| [X] | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||

| For the fiscal year-endedDecember 31, | ||||

| or | ||||

| [ ] | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||

For the transition period fromto | ||||

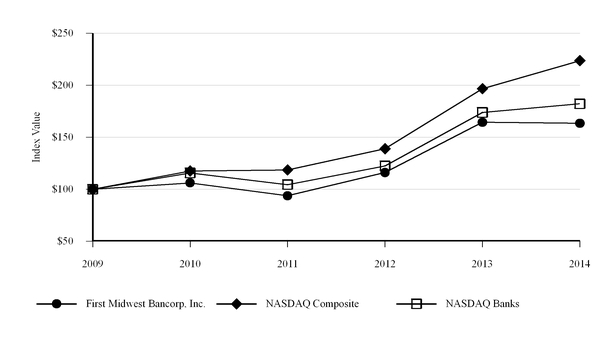

Act. $1,226,970,577. First Midwest Bancorp, Inc. (the In the normal course of business, the Company is signed and publicly announced. The Company's ability to engage in certain merger or acquisition transactions, whether or not any regulatory approval is required, will depend on the bank regulators' views at the time as to the capital levels, quality of management, and overall condition of the Company, in addition to their assessment of a variety of other factors. subsidiaries: Total assets Total deposits Banking offices Full-time equivalent employees 2014. Company guarantees payments of distributions on the trust-preferred securities and payments on redemption of the trust-preferred securities on a limited basis. assessing performance. Our Business activities. at December 31, 2014. The 1934, as amended (the "Exchange Act"). holding company to file an annual report of its operations and such additional information as the Federal Reserve may require. A bank holding company and its subsidiaries are subject to examination by the Federal Reserve. reputational consequences, including causing applicable bank regulatory authorities not to approve merger or acquisition transactions when regulatory approval is required or to prohibit such transactions even if approval is not required. consequences for the institution, including causing applicable bank regulatory authorities not to approve merger or acquisition transactions when regulatory approval is required or to prohibit such transactions even if approval is not required. Company or Bank reaches that size. the Company. The Bank is Act, and applicable state laws. prohibit such transactions even if approval is not required. product. Requirements Capital is classified in one of the following Tier 1 capital to risk-weighted assets Total capital to risk-weighted assets CET1 to risk-weighted assets Tier 1 capital to risk-weighted assets Total capital to risk-weighted assets Leverage ratio adequately capitalized. The Basel III its subsidiaries. anywhere in the country, subject to restrictions imposed on those other banks and thrifts, certain safety and soundness considerations, and prior notification to the IDFPR and the FDIC. Due to the current financial and economic environment, the Federal Reserve indicated that bank holding companies should carefully review their dividend policy and discourage payment ratios that are at maximum allowable levels unless both asset quality and capital are very strong. Employee Incentive Compensation soundness principles. Under these rules, financial organizations must review their compensation programs to and Regulation by e-mail at Company and other actions. business, financial condition, and results of operations. The Company's lending activities are subject to strict regulations. financial obligations is a function of its balance sheet structure, its ability to liquidate assets, and its access to alternative sources of funds. The Company seeks to ensure its funding needs are met by maintaining Standard & Poor's Rating Group, a division of the McGraw-Hill Companies, Inc. Moody's Investor Services, Inc. Fitch, Inc. Operational Risks discussion. relationship management, general ledger, deposit, loan, or other value hierarchies. Third-party sources also use assumptions, judgments, and estimates in determining securities values, and different third parties use different methodologies or provide different prices for similar securities. In addition, the nature of the business of the third party source that is valuing the securities at any given time could impact the valuation of the securities. The Company's ability to compete successfully depends on a number of factors, including: that the Company will not experience an adverse effect, which may be material, on its ability to access capital and on the Company's business, financial condition, and results of operations. environmental review before initiating any foreclosure action on real property, these reviews may not be sufficient to detect all potential environmental hazards. The remediation costs and any other financial liabilities associated with an environmental hazard could have a material adverse effect on the Company's business, financial condition, results of operations, and liquidity. Changes to statutes, regulations, Act, including the Volcker Rule. adjustment" to the interchange fee is available to those issuers that comply with certain standards outlined by the Federal Reserve. The Company and its subsidiaries may not be able to realize the benefit of deferred tax assets. Currently, there are certain For a detailed discussion on current legal proceedings, see Item 3, "Legal Proceedings," and Note 21 of "Notes to the Consolidated Financial Statements" in Item 8 of this Form 10-K. In addition, from time to time, banking regulators may restrict the Company from making acquisitions. See "History" and "Supervision and Regulation" in Item 1, "Business," of this Form 10-K for additional detail and further discussion of these matters. Failure to comply with the terms of loss share agreements with the FDIC may result in The FDIC Agreements have specific and detailed compliance, servicing, notification, and reporting requirements. be inaccurate. The Company's Restated Certificate of Incorporation, Amended and Restated By-laws, and Amended and Restated Rights Agreement, as well as certain banking laws, may have an anti-takeover effect. Market price of Common Stock High Low Quarter-end Cash dividends declared per common share Dividend yield at quarter-end (1) Book value per common share at quarter-end First Midwest S&P 500 S&P SmallCap 600 Banks October 1 – October 31, 2011 November 1 – November 30, 2011 December 1 – December 31, 2011 Total Operating Results (Amounts in thousands, except per share data) Operating Results (Amounts in thousands, except per share data) Net income (loss) Net income (loss) applicable to common shares Per Common Share Data Basic earnings (loss) per common share Diluted earnings (loss) per common share Common dividends declared Book value at year end Market price at year end Performance Ratios Return on average common equity Return on average assets Net interest margin — tax-equivalent Dividend payout ratio Average equity to average assets ratio Balance Sheet Highlights (Amounts in thousands) Balance Sheet Highlights (Amounts in thousands) Total assets Total loans, excluding covered loans Total loans, including covered loans Deposits Senior and subordinated debt Long-term portion of Federal Home Loan Bank advances Stockholders' equity Financial Ratios Allowance for credit losses as a percent of loans, excluding covered loans Total capital to risk-weighted assets Tier 1 capital to risk-weighted assets Tier 1 leverage to average assets Tangible common equity to tangible assets Operating Results Interest income Interest expense Net interest income Fee-based revenues Other noninterest income Noninterest expense, excluding losses realized on OREO, integration costs associated with FDIC-assisted transactions, severance-related costs, and an FDIC special assessment (1) Pre-tax, pre-provision operating earnings (2) Provision for loan losses Gains on securities sales, net Securities impairment losses Gains on FDIC-assisted transactions Gains on early extinguishment of debt Gain on acquisition of deposits Write-downs of OREO (1) Losses on sales of OREO, net (1) Integration costs associated with FDIC-assisted transactions (1) Severance-related costs (1) FDIC special deposit insurance assessment (1) Income (loss) before income tax (expense) benefit Income tax (expense) benefit Net income (loss) Preferred dividends and accretion on preferred stock Net (income) loss applicable to non-vested restricted shares Net income (loss) applicable to common shares Diluted earnings (loss) per common share Performance Ratios Return on average common equity Return on average assets Net interest margin – tax equivalent Efficiency ratio Balance Sheet Highlights Total assets Total loans, excluding covered loans Total loans, including covered loans Total deposits Transactional deposits Loans, excluding covered loans, to deposits ratio Transactional deposits to total deposits Asset Quality Highlights (1) Non-accrual loans 90 days or more past due loans (still accruing interest) Total non-performing loans Troubled debt restructurings ("TDRs") (still accruing interest) Other real estate owned Total non-performing assets 30-89 days past due loans Allowance for credit losses Allowance for credit losses as a percent of loans thousands, except per share data) 2013 non-deductible write-down of the cash surrender values ("CSV") of certain BOLI policies. Excluding these transactions, 2013 earnings per share was $0.90. Performance Overview for 2012 2012. Assets: Federal funds sold and other short-term investments Securities: Trading - taxable Investment securities - taxable Investment securities - nontaxable(1) Total securities FHLB and Federal Reserve Bank stock Loans, excluding covered loans(1)(2) Covered loans(3) Total loans Total interest-earning assets(1)(2) Cash and due from banks Allowance for credit losses Other assets Total assets Liabilities and Stockholders' Equity: Savings deposits NOW accounts Money market deposits Total interest-bearing transactional deposits Time deposits Total interest-bearing deposits Borrowed funds Senior and subordinated debt Total interest-bearing liabilities Demand deposits Other liabilities Stockholders' equity - common Stockholders' equity - preferred Total liabilities and stockholders' equity Net interest income/margin(1) Net interest income (GAAP) Tax-equivalent adjustment Tax equivalent net interest income Table 3 Federal funds sold and other short-term investments Securities: Trading – taxable Investment securities – taxable Investment securities – nontaxable (2) Total securities FHLB and Federal Reserve Bank stock Loans, excluding covered loans (2) Covered loans Total loans Total interest income (2) Savings deposits NOW accounts Money market deposits Total interest-bearing transactional deposits Time deposits Total interest-bearing deposits Borrowed funds Senior and subordinated debt Total interest expense Net interest income (2) Service charges on deposit accounts Wealth management fees Other service charges, commissions, and fees Card-based fees(1) Total fee-based revenues BOLI income(2) Other income(3) Total operating revenues Trading (losses) gains, net(4) Gains on securities sales, net(5) Securities impairment losses(5) Gains on FDIC-assisted Gains on early extinguishment of debt Gain on acquisition of deposits Total noninterest income 2013 2014. Compensation expense: Salaries and wages Retirement and other employee benefits Total compensation expense OREO expense: Write-downs of OREO Losses on the sales of OREO, net OREO operating expense, net (1) Total OREO expense Loan remediation costs Other professional services Total professional services FDIC premiums: FDIC special assessment FDIC insurance premiums Total FDIC premiums Net occupancy expense Equipment expense Technology and related costs Advertising and promotions Merchant card expense Other expenses Total noninterest expense Average full-time equivalent employees Efficiency ratio(2) implemented in the first half of 2015. net OREO expense OREO. Income (loss) before income tax expense (benefit) Income tax expense (benefit): Federal income tax expense (benefit) State income tax expense (benefit) Total income tax expense (benefit) Effective income tax rate year ended December 31, 2012. The decrease in income tax income subject to tax at statutory rates and a non-deductible BOLI modification loss recorded in the third quarter of 2013. value with unrealized gains and losses, net of related deferred income taxes, recorded in stockholders' equity as a separate component of accumulated other comprehensive loss. portfolio for the three years ended December 31, 2014. Available-for-Sale U.S. agency securities CMOs Other mortgage-backed securities Municipal securities CDOs Corporate debt securities Equity securities Total available-for- sale Held-to-Maturity Municipal securities Total securities Available-for-Sale U.S. agency securities CMOs Other mortgage-backed securities Municipal securities CDOs Other securities Total available-for-sale Held-to-Maturity Municipal securities Total securities Portfolio Composition securities portfolio. bonds. CMO portfolio totaled $4.7 million at December 31, 2014 compared to $15.2 million at December 31, 2013. CMOs Available-for-Sale U.S. agency securities CMOs (2) Other mortgage-backed securities (2) Municipal securities (3) CDOs Other securities (4) Total available-for-sale Held-to-Maturity Municipal securities (3) Total securities Commercial and industrial Agricultural Commercial real estate: Office Retail Industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans(1) Total loans portfolio. Total loans, excluding covered loans, as of December 31, 2011 were stable compared to December 31, 2010. Commercial and industrial Small business Tax-exempt loans(1) Overdrawn demand deposits Loan payment control and other(2) Total commercial and industrial Agricultural – operating Agricultural – farmland Total agricultural Total commercial, industrial, and agricultural loans Commercial, industrial, and agricultural loans as a percent of loans, excluding covered loans Commercial Real Estate Loans As of December 31, 2011 Raw land Developed land Construction Substantially completed structures Mixed and other Total Weighted-average maturity (in years) Construction loans as a percent of loans, excluding covered loans Construction loans as a percent of commercial real estate loans As of December 31, 2010 Raw land Developed land Construction Substantially completed structures Mixed and other Total Weighted-average maturity (in years) Construction loans as a percent of loans, excluding covered loans Construction loans as a percent of commercial real estate loans Service stations and truck stops Investor-owned rental properties Warehouses and storage Hotels Restaurants Automobile dealers Medical Religious Mobile home parks Recreational Other(1) Total other commercial real estate Commercial, industrial, and agricultural Commercial real estate Total Loans maturing after one year: Predetermined (fixed) interest rates Floating interest rates Total 2014. Consumer loans are centrally underwritten Home equity 1-4 family mortgages Installment loans Total consumer loans Home equity loans 1-4 family mortgages The home equity category consists mainly of revolving lines of credit secured by junior liens on owner-occupied real estate. Loan-to-value ratios on home equity loans and 1-4 family mortgages are based on the A discussion of our accounting policies for non-accrual loans, TDRs, and loans 90 days or more past due can be found in Note 1 of "Notes to the Consolidated Financial Statements" in Item 8 of this Form 10-K. As of December 31, 2011 Commercial and industrial Agricultural Commercial real estate: Office Retail Industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans Total loans As of December 31, 2010 Commercial and industrial Agricultural Commercial real estate: Office Retail Industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans Total loans to prior periods. Non-performing assets, excluding covered loans and covered OREO Non-accrual loans 90 days or more past due loans Total non-performing loans TDRs (still accruing interest) Other real estate owned Total non-performing assets 30-89 days past due loans Non-accrual loans to total loans Non-performing loans to total loans Non-performing assets to loans plus OREO Covered loans and covered OREO (1) Non-accrual loans 90 days or more past due loans Total non-performing loans TDRs (still accruing interest) Other real estate owned Total non-performing assets 30-89 days past due loans Non-performing assets, including covered loans and covered OREO Non-accrual loans 90 days or more past due loans Total non-performing loans TDRs (still accruing interest) Other real estate owned Total non-performing assets 30-89 days past due loans Non-accrual loans to total loans Non-performing loans to total loans Non-performing assets to loans plus OREO The effect of non-accrual loans on interest income for 2011 is presented below: Interest which would have been included at the contract rates Less: Interest included in income during the year Interest income not recognized in the financial statements loans. Non-performing assets, excluding acquired and covered loans and covered OREO, represented 2012. The continued improvement in non-performing assets and the related credit metrics reflects management's ongoing commitment to credit remediation. sales. Residential construction Commercial construction Total construction loans Non-accrual loans 90 days or more past due loans Total non-performing loans Commercial and industrial Agricultural Commercial real estate: Office Retail Industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Home equity loans 1-4 family mortgages Installment loan Total consumer Total TDRs TDRs, still accruing interest TDRs included in non-accrual Total TDRs Year-to-date charge-offs on restructured loans Valuation allowance related to restructured loans time, and these restructures remain classified as TDRs for the remaining terms of the loans. A discussion of our accounting policies for TDRs can be found in Note 1 of "Notes to the Consolidated Financial Statements" in Item 8 of this Form 10-K. Special mention loans (1) Substandard loans (2) Total potential problem loans $2.3 million. Single-family homes Land parcels: Raw land Farm land Commercial lots Single-family lots Total land parcels Multi-family units Commercial properties Total OREO properties Covered OREO Total OREO properties Loans sold or identified as held-for-sale in 2011 Commercial and industrial Commercial real estate: Office retail, and, industrial Residential construction Commercial construction Other commercial real estate Total commercial real estate Total loans sold or transferred to held-for-sale Partial sales and paydowns Total loans sold, paid off, or transferred to held-for-sale in 2011 Loans sold in 2010 Bulk sale of non-accrual loans (1) Sale of potential problem loans (2) Total loans sold in 2010 OREO sales Proceeds from sales Less: Basis of properties sold Losses on sales of OREO, net OREO transfers and write-downs OREO transferred to premises, furniture, and equipment (at fair value) OREO write-downs trends. 2014. Change in allowance for credit losses: Balance at beginning of year Loans charged-off: Commercial and industrial Agricultural Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Consumer 1-4 family mortgages Total loans charged-off Recoveries on loans previously charged-off: Commercial and industrial Agricultural Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Consumer 1-4 family mortgages Total recoveries on loans previously charged-off Net loans charged-off, excluding covered loans and covered OREO Net charge-offs on covered loans Net loans charged-off Provision charged to operating expense: Provision, excluding provision for covered loans Provision for covered loans Less: expected reimbursement from the FDIC Net provision for covered loans Total provision charged to operating expense Balance at end of year Allowance for loan losses Reserve for unfunded commitments Total allowance for credit losses Average loans, excluding covered loans Net loans charged-off to average loans, excluding covered loans Allowance for credit losses at end of period as a percent of: Total loans, excluding covered loans Non-performing loans, excluding covered loans Average loans, including covered loans Net loans charged-off to average loans Allowance for credit losses at end of period as a percent of: Total loans Non-performing loans 2013. 2014. The Commercial, industrial, and agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Other commercial real estate(2) Total commercial real estate Consumer Total, excluding allowance for covered loans Covered loans Total Total loans, excluding covered loans Total loans Allowance for credit losses as a percent of: Loans: Commercial, industrial, and agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Other commercial real estate Total commercial real estate Consumer Total, excluding covered loans expected future cash flows of the covered impaired loans. $206.5 million, which includes $10.4 million acquired in the Great Lakes transaction. Deferred tax assets Valuation allowance required as of December 31, 2014. carryforwards. Total deposits and borrowed funds as of December 31, Demand deposits Savings deposits NOW accounts Money market accounts Transactional deposits Time deposits Brokered deposits Total time deposits Total deposits Securities sold under agreements to repurchase Federal funds purchased and other borrowed funds Total borrowed funds Senior and subordinated debt Total funding sources repurchase agreements, FHLB advances, and federal funds purchased to supplement deposits. Securities sold under agreements to repurchase At year-end: Securities sold under agreements to repurchase Federal funds purchased FHLB advances Federal term auction facilities Total borrowed funds Average for the year: Securities sold under agreements to repurchase Federal funds purchased FHLB advances Federal term auction facilities Total borrowed funds Maximum amount outstanding at any day during the year: Securities sold under agreements to repurchase Federal funds purchased FHLB advances Federal term auction facilities Weighted-average maturity of FHLB advances Senior and Subordinated Debt 2012. The following table presents our significant fixed and determinable contractual obligations and significant commitments as of December 31, Transactional deposits (no stated maturity) Time deposits Borrowed funds Subordinated debt Operating leases Pension liability Uncertain tax positions liability Commitments to extend credit Letters of credit Regulatory capital ratios: Total capital to risk-weighted assets Tier 1 capital to risk-weighted assets Tier 1 leverage to average assets Regulatory capital ratios, excluding preferred stock (1): Total capital to risk-weighted assets Tier 1 capital to risk-weighted assets Tier 1 leverage to average assets Tier 1 common capital to risk-weighted assets (2)(3) Tangible common equity ratios: Tangible common equity to tangible assets Tangible common equity, excluding other comprehensive loss, to tangible assets Tangible common equity to risk-weighted assets Regulatory capital ratios, Bank only: Total capital to risk-weighted assets Tier 1 capital to risk-weighted assets Tier 1 leverage to average assets information on our minimum capital requirements. Reconciliation of Capital Components to Regulatory Requirements Total regulatory capital, as defined in federal regulations Preferred equity Total regulatory capital, excluding preferred stock Tier 1 capital, as defined in federal