| (Mark One) | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, | ||

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

17, 2017: 43,186,484 ITEM 5: ITEM 10: ITEM 15: expect to initiate a first-in-human Phase 1 study of RAD140 in women with hormone receptor positive breast cancer in 2017. we hold worldwide commercialization rights, except for Japan. synthetic peptide analog that engages the parathyroid hormone receptor, or PTH1 receptor, and was selected for clinical development based on its potential for favorable bone building activity. with respect to time to peak concentration, or Tmax, half-life, or T1/2, and area under the curve, or AUC, was successfully modified to improve comparability to abaloparatide-SC. The results of this clinical evaluation will inform the design of a pivotal bioequivalence study that will be initiated following completion of activities related to manufacturing scale-up, production, and other activities required for the initiation of that study. - Dose-Escalation Study cancer in the United States to determine the recommended dose for a Phase 2 clinical trial and to make a preliminary evaluation of the potential anti-tumor effect of RAD1901. We continue to enroll patients in the EU Phase I FES-PET study. 2016. In 2017, we plan to initiate a first-in-human Phase 1 study of RAD140 in women with hormone receptor positive breast cancer. In of PTHrP. Abaloparatide is manufactured using organic chemistry techniques to create the 34 amino acid peptide. We Japan. to 86 received daily doses of one of the following: 80 µg of abaloparatide, a matching placebo, or the approved dose of 20 µg of Forteo for 18 months. data. Breast Cancer Our Investigational Drug—RAD1901 cancers; and We continue to enroll patients in the EU Phase I FES-PET study. The first three enrolled patients dosed at the 400-mg cohort had a tumor FES-PET signal intensity reduction ranging from 79% to 91% at day 14 compared to baseline. In December 2016, we reported positive results from the ongoing EU Phase 1 FES-PET study including 1 patient with a confirmed partial response by RECIST criteria with all three enrolled patients remained on study drug with mean duration of treatment of 5.64 cycles as of the October 7, 2016 data cut-off date. Adverse events reported to date have been grade 1 and 2 and manageable. This study will enroll 5 additional patients in the 400-mg daily oral cohort followed by 8 patients in the 200-mg daily oral cohort. (ribociclib), a CDK 4/6 inhibitor and BYL719 (alpelisib), an investigational phosphoinositide 3-kinase inhibitor. cancer. patented microneedle technology to administer drugs through the skin, as an alternative to subcutaneous injection. The API In 2016, five U.S. patents that we licensed from Ipsen expired. We own the federal trademark registration in the United States for Radius United States (not including any patent term extension under the Hatch-Waxman Act). The intended therapeutic formulation for abaloparatide-SC is covered by Patent No. 8,148,333 until 2027 in the United States (not including any patent term extension under the Hatch-Waxman Act). Related patents granted in Australia, China, Israel, Japan, South Korea, Mexico, New Zealand, Russia, Singapore, and Ukraine, and We have worldwide rights to commercialize abaloparatide-TD, including in Japan. will or may be asserted against us by third-parties. Should we need to defend ourselves and our partners against any such claims, substantial costs may be incurred. Furthermore, parties making such claims may be able to obtain injunctive or other equitable relief, which could effectively block our ability to develop or commercialize some or all Brisdelle The Agreement. In consideration for the rights to abaloparatide and in recognition of certain milestones having been met to date, we have paid to Ipsen an aggregate amount of from confidential Ipsen know-how, the agreement provides that we terminated in accordance with its terms. develop, manufacture and commercialize RAD1901 in Japan, or the Eisai Amendment. Specifically, we licensed the patent application that subsequently issued as Manufacturing Agreements the other party 18 months prior to the end of the then-current term. The certain force majeure events. NDA based on a determination that the drug is safe and effective for the proposed indication(s). the IND application. In such a case, the IND application sponsor and the FDA must resolve any outstanding FDA concerns or questions before clinical trials can proceed. We cannot be sure that submission of an IND application will result in the FDA allowing clinical trials to begin. Detailed information about many clinical trials must be submitted to the National Institutes of Health, or NIH, for public disclosure on the government website ClinicalTrials.gov. Phase 3 trials typically are relied upon as the primary basis for approval because they provide the safety and effectiveness information needed to evaluate the overall benefit-risk relationship of the drug and to create the physician labeling. the application should be approved. The FDA is not bound by the recommendations of the advisory committee, but the Agency historically has tended to follow such recommendations. records related to safety reporting, distribution and/or manufacturing facilities; this latter effort includes assessment of ongoing compliance with cGMP regulations. Accordingly, manufacturers must continue to expend time, money and effort in the area of production and quality control to maintain cGMP compliance. We have used and intend to continue to use third-party manufacturers to produce our products in clinical and commercial quantities, and future FDA inspections may identify compliance issues at the facilities of our contract manufacturers that may disrupt production or distribution, or require substantial resources to correct. In addition, discovery of problems with a product after approval may result in restrictions on a product, including recall or withdrawal of the product from the market, labeling changes, imposition of REMS, or the requirement to conduct additional studies. In addition to the ANDA pathway, the Hatch-Waxman Act also established an abbreviated approval pathway under section 505(b)(2) of the FDCA for applications that contain full reports of investigations of safety and effectiveness, but where at least some of the information required for approval