “estimate,” “forecast,” “goal,” “intend,” “objective,” “plan,” “project,” “seek,” “strategy”“strategy,” "target," "will" and similar expressions are intended to identify forward-looking statements. These forward-looking statements are based on the beliefs and assumptions of management at the time that these statements were made and are inherently uncertain. Such forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements. These risks and uncertainties include, but are not limited to the risks set forth under “Risk Factors” in Part I, Item 1A of this Report and elsewhere throughout this Report. These cautionary statements should not be construed by you to be exhaustive and they are made only as of the date of this Report. While the Company believes these forward-looking statements to be reasonable, there can be no assurance that they will approximate actual experience or that the expectations derived from them will be realized. Further, neither SJI nor SJG undertakes no obligation to update or revise any of its forward-looking statements whether as a result of new information, future events or otherwise.

Available Information

| Units of Measurement | ||

| For Natural Gas: | ||

| 1 | = One billion cubic feet | |

| 1dt | = One decatherm | |

| 1 | = One million decatherms | |

| dts/d | = Decatherms per day | |

| MDWQ | = Maximum daily withdrawal quantity | |

| For Electric: | ||

| 1 MMmwh | = One million megawatt hours | |

| 1 mwh | = One megawatt hour | |

South Jersey Industries, Inc.

Part I

PART I

Item 1. Business

Description of Business

South Jersey Industries, Inc. (SJI or the Company), a New Jersey corporation, was formed in 1969 for the purpose of owning and holding all of the outstanding common stock of South Jersey Gas Company, a public utility, and acquiring and developing non-utility lines of business.

SJI currently provides a variety of energy-related products and services, primarily through the following wholly-owned subsidiaries:

South Jersey Gas Company (SJG) is a regulated natural gas utility. SJG distributes natural gas in the seven southernmost counties of New Jersey.

South Jersey Energy Company (SJE) acquires and markets natural gas and electricity to retail end users and provides total energy management services to commercial, industrial and residential customers.

South Jersey Resources Group, LLC (SJRG) markets natural gas storage, commodity and transportation assets along with fuel management services on a wholesale basis in the mid-Atlantic, Appalachian and southern states.

South Jersey Exploration, LLC (SJEX) owns oil, gas and mineral rights in the Marcellus Shale region of Pennsylvania.

Marina Energy, LLC (Marina) develops and operates on-site energy-related projects. It currently operates projects in New Jersey, Maryland, Massachusetts and Vermont. The significant wholly-owned subsidiaries of Marina include:

ACB Energy Partners, LLC (ACB) owns and operates a natural gas fueled combined heating, cooling and power facility located in Atlantic City, New Jersey.

AC Landfill Energy, LLC (ACLE), BC Landfill Energy, LLC (BCLE), SC Landfill Energy, LLC (SCLE) and SX Landfill Energy, LLC (SXLE) own and operate landfill gas-to-energy production facilities in Atlantic, Burlington, Salem and Sussex Counties in New Jersey.

MCS Energy Partners, LLC (MCS), NBS Energy Partners, LLC (NBS) and SBS Energy Partners, LLC (SBS) own and operate solar-generation sites located in New Jersey.

South Jersey Energy Service Plus, LLC (SJESP) serviced residential and small commercial HVAC systems, installed small commercial HVAC systems, provided plumbing services and serviced appliances under warranty via a subcontractor arrangement as well as on a time and materials basis. On September 1, 2017, SJESP sold certain assets of its residential and small commercial HVAC and plumbing business to a third party. SJESP will receive commissions paid on service contracts from the third party on a go forward basis. This transaction did not have a material impact on the consolidated financial statements.

SJI Midstream, LLC (Midstream) invests in infrastructure and other midstream projects, including a current project to build an approximately 118-mile natural gas pipeline in Pennsylvania and New Jersey.

In October 2017, SJI announced that it had entered into agreements to acquire the assets of Elizabethtown Gas and Elkton Gas from Pivotal Utility Holdings, Inc., a subsidiary of Southern Company Gas. SJI is acquiring the assets of both companies for total consideration of $1.7 billion. The transaction is expected to close in mid-2018, and is subject to approvals by the New Jersey Board of Public Utilities (BPU) and the Maryland Public Service Commission (PSC), with limited approvals also required from the Federal Energy Regulatory Commission (FERC) and the Federal Communications Commission (FCC), as well as certain anti-trust filings and approvals.

Additional informationInformation on the nature of our business is incorporated by reference to “Management’sSJI's and SJG's businesses can be found in “Management's Discussion and Analysis of Financial Condition and Results of Operations,” “Market Risk” and Note 3 to the financial statements.under Item 7 of this Report.

South Jersey Industries, Inc.

Part I

Financial Information About Reportable Segments

Information on our rates and regulatory affairsregarding Reportable Segments is incorporated by reference to “Management’s Discussion and AnalysisNote 8 of Financial Condition and Resultsthe consolidated financial statements included under Item 8 of Operations,” and Note 3 to the financial statements.this Report.

Sources and Availability of Raw Materials

South Jersey Gas Company

Transportation and Storage Agreements

SJG has direct connections to the interstate pipeline systems of both Transcontinental Gas Pipe Line Company, LLC (Transco) and Columbia Gas Transmission, LLC (Columbia). During 2015,2017, SJG purchased and had delivered approximately 44.8 million decatherms (MMdts)55.4 MMdts of natural gas for distribution to both on-system and off-system customers and for injections into storage. Of this total, 28.131.9 MMdts were transported on the Transco pipeline system while 16.723.5 MMdts were transported on the Columbia pipeline system. Moreover,Also during 20152017, third-party suppliers delivered 30.427.4 MMdts to SJG's system on behalf of end use customers behind ourSJG's city gate stations. SJG also secures other long-term services from Dominion Transmission, Inc. (Dominion), a pipeline upstream of the Transco and Columbia systems. Services provided by Dominion are utilized to deliver gas into either the Transco or Columbia systems for ultimate delivery to SJG. In addition, effective December 1, 2017, SJG initiated a new firm transportation service with Tennessee Gas Pipeline Company, L.L.C. (Tennessee). Gas transported by Tennessee will be delivered to the Columbia system for subsequent delivery to SJG. Services provided by all of the above-mentioned pipelines are subject to the jurisdiction of the Federal Energy Regulatory Commission (FERC). Unless otherwise indicated, our intentions are to renew or extend these service agreements before they expire.

Transco:

Transco is SJG’sSJG's largest supplier of long-term gas transmission services which includes both year-round and seasonal firm transportation (FT) service arrangements. When combined, these FT services enable SJG to purchase gas from third parties and have delivered to its city gate stations by Transco a total of 297,958 dts per day (dts/d). Of this total, 133,917 dts/d is long-haul FT (where gas can be transported from the production areas of the Southwest to the market areas of the Northeast) while 164,041 dts/d is market area FT. The terms of SJG’sSJG's year-round agreements with Transco extend for various periods through 2025. SJG's seasonalCertain of these agreements are currently operating under their respective evergreen provisions.

Of the 297,958 dts/d of Transco services mentioned above, SJG has released a total of 49,04110,000 dts/d of its long-haul and 20,000 dts/d of its market area FT service. These releases were made in association with SJG’sSJG's Conservation Incentive Program (CIP) discussed further under Item 7, "Management’s"Management's Discussion and Analysis of Financial Condition and Results of Operations." In addition, SJG released a total of 50,00035,000 dts/d of its long-haul FT and 5,000 dts/d of its market area FT as part of Asset Management Agreements (AMA). The AMA-related releases are discussed below under “Gas Supplies.” In addition, SJG released a total of 30,000 dts/d of its long-haul FT as an Off-System Sale capacity release.

