Use these links to rapidly review the document

Table of ContentsITEM 8. Financial Statements Table of ContentsITEM 15. Financial Statements Table of ContentsPART IV

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended October 31, | ||

Or | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission file number 1-4423 | ||

HEWLETT-PACKARD COMPANYHP INC.

(Exact name of registrant as specified in its charter)

| Delaware | 94-1081436 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification no.) | |

94304 | ||

| (Address of principal executive offices) | (Zip code) | |

Registrant's telephone number, including area code:(650) 857-1501 | ||

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filerý | Accelerated filero | Non-accelerated filero (Do not check if a smaller reporting company) | Smaller reporting companyo |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's common stock held by non-affiliates was $61,031,111,812$59,551,395,919 based on the last sale price of common stock on April 30, 2014.2015.

The number of shares of HP Inc. common stock outstanding as of November 30, 20142015 was 1,834,081,9931,791,848,366 shares.

| DOCUMENTS INCORPORATED BY REFERENCE | ||

|---|---|---|

DOCUMENT DESCRIPTION | 10-K PART | |

| Portions of the Registrant's proxy statement related to its | III | |

Hewlett-Packard CompanyHP INC. AND SUBSIDIARIES

Form 10-K

For the Fiscal Year Endedended October 31, 20142015

| | | Page | ||||

|---|---|---|---|---|---|---|

PART I | ||||||

Item 1. | Business | |||||

Item 1A. | Risk Factors | 18 | ||||

Item 1B. | Unresolved Staff Comments | |||||

Item 2. | Properties | |||||

Item 3. | Legal Proceedings | |||||

Item 4. | Mine Safety Disclosures | |||||

PART II | ||||||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |||||

Item 6. | Selected Financial Data | |||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |||||

Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | |||||

Item 8. | Financial Statements and Supplementary Data | |||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |||||

Item 9A. | Controls and Procedures | |||||

Item 9B. | Other Information | |||||

PART III | ||||||

Item 10. | Directors, Executive Officers and Corporate Governance | |||||

Item 11. | Executive Compensation | |||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |||||

Item 14. | Principal Accounting Fees and Services | |||||

PART IV | ||||||

Item 15. | Exhibits and Financial Statement Schedules | |||||

In this report on Form 10-K, for all periods presented, "we", "us", "our", "company", "HP" and "HP Inc." refer to HP Inc. and subsidiaries (formerly Hewlett-Packard Company).

Forward-Looking Statements

This Annual Report on Form 10-K, including "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Item 7, contains forward-looking statements that involve risks, uncertainties and assumptions. If the risks or uncertainties ever materialize or the assumptions prove incorrect, the results of Hewlett-Packard CompanyHP Inc. and its consolidated subsidiaries ("HP") may differ materially from those expressed or implied by such forward-looking statements and assumptions. All statements other than statements of historical fact are statements that could be deemed forward-looking statements, including but not limited to any projections of revenue, margins, expenses, effective tax rates, net earnings, net earnings per share, cash flows, benefit plan funding, deferred tax assets, share repurchases, currency exchange rates or other financial items; any projections of the amount, timing or impact of cost savings or restructuring charges; any statements of the plans, strategies and objectives of management for future operations, including, the previously announced separation transaction and the future performances of the post-separation companies if the separation is completed, as well as the execution of restructuring plans and any resulting cost savings, or revenue or profitability improvements; any statements concerning the expected development, performance, market share or competitive performance relating to products or services; any statements regarding current or future macroeconomic trends or events and the impact of those trends and events on HP and its financial performance; any statements regarding pending investigations, claims or disputes; any statements of expectation or belief; and any statements of assumptions underlying any of the foregoing. Risks, uncertainties and assumptions include the need to address the many challenges facing HP's businesses; the competitive pressures faced by HP's businesses; risks associated with executing HP's strategy, including the planned separation transaction; the impact of macroeconomic and geopolitical trends and events; the need to manage third-party suppliers and the distribution of HP's products and the delivery of HP's services effectively; the protection of HP's intellectual property assets, including intellectual property licensed from third parties; risks associated with HP's international operations; the development and transition of new products and services and the enhancement of existing products and services to meet customer needs and respond to emerging technological trends; the execution and performance of contracts by HP and its suppliers, customers, clients and partners; the hiring and retention of key employees; integration and other risks associated with business combination and investment transactions; the execution, timing and results of the separation transaction or restructuring plans, including estimates and assumptions related to the cost (including any possible disruption of HP's business) and the anticipated benefits of implementing the separation transaction and restructuring plans; the resolution of pending investigations, claims and disputes; and other risks that are described herein, including but not limited to the items discussed in "Risk Factors" in Item 1A of Part I of this report and that are otherwise described or updated from time to time in HP's Securities and Exchange Commission reports. HP assumes no obligation and does not intend to update these forward-looking statements.

Business Overview

We are a leading global provider of products, technologies, software, solutions and services to individual consumers, small- and medium-sized businesses ("SMBs") and large enterprises, including customers in the government, health and education sectors.

HP was incorporated in 1947 under the laws of the state of California as the successor to a partnership founded in 1939 by William R. Hewlett and David Packard. Effective in May 1998, we changed our state of incorporation from California to Delaware.

HP Separation Transaction

On November 1, 2015 (the "Distribution Date"), Hewlett-Packard Company completed the separation of Hewlett Packard Enterprise Company ("Hewlett Packard Enterprise"), Hewlett-Packard Company's former enterprise technology infrastructure, software, services and financing businesses (the "Separation"). In connection with the Separation, Hewlett-Packard Company changed its name to HP Inc. Accordingly, references to the "company" in this report refer to Hewlett-Packard Company with respect to events occurring on or prior to October 31, 2015, and to HP Inc. with respect to events occurring after October 31, 2015.

On November 1, 2015, each of our stockholders of record as of the close of business on October 21, 2015 (the "Record Date") received one share of Hewlett Packard Enterprise common stock for every one share of our common stock held as of the Record Date.

Hewlett Packard Enterprise is now an independent public company trading on the New York Stock Exchange ("NYSE") under the symbol "HPE". After the Separation, we do not beneficially own any shares of Hewlett Packard Enterprise common stock and beginning November 1, 2015, we no longer consolidate Hewlett Packard Enterprise within our financial results or reflect the financial results of Hewlett Packard Enterprise within our continuing results of operations.

The historical results of operations and the financial position of Hewlett Packard Enterprise are included in the consolidated financial statements of HP Inc. for each of the fiscal years included in this report and will be reported as discontinued operations beginning in the first quarter of fiscal 2016.

HP Products and Services; Segment Information

Our offerings span the following:

HP was incorporated in 1947 under the laws of the state of California as the successor to a partnership founded in 1939 by William R. Hewlett and David Packard. Effective in May 1998, we changed our state of incorporation from California to Delaware.

