| |

| CoStar Group, Inc. | |

| (Exact name of registrant as specified in its charter) | |

| |

| CoStar Group, Inc. | |

| (Exact name of registrant as specified in its charter) | |

| Delaware | 52-2091509 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1331 L Street, NW, Washington, DC 20005 |

| (Address of principal executive offices) (zip code) |

| Registrant’s telephone number, including area code |

| (877) 739-0486 |

| Registrant’s facsimile number, including area code |

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock, $.01 par value | NASDAQ Global Select Market |

Large accelerated filer o | Accelerated filer x | |

Non-accelerated filer o | Smaller reporting company o |

| PART I | ||

| Item 1. | ||

| Item 1A. | ||

| Item 1B. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | ||

| PART II | ||

| Item 5. | ||

| Item 6. | ||

| Item 7. | ||

| Item 7A. | ||

| Item 8. | ||

| Item 9. | ||

| Item 9A. | ||

| Item 9B. | ||

| PART III | ||

| Item 10. | ||

| Item 11. | ||

| Item 12. | ||

| Item 13. | ||

| Item 14. | ||

| PART IV | ||

| Item 15. | ||

| F-1 |

| Item 1. |

| • | Sales and leasing brokers | • | Government agencies |

| • | Property owners | • | Mortgage-backed security issuers |

| • | Property managers | • | Appraisers |

| • | Design and construction professionals | • | Pension fund managers |

| • | Real estate developers | • | Reporters |

| • | Real estate investment trust managers | • | Tenant vendors |

| • | Investment bankers | • | Building services vendors |

| • | Commercial bankers | • | Communications providers |

| • | Mortgage bankers | • | Insurance companies’ managers |

| • | Mortgage brokers | • | Institutional advisors |

| • | Retailers | • | Investors and asset managers |

| • | Location | • | Mortgage and deed information |

| • | Site and zoning information | • | For-sale information |

| • | Building characteristics | • | Income and expense histories |

| • | Space availability | • | Tenant names |

| • | Tax assessments | • | Lease expirations |

| • | Ownership | • | Contact information |

| • | Sales and lease comparables | • | Historical trends |

| • | Space requirements | • | Demographic information |

| • | Number of retail stores | • | Retail sales per square foot |

| · | calling our information sources on recently updated properties to re-verify information; |

| · |

| performing periodic research audits and field checks to determine if we correctly canvassed buildings; |

| · | providing training and retraining to our research professionals to ensure accurate data compilation; and |

| · | compiling measurable performance metrics for research teams and managers for feedback on data quality. |

| Brokers | Lenders, Investment Bankers | Institutional Advisors, Asset Managers | ||

CB Richard Ellis | BlackRock | |||

CB Richard Ellis — U.K. | Prudential | |||

Colliers | Prudential — U.K. | |||

Colliers | Metropolitan Life | |||

Cushman & Wakefield | ING Clarion Partners | |||

Cushman & Wakefield — U.K. | ||||

Weichert Commercial Brokerage | USAA Real Estate Company | |||

Jones Lang LaSalle | NorthMarq Capital | |||

Jones Lang LaSalle — U.K. | AEW Capital Management LP | |||

Grubb & Ellis | ||||

Hartford Investment Management Company | ||||

Lambert Smith Hampton — U.K. | ||||

Charles Dunn Company, Inc. | Owners, Developers | Appraisers, Accountants | ||

Marcus & Millichap | ||||

Hines | Integra | |||

LNR Property Corp | Deloitte | |||

Shorenstein Company, LLC | ||||

CRESA Partners | Tishman Speyer | KPMG | ||

Studley | ||||

Coldwell Banker Commercial NRT | ||||

Industrial Developments International (IDI) | ||||

FirstService | PGP Valuation | |||

Cassidy Turley | ||||

Binswanger | ||||

Re/Max | ||||

Carter | Retailers | Government Agencies | ||

USI Real Estate Brokerage Services | U.S. General Services Administration | |||

DAUM Commercial Real Estate Services | County of Los Angeles | |||

Internal Revenue Service | ||||

Massage Envy | City of Chicago | |||

7-Eleven | Cook County Assessor’s Office | |||

Dollar General Corporation | U.S. Department of Housing and | |||

Walgreens | Urban Development | |||

Scottish Enterprise — U.K. | ||||

GVA Grimley — U.K. | Federal Reserve Bank of New York | |||

Spencer Gifts LLC | Federal Deposit Insurance Corporation | |||

Avision Young Commercial Real Estate | Transportation Security Administration | |||

REITs | Property Managers | Vendors | ||

Transwestern Commercial Services | Turner Construction Company | |||

Lincoln Property Company | Kastle Systems | |||

PM Realty Group | Comcast Corporation | |||

Navisys Group | ADT Security | |||

Duke Realty Corporation | Osprey Management Company | |||

Kimco Realty | Leggat McCall Properties | |||

Vornado/Charles E. Smith | ||||

Verizon Communications, Inc. | ||||

| Item 1A. |

| Item 1B. |

| Item 2. |

| Item 3. |

| Item 4. | [Removed |

| Item 5. | Market for the Registrant’s Common Stock, Related Stockholder Matters and Issuer Purchases of Equity Securities |

| High | Low | |||||||

| Year Ended December 31, 2007 | ||||||||

| First Quarter | $ | 52.15 | $ | 43.44 | ||||

| Second Quarter | $ | 55.71 | $ | 44.95 | ||||

| Third Quarter | $ | 58.49 | $ | 50.70 | ||||

| Fourth Quarter | $ | 61.65 | $ | 44.48 | ||||

| Year Ended December 31, 2008 | ||||||||

| First Quarter | $ | 45.31 | $ | 36.55 | ||||

| Second Quarter | $ | 51.36 | $ | 44.39 | ||||

| Third Quarter | $ | 56.70 | $ | 43.57 | ||||

| Fourth Quarter | $ | 45.20 | $ | 27.00 | ||||

| High | Low | |||||||

| Year Ended December 31, 2009 | ||||||||

| First Quarter | $ | 35.93 | $ | 24.23 | ||||

| Second Quarter | $ | 40.09 | $ | 31.10 | ||||

| Third Quarter | $ | 41.57 | $ | 33.97 | ||||

| Fourth Quarter | $ | 44.43 | $ | 38.35 | ||||

| Year Ended December 31, 2010 | ||||||||

| First Quarter | $ | 42.97 | $ | 38.22 | ||||

| Second Quarter | $ | 45.95 | $ | 38.80 | ||||

| Third Quarter | $ | 49.53 | $ | 37.66 | ||||

| Fourth Quarter | $ | 57.75 | $ | 48.86 | ||||

| Month, 2008 | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||||||

| Month, 2010 | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||||||

| October 1 through 31 | ¾ | ¾ | ¾ | ¾ | ¾ | ¾ | ¾ | |||||||||||||

| November 1 through 30 | ¾ | ¾ | ¾ | ¾ | ¾ | ¾ | ¾ | |||||||||||||

| December 1 through 31 | 4,220 (1) | $29.37 | ¾ | ¾ | 30,400 | (1) | $ | 55.70 | ¾ | ¾ | ||||||||||

| Total | 4,220 | $29.37 | ¾ | ¾ | 30,400 | $ | 55.70 | ¾ | ¾ | |||||||||||

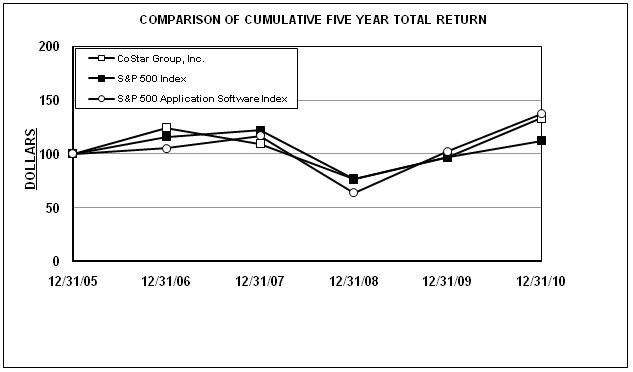

| · | An equal investment in the Standards & Poor's Stock 500 (“S&P 500”) Index. |

| · | An equal investment in the S&P 500 Application Software Index. |

Company / Index | 12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 | ||||||||||||||||||

CoStar Group, Inc. | 100 | 124.07 | 109.45 | 76.30 | 96.76 | 133.33 | ||||||||||||||||||

S&P 500 Index | 100 | 115.79 | 122.16 | 76.96 | 97.33 | 111.99 | ||||||||||||||||||

S&P 500 Application Software Index | 100 | 105.33 | 117.00 | 63.96 | 102.21 | 137.37 | ||||||||||||||||||

Company / Index | 12/31/03 | 12/31/04 | 12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 |

CoStar Group, Inc. | 100 | 110.74 | 103.53 | 128.44 | 113.31 | 78.99 |

S&P 500 Index | 100 | 110.88 | 116.33 | 134.70 | 142.10 | 89.53 |

S&P 500 Application Software Index | 100 | 111.63 | 123.57 | 130.15 | 144.57 | 79.03 |

| Item 6. | Se |

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||

| Consolidated Statement of Operations Data: | 2004 | 2005 | 2006 | 2007 | 2008 | 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||

| Revenues | $ | 112,085 | $ | 134,338 | $ | 158,889 | $ | 192,805 | $ | 212,428 | $ | 158,889 | $ | 192,805 | $ | 212,428 | $ | 209,659 | $ | 226,260 | ||||||||||||||||||||

| Cost of revenues | 35,384 | 44,286 | 56,136 | 76,704 | 73,408 | 56,136 | 76,704 | 73,408 | 73,714 | 83,599 | ||||||||||||||||||||||||||||||

| Gross margin | 76,701 | 90,052 | 102,753 | 116,101 | 139,020 | 102,753 | 116,101 | 139,020 | 135,945 | 142,661 | ||||||||||||||||||||||||||||||

| Operating expenses | 69,955 | 82,710 | 88,672 | 98,249 | 99,232 | 88,672 | 98,249 | 99,232 | 104,110 | 119,886 | ||||||||||||||||||||||||||||||

| Income from operations | 6,746 | 7,342 | 14,081 | 17,852 | 39,788 | 14,081 | 17,852 | 39,788 | 31,835 | 22,775 | ||||||||||||||||||||||||||||||

| Interest and other income, net | 1,314 | 3,455 | 6,845 | 8,045 | 4,914 | 6,845 | 8,045 | 4,914 | 1,253 | 735 | ||||||||||||||||||||||||||||||

| Income before income taxes | 8,060 | 10,797 | 20,926 | 25,897 | 44,702 | 20,926 | 25,897 | 44,702 | 33,088 | 23,510 | ||||||||||||||||||||||||||||||

| Income tax (benefit) expense , net | (16,925 | ) | 4,340 | 8,516 | 9,946 | 20,079 | ||||||||||||||||||||||||||||||||||

| Income tax expense, net | 8,516 | 9,946 | 20,079 | 14,395 | 10,221 | |||||||||||||||||||||||||||||||||||

| Net income | $ | 24,985 | $ | 6,457 | $ | 12,410 | $ | 15,951 | $ | 24,623 | $ | 12,410 | $ | 15,951 | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||||||||||||||||

Net income per share - basic | $ | 1.38 | $ | 0.35 | $ | 0.66 | $ | 0.84 | $ | 1.27 | $ | 0.66 | $ | 0.84 | $ | 1.27 | $ | 0.95 | $ | 0.65 | ||||||||||||||||||||

Net income per share - diluted | $ | 1.33 | $ | 0.34 | $ | 0.65 | $ | 0.82 | $ | 1.26 | $ | 0.65 | $ | 0.82 | $ | 1.26 | $ | 0.94 | $ | 0.64 | ||||||||||||||||||||

Weighted average shares outstanding - basic | 18,165 | 18,453 | 18,751 | 19,044 | 19,372 | 18,751 | 19,044 | 19,372 | 19,780 | 20,330 | ||||||||||||||||||||||||||||||

Weighted average shares outstanding - diluted | 18,827 | 19,007 | 19,165 | 19,404 | 19,550 | 19,165 | 19,404 | 19,550 | 19,925 | 20,707 | ||||||||||||||||||||||||||||||

| As of December 31, | As of December 31, | |||||||||||||||||||||||||||||||||||||||

| Consolidated Balance Sheet Data: | 2004 | 2005 | 2006 | 2007 | 2008 | 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||

| Cash, cash equivalents, short-term and long-term investments | $ | 117,069 | $ | 134,185 | $ | 158,148 | $ | 187,426 | $ | 224,590 | $ | 158,148 | $ | 187,426 | $ | 224,590 | $ | 255,698 | $ | 239,316 | ||||||||||||||||||||

| Working capital | 107,875 | 124,501 | 154,606 | 167,441 | 183,347 | 154,606 | 167,441 | 183,347 | 203,660 | 184,247 | ||||||||||||||||||||||||||||||

| Total assets | 232,691 | 248,059 | 275,437 | 321,843 | 334,384 | 275,437 | 321,843 | 334,384 | 404,579 | 439,648 | ||||||||||||||||||||||||||||||

| Total liabilities | 21,747 | 23,263 | 25,327 | 40,038 | 30,963 | 25,327 | 40,038 | 30,963 | 45,573 | 58,146 | ||||||||||||||||||||||||||||||

| Stockholders’ equity | 210,944 | 224,796 | 250,110 | 281,805 | 303,421 | 250,110 | 281,805 | 303,421 | 359,006 | 381,502 | ||||||||||||||||||||||||||||||

| As of December 31, | As of December 31, | |||||||||||||||||||||||||||||||||||||||

| Other Operating Data: | 2004 | 2005 | 2006 | 2007 | 2008 | 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||||||||||||||||

| Number of subscription client sites | 9,489 | 11,464 | 13,257 | 14,467 | 15,920 | 13,257 | 14,467 | 15,920 | 16,020 | 16,781 | ||||||||||||||||||||||||||||||

| Millions of properties in database | 1.6 | 1.8 | 2.1 | 2.7 | 3.2 | 2.1 | 2.7 | 3.2 | 3.6 | 4.0 | ||||||||||||||||||||||||||||||

| · | Purchase amortization in cost of revenues may be useful for investors to consider because it represents the use of our acquired database technology, which is one of the sources of information for our database of commercial real estate information. We do not believe these charges necessarily reflect the current and ongoing cash charges related to our operating cost structure. |

| · | Purchase amortization in operating expenses may be useful for investors to consider because it represents the estimated attrition of our acquired customer base and the diminishing value of any acquired trade names. We do not believe these charges necessarily reflect the current and ongoing cash charges related to our operating cost structure. |

| · | Depreciation and other amortization may be useful for investors to consider because they generally represent the wear and tear on our property and equipment used in our operations. We do not believe these charges necessarily reflect the current and ongoing cash charges related to our operating cost structure. |

| · | The amount of net interest income we generate may be useful for investors to consider and may result in current cash inflows or outflows. However, we do not consider the amount of net interest income to be a representative component of the day-to-day operating performance of our business. |

| · | Income tax expense (benefit) may be useful for investors to consider because it generally represents the taxes which may be payable for the period and the change in deferred income taxes during the period and may reduce the amount of funds otherwise available for use in our business. However, we do not consider the amount of income tax expense (benefit) to be a representative component of the day-to-day operating performance of our business. |

| · | Purchase amortization in cost of revenues, purchase amortization in operating expenses, depreciation and other amortization, interest income, net, and income tax expense (benefit) as previously described above with respect to the calculation of EBITDA. |

| · | Stock-based compensation expense may be useful for investors to consider because it represents a portion of the compensation of our employees and executives. Determining the fair value of the stock-based instruments involves a high degree of judgment and estimation and the expenses recorded may bear little resemblance to the actual value realized upon the future exercise or termination of the related stock-based awards. Therefore, we believe it is useful to exclude stock-based compensation in order to better understand the long-term performance of our core business. |

| · | The amount of acquisition related costs incurred may be useful for investors to consider because they generally represent professional service fees and direct expenses related to the acquisition. Because we do not acquire businesses on a predictable cycle we do not consider the amount of acquisition related costs to be a representative component of the day-to-day operating performance of our business. |

| · | The amount of restructuring costs incurred may be useful for investors to consider because they generally represent costs incurred in connection with a change in the makeup of our properties or personnel. We do not consider the amount of restructuring related costs to be a representative component of the day-to-day operating performance of our business. |

| · | The amount of headquarters acquisition and transition related costs incurred may be useful for investors to consider because they generally represent the overlapping rent and building carrying costs, legal costs and other related costs incurred to relocate our headquarters. We do not believe these charges necessarily reflect the current and ongoing charges related to our operating cost structure. |

| · | The amount of material settlement and impairment costs incurred outside of our ordinary course of business may be useful for investors to consider because they generally represent gains or losses from the settlement of litigation matters. We do not believe these charges necessarily reflect the current and ongoing cash charges related to our operating cost structure. |

| Year Ended December 31, | ||||||||||||

| 2006 | 2007 | 2008 | ||||||||||

| Net income | $ | 12,410 | $ | 15,951 | $ | 24,623 | ||||||

| Purchase amortization in cost of revenues | 1,205 | 2,170 | 2,284 | |||||||||

| Purchase amortization in operating expenses | 4,183 | 5,063 | 4,880 | |||||||||

| Depreciation and other amortization | 6,421 | 8,914 | 9,637 | |||||||||

| Interest income, net | (6,845 | ) | (8,045 | ) | (4,914 | ) | ||||||

| Income tax expense, net | 8,516 | 9,946 | 20,079 | |||||||||

| EBITDA | $ | 25,890 | $ | 33,999 | $ | 56,589 | ||||||

| Cash flows provided by (used in) | ||||||||||||

| Operating activities | $ | 32,587 | $ | 51,732 | $ | 40,908 | ||||||

| Investing activities | $ | (28,329 | ) | $ | (40,331 | ) | $ | 52,430 | ||||

| Financing activities | $ | 5,582 | $ | 8,161 | $ | 11,475 | ||||||

| Year Ended December 31, | ||||||||||||

| 2008 | 2009 | 2010 | ||||||||||

Net income | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||

Purchase amortization in cost of revenues | 2,284 | 2,389 | 1,471 | |||||||||

Purchase amortization in operating expenses | 4,880 | 3,412 | 2,305 | |||||||||

Depreciation and other amortization | 9,637 | 8,875 | 9,873 | |||||||||

Interest income, net | (4,914 | ) | (1,253 | ) | (735 | ) | ||||||

Income tax expense, net | 20,079 | 14,395 | 10,221 | |||||||||

EBITDA | $ | 56,589 | $ | 46,511 | $ | 36,424 | ||||||

| Net cash flows provided by (used in) | ||||||||||||

Operating activities | $ | 40,908 | $ | 38,445 | $ | 39,269 | ||||||

Investing activities | $ | 52,430 | $ | 4,532 | $ | (40,504 | ) | |||||

Financing activities | $ | 11,475 | $ | 2,172 | $ | 2,042 | ||||||

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | 2010 | |||||||||||||||||||||||||||||||||||||||||||

| Revenues | $ | 158,889 | 100.0 | % | $ | 192,805 | 100.0 | % | $ | 212,428 | 100.0 | % | $ | 212,428 | 100.0 | % | $ | 209,659 | 100.0 | % | $ | 226,260 | 100.0 | % | ||||||||||||||||||||||||

| Cost of revenues | 56,136 | 35.3 | 76,704 | 39.8 | 73,408 | 34.6 | 73,408 | 34.6 | 73,714 | 35.2 | 83,599 | 36.9 | ||||||||||||||||||||||||||||||||||||

| Gross margin | 102,753 | 64.7 | 116,101 | 60.2 | 139,020 | 65.4 | 139,020 | 65.4 | 135,945 | 64.8 | 142,661 | 63.1 | ||||||||||||||||||||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||||||||||||||||||||||||||

| Selling and marketing | 41,774 | 26.3 | 51,777 | 26.9 | 41,705 | 19.6 | 41,705 | 19.6 | 42,508 | 20.3 | 52,455 | 23.2 | ||||||||||||||||||||||||||||||||||||

| Software development | 12,008 | 7.6 | 12,453 | 6.5 | 12,759 | 6.0 | 12,759 | 6.0 | 13,942 | 6.6 | 17,350 | 7.7 | ||||||||||||||||||||||||||||||||||||

| General and administrative | 30,707 | 19.3 | 36,569 | 19.0 | 39,888 | 18.8 | 39,888 | 18.8 | 44,248 | 21.1 | 47,776 | 21.1 | ||||||||||||||||||||||||||||||||||||

| Gain on lease settlement, net | ¾ | 0.0 | (7,613 | ) | (3.9 | ) | ¾ | 0.0 | ||||||||||||||||||||||||||||||||||||||||

| Purchase amortization | 4,183 | 2.6 | 5,063 | 2.6 | 4,880 | 2.3 | 4,880 | 2.3 | 3,412 | 1.6 | 2,305 | 1.0 | ||||||||||||||||||||||||||||||||||||

| Total operating expenses | 88,672 | 55.8 | 98,249 | 51.0 | 99,232 | 46.7 | 99,232 | 46.7 | 104,110 | 49.7 | 119,886 | 53.0 | ||||||||||||||||||||||||||||||||||||

| Income from operations | 14,081 | 8.9 | 17,852 | 9.3 | 39,788 | 18.7 | 39,788 | 18.7 | 31,835 | 15.2 | 22,775 | 10.1 | ||||||||||||||||||||||||||||||||||||

| Interest and other income, net | 6,845 | 4.3 | 8,045 | 4.2 | 4,914 | 2.3 | 4,914 | 2.3 | 1,253 | 0.6 | 735 | 0.3 | ||||||||||||||||||||||||||||||||||||

| Income before income taxes | 20,926 | 13.2 | 25,897 | 13.4 | 44,702 | 21.0 | 44,702 | 21.0 | 33,088 | 15.8 | 23,510 | 10.4 | ||||||||||||||||||||||||||||||||||||

| Income tax expense, net | 8,516 | 5.4 | 9,946 | 5.2 | 20,079 | 9.5 | 20,079 | 9.5 | 14,395 | 6.9 | 10,221 | 4.5 | ||||||||||||||||||||||||||||||||||||

| Net income | $ | 12,410 | 7.8 | % | $ | 15,951 | 8.3 | % | $ | 24,623 | 11.6 | % | $ | 24,623 | 11.6 | % | $ | 18,693 | 8.9 | % | $ | 13,289 | 5.9 | % | ||||||||||||||||||||||||

| 2007 | 2008 | |||||||||||||||||||||||||||||||

| Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | |||||||||||||||||||||||||

| Revenues | $ | 44,831 | $ | 47,794 | $ | 49,340 | $ | 50,840 | $ | 52,264 | $ | 53,478 | $ | 53,757 | $ | 52,929 | ||||||||||||||||

| Cost of revenues | 17,826 | 19,318 | 19,551 | 20,009 | 19,721 | 18,341 | 17,613 | 17,733 | ||||||||||||||||||||||||

| Gross margin | 27,005 | 28,476 | 29,789 | 30,831 | 32,543 | 35,137 | 36,144 | 35,196 | ||||||||||||||||||||||||

| Operating expenses | 25,569 | 28,230 | 25,952 | 18,498 | 25,313 | 26,627 | 24,864 | 22,428 | ||||||||||||||||||||||||

| Income from operations | 1,436 | 246 | 3,837 | 12,333 | 7,230 | 8,510 | 11,280 | 12,768 | ||||||||||||||||||||||||

| Interest and other income, net | 1,862 | 1,891 | 2,072 | 2,220 | 1,938 | 1,243 | 951 | 782 | ||||||||||||||||||||||||

| Income before income taxes | 3,298 | 2,137 | 5,909 | 14,553 | 9,168 | 9,753 | 12,231 | 13,550 | ||||||||||||||||||||||||

| Income tax expense, net | 1,484 | 962 | 2,659 | 4,841 | 4,126 | 4,318 | 5,586 | 6,049 | ||||||||||||||||||||||||

| Net income | $ | 1,814 | $ | 1,175 | $ | 3,250 | $ | 9,712 | $ | 5,042 | $ | 5,435 | $ | 6,645 | $ | 7,501 | ||||||||||||||||

Net income per share - basic | $ | 0.10 | $ | 0.06 | $ | 0.17 | $ | 0.51 | $ | 0.26 | $ | 0.28 | $ | 0.34 | $ | 0.39 | ||||||||||||||||

Net income per share - diluted | $ | 0.09 | $ | 0.06 | $ | 0.17 | $ | 0.50 | $ | 0.26 | $ | 0.28 | $ | 0.34 | $ | 0.38 | ||||||||||||||||

| 2009 | 2010 | |||||||||||||||||||||||||||||||

| Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | |||||||||||||||||||||||||

| Revenues | $ | 51,370 | $ | 50,064 | $ | 53,590 | $ | 54,635 | $ | 55,093 | $ | 55,838 | $ | 57,144 | $ | 58,185 | ||||||||||||||||

| Cost of revenues | 16,894 | 16,744 | 19,149 | 20,927 | 21,200 | 20,360 | 20,762 | 21,277 | ||||||||||||||||||||||||

| Gross margin | 34,476 | 33,320 | 34,441 | 33,708 | 33,893 | 35,478 | 36,382 | 36,908 | ||||||||||||||||||||||||

| Operating expenses | 23,735 | 25,129 | 27,490 | 27,756 | 28,791 | 30,987 | 30,247 | 29,861 | ||||||||||||||||||||||||

| Income from operations | 10,741 | 8,191 | 6,951 | 5,952 | 5,102 | 4,491 | 6,135 | 7,047 | ||||||||||||||||||||||||

| Interest and other income, net | 442 | 322 | 263 | 226 | 238 | 196 | 156 | 145 | ||||||||||||||||||||||||

| Income before income taxes | 11,183 | 8,513 | 7,214 | 6,178 | 5,340 | 4,687 | 6,291 | 7,192 | ||||||||||||||||||||||||

| Income tax expense, net | 5,077 | 3,897 | 2,889 | 2,532 | 2,451 | 1,436 | 2,909 | 3,425 | ||||||||||||||||||||||||

| Net income | $ | 6,106 | $ | 4,616 | $ | 4,325 | $ | 3,646 | $ | 2,889 | $ | 3,251 | $ | 3,382 | $ | 3,767 | ||||||||||||||||

Net income per share - basic | $ | 0.31 | $ | 0.24 | $ | 0.22 | $ | 0.18 | $ | 0.14 | $ | 0.16 | $ | 0.17 | $ | 0.18 | ||||||||||||||||

Net income per share - diluted | $ | 0.31 | $ | 0.24 | $ | 0.22 | $ | 0.18 | $ | 0.14 | $ | 0.16 | $ | 0.16 | $ | 0.18 | ||||||||||||||||

| 2007 | 2008 | |||||||||||||||||||||||||||||||

| Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | |||||||||||||||||||||||||

| Revenues | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||||||

| Cost of revenues | 39.8 | 40.4 | 39.6 | 39.4 | 37.7 | 34.3 | 32.8 | 33.5 | ||||||||||||||||||||||||

| Gross margin | 60.2 | 59.6 | 60.4 | 60.6 | 62.3 | 65.7 | 67.2 | 66.5 | ||||||||||||||||||||||||

| Operating expenses | 57.0 | 59.1 | 52.6 | 36.4 | 48.5 | 49.8 | 46.2 | 42.4 | ||||||||||||||||||||||||

| Income from operations | 3.2 | 0.5 | 7.8 | 24.2 | 13.8 | 15.9 | 21.0 | 24.1 | ||||||||||||||||||||||||

| Interest and other income, net | 4.1 | 4.0 | 4.2 | 4.4 | 3.7 | 2.3 | 1.8 | 1.5 | ||||||||||||||||||||||||

| Income before income taxes | 7.3 | 4.5 | 12.0 | 28.6 | 17.5 | 18.2 | 22.8 | 25.6 | ||||||||||||||||||||||||

| Income tax expense, net | 3.3 | 2.0 | 5.4 | 9.5 | 7.9 | 8.0 | 10.4 | 11.4 | ||||||||||||||||||||||||

| Net income | 4.0 | % | 2.5 | % | 6.6 | % | 19.1 | % | 9.6 | % | 10.2 | % | 12.4 | % | 14.2 | % | ||||||||||||||||

| 2009 | 2010 | |||||||||||||||||||||||||||||||

| Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | Mar. 31 | Jun. 30 | Sep. 30 | Dec. 31 | |||||||||||||||||||||||||

| Revenues | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100. | % | ||||||||||||||||

| Cost of revenues | 32.9 | 33.4 | 35.7 | 38.3 | 38.5 | 36.5 | 36.3 | 36.6 | ||||||||||||||||||||||||

| Gross margin | 67.1 | 66.6 | 64.3 | 61.7 | 61.5 | 63.5 | 63.7 | 63.4 | ||||||||||||||||||||||||

| Operating expenses | 46.2 | 50.2 | 51.3 | 50.8 | 52.3 | 55.5 | 52.9 | 51.3 | ||||||||||||||||||||||||

| Income from operations | 20.9 | 16.4 | 13.0 | 10.9 | 9.3 | 8.0 | 10.7 | 12.1 | ||||||||||||||||||||||||

| Interest and other income,net | 0.9 | 0.6 | 0.5 | 0.4 | 0.4 | 0.4 | 0.3 | 0.2 | ||||||||||||||||||||||||

| Income before income taxes | 21.8 | 17.0 | 13.5 | 11.3 | 9.7 | 8.4 | 11.0 | 12.4 | ||||||||||||||||||||||||

| Income tax expense, net | 9.9 | 7.8 | 5.4 | 4.6 | 4.4 | 2.6 | 5.1 | 5.9 | ||||||||||||||||||||||||

| Net income | 11.9 | % | 9.2 | % | 8.1 | % | 6.7 | % | 5.2 | % | 5.8 | % | 5.9 | % | 6.5 | % | ||||||||||||||||

| Total | 2011 | 2012-2013 | 2014-2015 | 2016 and thereafter | ||||||||||||||||

| Operating leases | $ | 47,453 | $ | 8,691 | $ | 13,105 | $ | 6,908 | $ | 18,749 | ||||||||||

Purchase obligations(1) | 6,763 | 2,797 | 3,366 | 600 | ¾ | |||||||||||||||

| Total contractual principal cash obligations | $ | 54,216 | $ | 11,488 | $ | 16,471 | $ | 7,508 | $ | 18,749 | ||||||||||

| Total | 2009 | 2010-2011 | 2012-2013 | 2014 and thereafter | ||||||||||||||||

| Operating leases | $ | 23,596 | $ | 8,264 | $ | 10,041 | $ | 4,276 | $ | 1,015 | ||||||||||

Purchase obligations(1) | 2,971 | 2,242 | 294 | 290 | 145 | |||||||||||||||

| Total contractual principal cash obligations | $ | 26,567 | $ | 10,506 | $ | 10,335 | $ | 4,566 | $ | 1,160 | ||||||||||

(1)Amounts do not include (i) contracts with initial terms of twelve months or less, or (ii) multi-year contracts that may be terminated by a third party or us. Amounts do not include unrecognized tax benefits of $1.8 million due to uncertainty regarding the timing of future cash payments. |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk |

| Item 8. | Financial Statements and Supplementary Data |

| Item 9B. | Other |

| Item 10. | Directors, Executive Officers and Corporate Governance |

| Item 11. | Executive |

| Item 12. | Security |

| Item 13. | Certain |

| Item 14. | Principal |

Allowance for doubtful accounts and billing adjustments (1) | Balance at Beginning of Year | Charged to Expense | Write-offs, Net of Recoveries | Balance at End of Year | ||||||||||||

Year ended December 31, 2008 | $ | 2,959 | $ | 4,042 | $ | 3,788 | $ | 3,213 | ||||||||

Year ended December 31, 2009 | $ | 3,213 | $ | 4,172 | $ | 4,522 | $ | 2,863 | ||||||||

Year ended December 31, 2010 | $ | 2,863 | $ | 1,471 | $ | 1,919 | $ | 2,415 | ||||||||

| (1) | Additions to the allowance for doubtful accounts are charged to bad debt expense. Additions to the allowance for billing adjustments are charged against revenues. |

| COSTAR GROUP, INC. | ||

| By: | / | |

| Andrew C. Florance | ||

| President and Chief Executive Officer | ||

Signature | Capacity | Date | ||

| / | Chairman of the Board | February | ||

| Michael R. Klein | ||||

| / | Chief Executive Officer and | February | ||

| Andrew C. Florance | President and a Director | |||

| (Principal Executive Officer) | ||||

| / | Chief Financial Officer | February | ||

| Brian J. Radecki | (Principal Financial and Accounting Officer) | |||

| / | Director | February | ||

| David Bonderman | ||||

| / | Director | February | ||

| Warren H. Haber | ||||

| / | Director | February | ||

| Josiah O. Low, III | ||||

| / | Director | February | ||

| Christopher J. Nassetta | ||||

| / | Director | February | ||

| Michael J. Glosserman |

| Exhibit No. | Description | |

| 2.1 | Offer Document by CoStar Limited for the share capital of Focus Information Limited (Incorporated by reference to Exhibit 2.1 to Amendment No. 2 to the Registration Statement on Form S-3 of the Registrant (Reg. No. 333-106769) filed with the Commission on August 14, 2003). | |

| 3.1 | Restated Certificate of Incorporation (Incorporated by reference to Exhibit 3.1 the Registration Statement on Form S-1 of the Registrant (Reg. No. 333-47953) filed with the Commission on March 13, 1998 (the “1998 Form S-1”)). | |

| 3.2 | Certificate of Amendment of Restated Certificate of Incorporation (Incorporated by reference to Exhibit 3.1 to the Registrant’s Report on Form 10-Q for the quarter ended June 30, 1999). | |

| 3.3 | Amended and Restated By-Laws | |

| 4.1 | Specimen Common Stock Certificate (Incorporated by reference to Exhibit 4.1 to the Registrant’s Report on Form 10-K for the year ended December 31, 1999). | |

| *10.1 | CoStar Group, Inc. 1998 Stock Incentive Plan, as amended (Incorporated by reference to Exhibit 10.1 to the Registrant’s Report on Form 10-Q for the quarter ended September 30, 2005). | |

| *10.2 | CoStar Group, Inc. 2007 Stock Incentive Plan, as amended | |

| *10.3 | CoStar Group, Inc. 2007 Stock Incentive Plan French Sub-Plan (Incorporated by reference to Exhibit 10.3 to the Registrant’s Report on Form 10-K for the year ended December 31, 2007). | |

| *10.4 | Form of Stock Option Agreement between the Registrant and certain of its officers, directors and employees (Incorporated by reference to Exhibit 10.8 to the Registrant’s Report on Form 10-K for the year ended December 31, 2004). | |

| *10.5 | Form of Stock Option Agreement between the Registrant and Andrew C. Florance (Incorporated by reference to Exhibit 10.8.1 to the Registrant’s Report on Form 10-K for the year ended December 31, 2004). | |

| *10.6 | Form of Restricted Stock Agreement between the Registrant and certain of its officers, directors and employees (Incorporated by reference to Exhibit 10.9 to the Registrant’s Report on Form 10-K for the year ended December 31, 2004). | |

| *10.7 | Form of 2007 Plan Restricted Stock Grant Agreement between the Registrant and certain of its officers, directors and employees (Incorporated by reference to Exhibit 99.1 to the Registrant’s Report on Form 8-K filed June 22, 2007). | |

| *10.8 | Form of 2007 Plan Incentive Stock Option Grant Agreement between the Registrant and certain of its officers and employees | |

| *10.9 | Form of 2007 Plan Incentive Stock Option Grant Agreement between the Registrant and Andrew C. Florance | |

| *10.10 | Form of 2007 Plan Nonqualified Stock Option Grant Agreement between the Registrant and certain of its officers and employees | |

| *10.11 | Form of 2007 Plan Nonqualified Stock Option Grant Agreement between the Registrant and certain of its directors | |

| *10.12 | Form of 2007 Plan Nonqualified Stock Option Grant Agreement between the Registrant and Andrew C. Florance | |

| *10.13 | Form of 2007 Plan French Sub-Plan Restricted Stock Agreement between the Registrant and certain of its employees (Incorporated by reference to Exhibit 10.10 to the Registrant’s Report on Form 10-K for the year ended December 31, 2007). |

| Exhibit No. | Description | |

| *10.14 | CoStar Group, Inc. Employee Stock Purchase Plan, | |

| *10.15 | Employment Agreement for Andrew C. Florance (Incorporated by reference to Exhibit 10.2 to Amendment No. 1 to the Registration Statement on Form S-1 of the Registrant (Reg. No. 333-47953) filed with the Commission on April 27, 1998). |

| *10.16 | First Amendment to Andrew C. Florance Employment Agreement, effective January 1, 2009 | |

| *10.17 | Executive Service Contract dated February 16, 2007, between Property Investment Exchange Limited and Paul Marples (Incorporated by reference to Exhibit 10.14 to the Registrant’s Report on Form 10-K for the year ended December 31, 2007). | |

| *10.18 | Form of Indemnification Agreement between the Registrant and each of its officers and directors (Incorporated by reference to Exhibit 10.1 to the Registrant’s Report on Form 10-Q for the quarter ended March 31, 2004). | |

| 10.19 | ||

| 10.21 | Purchase and Sale Agreement between | |

| 21.1 | Subsidiaries of the Registrant (filed herewith). | |

| 23.1 | Consent of Ernst & Young LLP, Independent Registered Public Accounting Firm (filed herewith). | |

| 31.1 | Certification of Principal Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 (filed herewith). | |

| 31.2 | Certification of Principal Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 (filed herewith). | |

| 32.1 | Certification of Principal Executive Officer pursuant to 18 U.S.C. Sec. 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (filed herewith). | |

| 32.2 | Certification of Principal Financial Officer pursuant to 18 U.S.C. Sec. 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (filed herewith). | |

| Reports of Independent Registered Public Accounting Firm | F-2 |

| Consolidated Statements of Operations for the years ended December 31, | F-4 |

| Consolidated Balance Sheets as of December 31, | F-5 |

| Consolidated Statements of Stockholders’ Equity for the years ended December 31, | F-6 |

| Consolidated Statements of Cash Flows for the years ended December 31, | F-7 |

| Notes to Consolidated Financial Statements | F-8 |

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | 2010 | |||||||||||||||||||

| Revenues | $ | 158,889 | $ | 192,805 | $ | 212,428 | $ | 212,428 | $ | 209,659 | $ | 226,260 | ||||||||||||

| Cost of revenues | 56,136 | 76,704 | 73,408 | 73,408 | 73,714 | 83,599 | ||||||||||||||||||

| Gross margin | 102,753 | 116,101 | 139,020 | 139,020 | 135,945 | 142,661 | ||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||||||

| Selling and marketing | 41,774 | 51,777 | 41,705 | 41,705 | 42,508 | 52,455 | ||||||||||||||||||

| Software development | 12,008 | 12,453 | 12,759 | 12,759 | 13,942 | 17,350 | ||||||||||||||||||

| General and administrative | 30,707 | 36,569 | 39,888 | 39,888 | 44,248 | 47,776 | ||||||||||||||||||

| Gain on lease settlement, net | ¾ | (7,613 | ) | ¾ | ||||||||||||||||||||

| Purchase amortization | 4,183 | 5,063 | 4,880 | 4,880 | 3,412 | 2,305 | ||||||||||||||||||

| 88,672 | 98,249 | 99,232 | 99,232 | 104,110 | 119,886 | |||||||||||||||||||

| Income from operations | 14,081 | 17,852 | 39,788 | 39,788 | 31,835 | 22,775 | ||||||||||||||||||

| Interest and other income, net | 6,845 | 8,045 | 4,914 | 4,914 | 1,253 | 735 | ||||||||||||||||||

| Income before income taxes | 20,926 | 25,897 | 44,702 | 44,702 | 33,088 | 23,510 | ||||||||||||||||||

| Income tax expense, net | 8,516 | 9,946 | 20,079 | 20,079 | 14,395 | 10,221 | ||||||||||||||||||

| Net income | $ | 12,410 | $ | 15,951 | $ | 24,623 | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||||||||

Net income per share ¾ basic | $ | 0.66 | $ | 0.84 | $ | 1.27 | $ | 1.27 | $ | 0.95 | $ | 0.65 | ||||||||||||

Net income per share ¾ diluted | $ | 0.65 | $ | 0.82 | $ | 1.26 | $ | 1.26 | $ | 0.94 | $ | 0.64 | ||||||||||||

Weighted average outstanding shares ¾ basic | 18,751 | 19,044 | 19,372 | 19,372 | 19,780 | 20,330 | ||||||||||||||||||

Weighted average outstanding shares ¾ diluted | 19,165 | 19,404 | 19,550 | 19,550 | 19,925 | 20,707 | ||||||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2007 | 2008 | 2009 | 2010 | |||||||||||||

| ASSETS | ||||||||||||||||

| Current assets: | ||||||||||||||||

| Cash and cash equivalents | $ | 57,785 | $ | 159,982 | $ | 205,786 | $ | 206,405 | ||||||||

| Short-term investments | 129,641 | 35,268 | 20,188 | 3,722 | ||||||||||||

| Accounts receivable, less allowance for doubtful accounts of approximately $2,959 and $3,213 as of December 31, 2007 and 2008, respectively | 10,875 | 12,294 | ||||||||||||||

| Accounts receivable, less allowance for doubtful accounts of $2,863 and $2,415 as of December 31, 2009 and 2010, respectively | 12,855 | 13,094 | ||||||||||||||

| Deferred income taxes, net | 2,716 | 2,036 | 3,450 | 5,203 | ||||||||||||

Income tax receivable | ¾ | 4,940 | ||||||||||||||

| Prepaid expenses and other current assets | 4,661 | 2,903 | 5,128 | 5,809 | ||||||||||||

| Total current assets | 205,678 | 212,483 | 247,407 | 239,173 | ||||||||||||

| Long-term investments | ¾ | 29,340 | 29,724 | 29,189 | ||||||||||||

| Deferred income taxes, net | 2,233 | 3,392 | 1,978 | ¾ | ||||||||||||

| Property and equipment, net | 24,045 | 16,876 | 19,162 | 69,921 | ||||||||||||

| Goodwill | 61,854 | 54,328 | 80,321 | 79,602 | ||||||||||||

| Intangibles and other assets, net | 25,711 | 16,421 | 23,390 | 18,774 | ||||||||||||

| Deposits and other assets | 2,322 | 1,544 | 2,597 | 2,989 | ||||||||||||

| Total assets | $ | 321,843 | $ | 334,384 | $ | 404,579 | $ | 439,648 | ||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||||||||||

| Current liabilities: | ||||||||||||||||

| Accounts payable | $ | 3,299 | $ | 1,636 | $ | 3,667 | $ | 3,123 | ||||||||

| Accrued wages and commissions | 7,489 | 7,217 | 9,696 | 12,465 | ||||||||||||

| Accrued expenses | 15,505 | 7,754 | 14,167 | 18,411 | ||||||||||||

| Income taxes payable | 191 | 1,907 | ||||||||||||||

| Deferred revenue | 10,374 | 9,442 | 14,840 | 16,895 | ||||||||||||

| Deferred rent | 1,379 | 1,180 | 1,377 | 4,032 | ||||||||||||

| Total current liabilities | 38,237 | 29,136 | 43,747 | 54,926 | ||||||||||||

| Deferred income taxes, net | 1,801 | 132 | ¾ | 1,450 | ||||||||||||

| Income taxes payable | ¾ | 1,695 | 1,826 | 1,770 | ||||||||||||

| Commitments and Contingencies | ¾ | ¾ | ||||||||||||||

Commitments and contingencies | ¾ | ¾ | ||||||||||||||

| Stockholders’ equity: | ||||||||||||||||

| Preferred stock, $0.01 par value; 2,000 shares authorized; none outstanding | ¾ | ¾ | ¾ | ¾ | ||||||||||||

| Common stock, $0.01 par value; 30,000 shares authorized; 19,474 and 19,733 issued and outstanding as of December 31, 2007 and 2008, respectively | 195 | 197 | ||||||||||||||

| Common stock, $0.01 par value; 30,000 shares authorized; 20,617 and 20,773 issued and outstanding as of December 31, 2009 and 2010, respectively | 206 | 208 | ||||||||||||||

| Additional paid-in capital | 317,570 | 333,983 | 364,635 | 374,981 | ||||||||||||

| Accumulated other comprehensive income (loss) | 5,626 | (13,796 | ) | |||||||||||||

| Accumulated deficit | (41,586 | ) | (16,963 | ) | ||||||||||||

Accumulated other comprehensive loss | (7,565 | ) | (8,706 | ) | ||||||||||||

Retained earnings | 1,730 | 15,019 | ||||||||||||||

| Total stockholders’ equity | 281,805 | 303,421 | 359,006 | 381,502 | ||||||||||||

| Total liabilities and stockholders’ equity | $ | 321,843 | $ | 334,384 | $ | 404,579 | $ | 439,648 | ||||||||

Additional | Accumulated Other | Total | ||||||||||||||||||||||||||||||

Comprehensive Income | Common Stock | Paid-In Capital | Unearned Compensation | Comprehensive Income (Loss) | Accumulated Deficit | Stockholders’ Equity | ||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||

| Balance at December 31, 2005 | 18,674 | $ | 187 | $ | 295,920 | $ | (2,712 | ) | $ | 1,348 | $ | (69,947 | ) | $ | 224,796 | |||||||||||||||||

| Net income | 12,410 | ¾ | ¾ | ¾ | ¾ | ¾ | 12,410 | 12,410 | ||||||||||||||||||||||||

| Foreign currency translation adjustment | 2,950 | ¾ | ¾ | ¾ | ¾ | 2,950 | ¾ | 2,950 | ||||||||||||||||||||||||

| Net unrealized gain on short-term investments | 222 | ¾ | ¾ | ¾ | ¾ | 222 | ¾ | 222 | ||||||||||||||||||||||||

| Comprehensive income | $ | 15,582 | ||||||||||||||||||||||||||||||

| Exercise of stock options | 270 | 3 | 6,566 | ¾ | ¾ | ¾ | 6,569 | |||||||||||||||||||||||||

| Swaps of shares for exercise | (20 | ) | (1 | ) | (938 | ) | ¾ | ¾ | ¾ | (939 | ) | |||||||||||||||||||||

| Restricted stock grants | 165 | 2 | 34 | ¾ | ¾ | ¾ | 36 | |||||||||||||||||||||||||

| Restricted stock grants surrendered | (12 | ) | ¾ | (234 | ) | ¾ | ¾ | ¾ | (234 | ) | ||||||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 4,094 | ¾ | ¾ | ¾ | 4,094 | |||||||||||||||||||||||||

| Employee Stock Purchase Plan (ESPP) | 4 | ¾ | 206 | ¾ | ¾ | ¾ | 206 | |||||||||||||||||||||||||

| Impact upon adoption of SFAS 123R | ¾ | ¾ | (2,712 | ) | 2,712 | ¾ | ¾ | ¾ | ||||||||||||||||||||||||

| Balance at December 31, 2006 | 19,081 | 191 | 302,936 | ¾ | 4,520 | (57,537 | ) | 250,110 | ||||||||||||||||||||||||

| FIN 48 Adjustment | ¾ | ¾ | 26 | ¾ | ¾ | ¾ | 26 | |||||||||||||||||||||||||

| Balance at January 1, 2007 | 19,081 | 191 | 302,962 | ¾ | 4,520 | (57,537 | ) | 250,136 | ||||||||||||||||||||||||

| Net income | 15,951 | ¾ | ¾ | ¾ | ¾ | ¾ | 15,951 | 15,951 | ||||||||||||||||||||||||

| Foreign currency translation adjustment | 873 | ¾ | ¾ | ¾ | ¾ | 873 | ¾ | 873 | ||||||||||||||||||||||||

| Net unrealized gain on short-term investments | 233 | ¾ | ¾ | ¾ | ¾ | 233 | ¾ | 233 | ||||||||||||||||||||||||

| Comprehensive income | $ | 17,057 | ||||||||||||||||||||||||||||||

| Exercise of stock options | 289 | 3 | 8,127 | ¾ | ¾ | ¾ | 8,130 | |||||||||||||||||||||||||

| Restricted stock grants | 131 | 1 | (1 | ) | ¾ | ¾ | ¾ | ¾ | ||||||||||||||||||||||||

| Restricted stock grants surrendered | (58 | ) | ¾ | (635 | ) | ¾ | ¾ | ¾ | (635 | ) | ||||||||||||||||||||||

| Consideration for Propex | 22 | ¾ | 1,010 | ¾ | ¾ | ¾ | 1,010 | |||||||||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 5,440 | ¾ | ¾ | ¾ | 5,440 | |||||||||||||||||||||||||

| ESPP | 9 | ¾ | 407 | ¾ | ¾ | ¾ | 407 | |||||||||||||||||||||||||

| Excess tax benefit for exercised stock options | ¾ | ¾ | 260 | ¾ | ¾ | ¾ | 260 | |||||||||||||||||||||||||

| Balance at December 31, 2007 | 19,474 | 195 | 317,570 | ¾ | 5,626 | (41,586 | ) | 281,805 | ||||||||||||||||||||||||

| Net income | 24,623 | ¾ | ¾ | ¾ | ¾ | ¾ | 24,623 | 24,623 | ||||||||||||||||||||||||

| Foreign currency translation adjustment | (14,061 | ) | ¾ | ¾ | ¾ | ¾ | (14,061 | ) | ¾ | (14,061 | ) | |||||||||||||||||||||

| Net unrealized loss on short-term investments | (5,361 | ) | ¾ | ¾ | ¾ | ¾ | (5,361 | ) | ¾ | (5,361 | ) | |||||||||||||||||||||

| Comprehensive income | $ | 5,201 | ||||||||||||||||||||||||||||||

| Exercise of stock options | 198 | 2 | 6,555 | ¾ | ¾ | ¾ | 6,557 | |||||||||||||||||||||||||

| Restricted stock grants | 102 | 1 | ¾ | ¾ | ¾ | ¾ | 1 | |||||||||||||||||||||||||

| Restricted stock grants surrendered | (49 | ) | (1 | ) | (695 | ) | ¾ | ¾ | ¾ | (696 | ) | |||||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 4,907 | ¾ | ¾ | ¾ | 4,907 | |||||||||||||||||||||||||

| ESPP | 8 | ¾ | 329 | ¾ | ¾ | ¾ | 329 | |||||||||||||||||||||||||

| Excess tax benefit for exercised stock options | ¾ | ¾ | 5,317 | ¾ | ¾ | ¾ | 5,317 | |||||||||||||||||||||||||

| Balance at December 31, 2008 | 19,733 | $ | 197 | $ | 333,983 | $ | ¾ | $ | (13,796 | ) | $ | (16,963 | ) | $ | 303,421 | |||||||||||||||||

| Accumulated | Retained | ||||||||||||||||||||||||||||

| Additional | Other | Earnings | Total | ||||||||||||||||||||||||||

| Comprehensive | Common Stock | Paid-In | Comprehensive | (Accumulated | Stockholders’ | ||||||||||||||||||||||||

| Income | Shares | Amount | Capital | Income (Loss) | Deficit) | Equity | |||||||||||||||||||||||

| Balance at December 31, 2007 | 19,474 | $ | 195 | $ | 317,570 | $ | 5,626 | $ | (41,586 | ) | $ | 281,805 | |||||||||||||||||

| Net income | $ | 24,623 | ¾ | ¾ | ¾ | ¾ | 24,623 | 24,623 | |||||||||||||||||||||

| Foreign currency translation adjustment | (14,061 | ) | ¾ | ¾ | ¾ | (14,061 | ) | ¾ | (14,061 | ) | |||||||||||||||||||

| Net unrealized loss on investments | (5,361 | ) | ¾ | ¾ | ¾ | (5,361 | ) | ¾ | (5,361 | ) | |||||||||||||||||||

| Comprehensive income | $ | 5,201 | |||||||||||||||||||||||||||

| Exercise of stock options | 198 | 2 | 6,555 | ¾ | ¾ | 6,557 | |||||||||||||||||||||||

| Restricted stock grants | 102 | 1 | ¾ | ¾ | ¾ | 1 | |||||||||||||||||||||||

| Restricted stock grants surrendered | (49 | ) | (1 | ) | (695 | ) | ¾ | ¾ | (696 | ) | |||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 4,907 | ¾ | ¾ | 4,907 | |||||||||||||||||||||||

| ESPP | 8 | ¾ | 329 | ¾ | ¾ | 329 | |||||||||||||||||||||||

| Excess tax benefit for exercised stock options | ¾ | ¾ | 5,317 | ¾ | ¾ | 5,317 | |||||||||||||||||||||||

| Balance at December 31, 2008 | 19,733 | 197 | 333,983 | (13,796 | ) | (16,963 | ) | 303,421 | |||||||||||||||||||||

| Net income | 18,693 | ¾ | ¾ | ¾ | ¾ | 18,693 | 18,693 | ||||||||||||||||||||||

| Foreign currency translation adjustment | 3,671 | ¾ | ¾ | ¾ | 3,671 | ¾ | 3,671 | ||||||||||||||||||||||

| Net unrealized gain on investments | 2,560 | ¾ | ¾ | ¾ | 2,560 | ¾ | 2,560 | ||||||||||||||||||||||

| Comprehensive income | $ | 24,924 | |||||||||||||||||||||||||||

| Exercise of stock options | 85 | ¾ | 2,232 | ¾ | ¾ | 2,232 | |||||||||||||||||||||||

| Restricted stock grants | 237 | 2 | ¾ | ¾ | ¾ | 2 | |||||||||||||||||||||||

| Restricted stock grants surrendered | (44 | ) | ¾ | (672 | ) | ¾ | ¾ | (672 | ) | ||||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 6,438 | ¾ | ¾ | 6,438 | |||||||||||||||||||||||

| ESPP | 7 | ¾ | 230 | ¾ | ¾ | 230 | |||||||||||||||||||||||

| Consideration for PPR | 573 | 6 | 20,897 | ¾ | ¾ | 20,903 | |||||||||||||||||||||||

| Consideration for Resolve Technology | 26 | 1 | 1,124 | ¾ | ¾ | 1,125 | |||||||||||||||||||||||

| Excess tax benefit for exercised stock options | ¾ | ¾ | 403 | ¾ | ¾ | 403 | |||||||||||||||||||||||

| Balance at December 31, 2009 | 20,617 | 206 | 364,635 | (7,565 | ) | 1,730 | 359,006 | ||||||||||||||||||||||

| Net income | 13,289 | ¾ | ¾ | ¾ | ¾ | 13,289 | 13,289 | ||||||||||||||||||||||

| Foreign currency translation adjustment | (1,064 | ) | ¾ | ¾ | ¾ | (1,064 | ) | ¾ | (1,064 | ) | |||||||||||||||||||

| Net unrealized loss on investments | (77 | ) | ¾ | ¾ | ¾ | (77 | ) | ¾ | (77 | ) | |||||||||||||||||||

| Comprehensive income | $ | 12,148 | |||||||||||||||||||||||||||

| Exercise of stock options | 138 | 2 | 3,720 | ¾ | ¾ | 3,722 | |||||||||||||||||||||||

| Restricted stock grants | 113 | ¾ | ¾ | ¾ | ¾ | ¾ | |||||||||||||||||||||||

| Restricted stock grants surrendered | (103 | ) | ¾ | (2,906 | ) | ¾ | ¾ | (2,906 | ) | ||||||||||||||||||||

| Stock compensation expense, net of forfeitures | ¾ | ¾ | 8,270 | ¾ | ¾ | 8,270 | |||||||||||||||||||||||

| ESPP | 8 | ¾ | 360 | ¾ | ¾ | 360 | |||||||||||||||||||||||

| Excess tax benefit for exercised stock options | ¾ | ¾ | 902 | ¾ | ¾ | 902 | |||||||||||||||||||||||

| Balance at December 31, 2010 | 20,773 | $ | 208 | $ | 374,981 | $ | (8,706 | ) | $ | 15,019 | $ | 381,502 | |||||||||||||||||

| See accompanying notes. | |||||||||||||||||||||||||||||

| Year Ended December 31, | Year Ended December 31, | |||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | 2010 | |||||||||||||||||||

| Operating activities: | ||||||||||||||||||||||||

| Net income | $ | 12,410 | $ | 15,951 | $ | 24,623 | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||||||||||||||

| Depreciation | 5,734 | 7,778 | 8,360 | 8,360 | 7,583 | 8,607 | ||||||||||||||||||

| Amortization | 6,076 | 8,369 | 8,441 | 8,441 | 7,093 | 5,042 | ||||||||||||||||||

| Deferred income tax expense, net | 7,658 | 9,946 | 2,148 | 2,148 | (2,428 | ) | 1,675 | |||||||||||||||||

| Provision for losses on accounts receivable | 1,813 | 2,464 | 4,042 | 4,042 | 4,172 | 1,471 | ||||||||||||||||||

| Excess tax benefit from stock options | ¾ | ¾ | (5,317 | ) | (5,317 | ) | (403 | ) | (902 | ) | ||||||||||||||

| Stock-based compensation expense | 4,155 | 5,440 | 4,940 | 4,940 | 6,460 | 8,306 | ||||||||||||||||||

Fixed asset write-off | ¾ | 603 | 674 | |||||||||||||||||||||

| Changes in operating assets and liabilities, net of acquisitions: | ||||||||||||||||||||||||

| Accounts receivable | (5,080 | ) | (2,944 | ) | (6,196 | ) | (6,196 | ) | (1,610 | ) | (1,776 | ) | ||||||||||||

| Interest receivable | (164 | ) | (67 | ) | 533 | 533 | 97 | 70 | ||||||||||||||||

| Income tax receivable | ¾ | ¾ | (4,940 | ) | ||||||||||||||||||||

| Prepaid expenses and other current assets | (1,205 | ) | (755 | ) | 1,464 | 1,464 | (1,521 | ) | (714 | ) | ||||||||||||||

| Deposits | (246 | ) | (670 | ) | 652 | |||||||||||||||||||

| Accounts payable and accrued expenses | 688 | 6,721 | (3,044 | ) | ||||||||||||||||||||

Deposits and other assets | 652 | (1,013 | ) | (385 | ) | |||||||||||||||||||

Accounts payable and other liabilities | (3,044 | ) | 1,531 | 6,690 | ||||||||||||||||||||

| Deferred revenue | 748 | (501 | ) | 262 | 262 | (812 | ) | 2,162 | ||||||||||||||||

| Net cash provided by operating activities | 32,587 | 51,732 | 40,908 | 40,908 | 38,445 | 39,269 | ||||||||||||||||||

| Investing activities: | ||||||||||||||||||||||||

| Purchases of short-term investments | (108,876 | ) | (116,609 | ) | (4,839 | ) | ||||||||||||||||||

| Sales of short-term investments | 95,393 | 107,286 | 63,949 | |||||||||||||||||||||

Purchases of investments | (4,839 | ) | ¾ | ¾ | ||||||||||||||||||||

Sales of investments | 63,949 | 17,159 | 16,854 | |||||||||||||||||||||

| Purchases of property and equipment and other assets | (12,959 | ) | (14,271 | ) | (3,656 | ) | (3,656 | ) | (9,420 | ) | (57,358 | ) | ||||||||||||

| Acquisitions, net of cash acquired | (1,887 | ) | (16,737 | ) | (3,024 | ) | (3,024 | ) | (3,207 | ) | ¾ | |||||||||||||

| Net cash (used in) provided by investing activities | (28,329 | ) | (40,331 | ) | 52,430 | |||||||||||||||||||

Net cash provided by (used in) investing activities | 52,430 | 4,532 | (40,504 | ) | ||||||||||||||||||||

| Financing activities: | ||||||||||||||||||||||||

| Excess tax benefit from stock options | ¾ | ¾ | 5,317 | 5,317 | 403 | 902 | ||||||||||||||||||

| Proceeds from transactions in stock based plans | 5,582 | 8,161 | 6,158 | |||||||||||||||||||||

| Repurchase of restricted stock to satisfy tax withholding obligations | (695 | ) | (672 | ) | (2,904 | ) | ||||||||||||||||||

Proceeds from exercise of stock options and ESPP | 6,853 | 2,441 | 4,044 | |||||||||||||||||||||

| Net cash provided by financing activities | 5,582 | 8,161 | 11,475 | 11,475 | 2,172 | 2,042 | ||||||||||||||||||

| Effect of foreign currency exchange rates on cash and cash equivalents | 254 | 64 | (2,616 | ) | (2,616 | ) | 655 | (188 | ) | |||||||||||||||

| Net increase in cash and cash equivalents | 10,094 | 19,626 | 102,197 | 102,197 | 45,804 | 619 | ||||||||||||||||||

| Cash and cash equivalents at beginning of year | 28,065 | 38,159 | 57,785 | 57,785 | 159,982 | 205,786 | ||||||||||||||||||

| Cash and cash equivalents at end of year | $ | 38,159 | $ | 57,785 | $ | 159,982 | $ | 159,982 | $ | 205,786 | $ | 206,405 | ||||||||||||

| Year Ended December 31, | ||||||||

| 2007 | 2008 | |||||||

| Foreign currency translation adjustment | $ | 5,540 | $ | (8,521 | ) | |||

| Accumulated net unrealized gain (loss) on investments, net of tax | 86 | (5,275 | ) | |||||

| Total accumulated other comprehensive income (loss) | $ | 5,626 | $ | (13,796 | ) | |||

| Year Ended December 31, | ||||||||

| 2009 | 2010 | |||||||

Foreign currency translation adjustment | $ | (4,850 | ) | $ | (5,914 | ) | ||

| Accumulated net unrealized loss on investments, net of tax | (2,715 | ) | (2,792 | ) | ||||

Total accumulated other comprehensive loss | $ | (7,565 | ) | $ | (8,706 | ) | ||

| Income from operations | $ | (2,860 | ) | |

| Income before taxes | $ | (2,860 | ) | |

| Net income | $ | (1,784 | ) | |

| Basic earnings per share | $ | (0.10 | ) | |

| Diluted earnings per share | $ | (0.09 | ) |

| Year Ended December 31, | ||||||||||||

| 2006 | 2007 | 2008 | ||||||||||

| Cost of revenues | $ | 317 | $ | 926 | $ | 547 | ||||||

| Selling and marketing | 1,263 | 1,118 | 400 | |||||||||

| Software development | 202 | 340 | 423 | |||||||||

| General and administrative | 2,373 | 3,056 | 3,570 | |||||||||

| Total | $ | 4,155 | $ | 5,440 | $ | 4,940 | ||||||

| Year Ended December 31, | ||||||||||||

| 2008 | 2009 | 2010 | ||||||||||

| Cost of revenues | $ | 547 | $ | 888 | $ | 1,504 | ||||||

| Selling and marketing | 400 | 1,125 | 1,518 | |||||||||

| Software development | 423 | 588 | 949 | |||||||||

| General and administrative | 3,570 | 3,859 | 4,335 | |||||||||

| Total | $ | 4,940 | $ | 6,460 | $ | 8,306 | ||||||

| Building | Thirty-nine years | |

| Leasehold improvements | Shorter of lease term or useful life | |

| Furniture and office equipment | Five to | |

| Research vehicles | Five years | |

| Computer hardware and software | Two to five years |

| Working capital | $ | (5,479 | ) | |

| Acquired trade names and other | 810 | |||

| Acquired customer base | 5,300 | |||

| Acquired database technology | 3,700 | |||

| Goodwill | 16,572 | |||

| Total purchase consideration | $ | 20,903 |

| Purchase price in cash and stock | $ | 4,499 | ||

| Deferred consideration | 3,052 | |||

| Total purchase consideration | $ | 7,551 | ||

| Working capital | $ | (550 | ) | |

| Acquired trade names and other | 430 | |||

| Acquired customer base | 890 | |||

| Acquired database technology | 1,200 | |||

| Goodwill | 5,581 | |||

| Total purchase consideration | $ | 7,551 |

| Maturity | Fair Value | |||

| Due in: | ||||

| 2009 | $ | 5,226 | ||

| 2010-2013 | 26,881 | |||

| 2014-2018 | 917 | |||

| 2019 and thereafter | 31,131 | |||

| 64,155 | ||||

| Securities with multiple maturities | 453 | |||

| Investments | $ | 64,608 | ||

| Maturity | Fair Value | |||

| Due in: | ||||

| 2011 | $ | 46 | ||

| 2012-2015 | 3,603 | |||

| 2016-2020 | 73 | |||

| 2021 and thereafter | 29,189 | |||

| Available-for-sale investments | $ | 32,911 | ||

Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||

| Collateralized debt obligations | $ | 46 | $ | ¾ | $ | ¾ | $ | 46 | |||||||||

| Corporate debt securities | 3,407 | 196 | ¾ | 3,603 | |||||||||||||

Government-sponsored enterprise obligations | 74 | ¾ | (1 | ) | 73 | ||||||||||||

Auction rate securities | 32,175 | ¾ | (2,986 | ) | 29,189 | ||||||||||||

Available-for-sale investments | $ | 35,702 | $ | 196 | $ | (2,987 | ) | $ | 32,911 | ||||||||

Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||

| Collateralized debt obligations | $ | 12,987 | $ | 5 | $ | (14 | ) | $ | 12,978 | ||||||||

| Corporate debt securities | 6,396 | 331 | ¾ | 6,727 | |||||||||||||

Residential mortgage-backed securities | 394 | ¾ | (7 | ) | 387 | ||||||||||||

Government-sponsored enterprise obligations | 97 | ¾ | (1 | ) | 96 | ||||||||||||

Auction rate securities | 32,750 | ¾ | (3,026 | ) | 29,724 | ||||||||||||

Available-for-sale investments | $ | 52,624 | $ | 336 | $ | (3,048 | ) | $ | 49,912 | ||||||||

| December 31, | ||||||||||||||||

| 2009 | 2010 | |||||||||||||||

Aggregate Fair Value | Gross Unrealized Losses | Aggregate Fair Value | Gross Unrealized Losses | |||||||||||||

Collateralized debt obligations | $ | 7,578 | $ | (14 | ) | $ | ¾ | $ | ¾ | |||||||

| Residential mortgage-backed securities | 387 | (7 | ) | ¾ | ¾ | |||||||||||

Government-sponsored enterprise obligations | 96 | (1 | ) | 73 | (1 | ) | ||||||||||

Auction rate securities | 29,724 | (3,026 | ) | 29,189 | (2,986 | ) | ||||||||||

| $ | 37,785 | $ | (3,048 | ) | $ | 29,262 | $ | (2,987 | ) | |||||||

| December 31, | ||||||||||||||||

| 2007 | 2008 | |||||||||||||||

Aggregate Fair Value | Gross Unrealized Losses | Aggregate Fair Value | Gross Unrealized Losses | |||||||||||||

| Federal debt securities | $ | 1,592 | $ | (15 | ) | $ | ¾ | $ | ¾ | |||||||

| Corporate debt securities | 13,886 | (49 | ) | 22,136 | (1,494 | ) | ||||||||||

| $ | 15,478 | $ | (64 | ) | $ | 22,136 | $ | (1,494 | ) | |||||||

| December 31, | ||||||||||||||||

| 2007 | 2008 | |||||||||||||||

Aggregate Fair Value | Gross Unrealized Losses | Aggregate Fair Value | Gross Unrealized Losses | |||||||||||||

| Auction rate securities | $ | ¾ | $ | ¾ | $ | 29,340 | $ | (3,710 | ) | |||||||

| Federal debt securities | 531 | (1 | ) | 19 | (1 | ) | ||||||||||

| Corporate debt securities | 21,234 | (148 | ) | 6,976 | (366 | ) | ||||||||||

| $ | 21,765 | $ | (149 | ) | $ | 36,335 | $ | (4,077 | ) | |||||||

| Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||||||||

| Assets: | ||||||||||||||||||||||||||||||||

| Cash | $ | 29,297 | $ | ¾ | $ | ¾ | $ | 29,297 | $ | 55,496 | $ | ¾ | $ | ¾ | $ | 55,496 | ||||||||||||||||

| Money market funds | 130,685 | ¾ | ¾ | 130,685 | 150,909 | ¾ | ¾ | 150,909 | ||||||||||||||||||||||||

Collateralized debt obligations | ¾ | 46 | ¾ | 46 | ||||||||||||||||||||||||||||

| Corporate debt securities | ¾ | 35,132 | ¾ | 35,132 | ¾ | 3,603 | ¾ | 3,603 | ||||||||||||||||||||||||

| Government-sponsored enterprise obligations | ¾ | 136 | ¾ | 136 | ¾ | 73 | ¾ | 73 | ||||||||||||||||||||||||

| Auction rate securities | ¾ | ¾ | 29,340 | 29,340 | ¾ | ¾ | 29,189 | 29,189 | ||||||||||||||||||||||||

| Total | $ | 159,982 | $ | 35,268 | $ | 29,340 | $ | 224,590 | ||||||||||||||||||||||||

Total assets measured at fair value | $ | 206,405 | $ | 3,722 | $ | 29,189 | $ | 239,316 | ||||||||||||||||||||||||

| Liabilities: | ||||||||||||||||||||||||||||||||

Deferred consideration | $ | ¾ | $ | ¾ | $ | 3,222 | $ | 3,222 | ||||||||||||||||||||||||

Total liabilities measured at fair value | $ | ¾ | $ | ¾ | $ | 3,222 | $ | 3,222 | ||||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Assets: | ||||||||||||||||

Cash | $ | 38,721 | $ | ¾ | $ | ¾ | $ | 38,721 | ||||||||

Money market funds | 167,065 | ¾ | ¾ | 167,065 | ||||||||||||

Collateralized debt obligations | ¾ | 12,978 | ¾ | 12,978 | ||||||||||||

Corporate debt securities | ¾ | 6,727 | ¾ | 6,727 | ||||||||||||

Residential mortgage-backed securities | ¾ | 387 | ¾ | 387 | ||||||||||||

Government-sponsored enterprise obligations | ¾ | 96 | ¾ | 96 | ||||||||||||

Auction rate securities | ¾ | ¾ | 29,724 | 29,724 | ||||||||||||

Total assets measured at fair value | $ | 205,786 | $ | 20,188 | $ | 29,724 | $ | 255,698 | ||||||||

| Liabilities: | ||||||||||||||||

Deferred consideration | $ | ¾ | $ | ¾ | $ | 3,082 | $ | 3,082 | ||||||||

Total liabilities measured at fair value | $ | ¾ | $ | ¾ | $ | 3,082 | $ | 3,082 | ||||||||

Auction Rate Securities | Auction Rate Securities | |||||||

| Balance at December 31, 2007 | $ | 53,975 | $ | 53,975 | ||||

| Unrealized loss included in other comprehensive income | (3,710 | ) | ||||||

Unrealized loss included in other comprehensive loss | (3,710 | ) | ||||||

| Settlements | (20,925 | ) | (20,925 | ) | ||||

| Balance at December 31, 2008 | $ | 29,340 | 29,340 | |||||

Unrealized gain included in other comprehensive loss | 684 | |||||||

Settlements | (300 | ) | ||||||

Balance at December 31, 2009 | 29,724 | |||||||

Unrealized gain included in other comprehensive loss | 40 | |||||||

Settlements | (575 | ) | ||||||

Balance at December 31, 2010 | $ | 29,189 | ||||||

| Deferred Consideration | ||||

Balance at December 31, 2008 | $ | ¾ | ||

Deferred consideration upon acquisition | 3,052 | |||

Accretion for 2009 | 30 | |||

Balance at December 31, 2009 | 3,082 | |||

Accretion for 2010 | 140 | |||

Balance at December 31, 2010 | $ | 3,222 | ||

| December 31, | December 31, | |||||||||||||||

| 2007 | 2008 | 2009 | 2010 | |||||||||||||

Building | $ | ¾ | $ | 42,920 | ||||||||||||

| Leasehold improvements | $ | 8,357 | $ | 7,808 | 10,333 | 16,290 | ||||||||||

| Furniture, office equipment and research vehicles | 19,874 | 19,305 | 20,279 | 21,116 | ||||||||||||

| Computer hardware and software | 27,735 | 27,938 | 28,259 | 24,354 | ||||||||||||

| 55,966 | 55,051 | 58,871 | 104,680 | |||||||||||||

| Accumulated depreciation and amortization | (31,921 | ) | (38,175 | ) | (39,709 | ) | (34,759 | ) | ||||||||

| Property and equipment, net | $ | 24,045 | $ | 16,876 | $ | 19,162 | $ | 69,921 | ||||||||

| United States | International | Total | ||||||||||

Goodwill, December 31, 2008 | $ | 31,547 | $ | 22,781 | $ | 54,328 | ||||||

Acquisitions | 23,858 | ¾ | 23,858 | |||||||||

Effect of foreign currency translation | ¾ | 2,280 | 2,280 | |||||||||

Purchase accounting adjustment | (145 | ) | ¾ | (145 | ) | |||||||

Goodwill, December 31, 2009 | 55,260 | 25,061 | 80,321 | |||||||||

Effect of foreign currency translation | ¾ | (719 | ) | (719 | ) | |||||||

Goodwill, December 31, 2010 | $ | 55,260 | $ | 24,342 | $ | 79,602 | ||||||

| United States | International | Total | ||||||||||

| Goodwill, December 31, 2006 | $ | 30,428 | $ | 16,069 | $ | 46,497 | ||||||

| Acquisitions | ¾ | 14,806 | 14,806 | |||||||||

| Effect of foreign currency translation | ¾ | 551 | 551 | |||||||||

| Goodwill, December 31, 2007 | 30,428 | 31,426 | 61,854 | |||||||||

| Acquisitions | 1,119 | ¾ | 1,119 | |||||||||

| Effect of foreign currency translation | ¾ | (8,645 | ) | (8,645 | ) | |||||||

| Goodwill, December 31, 2008 | $ | 31,547 | $ | 22,781 | $ | 54,328 | ||||||

| Weighted-Average | ||||||||||||

| December 31, | Amortization Period | |||||||||||

| 2009 | 2010 | (in years) | ||||||||||

Building photography | $ | 11,504 | $ | 11,771 | 5 | |||||||

Accumulated amortization | (9,089 | ) | (10,311 | ) | ||||||||

Building photography, net | 2,415 | 1,460 | ||||||||||

Acquired database technology | 25,790 | 26,034 | 4 | |||||||||

Accumulated amortization | (21,144 | ) | (22,150 | ) | ||||||||

Acquired database technology, net | 4,646 | 3,884 | ||||||||||

Acquired customer base | 55,770 | 55,380 | 10 | |||||||||

Accumulated amortization | (41,208 | ) | (43,349 | ) | ||||||||

Acquired customer base, net | 14,562 | 12,031 | ||||||||||

Acquired trade names and other | 9,755 | 9,640 | 7 | |||||||||

Accumulated amortization | (7,988 | ) | (8,241 | ) | ||||||||

| Acquired trade names and other, net | 1,767 | 1,399 | ||||||||||

Intangibles and other assets, net | $ | 23,390 | $ | 18,774 | ||||||||

December 31, | Weighted- Average Amortization Period (in years) | ||||||||

| 2007 | 2008 | ||||||||

| Building photography | $ | 10,799 | $ | 11,011 | 5 | ||||

| Accumulated amortization | (6,708 | ) | (7,711 | ) | |||||

| Building photography, net | 4,091 | 3,300 | |||||||

| Acquired database technology | 21,390 | 20,711 | 4 | ||||||

| Accumulated amortization | (20,573 | ) | (20,361 | ) | |||||

| Acquired database technology, net | 817 | 350 | |||||||

| Acquired customer base | 50,891 | 48,198 | 10 | ||||||

| Accumulated amortization | (34,374 | ) | (37,192 | ) | |||||

| Acquired customer base, net | 16,517 | 11,006 | |||||||

| Acquired trade names and other | 9,089 | 7,744 | 6 | ||||||

| Accumulated amortization | (4,803 | ) | (5,979 | ) | |||||

| Acquired trade names and other, net | 4,286 | 1,765 | |||||||

| Intangibles and other assets, net | $ | 25,711 | $ | 16,421 | |||||

| Year Ended December 31, | ||||||||||||||||||||||||

| 2006 | 2007 | 2008 | Year Ended December 31, | |||||||||||||||||||||

| 2008 | 2009 | 2010 | ||||||||||||||||||||||

| Current: | ||||||||||||||||||||||||

| Federal | $ | 414 | $ | 574 | $ | 18,289 | $ | 18,289 | $ | 15,194 | $ | 7,061 | ||||||||||||

| State | 220 | 821 | 3,842 | 3,842 | 1,593 | 1,424 | ||||||||||||||||||

Foreign | ¾ | 26 | 61 | |||||||||||||||||||||

| Total current | 634 | 1,395 | 22,131 | 22,131 | 16,813 | 8,546 | ||||||||||||||||||

| Deferred: | ||||||||||||||||||||||||

| Federal | 7,497 | 9,716 | (408 | ) | (408 | ) | (2,097 | ) | 1,706 | |||||||||||||||

| State | 1,077 | 72 | (52 | ) | (52 | ) | (199 | ) | (6 | ) | ||||||||||||||

| Foreign | (692 | ) | (1,237 | ) | (1,592 | ) | (1,592 | ) | (122 | ) | (25 | ) | ||||||||||||

| Total deferred | 7,882 | 8,551 | (2,052 | ) | (2,052 | ) | (2,418 | ) | 1,675 | |||||||||||||||

| Total provision for income taxes | $ | 8,516 | $ | 9,946 | $ | 20,079 | $ | 20,079 | $ | 14,395 | $ | 10,221 | ||||||||||||

| December 31, | ||||||||||||||||

| 2007 | 2008 | December 31, | ||||||||||||||

| 2009 | 2010 | |||||||||||||||

| Deferred tax assets: | ||||||||||||||||

| Reserve for bad debts | $ | 799 | $ | 928 | $ | 1,093 | $ | 921 | ||||||||

| Accrued compensation | 1,286 | 2,144 | 3,156 | 3,030 | ||||||||||||

| Stock compensation | 1,603 | 2,115 | 3,168 | 3,087 | ||||||||||||

| Net operating losses | 3,177 | 3,077 | 2,985 | 3,365 | ||||||||||||

| Restructuring reserve | 45 | ¾ | ||||||||||||||

| Alternative minimum tax credits | 1,393 | ¾ | ||||||||||||||

Accrued reserve | 238 | 961 | ||||||||||||||

| Capital loss carryovers | ¾ | 345 | 348 | 312 | ||||||||||||

| Unrealized loss on securities | ¾ | 2,088 | 1,076 | 1,074 | ||||||||||||

| Deferred rent | 501 | 1,546 | ||||||||||||||

Deferred revenue | 214 | 1,154 | ||||||||||||||

| Other liabilities | 1,001 | 1,401 | 209 | 226 | ||||||||||||

| Total deferred tax assets | 9,304 | 12,098 | 12,988 | 15,676 | ||||||||||||

| Deferred tax liabilities: | ||||||||||||||||

| Prepaids | (739 | ) | (522 | ) | (638 | ) | (725 | ) | ||||||||

| Depreciation | (427 | ) | (626 | ) | (587 | ) | (2,396 | ) | ||||||||

| Identified intangibles associated with purchase accounting | (4,927 | ) | (2,607 | ) | ||||||||||||

Intangibles | (3,350 | ) | (4,132 | ) | ||||||||||||

| Total deferred tax liabilities | (6,093 | ) | (3,755 | ) | (4,575 | ) | (7,253 | ) | ||||||||

| Net deferred tax asset | 3,211 | 8,343 | 8,413 | 8,423 | ||||||||||||

| Valuation allowance | (63 | ) | (3,047 | ) | (2,985 | ) | (4,670 | ) | ||||||||

| Net deferred taxes | $ | 3,148 | $ | 5,296 | $ | 5,428 | $ | 3,753 | ||||||||

| Year Ended December 31, | ||||||||||||

| 2006 | 2007 | 2008 | ||||||||||

| Expected federal income tax provision at statutory rate | $ | 7,115 | $ | 8,805 | $ | 15,646 | ||||||

| State income taxes, net of federal benefit | 1,014 | 841 | 2,505 | |||||||||

| Foreign income taxes, net effect | 119 | 156 | 497 | |||||||||

| Stock compensation | 528 | 146 | 87 | |||||||||

| (Decrease) increase in valuation allowance | (267 | ) | (274 | ) | 1,023 | |||||||

| Other adjustments | 7 | 272 | 321 | |||||||||

| Income tax expense, net | $ | 8,516 | $ | 9,946 | $ | 20,079 | ||||||

| Year Ended December 31, | ||||||||||||

| 2008 | 2009 | 2010 | ||||||||||

| Expected federal income tax provision at statutory rate | $ | 15,646 | $ | 11,581 | $ | 8,229 | ||||||

State income taxes, net of federal benefit | 2,505 | 1,778 | 1,372 | |||||||||

Foreign income taxes, net effect | 497 | 347 | (1,688 | ) | ||||||||

Stock compensation | 87 | 300 | 289 | |||||||||

Increase in valuation allowance | 1,023 | 1,446 | 1,657 | |||||||||

Disregarded entity election | ¾ | (1,477 | ) | (992 | ) | |||||||

| Nondeductible compensation | ¾ | 140 | 945 | |||||||||

Other adjustments | 321 | 280 | 409 | |||||||||

Income tax expense, net | $ | 20,079 | $ | 14,395 | $ | 10,221 | ||||||

| Unrecognized tax benefit as of January 1, 2007 | $ | 217 | ||

| Increase for current year tax positions | 44 | |||

| Increase for prior year tax positions | (6 | ) | ||

| Expiration of the statute of limitation for assessment of taxes | (22 | ) | ||

| Unrecognized tax benefit as of December 31, 2007 | $ | 233 |

| Unrecognized tax benefit as of December 31, 2007 | $ | 233 | $ | 233 | ||||

| Increase for current year tax positions | 1,451 | |||||||

| Decrease for prior year tax positions | (9 | ) | ||||||

| Expiration of the statute of limitation for assessment of taxes | (117 | ) | ||||||

| Unrecognized tax benefit as of December 31, 2008 | 1,558 | |||||||

| Increase for current year tax positions | 1,451 | 69 | ||||||

| Increase for prior year tax positions | (9 | ) | 257 | |||||

| Expiration of the statute of limitation for assessment of taxes | (117 | ) | (28 | ) | ||||

| Unrecognized tax benefit as of December 31, 2008 | $ | 1,558 | ||||||

| Unrecognized tax benefit as of December 31, 2009 | 1,856 | |||||||

| Increase for current year tax positions | 70 | |||||||

| Decrease for prior year tax positions | (116 | ) | ||||||

| Expiration of the statute of limitation for assessment of taxes | (44 | ) | ||||||

| Unrecognized tax benefit as of December 31, 2010 | $ | 1,766 | ||||||

| 2009 | $ | 8,264 | ||||||

| 2010 | 5,652 | |||||||

| 2011 | 4,389 | $ | 8,691 | |||||

| 2012 | 3,221 | 7,774 | ||||||

| 2013 | 1,055 | 5,331 | ||||||

| 2014 and thereafter | 1,015 | |||||||

2014 | 3,567 | |||||||

2015 | 3,341 | |||||||

2016 and thereafter | 18,749 | |||||||

| $ | 23,596 | $ | 47,453 | |||||

| Year Ended December 31, | ||||||||||||

| 2006 | 2007 | 2008 | ||||||||||

| Revenues | ||||||||||||

| United States | $ | 146,073 | $ | 170,298 | $ | 190,075 | ||||||

| International | 12,816 | 22,507 | 22,353 | |||||||||

| Total revenues | $ | 158,889 | $ | 192,805 | $ | 212,428 | ||||||

| EBITDA | ||||||||||||

| United States | $ | 26,205 | $ | 32,872 | $ | 58,813 | ||||||

| International | (315 | ) | 1,127 | (2,224 | ) | |||||||

| Total EBITDA | $ | 25,890 | $ | 33,999 | $ | 56,589 | ||||||

| Reconciliation of EBITDA to net income | ||||||||||||

| EBITDA | $ | 25,890 | $ | 33,999 | $ | 56,589 | ||||||

| Purchase amortization in cost of revenues | (1,205 | ) | (2,170 | ) | (2,284 | ) | ||||||

| Purchase amortization in operating expenses | (4,183 | ) | (5,063 | ) | (4,880 | ) | ||||||

| Depreciation and other amortization | (6,421 | ) | (8,914 | ) | (9,637 | ) | ||||||

| Interest income, net | 6,845 | 8,045 | 4,914 | |||||||||

| Income tax expense, net | (8,516 | ) | (9,946 | ) | (20,079 | ) | ||||||

| Net income | $ | 12,410 | $ | 15,951 | $ | 24,623 | ||||||

| Year Ended December 31, | ||||||||||||

| 2008 | 2009 | 2010 | ||||||||||

| Revenues | ||||||||||||

United States | $ | 190,075 | $ | 191,556 | $ | 208,463 | ||||||

| International | ||||||||||||

External customers | 22,353 | 18,103 | 17,797 | |||||||||

Intersegment revenue | ¾ | 898 | 1,266 | |||||||||

Total international revenue | 22,353 | 19,001 | 19,063 | |||||||||

Intersegment eliminations | ¾ | (898 | ) | (1,266 | ) | |||||||

Total revenues | $ | 212,428 | $ | 209,659 | $ | 226,260 | ||||||

| EBITDA | ||||||||||||

United States | $ | 58,813 | $ | 47,697 | $ | 39,607 | ||||||

International | (2,224 | ) | (1,186 | ) | (3,183 | ) | ||||||

Total EBITDA | $ | 56,589 | $ | 46,511 | $ | 36,424 | ||||||

| Reconciliation of EBITDA to net income | ||||||||||||

EBITDA | $ | 56,589 | $ | 46,511 | $ | 36,424 | ||||||

Purchase amortization in cost of revenues | (2,284 | ) | (2,389 | ) | (1,471 | ) | ||||||

Purchase amortization in operating expenses | (4,880 | ) | (3,412 | ) | (2,305 | ) | ||||||

Depreciation and other amortization | (9,637 | ) | (8,875 | ) | (9,873 | ) | ||||||

Interest income, net | 4,914 | 1,253 | 735 | |||||||||

Income tax expense, net | (20,079 | ) | (14,395 | ) | (10,221 | ) | ||||||

Net income | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||

| December 31, | ||||||||

| 2007 | 2008 | |||||||

| Property and equipment, net | ||||||||

| United States | $ | 18,162 | $ | 13,927 | ||||

| International | 5,883 | 2,949 | ||||||

| Total property and equipment, net | $ | 24,045 | $ | 16,876 | ||||

| Goodwill | ||||||||

| United States | $ | 30,428 | $ | 31,547 | ||||

| International | 31,426 | 22,781 | ||||||

| Total goodwill | $ | 61,854 | $ | 54,328 | ||||

| Assets | ||||||||

| United States | $ | 308,373 | $ | 353,084 | ||||

| International | 72,659 | 43,474 | ||||||

| Total segment assets | $ | 381,032 | $ | 396,558 | ||||

| Reconciliation of segment assets to total assets | ||||||||

| Total segment assets | $ | 381,032 | $ | 396,558 | ||||

| Investment in subsidiaries | (18,343 | ) | (18,343 | ) | ||||

| Intercompany receivables | (40,846 | ) | (43,831 | ) | ||||

| Total assets | $ | 321,843 | $ | 334,384 | ||||

| Liabilities | ||||||||

| United States | $ | 21,581 | $ | 24,180 | ||||

| International | 61,025 | 40,053 | ||||||

| Total segment liabilities | $ | 82,606 | $ | 64,233 | ||||

| Reconciliation of segment liabilities to total liabilities | ||||||||

| Total segment liabilities | $ | 82,606 | $ | 64,233 | ||||

| Intercompany payables | (42,568 | ) | (33,270 | ) | ||||

| Total liabilities | $ | 40,038 | $ | 30,963 | ||||

| December 31, | ||||||||

| 2009 | 2010 | |||||||

| Property and equipment, net | ||||||||

| United States | $ | 14,851 | $ | 67,076 | ||||

| International | 4,311 | 2,845 | ||||||

| Total property and equipment, net | $ | 19,162 | $ | 69,921 | ||||

| Goodwill | ||||||||

| United States | $ | 55,260 | $ | 55,260 | ||||

| International | 25,061 | 24,342 | ||||||

| Total goodwill | $ | 80,321 | $ | 79,602 | ||||

| Assets | ||||||||

| United States | $ | 424,479 | $ | 469,449 | ||||

International | 44,558 | 39,038 | ||||||

Total segment assets | $ | 469,037 | $ | 508,487 | ||||

| Reconciliation of segment assets to total assets | ||||||||

| Total segment assets | $ | 469,037 | $ | 508,487 | ||||

| Investment in subsidiaries | (18,344 | ) | (18,344 | ) | ||||

| Intercompany receivables | (46,114 | ) | (50,495 | ) | ||||

| Total assets | $ | 404,579 | $ | 439,648 | ||||

| Liabilities | ||||||||

United States | $ | 37,838 | $ | 52,482 | ||||

| International | 46,678 | 47,944 | ||||||

| Total segment liabilities | $ | 84,516 | $ | 100,426 | ||||

| Reconciliation of segment liabilities to total liabilities | ||||||||

| Total segment liabilities | $ | 84,516 | $ | 100,426 | ||||

| Intercompany payables | (38,943 | ) | (42,280 | ) | ||||

Total liabilities | $ | 45,573 | $ | 58,146 | ||||

| Year Ended December 31, | ||||||||||||

| 2006 | 2007 | 2008 | ||||||||||

| Numerator: | ||||||||||||

| Net income | $ | 12,410 | $ | 15,951 | $ | 24,623 | ||||||

| Denominator: | ||||||||||||

Denominator for basic net income per share ¾ weighted-average outstanding shares | 18,751 | 19,044 | 19,372 | |||||||||

| Effect of dilutive securities: | ||||||||||||

| Stock options and restricted stock | 414 | 360 | 178 | |||||||||

Denominator for diluted net income per share ¾ weighted-average outstanding shares | 19,165 | 19,404 | 19,550 | |||||||||

Net income per share ¾ basic | $ | 0.66 | $ | 0.84 | $ | 1.27 | ||||||

Net income per share ¾ diluted | $ | 0.65 | $ | 0.82 | $ | 1.26 | ||||||

| Year Ended December 31, | ||||||||||||

| 2008 | 2009 | 2010 | ||||||||||

| Numerator: | ||||||||||||

Net income | $ | 24,623 | $ | 18,693 | $ | 13,289 | ||||||

| Denominator: | ||||||||||||