UNITED STATES | |

SECURITIES AND EXCHANGE COMMISSION | |

WASHINGTON, D.C. 20549 | |

FORM 10-K | |

FOR ANNUAL AND TRANSACTION REPORTS PURSUANT TO SECTIONS 13 OR 15(d) OF THE | |

SECURITIES EXCHANGE ACT OF 1934 | |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007 | |

OR | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to __________ | |

Commission File Number 1-10258 | |

TREDEGAR CORPORATION |

(Exact name of registrant as specified in its charter) |

Virginia | 54-1497771 |

(State or other jurisdiction | (I.R.S. Employer |

1100 Boulders Parkway, Richmond, Virginia | 23225 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 804-330-1000 | |

Securities registered pursuant to Section 12(b) of the Act: | |

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock | New York Stock Exchange | |

Preferred Stock Purchase Rights | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for at least the past 90 days.Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant'sregistrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a non-accelerated filer.smaller reporting company. See definitionthe definitions of “large accelerated filer,” “accelerated filerfiler” and large accelerated filer”“smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer x | ||

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 20062007 (the last business day of the registrant’s most recently completed second quarter): $479,651,105*

Number of shares of Common Stock outstanding as of January 31, 2007: 39,382,964 (38,790,2972008: 34,698,950 (39,595,524 as of June 30, 2006)

* In determining this figure, an aggregate of 8,471,0118,269,963 shares of Common Stock beneficially owned by Floyd D. Gottwald, Jr., John D. Gottwald, William M. Gottwald and the members of their immediate families has been excluded because the shares are held by affiliates. The aggregate market value has been computed based on the closing price in the New York Stock Exchange Composite Transactions on June 30, 2006,29, 2007, as reported by The Wall Street Journal.

Documents Incorporated By Reference |

Portions of the Tredegar Corporation Proxy Statement for the 2008 Annual Meeting of Shareholders (the “Proxy Statement”) are incorporated by reference into Part III of this Form 10-K. We expect to file our Proxy Statement with the Securities and Exchange Commission (the “SEC”) and mail it to shareholders on or about April 4, 2008. |

Documents Incorporated By Reference

Page | ||||

1-3 | ||||

4-6 | ||||

None | ||||

6 | ||||

None | ||||

None | ||||

7-10 | ||||

10-16 | ||||

17-34 | ||||

35 | ||||

39-73 | ||||

None | ||||

35-36 | ||||

None | ||||

36-37 | ||||

* | ||||

38 | ||||

38 | ||||

* | ||||

39 | ||||

*

Items 11 and 14 and portions of Items 10, 12 and 13 are incorporated by reference from the Proxy Statement.The Securities and Exchange Commission (the “SEC”)SEC has not approved or disapproved of this report or passed upon its accuracy or adequacy.

Item 1. | BUSINESS |

Description of Business

Tredegar Corporation (“Tredegar”), a Virginia corporation incorporated in 1988, is engaged, through its subsidiaries, in the manufacture of plastic films and aluminum extrusions. FinancialThe financial information related to Tredegar’s films and continuing aluminum segments included in Note 3 to the notes to financial statements is incorporated herein by reference.

Film Products

Tredegar Film Products Corporation and its subsidiaries (together, “Film Products”) manufacture plastic films, elastics and laminate materials primarily for personal and household care products and packaging and surface protection applications. These products are produced at locations in the United States and at plants in The Netherlands, Hungary, Italy, China and Brazil. Film Products competes in all of its markets on the basis of product innovation, quality, price and service.

Personal and Household Care Materials. Film Products is one of the largest global suppliers of apertured, breathable, elastic and embossed films, and laminate materials for personal care markets, including:

• | Apertured film and nonwoven materials for use as topsheet in feminine hygiene products, baby diapers and adult incontinent products (including materials sold under the ComfortQuilt®and ComfortAireTMbrand names); |

• | Breathable, embossed and elastic materials for use as components for baby diapers, adult incontinent products and feminine hygiene products (including elastic components sold under the FabriflexTM, StretchTabTMand FlexAireTMbrand names); and |

• | Absorbent transfer layers for baby diapers and adult incontinent products sold under the AquiDryTM and AquiSoftTM brand names. |

In each of the last three years, personal care products accounted for more than 30%approximately 40% of Tredegar’s consolidated net sales.

Film Products also makes apertured films, breathable barrier films and laminates that regulate vaporfluid or fluidvapor transmission. These products are typically used in industrial, medical, agricultural and household markets, including disposable mops, facial wipes, filter layers for personal protective suits, facial masks and landscaping fabric. Film Products supplies a family of laminates for use in protective apparel under the GuardDog Laminates

TM brand name.

Film Products also produces films that are disposable, protective coversheets for photopolymers used in the manufacture of circuit boards. Othersingle and multi-layer surface protection films sold under the UltraMask® and ForceFieldTM brand namesnames. These films are used as protective films to protectin high technology applications, including protecting components of flat panel display componentsdisplays and LCD televisions during fabrication, shipping and handling.the manufacturing process.

Raw Materials. The primary raw materials used by Film Products are low density, linear low density and high density polyethylene and polypropylene resins, which are obtained from domestic and foreign suppliers at competitive prices. We believe there will be an adequate supply of polyethylene and polypropylene resins in the immediate future. Film Products also buys polypropylene-based nonwoven fabrics based on these same resins, and we believe there will be an adequate supply of these materials in the immediate future.

P&G and Tredegar have had a successful long-term relationship based on cooperation, product innovation and continuous process improvement. The loss or significant reduction in sales associated with P&G would have a material adverse effect on our business.

Research and Development and Intellectual Property. Film Products has technical centers in Richmond, Virginia; Terre Haute, Indiana; Chieti, Italy; and Shanghai, China; and holds 189200 issued patents (73(76 of which are issued in the U.S.) and 110116 trademarks (10(15 of which are issued in the U.S.). Expenditures for research and development (“R&D”) have averaged $7.4$7.7 million annually over the past three years.

Aluminum Extrusions

The William L. Bonnell Company, Inc. and its subsidiaries (together, "Aluminum Extrusions"“Aluminum Extrusions”) produce soft-alloy aluminum extrusions primarily for building and construction, distribution, transportation, machinery and equipment, electrical and consumer durables markets.

Aluminum Extrusions manufactures mill (unfinished), anodized (coated) and painted aluminum extrusions for sale directly to fabricators and distributors that use our extrusions to produce window components, curtain walls and storefronts, tub and shower doors, industrial and agricultural machinery and equipment, ladders, bus bars, automotive parts, snowmobiles and tractor-trailer shapes, among other products. Sales are made primarily in the United States, and Canada, principally east of the Rocky Mountains. Aluminum Extrusions competes primarily on the basis of product quality, service and price.

Aluminum Extrusions sales volume from continuing operations by market segment over the last three years is shown below:

| by Market Segment | ||||||||||

2006 | 2005 | 2004 | ||||||||

| Building and construction: | ||||||||||

| Commercial | 48 | 44 | 41 | |||||||

| Residential | 14 | 18 | 21 | |||||||

| Distribution | 19 | 16 | 13 | |||||||

| Transportation | 9 | 9 | 10 | |||||||

| Machinery and equipment | 5 | 6 | 7 | |||||||

| Electrical | 3 | 4 | 5 | |||||||

| Consumer durables | 2 | 3 | 3 | |||||||

| Total | 100 | 100 | 100 | |||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

% of Aluminum Extrusions Sales Volume |

| |||||||||

| ||||||||||

|

| 2007 |

| 2006 |

| 2005 |

| |||

|

|

|

|

| ||||||

Building and construction: |

|

|

|

|

|

|

|

|

|

|

Commercial |

|

| 65 |

|

| 55 |

|

| 51 |

|

Residential |

|

| 17 |

|

| 19 |

|

| 25 |

|

Distribution |

|

| 9 |

|

| 18 |

|

| 16 |

|

Transportation |

|

| 4 |

|

| 3 |

|

| 4 |

|

Machinery and equipment |

|

| 2 |

|

| 2 |

|

| 2 |

|

Electrical |

|

| 2 |

|

| 2 |

|

| 1 |

|

Consumer durables |

|

| 1 |

|

| 1 |

|

| 1 |

|

Total |

|

| 100 |

|

| 100 |

|

| 100 |

|

Raw Materials. The primary raw materials used by Aluminum Extrusions consist of aluminum ingot, aluminum scrap and various alloys, which are purchased from domestic and foreign producers in open-market purchases and under short-term contracts. We believe there will be an adequate supply of aluminum and other required raw materials and supplies in the immediate future.

