UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual report pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934 for the fiscal year ended December 31, 20222023

Commission File Number 001-15811

MARKEL CORPORATIONGROUP INC.

(Exact name of registrant as specified in its charter)

A Virginia Corporation

IRS Employer Identification No. 54-1959284

4521 Highwoods Parkway, Glen Allen, Virginia 23060-6148

(Address of principal executive offices) (Zip code)

Registrant's telephone number, including area code: (804) 747-0136

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of exchange on which registered |

| Common Stock, no par value | | MKL | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | x | Accelerated filer | ☐ | Non-accelerated filer | ☐ |

| Smaller reporting company | ☐ | Emerging growth company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of the shares of the registrant's Common Stock held by non-affiliates as of June 30, 20222023 was approximately $17,203,000,000.$18,051,000,000.

The number of shares of the registrant's Common Stock outstanding at February 1, 2023: 13,408,610.January 31, 2024: 13,110,035.

Documents Incorporated By Reference: The portions of the registrant's Proxy Statement for the Annual Meeting of Shareholders scheduled to be held on May 17, 2023,22, 2024, referred to in Part III.

Markel CorporationGroup Inc.

Form 10-K

Index

| | | | | | | | |

| | Page Number |

| Part I | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | Unresolved Staff Comments | NONE |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | Mine Safety Disclosures | NONE |

| | |

| Part II | |

| Item 5. | | |

| Item 6. | [Reserved] | NONE |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | NONE |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | NONE |

| Part III | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| Part IV | |

| Item 15. | | |

| Item 16. | Form 10-K Summary | NONE |

| | |

| | |

PART I

Item 1. BUSINESS

Markel CorporationGroup Inc. (Markel Group) is a diverse financial holding company servingcomprised of a varietydiverse family of niche markets.businesses and investments. The leadership teams of our businesses operate with a high degree of independence, while at the same time living the values that we call the Markel Style. Our specialty insurance business, Markel, sits at the core of our company. Through decades of sound underwriting, Markel has provided the capital base from which we built a system of businesses and investments that collectively increase Markel Group's durability and adaptability. We aspire to build one of the world's great companies by creating win-win-win outcomes for our customers, associates and shareholders. We deploy three financial engines in pursuit of this goal.

Insurance - Our principal business markets and underwrites specialty insurance products using multipleour underwriting, fronting and insurance-linked securities platforms that enable us to best match risk and capital.capital

Investments - Our investing activities are primarily related toinvests premiums received by our underwriting operations. The majority ofoperations and any available earnings provided by our investable assets come from premiums paid by policyholdersoperating businesses in fixed maturity and the remainder is comprised of shareholder funds.equity securities

Markel Ventures - Through our Markel Ventures operations, we ownowns controlling interests in a diverse portfolio of businesses that operate in a variety of industries.industries

Our financial goals arethree interdependent engines form a system that provides diverse income streams, access to earn consistent underwritinga wide range of investment opportunities and the ability to efficiently move capital to the best ideas across our three engines. We allocate capital using a process that we have consistently followed for years. We first look to invest in our existing businesses for organic growth opportunities. After funding internal growth opportunities, we look to acquire controlling interests in businesses, build our portfolio of equity securities, or repurchase shares of our common stock. We believe our system is uniquely equipped for long-term growth. To mitigate the effects of short-term volatility and align with the long-term perspective that we apply to operating profitsour businesses and superior investment returnsmaking investments, we generally use five-year time periods to build shareholder value.measure our performance. We measure financial success by our ability to grow book value per common share and the market price per common share of our stock, or total shareholder return, at high rates of return over a long period of time. To mitigate effectsOver the past five years, our common share price increased at a compound annual rate of short-term volatility and align with6%. We also have considered the longer-term perspective we apply to operating our businesses, we generally use five-year time periods to measure our performance. Growth inperformance of book value per common share is an importantover the long-term, although we believe that as our business has evolved, this measure has become less reflective of shareholder value because a significant portion of our success because it includes all underwriting, operating and investing results.operations is not recorded at fair value. Over the past five years, the compound annual growth in book value per common share was 6%11%. Growth in total shareholder value is also an important measure of our success, as a significant portion of our operations are not recorded at fair value or otherwise captured in book value. Over the past five years, our common share price increased at a compound annual rate of 3%. While these measures, considered independently of other factors, fall below our internal targets, we remain confident in the strong operating performance of our businesses.

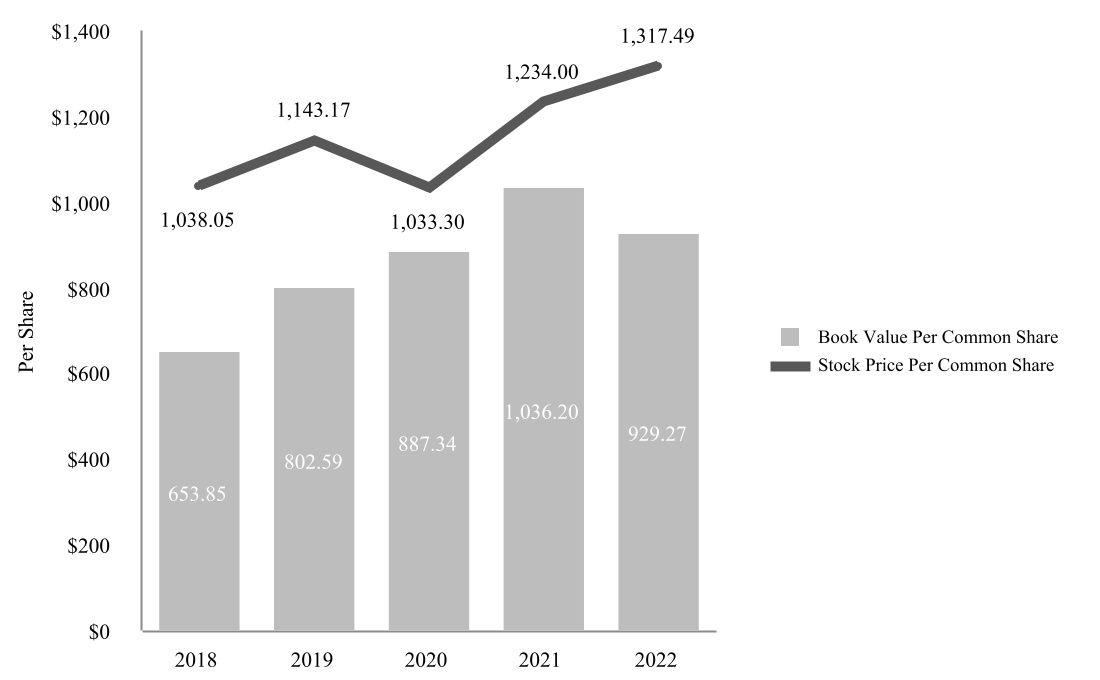

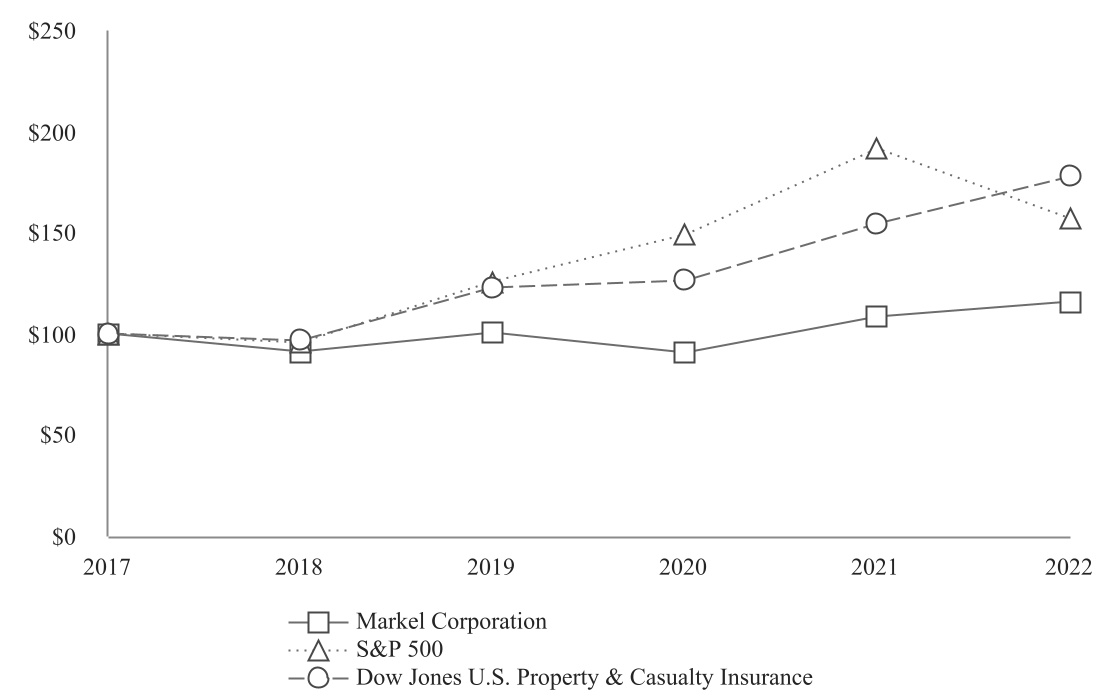

The following graph presents book valuestock price per common share and stock pricebook value per common share for the past five years as of December 31.

