Use these links to rapidly review the documentTABLE OF CONTENTS 1HMS HOLDINGS CORP. AND SUBSIDIARIES INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ☒ | ||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the fiscal year ended December 31, | ||

Or | ||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the transition period from to | ||

Commission File Number 000-50194

![]()

HMS HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 11-3656261 (I.R.S. Employer Identification No.) | |

5615 High Point Drive, Irving, TX (Address of principal executive offices) | 75038 (Zip Code) |

(Registrant'sRegistrant’s telephone number, including area code)

(214) 453-3000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | ||

|---|---|---|---|

| Common Stock $0.01 par value | The NASDAQ Stock Market LLC (NASDAQ Global Select |

Securities registered pursuant to section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý☒ No o☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ oNo ý☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ ýNo o☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ ýNo o☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant'sregistrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of "large“large accelerated filer," "accelerated filer"” “accelerated filer”, “smaller reporting company” and "smaller reporting company"“emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | ☒ | Accelerated Filer | ☐ | Non-Accelerated Filer (Do not check if a smaller reporting company) | Smaller reporting company |

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ☐ oNo ý☒

The aggregate market value of the registrant'sregistrant’s common stock held by non-affiliates as of June 30, 2014,2016, the last business day of the registrant'sregistrant’s most recently completed second quarter was $1.8$1.5 billion based on the last reported sale price of the registrant's Common Stockregistrant’s common stock on the NASDAQ Global Select Market on that date. Solely for purposes of this disclosure, shares of common stock held by executive officers, directors and persons who hold 10% or more of the outstanding shares of common stock of the registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination is not necessarily a conclusive determination for any other purposes.

There were 88,356,59183,909,845 shares of common stock outstanding as of February 25, 2015.May 31, 2017.

Documents Incorporated by Reference

Unless provided in an amendment to this Annual Report on Form 10-K, the information required by Part III is incorporated by reference to the Registrant's 2015 Proxy Statement, to the extent stated herein. Such proxy statement or amendment will be filed with the SEC within 120 days of the Registrant's fiscal year ended December 31, 2014.

None.

HMS HOLDINGS CORP. AND SUBSIDIARIES

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

Page | |||||||

| Glossary of Terms and Abbreviations

| 1 | ||||||

|

| ||||||

|

| ||||||

| Item 1. | Business | 3 | |||||

| Item 1A. | Risk Factors | 8 | |||||

| Item 1B. | Unresolved Staff Comments | 24 | |||||

| Item 2. | Properties | 24 | |||||

| Item 3. | Legal Proceedings | 24 | |||||

| Item 4. | Mine Safety Disclosures | 24 | |||||

| PART II | |||||||

|

| ||||||

Item | 5. |

| |||||

|

| ||||||

|

| ||||||

| |||||||

| Market for | ||||||

Item 6. | Selected Financial Data | ||||||

Item 7. |

| ||||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||||||

Item 8. | Consolidated Financial Statements and Supplementary Data | ||||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 40 | |||||

| Item 9A. | Controls and Procedures | 41 | |||||

| Item 9B. | Other Information | 42 | |||||

|

| ||||||

Item | 10. |

| |||||

| |||||||

| Directors, Executive Officers and Corporate Governance | ||||||

Item 11. | Executive Compensation | ||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related | ||||||

Item 13. | Certain Relationships and Related Transactions and Director Independence | ||||||

Item 14. | Principal Accounting Fees and Services | 94 | |||||

| |||||||

Item 15. | Exhibits, Financial Statement Schedules | 96 | |||||

| Item 16. | Form 10-K Summary | 96 | |||||

Glossary of Terms and Abbreviations

| ACA |

| |

| ACO | Accountable Care Organizations | |

| ADR | Additional Documentation Request | |

| ALJ | Administrative Law Judges | |

| ASC | Accounting Standards Codification | |

| ASO | Administrative Service Only | |

| CHIP | Children's Health Insurance Program | |

| CMS | Centers for Medicare & Medicaid Services | |

| CMS NHE Projections | Centers for Medicare & Medicaid Services National Health Expenditures | |

| COSO | Committee of Sponsoring Organizations of the Treadway Commission | |

| DMD | Domestic Manufacturing Deduction | |

| DRA | Deficit Reduction Act of 2005 | |

| DSO | Days Sales Outstanding | |

| ERISA | Employment Retirement Income Security Act of 1974 | |

| Exchange Act | Securities Exchange Act of 1934, as amended | |

| FASB | Financial Accounting Standards Board | |

| FFS | Fee For Services | |

| HIPAA | Health Insurance Portability and Accountability Act of 1996 | |

| HITECH | Health Information Technology for Economic and Clinical Health | |

| IRS | U.S Internal Revenue Service | |

| LIBOR | Intercontinental Exchange London Interbank Offered Rate | |

| Medicare Advantage | Medicaid and Medicare managed care | |

| MMIS | Medicaid Management Information Systems | |

| PBM | Pharmacy Benefit Managers | |

| PHI | Protected health information | |

| PI | Payment Integrity | |

| R&D Credits | Research and Development Tax Credits | |

| RAC | Recovery Audit Contractor | |

| RFI | Request for information | |

| RFP | Request for proposals | |

| SEC | U.S. Securities and Exchange Commission | |

| Securities Act | Securities Act of 1933, as amended | |

| Section 199 Deduction | U.S. Production activities deduction | |

| SG&A | Selling, general and administrative expenses | |

| TPL | Third-party liability | |

| U.S. GAAP | United States Generally Accepted Accounting Principles | |

| VHA | Veterans Health Administration | |

| Credit Agreement | The Credit Agreement dated December 16, 2011 among HMS Holdings Corp., the Guarantor Party thereto, the Lenders party thereto and Citibank, N.A. as Administrative Agent, as amended and restated in its entirety by the Amended and Restated Credit Agreement dated as of May 3, 2013 among HMS Holdings Corp., the Guarantor Party thereto, the Lenders party thereto and Citibank, N. A. as Administrative Agent | |

| 2006 Stock Plan | HMS Holdings Corp. Fourth Amended and Restated 2006 Stock Plan | |

| 2011 HDI Plan | HDI Holdings, Inc. Amended 2011 Stock Option and Stock Issuance Plan | |

| 2016 Omnibus Plan | HMS Holdings Corp. 2016 Omnibus Incentive Plan | |

| 401(k) Plan | HMS Holdings Corp. 401(k) Plan |

| 1 |

SpecialCautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K of HMS Holdings Corp. (together with its subsidiaries, “HMS,” the “Company,” “we,” “our” or “us”) contains "forward-looking statements"“forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. From time to time, we also provide forward-looking statements in other materials we release to the public, as well as oral forward-looking statements. Such statements givereflect our current expectations, projections and assumptions about our business, the economy and future events or forecasts of future events; theyconditions. They do not relate strictly to historical or current facts.

We have tried wherever possible, to identify suchforward-looking statements by using words such as "anticipate," "estimate," "expect," "project," "intend," "plan," "believe," "will," "target," "seek," "forecast"“aim,” “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “intend,” “likely,” “may,” “plan,” “project,” “seek,” “target,” “will,” “would,” “could,” “should,” and similar expressions and references to guidance. In particular, theseguidance, although some forward-looking statements may be expressed differently. These statements include, statements relating toamong other things, information concerning our possible future actions, business plans, objectives and prospects, our future operating or financial performance, orsales efforts and results of current and anticipated services, the benefits and synergies to be obtained from completed and future acquisitions, and the future performance of companies we have acquired, sales efforts,sufficiency of our appeals reserves, the future effect of different accounting determinations or remediation activities, our ability to successfully remediate material weaknesses in our internal control over financial reporting, our future expenses, interest rates and financial results, and the outcomeimpact of contingencies, such as financial results.changes to U.S. healthcare legislation or healthcare spending affecting Medicare, Medicaid or other publicly funded or subsidized health programs.