Intellectual Property. Aluminum Extrusions holds twoone U.S. patentspatent and two U.S. trademarks.

Patents, Licenses and Trademarks. Tredegar considers patents, licenses and trademarks to be of significance for Film Products. We routinely apply for patents on significant developments in this business. Our patents have remaining terms ranging from 1 to 19 years. We also have licenses under patents owned by third parties.

Research and Development. Tredegar’s spending for R&D activities in 2007, 2006 2005 and 20042005 was related to Film Products and AFBS, Inc. (formerly known as Therics, Inc.). R&D spending at Film Products was approximately $8.4 million in 2007, $8.1 million in 2006 and $6.6 million in 2005 and $7.5 million in 2004.2005.

On June 30, 2005, substantially all of the assets of AFBS, a wholly-owned subsidiary of Tredegar, were sold or assigned to a newly-created limited liability company, Therics, LLC, controlled and managed by an individual not affiliated with Tredegar. AFBS received a 17.5% equity interest in Therics, LLC, then valued at $170,000 and a 3.5% interest in Theken Spine, LLC, then valued at $800,000, along with potential future payments based on the sale of certain products by Therics, LLC. AFBS had operating losses of $3.5 million during the first six months of 2005 and $9.8 million in 2004.2005. There was no R&D spending at AFBS in 2007 and 2006. R&D spending at AFBS was approximately $2.4 million in 2005 and $7.8 million in 2004.

Backlog. Backlogs are not material to our operations.operations in Film Products. Overall backlog for continuing operations in Aluminum Extrusions at December 31, 2007 was down by approximately 7% compared with December 31, 2006. The demand for extruded aluminum shapes is down significantly in most market segments, which we believe is cyclical in nature. Aluminum extrusion volume from continuing operations decreased to 155.8 million pounds in 2007, down 15.9% from 185.2 million pounds in 2006. Shipments declined in most markets, especially extrusions used in hurricane protection products and residential construction. In addition, we began experiencing a softening of markets for extrusions used in non-residential construction in the fourth quarter of 2007.

Government Regulation. Laws concerning the environment that affect or could affect our domestic operations include, among others, the Clean Water Act, the Clean Air Act, the Resource Conservation Recovery Act, the Occupational Safety and Health Act, the National Environmental Policy Act, the Toxic Substances Control Act, the Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA"(“CERCLA”), as amended, regulations promulgated under these acts, and any other federal, state or local laws or regulations governing environmental matters. WeAt December 31, 2007, we believe that we arewere in substantial compliance with all applicable laws, regulations and permits. In order to maintain substantial compliance with such standards, we may be required to incur expenditures, the amounts and timing of which are not presently determinable but which could be significant, in constructing new facilities or in modifying existing facilities.

Employees. Tredegar employed approximately 3,0002,600 people in continuing operations at December 31, 2006.2007.

Available Information and Corporate Governance Documents.Our Internet address is www.tredegar.com. We make available, free of charge through our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the SEC. Information filed electronically with the SEC can be accessed on its website at www.sec.gov. In addition, our Corporate Governance Guidelines, Code of Conduct and the charters of our Audit, Executive Compensation and Nominating and Governance Committees are available on our website and are available in print, without charge, to any shareholder upon request by contacting Tredegar’s Corporate Secretary at 1100 Boulders Parkway, Richmond, Virginia 23225. The information on or that can be accessed through our website is not, and shall not be deemed to be, a part of this report or incorporated into other filings we make with the SEC.

RISK FACTORS |

There are a number of risks and uncertainties that can have a material effect on the operating results of our businesses and our financial condition. These risk factors include, but are not limited to, the following:

General

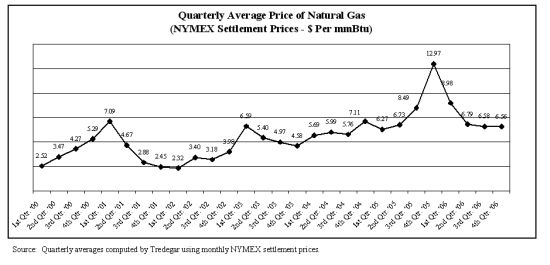

• | Our future performance is influenced by costs incurred by our operating companies including, for example, the cost of energy and raw materials.These costs include, without limitation, the cost of resin (the raw material on which Film Products primarily depends), aluminum (the raw material on which Aluminum Extrusions primarily depends), natural gas (the principal fuel necessary for Aluminum Extrusions’ plants to operate), electricity and diesel fuel. Resin, aluminum and natural gas prices are volatile, and the prices for resin and aluminum have |

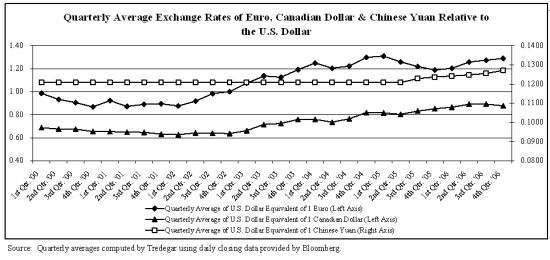

• | Our substantial international operations subject us to risks of doing business in foreign countries, which could adversely affect our business, financial condition and results of operations. Risks inherent in international operations include the following, by way of example: changes in general economic conditions, potential difficulty enforcing agreements and intellectual property rights, staffing and managing widespread operations, restrictions on foreign trade or investment, restrictions on the repatriation of income, fluctuations in exchange rates, imposition of additional taxes on our foreign income, nationalization of private enterprises and unexpected adverse changes in foreign laws and regulatory requirements. |

• | Non-compliance with any of the covenants in our $300 million credit facility could result in all outstanding debt under the agreement becoming due, which could have an adverse effect on our financial condition |

• | Our investments (primarily $10 million investment in Harbinger and $6.5 million investment in a drug delivery company) have high risk. Harbinger Capital Partners Special Situations Fund, L.P. (“Harbinger”) is a fund that seeks to achieve superior absolute returns by participating primarily in medium to long-term investments involving distressed/high yield debt securities, special situation equities and private loans and notes. The fund is a highly speculative investment subject to a two-year lock-up and additional limitations on withdrawal. The drug delivery company may need several more rounds of financing to have the opportunity to complete product development and bring its technology to market, which may never occur. There is no secondary market for selling our interests in Harbinger or the drug delivery company. |

Film Products | |

• | Film Products is highly dependent on sales associated with one customer, P |

• | Growth of Film Products depends on our ability to develop and deliver new products at competitive prices, especially in the personal care |

• | Continued growth in Film |

• | Our inability to protect our intellectual property rights or our infringement of the intellectual property rights of others could have a significant adverse impact on Film Products. Film Products operates in a field where our significant customers and competitors have substantial intellectual property portfolios. The continued success of this business depends on our ability not only to protect our own technologies and trade secrets, but also to develop and sell new products that do not infringe upon existing patents or threaten existing customer relationships. An unfavorable outcome in any intellectual property litigation or similar proceeding could have a |

• | As Film Products expands its personal care business, we have greater credit risk that is inherent in broadening our customer base. |

Aluminum Extrusions | |

• | Sales volume and profitability of Aluminum Extrusions is cyclical and highly dependent on economic conditions of end-use markets in the United States, |

• | The markets for our products are highly competitive with product quality, service, delivery performance and price being the principal competitive factors. Aluminum Extrusions has |

During improving economic conditions, excess industry capacity is absorbed and pricing pressure becomes less of a factor in many of our end-use markets. Conversely, during an economic slowdown, excess industry capacity often drives increased pricing pressure in many end-use markets as competitors protect their position with key customers. Because the business is susceptible to these changing economic conditions, Aluminum Extrusions targets complex, customized, service-intensive business with more challenging requirements which is competitively more defensible compared to higher volume, standard extrusion applications. |

Foreign imports, primarily from China, represent a |

There can be no assurance that we will be able to maintain current margins and profitability. Our continued success and prospects depend on our ability to retain existing customers and participate in overall industry cross-cycle growth. |

UNRESOLVED STAFF COMMENTS | |

None. | |

PROPERTIES | |

General |

Most of the improved real property and the other assets used in our operations are owned, and none of the owned property is subject to an encumbrance that is material to our consolidated operations. We consider the plants, warehouses and other properties and assets owned or leased by us to be in generally good condition.