The following table presents summary financial data over the last five years, including book valuestock price per common share, market pricebook value per common share and other important financial measures and metrics.

| | (dollars in millions, except per share data) | (dollars in millions, except per share data) | 2022 | | 2021 | | 2020 | | 2019 | | 2018 | | 5-Year CAGR (1) | (dollars in millions, except per share data) | 2023 | | 2022 | | 2021 | | 2020 | | 2019 | | 5-Year CAGR (1) |

| Results of Operations | Results of Operations | |

| Earned premiums | Earned premiums | $ | 7,588 | | | $ | 6,503 | | | $ | 5,612 | | | $ | 5,050 | | | $ | 4,712 | | | 12 | % |

| Earned premiums | |

| Earned premiums | | $ | 8,295 | | | $ | 7,588 | | | $ | 6,503 | | | $ | 5,612 | | | $ | 5,050 | | | 12 | % |

| Net investment income | Net investment income | 447 | | | 367 | | | 376 | | | 442 | | | 435 | | | 3 | % | Net investment income | $ | 735 | | | $ | | $ | 447 | | | $ | | $ | 367 | | | $ | | $ | 376 | | | $ | | $ | 442 | | | 11 | | 11 | % |

| Net investment gains (losses) | Net investment gains (losses) | (1,596) | | | 1,979 | | | 618 | | | 1,602 | | | (438) | | |

| Markel Ventures operating revenues | Markel Ventures operating revenues | 4,758 | | | 3,644 | | | 2,795 | | | 2,055 | | | 1,915 | | | 29 | % |

| Markel Ventures operating revenues | |

| Markel Ventures operating revenues | | $ | 4,985 | | | $ | 4,758 | | | $ | 3,644 | | | $ | 2,795 | | | $ | 2,055 | | | 21 | % |

| Total operating revenues | Total operating revenues | 11,675 | | | 12,846 | | | 9,735 | | | 9,526 | | | 6,841 | | | 14 | % | Total operating revenues | $ | 15,804 | | | $ | | $ | 11,675 | | | $ | | $ | 12,846 | | | $ | | $ | 9,735 | | | $ | | $ | 9,526 | | | 18 | | 18 | % |

| Markel Ventures operating income | |

| Total operating income (loss) | |

| Total operating income (loss) | |

| Total operating income (loss) | |

| Net income (loss) to common shareholders | Net income (loss) to common shareholders | (250) | | | 2,389 | | | 798 | | | 1,790 | | | (128) | | |

| Comprehensive income (loss) to shareholders | (1,309) | | | 2,078 | | | 1,192 | | | 2,094 | | | (376) | | |

| Net income (loss) to common shareholders | |

| Net income (loss) to common shareholders | |

| Diluted net income (loss) per common share | |

| Diluted net income (loss) per common share | |

| Diluted net income (loss) per common share | Diluted net income (loss) per common share | $ | (23.57) | | | $ | 176.51 | | | $ | 55.63 | | | $ | 129.07 | | | $ | (9.55) | | |

| Financial Position | Financial Position | |

| Total investments, cash and cash equivalents and restricted cash and cash equivalents (invested assets) | $ | 27,420 | | | $ | 28,292 | | | $ | 24,927 | | | $ | 22,258 | | | $ | 19,238 | | | 6 | % |

| Financial Position | |

| Financial Position | |

Invested assets (2) | |

Invested assets (2) | |

Invested assets (2) | | $ | 30,854 | | | $ | 27,420 | | | $ | 28,292 | | | $ | 24,927 | | | $ | 22,258 | | | 10 | % |

| Total assets | Total assets | 49,791 | | | 48,477 | | | 41,738 | | | 37,474 | | | 33,306 | | | 9 | % | Total assets | $ | 55,046 | | | $ | | $ | 49,791 | | | $ | | $ | 48,477 | | | $ | | $ | 41,738 | | | $ | | $ | 37,474 | | | 11 | | 11 | % |

| Unpaid losses and loss adjustment expenses | Unpaid losses and loss adjustment expenses | 20,948 | | | 18,179 | | | 16,222 | | | 14,729 | | | 14,276 | | | 9 | % | Unpaid losses and loss adjustment expenses | $ | 23,483 | | | $ | | $ | 20,948 | | | $ | | $ | 18,179 | | | $ | | $ | 16,222 | | | $ | | $ | 14,729 | | | 10 | | 10 | % |

| Shareholders' equity | Shareholders' equity | $ | 13,066 | | | $ | 14,717 | | | $ | 12,822 | | | $ | 11,071 | | | $ | 9,081 | | | 7 | % | Shareholders' equity | $ | 14,984 | | | $ | | $ | 13,151 | | | $ | | $ | 14,700 | | | $ | | $ | 12,822 | | | $ | | $ | 11,071 | | | 11 | | 11 | % |

| Common shares outstanding (at year end, in thousands) | Common shares outstanding (at year end, in thousands) | 13,423 | | | 13,632 | | | 13,783 | | | 13,794 | | | 13,888 | | |

| Consolidated Performance Measures | Consolidated Performance Measures | |

| Consolidated Performance Measures | |

| Consolidated Performance Measures | |

| Closing stock price | |

| Closing stock price | |

| Closing stock price | | $ | 1,419.90 | | | $ | 1,317.49 | | | $ | 1,234.00 | | | $ | 1,033.30 | | | $ | 1,143.17 | | | 6 | % |

5-Year CAGR in closing stock price (1) | |

| Book value per common share | |

| Book value per common share | |

| Book value per common share | Book value per common share | $ | 929.27 | | | $ | 1,036.20 | | | $ | 887.34 | | | $ | 802.59 | | | $ | 653.85 | | | 6 | % | $ | 1,095.95 | | | $ | | $ | 935.65 | | | $ | | $ | 1,034.92 | | | $ | | $ | 887.34 | | | $ | | $ | 802.59 | | | 11 | | 11 | % |

5-Year CAGR in book value per common share (1) | 5-Year CAGR in book value per common share (1) | 6 | % | | 11 | % | | 10 | % | | 8 | % | | 7 | % | |

| Closing stock price | $ | 1,317.49 | | | $ | 1,234.00 | | | $ | 1,033.30 | | | $ | 1,143.17 | | | $ | 1,038.05 | | | 3 | % |

5-Year CAGR in closing stock price (1) | 3 | % | | 6 | % | | 3 | % | | 11 | % | | 12 | % | |

(1) CAGR—compound annual growth rate.

(2) Invested assets include total investments, cash and cash equivalents and restricted cash and cash equivalents.

Insurance

Our insurance engine is comprised of the following types of operations:

•Underwriting - Our underwriting operations are comprised of our risk-bearing insurance and reinsurance operations.

•Insurance-linked securities - Our insurance-linked securities (ILS) operations provide investment management services for a variety of investment products, including insurance-linked securities, catastrophe bonds, insurance swaps and weather derivatives.

•Program services and other fronting - Our program services business serves as a fronting platform that provides other insurance entities and capacity providers access to the United States (U.S.) property and casualty insurance market.

•Insurance-linked securities (ILS) - provides investment management services to third-party capital providers for a variety of insurance-related investment products.

Through our underwriting, ILSprogram services and program servicesother fronting and ILS operations, we have a suite of capabilities through which we can access capital to support our customers' risks, which includes our own capital through our underwriting operations, as well as third-party capital through our ILSprogram services and program servicesother fronting and ILS operations. Within each of these insurance platforms, we believe that our specialty product focus and niche market strategy enableenables us to develop expertise and specialized market knowledge. We seek to differentiate ourselves from competitors by our expertise, service, continuity and other value-based considerations, including the multiple platforms through which we can manage risk and deploy capital. For example, through our program services and other fronting platform, we have programs through which we write insurance policies on behalf of our ILS operations that are supported by third-party capital. Additionally, we cede certain risks historically written through our underwriting operations to our ILS operations to the extent those risks are more aligned with the risk profile of our ILS investors than our own corporate tolerance. Our ability to access multiple insurance platforms allows us to achieve income

streams from our insurance operations beyond the traditional underwriting model. We believe this multi-platform approach provides us with a unique

advantage through which we have the ability to unlock additional value for our customers and business partners, which we refer to as "the power of the platform."

Underwriting

Specialty Insurance and Reinsurance

Within our underwriting operations, we underwrite specialty insurance products on a risk-bearing basis. The specialty insurance market differs significantly from the standard market. In the standard market, insurance rates and forms are highly regulated, products and coverages are largely uniform with relatively predictable exposures, and companies tend to compete for customers on the basis of price. In contrast, the specialty market provides coverage for hard-to-place risks that generally do not fit the underwriting criteria of standard carriers.

Competition in the specialty insurance market tends to focus less on price than in the standard insurance market and more on other value-based considerations, such as availability, service and expertise. While specialty market exposures may have higher perceived insurance risks than their standard market counterparts, we seek to manage these risks and achieve higher financial returns. To reach our financial and operational goals, we must have extensive knowledge and expertise in our chosen markets. Many of our larger accounts are considered on an individual basis where customized forms and tailored solutions are employed.

