| (Mark One) | |||||

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

| For the fiscal year ended December 31, | |||||

| or | |||||

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the transition period from to | |||||

| Iowa | 42-1447959 | ||||

| (State or other jurisdiction of Incorporation) | (I.R.S. Employer Identification No.) | ||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Common stock, par value $1 | AEL | New York Stock Exchange | ||||||||||||

| Depositary Shares, each representing a 1/1,000th interest in a share of 5.95% Fixed-Rate Reset Non-Cumulative Preferred Stock, Series A | AELPRA | New York Stock Exchange | ||||||||||||

| Depositary Shares, each representing a 1/1,000th interest in a share of 6.625% Fixed-Rate Reset Non-Cumulative Preferred Stock, Series B | AELPRB | New York Stock Exchange | ||||||||||||

| Large accelerated filer | ☒ | Accelerated filer | ☐ | ||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | ||||||||

| Emerging growth company | ☐ | ||||||||||

F-1 | ||||||||

| Exhibit 21.2 | Subsidiaries of American Equity Investment Life Holding Company | |||||||

| Exhibit 23.1 | Consent of Independent Registered Public Accounting Firm | |||||||

| Exhibit 31.1 | Certification | |||||||

| Exhibit 31.2 | Certification | |||||||

| Exhibit 32.1 | Certification | |||||||

| Exhibit 32.2 | Certification | |||||||

| Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Product Type | Product Type | Deposits Collected | Deposits as a % of Total | Deposits Collected | Deposits as a % of Total | Deposits Collected | Deposits as a % of Total | Product Type | Deposits Collected | Deposits as a % of Total | Deposits Collected | Deposits as a % of Total | Deposits Collected | Deposits as a % of Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | Fixed index annuities | $ | 3,171,420 | 95 | % | $ | 3,450,547 | 58 | % | $ | 2,337,578 | 64 | % | Fixed index annuities | $ | 7,034,426 | 93 | 93 | % | $ | 3,171,420 | 95 | 95 | % | $ | 3,450,547 | 58 | 58 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual reset fixed rate annuities | Annual reset fixed rate annuities | 5,709 | — | % | 6,483 | — | % | 8,225 | — | % | Annual reset fixed rate annuities | 5,092 | — | — | % | 5,709 | — | — | % | 6,483 | — | — | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Multi-year fixed rate annuities | Multi-year fixed rate annuities | 139,092 | 4 | % | 2,452,994 | 41 | % | 1,303,133 | 35 | % | Multi-year fixed rate annuities | 565,788 | 7 | 7 | % | 139,092 | 4 | 4 | % | 2,452,994 | 41 | 41 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Single premium immediate annuities | Single premium immediate annuities | 18,935 | 1 | % | 59,816 | 1 | % | 33,461 | 1 | % | Single premium immediate annuities | 1,224 | — | — | % | 18,935 | 1 | 1 | % | 59,816 | 1 | 1 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 3,335,156 | 100 | % | $ | 5,969,840 | 100 | % | $ | 3,682,397 | 100 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | $ | 7,606,530 | 100 | % | $ | 3,335,156 | 100 | % | $ | 5,969,840 | 100 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, | December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annuity Surrender Charges: | Annuity Surrender Charges: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average years at issue | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average years at issue | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average years at issue | Average years at issue | 11.6 | 11.8 | 12.4 | 11.2 | 11.6 | 11.8 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average years remaining | Average years remaining | 4.6 | 5.5 | 6.1 | Average years remaining | 4.6 | 5.5 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Average surrender charge percentage remaining | Average surrender charge percentage remaining | 7.9 | % | 9.1 | % | 9.9 | % | Average surrender charge percentage remaining | 7.9 | % | 7.9 | % | 9.1 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

| Annuity Account Value (net of coinsurance) | Annuity Account Value (net of coinsurance) | $ | 47,504,615 | $ | 53,191,277 | $ | 54,056,725 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Financial Strength Rating | Outlook Statement | ||||||||||

| A.M. Best Company, Inc. | |||||||||||

| August 2023 - current | A- | Watch | |||||||||

| January 2011 - | A- | Stable | |||||||||

| S&P Global | |||||||||||

| July 2023 - current | A- | Watch | |||||||||

| August 2020 - | A- | Stable | |||||||||

| March 2020 - August 2020 | A- | Negative | |||||||||

| August 2015 - March 2020 | A- | Stable | |||||||||

| June 2013 - August 2015 | BBB+ | Positive | |||||||||

| October 2011 - June 2013 | BBB+ | Stable | |||||||||

| Fitch Ratings Ltd. | |||||||||||

| April 2021 - current | A- | Stable | |||||||||

| April 2020 - April 2021 | A- | Negative | |||||||||

| August 2019 - April 2020 | A- | Stable | |||||||||

| September 2018 - August 2019 | BBB+ | Positive | |||||||||

| May 2013 - September 2018 | BBB+ | Stable | |||||||||

| High | Low | |||||||||||||||||||||||||||||

| 2022 | ||||||||||||||||||||||||||||||

| High | High | Low | ||||||||||||||||||||||||||||

| 2023 | ||||||||||||||||||||||||||||||

| First Quarter | ||||||||||||||||||||||||||||||

| First Quarter | ||||||||||||||||||||||||||||||

| First Quarter | First Quarter | $44.49 | $35.05 | $48.37 | $31.57 | |||||||||||||||||||||||||

| Second Quarter | Second Quarter | $42.18 | $32.65 | Second Quarter | $53.68 | $35.22 | ||||||||||||||||||||||||

| Third Quarter | Third Quarter | $43.55 | $33.22 | Third Quarter | $54.44 | $51.73 | ||||||||||||||||||||||||

| Fourth Quarter | Fourth Quarter | $46.76 | $28.05 | Fourth Quarter | $56.09 | $52.70 | ||||||||||||||||||||||||

