UNITED STATESSECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

TRANSMISSION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

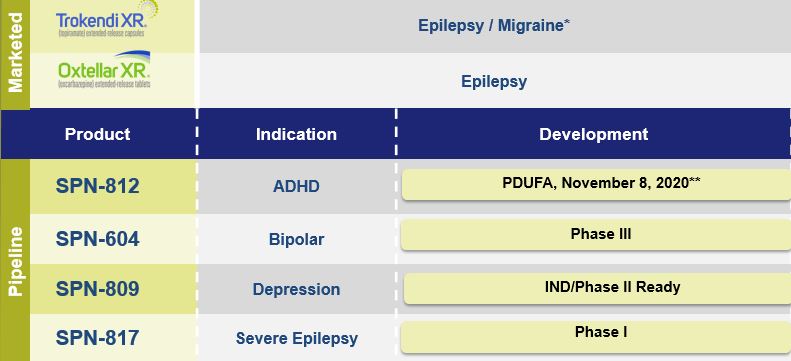

$1,677,874,611. psychiatry. Our extensive expertise in product development has been built over the past 25 years: initially as a Our net product IQVIA care physicians. therapies. Our key proprietary technology platforms include: Microtrol, Solutrol and EnSoTrol. These technologies have been utilized to create approved products; invest in sales and marketing resources for existing and new products; enter into agreements to purchase products or other companies; and invest in support of our business, technology, regulatory and intellectual property portfolio. Epilepsy Overview headaches. this program, because initial studies with immediate release formulations of non-synthetic huperzine A have shown dose-limiting serious side effects. research. We currently employ internal resources to manage our manufacturing contractors. current sales force of over 200 sales representatives is effectively targeting healthcare providers, primarily neurologists, to support and grow our epilepsy and migraine product franchise. Simultaneously promoting two neurology products allows us to leverage our commercial infrastructure and gain efficiencies in operations. amitriptyline. ADHD Overview

(State or other jurisdiction of

incorporation or organization) 20-2590184

(I.R.S. Employer

Identification Number)1550 East Gude Drive, Rockville MD (301)

including area code) 20850(zip code)TITLE OF EACH CLASS: Outstanding at February 13, 2020 Trading Symbol Common Stock, $0.001 Par Value 52,533,973 SUPN The NASDAQ Stock Market LLC o☒ No ý☐o☐Noý☒ý☒ No o☐and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesý☒ No o☐o☐or a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer",filer," "accelerated filer"filer," "smaller reporting company," and "smaller reporting"emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):Large accelerated filer ýAccelerated filer ☐ AcceleratedNon-accelerated filer o☐ Smaller reporting company ☐ Non-accelerated filero(Do not check if asmaller reporting company) Smaller reportingEmerging growth companyo☐ o☐ No ý☒2016,2019, the aggregate market value of the common stock held by non-affiliates of the registrant based on the closing price of the common stock on The NASDAQ Global Market was $966,994,822. The number of shares of the registrant's common stock outstanding as of March 9, 2017 was 50,162,496.20172020 Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission not later than 120 days after the end of the registrant's 20162019 fiscal year end, are incorporated by reference into Part III of this Annual Report on Form 10-K.2016

2019applications(™applications(TM), including the following marks referred to in this Annual Report on Form 10-K pursuant to applicable U.S. intellectual property laws: "Supernus®," "Oxtellar XR®," "Trokendi XR®," "Microtrol®," "Solutrol®," and the registered Supernus Pharmaceuticals logo.prospectusAnnual Report are the property of their respective owners. Solely for convenience, the trademarks and trade names in this Annual Report on Form 10-K are referred to without the ® andTM™ symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. specialty pharmaceutical company focused on developing and commercializing products for the treatment of central nervous system (CNS) diseases. In 2013, we launched Oxtellar XR (extended-release oxcarbazepine)diseases in neurology and Trokendi XR (extended-release topiramate), our two novel treatments for patients with epilepsy. In addition, we are developing multiple product candidates in psychiatry to address significant unmet medical needs and market opportunities for the treatment of impulsive aggression (IA) and for the treatment of attention deficit hyperactivity disorder (ADHD). We are initially developing SPN-810 (molindone hydrochloride) to treat IA in patients who have ADHD. We subsequently plan to develop SPN-810 for the treatment of IA in other CNS diseases, such as autism, post traumatic stress disorder (PTSD), bipolar disorder, schizophrenia, and some forms of dementia. There are currently no approved products indicated for the treatment of IA. We are developing SPN-812 (viloxazine hydrochloride) as a candidate to treat patients who have ADHD.standaloneprivately-held stand-alone development organization,organization; then, as a U.S.United States (U.S.) subsidiary of Shire plcPlc (Shire, a subsidiary of Takeda Pharmaceutical Company Ltd.); and upon our acquisition of substantially all of the assets of Shire Laboratories Inc. in late 2005, as Supernus Pharmaceuticals.

