This Amendment No. 1 on Form 10-K/A (the “Amendment”) amends our Annual Report (including the following section regarding Management's Discussion and Analysis of Financial Condition and Results of Operations) contains forward-looking statements regarding our business, financial condition, results of operations and prospects. Words such as "expects," "anticipates," "intends," "plans," "believes," "seeks," "estimates" and similar expressions or variations of such words are intended to identify forward-looking statements, but are not the exclusive means of identifying forward-looking statements in this Annual Report. Additionally, statements concerning future matters such as the development of new products, enhancements or technologies, sales levels, expense levels and other statements regarding matters that are not historical are forward-looking statements.

Although forward-looking statements in this Annual Report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include without limitation those discussed under the heading "Risk Factors" in Item 1A below, as well as those discussed elsewhere in this Annual Report. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report. We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this Annual Report. Readers are urged to carefully review and consider the various disclosures made in this Annual Report, which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

AXT, Inc. ("AXT", "we," "us," and "our" refer to AXT, Inc. and all of its subsidiaries) is a leading developer and producer of high-performance compound and single element semiconductor substrates, including substrates made from gallium arsenide (GaAs), indium phosphide (InP) and germanium (Ge). We currently sell the following substrate products in the sizes and for the applications indicated:

We manufacture all of our semiconductor substrates using our proprietary vertical gradient freeze (VGF) technology. Most of our revenue is from sales of GaAs substrates. We manufacture all of our products in the People's Republic of China (PRC or China), which generally has favorable costs for facilities and labor. We also have five joint ventures in China that provide us favorable pricing, reliable supply and shorter lead-times for raw materials central to our final manufactured products. We consolidate, for accounting purposes, three of these joint ventures and have equity interests of 25% in

each of the other two. We use our direct sales force in the United States and independent sales representatives in Europe and Asia to market our substrates. Our ten largest customers for 2007 were: Avago Technologies Manufacturing (Singapore) Pte. Ltd., IQE, plc. MAC Corporation, MBE Technology Pte. Ltd., Osram Opto Semiconductors GmbH, Picogiga International SAS, Sumika Epi Solution Co., Ltd., Tokyo Supply Ltd., Visual Photonics Epitaxy Co., Ltd., and Xiamen Xinde Co., Ltd. We believe that, as the demand for compound semiconductor substrates is expected to increase, we are positioned to leverage our PRC-based manufacturing capabilities and access to favorably priced raw materials to increase our market share.

We were incorporated in California in December 1986 and reincorporated in Delaware in May 1998. We changed our name from American Xtal Technology, Inc. to AXT, Inc. in July 2000. Our corporate office is located at 4281 Technology Drive, Fremont, California 94538, and our telephone number at this address is (510) 683-5900.

Industry Background

Certain electronic and opto-electronic applications have performance requirements that exceed the capabilities of conventional silicon substrates and often require high-performance compound or single element substrates. Examples of higher performance non-silicon based substrates include GaAs, InP, gallium nitride (GaN), silicon carbide (SiC) and Ge.

For example, power amplifiers and radio frequency integrated circuits for wireless handsets are made with semi-insulating GaAs substrates. Semi-conducting GaAs substrates are used to create opto-electronic products including high brightness light emitting diodes (HBLEDs) which are often used to backlight wireless handsets and liquid crystal display (LCD) TVs and for automotive and general illumination applications. InP is a high performance semiconductor substrate used in broadband and fiber optic applications. Ge substrates are used in emerging applications such as solar cells for space and terrestrial photovoltaic applications.

The total market for high performance GaAs and Ge substrates is expected to grow from $607 million in 2008 to $676 million in 2012, according to an October 2007 report from Strategy Analytics, an independent research firm.

The primary costs of manufacturing compound semiconductor substrates are labor, raw materials and manufacturing equipment such as crystal growing furnaces. Substrate manufacturers are shifting production to larger wafers to reduce manufacturing costs.

Suppliers of compound semiconductor substrates typically compete on product quality, product lead-time, price, device performance, meeting customer specifications and providing customer support. A compound semiconductor substrate customer typically has two or three substrate suppliers that it has qualified for the production of its products. These qualified suppliers must meet industry-standard specifications for quality, on-time delivery and customer support. Once a substrate supplier has qualified with a customer, price, consistent quality and current and future product delivery lead times become the most important competitive factors. A supplier that cannot meet customers' current lead times or that a customer perceives will not be able to meet future demand and provide consistent quality can lose current market share.

The AXT Advantage

We believe that we benefit from the following advantages:

•Low-cost manufacturing operation in the PRC.Since 2004, we have manufactured all of our products in China, which generally has favorable costs for facilities and labor compared to comparable facilities in the United States or Europe. Approximately 1,019 of our 1,057

•Favorable access to raw materials.Our joint ventures provide us favorable pricing, reliable supply and shorter lead-times for raw materials central to our final manufactured products. These materials include gallium, arsenic, germanium, germanium dioxide, paralytic boron nitride crucibles and boron oxide. As a result, we believe that our joint ventures will enable us to meet potential increases in demand from our customers by providing a more stable supply of raw materials at lower prices.•Flexible manufacturing infrastructure.Our total manufacturing space in China is approximately 190,000 square feet, 90,000 square feet of which we currently use and the remainder of which we have configured for relatively rapid expansion. We believe that our competitors typically purchase crystal growing furnaces from original equipment manufacturers. In contrast, we design and build our own VGF crystal growing furnaces, which should allow us to increase our production capacity more quickly and cost effectively.

employees are in China. Our primary competitors have their manufacturing operations in Germany or Japan.

Given these advantages, we believe that, as the demand for compound semiconductor substrates increases, we are positioned to leverage our PRC-based manufacturing capabilities and access to favorably priced raw materials to increase our market share.

Strategy

Our goal is to become the leading worldwide supplier of high-performance compound and single element semiconductor substrates. Key elements of our strategy include:

Continue to provide customers high and consistent quality products and service. We seek to improve our manufacturing processes continually in order to meet and exceed our customers' high product quality standards, ensure on-time delivery of our products and optimize the cost of ownership. We expect to continue to improve our manufacturing processes in 2008 by adding new or additional equipment, automating additional processes, and streamlining performance. In addition, we plan to continue to enhance our support functions, including service and applications engineering.

Increase market share. We intend to leverage our product quality, competitive pricing and lead times both to establish relationships with new customers and to increase our market share with current customers in the integrated circuits for wireless handsets and HBLED markets.

Add capacity to meet customers' increasing demand for substrates. We believe that the markets for our substrates are currently capacity constrained. We are adding additional capacity in order to meet our customers' current and anticipated increased demands, specifically in 6" GaAs substrates.

Establish leadership in emerging substrate applications. We intend to expand our served markets by exploring new opportunities for our substrates. For example, due to Ge's inherent high efficiency and the increasing supply constraints of traditional poly-silicon, some customers have begun to use of Ge substrates for terrestrial solar cell applications.

