UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

|

☒x

| ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 20182021

OR

|

|

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________to______________________

COMMISSION FILE NUMBER 001-38229

FIDELITY D & D BANCORP, INC.

COMMONWEALTH OF PENNSYLVANIA I.R.S. EMPLOYER IDENTIFICATION NO: 23-3017653

BLAKELY AND DRINKER STREETS

DUNMORE, PENNSYLVANIA 18512

TELEPHONE NUMBER (570) 342-8281

SECURITIES REGISTERED UNDER SECTION 12(b) OF THE ACT:

Common Stock, without par value

|

|

|

|

|

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

Common Stock, without par value |

| FDBC |

| The NASDAQ Stock Market, LLC |

NAME OF EACH EXCHANGE ON WHICH REGISTERED:

The NASDAQ Stock Market LLC

SECURITIES REGISTERED UNDER SECTION 12(g) OF THE ACT:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐o No ☒x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐o No ☒x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒x No ☐o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒Yes x No ☐o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by references in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

Large accelerated filer ☐o | Non-accelerated filer ☐x | Accelerated filer ☒o |

| Smaller reporting company ☒x | Emerging growth company ☐o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐o

Indicate by check mark whether the registrant has filed a report on the attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐o No ☒x

The aggregate market value of the voting common stock held by non-affiliates of the registrant was $172.4$216.2 million as of June 30, 2018,2021, based on the closing price of $61.99.$54.10. The number of shares of common stock outstanding as of February 28, 2019,2022, was 3,780,975.5,659,018.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement to be used in connection with the 20192022 Annual Meeting of Shareholders are incorporated herein by reference in partial response to Part III.

Fidelity D & D Bancorp, Inc.

20182021 Annual Report on Form 10-K

Table of Contents

FIDELITY D & D BANCORP, INC.

PART I

Forward-Looking Statements

Certain of the matters discussed in this Annual Report on Form 10-K may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended, and as such may involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. The words “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” and similar expressions are intended to identify such forward-looking statements.

The Company’s actual results may differ materially from the results anticipated in these forward-looking statements due to a variety of factors, including, without limitation:

| §

| | the effects of economic conditions on current customers, specifically the effect of the economy on loan customers’ ability to repay loans;

|

| §

| | the costs and effects of litigation and of unexpected or adverse outcomes in such litigation;

|

| §

| | the impact of new or changes in existing laws and regulations, including the Tax Cuts and Jobs Act and Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the regulations promulgated there under;

|

| §

| | impacts of the capital and liquidity requirements of the Basel III standards and other regulatory pronouncements, regulations and rules;

|

| §

| | governmental monetary and fiscal policies, as well as legislative and regulatory changes;

|

| §

| | effects of short- and long-term federal budget and tax negotiations and their effect on economic and business conditions;

|

| §

| | the effect of changes in accounting policies and practices, as may be adopted by the regulatory agencies, as well as the Financial Accounting Standards Board and other accounting standard setters;

|

| §

| | the risks of changes in interest rates on the level and composition of deposits, loan demand, and the values of loan collateral, securities and interest rate protection agreements, as well as interest rate risks;

|

| §

| | the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market area and elsewhere, including institutions operating locally, regionally, nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer and the internet;

|

| §

| | the interruption or breach in security of our information systems and other technological risks and attacks resulting in failures or disruptions in customer account management, general ledger processing and loan or deposit updates and potential impacts resulting therefrom including additional costs, reputational damage, regulatory penalties, and financial losses;

|

| §

| | acquisitions and integration of acquired businesses;

|

| §

| | the failure of assumptions underlying the establishment of reserves for loan losses and estimations of values of collateral and various financial assets and liabilities;

|

| §

| | volatilities in the securities markets;

|

| §

| | acts of war or terrorism;

|

| §

| | disruption of credit and equity markets; and

|

| §

| | the risk that our analyses of these risks and forces could be incorrect and/or that the strategies developed to address them could be unsuccessful.

|

the effects of economic conditions particularly with regard to the negative impact of severe, wide-ranging and continuing disruptions caused by the spread of Coronavirus Disease 2019 (COVID-19) and any other pandemic, epidemic or other health-related crisis and responses thereto on current customers and the operations of the Company, specifically the effect of the economy on loan customers’ ability to repay loans;

the costs and effects of litigation and of unexpected or adverse outcomes in such litigation;

the impact of new or changes in existing laws and regulations, including laws and regulations concerning taxes, banking, securities and insurance and their application with which the Company and its subsidiaries must comply;

impacts of the capital and liquidity requirements of the Basel III standards and other regulatory pronouncements, regulations and rules;

governmental monetary and fiscal policies, as well as legislative and regulatory changes;

effects of short- and long-term federal budget and tax negotiations and their effect on economic and business conditions;

the effect of changes in accounting policies and practices, as may be adopted by the regulatory agencies, as well as the Financial Accounting Standards Board and other accounting standard setters;

the risks of changes in interest rates on the level and composition of deposits, loan demand, and the values of loan collateral, securities and interest rate protection agreements, as well as interest rate risks;

the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market area and elsewhere, including institutions operating locally, regionally, nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer and the internet;

technological changes;

the interruption or breach in security of our information systems, continually evolving cybersecurity and other technological risks and attacks resulting in failures or disruptions in customer account management, general ledger processing and loan or deposit updates and potential impacts resulting therefrom including additional costs, reputational damage, regulatory penalties, and financial losses;

acquisitions and integration of acquired businesses;

the failure of assumptions underlying the establishment of reserves for loan losses and estimations of values of collateral and various financial assets and liabilities;

inflation, securities markets and monetary fluctuations and volatility;

the short-term and long-term effects of inflation, and rising costs to the Company, its customers and on the economy;

acts of war or terrorism;

disruption of credit and equity markets; and

the risk that our analyses of these risks and forces could be incorrect and/or that the strategies developed to address them could be unsuccessful.

The Company cautions readers not to place undue reliance on forward-looking statements, which reflect analyses only as of the date of this document. The Company has no obligation to update any forward-looking statements to reflect events or circumstances after the date of this document.

Readers should review the risk factors described in this document and other documents that we file or furnish, from time- to-time, with the Securities and Exchange Commission, including quarterly reports filed on Form 10-Q and any current reports filed or furnished on Form 8-K.

ITEM 1:

BUSINESS

Fidelity D & D Bancorp, Inc. (the Company) was incorporated in the Commonwealth of Pennsylvania, on August 10, 1999, and is a bank holding company, whose wholly-owned state chartered commercial bank subsidiary is The Fidelity Deposit and Discount Bank (the Bank) (collectively, the Company). The Company is headquartered at Blakely and Drinker Streets in Dunmore, Pennsylvania.