We cannot guarantee that any forward-looking statement will be realized. Forward-looking statements are based on our current expectationsnot guarantees and involve risks, uncertainties and assumptions regarding our business, the economythat are difficult to predict. Actual results may differ materially from past results and other future conditions. Shouldforward-looking statements if known or unknown risks or uncertainties materialize, or shouldif underlying assumptions prove inaccurate, actual results could differ materially from past resultsinaccurate. These risks and those anticipated, estimated or projected. We caution you, therefore, against relying on anyuncertainties include, among other things,

| § | our ability to execute our business plans or growth strategy; | |

| § | our ability to innovate, develop or implement new or enhanced solutions or services; | |

| § | the nature of investment and acquisition opportunities we are pursuing, and the successful execution of such investments and acquisitions; | |

| § | our ability to successfully integrate acquired businesses and realize synergies; | |

| § | variations in our results of operations; | |

| § | our ability to accurately forecast the revenue under our contracts and solutions; | |

| § | our ability to protect our systems from damage, interruption or breach, and to maintain effective information and technology systems and networks; | |

| § | our ability to protect our intellectual property rights, proprietary technology, information processes, and know-how; | |

| § | significant competition for our solutions and services; | |

| § | our failure to maintain a high level of customer retention or the unexpected reduction in scope or termination of key contracts with major customers; | |

| § | customer dissatisfaction, our non-compliance with contractual provisions or regulatory requirements; | |

| § | our failure to meet performance standards triggering significant costs or liabilities under our contracts; | |

| § | our inability to manage our relationships with information and data sources and suppliers; | |

| § | reliance on sub-contractors and other third party providers and parties to perform services; | |

| § | our ability to continue to secure contracts and favorable contract terms through the competitive bidding process and to prevail in protests or challenges to contract awards; | |

| § | pending or threatened litigation; | |

| § | unfavorable outcomes in legal proceedings; | |

| § | our success in attracting qualified employees and members of our management team; | |

| § | our ability to generate sufficient cash to cover our interest and principal payments under our credit facility or to borrow or use credit; | |

| § | unexpected changes in our effective tax rates; | |

| § | unanticipated increases in the number or amount of claims for which we are self-insured; | |

| § | changes in the U.S. healthcare environment or healthcare financing system, including regulatory, budgetary or political actions that affect procurement practices and healthcare spending; | |

| § | our failure to comply with applicable laws and regulations governing individual privacy and information security or to protect such information from theft and misuse; |

| 2 |

| § | negative results of government or customer reviews, audits or investigations; | |

| § | state or federal limitations related to outsourcing or certain government programs or functions; | |

| § | restrictions on bidding or performing certain work due to perceived conflicts of interests; | |

| § | the market price of our common stock and lack of dividend payments; and | |

| § | anti-takeover provisions in our corporate governance documents. |

These and other risks are discussed under the headings “Part I. Item 1. Business,” “Part I. Item 1A, Risk Factors,” “Part II, Item 7. Management’s Discussion and Analysis of these forward-looking statements. They are neither statementsFinancial Condition and Results of historical fact nor guarantees or assurancesOperations,” and “Part II, Item 7A. Quantitative and Qualitative Disclosures about Market Risk” of future performance. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Annual Report on2016 Form 10-K and in particular, the risks discussed under the heading "Risk Factors" in Part I, Item 1A of this Annual Report on Form 10-K and those discussed in other documents we file with the Securities and Exchange Commission.SEC.

Any forward-looking statements made by us in this Annual Report on2016 Form 10-K speak only as of the date on which they are made. Factors or events that could cause actual results to differ may emerge from time to time and it is not possible for us to predict all of them. We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by law. We caution readers not to place undue reliance upon any of these forward-looking statements. You are advised, however, to consult any further disclosures we make on related subjects in our Form10-QForm 10-Q and Form 8-K reports and our other filings with the SEC.

Market and Industry Data

This 2016 Form 10-K contains market, industry and government data and forecasts that have been obtained from publicly available information, various industry publications and other published industry sources. We have not independently verified the information and cannot make any representation as to the Securitiesaccuracy or completeness of such information. None of the reports and Exchange Commission.other materials of third party sources referred to in this 2016 Form 10-K were prepared for use in, or in connection with, this report.

Founded in 1974, HMS Holdings Corp. is a holding company whose principal business is conducted through its operating subsidiaries. Unless the context otherwise indicates, references in this Annual Report to the terms "we," "our" and "us" refer to HMS Holdings Corp., and its subsidiaries and its affiliates.

General Overview

We operateleading provider of cost containment solutions in the U.S. healthcare insurance benefit cost containment marketplace. We use innovative technology, extensive data services and powerful analytics, to deliver coordination of benefits, payment integrity and health management and engagement solutions to help healthcare payers improve performance and outcomes. We provide coordination of benefits services to government and privatecommercial healthcare payers and sponsors to ensure that the responsible party pays healthcare claims. Our payment integrity services ensure that healthcare claims billed are accurate and appropriate.appropriate; and our care management technology helps risk-bearing organizations manage the care delivered to their members. Together these various services help customers recover amounts from liable third parties; prevent future improper payments; reduce fraud, waste and abuse; better manage the care that members receive; and ensure regulatory compliance.

Demand for

HMS began its operations as Health Management Systems, Inc., which became our services arises,wholly owned subsidiary in part, from healthcare funds spentMarch 2003 when we assumed its business in error, where another payer was actually responsible forconnection with the costadoption of the healthcare claim, or a mistake was made in applying complex claim processing rules. According to the Centers for Medicare & Medicaid Services ("CMS") National Health Expenditures ("NHE") 2013-2023 projections and error rates published on paymentaccuracy.gov, the government estimates that improper payments in the Medicaid and Medicare programs totaled $89 billion

in 2014. Our services focus on containing costs by detecting and reducing the errors that result in improper payment, and our revenues are based, in part, on the amounts we recover for our customers.

Our customers are government health agencies, including CMS, the Veterans Health Administration ("VHA") and state Medicaid agencies; commercial health plans, including Medicaid managed care, Medicare Advantage and group and individual health lines of business; government and private employers; child support agencies; and other healthcare payers and sponsors.

We haveholding company structure. Since then HMS has grown both organically and through targeted acquisitions. Initially, we providedacquisitions of businesses that helped expand our product suite, including IntegriGuard, LLC (2009), HealthDataInsights, Inc.(“HDI”) (2011), Essette, Inc. (2016), Eliza Holding Corp. (2017) and others.

We were originally incorporated in the State of New York in October 2002 and reincorporated in the State of Delaware in July 2013. Our principal executive offices are located 5615 High Point Drive, Irving, Texas 75038 and our telephone number is (214) 453-3000.

We operate as one business segment with a single management team that reports to the Chief Executive Officer.