comes from studies not conducted by or for the applicant and for which the applicant has not obtained a right of reference. Section 505(b)(2) permits approval of applications other than those for duplicate products and permits reliance for such approvals on literature or on FDA’s finding of safety or effectiveness for an approved drug product. Under FDA’s “umbrella policy,” NCE exclusivity protects all drug products that contain the qualifying NCE, so if abaloparatide-TD is approved prior to the expiration to any NCE exclusivity granted to abaloparatide-SC, we would expect abaloparatide-TD to be protected by any remaining NCE exclusivity period. indication that has been approved for abaloparatide-TD. European Union. GMP, and product-specific European Union. The Medicare Prescription Drug, Improvement, and Modernization Act of 2003, or MMA, established the Medicare Part D program to provide a voluntary prescription drug benefit to Medicare beneficiaries. Under Part D, Medicare beneficiaries may enroll in prescription drug plans offered by private entities to provide coverage of outpatient prescription drugs. Part D plans include both stand-alone prescription drug benefit plans and prescription drug coverage as a supplement to Medicare Advantage plans. Unlike Medicare Parts A and B, Part D coverage is not standardized. Part D prescription drug plan sponsors are not required to pay for all covered Part D drugs, and each Part D prescription drug plan can develop its own drug formulary that identifies which drugs it will cover and at what tier or level. However, Part D prescription drug formularies must include drugs within each therapeutic category and class of covered Part D drugs, although not necessarily all of the drugs within each category or class. Any formulary used by a Part D prescription drug plan must be developed and reviewed by a pharmacy and therapeutic committee. We anticipate that a significant proportion of patients eligible for abaloparatide-SC will be Medicare beneficiaries and we expect that abaloparatide-SC, if approved, will be covered under Medicare Part D, although Control Act of 2011, among other things, created measures for spending reductions by Congress. A Joint Select Committee on Deficit Reduction, tasked with recommending a targeted deficit reduction of at least $1.2 trillion for the years 2013 through 2021, was unable to reach required goals, thereby triggering the legislation's automatic reduction to several government programs. This includes aggregate reductions to Medicare payments to providers of 2% per fiscal year, which went into effect on April 1, 2013 and, due to subsequent legislative amendments to the statute, will remain in effect through 2025 unless additional Congressional action is taken. stringent restrictions on manufacturers' communications regarding off-label uses. contain ambiguities as to what is required to comply with the laws. Given the lack of clarity in laws and their implementation, our actions could be subject to the penalty provisions of the pertinent state authorities. the License Agreement and other declaratory judgment. We asserted, among other things, that Ipsen's claimed rights to co-promote abaloparatide in France and to a license from us with respect to Japan have permanently expired, and that Ipsen has breached the License Agreement by, among other things, allowing certain patents to expire and by purporting to license to a third party certain manufacturing and other rights that we contend Ipsen exclusively licensed to us. We are discontinue product development, reduce or forego sales and marketing efforts for any product candidate that is approved, forego attractive business opportunities or discontinue our operations entirely. Any additional sources of financing may not be available or may not be available on favorable terms and will likely involve the issuance of additional equity securities, which will have a dilutive effect on stockholders. Our future studies and the expenses associated with our commercialization efforts for abaloparatide-SC. approved, the past or which we expect for the future. Our financial results in some quarters may fall below expectations. Any of these events as well as the various risk factors listed in this "Risk Factors" section could adversely affect our financial results and cause our stock price to fall. research and clinical approaches will result in drugs that the FDA considers safe for humans and effective for proposed uses. Any collaboration arrangements that we may enter into in the future may not be successful, which could adversely affect our ability to develop and commercialize abaloparatide-SC, or any of our other product candidates. In addition, we, the FDA, or other equivalent regulatory authorities and ethics committees with jurisdiction over our studies may suspend our clinical trials at any time if it appears that we are exposing participants to unacceptable health risks or if the FDA or foreign regulatory authorities find deficiencies in our regulatory submissions or the conduct of these trials. Therefore, we cannot predict with any certainty the schedule for existing or future clinical trials. Any such unexpected expenses or delays in our clinical trials could increase our need for additional capital, which may not be available on favorable terms or at all. In addition, the FDA's policies may change and additional government regulations may be enacted that could prevent, limit, or delay regulatory approval of our product candidates. We cannot predict the likelihood, nature, or extent of government regulation that may arise from future legislation or administrative action, either in the United States or abroad. If we are slow or unable to adapt to changes in existing requirements or the adoption of new requirements or policies, or if we are not able to maintain regulatory compliance, we may lose any marketing approval that we may have obtained and we may not achieve or sustain profitability, which would adversely affect our business. managed care providers and private insurance plans. Private insurers, such as health maintenance organizations and managed care providers, have implemented cost cutting and reimbursement initiatives and likely will continue to do so in the future. These include establishing formularies that govern the drugs and biologics that will be offered and also the on viable commercial products or