Technology enhancements. We continue to focus on technology development in the areas of VGF technology enhancements and Czochralski (CZ) and Liquid Encapsulated Czochralski (LEC) crystal growth for semi-conducting GaAs and Ge substrates. We also continue to focus on applying our technological expertise to the design of our manufacturing processes, to upgrade and improve these processes and deliver high quality products to our customers more efficiently and in higher volumes.

Technology

Our core technologies include our proprietary VGF technique used to produce high quality crystals that are processed into compound substrates, and the technologies of our joint venture companies,

which enable us to manufacture a range of products that are used in the manufacture of compound semiconductor substrates or can be sold as raw materials to third parties.

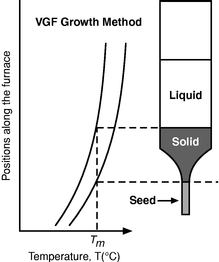

Our VGF technique is designed to control the crystal-growth process with minimal temperature variation and is the current technique we use to produce our GaAs, InP and Ge substrates. Unlike traditional techniques, our VGF technique places the hot compound melt above the cool crystal, and minimizes the temperature gradient between the crystal and the melt which reduces the turbulence at the interface of the melt and the solid crystal. In comparison, in the LEC technique the melt and crystal are inverted, there is a higher temperature gradient between the melt and the crystal, and more turbulence at the interface of the melt and solid crystal. These aspects of the VGF technique enable us to grow crystals that have a relatively low defect density and high uniformity. The crystal and the resulting substrate are mechanically strong, resulting in lower breakage rates during a customer's manufacturing process. Since the temperature gradient is controlled electronically rather than by physical movement, the sensitive crystal is not disturbed as it may be during some competitors' VGF-like growth processes. In addition, the melt and growing crystal are contained in a closed chamber, which isolates the crystal from the outside environment to reduce potential contamination. This substrate isolation allows for more precise control of the gallium-to-arsenic ratio, resulting in better consistency and uniformity of the crystals.

Although we are exploring the use of other methods to control the crystal-growth process, including the CZ and LEC methods for select applications, for our traditional GaAs substrates, our VGF technique offers several benefits for producing our GaAs substrates when compared to traditional crystal growing technologies. The Horizontal Bridgman (HB) technique is the traditional method for producing semi-conducting GaAs substrates for opto-electronic applications, but because of the techniques used to hold the GaAs melt, the HB technique cannot be used cost-effectively to produce substrates greater than three inches in diameter. In addition, the HB technique houses the GaAs melt in a quartz container during the growth process, which can contaminate the GaAs melt with silicon impurities, making it unsuitable for producing semi-insulating GaAs substrates.

Our VGF technique also offers advantages over the LEC technique for producing semi-insulating GaAs substrates for wireless applications. Unlike the VGF technique, the LEC technique can result in greater turbulence in the melt, and at a temperature gradient that is significantly higher than the VGF technique, which can cause LEC-grown crystals to have a higher dislocation density than VGF-grown crystals, resulting in a higher rate of breakage during the device manufacturing process. However, the LEC technique can be useful for GaAs semi-conducting substrates since the LED application specifications and requirements are less stringent than those of wireless applications.

We design, develop, manufacture and distribute high-performance semiconductor substrates. We make semi-insulating GaAs substrates used in applications such as amplifiers and switches for wireless handsets, and semi-conducting GaAs substrates used to create opto-electronic products including HBLEDs, which are often used to backlight wireless handsets and LCD TVs and for automotive and general illumination applications. InP is a high performance semiconductor substrate used in broadband and fiber optic applications. Ge substrates are used in emerging applications such as triple junction solar cells for space and terrestrial photovoltaic applications and for optical applications.

The table below sets forth our products and selected applications:

Substrates. We currently sell compound substrates manufactured from GaAs and InP, as well as single-element substrates manufactured from Ge. We supply GaAs substrates in two-, three-, four-, five- and six-inch diameters. We manufacture InP substrates in two-, three- and four-inch diameters and Ge substrates in two- and four-inch diameters.

Materials. We participate in five joint ventures in China that sell raw materials used by us in substrate manufacturing and by others. These joint ventures produce products including 99.99% pure gallium (4N Ga), high purity gallium, arsenic, and germanium, germanium dioxide, paralytic boron nitride (pBN) crucibles, and boron oxide (B2O3). In 2007 and 2006, sales of raw materials to parties other than us were approximately $13.8 million and $5.3 million, respectively, which comprised of all of these products.

Customers

We sell our compound semiconductor substrates and materials worldwide. Our top revenue producing customers include:

Historically, we have sold a significant portion of our products in any particular period to a limited number of customers. No customer represented greater than 10% of revenueForm 10-K for the year ended December 31, 2007 while one customer, Visual Photonics Epitaxy Co., Ltd., represented greater than 10% of revenue, totaling 12.8%, for the year ended December 31, 2006, while two customers, Osram Opto Semiconductors GmbH, and MBE Technology Pte. Ltd., represented greater than 10% of revenue, totaling 20.7%, for the year ended December 31, 2005. Our top five customers represented 33.0% of our revenue for the year ended December 31, 2007, 40.0% of our revenue for the year ended December 31, 2006, and 37.5% of our revenue for the year ended December 31, 2005. We expect that sales to a small number of customers will continue to comprise a significant portion of our revenue in the future.

There have been no third party customers for our raw materials that account for greater than 10% of revenue for the years ended December 31, 2007, 2006 and 2005. Our joint ventures are a key strategic benefit for us as they give us a strong competitive advantage of allowing our customers to work with one supplier for all their substrate and raw material requirements.

Manufacturing, Raw Materials and Supplies

We believe that our results are partially due to our manufacturing efficiency and high product yields and we continually emphasize quality and process control throughout our manufacturing operations. We manufacture all of our products at our facilities in Beijing, China, which generally has favorable costs for facilities and labor. We believe that our capital investment and subsequent operating costs are lower for our manufacturing facilities in China relative to the U.S. Many of our manufacturing operations are fully automated and computer monitored or controlled, enhancing reliability and yield, and we expect to continue to improve our processes and increase the number of automated processes in 2008. We use proprietary equipment in our substrate manufacturing operations to protect our intellectual property and control the timing and pace of capacity additions. All of our manufacturing facilities are ISO 9001 or 9002 certified. In January 2006, our Beijing facility successfully passed the ISO 14001 certification audit.

We have five joint ventures in China that provide us favorable pricing, reliable supply and shorter lead-times for raw materials central to our manufactured productsm including gallium, arsenic, germanium, germanium dioxide, pyrolitic boron nitride crucibles, and boron oxide. We believe that these joint ventures and investments will be advantageous in procuring materials to support our growth and cost management goals. In addition, we purchase supply parts, components and raw materials from several other domestic and international suppliers. We depend on a single or limited number of suppliers for certain critical materials used in the production of our substrates, such as quartz tubing, and polishing solutions. We generally purchase these materials through standard purchase orders and not pursuant to long-term supply contracts. Although we seek to maintain sufficient inventory levels of certain materials to guard against interruptions in supply and to meet our near term needs, and have to date been able to obtain sufficient supplies of materials in a timely manner, there may be shortages of certain key materials, such as gallium.