Our Solutions

Our coordination of benefits services to state Medicaid agencies. When Medicaid began to delegate members to managed care organizations, we began providing similar coordination of benefits services to those plans. We launched our payment integrity services in 2007 and have since acquired several businesses to expand our service offerings. In 2009, we began providing cost containment services for Medicare with our acquisition of IntegriGuard, LLC ("IntegriGuard"), which is now doing business as our wholly owned subsidiary HMS Federal, providing fraud, waste and abuse analytical services to the Medicare program, the Veterans Health Administration ("VHA") and the Department of Defense. In 2009 and 2010, we began providing cost containment services to large self-funded employers through our acquisitions of Verify Solutions, Inc. and Chapman Kelly, Inc. In 2011, we expanded our cost benefit services among federal, state and commercial payers with our acquisition of HealthDataInsights, Inc. ("HDI"). HDI provides improper payment identification services for government and commercial health plans, and is the Medicare Recovery Audit Contractor ("RAC") in CMS Region D, covering 17 states and three U.S. territories. In December 2012, we extended our workers' compensation recovery services to commercial health plans through our asset purchase of MedRecovery Management, LLC ("MRM").

As of December 31, 2014, we served CMS, the VHA, 46 state Medicaid programs and the District of Columbia. We also provided services to approximately 220 commercial customers and supported their multiple lines of business, including Medicaid managed care, Medicare Advantage and group and individual health. We also served as a subcontractor for certain business outsourcing and technology firms.

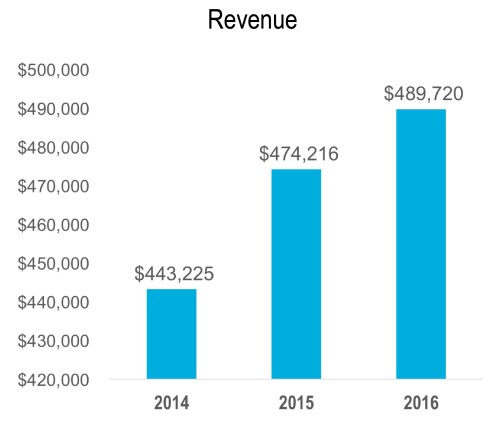

Our 2014 revenue was $443.2 million, a decrease of $48.6 million, or 9.9%, from 2013 revenue of $491.8 million, primarily as a result of the substantial decline in Medicare RAC revenue, which was partially offset by the expansion of services to our existing customers and growth through serving commercial customers.

The Healthcare Environment

The largest government healthcare programs are Medicare, the healthcare program for aged and disabled citizens that is administered individually by CMS and Medicaid, the program that provides medical assistance to eligible low income individuals, which is also regulated by CMS, but administered by each state. For 2015, Medicare and Medicaid are projected to pay approximately 44% of the nation's healthcare expenditures and to have served over 124 million beneficiaries. Many of these beneficiaries are enrolled in managed care plans, which have the responsibility for both patient care and claim adjudication; increasingly, states are expanding their use of managed care for certain populations and geographic areas.

By law, the Medicaid program is intended to be the payer of last resort; that is, all other available third party resources must meet their legal obligation to pay claims before the Medicaid program pays for the care of an individual enrolled in Medicaid. Under Title XIX of the Social Security Act, states are required to take all reasonable measures to ascertain the legal liability of "third parties" for healthcare services provided to Medicaid recipients. Since 1985, we have provided state Medicaid agencies with services to identify third parties with primary liability for Medicaid claims, and since 2005, we have provided similar services to Medicaid managed care plans.

Signed into law in February 2006, the Deficit Reduction Act of 2005 (the "DRA") established a Medicaid Integrity Program to increase the government's capacity to prevent, detect and address fraud,

waste and abuse in the Medicaid program. The DRA also added new entities, such as self-insured plans, Pharmacy Benefit Managers ("PBMs") and other "legally responsible" parties to the list of entities subject to the third party liability provisions of the Medicaid statute. These measures, at both the federal and state level, have strengthened our ability to identify and recover erroneous payments made by our customers.

The Patient Protection and Affordable Care Act (the "ACA") was signed into law on March 23, 2010, and amended on March 30, 2010. Upheld by the U.S. Supreme Court in June 2012, this legislation touches almost every sector of the healthcare system, and we believe it provides us with a range of growth opportunities across a number of services. We are focused on four critical areas related to this legislation:

Medicaid Expansion: States that expand their Medicaid programs in accordance with the ACA will receive federal funding for the total cost of the expansion for a period of three years, and reduced funding thereafter. By the end of 2014, more than half of the states opted to expand their Medicaid programs as provided under the ACA. According to CMS projections for national health expenditures for 2013-2023 ("CMS NHE Projections"), the number of individuals enrolled in Medicaid and the Children's Health Insurance Program ("CHIP") is expected to increase from 76 million in 2015 to 86 million in 2023, with expenditures over the same period expected to increase from $556 billion to $942 billion. As a result, we anticipate a considerable increase in the need for our cost containment services by states and the managed care organizations they use. We believe that our strong history of successful contracting with Medicaid agencies and Medicaid managed care organizations will enable us to provide value-added services to help control the costs for this expanded population.

Eligibility Verification: The ACA calls for increased efficiency, automation and administrative simplification in addressing program eligibility determination, both as a component of the health insurance exchange marketplaces and as a pathway to the more effective management of existing entitlement programs. Driven both by insurance marketplace requirements and by the pressures to achieve program efficiency and simplification, CMS and states are increasingly moving to implement solutions involving automation of the verification of eligibility, bringing in increased external data and analytics relating to supporting eligibility decision-making.

Payment Integrity: The ACA contains a number of provisions for combating fraud, waste and abuse throughout the healthcare system, including in Medicaid and Medicare. These initiatives include: (i) requiring state Medicaid agencies to contract with state Medicaid RACs and deploy programs modeled on CMS' existing Medicare RAC Program, (ii) expanding CMS' Medicare RAC Program to include Medicare Part C and D, (iii) establishing a national healthcare fraud, waste and abuse data collection program and (iv) increasing scrutiny of providers and suppliers who want to participate in Medicare, Medicaid and other federally-funded programs. In addition, the ACA allows for significant increases in funding for these and other fraud, waste and abuse efforts. We continue to expand our current partnerships with CMS, states and health plans to provide innovative ideas for increasing our support of their new payment integrity initiatives.

Employer-Sponsored Health Coverage: The ACA largely preserves and builds upon the existing employer-sponsored health coverage model. Though not all employers will be required to provide healthcare coverage, large employers (i.e. those with 50 or more full time equivalents) will be penalized starting in 2015 if (a) they do not offer coverage (or if they offer coverage that does not meet certain requirements) and (b) one or more of their full time employees receives a federal tax credit or cost sharing subsidy through a health insurance exchange. Employers will also be prohibited from imposing waiting

periods for enrollment of more than 90 days. We believe that these requirements, coupled with the Medicaid expansion and implementation of health insurance exchanges, will result in more overlapping coverage situations and an opportunity for our employer customers and Medicaid to collaborate. We expect that we will be able to offer a range of audit services to employers of all sizes, which will be valuable as these employers extend coverage to their employees.