profitable market opportunities. Our spending on current and future research and development programs and product candidates for specific indications may not yield any commercially viable products. If we do not accurately evaluate the commercial potential or target market for a particular product candidate, we may relinquish valuable rights to that product candidate through collaboration, licensing or other royalty arrangements in cases in which it would have been more advantageous for us to retain sole development and commercialization rights to such product candidate. entities, some of whom may compete with us. If our collaborators assist competitors at our expense, our competitive position would be harmed. have a financial interest that affected the reliability of the data from the ACTIVE Clinical Trials, we could be subject to additional regulatory scrutiny and the utility of the ACTIVE Clinical Trials for purposes of our planned regulatory submissions could be compromised, which could have a material adverse effect on our business and the value of our common stock. business and financial condition would be materially harmed. Because the manufacturing process for abaloparatide-TD requires the use of 3M's proprietary technology, 3M is our sole source for finished clinical trial supplies of abaloparatide-TD. To date, we have not entered into a commercial supply agreement with 3M. If we product revenue. If we are unable to effectively establish and manage the distribution process, the commercial launch and sales of abaloparatide-SC will be delayed or severely compromised and our results of operations may be harmed. If we cannot compete successfully for market share against other drug companies, we may not achieve sufficient product revenues and our business will suffer. We may incur substantial liabilities and may be required to limit commercialization of our products in response to product liability lawsuits. October 3, 2027, absent any issued SPCs. We may become party to, or threatened with, future adversarial proceedings or litigation regarding intellectual property rights with respect to patents issued or licensed to us, including interference proceedings before the USPTO. Third parties also may assert infringement claims against us. If we are found to infringe a third party's intellectual property rights, we could be required to obtain a license from such third party to continue developing and marketing our products and technology. However, we may not be able to obtain any required license on commercially reasonable terms or at all. Even if we were able to obtain a license, it could be non-exclusive, thereby giving our competitors access to the same technologies licensed to us. We could be forced, including by court order, to cease commercializing the infringing technology or product. In addition, we could be found liable for monetary damages. A finding of infringement could prevent us from commercializing our product candidates or force us to cease some of our business operations, which could materially harm our business. Claims that we have misappropriated the confidential information or trade secrets of third parties could have a similar negative impact on our business. For example, we are aware of a applications in the United States and other jurisdictions are typically not published until 18 months after filing, or in some cases not at all. Therefore, we cannot be certain that we or our licensors were the first to make the inventions claimed in our owned and licensed patents or pending patent applications, or that we or our licensors were the first to file for patent protection of such inventions. An adverse determination in any such proceeding could reduce the scope of, or invalidate our patent rights, allow third parties to commercialize our technology or products and compete directly with us, without payment to us, or result in our inability to manufacture or commercialize products without infringing third-party patent rights. assignment agreements with our employees and consultants. However, any of these parties may breach the agreements and disclose our proprietary information, and we may not be able to obtain adequate remedies for any breaches. Enforcing a claim that a party illegally disclosed or misappropriated a trade secret is difficult, expensive and time-consuming, and the outcome is unpredictable. In addition, some courts inside and outside the United States are less willing or unwilling to protect trade secrets. If any of our trade secrets were to be lawfully obtained or independently developed by a competitor, we would have no right to prevent them from using that technology or information to compete with us. If any of our trade secrets were to be disclosed to, or independently developed by a competitor, our competitive position would be harmed. Intellectual property litigation could cause us to spend substantial resources and distract our personnel from their normal responsibilities. conduct of various electronic healthcare transactions and protects the security and privacy of protected health information; affect our business, financial condition and results of operations. In addition, the federal, state and local laws and regulations governing the use, manufacture, storage, handling and disposal of hazardous or radioactive materials and waste products may require us to incur substantial compliance costs that could materially adversely affect our business, financial condition and results of operations. manage our development efforts effectively; If we are not successful in completing acquisitions that we may pursue in the future, we would be required to reevaluate our business strategy and we may have incurred substantial expenses and devoted significant management time and resources in seeking to complete the acquisitions. In addition, we could use substantial portions of our available cash as all or a portion of the purchase price, or we could issue additional securities as consideration for these acquisitions, which could cause our stockholders to suffer significant dilution. and our business. Material weaknesses in our internal control over financial reporting could also reduce our ability to obtain financing or could increase the cost of any financing we obtain. We may be required to pay severance benefits to our employees who are terminated in connection with a change in control, which could harm our