Sales and Marketing

We advertise in trade publications, distribute promotional materials, conduct marketing and sales programs, and participate in industry trade shows and conferences in order to raise market awareness of our products.

We sell our substrate products direct to customers through our direct sales force in the U.S. and through independent sales representatives in France, Germany, Japan, South Korea, Taiwan and the United Kingdom. Our direct sales force is knowledgeable in the use of compound and single-element substrates. Our applications engineers work with customers during all stages of the substrate

manufacturing process, from developing the precise composition of the substrate through manufacturing and processing the substrate to the customer's specifications. We believe that maintaining a close relationship with customers and providing them with ongoing engineering support improves customer satisfaction and will provide us with a competitive advantage in selling other substrates to our customers.

International Sales. International sales are an important part of our business. Sales to customers outside North America (primarily United States) accounted for 80% of our revenue in 2007, 71% of our revenue in 2006 and 81% of our revenue in 2005. The primary markets for sales of our substrate products outside of the United States are to customers located in Asia and Western Europe.

We also sell through our joint ventures raw materials including 4N, 6N, and 7N gallium, boron oxide, germanium, arsenic, germanium dioxide, paralytic boron nitride crucibles used in crystal growth and parts for MBE (Molecular Beam Epitaxy). Our joint ventures are a key strategic benefit for us as they give us a strong competitive advantage of allowing our customers to work with one supplier for all their substrate and raw material requirements.

Research and Development

To maintain and improve our competitive position, we focus our research and development efforts on designing new proprietary processes and products, improving the performance of existing products and reducing manufacturing costs. We have assembled a multi-disciplinary team of skilled scientists, engineers and technicians to meet our research and development objectives.

Our current substrate research and development activities focus on continued development and enhancement of GaAs, InP and Ge substrates, including haze reduction, improved yield, enhanced surface and electrical characteristics and uniformity, greater substrate strength and increased crystal length. During 2007, we continued to spend some research and development resources to reduce surface quality problems we experienced with our GaAs and InP substrates for some customers, particularly related to surface morphology. We continue to work on issues related to surface quality.

Research and development expenses were $1.7 million in 2007, compared with $2.4 million in 2006 and $1.7 million in 2005. We expect to modestly increase our rate of expenditure on research and development costs in 2008 as we explore other methods to grow our crystals.

Research and development at our joint ventures has been minimal.

Competition

The semiconductor substrate industry is characterized by rapid technological change and price erosion, as well as intense foreign and domestic competition. We believe we currently have a leading position in the market for GaAs substrates for HBLED applications primarily as a result of our expertise in VGF technology, overall product quality, response times and prices. However, we face actual and potential competition from a number of established domestic and international companies who may have advantages not available to us including substantially greater financial, technical and marketing resources; greater name recognition; and more established relationships in the industry and may utilize these advantages to expand their product offerings more quickly, adapt to new or emerging technologies and changes in customer requirements more quickly, and devote greater resources to the marketing and sale of their products.

We believe that the primary competitive factors in the markets in which our substrate products compete are:

•quality;•price;

•performance;•meeting customer specifications; and•customer support and satisfaction.

Our ability to compete in target markets also depends on factors such as:

•the timing and success of the development and introduction of new products and product features by us and our competitors;•the availability of adequate sources of raw materials;•protection of our products by effective use of intellectual property laws; and•general economic conditions.

A compound semiconductor substrate customer typically has two or three substrates suppliers that it has qualified for the production of its products. These qualified suppliers must meet industry-standard specifications for quality, on-time delivery and customer support. Once a substrate supplier has qualified with a customer, price, consistent quality and current and future product delivery lead times become the most important competitive factors. A supplier that cannot meet customers' current lead times or that a customer perceives will not be able to meet future demand and provide consistent quality can lose current market shares. Our primary competition in the market for compound semiconductor substrates includes China Crystal Technologies, Freiberger Compound Materials, Japan Energy, Mitsubishi Chemical Corporation, and Sumitomo Electric Industries. We believe that at least two of our competitors are shipping high volumes of GaAs substrates manufactured using a technique similar to our VGF technique. In addition, as a result of quality problems that we have experienced, we believe that some customers have allocated some of their requirements for VGF grown substrates across more competitors and we believe that we may have lost revenue and market share as a result of these customer decisions. In addition, we also face competition from compound semiconductor device manufacturers that produce substrates for their own internal use, including Hitachi, and from companies such as IBM that are actively developing alternative compound semiconductor materials.

We are the only compound semiconductor substrate supplier to offer a full suite of raw materials and we believe that it gives us a strong competitive advantage in our marketplace.

Protection of our Intellectual Property

Our success and the competitive position of our VGF technique depend on our ability to maintain trade secrets and other intellectual property protections. We rely on a combination of patents, trademark and trade secret laws, non-disclosure agreements and other intellectual property protection methods to protect our proprietary technology. We believe that, due to the rapid pace of technological innovation in the markets for our products, our ability to establish and maintain a position of technology leadership depends as much on the skills of our development personnel as upon the legal protections afforded our existing technologies. To protect our trade secrets, we take certain measures to ensure their secrecy, such as executing non-disclosure agreements with our employees, customers and suppliers. However, reliance on trade secrets is only an effective business practice insofar as trade secrets remain undisclosed and a proprietary product or process is not reverse engineered or independently developed.

To date, we have been issued two US patents which relate to our VGF products and processes that expire in 2021 and 2016, respectively. We have two US patent applications pending, seven foreign patent applications pending (in Patent Cooperation Treaty ("PCT")/national stage process) in Europe, Canada, China, Japan and South Korea which are based on our US patents that relate to our VGF processes. We have two issued foreign patents.

In connection with a final settlement of litigation, we entered into a global intellectual property cross-licensing agreement with Sumitomo Electric Industries, Ltd. (SEI). Under the terms of the settlement, we will make on-going royalty payments through 2012 on certain products sold by us in Japan.

In the normal course of business, we periodically receive and make inquiries regarding possible patent infringement. In dealing with such inquiries, it may become necessary or useful for us to obtain or grant licenses or other rights. However, there can be no assurance that such licenses or rights will be available to us on commercially reasonable terms. If weare not able to resolve or settle claims, obtain necessary licenses on commercially reasonable terms and/or successfully prosecute or defend its position, our business, financial condition and results of operations could be materially and adversely affected.

Environmental Regulations

We are subject to federal, state and local environmental laws and regulations, including laws in China as well as the U.S. These laws, rules and regulations govern the use, storage, discharge and disposal of hazardous chemicals during manufacturing, research and development and sales demonstrations. We maintain a number of environmental, health and safety programs that are primarily preventive in nature. As part of these programs, we regularly monitor ongoing compliance. If we fail to comply with applicable regulations, we could be subject to substantial liability for clean-up efforts, personal injury and fines or suspension or cessation of our operations.