SJG currently has six long-term gas storage service agreements with Transco that, when combined, are capable of storing approximately 5.0 MMdts. Through these agreements, SJG can inject gas into market and production area storages during periods of low demand and extract gas at a Maximum Daily Withdrawal Quantity (MDWQ) of up to 107,407 dts during periods of high demand. The longest term of these storage service agreements extends through March 31, 2023.

Dominion:

SJG subscribes to a firm storage service from Dominion, under its Rate Schedule GSS. This storage has an MDWQ of 10,000 dts during the period between November 16 and March 31 of each winter season, with an associated total storage capacity of 423,000 dts. Gas withdrawn from Dominion GSS storage is delivered through both the Dominion and Transco (Leidy Line) pipeline systems for delivery to SJG service territory. The primary term of this agreement extends through March 31, 2019.

Columbia:

SJG subscribes to four firm transportation agreements with Columbia which currently provide for an aggregate of 104,022124,022 dts/d with thed. The term of 9,000 dts/d of this capacity extendingextends through October 31, 2017 while2022; the term of 45,022 dts/d of this deliverability extends through October 31, 2019. The2019; and the remaining 50,00070,000 dts/d continuesextends through October 31, 2030. SJG released 8,671 dts/d of this amount to

South Jersey Resources Group, LLC (SJRG), an affiliate by common ownership, in conjunction with its Conservation Incentive Program ("CIP") thereby reducing the combined availability of firm transportation on the Columbia system to 95,351 dts/d. In addition, SJG released a total of 20,000 dts/d of this capacity to a gas marketer as part of an AMA leaving a net of 75,351 dts/d available to SJG. This AMA-related release is further discussed below under “Gas Supplies.”Industries, Inc.

Part I

SJG also subscribes to a firm storage service with Columbia under its Rate Schedule FSSFederal Supply Schedule (FSS) along with an associated firm transportation service under Rate Schedule SST, each of which extends through October 31, 2019. The CompanySJG has a total FSS MDWQ of 52,891 dts and a related 3,473,022 dts of storage capacity. SJG released to SJRG 19,029 dts/d of its FSS MDWQ along with 1,249,485 dts of its FSS storage capacity. Additionally, SJG released to SJRG 19,029 dts/d of its associated Columbia SST transportation service. Both releases made by SJG were in connection with its CIP and extend through September 30, 2016.2018.

Gas Supplies

During 2015,2017, SJG entered into an AMA with a gas marketer which extends through March 31, 2016.2018. Under this agreement, SJG released to the marketer its firm transportation rights equal to 30,000 dts/d of transportation capacity on Transco. The marketer manages this capacity and provides SJG with up to 30,000 dts/d of firm deliverability each day through March 31, 2016.2018. The marketer's intent was to optimize the capacity released to themSJG under this AMA and pay SJG a monthlyan asset management fee.

Also during 2015,2017, SJG entered into twoan additional AMA'sAMA with twoa separate gas marketersmarketer which both extendextends through October 31, 2016.2018. Under these agreements,this agreement, SJG has released to each of the marketers firm transportation rights equal tomarketer 10,000 dts/d of its firm transportation capacity on Transco.rights. As part of this transition the total quantity is split into two arrangements of 5,000 dts/d each under a separate Transco contract. The marketersmarketer manages their respectiveits capacity and provideprovides SJG with up to 10,000 dts/d each of firm deliverability every dayeveryday through March 31, 2018 in one case and through October 31, 2016. The marketers will seek2018 as to optimize the capacity released to them under these AMA's and pay SJG a one-time asset management fee.

SJG also has a long-term gas purchase agreement with an additional gas producer, with a primary term which extends ten years. The MDQ available for purchase under this agreement has started, effective December 1, 2017, at 55,000 dts/d and will increase to an MDQ of 70,000 dts/d. Gas purchased from this producer will be sourced in Northeast Pennsylvania and delivered into the Columbia pipeline system for delivery to SJG.

As part of its gas purchasing strategy, SJG uses financial contracts to hedge against forward price risk. These contracts are recoverable through SJG’s BGSS,Basic Gas Supply Service Clause (BGSS), subject to the New Jersey Board of Public Utilities (BPU) approval.

Supplemental Gas Supplies

SJG operates peaking facilities, which can storelocated in McKee City, NJ, where it liquefies, stores and vaporize LNGvaporizes liquefied natural gas (LNG) for injection into its distribution system. SJG’sSJG's LNG facility has a storage capacity equivalent to 434,300 dts of natural gas and has an installed capacity to vaporize up to 118,250 dts of LNG per day for injection into its distribution system.

Peak-Day Supply

SJG plans for a winter season peak-day demand on the basis of an average daily temperature of 2 degrees Fahrenheit (F). or 63 Heating Degree Days. Gas demand on such a design day for the 2015-20162017-2018 winter season is estimated to be 503,873527,490 dts (excluding industrial customers). SJG projects that it has adequate supplies and interstate pipeline entitlements to meet its design day requirements. SJG experienced its highest peak-day demand for calendar year 20152017 of 507,219480,820 dts (including industrial customers) on February 15,December 31, while experiencing an average temperature of 10.112.9 degrees F that day.

Natural Gas Prices

South Jersey Industries, Inc.

Part I

South Jersey Energy Company

Transportation and Storage Agreements - Natural Gas

Access to gas suppliers and cost of gas are significant to the operations of SJE. No material part of the business of SJE is dependent upon a single customer or a few customers. SJE purchases delivered gas only, primarily from SJRG. Consequently, SJE maintains no transportation or storage agreements.

Electric Supply

Due to the liquidity in the market, SJE primarily purchases delivered electric in the day-ahead and real-time markets through regional transmission organizations.

South Jersey Resources Group

Transportation and Storage Agreements

National Fuel Gas Supply Corporation:

SJRG has multiple storage service agreements with National Fuel Gas Supply Corporation (National Fuel). Two contracts totaling 2,581,420 dts of capacity have evergreen provisions that extend year to year. One additional contract covering 224,576 dts of storage capacity extends through March 31, 2020, while a final contract covering 150,040 dts of capacity expires March 31, 2023.

SJRG holds long-term firm transportation agreements with National Fuel associated with the above-mentioned agreements which expire between January 31, 2022 and October 31, 2027. Under these agreements, National Fuel provides various receipts and deliveries in Pennsylvania, which total 66,682 dts/d. National Fuel will also provide SJRG with 25,661 dts/d of maximum daily withdrawal transportation quantity, with a primary delivery point of the Transcontinental Gas Pipeline.

Transcontinental Gas Pipeline (Transco):

SJRG has a storage agreement with Transco for storage service at Transco's WSS facility which expires October 31, 2018. Under this contract, up to 24,479 dts/d may be injected and up to 46,380 dts/d may be withdrawn. Total storage capacity under the agreement is 4,406,135 dts.

SJRG holds various firm transportation agreements with Transco. SJRG has 10,000 dts/d of capacity from Leidy, PA to Con Edison, NY expiring March 31, 2043. SJRG also holds evergreen capacity of 41,400 dts/d with receipts in Texas and deliveries in New Jersey, which also expires March 31, 2043.

SJRG has transportation agreements with Transco acquired through a capacity release program from SJG of 47,500 dts/d from Pennsylvania to SJG, and 10,000 dts/d from Texas to SJG. These agreements expire between March 31, 2018 and April 30, 2020.

Dominion Gas Transmission:

SJRG has a firm transportation agreement with Dominion which expires October 31, 2022. Under this agreement, Dominion will provide SJRG with 5,000 dts/d of deliveries to Leidy, PA and receipts at Lebanon, OH.

Columbia Gas Transmission:

SJRG holds various firm transportation agreements with Columbia. SJRG has 50,000 dts/d capacity with receipts from Marcellus to southern NJ expiring October 31, 2018. SJRG also has 36,866 dts/d of capacity from Marcellus to southern NJ and PA expiring between October 31, 2019 and October 31, 2024.