October 2014 Announcement of HP Separation Transaction

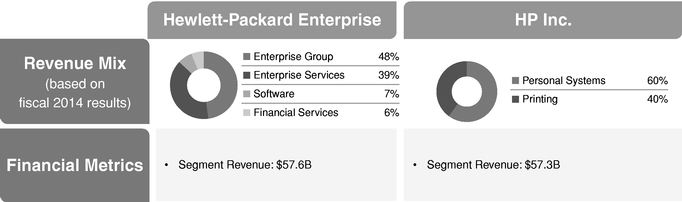

On October 6, 2014, we announced plans to separate into two independent publicly-traded companies: one comprising our enterprise technology infrastructure, software, services and financing businesses, which will conduct business as Hewlett-Packard Enterprise and one that will comprise our printing and personal systems businesses, which will conduct business as HP Inc. The separation is subject to certain conditions, including, among others, obtaining final approval from HP's Board of Directors, receipt of a favorable opinion and/or rulings with respect to the tax-free nature of the transaction for federal income tax purposes and the effectiveness of a Form 10 filing with the SEC. The separation is expected to be completed by the end of fiscal 2015. Under the separation plan, HP shareholders will own shares of both Hewlett-Packard Enterprise and HP Inc. The following chart provides an overview of the planned separation and segment revenues of the respective businesses based on HP's fiscal 2014 results, excluding Corporate Investments and intercompany eliminations.

HP Products and Services; Segment Information

We offer one of the IT industry's broadest portfolios of products and services that bring together infrastructure, software, and services through innovation to enable our customers to create value and solve business problems. As consumers and enterprises shift the way technology is created, delivered,

consumed and paid for, they are demanding a foundation that will support much greater agility, lower cost, facilitate quicker time-to-market, and provide a higher degree of accessibility by end-users to that technology. We design our solutions to provide that foundation, particularly in the areas of security, cloud, mobility and big data, by leveraging the breadth of our offerings and the strengths and capabilities of our individual business units.

Our operations are organized into seven business segments: Personal Systems; Printing; the Enterprise Group ("EG"); Enterprise Services ("ES"); Software; HP Financial Services ("HPFS"); and Corporate Investments. As a result of the Separation, effective November 1, 2015 EG, ES, Software, HPFS and certain parts of Corporate Investments are no longer reported in the continuing results of HP Inc. Personal Systems, Printing and the remaining parts of Corporate Investments segments will be HP Inc.'s reportable segments.

In each of the past three fiscal years, notebook personal computers ("PCs"), printing supplies, infrastructure technology outsourcing services, desktop PCs and industry standard servers ("ISS") each accounted for more than 10% of our consolidated net revenue.

The Personal Systems segment and the Printing segment are structured beneath a broader Printing and Personal Systems Group ("PPS"). While PPS is not a reportable segment, we may provide financial

data aggregating the Personal Systems and Printing segments to provide a supplementary view of its business.

A summary of our net revenue, earnings from operations and assets for our segments along with a description of our fiscal 20142015 organizational realignments can be found in Note 2 to the Consolidated Financial Statements in Item 8, which is incorporated herein by reference. A discussion of factors potentially affecting our operations is set forth in "Risk Factors" in Item 1A, which is incorporated herein by reference.

Printing and Personal Systems Group

The mission of PPS is to leverage the respective strengths of the Personal Systems segment and the Printing segment by creating a unified business that is customer-focused and poised to capitalize on rapidly shifting industry trends. Each of the business segments within PPS is described in detail below.

Personal Systems

Personal Systems provides commercial PCs, consumer PCs, workstations, thin client PCs, tablets, retail point-of-sale ("POS") systems, calculators and other related accessories, software, support and services for the commercial and consumer markets. We group commercial notebooks, commercial desktops, commercial tablets, workstations and thin clients into commercial clients and consumer notebooks consumer desktops and consumer tabletsdesktops into consumer clients when describing performance in these markets. Both commercial and consumer PCs and tablets are based predominately on the Microsoft Windows operating systemsystems and use processors from Intel Corporation ("Intel") and Advanced Micro Devices, Inc. ("AMD"). Personal Systems also maintains a multi-operating system, multi-architecture strategy using the Google Chrome and Android operating systems for notebooks and tablets, respectively.

Commercial PCs. Commercial PCs are optimized for use by customers including enterprise and SMB customers, and for connectivity, reliability and manageability in networked environments. Commercial PCs include the HP ProBook and HP EliteBook lines of notebooks and hybrids (detachable tablets), the HP Pro and HP Elite lines of business desktops and all-in-ones, retail POS systems, HP Thin Clients, HP ElitePad and HP Pro Tablet PCs. Commercial PCs also include workstations that are designed and optimized for high-performance and demanding application environments including Z desktop workstations, Z all-in-ones and Z mobile workstations.

Consumer PCs. Consumer PCs include the HP Spectre, HP ENVY, HP Pavilion, HP Chromebook, HP Split and HP Slate series of multi-media consumer notebooks, consumer tablets, hybrids and desktops, including the TouchSmart line of touch-enabled notebooks and all-in-one desktops.

Printing

Printing provides consumer and commercial printer hardware, supplies, media, software and services, as well as scanning devices. Printing is also focused on imaging solutions in the commercial markets. These solutions range from managed print services to areas such as industrial applications, outdoor signage and the graphic arts business. HP groups LaserJet, large format printers and commercial inkjet printers into Commercial Hardware and consumer and SMB inkjet printers into Consumer Hardware when describing performance in these markets.

LaserJet and Enterprise Solutions. LaserJet and Enterprise Solutions delivers LaserJet and enterprise products, services and solutions to the SMB and enterprise segments including LaserJet printers and supplies (toner), Officejet Pro X inkjet enterprise products and supplies, multi-function devices, scanners, web-connected hardware, managed services, and enterprise software solutions such as

Web Jetadmin. Managed Print Services provides printing equipment, supplies, support, workflow optimization and security features for SMB and enterprise customers around the world, utilizing proprietary HP tools and fleet management solutions, as well as third-party software.

Inkjet and Printing Solutions. Inkjet and Printing Solutions deliver consumer and SMB inkjet solutions (hardware, ink supplies, media, and web-connected hardware and services) and include single-function and all-in-one inkjet printers. Ongoing initiatives and programs, such as Ink in the Office and Ink Advantage, and newer initiatives, such as Instant Ink, are intended to provide innovative printing solutions to consumers and SMBs. Our Ink in the Office initiative is focused on providing high value inkjet printing solutions to SMBs through our Officejet Premium and Officejet Pro inkjet portfolios. Our Ink Advantage program aims to provide savings on the overall cost of printing in emerging markets. Instant Ink is an ink replacement service that allows customers to pay a monthly fee to print a specified number of pages per month.

Graphics Solutions. Graphics Solutions deliver large format printers (Designjet, Large Format Production and Scitex Industrial), specialty printing, digital press solutions (Indigo and Inkjet Webpress), supplies and services to print service providers and design and rendering customers. The solutions cover a wide range of printing applications such as technical design, photos, sign and display, direct mail, marketing collateral, labels and packaging, and publishing.

Software and Web Services. Software and Web Services delivers a suite of offerings, including photo-storage and printing offerings (such as Snapfish), document storage, entertainment services, web-connected printing, and PC back-up and related services.

Marketing Optimization. Marketing Optimization focuses on delivering solutions and software that help businesses engage audiences, reach new customer segments and markets and deliver compelling content across channels. The group provides solutions for augmented reality, contact center analytics, customer communications management and digital experience management.