| 2021 | ||||||||||||||||||||||||||||||

| 2022 | ||||||||||||||||||||||||||||||

| First Quarter | ||||||||||||||||||||||||||||||

| First Quarter | ||||||||||||||||||||||||||||||

| First Quarter | First Quarter | $32.54 | $26.21 | $44.49 | $35.05 | |||||||||||||||||||||||||

| Second Quarter | Second Quarter | $33.68 | $29.18 | Second Quarter | $42.18 | $32.65 | ||||||||||||||||||||||||

| Third Quarter | Third Quarter | $33.79 | $27.12 | Third Quarter | $43.55 | $33.22 | ||||||||||||||||||||||||

| Fourth Quarter | Fourth Quarter | $39.88 | $29.46 | Fourth Quarter | $46.76 | $28.05 | ||||||||||||||||||||||||

| Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (a) | Approximate Dollar Value of Shares That May Yet Be Purchased Under Program | |||||||||||||||||||||||

| Period | (shares) | (dollars) | (shares) | (dollars in thousands) | ||||||||||||||||||||||

| October 1, 2022 - October 31, 2022 | 304,688 | $ | 37.84 | 304,688 | $ | 201,586 | ||||||||||||||||||||

| November 1, 2022 - November 30, 2022 | 842,749 | $ | 36.32 | 842,749 | $ | 570,975 | ||||||||||||||||||||

| December 1, 2022 - December 31, 2022 | 50,272 | $ | 38.91 | 50,272 | $ | 569,018 | ||||||||||||||||||||

| Total | 1,197,709 | 1,197,709 | ||||||||||||||||||||||||

| Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (a) | Approximate Dollar Value of Shares That May Yet Be Purchased Under Program | |||||||||||||||||||||||

| Period | (shares) | (dollars) | (shares) | (dollars in thousands) | ||||||||||||||||||||||

| October 1, 2023 - October 31, 2023 | — | $ | — | — | $ | 275,825 | ||||||||||||||||||||

| November 1, 2023 - November 30, 2023 | — | $ | — | — | $ | 275,825 | ||||||||||||||||||||

| December 1, 2023 - December 31, 2023 | — | $ | — | — | $ | 275,825 | ||||||||||||||||||||

| Total | — | — | ||||||||||||||||||||||||

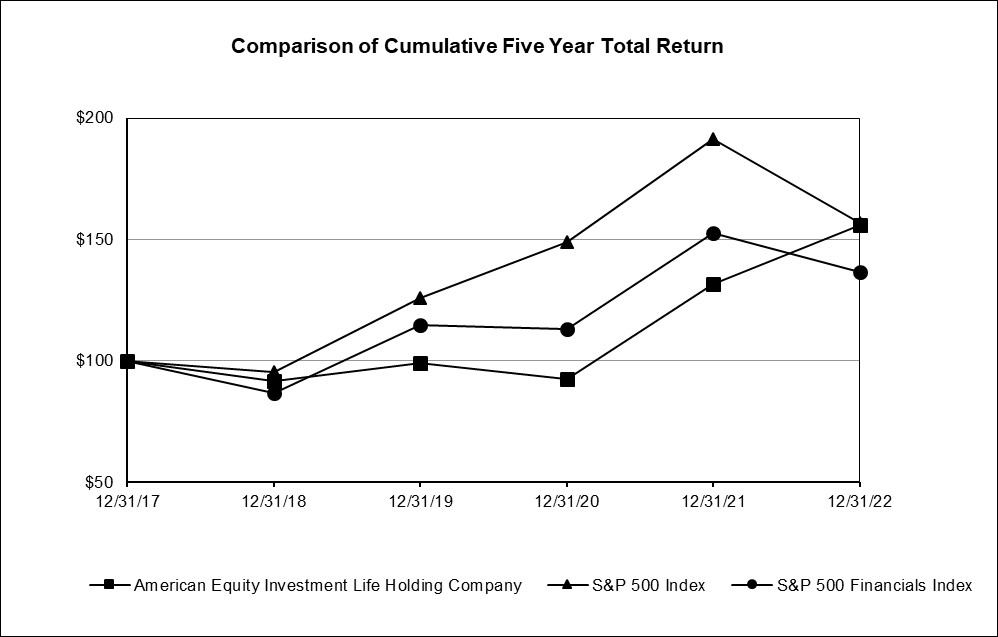

| 12/31/2017 | 12/31/2018 | 12/31/2019 | 12/31/2020 | 12/31/2021 | 12/31/2022 | ||||||||||||||||||||||||||||||||||||||||

| 12/31/2018 | 12/31/2018 | 12/31/2019 | 12/31/2020 | 12/31/2021 | 12/31/2022 | 12/31/2023 | |||||||||||||||||||||||||||||||||||||||

| American Equity Investment Life Holding Co. | American Equity Investment Life Holding Co. | 100.00 | 91.67 | 99.20 | 92.74 | 131.73 | 155.83 | ||||||||||||||||||||||||||||||||||||||

| S&P 500 Index | S&P 500 Index | 100.00 | 95.62 | 125.72 | 148.85 | 191.58 | 156.88 | ||||||||||||||||||||||||||||||||||||||

| S&P 500 Financials Index | S&P 500 Financials Index | 100.00 | 86.97 | 114.91 | 112.96 | 152.54 | 136.48 | ||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Average yield on invested assets | Average yield on invested assets | 4.34% | 3.73% | 4.12% | Average yield on invested assets | 4.55% | 4.34% | 3.73% | |||||||||||||||||||||||||||||||||||||||||||

| Aggregate cost of money | Aggregate cost of money | 1.71% | 1.55% | 1.69% | Aggregate cost of money | 1.90% | 1.71% | 1.55% | |||||||||||||||||||||||||||||||||||||||||||

| Aggregate investment spread | Aggregate investment spread | 2.63% | 2.18% | 2.43% | Aggregate investment spread | 2.65% | 2.63% | 2.18% | |||||||||||||||||||||||||||||||||||||||||||

| Impact of: | Impact of: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment yield - additional prepayment income | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment yield - additional prepayment income | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment yield - additional prepayment income | Investment yield - additional prepayment income | 0.03% | 0.11% | 0.08% | 0.01% | 0.03% | 0.11% | ||||||||||||||||||||||||||||||||||||||||||||