financial condition or results. Waltham, MA, USA Cambridge, MA, USA Quarter Ended June 30, 2014 (beginning June 6, 2014) Quarter Ended September 30, 2014 Quarter Ended December 31, 2014 On February 2016. Operating expenses: Research and development General and administrative Loss from operations Other (expense) income: Other (expense) income, net Interest (expense) income, net Net loss Other comprehensive loss, net of tax: Unrealized gain (loss) from available-for-sale securities Comprehensive loss Net (loss) earnings attributable to common stockholders Net (loss) earnings per share applicable to common stockholders—basic Net (loss) earnings per share applicable to common stockholders—diluted Weighted-average number of common shares used in net (loss) earnings per share applicable to common stockholders—basic Weighted-average number of common shares used in net (loss) earnings per share applicable to common stockholders—diluted Cash and cash equivalents Marketable securities Working capital Total assets Long-term liabilities Total liabilities Total convertible preferred stock and redeemable convertible preferred stock Total liabilities, convertible preferred stock, redeemable convertible preferred stock and stockholders' equity (deficit) expect to initiate a first-in-human Phase 1 study of RAD140 in women with hormone receptor positive breast cancer in 2017. with respect to Tmax, T1/2, and AUC was successfully modified so as to improve comparability to abaloparatide-SC. The results of this clinical evaluation will inform the design of a pivotal bioequivalence study that will be initiated following completion of activities related to manufacturing scale-up, production, and other activities required for the initiation of that study. - Dose-Escalation Study We continue to enroll patients in the EU Phase I FES-PET study. RAD140 in women with hormone receptor positive breast cancer in 2017. Abaloparatide-SC Abaloparatide-TD RAD1901 RAD140 Interest expense reflects interest due under our loan and security results of operations. and development expenses may be necessary in future periods. Historically, our estimated accrued clinical expenses have approximated actual expense incurred. Subsequent changes in estimates may result in a material change in our accruals. Performance Units Operating expenses: Research and development General and administrative Loss from operations Other (expense) income: Other (expense) income, net Loss on retirement of note payable Interest (expense) income, net Net loss Other (expense) income, net—For the year ended December 31, 2015, other expense, net of other income, was $35 thousand, as compared to Operating expenses: Research and development General and administrative Loss from operations Other (expense) income: Other (expense) income, net Loss on retirement of note payable Interest (expense) income, net Net loss Liquidity and Capital Resources opportunities will be available to us on favorable terms, and some could be dilutive to existing stockholders. Our future capital requirements will depend on many factors, including the scope and progress made in our research and development and commercialization activities, the results of our clinical trials, and the review and potential approval of our products by the Net cash (used in) provided by: Operating activities Investing activities Financing activities Net increase (decrease) in cash and cash equivalents 2015. 2015. offering costs, of approximately $281.5 million. Also, on July 28, 2015, the underwriters purchased an additional 608,108 shares by exercising an option to purchase additional shares that was granted to them in connection with the offering. As a result of the public offering and subsequent exercise of the underwriters' option, we received aggregate proceeds, net of underwriting discounts, commissions and estimated offering costs of approximately $323.8 million. Sales of Preferred Stock Series B redeemable convertible preferred stock(1) Series C redeemable convertible preferred stock(1) Series A-1 convertible preferred stock(1) Series A-5 convertible preferred stock(1) Series B convertible preferred stock Series B-2 convertible preferred stock Total On February 14, 2014, we entered into a Series B-2 Convertible Preferred Stock and Warrant Purchase Agreement, or Purchase Agreement, pursuant to which we were able to raise up to approximately $40.2 million through the issuance of (1) up to 655,000 series B-2 Shares convertible preferred stock, or Series B-2, par value $.0001 per share, and (2) warrants to acquire up to 718,201 shares of our common stock, at an exercise price of $14.004 per share. On February 14, 2014, February 19, 2014, February 24, 2014, March 14, 2014 and March 28, 2014, we consummated closings under the Series B-2 Purchase Agreement, whereby, in exchange for aggregate proceeds to us of approximately $27.5 million, we issued an aggregate of 448,060 Series B-2 Shares and warrants to purchase up to a total of 491,293 shares of our common stock. The warrants issuable pursuant to the Purchase Agreement are exercisable for a period of five years from issuance. Debt Borrowings The following table summarizes our contractual obligations at December 31, Operating lease obligations As of December 31, Work Statement NB-3 Total Payments License Agreement Obligations France (as discussed above). into an amendment to the Eisai Agreement 2036. Off-Balance Sheet Arrangements ASSETS Current assets: Cash and cash equivalents Marketable securities Prepaid expenses and other current assets Total current assets Property and equipment, net Other assets Total assets LIABILITIES AND STOCKHOLDERS' EQUITY Current liabilities: Accounts payable Accrued expenses and other current liabilities Total current liabilities Note payable, net of current portion and discount Total liabilities Commitments and contingencies Stockholders' equity: Common stock, $.0001 par value; 200,000,000 shares authorized, 42,984,243 shares and 32,924,535 shares issued and outstanding at December 31, 2015 and 2014, respectively Additional paid-in-capital Accumulated other comprehensive income (loss) Accumulated deficit Total stockholders' equity Total liabilities and stockholders' equity OPERATING EXPENSES: Research and development General and administrative Loss from operations OTHER (EXPENSE) INCOME: Other (expense) income, net Loss on retirement of note payable Interest income Interest