Use these links to rapidly review the documentTABLE OF CONTENTSTable of ContentsINDEX TO FINANCIAL STATEMENTSItem 8. Financial Statements and Supplementary Data

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the year ended December 31, | ||

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission File Number 001-36464

Agile Therapeutics, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 23-2936302 (I.R.S. Employer Identification No.) |

101 Poor Farm Road

Princeton, New Jersey 08540

(Address including zip code of principal executive offices)

(609) 683-1880

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of exchange on which registered: | ||

|---|---|---|---|---|

| Common stock, par value $0.0001 per share | AGRX | The |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or emerging growth company. See definition of "large accelerated filer," "accelerated filer"filer," "smaller reporting company," and "smaller reporting"emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer | Non-accelerated filer | Smaller reporting company ý Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the voting stock held by non-affiliates of the registrant as of June 30, 201628, 2019 was approximately $152.8$52.1 million.

As of March 10, 2017February 18, 2020, there were 28,776,39869,810,305 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement for its 20172020 Annual Meeting of Stockholders (the "Proxy Statement"), to be filed within 120 days of the registrant's fiscal year ended December 31, 2016,2019, are incorporated by reference in Part II and Part III of this Annual Report on Form 10-K. Except with respect to information specifically incorporated by reference in this Annual Report on Form 10-K, the Proxy Statement is not deemed to be filed as part of this Annual Report on Form 10-K10-K.

Agile Therapeutics, Inc.

Annual Report on Form 10-K

For Thethe Year Ended December 31, 20162019

Table of Contents

| | | Page | |||||||

|---|---|---|---|---|---|---|---|---|---|

PART I | |||||||||

Item 1. | Business | 3 | |||||||

Item 1A. | Risk Factors | ||||||||

Item 1B. | Unresolved Staff Comments | ||||||||

Item 2. | Properties | ||||||||

Item 3. | Legal Proceedings | ||||||||

Item 4. | Mine Safety Disclosures | ||||||||

| |||||||||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||||||||

Item 6. | Selected Financial Data | ||||||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||

Item 8. | Financial Statements and Supplementary Data | ||||||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | ||||||||

Item 9A. | Controls and Procedures | ||||||||

Item 9B. | Other Information | ||||||||

| |||||||||

Item 10. | Directors, Executive Officers and Corporate Governance | ||||||||

Item 11. | Executive Compensation | ||||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||||

Item 13. | Certain Relationships and Related Transactions and Director Independence | ||||||||

Item 14. | Principal Accounting Fees and Services | ||||||||

| |||||||||

Item 15. | Exhibits, | ||||||||

Item 16. | Form 10-K Summary | 133 | |||||||

i

SPECIAL CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This annual reportAnnual Report on Form 10-K includes statements that are, or may be deemed, "forward-looking statements." In some cases, these forward-looking statements can be identified by the use of forward-looking terminology, including the terms "believes," "estimates," "anticipates," "expects," "plans," "intends," "may," "designed," "could," "might," "will," "should," "approximately" or, in each case, their negative or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. They appear in a number of places throughout this Annual Report on Form 10-K and include statements regarding our current intentions, beliefs, projections, outlook, analyses or current expectations concerning, among other things, our ongoing and planned manufacturing and commercialization of Twirla®, the potential market uptake of Twirla® and the development of Twirla and our otherpotential product candidates, the strength and breadth of our intellectual property, our ongoing and planned clinical trials, the timing of and our ability to make regulatory filings and obtain and maintain regulatory approvals for our potential product candidates, the legal and regulatory landscape impacting our business, the degree of clinical utility of our products, particularly in specific patient populations, expectations regarding clinical trial data, our development and validation of manufacturing capabilities, our results of operations, financial condition, liquidity, prospects, growth and strategies, the length of time that we will be able to continue to fund our operating expenses and capital expenditures, our expected financing needs and sources of financing, the industry in which we operate and the trends that may affect the industry or us.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events, competitive dynamics, and healthcare, regulatory and scientific developments and depend on the economic circumstances that may or may not occur in the future or may occur on longer or shorter timelines than anticipated. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Annual Report on Form 10-K, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate may differ materially from the forward-looking statements contained in this Annual Report on Form 10-K. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, they may not be predictive of results or developments in future periods.

Some of the factors that we believe could cause actual results to differ from those anticipated or predicted include:

Any forward-looking statements that we make in this Annual Report on Form 10-K speak only as of the date of such statement, and we undertake no obligation to update such statements to reflect events or circumstances after the date of this Annual Report on Form 10-K. You should also read carefully the factors described in the "Risk Factors" section of this Annual Report on Form 10-K to better understand the risks and uncertainties inherent in our business and underlying any forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report on Form 10-K will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard any of these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified timeframe, or at all.

This Annual Report on Form 10-K includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third partythird-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third partythird-party research, surveys and studies are reliable, we have not independently verified such data.

We qualify all of our forward-looking statements by these cautionary statements. In addition, with respect to all of our forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Overview

We are a forward-thinking women's healthcare company dedicated to fulfilling the unmet health needs of today's women. Our currentTwirla® and our potential product candidates are designed to provide women with contraceptive options that offer greater convenience and facilitate compliance. Our leadTwirla, our first and only approved product, candidate, Twirla®, also known as AG200-15, is a once-weekly prescription combination hormonal contraceptive patch that is at the end of Phase 3 clinical development. We completed the third of three Phase 3 clinical trials for Twirla in December 2016 and expect to resubmit our new drug application, or NDA, in the first half of 2017. Our short-term goal is to establish a market-leading franchise in the U.S. hormonal contraceptive market, which had total market sales of approximately $5.5 billion in 2016. Over half of those sales were generated by branded products. Currently, there is only one other contraceptive patch available in the United States and we believe it has limitations due to its dose and physical characteristics.patch. Twirla is designed to address these limitations. We have developed ausing our proprietary transdermal patch technology, called Skinfusion®, which is designed to provide advantages over the currently available patch and is intendedwith properties to optimize patch adhesion and patient wearability.wearability, which may help support compliance while, for the first time in a contraceptive patch, delivering a dose of estrogen consistent with commonly prescribed combined hormonal contraceptives, or CHCs. We believe there is an unmet market need for a low-dose contraceptive patch that is designed to address the limitationsdeliver approximately 30 mcg of the existing patch, while increasing patient convenienceestrogen and 120 mcg of progestin in a convenient dosage form that may support compliance in a non-invasive fashion.

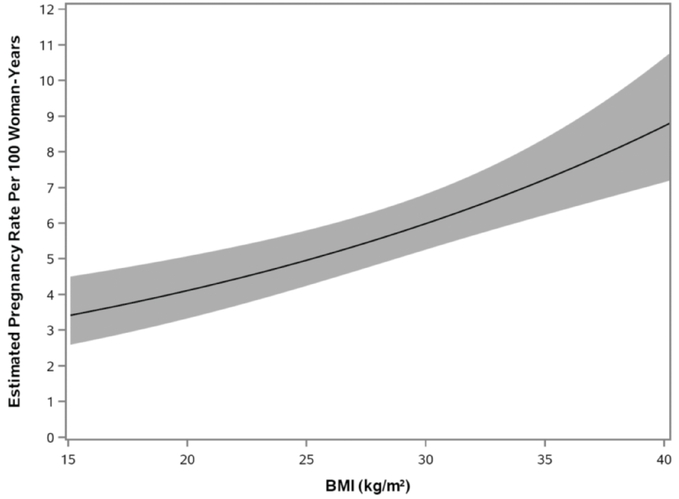

Twirla was approved for sale in the United States on February 14, 2020 as a method of contraception for use in women of reproductive potential with a body mass index (BMI) < 30 kg/m2 for whom a combined hormonal contraceptive is appropriate. Based on the observed relationship between efficacy and BMI in a Phase 3 clinical trial, Twirla's limitation of use instructs healthcare providers to consider Twirla's reduced effectiveness in women with a BMI³ 25 to <30 kg/m2 before prescribing. Twirla is contraindicated in women with a BMI³ 30 kg/m2 because compared to women with a lower BMI, women in this group had reduced effectiveness and may have a higher risk for VTEs.