We believe that the capacity of our plants is adequate to meet our immediate needs. Our plants generally have operated at 50-95% of capacity. Our corporate headquarters, which is leased, is located at 1100 Boulders Parkway, Richmond, Virginia 23225.

Our principal plants and facilities are listed below:

Film Products

Locations in the United States | Locations in Foreign Countries | Principal Operations | ||

Lake Zurich, Illinois | Chieti, Italy (technical center) | Production of plastic films and | ||

Pottsville, Pennsylvania | Guangzhou, China | laminate materials | ||

Red Springs, North Carolina | Kerkrade, The Netherlands | |||

(leased) | Rétság, Hungary | |||

Richmond, Virginia (technical | Roccamontepiano, Italy | |||

center) (leased) | São Paulo, Brazil | |||

Terre Haute, Indiana | Shanghai, China | |||

(technical center and | ||||

production facility) |

Aluminum Extrusions

Locations in the United States | Locations in Canada | Principal Operations | ||

Carthage, Tennessee | All locations in Canada were part | Production of aluminum extrusions, | ||

Kentland, Indiana | of the sale on February 12, 2008, | fabrication and finishing | ||

Newnan, Georgia | of the aluminum extrusions | |||

business in Canada (see Note 17 to | ||||

the notes to financial statements | ||||

for more information) |

LEGAL PROCEEDINGS | |

None. |

SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS | |

None. |

MARKET FOR TREDEGAR’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Prices of Common Stock and Shareholder Data

Our common stock is traded on the New York Stock Exchange (“NYSE”) under the ticker symbol TG. We have no preferred stock outstanding. There were 39,286,07934,765,450 shares of common stock held by 3,4823,486 shareholders of record on December 31, 2006.

The following table shows the reported high and low closing prices of our common stock by quarter for the past two years.

2006 | 2005 | ||||||||||||

High | Low | High | Low | ||||||||||

| First quarter | $ | 16.65 | $ | 13.06 | $ | 20.19 | $ | 16.08 | |||||

| Second quarter | 16.89 | 13.84 | 17.56 | 14.52 | |||||||||

| Third quarter | 16.94 | 14.39 | 16.67 | 12.09 | |||||||||

| Fourth quarter | 23.32 | 16.31 | 13.16 | 11.76 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2007 |

| 2006 |

| ||||||||

|

|

|

| ||||||||||

|

| High |

| Low |

| High |

| Low |

| ||||

|

|

|

|

|

| ||||||||

First quarter |

| $ | 24.44 |

| $ | 21.18 |

| $ | 16.65 |

| $ | 13.06 |

|

Second quarter |

|

| 24.45 |

|

| 20.57 |

|

| 16.89 |

|

| 13.84 |

|

Third quarter |

|

| 22.43 |

|

| 16.25 |

|

| 16.94 |

|

| 14.39 |

|

Fourth quarter |

|

| 18.27 |

|

| 13.33 |

|

| 23.32 |

|

| 16.31 |

|

The closing price of our common stock on February 20, 200726, 2008 was $23.86.

Dividend Information

We have paid a dividend every quarter since becoming a public company in July 1989. During 2007, 2006 2005 and 2004,2005, our quarterly dividend was 4 cents per share.

All decisions with respect to the declaration and payment of dividends will be made by the Board of Directors in its sole discretion based upon earnings, financial condition, anticipated cash needs, restrictions in our credit agreement and such other considerations as the Board deems relevant. See Note 8 beginning on page 5958 for the restrictions contained in our credit agreement related to minimum shareholders’ equity required and aggregate dividends permitted.

Issuer Purchases of Equity Securities

During 2006 2005 and 2004,2005, we did not purchase any shares of our common stock in the open market. UnderDuring 2007, under a standing authorization from our board of directors announced on August 8, 2006, we may purchase up to 5purchased approximately 4.8 million shares of our stock at an average price of $16.00 per share. The table below summarizes share repurchase activity by month during 2007:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

| Period |

| Total |

| Average |

| Total |

| Maximum |

| ||||||

| ||||||||||||||||

| January - July 2007 |

| — |

|

|

| $ | — |

|

| — |

|

| — |

|

|

| August 2007 |

| 687,100 |

|

|

|

| 17.25 |

|

| 687,100 |

|

| 4,312,900 |

|

|

| September 2007 |

| 1,005,600 |

|

|

|

| 17.03 |

|

| 1,692,700 |

|

| 3,307,300 |

|

|

| October 2007 |

| 518,800 |

|

|

|

| 17.32 |

|

| 2,211,500 |

|

| 2,788,500 |

|

|

| November 2007 |

| 1,236,900 |

|

|

|

| 14.13 |

|

| 3,448,400 |

|

| 1,551,600 |

|

|

| December 2007 |

| 1,385,100 |

|

|

|

| 15.73 |

|

| 4,833,500 |

|

| 166,500 |

|

|

| ||||||||||||||||

* On August 8, 2006, our board of directors approved a share repurchase program authorizing management at its discretion to purchase, in the open market or in privately negotiated transactions, up to 5 million shares of our outstanding common stock.

On January 7, 2008, we announced that our board of directors approved a new share repurchase program whereby management is authorized at prices management deems appropriate.

Annual Meeting

Our annual meeting of shareholders will be held on May 17, 2007,8, 2008, beginning at 9:00 a.m. EDT at Lewis Ginter Botanical Garden, 1800 Lakeside Avenue, Richmond, Virginia, 23229.23228. We expect to mail formal notice of the annual meeting, proxies and proxy statements to shareholders on or about March 28, 2007.

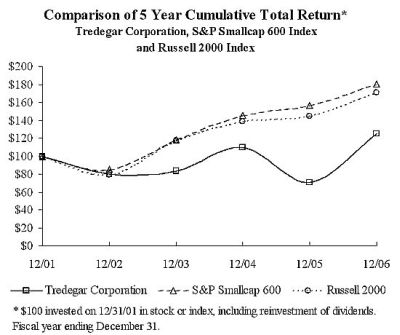

The following graph compares cumulative total shareholder returns for Tredegar, the S&P 600 Stock Index (an index comprised of companies with market capitalizations similar to Tredegar) and the Russell 2000 Index for the five years ended December 31, 2006.2007. Tredegar is part of both the S&P SmallCap 600 Index and Russell 2000 Index.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Tredegar Corporation, S&P Smallcap 600 Index

and Russell 2000 Index

* $100 invested on 12/31/02 in stock or index-including reinvestment of dividends. |

Fiscal year ending December 31. |

Inquiries

Inquiries concerning stock transfers, dividends, dividend reinvestment, consolidating accounts, changes of address, or lost or stolen stock certificates should be directed to:

National City Bank

All other inquiries should be directed to:

Tredegar Corporation

We do not generate or distribute quarterly reports to shareholders. Information on quarterly results can be obtained from our website. In addition, we file quarterly, annual and other information electronically with the SEC, which can be accessed on its website at

Legal Counsel | Independent Registered Public Accounting Firm | |

Hunton & Williams LLP | PricewaterhouseCoopers LLP | |

Richmond, Virginia | Richmond, Virginia | |

SELECTED FINANCIAL DATA |

The tables that follow on pages 10-1611-16 present certain selected financial and segment information for the eightfive years ended December 31, 2006.