Enterprise Group

EG provides a broad portfolio of enterprise technology solutions to address customer needs in building the foundation for the next generation of applications, web services and user experiences—which are only as rich, impactful and world-changing as the infrastructure solutions for a variety of operating environmentsplatforms that addressthey sit on. EG technology addresses a wide range of customer challenges, including the needsupporting new types of applications, new approaches to increase agilityIT operations, and accelerate innovation in ordernew demands and uses for insight, and managing new threats and risks. EG technology also allows customers to drivecapitalize on a wide range of trends and

opportunities, from servicing new segments and buying behaviors to inventing new consumption models and creating new revenue manage risk and lower costs. HP Helion, our enterprisestreams. EG technology infrastructuredelivers customer outcomes through its innovative, industry leading portfolio ofacross servers, storage, networking, management software, converged infrastructure solutions, and technology services. In today's rapidly changing technology landscape, customers face twin challenges when it comes to their infrastructure foundation: they must optimize their "traditional IT" to support existing applications, and they must simultaneously invest in "cloud-first, mobile-first" infrastructure that will support the next generation of applications, web services and user experiences. The EG portfolio delivers products and services across servers, storage and networking to reduce cost and continue high performance operations for traditional IT loads. For tomorrow's cloud-first, mobile first workloads, the EG portfolio provides products and services across converged solutions engineered for the world's most important workloads in cloud, mobility, infrastructure-as-a-service, and big data; HP OneView as the industry's only unified display software-defined infrastructure management solution; HP Helion cloud portfolio delivering a broad offering of hybrid cloud solutions, cloud services and cloud software; and technology services combined with HP's cloud services and software, allowsto advise customers on the right path to adopt a holistic approach to building a technology infrastructure that supportstransforming their current business and consumer demands and next generation applications and web services. HP's Converged Systems portfolio (servers, storage and networking) simplifies IT through quick deployment, intuitive management and system-level support. Optimizedenterprises for key workloads such as virtualization, cloud and big data, these complete, integrated solutions enable organizations of all sizes to efficiently utilize IT staffing resources and deploy applications faster.tomorrow's digital era.

Industry Standard Servers. Industry Standard ServersISS offers a range of products from entry-level servers through premium ProLiant servers, which run primarily Windows, Linux and virtualization platforms from software providers such as Microsoft Corporation ("Microsoft") and VMware, Inc. ("VMware"), and open source software from other major vendors while leveraging x86 processors from Intel and AMD. The business spans a range of server product lines, including microservers, towers, traditional rack, density-optimized rack and blades, solutions for large, distributed computing companies who buy and deploy nodes at a massive scale. Industry Standard ServersISS also offers HP Moonshot servers operating on ARM, AMD and Intel Atom-based processors which offer reduced cost, space, energy and complexity compared to traditional servers.

Business Critical Systems. Business Critical Systems delivers our mission-critical systems through a portfolio of HP Integrity servers based on the Intel Itanium processor that run the HP-UX and OpenVMS operating systems, as well as HP Integrity NonStop solutions and mission-critical x86 ProLiant servers.

Storage. Our storage offerings include platforms for enterprise and SMB environments. Our flagship product is the 3PAR StoreServ Storage Platform, which is designed for virtualization, cloud and IT-as-a-service. Traditional Storage solutions include tape, storage networking and legacy external disk products such as EVA and XP. Converged Storage solutions include 3PAR StoreServ, StoreOnce and StoreVirtual products. These offerings enable customers to optimize their existing storage systems, build new virtualization solutions and facilitate their transition to cloud computing.

Networking. Our networking offerings include switches, routers, wireless local area network ("WLAN") and network management products that deliver open, scalable, secure, agile and consistent solutions that span the data center, campus and branch environments and deliver software-defined networking and unified communications capabilities. Our unified wired and wireless networking offerings include both WLAN access points, controllers and switches. Our networking solutions are based on our FlexNetwork architecture, which is designed to enable simplified server virtualization, unified communications and multi-mediabusiness application delivery for the enterprise. Software-defined networking provides an end-to-end solution to automate the network from data center to campus and branch.

Technology Services. Technology Services provides support servicesSupport and technology consulting, focused on cloud, mobility and big data and provides IT organizations with advice, design, implementation, migration and optimization of EG's platforms: servers, storage, networking and converged infrastructure.Consulting services. Support services offerings span various levels of customer support needs and include: HP Foundation Care, our portfolio of reactive hardware and software support services; HP Proactive Care, which combines remote support technology for real-timereal time monitoring with rapid access to our technical experts; HP Datacenter Care, a comprehensive, and flexible capacity end-to-end support for HP and multi-vendor systems that enables customers to build, operate or consume IT in traditional, cloudprivate or hybrid cloud environments; and Lifecycle Event services, which are event-basedevent

based services, offering our technology expertise and consultingadvice for each phase of the technology life cycle. These services are available in the form of service contracts, pre-packaged offerings (HP Care Pack services) or on a customized basis. Consulting services are focused on cloud, mobility and big data and provide IT organizations with advice, design, implementation, migration and optimization of EG's platforms: servers, storage, networking and converged infrastructure.

Enterprise Services

ES provides technology consulting, outsourcing and support services across infrastructure, applications and business process domains.domains in traditional and Strategic Enterprise Services offerings which includes analytics and data management, security and cloud services. ES delivers toleverages our clients by leveraging investments in our consulting and support professionals, infrastructure technology, applications, standardized methodologies and global supply and delivery.delivery capabilities. ES also creates opportunities for us to sellmarket additional hardware and software by offering solutions that encompass bothleverage our other products and services.services in order to meet our clients' needs.

Infrastructure Technology Outsourcing. The Infrastructure Technology Outsourcing group delivers comprehensive services that streamline and help optimize our clients' technology infrastructure to efficiently enhance performance, reduce costs, mitigate risk and enable business change.optimization. These services encompass the management of data centers, IT security, cloud computing, workplace technology, networks, unified communications and enterprise service management. We also offer a set of managed services that provide a cross-section of our broader infrastructure services for smaller, discrete engagements.

Application and Business Services. The Application and Business Services portfolio helps our clients develop, revitalize and manage their applications and information assets. This fullOur complete application life cyclelifecycle approach encompasses application development, testing, modernization, system integration, maintenance and management for both packaged and custom-built applications and cloud offerings. TheOur Application and Business Services portfolio also includes intellectual property-based industry solutions, along with technologies and related services, all of which help our clients better manage their critical industry processes for customer relationship management, finance and administration, human resources, payroll and document processing.

Software

Software portfolio provides IT management,big data analytics and applications, enterprise security, application testing and delivery information management big data analytics, security intelligence and risk managementIT Operations Management solutions for businesses and other enterprises of all sizes. Our softwareSoftware offerings include licenses, support, professional services and software-as-a-service ("SaaS"). Described below are ourOur global business capabilities within Software.Software are described below.

Application Delivery Management Big Data. which is part of HP's IT management offerings, provides software that enables organizations to deliver high performance applications by automating and testing the processes required to ensure the quality and scalability of desktop, web, mobile and cloud-based applications.

Big Data group provides a full suite of software designed to help organizations capture, store, explore, govern,analyze, protect and serveshare information and insights that fundamentallywithin and outside their organizations to improve thebusiness outcomes, of businesseswhile also enabling them to manage risks and the environment, while managing risk and meetingmeet legal obligations. The group'sOur Big Data suite includes HP Vertica, the leading analytics platformdatabase technology for machine, structured and semi-structured data,data; HP IDOL, a unique analytics platformtool for human information from Autonomy,information; as well as market leading solutions for archiving, data protection, eDiscovery, information governance and Enterprise Content Management.