South Jersey Industries, Inc.

Part I

SJRG has a storage agreement with Columbia for service under Columbia's FSS rate schedule. Under this evergreen agreement, Columbia will provide SJRG with storage capacity of 1,249,515 dts. Under this agreement, 19,029 dts/d may be withdrawn from storage and 9,514 dts/d may be injected.

SJRG holds firm transportation related to the above mentioned storage agreement which provides for receipts from storage and deliveries to New Jersey of 19,029 dts/d. Under this evergreen contract, these services with Columbia were released to SJRG by SJG.

Columbia Gulf Transmission:

SJRG holds a firm transportation agreement with Columbia Gulf which expires October 31, 2019. Under this agreement, Columbia Gulf provides receipts in Louisiana with deliveries at Leach, Kentucky in the amount of 15,000 dts/d.

Tennessee Gas Transmission:

SJRG holds firm transportation agreements with the Tennessee Gas Pipeline which expire between October 31, 2018 and May 31, 2033. Under these agreements, the Tennessee Gas Pipeline provides various receipts and deliveries in Pennsylvania, which total 199,770 dts/d.

Texas Eastern Transmission (Tetco):

SJRG holds firm transportation agreements with Tetco. SJRG has an agreement for Tetco to provide 56,250 dts/d of capacity expiring October 31, 2025, and an additional evergreen contract of 15,125 dts/d of capacity expiring March 31, 2019.

Gas Supplies

SJRG has entered into several long-term natural gas supply agreements to purchase a minimum of 604,000 dts/d and up to 954,000 dts/d, depending upon production levels, for terms ranging from three to ten years at index-based prices.

Patents and Franchises

South Jersey Gas Company

SJG holds nonexclusive franchises granted by municipalities in the seven-county area of southern New Jersey that it serves. No other natural gas public utility presently serves the territory covered by SJG’sSJG's franchises. Otherwise, patents, trademarks, licenses, franchises and concessions are not material to the business of SJG.

Seasonal Aspects

South Jersey Gas Company

SJG experiences seasonal fluctuations in sales when selling natural gas for heating purposes. SJG meets this seasonal fluctuation in demand from its firm customers by buying and storing gas during the summer months, and by drawing from storage and purchasing supplemental supplies during the heating season. As a result of this seasonality, SJG’sSJG's revenues and net income are significantly higher during the first and fourth quarters than during the second and third quarters of the year.

Non-Utility Companies

Among SJI's non-utility activities, wholesale (including fuel supply management) and retail gas marketing have seasonal patterns similar to SJG's. Activities such as energy services and energy project development do not follow seasonal patterns. Other activities, such as retail electric marketing, can have seasonal earnings patterns that are different from the utility. The first and fourth quarters remain the periods where most of SJI's revenue and net income is produced.

South Jersey Industries, Inc.

Part I

Working Capital Practices

Reference is made to “Liquidity and Capital Resources” included in Item 7, “Management’s“Management's Discussion and Analysis of Financial Condition and Results of Operations,” of this Report.

Customers

No material part of SJG’sthe Company's business is dependent upon a single customer or a few customers, the loss of which would be expected to have a material adverse effect on SJG’s business.the results of operations of SJI or of SJG on a consolidated basis.

Backlog

Backlog is not material to an understanding of SJG’s business.SJI's business or that of any of its subsidiaries.

Government Contracts

No material portion of SJG’sthe business of SJI or any of its subsidiaries is subject to renegotiation of profits or termination of contracts or subcontracts at the election of any government.

Competition

Information on competition is incorporated by reference tofor SJI and its subsidiaries can be found in Item 7, “Management’s“Management's Discussion and Analysis of Financial Condition and Results of Operations,” of this Report.

Research

During the last three fiscal years, SJG did not engageneither SJI nor any of its subsidiaries engaged in research activities to any material extent.

Environmental Matters

Information on environmental matters for SJI and its subsidiaries can be found in Note 1215 of the consolidated financial statements.statements included under Item 8 of this Report.

Employees

Financial Information About Foreign and Domestic Operations and Export Sales

South Jersey Industries, Inc.

Part I

Item 1A. Risk Factors

SJI and its subsidiaries, including SJG, operatesoperate in an environment that involves risks, many of which are beyond our control. The CompanySJI has identified the following risk factors that could cause the Company’sSJI's operating results and financial condition to be materially adversely affected. Security holders should carefully consider these risk factors and should also be aware that this list is not all-inclusive of existing risks. In addition, new risks may emerge at any time, and the CompanySJI cannot predict those risks or the extent to which they may affect the Company’sSJI's businesses or financial performance. To the extent such risk factors may affect SJI's utility business, SJG, such risk factors may also affect SJG's business or performance.

SJI is a holding company and its assets consist primarily of investments in subsidiaries. Should SJI's subsidiaries be unable to pay dividends or make other payments to SJI for financial, regulatory, legal or other reasons, SJI's ability to pay dividends on its common stock could be limited. SJI's stock price could be adversely affected as a result.

Changes in the regulatory environment or unfavorable rate regulation at its utility may have an unfavorable impact on SJG’sSJI's and SJG's financial performance or condition. SJG’s businessSJG is regulated by the New Jersey Board of Public Utilities (BPU) which has authority over many of the activities of the utility business including, but not limited to, the rates it charges to its customers, the amount and type of securities it can issue, the nature of investments it can make, the nature and quality of services it provides, safety standards and other matters. The extent to which the actions of regulatory commissions restrict or delay SJG’sSJG's ability to earn a reasonable rate of return on invested capital and/or fully recover operating costs may adversely affect itsSJI's and SJG's results of operations, financial condition and cash flows.

SJI and SJG may not be able to respond effectively to competition, which may negatively impact SJG’stheir financial performance or condition.Regulatory initiatives may provide or enhance opportunities for competitors that could reduce utility income obtained from existing or prospective customers. Also, competitors in all of SJI's business lines may be able to provide superior or less costly products or services based upon currently available or newly developed technologies.

Warm weather, high commodity costs, or customer conservation initiatives could result in reduced demand for natural gas.some of SJI's and SJG's energy products and services. SJG currently has a conservation incentive program clause that protects its revenues and gross margin against usage that is lower than a set level. Should this clause be terminated without replacement, lower customer energy utilization levels would likely reduce SJG’sSJI's and SJG's net income. Further, during periods of warmer temperatures, demand and volatility in the natural gas market could decrease, which would negatively impact their financial results.

High natural gas prices could cause more of SJG’sSJI's and SJG's receivables to be uncollectible.Higher levels of uncollectibles from utilityeither residential or commercial customers would negatively impact SJG’sSJI's and SJG's income and could result in higher working capital requirements.

Climate change legislation could impact SJG’sSJI's and SJG's financial performance and condition. Climate change is receiving ever increasing attention from both scientists and legislators. The debate is ongoing as to the extent to which our climate is changing, the potential causes of this change and its future impacts. Some attribute global warming to increased levels of greenhouse gases, which has led to significant legislative and regulatory efforts to limit greenhouse gas emissions. The outcome of federal and state actions to address global climate change could result in a variety of regulatory programs, including additional charges to fund energy efficiency activities or other regulatory actions. These actions could affect the demand for natural gas and electricity, result in increased costs to our business and impact the prices we charge our customers. Because natural gas is a fossil fuel with low carbon content, it is possible that future carbon constraints could create additional demands for natural gas, both for production of electricity and direct use in homes and businesses. Any adoption by federal or state governments mandating a substantial reduction in greenhouse gas emissions could have far-reaching and significant impacts on the energy industry. We cannot predict the potential impact of such laws or regulations on our future consolidated financial condition, results of operations or cash flows.