Principal Products and Services

Our coordination of benefits offering to customers consists of services that draw principally upon proprietary information management and data mining techniques designed to assureensure that the rightcorrect party pays a healthcare claim. Our payment integrity offering to customers also consists of a variety of services are designed to assureensure that the billing itself ishealthcare billings and/or payments are accurate and appropriate. As a result of ourthese services, customers received billions of dollars in cash recoveries in 2014,2016, and saved billions more through the prevention of erroneous payments.

| 3 |

Our services are applicable to the federal, state and commercial health plans and prevent and address errors across the payment continuum, from an individual'sindividual’s enrollment in a program before any medical service is rendered, to pre-payment review of a claim by a payer, through recovery audit where discovery of an improper payment is made.made via audit. Our services also address thea wide spectrum of payment errors, from eligibility and coordination of benefits errors, to the identification and investigation of potential fraud, and extend to most claim types. Our services also assist customers in managing quality, risk, cost and compliance across all lines of business.

In general, our range of services includes the following:

| § | Coordination of benefits services |

We provide cost avoidance services, in which we provideinclude providing validated insurance coverage information that is used by government-sponsored payers to coordinate benefits properly for incomingfuture claims. With validated insurance information, Medicaid payers can avoid unnecessary costs by ensuring that it paysthey pay only after all other benefits available have been exhausted, thereby complying with federal regulations that require Medicaid to be the payer of last resort. Nevertheless, due to a variety of factors, some Medicaid claims are paid even when there is a known responsible third party. Our government-sponsored program customers rely on us to identify dollarsthose claims that were paid in error and recover these payments from the liable third party. Further, we also provide services to recover these amounts from the liable third party. Forassist customers in identifying other third-party insurance and recovering medical expenses where a member is involved in a casualty or tort incident. Lastly, for Medicaid agencies exclusively, we also provide estate recovery services to identify and recover Medicaid expenditures from the estates of deceased Medicaid members in accordance with state policies. Further, we provideFor the years ended December 31, 2016, 2015 and 2014, our coordination of benefits services to assist customers in identifying other third-party

Tablerepresented 72.3%, 71.2% and 70.5% of Contentsour total revenue, respectively.

insurance and recovering medical expenses where a member is involved in a casualty or tort incident.

| § | Payment integrity services |

Our payment integrity services are applicable to all markets that HMS serves, including the federal and state governments, commercial health plans and other at-risk entities. Our solutions are designed to verify that medical services are utilized, billed and paid appropriately. Our services combine data analytics, clinical expertise and proprietary technology to identify improper payments on both a pre-payment and post-payment basis; identify and recover overpayments/underpayments; detect and prevent fraud, waste and abuse; and identify process improvements.

Customers

Our customers are government health agencies, including CMS, the VHA and state Medicaid agencies; commercial health plans, including Medicaid managed care, Medicare Advantage and group and individual health lines of business; government and private employers; child support agencies; and other healthcare payers and sponsors.

Our largest customer in 2014 accounted for 9.5%, 5.6% and 6.4% of our total revenue for For the years ended December 31, 2016, 2015 and 2014, 2013our payment integrity services represented 24.3%, 24.5% and 2012, respectively. We provide services to this customer pursuant to a contract that was originally awarded in January 2008 and extends through April 2015. Our services were expanded in 2011 to designate us as the Medicaid RAC for this customer through September 2016. We are currently preparing for the reprocurement of this contract. Our failure to reprocure this contract would have a material adverse effect on our financial condition, results of operations and cash flows.

Our second largest customer in 2014 accounted for 5.3%, 4.6% and 5.2%24.5% of our total revenue, forrespectively.

| 4 |

| § | Care management and member analytics technologies |

We offer a web-based care management platform which helps risk-bearing healthcare organizations identify, engage, and manage at-risk patient populations to improve outcomes while managing costs.

Customers

For each of the years ended December 31, 2016, 2015 and 2014 2013 and 2012, respectively. We provide services to thisno one individual Company customer pursuant to a contract that expires in January 2016. Our failure to reprocure this contract would have a material adverse effect on our financial condition, results of operations and cash flows.

Our third largest customer in 2014 accounted for 5.0%, 22.3% and 18.2%more than 10% of our total revenue for the years ended December 31, 2014, 2013 and 2012, respectively. It has been our customer since 2006. Our largest contract with this customer is through HDI, under which HDI has served as the Medicare RAC for Region D since October 2008 and which, after multiple contract modifications, now provides for a term that expires December 31, 2015. Given that HDI's Medicare RAC contract with this customer is onerevenue.

The composition of our largest contracts and represents a significant potential business opportunity for us, our business, financial condition, results of operations and cash flows would be adversely affected if HDI was not awarded a region, if HDI was awarded a region but on substantially different terms from HDI's current contract or if contract awards continue to be delayed. In addition, if HDI is awarded a new Medicare RAC contract, the terms of that contract may change or delay the timing of HDI's revenue recognition from timing under the current contract.

The list of our ten10 largest customers changes periodically. For the years ended December 31, 2016, 2015 and 2014, 2013 and 2012, our ten10 largest customers represented 40.1%40.6%, 47.2%44.0% and 46.9%40.1% of our total revenue, respectively. OurThe current terms of our agreements with these customers have expiration dates ranging between 20152017 and 2018.

We provide products and services under contracts (or sub-contracts) that contain various fee structures, including contingency fee and fixed fee arrangements. Many of our contracts have terms of three to five years, including optional renewal terms. In many instances, we provide our services pursuant to agreements that are subject to periodic reprocurements.2020. Several of our contracts, including those with some of our largest customers, may be terminated for convenience. The early termination of a contract with one of our significant customers may have an adverse effect on our financial condition, results of operations and cash flows.

We provide products and services under contracts (or sub-contracts) that contain various revenue structures, including contingent revenue and fixed-fee arrangements. Most of our contracts have terms ranging from three to five years, including renewal terms at the option of the customer. In many instances, we provide our services pursuant to agreements that are subject to periodic reprocurements. Because we provide our services pursuant to agreements that are open to competition from various businesses in the U.S. healthcare

insurance benefit cost containment marketplace, we cannot provide assurance that our contracts, including those with our largest customers, will not be terminated for convenience, awarded to other parties, or renewed. Additionally, we cannot provide assurance that any of theseour contracts, will be renewed, and, if renewed, thatwill have the same fee structures willor otherwise be equal to those currently in effect.

Industry Trends/Opportunitieson satisfactory terms.

Containing

Industry Trends and Opportunities

U.S. healthcare expenditures presentscontinue to escalate and consume a large proportion of our GDP, presenting challenges for payers who wish to contain and reduce costs while also promoting quality healthcare outcomes. These aims are the same across all at-risk entities, including commercial health plans and government duehealthcare programs, such as Medicaid and Medicare.

Within the commercial market, health plans sell policies directly to individuals (on the open market or via health insurance exchanges), contract with employers to underwrite their employees’ care, or contract with self-insured employers to oversee benefit administration to their employees. This market also includes a growing number of risk bearing provider-sponsored plans that operate and varietymarket health plan benefits. According to CMS NHE projections, private health insurance covered 195 million individuals in 2016 at a cost of $1.09 trillion.