Enterprise Security software is designed to disrupt fraud, hackers and cyber criminals by scanning software and websites for security vulnerabilities, improving network defenses and providing real-time warning of threats as they emerge.

IT Operations Management which is part of HP's IT management offerings, provides software required to automate routine IT tasks and to pinpoint IT problems when they occur, helping enterprises to reduce operational costs and improve the reliability of applications running in a traditional, cloud or hybrid environment.

Marketing Optimization focuses on delivering solutions that help businesses engage audiences, reach new customer segments and markets and deliver compellingenterprise content across channels. The group provides solutions for augmented reality, contact center analytics, customer communications management and digital experience management.

Software'sOur big data platform, HAVEn, providesHaven, brings these unique assets together for processing and understanding machine and sensor data, business data and unstructured human information. A growing ecosystem of customers, partners and developers use this platform to build big data driven analytic applications. Our Software segment also leverages HAVEn'sHaven's unique analytic assets to deliver market-leading, purpose-built solutions for a variety of markets, including application testing and delivery, big data analytics and applications, IT operations management, marketing optimizationOperations Management, and enterprise security. These solutions are designed for businesses and enterprises of all sizes, and are available via on-premises,on-premise, as well as via SaaS and hybrid delivery models. Software's HAVEnHaven big data platform and purpose-built applications are augmented by our support and professional services offerings in order to provide an end-to-end solution to customers.

Application Delivery Management. The Application Delivery Management group provides software that enables organizations to deliver high-performance applications, accelerating the application delivery lifecycle and automating the testing processes to ensure the quality and scalability of desktop, web, mobile and cloud-based applications.

Enterprise Security. Enterprise Security software is designed to disrupt fraud, hackers and cyber criminals by testing and scanning software and websites for security vulnerabilities, improving network defenses and security, implementing security controls, safeguarding data at rest, in motion and in use (regardless of where software and data reside), and providing security intelligence, analytics, and information management to identify threats and manage risk.

IT Operations Management. The IT Operations Management group provides the software required to automate routine IT tasks and to pinpoint IT problems as they occur, helping enterprises to reduce operational costs and improve the reliability of applications running in a traditional, cloud or hybrid environment.

HP Financial Services

HPFS provides flexible investment solutions for our customers, such as leasing, financing, IT consumption and utility programs and asset management services for customers to enable the creation ofthat facilitate unique technology deployment models and the acquisition of complete IT solutions, including hardware, software and services from HP and others. ProvidingIn order to provide flexible services and capabilities that support the entire IT lifecycle, HPFS partners with our customers globally to help build investment strategies that enhance their business agility and support their business transformation. HPFS offers a wide selection of investment solution capabilities for large enterprise customers and channel partners, along with an array of financial options to SMBs and educational and governmental entities.

Corporate Investments

Corporate Investments includes HP Labs, and certain cloud-relatedenterprise-related business incubation projects and venture focused minority investments, among others.

Sales, Marketing and Distribution

We manage our business and report our financial results based on the business segments described above. Our customers are organized by consumer and commercial groups, and purchases of HP products, solutions and services may be fulfilled directly by HP or indirectly through a variety of partners, including:

The mix of our business conducted by direct sales or channel differs substantially by business and region. We believe that customer buying patterns and different regional market conditions require us to tailor our sales, marketing and distribution efforts accordingly. We are focused on driving the depth and breadth of our coverage, in addition to identifying efficiencies and productivity gains, in both our direct and indirect businesses. While each of our business segments manages the execution of its own go-to-market and distribution strategy, our business segments also collaborate to ensure strategic and process alignment where appropriate. For example, we typically assign an account manager generally from EG or ES, to manage relationships across our business with large enterprise customers. The account manager is supported by a team of specialists with product and services expertise. For other customers and for consumers, PPS typically manages direct online sales as well as channel relationships with retailers, while our business segments collaborate to manage relationships with commercial resellers targeting SMBs where appropriate.

Manufacturing and Materials

We utilize a significant number of outsourced manufacturers ("OMs") around the world to manufacture HP-designed products. The use of OMs is intended to generate cost efficiencies and reduce time to market for HP-designed products. We use multiple OMs to maintain flexibility in our supply chain and manufacturing processes. In some circumstances, third-party OEMs produce products that we purchase and resell under the HP brand. In addition to our use of OMs, we currently manufacture a limited number of finished products from components and subassemblies that we acquire from a wide range of vendors.

We utilize two primary methods of fulfilling demand for products: building products to order and configuring products to order. We build products to order to maximize manufacturing and logistics efficiencies by producing high volumes of basic product configurations. Alternatively, configuring products to order enables units to match a customer's particular hardware and software customization requirements. Our inventory management and distribution practices in both building products to order and configuring products to order seek to minimize inventory holding periods by taking delivery of the inventory and manufacturing shortly before the sale or distribution of products to our customers.

We purchase materials, supplies and product subassemblies from a substantial number of vendors. For most of our products, we have existing alternate sources of supply or such alternate sources of supply are readily available. However, we do rely on sole sources for laser printer engines, LaserJet supplies, certain customized parts and parts for products with short life cycles (although some of these sources have operations in multiple locations in the event of a disruption). We are dependent upon Intel and AMD as suppliers of x86 processors and Microsoft for various software products; however, we believe that disruptions with these suppliers would result in industry-wide dislocations and therefore would not disproportionately disadvantage us relative to our competitors. See "Risk Factors—We depend on third-party suppliers, and our financial results could suffer if we fail to manage our suppliers properly,effectively," in Item 1A, which is incorporated herein by reference.

Like other participants in the IT industry, we ordinarily acquire materials and components through a combination of blanket and scheduled purchase orders to support our demand requirements for periods averaging 90 to 120 days. From time to time, we may experience significant price volatility or supply constraints for certain components that are not available from multiple sources. Frequently, we are able to obtain scarce components for somewhat higher prices on the open market, which may have an impact on our gross margin but does not generally disrupt production. We also may acquire component inventory in anticipation of supply constraints or enter into longer-term pricing

commitments with vendors to improve the priority, price and availability of supply.supplies. See "Risk Factors—We depend on third-party suppliers, and our financial results could suffer if we fail to manage our suppliers properly,effectively," in Item 1A, which is incorporated herein by reference.

International

Our products and services are available worldwide. We believe this geographic diversity allows us to meet demand on a worldwide basis for both consumer and enterprise customers, draws on business and technical expertise from a worldwide workforce, provides stability to our operations, provides revenue streams that may offset geographic economic trends and offers us an opportunity to access new markets for maturing products. In addition, we believe that future growth is dependent in part on our ability to develop products and sales models that target developing countries. In this regard, we believe that our broad geographic presence gives us a solid base on which to build such future growth.

A summary of our domestic and international net revenue and net property, plant and equipment is set forth in Note 2 to the Consolidated Financial Statements in Item 8, which is incorporated herein by reference. Approximately 65%64% of our overall net revenue in fiscal 20142015 came from outside the United States ("U.S.").