As part of Twirla's approval, the FDA is requiring us to conduct a long-term prospective, observational post-marketing study comparing the risks for VTE and ATE in new users of Twirla to new users of other CHCs. The FDA's requirement for Twirla is similar to another post-marketing study requirement for a recently approved CHC. The final study report for the Twirla post-marketing study is scheduled to be submitted to the FDA in November 2032, with interim safety data reporting to the FDA due in November 2026. We have also agreed to a small post-marketing commitment PMC study to assess the residual drug content and strength of Twirla. The PMC study is similar to residual drug studies requested of patch developers in the FDA's November 2019 draft guidance entitled Transdermal and Topical Delivery Systems—Product Development and Quality Considerations. We are evaluating the design and cost of these post-marketing studies. With the approval of Twirla we now plan to focus on our transition from a clinical development stage company to a commercial company. During 2020, we plan to begin the implementation of our commercialization plan for Twirla and to manage the growth of our company. Our near-term plan for the commercialization of Twirla includes:

| Activity | Expected Timing | |

|---|---|---|

| Initiate coverage and reimbursement activities in the United States from third-party payors | First Quarter 2020 | |

Initiate hiring of contract sales force | Second Quarter 2020 | |

Complete pre-validation and validation of the commercial manufacturing process consistent with our approved marketing application | Second Half 2020 with first shipment of product anticipated in the Fourth Quarter 2020 |

Our Strategy

Our short-term goal is to establish an initial franchise in the multi-billion-dollar U.S. hormonal contraceptive market built on approval of Twirla in the U.S. Our resources are currently focused on the commercialization of Twirla. To that end, our goal is to begin the pre-validation and validation of the

commercial manufacturing process in the first half of 2020, manufacture three validation batches of Twirla and complete the validation process in the second half of 2020. At the same time, we will prepare for the availability of commercial product supply. In the first quarter of 2020, we plan to initiate work with managed care and patient payors to gain market access for Twirla. In the second quarter of 2020, we plan to begin hiring and training an initial sales team, which we estimate to be in the range of 70 to 100 persons. We intend to ship product to wholesalers in the fourth quarter of 2020. During 2020, we also expect to begin planning the buildout of our existing pipeline and explore other opportunities to add additional products to our business.

Our current priorities are as follows:

Twirla

Twirla is our first and only approved product, indicated as a method of contraception for use in women of reproductive potential with a BMI < 30 kg/m2 for whom a combined hormonal contraceptive is appropriate. Based on the reduced efficacy seen with increasing BMI in a Phase 3 clinical trial, Twirla's limitation of use instructs healthcare providers to consider Twirla's reduced effectiveness in women with a BMI³ 25 to <30 kg/m2 before prescribing. Twirla is contraindicated in women with a BMI³ 30 kg/m2 because compared to women with a lower BMI, women in this group had reduced effectiveness and may have a higher risk for VTEs.

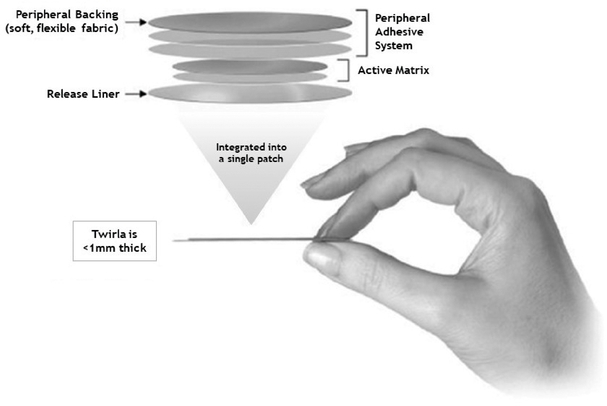

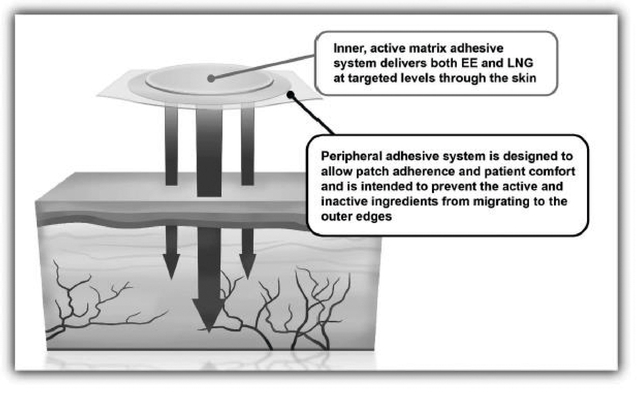

Twirla is a prescription combined hormonal contraceptive, or CHC, patch that contains the active ingredients ethinyl estradiol, or EE, which is a synthetic estrogen, and levonorgestrel, or LNG, which is a type of progestin, a synthetic steroid hormone, both of which have an established history of efficacy and safety in currently marketed combination low-dose, oral contraceptives. Twirla delivers approximately 30 micrograms of EE per day, a dose of EE consistent with the dose delivered by many commonly prescribed oral contraceptives. Our Skinfusion technology allows Twirla to be the first approved patch capable of delivering a contraceptive dose of LNG across the skin. The patch is applied once weekly for three weeks, followed by a week without a patch. Twirla is packaged with three individually wrapped patches per carton to provide for one 28-day cycle of therapy.

Twirla is designed using our proprietary Skinfusion technology to consistently deliver both hormones overfor convenient application by patients as a seven-day period at levels comparable to currently marketed low-dose oral contraceptives.method of contraception. By delivering these active ingredients over seven days, in a comfortable, convenient and easy-to-use weekly patch, Twirla is designed to promotearound principals of ease of use, andwhich may support enhanced patient compliance. It is also designed with properties to optimize patch adhesion and patient wearability with low levels of skin irritation. The patch is applied once weekly for three weeks, followed byround and made of a week withoutsoft, flexible fabric, designed to flex with the movement of a patch. If approved,woman's body. Twirla will be packaged with three patches per carton to provide for one 28-day cycleis a matrix patch consisting of therapy.

We have conducted a comprehensive clinical program, with completed Phase 1, Phase 2, and Phase 3 trials enrolling over 4,100 women, over 3,500several layers of whom received Twirla. Most recently, in December 2016, we completed a Phase 3 trial,material that contain the SECURE trial, in which we enrolled over 2,000 women for up to one year of treatment. In the Phase 1 and Phase 2 clinical trials, we demonstrated that Twirla delivers levels of bothactive ingredients EE and LNG, as well as the inactive ingredients Dimethylsulfoxide, Ethyl

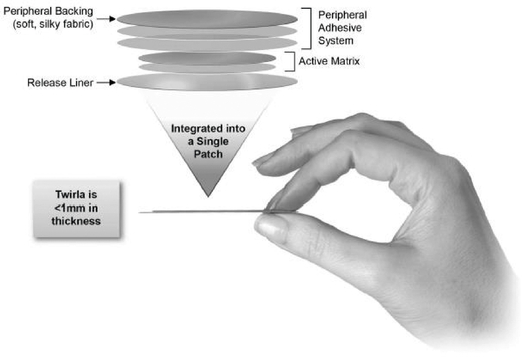

Lactate, Capric Acid and Lauryl Lactate, which are ingredients to assist in the transport of EE and LNG across the skin, and adhesives that enable adherence to the blood stream that are consistent with current low-dose oral contraceptives. Priorskin. The final top layer is the one seen when placed on the skin, and consists of a thin, cloth-like material consisting only of adhesive. There is a barrier formed between the inner portion of the patch, which contains the active ingredients, and the outer portion of the patch, which only contains the adhesive. This barrier is intended to prevent the active and inactive ingredients from migrating to the SECURE trial, we completed twoperipheral portion of the patch and breaking down the adhesive there. Twirla is also designed to help prevent seepage of the adhesives from around the edge of the patch where it could collect dirt and leave a sticky black ring on the skin. The five layers of the patch are integrated to create a patch that has a slim profile and is unobtrusive when applied.

Twirla Marketing Authorization

Twirla received FDA approval on February14, 2020 as a method of contraception for use in women of reproductive potential with a BMI < 30 kg/m2 for whom a combined hormonal contraceptive is appropriate. Based on the reduced efficacy seen with increasing BMI, Twirla's limitation of use instructs healthcare providers to consider Twirla's reduced effectiveness in women with a BMI³ 25 to <30 kg/m2 before prescribing. Twirla is contraindicated in women with a BMI³ 30 kg/m2 because compared to women with a lower BMI, women in this group had reduced effectiveness and may have a higher risk for VTEs.

Pregnancy Rates (Estimated*) in Twirla-Treated Patients as BMI Increases for Women£35 Years of Age in Study ATI-CL23

Twirla's approval is primarily based on safety and efficacy data from the Phase 3 clinical trials that enrolled over 1,900 women inSECURE trial. Because the aggregate for up to 12 months, and we demonstrated that Twirla generally had comparable efficacy and tolerability to an approved low-dose oral contraceptive. In the SECURE trial, we observed positive evidence of efficacy for Twirla based on use for up to one year. In our completed Phase 3 trials to date, over 1000 women have received Twirla for 12 months. Across all completed clinical trials, TwirlaNDA was generally well tolerated and had a favorable safety profile.

We have filed asubmitted under Section 505(b)(2) NDA, for approval of Twirla by the U.S.Federal Food, Drug and Drug Administration,Cosmetic Act, or FDA, which is required before marketing a new drug in the United States. Our 505(b)(2) NDA relies in part on clinical trials thatFDCA, and we conducted andrelied, in part, on the FDA's findings of safety and efficacy from investigations for approved products containing the active ingredientsEE and LNG and published scientific literature for which we have not obtained a right of reference.reference, we were not required to conduct preclinical studies.