By focusing on the distinctive risk characteristics of our insureds, we have been able to identify a variety of niche markets where we can add value with our specialty product offerings and alternative platforms through which we can access capital to support our customers' risks. Examples of nichespecialty insurance markets that we have targeted include liability coverage for highly specialized professionals, wind and earthquake-exposed commercial properties, equine-related risks, transaction-related risks, classic cars, credit and surety-related risks, collateral protection risks, and marine, energy and environmental-related activities. Our market strategy in each of these areas of specialization is tailored to the unique nature of the loss exposure, coverage and services required by insureds. In each of our nichethe markets we serve, we assign teams of experienced underwriters and claims specialists who provide a full range of insurance services.

We also participate in the reinsurance market in certain classes of reinsurance product offerings, primarily casualty lines and certain other specialty lines. In the reinsurance market, our clients are other insurance companies, or cedents. We typically write our reinsurance products in the form of treaty reinsurance contracts, which are contractual arrangements that provide for automatic reinsuring of a type or category of risk underwritten by cedents. Generally, we participate inTreaty reinsurance treaties withproducts are written globally on both a numberquota share and excess of other reinsurers, each with an allocated portion of the treaty, with the terms and conditions of the treaty being substantially the same for each participating reinsurer.loss basis. With treaty reinsurance contracts, we do not separately evaluate each of the individual risks assumed under the contracts and are largely dependent on the individual underwriting decisions made by the cedent. Accordingly, we review and analyze the cedent's risk management and underwriting practices in deciding whether to provide treaty reinsurance and in pricing of treaty reinsurance contracts. Additionally, we write casualty reinsurance on a facultative basis, which is distinct from treaty reinsurance in that we evaluate each risk individually to determine whether to assume the risk.

Our reinsurance products are written globally on both a quota share and excess of loss basis. Quota share contracts require us to share the losses and expenses in an agreed proportion with the cedent. Excess of loss contracts require us to indemnify the cedent against all or a specified portion of losses and expenses in excess of a specified dollar or percentage amount. Our reinsurance products may include features such as contractual provisions that require our cedent to share in a portion of losses resulting from ceded risks, may require payment of additional premium amounts or provide experience refunds if the losses we incur differ from those projected at the time of the execution of the contract or may require a reinstatement premium to restore coverage after there has been a loss occurrence.

We distinguish ourselves in the reinsurance market by the expertise of our underwriting teams, our access to global reinsurance markets, our ability to offer large capacity lines and our ability to customize reinsurance solutions to fit our cedents' needs. Additionally, as with our insurance underwriting operations, our ability to access third-party capital through our ILS and program services platforms provides additional capital alternatives to support certain risks, to the extent those risks do not align with our underwriting risk tolerance. For example, we do not write property reinsurance business, including catastrophe-exposed property business, on a risk-bearing basis. Such business is only written on behalf of our ILS operations, to the extent it matches the risk profile of our third-party ILS investors, who provide the capital to support the risk. See "Program Services and Other Fronting" for further discussion of business written on behalf of our ILS operations.

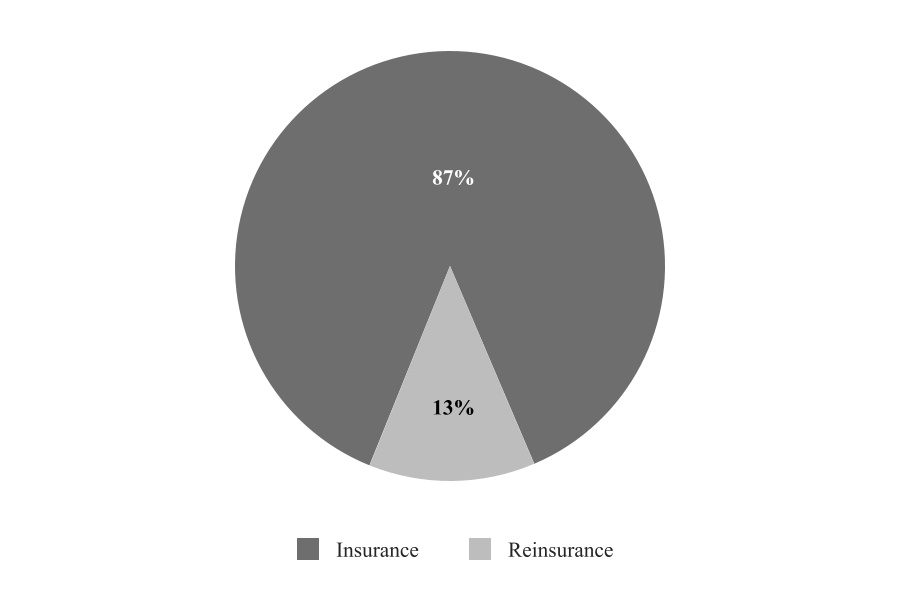

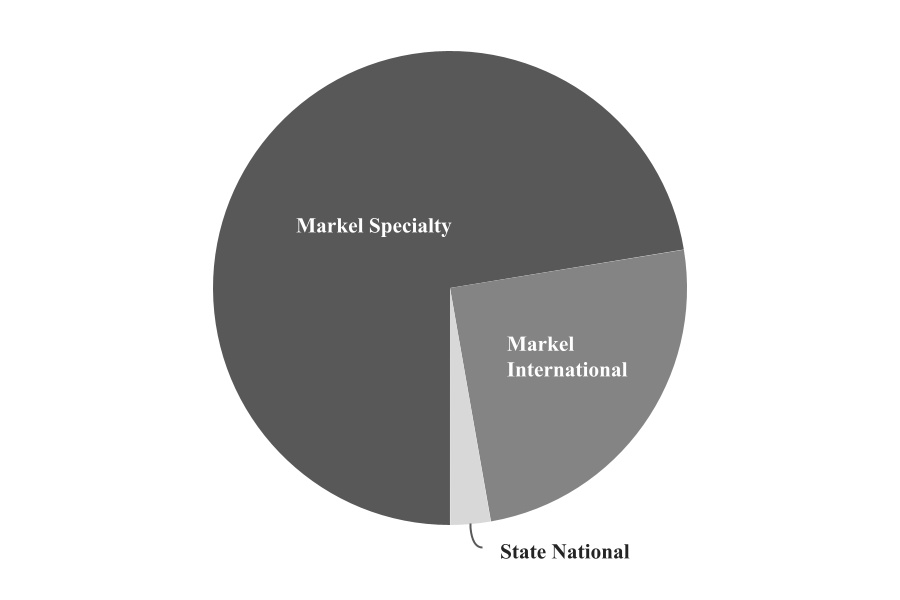

The following chart presents the composition of our underwriting operations between insuranceour Insurance segment and reinsuranceReinsurance segment based on 20222023 underwriting gross premium volume of $9.8 billion, which also aligns with our two reportable underwriting segments.

$10.3 billion. The Insurance segment includes all of our direct business, andas well as facultative placements and is written through our Markel Specialty, Markel International and State National divisions, with the exception of our State National division's program services business, which is not included in a reportable segment.reinsurance placements. The Reinsurance segment includes all treaty reinsurance and is primarily written through our Global Reinsurance division. Additional detail regarding our underwriting divisions and products is included in "Underwriting Segments."reinsurance.

The following table summarizes our U.S. insurance and reinsurance underwriting subsidiaries.

| | | | | | | | | | | | | | | | | | | | |

| U.S. Legal Entity | | Abbreviation | | Market | | State of Domicile |

| Essentia Insurance Company | | Essentia | | Insurance - admitted | | Missouri |

| Evanston Insurance Company | | EIC | | Insurance - non-admitted | | Illinois |

| FirstComp Insurance Company | | FCIC | | Insurance - admitted | | Nebraska |

| Markel American Insurance Company | | MAIC | | Insurance - admitted | | Virginia |

| Markel Global Reinsurance Company | | MGRC | | Reinsurance | | Delaware |

| Markel Insurance Company | | MIC | | Insurance - admitted | | Illinois |

| National Specialty Insurance Company | | NSIC | | Insurance - admitted | | Texas |

| State National Insurance Company, Inc. | | SNIC | | Insurance - admitted | | Texas |

| SureTec Insurance Company | | SIC | | Insurance - admitted | | Texas |

Through these U.S. insurance and reinsurance subsidiaries, we are licensed, authorized, or accredited to write business in all 50 states and the District of Columbia.

The following table summarizes our international insurance and reinsurance underwriting subsidiaries.

| | | | | | | | | | | | | | |

| International Legal Entity | | Abbreviation | | Country |

| Markel Bermuda Limited | | MBL | | Bermuda |

| Markel Insurance SE | | MISE | | Germany |

| Markel International Insurance Company Limited | | MIICL | | United Kingdom |

| Markel Syndicate 3000 | | Syndicate 3000 | | United Kingdom |

Markets and Distribution

Our underwriting operations write business on a global basis and utilize multiple distribution channels to access our targeted risks.

In the U.S., we write business in the excess and surplus lines (E&S) and admitted insurance markets, as well as the reinsurance market. The primary distribution channels through which our U.S. business is placed are wholesale insurance and reinsurance brokers, retail insurance agents and alternative channels, that includeincluding third-party managing general agents.