| Cost of money benefit from over hedging | Cost of money benefit from over hedging | 0.01% | 0.07% | 0.02% | Cost of money benefit from over hedging | 0.04% | 0.01% | 0.07% | |||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Product Type | Product Type | 2022 | 2021 | 2020 | Product Type | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| American Equity Life: | American Equity Life: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | Fixed index annuities | $ | 2,692,141 | $ | 2,753,479 | $ | 1,992,059 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual reset fixed rate annuities | Annual reset fixed rate annuities | 5,329 | 6,133 | 8,128 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Multi-year fixed rate annuities | Multi-year fixed rate annuities | 56,511 | 855,702 | 395,982 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Single premium immediate annuities | Single premium immediate annuities | 18,935 | 59,816 | 33,461 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2,772,916 | 3,675,130 | 2,429,630 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5,689,883 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Eagle Life: | Eagle Life: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | Fixed index annuities | 479,279 | 697,068 | 345,519 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual reset fixed rate annuities | Annual reset fixed rate annuities | 380 | 350 | 97 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Multi-year fixed rate annuities | Multi-year fixed rate annuities | 82,581 | 1,597,292 | 907,151 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 562,240 | 2,294,710 | 1,252,767 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,916,647 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated: | Consolidated: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities | Fixed index annuities | 3,171,420 | 3,450,547 | 2,337,578 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Annual reset fixed rate annuities | Annual reset fixed rate annuities | 5,709 | 6,483 | 8,225 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Multi-year fixed rate annuities | Multi-year fixed rate annuities | 139,092 | 2,452,994 | 1,303,133 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Single premium immediate annuities | Single premium immediate annuities | 18,935 | 59,816 | 33,461 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total before coinsurance ceded | Total before coinsurance ceded | 3,335,156 | 5,969,840 | 3,682,397 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance ceded | Coinsurance ceded | 968,906 | 424,819 | 35,667 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net after coinsurance ceded | Net after coinsurance ceded | $ | 2,366,250 | $ | 5,545,021 | $ | 3,646,730 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Increase (decrease) in amortization of deferred sales inducements | $ | 45,682 | $ | (45,107) | $ | 428,101 | |||||||||||

| Increase (decrease) in amortization of deferred policy acquisition costs | 56,853 | (45,662) | 646,785 | ||||||||||||||

| Increase (decrease) in interest sensitive and index product benefits | (53,042) | 243,658 | 285,825 | ||||||||||||||

| Decrease in change in fair value of embedded derivatives | (94,770) | (122,294) | (2,341,279) | ||||||||||||||

| Effect on net income available to common stockholders | 35,543 | (24,017) | 769,611 | ||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Increase (decrease) in market risk benefit (gain) loss | $ | (63,294) | $ | 229,439 | $ | 398,759 | |||||||||||

| Increase (decrease) in policy benefit reserves (1) | (2,296) | 3,051 | 801 | ||||||||||||||

| Increase (decrease) in change in fair value of embedded derivatives | 84,381 | (94,770) | (122,294) | ||||||||||||||

| Effect on net income available to common stockholders | (14,750) | (106,905) | (219,100) | ||||||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation from net income available to common stockholders to non-GAAP operating income available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income available to common stockholders | $ | 1,177,269 | $ | 430,317 | $ | 637,945 | |||||||||||||||||||||||||||||||||||||||||||||

| Adjustments to arrive at non-GAAP operating income available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Reconciliation from net income available to common stockholders to non-GAAP operating income (loss) available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income available to American Equity Investment Life Holding Company common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income available to American Equity Investment Life Holding Company common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income available to American Equity Investment Life Holding Company common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Adjustments to arrive at non-GAAP operating income (loss) available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net realized losses on financial assets, including credit losses | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net realized losses on financial assets, including credit losses | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net realized losses on financial assets, including credit losses | Net realized losses on financial assets, including credit losses | 36,428 | 10,299 | 59,355 | |||||||||||||||||||||||||||||||||||||||||||||||

| Change in fair value of derivatives and embedded derivatives | Change in fair value of derivatives and embedded derivatives | (1,080,356) | (187,290) | (784,005) | |||||||||||||||||||||||||||||||||||||||||||||||

| Capital markets impact on the change in fair value of market risk benefits | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Net investment income | Net investment income | 664 | — | — | |||||||||||||||||||||||||||||||||||||||||||||||

| Other revenue | Other revenue | 5,969 | — | — | |||||||||||||||||||||||||||||||||||||||||||||||

| Expenses incurred related to acquisition | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Income taxes | Income taxes | 222,966 | 37,184 | 155,808 | |||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income available to common stockholders | 362,940 | 290,510 | 69,103 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income (loss) available to common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of excluding notable items | Impact of excluding notable items | (26,572) | 78,036 | 310,117 | |||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income available to common stockholders, excluding notable items | $ | 336,368 | $ | 368,546 | $ | 379,220 | |||||||||||||||||||||||||||||||||||||||||||||

| Per common share - assuming dilution: | Per common share - assuming dilution: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income available to common stockholders | $ | 3.96 | $ | 3.07 | $ | 0.75 | |||||||||||||||||||||||||||||||||||||||||||||

| Per common share - assuming dilution: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Per common share - assuming dilution: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income (loss) available to common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income (loss) available to common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income (loss) available to common stockholders | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of excluding notable items | Impact of excluding notable items | (0.29) | 0.83 | 3.36 | |||||||||||||||||||||||||||||||||||||||||||||||

| Non-GAAP operating income available to common stockholders, excluding notable items | $ | 3.67 | $ | 3.90 | $ | 4.11 | |||||||||||||||||||||||||||||||||||||||||||||