Employees

As of December 31, 2007, we had 1,057 employees, of whom 857 were principally engaged in manufacturing, 116 in sales and administration, and 84 in research and development. Of these employees, 38 are located in the U.S., and 1,019 in China. As of December 31, 2006, we had 1,022 employees, of whom 819 were principally engaged in manufacturing, 119 in sales and administration, and 84 in research and development. Of these employees, 39 were located in the U.S., and 983 in China.

In December 2005, as part of our ongoing effort to reduce our Fremont, California facility headcount, we reduced the workforce at the facility by 15 full-time equivalent positions that we no longer required to support production and operations, or approximately 29% of the workforce based at this facility. Some of our employees in China are represented by a union, but we have never experienced a work stoppage. Although morale has been affected by our workforce reductions in California, we consider our relations with our employees to be good.

Available Information

Our principal executive offices are located at 4281 Technology Drive, Fremont, CA 94538, and our main telephone number is (510) 683-5900. The public may read and copy any material we fileoriginally filed with the Securities and Exchange Commission or SEC, at the SEC's Public Reference Room at 450 Fifth Street, N.W., Washington D.C., 20549.on March 14, 2008 (the “Original Filing”). The public may obtain information on the operationsAmendment solely amends Part IV, Item 15 of the Public Reference Room by callingOriginal Filing to refile paragraphs 1, 2, 4 and 5 of exhibits 31.1 and 31.2, certification of principal executive officer and principal financial officer, respectively.

Except for the SEC at 1-800-SEC-0330. The SEC maintains an Internet site,http://www.sec.gov, that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

Our web site is www.axt.com. We make available, free of charge, on or through our web site, our annual, quarterly and current reports, and any amendments to those reports as soon as reasonably practicable after those reports are filed with the SEC. The information on our seb siterevisions described above, this Amendment does not constitute a part of this Annual Report on Form 10-K and isamend, modify or update the Original Filing in any respect. This Amendment does not incorporated herein.

For ease of reference, wereflect events that have divided these risks and uncertainties intooccurred subsequent to the following general categories:

•Risks related to our general business;•Risks related to international aspects of our business;•Risks related to our financial results and capital structure;•Risks related to our intellectual property; and•Risks related to compliance and other legal matters.

Risks Related to Our General Business

The Chinese Government has indicated that it plans to shutdown polluting factories for nine weeks within a 200 kilometer radius of Beijing to clear the smog for the 2008 Olympics, and if such restrictions are imposed on our facilities, it could materially and adversely impact our results of operations and our financial condition.

Although we do not currently believe that we will have anyfiling of the following restrictions imposed on us,Original Filing and, we currently understand from the Chinese authorities that our operations are not a polluting factory and will not be affected by these restrictions, the Chinese government has indicated that it plans to shutdown polluting factories for nine weeks from July 17, 2008 through September 20, 2008 within a 200 kilometer radius of Beijing to clear the smog for the 2008 Olympics and Paralympics. The areas reported to be affected include Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia and Shandong provinces. The radius could be expanded by the Chinese Government if the air quality does not improve sufficiently prior to the Olympic Games. In addition, there could be a shut down of material transportation and power plants to clear the air. Some polluting factories have been given time limits to reduce emissions and others will have restricted operations from August 8, 2008 to August 24, 2008. Some companies may have to adjust their production time, some may have to reduce production and some may have to suspend their operations duringaccordingly, this period, particularly businesses in heavily-polluting industries of power, iron and steel, chemicals and concrete. If, in the future, restrictions are imposed on our operations, including any requirement to curtail or close production during the Olympic Games, our ability to meet customer demand or supply current or new orders would be significantly impacted. Customers could then be required to purchase product from our competitors, causing our competitors to take market share from us, and could result in our customers supplying future needs from our competitors. Land transportation and air transportation of certain raw materials is likely to be restricted during this period as well. Restrictions on material transport could limit our ability to transport our product, and could result in bottlenecks at shipping ports, limiting our ability to deliver products to our customers. We may increase our stock of critical materials (such as arsenic, gallium, and other chemicals) for use during the period that these restrictions are likely to last, which will increase our use of cash and increase in inventory level. Any of these restrictions could materially and adversely impact our results of operations and our financial condition.

Defects in our products could diminish demand for our products.

Our products are complex and may contain defects. We have experienced quality control problems with many of our products, which caused customers to return products to us, reduce orders for our products, or both. Although our quality has improved, resulting in some increases in product sales, we believe that we continue to experience some reduction in orders as a result of our prior product quality problems. If we continue to experience quality control problems, or experience these or other problems in new products, customers may cancel or reduce orders or purchase products from our competitors,

we may be unable to maintain or increase sales to our customers and sales of our products could decline. Defects in our products could cause us to incur higher manufacturing costs and suffer product returns and additional service expenses, all of which could adversely impact our operating results.

If new products developed by us contain defects when released, our customers may be dissatisfied and we may suffer negative publicity or customer claims against us, lose sales or experience delays in market acceptance of our new products.

Decreases in average selling prices of our products may reduce gross margins.

The market for compound semiconductor substrates is characterized by pressures on average selling prices resulting from factors such as increased competition or overcapacity. We have experienced and expect to continue to experience price pressures on our products, and if average selling prices decline in the future, our revenue and gross margins could decline. We may be unable to reduce the cost of our products sufficiently to offset the effect of lower selling prices and allow us to keep pace with competitive pricing pressures, and our margins could be adversely affected.

The loss of one or more of our key substrate customers would significantly hurt our operating results.

A small number of substrate customers have historically accounted for a substantial portion of our total revenue. Our top five customers represented 33.0% of revenues for the year ended December 31, 2007, 40.0% of revenue for the year ended December 31, 2006, and 37.5% of revenue for the year ended December 31, 2005. We expect that a significant portion of our future revenue will continue to be derived from a limited number of substrate customers. Our customers are not obligated to purchase a specified quantity of our products or to provide us with binding forecasts of product purchases. In addition, our customers may reduce, delay or cancel orders at any time without any significant penalty. In the past, we have experienced slower bookings, significant push-outs and cancellation of orders from customers. If we lose a major customer or if a customer cancels, reduces or delays orders, our revenue would decline. In addition, customers that have accounted for significant revenue in the past may not continue to generate revenue for us in any future period. Any delay in scheduled shipments of our products could cause revenue to fall below our expectations and the expectations of market analysts or investors, causing our stock price to decline.

Our results of operations may suffer if we do not effectively manage our inventory.

We must manage our inventory of component parts, work-in-process and finished goods effectively to meet changing customer requirements, while keeping inventory costs down and improving gross margins. Some of our products and supplies have in the past and may in the future become obsolete while in inventory due to changing customer specifications, or become excess inventory due to decreased demand for our products and an inability to sell the inventory within a foreseeable period. Furthermore, if current costs of production increase or sales prices drop below the standard prices at which we value inventory, we may need to take a charge for a reduction in inventory values. We have in the past had to take inventory valuation and impairment charges. Any future unexpected changes in demand or increases in costs of production that cause us to take additional charges for un-saleable, obsolete or excess inventory, or to reduce inventory values, could adversely affect our results of operations.