The E&S, or non-admitted, market focuses on hard-to-place risks and loss exposures that generally are not written in the standard market. U.S. insurance regulations generally require an E&S account to be declined by admitted carriers before an E&S company may write the business. E&S eligibility allows our insurance subsidiaries to underwrite unique loss exposures with more flexible policy forms and unregulated premium rates. This typically results in coverages that are more restrictive and more expensive than coverages in the standard market. The E&S market is accessed primarily through wholesale insurance and reinsurance brokers, which have limited quoting and binding authority. In 2021,2022, the E&S market represented $83$98 billion, or 10%11%, of the $798$875 billion U.S. property and casualty industry.1 In 2021,2022, we were the third largest E&S writer in the U.S. as measured by direct premium writings.1 Our E&S insurance operations are conducted through EIC.

Our U.S. business written in the admitted market focuses on unique and hard-to-place risks in the standard market, some of which must remain with an admitted insurance company for marketing and regulatory reasons. Hard-to-place risks written in the admitted market cover insureds engaged in similar, but highly specialized, activities that require a total insurance program not otherwise available from standard insurers or insurance products that are overlooked by large admitted carriers.insurers. The admitted market is subject to more state regulation than the E&S market, particularly with regard to rate and form filing requirements, restrictions on the ability to exit lines of business, premium tax paymentspayment requirements and membership in various state associations, such as state guaranty funds and assigned risk plans. Business written in the admitted market is placed primarily by retail insurance agents. We are looking for opportunities to expand our business placed through retail insurance agents in order to capture additional business in the admitted market that fits our risk profile. Our admitted business is also placed through managing general agents, which have broader underwriting authority than retail agents. These agents are carefully selected based on a track record of proficiency with their selected products, and the business written is controlled through regular audits and pre-approvals. In addition, certain products and programs written on an admitted basis are marketed directly to consumers. The majority of our admitted insurance operations are conducted through MIC, MAIC, FCIC and Essentia. Our admitted operations also include SIC, SNIC and NSIC.

1Market Segment Report - U.S. Surplus Lines, A.M. Best (September 13, 2023)

Our U.S. reinsurance operations are conducted through MGRC. Reinsurance business is placed primarily through wholesale reinsurance brokers. We were the 41st largest reinsurer in 20212022 as measured by worldwide gross reinsurance premium writings.2

In Bermuda, which is known for its significant concentration of insurance and reinsurance businesses, we participate in the worldwide insurance and reinsurance markets. The Bermuda property and casualty market is a significant source of capital for the U.S. market and the leading location for cessions by U.S. insurers.3 Business written in the Bermuda market is typically placed by a Bermuda-based wholesale broker. We conduct our Bermuda underwriting operations through MBL, which is registered as a Class 4 insurer and Class C long-term insurer under the insurance laws of Bermuda.

We also participate in the London insurance and reinsurance market, which is known for its ability to provide innovative, tailored coverage and capacity for unique and hard-to-place risks. Hard-to-place risks, inmany of which have significantly higher limits than risks placed through the London market are generally distinguishable from standard risks due to the complexity or significant size of the risk. It is primarily a broker market, which means that insurancemarket. Insurance brokers bringplace most of the business toin the London market. Risks written in this market are written on either a direct basis or a subscription basis, the latter of which means that loss exposures brought into the market are typically insured by more than one insurance company or Lloyd's of London (Lloyd's) syndicate, often due to the high limits of insurance coverage required. When we write business in the subscription market, we prefer to participate as lead underwriter in order to control underwriting terms, policy conditions and claims handling. We participate in the London insurance and reinsurance market primarily through Markel Capital Limited (Markel Capital) and MIICL. Markel Capital is the corporate capital provider for Syndicate 3000, through which our Lloyd's operations are conducted. Syndicate 3000 is managed by Markel Syndicate Management Limited. In addition to their headquarters in London, Markel Capital and MIICL havemaintain branch offices across the United Kingdom (U.K.), Europe, Canada, Asia, Australia and the Middle East through which we are able to offer insurance and reinsurance. The London insurance market produced approximately $94 billion of gross written premium in 2021, of which $53 billion was produced by Lloyd's syndicates.3,4 In 2021, our share of the London market was approximately 2% as measured by gross written premiums.

1Market Segment Report - U.S. Surplus Lines, A.M. Best (September 6, 2022)

2Market Segment Report - Global Reinsurance, A.M. Best (August 31, 2022)

3London Company Market Statistics Report, International Underwriting Association (September 2022)

4Lloyd's Annual Report 2021

In Bermuda, which is known for its significant concentration of insurance and reinsurance businesses, we participate in the worldwide insurance and reinsurance markets. The Bermuda property and casualty market is a significant source of capital for the U.S. market and the leading location for cessions by U.S. insurers.5 Business written in the Bermuda market is typically placed by a Bermuda-based wholesale broker. The Bermuda market produced $83 billion of gross written premium in 2020.6 In 2020, our share of the Bermuda market was approximately 1% as measured by gross written premiums in our underwriting operations. We conduct our Bermuda underwriting operations through MBL, which is registered as a Class 4 insurer and Class C long-term insurer under the insurance laws of Bermuda.

In Europe, we also write business through Syndicate 3000 and MISE, a regulated insurance carrier located in Munich, Germany. From its offices in Germany, MISE transacts business in European Union (E.U.) member states and throughout the European Economic Area (EEA).Area. MISE has established branches in Ireland, the Netherlands, Spain, Switzerland, France and the U.K. Syndicate 3000 supplements, or serves as an alternative to, MISE for access to the E.U. markets.

While we operate in various other markets, substantially all of our gross written premiums in 20222023 were written from our platforms in the United States, the United Kingdom, Bermuda and Germany. In 2022,2023, 80% of gross premium writings from our global underwriting operations were attributed to risks or cedents located in the United States. In each of the markets in which we operate, we seek to develop and capitalize on relationships with insurance and reinsurance brokers, insurance and reinsurance companies, large global corporations and financial intermediaries to develop and underwrite business. A significant volume of premium for the property and casualty insurance and reinsurance industry is produced through a small number of large insurance and reinsurance brokers. In 2022,2023, the top threefive independent brokers accounted for 28%37% of gross premiums written in our underwriting segments.operations. Additionally, a significant portion of the reinsurance contracts securitized through our ILS operations, for the benefit of third-party investors, are placed through these threefive independent brokers.

Ceded Reinsurance

In a reinsurance transaction, an insurance company transfers, or cedes, all or part of its exposure in return for a premium. In a retrocessional reinsurance transaction, a reinsured exposure is further ceded to another reinsurer. Within our underwriting operations, we seek to retain as much of our profitable business as possible while managing volatility within our underwriting results.results and capital requirements at our insurance subsidiaries. We purchase reinsurance and retrocessional reinsurance to manage our net retention on individual risks and overall exposure to losses, while providing us with the ability to offer policies with sufficient limits to meet policyholder needs. This includes purchasing sufficient coverage for our catastrophe-exposed policies to ensure that our net retained catastrophe risk is within our corporate tolerances. Our exposure to catastrophe risk has been significantly reduced over the past two years with the discontinuation of our retrocessional reinsurance business and the transition of our property reinsurance business from our underwriting operations to our Nephila ILS operations, where it is placed with third-party capital. See "Program Services and Other Fronting" for further discussion of this business. We continue to have exposure to property risks within our insurance operations.

For our professional liability and general liability lines of business within our insurance operations, we typically purchase excess of loss coverage. On product lines with property exposures, we purchase both excess of loss and proportionate coverages to reduce our exposure to large losses, including catastrophes. The structure of our reinsurance purchases may vary from year to year depending on our risk tolerance and the availability and cost of reinsurance, as determined by current market conditions. In such instances, we may in turn modify our gross premium writings in order to to manage our overall net loss exposures. Net retention of gross premium volume in our underwriting segments was 83%82% in 2022.2023.

Reinsurance and retrocessional treaties are generally purchased on an annual basis and are subject to renegotiation at renewal. In most circumstances, the reinsurer remains responsible for all business produced before termination. Treaties typically contain provisions concerning ceding commissions, required reports to reinsurers, responsibility for taxes, arbitration in the event of a dispute and provisions that allow us to demand that a reinsurer post letters of credit or assets as security if a reinsurer becomes an unauthorized reinsurer under applicable regulations or if its rating falls below an acceptable level.

Our cededCeded reinsurance and retrocessional contracts do not legally discharge us from our primary liability for the full amount of the policies, and we will be required to pay the loss and bear collection risk if the reinsurer fails to meet its obligations under the reinsurance agreement. We attempt to minimize credit exposure to reinsurers through adherence to internal ceded reinsurance guidelines. We manage our exposures so that no unsecured exposure to any one reinsurer is material to our ongoing business. Treaties typically contain provisions that allow us to demand that a reinsurer post letters of credit or assets as collateral if a reinsurer becomes an unauthorized reinsurer under applicable regulations or if its rating falls below an acceptable level.

52Market Segment Report - Global Reinsurance, A.M. Best (August 22, 2023)

3 Offshore Reinsurance in the U.S. Market, Reinsurance Association of America (2020)

6Bermuda Monetary Authority 2021 Annual Report(2022)

When appropriate, we pursue reinsurance commutations that involve the termination of ceded reinsurance and retrocessional reinsurance contracts. Our commutation strategy related to ceded reinsurance and retrocessional contracts is to reduce credit exposure and eliminate administrative expenses associated with the run-off of ceded reinsurance placed with certain reinsurers.