regulations Preferred equity Tier 1 regulatory capital, excluding preferred stock Trust preferred securities included in Tier 1 capital Tier 1 common capital Risk-weighted assets, as defined in federal regulations Average assets, as defined in federal regulations Total capital to risk-weighted assets Total capital, excluding preferred stock, to risk-weighted assets Tier 1 capital to risk-weighted assets Tier 1 capital, excluding preferred stock, to risk-weighted assets Tier 1 common capital to risk-weighted assets Tier 1 leverage to average assets Tier 1 leverage, excluding preferred stock, to average assets Reconciliation of Capital Components to GAAP Total stockholder's equity Preferred equity Common equity Goodwill and other intangible assets Tangible common equity Accumulated other comprehensive loss Tangible common equity, excluding accumulated other comprehensive loss Total assets Goodwill and other intangible assets Tangible assets Tangible common equity to tangible assets Tangible common equity, excluding accumulated other comprehensive loss, to tangible assets Tangible common equity to risk-weighted assets For further details of the regulatory capital requirements and ratios as of December 31, currently in effect. 30 Interest income Interest expense Net interest income Provision for loan losses Noninterest income Gains on securities sales, net Securities impairment losses Gain on FDIC-assisted transactions Gain on acquisition of deposits Noninterest expense Income (loss) before income tax (expense) benefit Income tax benefit (expense) Net income (loss) Preferred dividends and accretion on preferred stock Net loss (income) applicable to non-vested restricted shares Net income (loss) applicable to common shares Basic earnings (loss) per common share Diluted earnings (loss) per common share Dividends declared per common share Return on average common equity Return on average assets Net interest margin – tax-equivalent Income (loss) before taxes Provision for loan losses Pre-tax, pre-provision earnings Non-operating items Securities gains, net Gain on FDIC-assisted transactions Severance-related costs Integration costs associated with FDIC- assisted transactions Gain on acquisition of deposits Losses realized on OREO Total non-operating items Pre-tax, pre-provision core operating earnings Average for the quarter: Securities sold under agreements to repurchase Federal funds purchased FHLB advances Total borrowed funds Maximum amount outstanding at any day during the quarter: Securities sold under agreements to repurchase Federal funds purchased FHLB advances CRITICAL ACCOUNTING ESTIMATES value estimate. purchase price over the fair value of net assets acquired using the acquisition method of accounting. This method requires that all identifiable assets acquired and liabilities assumed in the transaction, both intangible and tangible, be recorded at their estimated fair value upon acquisition. Determining the fair value often involves estimates based on third-party valuations, such as appraisals, or internal valuations based on discounted cash flow analyses or other valuation techniques. Goodwill is not amortized, instead, we assess the potential for impairment on an annual basis or more frequently if events and circumstances indicate that goodwill might be impaired. this Form 10-K. rates. Due to the low interest rate environment as of December 31, 2014 and 2013, management determined that an immediate decrease in interest rates greater than 100 basis points was not meaningful for this analysis. simulated results due to timing, magnitude, and frequency of interest rate changes as well as changes in market conditions and management strategies. rates. December 31, 2011: Dollar change Percent change December 31, 2010: Dollar change Percent change December 31, 2011: Dollar change Percent change December 31, 2010: Dollar change Percent change Assets Cash and due from banks Interest-bearing deposits in other banks Trading securities, at fair value Securities available-for-sale, at fair value Securities held-to-maturity, at amortized cost (fair value 2011 – $61,477; 2010 – $82,525) Federal Home Loan Bank and Federal Reserve Bank stock, at cost Loans, excluding covered loans Covered loans Allowance for loan losses Net loans Other real estate owned ("OREO"), excluding covered OREO Covered OREO Federal Deposit Insurance Corporation ("FDIC") indemnification asset Premises, furniture, and equipment Accrued interest receivable Investment in bank-owned life insurance ("BOLI") Goodwill and other intangible assets Other assets Total assets Liabilities Noninterest-bearing deposits Interest-bearing deposits Total deposits Borrowed funds Senior and subordinated debt Accrued interest payable and other liabilities Total liabilities Stockholders' Equity Preferred stock Common stock Additional paid-in capital Retained earnings Accumulated other comprehensive loss, net of tax Treasury stock, at cost Total stockholders' equity Total liabilities and stockholders' equity Par value Shares authorized Shares issued Shares outstanding Treasury shares See accompanying notes to the consolidated financial statements. Interest Income Loans Investment securities – taxable Investment securities – tax-exempt Covered loans Federal funds sold and other short-term investments Total interest income Interest Expense Deposits Borrowed funds Senior and subordinated debt Total interest expense Net interest income Provision for loan losses Net interest income after provision for loan losses Noninterest Income Service charges on deposit accounts Wealth management fees Other service charges, commissions, and fees Card-based fees Total fee-based revenues Securities gains, net (reclassified from other comprehensive income (loss)) Gains on FDIC-assisted transactions Gains on early extinguishment of debt Other Total noninterest income Noninterest Expense Salaries and wages Retirement and other employee benefits OREO expense, net Net occupancy and equipment expense Technology and related costs Professional services FDIC premiums Advertising and promotions Merchant card expense Other expenses Total noninterest expense Income (loss) before income tax expense (benefit) Income tax expense (benefit) Net income (loss) Preferred dividends and accretion on preferred stock Net (income) loss applicable to non-vested restricted shares Net income (loss) applicable to common shares Per Common Share Data Basic earnings (loss) per common share Diluted earnings (loss) per common share Weighted-average common shares outstanding Weighted-average diluted common shares outstanding Net income (loss) Available-for-sale securities Unrealized holding gains: Before tax Tax effect Net of tax Reclassification of net gains included in net income: Before tax Tax effect Net of tax Net unrealized holding gains (losses) Unrecognized net pension costs Unrealized holding (losses) gains: Before tax Tax effect Net of tax Total other comprehensive income (loss) Comprehensive income (loss) Balance at January 1, 2009 Cumulative effect of change in accounting for other-than- temporary impairment Adjusted balance at January 1, 2009 2009 other comprehensive income Balance at December 31, 2009 2010 other comprehensive loss Balance at December 31, 2010 2011 other comprehensive income (loss) Balance at December 31, 2011 Balance at January 1, 2009 Cumulative effect of change in accounting for other-than- temporary impairment Adjusted beginning balance Comprehensive (loss) income Common dividends declared ($0.04 per common share) Preferred dividends declared ($50.00 per preferred share) Accretion on preferred stock Issuance of Common Stock Share-based compensation expense Restricted stock activity Treasury stock purchased for benefit plans Balance