The FDA has indicatedSECURE trial was a multicenter, single-arm, open-label, 13-cycle trial that evaluated the safety, efficacy and tolerability of Twirla in a Complete Response Letter, or CRL, that our NDA2,032 healthy women, aged 18 and over, at 102 experienced investigative sites across the United States. The trial was not sufficient for approval as originally submitted. After multiple communicationsdesigned in consultation with the FDA, we have received significant guidance asand incorporated a number of stringent trial design elements, including exclusion of treatment cycles not only for use of back-up contraception but also for lack of sexual activity. SECURE had broad entry criteria, placed no limitations on body mass index, or BMI, or other demographic factors during enrollment, and enrolled a large and diverse population from the United States in order to what additional clinical development and other activities needallow for efficacy to be completed priorassessed across different groups. These entry criteria resulted in the inclusion of a substantial number of women with high BMI, who have frequently been under-represented in past contraceptive studies. The efficacy measure for SECURE was the Pearl Index in an intent-to-treat population of subjects 35 years of age and under. The FDA also requested inclusion of pre-specified efficacy analyses related to approval. In accordance with the FDA's adviceBMI and comments, we conducted an additional Phase 3body weight.

clinical trial, As part of Twirla's approval, the SECURE trial, which was initiatedFDA is requiring us to conduct a long-term prospective, observational post-marketing study comparing the risks for VTE and ATE in 2014 and completed in December 2016. We announced the top-line resultsnew users of Twirla to new users of other CHCs. The FDA's requirement for Twirla is similar to another post-marketing study requirement for a recently approved CHC. The final study report for the SECURE trial in January 2017. Based on the guidance that we received fromTwirla post-marketing study is scheduled to be submitted to the FDA in connectionNovember 2032, with our discussions on clinical trial design, we believe thatinterim safety data reporting to the results fromFDA due in November 2026. We have also agreed to a post-marketing commitment, or PMC, study to assess the SECURE trial will address allresidual drug content and strength of the clinical issues raisedTwirla in a minimum of 25 women. The PMC study is similar to residual drug studies requested of patch developers in the CRL.FDA's November 2019 draft guidance entitledTransdermal and Topical Delivery Systems—Product Development and Quality Considerations. We expect to respond toare evaluating the CRLdesign and supplement our NDA with the resultscost of the trial in the first half of 2017, along with additional information relating to the manufacture of Twirla.

We intend to commercialize Twirla in the United States, if approved, through a direct sales force. Obstetricians and gynecologists, or ObGyns, contribute 43% of the U.S. contraception prescription volume, and Nurse Practitioners and Physician Assistants, or NP/PAs, who are often affiliated with an ObGyn practice, contribute an additional 29% of the U.S. prescriptions. We anticipate that a targeted sales force focused initially on ObGyns, NPs, PAs and primary care providers who comprise the top prescribers of contraceptives will be highly effective. We believe that we can address this market with a specialty sales force of approximately 70 to 100 representatives. We also intend to augment our sales force through digital marketing and other techniques to market directly to patients. We will require additional capital for the commercial launch of Twirla, if approved.

Our Skinfusion technology makes Twirla the first patch capable of delivering a contraceptive dose of LNG across the skin, allowing weekly application using a patch that is soft and flexible and is designed to adhere well with low levels of skin irritation. We, along with Corium International, Inc., or Corium, our manufacturing partner, have made a significant investment in a proprietary process to manufacture Twirla. We believe we have developed a robust process to reliably manufacture Twirla on a commercial scale. The materials produced for our clinical trials were manufactured using the same process that we expect will be used for our commercial-scale manufacturing, and we have made a significant investment in equipment for commercial-scale manufacturing if Twirla is approved. We believe that the technical challenges and know-how involved in manufacturing, including proprietary chemistry, production to scale and use of custom equipment and reproducibility, present significant barriers to entry for other pharmaceutical companies who might potentially want to replicate our Skinfusion technology.

Our intellectual property represents an additional barrier to potential competitors. We have thirteen issued U.S. patents, eight of which cover Twirla and that we intend to list in the Orange Book, the last of which expires in 2028, and five that provide additional coverage for other product candidates in our pipeline. The Orange Book lists drug products, including related patent and exclusivity information, approved by the FDA under the Federal Food, Drug, and Cosmetic Act. If a patent is listed in the Orange Book, potential competitors seeking approval of drug products under an Abbreviated New Drug Application, which provides for the marketing of a generic drug product that has the same active ingredients, dosage form, strength, route of administration, labeling, performance characteristics and intended use, among other things, of a previously approved product, or a 505(b)(2) application, for which the listed drug is a reference product, must provide a patent certification in their application stating either that (1) no patent information on the drug product has been submitted to the FDA; (2) such patent has expired; (3) the date on which such patent expires; or (4) such patent is invalid or will not be infringed upon by the manufacture, use or sale of the drug product for which the application is submitted. In addition, we continue to prosecute additional patent applications relating to Twirla, as well as our other product candidates, both in the United States and internationally. The intellectual property behind all of our product candidates in the pipeline and our Skinfusion technology consists of patent families developed and wholly-owned by us. There are no royalties or payments owed to third parties on our Skinfusion technology or any of our product candidates.

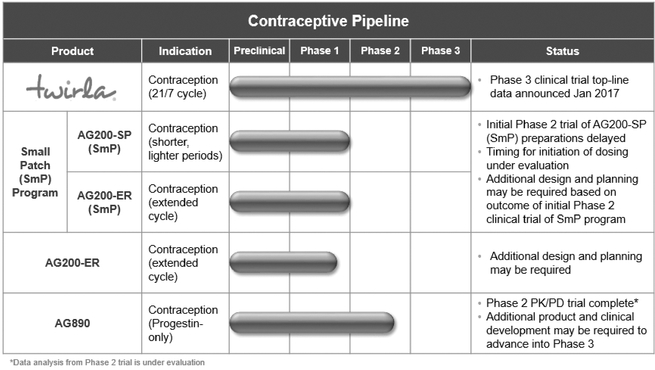

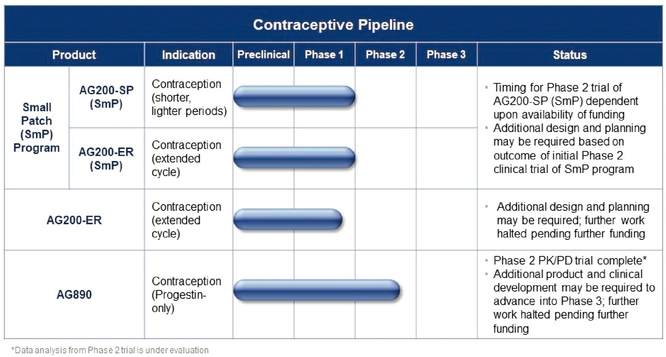

In addition to Twirla, we plan to develop a pipeline of other new transdermal contraceptive products, including AG200-ER, which is a regimen designed to allow a woman to extend the length of her cycle, AG200-SP, which is a regimen designed to provide shorter lighter periods, AG200-ER (SmP), which is a regimen designed to allow a woman to extend the length of her cycle and experience shorter,

lighter periods, and AG890, which is a progestin-only contraceptive patch intended for use by women who are unable or unwilling to take estrogen. Substantially all of our resources are currently dedicated to developing and seeking regulatory approval for Twirla. We will require additional capital to advance the development of our other product candidates.

Backgroundthese post-marketing studies.

Hormonal Contraception Overview

A woman is biologically capable of pregnancy from the time of her first menstrual cycle, at the average age of 12.6 years, to natural menopause, at the average age of 51.3 years. This is nearly half of a typical woman's lifespanContraceptive Landscape and for the typical woman, the majority of this time frame is spent trying to avoid pregnancy or is characterized by no desire to become pregnant. Nearly half of the pregnancies that occur each year in the United States are unplanned. The United States was the first country to approve a hormonal contraceptive, with the approval of the first contraceptive pill in 1960. The latest data from 2011 to 2013 from the Centers for Disease Control, or CDC, indicate that approximately 28% of women aged 15 to 44 use some form of hormonal contraception, which amounts to approximately 17 million U.S. women.

Hormonal contraceptives are composed of synthetic estrogens and progestins. Contraceptives containing both estrogen and a progestin are referred to as CHCs, and contraceptives containing only progestin are referred to as P-only. There are three synthetic estrogens approved in the United States for use in contraceptive products: EE, mestranol and estradiol valerate. EE has been available for over 40 years and is the estrogen component in nearly all CHCs today. There are 10 different progestins that have been used in contraceptives sold in the United States. The progestin component provides most of the contraceptive effect, while the estrogen component primarily provides cycle control, for example, minimizing bleeding or spotting between cycles. The progestin exerts its contraceptive effect by inhibiting ovulation, or release of an egg from the ovary, and by thickening cervical mucus. Thickening cervical mucus helps to prevent sperm entry into the upper genital tract. The estrogen component, in addition to providing cycle control, makes a small contribution to contraception by decreasing the maturation of the egg in the ovary.