Increasing interest rates would negatively impact the net income of SJI and SJG. Several of SJI's subsidiaries, including SJG, are capital intensive, resulting in the securityincurrence of significant amounts of debt financing. Some of the long-term debt of SJI and its subsidiaries is issued at fixed rates or has utilized interest rate swaps to mitigate changes in variable rates. However, long-term debt of SJI and SJG at variable rates, along with all variable rate short-term borrowings, are exposed to the impact of rising interest rates.

The inability to obtain capital, particularly short-term capital from commercial banks, could negatively impact the daily operations and financial performance of SJI and SJG. SJI and SJG use short-term borrowings under committed credit facilities provided by commercial banks to supplement cash provided by operations, to support working capital needs, and to finance capital expenditures, as incurred. SJG also relies upon short-term borrowings issued under a commercial paper program supported by a committed bank credit facility to support working capital needs, and to finance capital expenditures, as incurred. If the customary sources of short-term capital were no longer available due to market conditions, SJI and its subsidiaries may not be able to meet their working capital and capital expenditure requirements and borrowing costs could increase.

A downgrade in either SJI's or SJG's credit ratings could negatively affect our computer systems through cyberattacks, hackers or other sources, could haveability to access adequate and cost-effective capital. Our ability to obtain adequate and cost-effective capital depends to a material adverse impactsignificant degree on our businesscredit ratings, which are greatly influenced by our financial condition and results of operations. SJG uses computer systems and services that involve If the storage of confidential information onrating agencies downgrade either SJI's or SJG's credit ratings, particularly below investment grade, our employees, customers and vendors.borrowing costs would increase. In addition, we would likely be required to pay higher interest rates in future financings and potential funding sources would likely decrease. To the extent that a decline in SJG's credit rating has a negative effect on SJI, SJI could be required to provide additional support to certain computer systems monitorcounterparties.

Hedging activities of the Company designed to protect against commodity price or interest rate risk may cause fluctuations in reported financial results and control our distribution processes. Experienced hackers maySJI's stock price could be ableadversely affected as a result. Although SJI enters into various contracts to develop and deploy viruses that exploithedge the securityvalue of our computer systems and thusenergy assets, liabilities, firm commitments or forecasted transactions, the timing of the recognition of gains or losses on these economic hedges in accordance with accounting principles generally accepted in the United States of America does not always match up with the gains or losses on the items being hedged. The difference in accounting can result in volatility in reported results, even though the expected profit margin is essentially unchanged from the dates the transactions were consummated.

The inability to obtain confidential information and/natural gas or disrupt significant business processes. Unauthorized access to confidential information or disruptions to significant business processes could damage our reputation andelectricity from suppliers would negatively impact ourthe financial performance of SJI and SJG. Several of SJI's subsidiaries, including SJG, have businesses based upon the ability to deliver natural gas or electricity to customers. Disruption in the production or transportation to SJI or SJG from its suppliers could prevent SJI or SJG from completing sales to its customers.

South Jersey Industries, Inc.

Part I

Transporting and storing natural gas involves numerous risks that may result in accidents and other operating risks and costs. SJI's and SJG's gas distribution activities involve a variety of inherent hazards and operating risks, such as leaks, accidents, mechanical problems, natural disasters or terrorist activities which could cause substantial financial losses. In addition, these risks could result in loss of human life, significant damage to property, environmental pollution and impairment of operations, which in turn could lead to substantial losses. In accordance with customary industry practice, SJI and SJG maintain insurance against some, but not all, of these risks and losses. The occurrence of any of these events, even if fully covered by insurance, could adversely affect SJI's or SJG's financial position, results of operations and financial condition.cash flows.

Adverse results in legal proceedings could be detrimental to the financial condition of SJI or SJG. The outcomes of legalproceedings can be unpredictable and can result in adverse judgments.

Renewable energy projects at Marina receive significant benefit from regulatory incentives. A significant portion of the expected return on investment of these renewable energy projects is dependent upon the future market for renewable energy credits (RECs). The benefits from RECs are produced during the entire life of the project. As a result, earnings from existing projects would be adversely affected without a liquid REC market. Therefore, these projects are exposed to the risk that favorable regulatory incentives expire or are adversely modified. A decrease in the future value of electricity and Solar RECs (SRECs) impacted by market conditions and/or legislative changes may negatively impact Marina's return on its investments as well as lead to impairment of the respective assets.

Constraints in available pipeline capacity, particularly in the Marcellus Shale producing region, may negatively impact SJI's financial performance. Natural gas production and/or pipeline transportation disruptions in the Marcellus region, where SJI has natural gas receipt requirements, may cause temporary take-away constraints resulting in higher transportation costs and the sale of shale gas at a loss.

SJI's and SJG's business could be adversely impacted by strikes or work stoppages by its unionized employees.employees. The gas utility operations of SJG are dependent upon employees represented by unions and covered under collective bargaining agreements. A work stoppage could negatively impact operations, which could impact financial results as well as customer relationships.

The risk of terrorism may adversely affect the economy as well as SJI's and SJG's business. An act of terror could result in disruptions of natural gas supplies cause price volatility in the cost of natural gas and overall could cause instability in the financial and capital markets. This could adversely impact SJI's or SJG's ability to deliver products or raise capital and could adversely impact its results of operations.

Failure to obtain proper approvals and property rights in the pricePennEast pipeline could hinder SJI's equity investment in the project. Construction, development and availabilityoperation of energy investments, specifically the PennEast pipeline, are subject to federal and state regulatory oversight and require certain property rights from public and private property owners, as well as regulatory approvals, including environmental and other permits and licenses. SJI, as well as our joint venture partners in the PennEast pipeline, may be unable to obtain all such needed property rights, permits and licenses to successfully construct and develop the pipeline, and failing to do so could cause SJI's equity investment in the project to become impaired. Such impairment could have a materially adverse effect on SJI's financial condition and results of operations.

Our business could be harmed by cybersecurity threats and related disruptions. We rely extensively on information technology systems to process transactions, transmit and store information and manage our business. Disruption or failure of our information technology systems could shut down our facilities or otherwise harm our ability to safely deliver natural gas to our customers, serve our customers effectively, manage our assets, or otherwise materially disrupt our business. Cyber threats are constantly evolving, increasing the difficulty of detecting and successfully defending against them. SJI and SJG have experienced such attacks in the past; however, based on information currently available to SJI and SJG, none have had a material impact on our business, financial condition, results of operations or cash flows. In response, we have invested in expanded cybersecurity systems and procedures designed to safeguard the continuous and uninterrupted performance of our information technology systems and protect against unauthorized access. However, all information technology systems are potentially vulnerable to security threats, including hacking, viruses, other malicious software, and other unlawful attempts to disrupt or gain access to such systems. There is no guarantee that our cybersecurity systems and procedures will prevent or detect the unauthorized access by experienced computer programmers, hackers or others. An attack on or failure of our information technology systems could result in the unauthorized disclosure, theft, misuse or destruction of customer or employee data or business or confidential information, or disrupt the performance of our information technology

South Jersey Industries, Inc.

Part I

systems. These events could expose us to potential liability, litigation, governmental inquiries, investigations or regulatory actions, harm our brand and reputation, diminish customer confidence, disrupt operations, and subject us to payment of fines or other penalties, legal claims by our clients and significant remediation costs.