The Bank has offered a full range of traditional banking services since it commenced operations in 1903. The Bank has a personal and corporate trust department and also provides alternative financial and insurance products with asset management services. A full list of services provided by the Bank is detailed in the section entitled “Products and Services” contained

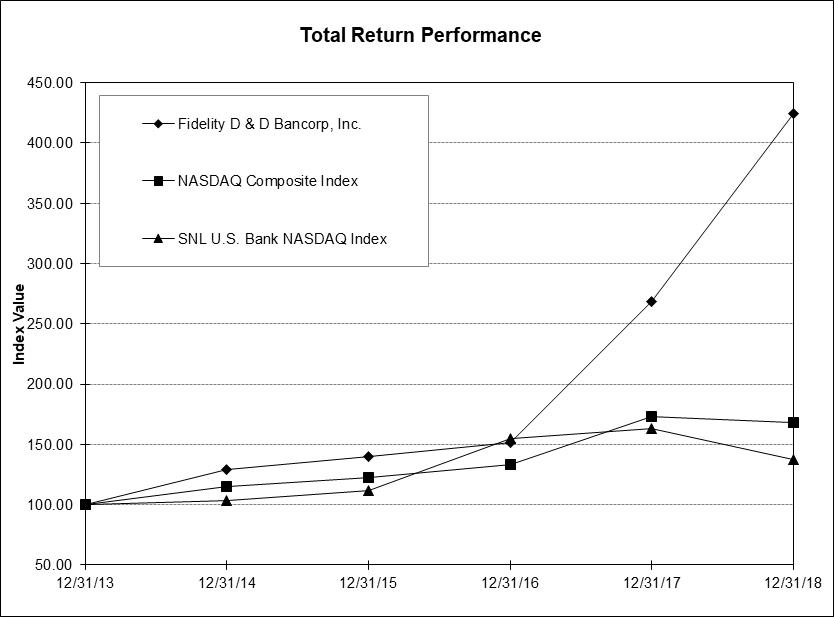

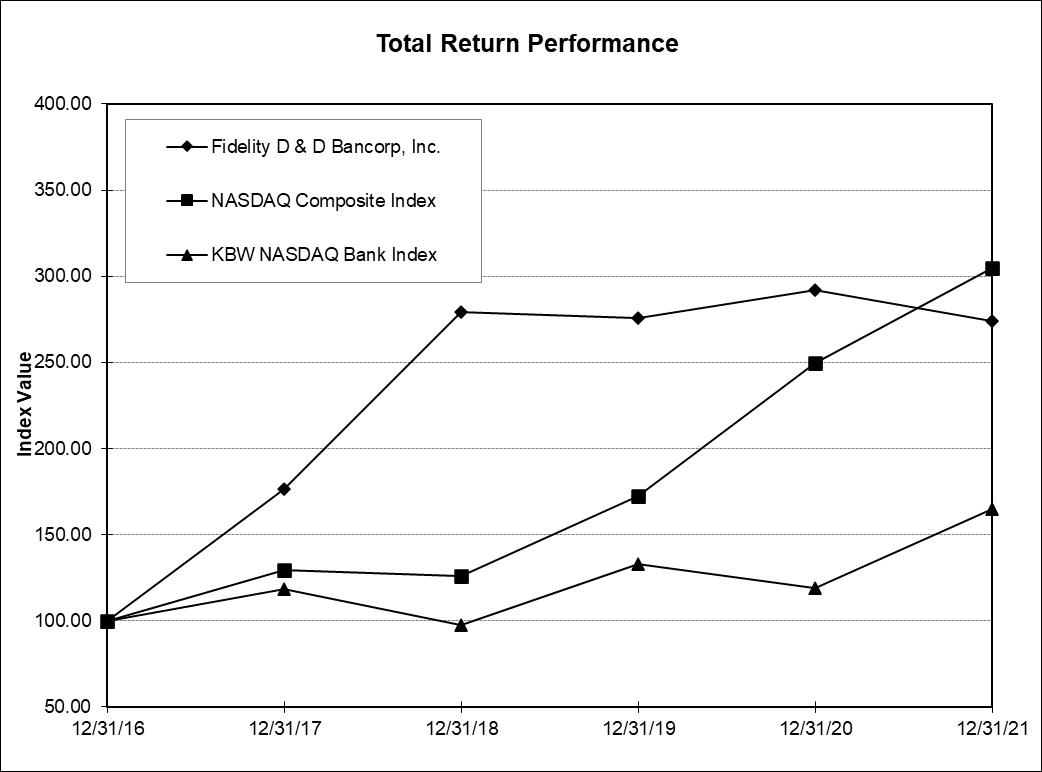

within the 20182021 Annual Report to Shareholders, incorporated by reference. The service area is comprised of the Borough of Dunmore and the surrounding communities within Lackawanna and Luzerne counties in Northeastern Pennsylvania and Northampton County in Eastern Pennsylvania. In 2018,2021, the Company had 6.12%12.95% of the Scranton-Wilkes-Barre metropolitan statistical area’sLackawanna County’s total deposit market share ranking 7th2nd in total deposits, 6.94% of Luzerne County’s total deposit market share ranking 6th in total deposits and 6.49% of Northampton County’s total deposit market share ranking 6th in total deposits. The

On July 1, 2021, the Company had 181 full-time equivalent employees on December 31, 2018,completed its acquisition of Landmark Bancorp, Inc. (“Landmark”) of Pittston, Pennsylvania. Landmark was the holding company of Landmark Community Bank (“Landmark Bank”) which includes exempt officers, exempt, non-exempt and part-time employees.operated 5 retail community banking offices in Northeastern Pennsylvania.

On May 1, 2020, the Company completed its acquisition of MNB Corporation (“MNB”) of Bangor, Pennsylvania. MNB was the holding company Merchants Bank of Bangor (“Merchants Bank”) which operated nine bank centers located in Northampton County, Pennsylvania.

The banking business is highly competitive, and the success and profitability of the Company depends principally on its ability to compete in its market area. Competition includes, among other sources: local community banks; savings banks; regional banks; national banks; credit unions; savings & loans; insurance companies; money market funds; mutual funds; small loan companies and other financial services companies. The Company has been able to compete effectively with other financial institutions by emphasizing customer service enhanced by local decision making. These efforts enable the Company to establish long-term customer relationships and build customer loyalty by providing products and services designed to address their specific needs.

The banking industry is affected by general economic conditions including the effects of inflation, recession, unemployment, real estate values, trends in national and global economies and other factors beyond the Company’s control. The Company’s success is dependent, to a significant degree, on economic conditions in Northeastern Pennsylvania, especially within Lackawanna and Luzerne counties and Eastern Pennsylvania, especially Northampton County which the Company defines as its primary market area.areas. An economic recession or a delayed economic recovery over a prolonged period of time in the Company’s market could cause an increase in the level of the Company’s non-performing assets and loan losses, and thereby cause operating losses, impairment of liquidity and erosion of capital. There are no concentrations of loans or customers that, if lost, would have a material adverse effect on the continued business of the Company. There is no material concentration within a single industry or a group of related industries that is vulnerable to the risk of a near-term severe impact.

The Company’s profitability is significantly affected by general economic and competitive conditions, changes in market interest rates, government policies and actions of regulatory authorities. The Company’s loan portfolio is comprised principally of residential real estate, consumer, commercial and commercial real estate loans. The properties underlying the Company’s mortgages are concentrated in Northeastern and Eastern Pennsylvania. Credit risk, which represents the possibility of the Company not recovering amounts due from its borrowers, is significantly related to local economic conditions in the areas where the properties are located as well as the Company’s underwriting standards. Economic conditions affect the market value of the underlying collateral as well as the levels of adequate cash flow and revenue generation from income-producing commercial properties.

During 2018,2021, the national economy continuedstarted to improverecover from the effects of the COVID-19 pandemic with the unemployment rate droppingfalling to 3.9% compared to 4.1%6.7% at the end of 2017.2020. The unemployment raterates in the Company’s local statistical market, Scranton-Wilkes-Barre, fellmarkets, Scranton-Wilkes-Barre-Hazleton and Allentown-Bethlehem-Easton, dropped to 4.8% and 4.0%, respectively, from 5.0%8.0% and 6.6%, respectively, at the end of 2017.2020. The local economy has been volatile in recent years and generally lags the national market trends. The Company’s credit function strives to mitigate the negative impact of economic conditions by maintaining strict underwriting principles for commercial and consumer lending and ensuring that home mortgage underwriting adheres to the standards of secondary market makers. In addition,As it has in the past, the Company strivescontinued to accelerate thepursue property foreclosure, process thereby lesseningwherever possible, to lessen the negative financial impact of foreclosed property ownership. However, during 2020 and 2021, the Company respected the foreclosure and eviction moratoriums for all loans similar to those outlined in the CARES Act for Federal National Mortgage Association (“FNMA”) and Federal Home Loan Mortgage Corporation (“FHLMC”) loans. Also, the pandemic forced the closure of courthouses which delayed the Company’s ability to affect foreclosures for those borrowers where CARES Act moratoriums would not reasonably apply. Refer to Item 1A, “Risk Factors” for material risks and uncertainties that management believes affect the Company.

Federal and state banking laws contain numerous provisions that affect various aspects of the business and operations of the Company and the Bank. The Company is subject to, among others, the regulations of the Securities and Exchange Commission (the SEC) and the Federal Reserve Board (the FRB) and the Bank is subject to, among others, the regulations of the Pennsylvania Department of Banking and Securities, the Federal Deposit Insurance Corporation (the FDIC) and the rules promulgated by the Consumer Financial Protection Bureau (the CFPB) but continues to be examined and supervised by federal banking regulators for consumer compliance purposes. Refer to Part II, Item 7 “Supervision and Regulation” for

descriptions of and references to applicable statutes and regulations which are not intended to be complete descriptions of these provisions or their effects on the Company or the Bank. They are summaries only and are qualified in their entirety by reference to such statutes and regulations. Applicable regulations relate to, among other things:

|

|

|

• operations | • consolidation | • disclosure |

• securities | • reserves | • community reinvestment |

• risk management | • dividends | • mergers |

• consumer compliance | • branches | |

• mergers

| • capital adequacy | |

The Bank is examined periodically by the Pennsylvania Department of Banking and Securities and the FDIC.

The Company’s website address is http://www.bankatfidelity.com. The Company makes available free of charge on or through this website the annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and amendments to those reports as soon as reasonably practical after filing with the SEC. You may read and copyThis reference to the Company’s website shall not, under any materialscircumstances, be deemed to incorporate the information available at such Internet address into this Form 10-K or other SEC filings. The information available at the Company’s website is not part of this Form 10-K or any other report filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.SEC. The SEC also maintains an internet site that contains reports, proxy and information statements and other information about the Company at http://www.sec.gov.

The Company’s accounting policies and procedures are designed to comply with accounting principles generally accepted in the United States of America (GAAP). Refer to “Critical Accounting Policies,” which are incorporated by reference in Part II, Item 7.

Human Capital

Mission and Core Values

Mission: We are Fidelity Bank. We are passionate about success and committed to building strong relationships through exceptional experiences. We will be the Best Bank for our Bankers to work, our Clients to bank, our Shareholders to invest and for our Community to prosper. Our bankers are our first stakeholder by design as their actions, knowledge and focus on the client experience drive our success. We continuously invest in our bankers by offering a competitive compensation, a strong benefit package for themselves and their families, opportunity to invest in the Company through stock ownership, continuous learning, career development and programs to engage and enhance the work experience.

Fidelity Bankers have a voice in the Company and are called upon to provide opinions and ideas through dialogue programs, Service Quality Surveys and the annual Climate Survey. Collectively, they have assisted in the development of the Core Values:

Relationships

Integrity

Commitment

Passion

Innovation

Success

Culturally, the Fidelity Model Experience provides a strategic vision to build a performance based corporation. It guides all bankers on solidifying internal and external relationships and becoming the Trusted Financial Advisor for our clients.

Demographics

As of December 31, 2021, the Company employed 319 bankers within our network located in Northeast and Lehigh Valley, Pennsylvania. The Company employed 28 part-time bankers and 291 full-time bankers. Employment levels are aligned with the needs of the business.

Health and Wellness - Supporting Bankers during the COVID-19 Pandemic.

In response to the pandemic, the Company took substantial steps to protect and to provide for the safety of the workforce. An immediate shift was made to provide support bankers with the tools to work from home. Safety protocols were put into place in all offices – bankers on-site were required to wear masks, handwashing protocols were established, social distancing measures were implemented including instruction for all bankers and signage for client entry into offices. Enhanced cleaning protocols were implemented in accordance with CDC guidelines. Protective barriers were installed in all areas of client interaction. The Company continues these mitigating practices and modifies as needed.

The Company adhered to the guidelines of the Families First Coronavirus Response Act (FFCRA) ensuring bankers were paid while encountering the effects of COVID-19 isolations, quarantines and child care needs. Where applicable, bankers were compensated above the requirements of the Act for needed time off. Additionally, special compensation practices were put into place including a Front Line Heroes Bonus to reward retail branch bankers that face clients daily. Incentive payouts were enhanced because of the bankers’ inability to cultivate face-to-face branch sales opportunities and earn rewards. To

help promulgate the health and wellness of our bankers, special well-being programs and initiatives were instituted. Bankers are granted additional time off for COVID-19 vaccine administration.

Diversity and Inclusion

We are committed to promoting a diverse and inclusive workforce and value the strength it brings to our organization. Our hiring practices include outreach to organizations representing groups of color and ethnicity, veteran status, disabled persons and women. Recruitment sources are varied to reach a broad audience. Our practices have resulted in a continuously increased diverse representation and an enhanced ability to provide for the diverse needs of the communities we serve. The Affirmative Action Plan monitors our success in creating equal employment opportunities for our bankers and our applicants and guides us in hiring practices.

Training and Development

The investment into the continuous improvement of all of our bankers is evident in the bank’s commitment of training dollars and resources. Key Performance Indicators (KPIs), tracked quarterly, outline training goals bank-wide and training dollars spent. The Company has a devoted training team and all bankers are offered and encouraged to participate in continuous training initiatives. Innovative programs, including Fidelity Bank University, are offered to educate bankers at all levels.

The bank monitors other Human Capital KPIs tracking banker activities; KPIs include and are not limited to community service and participation goals, turnover, new hire retention and climate survey scores. Results are monitored against goals.

We believe the banker engagement is a tenet of our success. Our practice of giving each banker a voice, providing fair compensation and opportunity for stock ownership, recognizing exceptional service, providing a quality benefit and retirement package, promoting career development opportunities and delivering strong programs and processes creates a strong and engaged workforce. The programs assist in aligning the interests of the bankers with those of the shareholders and they provide further incentive to bankers to enhance the financial results of the Company.

ITEM 1A:RISK FACTORS

An investment in the Company’s common stock is subject to risks inherent to the Company’s business. The material risks and uncertainties that management believes affect the Company are described below. Before making an investment decision, you should carefully consider the risks and uncertainties described below together with all of the other information included or incorporated by reference in this report. The risks and uncertainties described below are not the only ones facing the Company. Additional risks and uncertainties that management is not aware of or focused on or that management currently deems immaterial may also impair the Company’s business operations. This report is qualified in its entirety by these risk factors.

If any of the following risks actually occur, the Company’s financial condition and results of operations could be materially and adversely affected. If this were to happen, the value of the Company’s common stock could decline significantly, and you could lose all or part of your investment.

Risks Related to the Company’s Business

The short-term and long-term effects of inflation and rising costs may adversely affect the Company’s financial performance.

Inflation, both in the short-term and/or in the long-term, may adversely affect the Company’s business in that it may increase our overall costs even if it does not adversely affect every aspect of our business evenly. The Company employs various strategies to manage its costs but there is no assurance that these strategies will be successful in containing costs as higher rates of inflation may result in increased costs for goods and services, including employee salaries and benefits, which may adversely affect the Company’s results of operation and financial performance. Inflation may also increase the cost of doing business for the Company’s borrowers thereby affecting the creditworthiness of current or prospective customers.

The Company’s business is subject to interest rate risk and variations in interest rates may negatively affect its financial performance.

Changes in the interest rate environment may reduce profits. The Company’s earnings and cash flows are largely dependent upon its net interest income. Net interest income is the difference between the interest earned on loans, securities and other interest-earning assets, and interest paid on deposits, borrowings and other interest-bearing liabilities. As prevailing interest rates change, net interest spreads are affected by the difference between the maturities and re-pricing characteristics of interest-earning assets and interest-bearing liabilities. In addition, loan volume and yields are affected by market interest rates on loans, and rising interest rates generally are associated with a lower volume of loan originations. An increase in the general level of interest rates may also adversely affect the ability of certain borrowers to pay the interest on and principal of their obligations. Accordingly, changes in levels of market interest rates could materially adversely affect the Company’s net interest spread, asset quality, loan origination volume and overall profitability.

The Company is subject to lending risk.

There are inherent risks associated with the Company’s lending activities. These risks include, among other things, the impact of changes in interest rates and changes in the economic conditions in the markets where the Company operates as

well as those across the Commonwealth of Pennsylvania and the United States. Increases in interest rates and/or weakening economic conditions could adversely impact the ability of borrowers to repay outstanding loans or the value of the collateral securing these loans. The Company is also subject to various laws and regulations that affect its lending activities. Failure to comply with applicable laws and regulations could subject the Company to regulatory enforcement action that could result in the assessment of significant civil money penalties against the Company.

Commercial, commercial real estate and real estate construction loans are generally viewed as having more risk of default than residential real estate loans or consumer loans. These types of loans are also typically larger than residential real estate loans and consumer loans. Because these loans generally have larger balances than residential real estate loans and consumer loans, the deterioration of one or a few of these loans could cause a significant increase in non-performing loans. An increase in non-performing loans could result in a net loss of earnings from these loans, an increase in the provision for possible loan losses and an increase in loan charge-offs, all of which could have a material adverse effect on the Company’s financial condition and results of operations.

The Company’s allowance for possible loan losses may be insufficient.

The Company maintains an allowance for possible loan losses, which is a reserve established through a provision for possible loan losses charged to expense, that represents management’s best estimate of probable losses that have been incurred within the existing portfolio of loans. The allowance, in the judgment of management, is necessary to reserve for estimated loan losses and risks inherent in the loan portfolio. The level of the allowance reflects management’s continuing evaluation of industry concentrations; specific credit risks; loan loss experience; current loan portfolio quality; present economic, political and regulatory conditions and unidentified losses inherent in the current loan portfolio. The determination of the appropriate level of the allowance for possible loan losses inherently involves a high degree of subjectivity and requires the Company to make significant estimates of current credit risks and future trends, all of which may undergo material changes. Changes in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside of the Company’s control, may require an increase in the allowance for possible loan losses. In addition, bank regulatory agencies periodically review the Company’s allowance for loan losses and may require an increase in the provision for possible loan losses or the recognition of further loan charge-offs, based on judgments different than those of management. In addition,Further, if charge-offs in future periods exceed the allowance for possible loan losses, the Company will need additional provisions to increase the allowance for possible loan losses. Any increases in the allowance for loan losses will result in a decrease in net income and capital and may have a material adverse effect on the

Company’s financial condition and results of operations.

The FASB has recently issued an accounting standard update that will result in a significant change in how we recognize credit losses and may have a material impact on our financial condition or results of operations.

In June 2016, the Financial Accounting Standards Board (“FASB”) issued an accounting standard update (“ASU”) entitled “Financial Instruments-Credit Losses (Topic 326), Measurement of Credit Losses on Financial Instruments,” which replaces the current “incurred loss” model for recognizing credit losses with an “expected loss” model referred to as the Current Expected Credit Loss (“CECL”) model. Under the CECL model, banks will be required to present certain financial assets carried at amortized cost, such as loans held for investment and held-to-maturity debt securities, at the net amount expected to be collected. The measurement of expected credit losses is to be based on information about past events, including historical experience, current conditions, and reasonable and supportable forecasts that affect the collectability of the reported amount. This measurement will take place at the time the financial asset is first added to the balance sheet and periodically thereafter. This differs significantly from the “incurred loss” model required under current generally accepted accounting principles (“GAAP”), which delays recognition until it is probable a loss has been incurred.

TheUntil recently, the new CECL standard willwas expected to become effective for the Company for the fiscal year beginningon January 1, 2020, and for interim periods thereafter.within that year. In November 2019, FASB agreed to delay implementation of the new CECL standard for certain companies, including those companies that qualify as a smaller reporting company under SEC rules, until January 1, 2023. The Company is currently evaluatingexpects to continue to qualify as a smaller reporting company, based upon the current SEC definition, and as a result will likely be able to defer implementation of the new CECL standard for a period of time. Nevertheless, the Company continues to evaluate the impact the CECL model will have on its accounting. There is a risk thatthe accounting for credit losses, but the Company mayexpects to recognize a one-time cumulative-effect adjustment to itsthe allowance for loan losses as of the beginning of the first reporting period in which the new standard is effective, consistent with regulatory expectations set forth in interagency guidance issued at the end of 2016. The Company cannot yet determine the magnitude of any such one-time cumulative adjustment or of the overall impact of the new standard on its business, financial condition, and results of operations. Accordingly, it is possible the new standard may require an increase in the allowance for credit losses for the estimated life of the financial asset, including an allowance for debt securities. The amount of the change in the allowance for credit losses, if any, resulting from the new guidance will be impacted by the portfolio composition and asset quality at the adoption date, as well as economic conditions and forecasts at the time of adoption. Moreover, the CECL model may create more volatility in the level of the allowance for loan losses. If the Company is required to materially increase the level of its allowance for loan losses for any reason, such increase could adversely affect its business, financial condition and results of operations.

If we conclude that the decline in value of any of our investment securities is other-than-temporary, we will be required to write down the credit-related portion of the impairment of that security through a charge to earnings.

We review our investment securities portfolio at each quarter-end reporting period to determine whether the fair value is below the current carrying value. When the fair value of any of our investment securities has declined below its carrying value, we are required to assess whether the decline is other-than-temporary. If we conclude that the decline is other-than-temporary, we will be required to write down the credit-related portion of the impairment of that security through a charge to earnings.

The Basel III capital requirements may require us to maintain higher levels of capital, which could reduce our profitability.

Basel III targets higher levels of base capital, certain capital buffers and a migration toward common equity as the key source of regulatory capital. Although the new capital requirements are phased in over the next decade and may change substantially before final implementation, Basel III signals a growing effort by domestic and international bank regulatory agencies to require financial institutions, including depository institutions, to maintain higher levels of capital. The direction of the Basel III implementation activities or other regulatory viewpoints could require additional capital to support our business risk profile prior to final implementation of the Basel III standards. If the Company and the Bank are required to maintain higher levels of capital, the Company and the Bank may have fewer opportunities to invest capital into interest-earning assets, which could limit the profitable business operations available to the Company and the Bank and adversely impact our financial condition and results of operations.

The Company may need or be compelled to raise additional capital in the future, but that capital may not be available when it is needed and on terms favorable to current shareholders.

Federal banking regulators require the Company and Bank to maintain adequate levels of capital to support their operations. These capital levels are determined and dictated by law, regulation and banking regulatory agencies. In addition, capital levels are also determined by the Company’s management and board of directors based on capital levels that they believe are necessary to support the Company’s business operations. The Company is evaluating its present and future capital requirements and needs, is developing a comprehensive capital plan and is analyzing capital raising alternatives, methods and options. Even if the Company succeeds in meeting the current regulatory capital requirements, the Company may need to raise additional capital in the near future to support possible loan losses during future periods or to meet future regulatory capital requirements.

Further, the Company’s regulators may require it to increase its capital levels. If the Company raises capital through the issuance of additional shares of its common stock or other securities, it may dilute the ownership interests of current investors and may dilute the per-share book value and earnings per share of its common stock. Furthermore, it may have an adverse impact on the Company’s stock price. New investors may also have rights, preferences and privileges senior to the Company’s current shareholders, which may adversely impact its current shareholders. The Company’s ability to raise

additional capital will depend on conditions in the capital markets at that time, which are outside its control, and on its financial performance. Accordingly, the Company cannot assure you of its ability to raise additional capital on terms and time frames acceptable to it or to raise additional capital at all. If the Company cannot raise additional capital in sufficient amounts when needed, its ability to comply with regulatory capital requirements could be materially impaired. Additionally, the inability to raise capital in sufficient amounts may adversely affect the Company’s operations, financial condition and results of operations.

The Company is subject to environmental liability risk associated with lending activities.

A significant portion of the Company’s loan portfolio is secured by real property. During the ordinary course of business, the Company may foreclose on and take title to properties securing certain loans. In doing so, there is a risk that hazardous or toxic substances could be found on these properties. If hazardous or toxic substances are found, the Company may be liable for remediation costs, as well as for personal injury and property damage. Environmental laws may require the Company to incur substantial expense and may materially reduce the affected property’s value or limit the Company’s ability to use or sell the affected property. In addition, future laws or more stringent interpretations or enforcement policies with respect to existing laws may increase the Company’s exposure to environmental liability. Although the Company has policies and procedures to perform an environmental review before initiating any foreclosure action on real property, these reviews may not be sufficient to detect all potential environmental hazards. The remediation costs and any other financial liabilities associated with an environmental hazard could have a material adverse effect on the Company’s financial condition and results of operations.

The Company’s profitability depends significantly on economic conditions in the Commonwealth of Pennsylvania and the local region in which it conducts business.

The Company’s success depends primarily on the general economic conditions of the Commonwealth of Pennsylvania and the specific local markets in which the Company operates. Unlike larger national or other regional banks that are more geographically diversified, the Company provides banking and financial services to customers primarily in Lackawanna and Luzerne Counties in Northeastern Pennsylvania and Northampton County in Eastern Pennsylvania. The local economic conditions in these areas have a significant impact on the demand for the Company’s products and services as well as the

ability of the Company’s customers to repay loans, the value of the collateral securing loans and the stability of the Company’s deposit funding sources. A significant decline in general economic conditions caused by inflation, recession, acts of terrorism, an outbreak of hostilities or other international or domestic occurrences, unemployment, changes in securities markets or other factors could impact these local economic conditions and, in turn, have a material adverse effect on the Company’s financial condition and results of operations.

There is no assurance that the Company will be able to successfully compete with others for business.

The Company competes for loans, deposits and investment dollars with numerous regional and national banks and other community banking institutions, as well as other kinds of financial institutions and enterprises, such as securities firms, insurance companies, savings associations, credit unions, mortgage brokers and private lenders. Many competitors have substantially greater resources than the Company does, and operate under less stringent regulatory environments. The differences in resources and regulations may make it more difficult for the Company to compete profitably, reduce the rates that it can earn on loans and on its investments, increase the rates it must offer on deposits and other funds, and adversely affect its overall financial condition and earnings.

The Company is subject to extensive government regulation and supervision.

The Company, primarily through the Bank, is subject to extensive federal and state regulation and supervision. Banking regulations are primarily intended to protect depositors’ funds, federal deposit insurance funds and the banking system as a whole, not shareholders. These regulations affect the Company’s lending practices, capital structure, investment practices, dividend policy and growth, among other things. Federal or commonwealth regulatory agencies continually review banking laws, regulations and policies for possible changes. Changes to statutes, regulations or regulatory policies, including changes in interpretation or implementation of statutes, regulations or policies, could affect the Company in substantial and unpredictable ways. Such changes could subject the Company to additional costs, limit the types of financial services and products the Company may offer and/or increase the ability of non-banks to offer competing financial services and products, among other things. Failure to comply with laws, regulations or policies could result in sanctions by regulatory agencies, civil money penalties and/or reputation damage, which could have a material adverse effect on the Company’s business, financial condition and results of operations. While the Company has policies and procedures designed to prevent any such violations, there can be no assurance that such violations will not occur.

The Company’s controls and procedures may fail or be circumvented.

Management regularly reviews and updates the Company’s internal controls, disclosure controls and procedures, and corporate governance policies and procedures. Any system of controls, however well designed and operated, is based in part on certain assumptions and can provide only reasonable, not absolute, assurances that the objectives of the system are met. Any failure or circumvention of the Company’s controls and procedures or failure to comply with regulations related to controls and procedures could have a material adverse effect on the Company’s business, results of operations and financial condition.

New lines of business or new products and services may subject the Company to additional risks.

From time-to-time, the Company may implement new lines of business or offer new products and services within existing lines of business. There are substantial risks and uncertainties associated with these efforts, particularly in instances where the markets are not fully developed. In developing and marketing new lines of business and/or new products and services the Company may invest significant time and resources. Initial timetables for the introduction and development of new lines of business and/or new products or services may not be achieved and price and profitability targets may not prove feasible. External factors, such as compliance with regulations, competitive alternatives, and shifting market preferences, may also impact the successful implementation of a new line of business or a new product or service. Furthermore, any new line of business and/or new product or service could have a significant impact on the effectiveness of the Company’s system of internal controls. Failure to successfully manage these risks in the development and implementation of new lines of business or new products or services could have a material adverse effect on the Company’s business, results of operations and financial condition.

The Company’s future acquisitions could dilute your ownership and may cause it to become more susceptible to adverse economic events.

The Company may use its common stock to acquire other companies or make investments in banks and other complementary businesses in the future. The Company may issue additional shares of common stock to pay for future acquisitions, which would dilute your ownership interest in the Company. Future business acquisitions could be material to the Company, and the degree of success achieved in acquiring and integrating these businesses into the Company could have a material effect on the value of the Company’s common stock. In addition, any acquisition could require it to use substantial cash or other liquid assets or to incur debt. In those events, it could become more susceptible to economic downturns and competitive pressures.

The Company may not be able to attract and retain skilled people.

The Company’s success depends, in large part, on its ability to attract and retain key people. Competition for the best people in most activities engaged in by the Company can be intense and the Company may not be able to hire people or to retain

them. The unexpected loss of services of one or more of the Company’s key personnel could have a material adverse impact on the Company’s business because of their skills, knowledge of the Company’s market, years of industry experience and the difficulty of promptly finding qualified replacement personnel.

The Company’s information systems may experience an interruption or breach in security.

The Company relies heavily on communications and information systems to conduct its business. Any failure, interruption or breach in security of these systems could result in failures or disruptions in the Company’s customer relationship management, general ledger, deposit, loan and other systems. The Company has policies and procedures designed to prevent or limit the effect of the failure, interruption or security breach of its information systems, however there can be no assurance that any such failures, interruptions or security breaches will not occur. The occurrence of any failures, interruptions or security breaches of the Company’s information systems could damage the Company’s reputation, result in a loss of customer business, subject the Company to additional regulatory scrutiny, or expose the Company to civil litigation and possible financial liability, any of which could have a material adverse effect on the Company’s financial condition and results of operations.

The Company continually encounters technological change.

The financial services industry is continually undergoing rapid technological change with frequent introductions of new technology-driven products and services. The effective use of technology increases efficiency and enables financial institutions to better serve customers and to reduce costs. The Company’s future success depends, in part, upon its ability to address the needs of its customers by using technology to provide products and services that will satisfy customer demands, as well as to create additional efficiencies in the Company’s operations. Many of the Company’s competitors have substantially greater resources to invest in technological improvements. The Company may not be able to effectively implement new technology-driven products and services or be successful in marketing these products and services to its customers. Failure to successfully keep pace with technological change affecting the financial services industry could have a material adverse impact on the Company’s business and, in turn, the Company’s financial condition and results of operations.

The operations of our business, including our interaction with customers, are increasingly done via electronic means, and this has increased our risks related to cyber security.

We are exposed to the risk of cyber-attacks in the normal course of business. In general, cyber incidents can result from deliberate attacks or unintentional events. We have observed an increased level of attention in the industry focused on cyber-attacks that include, but are not limited to, gaining unauthorized access to digital systems for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. To combat against these attacks, policies and procedures are in place to prevent or limit the effect of the possible security breach of our information systems and we have insurance against some cyber-risks and attacks. While we have not incurred any material losses related to cyber-attacks, nor are we aware of any specific or threatened cyber-incidents as of the date of this report, we may incur substantial costs and suffer other negative consequences if we fall victim to successful cyber-attacks. Such negative consequences could include remediation costs that may include liability for stolen assets or information and repairing system damage that may have been

caused; deploying additional personnel and protection technologies, training employees, and engaging third party experts and consultants; lost revenues resulting from unauthorized use of proprietary information or the failure to retain or attract customers following an attack; litigation; and reputational damage adversely affecting customer or investor confidence.

The Company is subject to claims and litigation pertaining to fiduciary responsibility.

From time-to-time, customers make claims and take legal action pertaining to the Company’s performance of its fiduciary responsibilities. Whether customer claims and legal action related to the Company’s performance of its fiduciary responsibilities are founded or unfounded, if such claims and legal actions are not resolved in a manner favorable to the Company, they may result in significant financial liability and/or adversely affect the market perception of the Company and its products and services as well as impact customer demand for those products and services. Any financial liability or reputation damage could have a material adverse effect on the Company’s business, which, in turn, could have a material adverse effect on the Company’s financial condition and results of operations.

Pennsylvania Business Corporation Law and various anti-takeover provisions under our articles and bylaws could impede the takeover of the Company.

Various Pennsylvania laws affecting business corporations may have the effect of discouraging offers to acquire the Company, even if the acquisition would be advantageous to shareholders. In addition, we have various anti-takeover measures in place under our articles of incorporation and bylaws, including a supermajority vote requirement for mergers, a staggered board of directors, and the absence of cumulative voting. Any one or more of these measures may impede the takeover of the Company without the approval of our board of directors and may prevent our shareholders from taking part in a transaction in which they could realize a premium over the current market price of our common stock.

The Company is a holding company and relies on dividends from its banking subsidiary for substantially all of its revenue and its ability to make dividends, distributions, and other payments.

As a bank holding company, the Company’s ability to pay dividends depends primarily on its receipt of dividends from its subsidiary bank. Dividend payments from the bank are subject to legal and regulatory limitations, generally based on net profits and retained earnings, imposed by bank regulatory agencies. The ability of the bank to pay dividends is also subject to profitability, financial condition, regulatory capital requirements, capital expenditures and other cash flow requirements. There is no assurance that the bank will be able to pay dividends in the future or that the Company will generate cash flow to pay dividends in the future. The Company’s failure to pay dividends on its common stock may have a material adverse effect on the market price of its common stock.

The Company’s banking subsidiary may be required to pay higher FDIC insurance premiums or special assessments which may adversely affect its earnings.

The Company generally is unable to control the amount of premiums or special assessments that its subsidiary is required to pay for FDIC insurance. Any future changes in the calculation or assessment of FDIC insurance premiums may have a material adverse effect on our results of operations, financial condition, and our ability to continue to pay dividends on our common stock at the current rate or at all.

Severe weather, natural disasters, acts of war or terrorism, pandemics and other external events could significantly impact the Company’s business.

Severe weather, natural disasters, acts of war or terrorism, pandemics and other adverse external events could have a significant impact on the Company’s ability to conduct business. Such events could affect the stability of the Company’s deposit base, impair the ability of borrowers to repay outstanding loans, impair the value of collateral securing loans, cause significant property damage, result in loss of revenue and/or cause the Company to incur additional expenses. Severe weather or natural disasters, acts of war or terrorism, pandemics or other adverse external events may occur in the future. Although management has established disaster recovery policies and procedures, the occurrence of any such event could have a material adverse effect on the Company’s business, which, in turn, could have a material adverse effect on the Company’s financial condition and results of operations.

The increasing use of social media platforms presents new risks and challenges and our inability or failure to recognize, respond to and effectively manage the accelerated impact of social media could materially adversely impact our business.

There has been a marked increase in the use of social media platforms, including weblogs (blogs), social media websites, and other forms of Internet-based communications which allow individuals access to a broad audience of consumers and other interested persons. Social media practices in the banking industry are evolving, which creates uncertainty and risk of noncompliance with regulations applicable to our business. Consumers value readily available information concerning businesses and their goods and services and often act on such information without further investigation and without regard to its accuracy. Many social media platforms immediately publish the content their subscribers and participants post, often without filters or checks on accuracy of the content posted. Information posted on such platforms at any time may be adverse to our interests and/or may be inaccurate. The dissemination of information online could harm our business, prospects, financial condition, and results of operations, regardless of the information’s accuracy. The harm may be immediate without affording us an opportunity for redress or correction.

Other risks associated with the use of social media include improper disclosure of proprietary information, negative comments about our business, exposure of personally identifiable information, fraud, out-of-date information, and improper use by employees and customers. The inappropriate use of social media by our customers or employees could result in negative consequences including remediation costs including training for employees, additional regulatory scrutiny and possible regulatory penalties, litigation or negative publicity that could damage our reputation adversely affecting customer or investor confidence.

Federal income tax reform could have unforeseen effects on our financial condition and results of operations.

On December 22, 2017, the President of the United States signed into law H.R. 1, originally known as the “Tax Cuts and Jobs Act.” The Tax Cuts and Jobs Act includes a number of provisions, including the lowering of the U.S. corporate tax rate from 35 percent to 21 percent, effective January 1, 2018. There are also provisions that may partially offset the benefit of such rate reduction. Financial statement impacts include adjustments for, among other things, the re-measurement of deferred tax assets and liabilities. While there are benefits, there is also substantial uncertainty regarding the details of U.S. Tax Reform. The long-term intended and unintended consequences of Tax Cuts and Jobs Act on our business and on holders of our common shares is uncertain and could be adverse. The Company anticipates that the impact of Tax Cuts and Jobs Act may be material to our business, financial condition and results of operations.

Risks Associated with the Company’s Common Stock

The Company’s stock price can be volatile.

Stock price volatility may make it more difficult for you to resell your common stock when you want and at prices you find attractive. The Company’s stock price can fluctuate significantly in response to a variety of factors including, among other things:

Actual or anticipated variations in quarterly results of operations.

Recommendations by securities analysts.

Operating and stock price performance of other companies that investors deem comparable to the Company.

News reports relating to trends, concerns and other issues in the financial services industry.

Perceptions in the marketplace regarding the Company and/or its competitors.

New technology used, or services offered, by competitors.

Significant acquisitions or business combinations, strategic partnerships, joint ventures or capital commitments by or involving the Company or its competitors.

Failure to integrate acquisitions or realize anticipated benefits from acquisitions.

Changes in government regulations.

Geopolitical conditions such as acts or threats of terrorism or military conflicts.

General market fluctuations, industry factors and general economic and political conditions and events, such as economic slowdowns or recessions, interest rate changes or credit loss trends, could also cause the Company’s stock price to decrease regardless of operating results.

The trading volume in the Company’s common stock is less than that of other larger financial services companies.

The Company’s common stock is listed for trading on Nasdaq and the trading volume in its common stock is less than that of other larger financial services companies. A public trading market having the desired characteristics of depth, liquidity and orderliness depends on the presence in the marketplace of willing buyers and sellers of the Company’s common stock at any given time. This presence depends on the individual decisions of investors and general economic and market conditions over which the Company has no control. Given the lower trading volume of the Company’s common stock, significant sales of the Company’s common stock, or the expectation of these sales, could cause the Company’s stock price to fall.

Furthermore, from time to time, the Company’s common stock may be included in certain and various stock market indices. Inclusion in these indices may positively impact the price, trading volume, and liquidity of the Company’s common stock, in part, because index funds or other institutional investors often purchase securities that are in these indices. Conversely, if the Company’s market capitalization falls below the minimum necessary to be included in any of the indices at any annual reconstitution date, the opposite could occur. Further, the Company’s inclusion in indices may be weighted based on the size of its market capitalization, so even if the Company’s market capitalization remains above the amount required to be included on these indices, if its market capitalization is below the amount it was on the most recent reconstitution date, the Company’s common stock could be weighted at a lower level, holders attempting to track the composition of these indices will be required to sell the Company’s common stock to match the reweighting of the indices.

Risks Associated with the Company’s Industry

Future governmental regulation and legislation could limit the Company’s future growth.

The Company is a registered bank holding company, and its subsidiary bank is a depository institution whose deposits are insured by the FDIC. As a result, the Company is subject to various regulations and examinations by various regulatory authorities. In general, statutes establish the corporate governance and eligible business activities for the Company, certain acquisition and merger restrictions, limitations on inter-company transactions such as loans and dividends, capital adequacy requirements, requirements for anti-money laundering programs and other compliance matters, among other regulations. The Company is extensively regulated under federal and state banking laws and regulations that are intended primarily for the protection of depositors, federal deposit insurance funds and the banking system as a whole. Compliance with these statutes and regulations is important to the Company’s ability to engage in new activities and consummate additional acquisitions.

In addition, the Company is subject to changes in federal and state tax laws as well as changes in banking and credit regulations, accounting principles and governmental economic and monetary policies. The Company cannot predict whether any of these changes may adversely and materially affect it. Federal and state banking regulators also possess broad powers

to take supervisory actions as they deem appropriate. These supervisory actions may result in higher capital requirements, higher insurance

premiums and limitations on the Company’s activities that could have a material adverse effect on its business and profitability. While these statutes are generally designed to minimize potential loss to depositors and the FDIC insurance funds, they do not eliminate risk, and compliance with such statutes increases the Company’s expense, requires management’s attention and can be a disadvantage from a competitive standpoint with respect to non-regulated competitors.

The earnings of financial services companies are significantly affected by general business and economic conditions.

The Company’s operations and profitability are impacted by general business and economic conditions in the United States and abroad. These conditions include short-term and long-term interest rates, inflation, money supply, political issues, legislative and regulatory changes, fluctuations in both debt and equity capital markets, broad trends in industry and finance, and the strength of the U.S. economy and the local economies in which the Company operates, all of which are beyond the Company’s control. Deterioration in economic conditions could result in an increase in loan delinquencies and non-performing assets, decreases in loan collateral values and a decrease in demand for the Company’s products and services, among other things, any of which could have a material adverse impact on the Company’s financial condition and results of operations.

Financial services companies depend on the accuracy and completeness of information about customers and counterparties.

In deciding whether to extend credit or enter into other transactions, the Company may rely on information furnished by or on behalf of customers and counterparties, including financial statements, credit reports and other financial information. The Company may also rely on representations of those customers, counterparties or other third parties, such as independent auditors, as to the accuracy and completeness of that information. Reliance on inaccurate or misleading financial statements, credit reports or other financial information could have a material adverse impact on the Company’s business and, in turn, the Company’s financial condition and results of operations.

Consumers may decide not to use banks to complete their financial transactions.

Technology and other changes are allowing parties to complete financial transactions that historically have involved banks through alternative methods. For example, consumers can now maintain funds that would have historically been held as bank deposits in brokerage accounts or mutual funds. Consumers can also complete transactions such as paying bills and/or transferring funds directly without the assistance of banks. The process of eliminating banks as intermediaries, known as “disintermediation,” could result in the loss of fee income, as well as the loss of customer deposits and the related income generated from those deposits. The loss of these revenue streams and the lower cost deposits as a source of funds could have a material adverse effect on the Company’s financial condition and results of operations.