EIGHT-YEAR SUMMARY | |||||||||||||||||||||||||

| Tredegar Corporation and Subsidiaries | |||||||||||||||||||||||||

| Years Ended December 31 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands, Except Per-Share Data) | |||||||||||||||||||||||||

Results of Operations (a): | |||||||||||||||||||||||||

| Sales | $ | 1,116,525 | $ | 956,969 | $ | 861,165 | $ | 738,651 | $ | 753,724 | $ | 779,157 | $ | 879,475 | $ | 828,015 | |||||||||

| Other income (expense), net | 1,444 | (b) | (544 | ) (c) | 15,604 | (d) | 7,853 | 546 | 1,255 | 1,914 | 972 | ||||||||||||||

1,117,969 | 956,425 | 876,769 | 746,504 | 754,270 | 780,412 | 881,389 | 828,987 | ||||||||||||||||||

| Cost of goods sold | 944,839 | (b) | 810,621 | (c) | 717,120 | (d) | 606,242 | 582,658 | 618,323 | 706,817 | 648,254 | ||||||||||||||

| Freight | 28,096 | 24,691 | 22,398 | 18,557 | 16,319 | 15,580 | 17,125 | 15,221 | |||||||||||||||||

| Selling, general & administrative expenses | 68,360 | (b) | 64,723 | (c) | 60,030 | (d) | 53,341 | 52,252 | 47,954 | 47,321 | 44,675 | ||||||||||||||

| Research and development expenses | 8,088 | 8,982 | 15,265 | 18,774 | 20,346 | 20,305 | 15,305 | 11,500 | |||||||||||||||||

| Amortization of intangibles | 149 | 299 | 330 | 268 | 100 | 4,914 | 5,025 | 3,430 | |||||||||||||||||

| Interest expense | 5,520 | 4,573 | 3,171 | 6,785 | 9,352 | 12,671 | 17,319 | 9,088 | |||||||||||||||||

| Asset impairments and costs associated with exit and disposal activities | 4,080 | (b) | 16,334 | (c) | 22,973 | (d) | 11,426 | (e) | 3,884 | (f) | 16,935 | (g) | 23,791 | (h) | 4,628 | (i) | |||||||||

| Unusual items | - | - | - | 1,067 | (e) | (6,147 | ) (f) | (971 | ) (g) | (762 | ) (h) | - | |||||||||||||

1,059,132 | 930,223 | 841,287 | 716,460 | 678,764 | 735,711 | 831,941 | 736,796 | ||||||||||||||||||

| Income from continuing operations before income taxes | 58,837 | 26,202 | 35,482 | 30,044 | 75,506 | 44,701 | 49,448 | 92,191 | |||||||||||||||||

| Income taxes | 20,636 | (b) | 9,973 | 9,222 | (d) | 10,717 | 26,881 | 13,950 | (g) | 18,135 | 32,728 | ||||||||||||||

| Income from continuing operations (a) | 38,201 | 16,229 | 26,260 | 19,327 | 48,625 | 30,751 | 31,313 | 59,463 | |||||||||||||||||

| Discontinued operations (a): | |||||||||||||||||||||||||

| Income (loss) from venture capital investment activities | - | - | 2,921 | (46,569 | ) | (42,428 | ) | (16,627 | ) | 83,640 | (4,626 | ) | |||||||||||||

| Income (loss) from operations of Molecumetics | - | - | - | 891 | (8,728 | ) | (5,768 | ) | (3,577 | ) | (2,189 | ) | |||||||||||||

| Income from discontinued energy segment | - | - | - | - | - | 1,396 | - | - | |||||||||||||||||

| Income (loss) from discontinued operations (a) | - | - | 2,921 | (45,678 | ) | (51,156 | ) | (20,999 | ) | 80,063 | (6,815 | ) | |||||||||||||

| Net income (loss) | $ | 38,201 | $ | 16,229 | $ | 29,181 | $ | (26,351 | ) | $ | (2,531 | ) | $ | 9,752 | $ | 111,376 | $ | 52,648 | |||||||

| Diluted earnings (loss) per share: | |||||||||||||||||||||||||

| Continuing operations (a) | $ | .98 | $ | .42 | $ | .68 | $ | .50 | $ | 1.25 | $ | .79 | $ | .80 | $ | 1.54 | |||||||||

| Discontinued operations (a) | - | - | .08 | (1.19 | ) | (1.32 | ) | (.54 | ) | 2.06 | (.18 | ) | |||||||||||||

| Net income (loss) | $ | .98 | $ | .42 | $ | .76 | $ | (.69 | ) | $ | (.07 | ) | $ | .25 | $ | 2.86 | $ | 1.36 | |||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

EIGHT-YEAR SUMMARY | |||||||||||||||||||||||||

| Tredegar Corporation and Subsidiaries | |||||||||||||||||||||||||

| Years Ended December 31 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands, Except Per-Share Data) | |||||||||||||||||||||||||

Share Data: | |||||||||||||||||||||||||

| Equity per share | $ | 13.15 | $ | 12.53 | $ | 12.45 | $ | 11.72 | $ | 12.08 | $ | 12.53 | $ | 13.07 | $ | 9.88 | |||||||||

| Cash dividends declared per share | .16 | .16 | .16 | .16 | .16 | .16 | .16 | .16 | |||||||||||||||||

| Weighted average common shares outstanding during the period | 38,671 | 38,471 | 38,295 | 38,096 | 38,268 | 38,061 | 37,885 | 36,992 | |||||||||||||||||

| Shares used to compute diluted earnings per share during the period | 38,931 | 38,597 | 38,507 | 38,441 | 38,869 | 38,824 | 38,908 | 38,739 | |||||||||||||||||

| Shares outstanding at end of period | 39,286 | 38,737 | 38,598 | 38,177 | 38,323 | 38,142 | 38,084 | 37,661 | |||||||||||||||||

| Closing market price per share: | |||||||||||||||||||||||||

| High | 23.32 | 20.19 | 20.25 | 16.76 | 24.72 | 21.70 | 32.00 | 32.94 | |||||||||||||||||

| Low | 13.06 | 11.76 | 13.00 | 10.60 | 12.25 | 15.30 | 15.00 | 16.06 | |||||||||||||||||

| End of year | 22.61 | 12.89 | 20.21 | 15.53 | 15.00 | 19.00 | 17.44 | 20.69 | |||||||||||||||||

| Total return to shareholders (j) | 76.6 | % | (35.4 | )% | 31.2 | % | 4.6 | % | (20.2 | )% | 9.9 | % | (14.9 | )% | (7.3 | )% | |||||||||

Financial Position: | |||||||||||||||||||||||||

| Total assets | 781,787 | 781,758 | 769,474 | 753,025 | 837,962 | 865,031 | 903,768 | 792,487 | |||||||||||||||||

| Cash and cash equivalents | 40,898 | 23,434 | 22,994 | 19,943 | 109,928 | 96,810 | 44,530 | 25,752 | |||||||||||||||||

| Income taxes recoverable from sale of venture capital portfolio | - | - | - | 55,000 | - | - | - | - | |||||||||||||||||

| Debt | 62,520 | 113,050 | 103,452 | 139,629 | 259,280 | 264,498 | 268,102 | 270,000 | |||||||||||||||||

| Shareholders' equity (net book value) | 516,595 | 485,362 | 480,442 | 447,399 | 462,932 | 477,899 | 497,728 | 372,228 | |||||||||||||||||

| Equity market capitalization (k) | 888,256 | 499,320 | 780,066 | 592,889 | 574,845 | 724,706 | 664,090 | 779,112 | |||||||||||||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

| Net Sales (1) | |||||||||||||||||||||||||

| Segment | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands) | |||||||||||||||||||||||||

| Film Products | $ | 511,169 | $ | 460,277 | $ | 413,257 | $ | 365,501 | $ | 376,904 | $ | 382,740 | $ | 380,202 | $ | 342,300 | |||||||||

| Aluminum Extrusions | 577,260 | 471,749 | 425,130 | 354,593 | 360,293 | 380,387 | 479,889 | 461,241 | |||||||||||||||||

| AFBS (formerly Therics) | - | 252 | 380 | - | 208 | 450 | 403 | 161 | |||||||||||||||||

| Total ongoing operations (m) | 1,088,429 | 932,278 | 838,767 | 720,094 | 737,405 | 763,577 | 860,494 | 803,702 | |||||||||||||||||

| Divested operations (a): | |||||||||||||||||||||||||

| Fiberlux | - | - | - | - | - | - | 1,856 | 9,092 | |||||||||||||||||

| Total net sales | 1,088,429 | 932,278 | 838,767 | 720,094 | 737,405 | 763,577 | 862,350 | 812,794 | |||||||||||||||||

| Add back freight | 28,096 | 24,691 | 22,398 | 18,557 | 16,319 | 15,580 | 17,125 | 15,221 | |||||||||||||||||

| Sales as shown in Consolidated Statements of Income | $ | 1,116,525 | $ | 956,969 | $ | 861,165 | $ | 738,651 | $ | 753,724 | $ | 779,157 | $ | 879,475 | $ | 828,015 | |||||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