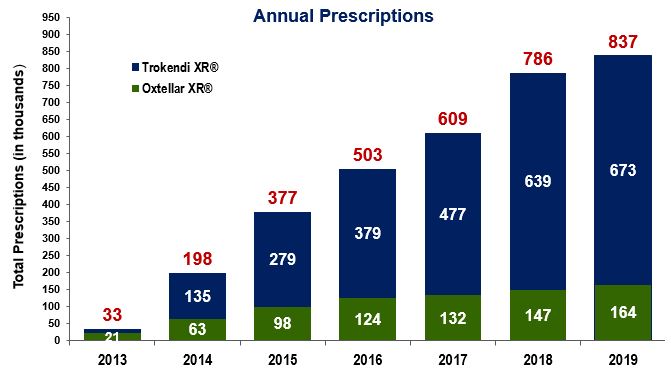

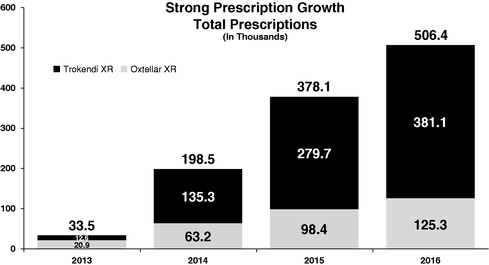

* Prophylaxis of migraine headache in adults and adolescents. ** Prescription Drug User Fee Act (PDUFA) ourtwo products, in the United States through our own specialty sales force and have and will continue to seek strategic collaborations with other pharmaceutical companies to license our products outside the United States.Our neurology portfolio consists of Oxtellar XR and Trokendi XR whichin the U.S. Oxtellar XR and Trokendi XR are the first once-daily extended release oxcarbazepine and topiramate products respectively, indicated for the treatment of epilepsy in the U.S. market. TheseIn April 2017, we launched Trokendi XR for the prophylaxis of migraine headache in adults and adolescents. In January 2019, we launched Oxtellar XR for monotherapy treatment of partial onset epilepsy seizures in adults and in children 6 to 17 years of age. We market our products are differentiated, comparedthrough our own sales force in the U.S. and seek strategic collaborations with other pharmaceutical companies to their immediate release counterpartcommercialize our products by offering convenient once-daily dosing and unique pharmacokinetic profiles. We believe that a once-daily dosing regimen improves compliance which in turn reducesoutside of the frequency of seizures. We also believe that the unique smooth and steady pharmacokinetic profiles of once-daily dosing mitigate the blood level fluctuations typically associated with immediate release products, which can result in adverse events (AEs) or decreased efficacy.revenuessales of $210.1$383.4 million in 20162019 were driven by strongcontinued growth in prescriptions for Oxtellar XR and Trokendi XR. Total prescriptions as reported by Intercontinental Marketing Services (IMS) have shown a steady increase year over yearXR, as shown in the following graph.graph:

IMS Monthly Prescriptions2016, our products2019, Trokendi XR represented approximately 5% of the topiramate market, and Oxtellar XR represented approximately 3% of the large and growing base ofoxcarbazepine market. Total annual prescriptions for the topiramate and oxcarbazepine (total annual prescriptions for topiramate market and oxcarbazepine market is 14.3markets are approximately 13.4 million and 4.54.7 million, respectively). respectively.expectare also developing multiple proprietary CNS product candidates to continueaddress significant unmet medical needs and market opportunities. We are developing SPN-812 (viloxazine hydrochloride) as a novel, non-stimulant product candidate to grow our revenues for Oxtellar XR and Trokendi XR for the foreseeable future by continuing to drive penetration in these markets. We believe these products have the potential to achieve combined peak net sales in excess of $500 million annually.Oxtellar XR is indicated for add-on, adjunctive or concomitant therapy of partial seizures in adults and intreat children 6 years to 17 years of age. Trokendi XR is indicated for initial monotherapy in patients 6 years of age and older with partial onset or primary generalized tonic-clonic seizures, and as add-on therapy in patients 6 years of age and older with partial onset or primary generalized tonic-clonic seizures or with seizures associated with Lennox-Gastaut syndrome.In August 2016, we received tentative approval to expand the label for Trokendi XR to include the indication of prophylaxis of migraine headaches in adults.who have ADHD. We continue to prepare and will be readyexpect to launch SPN-812, assuming FDA approval, in the migraine indication soon after receiving fullfourth quarter of 2020. Additionally, we initiated a Phase III ADHD program to study SPN-812 in adults during the third quarter of 2019.fromfor the treatment of bipolar disorder with oxcarbazepine in the U.S. FoodDrug Administration (FDA).development expenses related to the continued development of each of our product candidates through FDA approval or until the program terminates. We incurred total research and development expenses of $69.1 million, $89.2 million and $49.6 million for the years ended December 31, 2019, 2018 and 2017, respectively.receiving this approval duringcreating a sales force to market our products to the second quarterrelevant population of 2017.Regarding SPN-810, we initiated two Phase III clinical trials in 2015 (P301psychiatrists and P302) that will continue to enroll patients through 2017. Our Phase III clinical trial (P301) is being conducted under a Special Protocol Agreement (SPA). SPN-810 has been granted fast-track designation by the FDA.We completed a Phase IIb dose ranging trial for SPN-812 and announced topline results in 2016. The trial met the primary endpoint, demonstrating that SPN-812 at daily doses of 400 mg, 300 mg, and 200 mg achieved a statistically significant improvement in the symptoms of ADHD when compared to placebo. All SPN-812 doses tested in the trial were well tolerated. Of the patients treated with SPN-812, only 6.7% discontinued due to an AE. In addition, 87% of patients who completed the trial elected to enroll in the ongoing open-label extension. Based on these positive results, we plan to have an end-of-Phase II meeting with the FDA after which we will initiate Phase III clinical testing during the second half of 2017.therapies and expand the treatment to new indications.nineten marketed products, includingincluding: Trokendi XR and Oxtellar XR,XR; Adderall XR (developed for Shire),; Intuniv (developed for Shire),; Mydayis (developed for Shire); and Orenitram (developed for United Therapeutics Corporation); as well as our key product candidates SPN-810 andcandidate SPN-812.Products and Product CandidatesThe table below summarizes our current portfolio of novel products and product candidates.ProductIndicationStatusOxtellar XREpilepsyLaunched in 2013Trokendi XREpilepsyLaunched in 2013Adult Migraine ProphylaxisTentative ApprovalSPN-810IA*Phase IIISPN-812ADHDPhase IIbSPN-809DepressionPhase II ready*Initial program is in patients with ADHD, with plansWe continue to follow on in other indications, such as IA in patients with autism, PTSD, bipolar disorder, schizophrenia, and some forms of dementia.We are continuing to expandbuild our intellectual property portfolio to provide additional protection for our technologies, products and product candidates.currently have seven U.S. patents issued covering Oxtellar XRexpect to incur significant expenses as we: invest in research and eight U.S. patents issued covering Trokendi XR, providing patent protection expiring no earlier than 2027development related to the continued development of each of our product candidates through FDA approval or until the program terminates; expand product indications for each product.bebecome a leading specialty pharmaceutical company, developing and commercializing new medicines for treatment of CNS diseases in neurology and psychiatry. Key elements of our strategy to achieve this vision are to:•Drive growth and profitability. We will continue to drive the prescription growth of Trokendi XR and Oxtellar XR by continuing to dedicate sales and marketing resources in the United States.•Advance our pipeline toward commercialization. We initiated the Phase III clinical trials for SPN-810, a novel treatment for IA in patients who have ADHD, during the third quarter of 2015. We completed a Phase IIb dose ranging study for SPN-812 during 2016 and expect to initiate Phase III clinical testing during the second half of 2017.•Target strategic business development opportunities. We are actively exploring a broad range of strategic opportunities that fit well with our strong presence in CNS. These include: in-licensing products and entering into co-promotion partnerships which are synergistic with our sales force call point for our marketed products and product candidates; co-development partnerships for our pipeline products; and growth opportunities through value-creating and transformative merger and acquisition transactions, including both commercial stage and development stage products.•Continue to grow our pipeline. We plan to continue to evaluate and develop additional CNS product candidates that we believe have significant commercial potential through our internal research and development efforts.• • • • and Trokendi XR are the firsta once-daily extended release oxcarbazepine product that was initially approved for adjunctive treatment of partial onset epilepsy seizures. During January 2019, we launched Oxtellar XR for the monotherapy treatment of partial onset epilepsy seizures in adults and topiramate products indicated for patientsin children 6 to 17 years of age; andepilepsypharmacological activities in the U.S. market. These products differ from theCNS conditions such as epilepsy.immediate release products by offering once-daily dosing and unique pharmacokinetic profiles which we believe can have very positive clinical effects for many patients. We believe a once-daily dosing regimen improves adherence, making it more probable that patients maintain sufficient levels of medication in their bloodstreams to protect against seizures. In addition, we believe that the unique smooth and steady pharmacokinetic profiles of our once-daily formulations reduce the peak to trough blood level fluctuations that are typically associated with immediate release products and may result in increased AEs, more side effects and decreased efficacy.Improved tolerabilityExtended release products may help patients improve adherence, have fewer breakthrough seizuresmigraines and, correspondingly,consequently, help patients enjoy a better quality of life.the firstindicated for: initial monotherapy in patients 6 years of age and older with partial onset or primary generalized tonic-clonic (PGTC) seizures; as add-on therapy in patients 6 years of age and older with partial onset or PGTC seizures or with seizures associated with Lennox-Gastaut syndrome; and for prophylaxis of migraine headache in adults and adolescents 12 years of age and older. Trokendi XR's once-daily extended release topiramate product indicated for patients with epilepsy in the U.S. market, anddosing is designed to improve patient adherence over the current immediate release products, which must be taken multiple times per day. We believe a once-daily dosing regimen improves compliance, making it more probable that patients take their medication and maintain sufficient levels of medication in their bloodstreams. Trokendi XR's unique smooth pharmacokinetic profile results in lower peak plasma concentrations, higher trough plasma concentrations, and slower plasma uptake rates. This results in smoother and more consistent plasma concentrations than immediate release topiramate formulations can deliver.formulations. We believe that such a profile mitigates blood level fluctuations that are frequently associated with many side effects, as well as mitigatingthereby reducing the likelihood of breakthrough seizures or migraine headaches that patients can suffer when taking immediate release products. Side effects associated with immediate release products may lead patients to skip doses, which could place them at higher risk for breakthrough seizures.In August 2016, we received tentative approval to expand the label for Trokendi XR to include the indication of prophylaxis ofseizures or migraine headache in adults. We continue to prepare and will be ready to launch the adult migraine indication soon after receiving full FDA approval, which we anticipate will occur during the second quarter of 2017.the only once-daily extended release oxcarbazepine product indicated for adjunctive treatmentas therapy of patients with epilepsypartial onset seizures in the U.S.adults and in children 6 years to 17 years of age. With its novel pharmacokinetic profile showing lower peak plasma concentrations, a slower rate of plasma input, and smoother and more consistent blood levels as compared to immediate release products, we believe Oxtellar XR improves the tolerability of oxcarbazepine and thereby reduces side effects. In addition, Oxtellar XR once-per-day dosing is designed to improve patient adherencecompliance compared to the current immediate release products that must be taken multiple times per day.Sales and MarketingWeestablished a commercial organizationnew chemical entity status (NCE) in the U.S. market. We expect to support currenthave significant intellectual property (IP) protecting this product candidate through our own research and future sales of Oxtellar XR and Trokendi XR. We believe our current sales force of over 150 sales representatives is effectively targeting healthcare providers, primarily neurologists, to support and grow our epilepsy franchise. Simultaneously promoting two epilepsy products allows us to leverage our commercial infrastructure with these prescribers. Assuming we receive FDA approvaldevelopment efforts, as well as through in-licensed IP. SPN-817 represents a novel MOA for the prophylaxis of migraine in adults, we may expand the sales force dependingan anticonvulsant. Development will initially focus on the prescription uptake post launch.Assuming we obtain FDA approvaldrug's anticonvulsant activity, which has been shown in preclinical models for treatment of partial seizures and Dravet Syndrome. SPN-817 is in clinical development, and has received an Orphan Drug designation for Dravet Syndrome from the product candidatesFDA.our pipeline, we anticipate adding sales representatives to market our productssevere pediatric epilepsy disorders. A Phase I proof-of-concept trial is currently underway in adult patients with refractory complex partial seizures, studying the safety and pharmacokinetic profile of a new extended release formulation of non-synthetic huperzine A. The Company initiated an Investigational New Drug (IND) application, enabling preclinical activities in the U.S.relevant populationsuccess of physicians, primarily psychiatrists.productproducts for commercial use, as well as productsome products for preclinical research and clinical trials.Inc.Inc; and Catalent Pharma Solutions, for the manufacture and packaging of the final commercial products Oxtellar XR and Trokendi XR.XR, as well as for our pipeline candidate, SPN-812. These CMOs offer a comprehensive range of contract manufacturing and packaging services. Commercial products as well as our product candidates are single sourced from single third-party suppliers.for Phase III clinical materials or commercial products in the foreseeable future.currently employ internal resourceshave a commercial sales and marketing organization in the U.S. to managesupport sales of Oxtellar XR and Trokendi XR. We believe our manufacturing contractors.anti-epileptic products. Oxtellar XR competes with all immediate release oxcarbazepine products including Trileptalused for the prevention of migraine headaches. Most notably, this includes a new class of products introduced in 2018, anti-CGRPs (calcitonin gene related peptide); Botox; beta-blockers; valproic acid; and its related generic products as well as other anti-epileptic products.disorders. Thedisorders:SPN-810, has fast track statusis a novel non-stimulant product being developed for the treatment of ADHD. In January 2020, the FDA accepted the review of the NDA for SPN-812 for the treatment of children and is expected to be the first product approved for IA. SPN-812adolescents with ADHD and assigned a PDUFA target action date of November 8, 2020;employwhich employs the same active ingredient as in SPN-812, is Phase II ready and areis in development for the treatment of depression; andADHD and depression, respectively. SPN-812 recently completed athe treatment of bipolar disorder. A Phase IIbIII clinical trial and SPN-809 is Phase II ready.IA OverviewOur market research shows that, for adolescents and children, child psychiatrists, psychiatrists, child neurologists, and high prescribing pediatricians write approximately 40%was initiated during the fourth quarter of their ADHD prescriptions, representing approximately 13 million prescriptions. By 2020, we project that this group of physicians will collectively write approximately 16 million prescriptions for ADHD medication. Of these 16 million ADHD prescriptions, roughly one-third will be written for patients with IA or with IA and other comorbidities.IA is not limited to individuals with ADHD. We believe IA occurs in patients with other CNS disorders, including autism, Alzheimer's, bipolar disorder, PTSD, oppositional defiant disorder, conduct disorder, and intermittent explosive disorder. Market research we have conducted indicates that the prevalence of IA in autistic children and adolescents is approximately 45%, and the prevalence of IA in children and adolescents with bipolar disorder is approximately 60%.

Current Treatments

Currently, there prescriptions. The ADHD market is projected to grow approximately 4% annually, from approximately 75 million prescriptions in 2019 to approximately 78 million prescriptions by 2020. According to data from IQVIA, the U.S. market for ADHD prescription drugs was $8.5 billion for the year ended December 31, 2019.

In response, doctors have also tried to treat this group with off-label use of prescription medicines, such as mood stabilizers, stimulants and anti-psychotic drugs. Results have varied, but anti-psychotic drugs appear to have the best therapeutic potential. Unfortunately, many of these agents are associated with adverse effects including obesity, dyskinesia, lipid abnormalities, marked increases in prolactin, and increase in diabetes, which is of particular concern when treating pediatric populations.

SPN-810 (molindone hydrochloride)

We are developing SPN-810 (molindone hydrochloride) as a novel treatment for IA in patients who have ADHD and who are being treated with standard ADHD medication. During 2014, the FDA

U.S.

- (1)Dopheide, J.A.,Attention-Deficit- Hyperactivity Disorder: An Update, published June 2009 inPharmacotherapy.(2)Floet, A.M.W.,Attention- Deficit/Hyperactivity Disorder, published February 2010 inPediatrics in Review.

(3)The MTA Cooperative Group,A 14-month randomized clinical trial of treatment strategies for attention- deficit/hyperactivity disorder, published December 1999 inArchives of General Psychiatry(4) Harvard Medical School, 2007. National Comorbidity Survey (NSC). (2017, August 21).TableThe FDA accepted the review ofContentsgranted fast track designationthe NDA forSPN-810SPN-812 for the treatment ofIA inchildren and adolescents with ADHD inpatients being treated with standard ADHD medication. The fast track designation allows for more frequent interactions with theJanuary 2020 and assigned a PDUFA target action date of November 8, 2020. We plan to launch it, pending FDAfor the early submission of some sections of the marketing application, and carries the potential for an expedited review category for the New Drug Application (NDA). Currently, we and the FDA have a SPA for the conduct of our Phase III program for SPN-810, using an agreed upon novel scale to measure IA that was developed by us. We initiated two Phase III clinical trials in 2015 (P301 and P302) that continue to enroll patients in 2017.Molindone hydrochloride was previously marketedapproval, in theUnited States as an anti-psychoticfourth quarter of 2020. We expect SPN-812, if approved, totreat schizophrenia under the trade name Moban, albeit at much higher dosages (50 to 225mg/day) than we are using in our development program (18 and 36 mg/day). Moban has not been commercially available since 2010 and the FDA has confirmed that the withdrawal from thehave five-year marketwas notexclusivity due toissues with safety or efficacy. Molindone hydrochloride is differentiated from other anti-psychoticsits NCE status inthat it is less likely to be associated with weight gain and, in preclinical models, has not caused increases in prolactin levels as seen with other anti-psychotic drugs.In addition, we believethelower doses tested for the proposed indication of IA in ADHD should be better tolerated than the higher doses approved to treat schizophrenia. The Phase IIb trial with SPN-810, which included 121 patients, showed that there was no difference in weight gain between patients treated with SPN-810 and those treated with placebo. Although initiallyU.S. Furthermore, we are developingSPN-810 as a novel treatment for IA in patients who have ADHD, if we are successful in demonstrating the effectiveness of SPN-810 in ADHD, we may then develop the product as a candidate for treating other indications; e.g., patients with IA in autism, PTSD, bipolar disorder, schizophrenia, and some forms of dementia. In the aggregate, we believe the addressable market for SPN-810 is greater than $6.3 billion, including $3.2 billion in ADHD, $0.8 billion in autism and $2.3 billion in PTSD.We are developing an intellectual property position aroundIP covering the novel synthesis process for the active ingredient in SPN-812, its novel use inIA,ADHD and its novelformulations. Patents, if issued, could expireextended release delivery system.SPN-812 Development ProgramThe Phase III pivotal program consisted of four three-arm, placebo-controlled trials: P301 and P303 trials in patients 6 to 11 years old; and P302 and P304 trials in patients 12 to 17 years old. We announced positive topline results from2029 to 2033.the pediatric trials (P301 and P303) and the first adolescent trial (P302) in December 2018. Results of the second adolescent Phase III trial (P304) were released in March of 2019.Wehave one patent issued eachinitiated a Phase III program in adults in theU.S., Mexico, Australia and Japan, covering modified release formulationsthird quarter ofmolindone hydrochloride. In another patent family, covering2019.Refer to thenovel process of synthesisCompany's Annual Report on Form 10-K for the year ended December 31, 2017 for the results of theactive ingredient, we have two patents issuedpreviously completed Phase IIb trials.Results of P301 and P303 Phase III trialsBoth studies were randomized, double‑blind, placebo controlled, multicenter, parallel group clinical trials in children 6 to 11 years of age who are diagnosed with ADHD. After titration, each treatment was administered orally once a day over five weeks in study P301, and over seven weeks in study P302. A total of 477 patients were randomized in theU.S. InP301 study, across placebo and two doses (100mg; 200mg), and athird patent family, covering usetotal ofmolindone hydrochloride313 patients were randomized intreating IA, we have one patent issuedthe P303 study, across placebo and two doses (200mg; 400mg). The primary objective of both studies was to assess the efficacy of SPN‑812 inJapan. We own allreducing the symptoms of ADHD in children. The primary outcome measure was the change, from baseline to the end of thepending applications.SPN-810 Development Programstudy, in the ADHD Rating Scale (RS‑5) total score. Safety and tolerability were assessed by monitoring: adverse events (AEs); clinical laboratory tests; vital signs; electrocardiograms (ECGs); suicidality; and physical examinations. Patients who completed the study were offered the opportunity to continue into an open‑label phase, that is currently on‑going.

On December 6, 2018, we announced positive topline results from the P301 and P303 Phase III studies of SPN‑812, having successfully met the primary endpoint. At daily doses of 100 mg and 200 mg in study P301, and at daily doses of 200mg and 400mg in study P303, statistically significant improvement in the symptoms of ADHD, from baseline to end of study, as measured by the ADHD‑RS‑5, was achieved. Patients receiving SPN‑812 100 mg and 200 mg had a −16.6 point change (p=0.0004) and a−17.7 point change (p<0.0001) from baseline, respectively, in the primary endpoint, vs. a −10.9 point change for placebo at week 6. This primary result, based on Mixed Model Repeated Measures (MMRM) analysis in the Intent‑To‑Treat (ITT) population, was confirmed by sensitivity analyses using Analysis of Covariance (ANCOVA) (100 mg, p=0.0008; 200 mg, p<0.0001). All SPN‑812 doses tested in the trials were well tolerated.The study demonstrated fast onset of action, reaching statistical significance for 100 mg and 200 mg doses as early as week 1, with p‑ values of 0.0004 and 0.0244, respectively. Statistical significance was maintained on a weekly basis through the end of the trial at week 6. In2012,addition, at the end of the study, SPN‑812 100 mg and 200 mg reached statistical significance compared to placebo on the hyperactivity/impulsivity and inattention subscales of the ADHD‑RS‑5, scale with p‑ values ranging from <0.0001 to 0.0026. Finally, SPN‑812 100 mg and 200 mg met all secondary endpoints, including the important analysis of the Clinical Global Impression Improvement (CGI‑I) secondary endpoint, with p‑ values of 0.002 and <0.0001, respectively, compared to placebo.At the end of the P303 Study, SPN‑812 200 mg and 400 mg doses reached statistical significance, as compared to placebo, in the primary endpoint. Patients receiving 200 mg and 400 mg had a −17.6 point change (p=0.0038) and a −17.5 point change (p=0.0063) from baseline to end of study, respectively, in the primary endpoint vs. a −11.7 point change for placebo at week 8. This primary result, based on MMRM analysis in the ITT population, was confirmed by sensitivity analyses using ANCOVA (200 mg, p=0.0058; 400 mg, p<0.0121).Onset of action for SPN‑812 showed clear differences compared to placebo starting by week 1, reaching statistical significance at week 5, which was sustained through the rest of the trial.As with the P301 study, at the end of the P303 study, SPN‑812 200 mg and 400 mg reached statistical significance compared to placebo on the hyperactivity/impulsivity and inattention subscales of the ADHD‑RS‑5, scale with p‑ values ranging from 0.0020 to 0.0248. In addition, 200 mg and 400 mg met the CGI‑I secondary endpoint, with p‑ values of 0.0028 and 0.0099, respectively, compared to placebo.Overall, both trials exhibited favorable tolerability and safety profiles, with low incidence of AEs across all doses. AEs were mild, leading to low discontinuation rates due to AEs, ranging from 2.2% to 4.8%. Treatment related AEs that reported at more than or equal to 5% included somnolence, headache, decreased appetite, fatigue and upper abdominal pain.Results of P302 Phase III trialOn December 20, 2018, wecompletedannounced positive topline results from the P302 Phase III study of SPN‑812 in patients 12 to 17 years old for the treatment of ADHD. The trial was successful in meeting the primary endpoint, demonstrating that SPN‑812 at daily doses of 200 mg and 400 mg achieved statistically significant improvement in the symptoms of ADHD, from baseline to end of study, as measured by the ADHD‑RS‑5. Each of the SPN‑812 doses tested in the trials was well tolerated.The study was aPhase IIbrandomized, double‑blind, placebo controlled, multicenter,randomized, double-blind, placebo-controlledparallel group clinical trial, inthe United States in pediatric subjects 6adolescents 12 to1217 years of age diagnosed withADHDADHD. Each treatment was administered orally once a day over six weeks, including the titration phase of the 400 mg dose group.A total of 310 patients were randomized across placebo andwith IA that is not controlled by optimal stimulant and behavioral therapy.two doses of SPN-812 (200 mg/400 mg). The primary objectiveof the studywas to assess the effect ofSPN-810SPN‑812 in reducingIA as measured bytheRetrospective-Modified Overt Aggression Scale (R-MOAS) after at least three weekssymptoms oftreatment. Secondary endpoints includedADHD in adolescents 12 to 17 years old. The primary outcome measure was therate of remission of IA and measurementchange, from baseline to the end of theeffectiveness of SPN-810 onstudy, in theClinical Global Impression (CGI) and ADHD scales as well as evaluation of the safetyADHD‑RS‑5 total score. Safety and tolerability of SPN‑812 were assessed by thedrug.monitoring of: AEs; clinical laboratory tests; vital signs; ECGs; suicidality; and physical examinations. Patients who completed the study were offered the opportunity to continue into an open‑label phase, currently on‑going.At the end of the P302 Study, 200 mg and 400 mg doses reached statistical significance, as compared to placebo, for the primary endpoint. Patients receiving 200 mg and 400 mg had a −16.0 point change (p=0.0232) and a −16.5 point change (p=0.0091) from baseline, respectively, in the primary endpoint, vs. a −11.4 point change for placebo, at week 6. This primary result, based on MMRM analysis in the ITT population, was confirmed by sensitivity analyses using ANCOVA (200 mg, p=0.0163; 400 mg, p=0.0055).The study demonstrated fast onset of action, reaching statistical significance for the 400 mg dose as early as week 1, with a p‑value of 0.0085, and maintaining statistical significance on a weekly basis through the end of the trial at week 6. Onset of action for the 200 mg dose showed clear difference compared to placebo starting by week 1, reaching statistical significance at week 3. This difference was sustained through the rest of the trial.As with the P301 and P303 studies, at the end of the P302 study, 200 mg and 400 mg doses reached statistical significance compared to placebo on the hyperactivity/impulsivity and inattention subscales of the ADHD‑RS‑5 scale, with p‑values ranging from 0.0005 to 0.0424. In addition, 200 mg and 400 mg doses met the CGI‑I secondary endpoint, with p‑values of 0.0042 and 0.0003, respectively, compared to placebo.Overall, the trial exhibited favorable tolerability and safety profiles, with low incidence of AEs across all doses. AEs were mild, leading to low discontinuation rates due to AEs, ranging from 1.9% to 4.1%. Treatment related AEs that reported at more than or equal to 5% for SPN‑812 included somnolence, fatigue, decreased appetite, headache and nausea.Results of P304 Phase III trialOn March 28, 2019, we announced topline results from the P304 Phase III study of SPN-812, in patients 12 to 17 years old for the treatment of ADHD.The study is a randomized, double-blind, placebo controlled, multicenter, parallel group clinical trial in adolescents 12 to 17 years of age, diagnosed with ADHD. Each treatment was administered orally once a day over seven weeks, including one week of titration for 400 mg and two weeks of titration for 600 mg.A total of 297 patients were randomized across placebo and two doses of SPN-812 (400 mg/600 mg). The primary objective was to assess the efficacy of SPN-812 in reducing the symptoms of ADHD, in adolescents 12 to 17 years old. The primary outcome measure was the change, from baseline to the end of the study, in the ADHD-RS-5 total score tested on the 600 mg followed by the 400 mg in the statistical plan. Safety and tolerability of SPN-812 were assessed by the monitoring of: AEs; clinical laboratory tests; vital signs; ECGs; suicidality; and physical examinations. Patients who completed the study were offered the opportunity to continue into an open-label phase,of six months duration.Analysis of treatment was performed using both parametric and non-parametric statistical methods. The parametric method assumes that data are normally distributed. Under this method, mean results of each treatment group at the end of three weeks of treatment were compared to the baseline R-MOAS score for each of the four dose groups (high, medium, low and placebo) using the t-test. The non-parametric method does not assume that data are normally distributed. Under this method, the median results of the change in R-MOAS score from baseline at the end of three weeks of treatment were computed for each of the four dose groups (high, medium, low and placebo). These were compared using the Wilcoxon Rank-sum test. Statistical analyses were performed to compare the median of each of the treatment groups: high, medium, and low versus placebo at the end of three weeks of treatment. The change in score from baseline to visit 10 was used as the outcome variable. There was a statistically significant difference between the low dose and placebo (p=0.031) and also between the medium dose and placebo (p=0.024) at thea=0.05 level. There was no statistically significant difference between the high dose and placebo. Both the medium dose and low dose were superior to placebo. These results convinced us that both low and medium doses were effective. This range of doses is being further evaluated in Phase III clinical trials.A secondary efficacy variable was the proportion of children whose impulsive aggressive behavior remitted, with remission defined as R-MOAS£10 at the end of the study. Low and medium doses of SPN-810 showed statistically significant results versus placebo, with percent of patients who experienced remission of impulsive aggressive behavior of 51.9% (p=0.009) and 40.0% (p=0.043), respectively.The CGI results (Severity and Improvement) are consistent with the findings on the R-MOAS scale, in that notable improvement (reduction in severity) occurred primarily in the low dose and medium dose groups. Scores on SNAP-IV Hyperactivity and Impulsivity items did not exhibit statistically significant differences across treatment groups, indicating that efficacy against IA was specific, rather than being efficacious against the underlying ADHD. Numerical trends in SNAP-IV Oppositional Defiant Disorder scores, while not always significant, consistently favored the low dose and medium dose groups over placebo.SPN-810 was well tolerated throughout the study across all doses. Sedation was the most frequently reported adverse reaction, with two subjects (7%) reporting this event in each of the four treatment groups, including the placebo group. The next most frequently reported adverse reaction was increased appetite with two subjects (7%) reporting this event in each of the three active treatment groups and one subject (3%) in the placebo group.The two serious AEs that occurred were not drug-related. One patient in the low dose arm and two patients in the medium dose arm had severe AEs that were considered either possibly or definitely related to the drug. Six patients in total discontinued the study because of AEs in the active treatment arms: one in low dose; two in medium dose; and three in high dose. AEs requiring dose reduction were infrequent.The frequency of AEs associated with extra-pyramidal symptoms was also low and the events were reversible. The data are too sparse to evaluate dose-related aspects of these reports; thus, no clear dose-response relationship can be assessed. SPN-810 exhibited a very good safety and tolerability profile, with low incidence of AEs, and no unexpected, life threatening, or dose-limiting safety issues.SPN-812 (viloxazine hydrochloride)

on-going.ADHD affects 6% to 9% of all school-age children and 3% to 5% of all adults. Current non-stimulant treatments for ADHD account for about 8% of the total ADHD prescriptions in the U.S. As a novel non-stimulant, SPN-812 has the potential to address a $2.5 billion market opportunity for the treatment of ADHD with non-stimulants. SPN-812, a norepinepherine reuptake inhibitor, would provide an additional option to the few non-stimulant therapiescurrentlyavailable. We believe that SPN-812 could be more effective than other non-stimulant therapies due to its different pharmacological profile.We expect SPN-812, if approved, to have five year market exclusivity, given its new chemical entity (NCE) status in the U.S. We are developing an intellectual property position around the novel synthesis process for the active ingredient, its novel use in ADHD and its novel extended release delivery.Our SPN-812 product candidate has three families of pending U.S. non-provisional and foreign counterpart patent applications. Patents, if issued, could expire from 2029 to 2033. We have one patent issued in Europe and one in Canada in one of these families, covering a method of treating ADHD using viloxazine hydrochloride. In another family, covering the novel process of active ingredient synthesis, we have two patents issued in the U.S. and one patent issued each in Europe, Mexico, and Australia. We have one patent issued in the U.S. covering modified release formulations of viloxazine. We own all of the pending applications.SPN-812 Development ProgramWe are developing SPN-812 as a novel non-stimulant treatment for ADHD. During 2016, we completed a Phase IIb dose ranging trial and announced topline results. The trial met the primary endpoint, demonstrating that SPN-812 at daily doses of 400 mg, 300 mg, and 200 mg achieved a statistically significant improvement in the symptoms of ADHD when compared to placebo. All SPN-812 doses tested in the trial were well tolerated. Of the patients treated with SPN-812, only 6.7% discontinued due to an AE. In addition, 87% of patients who completed the trial elected to enroll in the ongoing open-label extension.At the end of the study (EOS), SPN-812

study,400 mg300 mg and 200 mg doses were statistically significantreached statistical significance as compared to placebo,in meetingfor the primary endpoint.With respect to the primary endpoint, patientsPatients receivingSPN-812400 mg300 mg and 200 mghada –19.0 pointan -18.3 Least Squares (LS) Mean change(p=0.021), –18.6 point change (p=0.027) and a –18.4 point change (p=0.031)from baselinerespectively, as compared to –10.5(p=0.0082) vs. LS Mean change of-13.2 from baseline forplacebo.The treatment groupsplacebo at week 7. SPN-812400600 mg300 mg and 200 mg showed a standardized mean effect sizedid not reach statistical significance with an LS Mean change of0.63, 0.60 and 0.55 compared to placebo, respectively. Patients receiving SPN-812 100 mg had 16.7average mean change-16.7 (p=0.0712) from baseline in the primary endpoint at week 7. The result, based on MMRM analysis in the ITT population, was consistent with the results from sensitivity analyses using ANCOVA (400 mg, p=0.0191; 600 mg, p=0.1002) at week 7 (EOS), with placebo based imputation for missing data.

In addition,AEs across all doses. AEs were mild leading to low discontinuation rates, ranging from 4.0% to 5.1%. Treatment related AEs that reported at more than or equal to 5% for SPN-812 400were somnolence, fatigue, decreased appetite, headache and nausea.

Based on these positive results in children with ADHD and the positive Phase IIa results in adults with ADHD, Supernus plans to have an end-of-Phase II meeting with the FDA after which it plansin November 2019, and received acceptance of the filing in January 2020. The FDA has assigned a PDUFA target action date of November 8, 2020. We expect to initiate Phase III clinical testing duringlaunch SPN-812, assuming FDA approval, in the second halffourth quarter of 2017.

2020.

for this indication.

Treatment options for ADHD in the U.S. market can be broadly classified as either stimulant or as non-stimulant products. Shire plc isPlc, one of the leaders in the U.S. ADHD market, with threehas four marketed products: Vyvanse, a stimulant prodrugdrug product launched in 2007; Intuniv, a non-stimulant treatmentproduct launched in November 2009; and Adderall XR, an extended release stimulant treatment designed to provideproduct providing once-daily dosing.dosing, launched in October 2001; and Mydayis, a stimulant product launched in August 2017. Other marketed stimulant products for the treatment of ADHD in the U.S. market include the following once-daily formulations: Concerta,Concerta; Metadate CD,CD; Ritalin LA,LA; Focalin XR; Daytrana; Adzenys XR-ODT; Cotempla XR Daytrana,ODT; and Adzenys XR-ODT.Aptensio XR. Other marketed non-stimulants arein the U.S. include Strattera and Kapvay.

second line therapy.

Microtrol was also utilized to develop Mydayis, which was launched by Shire in 2017.

We cannot be sure that any patents, if granted, will sustain legal challenge.

patents; our ability to preserve the confidentiality of our trade secretssecrets; and to operate our business without infringing the patents and proprietary rights of third parties.

We have established and continue to build proprietary positions for

Patents for both Oxtellar XR andCompany entered into settlement agreements that allow third parties to enter the market by selling a generic version of Trokendi XR have received numerous Paragraph IV Notice Letters and we have filed claims for infringement of our patents against the third-parties.by January 1, 2023, or earlier under certain circumstances. For more information, please see Part I, Item 3—

In addition to the We have two issued patents for extended release oxcarbazepine in both Europe and patent applications relating to Oxtellar XR, we currently have eight U.S. patents that cover Trokendi XR. We haveAustralia, and one patent issued in each in Mexico, Australia, Japanof the following countries: Canada; Japan; China and Canada forMexico. In addition, we have a pending U.S. patent application that covers various extended release topiramate. We have two patents issued in Europe for extended release topiramate. The eight issued U.S. patents covering Trokendi XR will expire no earlier than 2027. We own all of the issued patents and pending applications.

formulations containing oxcarbazepine.

term may be lengthened byvia a patent term adjustment (PTA), which compensates a patentee for administrative delays by the USPTO in granting a patent. In viewBecause of a recent court decision, the USPTO is under greater scrutiny regarding its calculations becausein which the USPTO erred in calculating the PTA which resulted inby denying the patentee a portion of the patent term to which it was entitled. entitled, the USPTO is under greater scrutiny regarding its calculations of PTAs.

risk that one or more of our patents will be held invalid (in whole or in part,part; on a claim-by-claim basis) or held unenforceable. Such an adverse court ruling could allow third parties to commercialize products or use technologies that are similar to ours, and then compete directly with us, without paymentcompensation to us. See "Risk Factors—IfPart I, Item 1A—

Afecta Pharmaceuticals, Inc.