expense NET LOSS OTHER COMPREHENSIVE LOSS, NET OF TAX: Unrealized gain (loss) from available-for-sale securities COMPREHENSIVE LOSS LOSS ATTRIBUTABLE TO COMMON STOCKHOLDERS—BASIC AND DILUTED (Note 12) LOSS PER SHARE: Basic and diluted WEIGHTED AVERAGE SHARES: Basic and diluted Balance at December 31, 2012 Net loss Stock options exercised Issuance of preferred stock Accretion of dividends on preferred stock Stock-based compensation expense Balance at December 31, 2013 Net loss Unrealized loss from available-for-sale securities Issuance of preferred stock Accretion of dividends on preferred stock Issuance of warrants Exercise of warrants Stock options exercised Stock-based compensation expense Issuance of common stock, net Conversion of convertible preferred stock into common stock Reclassification of warrant liability to additional paid in capital Balance at December 31, 2014 Net loss Unrealized gain from available-for-sale securities Exercise of warrants Exercise of options Stock-based compensation expense Issuance of common stock, net Balance at December 31, 2015 Balance at December 31, 2012 Net loss Stock options exercised Issuance of preferred stock Accretion of dividends on preferred stock Stock-based compensation expense Balance at December 31, 2013 Net loss Unrealized loss from available-for-sale securities Issuance of preferred stock Accretion of dividends on preferred stock Issuance of warrants Exercise of warrants Stock options exercised Stock-based compensation expense Issuance of common stock, net Conversion of convertible preferred stock into common stock Reclassification of warrant liability to additional paid in capital Balance at December 31, 2014 Net loss Unrealized gain from available-for-sale securities Exercise of warrants Exercise of options Stock-based compensation expense Issuance of common stock, net Balance at December 31, 2015 CASH FLOWS USED IN OPERATING ACTIVITIES: Net loss Adjustments to reconcile net loss to net cash used in operating activities: Depreciation and amortization Amortization of premium (accretion of discount) marketable securities, net Stock-based compensation expense Research and development expense settled in stock Change in fair value of other current assets, warrant liability and other liability Non-cash interest Loss on retirement of note payable Changes in operating assets and liabilities: Prepaid expenses and other current assets Other long-term assets Accounts payable Accrued expenses and other current liabilities Net cash used in operating activities CASH FLOWS (USED IN) PROVIDED BY INVESTING ACTIVITIES: Purchases of property and equipment Purchases of marketable securities Sales and maturities of marketable securities Net cash (used in) provided by investing activities CASH FLOWS PROVIDED BY FINANCING ACTIVITIES: Proceeds from exercise of stock options Net proceeds from the issuance of preferred stock, net Proceeds from note payable, net Proceeds from issuance of common stock, net Deferred financing costs Payments on note payable Fee for early prepayment of note payable Net cash provided by financing activities NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR CASH AND CASH EQUIVALENTS AT END OF YEAR SUPPLEMENTAL DISCLOSURES: Cash paid for interest NON-CASH FINANCING ACTIVITIES: Accretion of dividends on preferred stock Reclassification of preferred stock to common stock Fair value of series A-6 convertible preferred stock issued as settlement of liability Fair value of warrants issued the treatment of breast cancer. Company's common stock. All shares and per share amounts in the financial statements and accompanying notes have been retroactively adjusted to give effect to the reverse stock split. marketable securities by maintaining its deposits and investments at high-quality financial institutions. The Company invests any excess cash in money market funds and other securities, and the management of these investments is not discretionary on the part of the financial institution. The Company has no significant off-balance-sheet risks such as foreign exchange contracts, option contracts, or other hedging arrangements. Income Taxes—The Company recognizes deferred tax assets and liabilities for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis, as well as operating loss and tax credit carryforwards. The Company measures deferred tax assets and liabilities using enacted tax rates expected to apply to taxable income in the years in which those temporary differences and carryforwards are expected to be recovered or settled. Deferred tax assets are reduced by a valuation allowance to reflect the uncertainty associated with their ultimate realization. The effect on deferred tax assets and liabilities as a result of a change in tax rates is recognized as income in the period that includes the enactment date. 2015. uses an expected dividend yield of zero. The risk-free rate is based on the U.S. Treasury yield curve in effect at the time of grant valuation for a period commensurate with the option's expected term. These assumptions are highly subjective and changes in them could significantly impact the value of the option and hence the related compensation expense. Comprehensive Income (Loss)—Comprehensive income (loss) refers to revenues, expenses, gains and losses that are excluded from net income (loss), as these amounts are recorded directly as an adjustment to stockholders' equity (deficit), net of tax. The Company's other comprehensive (loss) income is comprised of unrealized gains (losses) on its available-for-sale marketable securities. In January 2016, the FASB issued Cash and cash equivalents: Cash Money market Domestic corporate commercial paper Government-sponsored enterprise debt securities Domestic corporate debt securities Asset-backed securities Total Marketable securities: Domestic corporate debt securities Domestic corporate commercial paper Asset-backed securities Total Cash and cash equivalents: Cash Money market funds Domestic corporate debt securities Total Marketable securities: Domestic corporate debt securities Domestic corporate commercial paper Total 2015. Furniture and fixtures Computer equipment and software Manufacturing equipment Leasehold improvements Less accumulated depreciation and amortization Property and equipment, net as of December 31, 2016. Research costs—Nordic(1) Research costs—other Payroll and employee benefits Professional fees