Operating Profit | |||||||||||||||||||||||||

| Segment | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands) | |||||||||||||||||||||||||

| Film Products: | |||||||||||||||||||||||||

| Ongoing operations | $ | 57,645 | $ | 44,946 | $ | 43,259 | $ | 45,676 | $ | 72,307 | $ | 61,787 | $ | 47,112 | $ | 59,554 | |||||||||

| Plant shutdowns, asset impairments and restructurings, net of gains on sale of assets and related income from LIFO inventory liquidations | 221 | (b) | (3,955 | ) (c) | (10,438 | ) (d) | (5,746 | ) (e) | (3,397 | ) (f) | (9,136 | ) (g) | (22,163 | ) (h) | (1,170 | ) (i) | |||||||||

| Unusual items | - | - | - | - | 6,147 | (f) | - | - | - | ||||||||||||||||

| Aluminum Extrusions: | |||||||||||||||||||||||||

| Ongoing operations | 22,031 | 19,302 | 22,637 | 15,117 | 27,304 | 25,407 | 52,953 | 56,501 | |||||||||||||||||

| Plant shutdowns, asset impairments and restructurings, net of gains on sale of assets | (1,434 | ) (b) | 122 | (c) | (10,553 | ) (d) | (644 | ) (e) | (487 | ) (f) | (7,799 | ) (g) | (1,628 | ) (h) | - | ||||||||||

| Gain on sale of land | - | 1,385 | - | - | - | - | |||||||||||||||||||

| Other | - | - | 7,316 | (d) | - | - | - | - | - | ||||||||||||||||

| AFBS (formerly Therics): | |||||||||||||||||||||||||

| Ongoing operations | - | (3,467 | ) | (9,763 | ) | (11,651 | ) | (13,116 | ) | (12,861 | ) | (8,024 | ) | (5,235 | ) | ||||||||||

| Loss on investment in Therics, LLC | (25 | ) | (145 | ) | - | - | - | - | - | - | |||||||||||||||

| Plant shutdowns, asset impairments and restructurings | (637 | ) (b) | (10,318 | ) (c) | (2,041 | ) (d) | (3,855 | ) (e) | - | - | - | (3,458 | ) (i) | ||||||||||||

| Unusual items | - | - | - | (1,067 | ) (e) | - | - | - | - | ||||||||||||||||

| Divested operations (a): | |||||||||||||||||||||||||

| Fiberlux | - | - | - | - | - | - | (264 | ) | 57 | ||||||||||||||||

| Unusual items | - | - | - | - | - | - | 762 | (h) | - | ||||||||||||||||

| Total | 77,801 | 46,485 | 40,417 | 39,215 | 88,758 | 57,398 | 68,748 | 106,249 | |||||||||||||||||

| Interest income | 1,240 | 586 | 350 | 1,183 | 1,934 | 2,720 | 2,578 | 1,419 | |||||||||||||||||

| Interest expense | 5,520 | 4,573 | 3,171 | 6,785 | 9,352 | 12,671 | 17,319 | 9,088 | |||||||||||||||||

| Gain on sale of corporate assets | 56 | 61 | 7,560 | 5,155 | - | - | - | 712 | |||||||||||||||||

| Loss from write-down of investment in Novalux | - | (b) | 5,000 | (c) | - | - | - | - | - | - | |||||||||||||||

| Stock option-based compensation costs | 970 | - | - | - | - | - | - | - | |||||||||||||||||

| Corporate expenses, net | 13,770 | 11,357 | 9,674 | 8,724 | (e) | 5,834 | 2,746 | (g) | 4,559 | 7,101 | |||||||||||||||

| Income from continuing operations before income taxes | 58,837 | 26,202 | 35,482 | 30,044 | 75,506 | 44,701 | 49,448 | 92,191 | |||||||||||||||||

| Income taxes | 20,636 | (b) | 9,973 | 9,222 | 10,717 | 26,881 | 13,950 | (g) | 18,135 | 32,728 | |||||||||||||||

| Income from continuing operations | 38,201 | 16,229 | 26,260 | 19,327 | 48,625 | 30,751 | 31,313 | 59,463 | |||||||||||||||||

| Income (loss) from discontinued operations (a) | - | - | 2,921 | (45,678 | ) | (51,156 | ) | (20,999 | ) | 80,063 | (6,815 | ) | |||||||||||||

| Net income (loss) | $ | 38,201 | $ | 16,229 | $ | 29,181 | $ | (26,351 | ) | $ | (2,531 | ) | $ | 9,752 | $ | 111,376 | $ | 52,648 | |||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

| Identifiable Assets | |||||||||||||||||||||||||

| Segment | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands) | |||||||||||||||||||||||||

| Film Products | $ | 498,961 | $ | 479,286 | $ | 472,810 | $ | 422,321 | $ | 379,635 | $ | 367,291 | $ | 367,526 | $ | 360,517 | |||||||||

| Aluminum Extrusions | 209,395 | 214,374 | 210,894 | 185,336 | 176,631 | 185,927 | 210,434 | 216,258 | |||||||||||||||||

| AFBS (formerly Therics) | 2,420 | 2,759 | 8,613 | 8,917 | 10,643 | 9,931 | 9,609 | 9,905 | |||||||||||||||||

| Subtotal | 710,776 | 696,419 | 692,317 | 616,574 | 566,909 | 563,149 | 587,569 | 586,680 | |||||||||||||||||

| General corporate | 30,113 | 61,905 | 54,163 | 61,508 | 52,412 | 40,577 | 30,214 | 22,419 | |||||||||||||||||

| Income taxes recoverable from sale of venture capital investment portfolio | - | - | - | 55,000 | - | - | - | - | |||||||||||||||||

| Cash and cash equivalents | 40,898 | 23,434 | 22,994 | 19,943 | 109,928 | 96,810 | 44,530 | 25,752 | |||||||||||||||||

| Identifiable assets from ongoing operations | 781,787 | 781,758 | 769,474 | 753,025 | 729,249 | 700,536 | 662,313 | 634,851 | |||||||||||||||||

| Divested operations (a): | |||||||||||||||||||||||||

| Fiberlux | - | - | - | - | - | - | - | 7,859 | |||||||||||||||||

| Discontinued operations (a): | |||||||||||||||||||||||||

| Venture capital | - | - | - | - | 108,713 | 158,887 | 236,698 | 145,028 | |||||||||||||||||

| Molecumetics | - | - | - | - | - | 5,608 | 4,757 | 4,749 | |||||||||||||||||

| Total | $ | 781,787 | $ | 781,758 | $ | 769,474 | $ | 753,025 | $ | 837,962 | $ | 865,031 | $ | 903,768 | $ | 792,487 | |||||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

| Depreciation and Amortization | |||||||||||||||||||||||||

| Segment | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands) | |||||||||||||||||||||||||

| Film Products | $ | 31,847 | $ | 26,673 | $ | 21,967 | $ | 19,828 | $ | 20,085 | $ | 22,047 | $ | 23,122 | $ | 18,751 | |||||||||

| Aluminum Extrusions | 12,323 | 11,484 | 10,914 | 10,883 | 10,506 | 11,216 | 9,862 | 9,484 | |||||||||||||||||

| AFBS (formerly Therics) | - | 437 | 1,300 | 1,641 | 463 | 2,262 | 1,782 | 1,195 | |||||||||||||||||

| Subtotal | 44,170 | 38,594 | 34,181 | 32,352 | 31,054 | 35,525 | 34,766 | 29,430 | |||||||||||||||||

| General corporate | 111 | 195 | 241 | 270 | 353 | 329 | 315 | 253 | |||||||||||||||||

| Total ongoing operations | 44,281 | 38,789 | 34,422 | 32,622 | 31,407 | 35,854 | 35,081 | 29,683 | |||||||||||||||||

| Divested operations (a): | |||||||||||||||||||||||||

| Fiberlux | - | - | - | - | - | - | 151 | 498 | |||||||||||||||||

| Discontinued operations (a): | |||||||||||||||||||||||||

| Venture capital | - | - | - | - | - | - | 18 | 22 | |||||||||||||||||

| Molecumetics | - | - | - | - | 527 | 2,055 | 1,734 | 1,490 | |||||||||||||||||

| Total | $ | 44,281 | $ | 38,789 | $ | 34,422 | $ | 32,622 | $ | 31,934 | $ | 37,909 | $ | 36,984 | $ | 31,693 | |||||||||