Our stated long-term goals are based on various assumptions and beliefs that may not prove to be accurate, and we may not achieve our stated long-term goals by 2020 or at all. Our current long-term goals are to (i) grow Economic Earnings to $160 million by 2020; (ii) improve the quality of our earnings; (iii) maintain the strength of our balance sheet; and (iv) maintain a low-to-moderate risk profile. The goal of $160 million does not include the expected financial impact of the acquisition of Elizabethtown Gas and Elkton Gas discussed below. Management established those goals in conjunction with our board of directors based upon a number of different internal and external factors that characterize and influence our current and expected future activities. For example, these long-term goals are based on certain assumptions regarding our participation in a current project to build an approximately 118-mile natural gas pipeline in Pennsylvania and New Jersey. However, construction on this project is not expected to begin until 2018 and is estimated to be completed in the second half of 2019, but may be subject to delay. As a result, no assurance can be given that this project will be completed on time or at all. Also, as noted below, the acquisition of Elizabethtown Gas and Gas is subject to many approvals, and no assurance can be given that the acquisition will be consummated, or, if consummated, that these two entities will perform as expected. Further, the economy of Southern New Jersey has remained depressed relative to other regions, which could cause increased customer delinquencies or otherwise negatively affect achievement of our long-term earnings goals. The 2017 New Jersey gubernatorial election resulted in a change in administration which could lead to unfavorable state and local regulatory changes that could delay approvals, require environmental remediation or capital or other expenditures or otherwise adversely affect SJG'sour results of operations, financial condition or cash flows. Other factors, assumptions and beliefs of management and our board of directors on which our long-term goals were based may also prove to differ materially from actual future results. Accordingly, we may not achieve our stated long-term goals by 2020 or at all, or our stated long-term goals may be negatively revised as a result of less than expected progress toward achieving these goals, and you are therefore cautioned not to place undue reliance on these goals.

Our acquisition of Elizabethtown Gas and Elkton Gas may not be consummated, and if consummated, may not perform as expected. Wehave entered into agreements to acquire the assets of New Jersey-based Elizabethtown Gas and Maryland-based Elkton Gas. Completion of the transaction is subject to a number of risks and uncertainties and we can provide no assurance that the various closing conditions to the acquisition agreement will be satisfied, including that the required governmental and other necessary approvals will be obtained. Although we have obtained a bridge commitment, subject to certain conditions, to fund the acquisition, our ability to raise the necessary funds to provide permanent financing through the issuance of equity or debt securities is subject to market conditions and other risks and uncertainties, and there can be no assurance that we will be able to raise the necessary funds on terms we consider favorable, or at all. The inability to complete the transaction, or to obtain permanent financing on terms that are favorable, or at all, could have a material adverse effect on our results of operations, financial condition and prospects. Historically, acquisitions have not been a part of our growth strategy. Although the acquired businesses have significant operating histories, we will have no history of owning and operating these businesses and limited or no experience operating in the territories served by these businesses. We can provide no assurance that the acquired businesses will perform as expected, that integration or other one-time costs will not be greater than expected, that we will not incur unforeseen obligations or liabilities or that the rate of return from such businesses will justify our decision to invest capital to acquire them.

We may experience difficulties in integrating the operations of Elizabethtown Gas and Elkton Gas into our business and in realizing the expected benefits of the proposed acquisition. The success of the proposed acquisition of Elizabethtown Gas and Elkton Gas, if completed, will depend in part on our ability to realize the anticipated business opportunities from combining the operations of Elizabethtown Gas and Elkton Gas with our business in an efficient and effective manner. The integration process could take longer than anticipated and could result in the loss of key employees, the disruption of each company’s ongoing businesses, tax costs or inefficiencies, or inconsistencies in standards, controls, information technology systems, procedures and policies, any of which could adversely affect our ability to maintain relationships with customers, employees or other third parties, or our ability to achieve the anticipated benefits of the transaction, and could harm our financial performance. If we are unable to successfully or timely integrate the operations of Elizabethtown Gas and Elkton Gas with our business, we may incur unanticipated liabilities and be unable to realize the revenue growth, synergies and other anticipated benefits resulting from the proposed transaction, and our business, results of operations and ability to raise capital.financial condition could be materially and adversely affected.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The principal property of SJGSJI consists of itsSJG's gas transmission and distribution systems that include mains, service connections and meters. The transmission facilities carry the gas from the connections with Transco and Columbia to SJG’sSJG's distribution systems for delivery to customers. As of December 31, 2015,2017, there were approximately 122.7146.2 miles of mains in the transmission systems and 6,5036,645 miles of mains in the distribution systems.

SJG owns approximately 154 acres of land in Folsom, New Jersey which is the site of itsSJI's corporate headquarters. Approximately 140 acres of this property areis deed restricted. SJG also has office and service buildings at six other locations in theits territory. There is a liquefied natural gas storage, liquefaction and vaporization facility at one of these locations.

As of December 31, 2015, SJG’s2017, SJG's utility plant had a gross book value of $2.2$2.7 billion and a net book value, after accumulated depreciation, of $1.8$2.2 billion. In 2015, $207.82017, SJG spent $248.9 million was spent on additions to utility plant and there were retirements of property having an aggregate gross carrying valuebook cost of $17.8$26.6 million.

Virtually all of SJG’sSJG's transmission pipeline, distribution mains and service connections are under streets or highways or on the property of others. The transmission and distribution systems are maintained under franchises or permits or rights-of-way, many of which are perpetual. SJG’sSJG's properties (other than property specifically excluded) are subject to a lien of mortgage under which its first mortgage bonds are outstanding. We believe these properties are generally well maintained and in good operating condition.

Nonutility property and equipment with a net book value of $546.1 million consists primarily of Marina's energy projects.

South Jersey Fuel, Inc., an inactive subsidiary, owns land in Deptford Township and owns real estate in Upper Township, New Jersey.

Item 3. Legal Proceedings

SJI and SJG isare subject to claims which arisearising in the ordinary course of business and other legal proceedings. We accrue liabilitiesSJI has been named in, among other actions, certain gas supply and capacity management contract disputes and certain product liability claims related to theseour former sand mining subsidiary.

SJI is currently involved in a pricing dispute related to 2 long-term gas supply contracts. On May 8, 2017, a jury from the United States District Court for the District of Colorado returned a verdict in favor of the plaintiff supplier. On July 21, 2017, the court entered final judgment against SJG and SJRG. As a result of this ruling, SJG and SJRG have accrued $20.4 million and $53.6 million, respectively, through December 31, 2017. We believe that the amount to be paid by SJG reflects a gas cost that ultimately will be recovered from SJG’s customers through adjusted rates. As such, this amount was recorded as both an Accounts Payable and a reduction of Regulatory Liabilities on the consolidated balance sheets of both SJI and SJG as of December 31, 2017. The amount associated with SJRG was also recorded as an Accounts Payable on the consolidated balance sheets of SJI as of December 31, 2017, with charges of $49.6 million to Cost of Sales - Nonutility on the consolidated statements of income of SJI for the year ended December 31, 2017. SJI also recorded $4.0 million to Interest Charges on the consolidated statements of income for the year ended December 31, 2017. The plaintiff supplier filed a second related lawsuit against SJG and SJRG in the United States District Court for the District of Colorado on December 21, 2017, alleging that SJG and SJRG have continued to breach the gas supply contracts notwithstanding the judgmentin the prior lawsuit. The plaintiff supplier is seeking recovery of the amounts disputed by SJI since the earlier judgment, and a declaration regarding the price under the disputed contracts going forward until the contracts terminate in October 2019. SJI moved to stay the second lawsuit pending resolution of the post-judgment motions in the first lawsuit and any appeal of that lawsuit. All legal reserves related to this second lawsuit are recorded as part of the accrued amounts disclosed above.

South Jersey Industries, Inc.

Part I

SJI was involved in a dispute in the Court of Common Pleas of Philadelphia related to a three-year capacity management contract with a counterparty. The counterparty claimed that it was owed approximately $13.3 million, plus interest, from SJRG under a sharing credit within the contract. SJI settled with the counterparty for $9.5 million, which amount was recorded to Cost of Sales - Nonutility on SJI's consolidated statements of income for the year ended December 31, 2017. SJI made the payment in September 2017.