For a discussion of risks attendant to HP's international operations, see "Risk Factors—Due to the international nature of our business, political or economic changes or other factors could harm our future revenue, costs and expenses,business and financial condition,performance," in Item 1A, "Quantitative and Qualitative Disclosure about Market Risk," in Item 7A and Note 11 to the Consolidated Financial Statements in Item 8, which are incorporated herein by reference.

Research and Development

Innovation is a key element of our culture. Our development efforts are focused on designing and developing products, services and solutions that anticipate customers' changing needs and desires, and emerging technological trends. Our efforts also are focused on identifying the areas where we believe we can make a unique contribution and the areas where partnering with other leading technology companies will leverage our cost structure and maximize our customers' experiences.

HP Labs, together with the various research and development groups within our business segments, are responsible for our research and development efforts. HP Labs is part of our Corporate Investments segment.

Expenditures for research and development were $3.5 billion in fiscal 2015, $3.4 billion in fiscal 2014 and $3.1 billion in fiscal 2013 and $3.4 billion in fiscal 2012.2013. We anticipate that we will continue to have significant research and development expenditures in the future to support the design and development of innovative, high-quality products and services to maintain and enhance our competitive position.

For a discussion of risks attendant to our research and development activities, see "Risk Factors—If we cannot successfully execute on our go-to-market strategy and continue to develop, manufacture and market innovative products and services, our business and solutions that meet customer requirements for innovation and quality, our revenue and gross marginfinancial performance may suffer," in Item 1A, which is incorporated herein by reference.

Patents

Our general policy has been to seek patent protection for those inventions likely to be incorporated into our products and services or where obtaining such proprietary rights will improve our competitive position. At October 31, 2014,2015, our worldwide patent portfolio included over 34,00033,000 patents, which represents a slight decrease over the number of patents in our portfolio at the end of fiscal 2013 and fiscal 2012. This decrease is attributable, in part,2014. As a result of the Separation, approximately 15,000 patents were transferred to the saleHewlett Packard Enterprise beginning November 1, 2015.

Table of a portfolio of mobile computing intellectual property ("IP") in January 2014.Contents

Patents generally have a term of twenty years from the date they are filed. As our patent portfolio has been built over time, the remaining terms of the individual patents across our patent portfolio vary. We believe that our patents and patent applications are important for maintaining the competitive differentiation of our products and services, enhancing our freedom of action to sell our products and services in markets in which we choose to participate, and maximizing our return on research and development investments. No single patent is in itself essential to HP as a whole or to any of HP's business segments.

In addition to developing our patent portfolio, we license IPintellectual property ("IP") from third parties as we deem appropriate. We have also granted and continue to grant to others licenses, and other rights, under our patents when we consider these arrangements to be in our interest. These license arrangements include a number of cross-licenses with third parties.

For a discussion of risks attendant to IP rights, see "Risk Factors—Our revenue, cost of sales, and expensesfinancial performance may suffer if we cannot continue to develop, license or enforce the IPintellectual property rights on which our business depends or if third parties assert that we violate their IP rights,businesses depend," in Item 1A, which is incorporated herein by reference.

Backlog

We believe that backlog is not a meaningful indicator of future business prospects due to our diverse products and services portfolio, including the large volume of products delivered from finished goods or channel partner inventories and the shortening of product life cycles. Therefore, we believe that backlog information is not material to an understanding of our overall business.

Seasonality

General economic conditions have an impact on our business and financial results. From time to time, the markets in which we sell our products and services experience weak economic conditions that may negatively affect sales. We experience some seasonal trends in the sale of our products and services. For example, European sales are often weaker in the summer months and consumer sales are often stronger in the fourth calendar quarter. Demand during the spring and early summer months also may be adversely impacted by market anticipation of seasonal trends. See "Risk Factors—Our uneven sales cycle makes planning and inventory management difficult and future financial results less predictable," in Item 1A, which is incorporated herein by reference.

Competition

We encounter strong competition in all areas of our business activity. We compete primarily on the basis of technology, performance, price, quality, reliability, brand, reputation, distribution, range of products and services, ease of use of our products, account relationships, customer training, service and support, security, availability of application software and internet infrastructure offerings.

The markets for each of our business segments are characterized by strong competition among major corporations with long-established positions and a large number of new and rapidly growing firms. Most product life cycles are short, and to remain competitive we must develop new products and services, periodically enhance our existing products and services and compete effectively on the basis of the factors listed above. In addition, we compete with many of our current and potential partners, including OEMs that design, manufacture and often market their products under their own brand names. Our successful management of these competitive partner relationships will be critical to our future success. Moreover, we anticipate that we will have to continue to adjust prices on many of our products and services to stay competitive.

We have a broad technology portfolio spanning personal computing and other access devices, imaging and printing-related products and services, enterprise IT infrastructure products and solutions,

multi-vendor customer services and IT management software and solutions. We are the leader or among the leaders in each of our business segments.

The competitive environments in which each segment operates are described below:

Personal Systems. The markets in which Personal Systems operates are highly competitive and are characterized by price competition and inventory obsolescence.competition. The decline in the PC market and the ongoing shift among customers to mobility products has further intensified competition in the PC market. Our primary competitors are Lenovo Group Limited ("Lenovo"), Dell Inc. ("Dell"), Acer Inc., ASUSTeK Computer Inc., Apple Inc., Toshiba Corporation and Samsung Electronics Co., Ltd. ("Samsung"). In particular regions, we also experience competition from local companies and from generically-branded or "white box" manufacturers. Our competitive advantages include our broad product portfolio, our innovation and research and development capabilities, our brand and procurement leverage, our ability to cross-sell our portfolio of offerings, our extensive service and support offerings and the accessibility of our products through a broad-based distribution strategy from retail and commercial channels to direct sales.

Printing. The markets for printer hardware and associated supplies are highly competitive. Printing's key customer segments each face competitive market pressures in pricing and the introduction of new products. Our primary competitors include Canon U.S.A., Inc., Lexmark International, Inc., Xerox Corporation Ltd., Seiko Epson Corporation, The Ricoh Company Ltd., Samsung and Brother Industries, Ltd. In addition, independent suppliers offer refill and remanufactured alternatives for HP original inkjet and toner supplies, which are often available for lower prices but generally offer lower print quality and reliability. Other competitors also have

developed and marketed new compatible cartridges for HP's laser and inkjet products, particularly outside of the U.S. where IP protection is inadequate or ineffective. Our competitive advantages include our comprehensive solutions for the home, office and publishing environments, our innovation and research and development capabilities, our brand, and the accessibility of our products through a broad-based distribution strategy from retail and commercial channels to direct sales.

Enterprise Group. EG operates in the highly competitive enterprise technology infrastructure market that is characterized by rapid and ongoing technological innovation and price competition. Our primary competitors include technology vendors such as International Business Machines Corporation ("IBM"), Dell, EMC Corporation ("EMC"), Cisco Systems, Inc. ("Cisco"), Lenovo, Oracle Corporation ("Oracle"), Fujitsu Limited ("Fujitsu"), Inspur Co. Ltd., Huawei Technologies Co. Ltd., NetApp, Inc., Hitachi Ltd., Juniper Networks, Inc., Arista Networks, Inc., Extreme Networks, Inc., Brocade Communications Systems, Inc., VMware, Microsoft, Google Inc., Rackspace Inc., and Amazon.com, Inc. ("Amazon"). In certain regions, we also experience competition from local companies and from generically-branded or "white-box" manufacturers. Our strategy is to deliver superior products, high-value technology support services and differentiated integrated solutions that combine our infrastructure, software and services capabilities. Our competitive advantages include our broad end-to-end solutions portfolio, supported by our strong IP portfolio and research and development capabilities, coupled with our global reach and partner ecosystem.