See note 12 of the notes to consolidated financial statements included under Item 8 and Item 7A Quantitative and Qualitative Disclosures About Market Risk for additional information about our ceded reinsurance programs and exposures.

Competition and Underwriting Philosophy

We compete with numerous domestic and international insurance companies and reinsurers, Lloyd's syndicates, risk retention groups, insurance buying groups, risk securitization programs, alternative capital sources, such as that provided through ILS, and alternative self-insurance mechanisms. We also compete with new companies that continue to be formed to enter the insurance and reinsurance markets, particularly companies with new or "disruptive" technologies or business models. Competition may take the form of lower prices, broader coverages, greater product flexibility, enhanced digital capabilities for distribution of insurance products, higher coverage limits, higher quality services or higher ratings by independent rating agencies. In all of our markets, we compete on the basis of overall financial strength, ratings assigned by independent rating agencies, development of specialty products to satisfy well-defined market needs and by maintaining relationships with agents, brokers and insureds who rely on our expertise. This expertise is our principal means of competing. We offer a diverse portfolio of products, each with its own distinct competitive environment, which requires us to be responsive to changes in market conditions for individual product lines. With each of our products, we seek to write business that produces consistent underwriting profits by competing with innovative ideas, appropriate pricing, expense control and quality servicemaintaining adequate rates for our premium writings in relation to policyholders, agents and brokers. We also leverage our underwriting capacity and expertise through relationships with start-ups and digital distribution partners through which we can develop ideas that leverage emerging technologies and modern customer acquisition strategies to create the service and experience that consumers have grown to expect and demand.expected loss cost trends.

Few barriers exist to prevent insurers and reinsurerscompetition from entering our markets within the property and casualty industry. Market conditions, risk tolerance and capital capacity influence the degree of competition at any point in time. During periods of excess underwriting capacity, as defined by availability of capital, competition can result in lower pricing and less favorable policy terms and conditions for insurers. During periods of reduced underwriting capacity, pricing and policy terms and conditions are generally more favorable for insurers. Historically, the performance of the property and casualty insurance and reinsurance industries has tended to fluctuate in cyclical periods of price competition and excess underwriting capacity, followed by periods of high premium rates and shortages of underwriting capacity. At any given time, our portfolio of insurance products could be experiencing varying combinations of these characteristics. This cyclical market pattern can be more pronounced in the specialty insurance and reinsurance markets in which we compete than the standard insurance market.

Following several years of price decreases and the high level of natural catastrophes that occurred in 2017, we began seeing more favorable rates in 2018, particularly onWithin our catastrophe-exposed and loss-affected business. Since 2018, we have continued to see rate strengthening across most product lines following the continued high level of natural catastrophes and significant losses attributed to the COVID-19 pandemic, as well as general market conditions. However, we began to see rate increases moderate on many of our product lines in 2022. In some product lines, such as directors and officers, we even began to see single digit rate decreases in the latter part of 2022. The overall strengthening of rates in recent years has been most prominent within our professional liability and general liability product lines, reflecting the impacts of both economic and social inflation on loss costs. Recent increases in economic and social inflation have created more uncertainty around the ultimate losses that will be incurred to settle claims on these longer-tail product lines. These factors, as well as the impacts of the low interest rate environment on interest income in recent years, have contributed to the strong rate environment. The primary exception to the favorable rate environment is workers' compensation, where we continue to see low single digit rate decreases given generally favorable loss experience in recent years.

By focusing on market niches where we have underwriting expertise, and leveraging capabilities offered through our multiple insurance platforms,operations, we seek to earn consistentan underwriting profits, which are a key component of our strategy.profit every year. The property and casualty insurance industry commonly defines underwriting profit or loss as earned premiums net of losses and loss adjustment expenses and underwriting, acquisition and insurance expenses. We believe that the ability to achieve consistent underwriting profits demonstrates knowledge and expertise, commitment to superior customer service and the ability to manage insurance risk. We use underwriting profit or loss as a basis for evaluating our underwriting performance. The combined ratio is a measure of underwriting performance and represents the relationship of incurred losses, loss adjustment expenses and underwriting, acquisition and insurance expenses to earned premiums. A combined ratio less than 100% indicates an underwriting profit, while a combined ratio greater than 100% reflects an underwriting loss. In 2022,2023, our

combined ratio was 92%98%. See Item 7 Management's Discussion & Analysis of Financial Condition and Results of Operations for a discussion of our underwriting results.

We routinely review the pricing for all of our major product lines. When we believe the prevailing market price will not support our underwriting profit targets, the business is not written. As a result of our underwriting discipline, gross premium volume may vary when we alter our product offerings to maintain or improve underwriting profitability.

Over the past few years, For example, in 2023, we have increasedadjusted our focus on growing our most profitable lines of business and have discontinued certain lines or programs that have not performed consistent with our expectations. This is particularly truewritings within our Reinsurance segment, whereU.S. and Bermuda directors and officers and errors and omissions product lines in 2021, we discontinued writing property reinsurance business, including catastrophe-exposed property business, on a risk-bearing basis, and in 2022, we discontinued writing property retrocessional reinsurance business. In more limited instances, we have taken similar actions within our Insurance segment. We saw the benefit of these changessegment in our underwriting results in 2022, which reflected a lower impact from Hurricane Ian than we would have expected absent these changes.response to unfavorable loss cost trends and downward pressure on rates.

Underwriting Segments

We monitor and assess the performance of our ongoing underwriting operations on a global basis in the following two segments: Insurance and Reinsurance. See note 2 of the notes to consolidated financial statements included under Item 8 for additional segment reporting disclosures.

Insurance Segment

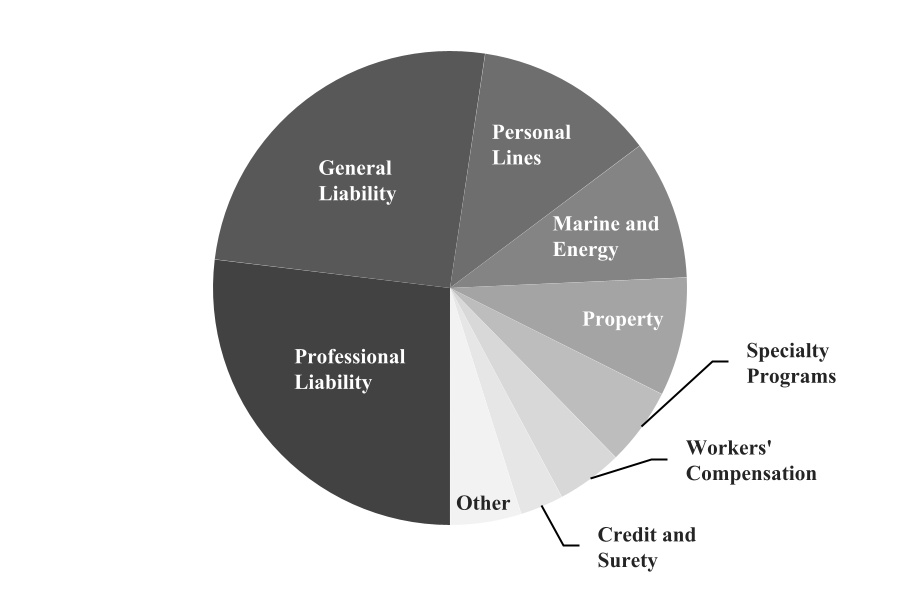

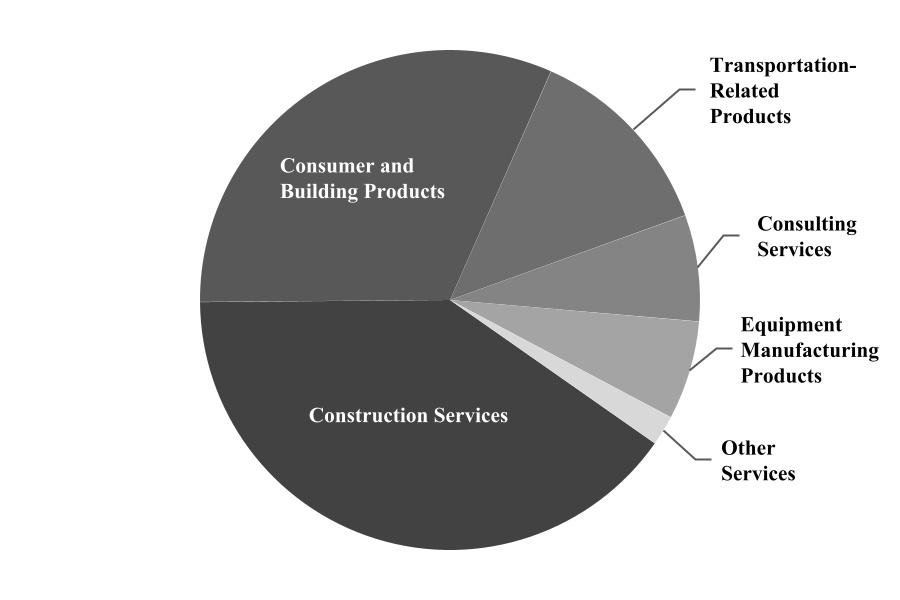

Our Insurance segment reported gross premium volume of $8.6$9.2 billion, earned premiums of $6.5$7.3 billion and an underwriting profit of $549.9$162.2 million in 2022.2023. The following chart presents the composition of our Insurance segment by division based on 20222023 gross premium volume.