| Notable items impacting non-GAAP operating income available to common stockholders: | Notable items impacting non-GAAP operating income available to common stockholders: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Notable items impacting non-GAAP operating income available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Notable items impacting non-GAAP operating income available to common stockholders: | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Expense associated with strategic incentive award | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Expense associated with strategic incentive award | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Expense associated with strategic incentive award | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of actuarial assumption updates | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Impact of actuarial assumption updates | $ | (26,572) | $ | 78,036 | $ | 340,895 | |||||||||||||||||||||||||||||||||||||||||||||

| Tax benefit related to the CARES Act | — | — | (30,778) | ||||||||||||||||||||||||||||||||||||||||||||||||

| Total notable items | Total notable items | $ | (26,572) | $ | 78,036 | $ | 310,117 | ||||||||||||||||||||||||||||||||||||||||||||

| Total notable items | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Total notable items | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Increase (decrease) in amortization of deferred sales inducements | $ | 8,670 | $ | (66,066) | $ | 57,467 | |||||||||||

| Increase (decrease) in amortization of deferred policy acquisition costs | 10,520 | (78,183) | 90,970 | ||||||||||||||

| Increase (decrease) in interest sensitive and index product benefits | (53,042) | 243,658 | 285,825 | ||||||||||||||

| Effect on non-GAAP operating income available to common stockholders | 26,572 | (78,036) | (340,895) | ||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Increase (decrease) in market risk benefit (gain) loss | $ | (32,822) | $ | 230,832 | $ | 398,753 | |||||||||||

| Increase (decrease) in policy benefit reserves (1) | (2,296) | 3,051 | 3,051 | ||||||||||||||

| Effect on non-GAAP operating income (loss) available to common stockholders | 27,568 | (181,890) | 317,425 | ||||||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Surrender charges | Surrender charges | $ | 72,699 | $ | 67,657 | $ | 72,551 | ||||||||||||||||||||||||||||||||||||||||||||

| Lifetime income benefit riders (LIBR) fees | Lifetime income benefit riders (LIBR) fees | 157,655 | 174,974 | 178,676 | |||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 230,354 | $ | 242,631 | $ | 251,227 | ||||||||||||||||||||||||||||||||||||||||||||||

| Withdrawals from annuity policies subject to surrender charges | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Withdrawals from annuity policies subject to surrender charges | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Withdrawals from annuity policies subject to surrender charges | Withdrawals from annuity policies subject to surrender charges | $ | 1,145,415 | $ | 1,099,098 | $ | 776,305 | ||||||||||||||||||||||||||||||||||||||||||||

| Average surrender charge collected on withdrawals subject to surrender charges | Average surrender charge collected on withdrawals subject to surrender charges | 6.3 | % | 6.2 | % | 9.3 | % | Average surrender charge collected on withdrawals subject to surrender charges | 6.4 | % | 6.3 | % | 6.2 | % | |||||||||||||||||||||||||||||||||||||

| Fund values on policies subject to LIBR fees | Fund values on policies subject to LIBR fees | $ | 19,473,279 | $ | 22,183,623 | $ | 22,986,903 | ||||||||||||||||||||||||||||||||||||||||||||

| Fund values on policies subject to LIBR fees | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Fund values on policies subject to LIBR fees | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Weighted average per policy LIBR fee | Weighted average per policy LIBR fee | 0.81 | % | 0.79 | % | 0.78 | % | Weighted average per policy LIBR fee | 0.89 | % | 0.81 | % | 0.79 | % | |||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Call options: | |||||||||||||||||

| Gain (loss) on option expiration | $ | (287,328) | $ | 1,368,381 | $ | 15,042 | |||||||||||

| Change in unrealized gains/losses | (831,440) | (20,456) | 19,562 | ||||||||||||||

| Warrants | 264 | 810 | — | ||||||||||||||

| Interest rate swaps | (19,624) | — | — | ||||||||||||||

| Interest rate caps | — | — | 62 | ||||||||||||||

| $ | (1,138,128) | $ | 1,348,735 | $ | 34,666 | ||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Call options: | |||||||||||||||||

| Proceeds received at option expiration | $ | 344,876 | $ | 312,133 | $ | 2,019,477 | |||||||||||

| Pro rata amortization of option cost | (682,918) | (647,132) | (630,015) | ||||||||||||||

| Change in unrealized gains/losses | 586,786 | (783,769) | (41,537) | ||||||||||||||

| Warrants | 1,206 | 264 | 810 | ||||||||||||||

| Interest rate swaps | 9,096 | (19,624) | — | ||||||||||||||

| $ | 259,046 | $ | (1,138,128) | $ | 1,348,735 | ||||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| S&P 500 Index | S&P 500 Index | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Point-to-point strategy | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Point-to-point strategy | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Point-to-point strategy | Point-to-point strategy | 0.0% - 12.5% | 0.0% - 42.6% | 0.0% - 17.4% | 0.0% - 14.0% | 0.0% - 12.5% | 0.0% - 42.6% | ||||||||||||||||||||||||||||||||||||||||||||

| Monthly average strategy | Monthly average strategy | 0.0% - 8.6% | 0.0% - 29.4% | 0.0% - 11.9% | Monthly average strategy | 0.0% - 8.7% | 0.0% - 8.6% | 0.0% - 29.4% | |||||||||||||||||||||||||||||||||||||||||||

| Monthly point-to-point strategy | Monthly point-to-point strategy | 0.0% - 12.9% | 0.0% - 21.7% | 0.0% - 14.0% | Monthly point-to-point strategy | 0.0% - 14.2% | 0.0% - 12.9% | 0.0% - 21.7% | |||||||||||||||||||||||||||||||||||||||||||

| Volatility control index point-to-point strategy | Volatility control index point-to-point strategy | 0.0% - 7.3% | 0.0% - 9.7% | 0.0% - 9.3% | Volatility control index point-to-point strategy | 0.0% - 5.6% | 0.0% - 7.3% | 0.0% - 9.7% | |||||||||||||||||||||||||||||||||||||||||||

| Fixed income (bond index) strategies | Fixed income (bond index) strategies | 0.0% - 6.5% | 0.0% - 10.0% | 0.0% - 13.6% | Fixed income (bond index) strategies | 0.0% - 6.0% | 0.0% - 6.5% | 0.0% - 10.0% | |||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Asset liability management fees | $ | 22,448 | $ | 12,686 | $ | 5,470 | |||||||||||