Enterprise Services. ES competes in the IT services, consulting and integration, infrastructure technology outsourcing, business process outsourcing and application serviceservices markets. Our primary competitors include IBM Global Services, Computer Sciences Corporation, systems integration firms such as Accenture plc.plc and offshore companies such as Fujitsu and India-based competitors Wipro Limited, Infosys Limited and Tata Consultancy Services Ltd. We also compete with other traditional hardware providers, such as Dell, which are increasingly offering services to support their products, new players in emerging areas like cloud such as Amazon, and smaller local players. Many of our competitors offer a wide range of global services, and some of our competitors enjoy significant brand recognition. ES teams with many companies to offer services, and those arrangements allow us to

extend our reach and augment our capabilities. Our competitive advantages include our deep technology expertise, especially in complex multi-country, multi-vendor and/or multi-language environments, our differentiated IP,intellectual property, our strong track record of collaboration with clients and partners, and the combination of our expertise in infrastructure management with skilled global resources on platforms from SAP AG ("SAP"), Oracle and Microsoft, among others.

Software. The markets in which our Software segment operates are fueledcharacterized by rapidly changing customer requirements and technologies. We design and develop enterprise IT management software in competition with IBM, CA Technologies, Inc., VMware, BMC Software, Inc. and others. Our big data solutions, which include data analytics, information governance and digital marketing offerings incorporating both structured and unstructured data, compete with products from companies like Adobe Systems Inc., IBM, EMC, Open Text Corporation, Oracle and Symantec Corporation. We also deliver enterprise security/risk intelligence solutions that compete with products from EMC, IBM, Cisco and Intel. As customers are becoming increasingly comfortable with newer delivery mechanisms such as SaaS, we are facing competition from smaller, less traditional competitors, particularly for customers with smaller IT organizations. Our differentiation lies in the breadth and depth of our software, our collaboration with EG and ES to provide comprehensive IT solutions and services portfolio and the scope of our market coverage.

HP Financial Services. In our financing solution business, our competitors are captive financing companies, mainly IBM Global Financing, as well as banks and other financial institutions.institutions in our financing business. We believe our competitive advantage in this business over banks and other financial institutions is our ability to deliver flexible investment solutions and expertise that help customers and other partners create unique technology deployments based on specific business needs.

For a discussion of risks attendant to these competitive factors, see "Risk Factors—CompetitiveWe operate in an intensely competitive industry and competitive pressures could harm our revenue, gross marginbusiness and prospects,financial performance," in Item 1A, which is incorporated herein by reference.

Environment

Our operations are subject to regulation under various federal, state, local and foreign laws concerning the environment, including laws addressing the discharge of pollutants into the air and water, the management and disposal of hazardous substances and wastes, and the cleanup of contaminated sites. We could incur substantial costs, including cleanup costs, fines and civil or criminal sanctions, and third-party damage or personal injury claims, if we were to violate or become liable under environmental laws.

Many of our products are subject to various federal, state, local and foreign laws governing chemical substances in products and their safe use, including laws regulating the manufacture and distribution of chemical substances and laws restricting the presence of certain substances in electronics products. Some of our products also are, or may in the future be, subject to requirements applicable to their energy consumption. In addition, we face increasing complexity in our product design and procurement operations as we adjust to new and future requirements relating to the chemical and materials composition of our products, their safe use, and their energy efficiency, including requirements relating to climate change. We are also subject to legislation in an increasing number of jurisdictions that makes producers of electrical goods, including computers and printers, financially responsible for specified collection, recycling, treatment and disposal of past and future covered products (sometimes referred to as "product take-back legislation"). In the event our products become non-compliant with these laws, our products could be restricted from entering certain jurisdictions and we could face other sanctions, including fines.

Our operations, and ultimately our products, are expected to become increasingly subject to federal, state, local and foreign laws, regulations and international treaties relating to climate change.

As these laws, regulations, treaties and similar initiatives and programs are adopted and implemented throughout the world, we will be required to comply or potentially face market access limitations or other sanctions, including fines. However, we believe that technology will be fundamental to finding solutions to achieve compliance with and manage those requirements, and we are collaborating with industry, business groups and governments to find and promote ways that HP technology can be used to address climate change and to facilitate compliance with related laws, regulations and treaties.

We are committed to maintaining compliance with all environmental laws applicable to our operations, products and services and to reducing our environmental impact across all aspects of our business. We meet this commitment with a comprehensive environmental, health and safety policy, strict environmental management of our operations and worldwide environmental programs and services.

A liability for environmental remediation and other environmental costs is accrued when we consider it probable that a liability has been incurred and the amount of loss can be reasonably estimated. Environmental costs and accruals are presently not material to our operations, cash flows or financial position. Although there is no assurance that existing or future environmental laws applicable to our operations or products will not have a material adverse effect on our operations, cash flows or financial condition, we do not currently anticipate material capital expenditures for environmental control facilities.

For a discussion of risks attendant to these environmental factors, see "Risk Factors—Unforeseen environmentalOur business is subject to various federal, state, local and foreign laws and regulations that could result in costs couldor other sanctions that adversely affect our business and results of operations," in Item 1A, which is incorporated herein by reference. In addition, for a discussion of our environmental contingencies see

Note 1516 to the Consolidated Financial Statements in Item 8, which is also incorporated herein by reference.

Executive Officers

The following are our current executive officers:

Martin Fink;Rob Binns; age 50; Executive47; Head of Global Treasury and Investor Relations

Mr. Binns has served as Head of Global Treasury and Investor Relations since November 2015. Mr. Binns joined Hewlett-Packard Company in 2006 as Finance Director for HP Software in the Europe, Middle East and Africa regions following the acquisition of Mercury Interactive. Since then, Mr. Binns has held a number of finance and business roles within HP Software, including Vice President of Worldwide Field Operations. Previously, Mr. Binns was Vice President of Investor Relations. Most recently, Mr. Binns was the Vice President and Chief TechnologyFinancial Officer for HP Software responsible for driving all finance activities.

Ron Coughlin; age 49; President, Personal Systems

Mr. Coughlin has served as President, Personal Systems since November 2015. Mr. Coughlin joined Hewlett-Packard Company from PepsiCo in June 2007 as the senior vice president of the Imaging and Printing Group Worldwide Strategy and Marketing team. In 2010, Mr. Coughlin transitioned to lead the LaserJet and Enterprise Solutions global business unit at Hewlett-Packard Company and later ran Consumer Personal Systems at Hewlett-Packard Company.

Jon Flaxman; age 58; Chief Operating Officer

Mr. FinkFlaxman has served as Executive Vice President, Chief TechnologyOperating Officer and Director of HP Labs since November 2012. Prior to that, he2015. Previously, Mr. Flaxman served as Senior Vice President and General ManagerChief Financial Officer for Hewlett-Packard Company's Printing

Table of the Business CriticalContents

and Personal Systems and Converged Application Systems from April 2005Group. Prior to October 2012. During his almost 30 year career at HP, Mr. Fink has worked in a wide range of roles across HP. He also serves as a director of Hortonworks, Inc.