The Markel Specialty division is comprised of our U.S. and Bermuda based insurance underwriting operations and writes business for insureds ranging from individuals and small businesses to Fortune 1000 companies in the U.S., Bermuda, the U.K., the E.U., Asia and the E.U.Australia. The Markel Specialty division is a unified platform that provides easy access to our diverse portfolio of products and capabilities. The Markel International division writes business worldwide from our London and Munich-based platforms, which include branch offices aroundin Canada, Asia, Australia and across the world.E.U. The State National division writes collateral protection insurance for automobile and other vehicle loans in the U.S., which insures personal automobiles and other vehicles held as collateral for loans made by credit unions, banks and specialty finance companies through its lender services product line on both an admitted and non-admitted basis.

The following chart displays the types of products written in our Insurance segment based on 20222023 gross premium volume.

General liability product offerings include a variety of primary and excess liability coverages. We focus on businesses in the construction, life sciences, energy, medical, healthcare, pharmaceutical, professional services, social welfare, recreational, transportation, heavy industrial and hospitality industries. Specific products include primary general liability, excess and umbrella products, products liability products, environmental liability products and casualty facultative reinsurance written for individual casualty risks.

Our professional liability product lines provide insurance solutions for small, middle market and risk management accounts with coverage that is tailored to their exposures and needs. Professional liability coverages include errors and omissions, directors and officers, cyber, employment practices liability, professional indemnity, transaction liability, intellectual property and union liability. Errors and omissions coverage provides solutions for specialized professions including lawyers, accountants, agents and brokers, service technicians and consultants, as well as other less-specialized professionals. Directors and officers coverage is provided for publicly-traded, private and non-profit companies, including financial institutions and Fortune 1000 companies. Cyber products provide coverage for, among other things, data breach and privacy liability, data breach loss to insureds and electronic media coverage. We also offer claims-made professional liability coverage for individual healthcare providers such as therapists, pharmacists, physician assistants and nurse anesthetists, and coverages for medical facilities and other allied healthcare risks, such as clinics, laboratories, pharmacies and senior living facilities.

General liability product offerings include a variety of primary and excess liability coverages. We focus on businesses in the construction, life sciences, energy, medical, healthcare, pharmaceutical, professional services, social welfare, recreational, transportation, heavy industrial and hospitality industries. Specific products include primary general liability, excess and umbrella products, products liability products, environmental liability products and casualty facultative reinsurance written for individual casualty risks.

Personal lines products provide first and third-party coverages in the U.S. for classic cars, motorcycles and a variety of personal watercraft, including vintage boats, high-performance boats and yachts and recreational vehicles, such as motorcycles, snowmobiles and ATVs. Based on the seasonal nature of much of our personal lines business, we generally will experience higher claims activity during the second and third quarters of the year. Additionally, property coverages are offered for mobile homes, dwellings and homeowners that do not qualify for standard homeowner's coverage, as well as personal umbrella coverage.

Marine and energy products include a portfolio of coverages for cargo, energy, hull, liability, war and terrorism risks worldwide. The cargo product line is an international transit-based book providing coverage for many types of cargo. Energy coverage includes all aspects of oil, gas and renewable energy activities. Our renewable energy activities include coverages for onshore and offshore wind farms, as well as alternative energy generation and storage technology projects. Hull coverages consist of coverage for physical damage to ocean-going tonnage, yachts and mortgagees' interests. Liability coverage provides coverage for a broad range of energy liabilities, as well as traditional marine exposures including charterers, terminal operators and ship repairers. WarMarine war coverage includes protections for the hulls of ships, and other related interests, against war and associated perils. Terrorism coverage providesincludes coverage for property damage and business interruption related to political and civil violence includingand war and civil war.on land.

Property coverages consist principally of fire, allied lines (including windstorm, hail and water damage) and other specialized property coverages, including catastrophe-exposed property risks such as earthquake and wind on both a primary and excess basis. Catastrophe-exposed property risks are typically lower frequency andcan present higher severity in nature than more standard property risks.risks due to the impacts from earthquakes and severe weather events such as hurricanes, convective storms and wildfires. Our property coverages are exposed to windstorm losses that, based on the seasonal nature of those events, are more likely to occur in the third and fourth quarters of the year. Our property risks range from small, single-location accounts

to large, multi-state, multi-location, multi-national accounts on a worldwide basis. Other types of property products include inland marine products, railroad-related products and specie coverage for fine art on exhibition and in private collections.

Specialty programs business is offered in the U.S. on a standalone or package basis and generally targets specialized commercial markets and various customer groups, such as amateur sports and fitness clubs. Certain specialty programs written in this segment use managing general agents to offer single source admitted and non-admitted programs for a specific industry, class or line of business, including first and third-party coverages such as packaged policies for providers of leisure and recreational activities.business.

Workers' compensation products are offered in the U.S. and provide wage replacement and medical benefits to employees injured in the course of employment and target main-street, service and artisan contractor businesses, retail stores and restaurants.

Credit and surety products consist primarily of trade credit and prepayment coverage and a range of bonds and guarantees that support contractual obligations, as well as other coverages for specific credit risks, markets and contingencies. Key credit risks covered include those of counterparty insolvency and defaults by government-owned entities. The key coverages under surety products include contractual performance and payment risks, commercial license and permit obligations and obligations related to judicial proceedings such as court and fiduciary bonds.

Other product lines within the Insurance segment primarily include auto and collateral protection insurance.insurance, which insures personal automobiles and other vehicles held as collateral for loans made by credit unions, banks and specialty finance companies.

Reinsurance Segment

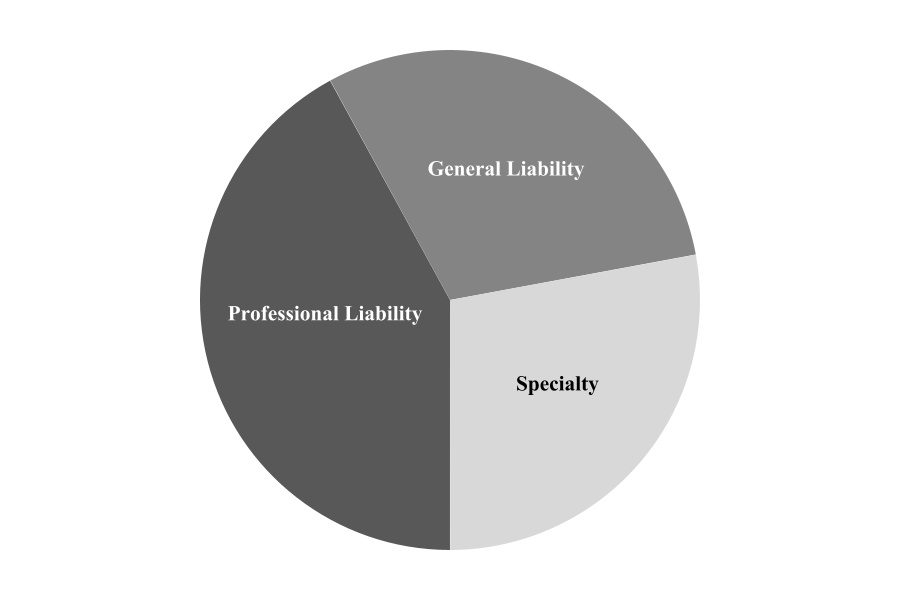

Our Reinsurance segment product offerings are underwritten primarily by our Global Reinsurance division, which operates from platforms in the U.S., Bermuda and the U.K. We write quota share and excess of loss reinsurance on a local, national and global basis. Our Reinsurance segment reported gross premium volume of $1.2$1.0 billion, earned premiums of $1.1$1.0 billion and an underwriting profitloss of $83.9$19.3 million in 2022.2023. The following chart displays the types of products written in our Reinsurance segment based on 20222023 gross premium volume.

Professional liability reinsurance primarily consists of the following:

•Transaction liability, which provides representation, warranty and indemnity coverage for mergers and acquisitions, including coverage for tax and contingent liability;

•Directors and officers liability for publicly-traded, private and non-profit companies;

•Cyber and technology errors and omissions covering both first and third-party exposures;

•Errors and omissions for lawyers, accountants, agents and brokers, services technicians and consultants; and

•Healthcare liability for physicians, hospitals, long-term care and other medical facilities.

General liability reinsurance primarily consists of umbrella and excess casualty products, as well as environmental liability products covering pollution legal liability and contractors' pollution exposures.

Our specialty treaty reinsurance products are also written on a quota share and excess of loss basis across a wide range of specialty product lines, primarily consisting of the following:

•Credit and surety products, including structured and whole turnover credit, political risk and contract and commercial surety reinsurance programs covering worldwide exposures;

•Workers' compensation and accident and health products covering both standard and catastrophe-exposed business in the U.S. and worldwide;

•Marine and energy products covering both offshore and onshore marine, energy and renewable energy risks on a worldwide basis, including hull, cargo and liability;

•Public entity reinsurance products offering casualty coverage for municipalities, schools, special districts, public housing authorities and public entity affiliated non-profits;

•Mortgage default insurance offering coverage for private mortgage insurers predominantly located in the U.S. and Australia;

•Aviation and space coverage, including major risk, general aviation, satellite launch and orbit;

•Agriculture reinsurance covering multi-peril crop insurance, hail and related exposures for risks located in the U.S. and Canada; and

•Discrete political violence and national terror pools in select jurisdictions globally.