| Amortization of deferred gain | 53,418 | 29,559 | 10,690 | ||||||||||||||

| $ | 75,866 | $ | 42,245 | $ | 16,160 | ||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Asset liability management fees | $ | 12,686 | $ | 5,470 | $ | — | |||||||||||

| Amortization of deferred gain | 31,235 | 10,200 | — | ||||||||||||||

| $ | 43,921 | $ | 15,670 | $ | — | ||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Index credits on index policies | $ | 305,292 | $ | 1,977,888 | $ | 747,489 | |||||||||||

| Interest credited (including changes in minimum guaranteed interest for fixed index annuities) | 249,579 | 253,725 | 198,745 | ||||||||||||||

| Lifetime income benefit riders | 334,779 | 449,793 | 597,036 | ||||||||||||||

| $ | 889,650 | $ | 2,681,406 | $ | 1,543,270 | ||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Index credits on index policies | $ | 326,471 | $ | 305,292 | $ | 1,977,888 | |||||||||||

| Interest credited (including changes in minimum guaranteed interest for fixed index annuities) | 240,952 | 249,579 | 253,679 | ||||||||||||||

| $ | 567,423 | $ | 554,871 | $ | 2,231,567 | ||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Amortization of deferred sales inducements before gross profit adjustments | $ | 234,778 | $ | 112,790 | $ | 243,067 | |||||||||||

| Gross profit adjustments: | |||||||||||||||||

| Fair value accounting for derivatives and embedded derivatives | 177,131 | 40,899 | 202,660 | ||||||||||||||

| Net realized losses on investments | (3,361) | (997) | (7,563) | ||||||||||||||

| Amortization of deferred sales inducements after gross profit adjustments | $ | 408,548 | $ | 152,692 | $ | 438,164 | |||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed index annuities - embedded derivatives | Fixed index annuities - embedded derivatives | $ | (2,561,676) | $ | (876,803) | $ | (1,922,085) | ||||||||||||||||||||||||||||||||||||||||||||

| Other changes in difference between policy benefit reserves computed using derivative accounting vs. long-duration contracts accounting | 648,580 | 520,863 | 635,298 | ||||||||||||||||||||||||||||||||||||||||||||||||

| Reinsurance related embedded derivative | Reinsurance related embedded derivative | (439,502) | (2,362) | — | |||||||||||||||||||||||||||||||||||||||||||||||

| $ | (2,352,598) | $ | (358,302) | $ | (1,286,787) | ||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||

| (Dollars in thousands) | |||||||||||||||||

| Amortization of deferred policy acquisition costs before gross profit adjustments | $ | 330,290 | $ | 181,589 | $ | 368,139 | |||||||||||

| Gross profit adjustments: | |||||||||||||||||

| Fair value accounting for derivatives and embedded derivatives | 290,905 | 88,576 | 293,827 | ||||||||||||||

| Net realized losses on investments | (5,895) | (1,837) | (12,412) | ||||||||||||||

| Amortization of deferred policy acquisition costs after gross profit adjustments | $ | 615,300 | $ | 268,328 | $ | 649,554 | |||||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | 2020 | |||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Salary and benefits | Salary and benefits | $ | 162,061 | $ | 139,155 | $ | 95,815 | ||||||||||||||||||||||||||||||||||||||||||||

| Other | Other | 77,555 | 104,557 | 87,821 | |||||||||||||||||||||||||||||||||||||||||||||||

| Total other operating costs and expenses | Total other operating costs and expenses | $ | 239,616 | $ | 243,712 | $ | 183,636 | ||||||||||||||||||||||||||||||||||||||||||||

| December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Carrying Amount | Percent | Carrying Amount | Percent | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, | December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Carrying Amount | Carrying Amount | Percent | Carrying Amount | Percent | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities: | Fixed maturity securities: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | U.S. Government and agencies | $ | 169,071 | 0.4 | % | $ | 1,078,746 | 1.9 | % | $ | 171,141 | 0.4 | 0.4 | % | $ | 169,071 | 0.4 | 0.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