Henry Gomez; age 51; Executivesuch role, he was Senior Vice President of Finance for Hewlett-Packard Company's Imaging and Printing Group for four years. From March 2007 to November 2008, Mr. Flaxman was Chief Marketing and Communications Officer

Mr. Gomez has served as Executive Vice President and Chief Marketing and Communications Officer since August 2013. Previously, he served as Chief CommunicationsAdministrative Officer and Executive Vice President from January 2012 to July 2013. Prior to that, he ran HSG Communications, a consulting business that he foundedof Hewlett-Packard Company. Mr. Flaxman joined Hewlett-Packard Company in September 2008. He also served on the leadership team of Ms. Whitman's gubernatorial campaign from February 2009 to November 2010. For most of the previous decade, he worked at eBay Inc. in a variety of roles including Senior Vice President for Corporate Communications and President of Skype. From September 2011 to September 2013 he served as a director of BJ's Restaurants, Inc.

John M. Hinshaw; age 44; Executive Vice President, Technology and Operations

Mr. Hinshaw has served as Executive Vice President, Technology and Operations since November 2011. Previously, Mr. Hinshaw served as Vice President and General Manager of Information Solutions at The Boeing Company, an aerospace company, from January 2011 to October 2011 and as Global Chief Information Officer for Boeing from June 2007 to December 2010. He also serves as a director of Bank of New York Mellon.

Abdo George Kadifa; age 55; Executive Vice President, Strategic Relationships

Mr. Kadifa has served as Executive Vice President, Strategic Relationships since May 2014. Previously, Mr. Kadifa served as Executive Vice President, Software from May 2012 to May 2014. Prior to that, he served as a director of Silver Lake, a private equity firm, from June 2007 to May 2012.1981.

Tracy S. Keogh; age 53; Executive Vice President,54; Chief Human Resources Officer

Ms. Keogh has served as Chief Human Resources Officer since November 2015. Previously, Ms. Keogh served as Executive Vice President, Human Resources sinceof Hewlett-Packard Company from April 2011. Previously,2011 to November 2015. Prior to joining Hewlett-Packard Company, Ms. Keogh served as Senior Vice President of Human Resources at Hewitt Associates, a provider of human resources consulting services, from May 2007 until March 2011.

Catherine A. Lesjak; age 55; Executive Vice President and56; Chief Financial Officer

Ms. Lesjak has served as Chief Financial Officer since November 2015. Previously, Ms. Lesjak served as Executive Vice President and Chief Financial Officer since January 2007.of Hewlett-Packard Company from 2007 to November 2015. Prior to that, Ms. Lesjak served as Hewlett-Packard Company's interim Chief Executive Officer from August 2010 until November 2010. She also serves as a director of SunPower Corporation.

Todd R. Morgenfeld;Enrique Lores; age 42; Treasurer50; President, Printing, Solutions and Senior Vice President, Corporate Development and Corporate Analytics

Mr. Morgenfeld has served as Treasurer and Senior Vice President, Corporate Development and Corporate Analytics since November 2013. Previously, Mr. Morgenfeld served as Senior Vice President, HP Mobility, supporting our strategy of providing integrated solutions for the rapidly changing information technology landscape, from June 2013 to October 2013. Prior to that, Mr. Morgenfeld served in several roles at Silver Lake, a private equity firm, from 2004 until May 2013, most recently serving as a director.

Michael G. Nefkens; age 45; Executive Vice President, Enterprise Services

Mr. NefkensLores has served as Executive Vice President, EnterprisePrinting, Solutions and Services since December 2012.November 2015. Throughout his 26-year tenure with Hewlett-Packard Company, Mr. Lores held leadership positions across the organization, most recently leading the Separation Management Office for HP Inc. Previously, he served in that role in an acting capacity since August 2012. Prior to that, Mr. Nefkens served asLores was the Senior Vice President and General Manager of Enterprise Services in the EMEA region from November 2009 to August 2012, after having served in client-facing roles for some of Enterprise Services' largest clients since joining the business in 2001. He also serves as a director of Riverbed Technology, Inc.

Jeff T. Ricci; age 53;Business Personal Systems. Before his Business Personal Systems role, Mr. Lores was Senior Vice President of Customer Support and Services.

Marie Myers; age 47; Global Controller and Principal Accounting OfficerHead of Finance Services

Mr. RicciMs. Myers has served as Senior Vice President,Global Controller and Principal Accounting OfficerHead of Finance Services since April 2014. Previously, Mr. Ricci served as Controller and Principal Accounting Officer on an interim basis from November 2013 to April 2014.2015. Prior to that Mr. Ricci served asfrom October 2014 to October 2015, Ms. Myers was Finance Lead for HP Inc. in the Separation, and held key leadership roles at Hewlett-Packard Company, including: Vice President offor PPS HQ and Strategy Finance for our Technology and Operations organization from May 2012 to November 2013. Mr. Ricci served as Vice President of Finance for Global Accounts and HP Financial Services from March 2011 to May 2012October 2015 and Vice President of Finance for HP SoftwarePSG Americas from March 20092010 to March 2011.May 2012.

Kim Rivera; age 47; Chief Legal Officer and General Counsel

Ms. Rivera has served as Chief Legal Officer and General Counsel since November 2015. Prior to joining HP, Mr. Riccius, at DaVita Health Care Partners she served as Senior Vice President of Finance for BEA Systems, Inc., an enterprise software company,the Chief Legal Officer from 2000 until June 2008.

John F. Schultz; age 50; Executive Vice President, General CounselJuly 2011 to October 2015, as Corporate Secretary from January 2010 to December 2013 and Secretary

Mr. Schultz has served as Executive Vice President, General Counsel and Secretary since April 2012. Previously, he served as Deputy General Counsel for Litigation, Investigations and Global Functions from September 2008 to April 2012. From March 2005 to September 2008, Mr. Schultz was a partner in the litigation practice at Morgan, Lewis & Bockius LLP, where, among other clients, he supported HP as external counsel on a variety of litigation and regulatory matters.

William L. Veghte; age 47; Executive Vice President and General Manager, Enterprise Group

Mr. Veghte hasCounsel from January 2010 to July 2011. From February 2006 to November 2009, she served as Executive Vice President and Associate General Manager of the Enterprise Group since August 2013. Previously, he served as Chief Operating Officer from May 2012 to August 2013.Counsel at The Clorox Company. Prior to that, Mr. VeghteMs. Rivera served as Executive Vice President of HP Software from May 2010Law and Chief Litigation Counsel to May 2012. Prior to joining HP, Mr. Veghte servedRockwell Automation as Senior Vice President of the Windows business group at Microsoft Corporation, a software company, from February 2008 until January 2010.well as General Counsel for its Automation Controls and Information Group.

Dion J. Weisler; age 47;48; President and Chief Executive Vice President, Printing and Personal Systems GroupOfficer

Mr. Weisler has served as President and Chief Executive Officer since November 2015. Previously, he served as Executive Vice President of the Printing and Personal Systems Group sinceof Hewlett-Packard Company from June 2013. Previously, he served2013 to November 2015 and as Senior Vice President and Managing Director, Printing and Personal Systems, Asia Pacific and Japan from January 2012 to June 2013. Prior to joining HP,

Hewlett-Packard Company, he was Vice President and Chief Operating Officer of the Product and Mobile Internet Digital Home Groups at Lenovo Group Ltd., a technology company, from January 2008 to December 2011.