Hormonal contraceptives are generally well-tolerated and are generally safer than pregnancy. A risk associated with hormonal contraceptives is a rare but serious adverse event called venous thromboembolism, or VTE, which involves the formation of a blood clot in a vein. VTEs can be life-threatening, and typically present as either deep vein thrombosis or pulmonary embolism. Evidence supports that the increased risk of VTE in CHC users is dependent upon the estrogen dose and duration of use. Estrogen increases formation of clotting factors in the liver and decreases production of elements that promote breakdown of blood clots. Most experts believe that progestins on their own have minimal to no impact on the clotting system, but some progestins, when combined with estrogen, can increase estrogen's effect on the clotting system.

The likelihood of a woman spontaneously developing a VTE is extremely low and the use of combination oral contraceptives, or COCs, increases the incidence only slightly, and less than

Table of ContentsMarket Opportunity

pregnancy. Epidemiologic studies evaluated by the FDA have demonstrated the incidence of VTE in women based on pregnancy or use of COCs as follows:

| ||

| ||

| ||

| ||

The available progestins are commonly categorized into generations, based on their history of introduction in the United States. The first and second generation progestins, including LNG, have been available in contraceptive formulations in the United States for over 25 years. The third and fourth generation progestins, for example desogestrel and drospirenone, respectively, were introduced to reduce androgenic side effects, such as oily skin and acne. Epidemiologic data suggest that CHCs containing third and fourth generation progestins are associated with an increased risk of VTE as compared to those containing the second generation progestin, LNG.

Effectiveness of Hormonal Contraceptives

For the purpose of FDA approval, contraceptive effectiveness is measured by a calculation called the Pearl Index, or PI and its associated 95% confidence interval (CI). The PI is a measure of the rate of pregnancies over a specific period of time in a clinical trial, and is expressed as the number of pregnancies per 100 woman years, or WY, of use. Each cycle lasts 28 days, so there are approximately 13 cycles in one year. According to recent FDA guidance, the PI calculation typically includes all pregnancies for which conception is estimated to have occurred while the subject was using the drug (i.e., on-treatment pregnancies), but only includes cycles where the woman indicates that she engaged in sexual activity and did not use backup contraception, such as a condom, and where she has completed a study diary. The PI values from clinical trials are affected by several factors, including differences in study design, increased sensitivity of early pregnancy tests, weight and body mass index, or BMI, of the study population, user experience and inconsistent or incorrect use of the contraceptive method. In addition, there has been an observable trend in PIs for approved combined hormonal contraceptives demonstrating an increase in the PIs over time, believed to be related to changes in study design and study populations. The FDA has not established any regulatory guidance on specific parameters for an acceptable PI or CI to support approval.

The contraceptive failure rates observed in clinical trials are generally lower than those seen once a CHC is approved and in use by a broad population, referred to as typical use, without the close monitoring of a clinical trial setting. There is a large difference in pregnancy rates under conditions of perfect use, where the method is used following the directions exactly, and typical use. For example, for CHCs, including oral contraceptives, the vaginal ring and the transdermal patch, the percent of women experiencing an unintended pregnancy during the first year of use is 0.3% for perfect use and 9.0% for typical use.

U.S. Hormonal Contraceptive Market Background

Contraceptive methods, other than sterilization, can be divided into non-hormonal and hormonal alternatives. Examples of non-hormonal products available in the United States include the diaphragm,

male condom, female condom, and female condom.non-hormonal intrauterine device, or IUD. Hormonal contraceptives containing both estrogen and a progestin are referred to as CHCs, and contraceptives containing only progestin are referred to as P-only. There are several categories of hormonal contraception products available in the United States, including:

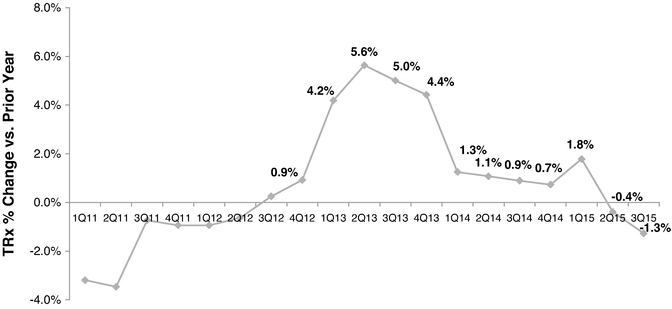

The U.S. hormonal contraceptive market recorded annual sales in 2016is a multi-billion-dollar market. Data from 2011 to 2013 from the Centers for Disease Control, or CDC, indicate that approximately 28% of women aged 15 to 44 use some form of hormonal contraception, which amounts to approximately $5.5 billion, according to IMS Health.17 million U.S. women. The CHC portion of the market, consisting ofwhich includes pills, atwo transdermal patchpatches, including Twirla, and atwo vaginal ring,rings, generates significantly greater prescription volume and sales compared to the P-only portion of the market, consisting of IUDs, injectables, implants, and P-only pills. In 2016, IMS Health reported total U.S. sales of $3.9 billion for the CHC market and $1.6 billion for the P-only market. Twirla is a CHC and, if approved, we believe it will compete primarily with products in the CHC market.

The U.S. hormonal contraceptive market is a mature market, with many branded and generic products available. InSince the past 10 years, themid-2000s, CHC market growth was flat to declining as measured by prescription volume (TRx) has been flat to declining, with the exception of a 4.8% increase in 2013 compared to 2012. In the past three years (2017-2019), while CHC TRx growth has appeared to decline more aggressively (by 6%-12% per year), we believe this is largely due to an increase in the average TRx size (i.e. number of contraceptive cycles dispensed per TRx), which has increased from 1.4 cycles/TRx in 2016 to 1.7 cycles/TRx in 2019. The average annualtotal cycles dispensed in 2018 and 2019 has remained relatively stable reflecting the continued flat growth rate in dollarof this mature market. While gross sales were relatively flat between 2014 and 2018 due to a lack of new product entries and increased generic competition for the five years ended December 31, 2016 was 1.0% forboth the total hormonal contraceptive market and –0.7% for the CHC market. Market growthmarket, CHC market sales grew by 5.9% in gross sales is primarily2019 vs. 2018 to a total of $4.1 billion, largely due to price increases amongst branded products.increases.

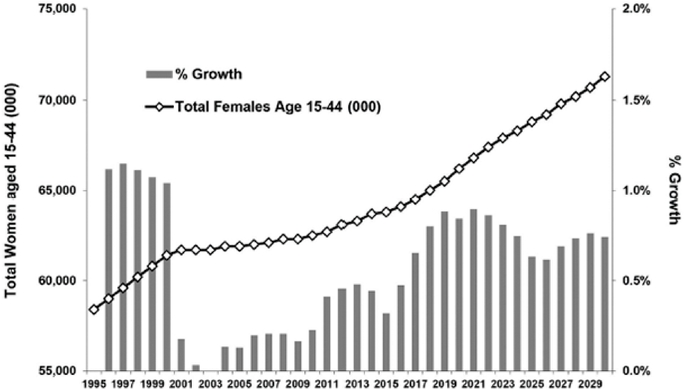

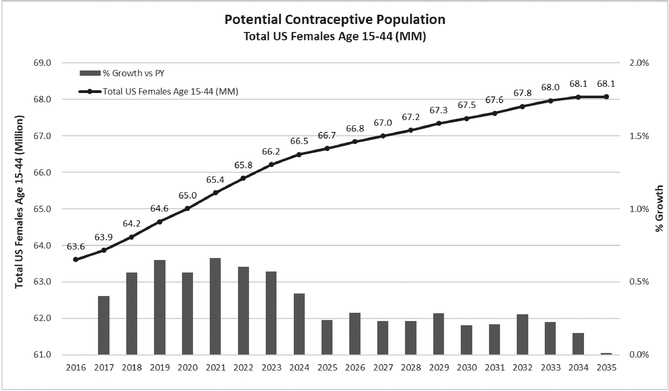

We believe there are twoseveral possible factors primarily affecting prescription volume growth in the contraceptive market. First, accordingAccording to U.S. Census Bureau data and projections, the population of women

aged 15 to 44 years has been growing at a rate of approximately 0.4%0.3% to 0.5%0.9% per year since 2011, increasing this population by 250,000approximately 200,000 to 300,000580,000 women per year.