If we have low product yields, the shipment of our products may be delayed and our operating results may be adversely impacted.

Our products are manufactured using complex technologies, and the number of usable substrates we produce can fluctuate as a result of many factors, including:

•impurities in the materials used;

•contamination of the manufacturing environment;•substrate breakage;•equipment failure, power outages or variations in the manufacturing process; and•performance of personnel involved in the manufacturing process.

If our yields decrease, our revenue could decline if we are unable to produce needed product on time. At the same time, our manufacturing costs could remain fixed, or could increase. We have experienced product shipment delays and difficulties in achieving acceptable yields on both new and older products, and delays and poor yields have adversely affected our operating results. We may experience similar problems in the future and we cannot predict when they may occur or their severity. In particular, many of our manufacturing processes are new and are still being refined, which can result in lower yields.

If our manufacturing processes result in defects in our products making them unfit for use by our customers, our products would be rejected, resulting in compensation costs paid to our customers, and possible disqualification. This could lead to revenue loss and market share loss.

If we do not successfully develop new products to respond to rapidly changing customer requirements, our ability to generate revenue, obtain new customers, and retain existing customers may suffer.

Our success depends on our ability to offer new products and product features that incorporate leading technology and respond to technological advances. In addition, our new products must meet customer needs and compete effectively on quality, price and performance. The life cycles of our products are difficult to predict because the markets for our products are characterized by rapid technological change, changing customer needs and evolving industry standards. If our competitors introduce products employing new technologies or performance characteristics, our existing products could become obsolete and unmarketable. During the past three years, we have seen our competitors selling more substrates manufactured using a crystal growth technology similar to ours, which has eroded our technological differentiation. Other companies, including Triquent, are actively developing substrate materials that could be used to manufacture devices that could provide the same high-performance, low-power capabilities as GaAs- and InP-based devices at competitive prices. If these substrate materials or VGF-derived products are successfully developed and semiconductor device manufacturers adopt them, demand for our GaAs substrates could decline and our revenue could suffer.

The development of new products can be a highly complex process, and we may experience delays in developing and introducing new products. Any significant delays could cause us to fail to timely introduce and gain market acceptance of new products. Further, the costs involved in researching, developing and engineering new products could be greater than anticipated. If we fail to offer new products or product enhancements or fail to achieve higher quality products, we may not generate sufficient revenue to offset our development costs and other expenses or meet our customers' requirements.

Intense competition in the markets for our products could prevent us from increasing revenue and sustaining profitability.

The markets for our products are intensely competitive. We face competition for our substrate products from other manufacturers of substrates, such as Freiberger Compound Materials, Hitachi Cable and Sumitomo Electric, from semiconductor device manufacturers that produce substrates for their own use, and from companies, such as Triquent, that are actively developing alternative materials to GaAs and marketing semiconductor devices using these alternative materials. We believe that at least two of our major competitors are shipping high volumes of GaAs substrates manufactured using a

technique similar to our VGF technique. Other competitors may develop and begin using similar technology. If we are unable to compete effectively, our revenue may not increase and we may be unable to become profitable. We face many competitors that have a number of significant advantages over us, including:

•greater experience in the business;•more manufacturing experience;•extensive intellectual property;•broader name recognition; and•significantly greater financial, technical and marketing resources.

Our competitors could develop new or enhanced products that are more effective than our products are.

The level and intensity of competition has increased over the past year and we expect competition to continue to increase in the future. Competitive pressures caused by the current economic conditions have resulted in reductions in the prices of our products, and continued or increased competition could reduce our market share, require us to further reduce the prices of our products, affect our ability to recover costs and result in reduced gross margins.

In addition, new competitors have and may continue to emerge, such as a small crystal growing company established by a former employee of ours in China that is supplying ingots to the market. While new competitors such as this company currently do not appear to be fully competitive, competition from sources such as this could increase, particularly if these competitors are able to obtain large capital investments.

Demand for our products may decrease if our customers experience difficulty manufacturing, marketing or selling their products.

Our products are used as components in our customers' products. Accordingly, demand for our products is subject to factors affecting the ability of our customers to introduce and market their products successfully, including:

•the competition our customers face in their particular industries;•the technical, manufacturing, sales and marketing and management capabilities of our customers;•the financial and other resources of our customers; and•the inability of our customers to sell their products if they infringe third-party intellectual property rights.

If demand for the end-user applications for which our products are used decreases, or our customers are unable to develop, market and sell their products, demand for our products will decrease.

The financial condition of our customers may affect their ability to pay amounts owed to us.

Many of our customers are facing business downturns that have reduced their cash balances and their prospects. We frequently allow our customers extended payment terms after shipping products to them. Subsequent to our shipping a product, some customers have been unable to make payments when due, reducing our cash balances and causing us to incur charges to allow for a possibility that some accounts might not be paid. Customers may also be forced to file for bankruptcy. If our

customers do not pay their accounts when due, we will be required to incur charges that would reduce our earnings.

We purchase critical raw materials and parts for our equipment from single or limited sources, and could lose sales if these sources fail to fill our needs.

We depend on a limited number of suppliers for certain raw materials, components and equipment used in manufacturing our products, including key materials such as quartz tubing, polishing solutions and paralytic boron nitride. Although several of these raw materials are purchased from suppliers in which we hold an ownership interest, we generally purchase these materials through standard purchase orders and not pursuant to long-term supply contracts and no supplier guarantees supply of raw materials or equipment to us. If we lose any of our key suppliers, our manufacturing efforts could be significantly hampered and we could be prevented from timely producing and delivering products to our customers. Prior to investing in our raw material joint ventures, we sometimes experienced delays obtaining critical raw materials and spare parts, including gallium, due to shortages of these materials and could experience such delays again in the future due to shortages of materials and may be unable to obtain an adequate supply of materials. These shortages and delays could result in higher materials costs and cause us to delay or reduce production of our products. If we have to delay or reduce production, we could fail to meet customer delivery schedules and our revenue and operating results could suffer.

We have made and may continue to make strategic investments in raw materials suppliers, which may not be successful and may result in the loss of all or part of our investment.

We have made investments through our five joint ventures in raw material suppliers in China, which provide us with opportunities to gain supplies of key raw materials that are important to our substrate business. These affiliates each have a market beyond that provided by us. We do not have influence over all of these companies, each of which is located in China, and in some we have made only a strategic, minority investment. We may not be successful in achieving the financial, technological or commercial advantage upon which any given investment is premised, and we could end up losing all or part of our investment.

Our substrate products have a long qualification cycle that makes it difficult to plan our expenses and forecast our results.