SJI was also involved in a tariff rate dispute with a counterparty, whereby SJI contended that the counterparty was overcharging for storage demand charges over a ten-year period. In November 2017, SJI received a favorable decision from the FERC on this matter, which resulted in a total pre-tax income impact of $9.3 million. Of this amount, $7.4 million related to the actual overcharges and was recorded as a decrease to Cost of Sales - Nonutility on the consolidated statements of income for the year ended December 31, 2017. The remaining $1.9 million related to interest income and was recorded in Other Income on the consolidated statements of income for the year ended December 31, 2017. SJI received payment from the counterparty in November 2017.

Liabilities related to claims are accrued when we can reasonably estimate the amount or range of amounts of probable settlement costs or other charges for these claims. The Companyclaims can be reasonably estimated. For matters other than the disputes that are noted above, SJI has accrued approximately $0.8$3.0 million and $0.5$3.1 million related to all claims in the aggregate as of December 31, 20152017 and 2014,2016, respectively, of which SJG has accrued approximately $0.7 million and $0.6 million as of December 31, 2017 and 2016, respectively. Management doesAlthough SJI and SJG do not presently believe that it is reasonably possible that there would be a material change in the Company's estimated liability in the near term and does not currently anticipate the disposition of any known claims that wouldthese matters will have a material adverse effect on our financial position, resultsits business, given the inherent uncertainties in such situations, SJI and SJG can provide no assurance regarding the outcome of operations or liquidity.litigation.

Item 4. Mine Safety Disclosures

Not applicable.

Item 4A. Executive Officers of the Registrant

Set forth below are the names, ages and positions of SJI's executive officers along with their business experience during the past five years. All executive officers of SJI are elected annually and serve at the discretion of the Board of Directors. All information is as of the date of the filing of this Report.

| Name, age and position with the Company | Period Served | |

Michael J. Renna, Age 50 | ||

| Chief Executive Officer | April 2015 - Present | |

| Director | January 2014 - Present | |

| President | January 2014 - Present | |

| Chief Operating Officer | January 2014 - April 2015 | |

| Senior Vice President | January 2013 - January 2014 | |

Stephen H. Clark, Age 59 | ||

| Executive Vice President | January 2017 - Present | |

| Senior Vice President | April 2015 - December 2016 | |

| Chief Financial Officer | November 2013 - Present | |

| Vice President | January 2013 - November 2013 | |

| Treasurer | January 2004 - April 2014 | |

Kenneth A. Lynch, Age 52 | ||

| Chief Risk Officer | January 2017 - Present | |

| Senior Vice President | April 2015 - Present | |

| Chief Accounting Officer | January 2013 - December 2016 | |

Kathleen A. McEndy, Age 64 | ||

| Chief Administrative Officer | June 2015 - Present | |

| Senior Vice President | April 2015 - Present | |

South Jersey Industries, Inc.

Part I

| Chief Human Resources Officer | March 2013 - June 2015 | |

| Vice President | March 2013 - April 2015 | |

| Principal, The McEndy Group, LLC | January 2009 - March 2013 | |

Gregory M. Nuzzo, Age 43 | ||

| President, South Jersey Energy Solutions | January 2017 - Present | |

| Chief Operating Officer, South Jersey Energy Solutions | January 2017 - Present | |

| Senior Vice President | April 2015 - Present | |

| Vice President | April 2014 - April 2015 | |

| Senior Vice President, South Jersey Energy Solutions | January 2013 - December 2016 | |

| Senior Vice President, South Jersey Resources Group | January 2013 - March 2014 | |

David Robbins, Jr., Age 55 | ||

| President, South Jersey Gas Company | January 2017 - Present | |

| Senior Vice President | April 2015 - Present | |

| Vice President | April 2014 - April 2015 | |

| Senior Vice President, South Jersey Energy Solutions | January 2013 - December 2016 | |

| Chief Operating Officer, South Jersey Energy Solutions | January 2013 - April 2014 | |

Steven R. Cocchi, Age 40 | ||

| Chief Strategy & Development Officer | January 2018 - Present | |

| Interim General Counsel | August 2017 - December 2017 | |

| Senior Vice President, Strategy and Growth | April 2017 - Present | |

| Vice President, Strategy and Growth | January 2017 - April 2017 | |

| Vice President, Rates and Regulatory Affairs | April 2015 - January 2017 | |

| Director, Rates and Revenue Requirements | October 2011 - April 2015 | |

Melissa Orsen, Age 42 | ||

| Senior Vice President & General Counsel | January 2018 - Present | |

| Chief Executive Officer, New Jersey Economic Development Authority | March 2015 - December 2017 | |

| Deputy Commissioner, New Jersey Department of Community Affairs | March 2014 - March 2015 | |

| Chief of Staff & Lieutenant Governor, Office of the New Jersey Governor | January 2011 - March 2014 | |

PART II

Item 5. Market for the Registrant’sRegistrant's Common Equity,

Related Stockholder Matters and Issuer Purchases of Equity Securities

South Jersey Industries, Inc.

Market Price of Common Stock and Related Information

| Quarter Ended | Market Price Per Share | Dividends | Quarter Ended | Market Price Per Share | Dividends | ||||||||||||||||

| Declared | Declared | ||||||||||||||||||||

| 2017 | High | Low | Per Share | 2016 | High | Low | Per Share | ||||||||||||||

| March 31 | $ | 35.97 | $ | 31.39 | $ | 0.273 | March 31 | $ | 29.14 | $ | 22.06 | $ | 0.264 | ||||||||

| June 30 | $ | 38.40 | $ | 33.93 | $ | 0.273 | June 30 | $ | 31.64 | $ | 26.29 | $ | 0.264 | ||||||||

| September 30 | $ | 36.41 | $ | 32.83 | $ | 0.273 | September 30 | $ | 32.03 | $ | 28.17 | $ | 0.264 | ||||||||

| December 31 | $ | 36.01 | $ | 30.75 | $ | 0.280 | December 31 | $ | 34.85 | $ | 27.51 | $ | 0.273 | ||||||||

These quotations are based on the list of composite transactions of the New York Stock Exchange. Our stock is traded on the New York Stock Exchange under the symbol SJI. We have declared and expect to continue to declare regular quarterly cash dividends. As of December 31, 2017, the latest available date, our records indicate there were 6,517 shareholders of record.

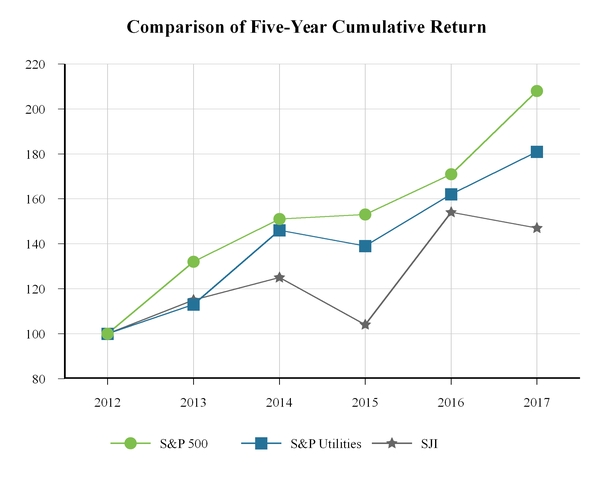

Stock Performance Graph

The performance graph below illustrates a five-year comparison of cumulative total returns based on an initial investment of $100 in South Jersey Industries, Inc. common stock, as compared with the S&P 500 Stock Index and the S&P Utility Index for the five-year period through December 31, 2017.