at December 31, 2009 Comprehensive loss Common dividends declared ($0.04 per common share) Preferred dividends declared ($50.00 per preferred share) Accretion on preferred stock Issuance of Common Stock Share-based compensation expense Restricted stock activity Treasury stock issued to benefit plans Balance at December 31, 2010 Comprehensive income Common dividends declared ($0.04 per common share) Preferred dividends declared ($44.86 per preferred share) Accretion on Preferred Shares Redemption of Preferred Shares Redemption of Warrant Share-based compensation expense Restricted stock activity Treasury stock issued to benefit plans Balance at December 31, 2011 Operating Activities Net income (loss) Adjustments to reconcile net income (loss) to net cash provided by operating activities: Provision for loan losses Depreciation of premises, furniture, and equipment Net amortization of premium on securities Net gains on securities Gains on FDIC-assisted transactions Gains on early extinguishment of debt Net losses on sales and write-downs of OREO Net losses (gains) on sales of premises, furniture, and equipment BOLI income Net pension cost Share-based compensation expense Tax (expense) benefit related to share-based compensation Deferred income taxes Net amortization of other intangible assets Originations and purchases of mortgage loans held-for-sale Proceeds from sales of mortgage loans held-for-sale Net decrease (increase) in trading account securities Net decrease in accrued interest receivable Net decrease in accrued interest payable Net decrease (increase) in other assets Net (decrease) increase in other liabilities Net cash provided by operating activities Investing Activities Proceeds from maturities, repayments, and calls of securities available-for-sale Proceeds from sales of securities available-for-sale Purchases of securities available-for-sale Proceeds from maturities, repayments, and calls of securities held-to-maturity Purchases of securities held-to-maturity Redemption (purchase) of FHLB and Federal Reserve Bank stock Net increase in loans Proceeds from claims on BOLI Proceeds from sales of OREO Proceeds from sales of premises, furniture, and equipment Purchases of premises, furniture, and equipment Net cash proceeds received in FDIC-assisted transactions Net cash provided by investing activities Financing Activities Net cash proceeds received in acquisition of deposits Net (decrease) increase in deposit accounts Net (decrease) in borrowed funds Proceeds (payments) for the issuance (retirement) of subordinated debt Redemption of Preferred Shares and related Warrant Proceeds from the issuance of Common Stock Cash dividends paid Restricted stock activity Excess tax benefit (expense) related to share-based compensation Net cash used in financing activities Net increase in cash and cash equivalents Cash and cash equivalents at beginning of year Cash and cash equivalents at end of year date in accordance with accounting guidance applicable to business combinations. See Note 3, "Acquisitions" for additional discussion related to these fair value adjustments. policies. Cash and Cash Equivalents – For purposes of the Consolidated Statements of Cash Flows, management income. recovery, an OTTI charge will be recognized through income as a realized loss and included in net securities gains (losses) in the Consolidated Statements of Income. If management does not expect to sell the security or believes it is not more likely than not that it will be required to sell the security prior to full recovery, the OTTI is separated into the amount related to credit deterioration, which is recognized through income as a realized loss, and the amount resulting from other factors, which is recognized in other comprehensive income (loss). basis. Expected future cash flows in excess of the fair value of loans at the purchase date ("accretable yield") are recorded as interest income over the life of the loans if the timing and amount of the expected future cash flows can be reasonably estimated. The non-accretable yield represents Subsequent determined. full or charged-off. installment loans. rate. covered PCI loans. On a periodic basis, the adequacy of this allowance is determined through a re-estimation of expected future cash flows on all of the outstanding covered PCI loans using either a probability of default/loss given default ("PD/LGD") methodology or a specific review methodology. The PD/LGD model is a loss model that estimates expected future cash flows using a probability of default curve and loss given default estimates. classifications by regulatory authorities. properties, are included in net OREO expense in the Consolidated Statements of Income. are included in other noninterest expense in the Consolidated Statements of Income. Maintenance and repairs are charged to operating expenses as incurred, while improvements that extend the useful life of assets are capitalized and depreciated over the estimated remaining life. Condition. Subsequent changes in a at inception. tables. Securities U.S. agency CMOs Other residential mortgage-backed securities Municipal securities CDOs Corporate debt securities Equity securities: Hedge fund investment Other equity securities Total equity securities Total Securities Held-to-Maturity Municipal Trading Securities One year or less One year to five years Five years to ten years After ten years CMOs Other residential mortgage-backed securities Equity securities Total Excluding securities issued or backed by the U.S. government and its agencies and U.S. government-sponsored enterprises, there were no investments in securities from one issuer that exceeded 10% of total stockholders' equity 2013. Proceeds from sales Gains (losses) on sales of securities: Gross realized gains Gross realized losses Net realized gains on securities sales Non-cash impairment charges: Other-than-temporary securities impairment Portion of other-than-temporary impairment recognized in other comprehensive income (loss) Net non-cash impairment charges Net realized gains Income tax expense on net realized gains Trading (losses) gains, net(1) Net non-cash impairment charges: CDOs Whole loan mortgage-backed security included in CMOs Equity securities Total Changes in Cumulative amount recognized at beginning of year Credit losses included in earnings(1): Losses recognized on securities that previously had credit losses Losses recognized on securities that did not previously have credit losses Cumulative amount recognized at end of year 2013. As of December 31, 2011 U.S. agency security CMOs Other residential mortgage- backed securities Municipal securities CDOs Corporate debt securities Total As of December 31, 2010 U.S. agency securities CMOs Other residential mortgage- backed securities Municipal securities CDOs Total The unrealized losses on CDOs as of December 31, Significant judgment is required to calculate the fair value of the CDOs, all of which are pooled. 1 2 3 4 5 6 7 The following table presents the Company's class. Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans(1) Total loans Deferred loan fees included in total loans Overdrawn demand deposits included in total loans Loans pledged to secure: Federal Home Loan Bank advances Federal term auction facilities Total Acquisition date Total assets of acquired institution at acquisition date Bargain-purchase gains Goodwill Stated loss threshold Reimbursement rate (2): Before stated loss threshold After stated loss threshold Home equity lines(1) Covered impaired loans Other covered loans(2) Total covered loans FDIC indemnification asset Covered other real estate owned Total covered assets Covered non-accrual loans Covered loans past due 90 days or more and still accruing interest In connection with the FDIC Agreements, the Company recorded an indemnification asset. To maintain eligibility for the loss share reimbursement, the Company is required to follow certain servicing procedures as specified in the FDIC Agreements. the carrying value of the FDIC indemnification asset for the years ended December 31, 2014, 2013, and 2012 is presented in the following table. Balance at beginning of year Additions Accretion (amortization) Expected reimbursements from the FDIC for changes in expected credit losses(1) Payments received from the FDIC Balance at end of year Balance at beginning of year Additions Accretion Reclassifications (to) from non-accretable difference, net(1) Balance at end of year AND TDRS Aging Analysis of Past Due Loans and Non-Performing Loans by Class December 31, 2011 Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans Total loans December 31, 2010 Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans, excluding covered loans Covered loans Total loans Balance at beginning of year Loans charged-off Recoveries of loans previously charged-off Net loans charged-off Provision for loan losses Balance at end of year Allowance for loan losses Reserve for unfunded commitments Total allowance for credit losses Allowance for Credit Losses by Portfolio Segment Balance at January 1, 2009 Loans charged-off Recoveries of loans previously charged-off Net loans charged-off Provision for loan losses Balance at December 31, 2009 Loans charged-off Recoveries of loans previously charged-off Net loans charged-off Provision for loan losses Balance at December 31, 2010 Loans charged-off Recoveries of loans previously charged-off Net loans charged-off Provision for loan losses Balance at December 31, 2011 Impaired loans individually evaluated for impairment: Impaired loans with a specific reserve for credit losses(1) Impaired loans with no specific reserve(2) Total impaired loans individually evaluated for impairment Corporate non-accrual loans not individually evaluated for impairment(3) Total corporate non-accrual loans TDRs, still accruing interest Total impaired loans Valuation allowance related to impaired loans Average recorded investment in impaired loans Interest income recognized on impaired loans(4) The table below provides a Loans and Related Allowance for Credit Losses by Portfolio Segment December 31, 2011 Commercial, industrial, and agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Other commercial real estate Total commercial real estate Total corporate loans Consumer Total loans, excluding covered loans Covered loans(1) Total loans included in the calculation of the allowance for credit losses December 31, 2010 Commercial, industrial, and agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Other commercial real estate Total commercial real estate Total corporate loans Consumer Total 2013. PCI loans are excluded from this disclosure. Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total impaired loans individually evaluated for impairment Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total impaired loans individually evaluated for impairment Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans Commercial and industrial Agricultural Commercial real estate: Office, retail and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total loans restructured TDRs, still accruing interest(2) TDRs included in non-accrual(3) Total Commercial and industrial Agricultural Commercial real estate: Office, retail and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans Home equity 1-4 family mortgages Installment loans Total consumer loans Total TDRs with charge-offs TDRs, still accruing interest TDRs included in non-accrual Total Credit Quality Indicators Corporate Credit Quality Indicators by Class, Excluding Covered Loans December 31, 2011 Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans December 31, 2010 Commercial and industrial Agricultural Commercial real estate: Office, retail, and industrial Multi-family Residential construction Commercial construction Other commercial real estate Total commercial real estate Total corporate loans December 31, 2011 Home equity 1-4 family mortgages Installment loans Total consumer loans December 31, 2010 Home equity 1-4 family mortgages Installment loans Total consumer loans Land Premises Furniture and equipment Total cost Accumulated depreciation Net book value of premises, furniture, and equipment held-for-investment Assets held-for-sale Total premises, furniture, and equipment Depreciation expense on premises, furniture, and equipment 2014. Year ending December 31, 2012 2013 2014 2015 2016 2017 and thereafter Total minimum lease payments Rental expense charged to operations(1) Rental income from premises leased to others(2) 2014, 2013, and 2012. Balance at December 31, 2008 2009 activity Balance at December 31, 2009 Goodwill acquired through FDIC-assisted transaction Balance at December 31, 2010 Adjustment to goodwill recorded in 2010 (1) Adjusted balance at January 1, 2011 2011 activity Balance at December 31, 2011 detail regarding these transactions. Balance at beginning of year Additions Amortization expense Fully amortized assets/other Balance at end of year Weighted-average remaining life (in years) Estimated useful lives (in years) Year ending December 31, 2012 2013 2014 2015 2016 2017 and thereafter Total type. Demand deposits Savings deposits NOW accounts Money market deposits Time deposits less than $100,000 Time deposits of $100,000 or more Total deposits Year ending December 31, 2012 2013 2014 2015 2016 2017 and thereafter Total Maturing within 3 months After 3 but within 6 months After 6 but within 12 months After 12 months Total Securities sold under agreements to repurchase FHLB advances Total borrowed funds The Bank is a member of the FHLB and has access to term financing from the FHLB. These advances are secured by designated assets that may include qualifying residential and multi-family mortgages, home equity loans, and municipal and mortgage-backed securities. During 2014, the Company prepaid $114.6 million of FHLB advances. This transaction resulted in a $2.1 million pre-tax loss on the early extinguishment of debt and is included in other noninterest income in the Consolidated Statements of Income. At December 31, December 1, 2011 December 4, 2012 December 4, 2013 December 18, 2013 Available federal funds lines (1) Federal Reserve Bank Discount Window's primary credit program 5.875% senior notes due in 2016 Principal amount Discount Total senior notes due in 2016 5.85% subordinated notes due in 2016 Principal amount Discount Total subordinated notes due in 2016 6.95% junior subordinated debentures due in 2033 Principal amount Discount Total junior subordinated debentures Total long-term debt share. 