Customers typically place orders with us for our substrate products three months to a year or more after our initial contact with them. The sale of our products may be subject to delays due to our customers' lengthy internal budgeting, approval and evaluation processes. During this time, we may incur substantial expenses and expend sales, marketing and management efforts while the customers evaluate our products. These expenditures may not result in sales of our products. If we do not achieve anticipated sales in a period as expected, we may experience an unplanned shortfall in our revenue. As a result, we may not be able to cover expenses, causing our operating results to vary. In addition, if a customer decides not to incorporate our products into its initial design, we may not have another opportunity to sell products to this customer for many months or even years. In the current competitive and economic climate, the average sales cycle for our products has lengthened even further and is expected to continue to make it difficult to forecast our future sales accurately. We anticipate that sales of any future substrate products will also have lengthy sales cycles and will, therefore, be subject to risks substantially similar to those inherent in the lengthy sales cycles of our current substrate products.

Risks Related to International Aspects of Our Business

Changes in tariffs, import restrictions, export restrictions or other trade barriers may reduce gross margins.

We may incur increases in costs due to changes in tariffs, import or export restrictions, or other trade barriers, or unexpected changes in regulatory requirements, any of which could reduce our gross margins. For example, in 2006, tax authorities in the PRC changed the treatment of refunds of value-added taxes that companies pay when they purchase certain raw materials, including gallium and arsenic. The cumulative effect is that our PRC joint venture companies no longer receive a refund of value-added tax for exports of gallium or arsenic, including certain shipments to our wholly-owned PRC subsidiary that are treated as exports under PRC tax regulations. Given the relatively fluid regulatory environment in the PRC, there could be additional tax or other regulatory changes in the future. Any such changes could directly and materially adversely impact our financial results and general business condition.

Our operating results depend in large part on continued customer acceptance of our substrate products manufactured in China and continued improvements in product quality.

We manufacture all of our products in China, and source most of our raw materials in China. Accordingly, we continue to seek customer qualification of our China-manufactured products. In addition, we have in the past experienced quality problems with our China-manufactured products. Our previous quality problems caused us to lose market share to our competitors, as some customers reduced their orders from us until our surface quality was as good and consistent as that offered by competitors and customers allocated their requirements for compound semiconductor substrates across more competitors. If we are unable to continue to achieve customer qualifications for our products, or if we again experience quality problems, customers may not increase purchases of our products, our China facility will become underutilized, and we will be unable to achieve expected revenue growth. We may again lose sales of our products to competitors and experience loss of market share. If we are unable to recover and retain our market share, we may be unable to grow our business.

Problems incurred by our joint ventures or venture partners could result in a material adverse impact on our financial condition or results of operations.

We have invested in five joint venture operations in China that produce products including 99.99% pure gallium (4N Ga), high purity gallium, arsenic, germanium, germanium dioxide, paralytic boron nitride (pBN) crucibles and boron oxide. We purchase a portion of the materials produced by these ventures for our use and sell the remainder of their production to third parties. Our ownership interest in these entities ranges from 25% to 83%. We consolidate the three ventures in which we own a majority or controlling financial interest and employ equity accounting for the two joint ventures in which we have a 25% interest. Several of these ventures occupy space within larger facilities owned and/or operated by one of the other venture partners. Several of these venture partners are engaged in other manufacturing activities at or near the same facility. In some facilities, we share access to certain functions, including water, hazardous waste treatment or air quality treatment. If any of our joint venture partners in any of these five ventures experiences problems with its operations, disruptions of our joint venture operations could result, having a material adverse effect on the financial condition and results of operation of our joint ventures, and correspondingly on our financial condition or results of operations.

In addition, if any of our joint ventures or venture partners with which our joint ventures share facilities is deemed to have violated applicable laws, rules or regulations governing the use, storage, discharge or disposal of hazardous chemicals during manufacturing, research and development, or sales demonstrations, the operations of our joint ventures could be adversely affected and we could be subject to substantial liability for clean-up efforts, personal injury and fines or suspension or cessation

of our joint venture operations as a result of the actions of the joint ventures or other venture partners. Employees working for our joint ventures or any of the other venture partners could bring litigation against us as a result of actions taken at the joint venture or venture partner facilities, even though we are not directly controlling the operations, including actions for exposure to chemicals or other hazardous materials at the facilities of our joint ventures or the facilities of any venture partner that are shared by our joint ventures. If litigation is brought against us, litigation is inherently uncertain and, while we would expect to defend ourselves vigorously, it is possible that our business, financial condition, results of operations or cash flows could be affected in any particular period by any litigation if brought against us, particularly if litigation with us, as a non-Chinese company, is deemed advantageous. Even if we are not deemed responsible for the actions of the joint ventures or venture partners, litigation could be costly, time consuming to defend and divert management attention; in addition, pursuit of us could occur if we are deemed to be the most financially viable of the partners.

Going forward, we believe that investing in additional joint ventures will be important to remaining competitive in our marketplace and ensuring a supply of critical raw materials. However, we may not be able to identify complementary joint venture opportunities or, even once opportunities are identified, we may not be able to reach agreement on the terms of the venture with the other venture partners. Additional joint ventures could cause us to incur contingent liabilities or other expenses, any of which could adversely affect our financial condition and operating results.

Since all of our joint venture activity is expected to occur in China, these activities could subject us to a number of risks associated with conducting operations internationally, including:

•difficulties in managing geographically disparate operations;•difficulties in enforcing agreements through non-U.S. legal systems;•unexpected changes in regulatory requirements that may limit our ability to export the venture products or sell into particular jurisdictions or impose multiple conflicting tax laws and regulations;•political and economic instability, civil unrest or war;•terrorist activities that impact international commerce;•difficulties in protecting our intellectual property rights, particularly in countries where the laws and practices do not protect proprietary rights to as great an extent as do the laws and practices of the United States;•changing laws and policies affecting economic liberalization, foreign investment, currency convertibility or exchange rates, taxation or employment; and•nationalization of foreign-owned assets, including intellectual property.

Changes in global economic conditions on our customers may adversely impact us, resulting in a decline in our revenue and profitability.

Our operating results can vary significantly based upon the impact of changes in global economic conditions on our customers. The revenue growth and profitability of our business depends on the overall demand for our substrates, and we are particularly dependent on the market conditions for the wireless, solid-state illumination, fiber optics and telecommunications industries. Because our sales are primarily to major corporate customers whose businesses fluctuate with general economic and business conditions, a softening of demand for products that use our substrates, caused by a weakening economy, may result in decreased revenue. Customers may find themselves facing excess inventory from earlier purchases, and may defer or reconsider purchasing products due to the downturn in their business and in the general economy.

We derive a significant portion of our revenue from international sales, and our ability to sustain and increase our international sales involves significant risks.

Our revenue growth depends in part on the expansion of our international sales and operations. International sales represented 80%, 71% and 81% of our total revenue for the years ended December 31, 2007, 2006 and 2005, respectively. We expect that sales to customers outside the U.S., particularly sales to customers in Asia, will continue to represent a significant portion of our revenue.