Accrued interest on notes payable Other Total accrued expenses and other current liabilties 6. Loan and Security Agreement NASDAQ Global Market on June 6, 2014. In connection with the offering, all outstanding shares of our convertible preferred stock converted into 19,465,132 shares of common stock and 2,862,654 shares of common stock were issued in satisfaction of accumulated dividends accrued on the preferred stock. In addition, all outstanding warrants to purchase shares of series A-1 convertible preferred stock and warrants to purchase shares of series B-2 convertible preferred stock were converted into the right to purchase 149,452 shares of common stock and the Company's warrant liability was reclassified to equity. On February 14, 2014, the Company entered into a Series B-2 Convertible Preferred Stock and Warrant Purchase Agreement (the "Series B-2 Purchase Agreement"), pursuant to which the Company was able to raise up to approximately $40.2 million through the issuance of (1) up to 655,000 shares of its preferred stock (the "Series B-2"), and (2) warrants to acquire up to 718,201 shares of its common stock with an exercise price of $14.004 per share. In February and March 2014, the Company consummated closings under the Series B-2 Purchase Agreement, whereby, in exchange for aggregate gross proceeds to the Company of approximately $27.5 million, the Company issued an aggregate of 448,060 shares of Series B-2 and warrants to purchase up to a total of 491,293 shares of its common stock. The warrants can be exercised at any time prior to the fifth anniversary of their issuance. Upon completion of the Company's initial public offering, all outstanding warrants to purchase shares of series B-2 convertible preferred stock were converted into the right to purchase shares of common stock. Assets Cash and cash equivalents: Cash Money market funds(1) Domestic corporate commercial paper(2) Government-sponsored enterprise debt securities(2) Domestic corporate debt securities(2) Asset-backed securities(2) Total Marketable Securities Domestic corporate debt securities(2) Domestic corporate commercial paper(2) Asset-backed securities(2) Total Assets Cash and cash equivalents: Cash Money market funds(1) Domestic corporate debt securities(2) Total Marketable securities: Domestic corporate debt securities(2) Domestic corporate commercial paper(2) Total 9. License Agreements In consideration for these The date of the last to expire of the abaloparatide patents licensed from or co-owned with Ipsen, barring any extension thereof, is expected to be March 26, 2028. milestones. The Eisai Agreement, as amended, also grants the Company the right to grant sublicenses with prior written approval from Eisai. If the Company sublicenses the licensed technology to a third party, the Company will be obligated to pay Eisai, in addition to the milestones referenced above, a fixed low double digit percentage of certain fees received from such sublicensee and royalties in the low single digit range based on net sales of the sublicensee. The license agreement expires on a country-by-country basis on the later of (1) the date the last remaining valid claim in the licensed patents expires, lapses or is invalidated in that country, the product is not covered by data protection clauses, and the sales of The Company Payments in cash to be made to Nordic Plans approximately 2016. Expected term (years) Volatility Expected dividend yield Risk-free interest rates Options outstanding at December 31, 2014 Granted Exercised Cancelled Expired Options outstanding at December 31, 2015 Options exercisable at December 31, 2015 Options vested or expected to vest at December 31, 2015 unvested RSUs, which is expected to be recognized over a weighted-average period of approximately 3 years. Research and development General and administrative Share-based compensation expense included in operating expenses Numerator: Net loss Accretion of preferred stock Loss attributable to common stockholders—basic Effect of dilutive convertible preferred stock Loss attributable to common stockholders—diluted Denominator: Weighted-average number of common shares used in loss per share—diluted Loss per share—basic and diluted Convertible preferred stock Options to purchase common stock Warrants Performance units A reconciliation of income taxes computed using the U.S. federal statutory rate to that reflected in operations follows (in thousands): Income tax benefit using U.S. federal statutory rate State income taxes, net of federal benefit Stock-based compensation Research and development tax credits Change in the valuation allowance Permanent items Other Current assets: Accrued expenses Gross current deferred tax assets Valuation allowance Net current deferred tax assets Non-current assets: Net operating loss carryforwards Capitalized research and development Research and development credits Depreciation and amortization Accrued Expenses Stock-based compensation Other Gross non-current deferred tax assets Valuation allowance Net non-current deferred tax assets tax planning strategies to generate future taxable income. The Company is obligated to make monthly rent payments pursuant to these non-cancellable agreements as set forth below (in thousands): 2016 2017 2018 2019 2020 Total minimum lease payments 2015: Net loss Net loss applicable to common stock Net loss per share—basic and diluted Weighted-average common shares outstanding—basic and diluted 2014: Net loss Net loss applicable to common stock Net loss per share—basic and diluted Weighted-average common shares outstanding—basic and diluted 2016. 2016. Code of Business Conduct and Ethics 24, 2017

Title of each class Name of each exchange on which registered Common Stock, par value $0.0001 per share The NASDAQ Global Market 20152016 was $2.1$1.0 billion. For the purpose of the foregoing calculation only, all directors and executive officers of the registrant are assumed to be affiliates of the registrant.19, 2016: 43,014,243proxy statementProxy Statement for its 2016 annual meeting2017 Annual Meeting of stockholdersStockholders are incorporated by reference into Part III of this Annual Report on Form 10-K.2015

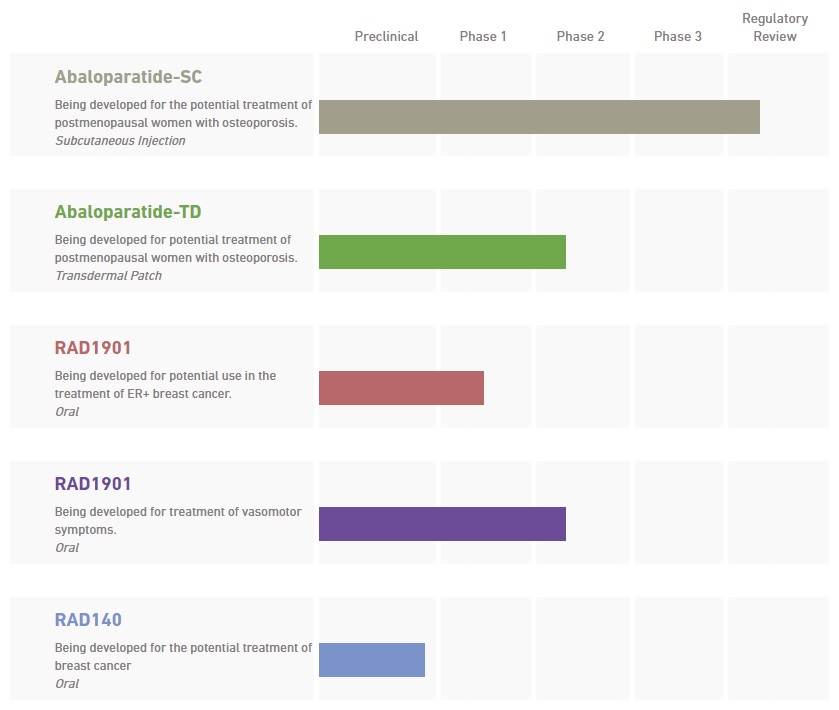