Contraceptive Population(Total women aged 15-44 yrs)

Source:

Second,Additionally, in 2010, the Patient Protection and Affordable Care Act, as amended by the Healthcare and Education Reconciliation Act, or collectively, the ACA, was signed into law, which, among other things, requires all health plans, with limited exceptions, to cover certain preventive services for women with no cost-sharing, which means no deductible, no co-insurance and no co-payments by the patient, effective August 1, 2012. These services include those set forth in the Guidelines for Women's Preventive Services, or HRSA Guidelines, and adopted by the U.S. Department of Health and Human Services Health Resources and Services Administration. Contraceptive methods and counseling, including all FDA approved contraceptive methods as prescribed, are included in the HRSA Guidelines. Since these new ACA provisions went into effect in August 2012, quarterly prescription volume growth for the CHC market rose from negative growth year-on-year to positive growth between 4.0% and 5.0% for each of the six quarters following implementation. However, this appears to be a one-time phenomenon, as the market volume growth fell to 0.8%has been relatively flat since 2014, with the exception of a one-time drop in 2014 and –0.9%TRx cycles dispensed in 2015.2017.

Effect of ACA on Market Growth

During the period following enactment of the ACA, generic oral contraceptives havecontraceptive volume has shown the greatest growth, primarily at the expense of branded oral contraceptives. This is likely due to the policies that were implemented by many managed care plans, which generally only provided generic oral contraceptives with no cost-sharing to the patient. The effect on non-oral products is less clear, but prescription volume for the vaginal ring showed a 5.1%6.8% decline from 20132015 to 2015,2019, while the prescription volume for the patch increased by 15.0%31% over the same time period. In May 2015, several government agencies, such asincluding the U.S. Department of Health and Human Services, or HHS, the Department of Labor, or DOL, and the U.S. Department of Treasury, or Treasury, jointly issued a clarification in the form of an FAQ which clarified the requirements for coverage of contraceptives under the ACA. The FAQ states

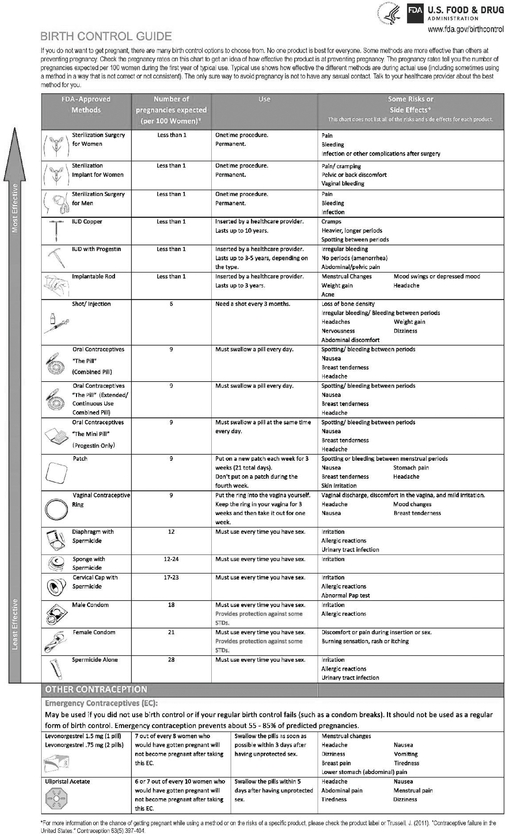

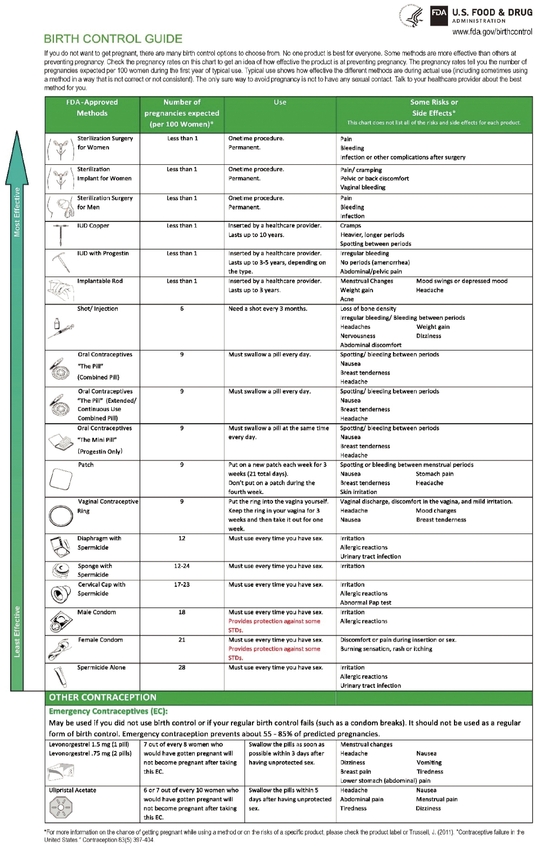

that plans and issuers must cover without cost-sharing at least one form of contraception in each of the 18 current methods that the FDA has identified for women in its current Birth Control Guide. The patch is identified as a specific method in the FDA Birth Control Guide, and therefore insurers must cover at least one patch product with no cost-sharing to the patient. Because this clarifying guidance is applied for plan years (or in the individual market, policy years) beginning on or after 60 days from the date of publication of the FAQs, patients did not have the benefit of this clarification until their new plan year, which generally started in January 2016.

In March 2017, the U.S. Congress proposed legislation, which, if signed into law by the new administration, would repeal certain aspects of the ACA. Further, on January 20, 2017, the new administration signed an Executive Order directing federal agencies with authorities and responsibilities under the ACA to waive, defer, grant exemptions from, or delay the implementation of any provision of the ACA that would impose a fiscal or regulatory burden on states, individuals, healthcare providers, health insurers, or manufacturers of pharmaceuticals or medical devices, among others. Congress also could consider subsequent legislation to repeal and replace elements of the ACA that are repealed. Therefore, it is difficult to determine the full effect of the ACA or any other healthcare reform efforts on our business. We will continue to monitor the healthcare reform efforts. We believe the CHC market will maintain a long-term neutral to slightly positive annual growth rate in line with contraceptive population growth.

In spite ofDespite the availability of generic contraceptives for over 25 years, branded products have maintained a significant, though declining, share of the CHC market, with 55% of dollar sales and 17% of prescriptions for 2016.sales. Branded contraceptives in the CHC market have driven significant increases in the value of branded total prescriptions, or TRx. In the five years ended December 2016,2019, the average annual price increase among the top branded products was 10.6%10.5%. The average price per cycle, referred to as the wholesale acquisition cost, or WAC, for a single 28-day cycle of the top branded products was $41.53 in 2006 and rose to $131.40$160.88 by December 2016.2019. As of October 2014, the branded CHC transdermal patch (Ortho Evra) has been discontinued, and the generic CHC transdermal patch (Xulane) is currently priced at $105.92$122.15 per cycle. The other non-oral form of CHC, the vaginal ring, is currently priced at $128.21$162.63 per cycle. We cannot predict whether the manufacturers of branded products will continue to increase prices going forward,forward. We have not yet set a WAC price for Twirla, but we believe we will be able to set a WAC price for Twirla, if approved,one that is comparable to other branded and branded generic CHC products at the time of launch. Based on IMS Health data, we estimate that each percentage point of market share of CHC total prescriptions in the United States currently represents approximately $166 million of annual gross sales potential for Twirla, if approved.

Contraceptive Pills

Based on 2014 data from the CDC, of women who choose to use a hormonal contraceptive, approximately 64% use thea contraceptive pill, vaginal ring or patch, the majority of whichwhom use the contraceptive pill. The remaining 36% of women using hormonal contraception are split between using injectables, implants, or IUDs. Based on this information, we believe that contraceptive pills are the most popular choice because:

However, compliance remains a significant draw-back with pills. Published studies have shown that the average woman who uses oral contraceptives misses approximately two to four pills per month, which increases the potential for unintended pregnancies. We believe that a patch can offer greater convenience than a pill, as it does not require daily administration and, for certain women, could lead to greater compliance and ease of use.

Contraceptive Patch Market Experience

The Ortho Evra® contraceptive patch, or Evra, was introduced in early 2002 and was the first FDA-approved contraceptive patch. The initial approved labeling for Evra indicated that it delivered a daily EE dose of 20 micrograms. Evra had rapid uptake in the contraceptive market and achieved a 10% share of the CHC market by September 2003. Following FDA approval of Evra, users of Evra began to report thrombotic and thromboembolic events to the FDA. Johnson & Johnson, the manufacturer of Evra, revised the Evra labeling in November 2005 to include information that EE exposure with Evra is 60% higher than that of an oral contraceptive containing EE of 35 micrograms, based on area under the curve, a commonly-used metric for measuring EE exposure in contraceptives. This information was ultimately included in a black boxan addition to the boxed warning and bolded warningsthat was unique to the Evra label. The Evra market share declined rapidly following the labeling changes, from a peak share of 11% in 2005, to 4% by the end of 2006, to 1.4% by the end of 2013, where it stabilized, with a 1.5% share of the market based on combined prescriptions for Evra and its generic equivalent (Xulane®) in 2014. In the past two years, the patch share of the CHC market grew slightly, with a 1.6% TRx share in 2015 and 1.7% TRx share in 2016.