This performance chart assumes:

$100 invested on December 31, 2012 in South Jersey Industries, Inc. common stock, in the S&P 500 Stock Index and in the S&P Utility Index; and

All dividends are reinvested.

| Dec-12 | Dec-13 | Dec-14 | Dec-15 | Dec-16 | Dec-17 | |||||||||||||

| S&P 500 | $ | 100 | $ | 132 | $ | 151 | $ | 153 | $ | 171 | $ | 208 | ||||||

| S&P Utilities | $ | 100 | $ | 113 | $ | 146 | $ | 139 | $ | 162 | $ | 181 | ||||||

| SJI | $ | 100 | $ | 115 | $ | 125 | $ | 104 | $ | 154 | $ | 147 | ||||||

Information required by this item is also found in Note 6 of the consolidated financial statements included under Item 8 of this Report.

SJI has a history of paying quarterly dividends and has a stated goal of increasing its dividend annually.

In 2017, non-employee members of SJI's Board of Directors received an aggregate of 30,394 shares of restricted stock, valued at that time at $1,022,454, as part of their compensation for serving on the Board.

Issuer Purchases of Equity Securities - There were no purchases by SJI of its own common stock during the year ended December 31, 2017.

South Jersey Gas Company

All of the outstanding common stock of SJG (its only class of equity securities) is owned by its parent company, South Jersey Industries, Inc.SJI. The common stock is not traded on any stock exchange.

SJG is restricted under its First Mortgage Indenture, as supplemented, as to the amount of cash dividends or other distributions that may be paid on its common stock. As of December 31, 2015,2017, these restrictions did not affect the amount that may be distributed from SJG’s retained earnings. SJG declared and paid cash dividends totaling $40.8 and $18.2of $20.0 million in 2017 to SJI. No dividends were declared or paid on itsSJG's common stock in 2015 and 2014, respectively.2016.

Item 6. Selected Financial Data

Five-Year Summary of Selected Financial Data

(In Thousands Where Applicable)

South Jersey Industries, Inc. and Subsidiaries

Year Ended December 31,

The following financial data has been obtained from SJI’s consolidated financial statements (in thousands, except for ratios, shares data and earnings per share):

| 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||

| Operating Results: | |||||||||||||||

| Operating Revenues | $ | 1,243,068 | $ | 1,036,500 | $ | 959,568 | $ | 886,996 | $ | 731,421 | |||||

| Operating Income | $ | 4,410 | $ | 189,276 | $ | 156,894 | $ | 127,603 | $ | 69,636 | |||||

| (Loss) Income from Continuing Operations | $ | (3,404 | ) | $ | 119,061 | $ | 105,610 | $ | 97,628 | $ | 82,389 | ||||

| Discontinued Operations - Net (1) | (86 | ) | (251 | ) | (503 | ) | (582 | ) | (796 | ) | |||||

| Net (Loss) Income | $ | (3,490 | ) | $ | 118,810 | $ | 105,107 | $ | 97,046 | $ | 81,593 | ||||

| Total Assets | $ | 3,865,086 | $ | 3,730,567 | $ | 3,480,900 | $ | 3,349,425 | $ | 2,924,855 | |||||

| Capitalization: | |||||||||||||||

| Equity | $ | 1,192,409 | $ | 1,289,240 | $ | 1,037,539 | $ | 932,432 | $ | 827,000 | |||||

| Long-Term Debt | 1,122,999 | 808,005 | 1,006,394 | 859,491 | 680,400 | ||||||||||

| Total Capitalization | $ | 2,315,408 | $ | 2,097,245 | $ | 2,043,933 | $ | 1,791,923 | $ | 1,507,400 | |||||

| Ratio of Earnings to Fixed Charges (2) | 0.5 | x | 5.4 | x | 3.8x | 3.8x | 3.0x | ||||||||

| Diluted Earnings Per Common Share (Based on Average Diluted Shares Outstanding) (3): | |||||||||||||||

| Continuing Operations | $ | (0.04 | ) | $ | 1.56 | $ | 1.53 | $ | 1.47 | $ | 1.29 | ||||

| Discontinued Operations - Net (1) | — | — | (0.01 | ) | (0.01 | ) | (0.01 | ) | |||||||

| Diluted Earnings Per Common Share (3) | $ | (0.04 | ) | $ | 1.56 | $ | 1.52 | $ | 1.46 | $ | 1.28 | ||||

| (Loss) Return on Average Equity (4) | (0.3 | )% | 10.2 | % | 10.7 | % | 11.1 | % | 10.5 | % | |||||

| Share Data: | |||||||||||||||

| Number of Shareholders of Record | 6.5 | 6.7 | 6.7 | 6.9 | 6.9 | ||||||||||

| Average Common Shares (3) | 79,541 | 76,362 | 68,735 | 66,278 | 63,978 | ||||||||||

| Common Shares Outstanding at Year End (3) | 79,549 | 79,478 | 70,966 | 68,334 | 65,430 | ||||||||||

| Dividend Reinvestment Plan: | |||||||||||||||

| Number of Shareholders | 5.0 | 5.2 | 5.2 | 5.2 | 5.2 | ||||||||||

| Number of Participating Shares (3) | 3,607 | 3,627 | 4,170 | 4,082 | 4,118 | ||||||||||

| Book Value at Year End (3) | $ | 14.99 | $ | 16.22 | $ | 14.62 | $ | 13.65 | $ | 12.64 | |||||

| Dividends Declared per Common Share (3) | $ | 1.10 | $ | 1.07 | $ | 1.02 | $ | 0.96 | $ | 0.90 | |||||

| Market Price at Year End (3) | $ | 31.23 | $ | 33.69 | $ | 23.52 | $ | 29.46 | $ | 27.98 | |||||

| Market-to-Book Ratio (3) | 2.1 | x | 2.1 | x | 1.6x | 2.2x | 2.2x | ||||||||

| Consolidated Economic Earnings (5) | |||||||||||||||

| (Loss) Income from Continuing Operations | $ | (3,404 | ) | $ | 119,061 | $ | 105,610 | $ | 97,628 | $ | 82,389 | ||||

| Minus/Plus: | |||||||||||||||

| Unrealized Mark-to-Market Losses/(Gains) on Derivatives and Realized Losses/(Gains) on Inventory Injection Hedges (6) | 14,558 | (26,867 | ) | (8,355 | ) | 8,211 | 23,422 | ||||||||

| Net Loss from Affiliated Companies, Not Part of Ongoing Operations (6,7) | — | — | — | — | 1,252 | ||||||||||

| Net Loss from Affiliated Companies (6,8) | — | — | (2,540 | ) | 2,540 | — | |||||||||

| Unrealized Loss on Property, Plant and Equipment (9) | 91,299 | — | — | — | — | ||||||||||

| Net Losses from Legal Proceedings (10) | 56,075 | — | — | — | — | ||||||||||

| Acquisition Costs (11) | 19,564 | — | — | — | — | ||||||||||

| Other (6,12) | 2,227 | (165 | ) | (165 | ) | (165 | ) | (165 | ) | ||||||

| Income Taxes (13) | (70,834 | ) | 10,813 | 4,424 | (4,235 | ) | (9,804 | ) | |||||||

| Additional Tax Adjustments (14) | (11,420 | ) | — | — | — | — | |||||||||

| Economic Earnings | $ | 98,065 | $ | 102,842 | $ | 98,974 | $ | 103,979 | $ | 97,094 | |||||

| (Loss) Earnings per Share from Continuing Operations (3) | $ | (0.04 | ) | $ | 1.56 | $ | 1.53 | $ | 1.47 | $ | 1.29 | ||||