Previously, we also wrote propertyProfessional liability reinsurance and retrocessional reinsurance business. We discontinued writing these lines effective January 1, 2021 and 2022, respectively, and effective January 1, 2022, we were off-risk for substantially all property loss exposures, including catastrophe exposures, previously written within our Reinsurance segment. Any such business is now written on behalfprimarily consists of our Nephila ILS operations to the extent it matches the risk-profile of our third-party ILS investors, who will ultimately assume the risk.following:

Insurance-Linked Securities•Transaction liability, which provides representation, warranty and indemnity coverage for mergers and acquisitions, including coverage for tax and contingent liability;

Our insurance-linked securities operations are primarily comprised of our Nephila operations•Cyber and are not included in a reportable segment. Nephila Holdings Ltd. (together with its subsidiaries, Nephila) provides investmenttechnology errors and insurance managementomissions covering both first and third-party exposures;

•Errors and omissions for lawyers, accountants, agents and brokers, services through which we offer alternative capital to the reinsurance market while providing investors with investment strategies that typically are uncorrelated with traditional asset classes. We receive management feestechnicians and consultants; and

•Healthcare liability for investmentphysicians, hospitals, long-term care and insurance management services provided through these operations primarily based on the net asset value of the accounts managed, and for certain funds, incentive fees based on their annual performance. Through 2022, we also provided risk origination services for our fund management operations, as well as for third parties, through our Velocity and Volante managing general agent companies and received commissions based on the direct written premiums of the insurance contracts placed. Total revenues from our insurance-linked securities operations for the year ended December 31, 2022 were $338.3 million, which included $225.8 million of gains from the sales of our managing general agent operations.

Our fund management operations provide insurance and investment management services for a broad range of investment products for insurance and reinsurance companies, government entities, banks, hedge funds, pension funds and institutional investors, including insurance-linked securities, catastrophe bonds, insurance swaps and weather derivatives. Nephila serves as the investment manager to several Bermuda based private funds (the Nephila Funds). To provide access for the Nephila Funds to a variety of insurance-linked securities in the property catastrophe, climate and specialty markets, Nephila acts as an insurance manager to certain Bermuda Class 3 and 3A reinsurance companies, Lloyd's Syndicate 2357 and Lloyd's Syndicate 2358 (collectively, the Nephila Reinsurers). The results of the Nephila Reinsurers are attributed to the Nephila Funds primarily through derivative transactions between these entities. Neither the Nephila Funds nor the Nephila Reinsurers are subsidiaries of Markel Corporation, and as such, these entities are not included in our consolidated financial statements.

The Nephila Reinsurers subscribe to various reinsurance contracts based on their investors' risk profiles, including property and specialty reinsurance business fronted through our underwriting and program services platforms. We write this business on behalf of our Nephila ILS operations to the extent it fits Nephila investors' risk profile and cede substantially all of the risk to Nephila Reinsurers. See note 18 of the notes to consolidated financial statements included under Item 8 for further details regarding transactions with entities managed through our Nephila operations.

Since our acquisition of Nephila in 2018, we experienced significant growth in the Velocity and Volante managing general agent operations. We realized the value created since 2018 through the sale of Velocity in February 2022 and Volante in October 2022. See Note 3 of the notes to consolidated financial statements included under Item 8 for additional details regarding these transactions.

Following the sales of our Velocity and Volante managing general agent operations, our Nephila ILS operations are solely comprised of our fund management operations. Since acquiring Nephila in 2018, investment performance in the broader ILS market has been adversely impacted by consecutive years of elevated catastrophe losses, most recently with Hurricane Ian in 2022. These events, as well as recent volatility in the capital markets, have impacted investor decisions around allocation of capital to ILS, which in turn has impacted our capital raises and redemptions within the funds we manage. As of December 31, 2022, Nephila's net assets under management were $7.2 billion.

Our insurance-linked securities operations also include our run-off Markel CATCo operations, the results of which are reported separately from our ongoing insurance-linked securities operations. Our Markel CATCo operations are conducted through Markel CATCo Investment Management Ltd. (MCIM), an ILS investment fund manager headquartered in Bermuda. MCIM serves as the insurance manager for Markel CATCo Re Ltd. (Markel CATCo Re), a Bermuda Class 3 reinsurance company, and as the investment manager for Markel CATCo Reinsurance Fund Ltd., a Bermuda exempted mutual fund company comprised of multiple segregated accounts (Markel CATCo Funds). In July 2019, these operations were placed into run-off. In March 2022, we completed a buy-out transaction that provided for an accelerated return of all remaining capital to investors in the Markel CATCo Funds. Following the completion of the buy-out transaction, we consolidate Markel CATCo Re as its primary beneficiary. Results attributable to the run-off of Markel CATCo Re are included with our other Markel CATCo operations within services and other expenses, and for the year ended December 31, 2022, these results were entirely attributable to noncontrolling interest holders in Markel CATCo Re. In connection with the buy-out transaction, we entered into a tail risk cover with Markel CATCo Re through which we have uncollateralized exposure to adverse development on loss reserves held by Markel CATCo Re for loss exposures in excess of limits that we believe are unlikely to be exceeded. For further details regarding our Markel CATCo operations and the consolidation of Markel CATCo Re, see note 17 of the notes to consolidated financial statements included under Item 8 and for further details regarding the buy-out transaction, see note 21 of the notes to consolidated financial statements included under Item 8.

Program Services and Other Fronting

Our program services and other fronting business generates fee income in the form of ceding fees in exchange for fronting insurance and reinsurance business tofor other insurance carriers (capacity providers). In general, fronting refers to business in which we write insurance on behalf of a general agent or capacity provider and then cede all, or substantially all, of the risk under these policies to the capacity provider in exchange for ceding fees. The results of our program services and other fronting operations are not included in a reportable segment.

Our program services business, which is provided through our State National division, offers issuing carrier capacity to both specialty managing general agents and other producers who sell, control and administer books of insurance business that are supported by third parties that assume reinsurance risk, including the Nephila Reinsurers. These reinsurers areinclude domestic and foreign insurers and institutional risk investors that want to access specific lines of U.S. property and casualty insurance business but may not have the required licenses, and filings or financial strength ratings to do so.

Beginning in 2024, our State National division is expanding internationally through a partnership with our Markel International division to create an international program services division to serve managing general agents in the U.K. market. The new division is another example of how we can leverage our array of capabilities to effectively and efficiently connect capital with risk.

Through our program services business, we write a wide variety of insurance and reinsurance products, principally including general liability, commercial liability, commercial multi-peril, property and workers' compensation. Program services business written through our State National division is separately managed from our underwriting divisions, which may write similar products, in order to protect our program services customers.

The following table summarizes the subsidiaries through which our program services business is written.

| | | | | | | | | | | | | | |

| Legal Entity | | Abbreviation | | State of Domicile |

| City National Insurance Company | | CNIC | | Texas |

Independent Specialty Insurance Company | | ISIC | | Delaware |

| National Specialty Insurance Company | | NSIC | | Texas |

| Pinnacle National Insurance Company | | PNIC | | Texas |

| State National Insurance Company, Inc. | | SNIC | | Texas |

| Superior Specialty Insurance Company | | SSIC | | Delaware |

| United Specialty Insurance Company | | USIC | | Delaware |

TheseThrough these subsidiaries, areour program services business is licensed or authorized or licensed to write property and casualty insurancebusiness in all 50 states and the District of Columbia. Many of our programs are arranged with the assistance of brokers that are seeking to provide customized insurance solutions for specialty insurance business that requires a carrier rated "A" by A.M. Best Company (Best)(A.M. Best). Our specialized

business model relies on third-party producers or capacity providers to provide the infrastructure associated with providing policy administration, claims handling, cash handling, underwriting, or other traditional insurance company services. We compete primarily on the basis of price, customer service, geographic coverage, financial strength ratings, licenses, reputation, business model and experience.

Total revenues attributed to our program services business for the year ended December 31, 20222023 were $133.3$151.8 million. Our program services business generated $2.8$2.9 billion of gross written premium volume for the year ended December 31, 2022.2023.

In our program services business, we generally enter into quota share reinsurance agreements whereby we cede to the capacity providers 100% of the premium written and substantially all of our gross liability under all policies issued by and on behalf of us by the producer. The capacity providers are generally entitled to 100% of the net premiums received on policies reinsured, less the ceding fee to us, the commission paid to the producer and premium taxes on the policies. In connection with writing this business, we also enter into agency agreements with both the producer and the capacity providers whereby the producer and capacity providers are generally required to deal directly with each other to develop business structures and terms to implement and maintain the ongoing contractual relationship. In a number of cases, the producer and capacity providers for a program are part of the same organization or are otherwise affiliated. As a result of our contract design, substantially all of the underwriting risk and operational risk inherent in the arrangement is borne by the capacity providers. The capacity providers assume and are liable for substantially all losses incurred in connection with the risks under the reinsurance agreement, including judgments and settlements.