Margaret C. Whitman; age 58; Chairman, President and Chief Executive Officer

Ms. Whitman has served as Chairman since July 2014, President and Chief Executive Officer since September 2011 and as a member of our Board of Directors since January 2011. From March 2011 to September 2011, Ms. Whitman served as a part-time strategic advisor to Kleiner Perkins Caufield & Byers, a private equity firm. Previously, Ms. Whitman served as President and Chief Executive Officer of eBay Inc., from 1998 to March 2008. Prior to joining eBay, Ms. Whitman held executive-level positions at Hasbro Inc., FTD, Inc., The Stride Rite Corporation, The Walt Disney Company, and Bain & Company. Ms. Whitman also serves as a director of The Procter & Gamble Company and is a former director of Zipcar, Inc.

Robert Youngjohns; age 63; Executive Vice President and General Manager, HP Software

Mr. Youngjohns has served as Executive Vice President and General Manager of HP Software since May 2014. Previously, Mr. Youngjohns served as Senior Vice President and General Manager of the HP Autonomy /Information Management business unit, within HP Software from September 2012 to May 2014. Prior to joining HP, he was President of Microsoft North America from September 2007 to September 2012 and was President and Chief Executive Officer of Callidus Software from August 2005 to September 2007. Prior to that, he spent 10 years at Sun Microsystems, where he had a variety of leadership positions in sales and general management both regionally and globally.

Employees

We had approximately 302,000287,000 employees worldwide as of October 31, 2014.2015.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, are available on our website at http://www.hp.com/investor/home, as soon as reasonably practicable after HP electronically files such reports with, or furnishes those reports to, the Securities and Exchange Commission. HP's Corporate Governance Guidelines, Board of Directors' committee charters (including the charters of the Audit Committee, Finance and Investment Committee, HR and Compensation Committee, Technology Committee, and Nominating, Governance and Social Responsibility Committee) and code of ethics entitled "Standards of Business Conduct" are also available at that same location on our website. Stockholders may request free copies of these documents from:

Hewlett-Packard CompanyHP Inc.

Attention: Investor Relations3000 Hanover Street1501 Page Mill Road,

Palo Alto, CA 94304

http://www.hp.com/investor/informationrequest

Additional Information

Microsoft® and Windows® are U.S.-registered trademarks of Microsoft Corporation. Intel®, Itanium® , Intel®AtomTM, and Intel® Itanium® are trademarks of Intel Corporation in the United States and other countries. AMD is a trademark of Advanced Micro Devices, Inc. ARM® is a registered trademark of ARM Limited. UNIX® is a registered trademark of The Open Group.

The following discussion of risk factors contains forward-looking statements. These risk factors may be important for understanding any statement in this Form 10-K or elsewhere. The following information should be read in conjunction with Part II, Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operation" and the Consolidated Financial Statements and related notes in Part II, Item 8, "Financial Statements and SupplementalSupplementary Data" of this Form 10-K.

Because of the following factors, as well as other variables affecting our results of operations, past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods.

Risks related to our business

If we are unsuccessful at addressing our business challenges, our business and results of operations may be adversely affected and our ability to invest in and grow our business could be limited.

We are in the process of addressing many challenges facing our business. One set of challenges relates to dynamic and accelerating market trends, such as the decline in the PC market, the growth of multi-architecture devices running competing operating systems the market shift towards tablets within mobility, the market shiftand movement to cloud-related infrastructure, software, and services, and the growth in software-as-a-service business models. Anothercontinuous ink supply systems. A second set of challenges relates to changes in the competitive landscape. Our major competitors are expanding their product and service offerings with integrated products and solutions; our business-specific competitors are exerting increased competitive pressure in targeted areas and are going afterentering new markets; our emerging competitors are introducing new technologies and business models; and our alliance partners in some businesses are increasingly becoming our competitors in others. A third set of challenges relates to business model changes and our go-to-market execution. For example, we may fail to develop innovative products and services, maintain the manufacturing quality of our products, manage our distribution network or successfully market new products and services, any of which could adversely affect our business and financial condition.

In addition, we are facing a series of significant macroeconomic challenges, including weakness across many geographic regions, particularly in the United States, Central and Eastern Europe and Russia, and certain countries and businesses in Asia. We may experience delays in the anticipated timing of activities related to our efforts to address these effortschallenges and higher than expected or unanticipated execution costs. In addition, we are vulnerable to increased risks associated with our efforts to address these effortschallenges given our large and diverse portfolio of businesses, the broad range of geographic regions in which we and our customers and partners operate, and the ongoing integration of acquired businesses. If we do not succeed in these efforts, or if these efforts are more costly or time-consuming than expected, our business and results of operations may be adversely affected, which could limit our ability to invest in and grow our business.

In May 2012, we announced a company-wide restructuring plan. The restructuring plan includes both voluntary early retirement programsWe operate in an intensely competitive industry and non-voluntary workforce reductions. Significant risks associated with these actions that may impair our ability to achieve anticipated cost reductions or that may otherwisecompetitive pressures could harm our business include delays in implementation of anticipated workforce reductions in highly regulated locations outside of the United States, particularly in Europe and Asia, decreases in employee morale and the failure to meet operational targets due to the loss of employees. In addition, our ability to achieve the anticipated cost savings and other benefits from these actions within the expected time frame is subject to many estimates and assumptions. These estimates and assumptions are subject to significant economic, competitive and other uncertainties, some of which are beyond our control. If these estimates and assumptions are incorrect, if we experience delays, or if other unforeseen events occur, our business and financial results could be adversely affected.

Competitive pressures could harm our revenue, gross margin and prospects.performance.

We encounter aggressive competition from numerous and varied competitors in all areas of our business, and our competitors may targethave targeted and are expected to continue targeting our key market segments. We compete primarily on the basis of our technology, innovation, performance, price, quality, reliability, brand, reputation, distribution, range of products and services, ease of use of our products, account relationships, customer training, service and support

security, availability of application software, and internet infrastructure offerings.security. If our products, services, support and cost structure do not enable us to compete successfully based on any of those criteria, our results of operations and business prospects could be harmed.

We have a large portfolio of businessesproducts and must allocate our financial, personnel and other resources across all of those businessesour products while competing with companies that have much smaller portfolios or

specialize in one or more of theseour product lines. As a result, we may invest less in certain areas of our businessesbusiness than our competitors do, and theseour competitors may have greater financial, technical and marketing resources available to them thancompared to the resources allocated to our businessesproducts and services that compete against them. Industry consolidation also may affect competition by creating larger, more homogeneous and potentially stronger competitors in the markets in which we compete, and our competitors also may affect our business by entering into exclusive arrangements with existing or potential customers or suppliers.their products.

Companies with whom we have alliances in somecertain areas may be or become our competitors in other areas. In addition, companies with whom we have alliances also may acquire or form alliances with our competitors, which could reduce their business with us. If we are unable to effectively manage these complicated relationships with alliance partners, our cash flowsbusiness and results of operations could be adversely affected.