2014. Net income (loss) Preferred dividends Accretion on preferred stock (1) Net (income) loss applicable to non-vested restricted shares Net income (loss) applicable to common shares Weighted-average common shares outstanding: Weighted-average common shares outstanding (basic) Dilutive effect of Common Stock equivalents Weighted-average diluted common shares outstanding Basic earnings (loss) per common share Diluted earnings (loss) per common share Anti-dilutive shares not included in the computation of diluted earnings per common share (2) Current tax expense (benefit): Federal State Total Deferred tax expense (benefit): Federal State Total Total income expense (benefit) Deferred tax assets: Alternative minimum tax ("AMT") and other credit carryforwards Federal net operating loss ("NOL") carryforwards Allowance for credit losses Unrealized losses OREO State NOL carryforwards Other state tax benefits Other Total deferred tax assets Deferred tax liabilities: Purchase accounting adjustments and intangibles Deferred loan fees Accrued retirement benefits Depreciation Cancellation of indebtedness income Other Total deferred tax liabilities Deferred tax valuation allowance Net deferred tax assets Tax effect of adjustments related to other comprehensive income (loss) Net deferred tax assets including adjustments Net operating loss carryforwards available to offset future taxable income: Federal gross NOL carryforwards, begin to expire in 2030 Illinois gross NOL carryforwards, begin to expire in 2018 Indiana gross NOL carryforwards, begin to expire in 2021 Wisconsin gross NOL carryforwards, begin to expire in 2025 Other credits (1) net deferred tax assets acquired from the Popular, National Machine Tool, and Great Lakes transactions. Statutory federal income tax rate Tax-exempt income, net of interest expense disallowance State income tax, net of federal income tax effect Other, net Effective tax rate The change in effective at statutory rates. The change in effective non-deductible BOLI modification loss recorded in 2013. The Company is no longer subject to examination by 2011. Balance at beginning of year Additions for tax positions relating to the current year Additions for tax positions relating to prior years Reductions for tax positions relating to prior years Reductions for settlements with taxing authorities Lapse in statute of limitations Balance at end of year Interest and penalties not included above (1): Interest expense (benefit), net of tax effect, and penalties Accrued interest and penalties, net of tax effect, at end of year Profit sharing expense Company dividends received by the Profit Sharing Plan Company shares held by the Profit Sharing Plan at year end: Number of shares Fair value Accumulated benefit obligation Change in benefit obligation: Projected benefit obligation at beginning of year Service cost Interest cost Actuarial losses Benefits paid Projected benefit obligation at end of year Change in plan assets: Fair value of plan assets at beginning of year Actual return on plan assets Benefits paid Employer contributions Fair value of plan assets at end of year Funded status recognized in the Consolidated Statements of Financial Condition: Noncurrent prepaid pension Noncurrent liabilities Amounts recognized in accumulated other comprehensive loss: Prior service cost Net loss Net amount recognized Actuarial losses included in accumulated other comprehensive loss as a percent of: Accumulated benefit obligation Fair value of plan assets Amounts expected to be amortized from accumulated other comprehensive loss into net periodic benefit cost in the next fiscal year: Prior service cost Net loss Net amount expected to be recognized Weighted-average assumptions at the end of the year used to determine the actuarial present value of the projected benefit obligation: Discount rate Rate of compensation increase Net Periodic Benefit Pension Cost Components of net periodic benefit cost: Service cost Interest cost Expected return on plan assets Recognized net actuarial loss Amortization of prior service cost Other (1) Net periodic cost Other changes in plan assets and benefit obligations recognized as a charge to other comprehensive income (loss): Net loss (gain) for the period Amortization of prior service cost Amortization of net loss Total Total recognized in net periodic pension cost and other comprehensive loss Weighted-average assumptions used to determine the net periodic cost: Discount rate Expected return on plan assets Rate of compensation increase Asset Category: Equity securities Fixed income Cash equivalents Total Year ending December 31, 2012 2013 2014 2015 2016 2017-2021 The fair value of the awards is determined based on the average of the high and low price of the Company's common stock on the grant date. restricted stock units, and performance share awards. Omnibus Plan Directors Plan periods presented. Effect of Recording Share-Based Compensation Expense Stock option expense Restricted stock/unit award expense Salary stock award expense Total share-based compensation expense Income tax benefit Share-based compensation expense, net of tax Basic earnings per common share Diluted earnings per common share Cash flows (used in) provided by operating activities Cash flows provided by (used in) financing activities (1) Outstanding at beginning of year Granted Expired Outstanding at end of period Ending vested and expected to vest Exercisable at end of period Expected life of the option (in years) Expected stock volatility Risk-free interest rate Expected dividend yield Weighted-average fair value of options at their grant date Share-based compensation expense Unrecognized compensation expense Weighted-average amortization period remaining (in years) Restricted Stock Awards Non-vested awards at beginning of year Granted Vested Forfeited Non-vested awards at end of year Restricted Stock Units Non-vested awards at beginning of year Granted Non-vested awards at end of year Share-based compensation expense Unrecognized compensation expense Weighted-average amortization period remaining (in years) Total fair value of vested restricted stock awards/unit, at end of period Income tax benefit realized from vesting/release of restricted stock awards/unit under regulatory accounting practices ("risk-weighted assets"). The capital amounts and classification are also subject to qualitative judgments by the regulators regarding components of capital and assets, risk weightings, and other factors. As of December 31, 2011: Total capital (to risk-weighted assets): First Midwest Bancorp, Inc. First Midwest Bank Tier 1 capital (to risk-weighted assets): First Midwest Bancorp, Inc. First Midwest Bank Tier 1 leverage (to average assets): First Midwest Bancorp, Inc. First Midwest Bank As of December 31, 2010: Total capital (to risk-weighted assets): First Midwest Bancorp, Inc. First Midwest Bank Tier 1 capital (to risk-weighted assets): First Midwest Bancorp, Inc. First Midwest Bank Tier 1 leverage (to average assets): First Midwest Bancorp, Inc. First Midwest Bank Fair Value Hedges Related to fixed rate commercial loans Notional amount outstanding Weighted-average interest rate received Weighted-average interest rate paid Weighted-average maturity (in years) Derivative liability fair value Cash pledged to collateralize net unrealized losses with counterparties (1) Aggregate fair value of assets needed to settle the instruments immediately (if the credit risk-related contingent features were triggered) Net hedge ineffectiveness recognized in noninterest income: Change in fair value of swaps Change in fair value of hedged items Net hedge ineffectiveness (1) Gains recognized in net interest income (2) instruments were not material for any period presented. The Company had no other derivative instruments as of December 31, 2014 and 2013. The Company does not enter into derivative transactions for purely speculative purposes. policy establishes limits on credit exposure to any single Contractual or Notional Amounts of Financial Instruments Commitments to extend credit: Home equity lines Credit card lines 1-4 family real estate construction Commercial real estate Commercial and industrial Overdraft protection program (1) All other commitments Total commitments Letters of credit: 1-4 family real estate construction Commercial real estate All other Total letters of credit Unamortized fees associated with letters of credit (2) (3) Remaining weighted-average term, in months Remaining lives, in years Recourse on assets securitized: Unpaid principal balance of assets securitized Cap on recourse obligation Carrying value of recourse obligation (2) Recourse loans repurchased during the year Recourse loans charged-off during