Our contracts with capacity providers do not legally discharge us from our primary liability for the full amount of the policies, and we will be required to pay the loss and bear collection risk if a capacity provider fails to meet its obligations under the reinsurance agreement. As a result, we remain exposed to the credit risk of capacity providers, orincluding the risk that one of our capacity providers becomes insolvent or is otherwise unable or unwilling to pay policyholder claims. We mitigate this credit risk generally by either selecting well capitalized, highly rated authorized capacity providers or requiring that the capacity provider post substantial collateral to secure the reinsured risks, which, in some instances, exceeds the related reinsurance recoverable.

In certain instances,our other fronting business, we also leverage the strength of our underwriting platform, including our highly rated insurance subsidiaries, to write business on behalf of our Nephila ILS operations, in exchange for ceding fees, to support theirits business plans and assist in meeting theirits desired return objectives. ThisOur other fronting business is conductedmanaged separately from our program services business. The results of our other fronting business are not included in a reportable segment. Total revenues attributed to our other fronting business for the year ended December 31, 2023 were $20.7 million. Our other fronting business generated $840.9 million of gross written premium volume for the year ended December 31, 2023.

Business written on behalf of our Nephila ILS operations within both our program services and other fronting operations primarily consists of catastrophe-exposed property insurance and reinsurance business, as well as specialty and specialtyclimate reinsurance business. The business written is ceded to the Nephila Reinsurers, whose investors ultimately assume the risk. To mitigate credit risk for this business, we require collateral up to a specified level of annual aggregate agreement year losses, which is held in a trust for which we are the beneficiary. See note 18 of the notes to consolidated financial statements included under Item 8 for further details regarding our programs with Nephila Reinsurers.

Although we reinsure substantially all of the risks inherent in our program services business and ILSother fronting arrangements,businesses, we have certain programs that contain limits on our reinsurers' obligations to us that expose us to underwriting risk, including loss ratio caps, aggregate reinsurance limits or exclusion of the credit risk of producers. Under certain programs, including programs and contracts with Nephila Reinsurers, we also bear underwriting risk for annual aggregate agreement year losses in excess of a limit that we believe is unlikely to be exceeded.

Insurance-Linked Securities

Our insurance-linked securities operations are primarily comprised of our Nephila operations and are not included in a reportable segment. Nephila Holdings Ltd. (together with its subsidiaries, Nephila) provides investment and insurance management services through which we offer alternative capital to the insurance and reinsurance markets while providing investors with investment strategies that typically are uncorrelated with traditional asset classes. We receive management fees for investment and insurance management services provided through these operations, and for certain funds, incentive fees based on their annual performance. Our management fees are based on the net asset value of the accounts managed for most of our funds and gross premium volume for the remaining funds. Total revenues from our insurance-linked securities operations for the year ended December 31, 2023 were $99.5 million. As of December 31, 2023, Nephila's net assets under management were $6.8 billion.

Our fund management operations provide insurance and investment management services for a broad range of investment products for insurance and reinsurance companies, government entities, banks, hedge funds, pension funds and institutional investors, including insurance-linked securities such as catastrophe bonds, insurance swaps, traditional reinsurance contracts, industry loss warranties and other financial instruments. Nephila serves as the investment manager to several Bermuda based private funds (the Nephila Funds). To provide access for the Nephila Funds to a variety of insurance-linked securities in the property catastrophe, climate and specialty markets, Nephila acts as an insurance manager to certain Bermuda Class 3, collateralized and special purpose reinsurance companies, Lloyd's Syndicate 2357 and Lloyd's Syndicate 2358 (collectively, the Nephila Reinsurers). The results of the Nephila Reinsurers are attributed to the Nephila Funds primarily through derivative transactions between these entities. Neither the Nephila Funds nor the Nephila Reinsurers are subsidiaries of Markel Group, and as such, these entities are not included in our consolidated financial statements.

The Nephila Reinsurers subscribe to various property, climate and specialty reinsurance contracts based on their investors' risk profiles, which include business ceded by our underwriting and program services and other fronting platforms. We write this business on behalf of our Nephila ILS operations to the extent it fits Nephila investors' risk profile and cede substantially all of the risk to Nephila Reinsurers. See note 18 of the notes to consolidated financial statements included under Item 8 for further details regarding transactions with entities managed through our programs with Nephila Reinsurers.operations.

Ratings

Financial stability and strength are important purchase considerations of policyholders, cedents and insurance agents and brokers. Because an insurance premium paid today purchases coverage for losses that might not be paid for many years, the financial viability of the insurer is of critical concern. Various independent rating agencies provide information and assign ratings to assist buyers in their search for financially sound insurers. Rating agencies periodically re-evaluate assigned ratings based upon changes in the insurer's operating results, financial condition or other significant factors influencing the insurer's business. ChangesDowngrades in assigned ratings and other negative actions could have an adverse impact on an insurer's ability to write new business.

Rating agencies assign financial strength ratings (FSRs) to property and casualty insurance companies, or group of companies, based on quantitative criteria such as profitability, leverage and liquidity, as well as qualitative assessments such as the spread of risk, themarket placement, business profile, adequacy and soundness of ceded reinsurance, the quality and estimated market value of assets, the adequacy of loss reserves and surplus and the competence, experience and integrity of management.

SeventeenSixteen of our eighteenseventeen insurance subsidiaries are rated by Best. All seventeen ofA.M. Best, while our insurance subsidiaries rated by Best have been assigned an FSR of "A" (excellent). Our Lloyd's syndicate is part of a group rating for the Lloyd's overall market, whichmarket. All sixteen of our insurance subsidiaries rated by A.M. Best have been assigned an FSR of "A" (excellent). The Lloyd's group has been assigned an FSR of "A" (excellent) by A.M. Best.

Nine of our eighteenseventeen insurance subsidiaries are rated by Standard & Poor's (S&P)., while our Lloyd's syndicate is part of a group rating for the Lloyd's overall market. All nine of our insurance subsidiaries rated by S&P have been assigned an FSR of "A" (strong). OurThe Lloyd's syndicate is part of a group rating for the Lloyd's overall market, which has been assigned an FSR of "A+" (strong) by S&P.

Five of our eighteenseventeen insurance subsidiaries are rated by Moody's Corporation (Moody's). All five insurance subsidiaries rated by Moody's have been assigned an FSR of "A2" (good).

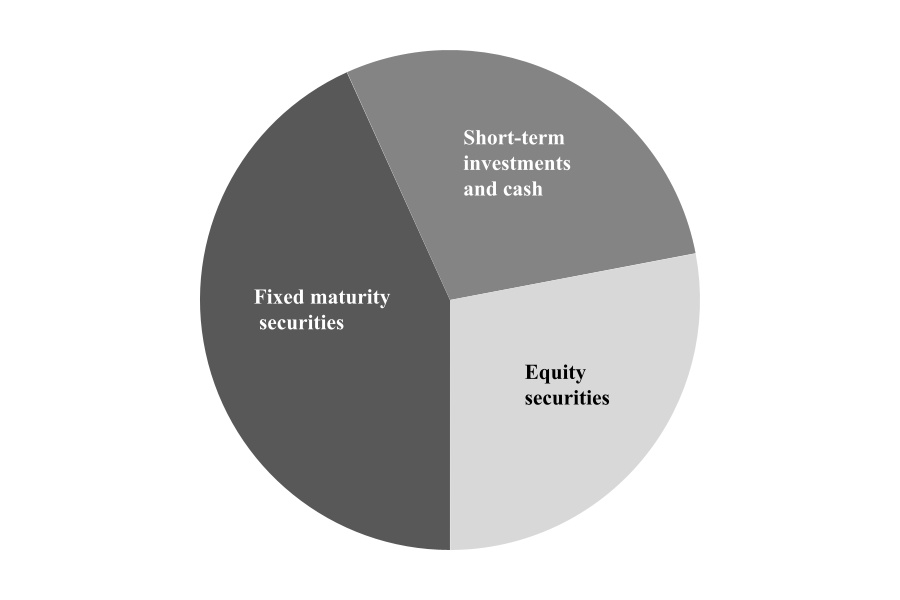

Investments

Our business strategy recognizesinvestment operations manage the importancecapital held within our underwriting operations, as well as capital allocated by Markel Group. Invested assets managed through our investment operations includes our portfolio of both consistentpublicly traded fixed maturity and equity securities, as well as cash and short-term investments.

Our underwriting and operating profits and superioroperations provide our investment returns to build shareholder value. The majorityoperations with steady inflows of our investable assets come from premiums paid by policyholders. We rely on sound underwriting practices to produce investable funds. Policyholderpremiums. These funds are invested predominantly in high-quality government and municipal bonds and mortgage-backed securities that generally match the duration and currency of our loss reserves. We typically hold these fixed maturity investments until maturity. As a result, unrealized holding gains and losses on these securities are generally expected to reverse as the securities mature. Premiums collected through our underwriting operations may also be held as short-term investments or cash and cash equivalents to provide short-term liquidity for projected claims payments, reinsurance costs and operating expenses. The balance of

Our investments in equity securities are predominantly held within our investable assets, comprised of shareholder funds,regulated insurance subsidiaries to support capital requirements. Capital held by our insurance subsidiaries beyond that which we anticipate will be needed to cover claims payments and operating expenses is available to be invested in equity securities, which overalong with additional capital allocated for investment purposes by Markel Group. We allocate a higher percentage of capital to equity securities than most other insurance companies. Over the long run, equity securities have produced higher returns relative to fixed maturity securities and short-term investments.