| Minus/Plus: | |||||||||||||||

| Unrealized Mark-to-Market Losses/(Gains) on Derivatives and Realized Losses/(Gains) on Inventory Injection Hedges (6) | 0.18 | (0.35 | ) | (0.12 | ) | 0.12 | 0.36 | ||||||||

| Net Loss from Affiliated Companies, Not Part of Ongoing Operations (6,7) | — | — | — | — | 0.02 | ||||||||||

| Net Loss from Affiliated Companies (6,8) | — | — | (0.04 | ) | 0.04 | — | |||||||||

| Unrealized Loss on Property, Plant and Equipment (9) | 1.14 | — | — | — | — | ||||||||||

| Net Losses from Legal Proceedings (10) | 0.70 | — | — | — | — | ||||||||||

| Acquisition Costs (11) | 0.25 | — | — | — | — | ||||||||||

| Other (6,12) | 0.03 | — | — | — | — | ||||||||||

| Income Taxes (13) | (0.89 | ) | 0.13 | 0.07 | (0.06 | ) | (0.16 | ) | |||||||

| Additional Tax Adjustments (14) | (0.14 | ) | — | — | — | — | |||||||||

| Economic Earnings per Share (3) | $ | 1.23 | $ | 1.34 | $ | 1.44 | $ | 1.57 | $ | 1.51 | |||||

| (1) | Represents discontinued business segments: sand mining and distribution operations sold in 1996 and fuel oil operations with related environmental liabilities in 1986 (See Note 3 to the consolidated financial statements). |

| (2) | Calculated as Income from Continuing Operations before Income Taxes and Interest Expense divided by Total Fixed Charges, which consists of Interest Expense and Capitalized Interest. |

| (3) | All share and per share amounts were adjusted for all periods presented for the 2-for-1 stock split, effected in the form of a stock dividend, effective on May 8, 2015. See Note 1 to the consolidated financial statements. |

| (4) | Calculated based on Income from Continuing Operations. |

| (5) | This section includes the non-generally accepted accounting principles (“non-GAAP”) financial measures of Economic Earnings and Economic Earnings per share. See "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Item 7 of this Report for a discussion regarding the use of non-GAAP financial measures and a reconciliation of income from Continuing Operations and earnings per share to Economic Earnings and Economic Earnings per share, respectively. |

| (6) | Certain reclassifications have been made to the prior period numbers in these tables to conform to the current period presentation. The 2013-2015 numbers in these line items have been adjusted to be presented before income taxes. |

| (7) | Resulting from the termination of the contract at LVE Energy Partners, LLC to design, build, own and operate a district energy system and central energy center for a planned resort in Las Vegas, Nevada. |

| (8) | Resulting from a reserve for uncollectible accounts recorded by an Energenic subsidiary that owned and operated a central energy center and energy distribution system for a hotel, casino and entertainment complex in Atlantic City, New Jersey (see Note 7 to the consolidated financial statements). In 2014, this charge was excluded from Economic Earnings as the total economic impact of the proceedings had not been realized. During the second quarter 2015, the Company, through its investment in Energenic, reduced the carrying value of the investment in this project. As such, this charge is included in Economic Earnings in 2015. |

| (9) | Represents several impairment charges recorded during the year, including impairments on solar generating facilities, landfill gas-to-energy (LFGTE) long-lived assets, LFGTE assets customer relationships, and goodwill (see Note 1 to the consolidated financial statements). The economic impact of these charges will not be realized until a future period. |

| (10) | Represents net losses from three separate legal proceedings: (a) $55.6 million of pre-tax charges, including interest and legal fees, resulting from a ruling in a legal proceeding related to a pricing dispute between SJI and a gas supplier that began in October 2014; (b) a $9.8 million pre-tax charge, including legal fees, resulting from a settlement with a counterparty over a dispute related to a three-year capacity management contract; and (c) a $9.3 million pre-tax gain resulting from a favorable FERC decision, including interest, over a tariff rate dispute with a counterparty, whereby SJI contended that the counterparty was overcharging for storage demand charges over a ten-year period. See Note 15 to the consolidated financial statements. Since these net losses relate to transactions that primarily occurred in prior periods, these net losses are excluded from Economic Earnings. |

| (11) | Represents costs incurred on the agreement to acquire the assets of Elizabethtown Gas and Elkton Gas (see Note 1 to the consolidated financial statements). Since the economic impact will not be realized until future periods, this amount is excluded from Economic Earnings. |

| (12) | Included in this amount are amendments made to an existing interest rate derivative linked to unrealized losses previously recorded in Accumulated Other Comprehensive Loss (AOCL), which SJI reclassified from AOCL to Interest Charges on the consolidated statements of income as a result of the prior hedged transactions being deemed probable of not occurring. Since the economic impact will not be realized until future periods, this amount is excluded from Economic Earnings. Also included is additional depreciation expense within Economic Earnings on two solar generating facilities where an impairment charge was recorded in the past, which reduced the depreciable basis and recurring depreciation expense, and the related reduction in depreciation expense is being added back. |

| (13) | Determined using a combined average statutory tax rate of approximately 39% for 2017 and 40% for 2016 and 2015. |

| (14) | Represents one-time tax adjustments, most notably for Tax Reform, which was signed into law in December 2017. See Note 4 to the consolidated financial statements. |

The following financial data has been obtained from SJG’s audited financial statements (In(in thousands, except for Ratio Dataratios and Customers)customers):

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||||||||||||||||

| Operating Revenues | $ | 534,290 | $ | 501,875 | $ | 446,480 | $ | 421,874 | $ | 412,449 | $ | 517,254 | $ | 461,055 | $ | 534,290 | $ | 501,875 | $ | 446,480 | ||||||||||||||||||

| Operating Income | $ | 119,585 | $ | 113,690 | $ | 105,822 | $ | 101,762 | $ | 102,663 | 136,487 | $ | 122,455 | $ | 119,585 | $ | 113,690 | $ | 105,822 | |||||||||||||||||||

| Net Income | $ | 66,578 | $ | 66,483 | $ | 62,236 | $ | 58,241 | $ | 52,889 | $ | 72,557 | $ | 69,045 | $ | 66,578 | $ | 66,483 | $ | 62,236 | ||||||||||||||||||

| Average Shares of Common Stock Outstanding | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | 2,339 | ||||||||||||||||||||||||||||

| Ratio of Earnings to Fixed Charges (1) | 5.4x | 5.4x | 5.3x | 5.5x | 5.3x | 5.4x | 5.5x | 5.4x | 5.4x | 5.3x | ||||||||||||||||||||||||||||

| As of December 31, | As of December 31, | |||||||||||||||||||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||||||||||||||||

| Property, Plant and Equipment, Net | $ | 1,770,766 | $ | 1,589,369 | $ | 1,424,775 | $ | 1,285,591 | $ | 1,158,029 | $ | 2,154,083 | $ | 1,952,912 | $ | 1,770,766 | $ | 1,589,369 | $ | 1,424,775 | ||||||||||||||||||

| Total Assets | $ | 2,288,204 | $ | 2,185,672 | $ | 1,909,126 | $ | 1,786,459 | $ | 1,615,723 | $ | 2,865,974 | $ | 2,551,923 | $ | 2,288,204 | $ | 2,185,672 | $ | 1,909,126 | ||||||||||||||||||

| Capitalization: | ||||||||||||||||||||||||||||||||||||||

| Common Equity | $ | 707,927 | $ | 680,568 | $ | 610,969 | $ | 521,395 | $ | 464,186 | $ | 921,433 | $ | 839,900 | $ | 707,927 | $ | 680,568 | $ | 610,969 | ||||||||||||||||||

| Long-Term Debt | 584,082 | 507,091 | 454,000 | 425,000 | 362,813 | 758,052 | 423,177 | 584,082 | 507,091 | 454,000 | ||||||||||||||||||||||||||||