Several commercial health plans also offer government-sponsored lines of business, including partnering with Medicare, Medicaid and CHIP to oversee care delivery for beneficiaries enrolled in those programs. Government managed care grew out of pressures to contain the growth of state and federal program spending and to address general concerns about healthcare access. Commercial health plan-related partnerships with government programs include the following:

| § | Within the Medicaid program, 38 states and the District of Columbia presently contract with managed care organizations to provide care to some or all of their Medicaid beneficiaries. In addition, many states have expanded the use of managed care organizations to new regions or to serve beneficiaries with more complex conditions. Of the 32 states and the District of Columbia that opted to expand Medicaid eligibility levels pursuant to the ACA, all except 5 use Medicaid managed care organizations. The majority of new lives that have entered the Medicaid program as a result of the ACA are enrolled in managed care plans. It is unclear at this time how, if at all, efforts in Congress to “repeal and replace” the ACA could affect any of the state expansions or future growth of Medicaid lives and expenditures. |

| § | Similarly, managed care health plans also continue to assume risk for Medicare lives, with the Kaiser Family Foundation estimating that in 2016, nearly one-third of all Medicare recipients were enrolled in a Medicare Advantage plan. |

| 5 |

HMS also continues to serve government-sponsored agencies’ legacy fee-for-service programs at the state and federal level,level. These plans are generally reliant on and susceptible to the government appropriations process that determines their budget and governs the rise in the cost of care and number of beneficiaries. The ACA adds increased pressure to states to cover more individuals, making cost containment a high priority.beneficiaries they serve.

Government healthcare programs continue to grow. CMS has projected that Medicaid, CHIP and Medicare expenditures will increase to nearly $2.1 trillion by 2023.

According to the CMS NHE Projections,projections, Medicare programs in 20142016 covered approximately 5356 million people and spentat a cost of approximately $616 billion. CMS projected that at the end of 2014$681 billion and Medicaid/CHIP programs covered approximately 7277 million people, and spentcosting approximately $521$593 billion. Altogether, it is projected that the government programs we serve covered approximately 125130 million people and spent nearly $1.1at a total cost of approximately $1.3 trillion in 2014. We believe that enrollment in these programs will continue to increase as a result of2016. Based on the ACA. CMS projects that in 2017, Medicare will cover approximately 58 million people and will spend approximately $714 billion, and, Medicaid/CHIP is expected to cover approximately 82 million people and will spend approximately $644 billion.

According to CMS NHE Projections, for 2013-2023, Medicaid enrollmentMedicare spending is projected to grow by 5.8% in 20152017 over 2016, and 6.7%CMS projects Medicaid enrollment will grow by 1.7% in 2017 over 2016. Total Medicaid spending is projected to increase at a rate of 6.7%4.8% in 20152017 over 2016.

As commercial and at a rate of 8.6% in 2016. In addition, Medicare spending is projectedgovernment health plans continue to grow from 2.7% in 2015 to up to 7.8% in 2018. There are a number of factors that could impact these projections, including medical utilization by the new enrollees under the ACA and any legislative action taken to reduce spending.

In response to pressuresfocus on strategies to contain the growthcosts across their different lines of statebusiness, we will continue to focus on serving them and federal Medicaid spending and to concerns about access to healthcare for low-income individuals, the use of managed care arrangements in Medicaid continues to grow. As of year-end 2014, 38 states and the District of Columbia contracted with managed care organizations to provide care to some or all ofmeeting their Medicaid beneficiaries. In addition, many states have expanded the use of managed care organizations to new regions or to serve beneficiaries with more complex conditions. Of the 27 states and the District of Columbia that opted to expand Medicaid eligibility levels by the end of 2014 pursuant to the ACA, all except for three did not use Medicaid managed care organizations. The majority of new lives that have entered the Medicaid program as a result of the ACA were enrolled in managed care organizations.

evolving needs. Regardless of the program, coordinating benefits among a growing number of healthcare payers and ensuring that claims are paid appropriately represents both an enormous challenge for our customers and an ongoing opportunity for us.

Competition

Regulatory Environment

The market for cost containment solutions is large and growing, driven by increasing healthcare costs and payment complexities. For 2017, Medicare and Medicaid are projected to pay approximately 45.9% of the nation’s healthcare expenditures and serve over 130 million beneficiaries. Many of these beneficiaries are enrolled in managed care plans, which have the responsibility for both patient care and claim adjudications. Since 1985, we have provided state Medicaid agencies with services to identify third parties with primary liability for Medicaid claims, and since 2005, we have provided similar services to Medicaid managed care plans.

In 2006, Congress enacted the DRA and created the Medicaid Integrity Program under the Social Security Act to increase the government’s capacity to prevent, detect and address fraud, waste and abuse in the Medicaid program. Later that year, Congress passed the Tax Relief and Health Care Act of 2006, which established the Medicare RAC program. HDI was awarded one of the first contracts under the program. In October 2016, CMS made a new round of awards and we again were awarded a region.

These measures, at both the federal and state level, have strengthened our ability to identify and recover erroneous payments on behalf of our customers.

The ACA was signed into law in 2010. It included many provisions impacting healthcare delivery and payment programs, including employer-sponsored health coverage, expansion of the Medicaid program, health insurance exchanges with premium subsidies, and payment integrity efforts. Following the 2016 Presidential and Congressional elections, some or all of the ACA provisions may be revised or repealed, although the scope and timing of such Congressional efforts are yet to be defined. Options that have been discussed include issuing block grants or establishing per capita caps for state Medicaid populations, and looking at program design alternatives for future enrollment criteria. We will monitor ACA-related changes as they develop and assess their potential impact, as well as any opportunities they may present for our customers and for us.

Competition

The U.S. healthcare insurance benefit cost containment marketplace is a dynamic industry with a range of businesses currently able to offer all or a subset of cost containment services, both directly or indirectly (through subcontracting)sub-contracting), to some or all of the various healthcare payers. In addition, with improvements in technology and the growth in healthcare spending, new businesses are incentivized to enter into this marketplace. SomeMany healthcare payers also have the ability to perform some or all of these cost containment services themselves and some, in fact, choose to exercise that option. Competition is therefore robust as customers have many alternatives available to them in their effort to contain healthcare costs.

| 6 |

We compete based on a variety of Contentsfactors, including our ability to perform a wide range of coordination of benefits and payment integrity related functions; proven results to maximize recoveries and cost avoidance; our in-depth government healthcare program experience; clinical staff expertise; extensive insurance eligibility database; proprietary systems and processes; existing relationships with various customer and other industry shareholders; and our ability to provide customers with actionable intelligence to improve outcomes and patient engagement.

Within our core coordination of benefits services, we compete primarily with large business outsourcing and technology firms, claims processors (including PBMs),and PBMs, clearinghouses, healthcare consulting firms, smaller regional vendors and other third party liabilityTPL service providers; these companies include Optum, Inc., Public Consulting Group, Inc., Emdeon Inc., EDS (affiliated with Hewlett Packard Company) and ACS (affiliated with Xerox Corporation).providers. In addition, as noted, we frequently work with customers who may elect to perform some or all of their recovery and cost avoidance functions in-house. Against these competitors, we try to compete favorably on the basis of a variety of factors, including our ability to perform a wide variety of coordination of benefits-related functions; maximize recoveries and cost avoidance; apply our in-depth government healthcare program experience, staff expertise, extensive insurance eligibility database, proprietary systems and processes; leverage our existing relationships; and sustain operations under contingency fee structures.