the year FMCT: Principal balance of debentures issued by the Company Related interest receivable Total FMCT assets Interest in trust-preferred capital securities issuances Investment in low-income housing tax credit partnerships operations, or cash flows. on a Recurring Basis Assets and liabilities measured at fair value on a recurring basis Assets: Trading securities: Money market funds Mutual funds Total trading securities Securities available-for-sale: U.S. agency securities CMOs Other residential mortgage-backed securities Municipal securities CDOs Corporate debt securities Hedge fund investment Other equity securities Total securities available-for-sale Mortgage servicing rights (1) Total assets Liabilities: Derivative liabilities (1) Assets measured at fair value on an annual basis Pension plan assets: Mutual funds (2) U.S. government and government agency securities Corporate bonds Common stocks Common trust funds Total pension plan assets Assets measured at fair value on a non-recurring basis Collateral-dependent impaired loans (3) OREO (4) Loans held-for-sale (5) Assets held-for-sale (6) Total assets Assets and liabilities measured at fair value on a recurring basis Assets: Trading securities: Money market funds Mutual funds Total trading securities Securities available-for-sale: U.S. agency securities CMOs Other residential mortgage-backed securities Municipal securities CDOs Corporate debt securities Hedge fund investment Other equity securities Total securities available-for-sale Mortgage servicing rights (1) Total assets Liabilities: Derivative liabilities (1) Assets measured at fair value on an annual basis Pension plan assets: Mutual funds (2) U.S. government and government agency securities Corporate bonds Common stocks Common trust funds Total pension plan assets Assets measured at fair value on a non-recurring basis Collateral-dependent impaired loans (3) OREO (4) Total assets thousands) Trading Securities Weighted-average coupon rate Weighted-average maturity, in years Information on underlying residential mortgages: Origination dates Weighted-average coupon rate Weighted-average maturity, in years the default, the magnitude of the default, and the timing and magnitude of the cure probability are directly interrelated. Defaults that occur sooner and/or are greater than anticipated have a negative impact on the valuation. In addition, a high cure probability assumption has a positive effect on the fair value, and, if a cure event takes place sooner than anticipated, the impact on the valuation is also favorable. Balance at beginning of year Total income (loss): Included in earnings (1) Included in other comprehensive income (loss) Principal paydowns Accretion Transfer out of Level 3 (2) Balance at end of year Change in unrealized losses recognized in earnings relating to securities still held at end of period Carrying Value of Mortgage Servicing Rights Balance at beginning of year New servicing assets Total gains (losses) included in earnings (1): Due to changes in valuation inputs and assumptions (2) Other changes in fair value (3) Balance at end of year Key economic assumptions used in measuring fair value, at end of year: Weighted-average prepayment speed Weighted-average discount rate Weighted-average maturity, in months Contractual servicing fees earned during the year (1) Total amount of loans being serviced for the benefit of others, at end of year (4) properties. In certain circumstances, Collateral-dependent impaired loans OREO Loans held-for-sale Assets held-for-sale Goodwill and Other Intangible Assets judgment and the use of significant unobservable inputs. As discussed in Note Financial Condition, the Company must disclose the estimated fair values and the level within the fair value hierarchy as shown in the following table. experience, current collateral valuations, borrower credit scores, and internal risk ratings. For individually significant loans or credit relationships, the estimated fair value is determined by a specific loan level review utilizing appraised values for collateral and projections of the timing and amount of expected future cash flows. Borrowed Funds – The fair value of Financial Assets: Cash and due from banks Interest-bearing deposits in other banks Loans held-for-sale Trading securities Securities available-for-sale Securities held-to-maturity Loans, net of allowance for loan losses FDIC indemnification asset Accrued interest receivable Investment in bank-owned life insurance Financial Liabilities: Deposits Borrowed funds Senior and subordinated debt Accrued interest payable Derivative liabilities Standby letters of credit Income taxes refunded Interest paid to depositors and creditors Dividends declared but unpaid Non-cash transfers of securities available-for-sale to securities held-to-maturity Non-cash transfer of securities available-for-sale to other assets Non-cash transfers of loans held-for-investment to loans held-for-sale Non-cash transfers of loans to OREO Non-cash transfer of loans to securities available-for-sale Non-cash exchange of non-performing loans for performing loans Non-cash transfers of OREO to premises, furniture, and equipment Issuance of Common Stock in exchange for the extinguishment of subordinated debt Assets Cash and interest-bearing deposits Investments in and advances to subsidiaries Goodwill Other assets Total assets Liabilities and Stockholders' Equity Senior and subordinated debt Accrued expenses and other liabilities Stockholders' equity Total liabilities and stockholders' equity Income Dividends from subsidiaries Interest income Gains on early extinguishment of debt Securities transactions and other Total income Expenses Interest expense Salaries and employee benefits Other expenses Total expenses Income (loss) before income tax benefit and equity in undistributed (loss) income of subsidiaries Income tax benefit Income (loss) before undistributed (loss) income of subsidiaries Equity in undistributed (loss) income of subsidiaries Net income (loss) Preferred dividends and accretion on preferred stock Net (income) loss applicable to non-vested restricted shares Net income (loss) applicable to common shares Operating Activities Net income (loss) Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: Equity in undistributed loss (income) of subsidiaries Depreciation of premises, furniture, and equipment Net losses on securities Gains on early extinguishment of debt Share-based compensation expense Tax (expense) benefit related to share-based compensation Net (increase) decrease in other assets Net increase (decrease) in other liabilities Net cash provided by (used in) operating activities Investing Activities Purchases of securities available-for-sale Proceeds from sales and maturities of securities available-for-sale Proceeds from sales of premises, furniture, and equipment Purchase of premises, furniture, and equipment Capital injection into subsidiary bank Capital injection into non-bank subsidiary Purchase of non-performing assets from subsidiary bank (1) Net cash used in investing activities Financing Activities Proceeds (payments) for the issuance (retirement) of subordinated debt Redemption of Preferred Shares and related Warrant Proceeds from the issuance of Common Stock Cash dividends paid Exercise of stock options and restricted stock activity Excess tax benefit (expense) related to share-based compensation Net cash (used in) provided by financing activities Net decrease in cash and cash equivalents Cash and cash equivalents at beginning of year Cash and cash equivalents at end of year Equity Compensation Plans Approved by security holders (1) Not approved by security holders (2) Total(State

incorporation or organization) (IRS60143-9768(Address60143-1254