2014. In more recent years, the Xulane share of the CHC market TRx has grown, with a 1.8% share in 2017, 2.4% share in 2018, and 2.4% share in 2019.

In April 2014, Mylan Inc. announced the launch of Xulane™,Xulane®. In recent years, the Xulane share of the CHC market has grown slightly, with a generic version of Evra.1.7% TRx share in 2016 and 1.8% TRx share in 2017. Generic pharmaceutical products are the chemical and pharmaceutical equivalents of the brand or a reference listed drug, or RLD. Generic drugs are bioequivalent to their reference brand name counterparts. Bioequivalence studies compare the bioavailability of the proposed drug product with that of the RLD product containing the same active ingredients. Bioavailability is a measure of the rate and extent to which the active ingredient is absorbed from a drug product and becomes available at the site of action. Under pharmacy dispensing rules governed by state law, depending on the state, if an automatic generic substitute is introduced, the pharmacist may dispense either the prescribed product, or they may replace it with an equivalent generic without being required to inform the patient or healthcare professional. In addition, the FDA offers a 180-day exclusivity period for generic products in specific cases. The first generic applicants to submit a substantially complete Abbreviated New Drug Application containing a paragraph IV certification to a listed patent are protected from competition from other generic versions of the same drug for the 180 days. As of December 2016, no other generic equivalents to Evra have been introduced.

The FDA has maintained, in spite of the wording in the labeling for Evra, which has been discontinued, and its approved branded generic, that none of the epidemiologic studies to date provides a definitive answer regarding the relative risk of VTE with Evra compared to combined oral contraceptive use or whether the increased risk that some studies demonstrated is directly attributable to Evra. An advisory committee for the FDA stated that the benefits of Evra outweigh the risks. In its denial of a Citizen's Petition calling for the withdrawal of Evra, the FDA followed the committee's recommendations stating that the increased VTE risk does not warrant removal from the market, and that the labeling revisions to the Evra label provide a sufficient update and guidance on the interpretation of the epidemiologic data about the risk of VTE with Evra. In spite of the labeling changes, and Johnson & Johnson ceasing promotion of Evra in 2007, Evra and its generic equivalent generated $211 million in gross sales in 2016.continue to generate significant sales.

With its approval on February 14, 2020, Twirla is now the only other transdermal contraceptive patch approved by the FDA. We believe that the rapid uptake and acceptance of Evra upon its introduction demonstrates that there is an unmetand its (and Xulane's) continued sales over the past several years demonstrate a market needopportunity for amultiple choices in transdermal patch as a contraceptive option. Also, the epidemiologic data on VTE risk suggest that there is a need for a contraceptive patch that delivers both a low dose of EE similar to oral contraceptives and a first or second generation progestin.patches.

Our Product CandidatesTwirla Potential Market Share

EachThree of our market research studies have included an allocation exercise to estimate the potential uptake of Twirla and peak market share. In all of these studies, ObGyns and nurse practioners, or NPs, indicated their allocation of contraceptive prescriptions before and after reviewing a product candidates utilizesprofile like Twirla that reflects the safety and efficacy results from our proprietary Skinfusion technology,SECURE clinical trial. In the 2010 study, which is designed to provide advantages over the currently available patch. Skinfusion is designed to deliver contraceptive levels of hormoneswas conducted prior to the blood stream throughimplementation of the skin overACA, ObGyns estimated use of a seven-day period. It is also designed to optimize patch adhesion and patient wearability. Our lead product candidate islike Twirla a prescriptionin 17% of their CHC patch which contains both EE and LNG and is designed to deliver a low dose of EE and LNG comparablepatients. A proprietary calibration model developed by the research firm was applied to the total dose delivered with low-dose oral contraceptives.peak share estimate, to adjust for physician overstatement, resulting in an estimated peak market share of 9% of the CHC market. In addition to Twirla, we plan to develop a pipeline of other new transdermal contraceptive products, including AG200-SP, which is a regimen designed to provide shorter, lighter periods; AG200-ER, which is a regimen designed to allow a woman to extend the length of her cycle; AG200-ER (SmP), which is a regimen designed to allow a woman to extend the length of her cyclestudy completed in December 2016, ObGyns, NPs, and experience shorter, lighter periods; and AG890, which is a progestin-only contraceptive patch intended for use by women who are unablephysicians assistants, or unwilling to take estrogen. AG200-SP, AG200-ER, and AG200-ER (SmP) are intended to be Twirla line extensions that would expand thePAs, estimated use of Twirla beyond its initial, approved use. In July 2016, we began preparationsin 22% of their CHC patients, which was also calibrated to adjust for overstatement, resulting in an initial Phase 2 clinical trial examiningestimated peak market share of 14% of the CHC market. This estimate was confirmed in our most recent study completed in September of 2019, in which ObGyns and NPs/PAs estimated use of AG200-SP along with a smaller lower-dose combination ethinyl estradiol/levonorgestrel patch (SmP)Twirla in the fourth week20% of their CHC patients, calibrated to 14% of the woman's cycle. The Phase 2 clinical trial is aimed at identifying the optimal dose of the SmP, and will evaluate bleeding profiles, pharmacokinetic parameters, ovulation inhibition and safety over three cycles of treatment with AG200-SP (SmP).CHC market.

We have decided to postpone the trial and will continue to evaluate the timing for

initiating dosing of subjects for this Phase 2 clinical trial, which is dependent on financial and other capital resources.

The National Institutes of Health, through a clinical trial agreement with us, conducted a Phase 1/2 trial with AG890. The Phase1/2 study was a multicenter study to evaluate the pharmacokinetics, safety and mechanisms of potential contraceptive efficacy of AG890. The trial is complete and we continue to evaluate the findings. After we complete our evaluation, we may need to perform additional patch development work to determine the optimal formulation and dose to advance to Phase 3. Based upon a number of factors, including, but not limited to, our available capital resources and feedback from the FDA, we continue to review the clinical path and budgetary requirements for each of AG200-SP, AG200-ER and AG890.

Our current product candidate pipeline is summarized in the graphic below:

Substantially all of our resources are currently dedicated to developing and seeking regulatory approvalcommercial opportunity for Twirla. We will require additional capital to advance the development of our other product candidates.

Twirla Product Overview

Twirla is a CHC patch which contains both EE and LNG. Twirla is designed to address an unmet medical need for increased compliance and improved ease of use as compared to oral contraceptives. A single Twirla patch delivers the active ingredients LNG and EE over a seven-day dosing interval, and thereby eliminates the need to take a daily pill as is necessary with an oral contraceptive. Twirla uses a traditional 28-day contraceptive regimen, where one patch is applied weekly for three consecutive weeks and then there is a fourth, patch-free week in each 28-day time period. Twirla may be applied to the buttock, abdomen or upper torso, but not the breast. In clinical trials reported to date, women most frequently chose the buttock and abdomen for patch placement. The exact patch location needs to be rotated with each patch change. Twirla has demonstrated a therapeutically equivalent pharmacokinetic profile when worn on the buttock, abdomen or upper torso. A drug's pharmacokinetic

profile refers to the specific way in which a given drug is handled by the body over time, reflecting the particular patterns of absorption, distribution and elimination of the drug in the body.

Twirla is designed to be highly appealing to patients as a method of contraception. The patch is round and made of a soft, flexible, silky fabric, designed to flex with the movement of a woman's body. Twirla is a matrix patch consisting of several layers of material that contain the active ingredients EE and LNG, as well as the inactive ingredients Dimethylsulfoxide, Ethyl Lactate, Capric Acid and Lauryl Lactate, which are ingredients to assist in the transport of EE and LNG across the skin, and adhesives that enable adherence to the skin. The final top layer is the one seen on the skin, and consists of a thin, silky material consisting of only adhesive. There is a barrier formed between the inner portion of the patch, which contains the active ingredients, and the outer portion of the patch, which only contains the adhesive. This barrier is intended to prevent the active and inactive ingredients from migrating to the peripheral portion of the patch, and from breaking down the adhesive in that portion of the patch. Twirla is also designed to help prevent seepage of the adhesives from around the edge of the patch where it could collect dirt and leave a sticky black ring on the skin. The six layers of the patch are integrated to create a patch which has a slim profile, and is unobtrusive when applied. The results of multiple clinical trials suggest that Twirla delivers the active ingredients needed for contraception over a

seven-day period and that it remains adhered to the skin of most subjects for the full seven-day period, even under conditions of heat, humidity, showering, exposure to water and vigorous exercise.