Currently, an increasing percentage of our sales is to customers headquartered in Asia. All of our manufacturing facilities and some of our suppliers are also located outside the U.S. Managing our overseas operations presents challenges, including periodic regional economic downturns, trade balance issues, varying business conditions and demands, political instability, variations in enforcement of intellectual property and contract rights in different jurisdictions, differences in the ability to develop relationships with suppliers and other local businesses, changes in U.S. and international laws and regulations including U.S. export restrictions, fluctuations in interest and currency exchange rates, the ability to provide sufficient levels of technical support in different locations, cultural differences, shipping delays and terrorist acts or acts of war, among other risks. Many of these challenges are present in China, which represents a large potential market for semiconductor devices and where we anticipate significant opportunity for growth. Global uncertainties with respect to: (i) economic growth rates in various countries; (ii) sustainability of demand for electronics products; (iii) capital spending by semiconductor manufacturers; (iv) price weakness for certain semiconductor devices; and (v) political instability in regions where we have operations may also affect our business, financial condition and results of operations.

Our dependence on international sales involves a number of risks, including:

•changes in tariffs, import restrictions, export restrictions, or other trade barriers;•unexpected changes in regulatory requirements;•longer periods to collect accounts receivable;•changes in export license requirements;•political and economic instability;•unexpected changes in diplomatic and trade relationships; and•foreign exchange rate fluctuations.

Our sales are denominated in U.S. dollars, except for sales to our Japanese and some Taiwanese customers, which are denominated in Japanese yen. Thus, increases in the value of the U.S. dollar could increase the price of our products in non-U.S. markets and make our products more expensive than competitors' products in these markets.

Also, denominating some sales in Japanese yen subjects us to fluctuations in the exchange rates between the U.S. dollar and the Japanese yen. The functional currency of our Chinese subsidiary and joint ventures is the local currency. We incur transaction gains or losses resulting from consolidation of expenses incurred in local currencies for these entities, as well as in translation of the assets and liabilities of their assets at each balance sheet date. If we do not effectively manage the risks associated with international sales, our revenue, cash flows and financial condition could be adversely affected.

If there are power shortages in the PRC, we may have to temporarily close our China operations, which would adversely impact our ability to manufacture our products and meet customer orders, and would result in reduced revenue.

In the past, the Chinese government has faced a power shortage resulting in power demand outstripping supply in peak periods. Instability in electrical supply in past years has caused sporadic outages among residential and commercial consumers causing the Chinese government to implement tough measures to ease the energy shortage, and as a result, we closed most of our operations for a week in late July 2004 in conformance with this policy.

In 2006 we were able to switch the electrical supply for our manufacturing facility onto the same power grid as that used by vital PRC government services such as hospitals and police. However, if even despite this switch, further problems with power shortages are incurred in the future, and we are required to make temporary closures of our subsidiary and joint venture operations, we may be unable to manufacture our products, and would then be unable to meet customer orders except from inventory on hand. As a result, our revenue could be adversely impacted, and our relationships with our customers could suffer, impacting our ability to generate future revenue. In addition, if power is shut off at our Beijing subsidiary at any time, either voluntarily or as a result of unplanned brownouts, during certain phases of our manufacturing process including our crystal growth phase, the work in process may be ruined and rendered unusable, causing us to incur expense that will not be covered by revenue, and negatively impacting our cost of revenue and gross margins.

Changes in China's political, social and economic environment may affect our financial performance.

Our financial performance may be affected by changes in China's political, social and economic environment. The role of the Chinese central and local governments in the Chinese economy is significant. Chinese policies toward economic liberalization, and laws and policies affecting technology companies, foreign investment, currency exchange rates and other matters could change, resulting in greater restrictions on our ability to do business and operate our manufacturing facilities in China. Any imposition of surcharges or any increase in Chinese tax rates or reduction or elimination of Chinese tax benefits could hurt our operating results. The Chinese government could revoke, terminate or suspend our license for national security and similar reasons without compensation to us. If the government of China were to take any of these actions, we would be prevented from conducting all or part of our business. Any failure on our part to comply with governmental regulations could result in the loss of our ability to manufacture our products in China.

We may face additional risks as a result of the revaluation of the Chinese currency.

In July 2005, China agreed to a shift in Chinese currency policy. It established a 2% revaluation of the renminbi and referenced the renminbi to a basket of currencies, with a daily trading band of +/-0.3%. Depending on market conditions and the state of the Chinese economy, it is possible that China will make more adjustments in the future. Over the next five to ten years, China may move to a managed float system, with opportunistic interventions. This reserve diversification may negatively impact the United States dollar and U.S. interest rates, which, in turn, could negatively impact our operating results and financial condition. The functional currency of our Chinese subsidiary, including our joint ventures, is the local currency; since most of our operations are conducted in China, most of our costs are incurred in Chinese currency, which subjects us to fluctuations in the exchange rates between the U.S. dollar and the Chinese renminbi. We incur transaction gains or losses resulting from consolidation of expenses incurred in local currencies for these subsidiaries, as well as in translation of the assets and liabilities of these assets at each balance sheet date. These risks may be increased by the fluctuation and revaluation of the Chinese renminbi. If we do not effectively manage the risks associated with this currency risk, our revenue, cash flows and financial condition could be adversely affected.

A reoccurrence of Severe Acute Respiratory Syndrome (SARS) or the outbreak of a different contagious disease such as the Avian Flu may adversely impact our manufacturing operations and some of our key suppliers and customers.

In 2003 one employee at our production facility in China contracted SARS, prompting us to close the facility for ten days. There was no significant impact to our ability to fill customer orders. Any reoccurrence of SARS or a different contagious disease, such as Avian Flu may cause us to temporarily close our manufacturing operations if any of our employees are again affected. Similarly, if one of our key suppliers is required to close for an extended period, we might not have enough raw material inventory to continue manufacturing operations. In addition, while we possess management skills among our China staff that enable us to maintain our manufacturing operations with minimal on-site supervision from our US-based staff, our business could also be harmed if travel to or from Asia and the United States is restricted or inadvisable, as it was during parts of 2003. None of our substrate competitors is as dependent on manufacturing facilities in China as we are. If our manufacturing operations were closed for a significant period, we could lose revenue and market share during that period, which would depress our financial performance and could be difficult to recapture. Finally, if one of our key customers is required to close for an extended period, we might not be able to ship product to them, our revenue would decline and our financial performance would suffer.

Risks Related to Our Financial Results and Capital Structure

The compound semiconductor industry is cyclical and has experienced a downturn which has adversely impacted our operating results.

Our continuing business depends in significant part upon manufacturers of electronic and opto-electronic compound semiconductor devices, as well as the current and anticipated market demand for these devices and products using these devices. As a supplier to the compound semiconductor industry, we are subject to the business cycles that characterize the industry. The timing, length and volatility of these cycles are difficult to predict. The compound semiconductor industry has historically been cyclical because of sudden changes in demand, the amount of manufacturing capacity and changes in the technology employed in compound semiconductors. The rate of changes in demand, including end demand, is high, and the effect of these changes upon us occurs quickly, exacerbating the volatility of these cycles. These changes have affected the timing and amounts of customers' purchases and investments in new technology. These industry cycles create pressure on our revenue, gross margin and net income.