A protracted government shutdown or issues relating to debt and the deficit may adversely affect the Company.

Extended shutdowns of parts of the federal government could negatively impact the financial performance of certain customers and could impact customers’ future access to certain loan and guarantee programs. As a result, this could impact the Company’s business, financial condition and results of operations.

As a result of past difficulties of the federal government to reach agreement over federal debt and issues connected with the debt ceiling, certain rating agencies placed the United States government's long-term sovereign debt rating on their equivalent of negative watch and announced the possibility of a rating downgrade. The rating agencies, due to constraints related to the rating of the United States, also placed government-sponsored enterprises in which the Company invests and receives lines of credit on negative watch and a downgrade of the United States government's credit rating would trigger a similar downgrade in the credit rating of these government-sponsored enterprises. Furthermore, the credit rating of other entities, such as state and local governments, may also be downgraded should the United States government's credit rating be downgraded. The impact that a credit rating downgrade may have on the national and local economy could have an adverse effect on the Company’s financial condition and results of operations.

The regulatory environment for the financial services is being significantly impacted by financial regulatory reform initiatives in the United States and elsewhere, including Dodd-Frank and regulations promulgated to implement it.

Dodd-Frank, which was signed into law on July 21, 2010, comprehensively reforms the regulation of financial institutions, products and services. Dodd-Frank requires various federal regulatory agencies to implement numerous rules and regulations. Because the federal agencies are granted broad discretion in drafting these rules and regulations, many of the details and the impact of Dodd-Frank may not be known for many months or years.

While much of how the Dodd-Frank and other financial industry reforms will change our current business operations depends on the specific regulatory reforms and interpretations, many of which have yet to be released or finalized, it is clear that the reforms, both under Dodd-Frank and otherwise, will have a significant effect on our entire industry. Although Dodd-Frank and other reforms will affect a number of the areas in which we do business, it is not clear at this time the full extent of the adjustments that will be required and the extent to which we will be able to adjust our businesses in response to the requirements. Although it is difficult to predict the magnitude and extent of these effects at this stage, we believe compliance with Dodd-Frank and implementing its regulations and initiatives will negatively impact revenue and increase the cost of

doing business, both in terms of transition expenses and on an ongoing basis, and it may also limit our ability to pursue certain business opportunities.

Risks related to the merger of Landmark Bancorp, Inc. (Landmark) into the Company

The combined company will incur significant transaction and merger-related costs in connection with the merger.

The Company expects to incur costs associated with combining the operations of the two companies. The Company is formulating detailed integration plans to deliver planned synergies. Additional unanticipated costs may be incurred in the integration of the businesses of the Company and Landmark. Whether or not the merger is consummated, the Company will incur substantial expenses, such as legal, accounting, printing, contract termination fees, and financial advisory fees, in pursuing the merger. Although the Company expects that the elimination of duplicative costs, as well as the realization of other efficiencies related to the integration of the businesses, may offset incremental transaction and merger-related costs over time, the net benefit may not be achieved in the near term, or at all.

Some of the conditions to closing of the merger may result in delay or prevent completion of the merger, which may adversely affect the value of the Company’s and Landmark’s securities.

Completion of the merger is conditioned upon the receipt of certain governmental consents and approvals, including consents and approvals required by the Federal Reserve Board, the FDIC, and the Pennsylvania Department of Banking and Securities. Failure to obtain these consents would prevent consummation of the merger. Even if the approvals are obtained, the effort involved may delay consummation of the merger. Governmental authorities may also impose conditions in connection with the merger that may adversely affect the combined company’s operations after the merger. However, the Company is not required to take any action or agree to any condition or restriction in connection with obtaining any approvals that would reasonably be expected to have a material adverse effect on the Company or the combined company.

The merger may distract the Company’s management team from its other responsibilities.

The merger could cause the management of the Company to focus their time and energies on matters related to the merger that otherwise would be directed to its business and operations. Any such distraction on the part of management, if significant, could affect management’s ability to service existing business and develop new business and adversely affect the combined company’s business and earnings following the merger.

Post-merger integration and operations may fail to achieve expected results.

The success of the transaction depends heavily on a smooth post-merger integration and operations of the combined bank. Benefits of the transaction to shareholders may not be realized if the post-merger integration and operations are not well executed or well received by each bank’s historical customers.

The Company may fail to realize the cost savings it expects to achieve from the merger.

The success of the merger will depend, in part, on the Company’s ability to realize the estimated cost savings from combining the businesses of the Company and Landmark. While the Company believes that the cost savings estimates are achievable, it is possible that the potential cost savings could be more difficult to achieve than the Company anticipates. The Company’s cost savings estimates also depend on its ability to combine the businesses of the Company and Landmark in a manner that permits those cost savings to be realized. If the Company’s estimates are incorrect or it is unable to combine the two companies successfully, the anticipated cost savings may not be realized fully or at all or may take longer to realize than expected.

Combining the Company and Landmark may be more difficult, costly, or time-consuming than expected.

The Company and Landmark have operated, and, until the completion of the merger, will continue to operate, independently. Following the completion of the merger, the combination process could result in the loss of key employees, the disruption of the Company’s ongoing business, and inconsistencies in standards, controls, procedures and policies that adversely affect the Company’s ability to maintain relationships with clients and employees or achieve the anticipated benefits of the merger. As with any merger of financial institutions, there also may be disruptions that cause the Company to lose customers or cause customers to withdraw their deposits from the Company, or other unintended consequences that could have a material adverse effect on the Company’s results of operations or financial condition.

Risks related to the COVID-19 pandemic

The COVID-19 Pandemic Has Adversely Impacted Our Business And Financial Results, And The Ultimate Impact Will Depend On Future Developments, Which Are Highly Uncertain And Cannot Be Predicted, Including The Scope And Duration Of The Pandemic And Actions Taken By Governmental Authorities In Response To The Pandemic.

The COVID-19 pandemic has negatively impacted the global, national and local economies, disrupted global and national supply chains, lowered equity market valuations, created significant volatility and disruption in financial markets, and increased unemployment levels. In addition, the pandemic resulted in temporary closures of many businesses and the institution of social distancing and sheltering in place requirements in many states and communities and may result in the same or similar restrictions in the future. As a result, the demand for our products and services have been and may continue to be significantly impacted, which could adversely affect our revenue and results of operations. Furthermore, the pandemic could continue to result in the recognition of credit losses in our loan portfolios and increases in our allowance for credit losses, particularly if businesses remain required to operate at diminished capacities or are required to close again, the impact on the global, national and local economies worsen, or more customers draw on their lines of credit or seek additional loans to help finance their businesses. Similarly, because of changing economic and market conditions affecting issuers, we may be required to recognize further impairments on the securities we hold as well as reductions in other comprehensive income. Our business operations may also be disrupted if significant portions of our workforce are unable to work effectively, including because of illness, quarantines, government actions, or other restrictions in connection with the pandemic. The extent to which the COVID-19 pandemic impacts our business, results of operations, and financial condition, as well as our regulatory capital and liquidity ratios, will depend on future developments, which are highly uncertain and cannot be predicted, including the scope and duration of the pandemic and actions taken by governmental authorities and other third parties in response to the pandemic.