Twirla Patch Profile

The following table compares Twirla with the Evra product and its generic equivalent, Xulane, as stated in their labels, based upon publicly-available information regarding the products and the characteristics of Twirla and other Twirla attributes observed in our completed Phase 3 clinical trials. We have not performed a head-to-head comparison of Twirla to Evra.

| ||||

| ||||

| ||||

| ||||

| ||||

|

|  |

Twirla employs our Skinfusion patch technology, resulting in a unique appearance and feel of the patch. Evra/Xulane does not utilize our Skinfusion technology; its active ingredients and adhesives are dispersed to its edges. One frequent complaint about patches that do not utilize Skinfusion is that they collect dirt and lint and may leave a sticky black ring of residue on the skin which can be difficult to remove. We do not have any direct comparison of the appearance of the patch on the skin at the end of seven days between Twirla and Evra/Xulane, but we believe, based on anecdotal feedback from our clinical trial investigators, as well as based upon the differences in the design of the patches, that Twirla may have an advantage in this regard.

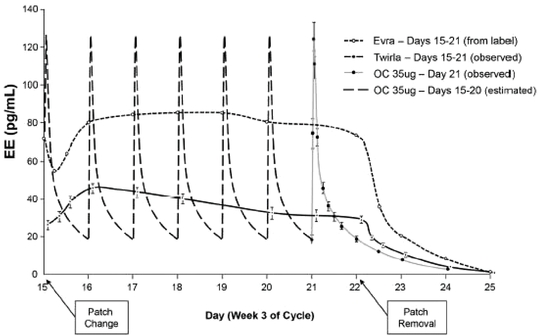

We have not performed a head-to-head comparison of Twirla to Evra/Xulane, however, a pharmacokinetic study that we conducted with Twirla was similar in design to the pharmacokinetic study conducted with Evra that provided the information regarding the daily amount of EE delivered that is currently in the Evra/Xulane package insert. The figure below combines the results for average EE concentrations from these two studies, and suggests a comparison of the observed blood concentration of EE for Twirla versus Evra versus observed and estimated data for the pill. The lower amount of EE delivered from Twirla as compared to Evra can be observed. If Twirla is approved by the FDA, we will not be able to make direct comparative claims regarding the safety, efficacy or pharmacokinetics of Twirla and Evra/Xulane, since none of our completed clinical trials studied Twirla in a head-to-head comparison with Evra/Xulane.

The Evra curve presented in the graphic above was estimated based on the graph provided in the Evra label. In the legend to the figure above, "OC" refers to an oral contraceptive containing 35 micrograms of EE. The OC data prior to Day 21 are estimated steady-state data based on Day 21 EE concentrations observed during our pharmacokinetic study.

Twirla contains LNG, which is the progestin used as the reference standard when comparing risk of VTE between progestins. Evra/Xulane contains the progestin norelgestromin, which is a prodrug of norgestimate, a second generation progestin that has not demonstrated an increased risk of VTE independent of EE. We do not expect any meaningful clinical differences between Twirla and Evra/Xulane based on the progestin component, but our market research with ObGyns has demonstrated that they perceive LNG to be one of the safest progestins available.

Twirla Product Profile

Assuming approval of our marketing application by the FDA based on the results of the SECURE trial, we believe the clinical trial data from the SECURE trial for Twirla will support our future marketing of Twirla as follows:

Twirla Clinical Development Program

Clinical Trials Completed prior to SECURE

Our clinical program includes three Phase 1 studies, one Phase 2 study, and three Phase 3 studies, as well as other supporting studies. In December 2016, we completed our third Phase 3 clinical trial, SECURE, in response to FDA comments and guidance. In Phase 1 and Phase 2 clinical trials, we demonstrated that Twirla delivers levels of both EE and LNG to the blood stream that are consistent with currently marketed low-dose oral contraceptives. In our Phase 3 clinical trials completed prior to SECURE, we demonstrated that Twirla was comparable to an approved low-dose oral contraceptive in two randomized studies, one that enrolled over 1,500 women over 12 months and the other that enrolled over 400 women over six months. Across all completed clinical trials, Twirla was generally well-tolerated and had a favorable safety profile. Because we relied, in part, on the FDA's findings of safety and efficacy from investigations for approved products containing EE and LNG and published scientific literature for which we have not obtained a right of reference, we were not required to conduct preclinical studies. In the pharmacokinetic study comparing Twirla to an approved low-dose oral contraceptive, results demonstrated that Twirla delivers a daily dose of EE that results in estrogen exposure similar to low-dose oral contraceptives containing approximately 30 micrograms.

Our two Phase 3 trials completed prior to SECURE enrolled over 1,900 subjects to evaluate the safety and efficacy of Twirla. Each of these studies included an active comparator arm with an approved low-dose oral contraceptive. The results of these studies demonstrated that Twirla was generally well-tolerated, with levels of adverse events generally comparable to those of low-dose oral contraceptives. In these studies, subjects had a higher rate of self-reported compliance when using the patch as compared with the group using oral contraceptives. However, as discussed further below, the FDA issued a CRL in response to our marketing application for Twirla and requested an additional Phase 3 study and additional chemistry manufacturing and control, or CMC, information. The results of our prior clinical trials demonstrated that approximately only 3% of patches became completely detached from the skin of subjects during the seven-day period, and that the patch generally remained adhered to the skin even when exposed to normal daily activities and conditions such as showering, swimming and other forms of exercise, heat and humidity.

More specifically, our safety population included subjects who received at least one dose of Twirla or COC. In the combined safety population of our two Phase 3 trials completed prior to SECURE, there were a total of 22 serious adverse events, or SAEs, of which 16 were from the Twirla cohort, which had approximately 2.3 times as many subjects as the oral contraceptive comparator cohort. Three of these SAEs (0.2% of the overall Twirla safety population) were considered to be possibly related to the study drug and included one drug overdose with Benadryl®, one case of uncontrollable nausea and vomiting and one instance of upper extremity deep vein thrombosis. In addition to the SAEs described above, some subjects taking Twirla experienced non-serious adverse events, such as nausea, headache, application site irritation and breast tenderness. Subjects receiving the oral contraceptive comparator also generally experienced similar non-serious adverse events such as nausea, headache, and breast tenderness, though at different rates. We believe that Twirla will have a label consistent with all

marketed low-dose CHC products, which include class labeling that warns of risks of certain serious conditions, including venous and arterial blood clots, such as heart attacks, thromboembolism and stroke, as well as liver tumors, gallbladder disease and hypertension, and a black box warning regarding risks of smoking and CHC use, particularly in women over 35 years old who smoke.

In our Phase 3 trials, the primary measure of efficacy is the Pearl Index, or PI, which is calculated based on the number of observed on-treatment pregnancies and total number of on-treatment cycles during the study. Specifically, the PI is expressed as the number of pregnancies per 100 WY of use. The pooled PI value in the previously completed Phase 3 trials for the Twirla patch was 5.76 and for the combined oral contraceptive control arms was 6.72, which were higher than the range of 1.34 to 3.19 in pivotal studies conducted on products approved by the FDA in the previous ten years. In addition, the upper bound of the associated confidence intervals were higher than those seen in clinical trials used for registration of other approved hormonal contraceptives.

We believe that the results for bothpotential new CHC users who are within Twirla's approved indication represent a significant population of women. Based on the patchCompany's market research, analysis of the current and oralexpected future U.S. contraceptive control armsmarket, and review of other product launches in the two Phase 3 trials completed priorcategory, the Company estimates that Twirla can potentially achieve a peak market share of 5-8%. As we prepare for the commercialization of Twirla, we will continue to SECURE were affected primarily by issues with study conduct at several study sites, including rapid enrollment which led to inability to manageanalyze the study population, poor subject compliance,contraceptive market and high rates of loss to follow-up. In the larger ofupdate our Phase 3 trials completed prior to SECURE, 96 sites enrolled subjects, 60 of which had no on-treatment pregnancies. Nineteen percent of the on-treatment pregnancies reported during this trial came from one site. This site represented approximately 8% of the randomized subject population. Thirty six percent of on-treatment pregnancies were reported at four of the 96 sites. These four sites represented approximately 15% of the randomized subject population.

Experts agree that the characteristic most likely to impact contraceptive failure and pregnancy rates is the subject's likelihood of using a method inconsistently or incorrectly. Consistent with expert opinions, our analyses have suggested that the resultsmarket research for both the patch and oral contraceptive control arms in the two Phase 3 trials completed prior to SECURE were also affected in part by the study population, which comprised a disproportionately high number of new users and minority subjects, known to be at higher risk of noncompliance and pregnancy, as compared to the majority of other recent CHC clinical trials which have gained approval in the United States.

Individuals who immediately switch from one hormonal contraception method to another, referred to as current users, or who have recently used another method of hormonal contraception, are less likely to experience contraceptive failure than a new user because they are less likely to have inconsistent or incorrect use. These experienced subjects are often selected for trial participation because their inclusion will lower failure rates. Indeed, many contraceptive trials have enrolled a high proportion of these subjects. Direct comparisons across multiple trials are limited by differences in study design and population, as well as differences in definitions of user status; however, as shown in the table below, some comparisons are possible. For example, when compared against trials that captured current hormonal contraceptive use, in the larger of our two Phase 3 trials completed prior to SECURE, we had a lower proportion of subjects randomized to receive Twirla that were current users, only 17.8%, reflecting a population with less experience using hormonal contraception, compared to two recently approved hormonal contraceptives. When compared against trials that categorized subject experience more broadly by their use of hormonal contraception within the 6 months prior to enrollment, our trial also had a lower proportion of experienced subjects, only 44%. In both the COC and Twirla groups, new users had approximately three times the rate of noncompliance compared to experienced users, as verified through blood tests revealing non-detectable blood levels of EE and LNG. Similarly, the pooled PI values from our two Phase 3 trials completed prior to SECURE were more than twice as high among new users compared to experienced users, and in the primary efficacy analysis population there were no pregnancies observed in current users of other hormonal contraception who immediately switched to the patch upon entry into the trial.