The competitive environment for payment integrity services includes some of the same companies that provide coordination of benefits services, as well asservices. Within the care management and risk analytics sector, we compete primarily with vendors who provide these and other Medicare RACs (CGI Federal, Inc., Connolly and Performant Financial Corp.); other claim audit vendors (including Cognosante, Myers & Stauffer LC and PRGX Global, Inc.); fraud, waste and abuse claim edit and predictive analysis companies (such as Emdeon, Inc., Verisk Health, Inc. and LexisNexis Risk Solutions); and numerous regional utilizationpopulation health management companies.technology services. Companies with whom we compete across our product offerings include:

| § | ChangeHealthcare | § | Experian Health | § | Verscend Technologies | |||

| § | Cotiviti | § | IBM/Truven | § | CaseNet | |||

| § | HP | § | LexisNexis | § | MedHok | |||

| § | Optum, Inc. | § | Performant Financial Corp. | § | Trizetto | |||

| § | Xerox | § | SCIO Health Analytics | § | ZeOmega |

Business Strategy

Over

We believe that the coursesteadily increasing enrollment and rising expenditures for Medicare and Medicaid, with most new enrollees entering managed care plans; an aging U.S. population with an increasing concentration of 2015,individuals with high cost chronic conditions; and the overall complexity of the healthcare claims payment system in the U.S. all combine to create substantial growth opportunities for the suite of cost containment solutions which we offer. We also believe that these factors similarly present growth opportunities for our care management solutions. We expect to grow our business throughover the course of 2017 and beyond, both organically and inorganically, by leveraging existing key assets (e.g., our data, analytics and in-house expertise, and distribution channel) and pursuing a number of strategic objectives or initiatives, that may include:

Employeesincluding:

| § | Expanding the scope of our relationship with existing customers– by selling additional products and services. |

| § | Adding new customers– by marketing to commercial health plans, including Medicaid managed care and Medicare Advantage plans, at-risk group and individual health lines of business and ASO; government healthcare payers, including Medicaid agencies, state employee health benefit plans and CHIP; at-risk provider organizations and ACOs; and commercial employers. |

| § | Introducing new “homegrown” products and services– through internal development initiatives designed to enhance or expand our existing suite of cost containment products. |

| § | Utilizing big data – to create a more nimble operating environment and to identify new revenue opportunities within our current service delivery models. |

| § | Promoting automation and innovation to improve the efficiency and effectiveness of our services – by continuing to implement new technology and process improvements designed to increase recovery yields and increase customer satisfaction. |

| § | Building out our new health management and member engagement technology platform – by establishing a broad foundation of technology and service solutions to help customers better manage quality, cost and compliance across all lines of business. Our first step in this strategy was the acquisition of Essette Inc., a care management platform, in September 2016. More recently, we acquired Eliza Holding Corp., which provides comprehensive and personalized outreach and health engagement solutions, in April 2017. |

| 7 |

| § | Continuing opportunistic growth via acquisition– by selectively seeking assets to complement our core cost-containment expertise; build care management and care coordination adjacencies to complement the Essette and Eliza acquisitions; and expand our data analytics capabilities. Our focus is on acquisitions that have long-term growth potential; target high-growth areas; are accretive to earnings; and fill a strategic need in our business portfolio as we seek to provide increasingly comprehensive solutions to our customers. |

Employees

As of December 31, 2014,2016, we had 2,2962,315 employees, of which 2,2282,287 were full time.full-time. Of our total employees, 230253 support selling, generalSG&A activities.

Intellectual Property

Our ability to develop and administrative activities.

Financial Information About Industry Segments

Sincemaintain the beginningproprietary aspects of our technology and operate without infringing the first quarterproprietary rights of 2007,others are important to our business and competitive position. We establish and protect our proprietary technology and intellectual property through a combination of patents, patent applications, trademarks, copyrights, domain names, trade secrets, including know-how, confidentiality and invention assignment agreements, security measures, non-disclosure agreements with third parties, and other contractual rights. As a result of acquiring Eliza Holding Corp. on April 17, 2017, we have been managednow own a patent portfolio comprised of approximately 55 domestic and operated as one business, with a single management team that reports to the chief executive officer.international patents and patent applications. We do not operate separate lines

Table of Contentsbelieve that any one individual technology is essential to our business.

of business with respect

Available Information

Additional information about HMS is available on our website at www.hms.com. The content on our website, or any website referred to anyin this Annual Report on Form 10-K, is not incorporated by reference into this Annual Report, unless expressly noted.

Copies of our product lines. Accordingly, we do not prepare discrete financial information with respect to separate product lines or by location and do not have separately reportable segments as defined by the guidance provided by the Financial Accounting Standards Board (the "FASB").

Available Information

We maintain a website (www.hms.com) that contains various information about our company and our services. Through our website, we make available, free of charge, access to all reports filed with the U.S. Securities and Exchange Commission (the "SEC"), including ourrecent Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and our Proxy Statements, as well as amendments to these reports or statements, as filed with or furnished toare available free of charge on our website through the SEC pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, (the "Exchange Act")Investor Relations page, as soon as reasonably practicalpracticable after we electronically file such materialthem with, or furnish itthem to, the SEC. In addition,These materials, as well as similar materials for SEC registrants, may be obtained directly from the SEC maintains athrough their website (www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.at www.sec.gov. You may also read and copy this information, for a copying fee,any materials we file with the SEC at the SEC'sSEC’s Public Reference Room at 100 F Street NE, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 to obtain informationInformation on the operation of the Public Reference Room. The content on any website referred to in this Form 10-K is not incorporatedRoom may be obtained by reference into this Form 10-K unless expressly noted.

We also makecalling the following documents available on our website under the Investor Relations/Corporate Governance tabs: the Audit Committee Charter, the Compensation Committee Charter, the Nominating & Governance Committee Charter, the Compliance Committee Charter, our Code of Conduct and our Corporate Governance Guidelines. You may also obtain a copy of any of the foregoing documents, free of charge, if you submit a written request to Attention: Investor Relations, 5615 High Point Drive, Irving, TX 75038.SEC at 1-800-SEC-0330.

Corporate Information

We are incorporated in the State of Delaware. We were originally incorporated on October 2, 2002 in the State of New York. On March 3, 2003, we adopted a holding company structure and assumed the business of our predecessor, Health Management Systems, Inc. In connection with the adoption of this structure, Health Management Systems, Inc., which began doing business in 1974, became our wholly owned subsidiary.

We provide

Our business is subject to significant risks, including the following cautionary discussion of risks and uncertainties and possibly inaccurate assumptions relevant to our business that, individually or in the aggregate, may cause our actual results to differ materially from expected and historical results. We note these factors for investors as permitted by the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995.described below. You should carefully consider these factors, but understand that it is not possible to predict or identify all such factors. Consequently, you should not considerrisks, as well as the following to be a complete discussion of all potential risks or uncertainties involved with investing in our stock. These risk factors should be read in connection with other information set forth in this Annual Report,2016 Form 10-K, including our Consolidated Financial Statements and the related Notes.

Table The occurrence of Contents

Risks Relating to Our Business

Changes in the United States healthcare environment, or in laws relating to healthcare programs and policies, and steps we take in anticipationany of such changes, particularly as they relate to the ACA and the Medicare and Medicaid programs,these risks could have a material adverse effect onadversely affect our business, financial condition, results of operations, and cash flows.