| States, municipalities and territories | States, municipalities and territories | 3,822,943 | 8.5 | % | 3,758,761 | 6.5 | % | States, municipalities and territories | 3,075,024 | 7.7 | 7.7 | % | 3,822,943 | 8.5 | 8.5 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Foreign corporate securities and foreign governments | Foreign corporate securities and foreign governments | 616,938 | 1.4 | % | 375,097 | 0.6 | % | Foreign corporate securities and foreign governments | 408,936 | 1.0 | 1.0 | % | 616,938 | 1.4 | 1.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate securities | Corporate securities | 20,201,774 | 44.8 | % | 32,631,189 | 57.0 | % | Corporate securities | 16,076,506 | 40.0 | 40.0 | % | 20,201,774 | 44.8 | 44.8 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Residential mortgage backed securities | Residential mortgage backed securities | 1,366,927 | 3.0 | % | 1,125,049 | 2.0 | % | Residential mortgage backed securities | 1,208,317 | 3.0 | 3.0 | % | 1,366,927 | 3.0 | 3.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commercial mortgage backed securities | Commercial mortgage backed securities | 3,447,075 | 7.6 | % | 4,682,900 | 8.2 | % | Commercial mortgage backed securities | 2,624,123 | 6.5 | 6.5 | % | 3,447,075 | 7.6 | 7.6 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other asset backed securities | Other asset backed securities | 5,155,254 | 11.4 | % | 5,146,567 | 9.0 | % | Other asset backed securities | 5,202,395 | 12.9 | 12.9 | % | 5,155,254 | 11.4 | 11.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total fixed maturity securities | Total fixed maturity securities | 34,779,982 | 77.1 | % | 48,798,309 | 85.2 | % | Total fixed maturity securities | 28,766,442 | 71.5 | 71.5 | % | 34,779,982 | 77.1 | 77.1 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mortgage loans on real estate | Mortgage loans on real estate | 6,778,977 | 15.0 | % | 5,650,480 | 9.9 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mortgage loans on real estate | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mortgage loans on real estate | 7,231,667 | 18.0 | % | 6,778,977 | 15.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Real estate investments | Real estate investments | 1,056,063 | 2.3 | % | 337,939 | 0.6 | % | Real estate investments | 1,334,247 | 3.3 | 3.3 | % | 1,056,063 | 2.3 | 2.3 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Limited partnerships and limited liability companies | Limited partnerships and limited liability companies | 1,266,779 | 2.8 | % | 520,120 | 0.9 | % | Limited partnerships and limited liability companies | 1,089,591 | 2.7 | 2.7 | % | 1,266,779 | 2.8 | 2.8 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Derivative instruments | Derivative instruments | 431,727 | 1.0 | % | 1,277,480 | 2.2 | % | Derivative instruments | 1,207,288 | 3.0 | 3.0 | % | 431,727 | 1.0 | 1.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other investments | Other investments | 829,900 | 1.8 | % | 690,344 | 1.2 | % | Other investments | 590,271 | 1.5 | 1.5 | % | 829,900 | 1.8 | 1.8 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| 45,143,428 | 100.0 | % | 57,274,672 | 100.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 40,219,506 | 40,219,506 | 100.0 | % | 45,143,428 | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | Coinsurance investments (1) | 6,181,870 | 3,101,832 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 51,325,298 | $ | 60,376,504 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2022 | 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rating Agency Rating | Amortized Cost | Carrying Amount | Percent of Fixed Maturity Securities | Amortized Cost | Carrying Amount | Percent of Fixed Maturity Securities | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, | December 31, | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2023 | 2023 | 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rating Agency Rating (2) | Rating Agency Rating (2) | Amortized Cost | Carrying Amount | Percent of Fixed Maturity Securities | Amortized Cost | Carrying Amount | Percent of Fixed Maturity Securities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aaa/Aa/A | Aaa/Aa/A | $ | 24,462,459 | $ | 21,723,282 | 62.5 | % | $ | 24,943,232 | $ | 27,496,506 | 56.4 | % | Aaa/Aa/A | $ | 19,237,683 | $ | $ | 17,030,736 | 59.8 | 59.8 | % | $ | 24,462,459 | $ | $ | 21,723,282 | 62.5 | 62.5 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Baa | Baa | 14,228,490 | 12,434,302 | 35.7 | % | 18,443,171 | 20,147,369 | 41.3 | % | Baa | 12,036,591 | 10,801,336 | 10,801,336 | 37.9 | 37.9 | % | 14,228,490 | 12,434,302 | 12,434,302 | 35.7 | 35.7 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total investment grade | Total investment grade | 38,690,949 | 34,157,584 | 98.2 | % | 43,386,403 | 47,643,875 | 97.7 | % | Total investment grade | 31,274,274 | 27,832,072 | 27,832,072 | 97.7 | 97.7 | % | 38,690,949 | 34,157,584 | 34,157,584 | 98.2 | 98.2 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ba | Ba | 554,605 | 485,166 | 1.4 | % | 899,253 | 930,321 | 1.9 | % | Ba | 539,417 | 489,286 | 489,286 | 1.7 | 1.7 | % | 554,605 | 485,166 | 485,166 | 1.4 | 1.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| B | B | 94,185 | 79,058 | 0.2 | % | 104,443 | 117,989 | 0.2 | % | B | 144,657 | 128,150 | 128,150 | 0.4 | 0.4 | % | 94,185 | 79,058 | 79,058 | 0.2 | 0.2 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Caa | Caa | 20,020 | 18,540 | 0.1 | % | 38,484 | 39,354 | 0.1 | % | Caa | 21,295 | 18,497 | 18,497 | 0.1 | 0.1 | % | 20,020 | 18,540 | 18,540 | 0.1 | 0.1 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ca and lower | Ca and lower | 40,664 | 39,634 | 0.1 | % | 61,352 | 66,770 | 0.1 | % | Ca and lower | 30,504 | 31,383 | 31,383 | 0.1 | 0.1 | % | 40,664 | 39,634 | 39,634 | 0.1 | 0.1 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total below investment grade | Total below investment grade | 709,474 | 622,398 | 1.8 | % | 1,103,532 | 1,154,434 | 2.3 | % | Total below investment grade | 735,873 | 667,316 | 667,316 | 2.3 | 2.3 | % | 709,474 | 622,398 | 622,398 | 1.8 | 1.8 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 39,400,423 | 34,779,982 | 100.0 | % | 44,489,935 | 48,798,309 | 100.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 32,010,147 | 32,010,147 | 28,499,388 | 100.0 | % | 39,400,423 | 34,779,982 | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | Coinsurance investments (1) | 5,465,596 | 5,024,635 | 2,509,248 | 2,507,634 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 44,866,019 | $ | 39,804,617 | $ | 46,999,183 | $ | 51,305,943 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NAIC Designation | NRSRO Equivalent Rating | |||||||

| 1 | Aaa/Aa/A | |||||||

| 2 | Baa | |||||||

| 3 | Ba | |||||||

| 4 | B | |||||||

| 5 | Caa | |||||||

| 6 | Ca and lower | |||||||

| December 31, 2022 | December 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NAIC Designation | Amortized Cost | Fair Value | Carrying Amount | Percentage of Total Carrying Amount | Amortized Cost | Fair Value | Carrying Amount | Percentage of Total Carrying Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | December 31, 2023 | December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