The industry has in the past experienced periods of oversupply that result in significantly reduced demand and prices for compound semiconductor devices and components, including our products, both as a result of general economic changes and overcapacity. When these periods occur and our operating results and financial condition are adversely affected, oversupply creates pressure on our revenue, gross margins and net income (loss). Inventory buildups in telecommunications products and slower than expected sales of computer equipment resulted in overcapacity and led to reduced sales by our customers, and therefore reduced purchases of our products. During periods of weak demand such as those experienced historically, customers typically reduce purchases, delay delivery of products and/or cancel orders of component parts such as our products. Increased price competition has resulted, causing pressure on our net sales, gross margin and net income (loss). We experienced cancellations, price reductions, delays and push-outs of orders, which have resulted in reduced revenue. If the economic downturn occurred again, further order cancellations, reductions in order size or delays in orders could occur and would materially adversely affect our business and results of operations. Actions to reduce our costs, such as those we have recently taken, may be insufficient to align our structure with prevailing business conditions. We may be required to undertake additional cost-cutting measures, and may be unable to invest in marketing, research and development and engineering at the levels we

believe are necessary to maintain our competitive position. Our failure to make these investments could seriously harm our business.

During periods of increasing demand for compound semiconductor devices, we must have sufficient manufacturing capacity and inventory to meet customer demand, and must be able to attract, hire, train and retain qualified employees to meet demand. We must effectively manage our resources and production capacity to meet rapidly changing demand. During periods of decreasing demand, we must be able to appropriately align our cost structure with prevailing market conditions, motivate and retain key employees and effectively manage our supply chain. During periods of increasing demand, we must have sufficient manufacturing capacity and inventory to meet customer demand. If we are unable to effectively manage our resources and production capacity during an industry upturn, there could be a material adverse effect on our business, financial condition and results of operations.

If we fail to manage periodic contractions, we may utilize our cash balances, resulting in the decline of our existing cash, cash equivalents and investment balances.

We anticipate that our existing cash resources will fund our operations and purchases of capital equipment, as well as provide adequate working capital for the next twelve months. However, our liquidity is affected by many factors including, among others, the extent to which we pursue additional capital expenditures, the level of our production, and other factors related to the uncertainties of the industry and global economies. If we fail to manage our contractions successfully we may draw down our cash reserves, which would adversely affect our operating results and financial condition, reduce our value and possibly impinge our ability to raise debt and equity funding in the future, at a time when we might be required to raise additional cash. Accordingly, there can be no assurance that events in the future will not require us to seek additional capital or, if required, that such capital would be available on terms acceptable to us, if at all. As part of our effort to reduce costs, we may lose key staff, production resources and technology that we will need to grow when end markets recover. These events could reduce our ability to grow profitably as markets recover.

Unpredictable fluctuations in our operating results could disappoint analysts or our investors, which could cause our stock price to decline.

We have experienced and may continue to experience significant fluctuations in our revenue and earnings. Our quarterly and annual revenue and operating results have varied significantly in the past and may vary significantly in the future due to a number of factors, including:

•our ability to develop, manufacture and deliver high quality products in a timely and cost-effective manner;•decline in general economic conditions or downturns in the industry in which we compete;•fluctuations in demand for our products;•expansion of our manufacturing capacity;•expansion of our operations in China;•limited availability and increased cost of raw materials;•the volume and timing of orders from our customers, and cancellations, push-outs and delays of customer orders once made;•fluctuation of our manufacturing yields;•decreases in the prices of our or our competitors' products;•costs incurred in connection with any future acquisitions of businesses or technologies; and

•increases in our expenses, including expenses for research and development.

Due to these factors, we believe that period-to-period comparisons of our operating results may not be meaningful indicators of our future performance.

A substantial percentage of our operating expenses is fixed in the short term, and we may be unable to adjust spending to compensate for an unexpected shortfall in revenue. As a result, any delay in generating revenue could cause our operating results to be below the expectations of market analysts or investors, which could also cause our stock price to fall.

We have adopted certain anti-takeover measures that may make it more difficult for a third party to acquire us.

Our board of directors has the authority to issue up to 2,000,000 shares of preferred stock and to determine the price, rights, preferences and privileges of those shares without any further vote or action by the stockholders. The rights of the holders of common stock will be subject to, and may be adversely affected by, the rights of the holders of any preferred stock that may be issued in the future. The issuance of shares of preferred stock could have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock. We have no present intention to issue additional shares of preferred stock.

We have adopted a preferred stock purchase rights plan intended to guard against certain takeover tactics. The adoption of this plan was not in response to any proposal to acquire us, and the board is not aware of any such effort. The existence of this plan could also have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock.

In addition, provisions in our amended and restated certificate of incorporation and amended and restated bylaws may have the effect of delaying or preventing a merger, acquisition or change of control, or changes in our management, which could adversely affect the market price of our common stock. The following are some examples of these provision:

•the division of our board of directors into three separate classes, each with three-year terms;•the right of our board to elect a director to fill a space created by a board vacancy or the expansion of the board;•the ability of our board to alter our amended and restated bylaws; and•the requirement that only our board or the holders of at least 10% of our outstanding shares may call a special meeting of our stockholders.

Furthermore, because we are incorporated in Delaware, we are subject to the provisions of Section 203 of the Delaware General Corporation Law. These provisions prohibit large stockholders, in particular those owning 15% or more of the outstanding voting stock, from consummating a merger or combination with a corporation unless:

•662/3% of the shares of voting stock not owned by these large stockholders approve the merger or combination, or•the board of directors approves the merger or combination or the transaction which resulted in the large stockholder owning 15% or more of our outstanding voting stock.

Risks Related to Our Intellectual Property

Intellectual property infringement claims may be costly to resolve and could divert management attention.

Other companies may hold or obtain patents on inventions or may otherwise claim proprietary rights to technology necessary to our business. The markets in which we compete are comprised of

competitors that in some cases hold substantial patent portfolios covering aspects of products that could be similar to ours. We could become subject to claims that we are infringing patent, trademark, copyright or other proprietary rights of others. For example, we have in the past been involved in two separate lawsuits alleging patent infringement, and could in the future be involved in similar litigation.

If we are unable to protect our intellectual property, we may lose valuable assets or incur costly litigation.

We rely on a combination of patents, copyrights, trademark and trade secret laws, non-disclosure agreements and other intellectual property protection methods to protect our proprietary technology. However, we believe that, due to the rapid pace of technological innovation in the markets for our products, our ability to establish and maintain a position of technology leadership also depends on the skills of our development personnel. Despite our efforts to protect our intellectual property, third parties can develop products or processes similar to ours. Our means of protecting our proprietary rights may not be adequate, and our competitors may independently develop similar technology, duplicate our products or design around our patents. We believe that at least two of our competitors have begun to ship GaAs substrates produced using a process similar to our VGF technique. Our competitors may also develop and patent improvements to the VGF technology upon which we rely, and thus may limit any exclusivity we enjoy by virtue of our patents or trade secrets.