The healthcare industryflows in the United States is subject to changing political, economic and regulatory influences that may affect the procurement practices and operations of federal, state and private healthcare organizations and agencies. In general, the ACA seeks to decrease over time the number of uninsured legal U.S. residents. Because of the ACA's strong emphasis on program integrity and cost containment, as well as provisions expanding the Medicaid-eligible population, we regard this legislation, on the whole, as creating potential new opportunities for the expansion of our business and service offerings. Until the ACA has been fully implemented, however, it will be difficult to predict its full impact and influence on future changes to Medicare policy, due not only to its complexity, but also to the wide range of other factors contributing to uncertainty of the healthcare landscape. These factors include the unpredictability of responses by states, providers, businesses and other entities to the various choices available to them under the law; the possibility that implementation of certain provisions of the legislation could still be blocked by court challenges, repealed by Congressional efforts or as a result of Supreme Court decisions or otherwise modified at the state level; and the increase in lobbying efforts from established provider organizations for further adverse changes to the Medicare RAC Program.

In addition, under the ACA, as states seek to contain costs with an expanding Medicaid population, we expect to continue to see an increase in the migration of Medicaid lives from fee-for-service to managed care plans. While we provide services to both types of Medicaid plans, we have historically had more success in providing services to states utilizing fee-for-service plans. The transition of Medicaid lives from fee-for-service to managed care requires that we commit more resources to attaining larger amounts of business from managed care plans.

We have made and will continue to make investments in personnel, infrastructure and product development, as well as in the overall expansion of the services that we offer in order to support existing and new customers as they implement the requirements of the ACA. However, future changes to the ACA and to the Medicare and Medicaid programs may also lower reimbursement rates, establish new payment models, increase or decrease government involvement in healthcare, decrease the Medicare RAC Program and/or otherwise change the operating environment for our customers. Our business, financial condition, results of operations and cash flows could be adversely affected if efforts to waive, modify or otherwise change the ACA, in whole or in part, are successful, if we are unable to adapt our products and services to meet changing requirements or expand service delivery into new areas, or the demand for our services is reduced as a result of healthcare organizations' reactions to changed circumstances and financial pressures.

Healthcare organizations may react to such changed circumstances and financial pressures, including those surrounding the implementation of the ACA, by taking actions such as curtailing or deferring their retention of service providers like us, which could reduce the demand for our services and, in turn, could have a material adverse effect on our business, financial condition, results of operations and cash flows.way.

Healthcare spending fluctuations, simplification of the healthcare payment process or other aspects of the healthcare financing system, budgetary pressures and/or programmatic changes diminishing the scope of program benefits, or limiting payment integrity initiatives, could reduce the need for and the price of our services, which would have a material adverse effect on our business, financial condition, results of operations and cash flows.

Risks Relating to Our projections and expectations are premised upon consistent growth rates in spending in the Medicare and Medicaid programs, the current healthcare financing system and the need for our services within that existing framework. It is expected that enrollment in government healthcare programs will

Table of ContentsCompany

continue to grow, particularly under the ACA. There are a number of factors that could impact our projections, including medical utilization by the new enrollees under the ACA and any legislative action taken to reduce spending. Compounding this are budgetary pressures that may drive changes at the state level, including shifting lives from traditional fee-for-service plans into Medicaid managed care plans to achieve cost savings.

Our experience in offering services that improve the ability of our customers to recover revenue that would otherwise be lost, often as a result of procedural inefficiencies and complexities, have contributed to the success of our service offerings. Although the complexities of the healthcare benefit and payment system continue to grow (due to factors such as the expansion of pay-for-performance programs), the need for our services, the price customers are willing to pay for them and/or the scope and profitability of our contracts could be negatively affected by: lower than projected growth in the Medicare and Medicaid programs; a simplification of the healthcare benefit and payment system through legislative or regulatory changes at the federal or state level (for example, legislative changes impacting the scope of mandatory audits, limiting or reducing the amount of reviewable claims and/or the look-back period for review in areas where we conduct audits); unanticipated reductions in the scope of program benefits (such as, for example, state decisions to eliminate coverage of optional Medicaid services or shifting lives into managed care plans); and/or limits placed on ongoing program integrity initiatives (for example, in February 2014, CMS announced a "pause" in operations of the Medicare RAC Program). Modifications in provider billing behavior and habits, often in response to the success of our services, could also reduce the profitability of our contracts and reduce the need for our services. Any of these factors could cause our financial projections to differ from our actual results, and could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our operating results are subject to significant fluctuations due to factors including variability in the timing of when we recognize contingency fee revenue and the challenges associated with forecasting revenue for new products and services. As a result, you will not be able to rely on our operating results in any particular period as an indication of our future performance.

Our operating results may fail to match our past or projected performance. We have experienced significant variations in our revenue between reporting periods due to the timing of periodic revenue recovery projects, the timing and delays in third party payers' claim adjudication and ultimate payment to our customers where our fees are contingent upon such collections and delays in receiving payment for our services. Our revenue and operating results have also been impacted from period to period as a result of a number of factors, including:

In addition, as we introduce new products and services, we may not be able to accurately estimate the costs and timing for implementing and completing contracts, making it difficult to reliably forecast revenue under those contracts. We cannot predict the extent to which future revenue variations could occur due to these or other factors. Consequently, our results of operations are subject to significant fluctuation and our results of operations for any particular quarter or fiscal year may not be indicative of results of operations for future periods.

Our ability to execute onexpand our business plans will be adversely affected if we fail to properly manageimplement our growth.growth strategy.

In recent years, our

The size and the scope of our business operations have expanded rapidly,over the past several years, and we expect that we willcurrently intend to continue to grow and expand into new areas within the government and commercial healthcare space; however, such growth and expansion carries costs and risks that, if not properly managed, could adversely affect our business. To effectively manageOur future growth will depend, among other things, on our ability to successfully execute our business plans we must continueand continued efforts to improve our operations, all while remaining competitive. We must also be flexible and responsive to our customers'customers’ needs and to changes in the political, economic and regulatory environment in which we operate. The greater size and complexity of our expanding business puts additional strain on our administrative, operational and financial resources and makes the determination ofcan make optimal resource allocation more difficult.difficult to determine. We may not be able to maintain or accelerate our growth. A failure to anticipate or properly address the demands and challenges that our growth strategy and potential diversification may have on our resources and existing infrastructure may result in unanticipated costs and inefficiencies and could negatively impact our ability to execute on our business plans and growth goals, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

| 8 |

Our business could be adversely affected ifIf we fail to maintain a high level of customer retention, lose a major customerinnovate and develop new or fail to reprocure a contract,enhanced solutions and services, or if these solutions and services are not adopted by our customers, elect to reduce the scope of our contracts or terminate them before their scheduled expiration dates.

We generateit could have a significant portion of our revenue from a limited number of large customers at the federal and state level. For the years ended December 31, 2014, 2013 and 2012, our three largest customers accounted for 19.8%, 32.5% and 29.8%, respectively, of our revenue from continuing operations.

One of our largest customers in 2014 was CMS, primarily related to our Medicare RAC contract through our wholly owned subsidiary HDI, which after a series of contract modifications, now expiresmaterial adverse effect on December 31, 2015. In February 2013, CMS began the reprocurement process for the Medicare RAC Program contracts. After a protest was filed on the initial Request for Quote ("RFQ"), CMS took corrective action and, between December 2013 and January 2014, issued five new RFQs for the Medicare RAC Program contracts. HDI and one of HDI's prospective competitors protested certain terms of the new RFQs, and these protests were denied by the Government Accountability Office ("GAO") in April 2014. On April 28, 2014, HDI's prospective competitor filed a lawsuit at the U.S. Court of Federal Claims challenging the terms of the solicitations for CMS Regions 1, 2, and 4 and seeking an injunction against CMS. On August 21, 2014, the U.S. Court of Federal Claims entered judgment in favor of the GAO and HDI's prospective competitor appealed to the U.S. Court of Appeals for the Federal Circuit on August 26, 2014. On September 2, 2014, the U.S. Court of Federal Claims granted a stay that prohibited CMS from awarding contracts for Regions 1, 2, and 4 pending the outcome of the appeal.