NAIC Designation (2) | NAIC Designation (2) | Amortized Cost | Fair Value | Carrying Amount | Percentage of Total Carrying Amount | Amortized Cost | Fair Value | Carrying Amount | Percentage of Total Carrying Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | 1 | $ | 24,466,961 | $ | 21,752,775 | $ | 21,752,775 | 62.5 | % | $ | 25,378,938 | $ | 28,006,835 | $ | 28,006,835 | 57.4 | % | $ | 19,330,614 | $ | $ | 17,116,519 | $ | $ | 17,116,519 | 60.1 | 60.1 | % | $ | 24,466,961 | $ | $ | 21,752,775 | $ | $ | 21,752,775 | 62.5 | 62.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | 2 | 14,185,506 | 12,398,001 | 12,398,001 | 35.7 | % | 18,028,077 | 19,667,529 | 19,667,529 | 40.3 | % | 2 | 11,895,433 | 10,680,088 | 10,680,088 | 10,680,088 | 10,680,088 | 37.5 | 37.5 | % | 14,185,506 | 12,398,001 | 12,398,001 | 12,398,001 | 12,398,001 | 35.6 | 35.6 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | 3 | 562,190 | 490,198 | 490,198 | 1.4 | % | 909,173 | 941,071 | 941,071 | 2.0 | % | 3 | 517,425 | 476,419 | 476,419 | 476,419 | 476,419 | 1.7 | 1.7 | % | 562,190 | 490,198 | 490,198 | 490,198 | 490,198 | 1.5 | 1.5 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | 4 | 109,409 | 91,495 | 91,495 | 0.3 | % | 133,070 | 147,160 | 147,160 | 0.3 | % | 4 | 168,694 | 147,692 | 147,692 | 147,692 | 147,692 | 0.5 | 0.5 | % | 109,409 | 91,495 | 91,495 | 91,495 | 91,495 | 0.3 | 0.3 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | 5 | 61,721 | 36,738 | 36,738 | 0.1 | % | 16,496 | 15,357 | 15,357 | — | % | 5 | 88,581 | 68,538 | 68,538 | 68,538 | 68,538 | 0.2 | 0.2 | % | 61,721 | 36,738 | 36,738 | 36,738 | 36,738 | 0.1 | 0.1 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6 | 6 | 14,636 | 10,775 | 10,775 | — | % | 24,181 | 20,357 | 20,357 | — | % | 6 | 9,400 | 10,132 | 10,132 | 10,132 | 10,132 | — | — | % | 14,636 | 10,775 | 10,775 | 10,775 | 10,775 | — | — | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 39,400,423 | 34,779,982 | 34,779,982 | 100.0 | % | 44,489,935 | 48,798,309 | 48,798,309 | 100.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 32,010,147 | 32,010,147 | 28,499,388 | 28,499,388 | 100.0 | % | 39,400,423 | 34,779,982 | 34,779,982 | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | Coinsurance investments (1) | 5,465,596 | 5,024,635 | 5,024,635 | 2,509,248 | 2,507,634 | 2,507,634 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 44,866,019 | $ | 39,804,617 | $ | 39,804,617 | $ | 46,999,183 | $ | 51,305,943 | $ | 51,305,943 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Amortized Cost | Unrealized Losses, Net of Allowance | Allowance for Credit Losses | Fair Value | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Number of Securities | Amortized Cost | Unrealized Losses, Net of Allowance | Allowance for Credit Losses | Fair Value | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | Fixed maturity securities, available for sale: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | U.S. Government and agencies | 27 | $ | 165,746 | $ | (4,637) | $ | — | $ | 161,109 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| States, municipalities and territories | States, municipalities and territories | 514 | 3,265,080 | (574,814) | — | 2,690,266 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Foreign corporate securities and foreign governments | Foreign corporate securities and foreign governments | 43 | 590,944 | (74,151) | — | 516,793 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate securities | Corporate securities | 2,103 | 21,393,656 | (3,224,609) | (3,214) | 18,165,833 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Residential mortgage backed securities | Residential mortgage backed securities | 219 | 1,235,672 | (126,368) | (133) | 1,109,171 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commercial mortgage backed securities | Commercial mortgage backed securities | 339 | 3,750,331 | (391,966) | — | 3,358,365 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other asset backed securities | Other asset backed securities | 567 | 4,579,149 | (382,563) | — | 4,196,586 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,049 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,639 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,812 | 34,980,578 | (4,779,108) | (3,347) | 30,198,123 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | 698 | 3,085,834 | (504,739) | — | 2,581,095 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4,510 | $ | 38,066,412 | $ | (5,283,847) | $ | (3,347) | $ | 32,779,218 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | Fixed maturity securities, available for sale: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Government and agencies | U.S. Government and agencies | 8 | $ | 761,102 | $ | (124) | $ | — | $ | 760,978 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| States, municipalities and territories | States, municipalities and territories | 42 | 173,106 | (2,485) | (2,776) | 167,845 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Foreign corporate securities and foreign governments | Foreign corporate securities and foreign governments | 3 | 34,673 | (801) | — | 33,872 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate securities | Corporate securities | 176 | 1,433,317 | (26,035) | — | 1,407,282 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Residential mortgage backed securities | Residential mortgage backed securities | 74 | 280,044 | (2,093) | (70) | 277,881 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Commercial mortgage backed securities | Commercial mortgage backed securities | 89 | 795,405 | (16,553) | — | 778,852 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other asset backed securities | Other asset backed securities | 577 | 3,118,385 | (50,018) | — | 3,068,367 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 969 | 6,596,032 | (98,109) | (2,846) | 6,495,077 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,812 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (1) | Coinsurance investments (1) | 458 | 1,327,173 | (14,261) | — | 1,312,912 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,427 | $ | 7,923,205 | $ | (112,370) | $ | (2,846) | $ | 7,807,989 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4,510 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NAIC Designation | Carrying Value of Securities with Gross Unrealized Losses | Percent of Total | Gross Unrealized Losses (1) | Percent of Total | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| NAIC Designation (2) | NAIC Designation (2) | Carrying Value of Securities with Gross Unrealized Losses | Percent of Total | Gross Unrealized Losses (1) | Percent of Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | 1 | $ | 18,396,691 | 60.9 | % | $ | (2,836,027) | 59.4 | % | $ | 15,299,508 | 59.8 | 59.8 | % | $ | (2,254,792) | 63.0 | 63.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | 2 | 11,207,008 | 37.1 | % | (1,825,520) | 38.2 | % | 2 | 9,631,686 | 37.7 | 37.7 | % | (1,240,985) | 34.7 | 34.7 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | 3 | 465,867 | 1.6 | % | (72,976) | 1.5 | % | 3 | 412,128 | 1.6 | 1.6 | % | (40,770) | 1.1 | 1.1 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | 4 | 89,686 | 0.3 | % | (17,922) | 0.4 | % | 4 | 145,172 | 0.6 | 0.6 | % | (21,005) | 0.6 | 0.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | 5 | 29,075 | 0.1 | % | (25,037) | 0.5 | % | 5 | 66,883 | 0.3 | 0.3 | % | (20,174) | 0.6 | 0.6 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6 | 6 | 9,796 | — | % | (1,626) | — | % | 6 | 1,838 | — | — | % | (148) | — | — | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 25,557,215 | 25,557,215 | 100.0 | % | (3,577,874) | 100.