2016 Currency and Conversions ITEM 1:Business3ITEM 1A:Risk Factors35ITEM 1B:Unresolved Staff Comments63ITEM 2:Properties63ITEM 3:Legal Proceedings63ITEM 4:Mine Safety Disclosures63 PART II Controls and Procedures120ITEM 9B:Other Information122 PART III Signatures130SPECIAL•the progress of, timing of and amount of expenses associated with our research, development and commercialization activities;•the success of our clinical studies for our investigational product candidates;•••••the timing of and our ability to commercialize abaloparatide following regulatory approval;•••••motivateretain key personnel; and• In this report, references to "dollar" or "$" are to the legal currency of the United States, and references to "euro" or "€" are to the single currency introduced on January 1, 1999 at the start of the third stage of European Economic and Monetary Union, pursuant to the Treaty establishing the European Communities, as amended by the Treaty on European Union and the Treaty of Amsterdam. Unless otherwise indicated, the financial information in this report has been expressed in U.S. dollars. Unless otherwise stated, the U.S. dollar equivalent information translating euros into U.S. dollars has been made, for convenience purposes, on the basis of the noon buying rate published by the Board of Governors of the Federal Reserve as of December 31, 2015, which was €1.00 = $1.0859. Such translations should not be construed as a representation that the euro has been, could have been or could be converted into U.S. dollars at the rate indicated, any particular rate or at all. Trademarks appearing in this report are the property of their respective holders. the investigational drug abaloparatide for subcutaneous injection, or abaloparatide-SC, has completed Phase 3 development for potential use in the reductiontreatment of fracture risk in postmenopausal women with osteoporosis andpostmenopausal osteoporosis. Our New Drug Application, or NDA, for abaloparatide-SC is currently under regulatory review by the U.S. Food and Drug Administration, or FDA, with a Prescription Drug User Fee Act, or PDUFA, date of March 30, 2017. Our European Marketing Authorisation Application, or MAA, for abaloparatide-SC is under review by the Committee for Medicinal Products for Human Use, or CHMP, of the European Medicines Agency, or EMA. We intend to commercialize abaloparatide-SC in Europe. the United States ourselves and our experienced commercial leaders are rapidly expanding the breadth of our capabilities and sales organization with highly skilled and tenured individuals.osteoporosisthe treatment of women with postmenopausal osteoporosis. We are focused on completing the manufacturing scale-up, production, and other activities required for the initiation of a pivotal bioequivalence study for abaloparatide-TD. In addition, we are evaluating our investigational drugproduct candidate, RAD1901, a selective estrogen receptor down-regulator/degrader, or SERD, for potential use in the treatment of hormone-driven and/or hormone-resistant breast cancer, andas well as for potential use in the treatment of vasomotor symptoms in postmenopausal women. We plan to complete our ongoing Phase 1 studies of RAD1901 in advanced metastatic breast cancer and our ongoing Phase 2b study of RAD1901 in postmenopausal vasomotor symptoms. In the first half of 2017, we plan to engage with regulatory agencies to gain alignment on defining the next steps for our RAD1901 breast cancer program, which would include the design of a Phase 2 trial. In the first half of 2017, we also expect to complete and report results from our ongoing Phase 2b vasomotor trial. Our preclinicalclinical pipeline also includes our internally developed investigational product candidate, RAD140, a non-steroidal selective androgen receptor modulator, or SARM, under investigation for potential applicationsuse in oncologythe treatment of breast cancer. In December 2016, we submitted an investigational new drug application, or IND, to the FDA and multiple conditions where androgen modulation may offer therapeutic benefit.proposedpotential indication and stage of development:

*submitted an MAA in the European Unionhold worldwide commercialization rights for all of these product candidates, excluding abaloparatide-SC, in November 2015,for which was validated in December 2015.

Abaloparatide was createda unique mechanismthe potential to provide the following advantages over other current standard of actioncare treatments for osteoporosis:the goallower vertebral and non-vertebral fracture risk;stimulating enhanced bone building activity including bone formation, increasing bone mineral density, restoring bone microarchitecturebone; augmenting bone strength. •Abaloparatide-SC—Abaloparatide abaloparatide-SC, an injectable subcutaneous formulation of abaloparatide, and abaloparatide-TD, a potential line extension of abaloparatide-SC in the form of a convenient, short-wear-time, transdermal patch.injection, which we refer to as abaloparatide-SC.injection. We hold worldwide commercialization rights to abaloparatide-SC, except for Japan. In December 2014, we announced the positive 18-month top-line data from our Phase 3 ACTIVE clinical trial of abaloparatide-SC. These results were published in which abaloparatide-SC met the primary endpoint with a statistically significant reductionJournal of the American Medical Association, or JAMA, in new vertebral fractures versus placebo, and inAugust 2016. In June 2015, we announced the positive top-line data from the first six months of theour 24-month ACTIVExtend clinical trial of abaloparatide-SC and the 24-month25-month combined fracture data from the ACTIVE and ACTIVExtend.ACTIVExtend clinical trials. These data were published in the Mayo Clinic Proceedings in February 2017. The combined 25-month fracture data from our Phase 3 clinical trial program for abaloparatide-SC formed the basis of our regulatory submissions in the United States and Europe. In November 2015, we submitted a marketing authorization application, oran MAA to the European Medicines Agency, or EMA, which was validated and is currently undergoing active regulatory reviewassessment by the EMA.CHMP. We anticipate that the CHMP may adopt an opinion regarding the MAA in 2017. In March 2016, we submitted an NDA to the FDA, which has been accepted for filing by the FDA with a PDUFA date of March 30, 2017. We intend to enter into one or more partnerships or collaborations for the potential commercialization of abaloparatide-SC prior to a commercial launch. We plan to submit a new drug application, or NDA, in the United States, at the end of the first quarter of 2016. Subject to regulatory review and a favorable regulatory outcome, we anticipate the first commercial sales of abaloparatide-SC willto take place in 2016.2017. We intend to commercialize abaloparatide-SC in the United States ourselves and our experienced commercial leaders are rapidly expanding the breadth of our capabilities and sales organization with highly skilled and tenured individuals. We expect to report the top-line results from our recently completed 24-month ACTIVExtend trial in the second quarter of 2017.