Capital Expenditures, Acquisitions and Investments | |||||||||||||||||||||||||

| Segment | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | |||||||||||||||||

| (In Thousands) | |||||||||||||||||||||||||

| Film Products | $ | 33,168 | $ | 50,466 | $ | 44,797 | $ | 57,203 | $ | 24,063 | $ | 24,775 | $ | 53,161 | $ | 25,296 | |||||||||

| Aluminum Extrusions | 7,381 | 11,968 | 10,007 | 8,293 | 4,799 | 8,506 | 21,911 | 16,388 | |||||||||||||||||

| AFBS (formerly Therics) | - | 36 | 275 | 219 | 1,621 | 2,340 | 1,730 | 757 | |||||||||||||||||

| Subtotal | 40,549 | 62,470 | 55,079 | 65,715 | 30,483 | 35,621 | 76,802 | 42,441 | |||||||||||||||||

| General corporate | 24 | 73 | 572 | 93 | 60 | 519 | 384 | 606 | |||||||||||||||||

| Capital expenditures for ongoing operations | 40,573 | 62,543 | 55,651 | 65,808 | 30,543 | 36,140 | 77,186 | 43,047 | |||||||||||||||||

| Divested operations (a): | |||||||||||||||||||||||||

| Fiberlux | - | - | - | - | - | - | 425 | 812 | |||||||||||||||||

| Discontinued operations (a): | |||||||||||||||||||||||||

| Venture capital | - | - | - | - | - | - | 86 | - | |||||||||||||||||

| Molecumetics | - | - | - | - | 793 | 2,850 | 2,133 | 1,362 | |||||||||||||||||

| Total capital expenditures | 40,573 | 62,543 | 55,651 | 65,808 | 31,336 | 38,990 | 79,830 | 45,221 | |||||||||||||||||

| Acquisitions and other | - | - | 1,420 | 1,579 | - | 1,918 | 6,316 | 215,227 | |||||||||||||||||

| Novalux investment | 542 | 1,095 | 5,000 | - | - | - | - | - | |||||||||||||||||

| Venture capital investments | - | - | - | 2,807 | 20,373 | 24,504 | 93,058 | 81,747 | |||||||||||||||||

| Total | $ | 41,115 | $ | 63,638 | $ | 62,071 | $ | 70,194 | $ | 51,709 | $ | 65,412 | $ | 179,204 | $ | 342,195 | |||||||||

Refer to notes to financial tables on page 16. | |||||||||||||||||||||||||

FIVE-YEAR SUMMARY |

Tredegar Corporation and Subsidiaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Years Ended December 31 |

| 2007 |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| |||||

(In Thousands, Except |

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Results of Operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales |

| $ | 922,583 |

| $ | 937,561 |

| $ | 808,464 |

| $ | 709,649 |

| $ | 609,077 |

|

Other income (expense), net |

|

| 1,782 | (b) |

| 1,444 | (c) |

| (2,211 | ) (d) |

| 15,604 | (e) |

| 6,468 |

|

|

|

| 924,365 |

|

| 939,005 |

|

| 806,253 |

|

| 725,253 |

|

| 615,545 |

|

Cost of goods sold |

|

| 761,509 | (b) |

| 779,376 | (c) |

| 672,465 | (d) |

| 580,893 | (e) |

| 486,065 |

|

Freight |

|

| 19,808 |

|

| 22,602 |

|

| 20,276 |

|

| 18,027 |

|

| 14,330 |

|

Selling, general & administrative expenses |

|

| 68,501 |

|

| 64,082 |

|

| 61,007 | (d) |

| 57,221 | (e) |

| 50,793 |

|

Research and development expenses |

|

| 8,354 |

|

| 8,088 |

|

| 8,982 |

|

| 15,265 |

|

| 18,774 |

|

Amortization of intangibles |

|

| 149 |

|

| 149 |

|

| 299 |

|

| 330 |

|

| 268 |

|

Interest expense |

|

| 2,721 |

|

| 5,520 |

|

| 4,573 |

|

| 3,171 |

|

| 6,785 |

|

Asset impairments and costs associated with exit and disposal activities |

|

| 4,027 | (b) |

| 4,080 | (c) |

| 15,782 | (d) |

| 12,566 | (e) |

| 11,426 | (f) |

Unusual items |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 1,067 | (f) |

|

|

| 865,069 |

|

| 883,897 |

|

| 783,384 |

|

| 687,473 |

|

| 589,508 |

|

Income from continuing operations before income taxes |

|

| 59,296 |

|

| 55,108 |

|

| 22,869 |

|

| 37,780 |

|

| 26,037 |

|

Income taxes |

|

| 24,366 |

|

| 19,791 | (c) |

| 9,497 |

|

| 10,201 | (e) |

| 9,837 |

|

Income from continuing operations (a) |

|

| 34,930 |

|

| 35,317 |

|

| 13,372 |

|

| 27,579 |

|

| 16,200 |

|

Discontinued operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (loss) from aluminum extrusions business in Canada |

|

| (19,681 | ) |

| 2,884 |

|

| 2,857 |

|

| (1,319 | ) |

| 3,127 |

|

Income (loss) from venture capital investment activities |

|

| — |

|

| — |

|

| — |

|

| 2,921 |

|

| (46,569 | ) |

Income from operations of Molecumetics |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 891 |

|

Income (loss) from discontinued operations (a) |

|

| (19,681 | ) |

| 2,884 |

|

| 2,857 |

|

| 1,602 |

|

| (42,551 | ) |

Net income (loss) |

| $ | 15,249 |

| $ | 38,201 |

| $ | 16,229 |

| $ | 29,181 |

| $ | (26,351 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted earnings (loss) per share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Continuing operations (a) |

| $ | .90 |

| $ | .91 |

| $ | .35 |

| $ | .72 |

| $ | .42 |

|

Discontinued operations (a) |

|

| (.51 | ) |

| .07 |

|

| .07 |

|

| .04 |

|

| (1.11 | ) |

Net income (loss) |

| $ | .39 |

| $ | .98 |

| $ | .42 |

| $ | .76 |

| $ | (.69 | ) |

Refer to notes to financial tables on page 16.

FIVE-YEAR SUMMARY |

Tredegar Corporation and Subsidiaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Years Ended December 31 |

| 2007 |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| |||||

(In Thousands, Except Per-Share Data) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Share Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Equity per share |

| $ | 14.13 |

| $ | 13.15 |

| $ | 12.53 |

| $ | 12.45 |

| $ | 11.72 |

|

Cash dividends declared per share |

|

| .16 |

|

| .16 |

|

| .16 |

|

| .16 |

|

| .16 |

|

Weighted average common shares outstanding during the period |

|

| 38,532 |

|

| 38,671 |

|

| 38,471 |

|

| 38,295 |

|

| 38,096 |

|

Shares used to compute diluted earnings per share during the period |

|

| 38,688 |

|

| 38,931 |

|

| 38,597 |

|

| 38,507 |

|

| 38,441 |

|

Shares outstanding at end of period |

|

| 34,765 |

|

| 39,286 |

|

| 38,737 |

|

| 38,598 |

|

| 38,177 |

|

Closing market price per share: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High |

|

| 24.45 |

|

| 23.32 |

|

| 20.19 |

|

| 20.25 |

|

| 16.76 |

|

Low |

|

| 13.33 |

|

| 13.06 |

|

| 11.76 |

|

| 13.00 |

|

| 10.60 |

|

End of year |

|

| 16.08 |

|

| 22.61 |

|

| 12.89 |

|

| 20.21 |

|

| 15.53 |

|

Total return to shareholders (g) |

|

| (28.2 | ) % |

| 76.6 | % |

| (35.4 | ) % |

| 31.2 | % |

| 4.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial Position: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