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (3) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 30,198,123 | 100.0 | % | (4,779,108) | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (2) | 2,581,095 | (504,739) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 32,779,218 | $ | (5,283,847) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1 | 1 | $ | 3,825,403 | 58.9 | % | $ | (33,823) | 34.4 | % | $ | 18,396,691 | 60.9 | 60.9 | % | $ | (2,836,027) | 59.4 | 59.4 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | 2 | 2,233,761 | 34.4 | % | (47,154) | 48.1 | % | 2 | 11,207,008 | 37.1 | 37.1 | % | (1,825,520) | 38.2 | 38.2 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | 3 | 376,933 | 5.8 | % | (13,723) | 14.0 | % | 3 | 465,867 | 1.6 | 1.6 | % | (72,976) | 1.5 | 1.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | 4 | 33,229 | 0.5 | % | (1,083) | 1.1 | % | 4 | 89,686 | 0.3 | 0.3 | % | (17,922) | 0.4 | 0.4 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | 5 | 9,506 | 0.1 | % | (1,140) | 1.2 | % | 5 | 29,075 | 0.1 | 0.1 | % | (25,037) | 0.5 | 0.5 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6 | 6 | 16,244 | 0.3 | % | (1,186) | 1.2 | % | 6 | 9,796 | — | — | % | (1,626) | — | — | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6,495,076 | 100.0 | % | (98,109) | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (2) | 1,312,912 | (14,261) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | 7,807,988 | $ | (112,370) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 30,198,123 | 30,198,123 | 100.0 | % | (4,779,108) | 100.0 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (3) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Amortized Cost, Net of Allowance (1) | Fair Value | Gross Unrealized Losses, Net of Allowance (1) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Number of Securities | Amortized Cost, Net of Allowance (1) | Fair Value | Gross Unrealized Losses, Net of Allowance (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | Fixed maturity securities, available for sale: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | Investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 984 | $ | 6,296,895 | $ | 5,968,793 | $ | (328,102) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 2,308 | 24,207,057 | 20,481,666 | (3,725,391) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | 427 | 3,761,294 | 3,153,240 | (608,054) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total investment grade | Total investment grade | 3,719 | 34,265,246 | 29,603,699 | (4,661,547) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Below investment grade: | Below investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 12 | 51,711 | 47,494 | (4,217) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 34 | 319,964 | 265,726 | (54,238) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | 47 | 340,310 | 281,204 | (59,106) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total below investment grade | 93 | 711,985 | 594,424 | (117,561) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total below investment grade (2) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,047 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,637 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,812 | 34,977,231 | 30,198,123 | (4,779,108) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (2) | 698 | 3,085,834 | 2,581,095 | (504,739) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4,510 | $ | 38,063,065 | $ | 32,779,218 | $ | (5,283,847) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fixed maturity securities, available for sale: | Fixed maturity securities, available for sale: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | Investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 567 | $ | 4,255,321 | $ | 4,223,368 | $ | (31,953) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 39 | 132,110 | 130,156 | (1,954) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | 281 | 1,752,779 | 1,705,640 | (47,139) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total investment grade | Total investment grade | 887 | 6,140,210 | 6,059,164 | (81,046) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Below investment grade: | Below investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 11 | 43,745 | 42,994 | (751) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 7 | 28,544 | 25,706 | (2,838) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | 64 | 380,686 | 367,213 | (13,473) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total below investment grade | Total below investment grade | 82 | 452,975 | 435,913 | (17,062) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 969 | 6,593,185 | 6,495,077 | (98,108) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (2) | 458 | 1,327,173 | 1,312,912 | (14,261) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,427 | $ | 7,920,358 | $ | 7,807,989 | $ | (112,369) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3,812 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4,510 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Amortized Cost, Net of Allowance (1) | Fair Value | Gross Unrealized Losses, Net of Allowance (1) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of Securities | Number of Securities | Amortized Cost, Net of Allowance (1) | Fair Value | Gross Unrealized Losses, Net of Allowance (1) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | (Dollars in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2023 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | Investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 333 | $ | 3,955,378 | $ | 3,062,075 | $ | (893,303) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 299 | 4,496,559 | 3,146,868 | (1,349,691) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | 1 | 40,351 | 26,854 | (13,497) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total investment grade | Total investment grade | 633 | 8,492,288 | 6,235,797 | (2,256,491) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Below investment grade: | Below investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | 8 | 61,481 | 47,057 | (14,424) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | 7 | 111,990 | 71,271 | (40,719) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total below investment grade | Total below investment grade | 15 | 173,471 | 118,328 | (55,143) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 648 | 8,665,759 | 6,354,125 | (2,311,634) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 455 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Coinsurance investments (2) | Coinsurance investments (2) | 423 | 1,250,509 | 859,395 | (391,114) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1,071 | $ | 9,916,268 | $ | 7,213,520 | $ | (2,702,748) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 740 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | Investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment grade: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | — | $ | — | $ | — | $ | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Six months or more and less than twelve months | Six months or more and less than twelve months | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Twelve months or greater | Twelve months or greater | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total investment grade | Total investment grade | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Below investment grade: | Below investment grade: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | Less than six months | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Less than six months | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||