In addition, our two Phase 3 trials completed prior to SECURE also included a higher proportion of black and Hispanic subjects than most recent hormonal contraceptive trials. Although the underlying reasons are not well-understood, several articles in medical journals, such asContraception and theAmerican Journal of Obstetrics & Gynecology, and in at least one report by HHS, state that contraceptive failure rates are highest in black and Hispanic subjects. In our two Phase 3 trials completed prior to SECURE, rates of laboratory-verified noncompliance were substantially higher in blacks and Hispanics compared to non-Hispanic white subjects in the larger of our Phase 3 trials, and as shown in the table below, there were substantially higher PI values in the black and Hispanic subpopulations than in non-Hispanic white subjects. Additionally, as shown in the table the observed PI values were more dramatically increased for new users who were also black or Hispanic.

Study Population Demographics in Selected Contraception Trials

| | | Contraceptive Product (Year of Approval) % of subjects in category* | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Parameter | | Twirla | Seasonique (2006) | Yaz (2006) | Lo- Seasonique (2008) | Natazia (2010) | Quartette (2013) | ||||||||||||||

Hormonal contraception use | |||||||||||||||||||||

Current Users | 18 | (a) | — | 60 | (b) | — | 59 | (c) | — | ||||||||||||

Within 6m of enrollment | Yes(d) | 44 | 68 | — | 61 | — | 44 | ||||||||||||||

| No(e) | 56 | 32 | — | 39 | 56 | ||||||||||||||||

Race/ethnicity | Hispanic | 15 | 5 | 5 | 10 | 13 | 11 | ||||||||||||||

| Black | 22 | 11 | 4 | 12 | 7 | 18 | |||||||||||||||

Current user definitions (extrapolated for approved products):

Use within 6 months of enrollment definitions:

Twirla Pearl Indices Stratified By New Users and Minority Subjects

| ||||||

| ||||||

| ||||||

CRL and FDA InteractionsCommercialization Strategy

In February 2013,January 2018, following our receipt of the complete response letter, or CRL, we received a CRL from the FDA indicating that the results from our two completed Phase 3 trials would not be sufficient for approval, and the FDA proposed that we conduct an additional Phase 3 trial. Among the comments expressed in the letter were some regarding the PI values seen in the studies. Specifically, the FDA indicated that the PI values and the upper bound of the associated confidence intervals in the studies, in both the subjects using the Twirla patch and the control arm using oral contraceptives, were higher than seen in clinical trials used for registration of other approved hormonal contraceptives. The confidence interval is a range around a measurement that conveys how precise a measurement is. The FDA recommended that we conduct an additional Phase 3 trial with a simplified clinical trial design and improved study conduct, including site monitoring and data collection procedures. The FDA also requested that we study Twirla in a representative sample of U.S. women who are seeking hormonal contraception, without enrollment restrictions based on demographic characteristics such as contraceptive user status, age, race, ethnicity, and body mass index, or BMI. The FDA also required additional information relating to the laser etching of label information on each patch and required that the patch used in the new trial utilize the same etching as will be used for the commercial product, in order to demonstrate that it does not adversely affect the performance of the patch. Furthermore, the FDA also requested in the CRL additional information on controls and release specifications related to the patch, and manufacturing and control information related to the Drug Master File of one of the raw materials in Twirla.

In October 2013, we met with the FDA and received further guidance on requirements for our planned Phase 3 trial. In addition, we had a follow-up written interaction with the FDA in February 2014 and have received substantial written comments from the FDA in subsequent interactions. We enrolled the first subject in the SECURE clinical trial in the third quarter of 2014, and completed the clinical trial in December 2016. The patches studied in the SECURE trial were laser etched using the same process as2017, or 2017 CRL, we anticipatesignificantly scaled back our preparations for commercialization of Twirla, if approved. Weincluding commercial pre-launch and manufacturing validation activities. With the approval of Twirla, we have continuedbegun to accelerate our commercial activities. In the first quarter of 2020, we plan to

interactinitiate work with managed care and patient payors to gain market access for Twirla. In the FDA on its CMC questionssecond quarter of 2020, we plan to begin hiring and continued additional supportive testing in ordertraining an initial sales team, which we estimate will consist of 70 to respond100 persons. At the same time, we are currently preparing to initiate the FDA's CMC questions.

The SECURE trial,validation of our third Phase 3 Clinical Trial

SECURE, our third Phase 3 clinical trial, was a multicenter, single-arm, open-label, 13-cycle trial that evaluatedcommercial manufacturing process and expect to complete the safety, efficacyvalidation process and tolerability of Twirla in 2032 healthy women, aged 18 and over, at 102 experienced investigative sites across the United States. The design and execution of SECURE was intendedcommence distributing product to address a number of issues identified in the CRL, including but not limited to, improved clinical trial conduct and demonstration of efficacy as measured by an acceptable Pearl Index and related 95% confidence interval in a representative sample of U.S. women who are seeking hormonal contraception, without enrollment restrictions based on demographic characteristics, such as contraceptive user status, age, race, ethnicity, and BMI. The trial was designed in consultation with the FDA, and comprised a number of stringent trial design elements, including exclusion of treatment cycles not only for use of back-up contraception but also for lack of sexual activity. SECURE had broad entry criteria, placed no limitations on BMI or other demographic factors during enrollment, and enrolled a large and diverse population from the United States in order to allow for efficacy to be assessed across different groups, as requested by the FDA. These entry criteria resulted in the inclusion of a substantial number of women with high BMI, who have frequently been under-represented in past contraceptive studies. The efficacy measure for SECURE was the Pearl Index in an intent-to-treat population of subjects 35 years of age and under. The FDA also requested inclusion of pre-specified efficacy analyses related to BMI and body weight.

We began enrollment for SECUREwholesalers in the fourth quarter of 20142020. We will need to raise additional funds to complete these activities, and completedour ability to complete such activities according to our current planned timelines will depend on our ability to successfully raise the clinical trialnecessary capital.

Twirla Promotion Strategy

We have a limited number of sales and marketing employees. We plan to expand our commercial team, but will primarily rely on third-party agencies with experience in December 2016. In January 2017, we announcedcommercializing pharmaceutical products to advance the following highlightscommercialization of the SECURE clinical trial top-line results:

BMI Category | BMI (kg/m2) | % of Trial Population | Pearl Index | Upper Bound of 95% CI | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Normal | < 25 | 39 | % | 3.03 | 4.62 | |||||||

Overweight | 25 - < 30 | 25 | % | 5.36 | 7.98 | |||||||

Obese* | ³ 30 | 35 | % | 6.42 | 8.88 | |||||||

Non-Obese* | < 30 | 65 | % | 3.94 | 5.35 | |||||||

Obese* | ³ 30 | 35 | % | 6.42 | 8.88 | |||||||

The Pearl Index for subjects by minority and ethnicity status was as follows:

Race/Ethnicity | % of Trial Population | Pearl Index | Upper Bound of 95% CI | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

White (not Hispanic) | 66.9 | % | 4.63 | 6.23 | ||||||

African-American | 24.3 | % | 4.05 | 6.69 | ||||||

Hispanic | 19.7 | % | 2.70 | 5.06 | ||||||

Adverse Event | SECURE Trial | Prior Agile Phase 3 Trial* | Ortho Evra Trials** | Quartette Trial** | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Total in Safety Population | 2032 | 1043 | 3322 | 3597 | |||||||||

Headache | 4.3 | % | 3.7 | % | 21.0 | % | 12.2 | % | |||||

Nausea | 4.1 | % | 4.3 | % | 16.6 | % | 6.7 | % | |||||

Breast tenderness/pain/discomfort | 2.0 | % | 1.8 | % | 22.4 | % | 2.2 | % | |||||

Mood swings/changes/depression | 2.7 | % | 2.8 | % | 6.3 | % | 2.9 | % | |||||

Heavy/irregular vaginal bleeding*** | 1.8 | % | 2.1 | % | 6.4 | % | 9.7 | % | |||||

commercial managed care plans. We believe that we can deploy a focused sales force effort targeting the efficacy results observed in SECURE were a reflectionObGyn, NP and PA prescribers who are responsible for approximately 70% of branded CHC prescriptions. In areas of the study populationcountry where it is not efficient to deploy a sales representative, remote promotion can be used to reach these prescribers.