Under the existing Medicare RAC contracts, on February 18, 2014, CMS announced its decision to pause the operations of the current Medicare RACs establishing June 1, 2014 as the last day that RAC contractors could transmit improper payment files for processing. On August 4, 2014, CMS announced that due to the continued delay in awarding new Recovery Auditor contracts, it was initiating contract modifications to allow the Medicare RACs to restart certain reviews through December 31, 2014. CMS stated that most reviews will be done on an automated basis, but a limited number will be complex reviews

of topics selected by CMS. On January 12, 2015, we entered into a new modification that extended our auditing services to CMS through December 31, 2015 and requires us to assist CMS with the appeals process through April 30, 2017.

Given that HDI's Medicare RAC contract with CMS is one of our largest contracts and represents a significant potential business opportunity for us, if HDI is not awarded a region, or is awarded a region but on substantially different terms from HDI's current contract, or if the contract awards continue to be delayed, or if CMS imposes or implements other changes to the Medicare RAC Program that materially reduce our revenue or profitability associated with such program, then our business, financial condition, results of operations and cash flows would be materially adversely affected.flows.

In August 2013, CMS issued CMS Rule 1599-FHospital Inpatient Admission Order and Certification and Two Midnight Benchmark for Inpatient Hospital Admissions for the Fiscal Year 2014 Inpatient Prospective Payment System ("IPPS")/Long-Term Care Hospital ("LTCH"). Under this final rule, CMS redefined the requirements for an inpatient stay with a new formal time-based standard. The new rule, termed the "Two Midnight Rule," states that surgical procedures, diagnostic tests and other treatments (in addition

Part of our growth strategy depends on our ability to services designated as inpatient-only), are generally appropriate for inpatient hospital admission and payment under Medicare Part A when a physician (i) expects the beneficiary to require a stay that crosses at least two midnights, and (ii) admits the beneficiaryrespond to the hospital based uponevolving healthcare landscape with new and enhanced solutions and services that expectation. As part of theour existing and potential customers are willing to adopt. The development, marketing and implementation of these solutions and services may require that we make substantial financial and resource investments. We face risks that our new or modified solutions and services may not be responsive to customer preferences or industry changes, and that the new rule, effective October 2013, CMS suspendedsolution and service development initiatives that we prioritize may not yield the review by Medicare RACs of inpatient hospital claims paid between October 1, 2013 and September 30, 2014 for a determination of whether the inpatient hospital admission and patient status was appropriate. In connection with this audit suspension, CMS announcedgains that it had initiated a provider education and compliance review program and stated that it would re-evaluate the retrospective review strategy after it evaluated the results of the compliance review. On April 1, 2014, the "Protecting Access to Medicare Act of 2014," was signed into law. A provision of this act further delayed the Two Midnight Rule's enforcement and RAC review of Two Midnight Rule claims until March 31, 2015.

These reviews have historically been a significant finding for the Recovery Audit Program; as a result, the Two Midnight Rule and the suspension of these reviews by the Medicare RACs could have a material negative impact on our future revenuewe anticipate, if HDI is awarded a new Medicare RAC Contract, depending upon, among other factors, how the Two Midnight Rule is applied by providers and the review strategies ultimately approved by CMS.

In addition, on August 29, 2014, CMS announced it would settle with hospitals willing to withdraw inpatient status claims currently pending in the appeals process by offering to pay hospitals 68% for all eligible claims that they have billed to Medicare. Although we accrue an estimated liability for appeals based on the amount of fees that are subject to appeals, closures or other adjustments, which we estimate are probable of being returned to providers following a successful appeal, and we similarly accrue an allowance against accounts receivables related to fees yet to be collected, the impact of CMS' settlement offer to hospitals remains uncertain and our financial condition and results of operations could be adversely affected if we are required to return certain fees we have already been paid under HDI's existing Medicare RAC contract orany. If we are unable to collect fees for auditspredict market preferences or healthcare industry changes, or if we have already performed. There could be a material negative impact on our revenue if under the current Medicare RAC contract, HDI isare unable to obtain full payments for properly provided servicesdevelop or is required to repay a portion of prior fees associated with the hospital settlement program or if future fees payable to HDI by CMS are reduced.

Our success also depends on relationships we develop with our customers that enable us to understand our customers' needs and deliveradapt solutions and services that are tailoredresponsive to meet those needs. If a customer is dissatisfied with the quality ofexisting and potential customers’ needs, we may fail to expand our work, or ifbusiness, which could constrain our products, technical infrastructure or services do not comply with the provisions of our contractual agreements or applicable regulatory requirements, we could incur additional costs that may impair the profitability of a contractfuture revenue growth and damage our ability to obtain additional work from that customer, or other current or prospective customers. For

example, some of our contracts contain liquidated damages provisions and financial penalties related to performance failures, which if triggered, couldmaterially adversely affect our reputation, business, financial condition, results of operations and cash flows. If liquidated damages or other

Our acquisition strategy may subject us to considerable business and financial penalties are assessed against us, we may be requiredrisk.

Historically, to disclose these damages or penalties in connection with future bids for services with other customers, which may reduceachieve our chances of winning such procurements. Althoughstrategic goals, we have liability insurance,made a significant number of acquisitions that have expanded the policy coveragesolutions and limits may not be adequateservices we offer, provided a presence in complementary business lines, or expanded our geographic presence and/or customer base. For example, we acquired IntegriGuard, LLC in September 2009; Verify Solutions, Inc. in December 2009; Allied Management Group-Special Investigation Unit in June 2010; Chapman Kelly, Inc. in August 2010; HDI in December 2011; MedRecovery Management, LLC in December 2012; Essette, Inc. in September 2016; and Eliza Holding Corp. in April 2017.

We intend to provide protection against all potential liabilities. Under the terms of one ofpursue future acquisitions that will continue to expand and diversify our contracts, we have an outstanding irrevocable letter of credit for $4.6 million, which we established against our existing revolving credit facility. If a claim is made against this letter of credit or any similar instrument that we obtainbusiness and to periodically engage in the future, we would be requireddiscussions regarding such possible acquisitions. We are subject to reimburse the issuer of the letter of credit for the amount of the claim.

From time to time, government customers may face financial pressures or pressure from stakeholders that may cause them to redefine or reduce the scope of our contracts (by, for example, significantly reducing the volume of data that we are permitted to audit) or terminate contracts for our services that may be regarded as non-essential. We also occasionally face challenges in obtaining timely or full payments for our properly provided services from customersrisks and parties who we provide services to, despite our right to prompt and full payment under the terms of our contracts. Since several of our contracts, including those with many of our largest customers, may be terminated upon short notice for convenience, dissatisfied customers might seek to exit existing contracts prior to their scheduled expiration date and could direct future businessuncertainties relating to our competitors.ability to identify suitable potential acquisition candidates, to consummate additional acquisitions that will be advantageous to us, and to successfully integrate future acquisitions. Future and potential business acquisitions involve a number of risk factors that could affect our operations, including, but not limited to: