UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

|

| | | | |

x☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 3, 20181, 2020

or

|

| | | | |

¨☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-30877

Marvell Technology Group Ltd.

(Exact name of registrant as specified in its charter)

|

| | | | | | | |

| Bermuda | | 77-0481679 |

(State or other jurisdiction of

incorporation or organization)

| | (I.R.S. Employer

Identification No.)

|

Canon’s Court, 22 Victoria Street, Hamilton HM 12, Bermuda

(Address of principal executive offices)

(441) 296-6395

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common shares, $0.002 par value per share | MRVL | The NASDAQNasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨☐No x☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨☐ No x☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x☒ No ¨☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x☒ No ¨☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large“large accelerated filer," "accelerated” “accelerated filer," "smaller” “smaller reporting company,"” and "emerging“emerging growth company"company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | | | | | | |

Large accelerated filer x☒ | Accelerated filer ¨ ☐ | Non-accelerated filer ¨ ☐ | Smaller reporting company ¨ ☐ | Emerging growth company ¨ ☐ |

| | (Do not check if a smaller reporting company) | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨☐ No x☒

The aggregate market value of the registrant’s common shares held by non-affiliates of the registrant was $5,333,299,261$16,535,444,225 based upon the closing price of $15.59$25.03 per share on the NASDAQNasdaq Global Select Market on July 28, 2017August 2, 2019 (the last business day of the registrant’s most recently completed second quarter). Common shares held by each director and executive officer of the registrant, as well as shares held by each holder of more than 5% of the common shares known to the registrant (based on Schedule 13G filings), have been excluded for purposes of the foregoing calculation.

As of March 22, 2018,16, 2020, there were 496.5663.1 million common shares of the registrant outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Part III of this Form 10-K are incorporated by reference from the registrant’s definitive proxy statement for its 20182020 annual general meeting of shareholders, which proxy statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year covered by this Form 10-K. Except with respect to information specifically incorporated by reference in this Form 10-K, the proxy statement is not deemed to be filed as part of this Form 10-K.

Marvell®, Alaska®, ARMADA® Avanta®, Avastar®, Kirkwood®, Link Street®, Prestera®, Xelerated® and Yukon® are registered trademarks of Marvell International Ltd. and/or its affiliates. Any other trademarks or trade names mentioned are the property of their respective owners.

TABLE OF CONTENTS

| | | | | | | | |

| | Page |

| | |

| | |

| Item 1. | | Page |

|

| | |

Item 1.1A. | | |

Item 1A.1B. | | |

Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | |

| | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| | |

| | |

| Item 15. | | |

| | |

| | |

MARVELL TECHNOLOGY GROUP LTD.

Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. These statements involve known and unknown risks, uncertainties and other factors, which may cause our actual results to differ materially from those implied by the forward-looking statements. Words such as “anticipates,” “expects,” “intends,” “plans,” “projects,” “believes,” “seeks,” “estimates,” "forecasts," "targets," “may,” “can,” “will,” “would” and similar expressions identify such forward-looking statements.

Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those indicated in the forward-looking statements. Factors that could cause actual results to differ materially from those predicted include, but are not limited to:

•the impact of actual or potential public health emergencies such as the Novel Coronavirus (COVID-19);

•our ability to completeimplement our plans, forecasts and other expectations with respect to our acquisitions and to fully realize the merger with Cavium, Inc. on a timely basis, or at all;anticipated synergies and cost savings in the time frame anticipated;

•our ability to define, design and develop products for the infrastructure and 5G market and to market and sell those products to infrastructure customers;

•our dependence on a small number of customers;

•severe financial hardship or bankruptcy of one or more of our major customers;

•the effects of any potential future acquisitions, strategic investments, divestitures, mergers or joint ventures;

•risks associated with acquisition and consolidation activity in the semiconductor industry;

•our ability and the ability of our customers to successfully compete in the markets in which we serve;

•our dependence upon the hard disk drivestorage market, which is highly cyclical and intensely competitive;

•our ability and our customers’ ability to develop new and enhanced products and the adoption of those products in the market;

•decreases in our gross margin and results of operations in the future due to a number of factors;

•our reliance on independent foundries and subcontractors for the manufacture, assembly and testing of our products;

•the risks associated with manufacturing and selling a majority of our products and our customers’ products outside of the United States;

•the effects of transitioning to smaller geometry process technologies;

•our ability to scale our operations in response to changes in demand for existing or new products and services;

•our ability to limit costs related to defective products;

•our ability to recruit and retain experienced executive management as well as highly-skilled engineering and sales and marketing personnel;

•our ability to mitigate risks related to our information technology systems;

•our ability to protect our intellectual property;property, particularly outside of the U.S.;

•our ability to estimate customer demand and future sales accurately;

•our reliance on third-party distributors and manufacturers' representatives to sell our products;

•the impact of international conflict, trade relations between the U.S. and other countries, and continued economic volatility in either domestic or foreign markets;

•the impact and costs associated with changes in international financial and regulatory conditions;conditions such as the addition of new trade tariffs or embargos;

•the impact of any change in our application of the United States federal income tax laws and the loss of any beneficial tax treatment that we currently enjoy;

•our maintenance of an effective system of internal controls;

•our ability to realize expected benefits from restructuring activities;

•the impact of natural disasters and other catastrophic events; and

•the outcome of pending or future litigation and legal proceedings.

Additional factors that could cause actual results to differ materially include the risks discussed in Part I, Item 1A, “Risk Factors.” These forward-looking statements speak only as of the date hereof. Unless required by law, we undertake no obligation to update publicly any forward-looking statements.

PART I

OverviewItem 1. Business

Our Company

Marvell Technology Group Ltd., together with its consolidated subsidiaries (“Marvell,” the “Company,” “we,” or “us”) is a global fabless semiconductor solutions provider of high-performance application-specific standarddata infrastructure products. Our core strength is developing complex System-on-a-Chip (“SoC”) devices, leveragingWe leverage our extensive and growing technology portfolio of intellectual property in the areas of analog, mixed-signal, compute, digital signal processing, networking, security, and embeddedstorage to address critical data infrastructure bottlenecks spanning performance, power, latency and standalone integrated circuits.scalability. Our semiconductor solutions are architected and designed to move, store, process and secure the world’s data faster and more reliably than anyone else. We also develop integrated hardware platforms along with software that incorporates digital computing technologies designedoffer essential technology to service the mounting compute, networking, security and configured to provide an optimized computing solution. Our broad product portfolio includes devices for storage networkingrequirements of the automotive, carrier, data center and connectivity.enterprise data infrastructure markets. We were incorporated in Bermuda in January 1995.

Recent Developments

On September 19, 2019, we completed the acquisition of Aquantia Corp. (“Aquantia”). Aquantia is a manufacturer of high speed transceivers which includes copper and optical physical layer products. The merger consideration was funded with a combination of cash on hand and funds from our revolving line of credit (“Revolving Credit Facility”). See “Note 3 - Business Combinations” for discussion of the acquisition and “Note 12- Debt” for discussion of the debt financing in the Notes to Consolidated Financial Statements set forth in Part II, Item 8 of the Annual Report on Form 10-K.

On November 19, 2017,5, 2019, we entered into an agreementacquired Avera Semiconductor (“Avera”), the Application Specific Integrated Circuit (“ASIC”) business of GlobalFoundries for $593.5 million in cash. An additional $90 million in cash will be paid to acquire additional assets if certain conditions are satisfied within the next 10 months. Avera is a leading provider of ASIC semiconductor solutions. We acquired Avera to expand our ASIC design capabilities. The merger consideration was funded with new debt financing. See “Note 3 - Business Combinations” for discussion of the acquisition and plan“Note 12 - Debt” for discussion of merger (the “Merger Agreement”) with Cavium, Inc. ("Cavium"), pursuantthe debt financing in the Notes to whichthe Consolidated Financial Statements set forth in Part II, Item 8 of the Annual Report on Form 10-K.

On December 6, 2019, we completed the sale of our Wi-Fi Connectivity business to NXP USA, Inc, a subsidiary of Marvell will merge withNXP Semiconductors, N.V. (“NXP”). The divestiture encompasses our portfolio of connectivity solutions, including Wi-Fi, and into Cavium, with Cavium survivingWi-Fi/Bluetooth integrated SOCs and becoming a wholly-owned indirect subsidiaryrelated assets. See “Note 1 - Basis of Marvell (the “Merger”). Cavium is a providerPresentation” for discussion of highly integrated semiconductor processors that enable intelligent processing for wired and wireless infrastructure and cloud for networking, communications, storage and security applications. The Merger is primarily intended to create an opportunity for the combined company to emerge as a leaderdivestiture in infrastructure solutions.

Pursuantthe Notes to the Merger Agreement,Consolidated Financial Statements set forth in Part II, Item 8 of the Annual Report on Form 10-K.

On December 31, 2019, we will issue 2.1757 common shares and pay $40.00 per share in cash, without interest, for each sharecompleted an intra-entity asset transfer of Cavium common stock. The merger consideration will be financed by a mix of cash, new debt financing and issuancecertain of our common shares.

Consummationintellectual property to a subsidiary in Singapore. The internal restructuring aligns the global economic ownership of our intellectual property rights with our current and future business operations. See “Note 16 - Income Taxes” for discussion of such tax effects in the Notes to the Consolidated Financial Statements set forth in Part II, Item 8 of the Merger is subject to customary closing conditions, including, without limitation: (i) the required approval by Cavium shareholders and the Company’s shareholders, which was obtainedAnnual Report on March 16, 2018; (ii) the expiration or early termination of the waiting period applicable to the consummation of the Merger under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, which expired on January 26, 2018, (iii) the receipt of approval from the Committee on Foreign Investment in the U.S. ("CFIUS"), and (iv) the receipt of certain foreign regulatory approvals. In certain circumstances, a termination fee of up to $180 million may be payable by Marvell or Cavium upon termination of the transaction, as more fully described in the Merger Agreement.Form 10-K.

Our registered and mailing address is Canon’s Court, 22 Victoria Street, Hamilton HM 12, Bermuda, and our telephone number there is (441) 296-6395. The address of our U.S. operating subsidiary is Marvell Semiconductor, Inc., 5488 Marvell Lane, Santa Clara, California 95054, and our telephone number there is (408) 222-2500. We also have operations in many countries, including China, India, Israel, Japan, Singapore, South Korea, Taiwan and Vietnam. Our fiscal year ends on the Saturday nearest January 31.

Available Information

Our website address is www.marvell.com. The information contained on ourany website referred to in this Form 10-K does not form any part of this Annual Report on Form 10-K and is not incorporated by reference herein.herein unless expressly noted. We make available free of charge through our website our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after we electronically file this material with, or furnish it to, the U.S. Securities and Exchange Commission (“SEC”). In addition, the SEC’s website, www.sec.gov, contains reports, proxy statements, and other information that we file electronically with the SEC.

Our Markets and Products

OverOur products address the lastdata infrastructure market with our four focus markets being automotive, carrier, data center and enterprise. Our compute, networking, security and storage technologies are essential and differentiating for these markets. The data infrastructure market has several years, we have transitioned from a suppliervery attractive attributes including long product lifecycles, deep customer relationships and are typically sole-sourced.

Our portfolio of stand-alone semiconductor components to a supplier of fully integrated platform solutions. Our platform solutions containintegrate multiple analog, mixed-signal and digital intellectual property components in integrated hardware, along withincorporating -hardware, firmware and software that incorporates digital, analogtechnologies and mixed-signal computing and communication technologies, designed and configuredour system knowledge to provide anour customers highly-integrated optimized solution. Our solutions have become increasingly integrated, with more and more components resulting in an all-in-one solution for their end products. In addition to selling standard product solutions, where the exact same product is sold to multiple customers, we also offer customized solutions which are tailored to a given customer’s end product.specific customer's requirements. The acquisition of Avera has extended our ability to offer custom semiconductor solutions for our data infrastructure customers. The demand for such highly integrated platformcustom solutions is generally driven by technological changes and anticipation of the future needs of device manufacturers and end users, including enterprises, campus and service provider networks and, to anhas been increasing extent, data center providers.

A device manufacturer may require technologies leveraged from one end market product into products for other end markets, integrating components and technologies traditionally associated with one end market with components and technologies from another end market. The integration of these various technologies onto a single piece of silicon is referred to as SoC.

In addition, software has become increasingly important to our business over the last several years and we believe software will become even more relevant as the market expects hardware and software to be delivered as an integrated solution. On-chip software, which acts as the “driver” for the functionality of the chip, has always been a critical part of our business. However, the software and application-level software that we deliver with our products has become significantly more complex as the range of uses and the needs has increased. For example, a solution that we develop for storage or networking can contain software that has a range of functionalities built in. Alternatively, our solution can allow our customers to deployseek greater optimizations and differentiation for their operative systems on top of our chip, as well as deploy their application software on top of our SoC.products and services.

Our current product offerings are primarily in threetwo broad product groups:categories: storage networking and connectivity.networking. In storage, we are a market leader in fibre channel products and data storage controller solutions spanning consumer, mobile, desktopprimarily addressing data center, enterprise, and enterpriseedge computing markets. Our storage solutions enable customers to engineer high-volume products for hard disk drives and solid state drives. Our networking products address end markets in cloud, enterprise, smallinclude custom ASICs, ethernet solutions and medium business and service provider networks. Our connectivityprocessors. These products address end markets in consumer, enterprise, desktop, service provider networks and automotive. Our storage, networking and connectivity products power cutting-edge networks and data centers around the world. The networking and connectivity product group was previously referred to as smart networked devices and solutions.

In connection with the November 2016 announcementall four of our plan to restructure our operations to refocus our researchfocus data infrastructure markets: automotive, carrier, data center and development, increase operational efficiency and improve profitability, we divested three businesses in fiscal 2018. As required, we have retrospectively recast our consolidated statements of operations and balance sheets for all periods presented to reflect these businesses as discontinued operations. Unless noted otherwise, the following discussion refers to our continuing operations. Our net revenue by product group for the last three fiscal years is as follows:enterprise.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended | | | | | | | | | | |

| February 1, 2020 | | | | February 2, 2019 | | | | February 3, 2018 | | |

| (in millions, except for percentages) | | | | | | | | | | |

| Networking | $ | 1,377 | | | 51 | % | | $ | 1,313 | | | 46 | % | | $ | 962 | | | 40 | % |

| Storage | 1,138 | | | 42 | % | | 1,377 | | | 48 | % | | 1,254 | | | 52 | % |

| Other | 184 | | | 7 | % | | 176 | | | 6 | % | | 193 | | | 8 | % |

| Total | $ | 2,699 | | | | | $ | 2,866 | | | | | $ | 2,409 | | | |

|

| | | | | | | | | | | | | | | | | | | | |

| | Year Ended |

| | February 3, 2018 | | | | January 28, 2017 | | | | January 30, 2016 | | |

| | (in millions, except for percentages) |

| Storage | $ | 1,254 |

| | 52 | % | | $ | 1,158 |

| | 50 | % | | $ | 1,201 |

| | 46 | % |

| Networking | 598 |

| | 25 | % | | 590 |

| | 26 | % | | 532 |

| | 20 | % |

| Connectivity | 364 |

| | 15 | % | | 318 |

| | 14 | % | | 441 |

| | 17 | % |

| Other | 193 |

| | 8 | % | | 235 |

| | 10 | % | | 428 |

| | 17 | % |

| Total | $ | 2,409 |

| | | | $ | 2,301 |

| | | | $ | 2,602 |

| | |

Storage

Hard Disk Drive Controllers

Hard disk drive ("HDD") controllers provide high-performance input/output ("I/O") interface control between the HDD and the host system. We support a variety of host system interfaces, including Serial Advanced Technology Attachment ("SATA") and Serial Attached SCSI ("SAS"), which support the complete range of enterprise, desktop and mobile HDDs.

We are a leading HDD controller supplier and currently supply products to all of the major hard drive manufacturers.

Our HDD controllers with advanced technology for HDDs provide a technological advantage that enables a higher level of data storage on smaller form factors and higher volumetric densities.

Our advanced HDD controller SoCs incorporate the latest Marvell IPs, using leading advanced semiconductor process nodes.

Solid-State Drive Controllers

Our solid-state-drive ("SSD") controller SoCs are targeted at the fast growing market for flash-based storage systems for the cloud, enterprise, consumer and mobile computing markets. We support a variety of host system interfaces, including SAS, SATA, peripheral component interconnect express ("PCIe"), and non-volatile memory express ("NVMe").

We are a leading supplier of SSD controllers across a range of customers and market segments.

Our advanced SSD controller SoCs incorporate the latest Marvell technology using leading advanced process nodes.

Our SSD controllers are complemented by our fully featured SDK (software development kit) and FTK (Full Turnkey software solutions.)

HDD Components

In fiscal 2017, Marvell re-entered the HDD preamps business. We are working with a number of customers in developing and qualifying our components.

Data Center Storage Solutions

We develop software-enabled silicon solutions for enterprise, data centers and cloud computing businesses. The solutions include SATA port multipliers, bridges, SATA, SAS and NVMe redundant array of independent disk controllers and converged storage processors.

Networking

Ethernet Solutions

We offer a broad portfolio of Ethernet connectivity is pervasive throughout networking infrastructures built for enterprise, smallsolutions spanning controllers, network adapters, physical transceivers and medium business, home office, service provider and data centers.switches. Our Ethernet solutions address a wide variety of end-customer data infrastructure products for those market spaces, from small, cost-effective applianceshigh-reliability automotive sub-systems to large, high-performance modular enterprise and data center solutions.

Our Ethernet controllers and network adapters are optimized to accelerate and simplify data center and enterprise networking. Our family of products include:provide exceptional value features and performance enabling the most agile and data-intensive applications. They deliver Ethernet connectivity for enterprise-class workstations all the way up to enterprise and cloud data centers.

A broad selection ofOur Ethernet switches withintegrate market-optimized innovative features, such as advanced tunneling and routing, high throughput forwarding, and packet processing that make networks more effective at delivering content.content with low-latency and high-reliability. Our Ethernet switch product portfolio ranges from low-power, five-port switches to highly integrated, multi-terabit Ethernet SoC devices that can be interconnected to form massive network solutions;solutions.

AWe complement our Ethernet switch and infrastructure processors with a broad selection of Ethernet physical-layer transceivers for both fiber and copper interconnect with advanced power management, link security, and time synchronization featuresfeatures. With the acquisition of Aquantia, we have added their multi-gigabit ethernet transceivers to our ethernet product portfolio.

Processors

We offer highly integrated semiconductors that complementprovide single or multiple core processors, along with intelligent Layer 2 through 7 processing of the OSI (Open Systems Interconnection) stack which is the framework that governs network communications within enterprise, datacenter, storage, and carrier markets. All of our Ethernet switchproducts are compatible with standards-based operating systems and embedded communication processors;general-purpose software to enable ease of programming, and are supported by our ecosystem partners.

A familyOur OCTEON multi-core infrastructure processor families provide integrated Layer 4 through 7 data and security processing with additional capabilities at Layers 2 and 3 at line speeds. These software-compatible processors integrate next-generation networking I/Os along with advanced security, storage, and application hardware accelerators, offering programmability for the Layer 2 through Layer 7 processing requirements of single-chip network interface devices offered in ultra-small form factor with low-power consumption andintelligent networks. The OCTEON processors are targeted for client-server network interface cards.

Embedded Communication Processors

Our rangeuse in a wide variety of SoC-embedded communication processors provide multi-core ARM processor architecture optimized to consume low power while simultaneously delivering high-performance per watt. They provide a combination of I/O peripherals,carrier, data center, and enterprise equipment, including Ethernet, SATA, SAS, PCIe and universal serial bus and are ideally suited for a range of end-customer networking applications, such as home gateways, networked storage, control plane applications, routers, switches, andsecurity UTM appliances, content-aware switches, application-aware gateways, wireless access points, 3G/4G/5G wireless base stations, storage arrays, smart network interface controllers, network functions virtualization (NFV) and base stations.software-defined networking (SDN) infrastructure.

Our OCTEON Fusion-M family of wireless baseband infrastructure processors is a highly scalable product family supporting enterprise small cells, high capacity outdoor picocells and microcells all the way up to multi-sector macrocells for multiple wireless protocols including 5G. The key features include highly optimized processor cores, a highly efficient caching subsystem, high memory bandwidth digital signal processing engines along with a host of hardware accelerators. Additionally, multiple OCTEON Fusion-M chips can be cascaded for even denser deployments or higher order multiple-input and multiple-output, or MIMO.

Our NITROX security processor family provides the functionality required for Layer 3 to Layer 5 secure communication in a single chip. These single chip, custom-designed processors provide complete security protocol processing, encryption, authentication and compression algorithms to reduce the load on the system processor and increase total system throughput. The LiquidSecurity product family is a high-performance hardware-based transaction security solution for data center and enterprise applications. It addresses the high-performance security requirements for private key management and administration. This family is available as an adapter with complete software or as a standalone appliance.

Our LiquidIO Server Adapter family is a high-performance, general-purpose programmable adapter platform that enables data centers and enterprises to offload their server processors for higher performance and power efficiencies. The LiquidIO Server Adapter family is supported by a feature rich software development kit that allows customers and partners to develop high-performance SDN (software defined networking) applications with packet processing, switching, security, tunneling, quality of service, and metering.

Our ThunderX server processor family is a highly integrated, scalable family of multi-core SoC processors optimized for cloud and datacenter servers. These processors incorporate highly optimized, full custom cores based on 64-bit ARMv8 instruction set architecture targeting data center and enterprise workloads. ThunderX2 is the second-generation workload optimized ARMv8 processor targeting high-performance cloud data centers and high-performance computing server applications.

Custom ASICs

We develop custom product solutions tailored to individual customer specifications that deliver system-level differentiation for next-generation carrier, networking, data center, machine learning, automotive, aerospace and defense applications. These custom offerings leverage our broad portfolio of technologies being used in our standard products.

Storage

Storage Controllers

We offer a broad portfolio of connectivitystorage controllers for hard disk drives (“HDDs”) and solid-state-drives (“SSDs”) across all high-volume markets. Our controllers integrate several key Marvell technologies spanning compute, networking, security and storage. These key technologies enable our controllers to be optimized performance-power solutions and help our customers high-efficient storage products. Our HDD controllers integrate Marvell’s industry-leading read channel technologies to enable higher volumetric densities at low power profiles and are being used by all the current HDD makers. Our technology density and power differentiators are critical for addressing the fast-growing high-capacity, nearline HDD data center and enterprise markets. To further enhance our HDD controller differentiation and value propositions, we offer customers preamplifier products as part of a chipset with our HDD controllers to increase our customers’ product efficiencies. Our HDD controllers support all the high-volume host system interfaces, including Wi-Fi,Serial Advanced Technology Attachment (“SATA”) and Wi-Fi/Bluetooth integrated SOCs.Serial Attached SCSI (“SAS”), which are critical for the data center and enterprise markets.

Our SSD” controller products leverage our strong HDD controller know-how and system-level expertise. We integrate several of our HDD controller IPs with our flash technologies to deliver optimal solutions for data center, enterprise and client computing markets. Our SSD controller products integrate hardware and firmware components to help accelerate our customers’ time to market and maximize the capabilities of our solutions. Like our HDD controllers, our SSD controllers support all the high-volume SSD host system interfaces, including SAS, SATA, peripheral component interconnect express (“PCIe”), non-volatile memory express (“NVMe”) and NVMe over Fabrics (“NVMe-oF”).

Recently, we have introduced new controller chipset products to enable innovative flash-based storage architectures in data centers and enterprises. These solutions increase overall data center performance, density and scalability while lowering overall power, resulting in lower total cost of ownership for the infrastructure organizations.

Fibre Channel Products

Our QLogic Fibre Channel product family comprises of host bus adapters (HBAs) and controllers for server and storage system connectivity. These products are integrated intoaccelerate enterprise and data center applications, deliver a wide varietyhighly resilient infrastructure, enable greater server virtualization density along with an advanced set of end devices, such as enterprise access points, home gateways, multimedia devices, gaming, printers, automotive infotainmentdata center diagnostic, orchestration and telematics units, and smart industrial devices.quality of service capabilities to optimize IT productivity. Our latest Fibre Channel products are well-positioned to deliver low-powerwell-suited for use with all-flash arrays by offering best-in-class latency and high-performance functionality with cutting-edge technologies, and to lead the fast-paced developments of Wi-Fi 802.11 and Bluetooth standards. Our connectivity product portfolio includes a single stream 1x1, as well as multi-stream 2x2, 4x4 and 8x8 multiple input multiple output devices. We deliver both the radio control and processing as well as the RF components for a complete customer solution.performance.

Other Products

Printing Solutions & Custom ASIC

Our other products include printer SoC products and application processors. Our printer SoC products power many of today’s laser and ink printers and multi-function peripherals. These SoCs include a family of printer-specific standard products, as well as full-custom, application-specific integrated circuits.

Application Processors

Our application processors are targeted for non-mobile applications and deliver leading-edge performance for today’s embedded and Internet of Things solutions.

Financial Information about Segments and Geographic Areas

We have determined that we operate in one reportable segment: the design, development and sale of integrated circuits. For information regarding our revenue by geographic area, and property and equipment by geographic area, please see “Note 15 —18 - Segment and Geographic Information” in our Notes to the Consolidated Financial Statements set forth in Part II, Item 8 of this Annual Report on Form 10-K. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K for a discussion of the risks associated with our international operations.

Customers, Sales and Marketing

Our target customers are original equipment manufacturers and original design manufacturers, both of which design and manufacture end market devices. Our sales force is strategically aligned along key customer lines in order to offer fully integrated platforms to our customers. In this way, we believe we can more effectively offer a broader set of content into our key customers’ end products, without having multiple product groups separately engage the same customer. We complement and support our direct sales force with manufacturers’ representatives for our products in North America, Europe and Asia. In addition, we have distributors who support our sales and marketing activities in the United States, Europe and Asia. We also use third-party logistics providers who maintain warehouses in close proximity to our customers’ facilities. We expect that a significant percentage of our sales will continue to come from direct sales to key customers.

We use field application engineers to provide technical support and assistance to existing and potential customers in designing, testing and qualifying systems designs that incorporate our products. Our marketing team works in conjunction with our field sales and application engineering force, and is organized around our product groups.

Historically, a relatively small number of customers have accounted for a significant portion of our net revenue. During fiscal year 2020, there was no net revenue attributable to a customer, other than one distributor, whose revenues as a percentage of net revenue was 10% or greater of total net revenues. Net revenue attributable to significant customers whose revenues as a percentage of net revenue was 10% or greater of total net revenues is presented in the following table:

| | | | | | | | | | | | | | | | | |

| Year Ended | | | | |

| February 1, 2020 | | February 2, 2019 | | February 3, 2018 |

| Customer: | | | | | |

| | | | | |

| Western Digital | * | | | 12 | % | | 20 | % |

| Toshiba ** | * | | | 11 | % | | 14 | % |

| Seagate | * | | | 10 | % | | 11 | % |

| Distributor: | | | | | |

| Wintech | 12 | % | | * | | | 10 | % |

| | | | | |

* Less than 10% of net revenue

** The percentage of net revenue reported for Toshiba for fiscal year 2019 excludes net revenue of Toshiba Memory Corporation after Toshiba divested Toshiba Memory Corporation during fiscal year 2019. | | | | | |

|

| | | | | | | | |

| | Year Ended |

| | February 3,

2018 | | January 28,

2017 | | January 30,

2016 |

| Customer: | | | | | |

| Western Digital* | 20 | % | | 21 | % | | 19 | % |

| Toshiba | 14 | % | | 14 | % | | **% |

|

| Seagate | 11 | % | | 9 | % | | 14 | % |

| Distributor: | | | | | |

| Wintech | 10 | % | | 10 | % | | **% |

|

| | | | | | |

| * The percentage of net revenues reported for Western Digital for fiscal year 2018 and fiscal year 2017 includes net revenue of SanDisk, which became a subsidiary of Western Digital in fiscal 2017. |

| ** Less than 10% of net revenue |

A significant numberSome of our products are being incorporated into consumer electronics products, including gaming devices and personal computers, which are subject to significant seasonality and fluctuations in demand. Seasonality, including holiday buying trends, may at times negatively impact our results in the first and fourth quarter, and positively impact our results in the second and third quarter of our fiscal years. In addition, the timing of new product introductions by our customers may cause variations in our quarterly revenues, which may not be indicative of future trends.

Inventory and Working Capital

We place firm orders for products with our suppliers generally up to 16 weeks prior to the anticipated delivery date and typically prior to an order for the product. These lead times typically change based on the current capacity at the foundries. We often maintain substantial inventories of our products because the semiconductor industry is characterized by short lead time orders and quick delivery schedules.

Backlog

We do not believe that backlog is a meaningful or reliable indicator for future demand, due to the following:

•an industry practice that allows customers to cancel or change orders prior to the scheduled shipment dates;

an increasing•a portion of our revenue comes from products shipped to customers using third-party logistics providers, or “hubs” wherein the product can be pulled at any time by the customer and is therefore never reflected in backlog; andbacklog

scheduled future shipments include shipments to distributors for which we do not recognize revenue until the products are sold to end customers.

Research and Development

We believe that our future success depends on our ability to introduce improvements to our existing products and to develop new products that deliver cost-effective solutions for both existing and new markets. Our research and development efforts are directed largely to the development of high-performance analog, mixed-signal, digital signal processing and embedded microprocessor integrated circuits with the smallest die size and lowest power. We devote a significant portion of our resources to expanding our product portfolio based on a broad intellectual property portfolio with designs that enable high-performance, reliable communications over a variety of physical transmission media. We are also focused on incorporating functions currently provided by stand-alone integrated circuits into our integrated platform solutions to reduce our customers’ overall system costs.

We have assembled a core team of engineers who have experience in the areas of mixed-signal circuit design, digital signal processing, embedded microprocessors, complementary metal oxide semiconductor (“CMOS”) technology and system-level architectures. We have invested and will continue to invest a significant amount in research and development. Our research and development expense was $0.7 billion, $0.8 billion and $1.0 billion in fiscal 2018, 2017 and 2016, respectively. See our discussion of research and development expenses in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K for further information.

Manufacturing

Integrated Circuit Fabrication

The vast majority of our integrated circuits are fabricated using widely available CMOS processes, which provide greater flexibility to engage independent foundries to manufacture integrated circuits at lower costs. By outsourcing manufacturing, we are able to avoid the cost associated with owning and operating our own manufacturing facility. This allows us to focus our efforts on the design and marketing of our products. We currently outsource a large percentage of our integrated circuit manufacturing to Taiwan Semiconductor Manufacturing Company. We also utilize United Microelectronics Corporation, with the remaining manufacturing outsourced to other foundries located primarily in Asia. We work closely with our foundry partners to forecast on a monthly basis our manufacturing capacity requirements. We closely monitor foundry production to ensure consistent overall quality, reliability and yield levels. Our integrated circuits are currently fabricated in several advanced manufacturing processes. Because finer manufacturing processes lead to enhanced performance, smaller silicon chip size and lower power requirements, we continually evaluate the benefits and feasibility of migrating to smaller geometry process technology in order to reduce cost and improve performance.

Assembly and Test

We outsource all product packaging and testing requirements for our products in production to several assembly and test subcontractors primarily located in China, Korea, Singapore, Canada and Taiwan.

Environmental Management

We believe that our products comply with the current Restriction of Hazardous Substances Directive, the European legislation that restricts the use of a number of substances, including lead, and the Regulation, Evaluation and Authorization of Chemicals SVHC Substances Directive. In addition, each of our manufacturing subcontractors compliescertifies to us compliance with ISO 14001:2004, the international standard related to environmental management. We are also working to establish a “conflict-free” supply chain, including ethical sourcing of certain minerals for our products.

Intellectual Property

Our future revenue growth and overall success depend in large part on our ability to protect our intellectual property. We rely on a combination of patents, copyrights, trademarks, trade secret laws,secrets, contractual provisions, confidentiality agreements and licenses to protect our intellectual property. As of February 3, 2018,1, 2020, we have approximately 9,50011,400 U.S. and foreign patents issued and approximately 2,3001200 U.S. and foreign patent applications pending on various aspects of our technology. While we believe the duration of our patents generally covers the expected lives of our products, our patents may not collectively or individually cover every feature on innovation in our product. In addition, our efforts may not be sufficient to protect our intellectual property from misappropriation or infringement. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K for a discussion of the risks associated with our patents and intellectual property.

We have expended and will continue to expend considerable resources in establishing a patent position designed to protect our intellectual property. While our ability to compete is enhanced by our ability to protect our intellectual property, we believe that in view of the rapid pace of technological change, the combination of the technical experience and innovative skills of our employees may be as important to our business as the legal protection of our patents and other proprietary information.

From time to time, we may desire or be required to renew or to obtain licenses from third parties in order to further develop and effectively market commercially viable products or in connection with a pending or future claim or action asserted against us. We cannot be sure that any necessary licenses will be available or will be available on commercially reasonable terms.

The integrated circuit industry is characterized by vigorous pursuit and protection of intellectual property rights, which has resulted in significant and often time consuming and expensive litigation. From time to time, we receive, and may continue to receive in the future, notices that claim we have infringed upon, misappropriated or misused the proprietary rights of other parties.

In addition, we have in the past and may in the future be sued by other parties who claim that we have infringed their patents or misappropriated or misused their trade secrets,other intellectual property rights, or who may seek to invalidate one or more of our patents.patents, trademarks, or other rights. Although we defend these claims vigorously, it is possible that we will not prevail in pending or future lawsuits. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K and “Note 10 —13 - Commitments and Contingencies” in our Notes to the Consolidated Financial Statements set forth in Part II, Item 8, of this Annual Report on Form 10-K for further discussion of the risks associated with patent litigation matters.

Competition

The markets for our products particularly in networking and connectivity, are intensely competitive, and are characterized by rapid technological change, evolving industry standards, frequent new product introductions and pricing pressures. Competition has intensified as a result of the increasing demand for higher levels of performance, and integration and smaller process geometries. We expect competition to further intensify as current competitors continue to strengthen the depth and breadth of their product offerings, either through in-house development or by acquiring existing technology. In addition, some of our customers have chosen to develop certain semiconductor products internally and this trend may continue to proliferate. We believe that our ability to compete successfully in the rapidly evolving markets for our products depends on a number ofmultiple factors, including, but not limited to:

•the performance, features, quality and price of our products;

•the timing and success of new product introductions by us, our customers and our competitors;

•emergence, rate of adoption and acceptance of new industry standards;

•our ability to obtain adequate foundry capacity with the appropriate technological capability; and

•the number and nature of our competitors in a given market.

Our major competitors for our products include Advanced Micro Devices Inc., Broadcom Limited, Cypress Semiconductor Corporation, Inphi Corporation, Intel Corporation, MediaTek Inc., QUALCOMM,Mellanox Technologies Limited, Microchip Technology Inc., Quantenna Communications Inc.NXP Semiconductors N.V., Phison Electronics Corporation and Silicon Motion Technology Corporation. We expect increased competition in the future from both emerging orand established companies, oras well as from alliances among competitors, customers or other third parties, any of which could acquire significant market share. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K for a discussion of competitive risks associated with our business.

Historically, average unit selling prices in the integrated circuit industry in general, and for our products in particular, have decreased over the life of a particular product. We expect that the average unit selling prices of our products will continue to be subject to significant pricing pressures. In order to offset expected declines in the selling prices of our products, we will need to continue to introduce innovative new products and reduce the cost of our products. To accomplish this, we intend to continue to implement design changes that lower the cost of manufacturing, assembly and testing of our products. See “Risk Factors” under Item 1A of this Annual Report on Form 10-K for a discussion of pricing risks.

Employees

As of February 3, 2018,1, 2020, we had a total of 3,7495,633 employees.

Item 1A. Risk Factors

Investing in our common shares involves a high degree of risk. You should carefully consider the risks and uncertainties described below and all information contained in this report before you decide to purchase our common shares. Many of these risks and uncertainties are beyond our control, including business cycles and seasonal trends of the computing, infrastructure, semiconductor and related industries and end markets. If any of the possible adverse events described below actually occurs, we may be unable to conduct our business as currently planned and our financial condition and operating results could be harmed. In addition, the trading price of our common shares could decline due to the occurrence of any of these risks, and you could lose all or part of your investment.

7SUMMARY OF FACTORS THAT MAY AFFECT OUR FUTURE RESULTS

Risks Related to Our Proposed Merger with Cavium

Our proposed acquisition of Cavium, Inc. (“Cavium”) involves a number of risks, including, among others, the risk that we fail to complete the acquisition in a timely manner or at all, regulatory risks, risks associated with our use of a significant portion of our cash and our taking on significant indebtedness, other financial risks, integration risks, and risk associated with the reactions of customers, suppliers and employees.

Our and Cavium’s obligations to consummate the proposed transaction (the "Merger") are subject to the satisfaction or waiver of certain conditions, including, among others: (i) the approval of Cavium's shareholders of the merger agreement; (ii) the approval of our shareholders to allow us to issue shares of common stock in connection with the merger agreement; (iii) the receipt of regulatory clearance under applicable U.S. and foreign regulations; (iv) the absence of any law or order prohibiting the proposed transaction; (v) there being no event that would have a material adverse effect on Cavium; and (vi) the accuracy of the representations and warranties of Cavium, subject to certain exceptions, and Cavium’s material compliance with its covenants, in the definitive agreement. We cannot provide assurance that the conditions to the completion of the proposed transaction will be satisfied in a timely manner or at all, and if the proposed transaction is not completed, we would not realize any of the expected benefits. While some of these conditions have been satisfied, several conditions to the Merger have not yet been satisfied.

The regulatory approvals required in connection with the proposed transaction may not be obtained or may contain materially burdensome conditions. If any conditions or changes to the structure of the proposed transaction are required to obtain these regulatory approvals, they may have the effect of jeopardizing or delaying completion of the proposed transaction or reducing our anticipated benefits. If we agree to any material conditions in order to obtain any approvals required to complete the proposed transaction, our business and results of operations may be adversely affected.

In addition, the use of a significant portion of our cash and the incurrence of substantial indebtedness in connection with the financing of the proposed transaction will reduce our liquidity, and may limit our flexibility in responding to other business opportunities and increase our vulnerability to adverse economic and industry conditions.

If the Merger is not completed by September 19, 2018 (subject to a potential extension to November 19, 2018 under certain circumstances, including in the event receipt of certain required regulatory approvals has not been obtained), either Marvell or Cavium may choose to terminate the Merger Agreement. Marvell or Cavium may also elect to terminate the Merger Agreement in certain other circumstances, or they may mutually decide to terminate the Merger Agreement at any time prior to the Effective Time, before or after obtaining shareholder approval, as applicable.

If the proposed transaction is not completed, our stock price could fall to the extent that our current price reflects an assumption that we will complete it. Furthermore, if the proposed transaction is not completed and the purchase agreement is terminated, we would not realize any of the expected benefits of the proposed transaction, and we may suffer other consequences that could adversely affect our business, results of operations and stock price, including, among others:

we could be required to pay a termination fee of up to $180 million;

we will have incurred and may continue to incur costs relating to the proposed transaction, many of which are payable by us whether or not the proposed transaction is completed;

matters related to the proposed transaction (including integration planning) require substantial commitments of time and resources by our management team and numerous others throughout our organization, which could other have been devoted to other opportunities;

we may be subject to legal proceedings related to the proposed transaction or the failure to complete the proposed transaction;

the failure to complete the proposed transaction may result in negative publicity and a negative perception of us in the investment community; and

any disruptions to our business resulting from the announcement and pendency of the proposed transaction, including any adverse changes in our relationships with our customers, supplied, partners or employees, may continue to intensify in the event the proposed transaction is not consummated.

The benefits we expect to realize from the proposed transaction will depend, in part, on our ability to integrate the businesses successfully and efficiently. See also the Risk Factor entitled “Any potential future acquisitions, strategic investments, divestitures, mergers or joint ventures may subject us to significant risks, any of which could harm our business."

Furthermore, uncertainties about the proposed transaction may cause our and/or Cavium’s current and prospective employees to experience uncertainty about their futures. These uncertainties may impair our and/or Cavium’s ability to retain, recruit or motivate key management, engineering, technical and other personnel. Similarly, our and/or Cavium’s existing or prospective customers, licensees, suppliers and/or partners may delay, defer or cease purchasing products or services from or providing products or services to us or Cavium; delay or defer other decisions concerning us or Cavium; or otherwise seek to change the terms on which they do business with us or Cavium. Any of the above could harm us and/or Cavium, and thus decrease the benefits we expect to receive from the proposed transaction.

The proposed transaction may also result in significant charges or other liabilities that could adversely affect our results of operations, such as cash expenses and non-cash accounting charges incurred in connection with our acquisition and/or integration of the business and operations of Cavium. Further, our failure to identify or accurately assess the magnitude of certain liabilities we are assuming in the proposed transaction could result in unexpected litigation or regulatory exposure, unfavorable accounting charges, unexpected increases in taxes due, a loss of anticipated tax benefits or other adverse effects on our business, results of operations, financial condition or cash flows.

Until the completion of the Merger or the termination of the Merger Agreement in accordance with its terms, Marvell and Cavium are each prohibited from entering into certain transactions and taking certain actions that might otherwise be beneficial to Marvell or Cavium and their respective shareholders.

Until the Merger is completed or the Merger Agreement is terminated, the merger agreement dated November 19, 2017 (the "Merger Agreement") restricts Marvell and Cavium from taking specified actions without the consent of the other party, and requires Cavium to conduct its business and operations in the ordinary course in all material respects and substantially in accordance with past practices. These restrictions may prevent Marvell and Cavium from making appropriate changes to their respective businesses or pursuing attractive business opportunities that may arise prior to the completion of the Merger.

The Merger Agreement limits each of Marvell’s and Cavium’s ability to pursue alternative transactions, and in certain instances requires payment of a termination fee, which could deter a third party from proposing an alternative transaction.

The Merger Agreement contains provisions that, subject to certain exceptions, limit each of Marvell’s and Cavium’s ability to solicit, initiate, encourage or facilitate, or enter into discussions or negotiations with respect to, any inquiries regarding or the making of any proposal or offer that constitutes or could reasonably be expected to lead to an alternative transaction. In addition, under specified circumstances, Marvell or Cavium is required to pay a termination fee of $180 million if the Merger Agreement is terminated. It is possible that these or other provisions might discourage a potential competing acquirer that might have an interest in acquiring all or a significant part of Marvell or Cavium from considering or proposing an acquisition or might result in a potential competing acquirer proposing to pay a lower per share price to acquire Marvell or Cavium than it might otherwise have proposed to pay.

The Merger is subject to the receipt of CFIUS Approval that may impose measures to protect U.S. national security or other conditions that could have an adverse effect on Marvell, Cavium, or the combined company, or, if not obtained, could prevent completion of the Merger.

Marvell’s obligation to complete the Merger is conditioned on obtaining CFIUS Approval. In deciding whether to grant CFIUS Approval, CFIUS will consider the effect of the Merger on U.S. national security. As a condition to granting CFIUS Approval, CFIUS may take measures and impose conditions, certain of which (a) could materially and adversely affect the combined company’s operating results due to the imposition of requirements, limitations or costs or the placement of restrictions on the conduct of the combined company’s business and (b) could adversely affect the financial position and prospects of the combined company and its ability to achieve the cost savings and other synergies projected to result from the Merger. There can be no assurance that CFIUS will not impose conditions, terms, obligations or restrictions, or that such conditions, terms, obligations or restrictions will not have the effect of delaying completion of the Merger or imposing additional material costs on, or materially limiting the revenues of, the combined company following the Merger.

Any delay in completing the Merger may significantly reduce the benefits expected to be obtained from the Merger.

In addition to the required regulatory clearances and approvals, the Merger is subject to a number of other conditions that are beyond the control of Marvell and Cavium and that may prevent, delay or otherwise materially adversely affect completion of the Merger. Marvell and Cavium cannot predict whether and when these other conditions will be satisfied. Further, the requirements for obtaining the required regulatory clearances and approvals could delay the completion of the Merger for a significant period of time or prevent it from occurring. Any delay in completing the Merger may significantly reduce the synergies projected to result from the Merger and other benefits that Marvell and Cavium expect to achieve if they complete the Merger within the expected timeframe and integrate their respective businesses.

There can be no assurance that Marvell will be able to secure the funds necessary to pay the cash portion of the Merger Consideration and refinance certain of Cavium’s existing indebtedness on acceptable terms, in a timely manner or at all.

Marvell intends to fund the cash portion of the Merger Consideration to be paid to holders of Cavium common stock with a combination of Marvell’s and Cavium’s cash on hand and debt financing. To this end, Marvell has entered into a debt commitment letter containing commitments for a $900 million term loan facility and an $850 million bridge loan facility. However, neither Marvell nor any of its subsidiaries has entered into definitive agreements for the debt financing (or other financing arrangements in lieu thereof), and the obligation of the lenders to provide the debt financing under the debt commitment letter is subject to a number of customary conditions. There can be no assurance that Marvell will be able to obtain the debt financing pursuant to the debt commitment letter.

In the event that the debt financing contemplated by the debt commitment letter is not available, other financing may not be available on acceptable terms, in a timely manner or at all. If Marvell is unable to obtain debt financing, the Merger may be delayed or not be completed.

Litigation filed against Marvell and Cavium could prevent or delay the completion of the Merger or result in the payment of damages following completion of the Merger.

Marvell, Cavium and members of Cavium’s board of directors currently are and may in the future be parties, among others, to various claims and litigation related to the Merger Agreement and the Merger, including putative shareholder class actions. Two lawsuits have been filed against Marvell and Cavium and its board of directors in federal court: Raul v. Cavium et al., No. 18 Civ. 00139 (N.D. Cal. filed Jan. 8, 2018) (“Raul”); and Rosenblatt v. Cavium et al., No. 18-Civ. 00300 (N.D. Cal. filed Jan. 12, 2018) (“Rosenblatt”). Also in connection with the Merger, two additional lawsuits have been filed against Cavium and its board of directors in federal court; Fineberg v. Cavium, Inc., 18-cv-00011 (filed January 2, 2018, Northern District of California) (“Fineberg”); and Stein v. Cavium, Inc., 18-cv-00141 (filed January 8, 2018, Northern District of California). The Fineberg and Stein complaints do not name Marvell as a defendant. However, as set forth in the Merger Agreement, no settlement of litigation related to the Merger may be agreed to by Cavium without the prior written consent of Marvell. These four complaints assert claims for violation of Section 14(a) of and Rule 14a-9 promulgated under the Exchange Act based on allegations that the registration statement on Form S-4 filed by Marvell with the SEC on December 21, 2017 omits material information. The complaints also assert control person claims under Section 20(a) of the Exchange Act against the Cavium board of directors.

Among other remedies, the plaintiffs in such matters are seeking to enjoin the Merger. The results of complex legal proceedings are difficult to predict, and could delay or prevent the Merger from becoming effective in a timely manner. Moreover, the pending litigation and any future additional litigation could be time consuming and expensive, could divert Marvell’s and Cavium’s management’s attention away from their regular businesses, and, if any one of these lawsuits is adversely resolved against either Marvell or Cavium, could have a material adverse effect on Marvell’s or Cavium’s respective financial condition or the condition of the combined company.

If a settlement or other resolution is not reached in the potential lawsuits referenced above and the plaintiffs secure injunctive or other relief prohibiting, delaying or otherwise adversely affecting Marvell’s or Cavium’s ability to complete the Merger on the terms contemplated by the Merger Agreement, or there is a pending or overtly threatened legal proceeding brought by a governmental party as described above, then the Merger may not become effective in a timely manner or at all.

Factors That May Affect Marvell's Future Results

Our financial condition and results of operations may vary from quarter to quarter, which may cause the price of our common shares to decline.

Our quarterly results of operations have fluctuated in the past and could do so in the future. Because our results of operations are difficult to predict, you should not rely on quarterly comparisons of our results of operations as an indication of our future performance.

Fluctuations in our results of operations may be due to a number of factors, including, but not limited to, those listed below and those identified throughout this “Risk Factors” section:

•the impact of the Novel Coronavirus (COVID-19), or other future pandemics, on the global economy and on our customers, suppliers, employees and business;

•our ability to realize anticipated synergies in connection with our acquisitions and our loss of synergies in connection with our divestitures;

•changes in general economic andconditions, such as the impact of Brexit on the economy in the E.U., political conditions, such as the recent tariffs and trade bans, and specific conditions in the end markets we address, including the continuing volatility in the technology sector and semiconductor industry;

•the effects of any future acquisitions, divestitures or significant investments, including our merger with Cavium, Inc.;investments;

•the highly competitive nature of the end markets we serve, particularly within the semiconductor industry;and infrastructure industries;

•our dependence on a few customers for a significant portion of our revenue;

severe financial hardship or bankruptcy of one or more of our major customers;

•our ability to maintain a competitive cost structure for our manufacturing and assembly and test processes and our reliance on third parties to produce our products;

•any current and future litigation and regulatory investigations that could result in substantial costs and a diversion of management’s attention and resources that are needed to successfully maintain and grow our business;

•cancellations, rescheduling or deferrals of significant customer orders or shipments, as well as the ability of our customers to manage inventory;

•gain or loss of a design win or key customer;

•seasonality inor volatility related to sales of consumer devices in which our products are incorporated;into the infrastructure market;

•failure to qualify our products or our suppliers’ manufacturing lines;

•our ability to develop and introduce new and enhanced products in a timely and effective manner, as well as our ability to anticipate and adapt to changes in technology;

•failure to protect our intellectual property;property, particularly outside the U.S.;

•impact of a significant natural disaster, including earthquakes, fires, floods and tsunamis, particularly in certain regions in which we operate or own buildings, such as Santa Clara, California, and where our third party suppliers operate, such as Taiwan and elsewhere in the Pacific Rim; and

•our ability to attract, retain and motivate a highly skilled workforce, especially managerial, engineering, sales and marketing personnel.personnel;

•severe financial hardship or bankruptcy of one or more of our major customers; and

•failure of our customers to agree to pay for NRE (non-recurring engineering) costs or failure to pay enough to cover the costs we incur in connection with NREs.

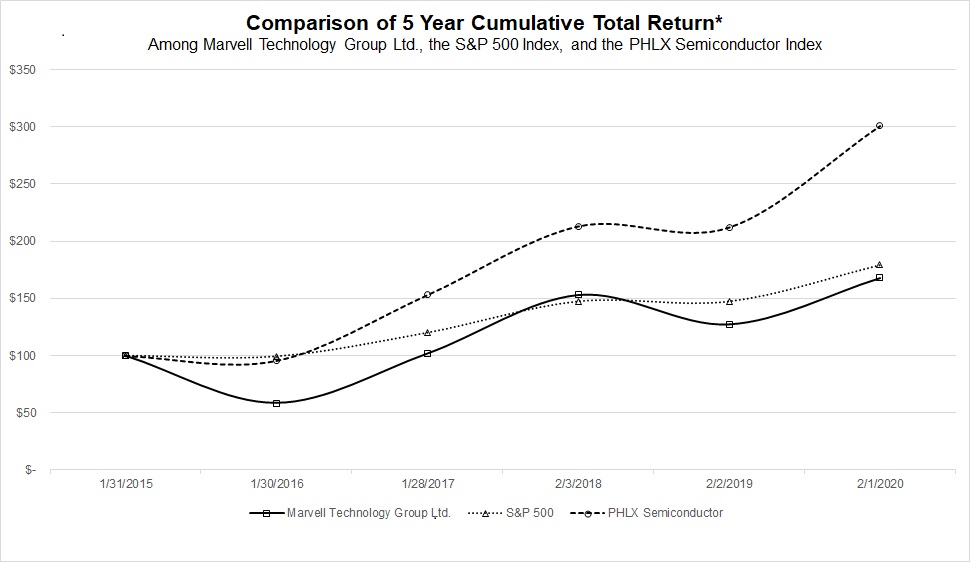

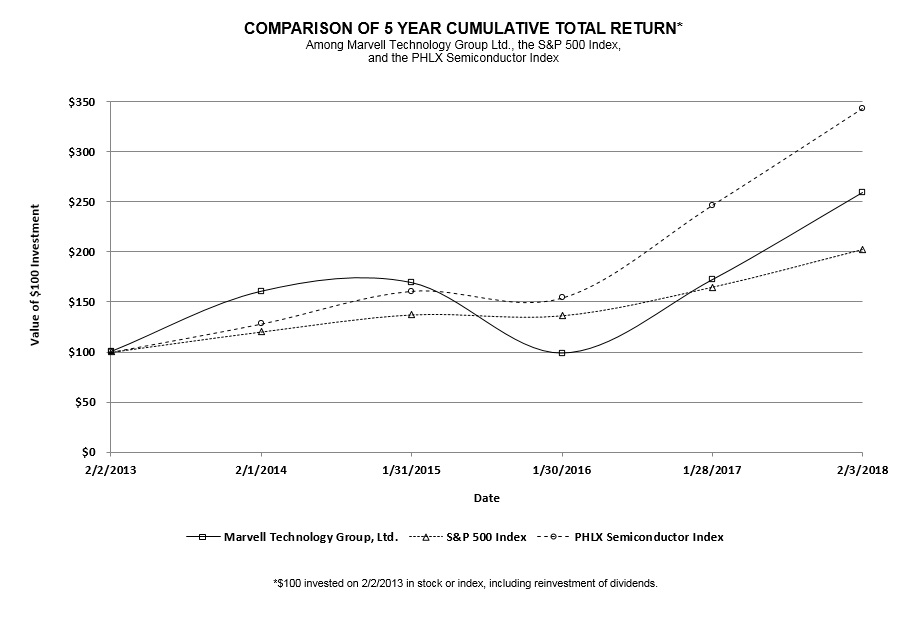

Due to fluctuations in our quarterly results of operations and other factors, the price at which our common shares will trade is likely to continue to be highly volatile. From January 31, 2016 through February 3, 2018, our common shares traded as low as $8.32 and as high as $24.22 per share. Accordingly, you may not be able to resell your common shares at or above the price you paid. In future periods, our stock price could decline if, amongst other factors, our revenue or operating results are below our estimates or the estimates or expectations of securities analysts and investors. Our stock is traded on the Nasdaq stock exchange under the ticker symbol “MRVL”. As a result of stock price volatility, we may be subject to securities class action litigation. Any litigation could result in substantial costs and a diversion of management’s attention and resources that are needed to successfully maintain and grow our business.

WE ARE SUBJECT TO RISKS ASSOCIATED WITH THE NOVEL CORONAVIRUS (COVID-19)

We face risks related to Novel Coronavirus (COVID-19) which could significantly disrupt our manufacturing, research and development, operations, sales and financial results.

Our business will be adversely impacted by the effects of the Novel Coronavirus (COVID-19). In addition to global macroeconomic effects, the Novel Coronavirus (COVID-19) outbreak and any other related adverse public health developments will cause disruption to our international operations and sales activities. Our third-party manufacturers, suppliers, third-party distributors, sub-contractors and customers have been and will be disrupted by worker absenteeism, quarantines and restrictions on our employees’ ability to work, office and factory closures, disruptions to ports and other shipping infrastructure, border closures, or other travel or health-related restrictions. Depending on the magnitude of such effects on our manufacturing, assembling, and testing activities or the operations of our suppliers, third-party distributors, or sub-contractors, our supply chain, manufacturing and product shipments will be delayed, which could adversely affect our business, operations and customer relationships. In addition, the Novel Coronavirus (COVID-19) or other disease outbreak will in the short-run and may over the longer term adversely affect the economies and financial markets of many countries, resulting in an economic downturn that will affect demand for our products and impact our operating results. There can be no assurance that any decrease in sales resulting from the Novel Coronavirus (COVID-19) will be offset by increased sales in subsequent periods. Although the magnitude of the impact of the Novel Coronavirus (COVID-19) outbreak on our business and operations remains uncertain, the continued spread of the Novel Coronavirus (COVID-19) or the occurrence of other epidemics and the imposition of related public health measures and travel and business restrictions will adversely impact our business, financial condition, operating results and cash flows. In addition, we have experienced and will experience disruptions to our business operations resulting from quarantines, self-isolations, or other movement and restrictions on the ability of our employees to perform their jobs that may impact our ability to develop and design our products in a timely manner or meet required milestones or customer commitments. See the Risk Factor entitled “If we are unable to develop and introduce new and enhanced products that achieve market acceptance in a timely and cost-effective manner, our results of operations and competitive position will be harmed.” These disruptions may also impact our ability to win in time sensitive competitive bidding selection processes. See the Risk Factor entitled “We rely on our customers to design our products into their systems, and the nature of the design process requires us to incur expenses prior to customer commitments to use our products or recognizing revenues associated with those expenses which may adversely affect our financial results.”

WE ARE SUBJECT TO RISKS ASSOCIATED WITH OUR STRATEGIC TRANSACTIONS

Recent or potential future acquisitions, strategic investments, divestitures, mergers or joint ventures may subject us to significant risks, any of which could harm our business.

Our long-term strategy may include identifying and acquiring, investing in or merging with suitable candidates on acceptable terms, or divesting of certain business lines or activities. In particular, over time, we may acquire, make investments in, or merge with providers of product offerings that complement our business or may terminate such activities.

On May 6, 2019, we entered into a definitive merger agreement to acquire all outstanding shares of Aquantia Corp. common stock for $13.25 per share in cash. On September 19, 2019, we completed the acquisition of Aquantia for total merger consideration in the amount of $502.2 million.

On May 20, 2019, we entered into a definitive agreement to purchase Avera Semiconductor, the Application Specific Integrated Circuit (ASIC) business of GlobalFoundries (“Avera”). On November 5, 2019, we completed the acquisition. Total purchase consideration consisted of cash consideration paid to GlobalFoundries of $593.5 million, net of final working capital adjustments. An additional $90 million in cash will be paid if certain business conditions are satisfied by the third quarter of our fiscal 2021. GlobalFoundries and the Company are currently discussing whether the necessary conditions have been satisfied to pay the $90 million. There can be no assurance that the discussions will be resolved in a way that is favorable to the Company.

On May 29, 2019, we entered into an Asset Purchase Agreement with NXP USA, Inc. (“NXP”) pursuant to which the we agreed to sell to NXP certain assets related to our Wi-Fi connectivity business for $1.76 billion in cash at closing, subject to working capital and other customary adjustments. In addition, we agreed to license certain intellectual property to NXP in connection with the transaction and to provide certain temporary transition services following completion of the transaction. On December 6, 2019, we completed the transaction.

Mergers, acquisitions and divestitures include a number of risks and present financial, managerial and operational challenges, including but not limited to:

•diversion of management attention from running our existing business;

•increased expenses, including, but not limited to, legal, administrative and compensation expenses related to newly hired or terminated employees;

•key personnel of an acquired company may decide not to work for us;

•increased costs to integrate or, in the case of a divestiture, separate the technology, personnel, customer base and business practices of the acquired or divested business or assets;

•assuming the legal obligations of the acquired company, including potential exposure to material liabilities not discovered in the due diligence process or assuming indemnity obligations in connection with divestitures;

•ineffective or inadequate control, procedures and policies at the acquired company may negatively impact our results of operations;

•potential adverse effects on reported operating results due to possible write-down of goodwill and other intangible assets associated with acquisitions;

•burdensome conditions required to obtain regulatory approvals;

•potential damage to relationships with customers, suppliers, partners or employees;

•loss of synergies, in the case of divestitures;

•reduction of potential benefits of a transaction in the event of a long delay between signing and closing;

•reduction of our cash in the case of acquisitions for which we are paying cash consideration and share dilution if we are using our shares as consideration; and

•unavailability of acquisition financing on reasonable terms or at all.

Any acquired business, technology, service or product could significantly under-perform relative to our expectations and may not achieve the benefits we expect on a timely basis or at all. Given that our resources are limited, our decision to pursue a transaction has opportunity costs; accordingly, if we pursue a particular transaction, we may need to forgo the prospect of entering into other transactions that could help us achieve our strategic objectives.