•Abaloparatide-TD—abaloparatide-transdermal, which we refer to as abaloparatide-TD,abaloparatide- TD, based on 3M's3M’s patented Microstructured Transdermal System technology for potential use as a short wear-time transdermal patch. We hold worldwide commercialization rights to the abaloparatide-TD technology. During 2014, we reported progress towards the development of an optimized transdermal patch that may be capable of demonstrating comparability to abaloparatide-SC. In preliminary, nonhuman primate pharmacokinetic studies, we achieved a desirable pharmacokinetic profile, with comparable AUC, Cmax, Tmax and T1/2 relative to abaloparatide-SC. We believe that these results support continued clinical development ofare developing abaloparatide-TD toward future global regulatory submissions as ato build upon the potential post-approval line extensionsuccess of theour investigational drug abaloparatide-SC.product candidate, abaloparatide-SC, if approved. We commenced a human replicative clinical evaluation of the optimized abaloparatide-TD patch in December 2015, with the goal of achieving comparability to abaloparatide-SC. We expect to complete our clinicalIn September 2016, we presented results from this evaluation, which showed that the pharmacokinetic profile of thean optimized abaloparatide-TD patch during 2016.hasis being evaluated for potential for use as an oral non-steroidal treatment for hormone-driven and/or hormone-resistant, breast cancer. We hold worldwide commercialization rights to RAD1901. RAD1901 is currently being investigated in postmenopausal women with advanced estrogen receptor positive, or ER-positive, and human epidermal growth factor receptor 2-negative, or HER2-negative breast cancer, the most common form of the disease. TheStudies completed to date indicate that the compound has the potential for use as a single agent, or in combination with other therapies to overcome endocrine resistance infor the treatment of breast cancer. In September 2015, we announced results from We believe that, subject to successful development, regulatory review and approval, RAD1901 could have the potential to offer the following advantages compared to current standard of care treatments for ER-positive and HER2-negative breast cancer:maximum tolerated dose, or MTD, study of RAD1901 in 52 healthy volunteers. In the study, RAD1901 was administered to healthy postmenopausal women in doses ranging from 200mg to 1000mg, and the data showed that RAD1901 was well-tolerated and the overall safety was supportive of continued development. In addition, a subset of subjects that received 18F estradiol positron emission tomography, or FES-PET, imaging demonstrated suppression of the FES-PET signal to background levels after six days of dosing.two-part,multiple-part, dose-escalation study of RAD1901 in postmenopausal women with advanced ER-positive and HER2-negative advanced breastWe expectPart A of this Phase 1 study was designed to completeevaluate escalating doses of RAD1901. The Part B expansion cohort was initiated at 400 mg daily dosing in March 2016 to allow for an evaluation of additional safety, tolerability and preliminary efficacy. The patients enrolled in this study byare heavily pretreated ER-positive, HER2-negative advanced breast cancer patients who have received a median of 3 prior lines of therapy including fulvestrant and CDK4/6 inhibitors, and more than 50% of the middle ofpatients had ESR1 mutations. Dose escalation is currently ongoing with no dose limiting toxicities to date and we expect to initiate expansion cohorts in 2016.Pfizer'sPfizer’s palbociclib, a cyclin-dependent kinase, or CDK 4/6 inhibitor, or Novartis'Novartis’ everolimus, ana mTOR inhibitor, was effective in shrinking tumors. In preclinical patient-derived xenograft or PDx, breast cancer models with either wild type or mutant ESR1, treatment with RAD1901 resulted in marked tumor growth inhibition, and the combination of RAD1901 with either agent, palbociclib or everolimus, showed anti-tumor activity that was significantly greater than either agent alone. We believe that thisthese preclinical data suggestssuggest that RAD1901 has the potential to overcome endocrine resistance, is well-tolerated, and has a profile that is well suited for use in combination therapy.Novartis'Novartis’ investigational agent LEE011 (ribociclib), a CDK 4/6 inhibitor, and BYL719 (alpelisib), an investigational phosphoinositide 3-kinase inhibitor. as an estrogen receptor ligand for the potential relief of the frequency and severity of moderate to severe hot flashes in postmenopausal women with vasomotor symptoms. We commenced aexpect to report results from our Phase 2b clinical study of RAD1901 for the potential treatment of postmenopausal vasomotor symptoms in the first half of 2017.2015.other serious endocrine diseases. To achieve this goal, we plan to:•aour Phase 3 clinical trial of abaloparatide-SC, or the ACTIVE trial, and the first six months of anrecently completed our 24-month extension trial of abaloparatide-SC, or the ACTIVExtend trial, for the potential use in the reduction of fractures in postmenopausal osteoporosis. We submitted anOur NDA for abaloparatide-SC in the United States is undergoing regulatory review by the FDA with a PDUFA date of March 30, 2017 and our MAA in the European Union for abaloparatide-SC is under review by the CHMP with an opinion anticipated in November 2015, which was validated in December 2015, and plan2017. We are building a commercial organization to submit an NDA forsupport the potential commercialization of abaloparatide-SC in the United States atU.S. We intend to complete the endhiring of our U.S. sales force in the first quarter of 2016.2017. We expect to report the top-line results from our recently completed 24-month ACTIVExtend trial in the second quarter of 2017.