| 784,478 |

|

| 781,787 |

|

| 781,758 |

|

| 769,474 |

|

| 753,025 |

|

Cash and cash equivalents |

|

| 48,217 |

|

| 40,898 |

|

| 23,434 |

|

| 22,994 |

|

| 19,943 |

|

Income taxes recoverable from sale of venture capital portfolio |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 55,000 |

|

Debt |

|

| 82,056 |

|

| 62,520 |

|

| 113,050 |

|

| 103,452 |

|

| 139,629 |

|

Shareholders’ equity (net book value) |

|

| 491,328 |

|

| 516,595 |

|

| 485,362 |

|

| 480,442 |

|

| 447,399 |

|

Equity market capitalization (h) |

|

| 559,021 |

|

| 888,256 |

|

| 499,320 |

|

| 780,066 |

|

| 592,889 |

|

Refer to notes to financial tables on page 16.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SEGMENT TABLES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tredegar Corporation and Subsidiaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Sales (i) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Segment |

| 2007 |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| |||||

(In Thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Film Products |

| $ | 530,972 |

| $ | 511,169 |

| $ | 460,277 |

| $ | 413,257 |

| $ | 365,501 |

|

Aluminum Extrusions |

|

| 371,803 |

|

| 403,790 |

|

| 327,659 |

|

| 277,985 |

|

| 229,246 |

|

AFBS (formerly Therics) |

|

| — |

|

| — |

|

| 252 |

|

| 380 |

|

| — |

|

Total net sales (j) |

|

| 902,775 |

|

| 914,959 |

|

| 788,188 |

|

| 691,622 |

|

| 594,747 |

|

Add back freight |

|

| 19,808 |

|

| 22,602 |

|

| 20,276 |

|

| 18,027 |

|

| 14,330 |

|

Sales as shown in Consolidated Statements of Income |

| $ | 922,583 |

| $ | 937,561 |

| $ | 808,464 |

| $ | 709,649 |

| $ | 609,077 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Identifiable Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Segment |

|

| 2007 |

|

| 2006 |

|

| 2005 |

|

| 2004 |

|

| 2003 |

|

(In Thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Film Products |

| $ | 488,035 |

| $ | 498,961 |

| $ | 479,286 |

| $ | 472,810 |

| $ | 422,321 |

|

Aluminum Extrusions |

|

| 115,223 |

|

| 128,967 |

|

| 130,448 |

|

| 126,425 |

|

| 105,753 |

|

AFBS (formerly Therics) |

|

| 2,866 |

|

| 2,420 |

|

| 2,759 |

|

| 8,613 |

|

| 8,917 |

|

Subtotal |

|

| 606,124 |

|

| 630,348 |

|

| 612,493 |

|

| 607,848 |

|

| 536,991 |

|

General corporate |

|

| 74,927 |

|

| 30,113 |

|

| 61,905 |

|

| 54,163 |

|

| 61,508 |

|

Income taxes recoverable from sale of venture capital investment portfolio |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 55,000 |

|

Cash and cash equivalents |

|

| 48,217 |

|

| 40,898 |

|

| 23,434 |

|

| 22,994 |

|

| 19,943 |

|

Identifiable assets from continuing operations |

|

| 729,268 |

|

| 701,359 |

|

| 697,832 |

|

| 685,005 |

|

| 673,442 |

|

Discontinued operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Aluminum extrusions business in Canada |

|

| 55,210 |

|

| 80,428 |

|

| 83,926 |

|

| 84,469 |

|

| 79,583 |

|

Total |

| $ | 784,478 |

| $ | 781,787 |

| $ | 781,758 |

| $ | 769,474 |

| $ | 753,025 |

|

| ||||||||||||||||

Refer to notes to financial tables on page 16. |

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SEGMENT TABLES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tredegar Corporation and Subsidiaries |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Profit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Segment |

| 2007 |

| 2006 |

| 2005 |

| 2004 |

| 2003 |

| |||||

(In Thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Film Products: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ongoing operations |

| $ | 59,423 |

| $ | 57,645 |

| $ | 44,946 |

| $ | 43,259 |

| $ | 45,676 |

|

Plant shutdowns, asset impairments and restructurings, net of gains on sale of assets and related income from LIFO inventory liquidations |

|

| (649 | ) (b) |

| 221 | (c) |

| (3,955 | ) (d) |

| (10,438 | ) (e) |

| (5,746 | ) (f) |

Aluminum Extrusions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ongoing operations |

|

| 16,516 |

|

| 18,302 |

|

| 17,084 |

|

| 14,526 |

|

| 12,495 |

|

Plant shutdowns, asset impairments and restructurings, net of gains on sale of assets |

|

| (634 | ) (b) |

| (1,434 | ) (c) |

| (993 | ) (d) |

| (146 | ) (e) |

| (644 | ) (f) |

Other |

|

| — |

|

| — |

|

| — |

|

| 7,316 | (e) |

| — |

|

AFBS (formerly Therics): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ongoing operations |

|

| — |

|

| — |

|

| (3,467 | ) |

| (9,763 | ) |

| (11,651 | ) |

Loss on investment in Therics, LLC |

|

| — |

|

| (25 | ) |

| (145 | ) |

| — |

|

| — |

|

Plant shutdowns, asset impairments and restructurings |

|

| (2,786 | ) (b) |

| (637 | ) (c) |

| (10,318 | ) (d) |

| (2,041 | ) (e) |

| (3,855 | ) (f) |

Unusual items |

|

| — |

|

| — |

|

| — |

|

| — |

|

| (1,067 | ) (f) |

Total |

|

| 71,870 |

|

| 74,072 |

|

| 43,152 |

|

| 42,713 |

|

| 35,208 |

|

Interest income |

|

| 1,212 |

|

| 1,240 |

|

| 586 |

|

| 350 |

|

| 1,183 |

|

Interest expense |

|

| 2,721 |

|

| 5,520 |

|

| 4,573 |

|

| 3,171 |

|

| 6,785 |

|

Gain on sale of corporate assets |

|

| 2,699 |

|

| 56 |

|

| 61 |

|

| 7,560 |

|

| 5,155 |

|

Loss from write-down of investment |

|

| 2,095 | (b) |

| — | (c) |

| 5,000 | (d) |

| — |

|

| — |

|

Stock option-based compensation costs |

|

| 978 |

|

| 970 |

|

| — |

|

| — |

|

| — |

|

Corporate expenses, net |

|

| 10,691 |

|

| 13,770 |

|

| 11,357 | (d) |

| 9,674 |

|

| 8,724 | (f) |

Income from continuing operations before income taxes |

|

| 59,296 |

|

| 55,108 |

|

| 22,869 |

|

| 37,778 |

|

| 26,037 |

|

Income taxes |

|

| 24,366 | (b) |

| 19,791 | (c) |

| 9,497 |

|

| 10,200 |

|

| 9,837 |

|

Income from continuing operations |

|

| 34,930 |

|

| 35,317 |

|

| 13,372 |

|

| 27,578 |

|

| 16,200 |

|

Income (loss) from discontinued operations (a) |

|

| (19,681 | ) |

| 2,884 |

|

| 2,857 |

|

| 1,603 |

|

| (42,551 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

| $ | 15,249 |

| $ | 38,201 |

| $ | 16,229 |

| $ | 29,181 |

| $ | (26,351 | ) |

| ||||||||||||||||

Refer to notes to financial tables on page 16. |

|

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SEGMENT TABLES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tredegar Corporation and Subsidiaries |

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Depreciation and Amortization |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Segment |

|

| 2007 |

|

| 2006 |

|

| 2005 |

|

| 2004 |

|

| 2003 |

|

(In Thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Film Products |

| $ | 34,092 |

| $ | 31,847 |

| $ | 26,673 |

| $ | 21,967 |

| $ | 19,828 |

|

Aluminum Extrusions |

|

| 8,472 |

|

| 8,378 |

|

| 7,996 |

|

| 7,474 |

|

| 7,502 |

|

AFBS (formerly Therics) |

|

| — |

|

| — |

|

| 437 |

|

| 1,300 |

|

| 1,641 |

|

Subtotal |

|

| 42,564 |

|

| 40,225 |

|

| 35,106 |

|

| 30,741 |

|

| 28,971 |

|

General corporate |

|

| 91 |

|

| 111 |

|

| 195 |

|

| 241 |

|

| 270 |

|

Total continuing operations |

|

| 42,655 |

|

| 40,336 |

|

| 35,301 |

|

| 30,982 |

|

| 29,241 |

|

Discontinued operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Aluminum extrusions business in Canada |

|

| 3,386 |

|

| 3,945 |

|

| 3,488 |

|

| 3,440 |

|

| 3,381 |

|

Total |

| $ | 46,041 |

| $ | 44,281 |

| $ | 38,789 |

| $ | 34,422 |

| $ | 32,622 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Capital Expenditures, Acquisitions and Investments |

|

|

|

|

|

|

|

|

|

|

|

| ||||

| ||||||||||||||||

Segment |

|

| 2007 |

|

| 2006 |

|

| 2005 |

|

| 2004 |

|

| 2003 |

|

(In Thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Film Products |

| $ | 15,304 |

| $ | 33,168 |

| $ | 50,466 |

| $ | 44,797 |

| $ | 57,203 |

|

Aluminum Extrusions |

|

| 4,391 |

|

| 6,609 |

|

| 5,750 |

|

| 7,263 |

|

| 7,656 |

|

AFBS (formerly Therics) |

|

| — |

|

| — |

|

| 36 |

|

| 275 |

|

| 219 |

|

Subtotal |

|

| 19,695 |

|

| 39,777 |

|

| 56,252 |

|

| 52,335 |

|

| 65,078 |

|

General corporate |

|

| 6 |

|

| 24 |

|

| 73 |

|

| 572 |

|

| 93 |

|

Capital expenditures for continuing operations |

|

| 19,701 |

|

| 39,801 |

|

| 56,325 |

|

| 52,907 |

|

| 65,171 |

|

Discontinued operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Aluminum extrusions business in Canada |

|

| 942 |

|

| 772 |

|

| 6,218 |

|

| 2,744 |

|

| 637 |

|

Total capital expenditures |

|

| 20,643 |

|

| 40,573 |

|

| 62,543 |

|

| 55,651 |

|

| 65,808 |

|

Acquisitions and other |

|

| — |

|

| — |

|

| — |

|

| 1,420 |

|

| 1,579 |

|

Investments |

|

| 23,513 |

|

| 542 |

|

| 1,095 |

|

| 5,000 |

|

| — |

|

Venture capital investments |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 2,807 |

|

Total |

| $ | 44,156 |

| $ | 41,115 |

| $ | 63,638 |

| $ | 62,071 |

| $ | 70,194 |

|

| ||||||||||||||||

Refer to notes to financial tables on page 16. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NOTES TO FINANCIAL TABLES |

(In Thousands, Except Per-Share Data) |

(a) | On February 12, 2008, we sold our aluminum extrusions business in Canada. All historical results for this business have been reflected as discontinued operations. In 2007, discontinued operations also includes $11,428 in cash income tax benefits from the sale that we expect to realize in 2008. In 2004, discontinued operations include a gain of $2,921 after-taxes primarily related to the reversal of a business and occupancy tax contingency accrual upon favorable resolution. The accrual was originally recorded in connection with our venture capital investment operation. In 2003, we sold substantially all of our venture capital investment portfolio. |

(b) | Plant shutdowns, asset impairments and restructurings for 2007 include a charge of $2,786 related to the estimated loss on the |

(c) | Plant shutdowns, asset impairments and restructurings for 2006 include a net gain of $1,454 associated with the shutdown of the films manufacturing facility in LaGrange, Georgia, including a gain of $2,889 for related LIFO inventory liquidations (included in |

(d) | Plant shutdowns, asset impairments and restructurings for 2005 include charges of $10,318 related to the sale or assignment of substantially all of |

(e) | Plant shutdowns, asset impairments and restructurings for 2004 include |

(f) | Plant shutdowns, asset impairments and restructurings for 2003 include charges of $4,514 for severance costs in connection with restructurings in Film Products ($1,922), Aluminum Extrusions ($256), AFBS ($1,155) and corporate headquarters ($1,181, included in |

(g) |

Total return to shareholders is defined as the change in stock price during the year plus dividends per share, divided by the stock price at the beginning of the year. |

(h) | Equity market capitalization is the closing market price per share for the period multiplied by the shares outstanding at the end of the period. |

(i) | Net sales represent gross sales less freight. Net sales is the measure used by the chief operating decision maker of each segment for purposes of assessing performance. |

(j) | Net sales include sales to P&G totaling $258,602 in 2007, $255,414 in 2006 and $236,554 in |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Forward-looking and Cautionary Statements

From time to time, we may make statements that may constitute “forward-looking statements” within the meaning of the “safe-harbor” provisions of the Private Securities Litigation Reform Act of 1995. These statements are based on our then current expectations and are subject to a number of risks and uncertainties that could cause actual results to differ materially from those addressed in the forward-looking statements. Some of the risk factors that may cause such a difference are summarized on pages 3-54-6 and are incorporated herein.

Executive Summary

General

Tredegar is a manufacturer of plastic films and aluminum extrusions. Descriptions of our businesses are provided on pages 1-5.

Income from continuing operations was $38.2$34.9 million (98(90 cents per diluted share) in 20062007 compared with $16.2$35.3 million (42(91 cents per diluted share) in 2005.2006. Gains on the sale of assets, investment write-downs and other items and losses related to plant shutdowns, assets impairments and restructurings are described in results of operations beginning on page 20.21. The business segment review begins on page 33.

Film Products

In Film Products, net sales were $531.0 million in 2007, up 3.9% versus $511.2 million in 2006, up 11.1% versus $460.3 million in 2005.2006. Operating profit from ongoing operations was $59.4 million in 2007, up 3.1% compared with $57.6 million in 2006, up 28.3% compared to $44.9 million in 2005. Operating profit from ongoing operations excluding the estimated effects of resin pass-through lag and year-end LIFO adjustments was $53.1 million in 2006, up 8.6% versus $48.9 million in 2005.2006. Volume decreased to 244.3 million pounds in 2007 from 253.5 million pounds in 2006. Volume was down in 2007 compared with 2006 from 261.1 million poundsprimarily due to a decrease in 2005.sales of commodity barrier films and packaging films, partially offset by an increase in sales of elastic materials used in baby diapers and adult incontinence products and apertured materials used as topsheet in feminine hygiene products. Certain commodity barrier films were discontinued in conjunction with the shutdown in the second quarter of 2006 of the plant in LaGrange, Georgia. Net sales increased primarily due to appreciation of the U.S. dollar value of currencies for operations outside of the U.S., higher volume of elastic and apertured materials and improved product mix of surface protection films, partially offset by a decline in volume of commodity barrier films and a decline in volume and prices of certain packaging films. We estimate that the growth in net sales excluding the effects of the pass-through of resin price changes and foreign exchange rate changes was approximately 6%3.5% in 2006. Sales2007.

Operating profit from ongoing operations in Film Products increased in 2007 versus 2006 primarily due to the net changes in sales noted above and appreciation of the U.S. dollar value of currencies for operations outside of the U.S. (the benefit from currency rate changes was approximately $3.0 million), partially offset by an estimated negative impact in 2007 of $2.5 million from the lag in the pass-through of changes in average resin costs and year-end adjustments for LIFO. In 2006, we estimated a favorable impact of $4.5 million from the lag in the pass-through of changes in average resin costs and year-end adjustments for LIFO.

Future operating profit levels in films will depend on our ability to deliver product innovations and cost reductions to support growth in 2006 were driven primarily by increasedthe sales of high-valuehigher value surface protection films elasticand to address competitive pressures facing our personal care and packaging materials and new apertured topsheets, partially offset by lower sales of certain commodity barrier films thatbusinesses.

Capital expenditures in Film Products were dropped in conjunction with the shutdown of the plant in LaGrange, Georgia. The plant was shut down in the first half of 2006 and had sales of commodity barrier films of approximately $20$15.3 million in 2005.

Aluminum Extrusions