We have two license agreements with Afecta Pharmaceuticals, Inc. (Afecta) pursuant to which we obtained exclusive worldwide rights to selected product candidates, including an exclusive license to SPN-810. We may pay up to $300,000 upon the achievement of certain milestones. If a product candidate is successfully developed and commercialized, we will be obligated to pay royalties to Afecta based on worldwide net product sales at a rate in the low-single digits.

Product Approval

Government authorities in the United States at the federal, state and local level, and in other countries extensively regulate, among other things, the research, development, testing, manufacture, quality control, approval, labeling, packaging, storage, recordkeeping, promotion, advertising, distribution, marketing, export and import of products such as those we are developing. Our product candidates must receive final approval from the FDA before they may be marketed legally in the U.S.

In the U.S., the FDA regulates drugs under the Federal Food, Drug,

Table identification of Contents

FDA's refusal to approve pending applications, to withdraw an approval, to institute or issue a clinical hold, warning letters, product recalls, product seizures, product detention, total or partial suspension of production or distribution, to impose injunctions, fines, refusal of government contracts, restitution, disgorgement or civil or criminal penalties.

molecule that has the desired effect against a given disease. The process required by the FDA before a drug may be marketed in the U.S. generally involves the following:

•Completion of preclinical laboratory tests, animal studies and formulation studies according to Good Laboratory Practices regulations;•Submission to the FDArequires submission of an IND, which must become effective before human clinicaltrialstrial testing maybegin;•Performancecommence. The results of pre-clinical testing, along with other information, including information about product chemistry, product manufacturing and controls, and a proposed clinical trial protocol are submitted to the FDA as part of the IND. Until the IND is approved, or becomes effective following a waiting period, we may not start the clinical trials. This is typically followed by additional preclinical laboratory and animal testing, as well as adequate and well-controlled human clinical trialsaccording to Good Clinical Practices (GCP)to establish the safety and efficacy of the proposed drug for its intendeduse;•Submissionuse. Satisfaction of FDA approval requirements typically takes many years. The actual time required may vary substantially based upon the type, complexity and novelty of the product or disease.

The testing and approval process requires substantial time, effort and financial resources and we cannot be certain that any approvals for our product candidates will be granted on a timely basis, if at all. Our total research and development expense was approximately $42.8 million and $29.1 million for each of 2016 and 2015, respectively. In order to continue the progress of our product candidates, significant increases in these expenditures will be required.

Once a suitable product candidate is successfully created, a preliminary development strategy is determined. Usually, an IND is opened with adequate preclinical and clinical trial material to permit initiation of the first proposed clinical trial. The IND automatically becomes effective 30 days after receipt by the FDA, unless the FDA places the clinical trial on a clinical hold within that 30-day time period. In such a case, the IND sponsor and the FDA must resolve any outstanding concerns before the clinical trial can begin. safety.

All clinical trials must be conducted underin compliance with applicable regulations and consistent with good clinical practices, as well as protocols detailing the supervisionobjectives of onethe trial, the parameters to be used in monitoring safety, and the parameters to determine effectiveness. Each protocol involving testing on patients, and subsequent protocol amendments, must be submitted to the FDA as part of the IND. The FDA may order the temporary halt or more qualified investigatorspermanent discontinuation of a clinical trial at any time, or to impose other sanctions if they believe that the clinical trial is not being conducted in accordance with GCP regulations. These regulations include the requirement that all research subjects provideapplicable requirements, or if continuing the trial presents an unacceptable risk to the clinical trial patients. The study protocol and informed consent. Further,consent information for patients in clinical trials must also be submitted to an institutional review board (IRB) must review and approve the planor ethics committee, for any clinical trial before it commences at any institution. An IRB considers, among other things, whether the risks to individuals participating in the trials are minimized and are reasonable in relation to anticipated benefits.approval. The IRBIRB/ethics committee may also approves the protocol for conductingrequire the clinical trial andat the consent form that mustsite to be providedhalted, either temporarily or permanently, for failure to each clinical trial subject or his or her legal representative and must monitor the clinical trial until completed.

Once an IND is in effect, each new clinical protocol and any amendments to the protocol must be submittedcomply with the IND for FDA review, and to the IRBs for approval. The protocol details, amongIRB/ethics committee requirements, or they may impose other things, the objectives of the clinical trial, dosing procedures, subject selection and exclusion criteria, and the parameters to be used to monitor subject safety.

Human clinical trials for product candidates are typically conducted in three sequential phases that may overlap or be combined:

•Phase I.The product is initially introduced into healthy human subjects and tested for safety, dosage tolerance, absorption, metabolism, distribution and excretion. In the case of some products for severe or life-threatening diseases, especially when the product may be too inherently toxic to ethically administer to healthy volunteers, the initial human testing may be conducted in patients.•Phase II.Phase II trials involve investigations in a limited patient population to identify possible adverse effects and safety risks, to preliminarily evaluate the efficacy of the product for specific targeted diseases and to determine dosage tolerance and optimal dosage and schedule.•Phase III.In Phase III, clinical trials are undertaken to further evaluate dosage, clinical efficacy and safety in an expanded patient population at geographically dispersed clinical trial sites. These trials are intended to establish the overall risk/benefit ratio of the product and provide an adequate basis for regulatory approval and product labeling.

Concurrent with clinical trials, companies usually complete additional animal studies, and must also develop additional information about the chemistry and physical characteristics of the product candidate andcandidate. They must finalize a process for manufacturing the product in commercial quantities, in accordance with cGMPcurrent good manufacturing practice (cGMP) requirements. Moreover, product used in late stage clinical trials must be manufactured under the proposed commercial process, and at the same scale as will be used commercially. The manufacturing process must be capable of consistently producing quality batches of the product candidate and, among other things, thecandidate. The manufacturer must develop methods for testing the identity, strength, quality and purity of the final product. Additionally, appropriate packaging must be selected and tested and stabilitytested. Stability studies must be conducted to demonstrate that the product candidate does not undergo unacceptable deterioration over its shelf life.